overall audit plan and audit program how much and what kind of testing will get the job done? how...

Post on 20-Dec-2015

217 views

TRANSCRIPT

OVERALL AUDITOVERALL AUDITPLAN AND AUDITPLAN AND AUDIT

PROGRAMPROGRAM

OVERALL AUDITOVERALL AUDITPLAN AND AUDITPLAN AND AUDIT

PROGRAMPROGRAM

HOW MUCH AND WHAT KINDHOW MUCH AND WHAT KINDOF TESTING WILL GETOF TESTING WILL GET

THE JOB DONE? THE JOB DONE?

HOW MUCH AND WHAT KINDHOW MUCH AND WHAT KINDOF TESTING WILL GETOF TESTING WILL GET

THE JOB DONE? THE JOB DONE?

13131313

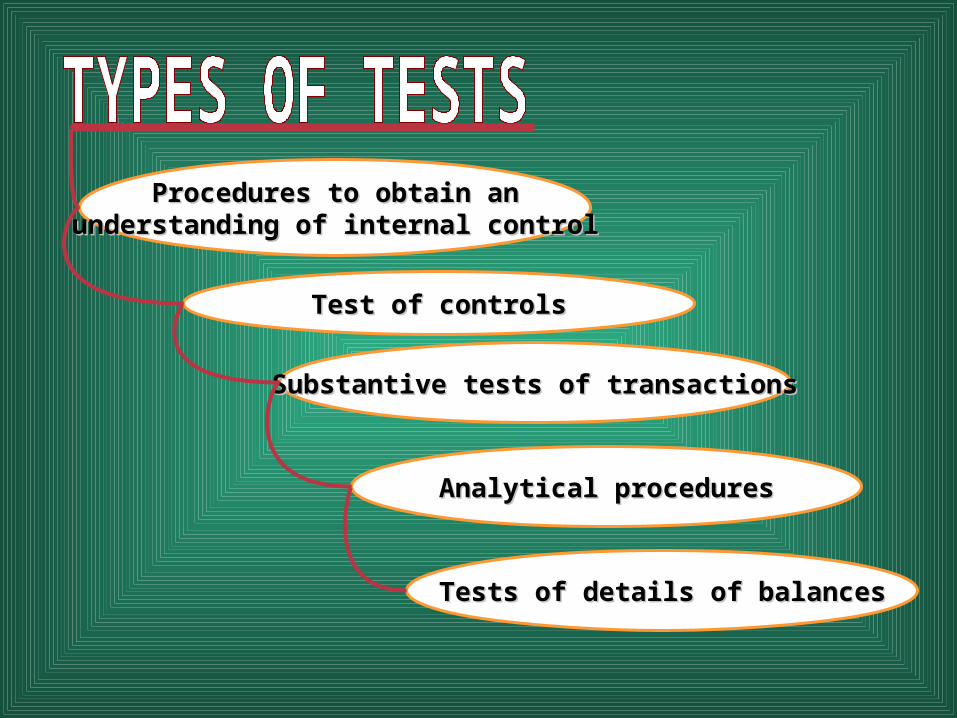

Procedures to obtain anProcedures to obtain anunderstanding of internal controlunderstanding of internal control

Test of controlsTest of controls

Substantive tests of transactionsSubstantive tests of transactions

Analytical proceduresAnalytical procedures

Tests of details of balancesTests of details of balances

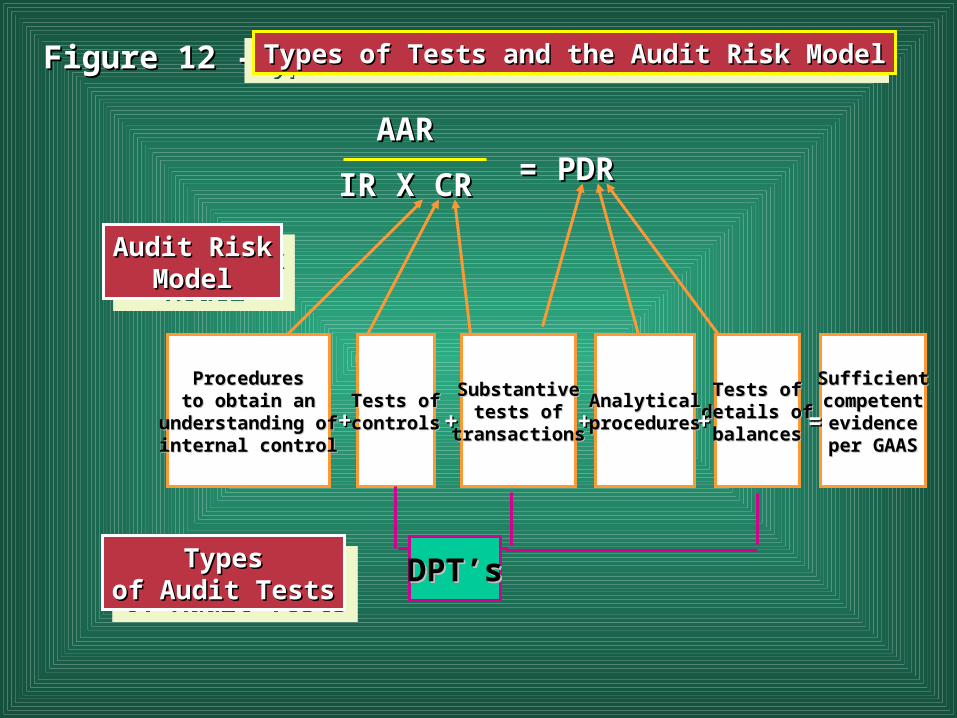

ProceduresProceduresto obtain anto obtain an

understanding ofunderstanding ofinternal controlinternal control

Tests ofTests ofcontrolscontrols

SubstantiveSubstantivetests oftests of

transactionstransactions

AnalyticalAnalyticalproceduresprocedures

SufficientSufficientcompetentcompetentevidenceevidence

per GAASper GAAS

Tests ofTests ofdetails ofdetails ofbalancesbalances

++ ++ ++ ++ ==

Audit RiskAudit RiskModelModel

Audit RiskAudit RiskModelModel

TypesTypesof Audit Testsof Audit Tests

TypesTypesof Audit Testsof Audit Tests

AARAAR

IR X CRIR X CR = PDR= PDR

Figure 12 - 1Figure 12 - 1 Types of Tests and the Audit Risk ModelTypes of Tests and the Audit Risk ModelTypes of Tests and the Audit Risk ModelTypes of Tests and the Audit Risk Model

DPT’sDPT’s

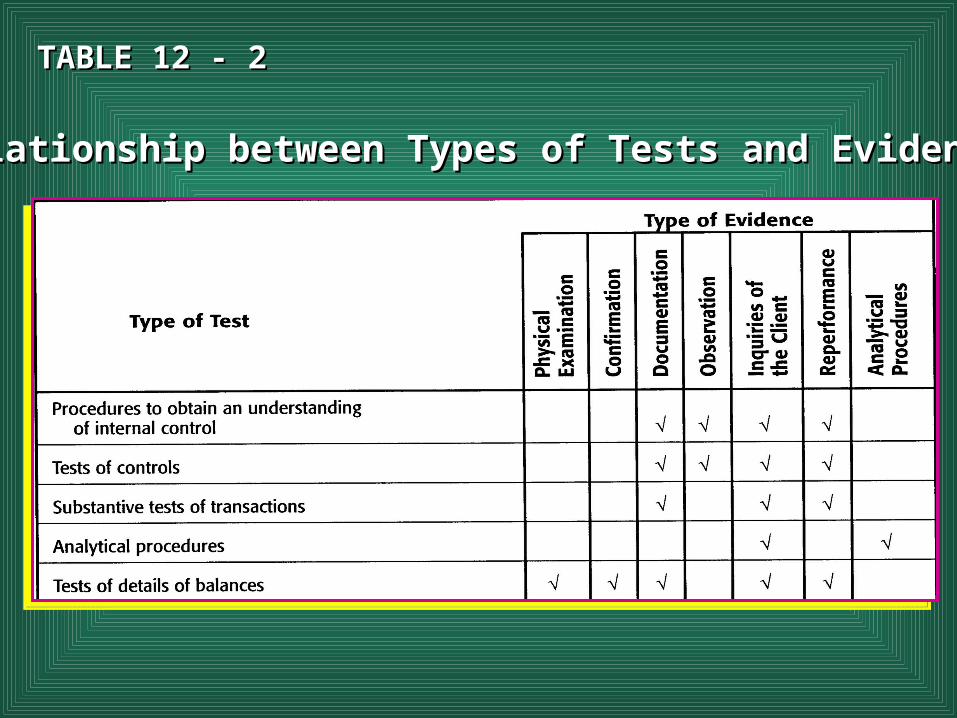

TABLE 12 - 2TABLE 12 - 2

Relationship between Types of Tests and EvidenceRelationship between Types of Tests and Evidence

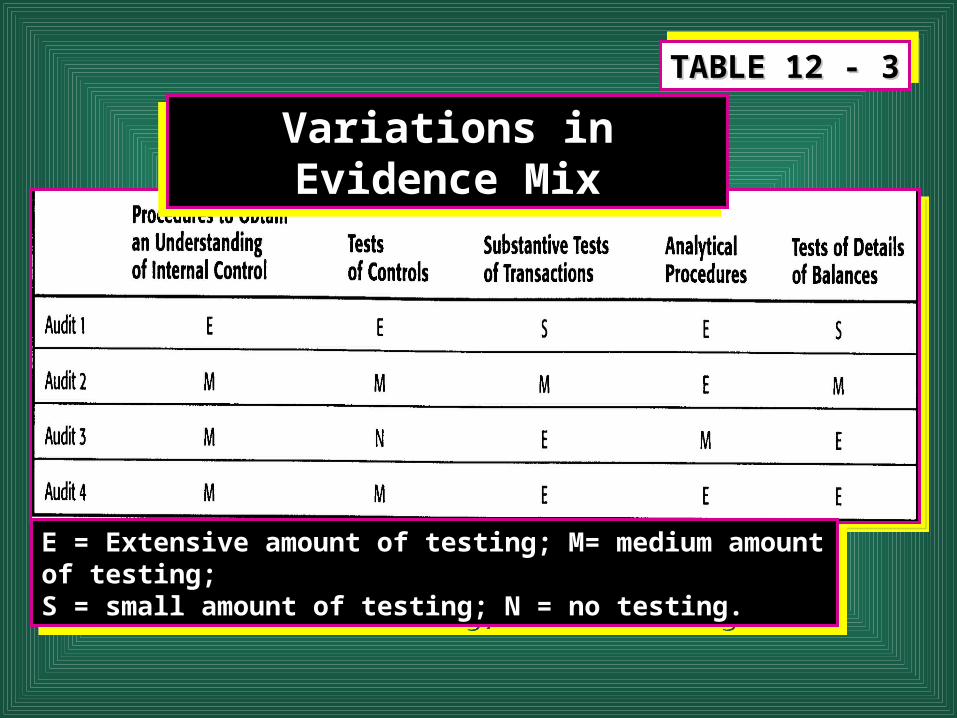

E = Extensive amount of testing; M= medium amount of testing;E = Extensive amount of testing; M= medium amount of testing;S = small amount of testing; N = no testing.S = small amount of testing; N = no testing.

E = Extensive amount of testing; M= medium amount of testing;E = Extensive amount of testing; M= medium amount of testing;S = small amount of testing; N = no testing.S = small amount of testing; N = no testing.

TABLE 12 - 3TABLE 12 - 3TABLE 12 - 3TABLE 12 - 3

Variations in Evidence MixVariations in Evidence MixVariations in Evidence MixVariations in Evidence Mix

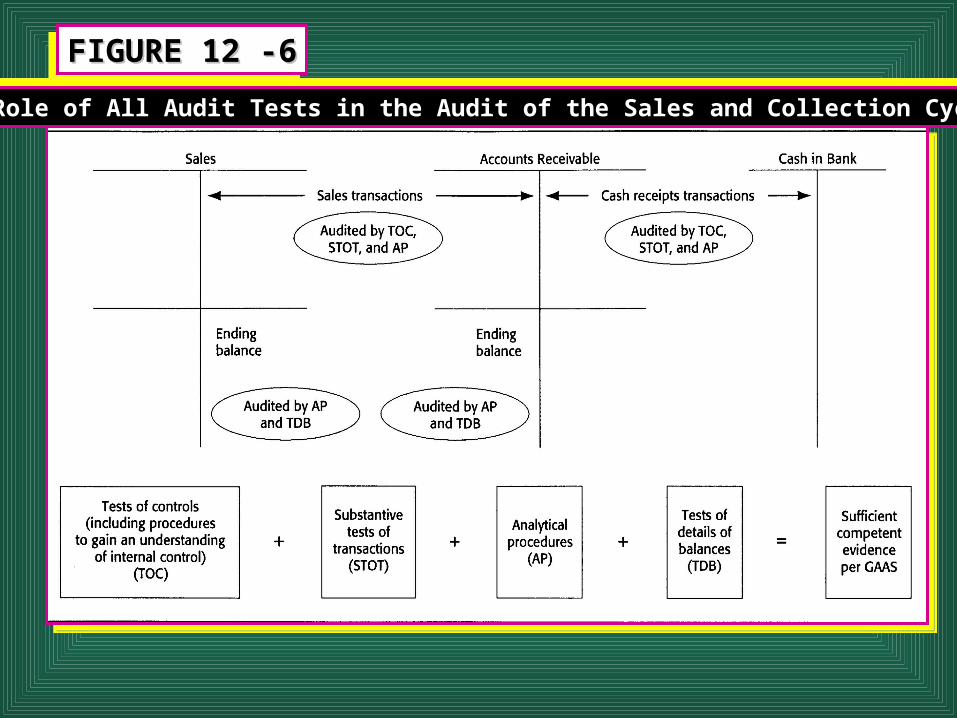

FIGURE 12 -6FIGURE 12 -6FIGURE 12 -6FIGURE 12 -6

Role of All Audit Tests in the Audit of the Sales and Collection CycleRole of All Audit Tests in the Audit of the Sales and Collection CycleRole of All Audit Tests in the Audit of the Sales and Collection CycleRole of All Audit Tests in the Audit of the Sales and Collection Cycle

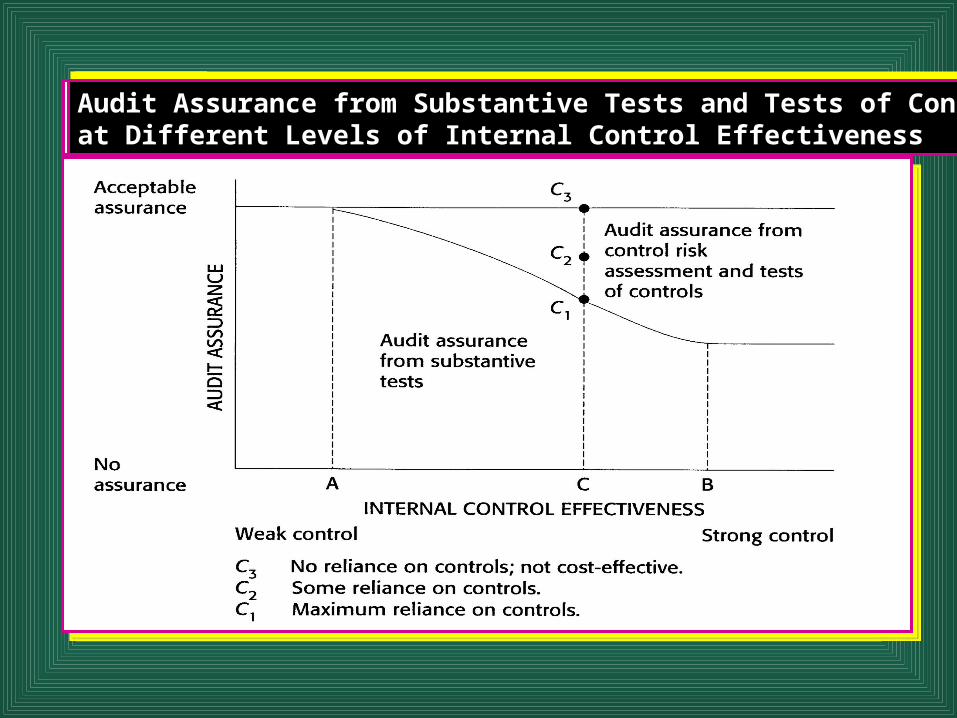

FIGUREFIGURE12 - 712 - 7

FIGUREFIGURE12 - 712 - 7

Audit Assurance from Substantive Tests and Tests of ControlsAudit Assurance from Substantive Tests and Tests of Controlsat Different Levels of Internal Control Effectivenessat Different Levels of Internal Control Effectiveness

Audit Assurance from Substantive Tests and Tests of ControlsAudit Assurance from Substantive Tests and Tests of Controlsat Different Levels of Internal Control Effectivenessat Different Levels of Internal Control Effectiveness

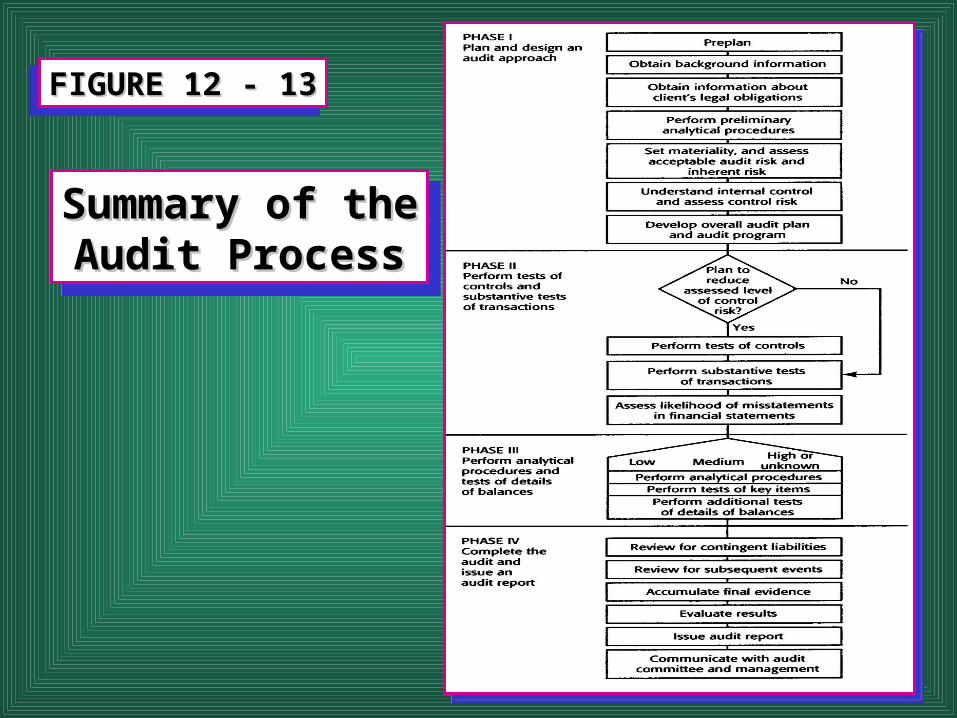

FIGURE 12 - 13FIGURE 12 - 13FIGURE 12 - 13FIGURE 12 - 13

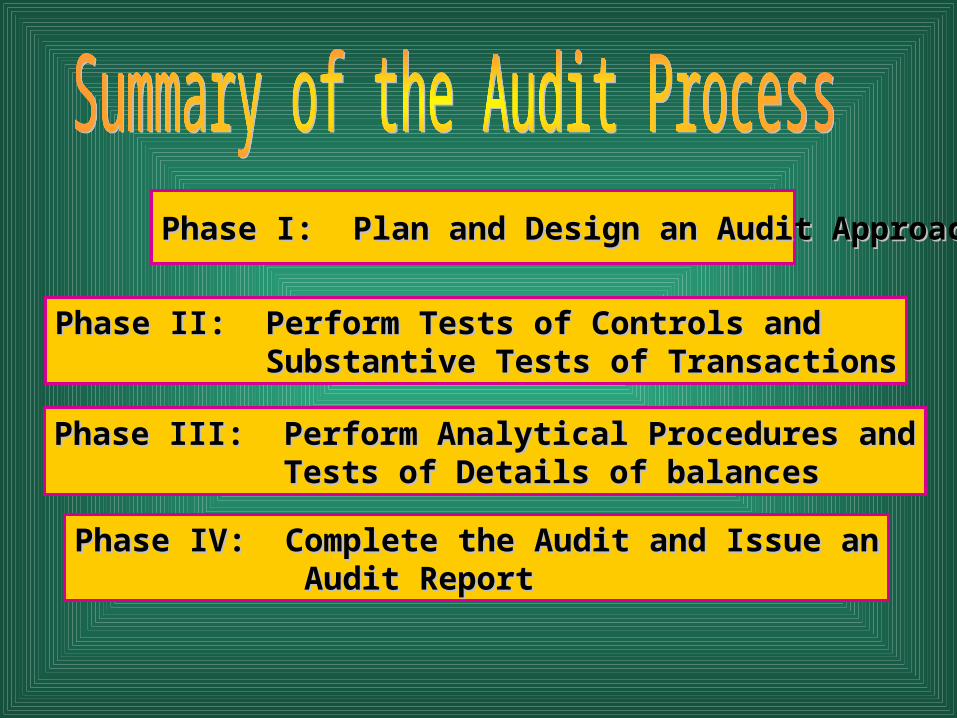

Summary of theSummary of theAudit ProcessAudit Process

Summary of theSummary of theAudit ProcessAudit Process

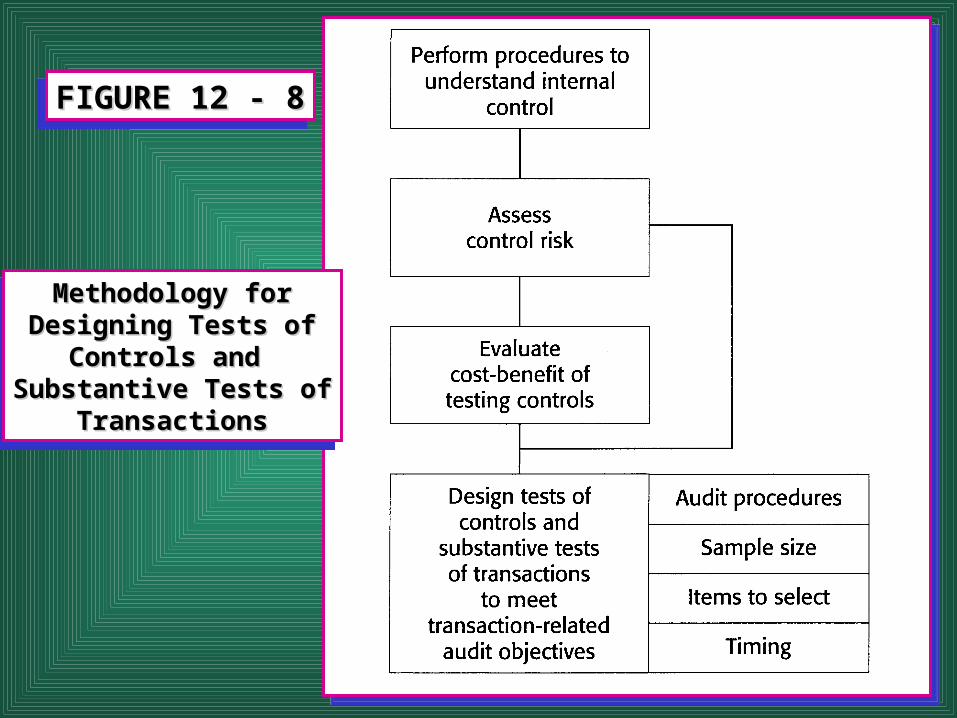

FIGURE 12 - 8FIGURE 12 - 8FIGURE 12 - 8FIGURE 12 - 8

Methodology forMethodology forDesigning Tests ofDesigning Tests of

Controls and Controls and Substantive Tests ofSubstantive Tests of

TransactionsTransactions

Methodology forMethodology forDesigning Tests ofDesigning Tests of

Controls and Controls and Substantive Tests ofSubstantive Tests of

TransactionsTransactions

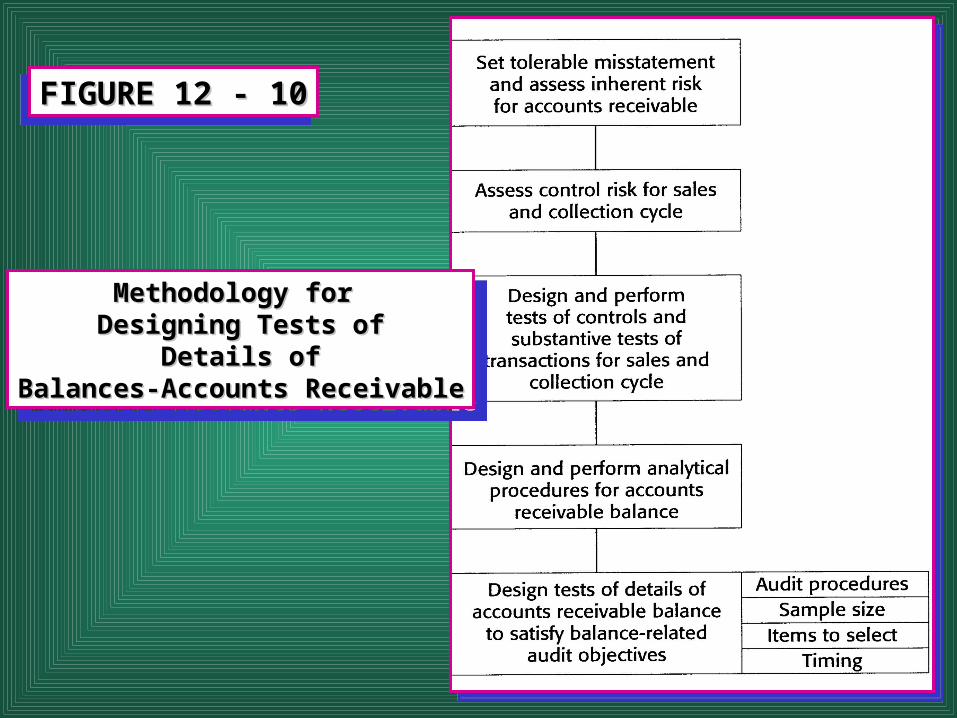

FIGURE 12 - 10FIGURE 12 - 10FIGURE 12 - 10FIGURE 12 - 10

Methodology for Methodology for Designing Tests ofDesigning Tests of

Details ofDetails ofBalances-Accounts ReceivableBalances-Accounts Receivable

Methodology for Methodology for Designing Tests ofDesigning Tests of

Details ofDetails ofBalances-Accounts ReceivableBalances-Accounts Receivable

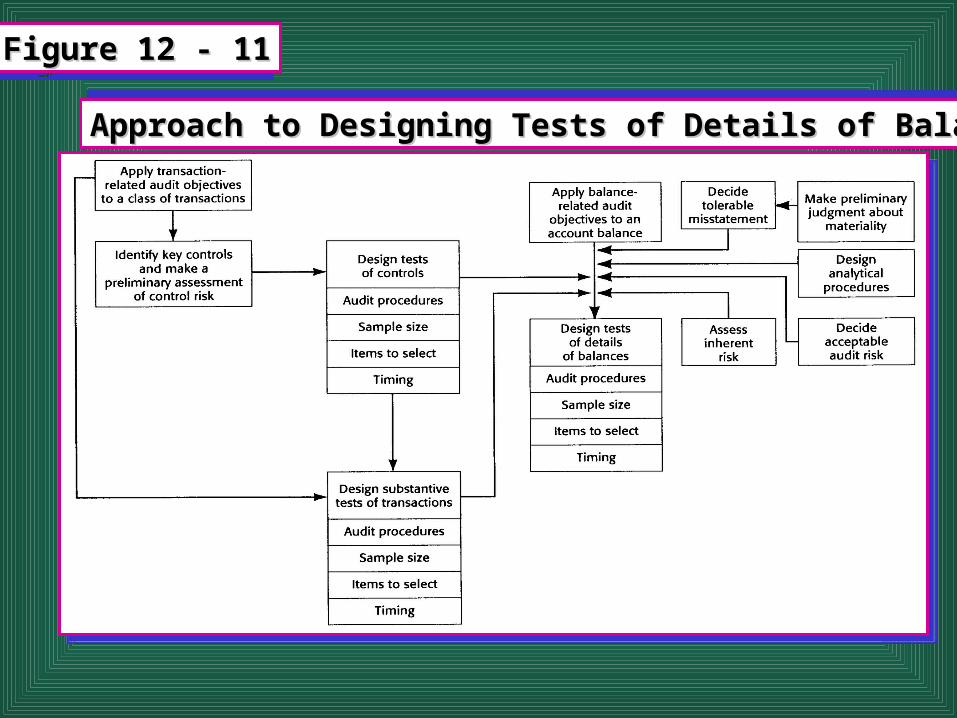

Figure 12 - 11Figure 12 - 11Figure 12 - 11Figure 12 - 11

Approach to Designing Tests of Details of BalancesApproach to Designing Tests of Details of BalancesApproach to Designing Tests of Details of BalancesApproach to Designing Tests of Details of Balances

Phase I: Plan and Design an Audit ApproachPhase I: Plan and Design an Audit Approach

Phase II: Perform Tests of Controls and Phase II: Perform Tests of Controls and Substantive Tests of TransactionsSubstantive Tests of Transactions

Phase III: Perform Analytical Procedures andPhase III: Perform Analytical Procedures and Tests of Details of balancesTests of Details of balances

Phase IV: Complete the Audit and Issue anPhase IV: Complete the Audit and Issue an Audit ReportAudit Report

• Review for Contingent LiabilitiesReview for Contingent Liabilities

• Review for Subsequent EventsReview for Subsequent Events

• Accumulate Final EvidenceAccumulate Final Evidence

• Issue Audit ReportIssue Audit Report• Communicate with AuditCommunicate with Audit Committee and ManagementCommittee and Management

• Review for Contingent LiabilitiesReview for Contingent Liabilities

• Review for Subsequent EventsReview for Subsequent Events

• Accumulate Final EvidenceAccumulate Final Evidence

• Issue Audit ReportIssue Audit Report• Communicate with AuditCommunicate with Audit Committee and ManagementCommittee and Management

• Analytical proceduresAnalytical procedures

• Evidence mixEvidence mix

• Phases of the audit processPhases of the audit process

• Procedures to obtain anProcedures to obtain an understanding ofunderstanding of internal controlinternal control

• Analytical proceduresAnalytical procedures

• Evidence mixEvidence mix

• Phases of the audit processPhases of the audit process

• Procedures to obtain anProcedures to obtain an understanding ofunderstanding of internal controlinternal control

• Substantive testsSubstantive tests

• Substantive tests ofSubstantive tests of transactionstransactions

• Tests of controlsTests of controls

• Tests of details of balanceTests of details of balance

• Types of testsTypes of tests

• Substantive testsSubstantive tests

• Substantive tests ofSubstantive tests of transactionstransactions

• Tests of controlsTests of controls

• Tests of details of balanceTests of details of balance

• Types of testsTypes of tests