organic production and horticulture aec 317 fall 2012

TRANSCRIPT

Organic Production andHorticulture AEC 317 Fall 2012

Organic Produce Markets Initially grass roots program Movement toward commercialization led to

state-by-state certification Flexible to growing region But variable standards across states Cap on market scale Push by national and regional retailers for

universal standards 2002 USDA National Organic Standards

adopted

http://www.ams.usda.gov/AMSv1.0/nop

Inputs and practices governed by National Organic Standards Board

Limits pesticides, fertilizers, no genetically engineered products

Third party certification and enforcement

Unlawful to wrongfully use term “organic” without certification

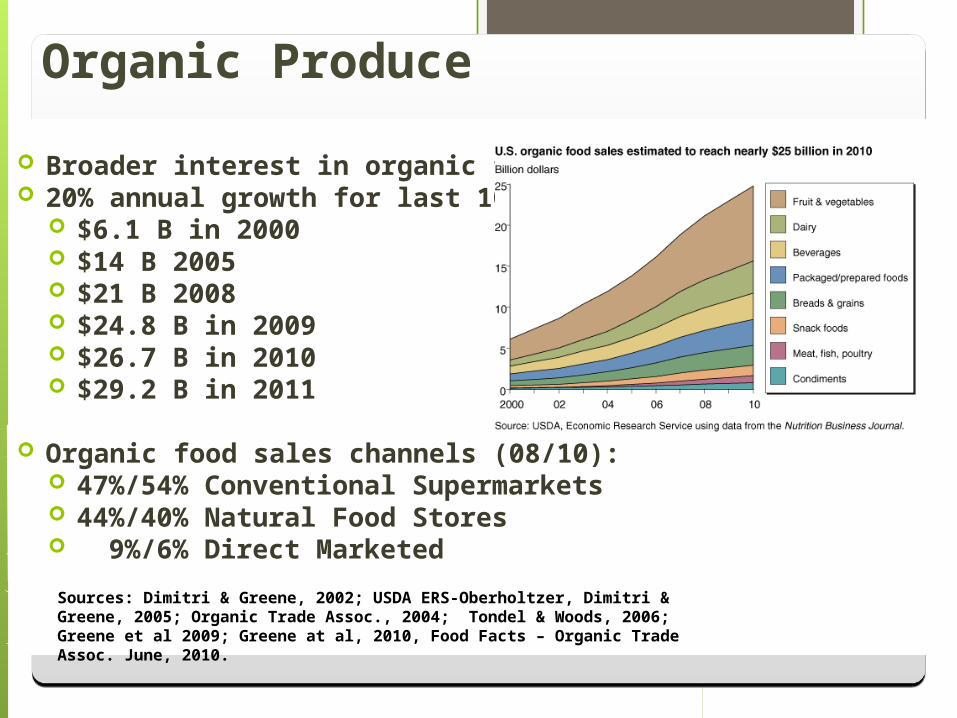

Organic Produce

Broader interest in organic food 20% annual growth for last 10 years

$6.1 B in 2000 $14 B 2005 $21 B 2008 $24.8 B in 2009 $26.7 B in 2010 $29.2 B in 2011

Organic food sales channels (08/10): 47%/54% Conventional Supermarkets 44%/40% Natural Food Stores 9%/6% Direct Marketed

Sources: Dimitri & Greene, 2002; USDA ERS-Oberholtzer, Dimitri & Greene, 2005; Organic Trade Assoc., 2004; Tondel & Woods, 2006; Greene et al 2009; Greene at al, 2010, Food Facts – Organic Trade Assoc. June, 2010.

In 2010, U.S. surpassed the European Union as the largest market for organic products in the world.

Organic food and beverages represents 4.2% of all U.S. food and beverage sales (2011)

Organic trends Fresh produce accounts for 42%/38% of all organic food

sales - - about 12% of all produce sales in U.S. are organic.

1/3 of organic produce sold under contract

Trend towards larger growers & direct to retailer sales

Still tiny in KY: 111 farms (all products)

Organic Trade Association http://www.ota.com/

USDA Programs in Organic/Sustainable Ag Sustainable Ag Research and Education

Some of the Issues1. International growth and marketing of organic – what are

the standards?: Equivalency agreements2. Expansion of GMO production: Industry pushes for

mandatory GMO labeling3. Scale production economies lower costs, but also premiums4. Growth in other eco-labels