opportunities nb webinar - emerging trends in hedge fund administration

TRANSCRIPT

Opportunities NB Webinar Series

Emerging Trends in Hedge Fund Administration

May 26, 2016

Host: Heather MacLean Manager, Social Media

Opportunities

Guest: Michael Cyran Partner

Ernst & Young

Client-focused, proactive, professional and accountable, Opportunities NB is the first point of contact for local and foreign businesses looking to grow, expand or locate. We are focused on performance, high growth opportunities and growing New Brunswick. Opportunities NB is poised to:

• Support business development inside New Brunswick, including business support services for small, medium-sized and large businesses;

• Proactively pursue high growth opportunities through exports and foreign investment; and

• Work with industry partners, economic development stakeholders and public sector partners to identify, build and support a portfolio of significant high growth opportunities both within and outside the province!

We will offer you the ideal operational expansion and labour solution tailored to your needs to grow in

New Brunswick. We will go above and beyond to ensure your success in the province.

New Brunswick is built for business. We look forward to working with you to grow your business.

Our guest today

Michael Cyran

Partner Ernst & Young

Julie Sullivan Partner– Shared Services and Outsourcing

Background • Mike is a partner in the New York Financial Services Office with over 25 years

of experience in the financial services sector. He focuses on asset management organizations, and specializes in working with investment advisers, registered investment companies, alternative investment funds, structured products and investment management operations. Mike possesses deep knowledge in investment management and transfer agency operations, fund administration, and valuation and accounting for derivatives, asset-backed and illiquid securities. Mike is a frequent speaker on various technical and operational topics at industry conferences.

• He is the Service Organization Controls (SOC) Reports leader for Ernst & Young’s Financial Services Office as well as Ernst & Young’s Global Asset Management practice. He leads many of the global fund administration SOC 1 reports that the Firm services.

• Mike has extensive experience in the securitization of collateralized debt obligations and other asset backed securities, having worked in E&Y’s Structured Finance Advisory Services group for over two years as a senior manager, and is a subject matter expert within the Firm related to these topics.

• Mike is a Certified Public Accountant and is a member of the New York State Society of CPAs, the New Jersey State Society of CPAs and the American Institute of Certified Public Accountants.

Michael Cyran Partner

Ernst & Young Work: +1 212 773 2561 Cell: +1 908 391 1653 [email protected]

Page 7

Key Themes and Trends ► Hedge fund administration overview ► Competitor landscape ► Shadow accounting ► Middle office services ► PE and RE services ► Regulatory reporting

Page 8

Hedge Fund Administration Overview Who they are, what they do ► A Hedge Fund Administrator (HFA) assumes the day-to-day administrative duties with respect to key tasks

such as:

► Fund accounting

► Portfolio valuations

► Investor Servicing

► Middle office servicing

► Independence in functionality from other service providers

► Administrators serve the hedge funds and their investors

► Important liaison between hedge funds and investors

► Provide transparency into fund activities

► The fundamental value proposition of Hedge Fund Administrators is their ability to:

► Process the fund’s activities efficiently and seamlessly

► Report breaks and P&L

► Provide investors with independently prepared, accurate and timely information on fund activity

Page 9

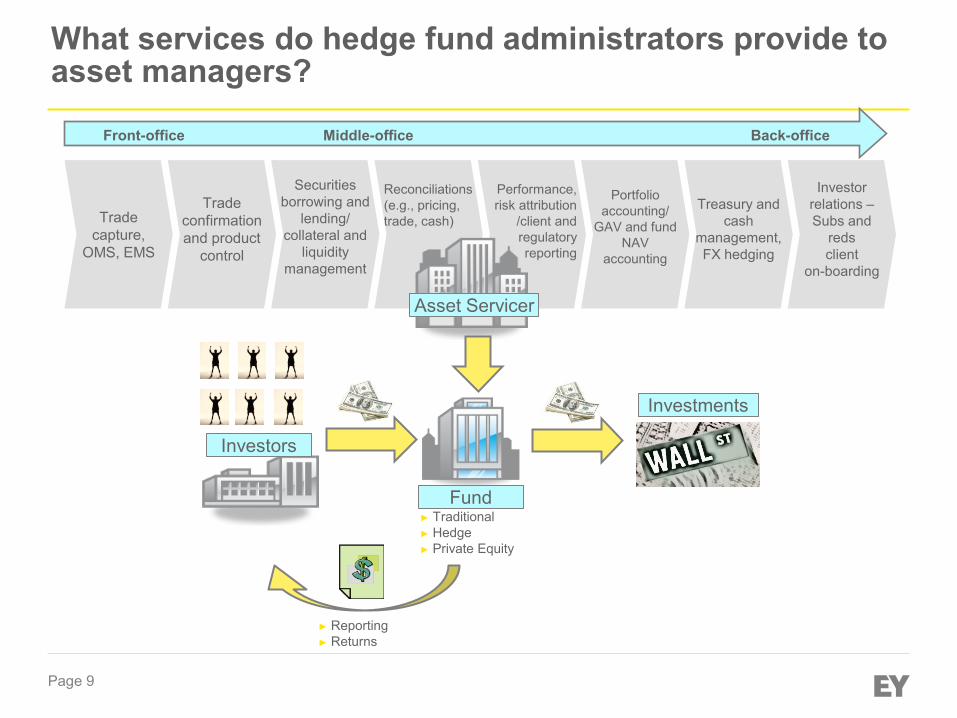

Front-office Middle-office Back-office

Treasury and cash

management, FX hedging

Trade capture,

OMS, EMS

Securities borrowing and

lending/ collateral and

liquidity management

Performance, risk attribution

/client and regulatory reporting

Trade confirmation and product

control

Reconciliations (e.g., pricing, trade, cash)

Portfolio accounting/

GAV and fund NAV

accounting

Investor relations – Subs and

reds client

on-boarding

► Traditional ► Hedge ► Private Equity

Fund

Investors

► Reporting ► Returns

Asset Servicer

Investments

What services do hedge fund administrators provide to asset managers?

Page 10

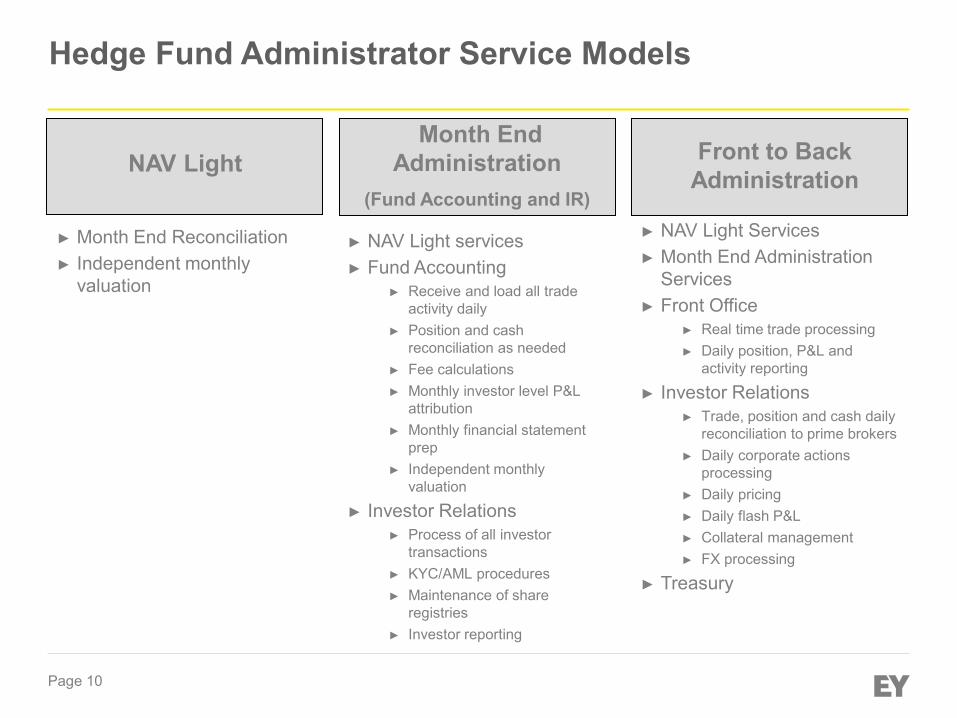

Hedge Fund Administrator Service Models

NAV Light Front to Back Administration

Month End Administration

(Fund Accounting and IR)

► Month End Reconciliation ► Independent monthly

valuation

► NAV Light services ► Fund Accounting

► Receive and load all trade activity daily

► Position and cash reconciliation as needed

► Fee calculations ► Monthly investor level P&L

attribution ► Monthly financial statement

prep ► Independent monthly

valuation

► Investor Relations ► Process of all investor

transactions ► KYC/AML procedures ► Maintenance of share

registries ► Investor reporting

► NAV Light Services ► Month End Administration

Services ► Front Office

► Real time trade processing ► Daily position, P&L and

activity reporting

► Investor Relations ► Trade, position and cash daily

reconciliation to prime brokers ► Daily corporate actions

processing ► Daily pricing ► Daily flash P&L ► Collateral management ► FX processing

► Treasury

Page 11

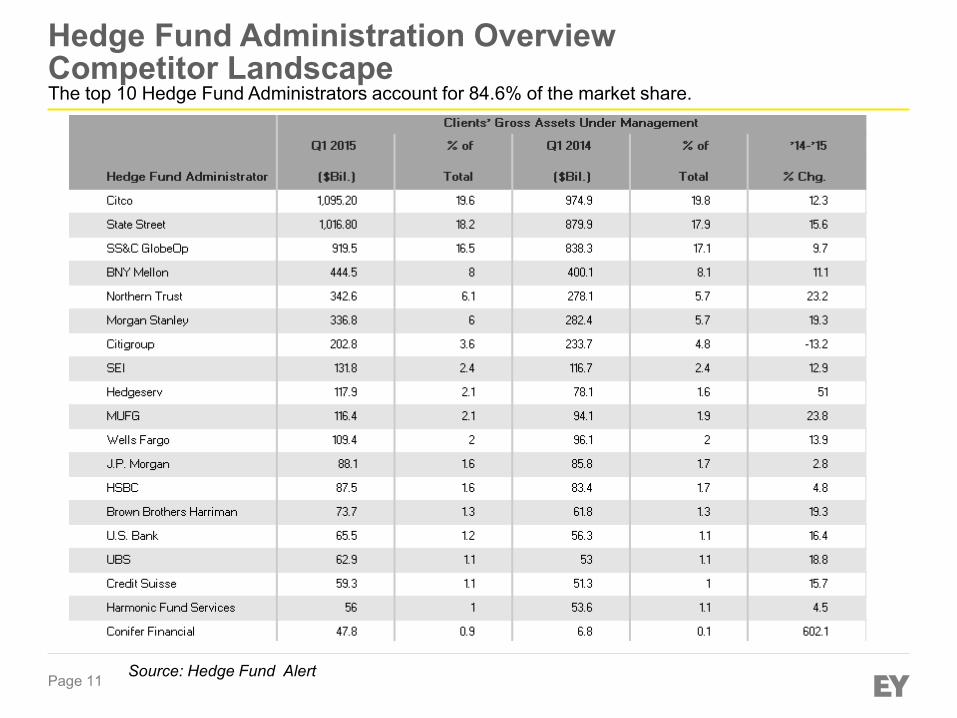

Hedge Fund Administration Overview Competitor Landscape

Source: Hedge Fund Alert

The top 10 Hedge Fund Administrators account for 84.6% of the market share.

Page 12

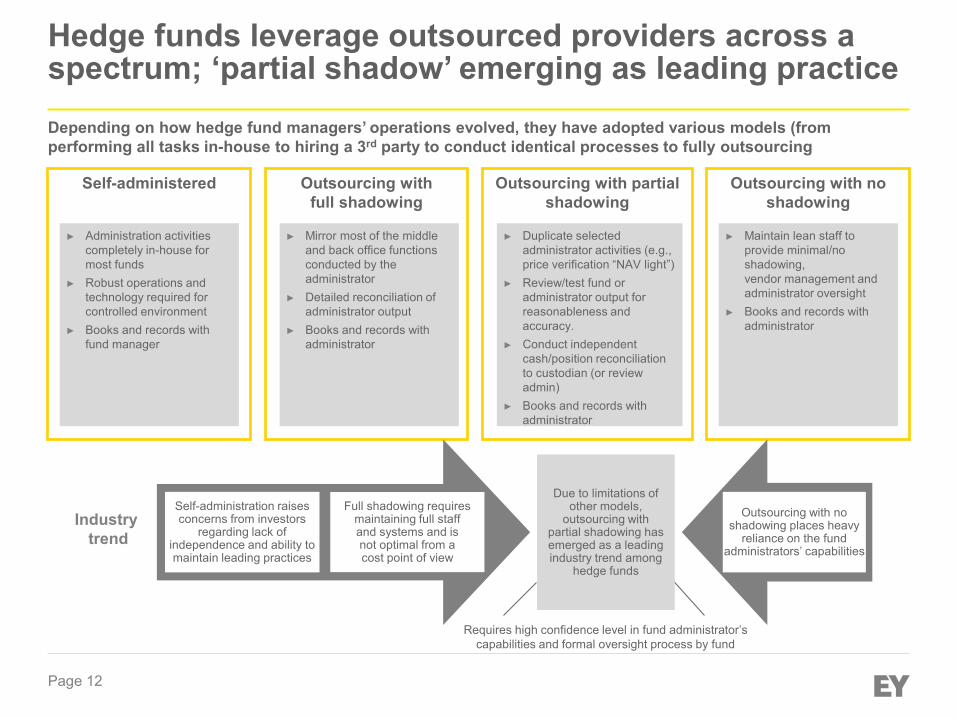

Hedge funds leverage outsourced providers across a spectrum; ‘partial shadow’ emerging as leading practice

Self-administered

► Administration activities completely in-house for most funds

► Robust operations and technology required for controlled environment

► Books and records with fund manager

Outsourcing with full shadowing

► Mirror most of the middle and back office functions conducted by the administrator

► Detailed reconciliation of administrator output

► Books and records with administrator

Outsourcing with partial shadowing

► Duplicate selected administrator activities (e.g., price verification “NAV light”)

► Review/test fund or administrator output for reasonableness and accuracy.

► Conduct independent cash/position reconciliation to custodian (or review admin)

► Books and records with administrator

Outsourcing with no shadowing

► Maintain lean staff to provide minimal/no shadowing, vendor management and administrator oversight

► Books and records with administrator

Industry trend

Requires high confidence level in fund administrator’s capabilities and formal oversight process by fund

Self-administration raises concerns from investors

regarding lack of independence and ability to maintain leading practices

Full shadowing requires maintaining full staff and systems and is not optimal from a cost point of view

Due to limitations of other models,

outsourcing with partial shadowing has emerged as a leading industry trend among

hedge funds

Outsourcing with no shadowing places heavy

reliance on the fund administrators’ capabilities

Depending on how hedge fund managers’ operations evolved, they have adopted various models (from performing all tasks in-house to hiring a 3rd party to conduct identical processes to fully outsourcing

Page 13

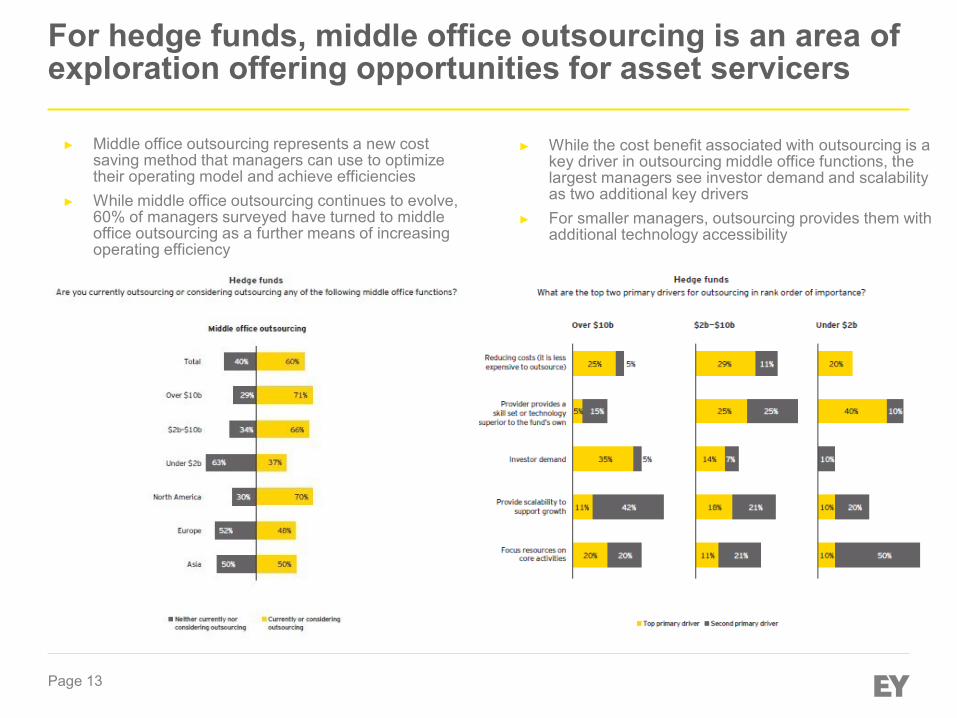

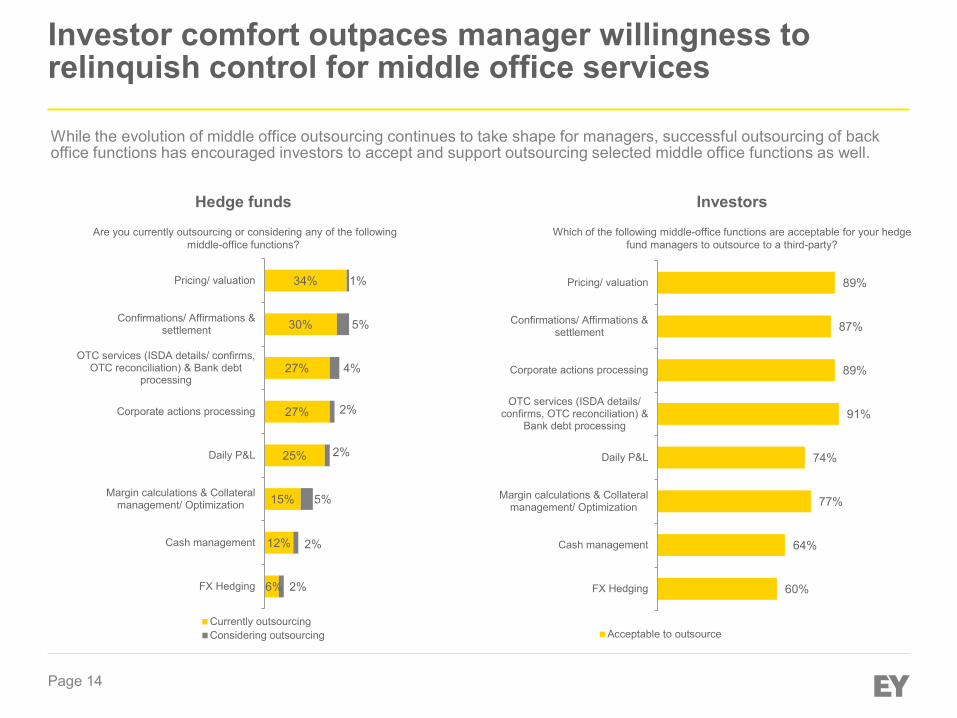

► While the cost benefit associated with outsourcing is a key driver in outsourcing middle office functions, the largest managers see investor demand and scalability as two additional key drivers

► For smaller managers, outsourcing provides them with additional technology accessibility

For hedge funds, middle office outsourcing is an area of exploration offering opportunities for asset servicers

► Middle office outsourcing represents a new cost saving method that managers can use to optimize their operating model and achieve efficiencies

► While middle office outsourcing continues to evolve, 60% of managers surveyed have turned to middle office outsourcing as a further means of increasing operating efficiency

Page 14

While the evolution of middle office outsourcing continues to take shape for managers, successful outsourcing of back office functions has encouraged investors to accept and support outsourcing selected middle office functions as well.

Investor comfort outpaces manager willingness to relinquish control for middle office services

34%

30%

27%

27%

25%

15%

12%

6%

1%

5%

4%

2%

2%

5%

2%

2%

Pricing/ valuation

Confirmations/ Affirmations &settlement

OTC services (ISDA details/ confirms,OTC reconciliation) & Bank debt

processing

Corporate actions processing

Daily P&L

Margin calculations & Collateralmanagement/ Optimization

Cash management

FX Hedging

Currently outsourcingConsidering outsourcing

89%

87%

89%

91%

74%

77%

64%

60%

Pricing/ valuation

Confirmations/ Affirmations &settlement

Corporate actions processing

OTC services (ISDA details/confirms, OTC reconciliation) &

Bank debt processing

Daily P&L

Margin calculations & Collateralmanagement/ Optimization

Cash management

FX Hedging

Acceptable to outsource

Hedge funds

Are you currently outsourcing or considering any of the following middle-office functions?

Investors

Which of the following middle-office functions are acceptable for your hedge fund managers to outsource to a third-party?

Page 15

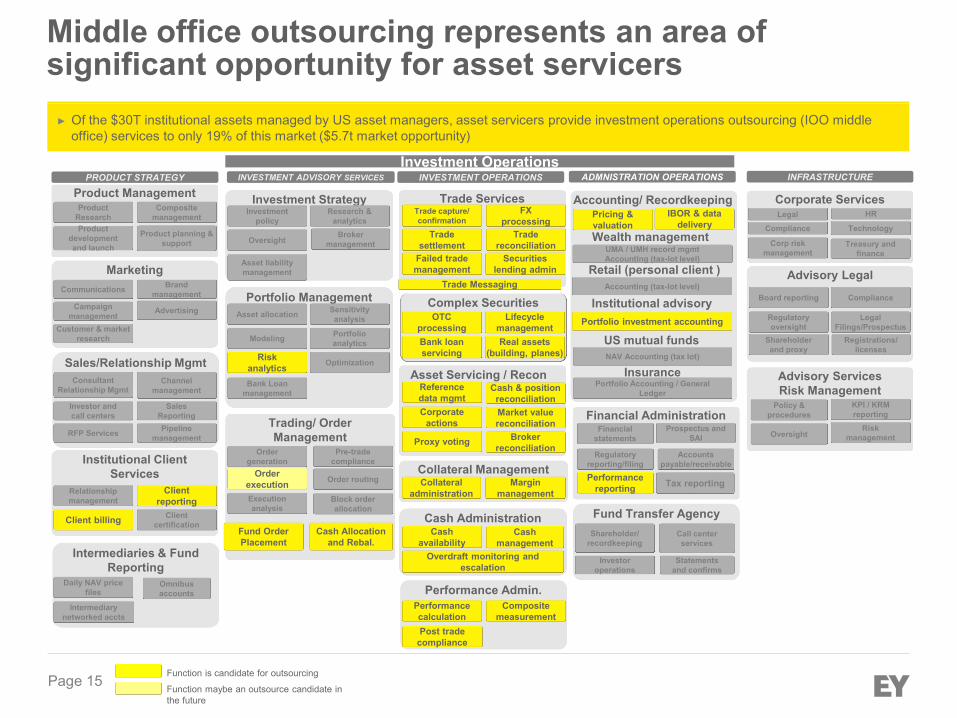

PRODUCT STRATEGY INVESTMENT ADVISORY SERVICES INVESTMENT OPERATIONS INFRASTRUCTURE

Investment Strategy Investment

policy Research &

analytics

Oversight

Institutional Client Services

Relationship management

Client reporting

Client billing Client certification

Product Management Product

Research

Product planning & support

Product development and launch

Composite management

Performance Admin. Performance calculation

Composite measurement

Corporate Services

Compliance Technology

Legal

Corp risk management

HR

Advisory Services Risk Management

Policy & procedures

KPI / KRM reporting

Risk management Oversight

Financial Administration Financial

statements

Regulatory reporting/filing

Tax reporting Performance reporting

Accounts payable/receivable

Prospectus and SAI

Investment Operations

Sales/Relationship Mgmt Consultant

Relationship Mgmt Channel

management

RFP Services

Pipeline

management

Broker management

Trading/ Order Management

Order generation

Block order allocation

Pre-trade compliance

Order routing Order execution Execution analysis

Cash Administration Cash

management Overdraft monitoring and

escalation

Advisory Legal

Board reporting

Regulatory oversight

Compliance

Legal Filings/Prospectus

Shareholder and proxy

Registrations/ licenses

Treasury and finance

Asset liability management

Fund Transfer Agency Call center services

Shareholder/ recordkeeping

Investor operations

Statements and confirms

Asset Servicing / Recon

Corporate actions

Proxy voting

Cash & position reconciliation

Reference data mgmt

ADMNISTRATION OPERATIONS

Accounting/ Recordkeeping Pricing & valuation Wealth management

UMA / UMH record mgmt Accounting (tax-lot level)

Retail (personal client )

Portfolio investment accounting

US mutual funds NAV Accounting (tax lot)

Portfolio Accounting / General Ledger

Insurance

Accounting (tax-lot level)

Institutional advisory

Marketing Communications Brand

management Campaign

management Advertising

Customer & market research

Portfolio Management Asset allocation

Portfolio analytics Modeling

Optimization Risk analytics

Sensitivity analysis

Bank Loan management

Trade Services

Trade settlement

Trade capture/ confirmation

Failed trade management

Trade reconciliation

FX processing

Investor and call centers

Sales

Reporting

Intermediaries & Fund Reporting

Daily NAV price files

Omnibus accounts

Intermediary networked accts

Collateral Management

Securities lending admin

Margin management

Market value reconciliation

Broker reconciliation

Complex Securities OTC

processing Lifecycle

management

IBOR & data delivery

Cash availability

Post trade compliance

Bank loan servicing

Real assets (building, planes)

Collateral administration

Cash Allocation and Rebal.

Fund Order Placement

Function maybe an outsource candidate in the future

Function is candidate for outsourcing

► Of the $30T institutional assets managed by US asset managers, asset servicers provide investment operations outsourcing (IOO middle office) services to only 19% of this market ($5.7t market opportunity)

Middle office outsourcing represents an area of significant opportunity for asset servicers

Trade Messaging

Page 16

When making decisions to outsource, asset managers review potential inhibitors that either prevent outsourcing, or impose operational complexities on their selected provider. Those inhibitors include: ► Loss of control –Typically can be mitigated through effective service level agreements, escalation policies, auditable operations and

transparency via web portals and data delivery

► Fund board or client requirements – Depending on the size of business and/or activity of the fund board, both boards and clients can be prescriptive as to what functions should or shouldn’t be performed directly by the asset manager

► Customized functions – The level of customization required by the asset manager exceeds the service providers capabilities. In certain cases, the time required by the service provider to meet customization requirements is too long, imparting significant financial and operation risk to the firm

Market drivers and inhibitors to Middle Office Outsourcing

Market Driver Americas EMEA

Aging technology and outgrowing existing manager infrastructure

Ability to consolidate data across disparate systems and aggregate for regulatory reporting Complex and evolving regulatory landscape

Greater operational requirements to support new investment solutions / scale for managed accounts

Cost reduction – due to compressed profit margins and need for predictable operating cost Complexity introduced by new markets / operating in new geographies

Talent management /key person risk - seeking specialized skills for complex instruments Second generation outsourcing, i.e. switching administrators

Critical

Low

Level of impact

Page 17

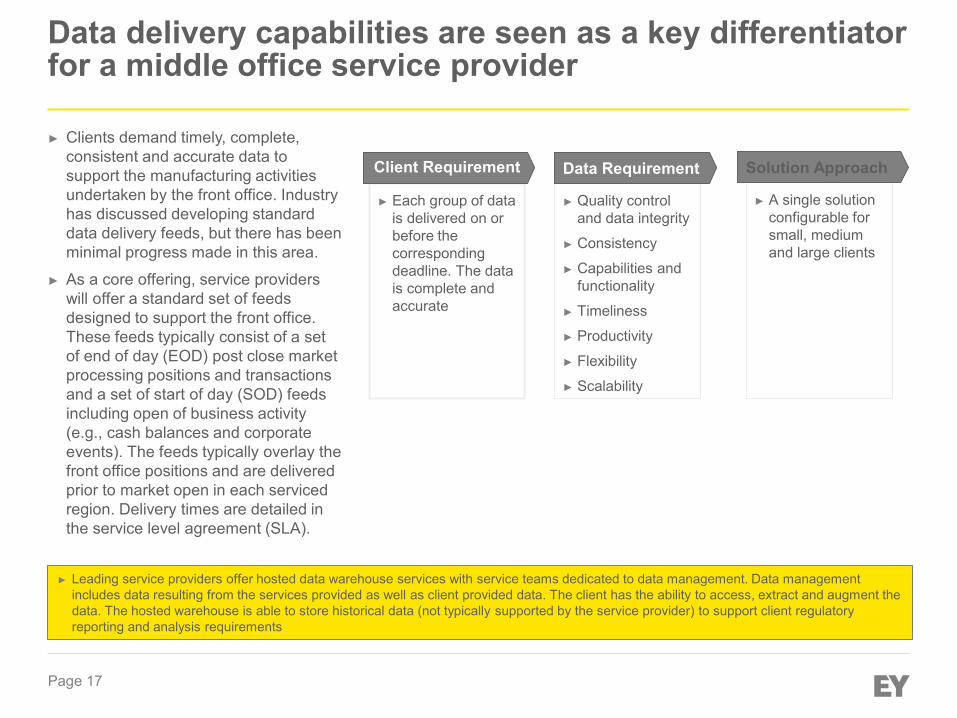

Data delivery capabilities are seen as a key differentiator for a middle office service provider

► Clients demand timely, complete, consistent and accurate data to support the manufacturing activities undertaken by the front office. Industry has discussed developing standard data delivery feeds, but there has been minimal progress made in this area.

► As a core offering, service providers will offer a standard set of feeds designed to support the front office. These feeds typically consist of a set of end of day (EOD) post close market processing positions and transactions and a set of start of day (SOD) feeds including open of business activity (e.g., cash balances and corporate events). The feeds typically overlay the front office positions and are delivered prior to market open in each serviced region. Delivery times are detailed in the service level agreement (SLA).

► Quality control and data integrity

► Consistency

► Capabilities and functionality

► Timeliness

► Productivity

► Flexibility

► Scalability

Data Requirement

► Each group of data is delivered on or before the corresponding deadline. The data is complete and accurate

Client Requirement

► A single solution configurable for small, medium and large clients

Solution Approach

► Leading service providers offer hosted data warehouse services with service teams dedicated to data management. Data management includes data resulting from the services provided as well as client provided data. The client has the ability to access, extract and augment the data. The hosted warehouse is able to store historical data (not typically supported by the service provider) to support client regulatory reporting and analysis requirements

Page 18

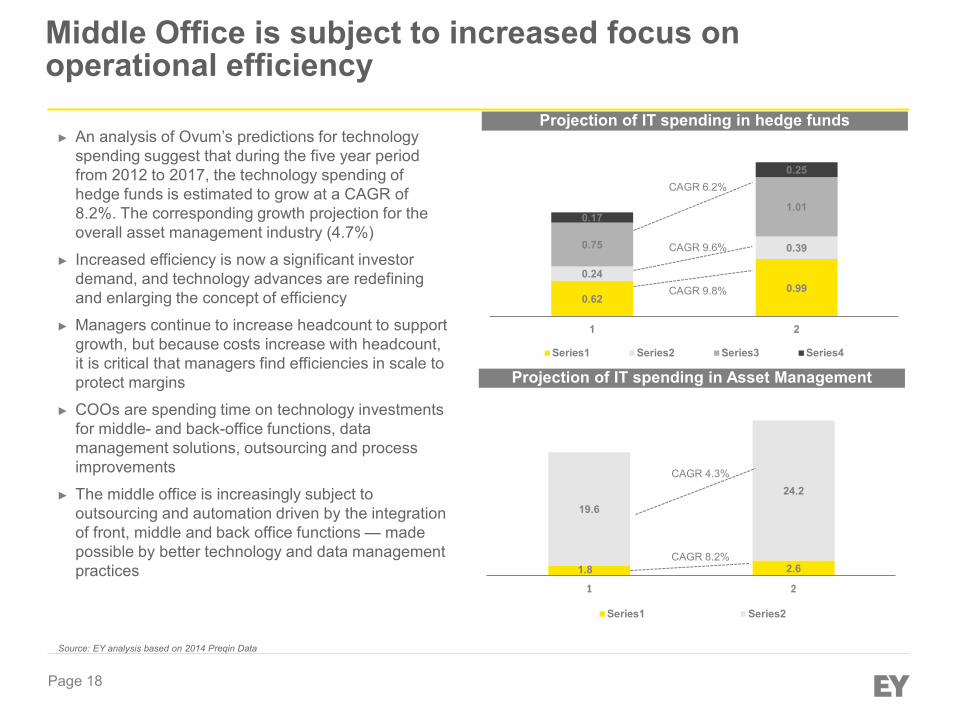

► An analysis of Ovum’s predictions for technology spending suggest that during the five year period from 2012 to 2017, the technology spending of hedge funds is estimated to grow at a CAGR of 8.2%. The corresponding growth projection for the overall asset management industry (4.7%)

► Increased efficiency is now a significant investor demand, and technology advances are redefining and enlarging the concept of efficiency

► Managers continue to increase headcount to support growth, but because costs increase with headcount, it is critical that managers find efficiencies in scale to protect margins

► COOs are spending time on technology investments for middle- and back-office functions, data management solutions, outsourcing and process improvements

► The middle office is increasingly subject to outsourcing and automation driven by the integration of front, middle and back office functions — made possible by better technology and data management practices

Source: EY analysis based on 2014 Preqin Data

Projection of IT spending in hedge funds

0.62 0.99

0.24

0.39 0.75

1.01 0.17

0.25

1 2

Series1 Series2 Series3 Series4

CAGR 6.2%

CAGR 9.6%

CAGR 9.8%

Projection of IT spending in Asset Management

1.8 2.6

19.6 24.2

1 2

Series1 Series2

CAGR 4.3%

CAGR 8.2%

Middle Office is subject to increased focus on operational efficiency

Page 19

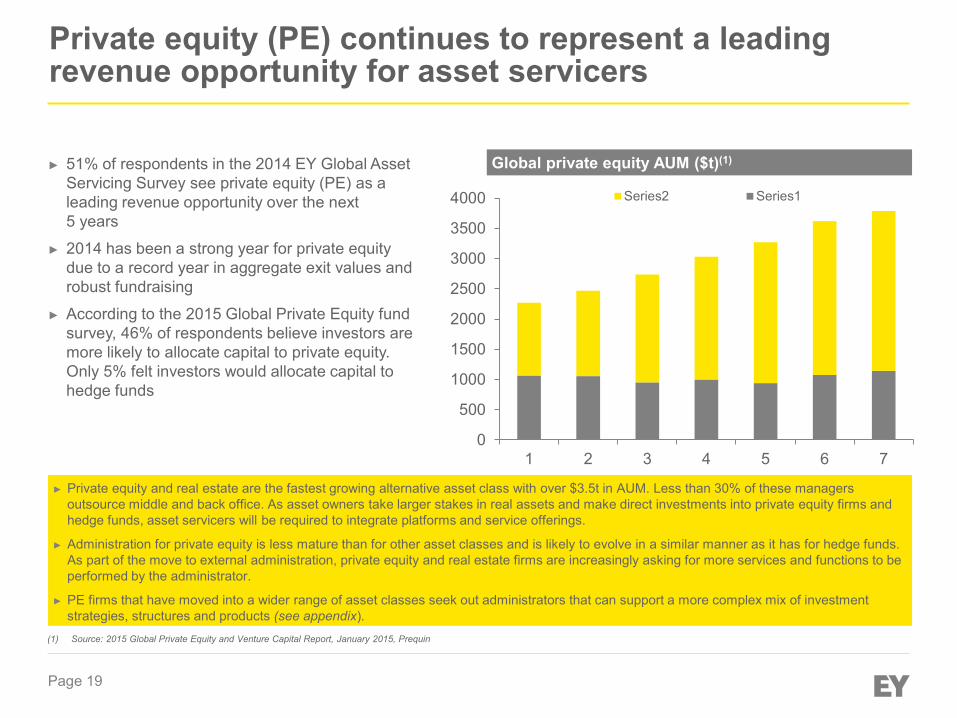

Private equity (PE) continues to represent a leading revenue opportunity for asset servicers

► 51% of respondents in the 2014 EY Global Asset Servicing Survey see private equity (PE) as a leading revenue opportunity over the next 5 years

► 2014 has been a strong year for private equity due to a record year in aggregate exit values and robust fundraising

► According to the 2015 Global Private Equity fund survey, 46% of respondents believe investors are more likely to allocate capital to private equity. Only 5% felt investors would allocate capital to hedge funds

Global private equity AUM ($t)(1)

47.0% 42.8% 34.9% 33.1% 30.2% 28.7% 29.7%

► Private equity and real estate are the fastest growing alternative asset class with over $3.5t in AUM. Less than 30% of these managers outsource middle and back office. As asset owners take larger stakes in real assets and make direct investments into private equity firms and hedge funds, asset servicers will be required to integrate platforms and service offerings.

► Administration for private equity is less mature than for other asset classes and is likely to evolve in a similar manner as it has for hedge funds. As part of the move to external administration, private equity and real estate firms are increasingly asking for more services and functions to be performed by the administrator.

► PE firms that have moved into a wider range of asset classes seek out administrators that can support a more complex mix of investment strategies, structures and products (see appendix).

(1) Source: 2015 Global Private Equity and Venture Capital Report, January 2015, Prequin

0

500

1000

1500

2000

2500

3000

3500

4000

1 2 3 4 5 6 7

Series2 Series1

Page 20

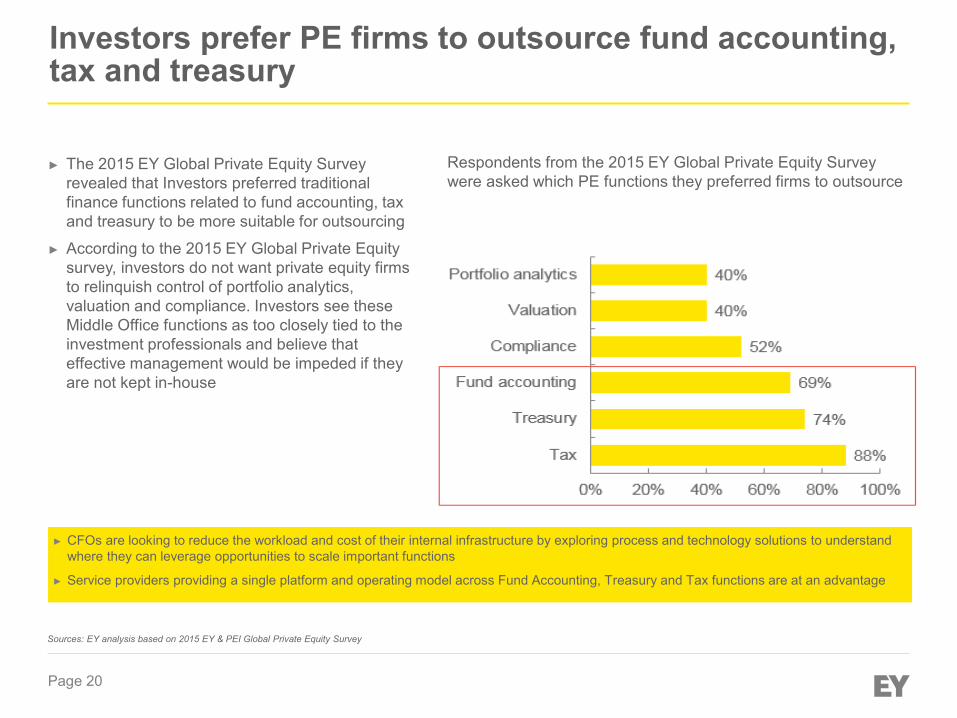

Investors prefer PE firms to outsource fund accounting, tax and treasury

► The 2015 EY Global Private Equity Survey revealed that Investors preferred traditional finance functions related to fund accounting, tax and treasury to be more suitable for outsourcing

► According to the 2015 EY Global Private Equity survey, investors do not want private equity firms to relinquish control of portfolio analytics, valuation and compliance. Investors see these Middle Office functions as too closely tied to the investment professionals and believe that effective management would be impeded if they are not kept in-house

► CFOs are looking to reduce the workload and cost of their internal infrastructure by exploring process and technology solutions to understand where they can leverage opportunities to scale important functions

► Service providers providing a single platform and operating model across Fund Accounting, Treasury and Tax functions are at an advantage

Sources: EY analysis based on 2015 EY & PEI Global Private Equity Survey

Respondents from the 2015 EY Global Private Equity Survey were asked which PE functions they preferred firms to outsource

Page 21

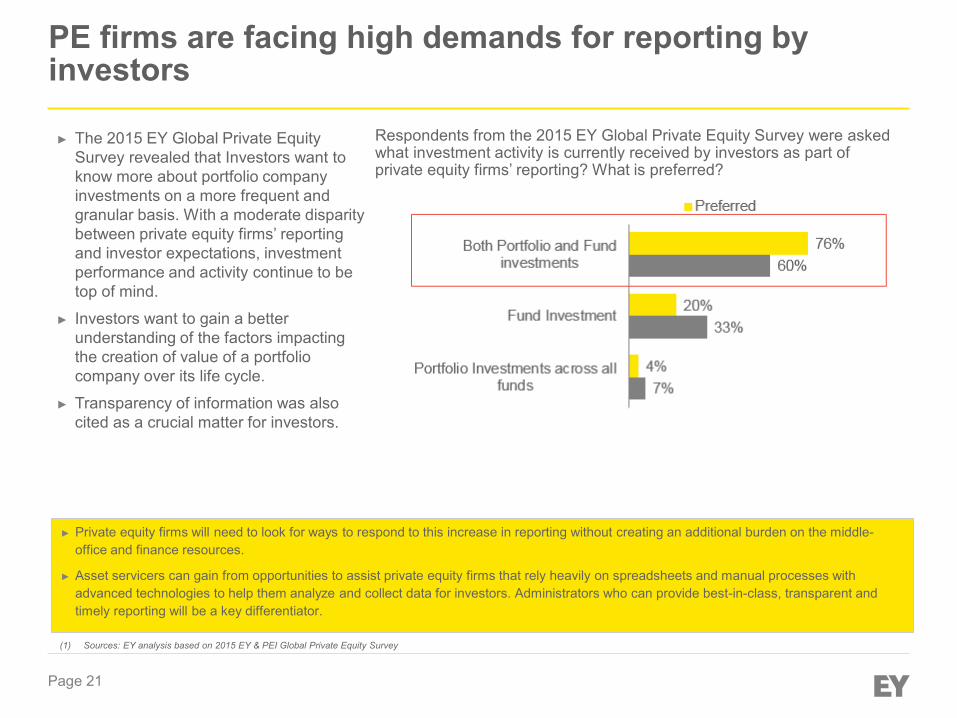

PE firms are facing high demands for reporting by investors

Respondents from the 2015 EY Global Private Equity Survey were asked what investment activity is currently received by investors as part of private equity firms’ reporting? What is preferred?

► Private equity firms will need to look for ways to respond to this increase in reporting without creating an additional burden on the middle- office and finance resources.

► Asset servicers can gain from opportunities to assist private equity firms that rely heavily on spreadsheets and manual processes with advanced technologies to help them analyze and collect data for investors. Administrators who can provide best-in-class, transparent and timely reporting will be a key differentiator.

► The 2015 EY Global Private Equity Survey revealed that Investors want to know more about portfolio company investments on a more frequent and granular basis. With a moderate disparity between private equity firms’ reporting and investor expectations, investment performance and activity continue to be top of mind.

► Investors want to gain a better understanding of the factors impacting the creation of value of a portfolio company over its life cycle.

► Transparency of information was also cited as a crucial matter for investors.

(1) Sources: EY analysis based on 2015 EY & PEI Global Private Equity Survey

Page 22

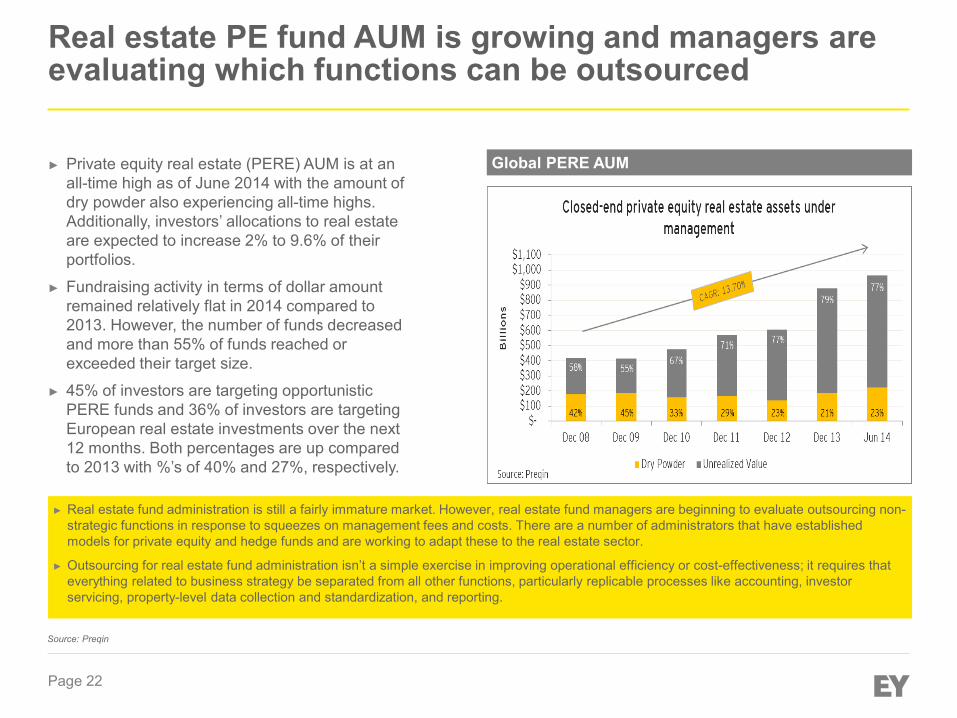

Real estate PE fund AUM is growing and managers are evaluating which functions can be outsourced

► Private equity real estate (PERE) AUM is at an all-time high as of June 2014 with the amount of dry powder also experiencing all-time highs. Additionally, investors’ allocations to real estate are expected to increase 2% to 9.6% of their portfolios.

► Fundraising activity in terms of dollar amount remained relatively flat in 2014 compared to 2013. However, the number of funds decreased and more than 55% of funds reached or exceeded their target size.

► 45% of investors are targeting opportunistic PERE funds and 36% of investors are targeting European real estate investments over the next 12 months. Both percentages are up compared to 2013 with %’s of 40% and 27%, respectively.

► Real estate fund administration is still a fairly immature market. However, real estate fund managers are beginning to evaluate outsourcing non-strategic functions in response to squeezes on management fees and costs. There are a number of administrators that have established models for private equity and hedge funds and are working to adapt these to the real estate sector.

► Outsourcing for real estate fund administration isn’t a simple exercise in improving operational efficiency or cost-effectiveness; it requires that everything related to business strategy be separated from all other functions, particularly replicable processes like accounting, investor servicing, property-level data collection and standardization, and reporting.

Source: Preqin

Global PERE AUM

Page 23

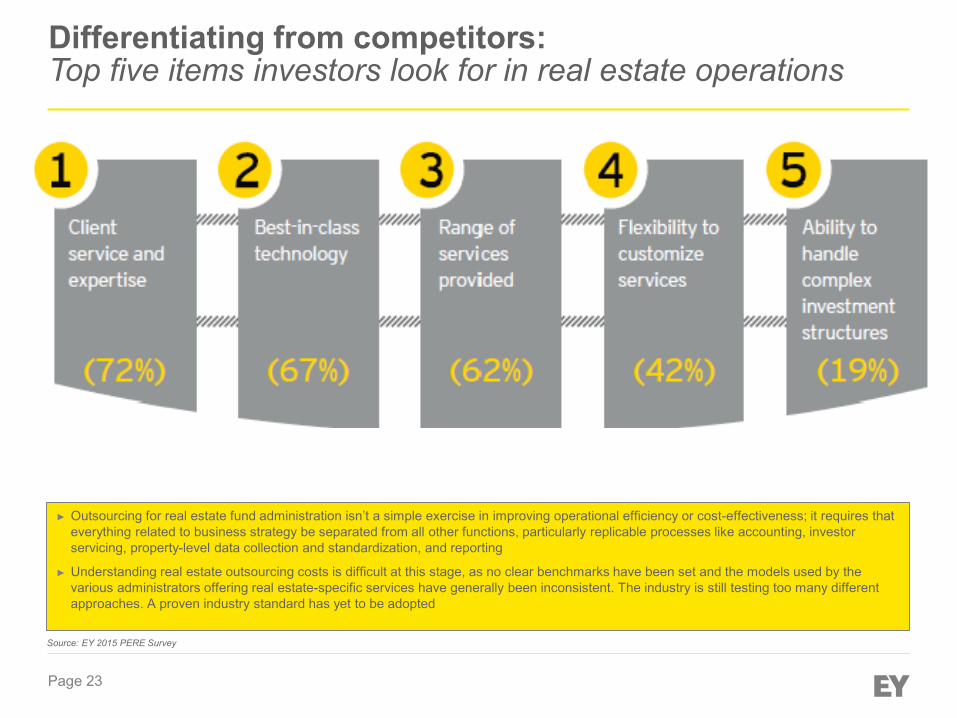

Differentiating from competitors: Top five items investors look for in real estate operations

► Outsourcing for real estate fund administration isn’t a simple exercise in improving operational efficiency or cost-effectiveness; it requires that everything related to business strategy be separated from all other functions, particularly replicable processes like accounting, investor servicing, property-level data collection and standardization, and reporting

► Understanding real estate outsourcing costs is difficult at this stage, as no clear benchmarks have been set and the models used by the various administrators offering real estate-specific services have generally been inconsistent. The industry is still testing too many different approaches. A proven industry standard has yet to be adopted

Source: EY 2015 PERE Survey

Page 24

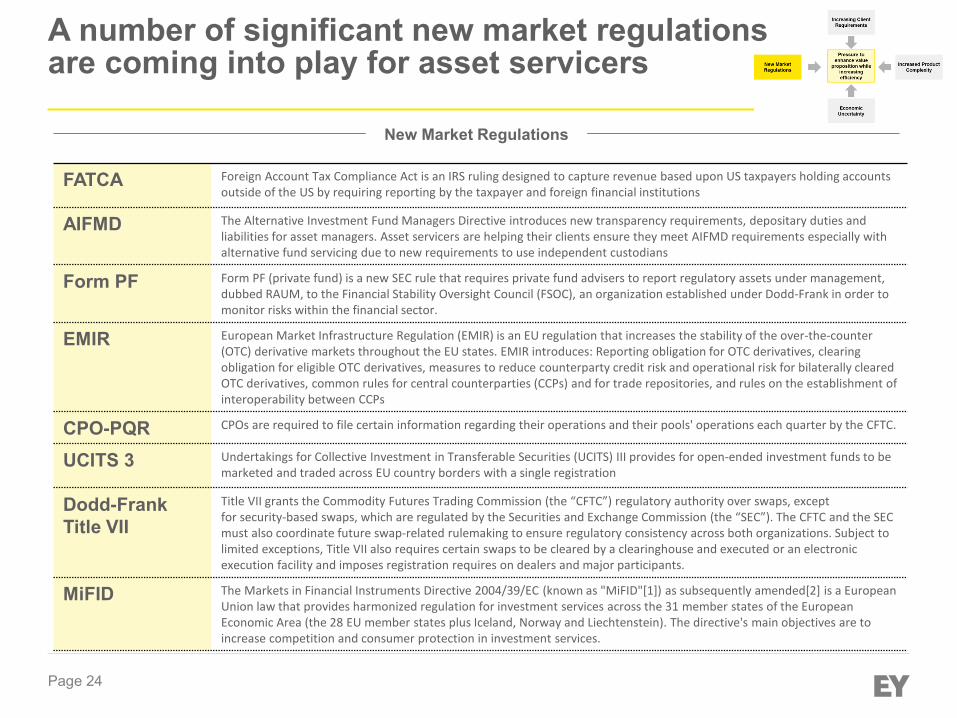

FATCA Foreign Account Tax Compliance Act is an IRS ruling designed to capture revenue based upon US taxpayers holding accounts outside of the US by requiring reporting by the taxpayer and foreign financial institutions

AIFMD The Alternative Investment Fund Managers Directive introduces new transparency requirements, depositary duties and liabilities for asset managers. Asset servicers are helping their clients ensure they meet AIFMD requirements especially with alternative fund servicing due to new requirements to use independent custodians

Form PF Form PF (private fund) is a new SEC rule that requires private fund advisers to report regulatory assets under management, dubbed RAUM, to the Financial Stability Oversight Council (FSOC), an organization established under Dodd-Frank in order to monitor risks within the financial sector.

EMIR European Market Infrastructure Regulation (EMIR) is an EU regulation that increases the stability of the over-the-counter (OTC) derivative markets throughout the EU states. EMIR introduces: Reporting obligation for OTC derivatives, clearing obligation for eligible OTC derivatives, measures to reduce counterparty credit risk and operational risk for bilaterally cleared OTC derivatives, common rules for central counterparties (CCPs) and for trade repositories, and rules on the establishment of interoperability between CCPs

CPO-PQR CPOs are required to file certain information regarding their operations and their pools' operations each quarter by the CFTC.

UCITS 3 Undertakings for Collective Investment in Transferable Securities (UCITS) III provides for open-ended investment funds to be marketed and traded across EU country borders with a single registration

Dodd-Frank Title VII

Title VII grants the Commodity Futures Trading Commission (the “CFTC”) regulatory authority over swaps, except for security-based swaps, which are regulated by the Securities and Exchange Commission (the “SEC”). The CFTC and the SEC must also coordinate future swap-related rulemaking to ensure regulatory consistency across both organizations. Subject to limited exceptions, Title VII also requires certain swaps to be cleared by a clearinghouse and executed or an electronic execution facility and imposes registration requires on dealers and major participants.

MiFID The Markets in Financial Instruments Directive 2004/39/EC (known as "MiFID"[1]) as subsequently amended[2] is a European Union law that provides harmonized regulation for investment services across the 31 member states of the European Economic Area (the 28 EU member states plus Iceland, Norway and Liechtenstein). The directive's main objectives are to increase competition and consumer protection in investment services.

New Market Regulations

A number of significant new market regulations are coming into play for asset servicers

Page 25

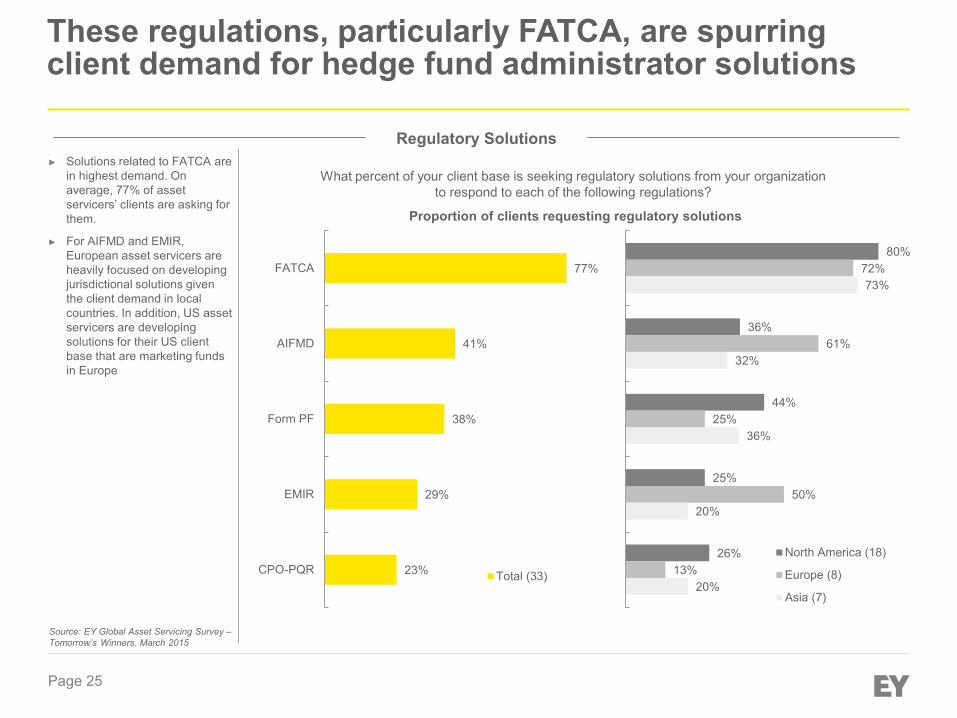

► Solutions related to FATCA are in highest demand. On average, 77% of asset servicers’ clients are asking for them.

► For AIFMD and EMIR, European asset servicers are heavily focused on developing jurisdictional solutions given the client demand in local countries. In addition, US asset servicers are developing solutions for their US client base that are marketing funds in Europe

Source: EY Global Asset Servicing Survey – Tomorrow’s Winners, March 2015

What percent of your client base is seeking regulatory solutions from your organization to respond to each of the following regulations?

Proportion of clients requesting regulatory solutions

80%

36%

44%

25%

26%

72%

61%

25%

50%

13%

73%

32%

36%

20%

20%

North America (18)

Europe (8)

Asia (7)

77%

41%

38%

29%

23%

FATCA

AIFMD

Form PF

EMIR

CPO-PQR Total (33)

Regulatory Solutions

These regulations, particularly FATCA, are spurring client demand for hedge fund administrator solutions

Page 26

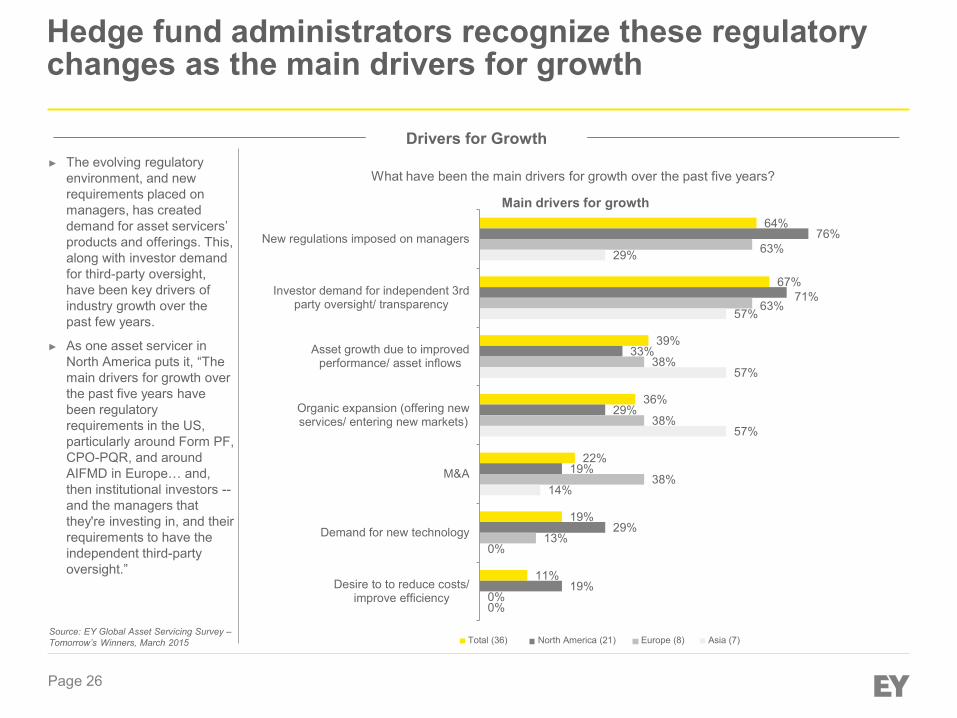

Hedge fund administrators recognize these regulatory changes as the main drivers for growth

► The evolving regulatory environment, and new requirements placed on managers, has created demand for asset servicers’ products and offerings. This, along with investor demand for third-party oversight, have been key drivers of industry growth over the past few years.

► As one asset servicer in North America puts it, “The main drivers for growth over the past five years have been regulatory requirements in the US, particularly around Form PF, CPO-PQR, and around AIFMD in Europe… and, then institutional investors -- and the managers that they're investing in, and their requirements to have the independent third-party oversight.”

Source: EY Global Asset Servicing Survey – Tomorrow’s Winners, March 2015 Asia (7)

What have been the main drivers for growth over the past five years?

Main drivers for growth

Total (36) North America (21) Europe (8)

64%

67%

39%

36%

22%

19%

11%

76%

71%

33%

29%

19%

29%

19%

63%

63%

38%

38%

38%

13%

0%

29%

57%

57%

57%

14%

0%

0%

New regulations imposed on managers

Investor demand for independent 3rdparty oversight/ transparency

Asset growth due to improvedperformance/ asset inflows

Organic expansion (offering newservices/ entering new markets)

M&A

Demand for new technology

Desire to to reduce costs/improve efficiency

Drivers for Growth

Page 27

Developing successful partnerships with local market players is crucial for real estate fund managers

Real estate considerations for fund administration functions: ► Complex legal entity structures ► Fee calculations ► Waterfall calculations (fund and deal-level) ► Debt financing ► REIT compliance and reporting ► GAAP, Tax, IFRS, etc. reporting ► Portfolio exposure reporting ► Performance measurement (i.e. real estate

return)

Additional considerations for gaining greater transparency at the property level with the goal of enhancing investor confidence, mitigating reputational risk and controlling costs: ► Management fee calculations ► Lease administration ► Cash management ► Vendor management ► Property and tenant insurance compliance

Hotel A, LLC

Hotel B, LLC

Plaza C, LLC

Office D, LLC

REIT, LLC

RE Fund,

LP

Offshore investors

LP investors

Separate account investors

Fund administration

Property management (including property accounting) Hotel A,

LLC Hotel B,

LLC Plaza

C, LLC Office D, LLC

JV Partner JV Partner

RE Partners GP, LLC

Offshore Feeder,

LP Separate Account

Sample real estate fund structure:

Page 28

Disclaimer

The following training slides are based on EY’s knowledge and in certain cases intellectual property (e.g., surveys, hot topics, industry trends). This reflects our understanding of the current industry environment & regulatory requirements upon date of delivery.

Opportunities NB Webinar Series

Tel: 1.506.453.5471 Toll free: 1.855.746.4662

Email: [email protected]