oil price recovery: what does that mean for steel? content below the line no content below the line...

TRANSCRIPT

No content below the line No content below the line

Oil Price Recovery: What does that mean for steel? Nicole J. Leonard, Senior Consultant Commodities Consulting, Bentek Energy

No content below the line No content below the line

Why I’m bearish short-term oil prices, bullish long-term prices

2

No content below the line No content below the line

Crude and liquids drive drilling and production activity, not much gas-by-rail activity

$- $2.00 $4.00 $6.00 $8.00

$10.00 $12.00 $14.00 $16.00 $18.00 $20.00

$/M

MB

tu E

quiv

alen

t

Historical Commodity Price Spreads

Brent WTI Mont Belvieu HH CAPP

3 Source: S&P Global Platts Analytics

No content below the line No content below the line

Bentek maintains bearish stance through 2017, remains bullish compared to the market

4

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$/bb

l

Bentek’s Brent Price Forecast

History Feb-15 Current

Source: S&P Global Platts Analytics, Bentek

Volatility driven by

supply uncertainty

No content below the line No content below the line

OPEC cuts seem to be on target, risks and duration create uncertainty and volatility

5

(0.60)

(0.50)

(0.40)

(0.30)

(0.20)

(0.10)

0.00

0.10

0.20

MM

b/d

Change in OPEC Production by Country (Oct – Jan)

Change in Production Proposed Cut

Proposed cut: 1.2 MMb/d Platts estimate: 0.9 MMb/d

Source: S&P Global Platts Estimates

No content below the line No content below the line

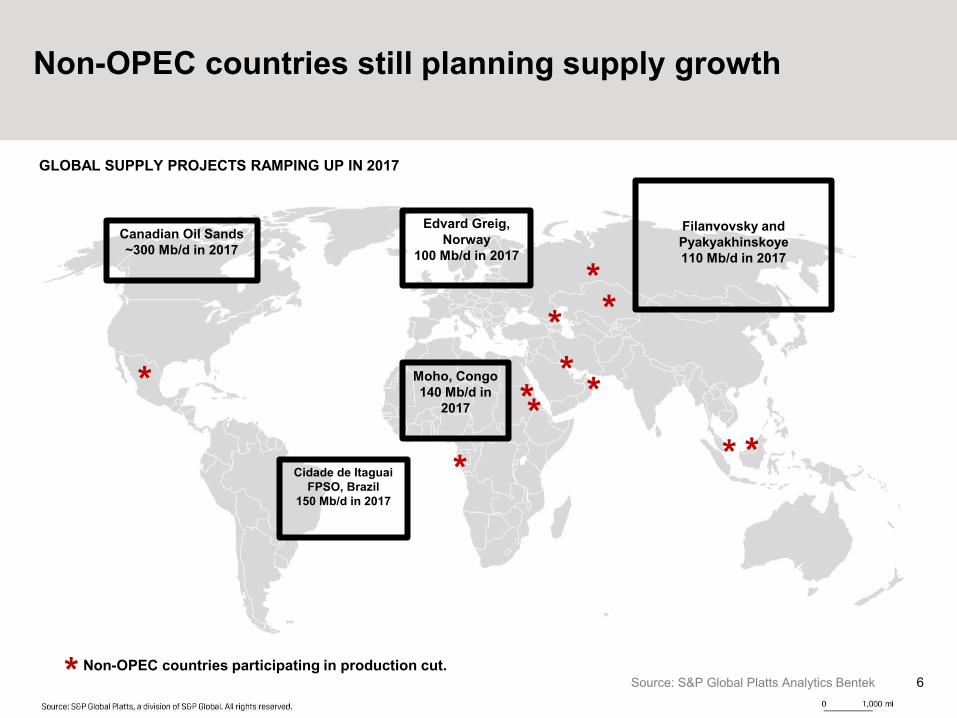

Non-OPEC countries still planning supply growth

6

Moho, Congo 140 Mb/d in

2017

Edvard Greig, Norway

100 Mb/d in 2017

Cidade de Itaguai FPSO, Brazil

150 Mb/d in 2017

Filanvovsky and Pyakyakhinskoye 110 Mb/d in 2017

GLOBAL SUPPLY PROJECTS RAMPING UP IN 2017

Canadian Oil Sands ~300 Mb/d in 2017

*

*

* * *

* * *

* * *

* Non-OPEC countries participating in production cut. Source: S&P Global Platts Analytics Bentek

No content below the line No content below the line

“But don’t worry, America still has more oil than we can use in 500 years.”

7

$25

$45

$65

$85

$105

$125

$/bb

l

Historical Brent Prices and Forward Curve

Hisory Forward Curve (Mar 3)

Source: S&P Global Platts Analytics, Bentek

No content below the line No content below the line

Bakken 40/+9 (30%)

Anadarko 113/+41 (57%)

Niobrara 26/+8 (44%)

Eagle Ford 74/+28 (61%)

Permian 318/+166 (112%)

Active rig count: Mar 3, 2017 / Change in rig count from Mar 4, 2016

Rigs return to oil plays on higher prices, rigs also return to gas plays on bullish market

TOTAL US 874/+353

(68%)

US Rig Count (Oct ’14)

2,143 -60% from

peak

Source: S&P Global Platts Analytics RigData 8

No content below the line No content below the line

Do breakevens even matter?

9

Henry Hub (Jan 19):

$3.26/MMbtu

Source: S&P Global Platts Analytics Bentek 9

No content below the line No content below the line

Prices remain above breakeven floor, yet production does not recover

10

$0

$1

$2

$3

$4

$5

$6

$7

50

55

60

65

70

75

Pric

e ($

/Mm

btu)

Prod

uctio

n (B

cf/d

)

US Natural Gas Production v Prices

ProductionHenry Hub Natural Gas PriceAvg Gas Breakeven Price

$0

$20

$40

$60

$80

$100

$120

5

6

6

7

7

8

8

9

9

10

10

Pric

e ($

/Mm

btu)

Prod

uctio

n (M

Mb/

d)

US Crude Oil Production v Prices

ProductionWTI Crude Oil PriceAvg Oil Breakeven Price

Source: S&P Global Platts Analytics

No content below the line No content below the line

What happened to efficiencies or has debt finally crippled US producers?

11

-$40

-$20

$0

$20

$40

$60

$80

$bn

Debt/Stock Issued v Repaid

Issuance of Common Stock Repurchase of Common Stock

Total Debt Repaid Total Debt Issued

Balance

Source: S&P Global Platts Analytics Bentek, S&P Capital IQ

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

$bn

US/Canada E&P Net Debt/EBITDA

No content below the line No content below the line

Public producers selling, not acquiring, selling mostly private money and independents

12

-$15-$10

-$5$0$5

$10$15$20

bn$

US/Canada Acquisitions v Divestitures

Divestitures Sale of Property Cash Acquisitions

0.00.51.01.52.02.53.03.54.04.5

bn$

Publically Announced Private M&A by Value

Source: S&P Global Platts Analytics Bentek, S&P Capital IQ

No content below the line No content below the line

Private money more suited toward quick “flip” of assets rather than long-term investments

13

$-

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Cum

. Inc

ome

($bn

)

Prod

uctio

n (M

b/d)

Oil Production from $300MM Investment

Shale (2-year, 5-rig program) Offshore Platform Cum. Income (Shale) Cum. Income (Offshore)

Source: S&P Global Platts Analytics Bentek

No content below the line No content below the line

Who’s investing in the long-term, low-decline assets?

14

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$/bb

l

Bentek’s Brent Price Forecast

History Feb-15 Current

Source: S&P Global Platts Analytics, Bentek

Prices incent production growth to meet demand growth

No content below the line No content below the line

IOC capex needed to drive global supply growth, but they have to make money first

15

0

5

10

15

20

25

30

35

40

45

BP Exxon Mobil

USD

bn

Quarterly Capital Expenditures

2012 2013 2014 2015 2016

Source: S&P Global Platts Analytics, Bentek, CapIQ

0

20

40

60

80

100

120

140

BP Exxon Mobil

USD

bn

Net Undeveloped Acreage

2012 2013 2014 2015 2016

No content below the line No content below the line

Exports drive natural gas demand growth of over 15 Bcf/d in just five years

16 Source: S&P Global Platts Analytics, Bentek

-5.0

0.0

5.0

10.0

15.0

20.0

Bcf

/d

US Natural Gas Demand Growth from 2016

Mexico ExportsLNG ExportIndustrialRes/CommPower Burn

No content below the line No content below the line

Higher gas prices on higher exports could drive drilling activity in dry gas plays

17

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$/M

Mbt

u

Henry Hub Price Forecast v NYMEX Forward Curve

Bentek NYMEX Forward Curve

Source: S&P Global Platts Analytics, Bentek

No content below the line No content below the line

What does this mean for steel?

18

No content below the line No content below the line

Three-year rig forecast suggests a return to 80% of previous rig count in high case

19

0200400600800

1,0001,2001,4001,600

# of

act

ive

rigs

RigData’s Historical and Forecast Rig Count

Actual Low Case Base Case High Case

Source: S&P Global Platts Analytics, Bentek

No content below the line No content below the line

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Anadarko Delaware DJ Basin Eagle Ford Marcellus Midland

Late

ral L

engt

h (fe

et)

Producer-Reported Average Lateral Lengths by Play

2013 2014 2015 2016

Lateral lengths increase 20% YOY, differs on geology of play, expected to increase

20 Source: S&P Global Platts Analytics, Bentek

No content below the line No content below the line

All drilling is getting deeper, resulting in 45% increase in steel demand per well since 2010

21

0

5,000

10,000

15,000

20,000

25,000

Wel

l Dep

th

Historical Oil/Gas Well Depths by Producing Area

Northeast Wet Gas Permian Delaware Denver-Julesburg Permian MidlandEagle Ford Bakken Average US

No content below the line No content below the line

Drilling activity not expected to reach shale-revolution levels, incremental 22,000 wells/year expected

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

# of

wel

ls d

rille

d

Historical and Forecasted Wells Drilled in North America

Drilled Forecast

Source: S&P Global Platts Analytics, Bentek, RigData 22

No content below the line No content below the line

Steel demand in West Texas expected to grow to 2014 levels, prime steel demand area for E&P

23

0.00.51.01.52.02.53.03.54.0

Mill

ion

Tons

Historical and Forecasted Steel Tube and Casing Demand in the Permian

Delaware NM Midland Delaware TX Permian Other

Assumptions: 2016 average well depth/lateral length held constant

No content below the line No content below the line

Line pipe demand could grow, pipeline projects at risk on less production

Source: Bentek

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2016 2017 2018 TBD

% o

f mile

s at

risk

Mile

s of

Lin

e Pi

pe

Miles of New Pipeline and Risk to Completion

Miles of Line Pipe % of miles at risk

No content below the line No content below the line

Energy demand consolidating in the US Gulf Coast, fewer long-haul pipelines needed

25

690 Mb/d of new pipeline capacity announced in the Permian this year

Eagle Ford rig count doubles since

October

Crude exports to grow to +1.0 MMb/d

by 2023

USGC accounts for 54% of total US crude demand

Refined products exports growing 15% every year

Natural gas liquids export and petchem

demand growth

No content below the line No content below the line

Key Takeaways

26

- Short-term oil market could be oversupplied once OPEC resumes production and if US private equity buoys US production.

- Long-term oil supply is being overlooked due to market optimism around US shale production, but investment is needed now for long-term supply growth to meet demand.

- Increasing natural gas demand in the US for exports as LNG and to Mexico could spur dry gas drilling and the need for new pipelines over the next ten years.

- Oil and gas wells are getting deeper and utilizing more steel than historically, though the number of wells drilled are unlikely to reach pre-price collapse levels.

- Less line pipe needed as US energy market centralizes in the US Gulf Coast, but a resurgence in drilling elsewhere would require more pipe.

No content below the line No content below the line

Questions?

Nicole Leonard, Project Manager, Oil & Gas Consulting

[email protected] Direct: (720) 264-6680