oil and gas sector

DESCRIPTION

Sector UpdatesTRANSCRIPT

OIL AND GAS SECTORFinshodhan 2

CONTENTS

Executive Summary India at advantage O&G – Various Segments with stats Key Players M&A Activity Growth Drivers Opportunities Recent News Conclusion

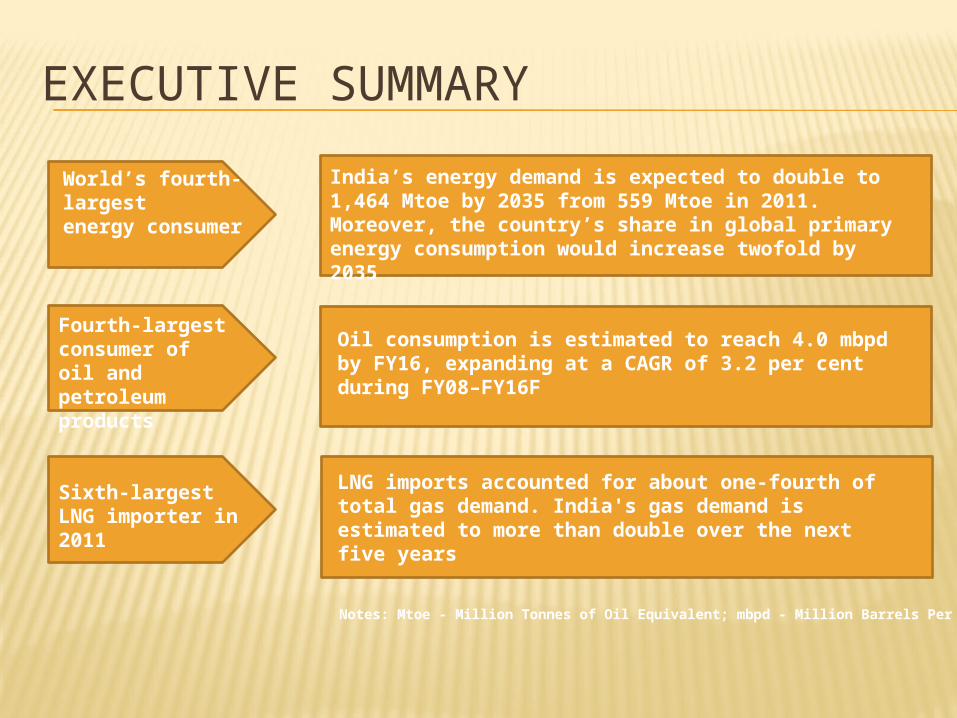

EXECUTIVE SUMMARY

World’s fourth-largestenergy consumer

Fourth-largest consumer of oil and petroleum products

Sixth-largest LNG importer in 2011

LNG imports accounted for about one-fourth of total gas demand. India's gas demand is estimated to more than double over the next five years

Oil consumption is estimated to reach 4.0 mbpd by FY16, expanding at a CAGR of 3.2 per cent during FY08–FY16F

India’s energy demand is expected to double to 1,464 Mtoe by 2035 from 559 Mtoe in 2011. Moreover, the country’s share in global primary energy consumption would increase twofold by 2035

Notes: Mtoe - Million Tonnes of Oil Equivalent; mbpd - Million Barrels Per Day

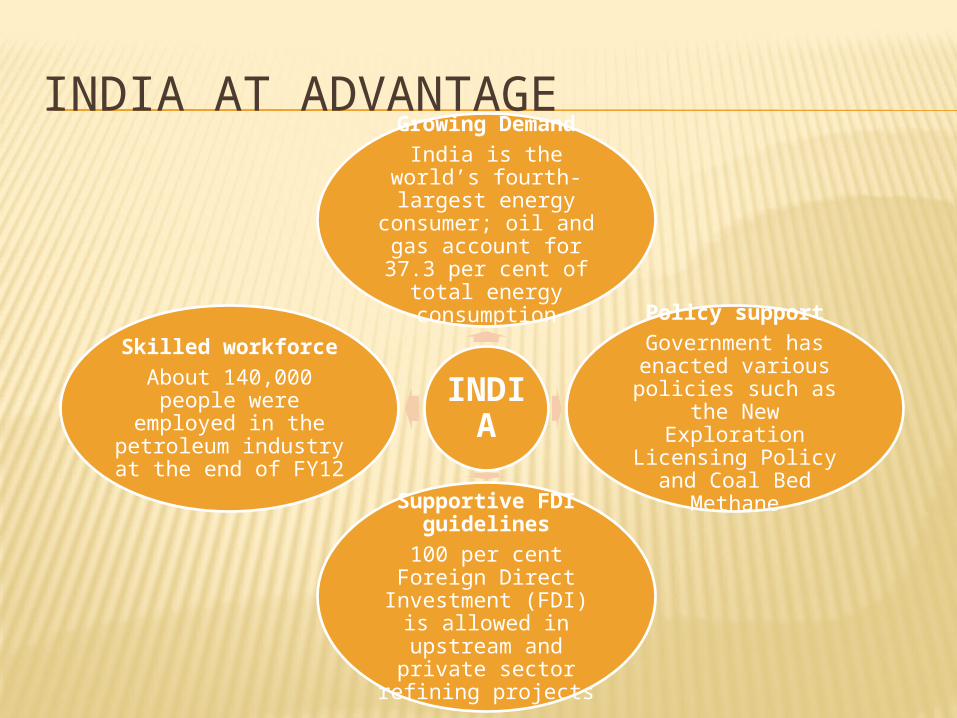

INDIA AT ADVANTAGE

INDIA

Growing DemandIndia is the world’s fourth-

largest energy consumer; oil and gas account for 37.3 per

cent of total energy consumption

Policy supportGovernment has enacted

various policies such as the New Exploration Licensing

Policy and Coal Bed Methane

Supportive FDI guidelines100 per cent Foreign Direct

Investment (FDI) is allowed in upstream and private sector

refining projects

Skilled workforceAbout 140,000 people were employed in the petroleum industry at the end of FY12

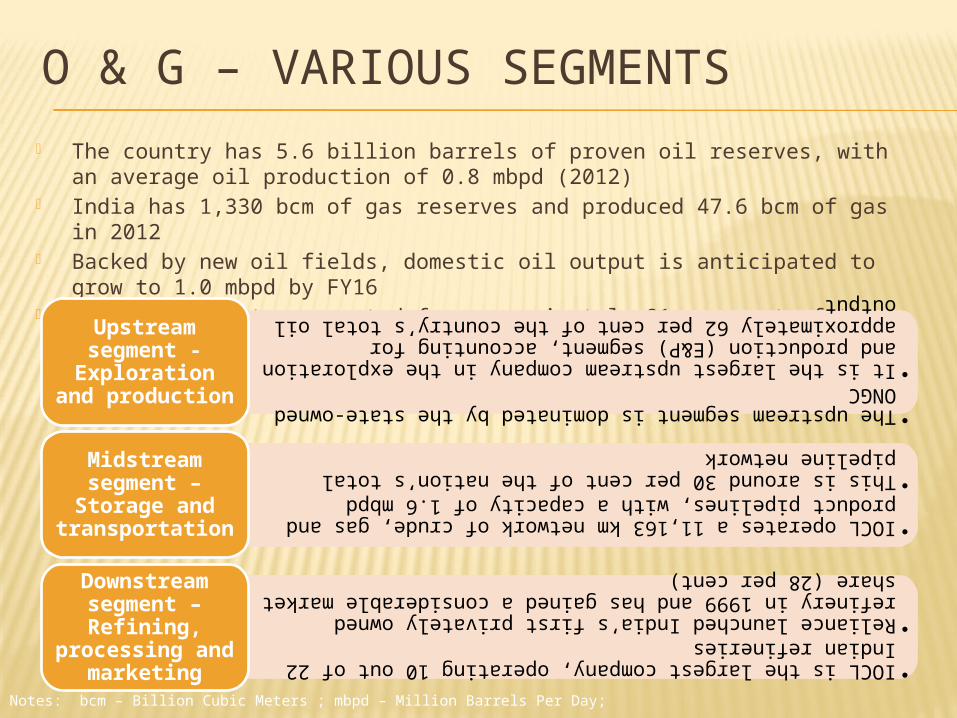

O & G – VARIOUS SEGMENTS

The country has 5.6 billion barrels of proven oil reserves, with an average oil production of 0.8 mbpd (2012)

India has 1,330 bcm of gas reserves and produced 47.6 bcm of gas in 2012 Backed by new oil fields, domestic oil output is anticipated to grow to 1.0 mbpd

by FY16 In FY12, imports accounted for approximately 81 per cent of the country’s total

oil demand

•The upstream segment is dominated by the state-owned ONGC

•It is the largest upstream company in the exploration and production (E&P) segment, accounting for approximately 62 per cent of the country’s total oil output

Upstream segment -

Exploration and production

•IOCL operates a 11,163 km network of crude, gas and product pipelines, with a capacity of 1.6 mbpd

•This is around 30 per cent of the nation’s total pipeline network

Midstream segment –

Storage and transportation

•IOCL is the largest company, operating 10 out of 22 Indian refineries

•Reliance launched India’s first privately owned refinery in 1999 and has gained a considerable market share (28 per cent)

Downstream segment – Refining,

processing and marketing

Notes: bcm – Billion Cubic Meters ; mbpd – Million Barrels Per Day;

SOME STATS With India developing gas-fired power stations, consumption is up more than

160 per cent since 1995 Domestic production accounts for more than three-quarters of total gas

consumption in the country Imports constitute the rest; in 2012, the share of imports was 22.0 per cent India increasingly relies on imported LNG; the country was the sixth-largest LNG

importer in 2011 and accounted for 5.3 per cent of global imports Total crude oil production was 38.0 mmt during FY12 ONGC, the largest crude oil producer in country, accounted for 62 per cent of

total crude oil production in India As Per Aranca Research, Demand is not likely to simmer down any time soon, given strong economic

growth and rising urbanisation; during FY2008–17F, gas consumption is likely to expand at a CAGR of 21.0 per cent

Backed by new oil fields, domestic oil output is anticipated to grow to 1.0 mbpd by FY16 from 0.8 mbpd in FY12

India’s LNG imports are forecast to increase at a CAGR of 33 per cent during 2012–17

Notes: * – Provisional; mmt – Million Metric Tonne, mmtpa – Million Metric Tonnes Per Annum

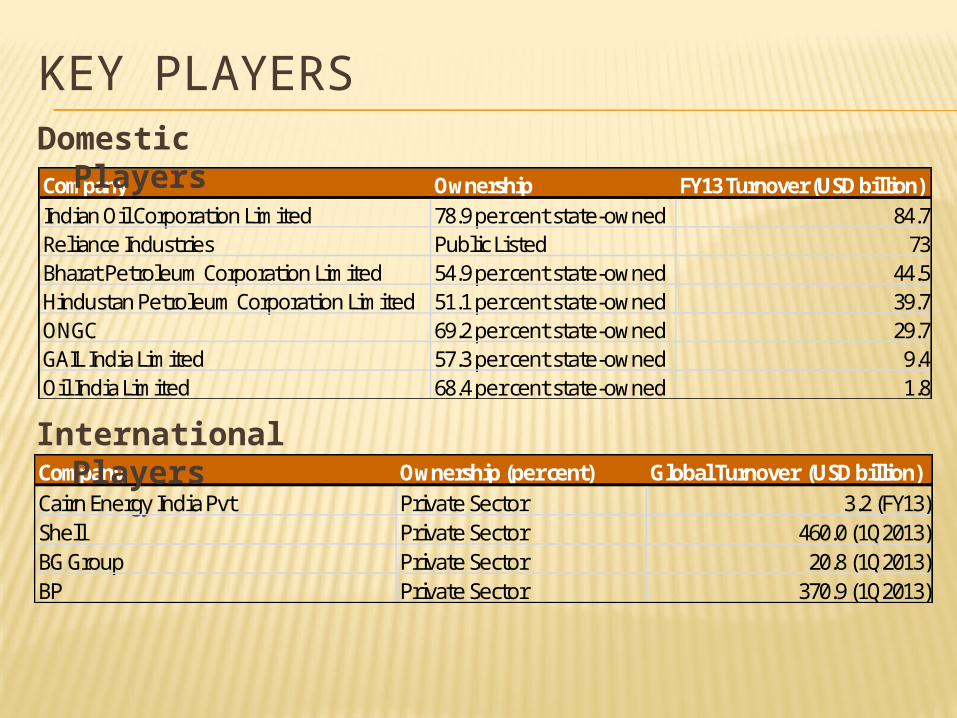

KEY PLAYERS

Company Ownership FY13 Turnover (USD billion)Indian Oil Corporation Limited 78.9 per cent state-owned 84.7Reliance Industries Public Listed 73Bharat Petroleum Corporation Limited 54.9 per cent state-owned 44.5Hindustan Petroleum Corporation Limited 51.1 per cent state-owned 39.7ONGC 69.2 per cent state-owned 29.7GAIL India Limited 57.3 per cent state-owned 9.4Oil India Limited 68.4 per cent state-owned 1.8

Company Ownership (per cent) Global Turnover (USD billion)Cairn Energy India Pvt Private Sector 3.2 (FY13)Shell Private Sector 460.0 (1Q2013)BG Group Private Sector 20.8 (1Q2013)BP Private Sector 370.9 (1Q2013)

Domestic Players

International Players

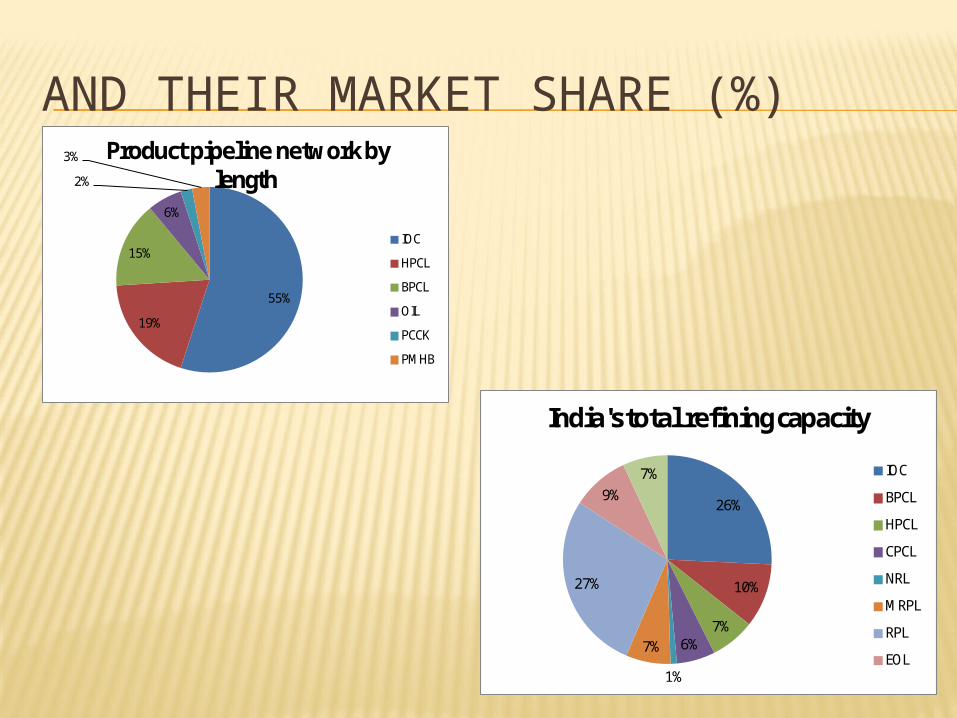

AND THEIR MARKET SHARE (%)

55%

19%

15%

6%

2%

3% Product pipeline network by length

IOC

HPCL

BPCL

OIL

PCCK

PMHB

26%

10%

7%6%

1%

7%

27%

9%7%

India's total refining capacity

IOC

BPCL

HPCL

CPCL

NRL

MRPL

RPL

EOL

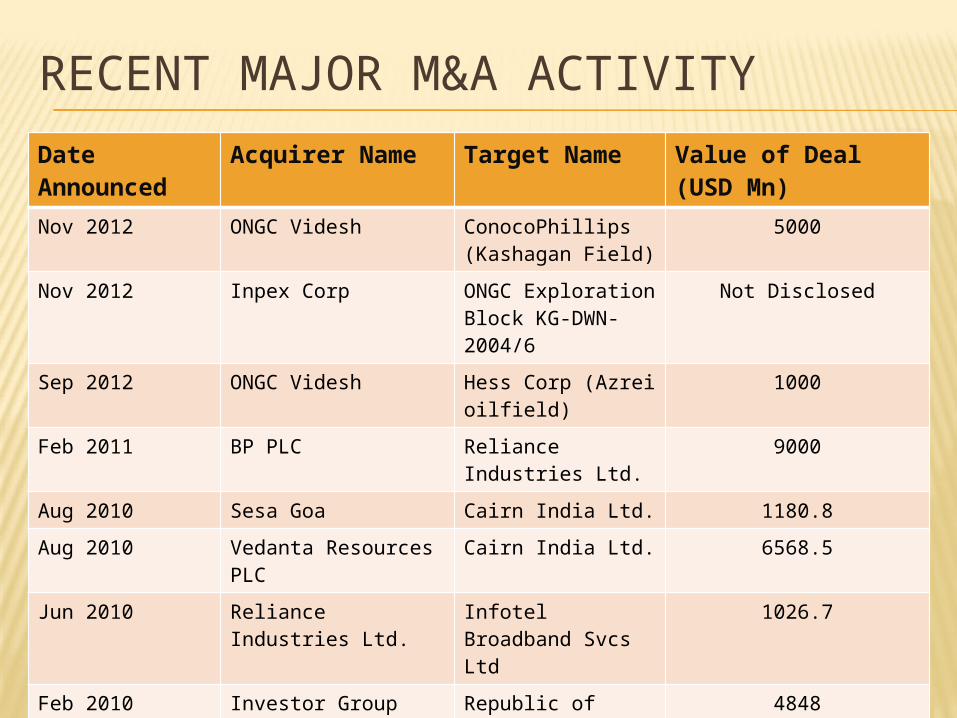

RECENT MAJOR M&A ACTIVITYDate Announced

Acquirer Name Target Name Value of Deal (USD Mn)

Nov 2012 ONGC Videsh ConocoPhillips (Kashagan Field)

5000

Nov 2012 Inpex Corp ONGC Exploration Block KG-DWN-2004/6

Not Disclosed

Sep 2012 ONGC Videsh Hess Corp (Azrei oilfield)

1000

Feb 2011 BP PLC Reliance Industries Ltd.

9000

Aug 2010 Sesa Goa Cairn India Ltd. 1180.8

Aug 2010 Vedanta Resources PLC

Cairn India Ltd. 6568.5

Jun 2010 Reliance Industries Ltd.

Infotel Broadband Svcs Ltd

1026.7

Feb 2010 Investor Group Republic of Venezuela-Carabobo

4848

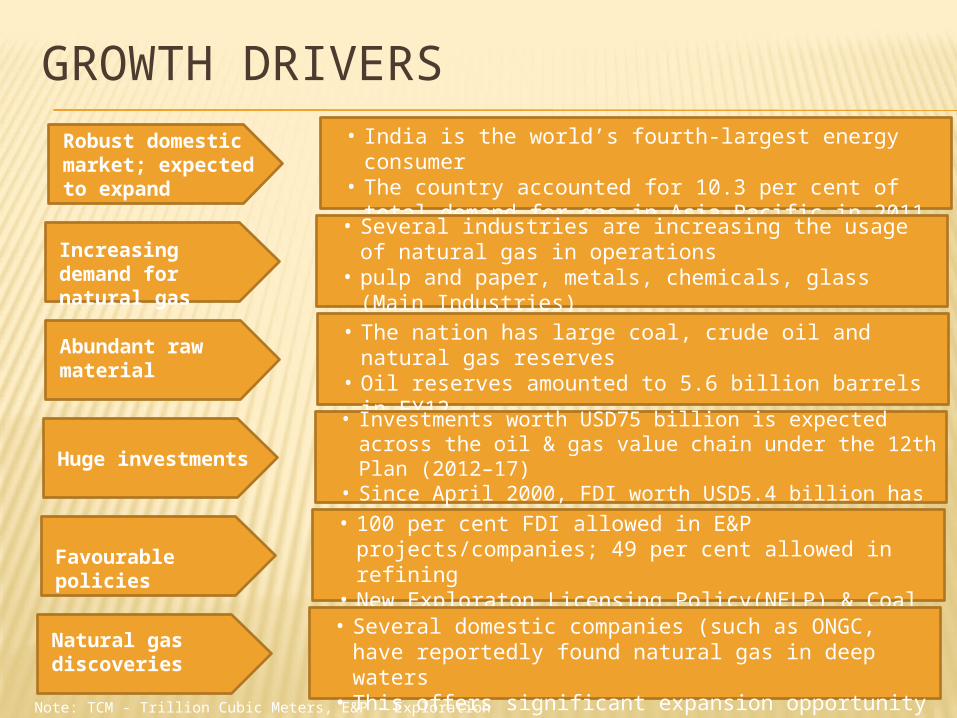

GROWTH DRIVERSRobust domestic market; expected to expand

• India is the world’s fourth-largest energy consumer• The country accounted for 10.3 per cent of total

demand for gas in Asia-Pacific in 2011

Increasing demand for natural gas

• Several industries are increasing the usage of natural gas in operations

• pulp and paper, metals, chemicals, glass (Main Industries)

Abundant raw material

• The nation has large coal, crude oil and natural gas reserves

• Oil reserves amounted to 5.6 billion barrels in FY12 • Natural gas reserves stood at 1.3 tcm in FY12

Huge investments

• Investments worth USD75 billion is expected across the oil & gas value chain under the 12th Plan (2012–17)

• Since April 2000, FDI worth USD5.4 billion has been invested in India’s petroleum and natural gas sectors

Favourable policies

• 100 per cent FDI allowed in E&P projects/companies; 49 per cent allowed in refining

• New Exploraton Licensing Policy(NELP) & Coal Bed Methane (CBM)

Natural gas discoveries

• Several domestic companies (such as ONGC, have reportedly found natural gas in deep waters

• This offers significant expansion opportunity for the next decade Note: TCM - Trillion Cubic Meters, E&P - Exploration and

Production

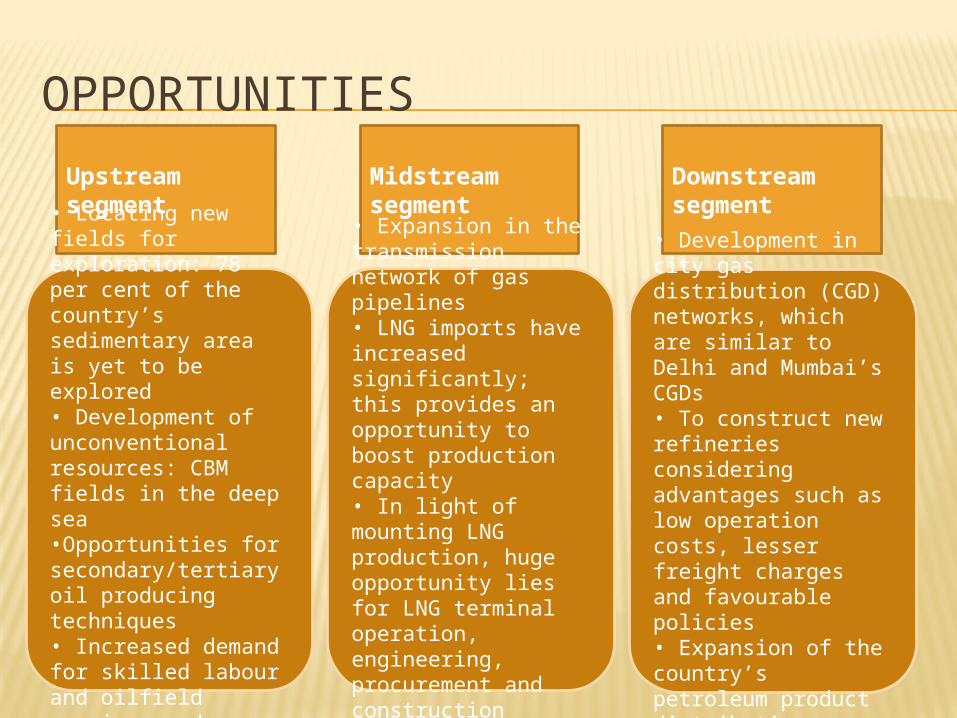

OPPORTUNITIES

Upstream segment

Midstream segment

Downstream segment

• Locating new fields for exploration: 78 per cent of the country’s sedimentary area is yet to be explored • Development of unconventional resources: CBM fields in the deep sea •Opportunities for secondary/tertiary oil producing techniques • Increased demand for skilled labour and oilfield services and equipment

• Expansion in the transmission network of gas pipelines • LNG imports have increased significantly; this provides an opportunity to boost production capacity • In light of mounting LNG production, huge opportunity lies for LNG terminal operation, engineering, procurement and construction services

• Development in city gas distribution (CGD) networks, which are similar to Delhi and Mumbai’s CGDs • To construct new refineries considering advantages such as low operation costs, lesser freight charges and favourable policies • Expansion of the country’s petroleum product distribution network

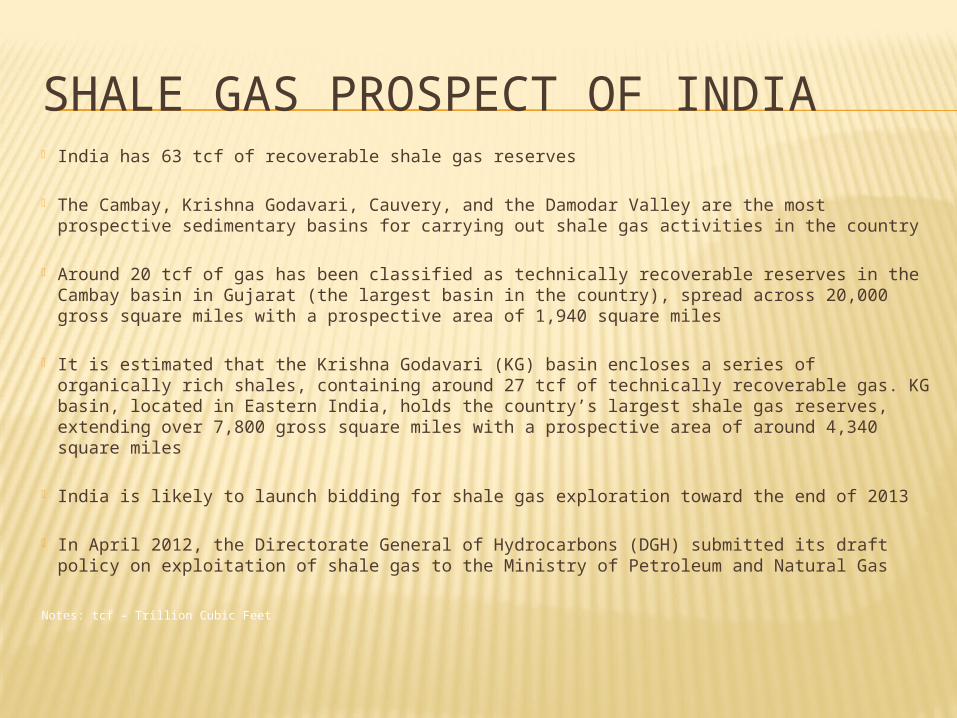

SHALE GAS PROSPECT OF INDIA India has 63 tcf of recoverable shale gas reserves

The Cambay, Krishna Godavari, Cauvery, and the Damodar Valley are the most prospective sedimentary basins for carrying out shale gas activities in the country

Around 20 tcf of gas has been classified as technically recoverable reserves in the Cambay basin in Gujarat (the largest basin in the country), spread across 20,000 gross square miles with a prospective area of 1,940 square miles

It is estimated that the Krishna Godavari (KG) basin encloses a series of organically rich shales, containing around 27 tcf of technically recoverable gas. KG basin, located in Eastern India, holds the country’s largest shale gas reserves, extending over 7,800 gross square miles with a prospective area of around 4,340 square miles

India is likely to launch bidding for shale gas exploration toward the end of 2013

In April 2012, the Directorate General of Hydrocarbons (DGH) submitted its draft policy on exploitation of shale gas to the Ministry of Petroleum and Natural Gas

Notes: tcf – Trillion Cubic Feet

RECENT NEWS RIL slapped with a fine of USD 800 mn for

failing to produce expected amount of gas Price of petrol is falling while diesel price is

rising. Since Jan13 the government raised diesel prices recently for the 10th time

Kuwait, Qatar & UAE eye stake in ONGC petchem project

News of recent tension in Syria leads to rise in crude prices

CONCLUSION The sector presents great opportunity for

economic growth of the country. Increase in exploration activity can help in

finding new reserves. Reducing the price and currency pressure in the

economy by reducing the dependence on imports.

Government policy needs to be uniform and clearly stated. Recent case of RIL vs. the state sour investor sentiment for the sector.

Rise in investment crucial for growth in the sector.

SOURCES BP Statistical Review, June 2012 BMI forecasts http://petroleum.nic.in/ World Oil Outlook 2012 US Energy Information Administration

(EIA) Crisil Research

THANK YOU

• YOGESHKUMAR MUNDADA

• BHUVANESH KUMAR