ogilvyred - dollars and sense of connectivity

TRANSCRIPT

1

T H E D O L L A R SS E N S E O F

C O N N E C T I V I T Y

OGILVYREDTHINK SERIES

VOLUME 2

M A R C H 2 0 1 6

AN

D

2

Meanwhile, Gens X, Y, and Z probably don’t

give much thought to the word, if any at

all. The difference in perspective exists for

many reasons, but the primary one is the

fundamental shift in the definition, scope,

and impact of telecommunications. This

report will explore the brand and marketing

opportunities presented by that shift and

cite potential scenarios for leveraging it.

BOOMERSBABY

THE WORD “TELECOMMUNICATIONS” MAY CONJURE LANDLINES, ANALOG DESK SETS, AND POSSIBLY EVEN A SHOE PHONE.

FOR

3

WATER ENERGY.

MOBILE CONNECTIVITY’S EXPLOSIVE GROWTH IN THE PAST 15 YEARS HAS MADE IT AKIN TO A UTILITY, LIKE

Telecommunications corporations

have essentially become utility

companies, providing something

that people need rather than

something they simply want for

entertainment, or to connect

with family and friends, perform

transactions, and do their jobs

on the go. With this in mind, it’s

interesting to note that access

to mobile devices worldwide is

growing much faster than access

to many of life’s bare essentials.

or

4

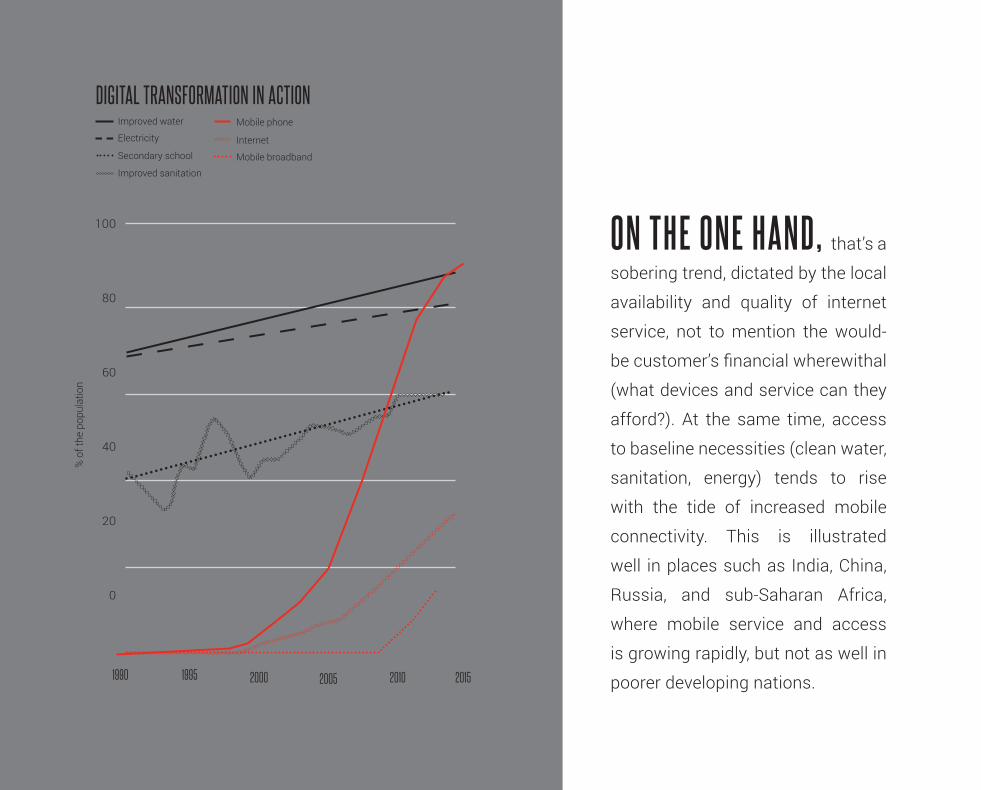

DIGITAL TRANSFORMATION IN ACTION

Source: World Development Report 2016: Digital Dividends, The World Bank.

% o

f the

pop

ulat

ion

100

80

60

40

20

0

1990 1995 2000 2005 2010 2015

ON THE ONE HAND, that’s a

sobering trend, dictated by the local

availability and quality of internet

service, not to mention the would-

be customer’s financial wherewithal

(what devices and service can they

afford?). At the same time, access

to baseline necessities (clean water,

sanitation, energy) tends to rise

with the tide of increased mobile

connectivity. This is illustrated

well in places such as India, China,

Russia, and sub-Saharan Africa,

where mobile service and access

is growing rapidly, but not as well in

poorer developing nations.

Mobile broadband

Internet

Mobile phone

Improved sanitation

Secondary school

Electricity

Improved water

5

By 2020, mobile technology will reach an

estimated value of $4 trillion worldwide,

which represents more than 4 percent of the

global Gross Domestic Product. Two factors

are driving the expected growth, in a simple

supply-and-demand equation: increased

mobile access among people who have

never been connected will produce more

(paying) subscribers to existing services,

and the drive to create more services to

meet the rising demand.

THAT MOBILE TECHNOLOGY CAN BE A FORCE FOR GOOD — AND NO DOUBT WHATSOEVER THAT IT IS AN ECONOMIC FORCE.

THERE’S LITTLE DOUBT

“Access to the Internet is a fundamental challenge of our time.”

- Mark Zuckerberg, Founder of Facebook

2,346

2008

3,210

2012

4,470

2019

2,798

2010

4,191

2017

3,636

2014

2,569

2009

4,020

2016

3,463

2013

4,596

2020

3,013

2011

4,336

2018

3,838

2015

(Millions)

UNIQUE SUBSCRIBERS BY REGION

Asia Pacific

Commonwealth of Independent States

Latin America

Europe

Middle East & North Africa

North America

Sub-Saharan Africa

Source: GSMA: The Mobile Economy, 2015

6

IN SHORT, mobile connectivity can

provide the means to fulfill fundamental needs, like

healthcare, education, and social interaction, as well

as to utilize advanced services such as financial

support, business information, real-time navigation,

and banking and commercial transactions. But giving

more people the ability to live more efficiently and

increase their personal wealth is just part of mobile

connectivity’s promise. The growth of machine-to-

machine (M2M) communication has created billions

of new connection points among the internet of

things (IoT), from smart-home devices (thermostats,

fridges, televisions, etc.), to connected cars and

agricultural machinery. More connection points

means more interactions, which in turn creates more

brand and marketing opportunities.

This produces yet another

potential economic driver: The

network of connection points is

growing exponentially, and with

it the demand for more data

bandwidth and IP addresses, as

well as lower latency.

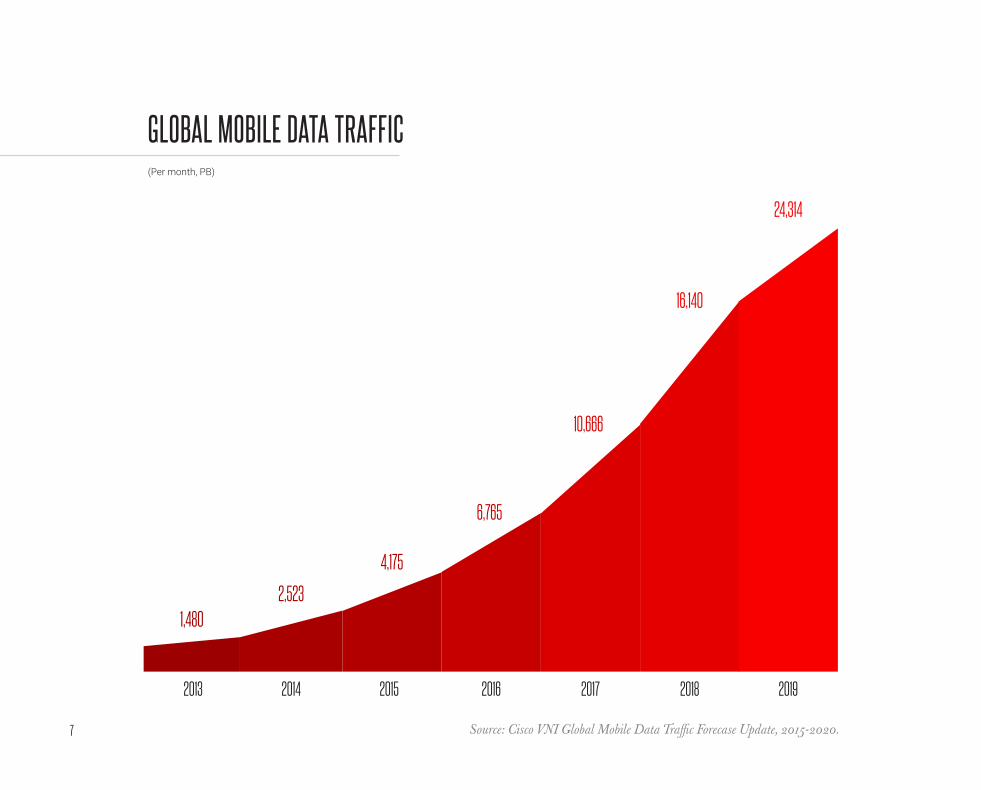

7

GLOBAL MOBILE DATA TRAFFIC(Per month, PB)

2013 2014 2015 2016 2017 2018 2019

Source: Cisco VNI Global Mobile Data Traffic Forecase Update, 2015-2020.

1,4802,523

4,175

6,765

10,666

16,140

24,314

8

While continuing to be

profitable businesses, carriers

face an increasing challenge

to financially support (e.g.

through investments) the

increasing demand for data and

voice services. Infrastructure

costs in developing markets

are dropping, thanks to the

development of more efficient

hardware. But that’s just one

part of the economic equation,

and carriers now face a

conundrum. The increase

in demand creates more

connection points and data,

which in turn require more

infrastructure. The fundamental

problem is that the increase in

demand doesn’t guarantee the

returns necessary to justify the

investment in infrastructure

growth. This is especially

true because many of the

new users (that is, the people

and businesses creating the

demand) that carriers would

like to bring online are low-

income. Carriers rely on a

certain average revenue per

user (ARPU) not only to make

a profit but also to invest in

infrastructure to ensure growth.

Things start to unravel if

users are ultimately unable or

unwilling pay for the increase

in connections and data

bandwidth at the carriers’

required rate.

9

While the benefits of connectivity

are well documented, actual

access, together with the desired

bandwidth and data for mobile

devices, is restricted by a diverse

set of factors. They range in scale

from personal (an individual’s

ability to pay for service) to

infrastructure (insufficient reach

and bandwidth, and regulatory

constrictions). A complex network

of industry players has built the

infrastructure to enable wide-

spread access as well as the

required bandwidth. At the core

of this network sit mobile carriers,

or Mobile Network Operators

(MNOs), that typically own the

end-consumer relationship for

businesses and individuals.

1 0

For non-telco brands and marketers,

everything noted to this point provides

important context for their ultimate goal:

to engage with customers on their mobile

devices. However, the marketing industry

still struggles with finding the right value

offer to a customer, value which would make

consumers engage with a brand. Marketers

have struggled with developing the right

engagement mechanisms for existing users

(mobile display ads only take you so far and

don’t yet leverage the creative potential that

mobile broadband offers). The emergence

of a new audience presents an additional

challenge, one whose solution is highly

unlikely to be found by traditional means.

And so, marketers should not

simply apply legacy advertising

mechanics to a fundamentally

new engagement ecosystem. New

strategies are required to leverage

mobile connections in a more

meaningful and effective way.

1 1

This paper, the second in the REDThink

series by OgilvyRED, acts as springboard for

companies, vertical markets, and brands, which

will directly or indirectly benefit from enhanced

connectivity around the world. It will draw a

high-level picture of the current ecosystem and

its constraints. It will also highlight innovative

concepts currently being used to meet the

challenge of providing internet accessibility

through mobile broadband. We hope to provide

thought starters for carriers as well as for

marketers on how to think about new ways

to create winning propositions that benefit

customers, carriers, and other members of the

connectivity ecosystem.

1 2

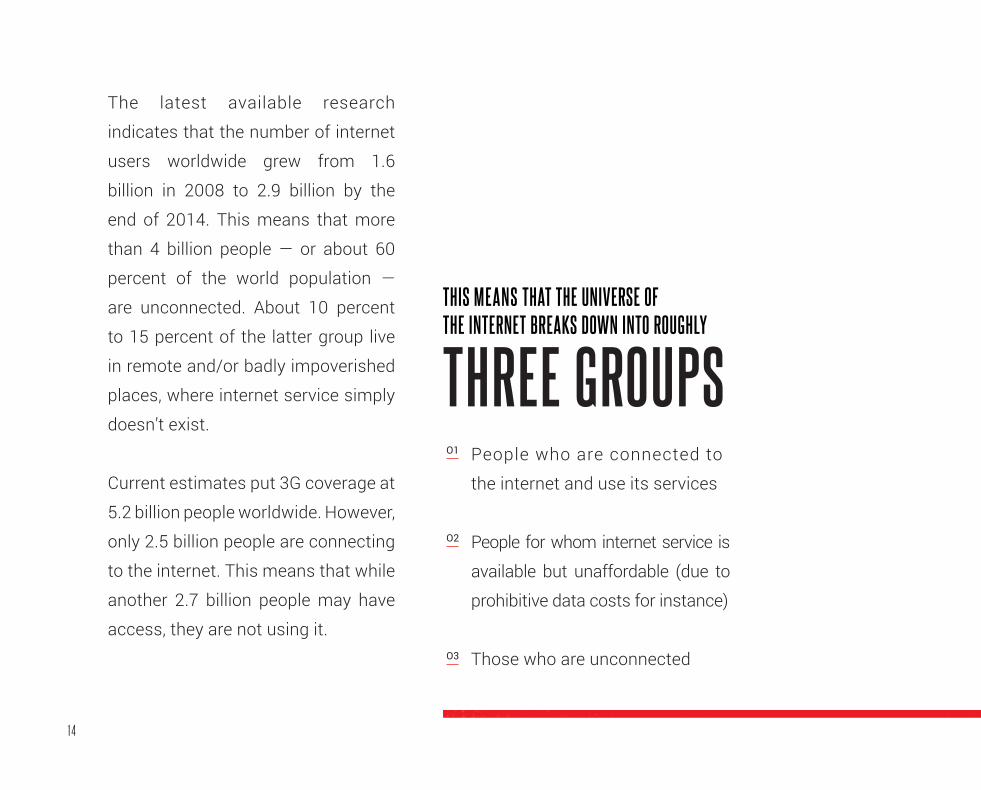

1WHO’S CONNECTED,WHO ISN’T,

AT WHAT COST?

1 3

17 B I L L I O N

Regardless of which source you believe — the United

Nations or the U.S. Census Bureau — the world population

stands at about 7 billion. Mobile broadband has emerged as

a standard utility in technologically developed markets, but

elsewhere it is scarce to nonexistent.

1 4

THREE GROUPSPeople who are connected to

the internet and use its services

People for whom internet service is

available but unaffordable (due to

prohibitive data costs for instance)

Those who are unconnected

THIS MEANS THAT THE UNIVERSE OF THE INTERNET BREAKS DOWN INTO ROUGHLY

O1

O2

O3

The latest available research

indicates that the number of internet

users worldwide grew from 1.6

billion in 2008 to 2.9 billion by the

end of 2014. This means that more

than 4 billion people — or about 60

percent of the world population —

are unconnected. About 10 percent

to 15 percent of the latter group live

in remote and/or badly impoverished

places, where internet service simply

doesn’t exist.

Current estimates put 3G coverage at

5.2 billion people worldwide. However,

only 2.5 billion people are connecting

to the internet. This means that while

another 2.7 billion people may have

access, they are not using it.

1 5

Mobile costs hit poor

nations the hardest. As

a result, people decline

data plans, and carriers

lack profits to improve

networks.

THE BITE OF MEGABYTES

Brazil

China

U.S.

Turkey

India 39.25

15.2

13.2

12.83

8.79

HOURS WORKED TO PAY A MOBILE PHONE BILL

India

Brazil

China

U.S.

Turkey

1,240

355

200

76

286

HOURS WORKED TO PURCHASE A SMARTPHONE

India

Brazil

China

U.S.

Turkey

57

43

77

96

49

% OF SMARTPHONE USERS WITH A DATA PLANBased on Minimum Wage

Sources: McKinsey, ITU, Nielsen,Forbes August 2015

1 6

But even in developed markets,

the ability to pay for connectivity

is neither a given nor factored into

household budgets. Consumers

are very conscious of their data

allowances and turn to wifi as

often as possible.

Consider the statistics:

Among the smartphone-dependent

population of the United States, 51

percent of users report exceeding

their mobile plan’s data allowance;

among those people, 15 percent say

they “frequently” tap out of data.

It’s safe to conclude that restrictive

allowances are a significant

bottleneck for people who rely

heavily on mobile-data usage.

About 20 percent of smartphone

users say they considered it a

financial burden.

AFFORDABILITY AND DISCRETIONARY INCOME ARE FUNDAMENTAL DETERMINING FACTORS FOR BEING CONNECTED.

In developing nations,

1 7

In many cases the costs are

“invisible.” If a user has a contract

that charges $60 a month for up

to 6GB of data, a 360MB game

app costs $3.60 for the download

alone. Streaming Netflix for an hour

under the same plan, at a medium

download rate, costs about $7.

The people who complain about the

high cost of using a smartphone

are not simply whining. With the

widening income gap and major

carriers increasingly targeting high-

income customers with plans that

cost $60-plus a month for a single

device, a significant portion of the

population in developing markets is

very self-conscious as to when they

use their data plan vs. tapping into

the increasing amount of free wifi

options. This situation is projected

to worsen, as more devices per

household become connected at the

same time that the per-household

cost of connectivity increases.

1 8

THE BOTTOM LINE IS that the cost of

being connected is a significant

line item in the household budget

-- one that proves prominent on

consumers’ minds to the extent that

it can potentially be prohibitive to

certain segments of the population.

1 92WINNERS

LOSERSMOBILE-CONNECTIVITYECOSYSTEM

IN THE

2 0

2is in some respects a social equalizer, in many ways it benefits some more than others. To understand this apparent contradiction, it’s helpful to know the three basic components of, or players in, the mobile-connectivity ecosystem:

WHILE MOBILE CONNECTIVITY

2 1

INFRASTRUCTURE PROVIDERS, AND IN PARTICULAR,

CARRIERS.

Carriers — also called telcos or providers — play the most pivotal role in the ecosystem. They include such companies as Vodafone, Verizon, Airtel, Claro, Singtel, and SK Telecom. The carriers’ power (and thus their value) derives from acquiring or licensing access to the infrastructure that connects consumers with providers of services and content. The providers’ primary function is the very thing that enables mobile connectivity. They operate the network and provide the access point for devices and consumers.

O1

2 2

PROVIDERS OFSERVICES AND

CONTENT.

This diverse group includes services such as entertainment companies (Netflix), finance and payment services (PayPal), information providers (news outlets, directories, maps, traffic), educational products, ecommerce outlets, OTT messaging or social media platforms. While the majority of interactions of services and content involve actual consumers, there will be a dramatic increase in machine-to-machine (M2M) protocols as more “objects” beyond mobile devices go online (see IoT). To date, content and service providers have not played a key role in providing access; rather, they have simply relied on the connectivity supplied by carriers, to serve consumers.

O2

2 3

CONSUMERS OFSERVICES AND

CONTENT.

“Consumers” is a bit of a misnomer in this context. For the most part, in the mobile-connectivity ecosystem, the term applies to individuals, businesses, or government entities that benefit from the services provided. Consumers have paid carriers for baseline connectivity, and occasionally for access to select services, based on the providers’ service model. With the advent and growth of the IoT — essentially, machines connecting to the infrastructure — we expect a dramatic increase in the exchange of data between machines in the IoT to either individuals (this is called an M2P interface) or machines (as mentioned above, this is an M2M connection).

O3

2 4

INFRASTRUCTURE

CONSUMPTION SERVICES & CONTENTEducation, Health Care, Navigation,

Entertainment, Cities, Financial

Services, Messaging & Social

Individual, Business, IoT

Carriers, Infrastructure Providers

CONSUMERS OFSERVICES & CONTENT

2 5

are multidimensional and well documented on several geographical scales: local, city, regional (often, rural versus urban), and national.

The extent of a nation’s mobile connectivity, and the benefits arising from that connectivity, depends on many factors. Figuring into the equation are

things such as the size and health of a nation’s economy (often, as measured by the GDP and per-capita income); literacy, poverty, and employment rates; technological progress; and a variety of socioeconomic and cultural factors, such as racial and gender equality and access to healthcare.

THE BENEFITS OFMOBILE CONNECTIVITY

“Around 400 million people in the last year got a smartphone. If you think that’s a big deal, imagine the impact on that person in the developing world.”

- Eric Schmidt, Executive Chairman, Google

2 6

In developing nations with low connectivity, programs to increase connectivity can show dramatic

results. For instance, access to information and transparency about political instability, nutrition, the

environment, and living conditions can help predict the outbreak of an infectious disease. A nation’s

agricultural production and economy can improve quickly when mobile connectivity gives farmers

access to information about such basic things as weather forecasts and commodity prices. Villages and

communities that emerge from isolation thanks to mobile connectivity are often able to introduce better

health and education programs.

2 7

In developed nations, the benefits of higher bandwidth may seem more trivial, providing

such luxuries as access to video streaming or graphics-and-data–intensive mobile

games. Higher bandwidth can also instantly improve productivity in businesses that

rely on data-heavy formats. Research by companies such as Google and Huawei

estimates that “increasing the internet connectivity by 10 percent in a country increases

the GDP by up to 1.4 percent.”

2 8

Smart cities constitute another focal point of development, with the promise of faster predictive emergency response, more efficient energy management, better traffic control and more effective municipal servicing.

2 9

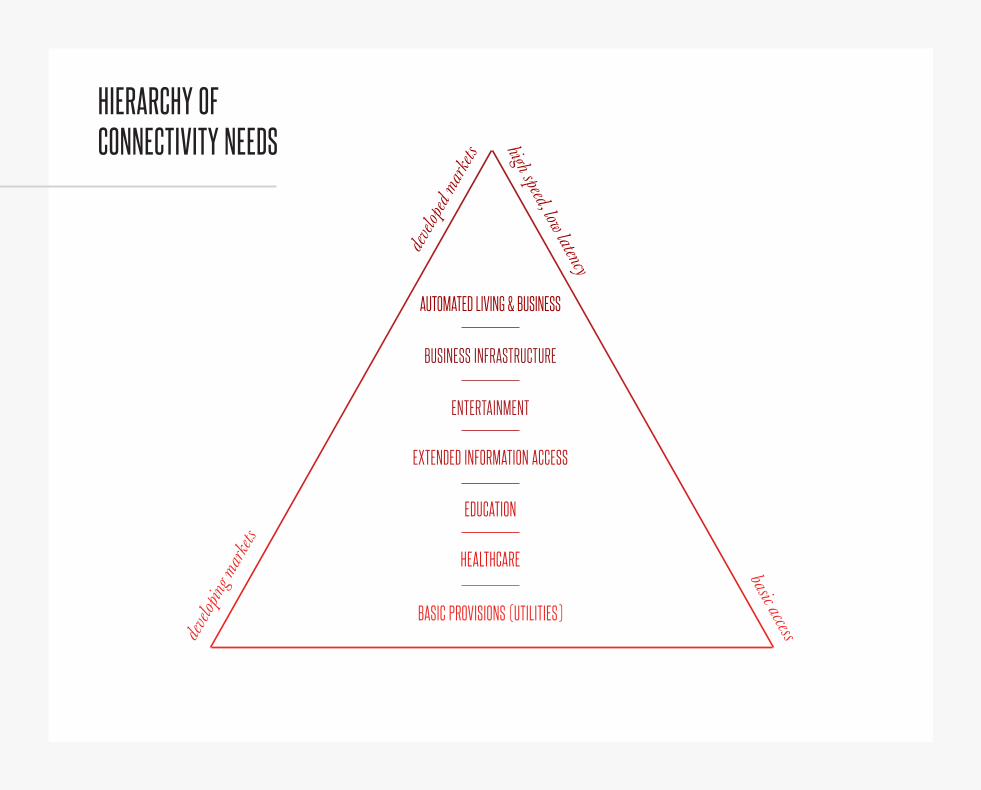

HIERARCHY OFCONNECTIVITY NEEDS

basic access

devel

oped

mar

kets high speed, low latency

devel

oping

mar

kets

ENTERTAINMENT

BASIC PROVISIONS (UTILITIES)

AUTOMATED LIVING & BUSINESS

EDUCATION

BUSINESS INFRASTRUCTURE

HEALTHCARE

EXTENDED INFORMATION ACCESS

3 0

The many potentially profit-generating benefits

to a company also include access to a larger

group of consumers/customers outside of

their direct physical reach as larger groups of

the population connect more frequently.

At the company or business level, Verizon

predicts that some of the world’s top

corporations could become 10 percent more

profitable by 2025, if they use IoT products

and solutions intensively.

3 1

2GREATESTCHALLENGE

TO THE ECOSYSTEM?

What is the

3 2

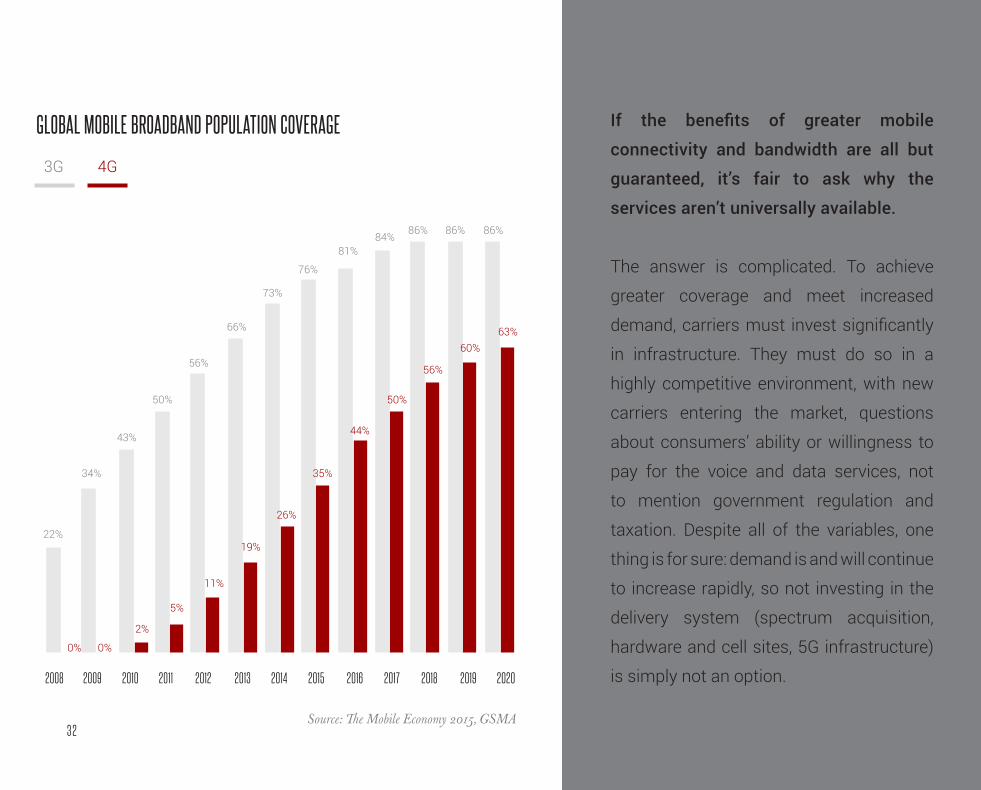

If the benefits of greater mobile

connectivity and bandwidth are all but

guaranteed, it’s fair to ask why the

services aren’t universally available.

The answer is complicated. To achieve

greater coverage and meet increased

demand, carriers must invest significantly

in infrastructure. They must do so in a

highly competitive environment, with new

carriers entering the market, questions

about consumers’ ability or willingness to

pay for the voice and data services, not

to mention government regulation and

taxation. Despite all of the variables, one

thing is for sure: demand is and will continue

to increase rapidly, so not investing in the

delivery system (spectrum acquisition,

hardware and cell sites, 5G infrastructure)

is simply not an option.

4G3G

GLOBAL MOBILE BROADBAND POPULATION COVERAGE

22%

0%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

34%

0%

43%

5%

2%

50%

56%

11%

66%

19%

73%

26%

76%

35%

81%

44%

84%

50%

86%

56%

86%

60%

86%

63%

Source: The Mobile Economy 2015, GSMA

3 3

— in some cases, with significant investments.

In the U.S., T-Mobile’s recent network upgrades

reportedly cost $4 billion. That’s just part of

category-wide capital expenditures (CapEx)

expected to reach $1.4 trillion globally by 2020.

Not surprisingly, there is risk associated with this

kind of capital outlay. An analysis of 45 carriers

by the telecommunications research firm Ovum

published in 2014 found a CapEx increase of 3

percent year-over-year but revenue growth of

just 0.6 percent. According to Ovum and GSMA,

the largest association of mobile carriers in the

world, the industry’s compound annual growth

rate (CAGR) between 2014 and 2019 will improve

to as much as 2.5 percent. In past years, that

number reached as high as 4 percent.

The low return on investment puts

pressure on carriers to find new ways

to increase revenue, which is tricky

in a market that is still developing,

highly competitive, and that faces

increasing costs to comply with new

government regulations.

CARRIERS ARE RESPONDING

3 4

(US$ BN)

TOTAL GLOBAL REVENUES(US$ BN)

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

1,0291,085

1,148

1,2441,321

1,382

1,1241,200

1,2841,353

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

161183

216

233236

250

198229

233244

GLOBAL MOBILE OPERATOR CAPEX

Source: GSMA: The Mobile Economy, 2015

3 5

In developed markets, carriers are

struggling to justify consumer-service

pricing. Criticisms include a lack

of transparency and a bias toward

wealthy users, which invites scrutiny

by consumer-advocacy groups. The

core financial issue, which we alluded

to earlier, is whether investing in new

infrastructure will provide sufficient cost

savings and revenue enhancement to

offset the decline in consumer pricing.

For now, the answer appears to be “no.”

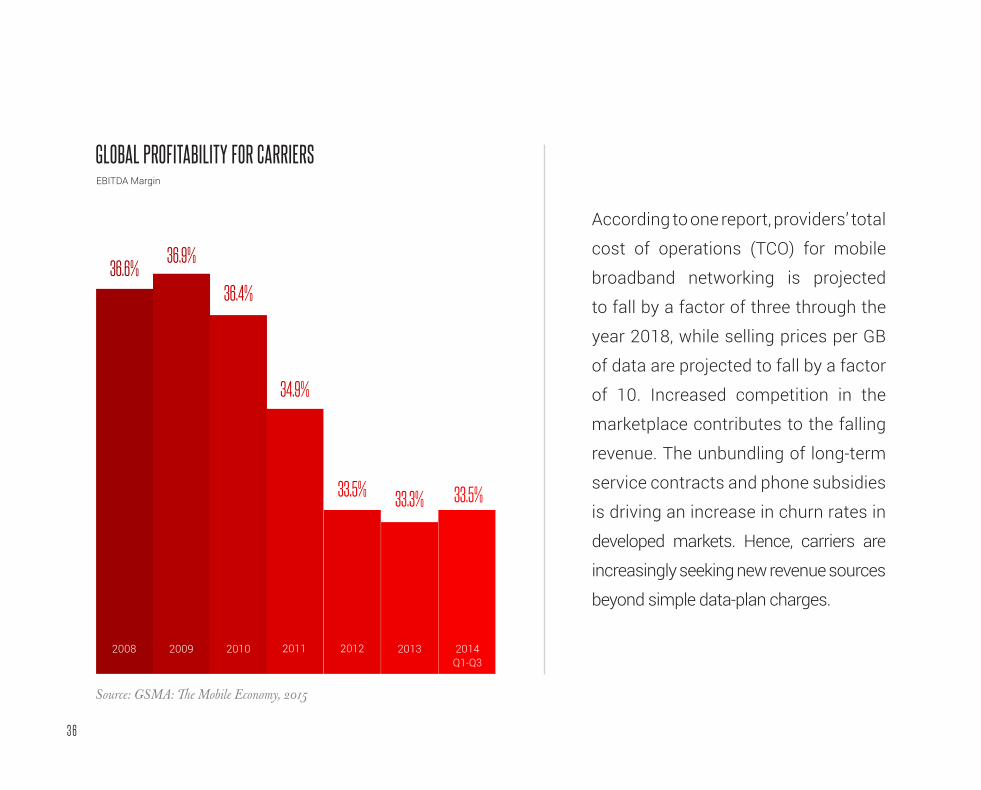

3 6

According to one report, providers’ total

cost of operations (TCO) for mobile

broadband networking is projected

to fall by a factor of three through the

year 2018, while selling prices per GB

of data are projected to fall by a factor

of 10. Increased competition in the

marketplace contributes to the falling

revenue. The unbundling of long-term

service contracts and phone subsidies

is driving an increase in churn rates in

developed markets. Hence, carriers are

increasingly seeking new revenue sources

beyond simple data-plan charges.

EBITDA Margin

GLOBAL PROFITABILITY FOR CARRIERS

Source: GSMA: The Mobile Economy, 2015

36.6%36.4%

33.5% 33.5%33.3%

34.9%

36.9%

Q1-Q32008 2009 2010 2011 2012 2013 2014

23 7

SUPPLY DEMAND

The

EQUATION

3 8

Let’s look at sticking points and solutions

on both the supply and demand sides.

SO, HOW CAN CARRIERSADDRESS THE MARKET CHALLENGES?

3 9

In the mobile market, supply consists

primarily of the carriers and their

services, as well as the adjacent

supplier infrastructure. With lower

data rates in developing markets and

higher churn rates in developed markets,

ARPU is decreasing.

SUPPLYO1

4 0

which they are seeking to capitalize on

by replacing unlimited data plans with

tiered plans. Interestingly, carriers are

now adding service contingents (e.g.

free usage of messenger platforms)

for additional fees on top of their tiered

plans to capture incremental revenue.

In urban areas, however, larger carriers

are facing competition and a decreased

demand for data services, as new

companies offer wifi solutions. At the

same time, infrastructure sourcing

is becoming more complex and

competitive, also due to the entrance

of new companies to the market. They

are offering higher bandwidth with

lower latency, and also more readily

employing new technologies — satellites

and drones, for example — to introduce

connectivity in developing areas.

CARRIERS IN DEVELOPEDMARKETS ARE SEEING ANINCREASE IN DATA CONSUMPTION,

4 1

Traditional carriers are also facing

competition from significant players,

such as Google, that are providing

direct-to-consumer data solutions

as mobile virtual network operators,

or MVNOs. Currently MVNOs are

addressing certain segments in the

population with specific needs (e.g.,

low-cost, specific long-distance

destination calling etc.). They do

not necessarily provide the largest

network or best bandwidth. However,

more players besides Google with

significant market access might be

testing their way into this market soon.

4 2

Regulation and taxation can also be an issue;

generally speaking, they vary greatly depending

on market and do not support a highly innovative

business environment.

Faced with slowing revenue growth from voice

and text services, carriers are seeking new

sources of income through value-added services,

or VAS. Over-the-top (OTT) providers, such as

Skype, WhatsApp, and Line currently own this

competitive environment. Carriers are responding

now with a GSMA supported platform called RCS

(Rich Communications Services). This platform

allows carriers to offer similar services as OTT

messaging providers (e.g., image or file sharing

and VoIP), but without having to tap into the data

allowance of the consumer. The success of this

platform is likely going to succeed or fail with the

quality of the user experience.

OTT messenger platforms

4 3

Demand for basic connectivity

and increased data is driven by

three factors:

A significant increase in consumers

being connected to voice or voice/

data services.

A significant increase in the number

of connected devices in the IoT.

New services requiring higher

data bandwidth (video and games,

for instance) and lower latency

(connected cars, for example).

DEMANDO2

O1

O2

O3

4 4

Ericsson predicts mobile data usage

will grow more than tenfold by 2021,

with video streaming accounting for

almost 70 percent of traffic. The vast

majority of the so-called next billion

— that is, masses of new users — will

go online via mobile devices. GSMA

estimates 1 billion new mobile users

over the course of the next five years

until 2020, which represents an

increase of 27 percent from today’s

3.6 billion users.

(PB per month)

VIDEO FUELING STRONGMOBILE DATA GROWTH

Source: Cisco VNI Global Mobile Data Traffic Forecase Update, 2015-2020

Web/data

File sharing

Video

Audio streaming

2,523

4,175

6,765

10,666

16,140

24,314

2015 2016 2017 2018 20192014

4 5

not only because of the increase in new

users, but also because data-intensive

services grow as connection speeds

increase, and people become more

comfortable with smaller screens (which

is definitely the case). From a consumer

perspective, video is by far the No. 1

driver for exponential growth in data

demand.

At the same time, the growth of the IoT

will produce more connection points and

data exchanges. According to Cisco,

by the year 2019 more than 10 billion

devices will exchange an estimated

35 quintillion bytes of information per

month. (We don’t have room for all of the

zeros here, but for the record, a quintillion

is a million raised to the power of 5.) You

heard about the traffic jams in New York

when the Pope visited? That’s going to

be a picnic compared to the radio-wave

congestion caused by the increase in

connected devices in the IoT.

DATA DEMANDSWILL INCREASE

4 6

So, consumers need more bandwidth,

and 5G is part of the answer. In fact, 5G

is even more important to industries such

as healthcare and driverless cars. 5G

promises to reduce latency and increase

data speeds to the extent that autonomous

cars will be able to make driving decisions

in milliseconds based on real-time

information from a variety of sources

around them.

4 7

3TACKLINGCONNECTIVITYCHALLENGE

HOW ARE INNOVATORS

the

3The connectivity market place is

complex, and challenged. But it is

equally obvious, that the benefits

of enhanced connectivity and

increased access to the internet

are tremendous and desirable.

The logical conclusion is a market

that sees a great amount of

innovation both from incumbents

as well as new entrants.

4 8

ACCESS SPONSORHIPSO1

CARRIER SPONSORED ACCESS AND DATA

BRAND/PROVIDER SPONSORED MODELS

DIRECT-TO-CONSUMER INFRASTRUCTURE

1.1

1.2

1.3

LOCAL EMPOWERMENTO2

IOTO3

FINANCIAL SERVICESO4

4 9

In any case, zero-rating certain

data packages provides a

fundamental pillar for later

business opportunities. Since

consumers, by definition, don’t

bear the cost of zero-rating

service, it is covered by either

carriers, brands or content

services. Let’s look at various

sponsorship scenarios.

Typical access sponsorship is

making use of a practice called

“zero-rating,” which means

providing access to certain

content or services at no charge

to the consumer. Zero-rating,

if misused, draws scrutiny and

sometimes harsh criticism, as

evidenced by the controversy

that surrounded Facebook’s

recent attempt to introduce its

Free Basics service in India.

ACCESS SPONSORSHIPSACCESS SPONSORSHIPS CAN COME IN A VARIETY OF FASHIONS.

O1

The majority of access sponsorships are underwritten by

the carriers, which provide limited data and bandwidth for free.

In some cases, this free data

is used to gain a competitive

product advantage, as T-Mobile

did with Binge On. In other cases,

fronting partners provide content

for free but have agreements with

the carriers not to charge for the

engagement, as is the case with

Facebook’s Free Basics.

Either way, carriers have

an incentive to zero-rate

in order to enhance their

product, engage users

who will eventually pay for

services, and upsell existing

subscribers more expensive

data plans.

1.1

ACCE

SS A

ND D

ATA

CARR

IER-

SPON

SORE

D

5 0

A C C E S S S P O N S O R S H I P SO1

A C C E S S S P O N S O R S H I P S

5 1

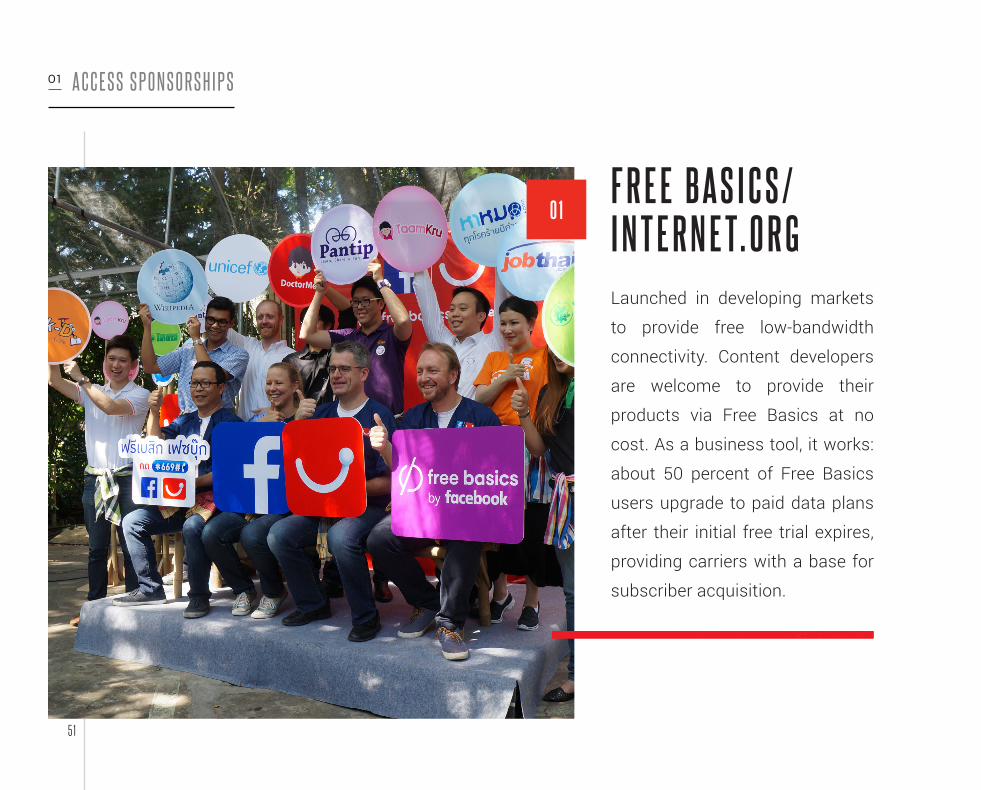

F R E E B A S I C S /I N T E R N E T. O R G

O1

Launched in developing markets

to provide free low-bandwidth

connectivity. Content developers

are welcome to provide their

products via Free Basics at no

cost. As a business tool, it works:

about 50 percent of Free Basics

users upgrade to paid data plans

after their initial free trial expires,

providing carriers with a base for

subscriber acquisition.

O 1

5 2

Launched in 2012 and reportedly

now reaching 600 million people

in 60 countries, Wikipedia Zero

provides free access to its content.

Data is positioned as educational,

and access is being paid for by

about 80 carriers who believe

there is a halo effect on their

brands by being associated with

an ostensibly educational effort.

W I K I P E D I AZ E R O

O 2

A C C E S S S P O N S O R S H I P SO1

5 3

T - M O B I L E U . S .B I N G E O NFollowing the success of its Music

Freedom initiative, which lets users

stream music services like Spotify at

no cost, T-Mobile launched Binge

On. It enables subscribers to watch

low-bandwidth (480p) versions of

certain video services over their

network. Services include Netflix,

Hulu, and HBO Go. T-Mobile hopes

to pick up more subscribers, but

there’s a hitch: the current service is

under scrutiny as a violation of net-

neutrality, because only select video

services are offered.

O 3

A C C E S S S P O N S O R S H I P SO1

5 4

A P P - B U N D L E DD ATA P L A N SStrictly speaking, this is not a zero-rating

practice, since consumers do have to pay

for them. Providers, however, such as

Singtel in Singapore, are offering prepaid

data plans that include free (up to a daily

limit) use of prechosen social or messenger

apps, such as Facebook, Line or WhatsApp.

The consumer essentially pays a flat fee

for all data used by the specifically chosen

app. Interestingly but not surprisingly, the

free use of WhatsApp does not include the

use of its VoIP solution for voice calls. Cell

C and other African carriers are pursuing

similar offer packages.

O 4

A C C E S S S P O N S O R S H I P SO1

In some cases, content

companies will pay carriers to

compensate for the increase

in data usage.

1.2

SPON

SORE

D MO

DELS

BRAN

D/PR

OVID

ER

5 5

A C C E S S S P O N S O R S H I P SO1

5 6

to a limited set of Google

services (search and Gmail),

but are prompted to pay

if they surf “too far away”

from the original property,

but executing multiple click-

throughs from a single

search. Google reimburses

carriers for Free Zone access.

App developers can be

incentivized to co-sponsor

content access through

“free data,” and Google is

charting the technological

waters for certain Android

apps to provide “free access.”

A recent report noted that

Google’s version of zero-

rating goes beyond a one-

off deal, allowing developers

to create apps that live on.

Google also offers sponsored

access via Google Free Zone,

where users have access

India’s largest carrier, which

also has significant presence

in Africa, recently confirmed

that it is launching Airtel Zero,

which will allow companies

to buy data in order to offer

their apps to consumers at

no cost.

A C C E S S S P O N S O R S H I P SO1

O 2O 1

5 7

&

A C C E S S S P O N S O R S H I P SO1

O 3

program (non-Prime members

can still access the entire

content catalogue for a

rental fee per movie/show),

and Amazon has found a

new outlet to acquire new

Prime members on the fly,

so to speak.

Amazon Prime members are

now able to stream Amazon

Prime video content for

free over JetBlue’s inflight

network. It is a win-win deal

for the companies. JetBlue

is offering an extremely

competitive entertainment

5 8

A C C E S S S P O N S O R S H I P SO1

O 3

on its head, by rewarding

consumers with free data for

clicking on ads. The mCent

app provides over 30 million

consumers access to free

apps. For each app trial that

consumers undertake they

are granted free data, paid

for by the app advertiser. This

model enables advertisers,

which include app developers

Zynga, Hulu, Saavn, and Kakao

to create a trial with a well-

documented but previously

unengaged audience. Jana

has integrated the system

into the billing systems of

311 carriers in 93 countries.

Used almost exclusively in

developing nations, this is

essentially an advertising

platform for marketers

and brands to engage

with consumers via their

mobile devices. The model

works around a well-known

impediment to the success

of mobile advertising, namely

that consumers know that

clicking on ads will count

against their data plan. Jana

has turned this principle

5 9

passing along the cost to

the advertising app/brand.

Opera has also introduced

a sponsored web pass,

which enables consumers

(especially, first-time mobile

users) such things as a

free day of mobile-internet

usage, or a free hour

on Twitter. Advertisers

sponsor these offerings.

Through a feature called

App Pass, carriers provide

subsidized data access to

applications. Carriers can

present app offers through

the browser, allowing cost-

free use of the apps, albeit

for a limited time. Carriers

decide whether they want

to provide this access for

free, and capitalize on it

with their own brand or

by generating revenue by

A C C E S S S P O N S O R S H I P SO1

O 5

6 0

Another way to provide

access is based on an

ad model where the

advertising revenues pay

for access through wifi.

1.3

INFR

ASTR

UCTU

REDI

RECT

-TO-

CONS

UMER

A C C E S S S P O N S O R S H I P SO1

L I N K N Y C

This ambitious project will provide New York City

with free, super-high-speed wifi in all five boroughs.

LinkNYC is being built by a newly founded company

called Intersection. The company builds digital

billboards that double as wifi towers. The project is

funded by the advertising revenue from these digital

billboards (OOH). Intersection and the City of New

York will share this revenue. This project allows

users to dramatically reduce their data usage while

in the city (and thus potentially the revenue for

carriers) and it allows tourists from outside of the

country to omit roaming fees for data services. The

first “links” have already been fired up, and the group

expects to have over 2,000 installed throughout the

city within a year.

O 1

6 1

A C C E S S S P O N S O R S H I P SO1

6 2

LOCALEMPOWERMENTEspecially in developing

markets we are observing

a variety of projects to

provide basic accessibility

by empowering local

groups to establish self-

sufficient access points.

O2

L O C A L E M P O W E R M E N TO2

Tone is a OTT service which

provides a platform to locally

empower communities.

It provides connectivity

and service in previously

underserved regions. One

such empowerment program

is mFish, in Indonesia. Tone

is providing a kit to local

fishermen that includes a

phone, an educational set,

and a SIM card for a local

carrier. The data is not free,

but it comes at a lower rate for

a promotional period to allow

the fishermen to understand

the value of having access

to services such as GPS,

local weather, fish maps and

chat functionality. The idea

is that the service will pay for

itself, and thus be “free,” by

enabling fishermen to realize

cost savings by running their

business more efficiently.

Just as importantly, mFish

overcomes the challenge

of digital literacy with an

educational introductory

kit. This allows local NGOs

that work with Tone and

the carrier on the ground to

educate the fishermen on

the usage of the phones. The

kit also comes with a solar

power-based charger for

the phone to overcome any

electricity shortages. Local

NGO employees also have the

opportunity through Tone’s

software to directly chat with

the fishermen and support

them with any queries.

6 3

O 1

6 4

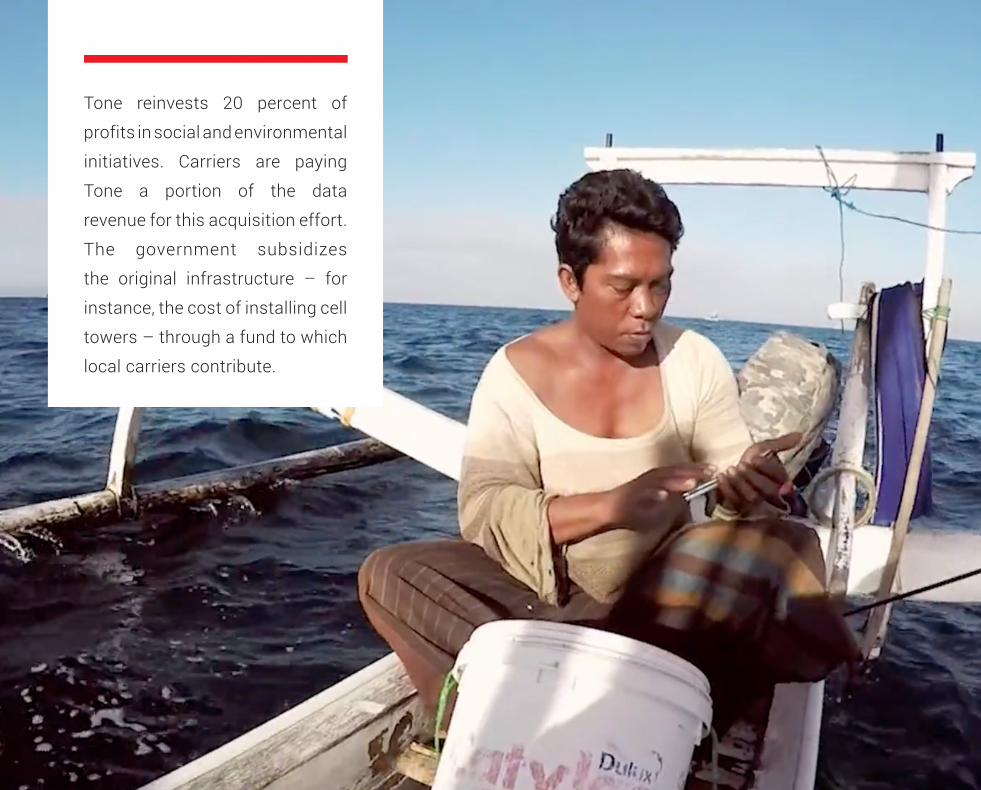

Tone reinvests 20 percent of

profits in social and environmental

initiatives. Carriers are paying

Tone a portion of the data

revenue for this acquisition effort.

The government subsidizes

the original infrastructure – for

instance, the cost of installing cell

towers – through a fund to which

local carriers contribute.

This Gilat Satcom offering provides

internet infrastructure via a private

satellite network to what the company

calls a nano-ISP. Examples of nano-

ISPs include schools, shops, and

churches, where the carrier installs

hardware to receive the satellite

signals. The carrier resells the signal to

nano-ISPs for a very low cost. Prices are

expected to be as low as $1 a month,

and the network is designed to scale

up. It thus enables local entities (nano-

ISPs) to become small businesses.

6 5

L O C A L E M P O W E R M E N TO2

O 2 V I L L A G E I S L A N D

6 6

allowing locals internet access and real-time

upstream and downstream data sharing

to optimize the supply chain to the local

kiosks and measure the efficiency of power

generation. In addition, this connectivity allows

for a range of other services to be considered,

such as real-time medical information sharing

or access to market prices for agricultural

products. EKOCENTER is run as a social

enterprise, meaning it combines philanthropic

and commercial interests of Coca-Cola and

its partners. For Coca-Cola, there are not

only clear, tangible benefits (increased sales

inpreviously undersupplied regions), but also

intangible benefits to generate positive brand

impact with stakeholders and consumers.

E K O C E N T E R

At Mobile World Congress 2015 (MWC),

Ericsson and Coca-Cola revealed the

“EKOCENTER” project, which is intended to

bring safe drinking water, solar energy and

mobile connectivity to communities in the

developing world. EKOCENTER is a modular

community market (kiosk) that is run by a

local entrepreneur and supplies basic goods

and services to underserved communities.

Functionality that can be added beyond safe

water, electricity and connectivity to jump-

start community development includes social

facilities and entertainment; power generation

for charging phones; cooling/refrigeration

of vaccines; education opportunities; and

much more. Connectivity is fully integrated,

O 3

L O C A L E M P O W E R M E N TO2

This company addresses the lack of

energy availability in certain parts

of some developing nations, which

ironically are within reach of service

but unable to use it for lack of a

power source. Intelligent Energy thus

addresses two essential elements of

connectivity: network availability and

power. Intelligent Energy develops

portable fuel cell systems that can

remotely power phones without access

to “the grid,” thus overcoming another

large barrier in developing countries

that are struggling with energy more

than with connectivity provisioning. 6 7

L O C A L E M P O W E R M E N TO2

0 4

6 8

IOTINITIATIVES

O3

6 9

When it comes to connecting the internet

of things, the most prominent efforts from

a consumer-facing perspective seem to be

made in the area of connected cars. AT&T

just announced a major deal with Ford to

bring more than 10 million connected cars

to the street within 5 years. AT&T also now

allows users to add their car as another

device in a data plan. While adding a car still

comes at the cost of a monthly fee, Tesla is

offering 3 years of free connectivity to AT&T’s

3G network within its innovative EVs. Carriers

including Vodafone and Deutsche Telekom

are creating models similar to AT&T’s.

C O N N E C T E D C A R SO 1

I O T I N I T I AT I V E SO3

IOT INTEGRATION AT SCALEO 2

7 0

I O T I N I T I AT I V E SO3

Many major carriers have announced and

piloted IoT connectivity platforms aimed at

specific verticals. Telefonica, AT&T, Verizon,

Deutsche Telekom, Orange, Telstra and

others are tackling topics such as smart

cities, connected homes, health tracking,

manufacturing and even cattle tracking.

In some instances, these platforms have

been built for a certain vertical or challenge,

while in other examples they are a direct

collaboration with a specific brand, such as

Coca-Cola or Nestle. At the moment, neither

of these platforms seems to drive significant

revenue compared to the core business, and

remains an innovation opportunity rather

than a scalable business play.

7 1

FINANCIALSERVICES

O4

7 2

Arguably, the industry that has embraced

mobile accessibility the most and made huge

strides is the financial services industry –

specifically providers of payment solutions,

credit/lending services and insurance,

particularly in developing nations. In this

space, start-ups, established banking players

and carriers are working together to provide

these services. Vodafone’s m-pesa service in

Africa, India, and Eastern Europe is one of the

more prominent and successful examples of

this. In 2015 in South Africa, the local bank FNB

offered its customers pre- and post-paid cell

coverage. It currently uses a specific carrier’s

cell towers, but says it is open to expanding to

other carriers as well. The service is a natural

extension of the bank’s financial services

business, which includes a rewards program

and mobile bill-pay capability.

F I N A N C I A L S E R V I C E S C A R R I E R I N T E G R AT I O NO 1 W I T H

F I N A N C I A L S E R V I C E SO4

7 3

(2001-2014; year-end)

NUMBER OF LIVE MOBILE MONEY SERVICES BY REGION

2001

1

2002

1

2003

1

2004

4

2005

5

2006

6

2007

10

2008

16

2009

38

2010

66

2011

116

2012

174

2013

232

2014

255

As of December 2014, there were 255 live mobile money services in 89 markets.

Sub-Saharan Africa

South Asia

East Asia & Pacific

Latin America

Middle East & North Africa

Europe & Central Asia

Source: GSMA: The MobileEconomy, 2015

D E L I V E R I N G T H E B U S I N E S S C A S E A N D R O A D M A P T O B U I L DA M O B I L E C O M M E R C E P L AT F O R M I N E A S T A F R I C A

M O B I L E C O N S U LT I N G F O R G L O B A L C P G

74

Through in-depth market

research, OgilvyRED was able to

convince local carriers in Africa

that their mobile payments

system should be evolved

from a peer-to-peer system

to a system that allows for

payments at retailers. Costs for

the SMS, that were required to

make payments, were absorbed

by the carriers. This in return

created brand preference for

these carriers in a market, where

consumers would typically carry

multiple SIM cards.

Furthermore, mobile payments

were introduced for payments

along the supply chain from

distributor to retailer. The

risk of fraud and simple cash

theft was mitigated and all

transactions could electronically

be accounted for.

7 5

4WHAT IS OPPORTUNITY?

the

7 6

As carriers are trying to identify new

sources of revenue and potential investors

in the ecosystem, there is an opportunity

for companies and brands to step in to

collaborate for success. Beneficiaries

differ based on the region and their state

of technology maturity. Some (few)

companies might be looking towards

becoming connectivity providers with

direct contact to the end consumers of

such services.

But the majority should probably be

looking at opportunities to create value

for the company through sponsorship or

subsidizing deals. Third-party platforms,

such as Jana and Opera Max, have already

shown success by tapping into this

space to garner advertising dollars. The

challenge with this model will be whether

pure sponsoring can be a sustainable

tactic given the relatively negative

sentiment towards advertisements

among consumers.

Meanwhile, verticals that will benefit

from a more connected ecosystem

through IoT are starting to form alliances

with automotive and manufacturing

companies. While Verizon and AT&T are

currently focusing much of their attention

on connecting mobile devices to their

networks, both appear to be placing

greater emphasis on IoT connections and

management.

7 7

MOBILE-ENABLED PRODUCTS AND SERVICES IN THE DEVELOPING WORLD

Source: GSMA: The Mobile Economy, 2015Note that others include disaster response, energy access, green networks, midentity, NFC and smart cities

PRE 2009 2009 2010 2011 2012 2013 20140

200

400

600

800

1000

1200

1400

Health MoneyLearning Others

7 8

4WHYBRANDSSHOULDCARE

7 9

BRANDS ARE STILL STRUGGLING with

how to engage with consumers on

mobile devices beyond buying media

to gain click-throughs. This model is

quickly becoming outdated in a new

era of consumer behavior. Simply

put, mobile users dislike the current

mobile-advertising model, and are

rejecting it by not clicking through.

Companies planning to enter the

connectivity space for branding

and marketing purposes have to re-

evaluate how they can produce value

for their enterprises beyond ad clicks.

8 0

This new way of thinking and acting as

a marketer does not obviate the need to

establish and move toward a commercial

goal, albeit with greater transparency

to consumers. Brand benefits do not

necessarily have to be directly tied to

revenue or margin (tangible benefits). They

can also provide intangible (emotional,

psychological) benefits. It also may

not be limited to individual companies

making investments in providing access

and connectivity, as it is likely more

economical to form consortiums or

industry associations.

“BRANDS THAT DO: BUILDING BEHAVIOR BRANDS,” In its paper

OgilvyRED explains how modern brands take action to create value

instead of just asserting the brand’s message and raison d’étre.

The basic tenet is that marketing is a service that delivers

real consumer benefits, such as mobile connectivity.

8 1

4TANGIBLEBENEFITS

8 2

THROUGH LONG-TERM BUSINESS MODEL INNOVATIONFor example:

TA N G I B L E B E N E F I T S

New pricing, new revenue

sources, new product pipelines.

Bringing the next billion online

will create a huge market for

direct-to-consumer offerings.

Increased levels of income will

improve consumer ability to pay

for incremental goods.

Fundamental cost-structure

enhancements. In healthcare,

for example, better data may

be voluntarily provided by

patients (mobile users) to help

healthcare providers with risk

assessment, to reduce the cost

of insurance products.

O1 O2

8 3

DIRECT REVENUE INCREASE THROUGH INCREASED SALES

TA N G I B L E B E N E F I T S

For example:

Through mobile commerce and

direct-to-consumer sales. For

example, fast-food restaurants

could own car connectivity, and

the in-car screen for preordering

when driving near restaurants.

By increasing sales outlets,

as the Coke EKOCENTER

example illustrates.

Product bundling and co-

marketing, as shown in

the collaboration between

JetBlue and Amazon Prime.

O4O3 O5

8 4

TA N G I B L E B E N E F I T S

Through efficiency gains achieved

with better value-chain visibility,

decreased cost of acquisition, and

decreased cost of advertising.

In the example of mFish, in

Indonesia, brands get direct and

highly targeted access to specific

groups, directing acquisition

investments to the precise

audience for a brand.

By capturing government

subsidies or tax breaks.

With more efficient customer

servicing rerouting calls to

messaging services using

Facebook Messenger as a

customer service outlet.

O7O6 O8

For example:

BY INDIRECTBOT TOM-LINE CONTRIBUTION

8 5

BY INDIRECTBOT TOM-LINE CONTRIBUTION

TA N G I B L E B E N E F I T S

By enhancing business decision-

making capabilities, such as

demand-based pricing on the fly,

or using real-time data analysis.

Insurance companies, for

example, could tailor premium

pricing in real time according to

data they can collect if they “own”

the consumer’s connectivity.

11

For example:(CONTINUED)

By providing mobile connectivity

to previously unconnected users.

Direct marketing through OTT

services such as WhatsApp

are especially relevant in this

case. Messenger platforms are

increasingly being used not just

for communication but also as

transaction touchpoints (e.g.,

WeChat).

Through an increase in

customer base and brand

exposure, using physical

or digital trials, such as

Jana has.

1009

8 6

4INTANGIBLEBENEFITS

8 7

Increase perception of brand as a digital and

contemporary leader. Brands that have previously

not been perceived as technology leaders can

gain advantages. In agriculture, for instance,

technology is making vast strides to enable better

decision-making, with such simple products as

mobile weather forecasting, and data-gathering

and data-analysis tools.

Improved positioning vis-a-vis indirect stakeholders,

such as governmental bodies, NGOs, and supply

chain partners (see Coke Ekocenter).

Using mobile connectivity to enhance

consumers’ perceptions of brands

as innovative and service oriented.

For example, Tesla is now updating

its cars’ operating systems through

a 3G connection, which frees owners

from having to schedule a service

appointment.

Allow consumers to see brands as

beneficial to communities, as Coke has

done with the Coke Ekocenter.

CAPITALIZE ONBRAND DIFFERENTIATION

I N TA N G I B L E B E N E F I T S

For example:

01

03

02

04

8 8

By driving an innovation

agenda and introducing

opportunities for first-time

mobile users to test and

learn about a product.

Through talent acquisition

and retention.

By building a company’s

capabilities, exposing it to new

technologies, and introducing it

to new partners.

INCREASE COMPANYFUTURE PROOFING

I N TA N G I B L E B E N E F I T S

For example:

05 06 07

8 9

4BARRIERSKEY ISSUES

SOLVEto

9 0

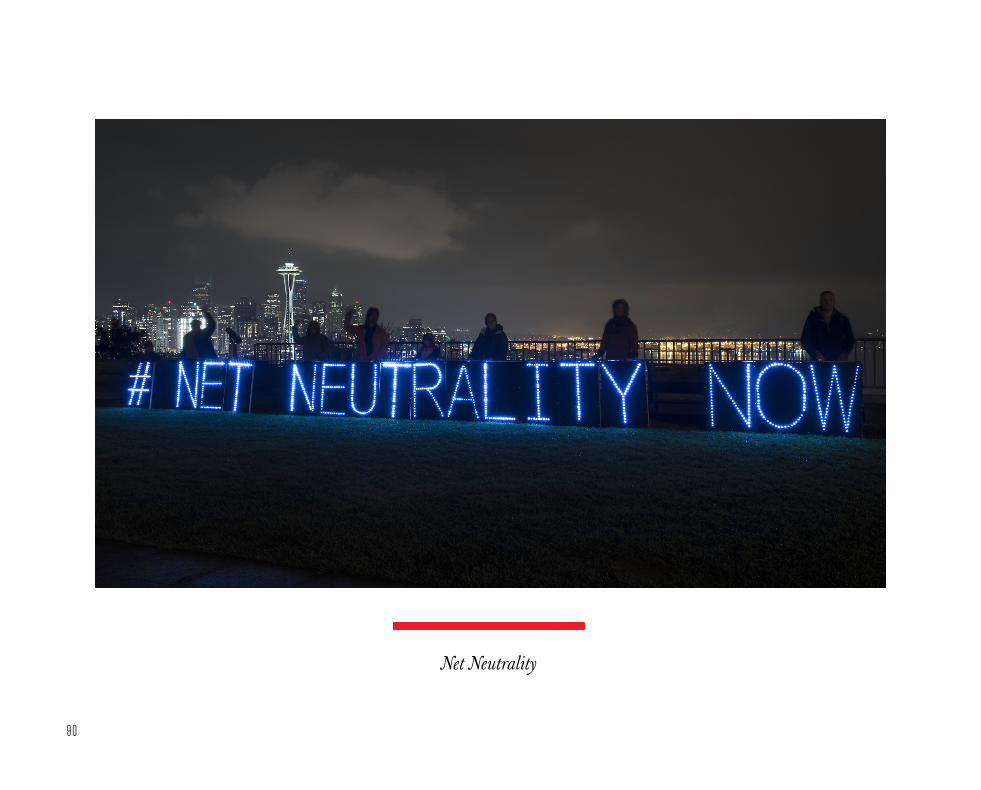

Net Neutrality

9 1

N E T N E U T R A L I T Y

According to Wikipedia, “Net neutrality…

is the principle that internet service

providers and governments should

treat all data on the internet the

same, not discriminating or charging

differentially by user, content,

site, platform, application, type of

attached equipment, or mode of

communication.”

The moment that companies (whether

they are brands, social platforms, or

carriers) provide access to content

for free or for a lower price than other

services, the issue of net neutrality

kicks in. The aforementioned example

of Facebook’s attempted introduction

of Free Basics in India illustrates

this point precisely. The message

to marketers is that any potential

opportunity or proposition must

be vetted to ensure that it does not

discriminate by limiting access to a

single provider, or by allowing access

to a single competitor’s product.

Services like Jana have solved this

equation, since it can be used to

access any content or service.

O 1

9 2

Transparency of Business Models to the Customers

9 3

T R A N S PA R E N C Y O F B U S I N E S SM O D E L S T O C U S T O M E R S

The mobile connectivity ecosystem

is not considered by consumers to

be transparent. Companies that

want to enter the ecosystem should

make transparency a priority, to

avoid alienating consumers or

attracting the scrutiny of regulators.

Consumers are not easily fooled

and understand the popular phrase,

“If you are not paying for it, you are

the product.” Examples of success

through transparency include

Tone, which makes it clear that the

company is making money from

the mFish solution. This is tolerated

and even appreciated by consumers

because they perceive mFish as

beneficial to the community due

to the (transparent) way it has

structured deals with the carrier and

government. In the United States,

Google Fi is showing carriers what

it means to communicate with

their customers in a simple manner

about pricing, avoiding jargon or

hidden fees.

O 2

9 4

Digital Literacy and Relevancy of Offers

9 5

A key obstacle for many developing

markets is digital literacy. People

are often not aware of the benefits

of the internet, if provided through

mobile devices, which are not

affordable to large parts of the

world’s population. Educational

campaigns need to start here, and

should not assume that everyone

would be online if they just had

access to a connection. The second

obstacle is that it takes training to

become familiar with navigating

the offers and services including

the pitfalls (e.g. spam, data

security). The simpler the offer and

value proposition, the better. Last

but not least, many services have

not been fully adapted into local

context (language, data speeds).

Especially in developing markets it

cannot be assumed that English is

the spoken language. Any service

which adapts to local language

and available bandwidth will have a

clear advantage.

DIGITAL L ITERACY AND RELEVANCY OF OFFERS0 3

9 6

5THOUGHTSTARTERS

WHY SHOULDN’T WE...

9 7

the car’s telematics data. Healthcare

providers could sponsor connectivity

for underserved communities in

exchange for using the data to move

from reactive to proactive prevention

mechanisms.

By sponsoring access in highly

frequented areas, companies could be

granted exclusive access to data that

is being collected within these areas,

allowing for dynamic pricing or product

adjustment concepts. Think about an

insurance company sponsoring all

mobile access along highways, and

thus being able to monitor real-time

traffic behavior and adjust premium

pricing accordingly. An insurance

company could also simply pay for the

car’s data contract, taking that burden

off of the consumer in exchange for

TAKE ADVANTAGERETURN ON INSIGHTS (DATA)THAT MOBILE CONNECTIVITY PROVIDES

of the

01

“One of the myths about the Internet of Things is that companies have all the data they need, but their real challenge is making sense of it. In reality, the cost of collecting some kinds of data remains too high, the quality of the data isn’t always good enough, and it

remains difficult to integrate multiple data sources.”

— Chris Murphy, Editor, Information Week

9 8

If the healthcare industry could

monitor compliance of medication

intake in a real-time manner, it

would be able to save billions in

post-symptomatic treatment costs

by preemptively improving positive

outcome rates. Connected pillboxes

are making a slow entry to the

marketplace, but there are currently

no scaled concepts in place to provide

them free of data cost or to sponsor

the data it takes to communicate with

healthcare providers or caretakers.

USE MOBILE CONNECTIVITY

INTAKE OF MEDICATION

02

to monitorcompliance of

9 9

SOCIAL ENTERPRISE CONCEPTTO INCREASE BRAND IMPACT

CPG/FMCG companies in particular

struggle for differentiation because

of the broad exposure of their brands

and products. Becoming a sponsor

of connectivity or empowering local

communities through, for example,

helping to overcome digital literacy

barriers, could significantly boost

their value proposition beyond the

product, and create a more favorable

selling environment. Think about a

CPG company helping local women

to become small business owners

as resellers of data plans, or simply

providing them with access to

information to build new communal

marketplaces. Or, consumer brands

might sponsor the local adaptation

of non-native content and services

into the local language and data

ecosystem.

Use the

03

1 0 0

RETAILERS

As carriers are connecting more and

more devices, is there a chance to

become a retailer for more than just

phones and tablets? What if household

appliance manufacturers or home

electronics companies sold their

goods through the ecommerce sites

of carriers?

04

CONSIDER CARRIERSas

1 0 1

Carriers already bill for data plans to

their customers, and some (though

few) other regular billing activities

can be processed through these

carrier bills. Are there efficiency and

convenience gains to be conceived

by integrating other regular billing

activities (e.g. utilities, media

subscriptions) through a carrier’s

system? This would potentially allow

for a more comprehensive data view

of individuals’ financial transactions

and would also provide acquisition

opportunities for subscription-based

models (especially if these services

are based on data usage).

05

F INANCIAL SERVICE COMPANIESCONSIDER CARRIERS

as

1 0 2

As we are connecting more and

more devices, including our cars,

will these brands be selling us

connectivity and data plans as

well connecting into a multitude of

carriers in the background through

soft SIM cards? What if major

marketplaces or financial service

providers become MVNOs? This

would let them take ownership of

consumer/customer data, contact,

and reward activity, directly,

through sponsored data.

06

MVNOsCREATE NEW

1 0 3

SPONSOR

ACCESSACCESSCONTENT

With the advertising industry

struggling to find meaningful

ways to engage consumers on

their phones, could content and

the sponsorship of access to

content become positive value

components in the lives of the

consumer and the brands?

Consider, for instance, the

WhatsApp video channel from

Coca-Cola bringing consumers

exclusive World Cup video

coverage, free of data charges.

07

1 0 4

Any company that already has or

is looking into opportunities to sell

directly to consumers might have

an interest in expanding its potential

customer base by providing them

with free access to their mcommerce

sites. Could marketplaces like OLX,

eBay or Amazon or a consortia of

brands look into creating unique, “free-

of-charge” DTC offerings, providing

more convenient and potentially more

cost-effective ways for consumers

to shop on their phones or tablets?

This model could become especially

interesting if carriers were paid for

data-based on revenue share instead

of fixed per-MB pricing.

ENABLE

E -COMMERCE

08

more

1 0 5

Messenger apps (Whatsapp, FB

Messenger, Line, Kik, KaKao Talk)

have seen a massive surge in person-

to-person traffic. Some of these

platforms (e.g. FB Messenger) have

already openly started to use their

platform for business-to-person

communication, opening the system

up for customer service channels or

even machine-initiated messaging

(access or confirmation codes, etc.).

Given that messaging is moving

towards more video-based platforms,

brands might innovate their customer

service experience through video chat

functionality, with the chat traffic paid

for by the brands themselves.

USE MESSENGER SYSTEMS

CUSTOMER SERVICE

09

toprovide

1 0 6

If brands engage in larger-scale

provisioning or sponsorship of

accessibility, should governments

not provide them with tax breaks as

the brands are actually creating a

community service?

10

PROVIDE RE-COMPENSATION SCENARIOS

GOVERNMENTAL INCENTIVESthrough

1 0 7

Loyalty programs are struggling with

creating proper value exchange to

promote for repeat engagements with

their underlying brands. In developing

markets, loyalty programs have long

embraced “airtime” as one of the most

coveted currencies to their consumers.

Can data plans for connected devices

not simply be paid off with loyalty

points? If a customer can pay for taxis

in New York with American Express

Membership Rewards points, why

can’t the same customer have an

American express phone that is paid

for via American Express purchases

made with the mobile payment option?

Why could frequent flyer programs not

cover roaming charges with mileage?

11

LOYALTY PROGRAMSBET TER INTEGRATION

for

PROVIDE

1 0 8

With communities or public/private

partnerships providing cities with

“free” wifi services that still need

individual authentication (e.g.,

LinkNYC), can companies with

preexisting accounts (Amazon Prime,

Facebook, carrier accounts) not

automatically pre-authorize access?

And if these companies tracked

movements through these networks,

are there relevant offers they could

provide in context, e.g. transportation

subsidies by knowing when and where

their customers are traveling (“Ikea

just sponsored your subway ride to our

store”)?

12

FREE ACCESS PROGRAMSwith

in cities

INTEGRATE BRANDS

1 0 9

13

INCREASED ACCESSIBILITYthroughENGAGE IN GLOBAL TALENT DEVELOPMENT

Certain industries (e.g., software, tech

sectors) are struggling to grow and

identify the right talent going forward.

If increased connectivity means more

access to education, can there be a

long-term investment goal to bring this

connectivity to regions where talent

will most likely be sourced in the next

10 to 20 years?

1 1 0

Parts of the world are or will soon be

struggling with ways to better serve an

aging population. If accessibility and

connectivity mean better education,

improved medical care, and potentially

higher mobility, should a consortia

from the public and private sectors

not invest in overcoming certain levels

of digital illiteracy and provide people

with generation-specific services

independent of a person’s financial

capability? Ogilvy & Mather Singapore

worked with Singtel to redesign the

functionality of a smartphone that

was then distributed to Singapore’s

aging population. The restructuring

dramatically simplified the phone’s

interface and functions, allowing less

digitally savvy customers to take

advantage of basic functions such as

games, camera and emergency calls.

14

AGING, CONNECTED POPULATIONto serve anPOSITION BRANDS

1 1 1

CLOSING

THOUGHTS

1 1 2

Not really.

Certain institutions have demanded “the

internet” be considered equal to basic

life requirements like air and water. But

this does not mean that the internet

is equally as accessible and abundant

(after all, clean water is certainly not

ubiquitous or always free). It still requires

an enormous amount of investment to

keep the internet infrastructure operating,

and the cost for this is not as easily

redistributed throughout the complex

ecosystem that has sprung up. The

benefits the internet brings are in some

cases hard to measure or attribute to the

providers within the ecosystem.

These market forces are not trivial, as they

relate to trillions of dollars in investment

and trillions in potential revenue.

?

INTERNET

“FREE”FOR

Will we ever have

1 1 3

Do we have

A HOMEMADEINNOVATIONDILEMMA?

To me the biggest question for the future is will we

really continue in the future to license spectrum – do

governments license oxygen? No. The Internet is oxygen,

it’s water.” – Vittorio Colao, CEO of Vodafone Group

Currently governments are generating a

significant income from auctioning off

spectrum to carriers. Carriers, in turn,

are forced into high-stakes auctions for

this spectrum to remain competitive.

The lease investment required, however,

is directly subtracted from the carrier’s

ability to invest further in infrastructure

extension. The lack of this investment

slows down growth in the economy, at the

country level, from enhanced connectivity.

Is it worth re-doing the math to see if the

benefits of an extended infrastructure

investment would not overcompensate

for the short term gains from these

auctions at the federal level?

“

1 1 4

WILL WE, IN 5 YEARS,

REALLY CAREThe simple answer is “maybe.”

who provides us with access?

Google Fi and Apple are already providing

services that are carrier-independent.

In many developing countries people

carry two SIM cards and phones because

the individual carriers services are either

cheaper or better based on whether

someone is in a rural or metro area, or

whether people are making short or long

distance calls. Carriers will obviously do

everything to keep their brands relevant

through a combination of direct (network

strength) and indirect (value-added

services) value propositions.

In a best-case scenario, consumers do

not have to worry about connectivity

at all, because their devices will be

automatically switching to the strongest

signals, and their services will be

provided by a third party that is invested

in the content and service platform

rather than the sheer connectivity.

1 1 5

WILL CARRIERSBECOME B2B PLAYERS?

If the scenario just described prevails,

then carriers could find themselves

becoming B2B players at scale and target

resell partners (such as banks as MVNOs).

This might dramatically decrease their

individual cost of acquisition, as they

might be selling in bulk. The effect on

competition and innovation potential will

have to be evaluated in this scenario.

?

WHO ARE

BUYERSTHE

and if so

1 1 6

THEOPPORTUNITY FOR ALL When asked what lessons she

would provide the audience

about marketing in the digital

age, Linda Boff, the CMO at GE,

said: “Be sherpas for what is

new and what is next. I think

there is a real role today for

marketers to identify what’s

around the corner and then to

translate that into business

terms to help drive growth.”

This applies to all companies

and brands, whether they

provide infrastructure and

access, services and content,

or are looking to profit from an

increasingly connected global

population.

1 1 7

and then, together, they might just be able

to create a brighter, more connected

world while also doing good business.

MOBILE ECOSYSTEM PLAYERS,WILL NEED TO COLLABORATE & COEXIST

But thewhether newor incumbent,

1 1 8

CREDITSOGILVY CONTRIBUTORS: Carla Hendra

Caylin Lo

Chelsea Jones

Devon Cottle

Elizabeth Stroud

Emily Arnold

Jay Kurahashi Sofue

Jeremy Katz

Jess Kimball

Joe Bargmann

Mary McFarland

Peter Fasano

Priyank Mathur

Sarah Tran

Seth Greenberg

Spencer Schrage

Sydney Sadler

EXPERTS & SOUNDING BOARDS: Colin O’DonnellChief Innovation Officer, Intersection

Derk HendriksenVP Business Integration & GM EKOCENTER, The Coca-Cola Company

Harald NeidhartFounder & Curator at MLOVE

Mark KaplanCEO and Founder, Tone

Nathan EagleCEO & Co-Founder, Jana

DESIGN: Lori Argyle

AUTHOR:Martin LangeGlobal Consulting Partner, OgilvyRED

1 1 9