office outlook - jll · office outlook. indianapolis | q4 2016. cbd ... full service class a asking...

TRANSCRIPT

Office Outlook

Indianapolis | Q4 2016

CBD occupancy grows while suburbs see investment

Office Overview

Indianapolis | Q4 2016

The Indianapolis office market consists of 31.8 million square feet in 331 buildings with a 19.8 million square foot suburban inventory and a 12.0 million

square foot inventory in the CBD. The total vacancy rate for the office market in fourth quarter 2016 was 16.4 percent. In addition to the CBD, the bulk of

the Class A and B office inventory is located in four major northern suburban submarkets - Keystone, North Meridian/Carmel, Northeast and Northwest.

Fourth Quarter 2016 Statistics

Total

Inventory

YTD Net

Absorption

Vacancy

Rate

Full Service Class A

Asking Rent

Full Service Class B

Asking Rent

31,818,290 sf -53,454 sf 16.4 % $21.97 psf $17.01 psf

Trends

(Q over Q)

Vacancy Rate

Concessions

Rental Rates

New Construction

Historical Indianapolis Vacancy Rate Historical Indianapolis Absorption

Keystone: The Keystone office market consists of four major office parks – Keystone at the Crossing, Woodfield Crossing, River Crossing, and the Precedent. The Keystone

office market provides high level suburban amenities with abundant dining, shopping and entertainment options.

Inventory (sf) YTD Net Absorption (sf) Vacancy Rate Asking rent YTD Completions (sf) Under Construction (sf)

Class A 3,283,647 55,206 15.3 % $22.20 psf 102,000 55,000

Class B 768,823 16,495 7.8 % $18.41 psf 0 0

Total 4,052,470 71,701 13.9 % $21.48 psf 102,000 55,000

North Meridian/Carmel: The North Meridian/Carmel submarket provides the best interstate access of the four major suburban office markets with a full cloverleaf interchange

at 96th Street and I-465. Work is wrapping up on a limited access highway that will help ease congestion in the area. Three major medical campuses – St. Vincent Carmel

Hospital, the Heart Center of Indiana, and IU Health North Hospital – are located in this submarket.

Inventory (sf) YTD Net Absorption (sf) Vacancy Rate Asking rent YTD Completions (sf) Under Construction (sf)

Class A 4,125,988 -12,339 9.4 % $22.47 psf 90,250 192,361

Class B 2,385,880 32,797 10.9 % $17.16 psf 0 0

Total 6,511,868 20,458 9.9 % $20.52 psf 90,250 192,361

Northeast: The Northeast submarket is located along Interstate 69 and includes the rapidly growing suburbs of Fishers and Noblesville. As the population of these communities

have exploded over the last fifteen years, developers have aggressively built new office complexes along this corridor.

Inventory (sf) YTD Net Absorption (sf) Vacancy Rate Asking rent YTD Completions (sf) Under Construction (sf)

Class A 1,556,579 -106,285 28.9 % $20.35 psf 0 155,255

Class B 1,801,078 -76,976 25.2 % $17.41 psf 0 0

Total 3,357,657 -183,261 27.0 % $18.77 psf 0 155,255

Northwest: The Northwest submarket consists of four major office parks – INTECH Park, College Park, Woodland Corporate Park and Fortune Park. There is also a significant

flex/industrial component in this submarket. Indianapolis-based developers Lauth Property Group and Duke Realty developed much of the Class A and B office product in this

area.

Inventory (sf) YTD Net Absorption (sf) Vacancy Rate Asking rent YTD Completions (sf) Under Construction (sf)

Class A 1,550,100 12,354 19.8 % $19.95 psf 115,358 0

Class B 1,468,533 -77,849 27.3 % $16.55 psf 0 0

Total 3,018,633 -65,495 23.5 % $18.28 psf 115,358 0

Midtown, West/Southwest, East/Southeast, Greenwood: This group of smaller submarkets includes mostly small, local developers and Class B buildings.

Suburban Overview:

Inventory (sf) YTD Net Absorption (sf) Vacancy Rate Asking rent YTD Completions (sf) Under Construction (sf)

Class A 10,630,462 -32,782 15.5 % $21.64 psf 307,608 402,616

Class B 9,168,978 -125,220 18.5 % $16.55 psf 0 0

Total 19,799,440 -158,002 16.9 % $19.28 psf 307,608 402,616

CBD: The tenant mix in the CBD appeals to traditional businesses that need access to the state and local governments and court system. The CBD also provides an ample

amenity base such as The Conrad, Circle Center Mall, Lucas Oil Stadium, Bankers Life Fieldhouse, and several upscale dining establishments. Parking is limited in most Class

A buildings and will add an additional occupancy cost of $3.00 - $4.00 PSF.

Inventory (sf) YTD Net Absorption (sf) Vacancy Rate Asking rent YTD Completions (sf) Under Construction (sf)

Class A 7,101,003 68,344 18.3 % $22.48 psf 0 25,361

Class B 4,917,847 36,204 11.5 % $17.88 psf 0 0

Total 12,018,850 104,548 15.5 % $20.60 psf 0 25,361

13.0%

16.0%

19.0%

22.0%

2008 2009 2010 2011 2012 2013 2014 2015 Q42016

Class A

Class B

Total

-400

-200

0

200

400

600

800

2008 2009 2010 2011 2012 2013 2014 2015 2016

s.f.

thou

sand

s

Notable new tenants to the CBD

Source: JLL Research

YTD net absorption by submarket (s.f.)

Source: JLL Research

Sale volume by submarket (s.f.)

Source: JLL Research

More companies relocating from suburbs to downtownThis year, nearly 170,000 square feet was leased by tenants new to the CBD. This total is more than the past two years combined. With more companies looking to relocate from the suburbs to downtown, it is no surprise that the CBD posted the highest level of net absorption in the Indianapolis market for the year. It was also one of the only submarkets to see vacancy decrease since last quarter. This trend will surely continue as almost 150,000 square feet in active requirements of current suburban tenants are looking to move downtown.

CBD, Keystone see greatest occupancy growthOccupancy growth this quarter was limited as a result of a few large tenants vacating their space for owner-occupied locations. Most notably was Roche Diagnostics bringing employees located in 10300 Kincaid Drive in the Northeast submarket back to its headquarters, creating nearly 200,000 square feet of newly vacant space. The CBD, Keystone, and North Meridian/Carmel all finished off 2016 with positive net absorption, with the CBD showing the greatest amount with over 50,000 square feet for the quarter and 100,000 square feet for the year.

Investors focus on northern suburbsSix million square feet of office space traded hands this year, resulting in almost $600 million in sales activity. Three sales closed this quarter, and unlike previously this year, all occurred in the suburbs. In North Meridian/Carmel, Northpoint Center and Pennwood I & II were sold to Tryperion Partners and Kimmel Square, LLC, respectively. Nearby in Keystone, Haverstick I & II were acquired by Priam Capital. In total, 23 sales transactions occurred this year with several more set to close in early 2017.

CBD occupancy grows while suburbs see investment

Office Insight

Indianapolis| Q4 2016

31,818,290Total inventory (s.f.)

-332,956Q4 2016 net absorption (s.f.)

$19.78Direct average asking rent

427,977Total under construction (s.f.)

16.4%Total vacancy

-53,454YTD net absorption (s.f.)

4.7%12-month rent growth

56.4% Total preleased

Tenant Size (s.f.) New location Previous submarket

Flaherty & Collins 24,503 Regions Tower Keystone

Teradata Corp. 20,454 BMO Plaza North Meridian/Carmel

Section 127 11,924 425 W South St East/Southeast

Pondurance 10,500 500 North (sublease) Keystone

56.3%23.5%

9.0%

5.0%3.4% 1.7% 1.2% CBD

North Meridian / CarmelNortheastNorthwestWest/SouthwestKeystoneMidtown

-183,261

-65,495

20,458

71,701

104,548

-200,000 -100,000 0 100,000 200,000

Northeast

Northwest

North Meridian/Carmel

Keystone

CBD

Overview of asking rents Historical asking rents ($ p.s.f.)

Source: JLL Research

Overview of vacancy Historical vacancy rates

Source: JLL Research

Current conditions – Indianapolis Historical leasing activity (s.f.)

Source: JLL Research Source: JLL Research

Indianapolis, CBD

Land

lord l

ever

age Tenant leverage

Peaking market

Falling market

Bottoming market

Rising market

North Meridian/Carmel continues to have lowest vacancy in IndyOverall Indianapolis office vacancy ticked up slightly from last quarter as a result of the previously mentioned tenants moving into owner-occupied space. The overall Indianapolis office market vacancy rate now sits at 16.4 percent, with Class A at 16.6 percent and Class B at 16.1 percent. North Meridian/Carmel still boasts the lowest overall vacancy rate in the market at 9.9 percent. The CBD was the only one of the five major submarkets to see vacancy drop since last quarter and is now under the market average at 15.5 percent.

Asking rates continue to riseGross asking rates in metro Indianapolis currently stand at $19.78 per square foot, an increase of over four percent since this same time last year. The combination of strong leasing activity, new construction deliveries earlier this year with more on the way, and investors pumping capital into recently purchased buildings have driven up rental rates. This is especially true for Class A, which has seen rental rates increase by over one dollar since last year. Submarkets commanding the highest rents continue to be the CBD, Keystone and North Meridian/Carmel. All three of these submarkets currently have asking rents greater than $20.50 per square foot.

Overview of net absorption Historical net absorption (s.f.)

Source: JLL Research

Non-CBD1,538,661 1,630,041 1,499,520

2,469,1042,897,395

0500,000

1,000,0001,500,0002,000,0002,500,0003,000,000

2012 2013 2014 2015 2016

Class A finishes year with occupancy growthDespite negative absorption for the quarter, Class A office product still posted occupancy growth in 2016. CBD and Keystone Class A product showed the greatest amount of growth, both with over 50,000 square feet in net absorption. In fact, the CBD’s overall net absorption for the quarter was greater than for the past three quarters combined. Additionally, the CBD will receive another boost when Salesforce moves into its new location in Salesforce Tower next year and occupies over 230,000 square feet. Several northern submarkets are also poised to have occupancy growth next year when new construction comes online with the majority of space pre-leased.

14.0%15.0%16.0%17.0%18.0%19.0%20.0%

2012 2013 2014 2015 Q4 2016

Total Class A Class B

-200,000-100,000

0100,000200,000300,000400,000500,000

2012 2013 2014 2015 2016

Total Class A Class B

$14.00

$16.00

$18.00

$20.00

$22.00

$24.00

2012 2013 2014 2015 Q4 2016

Total Class A Class B

Office Statistics

Indianapolis | Q4 2016

Class Inventory (s.f.) Total net absorption (s.f.)

YTD total net absorption (s.f.)

YTD total net absorption (%

of stock)

Direct vacancy (%)

Total vacancy (%)

Average direct asking rent ($

p.s.f.)

YTD completions

(s.f.)

Under construction

(s.f.)CBD Totals 12,018,850 56,474 104,548 0.9% 15.3% 15.5% $20.60 0 25,361CBD Totals 12,018,850 56,474 104,548 0.9% 15.3% 15.5% $20.60 0 25,361Midtown Totals 874,212 -6,371 -14,556 -1.7% 19.1% 19.1% $14.98 0 0Northeast Totals 3,357,657 -342,046 -183,261 -5.5% 26.9% 27.0% $18.77 0 155,255Northwest Totals 3,018,633 -43,917 -65,495 -2.2% 19.6% 23.5% $18.28 115,358 0East/Southeast Totals 252,032 -908 -8,967 -3.6% 19.0% 19.0% $15.44 0 0Keystone Totals 4,052,470 18,474 71,701 1.8% 13.2% 13.9% $21.48 102,000 55,000North Meridian/Carmel Totals 6,511,868 -28,549 20,458 0.3% 9.8% 9.9% $20.52 90,250 192,361West/Southwest Totals 1,274,849 744 -7,257 -0.6% 20.5% 20.5% $14.59 0 0Greenwood Totals 457,719 13,143 29,375 6.4% 11.2% 11.2% $15.74 0 0Suburbs Totals 19,799,440 -389,430 -158,002 -0.8% 16.1% 16.9% $19.28 307,608 402,616Metro Totals 31,818,290 -332,956 -53,454 -0.2% 15.8% 16.4% $19.78 307,608 427,977

CBD A 7,101,003 75,624 68,344 1.0% 18.1% 18.3% $22.48 0 25,361CBD A 7,101,003 75,624 68,344 1.0% 18.1% 18.3% $22.48 0 25,361Midtown A 0 0 0 0.0% 0.0% 0.0% $0.00 0 0Northeast A 1,556,579 -243,519 -106,285 -6.8% 28.9% 28.9% $20.35 0 155,255Northwest A 1,550,100 -12,505 12,354 0.8% 12.4% 19.8% $19.95 115,358 0East/Southeast A 0 0 0 0.0% 0.0% 0.0% $0.00 0 0Keystone A 3,283,647 11,879 55,206 1.7% 14.5% 15.3% $22.20 102,000 55,000North Meridian/Carmel A 4,125,988 -32,349 -12,339 -0.3% 9.3% 9.4% $22.47 90,250 192,361West/Southwest A 0 0 0 0.0% 0.0% 0.0% $0.00 0 0Greenwood A 114,148 0 18,282 16.0% 2.8% 2.8% $15.75 0 0Suburbs A 10,630,462 -276,494 -32,782 -0.3% 14.2% 15.5% $21.64 307,608 402,616Metro A 17,731,465 -200,870 35,562 0.2% 15.7% 16.6% $21.97 307,608 427,977

CBD B 4,917,847 -19,150 36,204 0.7% 11.3% 11.5% $17.88 0 0CBD B 4,917,847 -19,150 36,204 0.7% 11.3% 11.5% $17.88 0 0Midtown B 874,212 -6,371 -14,556 -1.7% 19.1% 19.1% $14.98 0 0Northeast B 1,801,078 -98,527 -76,976 -4.3% 25.1% 25.2% $17.41 0 0Northwest B 1,468,533 -31,412 -77,849 -5.3% 27.1% 27.3% $16.55 0 0East/Southeast B 252,032 -908 -8,967 -3.6% 19.0% 19.0% $15.44 0 0Keystone B 768,823 6,595 16,495 2.1% 7.8% 7.8% $18.41 0 0North Meridian/Carmel B 2,385,880 3,800 32,797 1.4% 10.7% 10.9% $17.16 0 0West/Southwest B 1,274,849 744 -7,257 -0.6% 20.5% 20.5% $14.59 0 0Greenwood B 343,571 13,143 11,093 3.2% 13.9% 13.9% $15.74 0 0Suburbs B 9,168,978 -112,936 -125,220 -1.4% 18.4% 18.5% $16.55 0 0Metro B 14,086,825 -132,086 -89,016 -0.6% 15.9% 16.1% $17.01 0 0

Office Demand in the market

Indianapolis | Q4 2016

Requirements by size (by #) Quick statsSize Requirements250,000 + 2 Active requirements 119100,000 - 249,999 650,000 - 99,999 625,000 - 49,999 12 SF of active requirements 2,699,09515,000 - 24,999 65,000 – 14,999 54≤ 4,999 34 SF of average requirement 22,681

Requirements by industry (in SF)Industry RequirementsHealthcare 447,743Aerospace defense transportation 375,000Unknown 362,000Banking finance insurance 341,174Technology 257,559Law firm 207,500Government 186,749Association nonprofit union 114,944Media and entertainment 107,300Architecture engineering construction design 83,239Real estate 51,000Life sciences 35,000Other professional and business services 34,603 *Several requirements span multiple submarketsTelecom 30,000Accounting consulting research strategy 24,000 Industry concentrationsManufacturing and distribution 15,684Marketing advertising communications PR 13,500 CBDEducation 6,500 Largest industry demand: Law firmRetail and hospitality 4,000 Total active industry requirements: 191,500 SFEnergy and utilities 0 Northeast

Largest industry demand: Healthcare

Requirements by broker (by SF) Total active industry requirements: 282,000 SF

KeystoneLargest industry demand: Aerospace defense transportationTotal active industry requirements: 250,000 SF

North MeridianLargest industry demand: HealthcareTotal active industry requirements: 285,000 SF

NorthwestLargest industry demand: HealthcareTotal active industry requirements: 278,743 SF

Industry footprint

Industry footprint

Tenant footprint

42 16 28Growing Shrinking Stable

JLL16.9%

C + W26.7%

CBRE9.7%

Avison Young9.2%

Colliers8.7%

Newmark8.1%

Lee & Associates

4.2%

Resource4.1%

Other12.5%

Requirements by target submarket (in SF)

Q-to-Q change

304,000

728,147

919,278

1,094,322

1,100,130

1,233,405

0 200,000 400,000 600,000 800,000 1,000,000 1,200,000 1,400,000

Other

CBD

Northwest

Keystone

Northeast

North Meridian

0

10

20

30

40

Science andtechnical

Finance Nonprofit Professionaland business

services

Creative Unknown Consumeroriented

Shrinking Stable Growing

# of a

ctive

tena

nts

Office Leasing Activity Report Completed Transactions

Indianapolis | Q4 2016

This report analyzes all closed office leases > 5,000 s.f. in Class A and B office buildings

At a glance Leasing activity by size

Total s.f. leased YTD 2,897,395

Total transactions YTD 141

Total s.f. leased QTR 582,765

Total transactions QTR 41

Total Class A s.f. leased YTD 2,341,566

Total Class B s.f. leased YTD 555,829

Average term (mos) 83.0

Tenant footprint Leasing activity by industry Leasing activity by submarket

76 12 40Growing Shrinking Stable

Leasing activity by transaction typeRenewal 1,133,350Expansion in building 277,269Relocation within market 690,802Expansion in market 515,464New to market 196,193

Tenant movement Tenant movement by submarket (by # tenants)

Top 5 lease transactions during the yearTenant Address Submarket Size Type Footprint Term (mos)

Salesforce.com 111 Monument Circle CBD 227,781 Expansion in market Growing 162

Allied Solutions 340 1st Ave Sw North Meridian/Carmel 109,600 Expansion in market Growing 156

Stanley Security Solutions 8350 Sunlight Dr Northeast 80,000 Expansion in market Growing 132

Sallie Mae 8425 Woodfield Crossing Blvd Keystone 75,558 Relocation within market Growing 132

JD Byrider 12722 Hamilton Crossing North Meridian/Carmel 70,320 Renewal Growing 64

Historical leasing activity

12 4 20 37 68 0

500,000

1,000,000

1,500,000

40,000+ 30,000-39,999 20,000-29,999 10,000-19,999 <9,999

Total leased Number of leases

0

500,000

1,000,000

1,500,000

Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016

44.5%

20.9%

18.8%

7.1%6.1% 2.5%

Scientific andtechnicalProfessional andbusiness servicesFinance

Nonprofit

Consumer Oriented

Creative

30.1%

23.1%19.7%

13.0%

12.4%1.8% CBD

North Meridian/Carmel

Northwest

Keystone

Northeast

Other

49.2%

27.3%

11.5%7.1%

4.4% 0.5% Renewal/Expansion inBuildingRelocation in samesubmarketSuburban to Suburban

New to market

Suburban to CBD

CBD to Suburban

10 2

2

3 3

4

1 2

2 3

3

4 7 1

2

1 4 1

1 1 1 1 1 1 1

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

CBD Keystone North Meridian/Carmel Northeast NorthwestNew Submarket

MidtownNorthwestWest/SouthwestNortheastNorth Meridian/CarmelNew to marketKeystoneCBD

Old Submarket

*New deals only; excludes renewals and expansions in building

Office Development Report

Indianapolis | Q4 2016

This report analyzes all office developments under construction / renovation > 20,000 s.f.

Construction completions

307,608 Total delivered YTD (s.f.)

Completions in-depthTotal available at delivery (%) 29.4%

Total leased at delivery (%) 70.6%

Average floor plate (s.f.) 33,076

Average number of stories 3

Average rental rate $22.33 Historical completions

Top 5 projects delivered to date

Building Submarket Owner/developer RBA (s.f.) Spec or BTS Delivery date Leased at delivery (%)

7676 Interactive Way Northwest Duke Realty Corporation 115,358 BTS Q3 2016 100.0%River North at Keystone 8801 River Crossing Keystone PK Partners 102,000 BTS Q3 2016 92.6%

Lakeside Green Business Center 645 W Carmel Dr

North Meridian/Carmel Atapco Properties 61,050 Speculative Q3 2016 0.0%

580 E Carmel Dr North Meridian/Carmel The Garg Group 29,200 BTS Q1 2016 25.0%

#NUM!

Under construction / proposed

772,437 Under construction / proposed (s.f.)

Under construction/renovation in-depthTotal pre-leased (%) 56.4%

Total under construction (s.f.) 427,977

Total proposed (s.f.) 344,460

Average floor plate (s.f.) 16,638

Average rental rate $16.00 Amount preleased by building status (s.f., excludes YTD completions)

Top 5 projects currently under construction

Building Submarket Owner/developer RBA (s.f.) Spec or BTS Delivery date Pre-leased (%)

340 1st Ave SW North Meridian/Carmel Old Town Development 132,361 BTS Q4 2017 94.7%

8350 Sunlight Dr Northeast Ambrose Property Group 80,000 BTS Q3 2017 100.0%

11939 N Meridian St North Meridian/Carmel Citimark 60,000 BTS Q1 2017 61.1%Walker Place at River North -8940 River Crossing Blvd Keystone Walker Information / PK Partners 55,000 BTS Q4 2017 78.2%

3 Municipal Dr Northeast Braden Business Systems 45,255 BTS Q3 2017 49.2%

050,000

100,000150,000200,000250,000300,000350,000

2012 2013 2014 2015 2016

0

100,000

200,000

300,000

400,000

500,000

Under Construction Proposed

RBA SF Amount Preleased

Office Sales Activity Report

Indianapolis | Q4 2016

This report analyzes all year-to-date office sales > 20,000 s.f.

At a glance Sales activity by building class

Total volume YTD $592,866,531

Number of transactions 23

Average Class A price p.s.f. $81

Average Class A cap rate 7.9%

Urban sales volume as % of total 56.3%

Suburban sales volume as % of total 43.7%

Cap rate range Transactions details

Core Class A CBD 8.5-9.5% Number of partial interest transactions 3 Number of foreign buyers - Foreign capital $ $0

Core Class A suburban 8.0-9.0% Number of domestic buyers 23 Domestic Capital $ $592,866,531

Sales volume $ by submarket Top buyers (s.f.) Top sellers (s.f.)

Top 10 sales transactions year-to-date

Building address Buyer company Seller company Size (s.f.) Sale price ($) $ p.s.f. Sale date

Parkwood Crossing Rubenstein Partners / Strategic Capital Partners Duke Realty Corporation 1,202,076 $162,900,000 $136 Aug-16

111 Monument Cir Hertz Investment Group Equity Commonwealth 1,121,763 $151,438,005 $135 Aug-16

101-115 W Washington St Hertz Investment Group Equity Commonwealth 650,244 $78,029,280 $120 Aug-16

135 N. Pennsylvania St The Hearn Company / CrossHarbor Capital Partners True North Management Group 435,000 $40,000,000 $92 Apr-16

Castle Creek Zeller Realty Group Starwood Property Trust, Inc. 321,044 $21,500,000 $67 Sep-16

Lockerbie Marketplace Gersham Partners / Citimark Christel Dehaan Family Foundation 179,870 $16,750,000 $93 Mar-16

Woodland Corporate Park Coastal Partners, LLC. Duke Realty Corporation 209,056 $14,509,000 $69 Aug-16

550 Congressional Blvd Tryperion Partners REI Real Estate Services/Perennial Investments 106,433 $11,250,000 $106 Oct-16

41 E. Washington St Drury Hotels IBJ Media 57,625 $11,000,000 $191 Feb-16

Allison Pointe C-III Asset Management Receivership 216,555 $10,600,000 $49 Aug-16

$489,866,531

$103,000,000

$592,866,531

$0$100,000,000$200,000,000$300,000,000$400,000,000$500,000,000$600,000,000$700,000,000

A B Grand Total

38.7%

27.5%

6.7%3.6%

15.6%

Hertz Investment GroupRubenstein Partners / Strategic Capital PartnersThe Hearn Company / CrossHarbor Capital PartnersZeller Realty GroupGersham Partners / CitimarkMission Peak CapitalCoastal Partners, LLC.Other

$3,200,000

$7,300,000

$11,550,000

$20,509,000

$32,100,000

$187,600,000

$330,607,531

Midtown

West/Southwest

Keystone

Northwest

Northeast

North Meridian / Carmel

CBD

38.7%

29.9%

6.7%3.6%

5.8%

Equity CommonwealthDuke Realty CorporationTrue North Management GroupStarwood Property Trust, Inc.Christel Dehaan Family FoundationHSBC BankREI Real Estate Services/Perennial InvestmentsOther

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000 Total Employment Unemployment

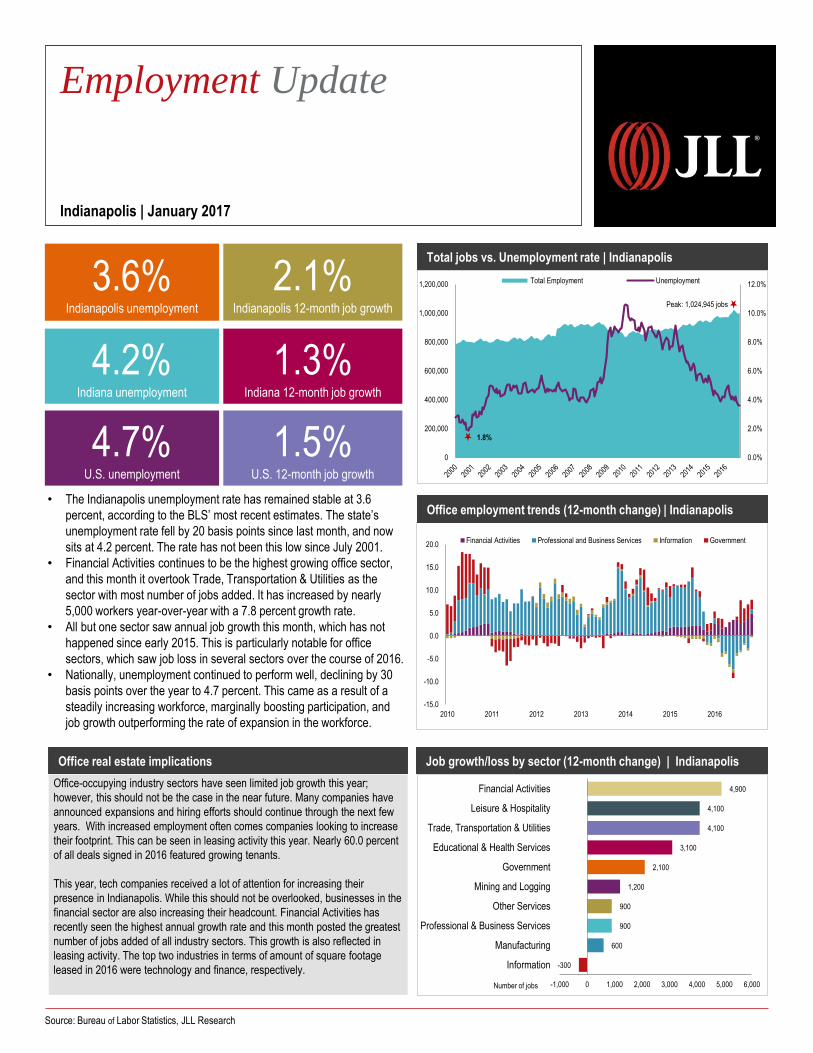

Office-occupying industry sectors have seen limited job growth this year;

however, this should not be the case in the near future. Many companies have

announced expansions and hiring efforts should continue through the next few

years. With increased employment often comes companies looking to increase

their footprint. This can be seen in leasing activity this year. Nearly 60.0 percent

of all deals signed in 2016 featured growing tenants.

This year, tech companies received a lot of attention for increasing their

presence in Indianapolis. While this should not be overlooked, businesses in the

financial sector are also increasing their headcount. Financial Activities has

recently seen the highest annual growth rate and this month posted the greatest

number of jobs added of all industry sectors. This growth is also reflected in

leasing activity. The top two industries in terms of amount of square footage

leased in 2016 were technology and finance, respectively.

Source: Bureau of Labor Statistics, JLL Research

Employment Update

Metro Indianapolis | August 2015

Employment Update

Indianapolis | January 2017

Office employment trends (12-month change) | Indianapolis

Total jobs vs. Unemployment rate | Indianapolis

Office real estate implications

• The Indianapolis unemployment rate has remained stable at 3.6

percent, according to the BLS’ most recent estimates. The state’s

unemployment rate fell by 20 basis points since last month, and now

sits at 4.2 percent. The rate has not been this low since July 2001.

• Financial Activities continues to be the highest growing office sector,

and this month it overtook Trade, Transportation & Utilities as the

sector with most number of jobs added. It has increased by nearly

5,000 workers year-over-year with a 7.8 percent growth rate.

• All but one sector saw annual job growth this month, which has not

happened since early 2015. This is particularly notable for office

sectors, which saw job loss in several sectors over the course of 2016.

• Nationally, unemployment continued to perform well, declining by 30

basis points over the year to 4.7 percent. This came as a result of a

steadily increasing workforce, marginally boosting participation, and

job growth outperforming the rate of expansion in the workforce.

1.8%

Peak: 1,024,945 jobs

Number of jobs

Job growth/loss by sector (12-month change) | Indianapolis

2.1%Indianapolis 12-month job growth

4.2%Indiana unemployment

1.3%Indiana 12-month job growth

3.6%Indianapolis unemployment

4.7%U.S. unemployment

1.5%U.S. 12-month job growth

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

2010 2011 2012 2013 2014 2015 2016

Financial Activities Professional and Business Services Information Government

-300

600

900

900

1,200

2,100

3,100

4,100

4,100

4,900

-1,000 0 1,000 2,000 3,000 4,000 5,000 6,000

Information

Manufacturing

Professional & Business Services

Other Services

Mining and Logging

Government

Educational & Health Services

Trade, Transportation & Utilities

Leisure & Hospitality

Financial Activities

News on the street | Indianapolis businesses expanding, contracting, etc.

HomeAdvisor│ Technology: Expanding

After opening its first Indianapolis office earlier this year, HomeAdvisor is already expanding into a second office location downtown. This will create up to 170 new

jobs by early 2017.

TriMedx│ Technology: Expanding

The healthcare technology company announced that it is spending $21.5 million to expand its operations and will hire more than 100 workers by 2020.

Angie’s List│ Technology: Contracting

After facing increased competition and the need to be more profitable, Angie’s List has begun to layoff an undisclosed number of its 1,800 employee workforce. Cuts

being made are part of an effort to save between $15 and $20 million for the company.

Realync Corp.│ Technology: Expanding

The Chicago-based real estate technology firm plans to expand into Indianapolis, creating 50 jobs by the end of 2020.

Covideo│ Technology: Expanding

The video-email technology company will nearly double the size of its Broad Ripple office to make room for 10 new hires planned for 2017.

Rx Help Centers│ Healthcare: Expanding

The firm specializing in prescription discounts announced it will open an operations center on the northwest side near its current facility in Ten Fortune Park. The

expansion will result in 230 jobs by 2020.

CliqStudios│ e-Commerce: Expanding

The online retailer of semi-custom kitchen cabinets is opening a design studio in Indianapolis, the first outside of Minnesota. The company expects to hire 200

employees by 2020.

November 2014 November 2015 November 2016

Total non-farm

employment1,0016,800

1.5%

1,034,900

1.4%

1,056,500

2.1%

Unemployment rate 5.5% 4.2% 3.6%

Indianapolis supersectors November 2014 November 2015 November 2016

Mining, Logging & Construction 45,600 -2.4% 47,500 4.2% 48,700 2.5%

Manufacturing 89,800 2.5% 89,900 0.1% 90,500 0.7%

Trade, Transportation, & Utilities 215,000 0.5% 221,400 3.0% 225,500 1.9%

Information 16,500 -1.2% 16,000 -3.0% 15,700 -1.9%

Financial Activities 61,900 1.8% 62,900 1.6% 67,800 7.8%

Professional & Business

Services167,800 5.5% 166,300 -0.9% 167,200 0.5%

Educational & Health Services 144,700 -0.4% 149,900 3.6% 153,000 2.1%

Leisure & Hospitality 101,700 2.4% 104,900 3.1% 109,000 3.9%

Other Services 43,800 1.9% 44,500 1.6% 45,400 2.0%

Government 130,000 0.2% 131,600 1.2% 133,700 1.6%

Employment statistics | Indianapolis Industry stratification | Indianapolis

21.3%

15.8%

14.5%12.7%

10.3%

8.6%

6.4%

4.6%4.3% 1.5% Trade, transportation and Utilities

Professional and Business Services

Educational and Health Services

Government

Leisure and Hospitality

Manufacturing

Financial Activities

Mining, Logging and construction

Other Services

Information

Quarter in review

The CBD closed out a strong year of leasing activity by posting 56,000 square feet

of net absorption in the fourth quarter. This brings the year-end total to 105,000

square feet, easily the highest in metro Indianapolis. This occupancy growth

enabled the vacancy rate to decrease by two full percentage points since the end

of 2015.

Tenants new to downtown was a key driver for this increase in leasing activity.

2016 saw 23 deals signed totaling 226,000 square feet involving tenants either

new to the Indianapolis office market or moving from the suburbs to the CBD. This

is more than the previous two years combined (16 deals totaling 172,000 square

feet).

The decision by Salesforce.com to lease 228,000 square feet in the since

renamed Salesforce Tower had a profound impact leasing activity. The technology

sector accounted for 31.0 percent of this tenant movement.

Outlook

Downtown Indianapolis is poised for continued growth in 2017 with the technology

industry continuing to lead the way. In addition to the pending occupancy by

Salesforce, a group of investors stand ready to open The Union in January.

The Union will be housed in the former Brougher Building, past home to Eli Lilly

and once a candidate for conversion to multi-family. Instead, the century-old

122,000-square-foot-building has been re-purposed to cater to Indianapolis’

burgeoning tech scene by offering office space with short-term leases. The

building will open almost fully occupied with leases already in place with such

companies as Springbuk, SmartFile and E-Lilly to name a few.

With all this growth, it’s no surprise that the CBD is currently enjoying 7.0 percent

rent growth year-over-year, highest in metro Indianapolis by a wide margin. Look

for rental rates to continue ticking upwards next year as improvements to several

buildings that traded hands in 2016 begin taking shape.

Historical net absorption (s.f.)

Historical vacancy rates

Historical asking rents ($ p.s.f.)

CBD | Q4 2016

Tenant migration keys occupancy growth

Office Insight

12,018,850Total inventory (s.f.)

56,474Q4 2016 net absorption (s.f.)

$20.60Direct average asking rent

25,361Total under construction (s.f.)

15.5%Total vacancy

104,548YTD net absorption (s.f.)

7.0%12-month rent growth

0.0% Total preleased

-200,000

0

200,000

400,000

2013 2014 2015 2016

Total Class A Class B

0.0%

10.0%

20.0%

30.0%

2013 2014 2015 2016

Total Class A Class B

$14.00

$19.00

$24.00

2013 2014 2015 2016

Total Class A Class B

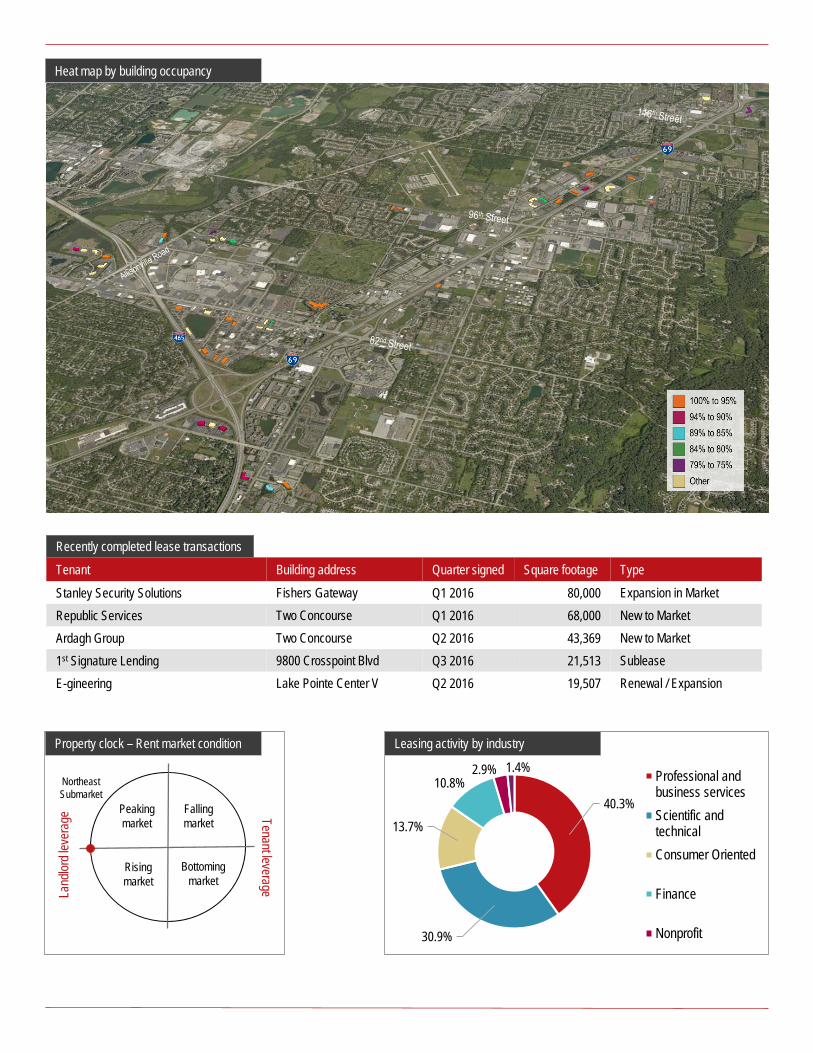

Property clock – Rent market condition

Land

lord

leve

rage

Tenant leverage

CBD

Submarket

Peaking

market

Falling

market

Bottoming

marketRising

market

Heat map by building occupancy

Tenant Building address Quarter signed Square footage Type

Salesforce.com Salesforce Tower Q2 2016 227,781 Expansion in Market

Milliman Market Tower Q3 2016 42,236 Relocation / Expansion

HNTB Salesforce Tower Q2 2016 31,686 Renewal

Finishmaster PNC Center Q4 2016 27,516 Renewal

E-Lilly The Union Q4 2016 26,517 Relocation / Expansion

Recently completed lease transactions

Leasing activity by industry

46.4%

17.8%

16.2%

7.4%

6.1% 6.1%Scientific andtechnical

Nonprofit

Professional andbusiness services

Finance

Creative

Quarter in review

Keystone ended 2016 on a high note. The submarket was second only to the CBD

for net absorption in the fourth quarter and for the year. Much of this occupancy

growth is due to tenants taking down space in the newly constructed River North

at Keystone as well as several expansions and relocations. In fact, seven of the 10

largest deals in Keystone this year were for tenants growing their footprint.

With such occupancy growth, it should be no surprise that Keystone boasts one of

the lowest vacancy rates in the Indianapolis office market. Total vacancy dropped

by 50 basis points since last quarter. Class B vacancy has declined even further

and now sits at 7.8 percent, the lowest in the market by nearly four percentage

points (CBD has the second lowest Class B vacancy at 11.5 percent).

Due to continued demand and low vacancy rates, overall asking rates are the

highest in Indianapolis. Asking rates in Keystone are nearly one dollar more than

the next highest suburban submarket ($20.52 in North Meridian/Carmel). Overall

asking rates have grown by 3.3 percent year-over-year. Class A asking rates have

grown by even more, increasing by 3.9 percent since this time last year and by 6.2

percent since 2013.

Outlook

Keystone continues to prove to be one of the best submarkets to locate in

Indianapolis for office space. Following the success of River North at Keystone,

PK Partners broke ground this quarter on a 55,000-square-foot building in which

Walker Information will lease over three-quarters of that space. Recently,

Keystone Realty Group affiliate Green Indy, LLC announced plans to build a

60,000-square-foot commercial building, half of which being speculative office

space, named Alexander at the Crossing. With over one million square feet in

active tenants looking in Keystone, the submarket is poised to have continued

occupancy growth in the future.

Historical net absorption (s.f.)

Historical vacancy rates

Historical asking rents ($ p.s.f.)

Keystone | Q4 2016

Keystone submarket ends year on a high note

Office Insight

4,052,470Total inventory (s.f.)

18,474Q4 2016 net absorption (s.f.)

$21.48Direct average asking rent

55,000Total under construction (s.f.)

13.9%Total vacancy

71,701YTD net absorption (s.f.)

3.3%12-month rent growth

78.2%Total preleased

-50,000

0

50,000

100,000

2013 2014 2015 2016

Total Class A Class B

0.0%

5.0%

10.0%

15.0%

20.0%

2013 2014 2015 2016

Total Class A Class B

$14.00

$17.00

$20.00

$23.00

2013 2014 2015 2016

Total Class A Class B

Heat map by building occupancy

Tenant Building address Quarter signed Square footage Type

Sallie Mae Three Woodfield Q1 2016 75,558 Relocation / Expansion

Walker Information 8904 River Crossing Q3 2016 42,500 Relocation

Paychex 8335 Keystone Crossing Q3 2016 41,182 Renewal / Expansion

Blackboard One River Crossing Q3 2016 28,674 Relocation

Oak Street Funding 8888 Keystone Crossing Q2 2016 23,891 Sublease

Recently completed lease transactions

Property clock – Rent market condition

Land

lord

leve

rage

Tenant leverage

Keystone

Submarket

Peaking

market

Falling

market

Bottoming

marketRising

market

46.5%

30.4%

16.9%

3.7% 2.6%Finance

Professional and businessservices

Scientific and technical

Consumer Oriented

Nonprofit

Leasing activity by industry

Quarter in review

North Meridian/Carmel finished off the year with one of the lowest vacancy rates

and highest asking rates in the Indianapolis office market. Overall vacancy sits at

9.9 percent, the only submarket to have this rate in the single digits. The Class A

rate is even lower at 9.4 percent. This is an increase from last quarter, but is

mainly due to a few tenants vacating large spaces. Occupancy growth was also

limited during the fourth quarter because of this; however, net absorption was still

positive for the year.

Due to consistently low vacancy rates and high asking rates, it is unsurprising that

numerous construction projects began or were announced in 2016. In addition to

the four projects that either completed or started construction this year, three more

buildings have been announced. Carmel Pointe (117,500 square feet), Midtown

West (80,000 square feet), and Merchants Bank Building (80,000 square feet) are

all slated to break ground in the first half of 2017 and be completed in 2018. When

completed, over 550,000 square feet of office product would be added to the

submarket over the next two years.

Investment activity continued this quarter with two additional sales. Northpoint

Center (550 Congressional Blvd.) and Pennwood I & II (11405-11495 N

Pennsylvania St.) were purchased by Tryperion Partners and Kimmel Square,

LLC, respectively. With four sales totaling nearly $188 million, North

Meridian/Carmel had the most investment activity of the suburban submarkets.

Outlook

Expect to see vacancy rates increase in 2017 as several large tenants are

downsizing or exiting the market. Firestone will be vacating its space in Parkwood

West following the opening of parent company Bridgestone Americas, Inc.’s new

headquarters in Nashville, Tennessee. Additionally, Technicolor will downsize

from its current space at 101 W. 103rd Street, with 100,000 square feet already

available for sublease. However, North Meridian/Carmel is poised to remain

popular to tenants and investors alike. The submarket remains a favorite among

active tenants and additional investment activity is expected in early 2017.

Historical net absorption (s.f.)

Historical vacancy rates

Historical asking rents ($ p.s.f.)

North Meridian/Carmel | Q4 2016

More options coming soon to constricted market

Office Insight

6,511,868Total inventory (s.f.)

-28,549Q4 2016 net absorption (s.f.)

$20.52Direct average asking rent

192,361Total under construction (s.f.)

9.9%Total vacancy

20,458YTD net absorption (s.f.)

3.0%12-month rent growth

84.2% Total preleased

-100,000

0

100,000

200,000

300,000

2013 2014 2015 2016

Total Class A Class B

0.0%

5.0%

10.0%

15.0%

2013 2014 2015 2016

Total Class A Class B

$14.00

$17.00

$20.00

$23.00

2013 2014 2015 2016

Total Class A Class B

Tenant Building address Quarter signed Square footage Type

Allied Solutions Midtown Carmel Building 1 Q1 2016 109,600 Expansion in Market

JD Byrider Hamilton Crossing I Q3 2016 70,320 Renewal / Expansion

NextGear Capital, Inc. 1320 City Center Dr Q1 2016 44,479 Expansion in Building

Morgan Stanley Eight Parkwood Q3 2016 30,571 Renewal

Blue & Co., LLC. Hamilton Crossing III Q1 2016 29,671 Expansion in Building

Recently completed lease transactions

Property clock – Rent market condition

Land

lord

leve

rage T

enant leverage

North Meridian/Carmel

Submarket

Peaking

market

Falling

market

Bottoming

marketRising

market

Heat map by building occupancy

Nor

th M

erid

ian

39.2%

36.1%

20.0%

3.0% 0.9%0.8%

Finance

Scientific and technical

Professional and businessservicesConsumer Oriented

Creative

Nonprofit

Leasing activity by industry

116th Street

Quarter in review The Northeast submarket felt the impact of corporate consolidation this quarter as Roche Diagnostics vacated nearly 200,000 square feet of tracked office space in favor of having everyone under one roof in newly constructed space on its corporate campus. This is just one example of several companies downsizing in the submarket (Comcast, Marsh and Schwab are others) that led to over 300,000 square feet of negative net absorption in the fourth quarter and -180,000 square feet for the year. This corporate downsizing led overall vacancy to increase by nearly 10 percentage points since last quarter.

However, the submarket stands ready to bounce back quickly in 2017. Construction will wrap up on build-to-suit projects for Blue Sky Technology Partners, Braden Business Systems and Stanley Security next year. This space is already nearly 80.0 percent preleased. Further, RQAW Corporation should break ground on its new headquarters in downtown Fishers as well.

Meanwhile the purchases of Castle Creek III-VI by Zeller Realty Group and Woodland Center I & II and Lake Pointe Center II by C-III Asset Management out of receivership will help to reposition the assets that have been neglected for some time.

Outlook The Northeast continues to offer one of the lowest asking rates among the five major Indianapolis office submarkets. With several large tracts now available for lease, investment capital being pumped into the submarket and new amenities on the way (Ikea, TopGolf, The Yard), the Northeast should continue to see high levels of tenant activity next year. Currently, there remains 1.2 million square feet of active tenants considering space in the Northeast, second only to North Meridian/Carmel.

Historical net absorption (s.f.)

Historical vacancy rates

Historical asking rents ($ p.s.f.)

Northeast | Q4 2016

Corporate consolidations impact Northeast

Office Insight

3,357,657Total inventory (s.f.)

-342,046Q4 2016 net absorption (s.f.)

$18.77Direct average asking rent

155,255Total under construction (s.f.)

27.0%Total vacancy

-183,261YTD net absorption (s.f.)

5.2%12-month rent growth

78.8% Total preleased

-200,000

-100,000

0

100,000

2013 2014 2015 2016

Total Class A Class B

0.0%

10.0%

20.0%

30.0%

40.0%

2013 2014 2015 2016

Total Class A Class B

$14.00

$16.00

$18.00

$20.00

$22.00

2013 2014 2015 2016

Total Class A Class B

Tenant Building address Quarter signed Square footage Type

Stanley Security Solutions Fishers Gateway Q1 2016 80,000 Expansion in MarketRepublic Services Two Concourse Q1 2016 68,000 New to MarketArdagh Group Two Concourse Q2 2016 43,369 New to Market1st Signature Lending 9800 Crosspoint Blvd Q3 2016 21,513 SubleaseE-gineering Lake Pointe Center V Q2 2016 19,507 Renewal / Expansion

Recently completed lease transactions

Heat map by building occupancy

Property clock – Rent market condition

Land

lord l

ever

age Tenant leverage

NortheastSubmarket

Peaking market

Falling market

Bottoming market

Rising market

40.3%

30.9%

13.7%

10.8%2.9% 1.4% Professional and

business servicesScientific andtechnicalConsumer Oriented

Finance

Nonprofit

Leasing activity by industry

Quarter in review

The Northwest submarket closed out 2016 with -44,000 square feet of net

absorption during the fourth quarter. This brings the year-end absorption total to

-65,000 square feet. As a result of this occupancy loss, total vacancy in the

submarket increased by more than five percentage points and currently sits at

23.5 percent. Only the Northeast has a higher vacancy rate at 27.0 percent.

However, leasing activity began to pick up towards the end of the year. In fact,

36.0 percent of all leasing activity that took place in the Northwest submarket this

year occurred during the fourth quarter, including four of the top 10. Further, the

Northwest saw three transactions close in 2016 involving tenants new to the

Indianapolis office market (leasing data accounts for all leases signed in excess of

5,000 square feet). The CBD was the only one of the five major submarkets with

more.

Additionally, nearly 65.0 percent of Northwest leases signed this year were new

deals or expansions compared to only 40.0 percent in 2015. The top of the

market, namely Class A, also performed well in 2016 with 12,000 square feet of

absorption. This ranks ahead of both the Northeast and North Meridian/Carmel

submarkets this year.

Outlook

The Northwest submarket continues to boast the lowest asking rates among the

five major office submarkets in metro Indianapolis and is currently seeing just

under 1 million square feet of active tenant requirements. The submarket could be

poised for continued leasing velocity due to its affordability and amount of

available space. The recently constructed Woodland Corporate Park VII, for

example, is available for sublease following the acquisition of Interactive

Intelligence by California-based Genesys, offering in excess of 100,000 square

feet of Class A space.

Historical net absorption (s.f.)

Historical vacancy rates

Historical asking rents ($ p.s.f.)

Northwest ends year with rise in leasing velocity

Office Insight

Northwest | Q4 2016

3,018,633Total inventory (s.f.)

-43,917Q4 2016 net absorption (s.f.)

$18.28Direct average asking rent

0Total under construction (s.f.)

23.5%Total vacancy

-65,495YTD net absorption (s.f.)

1.7%12-month rent growth

0.0% Total preleased

-100,000

0

100,000

200,000

300,000

2013 2014 2015 2016

Total Class A Class B

0.0%

10.0%

20.0%

30.0%

2013 2014 2015 2016

Total Class A Class B

$14.00

$16.00

$18.00

$20.00

$22.00

2013 2014 2015 2016

Total Class A Class B

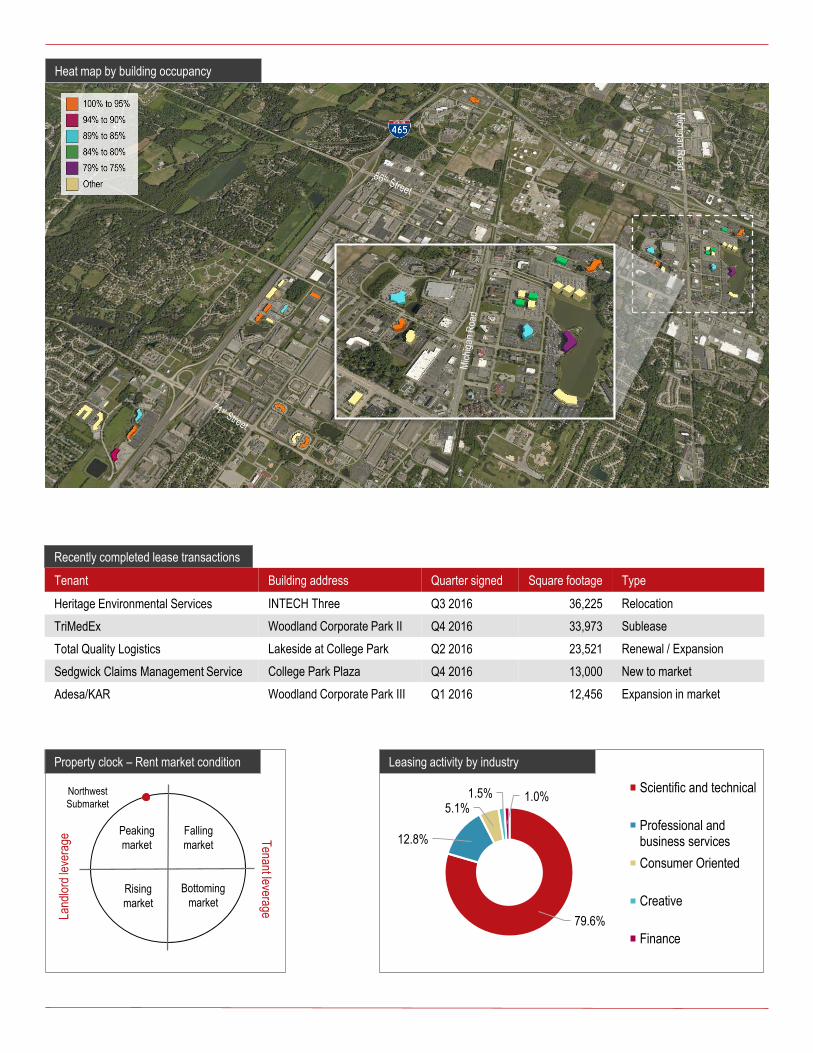

Heat map by building occupancy

Tenant Building address Quarter signed Square footage Type

Heritage Environmental Services INTECH Three Q3 2016 36,225 Relocation

TriMedEx Woodland Corporate Park II Q4 2016 33,973 Sublease

Total Quality Logistics Lakeside at College Park Q2 2016 23,521 Renewal / Expansion

Sedgwick Claims Management Service College Park Plaza Q4 2016 13,000 New to market

Adesa/KAR Woodland Corporate Park III Q1 2016 12,456 Expansion in market

Recently completed lease transactions

Property clock – Rent market condition

Land

lord

leve

rage T

enant leverage

Northwest

Submarket

Peaking

market

Falling

market

Bottoming

marketRising

market

Michigan R

oad

Leasing activity by industry

79.6%

12.8%

5.1%1.5% 1.0%

Scientific and technical

Professional andbusiness services

Consumer Oriented

Creative

Finance

About JLL

JLL (NYSE: JLL) is a professional services and investment management firm offering specialized real estate services to clients seeking increased

value by owning, occupying and investing in real estate. A Fortune 500 company with annual fee revenue of $5.2 billion and gross revenue of $6.0

billion, JLL has more than 280 corporate offices, operates in more than 80 countries and has a global workforce of more than 60,000. On behalf of its

clients, the firm provides management and real estate outsourcing services for a property portfolio of 4.0 billion square feet, or 372 million square

meters, and completed $138 billion in sales, acquisitions and finance transactions in 2015. Its investment management business, LaSalle Investment

Management, has $58.3 billion of real estate assets under management. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle

Incorporated. For further information, visit www.jll.com.

About JLL Research

JLL’s research team delivers intelligence, analysis and insight through market-leading reports and services that illuminate today’s commercial real

estate dynamics and identify tomorrow’s challenges and opportunities. Our more than 400 global research professionals track and analyze economic

and property trends and forecast future conditions in over 60 countries, producing unrivalled local and global perspectives. Our research and expertise,

fueled by real-time information and innovative thinking around the world, creates a competitive advantage for our clients and drives successful

strategies and optimal real estate decisions.

This publication is the sole property of Jones Lang LaSalle IP, Inc. and must not be copied, reproduced or transmitted in any form or by any means,

either in whole or in part, without prior written consent of Jones Lang LaSalle IP, Inc.

COPYRIGHT © JONES LANG LASALLE IP, INC. 2017

Mike Cagna

Senior Research Analyst

+1 317 810 7358

Brianna Marshall

Research Analyst

+ 1 317 810 7360

For more information, please contact: