nucor’s - covering steel, scrap metal, stainless ... · pdf filerebar steel cold...

TRANSCRIPT

2

Nucor’s Position Of Strength

• Financial Strength

• Low & Highly Variable Cost Structure

• Highly Flexible Production Capabilities

• Product Diversification and Market Leadership Positions

• Nucor’s People = THE RIGHT PEOPLE for our culture!!!

• Strong Balance Sheet

• Conservative Financial Practices

• Healthy Cash Flow Generation Through The Cycle

• Highest Credit Rating Among North American Steel Producers, tied for highest Globally

• No Pension Obligations and immaterial Post-Retirement Medical Liabilities

• Superior Financial Flexibility

25

Nucor’s Financial Strength

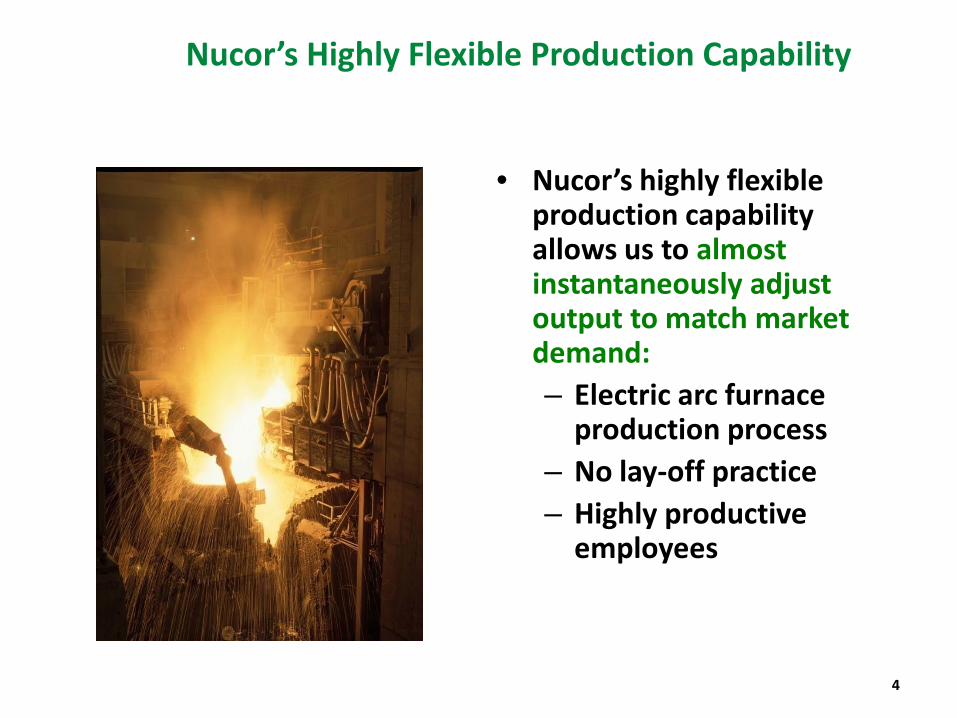

Nucor’s Highly Flexible Production Capability

• Nucor’s highly flexible production capability allows us to almost instantaneously adjust output to match market demand:– Electric arc furnace

production process – No lay-off practice– Highly productive

employees

4

Nucor’s People –Our Biggest Competitive Advantage

5

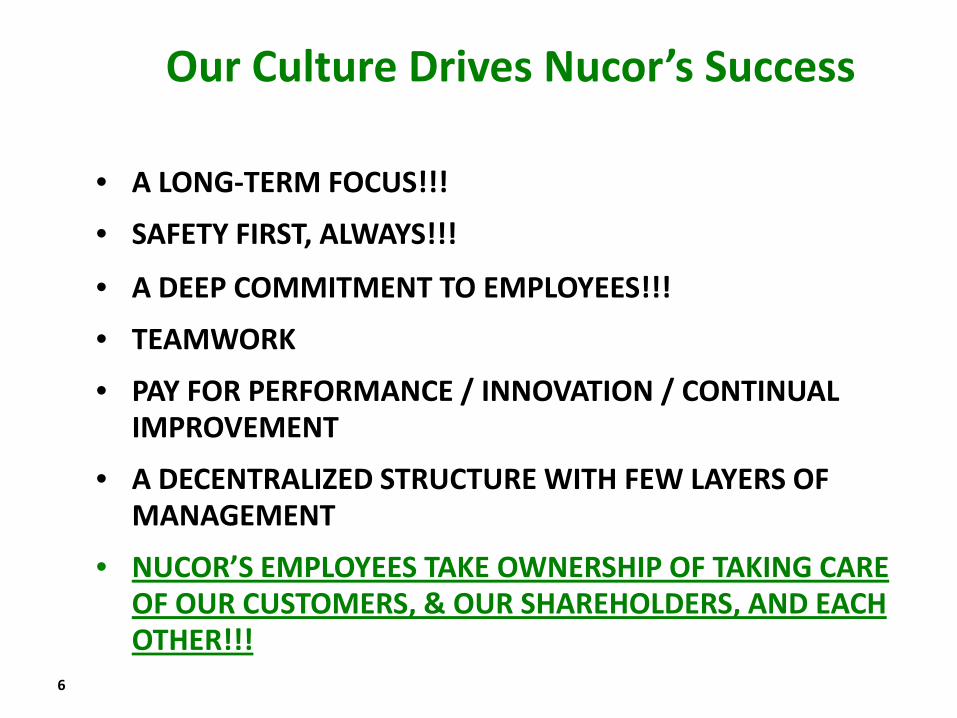

Our Culture Drives Nucor’s Success

• A LONG-TERM FOCUS!!!

• SAFETY FIRST, ALWAYS!!!

• A DEEP COMMITMENT TO EMPLOYEES!!!

• TEAMWORK

• PAY FOR PERFORMANCE / INNOVATION / CONTINUAL IMPROVEMENT

• A DECENTRALIZED STRUCTURE WITH FEW LAYERS OF MANAGEMENT

• NUCOR’S EMPLOYEES TAKE OWNERSHIP OF TAKING CARE OF OUR CUSTOMERS, & OUR SHAREHOLDERS, AND EACH OTHER!!!

6

7

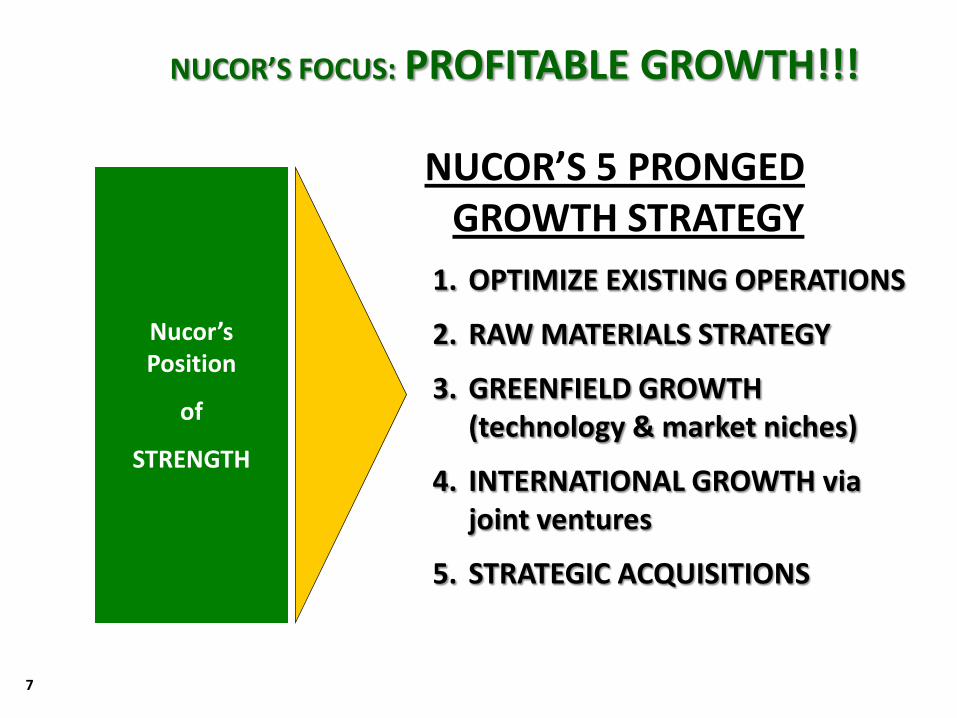

NUCOR’S FOCUS: PROFITABLE GROWTH!!!

NUCOR’S 5 PRONGED GROWTH STRATEGY

Nucor’s Position

of

STRENGTH

1. OPTIMIZE EXISTING OPERATIONS

2. RAW MATERIALS STRATEGY

3. GREENFIELD GROWTH (technology & market niches)

4. INTERNATIONAL GROWTH via joint ventures

5. STRATEGIC ACQUISITIONS

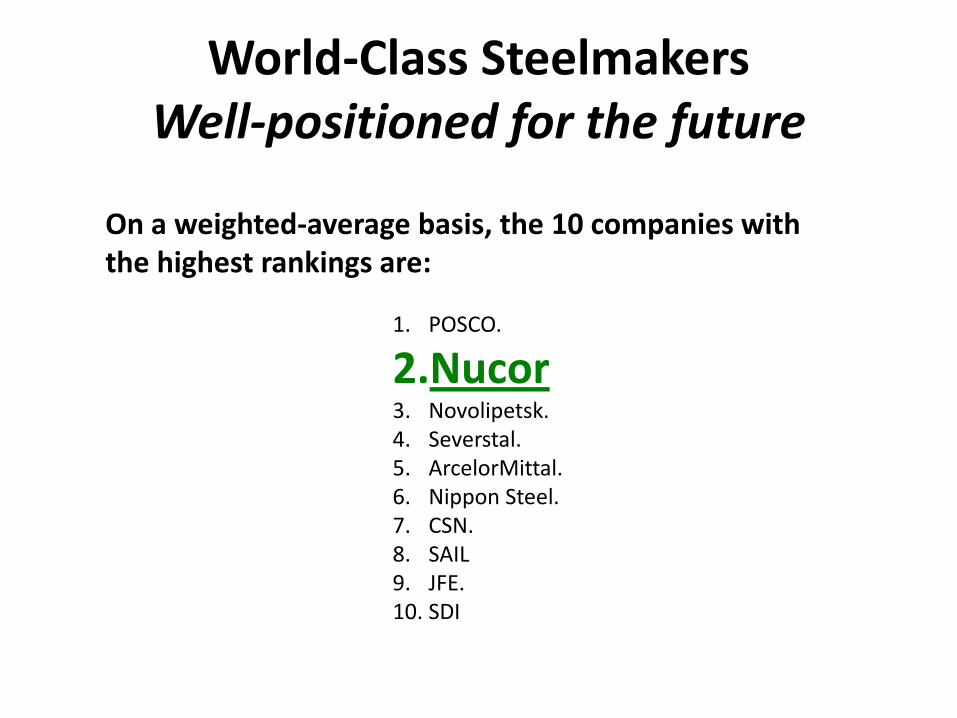

World-Class SteelmakersWell-positioned for the future

On a weighted-average basis, the 10 companies with the highest rankings are:

1. POSCO.

2.Nucor3. Novolipetsk. 4. Severstal. 5. ArcelorMittal. 6. Nippon Steel.7. CSN. 8. SAIL9. JFE. 10. SDI

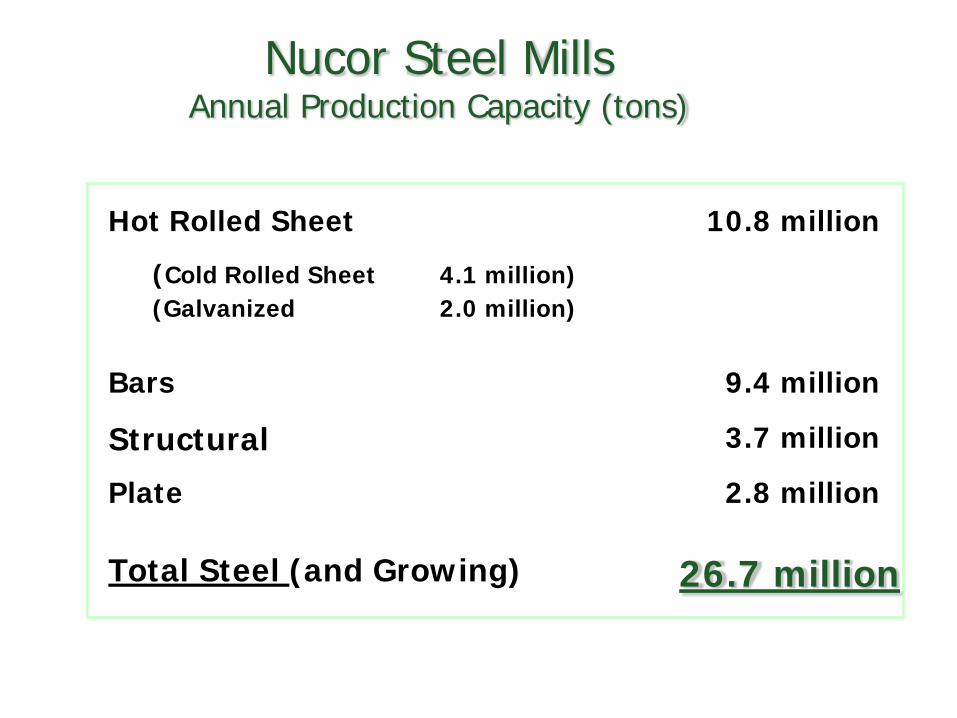

Nucor Steel Mills-23

Nucor Steel Mills Annual Production Capacity (tons)

Hot Rolled Sheet

(Cold Rolled Sheet 4.1 million)(Galvanized 2.0 million)

10.8 million

Bars 9.4 million

Structural 3.7 million

Plate 2.8 million

Total Steel (and Growing) 26.7 million

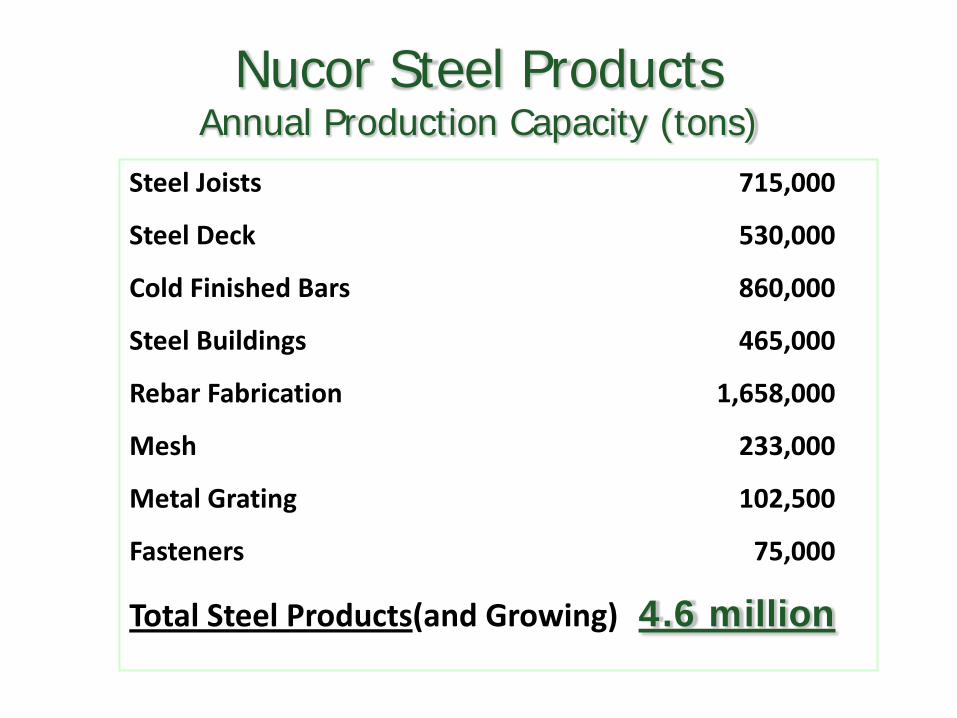

Nucor Steel Products

Nucor Steel Products Annual Production Capacity (tons)

Steel Joists 715,000

Steel Deck 530,000

Cold Finished Bars 860,000

Steel Buildings 465,000

Rebar Fabrication 1,658,000

Mesh 233,000

Metal Grating 102,500

Fasteners 75,000

Total Steel Products(and Growing) 4.6 million

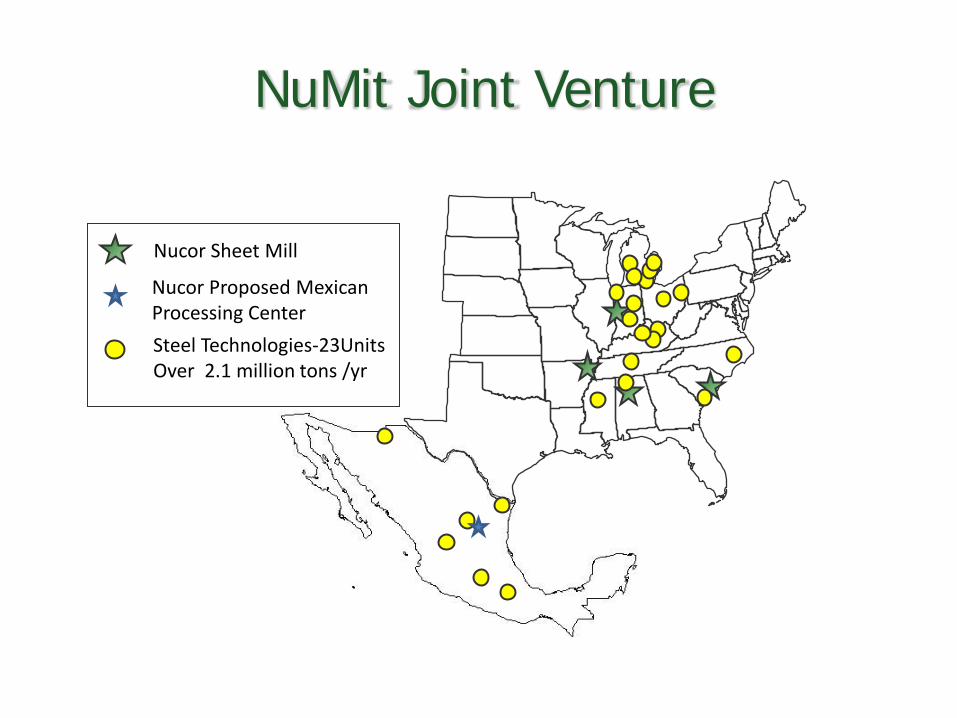

Nucor Proposed MexicanProcessing Center

NuMit Joint Venture

Nucor Sheet Mill

Steel Technologies-23UnitsOver 2.1 million tons /yr

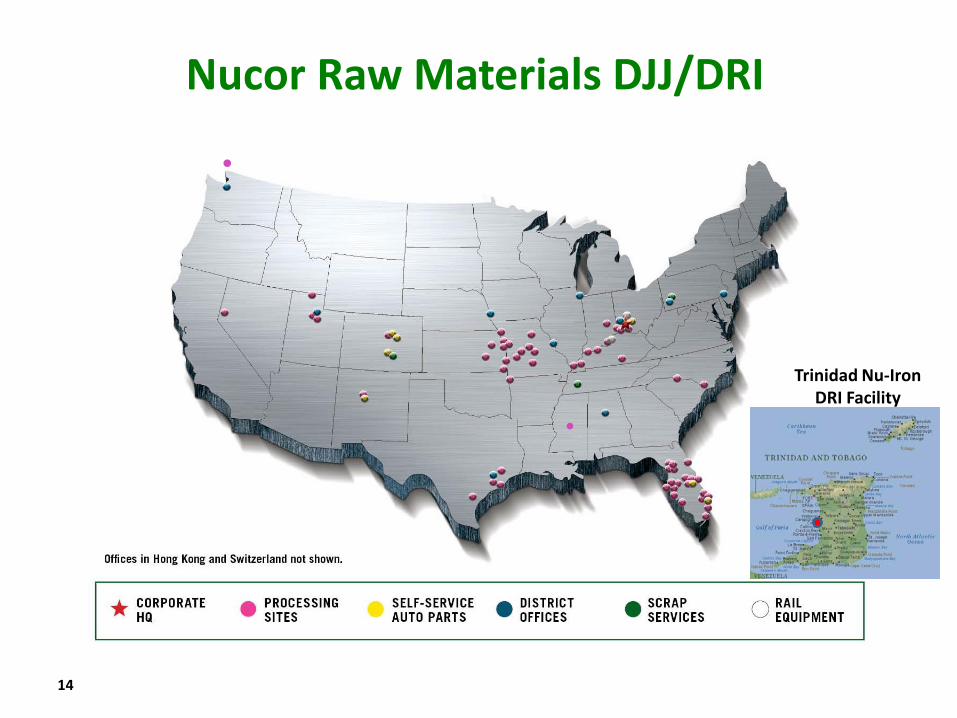

Nucor Raw Materials DJJ/DRI

14

Trinidad Nu-Iron DRI Facility

Nucor Steel Louisiana • Selected St. James Parrish, Louisiana for construction of $750 million iron making

facility. 2.5 million tons annual capacity of direct reduced iron (DRI). First phase of a multi-phase plan that may include an additional DRI facility, coke plant, blast furnace, & steel mill.

• Next step implementing Nucor’s raw materials strategy’s goal of controlling 6 to 7 million tons-per-year supply of high quality scrap substitutes (builds on 2.0 million tons at Trinidad DRI plant, Nu-Iron).

• Leverages strong skill set established by our Nu-Iron Team in applying direct reduction technology – achieved world class DRI quality levels in metallization rates, iron content, and productivity.

• Consistent with Nu-Iron’s highly successful business model, Nucor has secured for the Louisiana DRI facility a long-term supply of natural gas at an attractive cost by means of E&P drilling (on-shore) partnership with one of North America’s largest natural gas producers.

16

Nucor’s Market Leadership in North America

Structural Steel

Bar Steel

Rebar Steel

Cold Finished Bar Steel

Steel Joist

Steel Deck

Rebar Fabrication, Distribution, & Placement Company

Sheet SteelPlate Steel

Metal Buildings

#1North AmericanMarket Leader

#2North American Market Leader

#3North American Market Leader

Growth Platform – International Duferdofin-Nucor beams & long products joint venture

San Giovanni

San Zeno

Pallanzeno

Italy

SicilyGiammoro

International Sales Offices

NUCOR TRADINGNUCOR INTERNATIONAL SALES

USA’s biggest economic problem today that is NOT being dealt with:

JOB CREATION

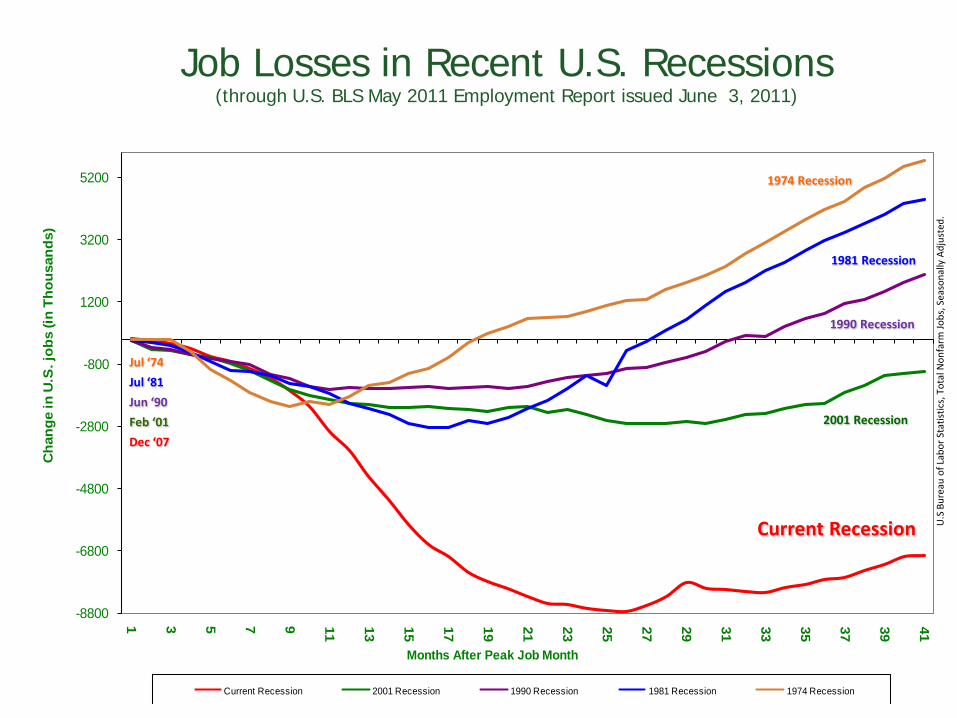

Job Losses in Recent U.S. Recessions(through U.S. BLS May 2011 Employment Report issued June 3, 2011)

-8800

-6800

-4800

-2800

-800

1200

3200

5200

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41C

hang

e in

U.S

. job

s (in

Tho

usan

ds)

Months After Peak Job Month

Current Recession 2001 Recession 1990 Recession 1981 Recession 1974 Recession

2001 Recession

Current Recession

1990 Recession

1981 Recession

1974 Recession

Jul ‘74

Jul ‘81

Jun ‘90

Feb ‘01

Dec ‘07

U.S

Bur

eau

of L

abor

Sta

tistic

s, T

otal

Non

farm

Jobs

, Sea

sona

lly A

djus

ted.

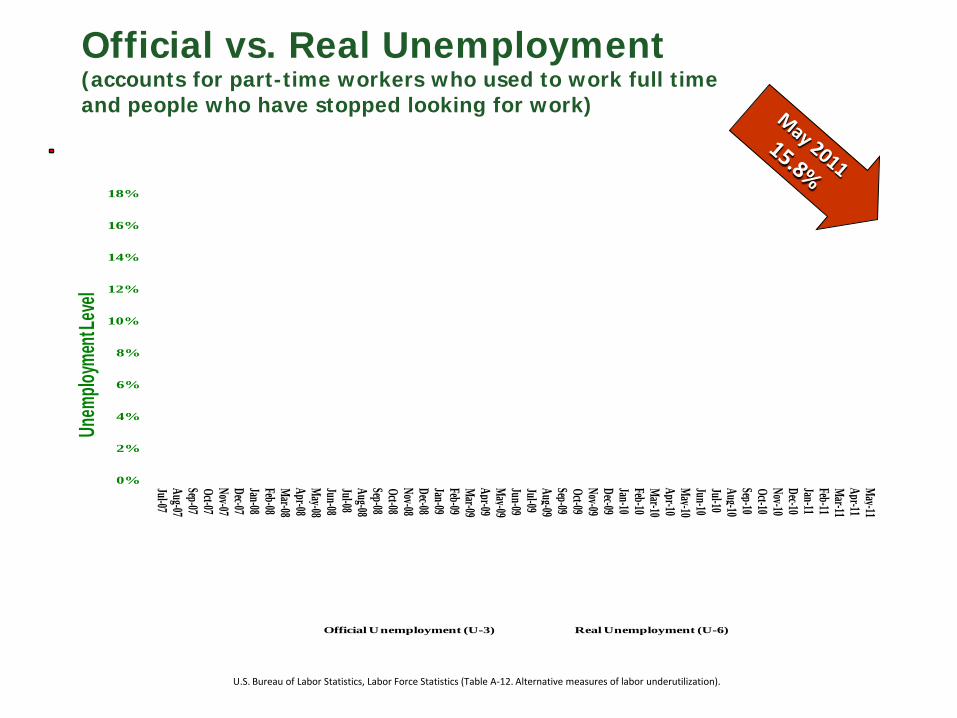

Official vs. Real Unemployment(accounts for part-time workers who used to work full timeand people who have stopped looking for work)

U.S. Bureau of Labor Statistics, Labor Force Statistics (Table A-12. Alternative measures of labor underutilization).

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Jul-07Aug-07Sep-07Oct-07Nov-07Dec-07Jan-08Feb-08Mar-08Apr -08May-08Jun-08Jul-08Aug-08Sep-08Oct- 08Nov-08Dec-08Jan-09Feb-09Mar-09Apr-09May-09Jun-09Jul-09Aug-09Sep-09Oct-09Nov-09Dec-09Jan-10Feb-10Mar-10Apr-10May-10Jun-10Jul-10Aug-10Sep-10Oct-10Nov-10Dec-10Jan-11Feb-11Mar-11Apr-11May-11

Unem

ploym

entL

evel

Official Unemployment (U-3) Real Unemployment (U-6)

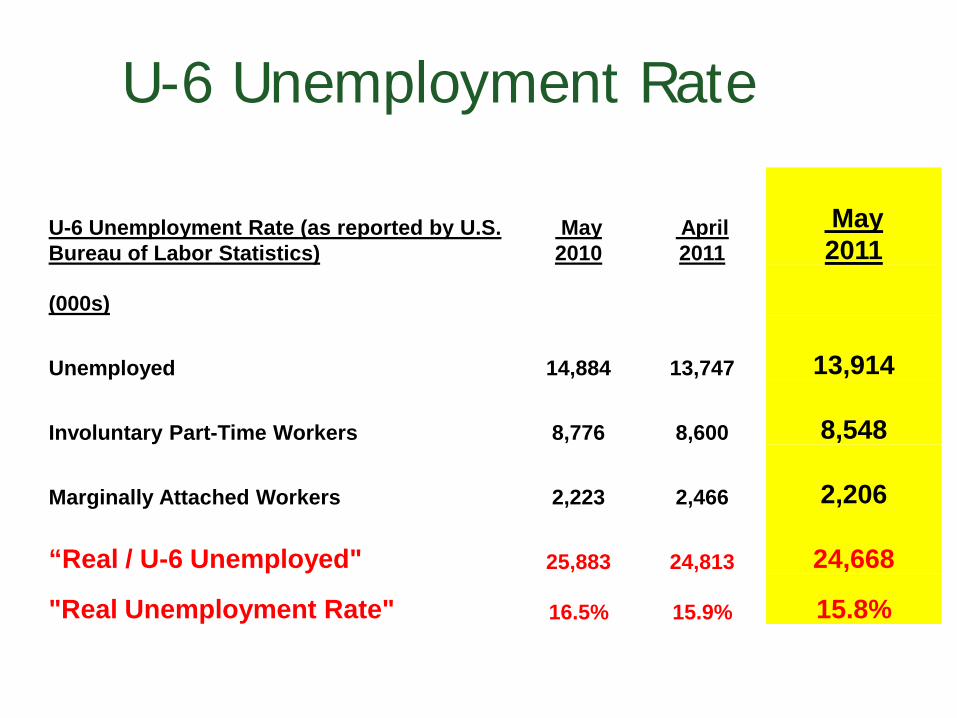

U-6 Unemployment Rate

U-6 Unemployment Rate (as reported by U.S. Bureau of Labor Statistics)

May 2010

April2011

May 2011

(000s)

Unemployed 14,884 13,747 13,914

Involuntary Part-Time Workers 8,776 8,600 8,548

Marginally Attached Workers 2,223 2,466 2,206

“Real / U-6 Unemployed" 25,883 24,813 24,668

"Real Unemployment Rate" 16.5% 15.9% 15.8%

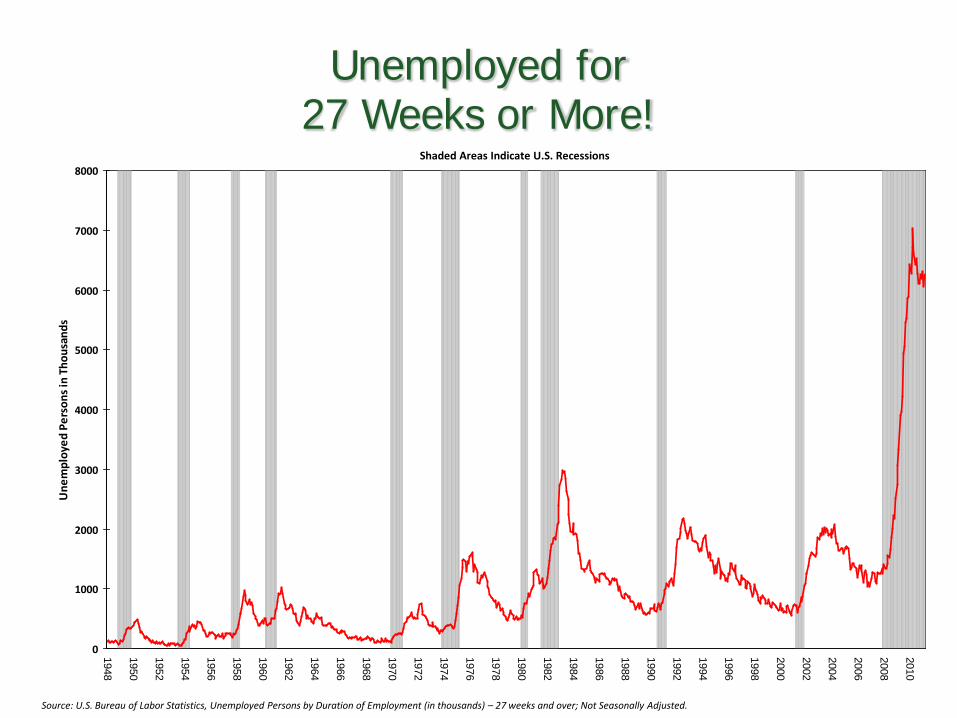

Unemployed for 27 Weeks or More!

0

1000

2000

3000

4000

5000

6000

7000

8000

1948

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010U

nem

ploy

ed P

erso

ns in

Tho

usan

ds

Source: U.S. Bureau of Labor Statistics, Unemployed Persons by Duration of Employment (in thousands) – 27 weeks and over; Not Seasonally Adjusted.

Shaded Areas Indicate U.S. Recessions

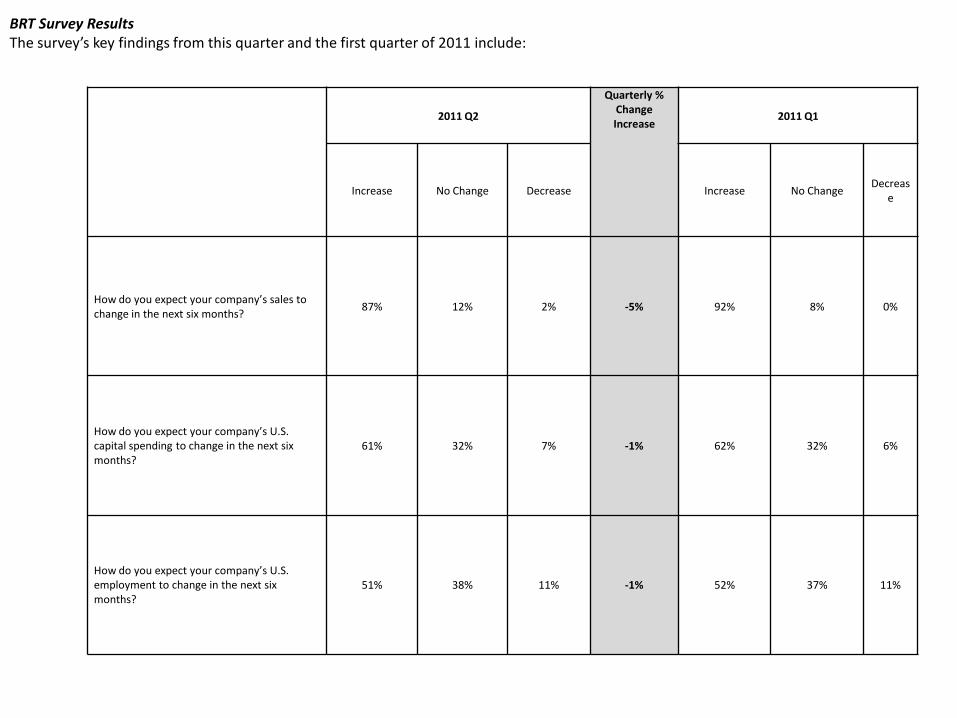

2011 Q2

Quarterly % Change Increase

2011 Q1

Increase No Change Decrease Increase No ChangeDecreas

e

How do you expect your company’s sales to change in the next six months?

87% 12% 2% -5% 92% 8% 0%

How do you expect your company’s U.S. capital spending to change in the next six months?

61% 32% 7% -1% 62% 32% 6%

How do you expect your company’s U.S. employment to change in the next six months?

51% 38% 11% -1% 52% 37% 11%

BRT Survey ResultsThe survey’s key findings from this quarter and the first quarter of 2011 include:

SOLUTIONS

MAKES

BUILDSSERVICES

INNOVATESREAL

WEALTH CREATION

CYCLE

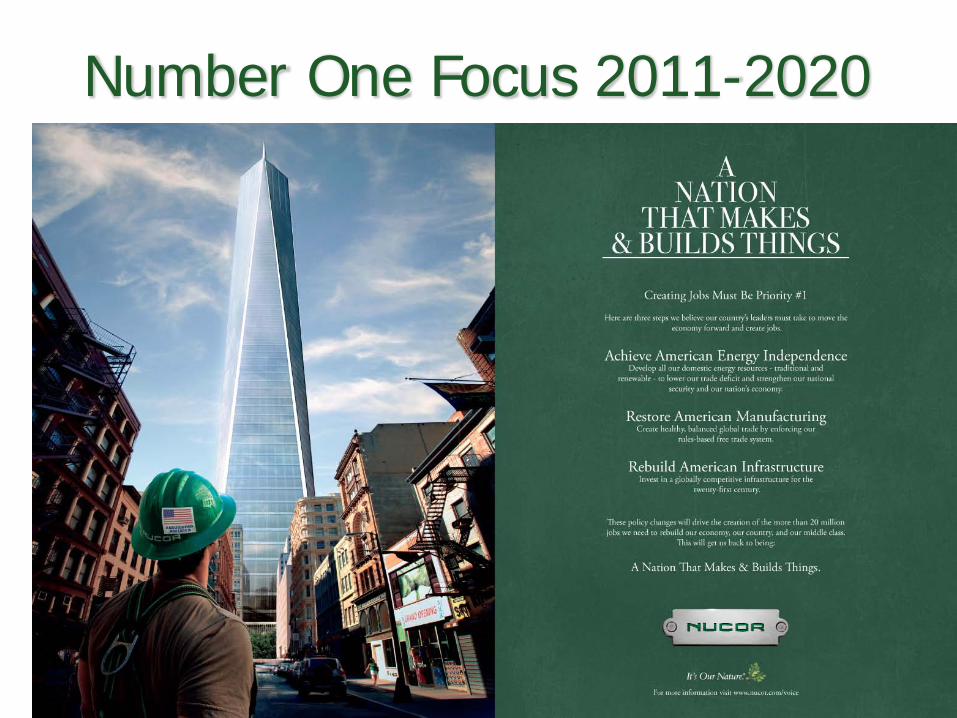

Number One Focus 2011-2020

Rules Based/Enforced Free Trade

• Free and open markets where governments enforce the rules of trade

• Healthy exchange of imports and exports among nations

• Joint ventures among companies from a multitude of countries

• Innovation and exchange of ideas

• Balanced trade volumes and economic growth

• Increasing global employment with rising standards of living

BARRIERS TO SOLUTIONS

• INTERNAL—MULTIPLE, SELF-INFLICTED

• EXTERNAL—TRADE MERCANTILISM, SOE’s

WORLD STEEL ASSOCIATION ANNUAL MEETING-PANELTHE 3 GREATEST CHALLENGES FACING THE GLOBAL

STEEL INDUSTRY OVER THE NEXT 10 YEARS

• SOE’s

• RAW MATERIAL/COMMODITY PRICES

• ENVIRONMENTAL ISSUES---CARBON, etc.

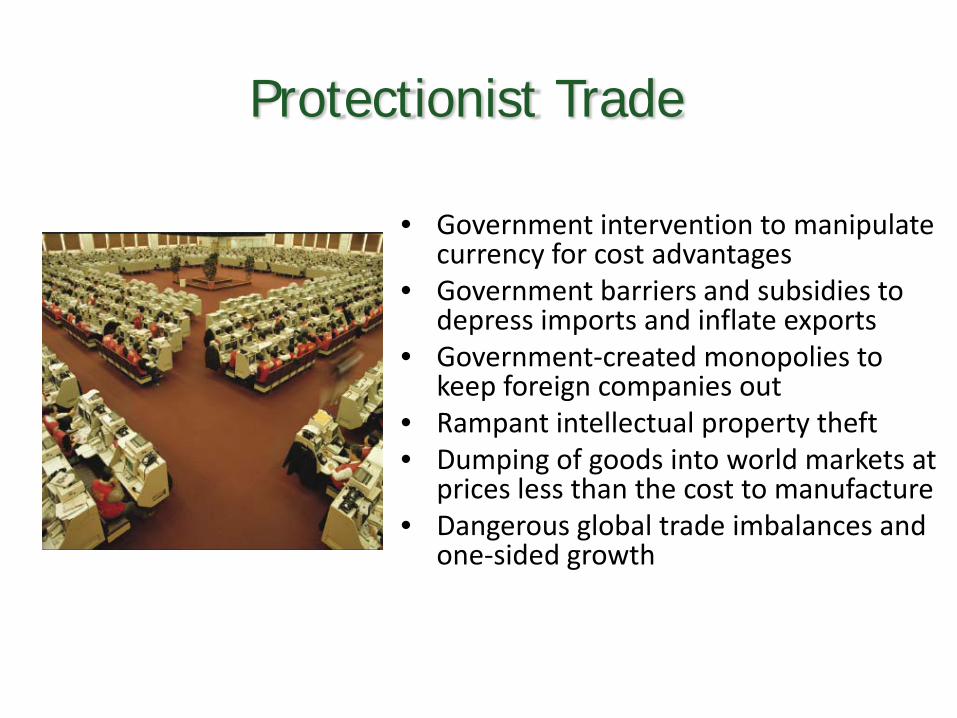

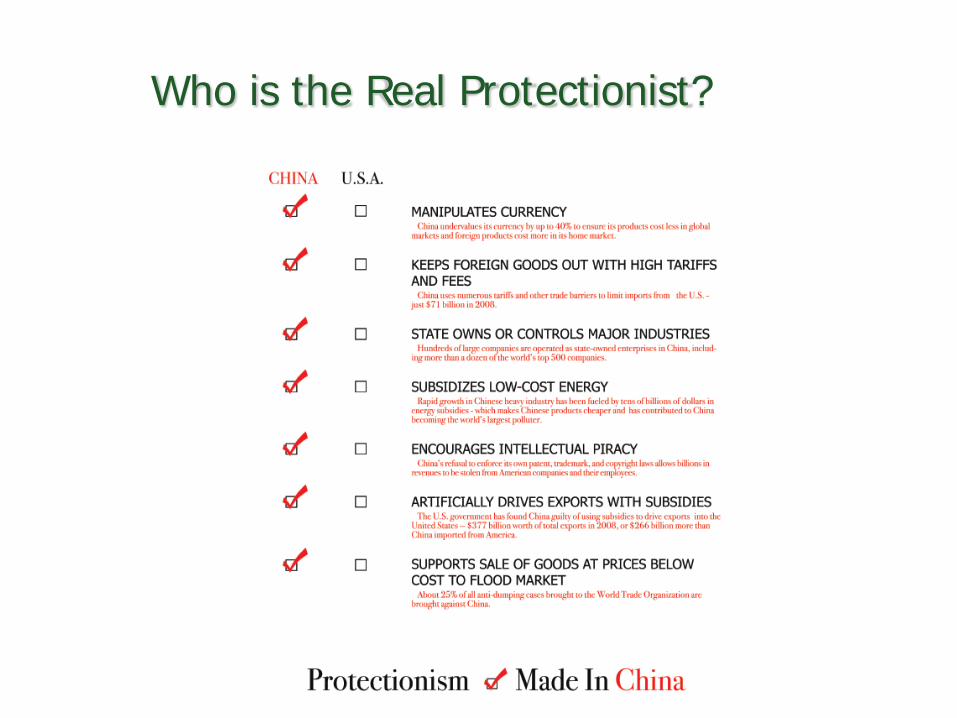

Protectionist Trade

• Government intervention to manipulate currency for cost advantages

• Government barriers and subsidies to depress imports and inflate exports

• Government-created monopolies to keep foreign companies out

• Rampant intellectual property theft• Dumping of goods into world markets at

prices less than the cost to manufacture• Dangerous global trade imbalances and

one-sided growth

Who is the Real Protectionist?

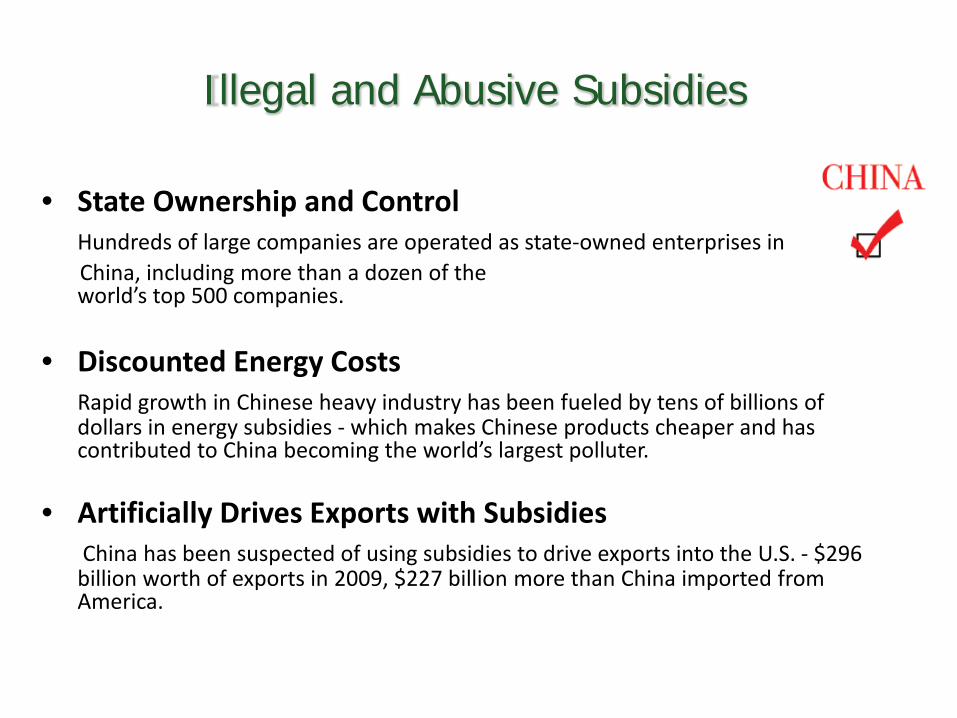

Illegal and Abusive Subsidies

• State Ownership and ControlHundreds of large companies are operated as state-owned enterprises in China, including more than a dozen of the world’s top 500 companies.

• Discounted Energy CostsRapid growth in Chinese heavy industry has been fueled by tens of billions of dollars in energy subsidies - which makes Chinese products cheaper and has contributed to China becoming the world’s largest polluter.

• Artificially Drives Exports with SubsidiesChina has been suspected of using subsidies to drive exports into the U.S. - $296 billion worth of exports in 2009, $227 billion more than China imported from America.

• SOE’s—State Owned Enterprises

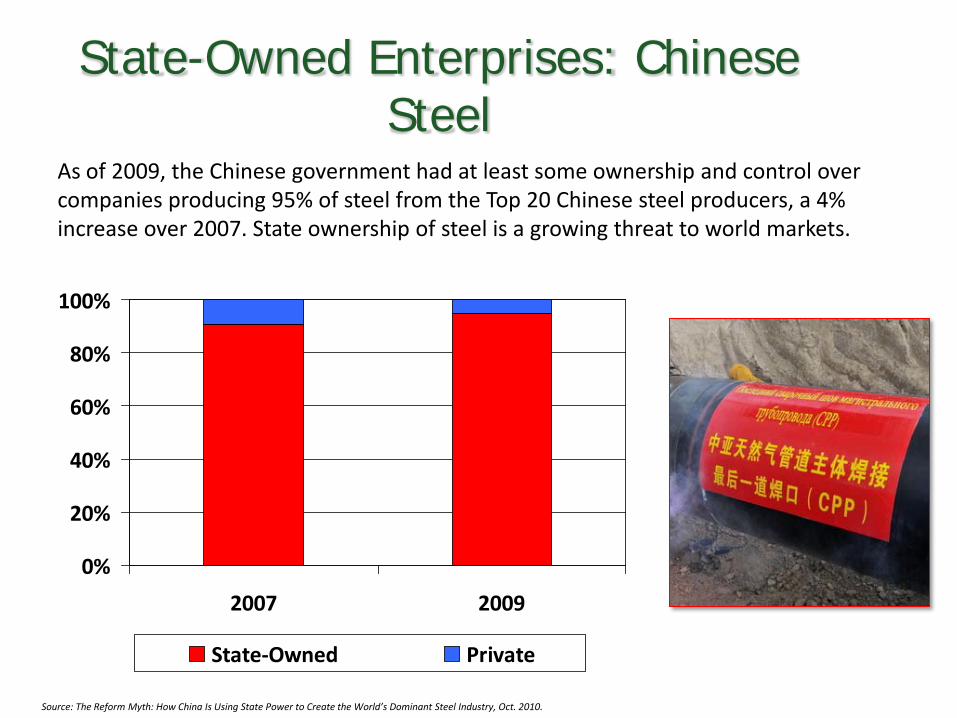

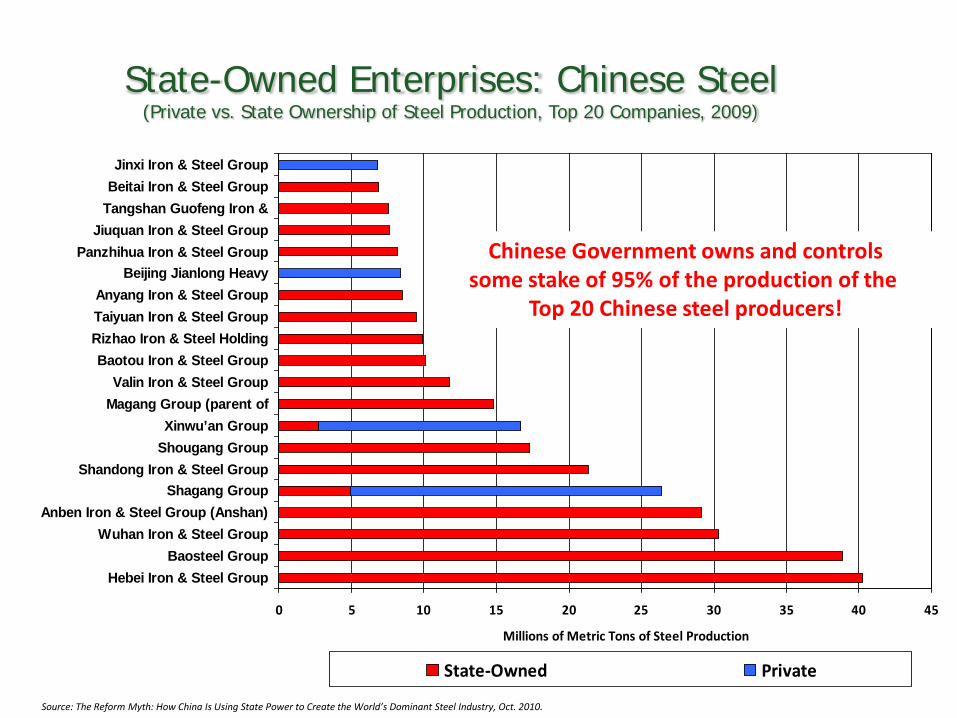

State-Owned Enterprises: Chinese Steel

As of 2009, the Chinese government had at least some ownership and control over companies producing 95% of steel from the Top 20 Chinese steel producers, a 4% increase over 2007. State ownership of steel is a growing threat to world markets.

Source: The Reform Myth: How China Is Using State Power to Create the World’s Dominant Steel Industry, Oct. 2010.

0%

20%

40%

60%

80%

100%

2007 2009

State-Owned Private

The Chinese government largely controls steel companies in which it only has partial ownership.• Private owners are often minority shareholders of non-tradable shares,

while the government is generally a majority shareholder.

• The Chinese government heavily regulates foreign investment in the steel industry.

– Foreign investors may not own a controlling interest in Chinese steel producers

– Reduced benefits for foreign investors

– Foreign investors must possess proprietary technology and/or intellectual property (technology transfer)

• The Chinese government controls raw materials for the steel industry.

• State-owned enterprises are now investing in the U.S. and other countries – not always with the intention of making money.

State-Owned Enterprise: Chinese Steel

Source: The Reform Myth: How China Is Using State Power to Create the World’s Dominant Steel Industry, Oct. 2010.

State-Owned Enterprises: Chinese Steel(Private vs. State Ownership of Steel Production, Top 20 Companies, 2009)

0 5 10 15 20 25 30 35 40 45

Hebei Iron & Steel GroupBaosteel Group

Wuhan Iron & Steel GroupAnben Iron & Steel Group (Anshan)

Shagang GroupShandong Iron & Steel Group

Shougang GroupXinwu’an Group

Magang Group (parent ofValin Iron & Steel Group

Baotou Iron & Steel GroupRizhao Iron & Steel HoldingTaiyuan Iron & Steel GroupAnyang Iron & Steel Group

Beijing Jianlong HeavyPanzhihua Iron & Steel Group

Jiuquan Iron & Steel GroupTangshan Guofeng Iron &Beitai Iron & Steel GroupJinxi Iron & Steel Group

Millions of Metric Tons of Steel Production

State-Owned Private

Chinese Government owns and controlssome stake of 95% of the production of the

Top 20 Chinese steel producers!

Source: The Reform Myth: How China Is Using State Power to Create the World’s Dominant Steel Industry, Oct. 2010.

Illegal and Abusive Subsidies

• State Ownership and ControlHundreds of large companies are operated as state-owned enterprises in China, including more than a dozen of the world’s top 500 companies.

• Discounted Energy CostsRapid growth in Chinese heavy industry has been fueled by tens of billions of dollars in energy subsidies - which makes Chinese products cheaper and has contributed to China becoming the world’s largest polluter.

• Artificially Drives Exports with SubsidiesChina has been suspected of using subsidies to drive exports into the U.S. - $296 billion worth of exports in 2009, $227 billion more than China imported from America.

• Foreign government subsidies are a major cause of overcapacity in the global steel

industry and steel-related industries

• Subsidies to steel and steel-related industries that 1) support inefficient and excess

capacity and/or 2) distort trade; are continuing, and remain a strong concern

• Examples include:

– Fundamental currency misalignment/undervalued currencies

– Preferential financing to add new capacity

– Loan forgiveness/equity infusions to prop up obsolete capacity

Steel

40

RAW MATERIALS

BARRIERS TO OPEN MARKETS

• Governments, including China, Russia, the Ukraine and

India, have become increasingly involved in the race for raw

materials.

•These governments provide subsidized government

investment, and control the movement of raw materials

through trade barriers, most of which directly violate WTO

agreements.

NUCOR

Raw Materials

Rules Associated with Raw Material Cost and Availability is a top Issue for U.S. Steel Producers

• Many countries continue to impose a variety of restrictions on exports of vital raw materials

– Export prohibitions

– Export duties

– Export quotas

– Other measures

• Trade-distorting restrictions on exports of raw materials

– Give domestic producers in the exporting country an unfair advantage

– Increase worldwide costs of production

– Place a heavy burden on steel industries in developing countries that do not have substantial iron ore reserves or steel scrap supplies

Raw Materials

43