nstar electric company and western massachusetts … commonwealth of massachusetts office of the...

TRANSCRIPT

THE COMMONWEALTH OF MASSACHUSETTS

OFFICE OF THE ATTORNEY GENERAL

ONE ASHBURTON PLACE

BOSTON, MASSACHUSETTS 02108

(617) 727-2200

(617) 727-4765 TTY

www.mass.gov/ago

July 21, 2017

Mark D. Marini, Secretary

Department of Public Utilities

One South Station, 2nd Floor

Boston, Massachusetts 02110

Re: NSTAR Electric Company and Western Massachusetts Electric

Company d/b/a Eversource Energy, D.P.U. 17-05

Dear Secretary Marini:

Enclosed please find the Office of the Attorney General’s Initial Brief.

Thank you for your attention to this matter. Please do not hesitate to contact me if you have any

questions about this filing.

Sincerely,

Joseph W. Rogers

Assistant Attorney General

Enclosure

cc: Mark Tassone, Hearing Officer

Cheryl Kimball, Esq.

Service List

COMMONWEALTH OF MASSACHUSETTS

DEPARTMENT OF PUBLIC UTILITIES

__________________________________________

)

NSTAR ELECTRIC COMPANY AND )

WESTERN MASSACHUSETTS ELECTRIC ) D.P.U. 17-05

COMPANY d/b/a EVERSOURCE ENERGY )

__________________________________________)

CERTIFICATE OF SERVICE

I certify that I have this day served the foregoing documents upon each person designated

on the official service list compiled by the Secretary in this proceeding. Dated at Boston this

21st day of July, 2017.

Joseph W. Rogers

Assistant Attorney General

Massachusetts Attorney General

Office of Ratepayer Advocacy

One Ashburton Place

Boston, Massachusetts 02108

(617) 727-2200

cc: Service List

COMMONWEALTH OF MASSACHUSETTS

DEPARTMENT OF PUBLIC UTILITIES

_________________________________________

)

NSTAR ELECTRIC COMPANY AND )

WESTERN MASSACHUSETTS ELECTRIC ) D.P.U. 17-05

COMPANY d/b/a EVERSOURCE ENERGY )

_________________________________________)

INITIAL BRIEF OF THE OFFICE OF THE

ATTORNEY GENERAL

Respectfully submitted,

MAURA HEALEY

ATTORNEY GENERAL

By: Joseph W. Rogers

Assistant Attorneys General

Office for Ratepayer Advocacy

One Ashburton Place

Boston, MA 02108

(617) 727-2200

July 21, 2017

TABLE OF CONTENTS

Page

I. INTRODUCTION .................................................................................................................. 1

II. OVERVIEW ........................................................................................................................... 3

III. DESCRIPTION OF THE COMPANY ............................................................................... 6

IV. STANDARD OF REVIEW ................................................................................................ 7

V. ARGUMENT .......................................................................................................................... 9

A. ALTERNATE REGULATORY MECHANISMS ............................................................. 9

1. The Department Should Reject The Company’s Proposed Performance-Based

Ratemaking Mechanism Because It Will Not Produce Just and Reasonable Rates ............... 9

a) Introduction ............................................................................................................... 9

b) The Company’s Proposal Is Inconsistent with Established Department Policy ..... 11

c) The Company’s Proposal Will Allow Near-Guaranteed Rate Increases at

Abnormally High Rates .................................................................................................... 20

d) The Company’s Proposal to Have a Separate Adjustment for Capital Investments

Undermines the Purpose of A PBRM Formula and Allows Dollar-For-Dollar Recovery

Without a Prudence Review.............................................................................................. 22

e) The Company Has Not Provided Any Evidence That The PBRM Is Necessary to

Fund Grid Modernization Investments ............................................................................. 23

f) The Company’s Proposed PBRM Includes a Negative X Factor Far Lower Than

That Approved for Any North American Energy Utility .................................................. 24

g) The Company’s Total Factor Productivity (“TFP”) Study Is Flawed and Provides

an Inadequate Analysis of the Company’s Costs .............................................................. 28

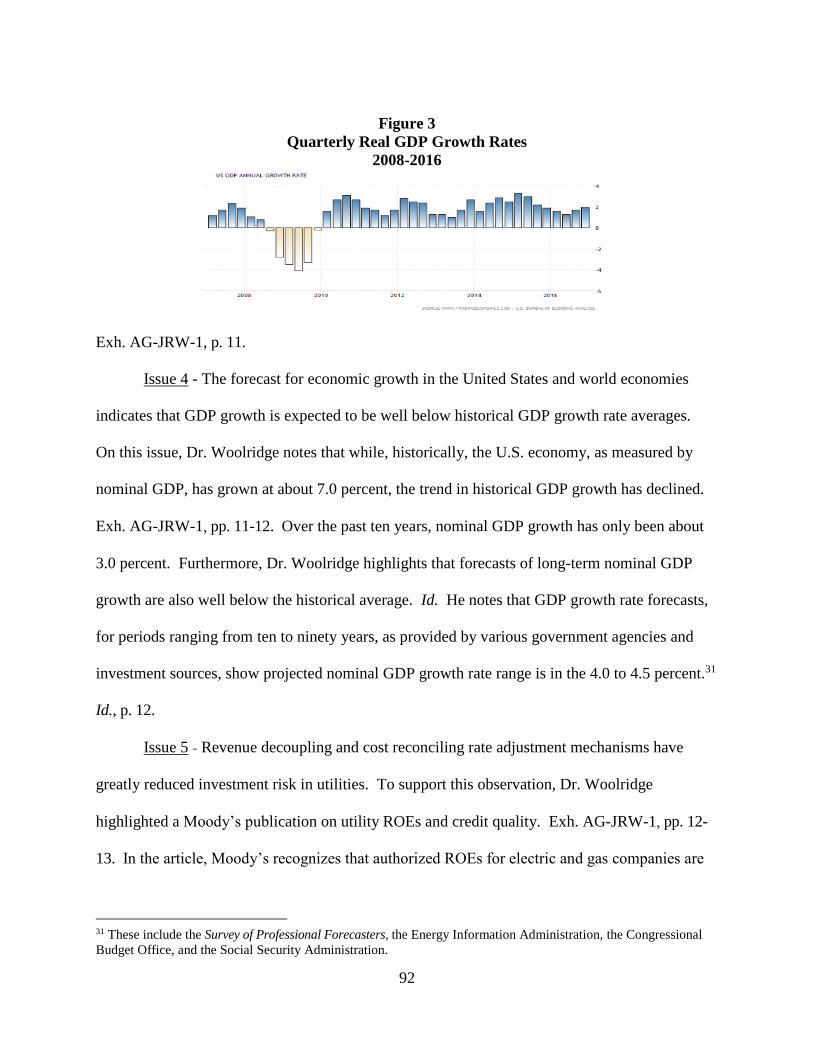

h) The Company’s Proposed Earnings Sharing Mechanism (“ESM”) Has A Number

of Deficiencies .................................................................................................................. 32

i) The PBRM Stay-Out Provision .................................................................................. 33

2. Grid Modernization Base Commitment ........................................................................ 34

a) Proposed Grid Modernization Investments ............................................................ 35

(1) Introduction and Background .............................................................................. 35

(2) The Company’s Proposed Grid Modernization Investments Do Not Qualify for

Exceptional, Targeted Cost Recovery Mechanisms ..................................................... 38

(3) The Department Need Not Approve the PBRM nor the GMBC to Move Forward

with Grid Modernization............................................................................................... 38

(4) Many of the Proposed Investments Are Not “Grid Modernization” Investments

39

1

b) Energy Storage ........................................................................................................ 40

c) EV Charging Infrastructure..................................................................................... 43

(1) The Department Should Consider the Company’s Make-Ready Electric Vehicle

Infrastructure Program in a Separate Proceeding Outside of this Rate Case ................ 43

(2) The Department Should Establish Statewide Goals and Standards Before

Approving Any EV Charging Proposal ........................................................................ 46

(3) If the Department Decides to Review Eversource’s EV Proposal in this

Proceeding, it Should Adopt Several Modifications..................................................... 48

(a) The Company Should Not Be Permitted to Own Infrastructure Behind the Meter ... 48

(b) Recovery of Make-Ready Infrastructure Should Occur in the Normal Course of

Ratemaking ............................................................................................................................. 50

(c) Electrification of the Company’s Own Fleet Should Not Be Included as Part of the

Make Ready Program .............................................................................................................. 51

(d) The Department Should Put Other Mechanisms in Place to Ensure Greater

Accountability and Program Coordination ............................................................................. 53

d) The Department Should Reject the GMBC Performance Metrics as Proposed

Because They Do Not Meaningfully Assess Company Performance or Mandate Good

Performance ...................................................................................................................... 54

(1) The Department Should Include Performance Penalties and/or Incentives. ....... 55

(2) The Company’s Proposed Performance Metrics Are Deficient. ......................... 56

(3) The Company Should Add to Its Performance Metrics. ..................................... 58

e) The Company’s Annual Stakeholder Process Will Not Provide an Opportunity for

Meaningful Stakeholder Participation or Comment ......................................................... 59

B. CAPITAL STRUCTURE AND COST OF CAPITAL .................................................... 62

1. Introduction ................................................................................................................... 62

2. Capital Structure ........................................................................................................... 64

a) The Company Failed to Include NSTAR’s Most Recent Long-Term Debt Issuance

in Its Capital Structure ...................................................................................................... 65

b) The Company’s Embedded Cost Rate of Long-Term Debt Is Miscalculated ........ 66

3. Return on Common Equity ........................................................................................... 67

a) Proxy Groups .......................................................................................................... 67

b) Discounted Cash Flow Analysis Results ................................................................ 70

c) Capital Asset Pricing Model Analysis Results ....................................................... 76

(1) Mr. Hevert’s CAPM Analysis Is Fatally Flawed ................................................ 79

(2) Mr. Hevert’s Market Risk Premium Is Grossly Over-Inflated............................ 79

d) The Department Should Reject Mr. Hevert’s Bond Yield Risk Premium Approach

82

2

4. Other Cost Of Equity Issues ......................................................................................... 84

a) Capital Market Conditions ...................................................................................... 84

b) Rate Making Mechanisms....................................................................................... 86

5. The Attorney General’s Position on Massachusetts ROEs ........................................... 88

6. The Attorney General’s Recommendation. .................................................................. 98

C. RATE BASE ................................................................................................................... 101

1. The Company Over-Inflates Its Cost of Service ......................................................... 101

2. The Company’s Proposal to Adjust its Rate Base for Post-Test Year Plant Additions

Should Be Rejected ............................................................................................................. 104

D. OPERATIONS AND MAINTENANCE EXPENSES ................................................... 109

1. The Pro Forma Test Year WMECo Payroll Expense Should Not Be Annualized to

Reflect the Employee Complement as of the End of the Test Year ................................... 109

2. Test Year Insurance Policy Surplus Payments Are Recurring and Should Not be

Removed from the Test Year .............................................................................................. 109

3. Overhead Costs Charged by ESC During the Test Year Should be Reduced to Reflect

the Return on Equity Approved by the Department in This Proceeding ............................ 111

4. The Test Year Charges from Eversource Service Company Should Be Reduced for the

Impacts of the Acquisition of the Aquarion Water Companies .......................................... 112

5. Pursuant to Department Precedent, the Department Should Disallow the Company’s

Incentive Compensation Based on Financial Goals............................................................ 118

6. The Company’s Inflated Medical Expense Projection Result in the Company Over-

Stating Its Future Employee Medical Costs........................................................................ 122

7. The Department Should Reject the Company’s Proposal to Increase Information

System Expense Charged from Eversource Service Company for a Post-Test Year

Information System Plant Addition .................................................................................... 125

a) The Supply Chain Project Is a Post-Test Year Plant Addition at the Service

Company Level That Was Not Placed into Service Prior to the End of Hearings in This

Case 127

b) The Amount of Costs Associated with the Supply Chain Project to Be Charged to

NSTAR and WMECo in the Rate Effective Period Are Not Known and Measurable ... 127

c) The Company’s Expected Cost Savings Associated with the Supply Chain Project

Implementation Exceed the Annual Revenue Requirements Associated with the ESC

Plant Addition ................................................................................................................. 129

d) The Company Has Failed to Consider the Impact That the Company’s Acquisition

of the Aquarion Water Companies Will Have on the Amounts to Be Charged to NSTAR

and to WMECo ............................................................................................................... 131

e) The Company Overstates the Expected Costs of the Supply Chain Project ......... 131

f) Summary and Recommendation ........................................................................... 133

3

8. Customers Should Not Have to Pay for Two Corporate Headquarters ...................... 133

a) The Hartford, Connecticut Headquarters is Unnecessary to Provide Electric

Distribution Service to Massachusetts Customers .......................................................... 134

b) The Connecticut Public Utility Regulatory Authority Has Disallowed Costs

Associated with the Unneeded Hartford Headquarters ................................................... 135

9. The Department Should Deny the Company’s Proposed 2018 Non-Union Payroll

Expense Adjustment ........................................................................................................... 136

10. “Fee Free” Credit/Debit Card Payment System ....................................................... 138

a) The Department Should Reject the Company’s Proposed “Fee Free” Credit/Debit

Card Payment System Because It Is Inconsistent with the Provision of Least-Cost

Service, creates a Cross-Subsidy, and Could Result in More Customers Paying High

Credit Card Interest Rates ............................................................................................... 138

b) The Proposed Pro Forma Adjustments for Fee Free Payment Processing Are

Speculative and Should Be Rejected .............................................................................. 141

11. The Department Should Reject the Company’s Proposal To Assign One Third Of

Regulatory Assessments To Basic Service Customers ....................................................... 142

12. The Proposed Pro Forma Adjustment for GIS Verification Costs is Speculative and

Should be Rejected ............................................................................................................. 146

13. Rate Case Expense .................................................................................................... 147

a) Ratepayers Should Not Pay for Rate Design Twice ............................................. 148

b) The Company’s Rate Case Expense for its PBRM and Allocated Cost of Service

Experts Is Excessive ....................................................................................................... 150

c) The Company Should Not Recover Rate Case Expense for Its Temporary

Employees ....................................................................................................................... 151

E. DEPRECIATION ........................................................................................................... 154

1. Eversource’s Percent Reserve Is Large and Growing ................................................. 154

2. The Company Proposes to Charge Ratepayers Almost Three Times the Net Salvage

Actually Incurred ................................................................................................................ 156

3. Mr. Spanos Inappropriately Charges Today’s Ratepayers for Future Inflation .......... 158

4. Ratepayers Will Be Harmed by the Company’s Proposal .......................................... 160

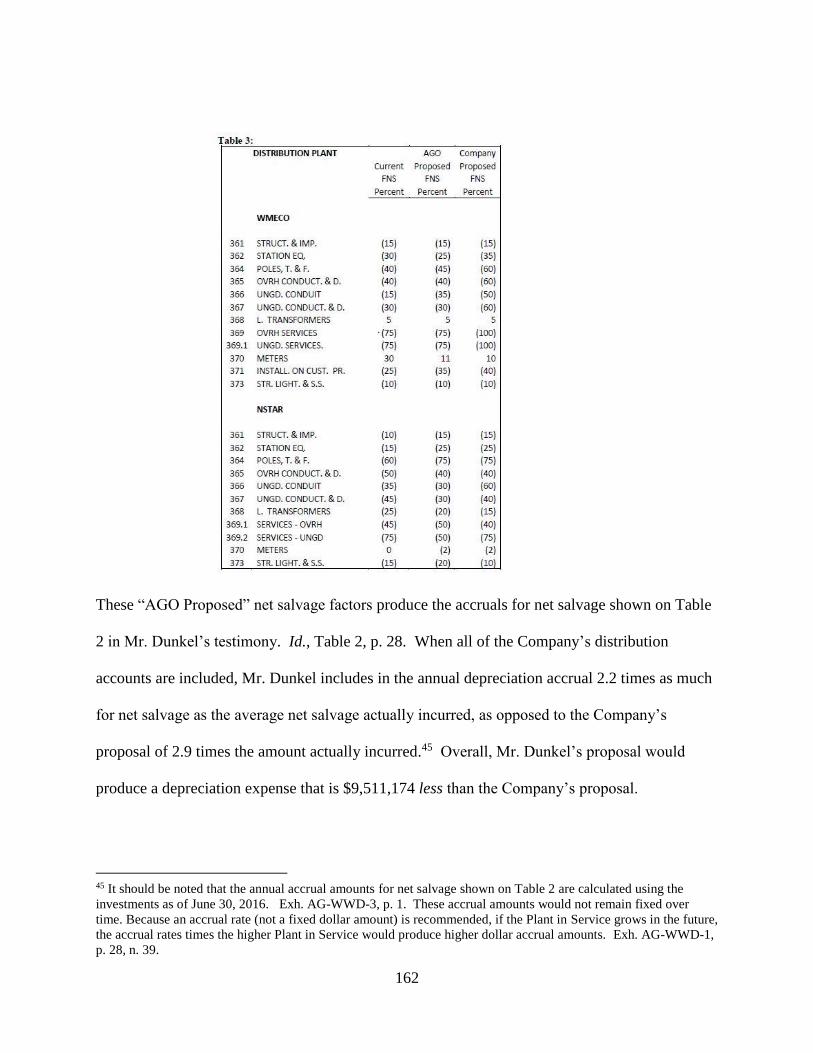

5. The Department Should Adopt Mr. Dunkel’s Recommendations .............................. 161

6. In the Alternative, the Department Should Employ Gradualism and Not Adopt All of

the Company’s Proposed Net Salvage Factors ................................................................... 163

F. VEGETATION MANAGEMENT ................................................................................. 164

1. Introduction ................................................................................................................. 164

a) Reliability Indices for Eversource ........................................................................ 165

b) Eversource Arborists ............................................................................................. 166

2. RTW Pilot Program .................................................................................................... 167

4

a) 2017 RTW Pilot Program ..................................................................................... 168

b) 2018 RTW Pilot Program ..................................................................................... 169

3. LiDAR......................................................................................................................... 171

4. Accounting for NSTAR’s First-Cycle Enhanced Vegetation Management Activities

173

a) Capitalization of ETT and ETR Costs .................................................................. 174

5. Maintenance of Overhead Lines and Devices ............................................................ 175

a) Account 593 – Maintenance of Overhead Lines ................................................... 175

b) Account 365 – Overhead Conductors and Devices .............................................. 177

G. STORM FUND PROPOSAL ......................................................................................... 178

1. The Department Should Not Allow the Company to Recover Deferred Costs Through

the Replenishment Factor ................................................................................................... 179

2. Carrying Charges for Deferred Amounts Not Eligible for Storm Fund Recovery Must

Not Be Collected in the Replenishment Factor ................................................................... 180

3. The Department Should Reject the Company’s Request to Recover Certain Lean-in

Costs Through Its Storm Fund ............................................................................................ 181

4. Recovery of Outstanding Storm Cost Balance ........................................................... 182

5. Billings to Verizon for Jointly Operated Poles ........................................................... 183

H. TAXES ............................................................................................................................ 186

1. Income Taxes .............................................................................................................. 186

a) There is No Evidentiary Support for WMECo’s Increase to Taxable Income for

“Property Tax Expense” ................................................................................................. 186

2. Property Taxes ............................................................................................................ 188

a) The Company’s Projected Property Tax Calculations Are Inconsistent with

Department Precedent ..................................................................................................... 188

b) The Department Should Ensure There Are Appropriate Property Tax Allocations to

Other Businesses ............................................................................................................. 190

c) WMECo’s Deferred Property Tax Claims ............................................................ 191

(1) WMECo’s Deferred Property Tax Claims for 2012-2015 Should Be Adjusted to

Net Out State and Federal Income Tax Benefits ........................................................ 191

(2) The Company Is Not Entitled to Deferral of WMECo ’S 2016 Property Taxes

192

(a) WMECo’s 2016 Distribution-Related Property Tax Increment Does Not Represent an

Extraordinary Expense .......................................................................................................... 193

(b) The Company Has Failed to Demonstrate That the Denial of the Request for Deferral

Would Significantly Harm the Overall Financial Condition of the Company ........................ 194

5

(c) WMECo’s 2016 Incremental Tax Obligation Was Not Likely to and Did Not Prompt

the Filing of a Rate Case ........................................................................................................ 195

I. OTHER REVENUES ..................................................................................................... 196

1. The Pro Forma Adjustment to Eliminate Belmont Wholesale Distribution Contract

Revenues from Test Year NSTAR Miscellaneous Revenues is Selective and Speculative 196

2. The Department Should Adjust the Company’s Pole Attachment Revenues to Reflect

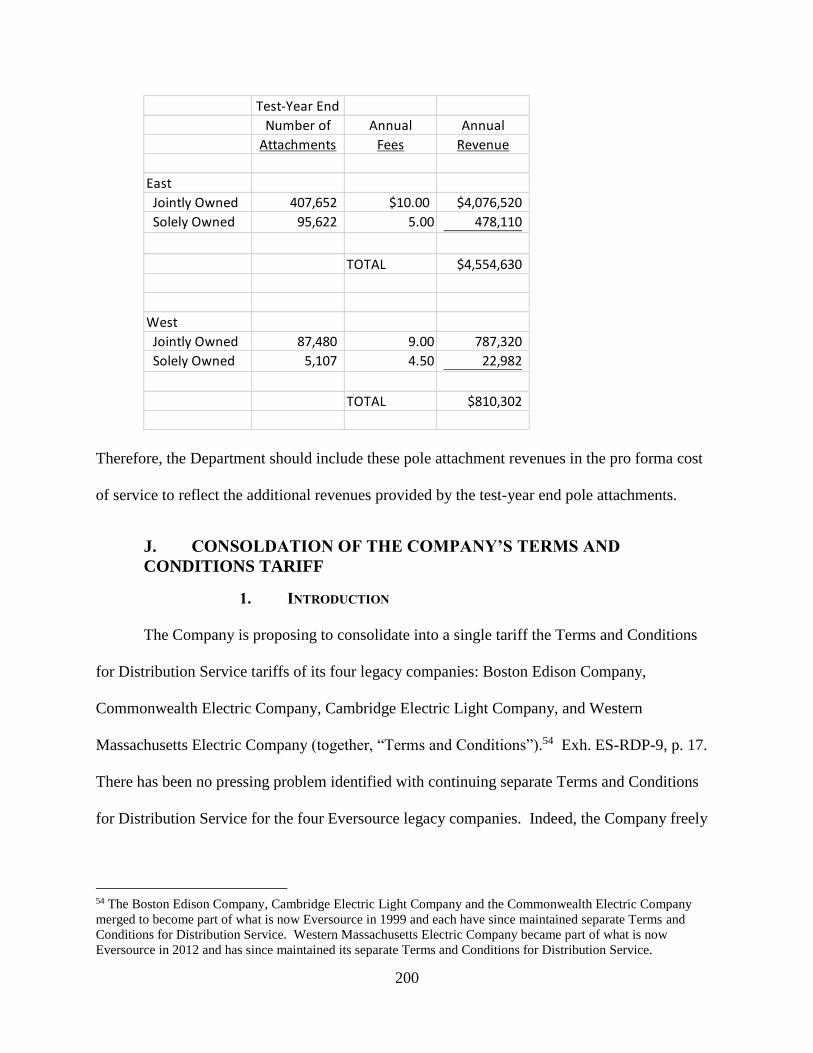

the Number of Pole Attachments at Test-Year End ............................................................ 199

J. CONSOLDATION OF THE COMPANY’S TERMS AND CONDITIONS TARIFF.. 200

1. Introduction ................................................................................................................. 200

2. Eliminate the Company’s Proposed Force Majeure Provision ................................... 202

3. Limit the Company Obligation for Meter and Communication Device Installation to 30

Days .................................................................................................................................... 204

4. Eliminate the Limitation of Liability Provision for Curtailment of Service ............... 204

5. Fee Increases ............................................................................................................... 206

6. The Department Should Require Additional Customer Education, Outreach, and

Company Ownership of Private Poles ................................................................................ 207

K. MERGER REVIEW - SECTION 96 .............................................................................. 210

1. Background ................................................................................................................. 210

2. The Department Should Consider Rate Impacts Before Approving the Company’s

Section 96 Petition .............................................................................................................. 211

VI. CONCLUSION ............................................................................................................... 213

6

COMMONWEALTH OF MASSACHUSETTS

DEPARTMENT OF PUBLIC UTILITIES

_________________________________________

)

NSTAR ELECTRIC COMPANY AND )

WESTERN MASSACHUSETTS ELECTRIC ) D.P.U. 17-05

COMPANY d/b/a EVERSOURCE ENERGY )

_________________________________________)

INITIAL BRIEF OF THE OFFICE OF THE

ATTORNEY GENERAL

I. INTRODUCTION

Pursuant to the briefing schedule established by the Department of Public Utilities

(“Department”) in this proceeding, the Office of the Attorney General (“AGO”) submits its

Initial Brief. On January 17, 2017, NSTAR Electric Company (“NSTAR”) and Western

Massachusetts Electric Company (“WMECo”) d/b/a Eversource Energy (together, “Eversource”

or the “Company”), pursuant to G.L. c. 164, § 94 (“Section 94”), filed two requests seeking

approval from the Department for a general increase in base rates. Specifically, Eversource

seeks an increase of $61.6 million for the three divisions of NSTAR and $35.8 million increase

for WMECo.1

In addition to the proposed rate increases, the Company seeks Department approval for

numerous significant changes in its electric distribution companies’ operations and finances.

First, the Company requests to implement revenue decoupling for NSTAR. See Rate Structures

1 These are the updated number provided in the Company’s May 25, 2017 Update to its revenue requirements. See

Exh. ES-DPH-2 (East) and (West) May 25, 2017 Update.

2

that will Promote Efficient Deployment of Demand Resources, D.P.U. 07-50-A (2008).2 Second,

the Company proposes an “Eversource Grid-Wise Performance Plan,” which includes a

performance-based ratemaking mechanism (“PBRM”) that would adjust rates annually in

accordance with a formula to be approved by the Department. Third, within the PBRM formula,

the Company proposes a Grid Modernization Base Commitment (“GMBC”) of $400 million in

incremental capital investment over the next five years. Fourth, the Company proposes to make

major changes in its existing rate designs to streamline and align rate classifications between

western and eastern Massachusetts.3 Fifth, the Company seeks to recover merger related costs.

The Company asserts that the annual pro forma amortization for merger-related costs to achieve

is $2,621,089 for NSTAR and $442,169 for WMECo over the next ten years. Sixth, the

Company proposes changes to its storm fund.

In addition to the rate increase requests under Section 94, the Company requests that the

Department review and approve the corporate consolidation of NSTAR and WMECo in this

proceeding pursuant to the Department’s authority under G.L. c. 164, § 96 (“Section 96”).

Thus, although the Company chose to package its requests in a single docket, the

Company has actually filed three cases with the Department: two Section 94 rate cases and one

Section 96 merger. In support of its three cases, the Company’s filing includes fourteen (14)

pieces of testimony by eighteen (18) witnesses.

2 WMECo implemented revenue decoupling in 2011, following the Department’s decision in Western

Massachusetts Electric Company, D.P.U. 10-70 (2011). 3 Specifically, the Company proposes a Transition Period over which it will eliminate the four legacy rates (Boston

Edison, Cambridge, Commonwealth and WMECo) and transition to one statewide rate for each of the proposed rate

classes. On June 9, 2017, the Department established a separate procedural schedule for rate design issues.

Interlocutory Order on Attorney General’s Motion to Protect Intervenors’ Due Process Rights, D.P.U. 17-05 (June

19, 2017).

3

II. OVERVIEW

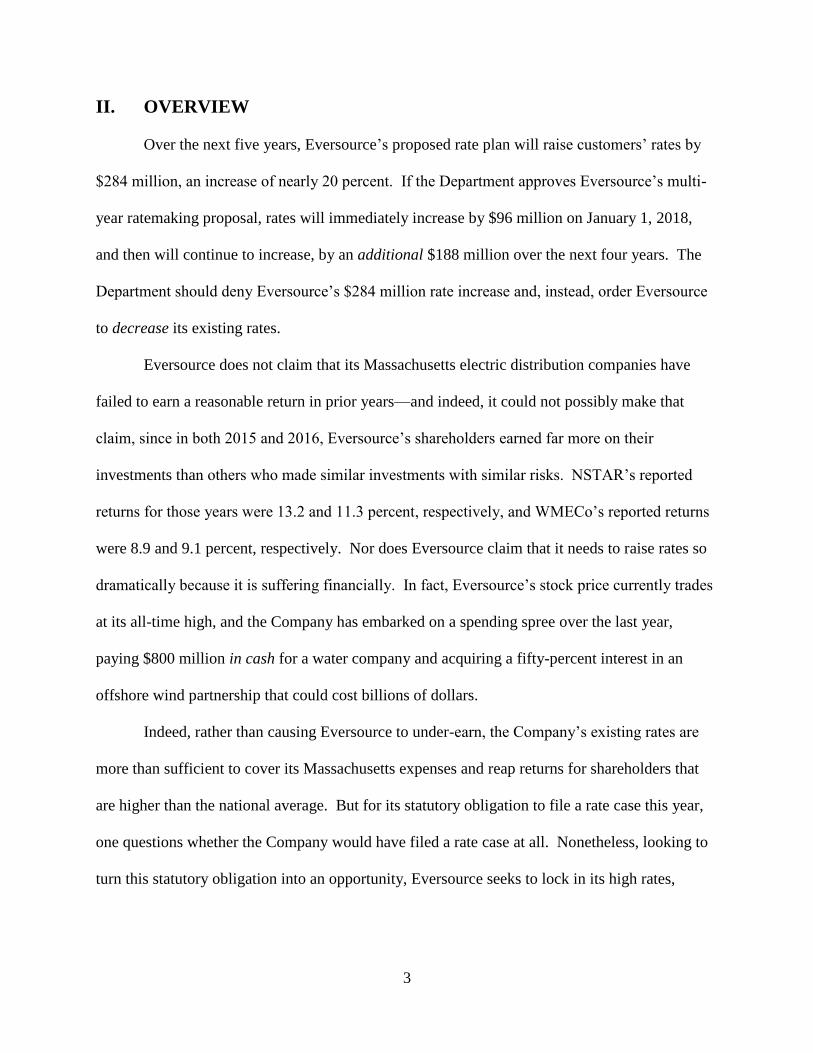

Over the next five years, Eversource’s proposed rate plan will raise customers’ rates by

$284 million, an increase of nearly 20 percent. If the Department approves Eversource’s multi-

year ratemaking proposal, rates will immediately increase by $96 million on January 1, 2018,

and then will continue to increase, by an additional $188 million over the next four years. The

Department should deny Eversource’s $284 million rate increase and, instead, order Eversource

to decrease its existing rates.

Eversource does not claim that its Massachusetts electric distribution companies have

failed to earn a reasonable return in prior years—and indeed, it could not possibly make that

claim, since in both 2015 and 2016, Eversource’s shareholders earned far more on their

investments than others who made similar investments with similar risks. NSTAR’s reported

returns for those years were 13.2 and 11.3 percent, respectively, and WMECo’s reported returns

were 8.9 and 9.1 percent, respectively. Nor does Eversource claim that it needs to raise rates so

dramatically because it is suffering financially. In fact, Eversource’s stock price currently trades

at its all-time high, and the Company has embarked on a spending spree over the last year,

paying $800 million in cash for a water company and acquiring a fifty-percent interest in an

offshore wind partnership that could cost billions of dollars.

Indeed, rather than causing Eversource to under-earn, the Company’s existing rates are

more than sufficient to cover its Massachusetts expenses and reap returns for shareholders that

are higher than the national average. But for its statutory obligation to file a rate case this year,

one questions whether the Company would have filed a rate case at all. Nonetheless, looking to

turn this statutory obligation into an opportunity, Eversource seeks to lock in its high rates,

4

further increase its revenue, and reduce its risk with automatic cost of living-plus yearly rate

increases.

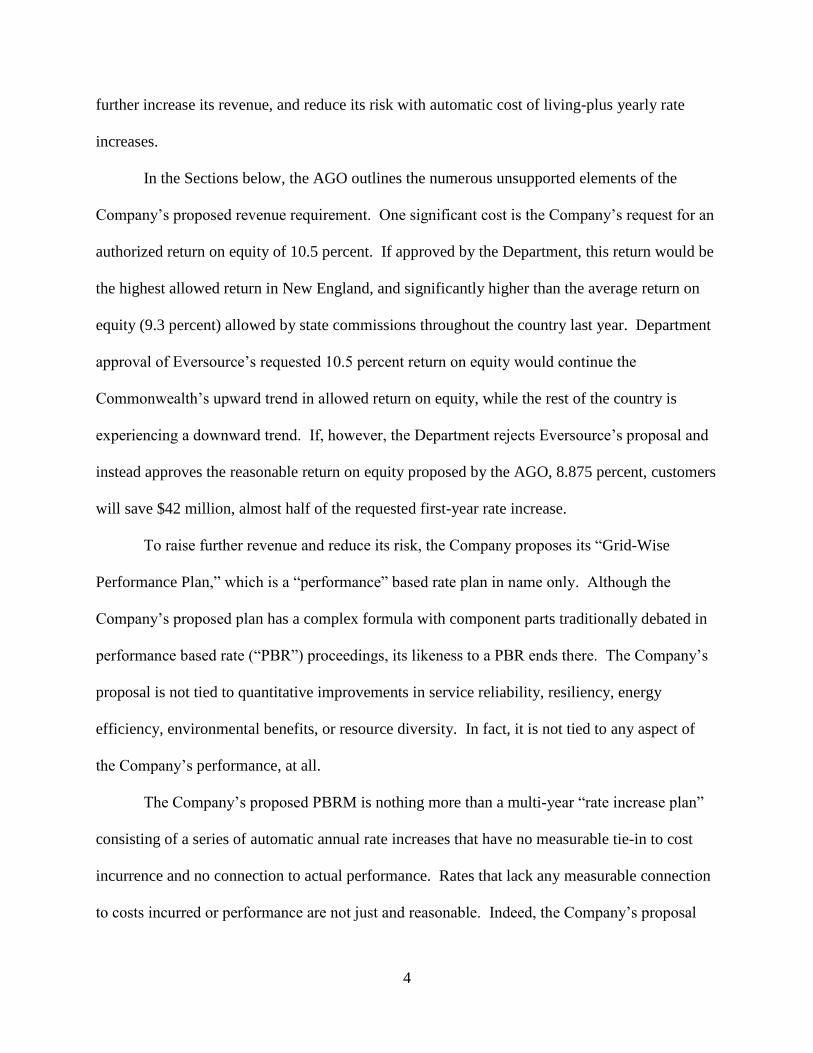

In the Sections below, the AGO outlines the numerous unsupported elements of the

Company’s proposed revenue requirement. One significant cost is the Company’s request for an

authorized return on equity of 10.5 percent. If approved by the Department, this return would be

the highest allowed return in New England, and significantly higher than the average return on

equity (9.3 percent) allowed by state commissions throughout the country last year. Department

approval of Eversource’s requested 10.5 percent return on equity would continue the

Commonwealth’s upward trend in allowed return on equity, while the rest of the country is

experiencing a downward trend. If, however, the Department rejects Eversource’s proposal and

instead approves the reasonable return on equity proposed by the AGO, 8.875 percent, customers

will save $42 million, almost half of the requested first-year rate increase.

To raise further revenue and reduce its risk, the Company proposes its “Grid-Wise

Performance Plan,” which is a “performance” based rate plan in name only. Although the

Company’s proposed plan has a complex formula with component parts traditionally debated in

performance based rate (“PBR”) proceedings, its likeness to a PBR ends there. The Company’s

proposal is not tied to quantitative improvements in service reliability, resiliency, energy

efficiency, environmental benefits, or resource diversity. In fact, it is not tied to any aspect of

the Company’s performance, at all.

The Company’s proposed PBRM is nothing more than a multi-year “rate increase plan”

consisting of a series of automatic annual rate increases that have no measurable tie-in to cost

incurrence and no connection to actual performance. Rates that lack any measurable connection

to costs incurred or performance are not just and reasonable. Indeed, the Company’s proposal

5

creates an up-front guessing game that creates substantial risks for ratepayers that Eversource’s

electric distribution companies will be over-compensated, with very little risk for Eversource that

it will suffer low returns. The Department should deny the Company’s request for a $96 million

rate increase and four yearly rate increases through the PBRM because it will result in unjust and

unreasonable rates.

The Company claims that its Grid-Wise Performance Plan will enable investment in grid

modernization, electric vehicles and storage, and help meet Massachusetts’ clean energy goals.

The AGO strongly supports the Commonwealth’s efforts to meet its statutory obligation to

reduce greenhouse gas emissions and to invest in our clean energy future. However, the

Department need not approve a $284 million rate increase nor pre-approve a $400 million

investment plan lacking in critical details and providing no guarantee that ratepayers will benefit

from the proposed investments, essentially amounting to a request for a blank check. The

Department and the Department of Energy Resources have established proceedings and

regulatory constructs to address grid modernization, electric vehicles and storage, and the role

that utilities should play in their advancement. Rather than working within the existing

framework, the Company chose to include them in its rate case filing, perhaps seeking to obscure

or deemphasize the magnitude of the large proposed rate increases and bill impacts on customers

with the promise of green benefits. Yet, with or without the Grid Wise-Performance Plan and

the GMBC, the Company is free to move forward with its “grid facing” grid modernization

investments for its distribution system and seek recovery as it would for any other capital

investment. And, the Department can—and should—address electric vehicle and storage

investments, as it has with similar investments, by developing statewide policies, followed by the

individual review of specific proposals.

6

These are important investments for our future. Before pre-authorizing $400 million of

investment, the Department should take the time outside of this rate case to: (1) determine how

the proposed investment fits within the state’s overall clean energy and greenhouse gas emission

reduction strategies; (2) compare it to alternatives; and (3) ensure that the Company is buying the

right equipment, locating it in the best places, and providing real benefits to customers at the

lowest possible cost.

For these reasons and the reasons set forth below, the Company’s petition will result in

unjust and unreasonable rates. The Department should deny the petition and order Eversource to

decrease its rates.

III. DESCRIPTION OF THE COMPANY

NSTAR and WMECo are affiliated Massachusetts electric and gas distribution

companies. In addition to NSTAR and WMECo, Eversource Energy owns affiliated electric

distribution companies operating in Connecticut, Massachusetts and New Hampshire. In

Massachusetts, Eversource operates NSTAR and WMECo electric distribution systems on a fully

consolidated basis. For purposes of this docket, the Company has designated these two

geographic areas as “Eversource East” and “Eversource West.” Through its Massachusetts

electric operations, Eversource serves approximately 1.4 million customers in 139 cities and

towns.

The service area designated as NSTAR/Eversource East encompasses the City of Boston

and 20 surrounding communities, extending west to Sudbury, Framingham, and Hopkinton, as

well as communities in southeastern Massachusetts extending from Marshfield south through

Plymouth, Cape Cod and Martha’s Vineyard, and through New Bedford and Dartmouth. Within

this geographic area, the Company serves approximately 1.2 million residential, commercial and

7

industrial customers in approximately 80 communities, covering approximately 1,700 square

miles. The customer base includes approximately 1,013,077 residential customers and 164,869

business customers.

The service area designated as WMECo/Eversource West encompasses the City of

Springfield and surrounding communities, extending west to the New York border and north to

Greenfield and the Vermont border. Within this geographic area, the Company serves

approximately 209,000 residential, commercial and industrial customers in approximately 59

communities in western Massachusetts, covering approximately 1,500 square miles. The

customer base includes approximately 189,507 residential customers and 18,961 business

customers.

IV. STANDARD OF REVIEW

The Department must review the “propriety” of general rate increases under Section 94.

In reviewing the “propriety” of a proposal by a utility under Section 94, the Department must

determine whether the proposed rates are just and reasonable. Attorney General v. Department

of Telecommunications and Energy, 438 Mass 256, 264 n. 13 (2002); Berkshire Gas Company,

D.P.U. 96-67, p. 6 (1996). An application of a generic public interest test derived from organic

authority must give way to the specific statutory just and reasonable analysis required when

examining a request for a general increase in rates. Attorney General v. Department of

Telecommunications and Energy, 438 Mass at 270; see also Cambridge Electric Light Company

v. Department of Public Utilities, 333 Mass. 536 (1956).

The party seeking the rate increase bears the burden of proof. Town of Hingham v.

Department of Telecommunications and Energy, 433 Mass. 198, 213-14 (2001), citing

Metropolitan District Commission v. Department of Public Utilities, 352 Mass. 18, 24 (1967);

8

Wannacomet Water Company v. Department of Public Utilities, 346 Mass. 453, 463 (1963).

Included in that burden is a responsibility to develop a record sufficiently complete to support a

Department order in its favor on any contested issue. Fitchburg Gas and Electric Light

Company, D.T.E. 99-118, p. 7, n.5 (2001) (the Company bears the burden of proving each and

every element of its case by a preponderance of “such evidence as a reasonable mind might

accept as adequate to support a conclusion.”); G. L. c. 30A, § 11(6); P. LIACOS, HANDBOOK OF

MASSACHUSETTS EVIDENCE, § 14.2 (7th ed. 1999). In Section 94 proceedings, the intervenors

have neither the burden of production nor the burden of proof. D.T.E. 99-118, p. 7 (2001). To

prevail, however, intervenors must produce evidence necessary to rebut a Company’s

allegations. D.T.E. 99-118, p. 9.4 G.L. c. 30A, §§ 10, 11.

The Department must evaluate all evidence, including rebuttal evidence and negative

evidence, and make findings that result in just and reasonable rates.5 The Department, however,

cannot validly do so without furnishing detailed and subsidiary findings of fact and conclusions

of law sufficient to demonstrate that the overall rate determination is just and reasonable.6 “G.L.

c. 30A, s 11(8), requires the decision of the Department to ‘be accompanied by a statement of

reasons ... including determination of each issue of fact or law necessary to the decision.’”

4 “[T]he burden of proof is the duty imposed upon a proponent of a fact whose case requires proof of that fact to

persuade the factfinder that the fact exists or, where a demonstration of non-existence is required, to persuade the

factfinder of the non-existence of that fact.”). Fitchburg Gas and Electric Light Company, D.T.E. 99-118, p. 7,

(2001.) 5 The Department must weigh all of the evidence, not just the evidence that supports the conclusion reached, but also

contrary evidence that derogates from that conclusion.” Town of Hingham v. Department of Telecommunications

and Energy, 433 Mass. 198, 215 (2001). 6 “[W]e have insisted that the agency make subsidiary findings of fact on all issues relevant and material to the

ultimate issue to be decided, and that it ‘set forth the manner in which it reasoned from the subsidiary facts so found

to the ultimate decision reached’.” Massachusetts Institute of Technology v. Department of Public Utilities, 425

Mass 856, 871 (1997) citing School Comm. of Chicopee v. Massachusetts Commission Against Discrimination, 361

Mass. 352, 354-355 (1972).

9

Massachusetts Institute of Technology v. Department of Public Utilities, 425 Mass 856, 867

(1997). NSTAR Electric Company v. Department of Public Utilities 462 Mass. 381, 387 (2012).

A rate is not just and reasonable simply because a utility says so. If the Company fails to

carry its burden by a preponderance of the evidence, the Department must deny the Company’s

requested rate treatment for the proposed adjustment. Fitchburg Gas & Electric Light Company

v. Department of Public Utilities, 375 Mass. 571, 582-583 (1978). The Department should be

guided by its duty to protect public interests and not promote private interests. Mass.-American

Water Company, D.P.U. 95-118, p. 77 (1996). Fitchburg Gas and Electric Light Company,

D.P.U. 09-09 pp. 22-23, citing Commonwealth Electric Company v. Department of Public

Utilities, 397 Mass. 361, 369 (1986); Attorney General v. Department of Pub. Utilities, 390

Mass. 208, 235 (1983); Lowell Gas Light Company v. Department of Pub. Utilities, 319 Mass.

46, 52 (1946).

V. ARGUMENT

A. ALTERNATE REGULATORY MECHANISMS

1. THE DEPARTMENT SHOULD REJECT THE COMPANY’S PROPOSED

PERFORMANCE-BASED RATEMAKING MECHANISM BECAUSE IT WILL

NOT PRODUCE JUST AND REASONABLE RATES

a) Introduction

Eversource, in its first post-merger rate case proceeding, proposes to implement its “Grid-

Wise Performance Plan.” Exh. ES-GWPP-1. The Grid-Wise Performance Plan encompasses

two major components. First, the Company proposes to implement what it calls a performance-

based ratemaking mechanism (“PBRM”) that would allow the Company to increase rates

significantly each year until the Company’s next rate case, pursuant to a proposed revenue-cap

formula. Exh. ES-GWPP-1 and Exh. ES-PBRM-1. As stated by the Company, the PBRM

10

would substitute for a capital-cost recovery mechanism, while furthering policy goals of the

Commonwealth. Exh. ES-CAH-1, pp. 5-6. Second, the Company proposes a Grid

Modernization Base Commitment (“GMBC”) of $400 million in incremental capital investments

over the next five years without a new or separate cost recovery mechanism. Exh. ES-GMBC-1.

The Company asserts that the adoption of the PBRM allows its proposed GMBC investments.

Id.

The Department should reject the proposed PBRM because it is fatally flawed. The

Department is no stranger to performance-based ratemaking (“PBR”), having experience with

such mechanisms that dates back many years. See e.g. Bay State Gas Company, D.T.E. 05-27

(2005); Boston Gas Company, D.T.E. 03-40 (2003); Berkshire Gas Company, D.T.E. 01-56

(2001); and Boston Gas Company, D.P.U. 96-50 (1996). Recent Department policies date back

to at least the mid-1990s.7 The Department has previously held, in part, that proposed PBR

mechanisms should be designed to achieve specific, measurable results, and not focus

excessively on cost recovery issues. Id. The Company’s proposed PBRM satisfies neither of

those criteria, being superficially concerned with capital cost recovery issues, and devoid of any

serious proposal to assure definitive benefits to ratepayers. Furthermore, the PBRM ignores the

Department’s past experience with PBR and its concern with the appropriateness of the type of

PBR proposed here, as well as the criticism such approaches have received in the

Commonwealth and other states. See e.g. Bay State Gas Company, D.P.U. 09-30, pp. 19-25

(2009) and Boston Gas Company, D.P.U. 10-55 (2010). At bottom, while the Company urges

approval of the PBRM on the ground that it is necessary to further investment in grid

modernization, the Company has failed to demonstrate that it lacks the ability to finance these

7 Incentive Regulation, D.P.U. 94-158 (1995).

11

important investments under traditional cost-of-service regulation. The Company can and should

make those worthy investments—but the evidence clearly shows that the PBRM is not needed to

enable it to do so.

b) The Company’s Proposal Is Inconsistent with Established

Department Policy

The current proceeding is not the Department’s first experience with incentive regulation

or PBR. The Department observed over a decade ago that electric and gas utility industries were

becoming increasingly more competitive starting with the Public Utility Regulatory Policies Act

(“PURPA”) of 1978 through the Energy Policy Act of 1992 (“EPAct 92”). The scope of utility

services that had historically been regulated as a monopoly, were opening to competition and

competitive pressures raising questions about the role that traditional regulation would play in

this new competitive environment. It was against this backdrop that the Department opened an

investigation in Incentive Regulation, D.P.U. 94-158 to make certain that its ratemaking policies

were compatible with these competitive trends.

Within D.P.U. 94-158, the Department set forth several general and specific criteria that

it would apply in evaluating incentive regulation proposals from electric and gas utilities.

Similar to traditional cost of service regulation, rates charged under an incentive regulation

proposal would be judged against the “just and reasonable” standard. In addition, the

Department required all petitioners to show that proposals would advance the Department’s

long-standing goals of safe, reliable, and least-cost energy service. Proposals must also promote

the objectives of economic efficiency, cost control, lower rates, and reduced administrative costs.

A well-designed proposal would provide a utility with an opportunity to earn higher rewards than

under traditional regulation, but also assume higher risks as well. Compared with traditional

regulation, the Department noted that an appropriately designed incentive plan should provide a

12

greater incentive to reduce costs for the utility while concurrently providing greater benefits to

ratepayers through lower prices or better service. In addition to these general criteria, the

Department held that a well-designed proposal must meet the following specific criteria:

(1) A proposal must comply with Department regulations, unless

accompanied by a request for a specific waiver. The Department

added that proposals that comply with statutes and governing

precedent are strongly preferred;

(2) A proposal should be designed to serve as a vehicle to a more

competitive environment and to improve the provision of monopoly

services. Incentive proposals should avoid the cross-subsidization of

competitive services by revenues derived from the provision of

monopoly services;

(3) A proposal may not result in reductions in safety, service

reliability or existing standards of customer service;

(4) A proposal must not focus excessively on cost recovery issues.

If a proposal addresses a specific cost recovery issue, its proponent

must demonstrate that these costs are exogenous to the company's

operation;

(5) A proposal should focus on comprehensive results. In general,

broad-based proposals should satisfy this criterion more effectively

than narrowly-targeted proposals;

(6) A proposal should be designed to achieve specific, measurable

results. Proposals should identify, where appropriate, measurable

performance indicators and targets that are not unduly subject to

miscalculation or manipulation; and

(7) A proposal should provide a more efficient regulatory approach,

thus reducing regulatory and administrative costs. Proposals should

present a timetable for program implementation and specify

milestones and a program tracking and evaluation method.

Boston Gas Company, D.P.U. 96-50 (Phase 1), p. 242 (1996); citing Incentive Regulation,

D.P.U. 94-158, pp. 58-64.

The Company’s proposal in this proceeding fails to comply with several of those criteria.

While the Department has made clear that PBR proposals “must not focus excessively on cost

recovery issues,” the Company’s proposed PBRM appears to be focused nearly exclusively on

cost recovery. In its initial petition to the Department, the Company presented the PBRM as a

13

substitute for a capital-cost recovery mechanism, Tr. Vol. III, pp. 522-523, a ratemaking

mechanism that would allow the Company to adjust rates to recover costs associated with capital

investments outside a normal, traditional rate case.

[T]he Company is proposing to implement performance-based

ratemaking mechanism (“PBRM”) that would adjust rates annually

in accordance with a revenue-cap formula to be approved by the

Department in this case. The PBRM would substitute for a capital-

cost recovery mechanism with the goal of furthering the

Commonwealth’s clean energy goals, creating stronger incentives

for cost efficiency, and assuring continued achievement of top-tier

service-quality performance.

Petition for Approval, p. 3 (emphasis added).

Similar language is included within the Direct Testimony supporting the Company’s

filing. Exh. ES-GWPP-1, p. 9. Likewise, elsewhere within the Direct Testimony supporting the

Company’s filing, Eversource presents the “revenue cap” formula of its PBRM as allowing the

Company to adjust rates on an annual basis in lieu of a potential capital cost recovery

mechanism.

The Company’s proposed PBRM is designed as a “revenue cap”

formula that would be used to adjust rates on an annual basis in lieu

of an annual capital cost recovery mechanism.

Exh. ES-GWPP-1, p. 10.

Indeed, the desire to mitigate Company risks through a regulatory mechanism to assist in

the recovery of capital costs appears to have predated the formulation of the PBRM. In

examining potential options before hiring its outside consultant for the PBRM, the Company

requested the consultant assist the Company in evaluating ratemaking alternatives, which

included discussions of potential capital funding options. Tr. Vol. III, p. 527. As described by

Eversource itself, these discussions prior to the creation of the PBRM included consideration of

14

whether to propose a traditional capital cost recovery mechanism in conjunction with its

proposed revenue decoupling mechanism, or to propose a PBR mechanism. See Exh. AG-28-1.

The terms of the arrangement between Dr. Meitzen and the

Company regarding his work related to the development,

implementation, testimonial, and/or analytical support of the

Company’s PBRM were provided in response to Information

Request AG-4-5, as Attachment AG-4-5(n). Prior to final execution

of the arrangement, the Company requested Christensen Associates

to assist the Company in evaluating ratemaking alternatives,

including consideration of whether the Company would propose a

traditional capital cost recovery mechanism in conjunction with

revenue decoupling or performance-based ratemaking mechanism.

Id., (emphasis added).

Furthermore, the Department’s fourth criteria notes that “[i]f a proposal addresses

a specific cost recovery issue, its proponent must demonstrate that these costs are

exogenous to the company’s operation.” The Company has not demonstrated or even

attempted to demonstrate that the cost in question are exogenous to the Company. Tr.

Vol. III, pp. 529-530. This is for the simple reason that it is impossible to make such an

argument. The cost recovery issue the PBRM is intended to address is nothing less than

all of the capital spending of the Company.

The Department also requires an incentive regulation proposal to be designed to

achieve “specific, measurable results,” and to identify metrics to measure progress

towards utility targets. D.P.U. 96-50. First, the Company has not identified any targeted

results for its proposed PBRM. The Company claims that its proposal will help the

Company in furthering the Commonwealth’s clean energy goals, while creating stronger

incentives for cost efficiency, and assuring continued achievement of top-tier service-

quality performance. Exh. ES-CAH-1, pp. 5-6. Elsewhere, the Company claims that the

GMBC portion of its proposed Grid-Wise Performance Plan will advance three key

15

characteristics necessary for the modern grid: (1) system resiliency and carbon-emissions

reduction; (2) integration of distributed energy resources (“DER”) and visibility into the

performance and impact of DER on the Company’s system real-time; and (3) facilitation

of DER customer engagement. Exh. ES-GWPP-1, p. 16. These broad general goals do

not constitute a design sufficient to achieve “specific, measurable results.” Indeed,

Eversource candidly admits that its proposal is not designed to achieve specific results:

As a first-step grid-modernization enablement plan, the GMBC is

not designed to achieve a specific end-state vision, nor is it intended

to confine the scope of the Company’s work to reach a specific end-

state. To the contrary, the Company fully anticipates that the

GMBC will be expanded upon, modified and supplemented in

significant dimension into the future.

Exh. ES-GWPP-1, pp. 16-17.

Yet, the Company is unable to identify basic measurable improvements that should result

from the Company’s proposal if it is to accomplish the goals outlined by the Company.

Eversource claims that its proposal will advance distribution system resiliency, i.e., the ability of

Eversource’s distribution system to withstand and adapt to potential future severe weather events

such as hurricanes and northeasters. However, the Company is unable to identify, specifically,

the expected improved system reliability during severe weather events, and did not even prepare

any forecasts of future system reliability performance where maximum event days are included.

See Exh. AG-18-14. Likewise, Eversource claims that its proposal will assist the

Commonwealth in reducing greenhouse gas emissions, but has not prepared any analysis

examining future emissions with and without adoption of its proposal. Id. Finally, the Company

claims its proposal will assist in promoting the adoption of DERs within its service territory, but

has again not identified with specificity the number of additional DERs or increase in DER

adoption rate the Department can expect to see with the adoption of its proposal. Id. When

16

asked for his opinion on whether the Company’s proposals identified appropriate measurable

performance indicators and targets, the Company’s outside consultant responded that he had no

opinion on the matter. Tr. Vol. III, pp. 36-37.

To the extent the Company has identified what it refers to as performance metrics, they

are wholly inadequate and inconsistent with the clear intentions of the Department’s guidelines.

Within the current proceeding, the Company first provided a set of fourteen parameters the

Company referred to as performance metrics for customer benefits. Exh. ES-GMBC-3. These

metrics, however, only address reporting requirements the Company proposed to commit to,

without identifying any threshold level for the Department to identify whether the Company was

sufficiently meeting its requirements. For example, with regard to measuring the Company’s

success involving its improvements to distribution system load flow operations, Eversource

merely stated that it would “measure average [distributed generation] application by type.” Id. p.

1. Indeed, the Company proposes to spend $111 million on what Eversource has termed

“Foundational Technology for DMS and Automation,” yet the Company does not propose any

performance metric to measure customer benefits associated with any of these expenditures,

instead providing a nebulous note that benefits will be seen in other activities:

Benefits of foundational investments are realized without other

investments […], primarily the effectiveness and reach of advanced

distribution system.

Tr. Vol III, p. 550.

In response to discovery, the Company included new metrics to measure both the

Company’s implementation efforts and customer benefits. Exh. DPU-41-7,

Supplemental 1. Specifically, the Company identified thirty additional possible metrics

that it could add to the fourteen metrics proposed by the Company in its initial filing,

finding that it would only be able to track data in relation to fourteen of the thirty

17

additional metrics. Id. Eversource explicitly stated that some of the additional metrics

measure customer benefit and/or progress towards meeting the Commonwealth’s energy

policy goals. Id. However, these new possible metrics still fail to identify target

performance, and thus are inconsistent with the Department’s criteria requiring “specific

and measurable results.” For example, the first of the new benefit metrics states that the

Company will measure the increase in feeders with DMS control. Id. Eversource

identifies no target level of increase in the number of feeders on its system with DMS

control. Likewise, the Company proposes to measure both reductions in carbon-dioxide

emissions and improvements in customer service reliability. Id. Again, the Company

provides no target improvement for the Department to measure potential future

improvements against.

The proposed PBRM also fails to provide a more efficient regulatory approach,

including reducing regulatory and administrative costs. D.P.U. 96-50. The Company

states in its filing that the proposed regulatory mechanism will produce a number of

potential regulatory cost savings for both the Company and the Department. Tr. Vol. III,

p. 538. Yet, when asked to identify specific filings the Company has made in the last five

years that the proposed mechanism would have allowed Eversource and Department to

avoid, the Company could not identify a single filing that the proposed mechanism would

have avoided. Tr. Vol. III, pp. 539-540. It is undisputed, however, that the proposed

mechanism will add new annual compliance filings that the Company must make. Tr.

Vol III, p. 541.

The Company’s proposal also ignores the experiences the Department has

encountered in the past regarding PBR. In 1996, the Department approved Boston Gas

18

Company’s (“Boston Gas”) request to implement a PBR mechanism. D.P.U. 96-50

(Phase 1).

After the expiration of its initial five-year term in the early 2000s, the Department

approved a new 10-year PBR for Boston Gas. D.T.E. 03-40. In 2010, however, Boston

Gas sought to terminate its PBR mechanism, due in part to its admission that the

available cost-reduction alternatives were not sufficient to reduce, or even hold constant,

Boston Gas’ overall O&M expenses. D.P.U. 10-55. Importantly, Boston Gas’ decision

came after the Department’s 2009 decision to terminate early a PBR mechanism in use by

then-Bay State Gas Company. D.P.U. 09-30. The Department was clear in its decision

that the PBR plan in question was not working as intended, requiring Bay State Gas

Company to seek relief under the exogenous cost, earnings sharing mechanism, and

extraordinary economic circumstances provisions of the plan on several occasions during

its implementation. Furthermore, the Department found that there was nothing in the

record of the proceeding that convinced it that Bay State Gas’ historic initiatives to

promote operational efficiencies and cost reductions would not have been undertaken

absent a PBR mechanism, and that Bay State Gas’ was unable to quantify any significant

cost savings or benefits to ratepayers associated with continuing its PBR plan.

[…] [W]e find that the Company’s PBR plan is not working as

intended. Although the Company advocates for the continuation of

PBR plan or, at least the continued applicability of the earnings

sharing mechanism, exogenous cost recovery mechanism and the

PBR rate adjustment formula, it is evident that Bay State’s

experience with the PBR plan has been less than successful. The

Company concedes that the PBR plan has failed to provide sufficient

revenues to cover the Company’s operating and maintenance costs,

declining use per customer, and capital investment needs.

Additionally […] the Company has, on several occasions in the past

four years, sought relief under the exogenous cost, earnings sharing

19

mechanism, and extraordinary economic circumstances provisions

of the PBR plan. The Company provides numerous reasons for the

rate plan’s substandard performance, such as the historic time frame

underlying the construction of PBR, fundamental changes in the

utility industry, the lengthy term of the PBR, and capital investment

demands. Regardless of the reasons, the fact remains that the

Company has been unable to effectively and efficiently operate

within the parameters of the existing PBR plan.

In addition, although the Company identifies various efforts to

promote operational efficiency and/or reduce its costs, we are not

persuaded that the tangible benefits to ratepayers, if any, flowing

from the continuation of the PBR plan, including the establishment

of new base rates, outweigh terminating the PBR plan. There is

nothing in the record to convince us that such initiatives would not

have been undertaken absent the PBR. Indeed, the Company is

unable to quantify any significant cost savings and benefits to

ratepayers associated with its PBR plan.

Bay State Gas Company, D.P.U. 09-30, pp. 24-25 (emphasis added).

As in Bay State, Eversource’s PBRM does not deliver adequate benefits for

utility customers. The Company fails to “quantify any significant cost savings and

benefits to ratepayers associated with its PBR plan.” Bay State Gas Company, D.P.U.

09-30, pp. 24-25. Indeed, the record here is near-exclusively focused on capital cost

recovery matters. As discussed further below, the proposed capital addition can be made

absent the PBRM.

As of today, there is no major U.S. utility providing electric or natural gas

distribution service that currently operates under a PBR mechanism like Eversource

proposes here. The only exception is a single California electric utility whose mechanism

terminates at the end of this year. Exh. AG/DED-1, Sch. DED-1. The Company does not

dispute this reality. Tr. Vol. III, pp. 620-621. It offers no reason why the Department

should return to the past.

20

The Department should also reject the proposed PBRM on the grounds that it is

inconsistent with the Department’s established criteria in D.P.U. 96-50 that incentive

regulation proposals in part (1) not focus excessively on cost recovery issues; (2) be

designed to achieve specific and measurable results; and (3) provide regulatory and

administrative cost efficiencies. The proposed PBRM accomplishes none of these.

c) The Company’s Proposal Will Allow Near-Guaranteed Rate

Increases at Abnormally High Rates

The Company proposes to implement the PBRM in the current proceeding in lieu of an

annual capital cost recovery mechanism. Exh. ES-CAH-1, p. 5. The proposed mechanism

would be used to adjust rates on an annual basis through the use of a “revenue cap” formula that

is derived through economic analysis of utility cost trends as indicated by measures of inflation,

input prices, and total factor productivity. Exh. ES-GWPP-1, p. 10. Through the PBRM, rates

would be allowed to increase by the rate of inflation as measured by the Gross Domestic Product

Price Index (“GDP-PI”) published by the U.S. Department of Commerce, Bureau of Economic

Analysis (“BEA”) plus 2.56 percent, Eversource’s proposed “X factor” based upon a Total

Factor Productivity (“TFP”) analysis. Id., pp. 46-47. Assuming that inflation as measured by the

GDP-PI is greater than 2 percent, the Company proposes to subtract 0.25 percent from this rate

escalation to service as a Consumer Dividend (“CD”). Id., p. 54. This calculation does not

include the possibility of any potential recovery of GMBC expenses above the Company’s

committed $400 million, exogenous cost increases, or the potential interaction of the Company’s

Earnings Sharing Mechanism (“ESM”).

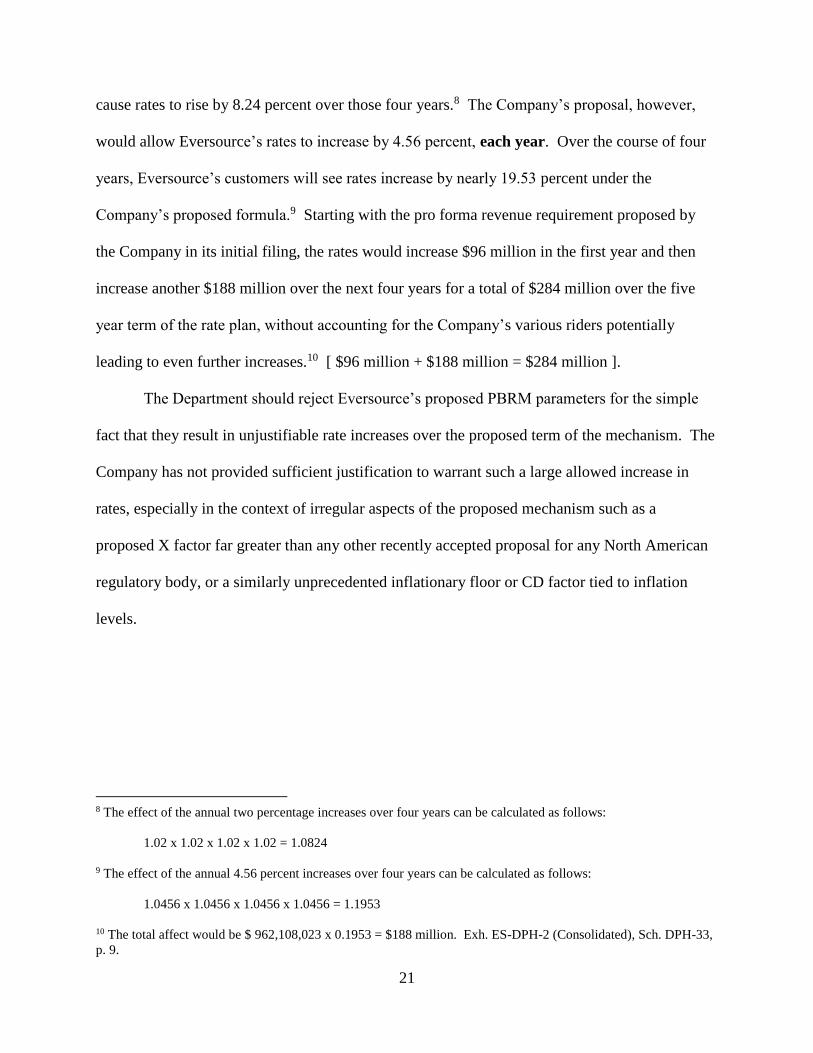

Large rate increases are embedded in the Company’s proposal. If GDP-PI is assumed to

be 2 percent per year for the four years following the rate year, increases in GDP-PI alone would

21

cause rates to rise by 8.24 percent over those four years.8 The Company’s proposal, however,

would allow Eversource’s rates to increase by 4.56 percent, each year. Over the course of four

years, Eversource’s customers will see rates increase by nearly 19.53 percent under the

Company’s proposed formula.9 Starting with the pro forma revenue requirement proposed by

the Company in its initial filing, the rates would increase $96 million in the first year and then

increase another $188 million over the next four years for a total of $284 million over the five

year term of the rate plan, without accounting for the Company’s various riders potentially

leading to even further increases.10 [ $96 million + $188 million = $284 million ].

The Department should reject Eversource’s proposed PBRM parameters for the simple

fact that they result in unjustifiable rate increases over the proposed term of the mechanism. The

Company has not provided sufficient justification to warrant such a large allowed increase in

rates, especially in the context of irregular aspects of the proposed mechanism such as a

proposed X factor far greater than any other recently accepted proposal for any North American

regulatory body, or a similarly unprecedented inflationary floor or CD factor tied to inflation

levels.

8 The effect of the annual two percentage increases over four years can be calculated as follows:

1.02 x 1.02 x 1.02 x 1.02 = 1.0824

9 The effect of the annual 4.56 percent increases over four years can be calculated as follows:

1.0456 x 1.0456 x 1.0456 x 1.0456 = 1.1953

10 The total affect would be $ 962,108,023 x 0.1953 = $188 million. Exh. ES-DPH-2 (Consolidated), Sch. DPH-33,

p. 9.

22

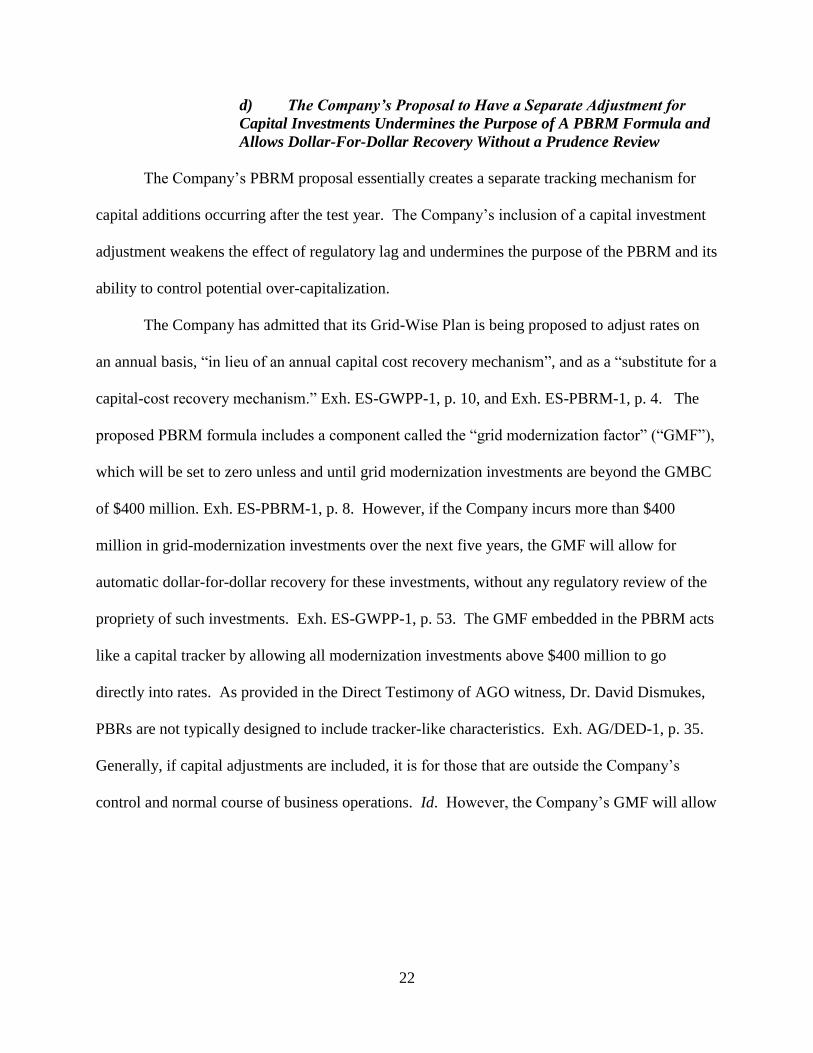

d) The Company’s Proposal to Have a Separate Adjustment for

Capital Investments Undermines the Purpose of A PBRM Formula and

Allows Dollar-For-Dollar Recovery Without a Prudence Review

The Company’s PBRM proposal essentially creates a separate tracking mechanism for

capital additions occurring after the test year. The Company’s inclusion of a capital investment

adjustment weakens the effect of regulatory lag and undermines the purpose of the PBRM and its

ability to control potential over-capitalization.

The Company has admitted that its Grid-Wise Plan is being proposed to adjust rates on

an annual basis, “in lieu of an annual capital cost recovery mechanism”, and as a “substitute for a

capital-cost recovery mechanism.” Exh. ES-GWPP-1, p. 10, and Exh. ES-PBRM-1, p. 4. The

proposed PBRM formula includes a component called the “grid modernization factor” (“GMF”),

which will be set to zero unless and until grid modernization investments are beyond the GMBC

of $400 million. Exh. ES-PBRM-1, p. 8. However, if the Company incurs more than $400

million in grid-modernization investments over the next five years, the GMF will allow for

automatic dollar-for-dollar recovery for these investments, without any regulatory review of the

propriety of such investments. Exh. ES-GWPP-1, p. 53. The GMF embedded in the PBRM acts

like a capital tracker by allowing all modernization investments above $400 million to go

directly into rates. As provided in the Direct Testimony of AGO witness, Dr. David Dismukes,

PBRs are not typically designed to include tracker-like characteristics. Exh. AG/DED-1, p. 35.

Generally, if capital adjustments are included, it is for those that are outside the Company’s

control and normal course of business operations. Id. However, the Company’s GMF will allow

23

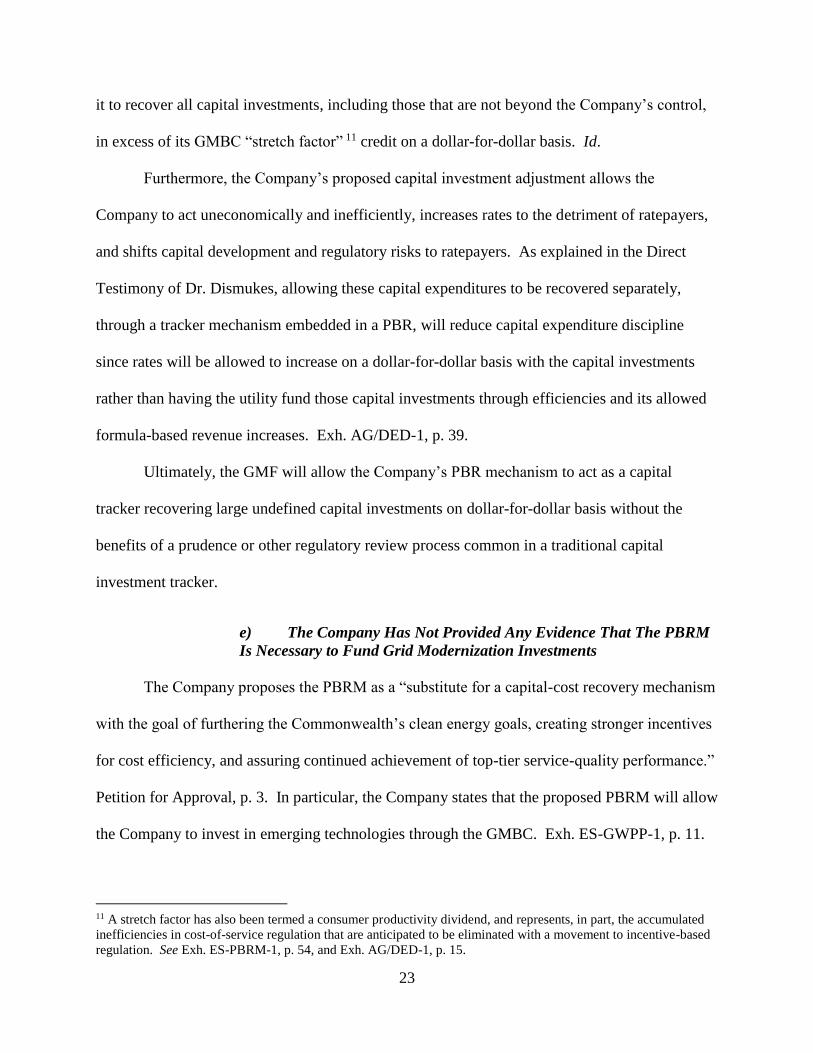

it to recover all capital investments, including those that are not beyond the Company’s control,

in excess of its GMBC “stretch factor” 11 credit on a dollar-for-dollar basis. Id.

Furthermore, the Company’s proposed capital investment adjustment allows the

Company to act uneconomically and inefficiently, increases rates to the detriment of ratepayers,

and shifts capital development and regulatory risks to ratepayers. As explained in the Direct

Testimony of Dr. Dismukes, allowing these capital expenditures to be recovered separately,

through a tracker mechanism embedded in a PBR, will reduce capital expenditure discipline

since rates will be allowed to increase on a dollar-for-dollar basis with the capital investments

rather than having the utility fund those capital investments through efficiencies and its allowed

formula-based revenue increases. Exh. AG/DED-1, p. 39.

Ultimately, the GMF will allow the Company’s PBR mechanism to act as a capital

tracker recovering large undefined capital investments on dollar-for-dollar basis without the

benefits of a prudence or other regulatory review process common in a traditional capital

investment tracker.

e) The Company Has Not Provided Any Evidence That The PBRM

Is Necessary to Fund Grid Modernization Investments

The Company proposes the PBRM as a “substitute for a capital-cost recovery mechanism

with the goal of furthering the Commonwealth’s clean energy goals, creating stronger incentives

for cost efficiency, and assuring continued achievement of top-tier service-quality performance.”

Petition for Approval, p. 3. In particular, the Company states that the proposed PBRM will allow

the Company to invest in emerging technologies through the GMBC. Exh. ES-GWPP-1, p. 11.

11 A stretch factor has also been termed a consumer productivity dividend, and represents, in part, the accumulated

inefficiencies in cost-of-service regulation that are anticipated to be eliminated with a movement to incentive-based

regulation. See Exh. ES-PBRM-1, p. 54, and Exh. AG/DED-1, p. 15.

24

However, there is no record evidence that Eversource requires the PBRM to fund its proposed

$400 million GMBC or even its normal capital additions. Existing rates are sufficient to allow

the financing of grid modernization activities.

The evidence in the record shows that the Company’s current cost of service recovers

$183 million per year in depreciation expense or capital recovery for the combined services of

WMECo and NSTAR, which will yield approximately $915 million over the next five years.

Exh. ES-DPH-2 (Consolidated), Sch. DPH-33, p. 3. [ $915 million = $183 million x 5 ].

Recovery of depreciation expense reduces net plant investment and the utility’s corresponding

rate base as existing plant investments are depreciated. Incremental new rate base investments

offset this decrease – i.e. depreciation expense, and the buildup of accumulated depreciation

reserve. Exh. FEA-MPG-1, p. 23.

Therefore, since the Company’s existing capital recovery is so many times greater than

the proposed investment under the GMBC, the Department should reject the arguments that

existing rates are insufficient to allow the financing of GMBC investment, and that the proposed

PBRM is required to support the Company’s proposal to invest in grid modernization activities.

f) The Company’s Proposed PBRM Includes a Negative X Factor

Far Lower Than That Approved for Any North American Energy Utility

The Company’s proposed PBRM formula includes a productivity adjustment known as

the “X-factor.” The X factor is an adjustment in a PBR formula that often “tempers” the degree

to which a utility can increase its rates (or revenues) due to changes in inflation alone. The

higher the X factor, other things being equal, the lower the overall net increase in rates

(revenues) that will be allowed through the PBR formulation.

25

Eversource has failed to show that its proposed X factor is a reasonable productivity

offset for the Department to utilize in setting rates for the Company’s distribution services. The

Company proposed a productivity factor of negative 2.56 % (-2.56), Exh. ES-PBRM-1, p. 61,

comprised of a negative 1.37 % (-1.37) TFP differential and an input price differential of

negative 1.19 % (-1.19). Because the Company’s proposed X factor adjustment is negative, it

will not offset the annual inflation adjustment made to rates relative to industry inflation. Rather,

it is a supplement to allow additional increase over industry inflation rates under the PBRM.

The record demonstrates that, if accepted, the Company’s proposed X factor for the

PBRM would be by far the lowest X factor accepted in at least the last ten years for a U.S.

electric or natural gas utility and no company currently is operating with a negative X factor.

Exh. AG/DED-1, pp. 13-14. Including recent Canadian regulation, the proposed PBRM would

be the only incentive regulation mechanism in North America that is designed with a negative X

factor. Exh. AG/DED-1, pp. 47-48. The record shows that the use of negative X factors is an

outcome most regulatory jurisdictions have avoided. For example, in a recent Alberta Utilities

Commission (“AUC”) consideration of PBR plans, the AUC found that the range of acceptable

X factors based on its evidentiary record was anywhere from -0.79 to +0.75 %. Even when faced

with a potential finding of an ‘acceptable’ negative X factor, the AUC decided upon a positive X

factor, inclusive of a stretch factor, of +0.3 %. Exh. ES-12, pp. 44-45.

Indeed, in considering its record evidence, the AUC specifically noted the problematic

policy consideration of allowing utility rates to increase faster than general inflation through a

negative X factor. Id.

26

The Commission is aware that the value of the X factor can be

negative, and there was considerable discussion of this issue in

Decision 2012-237, as well as in this proceeding. However, given

the manner in which TFP growth is calculated in the studies in

evidence, negative values of TFP growth mean that more inputs are

used to produce the same amount of output or that less output is

produced using the same amounts of inputs. Any industry, including

the electricity (and gas) distribution industry, may have periods

when this phenomenon is observed, but it is not clear why such a

phenomenon should persist over a long period. In the Brattle and

Meitzen studies, TFP growth is negative in nine of the last 15 years,

and more particularly, in seven of the last nine years. Yet, many of

the utilities in the current proceeding went to great lengths to explain

some of the efficiency-improving procedures (productivity

improvements) they have adopted, and there is no reason to expect

that at least some of this type of behaviour would not be observed in

many of the U.S. firms in the sample used in the TFP growth

calculations being examined here. These findings suggest that there

may be some concerns with the calculation of TFP growth using

only volume as the measure of output, whatever the time period

used, especially when combined with the particular data and input

growth assumptions utilized in the Brattle and Meitzen studies, with

the sample of U.S. electric distribution utilities. The evidence is not

conclusive, but it does cause the Commission to be mindful of the

extent to which the results differ with different choices of

assumptions, including output measures.

Id. (emphasis added). 12

The Company has premised a great deal of the specifics of its proposed PBRM on the

idea that the utilities industry is currently seeing a prolonged period of negative productivity

growth relative to the economy as a whole. However, this position is not supported by the

Bureau of Labor Statistics (“BLS”) which measures productivity growth in America industries.

In rebuttal, the Company provided information which it argued supported the notion that

negative productivity growth occurs in numerous U.S. industries. Exh. ES-PBRM-Rebuttal-1,

pp. 17-18. Specifically, the Company produced analysis of productivity growth from the years

12 2018-2022 Performance-Based Regulation Plans for Alberta Electric and Gas Distribution Utilities, Alberta

Utilities Commission Proceeding ID No. 20414, Decision 20414-D01-2016 (Errata), ¶167, emphasis added.

27

2000 through 2014 from the BLS, which produces a multifactor productivity (“MFP”) measure,

a version of a TFP. The analysis showed sixteen separate American industries that have a

negative MFP according to BLS. Included in this presentation was North American Industry

Classification System (“NAICS”) sector 22, which covers the utilities sector. The Company’s

analysis found that the BLS had estimated that the average productivity growth in the utilities

sector over the years 2000 through 2014 was negative 0.42 percent (-0.42).

The Company’s analysis, however, actually did not show the wide-spread negative

productivity growth claimed in the Company’s narrative rebuttal. The Company inadvertently

used BLS measures for changes in sector output for the presented industries, and not MFP as is