november 2017 investor presentation

TRANSCRIPT

Investor Presentation

November 2017

1) As of 12/31/14, unless otherwise noted, and does not include acreage or reserves associated with Sanish that were divested in March 2014

2) Guidance issued 2/26/15

2

Forward-Looking Statements

This presentation, including the oral statements made in connection herewith, contains forward-looking

statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the

Securities Exchange Act of 1934. All statements, other than statements of historical facts, included in

this presentation that address activities, events or developments that the Company expects, believes

or anticipates will or may occur in the future are forward-looking statements. Without limiting the

generality of the foregoing, forward-looking statements contained in this presentation specifically

include the expectations of plans, strategies, objectives and anticipated financial and operating results

of the Partnership, including the Partnership's drilling program, production, derivative instruments,

capital expenditure levels and other guidance included in this presentation. When used in this

presentation, the words "could," "should," "will,“ "believe," "anticipate," "intend," "estimate," "expect,"

"project," the negative of such terms and other similar expressions are intended to identify forward-

looking statements, although not all forward-looking statements contain such identifying words. These

statements are based on certain assumptions made by the Partnership based on management's

experience and perception of historical trends, current conditions, anticipated future developments and

other factors believed to be appropriate. Such statements are subject to a number of assumptions,

risks and uncertainties, many of which are beyond the control of the Partnership, which may cause

actual results to differ materially from those implied or expressed by the forward-looking statements.

When considering forward-looking statements, you should keep in mind the risk factors and other

cautionary statements described under the headings “Risk Factors” and “Cautionary Statement

Regarding Forward-Looking Statements” included in the filings. These include, but are not limited to,

the Partnership’s ability to integrate acquisitions into its existing business, changes in oil and natural

gas prices, weather and environmental conditions, the timing of planned capital expenditures,

availability of acquisitions, uncertainties in the estimates of proved reserves and forecasted production

results of the Partnership’s customers, operational factors affecting the commencement or

maintenance of producing wells, the condition of the capital markets generally, as well as the

Partnership's ability to access them, the proximity to and capacity of transportation facilities, and

uncertainties regarding environmental regulations or litigation and other legal or regulatory

developments affecting the Partnership's business and other important factors. Should one or more of

these risks or uncertainties occur, or should underlying assumptions prove incorrect, the Partnership's

actual results and plans could differ materially from those expressed in any forward-looking

statements.

Any forward-looking statement speaks only as of the date on which such statement is made and the

Partnership undertakes no obligation to correct or update any forward-looking statement, whether as a

result of new information, future events or otherwise, except as required by applicable law.

Cautionary Statement Regarding Oil and Gas Quantities

Reserve engineering is a process of estimating underground accumulations of hydrocarbons that cannot

be measured in an exact way. The accuracy of any reserve estimate depends on the quality of available

data, the interpretation of such data and price and cost assumptions made by reserve engineers. In

addition, the results of drilling, testing and production activities of the exploration and development

companies may justify revisions of estimates that were made previously. If significant, such revisions

could impact the Partnership’s strategy and future prospects. Accordingly, reserve estimates may differ

significantly from the quantities of oil and natural gas that are ultimately recovered. Any negative

revisions in the reserve estimates of the Partnership’s customers, including Oasis Petroleum Inc., could

have a negative impact on the Partnership’s business and future prospects.

Estimated Ultimate Recovery (“EUR”) refers to estimates of the sum of reserves remaining as of a given

date and cumulative production as of that date from a currently producing or hypothetical future well, as

applicable. These quantities do not necessarily constitute or represent reserves as defined by the SEC.

Type curves do not represent EURs of individual wells.

Non-GAAP Financial Measures

Adjusted EBITDA is a financial measure that is not presented in accordance with generally accepted

accounting principles in the United States (“GAAP”). Reconciliations of this non-GAAP financial measure

can be found in the Registration Statement. Amounts excluded from this non-GAAP measure in future

periods could be significant.

Industry and Market Data

This presentation has been prepared by the Partnership and includes market data and other statistical

information from sources believed by the Partnership to be reliable, including independent industry

publications, government publications or other published independent sources. Although the Partnership

believes these sources are reliable, it has not independently verified the information and cannot

guarantee its accuracy and completeness. Some data is also based on the Partnership’s good faith

estimates, which are derived from its review of internal sources as well as the independent sources

described above.

Trademarks and Trade Names

The Partnership owns or has rights to various trademarks, service marks and trade names that it uses

in connection with the operation of its business. This presentation also contains trademarks, service

marks and trade names of third parties, which are the property of their respective owners. The

Partnership’s use or display of third parties’ trademarks, service marks, trade names or products in this

presentation is not intended to, and does not imply, a relationship with the Partnership or an

endorsement or sponsorship by or of the Partnership. Solely for convenience, the trademarks, service

marks and trade names referred to in this presentation may appear without the ®, TM or SM symbols,

but such references are not intended to indicate, in any way, that the Partnership will not assert, to the

fullest extent under applicable law, its rights or the right of the applicable licensor to these trademarks,

service marks and trade names.

Forward-Looking / Cautionary Statements

3

Oasis Petroleum Inc. (our “Sponsor” or “Oasis”) is top pure play in the Williston Basin

20+ years of inventory life in the core and extended core economic at or below $45/bbl WTI

OMP’s assets directly improve Oasis' efficiency and economics

Integral to Our Sponsor’s

Development Plans

Strategic Assets in the

Basin’s Core

Stable Cash Flows

Financial Flexibility,

Strong Capital Structure

Extensive infrastructure in the core of the Williston Basin

Strategic connectivity to economic takeaway markets

Interconnected system provides substantial third-party connection opportunities

15-year, fixed-fee contracts with our Sponsor

Oasis’ strong hedge book protects OMP cash flows

Pro forma leverage after assignment of Gas Plant II of $66.7MM under $200MM credit

facility

Balance sheet flexibility promotes successful execution of growth strategy

No requirement to access capital markets for the foreseeable future

Top Midstream Provider in Williston Basin

Visible and Achievable

Growth

Targeting long-term 20% annual distribution growth per unit

Enhancing visibility of growth through Gas Plant II

Robust drop-down backlog supplements organic growth, supported by ROFO on Oasis’

retained interests in our DevCos and future midstream assets on current acreage, which

converts to ROFR applicable to a successor upon change of control of our Sponsor

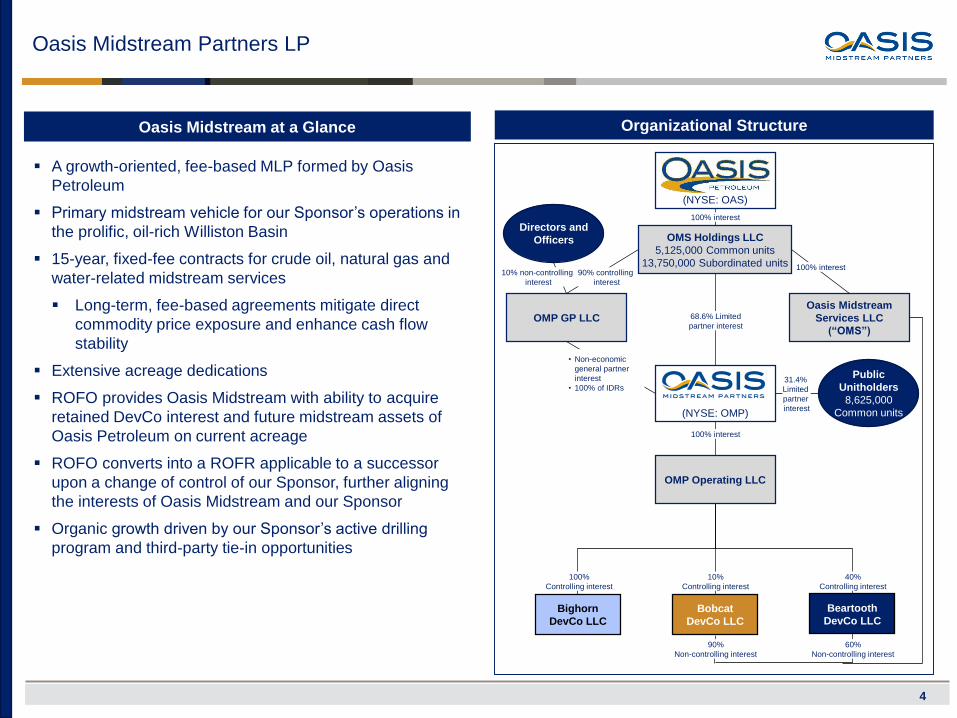

Oasis Midstream Partners LP

4

A growth-oriented, fee-based MLP formed by Oasis

Petroleum

Primary midstream vehicle for our Sponsor’s operations in

the prolific, oil-rich Williston Basin

15-year, fixed-fee contracts for crude oil, natural gas and

water-related midstream services

Long-term, fee-based agreements mitigate direct

commodity price exposure and enhance cash flow

stability

Extensive acreage dedications

ROFO provides Oasis Midstream with ability to acquire

retained DevCo interest and future midstream assets of

Oasis Petroleum on current acreage

ROFO converts into a ROFR applicable to a successor

upon a change of control of our Sponsor, further aligning

the interests of Oasis Midstream and our Sponsor

Organic growth driven by our Sponsor’s active drilling

program and third-party tie-in opportunities

Oasis Midstream at a Glance Organizational Structure

Bobcat

DevCo LLC

Beartooth

DevCo LLCBighorn

DevCo LLC

100% interest

90% controlling

interest

68.6% Limited

partner interest

100% interest

10%

Controlling interest

100%

Controlling interest

40%

Controlling interest

60%

Non-controlling interest

31.4%

Limited

partner

interest

OMS Holdings LLC

5,125,000 Common units

13,750,000 Subordinated units

(NYSE: OAS)

OMP GP LLC

Public

Unitholders

8,625,000

Common units

OMP Operating LLC

(NYSE: OMP)

Oasis Midstream

Services LLC

(“OMS”)

90%

Non-controlling interest

100% interest

• Non-economic

general partner

interest

• 100% of IDRs

Directors and

Officers

10% non-controlling

interest

55%

14%

31%

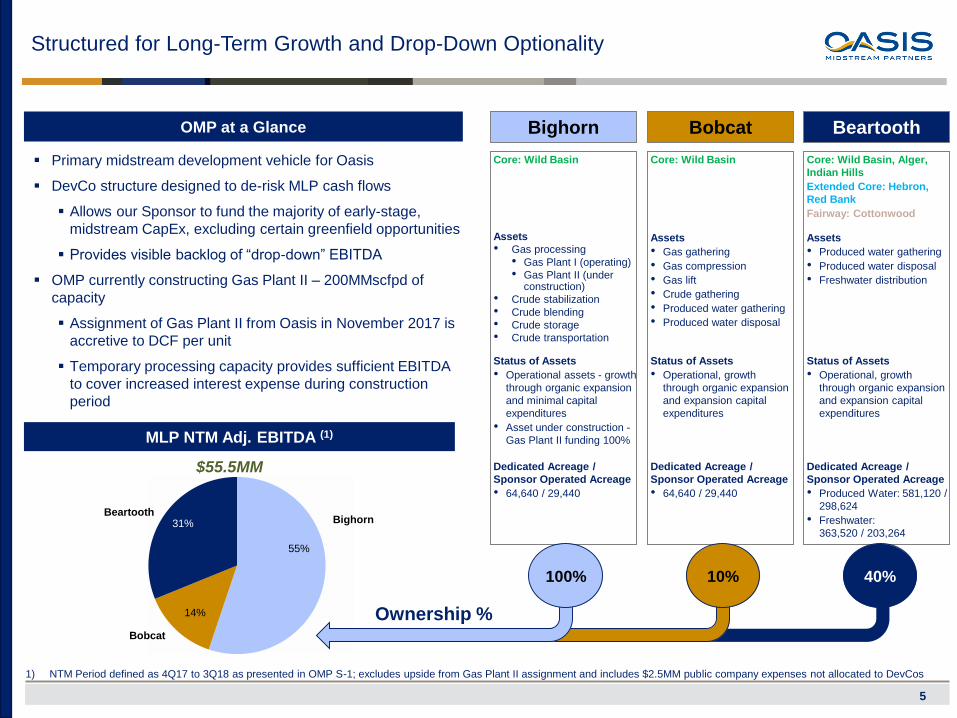

Structured for Long-Term Growth and Drop-Down Optionality

5

Primary midstream development vehicle for Oasis

DevCo structure designed to de-risk MLP cash flows

Allows our Sponsor to fund the majority of early-stage,

midstream CapEx, excluding certain greenfield opportunities

Provides visible backlog of “drop-down” EBITDA

OMP currently constructing Gas Plant II – 200MMscfpd of

capacity

Assignment of Gas Plant II from Oasis in November 2017 is

accretive to DCF per unit

Temporary processing capacity provides sufficient EBITDA

to cover increased interest expense during construction

period

Bighorn Bobcat Beartooth

40%

MLP NTM Adj. EBITDA (1)

$55.5MM

BeartoothBighorn

Bobcat

1) NTM Period defined as 4Q17 to 3Q18 as presented in OMP S-1; excludes upside from Gas Plant II assignment and includes $2.5MM public company expenses not allocated to DevCos

100% 10%

Assets

• Gas processing

• Gas Plant I (operating)

• Gas Plant II (under construction)

• Crude stabilization

• Crude blending

• Crude storage

• Crude transportation

Status of Assets

• Operational assets - growth

through organic expansion

and minimal capital

expenditures

• Asset under construction -

Gas Plant II funding 100%

Dedicated Acreage /

Sponsor Operated Acreage

• 64,640 / 29,440

Core: Wild Basin

Assets

• Gas gathering

• Gas compression

• Gas lift

• Crude gathering

• Produced water gathering

• Produced water disposal

Status of Assets

• Operational, growth

through organic expansion

and expansion capital

expenditures

Dedicated Acreage /

Sponsor Operated Acreage

• 64,640 / 29,440

Core: Wild Basin

Dedicated Acreage /

Sponsor Operated Acreage

• Produced Water: 581,120 /

298,624

• Freshwater:

363,520 / 203,264

Status of Assets

• Operational, growth

through organic expansion

and expansion capital

expenditures

Assets

• Produced water gathering

• Produced water disposal

• Freshwater distribution

Core: Wild Basin, Alger,

Indian Hills

Extended Core: Hebron,

Red Bank

Fairway: Cottonwood

Ownership %

OMP at a Glance

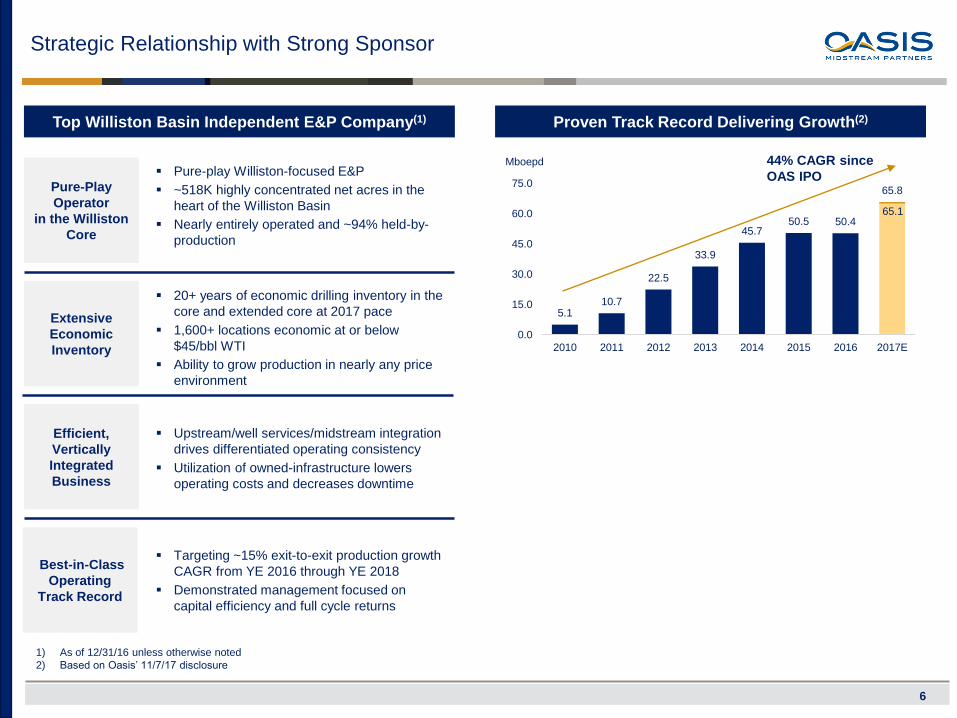

5.110.7

22.5

33.9

45.750.5 50.4

65.8

0.0

15.0

30.0

45.0

60.0

75.0

2010 2011 2012 2013 2014 2015 2016 2017E

Pure-play Williston-focused E&P

~518K highly concentrated net acres in the

heart of the Williston Basin

Nearly entirely operated and ~94% held-by-

production

6

Strategic Relationship with Strong Sponsor

Mboepd

Proven Track Record Delivering Growth(2)

Pure-Play

Operator

in the Williston

Core

Extensive

Economic

Inventory

Best-in-Class

Operating

Track Record

Efficient,

Vertically

Integrated

Business

20+ years of economic drilling inventory in the

core and extended core at 2017 pace

1,600+ locations economic at or below

$45/bbl WTI

Ability to grow production in nearly any price

environment

Targeting ~15% exit-to-exit production growth

CAGR from YE 2016 through YE 2018

Demonstrated management focused on

capital efficiency and full cycle returns

Upstream/well services/midstream integration

drives differentiated operating consistency

Utilization of owned-infrastructure lowers

operating costs and decreases downtime

Top Williston Basin Independent E&P Company(1)

65.1

44% CAGR since

OAS IPO

1) As of 12/31/16 unless otherwise noted

2) Based on Oasis’ 11/7/17 disclosure

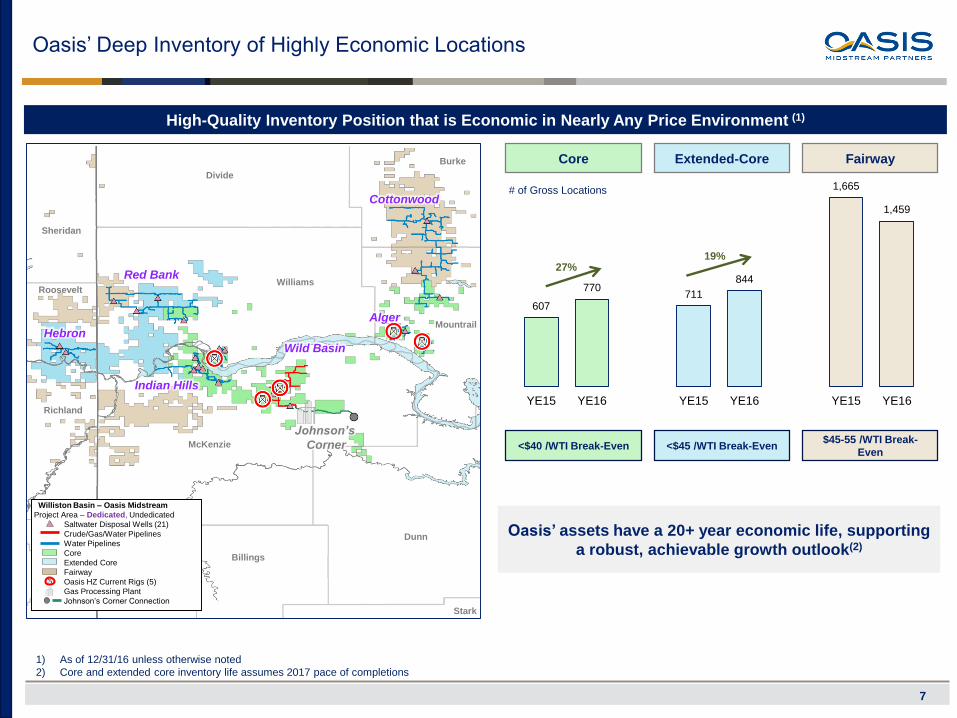

607

770711

844

1,665

1,459

YE15 YE16 YE15 YE16 YE15 YE16

Oasis’ Deep Inventory of Highly Economic Locations

7

<$40 /WTI Break-Even <$45 /WTI Break-Even$45-55 /WTI Break-

Even

Core Extended-Core Fairway

High-Quality Inventory Position that is Economic in Nearly Any Price Environment (1)

27%19%

# of Gross Locations

Oasis’ assets have a 20+ year economic life, supporting

a robust, achievable growth outlook(2)

1) As of 12/31/16 unless otherwise noted

2) Core and extended core inventory life assumes 2017 pace of completions

McKenzie

Dunn

Divide

Burke

Mountrail

Sheridan

RooseveltWilliams

Richland

Wild Basin

Stark

Billings

Alger

Cottonwood

Red Bank

Hebron

Indian Hills

Johnson’s

Corner

Williston Basin – Oasis Midstream

Project Area – Dedicated, Undedicated

Saltwater Disposal Wells (21)

Crude/Gas/Water Pipelines

Water Pipelines

Core

Extended Core

Fairway

Oasis HZ Current Rigs (5)

Gas Processing Plant

Johnson’s Corner Connection

72

>83

62

4Q16 2017E Exit 2018E Exit0

50

100

150

200

250

300

350

0 50 100 150 200 250 300 350 400

50 Stg 4 mmlb (8 wells)1,550 MBOE Type CurveJohnsrud 3BX (20 mmlb)Rolfson 3BX (10 mmlb)Recent 10mmlbs (10 wells)

8

Overview of Oasis (1)

Type curve IRR >70% for Bakken wells in Wild Basin at strip pricing

□ At $6.8MM current well costs for a 4MM pound completion

□ Wild Basin represents approximately 1/3 of core inventory and is

at the center of sponsor’s development plans

Innovation in well design yielding further improvements in economics

□ Promising early-time results in Wild Basin from high-intensity

completions

□ Limited data on 10+MM pound fracs outside of Wild Basin at

present, but encouraging results from several peers yield potential

for increasing recoveries

Running 5 rigs: two rigs in Wild Basin and three rigs in other core

areas (Indian Hills and Alger) as of 9/30/17

Well Performance

Capital discipline and returns-focused management team

Significant hedge position provides cash flow stability for growth plans,

driving further deleveraging

Borrowing base of $1.6Bn ($1.15Bn committed) with only $395MM

drawn at 9/30/17 yields substantial liquidity

No near-term debt maturities or covenant concerns

Financial Highlights

Wild Basin Bakken Well Performance

Cumulative Avg. Normalized Oil Rate (Mbbls)

Producing Days

Constrained

Production

1) Based on Oasis’ 11/7/17 disclosure

Production Growth Profile

Historical Estimated / Pro Forma Exit

Mboe/d

4Q16 Exit

16%

>15%

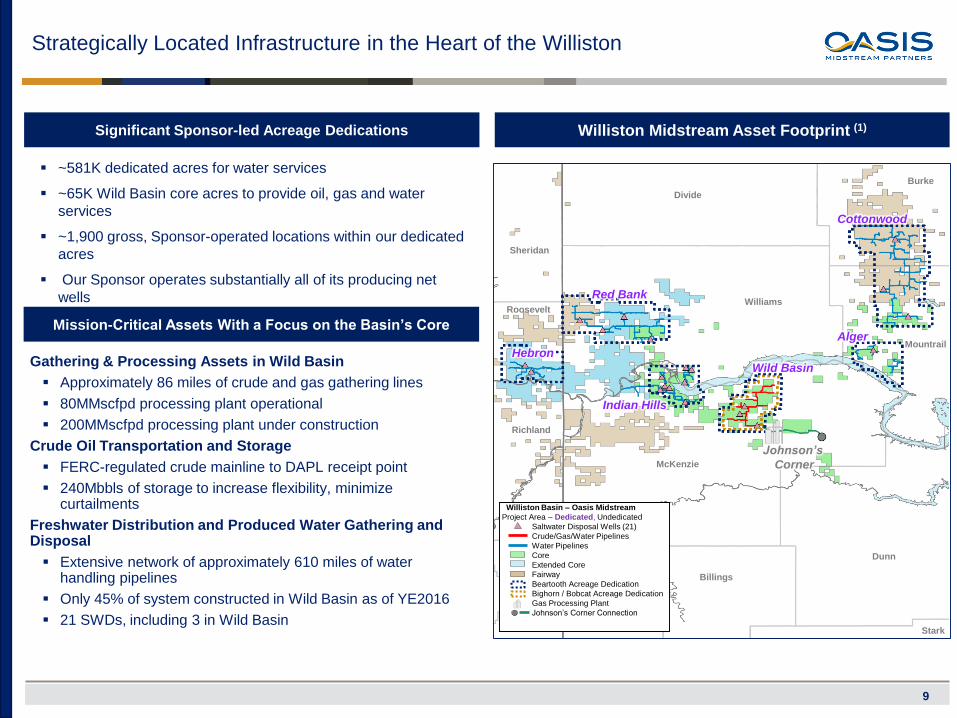

Strategically Located Infrastructure in the Heart of the Williston

9

Williston Midstream Asset Footprint (1)

Mission-Critical Assets With a Focus on the Basin’s Core

McKenzie

Dunn

Divide

Burke

Mountrail

Sheridan

RooseveltWilliams

Richland

Wild Basin

Stark

Billings

Alger

Cottonwood

Red Bank

Hebron

Indian Hills

Johnson’s

Corner

Williston Basin – Oasis Midstream

Project Area – Dedicated, Undedicated

Saltwater Disposal Wells (21)

Crude/Gas/Water Pipelines

Water Pipelines

Core

Extended Core

Fairway

Beartooth Acreage Dedication

Bighorn / Bobcat Acreage Dedication

Gas Processing Plant

Johnson’s Corner Connection

Gathering & Processing Assets in Wild Basin

Approximately 86 miles of crude and gas gathering lines

80MMscfpd processing plant operational

200MMscfpd processing plant under construction

Crude Oil Transportation and Storage

FERC-regulated crude mainline to DAPL receipt point

240Mbbls of storage to increase flexibility, minimize curtailments

Freshwater Distribution and Produced Water Gathering and Disposal

Extensive network of approximately 610 miles of water handling pipelines

Only 45% of system constructed in Wild Basin as of YE2016

21 SWDs, including 3 in Wild Basin

Significant Sponsor-led Acreage Dedications

~581K dedicated acres for water services

~65K Wild Basin core acres to provide oil, gas and water

services

~1,900 gross, Sponsor-operated locations within our dedicated

acres

Our Sponsor operates substantially all of its producing net

wells

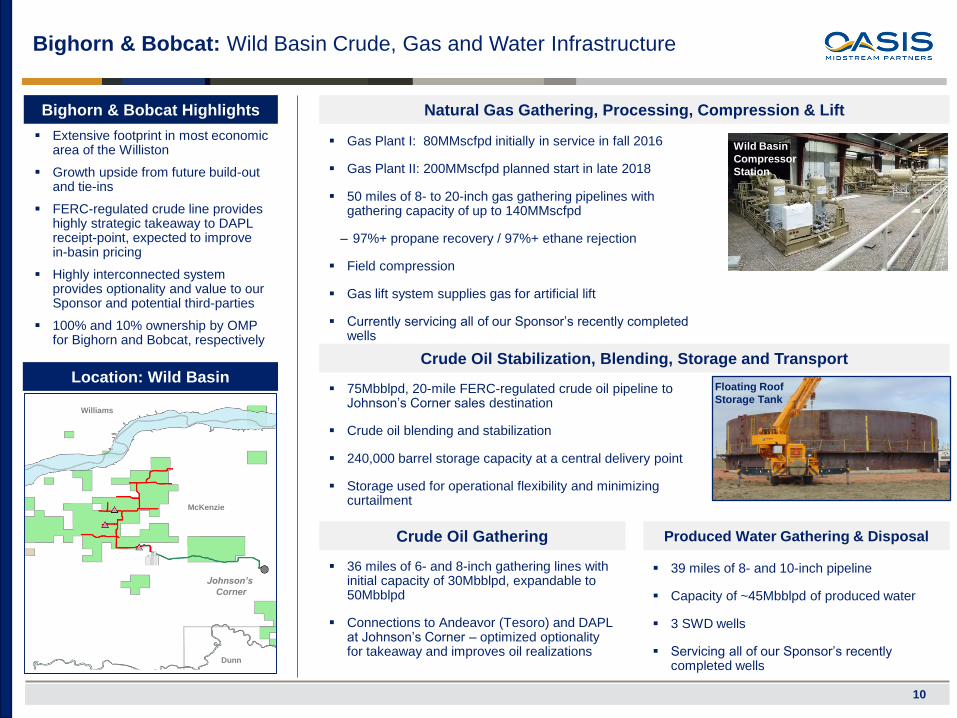

Bighorn & Bobcat: Wild Basin Crude, Gas and Water Infrastructure

10

Bighorn & Bobcat Highlights

Extensive footprint in most economic area of the Williston

Growth upside from future build-out and tie-ins

FERC-regulated crude line provides highly strategic takeaway to DAPL receipt-point, expected to improve in-basin pricing

Highly interconnected system provides optionality and value to our Sponsor and potential third-parties

100% and 10% ownership by OMP for Bighorn and Bobcat, respectively

Natural Gas Gathering, Processing, Compression & Lift

Gas Plant I: 80MMscfpd initially in service in fall 2016

Gas Plant II: 200MMscfpd planned start in late 2018

50 miles of 8- to 20-inch gas gathering pipelines with gathering capacity of up to 140MMscfpd

– 97%+ propane recovery / 97%+ ethane rejection

Field compression

Gas lift system supplies gas for artificial lift

Currently servicing all of our Sponsor’s recently completed wells

Crude Oil Gathering

36 miles of 6- and 8-inch gathering lines with initial capacity of 30Mbblpd, expandable to 50Mbblpd

Connections to Andeavor (Tesoro) and DAPL at Johnson’s Corner – optimized optionality for takeaway and improves oil realizations

Produced Water Gathering & Disposal

39 miles of 8- and 10-inch pipeline

Capacity of ~45Mbblpd of produced water

3 SWD wells

Servicing all of our Sponsor’s recently completed wells

Wild Basin

Compressor

Station

McKenzie

Dunn

Williams

Johnson’s

Corner

Location: Wild BasinCrude Oil Stabilization, Blending, Storage and Transport

75Mbblpd, 20-mile FERC-regulated crude oil pipeline to Johnson’s Corner sales destination

Crude oil blending and stabilization

240,000 barrel storage capacity at a central delivery point

Storage used for operational flexibility and minimizing curtailment

Floating Roof

Storage Tank

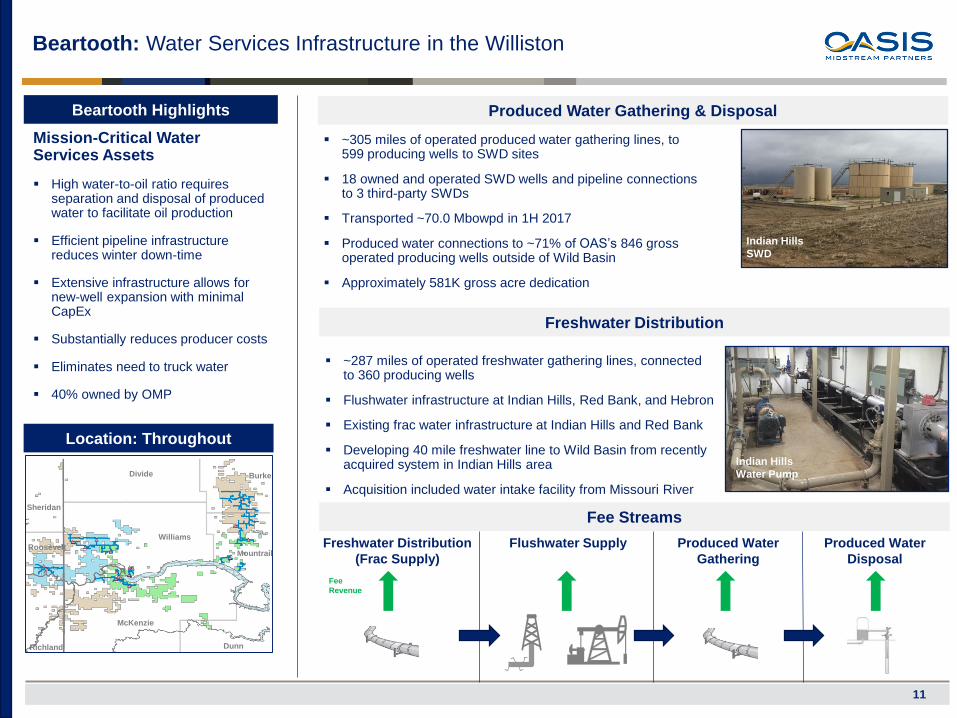

Beartooth: Water Services Infrastructure in the Williston

11

Beartooth Highlights

Mission-Critical Water Services Assets

High water-to-oil ratio requires separation and disposal of produced water to facilitate oil production

Efficient pipeline infrastructure reduces winter down-time

Extensive infrastructure allows for new-well expansion with minimal CapEx

Substantially reduces producer costs

Eliminates need to truck water

40% owned by OMP

Freshwater Distribution

~287 miles of operated freshwater gathering lines, connected to 360 producing wells

Flushwater infrastructure at Indian Hills, Red Bank, and Hebron

Existing frac water infrastructure at Indian Hills and Red Bank

Developing 40 mile freshwater line to Wild Basin from recently acquired system in Indian Hills area

Acquisition included water intake facility from Missouri River

Produced Water Gathering & Disposal

~305 miles of operated produced water gathering lines, to 599 producing wells to SWD sites

18 owned and operated SWD wells and pipeline connections to 3 third-party SWDs

Transported ~70.0 Mbowpd in 1H 2017

Produced water connections to ~71% of OAS’s 846 gross operated producing wells outside of Wild Basin

Approximately 581K gross acre dedication

Indian Hills

SWD

Fee Streams

Indian Hills

Water Pump

Fee

Revenue

Freshwater Distribution

(Frac Supply)

Flushwater Supply Produced Water

Gathering

Produced Water

Disposal

Location: Throughout

McKenzie

Dunn

Divide Burke

Mountrail

Sheridan

Roosevelt

Williams

Richland

Our Core Financial Strategy

12

Generate Stable,

Growing Cash Flows

Drive Consistent

Distribution Growth,

Target Appropriate

Coverage

Maintain Conservative

Leverage and Ample

Liquidity

Deliver stable, fee-based revenues under acreage dedications

Maintain long-term contracts with cash flow visibility and acreage dedications (e.g. 15-year contracts

with our Sponsor and Oasis Midstream Services LLC (“OMS”), low maintenance assets, reduced

development risk, 30+ year production life for majority of wells)

Minimize direct commodity price exposure

Preferred midstream service provider to Sponsor through acreage dedications

Aligned interests with Sponsor through ownership of 68.6% of OMP and IDR interests

Peer-leading drop-down runway to propel future growth

Financial flexibility enables growth strategy execution

Conservative, long-term capital structure

Borrowing to fund Gas Plant II with ample liquidity to fund drops and growth projects

Maintaining long term leverage under 2x net debt to NTM EBITDA

Flexibility to fund organic growth and acquisitions with appropriate capital mix

No need to access public equity markets for foreseeable future based on current plan

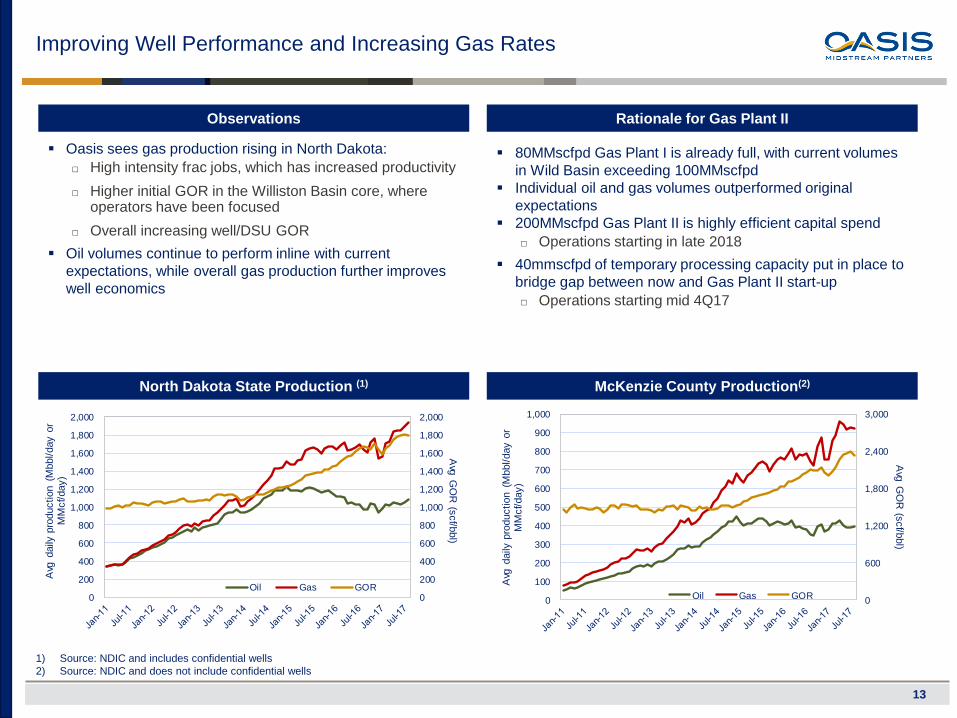

Improving Well Performance and Increasing Gas Rates

13

Observations Rationale for Gas Plant II

Oasis sees gas production rising in North Dakota:

□ High intensity frac jobs, which has increased productivity

□ Higher initial GOR in the Williston Basin core, where operators have been focused

□ Overall increasing well/DSU GOR

Oil volumes continue to perform inline with current

expectations, while overall gas production further improves

well economics

80MMscfpd Gas Plant I is already full, with current volumes

in Wild Basin exceeding 100MMscfpd

Individual oil and gas volumes outperformed original

expectations

200MMscfpd Gas Plant II is highly efficient capital spend

□ Operations starting in late 2018

40mmscfpd of temporary processing capacity put in place to

bridge gap between now and Gas Plant II start-up

□ Operations starting mid 4Q17

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Avg

GO

R (s

cf/b

bl)

Avg

daily

pro

duction (

Mbbl/day o

r M

Mcf/day)

Oil Gas GOR

North Dakota State Production (1) McKenzie County Production(2)

1) Source: NDIC and includes confidential wells

2) Source: NDIC and does not include confidential wells

0

600

1,200

1,800

2,400

3,000

0

100

200

300

400

500

600

700

800

900

1,000

Avg

GO

R (s

cf/b

bl)

Avg

daily

pro

duction (

Mbbl/day o

r M

Mcf/day)

Oil Gas GOR

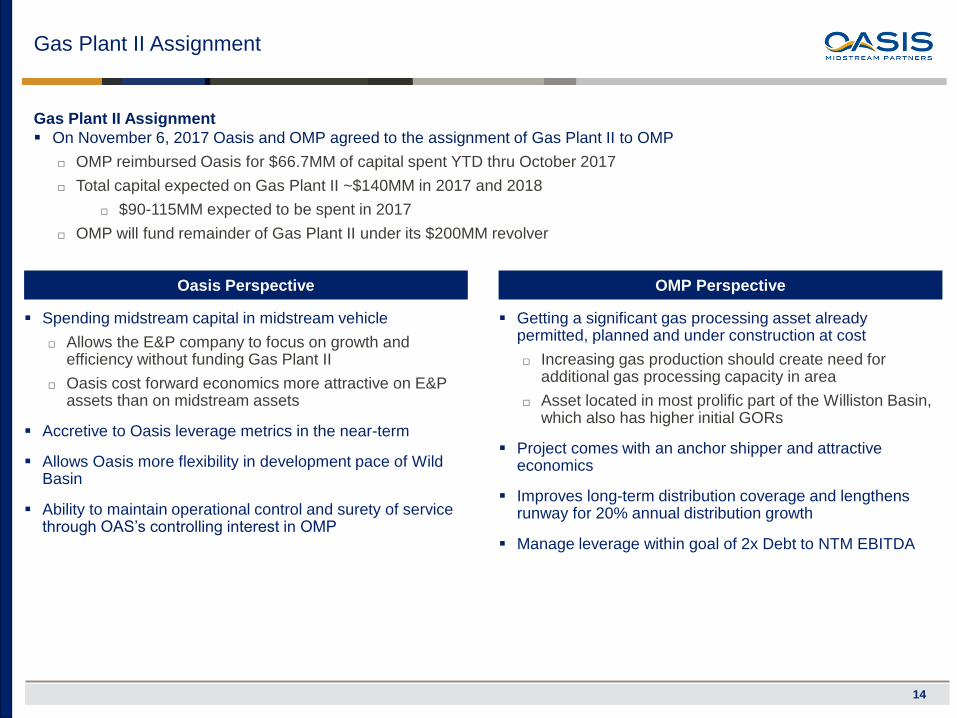

Gas Plant II Assignment

14

Gas Plant II Assignment

On November 6, 2017 Oasis and OMP agreed to the assignment of Gas Plant II to OMP

□ OMP reimbursed Oasis for $66.7MM of capital spent YTD thru October 2017

□ Total capital expected on Gas Plant II ~$140MM in 2017 and 2018

□ $90-115MM expected to be spent in 2017

□ OMP will fund remainder of Gas Plant II under its $200MM revolver

Oasis Perspective OMP Perspective

Getting a significant gas processing asset already permitted, planned and under construction at cost

□ Increasing gas production should create need for additional gas processing capacity in area

□ Asset located in most prolific part of the Williston Basin, which also has higher initial GORs

Project comes with an anchor shipper and attractive economics

Improves long-term distribution coverage and lengthens runway for 20% annual distribution growth

Manage leverage within goal of 2x Debt to NTM EBITDA

Spending midstream capital in midstream vehicle

□ Allows the E&P company to focus on growth and efficiency without funding Gas Plant II

□ Oasis cost forward economics more attractive on E&P assets than on midstream assets

Accretive to Oasis leverage metrics in the near-term

Allows Oasis more flexibility in development pace of Wild Basin

Ability to maintain operational control and surety of service through OAS’s controlling interest in OMP

15

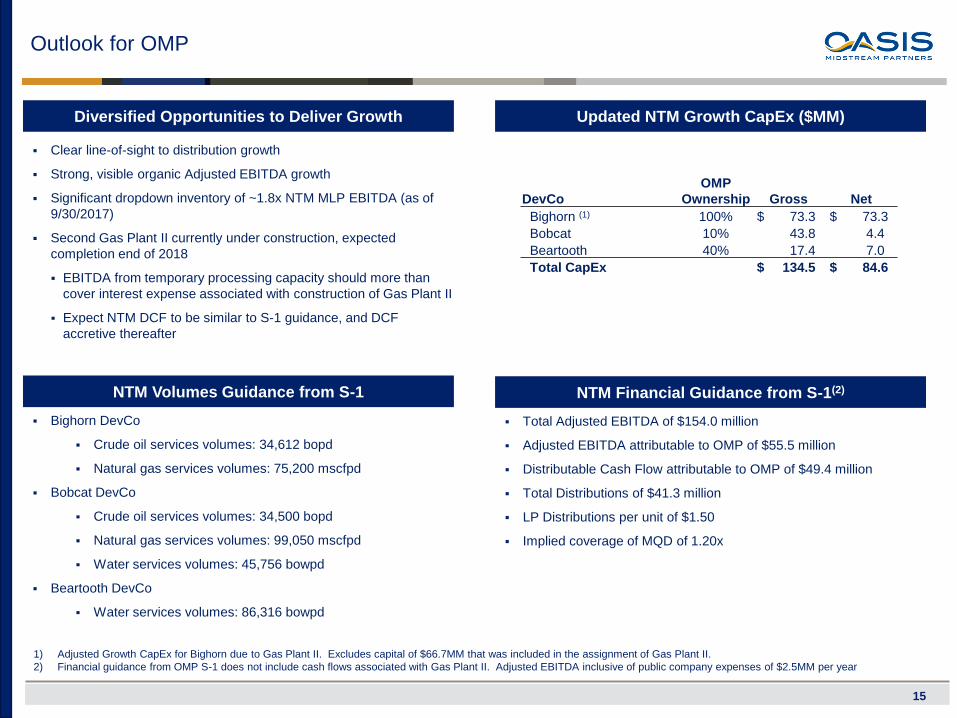

Outlook for OMP

Clear line-of-sight to distribution growth

Strong, visible organic Adjusted EBITDA growth

Significant dropdown inventory of ~1.8x NTM MLP EBITDA (as of

9/30/2017)

Second Gas Plant II currently under construction, expected

completion end of 2018

EBITDA from temporary processing capacity should more than

cover interest expense associated with construction of Gas Plant II

Expect NTM DCF to be similar to S-1 guidance, and DCF

accretive thereafter

Diversified Opportunities to Deliver Growth

1) Adjusted Growth CapEx for Bighorn due to Gas Plant II. Excludes capital of $66.7MM that was included in the assignment of Gas Plant II.

2) Financial guidance from OMP S-1 does not include cash flows associated with Gas Plant II. Adjusted EBITDA inclusive of public company expenses of $2.5MM per year

NTM Volumes Guidance from S-1 NTM Financial Guidance from S-1(2)

Bighorn DevCo

Crude oil services volumes: 34,612 bopd

Natural gas services volumes: 75,200 mscfpd

Bobcat DevCo

Crude oil services volumes: 34,500 bopd

Natural gas services volumes: 99,050 mscfpd

Water services volumes: 45,756 bowpd

Beartooth DevCo

Water services volumes: 86,316 bowpd

Total Adjusted EBITDA of $154.0 million

Adjusted EBITDA attributable to OMP of $55.5 million

Distributable Cash Flow attributable to OMP of $49.4 million

Total Distributions of $41.3 million

LP Distributions per unit of $1.50

Implied coverage of MQD of 1.20x

Updated NTM Growth CapEx ($MM)

DevCo

OMP

Ownership Gross Net

Bighorn (1) 100% $ 73.3 $ 73.3

Bobcat 10% 43.8 4.4

Beartooth 40% 17.4 7.0

Total CapEx $ 134.5 $ 84.6

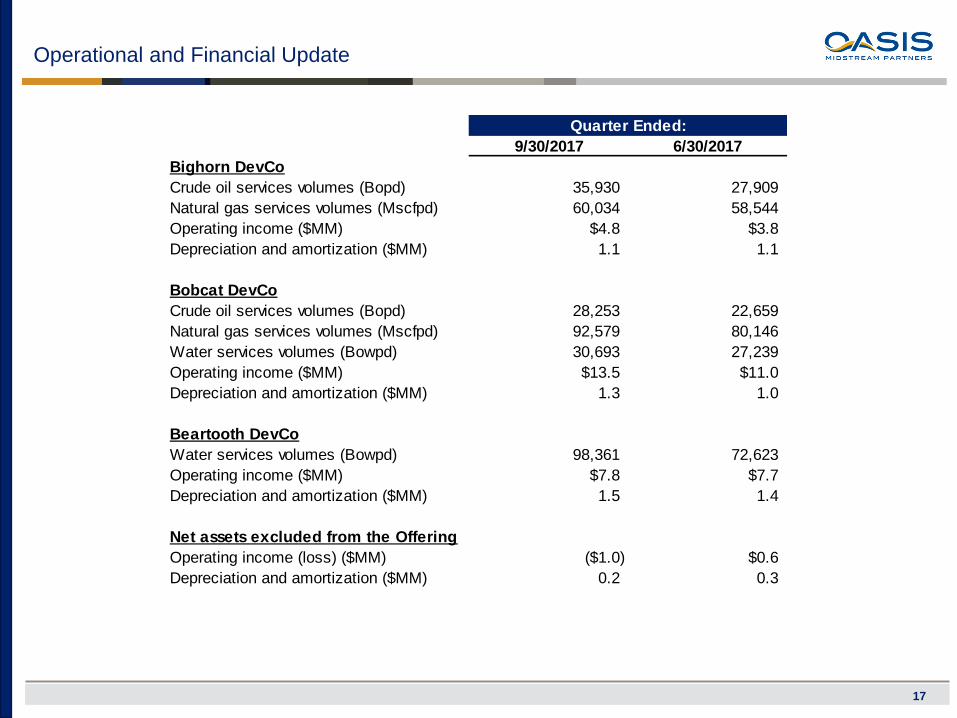

Operational and Financial Update

17

Quarter Ended:

9/30/2017 6/30/2017

Bighorn DevCo

Crude oil services volumes (Bopd) 35,930 27,909

Natural gas services volumes (Mscfpd) 60,034 58,544

Operating income ($MM) $4.8 $3.8

Depreciation and amortization ($MM) 1.1 1.1

Bobcat DevCo

Crude oil services volumes (Bopd) 28,253 22,659

Natural gas services volumes (Mscfpd) 92,579 80,146

Water services volumes (Bowpd) 30,693 27,239

Operating income ($MM) $13.5 $11.0

Depreciation and amortization ($MM) 1.3 1.0

Beartooth DevCo

Water services volumes (Bowpd) 98,361 72,623

Operating income ($MM) $7.8 $7.7

Depreciation and amortization ($MM) 1.5 1.4

Net assets excluded from the Offering

Operating income (loss) ($MM) ($1.0) $0.6

Depreciation and amortization ($MM) 0.2 0.3

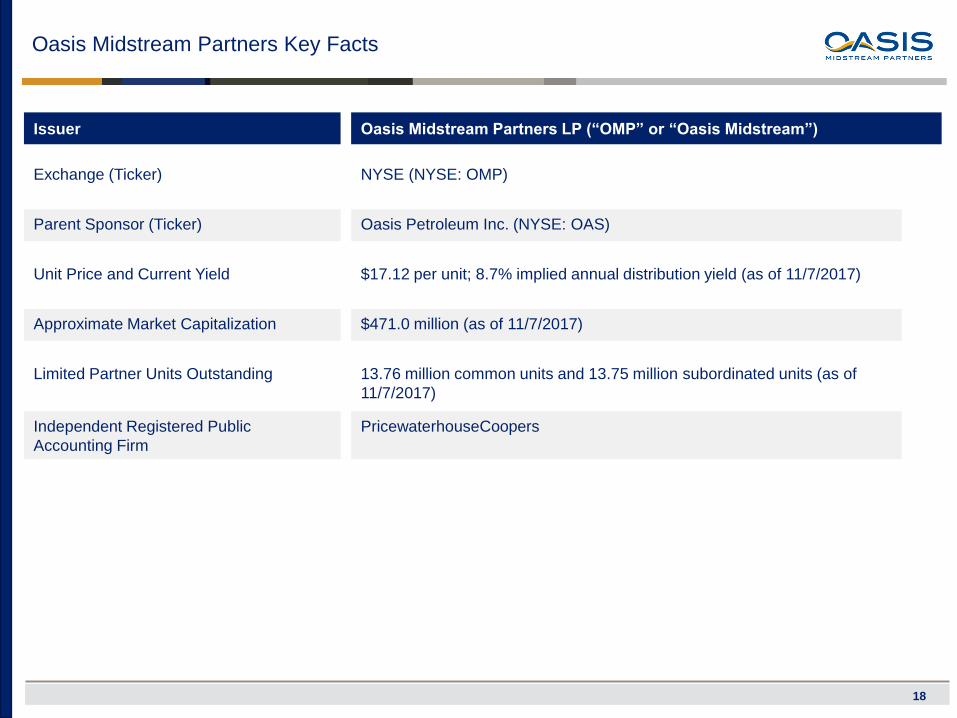

Oasis Midstream Partners Key Facts

18

Issuer

Exchange (Ticker)

Parent Sponsor (Ticker)

Unit Price and Current Yield

Approximate Market Capitalization

Limited Partner Units Outstanding

Oasis Midstream Partners LP (“OMP” or “Oasis Midstream”)

NYSE (NYSE: OMP)

Oasis Petroleum Inc. (NYSE: OAS)

$17.12 per unit; 8.7% implied annual distribution yield (as of 11/7/2017)

$471.0 million (as of 11/7/2017)

13.76 million common units and 13.75 million subordinated units (as of

11/7/2017)

Independent Registered Public

Accounting Firm

PricewaterhouseCoopers