next generation working capital - c2fo — the … · next generation working capital the new face...

TRANSCRIPT

3

The new face of liquiditySeptember 2015

Next Generation Working Capital

2

Digital approaches allow companies to truly exploit their strengths and ensure that they can counter the threats from innovative start-ups. But the pace of change makes it challenging to keep abreast of the opportunities that are available.

This is why thought leadership such as this is a key component of the way we work together with our clients.

KPMG aims to continually develop new ideas and present them to our clients in all areas of business. Working capital has often been seen as a necessary evil of doing business; but as the work by Mark Raddan, who leads KPMG’s Global Working Capital practice, and his team shows in this report, using the flexibility that digital offers, it can be a tool to allow a wide range of business objectives to be achieved – and for those objectives to be easily changed as priorities change.

Digital is something to be embraced, and I hope you find this report thought provoking.

Alwin Magimay Head of Digital and InnovationKPMG in the UK

Foreword

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Next Generation Working Capital – The new face of liquidity

We’re moving into the digital world, where we are all connected and where flexible, intuitive approaches are being used in all walks of life. Businesses can now collaborate with their customers and suppliers wherever they are, resulting in a stronger and more resilient economy, and more competitive businesses.

Working capital should be viewed as a tool to achieve a wide range of strategic objectives.

Alwin Magimay Head of Digital and Innovation KPMG in the UK

Mark Raddan Global Head of Cash and Working Capital KPMG

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Working capital management is evolving. Organisations are now focusing

on driving maximum value from their working capital, rather than simply reducing it. Technology is bringing levels

of transparency and flexibility not previously imaginable and it is vital that

organisations harness these new tools to optimise their working capital

like never before.

Next generation working capital – The new face of liquidity

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Next Generation Working Capital – The new face of liquidity

Working capital management is evolving ......................................... p5

Optimisation, not minimisation, is the answer ................................ p8

Technology enables optimisation ....................................................... p9

Step 1: Remove inefficiencies in the working capital cycle ............. p11

Step 2: Implement tools to ‘flex’ working capital (the Dynamic Discount marketplace) ................................... p12

A marketplace for working capital ..................................................... p14

A marketplace provides a rich source of data .................................. p15

A marketplace increases participation and margin improvement .... p16

In conclusion: Digital enhances the value of your working capital ......................... p17

Contents

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Next Generation Working Capital – The new face of liquidity

4© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Next Generation Working Capital – The new face of liquidity

5

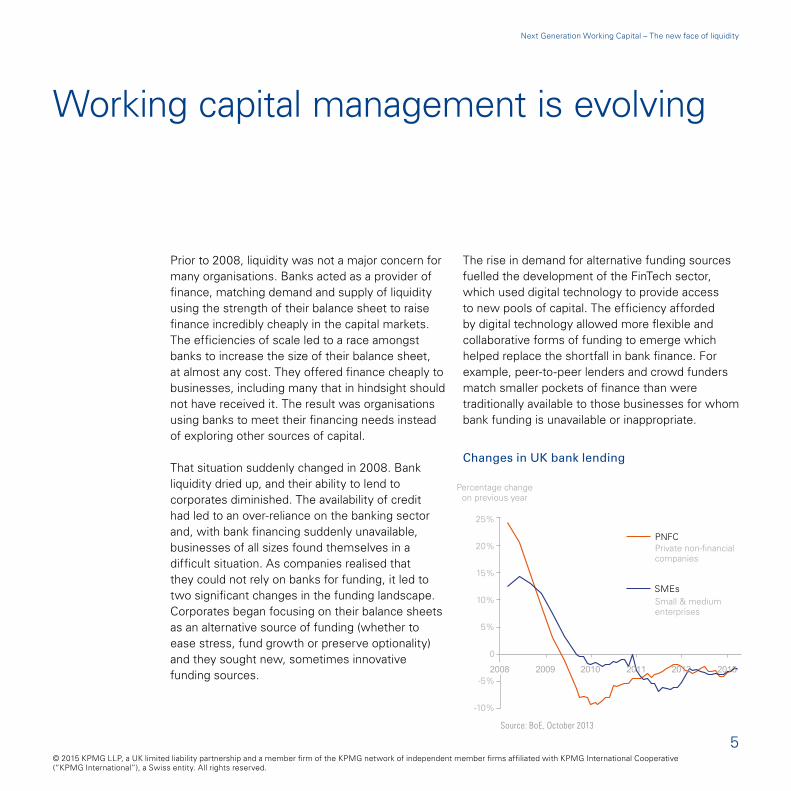

Prior to 2008, liquidity was not a major concern for many organisations. Banks acted as a provider of finance, matching demand and supply of liquidity using the strength of their balance sheet to raise finance incredibly cheaply in the capital markets. The efficiencies of scale led to a race amongst banks to increase the size of their balance sheet, at almost any cost. They offered finance cheaply to businesses, including many that in hindsight should not have received it. The result was organisations using banks to meet their financing needs instead of exploring other sources of capital.

That situation suddenly changed in 2008. Bank liquidity dried up, and their ability to lend to corporates diminished. The availability of credit had led to an over-reliance on the banking sector and, with bank financing suddenly unavailable, businesses of all sizes found themselves in a difficult situation. As companies realised that they could not rely on banks for funding, it led to two significant changes in the funding landscape. Corporates began focusing on their balance sheets as an alternative source of funding (whether to ease stress, fund growth or preserve optionality) and they sought new, sometimes innovative funding sources.

The rise in demand for alternative funding sources fuelled the development of the FinTech sector, which used digital technology to provide access to new pools of capital. The efficiency afforded by digital technology allowed more flexible and collaborative forms of funding to emerge which helped replace the shortfall in bank finance. For example, peer-to-peer lenders and crowd funders match smaller pockets of finance than were traditionally available to those businesses for whom bank funding is unavailable or inappropriate.

Working capital management is evolving

Source: BoE, October 2013

2008 20132012201120102009

PNFC

SMEs

Private non-financialcompanies

Small & mediumenterprises

Percentage changeon previous year

25%

20%

15%

10%

5%

0

-5%

-10%

Changes in UK bank lending

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Next Generation Working Capital – The new face of liquidity

6

The digital revolution is also allowing corporates to shine a spotlight on the way their own businesses are operating. The ease of adoption and use of these approaches means that corporates can now gather far more data about their business than before. Coupled with the increasing power of data analytics tools, this means that organisations can use this information in ways that were previously unimaginable, helping open up new opportunities to lower operational costs and generate revenue.

Working capital is one area that is being revolutionised by these new approaches. There are many moving parts involved in the management of working capital, and digital models have emerged that provide benefits across them; combining analytical tools with collaborative approaches to funding. The ease of implementation and use of these approaches mean that they can be used by every company, no matter what the sector or size.

As a result, the traditional view of ‘working capital’ is evolving. Technology enables companies to take control of their working capital and provides a platform for flexibility not previously possible. Working capital should now be viewed as a controllable source of cheap and easily obtainable liquidity.

Many new approaches to managing liquidity are as easy to use as streaming the latest jazz tunes. Alwin Magimay, Head of Digital and Innovation, KPMG LLP

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Next Generation Working Capital – The new face of liquidity

7

Cash is becoming an increasingly important Board agenda item and analysts now expect organisations to be more intelligent in how they manage their working capital. In a world where

rapid technological advances are occurring on what feels like a daily basis, organisations must take advantage of technology as a tool for optimising their working capital.

Banks used to be the only place in town for debt; now liquidity is a traded commodity. Julian Ramsey, KPMG Director

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Next Generation Working Capital – The new face of liquidity

8

Contrary to popular belief, falling working capital should not always be viewed as a positive or a necessity. Working capital requirements are unique and will differ by industry, product mix and geography, and will also change over time. Organisations need to ensure that their working capital targets reflect the flexibility afforded by digital technology and be careful not to set over-simplistic targets and KPIs, such as reducing working capital levels as far as possible.

Whilst the traditional focus of working capital was on minimisation to enable a business to operate in a capital efficient manner, the credit crunch has taught us that liquidity is a commodity that we should optimise in the context of business plans. However we may also deploy our working capital to generate profit or to support a symbiotic supplier base.

In an uncertain world where the next financial crisis could be around the corner and financial objectives are often in flux, an optimised working capital strategy must be flexible and balanced.

Flexible Businesses should view working capital as a lever that allows them to meet multiple objectives over time. One of these is cash generation, but others include profit enhancement and supply chain risk management.

Balanced A working capital strategy should be a fully integrated part of wider financial and supply chain strategies. If a company manages working capital in isolation, then improvement initiatives can have unforeseen negative consequences on other parts of the business.

Optimisation, not minimisation, is the answer

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Next Generation Working Capital – The new face of liquidity

9

There are two steps needed for a business to be in a position to optimise its working capital on a sustainable basis. After completion, optimised working capital can be utilised to help achieve specific business priorities at any point in time:

1. Remove inefficiencies in the working capital cycle Improving working capital efficiency is a major focus for corporates today. The objective is to allow working capital balances to be optimised sustainably to generate a cash release. This requires experience and a robust improvement methodology and toolkit.

2. Implement tools to ‘flex’ working capital (the Dynamic Discount marketplace) Once inefficiencies have been removed (or in parallel with step 1) companies are in a position to choose how to ‘work’ their working capital to help meet current objectives. One tool that illustrates this concept is Dynamic Discounting. Dynamic Discounting allows organisations to choose when to offer early payment to their suppliers in return for a discount on approved invoices.

Technology enables both steps to be completed more effectively than ever before. It does this by providing visibility of working capital performance at both micro and macro level (and both historic and forward-looking), and by allowing organisations to communicate en masse across their supply chain in real-time.

Technology enables optimisation

Corporate Treasurers don’t frequently have the ability to enhance both the P&L and the Balance Sheet - digital platforms do just that and are an extremely powerful tool for any Treasurer’s toolkit.

Jason Bristow, former VP Finance and Treasurer of Amazon.com, implemented C2FO.

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Next Generation Working Capital – The new face of liquidity

10© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Next Generation Working Capital – The new face of liquidity

11

There are a vast number of ways to remove inefficiencies across the working capital cycle. Detailed toolkits and methodologies allow for rapid and effective working capital optimisation, and effective implementation of these can lead to

sustainable change and improvement. Some of these levers are sector specific; others are cross-sector. Levers generally fall into four categories and cover all working capital cycles:

Technology is playing a key role in helping the optimisation of working capital cycles in a number of different ways. These range from rapid analysis and identification of opportunity areas, through to enhanced processes and ways of working, and

finally to transparency and reporting of cash and working capital across organisations. As a result, technology is a key facilitator in driving sustainable change and establishing an organisation-wide ‘cash culture.’

STEP 1: Remove inefficiencies in the working capital cycle

Compliance and process

In the vast amount of cases organisations can, and should, be doing better with current ways of working. Significant working capital benefit can often be generated through improved compliance (e.g. eliminating non-discounted early payments to suppliers or improving credit control to reduce overdue debtors) and by amending current processes.

Terms and policies Whilst more difficult to implement than compliance and process changes, terms and policy enhancements can yield significant improvements in working capital (e.g. optimising supplier payment terms). Knowledge is often key here, and should be viewed as both top-down (e.g. benchmarks) and bottom-up (e.g. working with suppliers to understand specific situations and risks)

Structural change Often the most challenging area of opportunity, these hypotheses can require significant changes to current operating procedures. However, if implemented effectively, they can have a radical impact on organisations’ working capital cycles.

Financing This area of opportunity is becoming increasingly popular globally. Financing can be an effective way of aligning working capital and profitability targets to organisations’ overall strategies.

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Next Generation Working Capital – The new face of liquidity

12

Once a company’s working capital cycle has been optimised it needs to decide how to use its working capital to meet its objectives. Whilst enhancements to working capital can be permanent and used for initiatives such as reducing debt or funding investment, businesses can use models such as Dynamic Discounting as an alternative deployment of short-term cash to boost profit. Tools are needed to allow this to happen, and technology once again can provide the answers.

An example of this is making early payments to suppliers in exchange for discounts on approved invoices. This model allows companies to generate additional margin from their accounts payable when they have cash available and they choose to offer early payment to suppliers. At the same time, it allows them to replenish cash levels quickly by stopping early payments when that is their objective.

This not only allows organisations to trade working capital for profit but can help build partnerships across the supply chain. A legacy of the credit crunch is that organisations have a greater corporate responsibility and the introduction of new legislation (such as the Prompt Payment Code and SupplierPay) has put greater emphasis on ethical business practices. Allowing customers and suppliers to communicate real-time and select mutually beneficial early payment rates is an excellent example of how technology is helping the development of supply chain partnerships.

STEP 2: Implement tools to ‘flex’ working capital (the Dynamic Discount marketplace)

Having the ability to deploy cash based on business cycles and seasonality proved to be extremely valuable - the C2FO model allows for both suppliers and corporates to be extremely flexible in their approach.Jason Bristow, former VP Finance and Treasurer of Amazon.com, implemented C2FO.

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Next Generation Working Capital – The new face of liquidity

13

In order for this to work, a mechanism is required to allow suppliers to request early payment from their corporate customers. Whilst some corporates arrange this manually on an ad hoc basis, the challenges of continually negotiating discounts and the resources required to do this limit scalability. However, the recent advances in technology and emergence of digital/cloud-based Dynamic Discounting platforms and their supplier networks has made the automated mass negotiation of early payments possible.

However, as with any new technology, different Dynamic Discounting models have emerged and companies must be careful to understand the implications of each. A successful acceleration programme must be easy to implement, non-disruptive to payment processes and maximise benefits to both buyers and their suppliers.

The methodology used by traditional Dynamic Discounting models is restrictive: ‘buyer push,’ where corporates set the discount rate at which suppliers can participate in their programme. This

places the onus on the buyer to have a complete understanding of their suppliers’ cash needs in terms of their alternative cost to borrow and timings. The end result is lower adoption and little impact on supply chain risk or profit margins.

A more successful model developed by C2FO leverages technology to facilitate real-time two way communication between buyers and their suppliers, giving suppliers control over what price they offer in exchange for early payment. By introducing a working capital marketplace, both parties can benefit.

Costco wanted a solution that was a win-win-win for Costco, its suppliers and ultimately its members… a great example of what can be accomplished when thoughtful, ethical people are willing to challenge the status quo.

J Grachek, VP Merchandise, Costco (C2FO user)

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Next Generation Working Capital – The new face of liquidity

14

A marketplace is arguably the most efficient way for buyers and suppliers to negotiate the price of goods or services. As technology has now turned cash on corporate balance sheets into a tradeable commodity, using a marketplace to match the supply of buyer cash with the demand for cash from their suppliers is the logical way forward. This approach allows both buyers and suppliers to express the value to them of that cash in real time, and to change it as their situation and priorities change. The marketplace essentially determines the “clearing price” for working capital at each point in time.

For a buyer, making available their cash to suppliers via a marketplace has two main benefits:

• firstly, it provides a rich source of data for the buyer on the health of its supply chain; and

• secondly, it increases the overall participation of suppliers and the margin impact.

A marketplace for working capital

…a real-time market creates more efficient transactions than buyers and suppliers can create for themselves…Mark Thomas, C2FO Director of Client Operations

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Next Generation Working Capital – The new face of liquidity

151 5 10 15 20 25

AP

R %

Time (weeks in market)

16%

14%

12%

10%

8%

6%

4%

2%

0

Supplier B

Need for cash spikes in week 8, providing signal that there may

be risk in your supplier base to

mitigate

Supplier A

Regularly bids at 4% APR (below

alternative cost of funding); bids higher

at quarter end to accelerate as many invoices as possible

1 5 10 15 20 25

AP

R %

Market Close

16%

14%

12%

10%

8%

6%

4%

2%

0

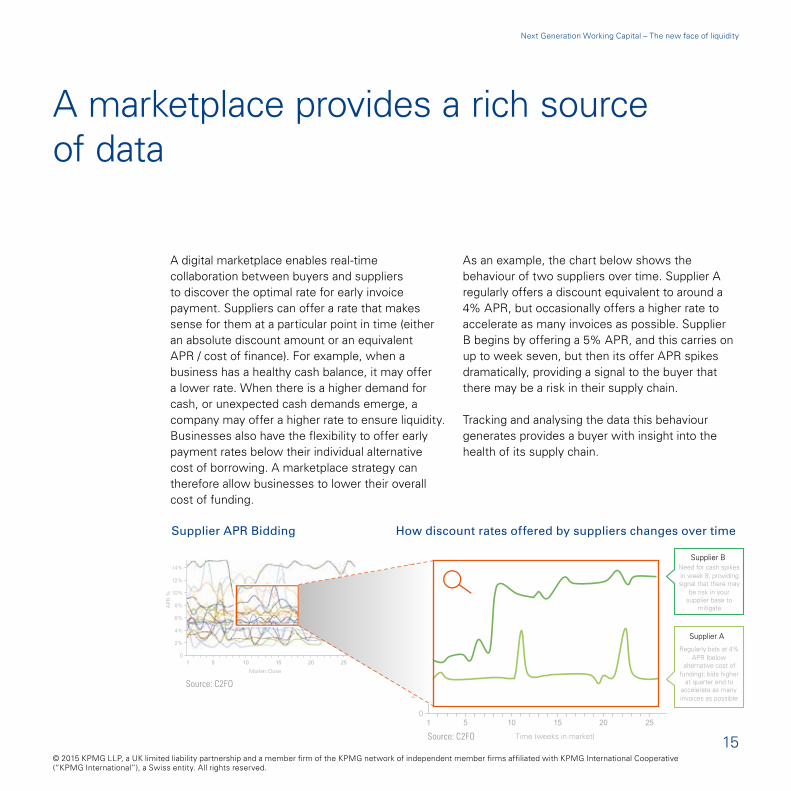

A digital marketplace enables real-time collaboration between buyers and suppliers to discover the optimal rate for early invoice payment. Suppliers can offer a rate that makes sense for them at a particular point in time (either an absolute discount amount or an equivalent APR / cost of finance). For example, when a business has a healthy cash balance, it may offer a lower rate. When there is a higher demand for cash, or unexpected cash demands emerge, a company may offer a higher rate to ensure liquidity. Businesses also have the flexibility to offer early payment rates below their individual alternative cost of borrowing. A marketplace strategy can therefore allow businesses to lower their overall cost of funding.

As an example, the chart below shows the behaviour of two suppliers over time. Supplier A regularly offers a discount equivalent to around a 4% APR, but occasionally offers a higher rate to accelerate as many invoices as possible. Supplier B begins by offering a 5% APR, and this carries on up to week seven, but then its offer APR spikes dramatically, providing a signal to the buyer that there may be a risk in their supply chain.

Tracking and analysing the data this behaviour generates provides a buyer with insight into the health of its supply chain.

A marketplace provides a rich source of data

How discount rates offered by suppliers changes over time Supplier APR Bidding

Source: C2FO

Source: C2FO

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Next Generation Working Capital – The new face of liquidity

16

By adopting a marketplace-based approach, the buyer sets the minimum rate of return that it needs to receive on its cash in aggregate (e.g. the buyer will make available £10m in cash for early payment and require a return on that cash of at least 6.8% APR). In parallel, each supplier expresses their individual rate when they submit an early payment offer. This ability for suppliers to control the rate increases participation over and above one-size-fits-all pricing models.

Suppliers have different cash flow needs and costs. Some have a cost of borrowing of less than 1%; some have a cost of 20% or more. A marketplace approach blends higher offers and lower offers to optimise buyer return on cash while making sure that each supplier is funded at a rate that is lower than their alternative cost of funding.

In the chart below, each supplier’s offer and the income created is shown as a bubble. By allowing each supplier to offer the rate that makes sense for them at that point in time, the buyer captures a much broader range of discounts while providing its entire supply chain more flexibility on timing and frequency of usage. In addition, the marketplace is an efficient way to allocate a corporate’s cash to the suppliers that need it the most.

A marketplace increases participation and margin improvement

Marketplace real-time supplier behaviour

10 20 30 40 50 60 70 80

AP

R %

Days paid early

24%

18%

12%

6%

0

Quarter End Player

Discount 0.15%DPE 18APR 3%

2

Discount Arbitrager

Discount 0.10%DPE 8APR 4.5%

1

Fortune 500 with LowCost of CapitalDiscount 0.30%DPE 53APR 2%

4

Cash Constrained

Discount 2%DPE 49APR 15%

3

Factoring Supplier

Discount 3.5%DPE 70APR 18%

5

Source: C2FO

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Next Generation Working Capital – The new face of liquidity

17

To summarise, technology is driving a rapid cultural change with regards to working capital and liquidity management. Businesses are now looking to maximise value from working capital and are moving away from simply driving down working capital levels as far as possible.

Based on what we see across the market, and the programmes KPMG are involved in, there are two key points to maximise value from working capital:

Conclusion: digital enhances the value of your working capital

1. Use data analytics to identify opportunities, drive efficiencies and to support sustainability

2. Take advantage of a Dynamic Discount marketplace to trade the new commodity that is working capital

17

Get these right, and significant value can be created and sustained over the short, medium and long-term.

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Your contacts

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the United Kingdom.

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

Produced by Create Graphics | CRT047454 | September 2015kpmg.com/uk

Mark Raddan Global Head of Cash and Working Capital KPMG 15 Canada Square London E14 5GLE: [email protected] M: +44 (0) 7810 854 152

Alwin Magimay Head of Digital and Innovation KPMG in the UK 15 Canada Square London E14 5GLE: [email protected] M: +44 (0) 44 7768 848 110

Mark Thomas Director of Client Operations C2FO 15 Stratton Street London W1J 8LQE: [email protected] M: +44 (0) 7557 515 512