negotiable instruments law 2031

TRANSCRIPT

8/20/2019 Negotiable Instruments Law 2031

http://slidepdf.com/reader/full/negotiable-instruments-law-2031 1/47

1Cesar Nickolai F. Soriano Jr. Arellano University School of Law 2011-0303NEGOTIABLE INSTRUMENTS LAW (Act No. 2031) based on the book of Aquino and De Leon and Audio Lecture of Dean Sundiang

NEGOTIABLE INSTRUMENTS LAW

INTRODUCTION

GOVERNING LAWS – ACT No. 2031 effective June 2, 1911 (whichamended some of the provisions of the Rules of the Law Merchant),the Code of Commerce and the Civil Code.

APPLICABILITY OF THE NEGOTIABLE INSTRUMENTS LAW – the Act applies only to negotiable instruments or those that meet therequirements under Sec. 1 of Act No. 2031.

KRAUFFMAN VS. PNB (GR No. 16454, Sept. 29, 1921) - Herein plaintiffwas entitled to P98,000 of the Philippine Fiber and Produce Company’sdividend for the year 1917. George B. Wicks, treasurer of the Company,requested that a telegraphic transfer of $45,000 to the plaintiff in New

York City. Wicks drew and delivered a check for the amount ofP90,355.50, total cost of said transfer, including exchange and cost ofmessage which was accepted by the officer selling the exchange inpayment of the transfer in question. As evidence of this transaction adocument was made out and delivered to Wicks, which is referred to bythe bank's assistant cashier as its official receipt. On the same day thePhilippine National Bank dispatched to its New York agency a cablegramfor $45,000. However, the bank's representative in New York repliedsuggesting the advisability of withholding this money from Kauffman. ThePNB dispatched to its New York agency another message to withhold theKauffman payment as suggested. Meanwhile, upon advice of Wicks thatthe money has been placed to his credit, Kauffman presented himself atthe office of the Philippine National Bank in New York and demanded the

money. By this time, however, the message from the Philippine NationalBank directing the withholding of payment had been received in New York, and payment was therefore refused. Thus the present complaint torecover said sum, with interest and costs. ISSUE: WON Act No. 2031 isapplicable in the above case? HELD: NO. The provisions of theNegotiable Instruments Law to come into operation, there must be adocument in existence of the character described in section 1 of the Law;and no rights properly speaking arise in respect to said instrument until itis delivered. In the case before us there was an order transmitted by thedefendant bank to its New York branch, for the payment of a specifiedsum of money to George A. Kauffman. But this order was not madepayable "to order or "to bearer," as required in Section 1(d) of that Act;and inasmuch as it never left the possession of the bank, or itsrepresentative in New York City, there was no delivery in the senseintended in Section 16 of the same Law. In this connection it isunnecessary to point out that the official receipt delivered by the bank to

the purchaser of the telegraphic order, and already set out above, cannotitself be viewed in the light of a negotiable instrument, although it affordscomplete proof of the obligation actually assumed by the bank.

GSIS VS. CA (GR No. L-40824, Feb. 23, 1989) - Private respondents, Mr.and Mrs. Isabelo R. Racho, together with the Lagasca spouses, executed adeed of mortgage in favor of petitioner GSIS. Subsequently, another deedof mortgage was executed in connection with earlier two loans granted. Aparcel of land, co-owned by said mortgagor spouses, was given assecurity under the aforesaid two deeds and they also executed a"promissory note". The Lagasca spouses executed an instrumentdenominated "Assumption of Mortgage" under which they obligatedthemselves to assume obligation to the GSIS. This undertaking was notfulfilled. Upon failure of the mortgagors to comply with the conditions ofthe mortgage, particularly the payment of the amortizations due, GSISextra-judicially foreclosed the mortgage and caused the mortgaged

property to be sold at public auction. Private respondents filed a complaintagainst the petitioner and the Lagasca spouses praying that theextrajudicial foreclosure be declared null and void. In their aforesaidcomplaint, they alleged that they signed the mortgage contracts not assureties or guarantors for the Lagasca spouses but they merely gave theircommon property to the said co-owners who were solely benefited by theloans from the GSIS. Trial court dismissed the case. CA reversed decisionstating that the respondents are that only of an accommodation party.ISSUE: WON the NIL is applicable to the promissory note and mortgagedeed? HELD: No. Both parties relied on the provisions of Section 29 of ActNo. 2031, otherwise known as the Negotiable Instruments Law, which

provide that an accommodation party is one who has signinstrument as maker, drawer, acceptor of indorser without receivingtherefor, but is held liable on the instrument to a holder for value altthe latter knew him to be only an accommodation party. This approboth parties appears to be misdirected and their reliance misplacepromissory note hereinbefore quoted, as well as the mortgage subject of this case, are clearly not negotiable instruments. documents do not comply with the fourth requisite to be considesuch under Section 1 of Act No. 2031 because they are neither payorder nor to bearer. The note is payable to a specified party, the

Absent the aforesaid requisite, the provisions of Act No. 2031 wouapply, governance shall be afforded, instead, by the provisions of thCode and special laws on mortgages.

C. CONCEPT OF NEGOTIABLE INSTRUMENTS

1. DEFINITION: Negotiable Instruments are written statesigned by the maker or drawer containing an unconditional por order to pay a sum certain money, payable on demand ofixed or determinable future time, to order or to bearer.

2. FUNCTIONS OF NEGOTIABLE INSTRUMENTSa. Substitute for money - although they are not cons

legal tender. One of its distinct characteristics is its negotwhich allows it to go from hand to hand in the commmarkets and to take the part of money in commtransactions free from all personal defenses available a

the original owner. b.

Media of exchange – they thus increase the purcmedium in circulation. They are a safe and convenient medoing business that eliminate the risk of dealing in cash.

c.

Medium of credit transactions – they allow mundoubted credit (such as those with illiquid properties) ton business enterprise upon their promissory notes, bexchange and checks knowing that other businessmen wthese promises as cash.

Checks are primarily used for immediate payment (subsfor money); while ordinary bill of exchange and the promnote are intended for the circulation of credits (instruments)

3. LEGAL TENDER – that amount which the creditor can be com

to accept as payment.

Sec. 52,NewCentralBank

Act

Legal Tender Power. — All notes and coins issued Bangko Sentral shall be fully guaranteed by the Goverof the Republic of the Philippines and shall be legal tenthe Philippines for all debts, both public and pProvided, however , That, unless otherwise fixed Monetary Board, coins shall be legal tender in amounexceeding Fifty pesos (P50.00) for denominations of Tfive centavos and above, and in amounts not excTwenty pesos (P20.00) for denominations of Ten centa

Sec. 60 Legal Character. — Checks representing demand dedo not have legal tender power and their acceptance payment of debts, both public and private, is at the opthe creditor: Provided, however, That a check whibeen cleared and credited to the account of the credito

be equivalent to a delivery to the creditor of cash amount equal to the amount credited to his account

TIBAJIA VS. CA (GR No. 100290, June 4, 1993) - A writ of attacwas issued by the trial court in connection to the collection of a smoney filed by Eden Tan against the Tibajia spouses. The fund waon deposit with the cashier of the Regional Trial Court of PasigTibajia spouses thereafter delivered to the Deputy Sheriff the total

judgment in the form of Cashier's Check worth P262,750.00. HoEden Tan, refused to accept the payment made and instead insistethe garnished funds deposited with the cashier of the Regional Tria

8/20/2019 Negotiable Instruments Law 2031

http://slidepdf.com/reader/full/negotiable-instruments-law-2031 2/47

2Cesar Nickolai F. Soriano Jr. Arellano University School of Law 2011-0303NEGOTIABLE INSTRUMENTS LAW (Act No. 2031) based on the book of Aquino and De Leon and Audio Lecture of Dean Sundiang

of Pasig be withdrawn to satisfy the judgment obligation. Petitioners fileda motion to lift the writ of execution on the ground that the judgmentdebt had already been paid but was denied by the trial court on theground that payment in cashier's check is not payment in legal tender.When the petitioners' motion for reconsideration was denied, the spousesTibajia filed herein petition. ISSUE: WON the delivery of the cashier'scheck is considered payment in legal tender? HELD: No. A check, whethera manager's check or ordinary check, is not legal tender, and an offer of acheck in payment of a debt is not a valid tender of payment and may berefused receipt by the obligee or creditor. (Philippine Airlines, Inc. vs.Court of Appeals and Roman Catholic Bishop of Malolos, Inc. vs.Intermediate Appellate Court). The ruling in the two (2) abovementionedcases decided by the Supreme Court applies the statutory provisionswhich lay down the rule that a check is not legal tender and that a creditor

may validly refuse payment by check, whether it be a manager's, cashier'sor personal check.

PAL VS. CA (GR No. 49188, Jan. 30, 1990) - CFI Manila ruled in favor of Amelia Tan [under the name and style of Able Printing Press] in acomplaint for damages against petitioner Philippine Airlines. On appeal,the CA upheld the decision of the CFI with minor modifications as to thedamages to be awarded. The corresponding writ of execution was dulyreferred to Deputy Sheriff Emilio Z. Reyes for enforcement with checks inthe name of the latter. Four months later, Amelia Tan moved for theissuance of an alias writ of execution since the judgment remainedunsatisfied. The petitioner filed an opposition to the motion for theissuance of an alias writ of execution stating that it had already fully paidits obligation to plaintiff through the deputy sheriff of the respondentcourt, Emilio Z. Reyes, as evidenced by cash vouchers properly signed andreceived by said Emilio Z. Reyes. On March 3,1978, the Court of Appealsdenied the issuance of the alias writ for being premature, ordering theexecuting sheriff Emilio Z. Reyes to appear with his return and explain thereason for his failure to surrender the amounts paid to him by petitionerPAL. However, the order could not be served upon Deputy Sheriff Reyesbecause he already absconded or disappeared. ISSUE: WON the paymentrendered through a check made by PAL to the absconding sheriff in hisname operate to satisfy the judgment debt? HELD: Under ordinarycircumstances, payment by the judgment debtor to the sheriff should bevalid payment to extinguish the judgment debt. There are circumstances,however, which compel a different conclusion such as when the paymentmade by the petitioner to the absconding sheriff was not in cash or legaltender but in checks. The delivery of promissory notes payable to order,or bills of exchange or other mercantile documents shall produce theeffect of payment only when they have been cashed, or when through thefault of the creditor they have been impaired. In the meantime, the action

derived from the original obligation shall be held in abeyance. Since anegotiable instrument is only a substitute for money and not money, thedelivery of such an instrument does not, by itself, operate as payment. Acheck, whether a manager’s check or ordinary check, is not legal tender,and an offer of a check in payment of a debt is not a valid tender ofpayment and may be refused receipt by the obligee or creditor. Meredelivery of checks does not discharge the obligation under a judgment.The obligation is not extinguished and remains suspended until thepayment by commercial document is actually realized (Art. 1249, CivilCode, par. 3). PAL created a situation which permitted the said Sheriff topersonally encash said checks and misappropriate the proceeds thereof tohis exclusive personal benefit. For the prejudice that resulted, thepetitioner himself must bear the fault. As between two innocent persons,one of whom must suffer the consequence of a breach of trust, the onewho made it possible by his act of confidence must bear the loss.

CHARACTERISTICS OF NEGOTIABLE INSTRUMENTS

1. NEGOTIABILITY – is that quality or attribute of a bill or notewhereby it may pass from one person to another similar to money,so as to give the holder in due course the right to collect on theinstrument the sum payable for himself free from any defect in thetitle of any of the prior parties or defenses available to them amongthemselves.

2. ACCUMULATION OF SECONDARY CONTRACTS – as they aretransferred from one person to another. Once an instrument isissued, additional parties can become involved.

E. INCIDENTS IN THE LIFE OF NEGOTIABLE INSTRUMENTS

PROMISSORY NOTE BILL OF EXCHANGE

Preparation & SigningIssuance

Negotiation

Presentment for Acceptanc Acceptance

Dishonor by Non-acceptan

Presentment for payment

Dishonor by Non-payment

Notice of DishonorPayment

Discharge

F. KINDS OF NEGOTIABLE INSTRUMENTS

1. PROMISSORY NOTES (Sec. 184, NIL) – An unconditional pin writing mace by one person to another, signed by the mengaging to pay on demand, or at a fixed or determinable time, a sum certain in money to order or to bearer. a. Parties to a Negotiable Promissory Note are (1) Mak

(2) Payee; b. Kinds of Negotiable Promissory Note include certific

deposits, bank notes, due bills and bonds.

2. BILLS OF EXCHANGE (Sec. 126, 185, NIL) – An uncondorder in writing addressed by one person to another, signed person giving it, requiring the person to whom it is addressed

on demand, or at a fixed or determinable future time, a sum cin money to order or bearer. a. Parties to a Bill of Exchange are (1) Drawer, (2) Pay

(3) Drawee; b. Kinds of Bills of Exchange include drafts, trade accep

and banker’s acceptances.

G. WHEN BILLS TREATED AS NOTES

Sec. 130 When bill may be treated as promissory note. - Win a bill the drawer and drawee are the same person or wthe drawee is a fictitious person or a person not hcapacity to contract, the holder may treat the instrumehis option either as a bill of exchange or as a promissory

Sec. 17(e) Construction where instrument is ambiguous. - Wthe language of the instrument is ambiguous or there

omissions therein, the following rules of construction app

(e) Where the instrument is so ambiguous that there is dwhether it is a bill or note, the holder may treat it as eithhis election;

H. BILLS AND NOTES DISTINGUISHED

PROMISSORY NOTES BILLS OF EXCHANGE

2 parties – Maker and Payee 3 parties – Drawer, Payee Drawee

Maker cannot be the payee Drawer and payee may be the person

There is unconditional PROMISE bythe maker

There is unconditional ORDER bdrawer to the drawee

Presentment for payment withoutprior acceptance

Some Bills need prior acceptanthe drawee before presentmenpayment

Liability of the maker is primary andabsolute

Liability of the drawer is secoand conditional

I. NEGOTIABLE INSTRUMENTS COMPARE WITH OTHER PA(Negotiability vs. Assignability)

SESBRENO VS. CA (GR No. 89252, May 24, 1993) - Petitioner Semade a money market placement in the amount of P300,000 wi

8/20/2019 Negotiable Instruments Law 2031

http://slidepdf.com/reader/full/negotiable-instruments-law-2031 3/47

3Cesar Nickolai F. Soriano Jr. Arellano University School of Law 2011-0303NEGOTIABLE INSTRUMENTS LAW (Act No. 2031) based on the book of Aquino and De Leon and Audio Lecture of Dean Sundiang

Philippine Underwriters Finance Corporation (PhilFinance), with a term of32 days. PhilFinance issued to Sesbreno (1) the Certificate of Confirmationof Sale of a Delta Motor Corporation Promissory Note, (2) the Certificate ofSecurities Delivery Receipt indicating the sale of the note with notationthat said security was in the custody of Pilipinas Bank, and (3) post-datedchecks drawn against the Insular Bank of Asia and America forP304,533.33 payable on March 13, 1981. The checks were dishonored forhaving been drawn against insufficient funds. Pilipinas Bank neverreleased the note, nor any instrument related thereto, to Sesbreno; butSesbreno learned that the Delta Promissory Note maturing on 6 April1981, has a face value of P2,300,833.33 with PhilFinance as payee andDelta Motors as maker; and was stamped “non-negotiable” on its face.PhilFrance was later on placed under the custody of the Securities andExchange Commission. As Sesbreno was unable to collect his investment

and interest thereon, he filed an action for damages against Delta Motorsand Pilipinas Bank. Delta Motors contends that said promissory note wasnot intended to be negotiated or otherwise transferred by Philfinance asmanifested by the word "non-negotiable" stamped across the face of theNote. The trial court and the CA dismissed petitioner’s complaint andappeal, respectively, for lack of cause of action. If anything, petitioner hasa cause of action against Philfrance, which, however, was not impleaded.ISSUE: WON the non-negotiability of a promissory note prevents itsassignment? HELD: No. A negotiable instrument, instead of beingnegotiated, may also be assigned or transferred. The legal consequencesof negotiation and assignment of the instrument are different. A non-negotiable instrument may not be negotiated but may beassigned or transferred, absent an express prohibition againstassignment or transfer written in the face of the instrument. Thesubject promissory note, while marked "non-negotiable," was not at thesame time stamped "non-transferable" or "non-assignable." It containedno stipulation which prohibited Philfinance from assigning or transferringsuch note, in whole or in part.

SOME NON-NEGOTIABLE INSTRUMENTS1. Document of Title – like a certificate of stock, bill of lading and

warehouse receipt (non-negotiable because there is no unconditionalpromise or order to pay a certain sum in money);

2. Letter of Credit – a letter from a merchant or bank or banker inone place, addressed to another, in another place or country,requesting the addressee to pay money or deliver goods to a thirdparty therein named, the writer of the letter undertaking to providehim the money for the goods or to repay him. It is a letter requestingone person to make advances to a third person on the credit of thewriter. (It is in favor of a certain person and not to order)

3. Treasury Warrant - it is a government warrant for the payment of

money such as that issued in favor of a public officer or employeecovering payment or replenishment of cash advances for officialexpenditures. (It is payable out of a specific fund or appropriation)

4. Postal Money Order

PHILIPPINE EDUCATION CO. VS. SORIANO (GR No. L-22405, June30, 1971) - Enrique Montinola sought to purchase from the Manila PostOffice 10 money orders (P200 each), offering to pay for them with aprivate check. Montinola was able to leave the building with his check andthe 10 money orders without the knowledge of the teller. Upon discovery,message was sent to all postmasters and banks involving the unpaidmoney orders. One of the money orders was received by the PhilippineEducation Co. as part of its sales receipt. It was deposited by the companywith the Bank of America, which cleared it with the Bureau of Post. ThePostmaster, through the Chief of the Money Order Division of the ManilaPost Office informed the bank of the irregular issuance of the money

order. The bank debited the account of the company. The companymoved for reconsideration. ISSUE: WON postal money orders arenegotiable instruments? HELD: No. Philippine postal statutes arepatterned from those of the United States, and the weight of authority insaid country is that Postal money orders are not negotiable instrumentsinasmuch as the establishment of a postal money order is an exercise ofgovernmental power for the public’s benefit. Furthermore, some of therestrictions imposed upon money order by postal laws and regulations areinconsistent with the character of negotiable instruments. For instance,postal money orders may be withheld under a variety of circumstances,and which are restricted to not more than one indorsement

II. FORM AND INTERPRETATION OF NEGOTIABLE INSTRUMENT

A. HOW NEGOTIABILITY IS DETERMINED?

CALTEX VS. COURT OF APPEALS (GR No. 97753, Aug. 10, 1Respondent bank issued 280 certificates of time deposit (CTDs) in fa

Angel dela Cruz who delivered the same to herein petitioner in connwith his purchased fuel products. Eventually, dela Cruz executedelivered an Affidavit of Loss for the reissuance of the CTDs. Dellater on obtained a loan from respondent bank and negotiated thCTDs, executing a Deed of Assignment of Time Deposit which samong others, that the bank has full control of the indicated time defrom and after date of the assignment and may set-off such and apsame to the payment of amount or amounts that may be due on th

upon maturity.

Petitioner then went to the Sucat branch for verification of thedeclared lost, alleging that the same were delivered to herein petitio

“security for purchases made with Caltex Philippines, Inc.” and reqthat the CTDs be pre-terminated, which was refused by the respobank due to the failure of petitioner to present requested documeprove such allegation. Petitioner then filed a complaint in the RTC,was dismissed. On appeal, the CA affirmed the decision of the RTCthe present petition. ISSUE: WON the CTDs are considered negoHELD: Yes. A sample text of the certificates of time deposit is reprobelow:

SECURITY BANK

AND TRUST COMPANY

6778 Ayala Ave., Makati No. 90101

Metro Manila, PhilippinesSUCAT OFFICE P4,000.00

CERTIFICATE OF DEPOSIT

Rate 16%

Date of Maturity FEB. 23, 1984 FEB 22, 1982, 19____

This is to Certify that B E A R E R has deposited in this Bank the sum of

PESOS: FOUR THOUSAND ONLY, SECURITY BANK SUCAT OFFI

P4,000 & 00 CTS Pesos, Philippine Currency, repayable to said depositor

days. after date, upon presentation and surrender of this certificate, with i

at the rate of 16% per cent per annum.

(Sgd. Illegible) (Sgd. Illegible)

AUTHORIZED SIGNATURES

Section 1, of Act No. 2031, otherwise known as the NegInstruments Law, enumerates the requisites for an instrument to bnegotiable. The CTDs in question undoubtedly meet the requiremethe law for negotiability. The accepted rule is that the negotiability onegotiability of an instrument is determined from the writing, that is

the fact of the instrument itself. Contrary to what respondent cou(that the CTDs are payable to the “depositor” which is Angel dela the documents provide that the amounts deposited shall be repayathe depositor. And who, according to the document is the depositothe “bearer”. The documents do not say that the depositor is AngCruz and that the amounts deposited are repayable specifically tRather, the amounts are to be repayable to the bearer of the docuor, for that matter, whosoever may be the bearer at the tipresentment.

B. EFFECT OF ESTOPPEL

BANCO DE ORO SAVINGS VS. EQUITABLE BANKING CORP. (74917, Jan. 20, 1988) - Manager's checks (Checks) having an aggamount of P45,982.23 and payable to certain member establishme

Visa Card. Subsequently, the Checks were deposited with the def

(respondent Equitable) to the credit of its depositor (Aida Traccount). Following normal procedures, and after stamping at the bthe Checks the usual endorsements (All prior and/or lack of endorsguaranteed), Equitable sent the checks for clearing through the PhiClearing House Corporation (PCHC). Accordingly, BDO paid the Checclearing account was debited for the value of the Checks and defenclearing account was credited for the same amount. Thereaftediscovered that the endorsements appearing at the back of the Cpurporting to be that of the payees, were forged and/or unauthoriotherwise belong to persons other than the payees. Pursuant to theClearing Rules and Regulations, it presented the Checks direc

8/20/2019 Negotiable Instruments Law 2031

http://slidepdf.com/reader/full/negotiable-instruments-law-2031 4/47

4Cesar Nickolai F. Soriano Jr. Arellano University School of Law 2011-0303NEGOTIABLE INSTRUMENTS LAW (Act No. 2031) based on the book of Aquino and De Leon and Audio Lecture of Dean Sundiang

Equitable for the purpose of claiming reimbursement from the latter.However, Equitable refused to do so. After an exhaustive investigation andhearing, the Arbiter rendered a decision in favor of BDO and againstEquitable ordering the PCHC to debit the clearing account of thedefendant (E), and to credit the clearing account of the plaintiff (B) of theforegoing amount with interest at the rate of 12% per annum from date ofthe complaint. The Board of Directors of the PCHC affirmed the decision ofthe Arbiter. Hence this petition. ISSUE 1: Were the subject checks non-negotiable and if not, does it fall under the ambit of the power of thePCHC? OR Does the PCHC has jurisdiction over the controversy involved inview of petitioner’s claim that the subject matter of the case (the Checks)was not negotiable. HELD: Yes. As provided in the articles ofincorporation of PCHC, its operation extend to "clearing checks and otherclearing items." No doubt transactions on non-negotiable checks are

within the ambit of its jurisdiction. The term check as used in the said Articles of Incorporation of PCHC can only connote checks in general usein commercial and business activities. It cannot be conceived to be limitedto negotiable checks only. Checks are used between banks and bankersand their customers, and are designed to facilitate banking operations. Itis of the essence to be payable on demand, because the contract betweenthe banker and the customer is that the money is needed on demand.Further, the participation of the two banks, petitioner and privaterespondent, in the clearing operations of PCHC is a manifestation of theirsubmission to its jurisdiction. ISSUE 2: How does principle of estoppelapply? HELD: Petitioner is estopped from raising the defense of non-negotiability of the checks in question. It stamped its guarantee on theback of the checks and subsequently presented these checks for clearingand it was on the basis of these endorsements by the petitioner that theproceeds were credited in its clearing account. The principle of estoppeleffectively prevents the defendant from denying liability for any damagessustained by the plaintiff which, relying upon an action or declaration ofthe defendant, paid on the Checks. The same principle of estoppeleffectively prevents the defendant from denying the existence of theChecks. The petitioner by its own acts and representation cannot nowdeny liability because it assumed the liabilities of an endorser by stampingits guarantee at the back of the checks. The petitioner having stamped itsguarantee of "all prior endorsements and/or lack of endorsements" (Exh.

A-2 to F-2) is now estopped from claiming that the checks underconsideration are not negotiable instruments. The checks were acceptedfor deposit by the petitioner stamping thereon its guarantee, in order thatit can clear the said checks with the respondent bank. By such deliberateand positive attitude of the petitioner it has for all legal intents andpurposes treated the said cheeks as negotiable instruments andaccordingly assumed the warranty of the endorser when it stamped itsguarantee of prior endorsements at the back of the checks. It led the said

respondent to believe that it was acting as endorser of the checks and onthe strength of this guarantee said respondent cleared the checks inquestion and credited the account of the petitioner. Petitioner is nowbarred from taking an opposite posture by claiming that the disputedchecks are not negotiable instrument.

PBCOM VS. JOSE ARUEGO (GR No. L-25836-37, Jan. 31, 1981) - Hereinplaintiff instituted against an action against defendant for the recovery ofthe total sum of money plus interests and attorney’s fees. The complaintfiled by the Philippine Bank of Commerce contains twenty-two (22) causesof action referring to twenty-two (22) transactions entered into by the saidBank and Aruego on different dates. The sum sought to be recoveredrepresents the cost of the printing of "World Current Events," a periodicalpublished by the defendant. To facilitate the payment of the printing thedefendant obtained a credit accommodation from the plaintiff. Thus, forevery printing of the "World Current Events," the printer collected the cost

of printing by drawing a draft against the plaintiff, said draft being sentlater to the defendant for acceptance. As an added security for thepayment of the amounts advanced to printer, the plaintiff bank alsorequired defendant Aruego to execute a trust receipt in favor of said bankwherein said defendant undertook to hold in trust for plaintiff theperiodicals and to sell the same with the promise to turn over to theplaintiff the proceeds of the sale of said publication to answer for thepayment of all obligations arising from the draft. Defendant filed ananswer interposing for his defense that he signed the drafts in arepresentative capacity, that he signed only as accommodation party andthat the drafts signed by him were not really bills of exchange but mere

pieces of evidence of indebtedness because payments were made acceptance. ISSUE1: WON the drafts Aruego signed were bexchange? HELD: YES. Under the Negotiable Instruments Law, aexchange is an unconditional order in writing addressed by one peranother, signed by the person giving it, requiring the person to whoaddressed to pay on demand or at a fixed or determinable future sum certain in money to order or to bearer. As long as a commerciaconforms with the definition of a bill of exchange, that paper is consa bill of exchange. The nature of acceptance is important only determination of the kind of liabilities of the parties involved, but the determination of whether a commercial paper is a bill of exchanot. ISSUE2: WON Aruego is personally liable? HELD: YES. FSection 20 of the Negotiable Instruments Law provides that "Wheinstrument contains or a person adds to his signature words ind

that he signs for or on behalf of a principal or in a representative cahe is not liable on the instrument if he was duly authorized; but theaddition of words describing him as an agent or as filing a represencharacter, without disclosing his principal, does not exempt himpersonal liability." An inspection of the drafts accepted by the defeshows that nowhere has he disclosed that he was signing representative of the Philippine Education Foundation Companmerely signed as follows: "JOSE ARUEGO (Acceptor) (SGD)

ARGUEGO For failure to disclose his principal, Aruego is personallyfor the drafts he accepted. Secondly, an accommodation party who has signed the instrument as maker, drawer, indorser, wreceiving value therefor and for the purpose of lending his name toother person. Such person is liable on the instrument to a holder fornotwithstanding such holder, at the time of the taking of the instrknew him to be only an accommodation party. In lending his nameaccommodated party, the accommodation party is in effect a surethe latter. He lends his name to enable the accommodated party tocredit or to raise money. He receives no part of the consideration finstrument but assumes liability to the other parties thereto becawants to accommodate another. In the instant case, the defendant as a drawee/acceptor. Under the Negotiable Instrument Law, a draprimarily liable. Thus, if the defendant who is a lawyer, he shouhave signed as an acceptor/drawee. In doing so, he became primarpersonally liable for the drafts.

C. REQUISITES OF NEGOTIABILITY

Section 1. Form of negotiable instruments. - An instrument negotiable must conform to the following requirements

(a) It must be in writing and signed by the maker or drawer;

(b)

Must contain an unconditional promise or order to pay a sum cermoney;(c) Must be payable on demand, or at a fixed or determinable future ti(d) Must be payable to order or to bearer; and(e) Where the instrument is addressed to a drawee, he must be nam

otherwise indicated therein with reasonable certainty.

(a) It must be in writing and signed by the maker or drawer;

Section 191. Definition and meaning of terms .

“Written ” includes printed, and “writing ” includes print.

Signature of the maker or drawer is usually written, preferably with tname or at least the surname. However, initials or any mark will be sufprovided that such signature be used as a substitute and the maker or d

intends to be bound by it.

Signature is presumed valid , the person denying and to whosignature operates must provide evidence of its invalidity.

(b) Must contain an unconditional promise or order to pay certain in money;

Money is the medium of exchange authorized or adopted by a domeforeign government as part of its currency. In a literal sense, the term

“cash”. It includes all legal tender which has been defined in p.1.

8/20/2019 Negotiable Instruments Law 2031

http://slidepdf.com/reader/full/negotiable-instruments-law-2031 5/47

5Cesar Nickolai F. Soriano Jr. Arellano University School of Law 2011-0303NEGOTIABLE INSTRUMENTS LAW (Act No. 2031) based on the book of Aquino and De Leon and Audio Lecture of Dean Sundiang

1. Promise or Order to Pay

ec. 10 Terms, when sufficient. - The instrument need not follow thelanguage of this Act, but any terms are sufficient which clearlyindicate an intention to conform to the requirements hereof.

lear intention of the parties – the substance of the transaction rather thane form is the criterion of negotiability. Instead of “promise” the words “bindyself” may be used; instead of “on demand”, the words “on call” may be usedd instead of “bearer”, the word “holder” may be used.

ere defect in language or grammatical error – The words “himselfder” may be construed as “himself or order” and thus not render the

strument non-negotiable.

2. Promise or Order to Pay Must be Unconditional

ondition – Resolutory or Suspensive - In conditional obligations, thequisition of rights, as well as the extinguishment or loss of those alreadyquired, shall depend upon the happening of the event which constitutes thendition (Art. 1181, NCC)

eriod – As opposed to a condition, is when the event is certain to happen orme.

3. When is a promise unconditional

romissory Notes :is not essential that the word “promise” be used. Any words equivalent to aomise or assumption of responsibility for the payment of the note (likeayable”, “to be paid”, “I agree to pay”, “I guarantee to pay”, “M obligesmself to pay”, “good for”, “due on demand”, etc.) are sufficient to constitute“promise to pay”.

owever, bare acknowledgements like “IOU”, “Due P1,000” or “for valueceived” do not constitute promise to pay and are non-negotiable, unlessords constituting a promise to pay is added, like “IOU (or Due) P1,000 to beid on Jan. 8”.

ills of Exchange:is not necessary to use the word “order”. Any other words like “Let thearer” or “Drawer obliges the drawee to pay P or order” are sufficient.

n order is a command or imperative direction and, therefore, a mere request,

pplication, or authority (like “I request you to pay”, or “I hope you will pay”“I authorize you to pay”) is not sufficient. However, the use of polite wordse “please” does not convert an order to a request.

ec. 3 When promise is unconditional. - An unqualified order orpromise to pay is unconditional within the meaning of this Actthough coupled with:

(a) An indication of a particular fund out of whichreimbursement is to be made or a particular account to bedebited with the amount; or(b) A statement of the transaction which gives rise to theinstrument.

But an order or promise to pay out of a particular fund is notunconditional.

ec. 39 Conditional indorsement., - see Part III, ConditionalIndorsement, p. 13.

ec. 3 (a): does not render the instrument non-negotiable because thembursement is a subsequent act to the payment, which still makes itsolute. Same is true if there is indication of a particular fund to be “debited”,e “Pay P or order the sum of P10,000 and charge it to my account”, becausere the instrument is payable absolutely, the “debit” of the account is also a

ubsequent act to the payment.

ec. 3, last paragraph : The instrument is deemed non-negotiable because

the payment depends upon the adequacy or existence of the fund desigIt is immaterial, whether the fund has sufficient funds at maturity.

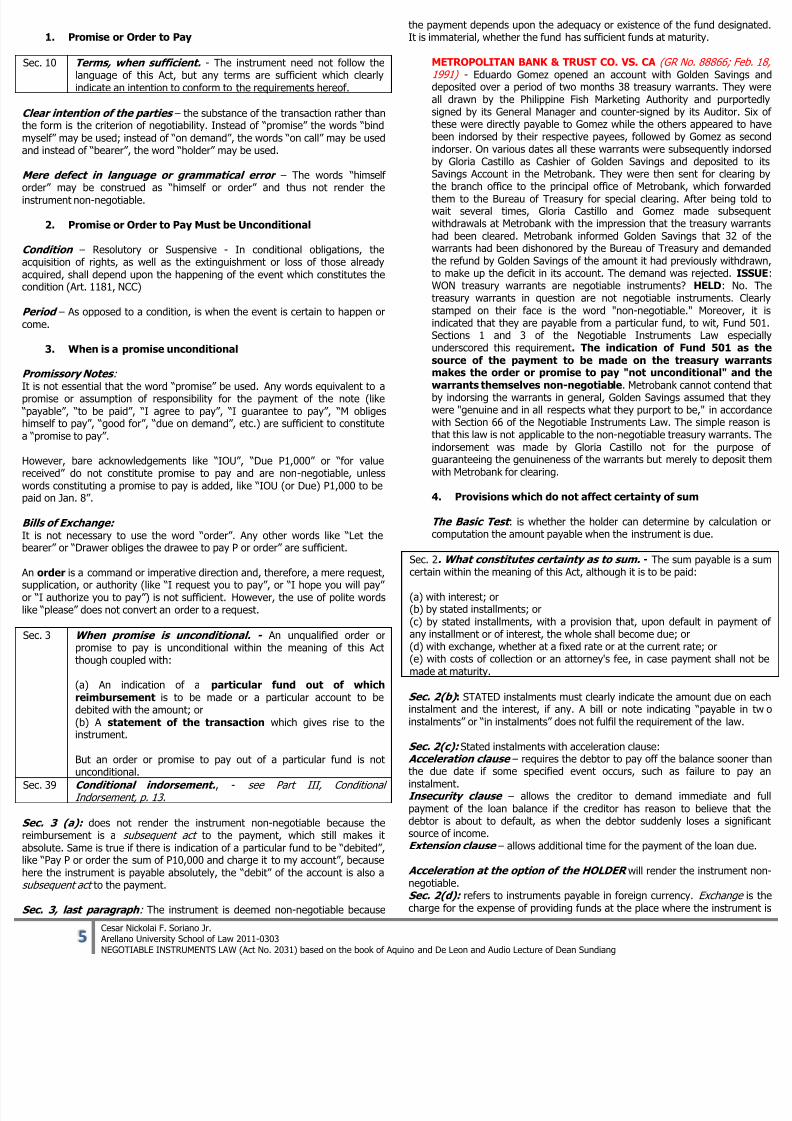

METROPOLITAN BANK & TRUST CO. VS. CA (GR No. 88866; F1991) - Eduardo Gomez opened an account with Golden Savingdeposited over a period of two months 38 treasury warrants. Theyall drawn by the Philippine Fish Marketing Authority and purposigned by its General Manager and counter-signed by its Auditor.these were directly payable to Gomez while the others appeared tbeen indorsed by their respective payees, followed by Gomez as sindorser. On various dates all these warrants were subsequently inby Gloria Castillo as Cashier of Golden Savings and deposited Savings Account in the Metrobank. They were then sent for clearthe branch office to the principal office of Metrobank, which forw

them to the Bureau of Treasury for special clearing. After being wait several times, Gloria Castillo and Gomez made subsewithdrawals at Metrobank with the impression that the treasury wahad been cleared. Metrobank informed Golden Savings that 32 warrants had been dishonored by the Bureau of Treasury and demthe refund by Golden Savings of the amount it had previously withdto make up the deficit in its account. The demand was rejected. IWON treasury warrants are negotiable instruments? HELD: Notreasury warrants in question are not negotiable instruments. Cstamped on their face is the word "non-negotiable." Moreoverindicated that they are payable from a particular fund, to wit, FunSections 1 and 3 of the Negotiable Instruments Law espunderscored this requirement. The indication of Fund 501 asource of the payment to be made on the treasury wamakes the order or promise to pay "not unconditional" anwarrants themselves non-negotiable. Metrobank cannot contenby indorsing the warrants in general, Golden Savings assumed thawere "genuine and in all respects what they purport to be," in accowith Section 66 of the Negotiable Instruments Law. The simple reathat this law is not applicable to the non-negotiable treasury warranindorsement was made by Gloria Castillo not for the purpoguaranteeing the genuineness of the warrants but merely to deposiwith Metrobank for clearing.

4. Provisions which do not affect certainty of sum

The Basic Test : is whether the holder can determine by calculatcomputation the amount payable when the instrument is due.

Sec. 2. What constitutes certainty as to sum. - The sum payable iscertain within the meaning of this Act, although it is to be paid:

(a) with interest; or(b) by stated installments; or(c) by stated installments, with a provision that, upon default in paymany installment or of interest, the whole shall become due; or(d) with exchange, whether at a fixed rate or at the current rate; or(e) with costs of collection or an attorney's fee, in case payment shall made at maturity.

Sec. 2(b) : STATED instalments must clearly indicate the amount due oinstalment and the interest, if any. A bill or note indicating “payable instalments” or “in instalments” does not fulfil the requirement of the law

Sec. 2(c): Stated instalments with acceleration clause: Acceleration clause – requires the debtor to pay off the balance soonethe due date if some specified event occurs, such as failure to p

instalment.Insecurity clause – allows the creditor to demand immediate anpayment of the loan balance if the creditor has reason to believe thdebtor is about to default, as when the debtor suddenly loses a signsource of income.Extension clause – allows additional time for the payment of the loan d

Acceleration at the option of the HOLDER will render the instrumennegotiable.Sec. 2(d): refers to instruments payable in foreign currency. Exchangecharge for the expense of providing funds at the place where the instrum

8/20/2019 Negotiable Instruments Law 2031

http://slidepdf.com/reader/full/negotiable-instruments-law-2031 6/47

6Cesar Nickolai F. Soriano Jr. Arellano University School of Law 2011-0303NEGOTIABLE INSTRUMENTS LAW (Act No. 2031) based on the book of Aquino and De Leon and Audio Lecture of Dean Sundiang

yable to meet the instrument which is issued at another place. It may be at aed rate or at the current rate. Ex. M promises to pay P or order $1,000 “withchange at ¾%” or “at the current rate”.

ec. 2(e): does not affect negotiability because such takes place afteraturity.

ec. 5 Additional provisions not affecting negotiability. - Aninstrument which contains an order or promise to do any act inaddition to the payment of money is not negotiable. But thenegotiable character of an instrument otherwise negotiable is notaffected by a provision which:

(a) authorizes the sale of collateral securities in case the instrument

be not paid at maturity; or(b) authorizes a confession of judgment if the instrument be not paidat maturity; or(c) waives the benefit of any law intended for the advantage orprotection of the obligor; or(d) gives the holder an election to require something to be done inlieu of payment of money.But nothing in this section shall validate any provision or stipulationotherwise illegal.

ec. 6 Omissions; seal; particular money. - The validity and negotiablecharacter of an instrument are not affected by the fact that:

(e) designates a particular kind of current money in which paymentis to be made.

eneral Rule is that, an additional act, aside from payment of money, isohibited. This is based on the fact that while the “payment of money” may bedorsed, the “additional act” would have to be assigned. The following clausesve been held to render non-negotiable the instrument:“pay for taxes assessed upon the note or its mortgage security” (Hubard vs.

obert Wallace Co.);“keep free from encumbrance property on which the value of collateral

edged for security of the instrument depends” (Streckhold vs. National Salto.)“promise to insure the property pledged as security” (First State Savingsnk vs. Russel)

xceptions are:ec. 5(a) : “I promise to pay P or order the sum of P1,000 secured by a ring Ilivered to him by way of pledge and which he could sell should I fail to paym at maturity” – the additional act is to be performed after non-payment at

aturity. Until maturity, the promise is to pay money only.

ec. 5(b) : “I promise to pay P or order P10,000 and I hereby authorize mytorney-at-law to appear in any court of record after the obligation becomese and waive the issuing and service of processes and confess a judgmentainst me in favor of the holder and thereupon waive all errors in any suchoceedings and waive all right of appeal” – confession of judgment is a writtenknowledgment by the defendant of his indebtedness and liability to theaintiff. It enables the holder to obtain a judgment without the delay usuallycident to a lawsuit. While not authorized in this jurisdiction, because itprives the maker or drawer a day in court, it nevertheless does not affectgotiability. A confession of judgment given AFTER the action is brought tove expenses is valid.

ec. 5(c): “Notice of dishonor waived” – even waiver of protest, presentmentr payment, or demand, would not destroy negotiability.

ec. 5(d): “or an airconditioner at the option of the holder” – since the holders the choice, the instrument is still negotiable because he can still demandyment of money. If the option is on the promisor, it would be difficult tompel him to make payment in money.

(c) Payable on demand or at a fixed or determinable future time

me must be certain so that the holder will know when he may enforce thestrument, and the person liable – maker, drawee, or acceptor – when he may

required to pay, or the secondary parties – drawer, indorser or

accommodation party – when his obligation will arise.

Sec. 4. Determinable future time; what constitutes . - An instrumpayable at a determinable future time, within the meaning of this Act, wexpressed to be payable:(a) At a fixed period after date or sight; or(b) On or before a fixed or determinable future time specified therein; or(c) On or at a fixed period after the occurrence of a specified event wcertain to happen, though the time of happening be uncertain.

An instrument payable upon a contingency is not negotiable, anhappening of the event does not cure the defect

Time Instruments

Sec. 4(a): To pay on Aug. 12, 2013;Sec. 4(b): To pay sixty days after date;Sec. 4(c): To pay after P dies.

Sec. 4, last paragraph: refers to a condition which may or may not hapnegotiable instrument must be payable in all events.

Sec. 7. When payable on demand. - An instrument is payabdemand:(a) When it is so expressed to be payable on demand, or at sight, presentation; or(b) In which no time for payment is expressed.

Where an instrument is issued, accepted, or indorsed when overdue, itregards the person so issuing, accepting, or indorsing it, payable on dem

Demand Instruments are those which are payable on demand, dupayable immediately after delivery. It is a present debt due at once.

(d) Payable to order or bearer

Sec. 8 When payable to order . - The instrument is payable towhere it is drawn payable to the order of a specified personhim or his order. It may be drawn payable to the order of:

(a) A payee who is not maker, drawer, or drawee; or(b) The drawer or maker; or(c) The drawee; or(d) Two or more payees jointly; or(e) One or some of several payees; or(f) The holder of an office for the time being.

Where the instrument is payable to order, the payee must be or otherwise indicated therein with reasonable certainty.

Sec. 9 When payable to bearer . - The instrument is payabearer:(a) When it is expressed to be so payable; or(b) When it is payable to a person named therein or bearer; or(c) When it is payable to the order of a fictitious or non-eperson, and such fact was known to the person makingpayable; or(d) When the name of the payee does not purport to be the naany person; or(e) When the only or last indorsement is an indorsement in bla

Payable to Order : when it is payable to the (1) order of a specified per(2) to him or his order. Consequently, an instrument payable to a sp

person (Pay to P), is not a negotiable order instrument.

Sec. 8(b) : An instrument payable to the maker is not complete until indby him. (Sec. 184)Sec. 8(c): Being payable to the drawee, he may pay himself at maturitthe funds of the drawer.Sec. 8(d): Pay to A and B; for Sec. 8(e), Pay to A or B.Sec. 8(f): Pay to the order of the Commissioner of Internal Revenue.

Sec. 8, last paragraph : If there is no payee, there is nobody who couthe order or authority to collect or otherwise indorse and, therefore, ther

8/20/2019 Negotiable Instruments Law 2031

http://slidepdf.com/reader/full/negotiable-instruments-law-2031 7/47

7Cesar Nickolai F. Soriano Jr. Arellano University School of Law 2011-0303NEGOTIABLE INSTRUMENTS LAW (Act No. 2031) based on the book of Aquino and De Leon and Audio Lecture of Dean Sundiang

int in considering it negotiable.

earer Instruments produce the following effect: (a) it is payable to bearer;) payment to any person in possession thereof in good faith and withouttice that his title is defective, at or after maturity (Sec. 88) discharges thestrument (Sec. 119); (c) Delivery alone is enough to effect negotiation (Sec.).

ec. 9(a) and (b) are originally bearer instruments. Those under subsection), (d) and (e) are order instruments on the face converted to bearerstruments.

ec. 9(c): A fictitious person is meant to be one who, though named, asyee, has no right to it because the maker or drawer so intended and it

atters not, whether the name of the payee used by him be that one living orad, or one who never existed. (Snyder vs. Com. Exch. Nat. Bank)

ec. 9(c) and (d): They are treated as bearer instruments because it ispossible to indorse when it is payable to “cash, sundries” or a fictitiousrson.

ANG TEK LIAN VS. CA (GR No. L-2516; Sept. 25, 1950) - Petitioner AngTek Lian approached Lee Hua and asked him if he could give himP4,000.00. He said that he is supposed to withdraw from the bank but hisbank was already closed. In exchange, he gave respondent Lee Hua acheck which is “payable to the order of ‘cash”. When Lee Hua presentedthe check for payment the next day, he discovered that it has aninsufficient funds, hence, was dishonored by the bank. In his defense, AngTek Lian argued that he did not indorse the check to Lee Hua when thelatter accepted the check without his indorsement. ISSUE: WON Ang TekLian’s indorsement of the said check is necessary to hold him liable for thedishonored check? HELD: No. Under Section 9 of the NegotiableInstruments Law, a check drawn payable to the order of “cash” is acheck payable to bearer and the bank may pay it to the personpresenting it for payment without drawer’s indorsement.Consequently, the form of the check was totally unconnected with itsdishonor. The check was returned unsatisfied because the drawer hadinsufficient funds and not because the drawer’s indorsement was lacking .Hence, Ang Tek Lian may be held liable for estafa because under article315, paragraph d, subsection 2 of the Revised Penal Code, one who issuesa check payable to cash to accomplish deceit and knows that at the timehe had no sufficient deposit with the bank to cover the amount of thecheck and without informing the payee of such circumstances is guilty ofestafa.

(e)

Identity of the drawee

Sec. 130. When bill may be treated as promissory note. - Where in abill the drawer and drawee are the same person or where the drawee is aictitious person or a person not having capacity to contract, the holder mayreat the instrument at his option either as a bill of exchange or as a

promissory note

OMISSIONS AND PROVISIONS THAT DO NOT AFFECTNEGOTIABILITY

PNB VS. MANILA OIL REFINING (GR No. L-18103; June 8, 1922) -The manager and treasurer of respondent company executed anddelivered to the Philippine National Bank (PNB), a promissory note whichprovides a promise to pay petitioner bank the amount of P61,000 and thatin case payment was not made at time of maturity, any lawyer in the

Philippines is authorize to represent the company and confess judgmentfor the said sum with interest, cost of suit and attorney's fees of ten% forcollection, a release of all errors and waiver of all rights to inquisition andappeal, and to the benefit of all laws exempting property, real or personal,from levy or sale. Indeed, Manila Oil has failed to pay on demand. Thisprompted the bank to file a case in court, wherein an attorney associatedwith them entered his appearance for the defendant. To this thedefendant objected. ISSUE: WON provisions in notes authorizingattorneys to appear and confess judgments against makers should not berecognized in Philippine jurisdiction by implication? HELD: No. Judgmentsby confession as appeared at common law were considered an amicable,

easy, and cheap way to settle and secure debts. They are quick rserve to save the court's time. They also save time and money litigants and the government the expenses that a long litigation entone sense, instruments of this character may be considered as agreements, with power to enter up judgments on them, bindiparties to the result as they themselves viewed it. On the other handisadvantages to the commercial world which outweigh the conside

just mentioned. Such warrants of attorney are void as against policy, because they enlarge the field for fraud, because undeinstruments the promissor bargains away his right to a day in coubecause the effect of the instrument is to strike down the right of accorded by statute. The recognition of such form of obligation bring about a complete reorganization of commercial custompractices, with reference to short-term obligations. It can readily b

that judgment notes, instead of resulting to the advantage of commlife in the Philippines, might be the source of abuse and oppressiomake the courts involuntary parties thereto. If the bank has a meritcase, the judgment is ultimately certain in the courts. The Court isopinion thus that warrants of attorney to confess judgment aauthorized nor contemplated by Philippine law; and that provisinotes authorizing attorneys to appear and confess judgments amakers should not be recognized in this jurisdiction by implicatioshould only be considered as valid when given express legislative sa

1. OMISSIONS

Sec. 6 Omissions; seal; particular money. - The validity negotiable character of an instrument are not affected byfact that:

(a) it is not dated; or(b) does not specify the value given, or that any value been given therefor; or(c) does not specify the place where it is drawn or the pwhere it is payable; or(d) bears a seal; or(e) designates a particular kind of current money in wpayment is to be made.

But nothing in this section shall alter or repeal any starequiring in certain cases the nature of the consideration tostated in the instrument.

Sec. 11 Date, presumption as to. - Where the instrument oacceptance or any indorsement thereon is dated, such datdeemed prima facie to be the true date of the making, draw

acceptance, or indorsement, as the case may be. Sec. 12 Ante-dated and post-dated. - The instrument is not invfor the reason only that it is ante-dated or post-dated, provthis is not done for an illegal or fraudulent purpose. The peto whom an instrument so dated is delivered acquires the thereto as of the date of delivery.

Sec. 13 When date may be inserted. - Where an instrumentexpressed to be payable at a fixed period after date is issundated , or (2) where the acceptance of an instrument payat a fixed period after sight is undated , any holder may intherein the true date of issue or acceptance, and the instrumshall be payable accordingly. The insertion of a wrong does not avoid the instrument in the hands of a subseqholder in due course; but as to him, the date so inserted be regarded as the true date. (emphasis supplied)

Sec. 14 Blanks; when may be filled. - Where the instrumen

wanting in any material particular, the personpossession thereof has a prima facie authority to complete filling up the blanks therein.

And a signature on a blank paper delivered by the pemaking the signature in order that the paper may be conveinto a negotiable instrument operates as a prima facie authto fill it up as such for any amount.

In order, however, that any such instrument when complmay be enforced against any person who became a p

8/20/2019 Negotiable Instruments Law 2031

http://slidepdf.com/reader/full/negotiable-instruments-law-2031 8/47

8Cesar Nickolai F. Soriano Jr. Arellano University School of Law 2011-0303NEGOTIABLE INSTRUMENTS LAW (Act No. 2031) based on the book of Aquino and De Leon and Audio Lecture of Dean Sundiang

thereto prior to its completion , it must be (1) filled up strictly inaccordance with the authority given and (2) within a reasonabletime.

But if any such instrument, after completion, is negotiated to aholder in due course, it is valid and effectual for all purposesin his hands , and he may enforce it as if it had been filled upstrictly in accordance with the authority given and within areasonable time.

(separation and emphasis supplied)

Sec. 17 Construction where instrument is ambiguous. – see E.Interpretation of Instruments.

Sec. 53 When person not deemed holder in due course. – seeHOLDER IN DUE COURSE, p. 16

Sec. 71 Presentment where instrument is not payable ondemand and where payable on demand. – (1) Where theinstrument is not payable on demand, presentment must bemade on the day it falls due. Where it is payable on demand,presentment must be made within a reasonable time after itsissue, except that in the case of a bill of exchange, presentmentfor payment will be sufficient if made within a reasonable timeafter the last negotiation thereof.

ec. 11: He who claims that some other date is the true date has the burdenestablishing such claim.

ec. 13: If an undated note payable to P matures on Aug. 29, 2013, 30 dayster issuance, but P inserted July 15 to hasten maturity date, P cannot enforce

yment because it is avoided as to him who ante-dated for fraudulentrposes (Sec. 12). But if it was indorsed to A, a holder in due course, he mayllect on Aug. 14, as if the date inserted was the true date.

ec. 14 : Material Particular is any particular proper to be inserted in agotiable instrument to make it complete.

uthority to Complete does not carry with it the authority to alter (Sec.4).

uthority to put any amount – there must be showing of intention toonvert it to a negotiable instrument. Otherwise, it cannot be enforcedainst the maker, even by a holder in due course (Sec. 15).

older NOT in due course of an instrument filled up in excess of thethority given is treated as a holder of a materially altered instrument (Sec.

4) and therefore cannot collect to parties prior to completion who did notsent to the alteration. If M issues a note and authorized P, payee, to insert,000, but P inserts P2,000, N, a subsequent holder NOT in due course cannotforce it against M. But if N was a holder in due course, he can enforce thestrument against M upto the stated amount of P2,000 since it is conclusiveat there was authority to fill up the instrument and the same was not done incess of authority.

2. ADDITIONAL PROVISIONS NOT AFFECTING NEGOTIABILITY – Sec. 5 (supra, p.6)

a. Confession of Judgment – see p.6 a.1 Warrant of attorney – to confess judgment, however, arenot authorized nor contemplated by our law because underthese instruments, the promisor bargains away his right to aday in court. (PNB vs. MANILA OIL REFINING, supra, p.6 )

a.2 Cognovit Actionem – “he has confessed the action” a.3 Relicta Verificationem – “his pleading being abandoned”;a confession of judgment accompanied by a withdrawal of theplea.

b. Waiver of Obligor – Sec. 109. Waiver of notice . - Notice ofdishonor may be waived either before the time of giving notice hasarrived or after the omission to give due notice, and the waiver maybe expressed or implied.

E. INTERPRETATION OF INSTRUMENTS

Sec. 17. Construction where instrument is ambiguous . - Whelanguage of the instrument is ambiguous or there are omissions tthe following rules of construction apply:

(a) Where the sum payable is expressed in words and also in figurethere is a discrepancy between the two, the sum denoted by the wthe sum payable; but if the words are ambiguous or uncertain, refmay be had to the figures to fix the amount;(b) Where the instrument provides for the payment of interest, wspecifying the date from which interest is to run, the interest runthe date of the instrument, and if the instrument is undated, froissue thereof;

(c) Where the instrument is not dated, it will be considered to be daof the time it was issued;(d) Where there is a conflict between the written and printed provisthe instrument, the written provisions prevail;(e) Where the instrument is so ambiguous that there is doubt whetha bill or note, the holder may treat it as either at his election;(f) Where a signature is so placed upon the instrument that it is noin what capacity the person making the same intended to sign, he isdeemed an indorser;(g) Where an instrument containing the word "I promise to pay" is by two or more persons, they are deemed to be jointly and severallthereon.

Sec. 17(d): Reason for this rule is that, the written words are deemexpress the true intention of the maker or drawer because they are there by himself. Also, because the amount in words are harder t(Sundiang, 2010 audio lecture).

Sec. 17(g): Joint and Solidary Obligation

REPUBLIC PLANTERS BANK VS. CA (GR No. 93073; Dec. 21, 1In 1979, World Garment Manufacturing, through its board authShozo Yamaguchi (president) and Fermin Canlas (treasurer) to credit facilities from Republic Planters Bank (RPB). For this, 9 promnotes were executed. Each promissory note was uniformly written following manner:

___________, after date, for value received, I/we, jointly and s

promise to pay to the ORDER of the REPUBLIC PLANTERS BANK, at its Manila, Philippines, the s um of ___________ PESOS(….) Philippine Curr

Please credit proceeds of this note to:

________ Savings Account ______XX Current Account No. 1372-002WORLDWIDE GARMENT MFG. CORP.

Sgd. Shozo YamaguchiSgd. Fermin Canlas

The note became due and no payment was made. RPB eventually Yamaguchi and Canlas. Canlas, in his defense, averred that he shobe held personally liable for such authorized corporate acts thperformed inasmuch as he signed the promissory notes in his capaofficer of the defunct Worldwide Garment Manufacturing. ISSUECanlas should be held liable for the promissory notes? HELD: Yesolidary liability of private respondent Fermin Canlas is made clearcertain, without reason for ambiguity, by the presence of the phraseand several” as describing the unconditional promise to pay to theof Republic Planters Bank. Where an instrument containinwords “I promise to pay” is signed by two or more personsare deemed to be jointly and severally liable thereon . Casolidarily liable on each of the promissory notes bearing his signatuthe following reasons: The promissory notes are negotiable instruand must be governed by the Negotiable Instruments Law. UndNegotiable lnstruments Law, persons who write their names on the promissory notes are makers and are liable as such. By signing thethe maker promises to pay to the order of the payee or any according to the tenor thereof.

8/20/2019 Negotiable Instruments Law 2031

http://slidepdf.com/reader/full/negotiable-instruments-law-2031 9/47

9Cesar Nickolai F. Soriano Jr. Arellano University School of Law 2011-0303NEGOTIABLE INSTRUMENTS LAW (Act No. 2031) based on the book of Aquino and De Leon and Audio Lecture of Dean Sundiang

SPS. EVANGELISTA VS. MERCATER FINANCE CORP. (GR No.148864; Aug. 21, 2003) - Petitioner spouses filed a complaint againstrespondents for the foreclosure of the mortgage on their property andeventual its eventual sale, claiming, among others, that they executed thesaid mortgage on their capacity as officers of Embassy Farms, and not ontheir personal capacity, thus, there is no consideration received by them,making the mortgage voidable. Respondent, on the other hand, claimsthat the promissory note for the loan, for which the mortgage wasexecuted, shows that the spouses signed as co-makers, also with thesucceeding promissory notes. The RTC, upon motion of the respondent,granted summary judgment and dismissed the complaint. On appeal, theCA affirmed in toto the decision of the RTC. ISSUE: WON petitioners aresolidarily liable with Embassy Farms for the loan as evidenced by thepromissory note? HELD: Yes. The promissory note reads:

For value received, I/We jointly and severally promise to pay to the order of MERCATOR FINANCECORPORATION at its office, the principal sum of EIGHT HUNDRED FORTY-FOUR THOUSAND SIXHUNDRED TWENTY-FIVE PESOS & 78/100 (P 844,625.78), Philippine currency, x x x, ininstallments as follows:

September 16, 1982 - P154,267.87

October 16, 1982 - P154,267.87

November 16, 1982 - P154,267.87

December 16, 1982 - P154,267.87

January 16, 1983 - P154,267.87

February 16, 1983 - P154,267.87

The note was signed by petitioners and Embassy Farms, Inc. with thesignature of Eduardo Evangelista below it. Sec. 17 of the NegotiableInstruments Law provide: “Construction where instrument is ambiguous – Where the language of the instrument is ambiguous or there areomissions therein, the following rules of construction shall apply: (g)Where an instrument containing the word “I promise to pay” is signed bytwo or more persons, they are deemed to be jointly and severally liablethereon. As such, the promissory note itself proves that petitionersare solidarily liable with Embassy Farms. Moreover, even ifpetitioners signed merely as officers, it does not erase the factthat they subsequently executed a continuing suretyshipagreement which makes them solidarily liable with the principal.They cannot eventually claim that they did not personably receive anyconsideration for the contract.

I. ISSUE, TRANSFER AND NEGOTIATION

ISSUANCE/DELIVERY OF NEGOTIABLE INSTRUMENTS

c. 15 Incomplete instrument not delivered. - Where an incompleteinstrument has not been delivered, it will not, if completed andnegotiated without authority, be a valid contract in the hands ofany holder, as against any person whose signature was placedthereon before delivery.

c. 16 Delivery; when effectual; when presumed. - Every contract ona negotiable instrument is incomplete and revocable untildelivery of the instrument for the purpose of giving effect thereto.

As between immediate parties and as regards a remote party otherthan a holder in due course, the delivery, in order to be effectual,must be made either by or under the authority of the party making,drawing, accepting, or indorsing, as the case may be; and, in suchcase, the delivery may be shown to have been conditional, or for a

special purpose only, and not for the purpose of transferring theproperty in the instrument. But where the instrument is in thehands of a holder in due course, a valid delivery thereof by allparties prior to him so as to make them liable to him is conclusivelypresumed. And where the instrument is no longer in the possessionof a party whose signature appears thereon, a valid and intentionaldelivery by him is presumed until the contrary is proved.

c. 191 Definition and meaning of terms . - In this Act, unless thecontract otherwise requires:

" Delivery " means transfer of possession, actual or constructive,

from one person to another;

" Issue " means the first delivery of the instrument, compform, to a person who takes it as a holder

Section 15 : Example: M makes a note for P10,000 with the name payee in blank and keeps it in his drawer. P steals the note, names himthe payee and indorses the note to A, A to B, B to C, a holder in due cour

NOTE: C, even though a holder in due course, cannot enforce said note aM by virtue of Sec. 15, but C can go after P, A and B.

Section 16 : As regards immediate parties and a remote party other holder in due course, delivery is a rebuttable presumption, as such can

be conditional or for a special purpose (without intention of transferring t

As regards a holder in due course, valid delivery, of a complete instrumopposed to an incomplete instrument under Sec. 15), by all parties prior is conclusively presumed (admission of evidence to the contrary is not allo

B. NEGOTIATION DEFINED

Sec. 30. What constitutes negotiation. - An instrument is negotiatedit is transferred from one person to another in such manner as to constittransferee the holder thereof . If payable to bearer, it is negotiated by deif payable to order, it is negotiated by the indorsement of the holdecompleted by delivery. (emphasis supplied)

1. Instruments payable to order: two steps are required for negot

(a) indorsement and (b) delivery.2. Instruments payable to bearer: delivery alone without indorsem

C. ASSIGNMENT AND NEGOTIATION DISTINGUISHED

Assignment is the transfer of the title to an instrument, with the asgenerally taking only such title or rights as his assignor has, subjectdefenses available against his assignor. It is the less usual method whicor may not involve an indorsement in the sense of writing on the back instrument.

NEGOTIATION ASSIGNMENT

ApplicableLaw

Negotiable Instruments Law Civil Code of the Philipp

Type oftransaction

orinstrument:

Negotiable instruments only Contracts in generaassignable rights

Nature ofthetransferee:

Transferee is a holder who maybe a holder in due course

Transferee is a assignee and can neverholder in due course

Rightsacquired:

The transferee-holder mayacquire more rights than thetransferor if he is a holder indue course

Transferee cannot acmore rights than transferor because he msteps into the shoes otransferor

Availabilityof personaldefenses

Transferee-holder may be freefrom personal defenses if he isa holder in due course

Transferee is always suto personal defenses

CASABUENA VS. COURT OF APPEALS (GR No. 115410; Feb. 27,- Ciriaco Urdaneta was a grantee of a parcel of land purchased by t

of Manila and conveyed to its less privileged inhabitants, through ireform program. Subsequently, he assigned his rights and interestsof the lot to Arsenia Benin covering full payment of his indebtednessamount of P500. A deed of sale with mortgage was executedUrdaneta undertaking to pay the City the amount figured for a peforty years in 480 equal installments. Another deeassignment involving the whole lot, with assignee Benin agreeshoulder all obligations including the payment of amortization to thin accordance with the contract between it and Urdaneta. As statheir verbal agreement, Urdaneta could redeem the property

8/20/2019 Negotiable Instruments Law 2031

http://slidepdf.com/reader/full/negotiable-instruments-law-2031 10/47

10Cesar Nickolai F. Soriano Jr. Arellano University School of Law 2011-0303NEGOTIABLE INSTRUMENTS LAW (Act No. 2031) based on the book of Aquino and De Leon and Audio Lecture of Dean Sundiang

payment of the loan within 3yrs. from the date of assignment; failure topay would transfer physical possession of the lot to Benin for a period of15 years, without actual transfer of title and ownership thereto.Meanwhile, the administration of the property was assigned to brothersCandido and Juan Casabuena, to whom Benin had transferred her right,title and interest for a consideration of P7,500. Notwithstanding thisassignment, Benin constructed a duplex (apartment) on the lot separatelyoccupied by Jose Abejero and Juan Casabuena, who collected rentals fromthe former. After the lot was fully paid for by the Urdanetas, a Release ofMortgage was executed and period of non-alienation of the land wasextended from 5 to 20 years. Casabuena was Benin's rental collector buttheir relationship soured resulting in a litigation involving issue onownership, of which the cause was the latter’s failure to pay rentals. Uponlearning of the litigation between petitioner and Benin, Urdaneta asked

them to vacate the property and surrender to him possession thereofwithin 15 days from notice. Petitioner's adamant refusal to comply withsuch demand resulted in a complaint for ejectment and recovery ofpossession of property filed by Urdaneta against Casabuena and Benin.

Amid the sprouting controversies involving the lot, the Urdaneta spousessucceeded in having the Court declare them as its true and lawful ownerswith the deed of assignment to Benin merely serving as evidence ofCiriaco's indebtedness to her in view of the prohibition against the sale ofthe land imposed by the City government. ISSUE: WON a deed ofassignment can transfer ownership of the property to the assignee?HELD: At the bottom of this controversy is the undisputed fact thatCiriaco Urdaneta was indebted to Benin, to secure which debt the spousesceded their rights over the land through a deed of assignment. Anassignment of credit is an agreement by virtue of which theowner of a credit, known as the assignor, by a legal cause,transfers his credit and its accessory rights to another, known asthe assignee, who acquires the power to enforce it to the sameextent as the assignor could have enforced it against thedebtor. Stated simply, it is the process of transferring the right ofthe assignor to the assignee, who would then be allowed toproceed against the debtor. The assignment involves no transferof ownership but merely effects the transfer rights which theassignor has at the time, to the assignee. Benin having been deemedsubrogated to the rights and obligations of the spouses, she was bound byexactly the same conditions to which the latter were bound. This being so,she and the Casabuenas were bound to respect the prohibition againstselling the property within the five-year period imposed by the Citygovernment. The act of assignment could not have operated to effaceliens or restrictions burdening the right assigned, because an assigneecannot acquire a greater right than that pertaining to the assignor. Atmost, an assignee can only acquire rights duplicating those which his

assignor is entitled by law to exercise. In the case at bar, the Casabuenasmerely stepped into Benin's shoes, who was not so much an owner as amere assignee of the rights of her debtors. Not having acquired any rightover the land in question, it follows that Benin conveyed nothing todefendants with respect to the property.

Art. 348, Code of Commerce. The conveyer shall answer for thelegality of the credit and for the capacity in which he made the transfer;but he shall not answer for the solvency of the debtor, unless there is anexpress agreement requiring him to do so

HOW ARE NEGOTIABLE INSTRUMENTS AND NON-NEGOTIABLEINSTRUMENTS TRANSFERRED?

SESBRENO VS. COURT OF APPEALS (supra, p.3)

CONSOLIDATED PLYWOOD INDUSTRIES, INC. VS. IFC LEASING(GR No. 72593; April 30, 1987) - Consolidated Plywood Industries, Inc.(CPII) needed two tractors for its logging business. Atlantic Gulf & PacificCompany through its sister company Industrial Products Marketing (IPM)offered to sell two “used" tractors. IPM inspected the job site and assuredthat the tractors were fit for the job and gave a 90-day warranty formachine performance and availability of parts. CPII officers Wee and

Vergara purchased the tractors on installment and paid the downpayment. The deed of sale with chattel mortgage with promissory noteand the deed of assignment, where IPM assigned its rights and interest inthe chattel mortgage in favor of IFC Leasing and Acceptance Corp., were

all executed on the same day by and among the parties. Barely 1after delivery, the tractors broke down. Mechanics were sent to do but the tractors were no longer serviceable. CPII logging operationdelayed so Vergara advised IPM that the installment payments likewise be delayed until it fulfills its obligation under its warrantthen filed a collection suit against petitioners for the recovery principal sum plus interest, attorney's fees and costs of suit contthat it was a holder in due course of a negotiable promissoryISSUE: WON IFC is a holder in due course of a negotiable promnote so as to bar all defenses of CPII against IPM? HELD: No. The question fails to meet the requirement under Sec. 1(d) of Act No.IFC is not and will never be a holder in due course of the promissorbut is merely an assignee. The note in question is not a neginstrument for lack of the so-called words of negotiability. The

assignor IPM is liable for breach of warranty and such liability as a grule extends to the corporation (IFC) to whom it assigned its righinterests. Even assuming that the note is negotiable, IFC which aparticipated in the sale on installment transaction from its inception be regarded as a holder in due course. Thus, petitioners may raise athe respondent all defenses available to it as against the seller-assIPM.

TRADERS ROYAL BANK VS. COURT OF APPEALS (GR No. Mar. 3, 1997) - Assailed in this Petition is the Decision of the Co

Appeals affirming the nullity of the transfer of Central Bank CertificIndebtedness (CBC), with a face value of P500,000 from PhiUnderwriters Finance Corporation (Philfinance) - without authorizatipetitioner Traders Royal Bank. ISSUE: WON Central Bank CertificIndebtedness (CBCI) is a negotiable instrument? HELD: Noinstrument provides for a promise to pay the registered owner F

Very clearly, the instrument was only payable to Filriters. It lackwords of negotiability which should have served as an expression consent that the instrument may be transferred by negotiationlanguage of negotiability which characterizes a negotiable papecredit instrument is its freedom to circulate as a substitute for mHence, freedom of negotiability is the touchstone relating to the proof holders in due course, and the freedom of negotiability foundation for the protection, which the law throws around a hodue course. This freedom in negotiability is totally absent in a certifiindebtedness as it merely acknowledges to pay a sum of monespecified person or entity for a period of time. The transfer instrument from Philfinance to TRB was merely an assignment, andgoverned by the negotiable instruments law. The pertinent questiois —was the transfer of the CBCI from Filriters to Philfinancsubsequently from Philfinance to TRB, in accord

existing law, so as to entitle TRB to have the CBCI registered in itswith the Central Bank? Clearly shown in the record is the facPhilfinance’s title over CBCI is defective since it acquired the instrfrom Filriters fictitiously. Although the deed of assignment stated thtransfer was for ‘value received‘, there was really no consideinvolved. What happened was Philfinance merely borrowed CBCFilriters, a sister corporation. Thus, for lack of any consideratioassignment made is a complete nullity. Furthermore, the transfer waconformity with the regulations set by the CB. Giving more crederule that there was no valid transfer or assignment to petitioner.

E. HOW NEGOTIATION TAKES PLACE

Sec. 30 What constitutes negotiation. (supra, p. 9)

Sec. 40 Indorsement of instrument payable to bearer. - Whinstrument, payable to bearer, is indorsed specially, it

nevertheless be further negotiated by delivery; but the indorsing specially is liable as indorser to only such holders astitle through his indorsement.