narrative reporting (part 3) s172 and beyond

TRANSCRIPT

© ICAEW 2020

ICAEW KNOW-HOW

FINANCIAL REPORTING FACULTY

Narrative reporting (part 3) – s172 and beyond

This webinar will commence shortly ……

22 OCTOBER 2020

Introduction

Olivia Cox

Technical Strategy Department

ICAEW

© ICAEW 2020

Today’s presenters

Vicki Tibbitts

Senior Manager

Deloitte

Elaine Forrest

Senior Manager

PwC

© ICAEW 2020

Customise your screen

• You can customise the webinar console by moving and resizing the widgets

• You can also minimise and maximise the widgets by clicking on the icons

located in the dock at the bottom of the console

© ICAEW 2020

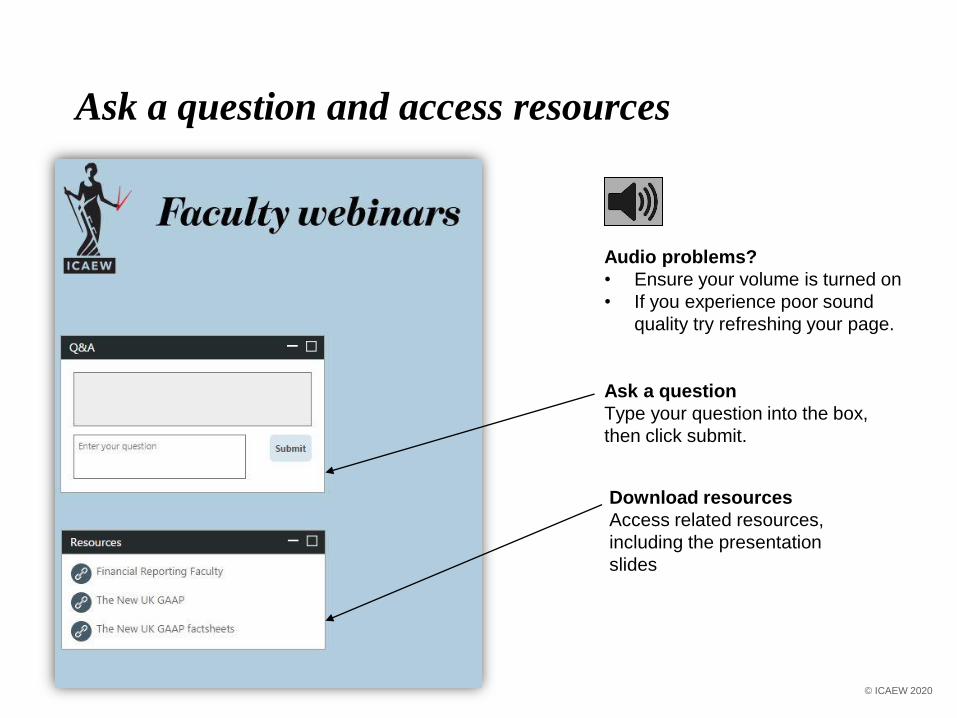

Ask a question and access resources

VAT Changes in 2015

Audio problems?

• Ensure your volume is turned on

• If you experience poor sound

quality try refreshing your page.

Ask a question

Type your question into the box,

then click submit.

Download resources

Access related resources,

including the presentation

slides

© ICAEW 2020

Contents

Reminder of the requirements

Year 1 reflections

Private companies and subsidiaries

Tips for year 2

Other narrative reporting developments

Resources

Questions

© ICAEW 2020

VAT Changes in 2015

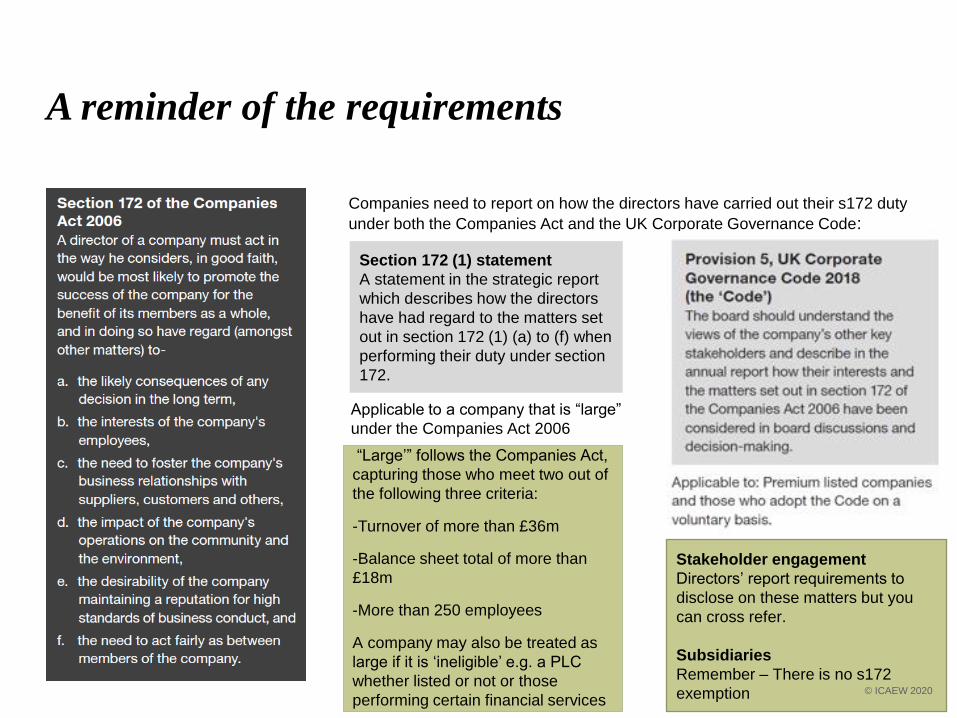

A reminder of the requirements

“Large’” follows the Companies Act,

capturing those who meet two out of

the following three criteria:

-Turnover of more than £36m

-Balance sheet total of more than

£18m

-More than 250 employees

A company may also be treated as

large if it is ‘ineligible’ e.g. a PLC

whether listed or not or those

performing certain financial services

Companies need to report on how the directors have carried out their s172 duty

under both the Companies Act and the UK Corporate Governance Code:

Section 172 (1) statement

A statement in the strategic report

which describes how the directors

have had regard to the matters set

out in section 172 (1) (a) to (f) when

performing their duty under section

172.

Applicable to a company that is “large”

under the Companies Act 2006

Stakeholder engagement

Directors’ report requirements to

disclose on these matters but you

can cross refer.

Subsidiaries

Remember – There is no s172

exemption © ICAEW 2020

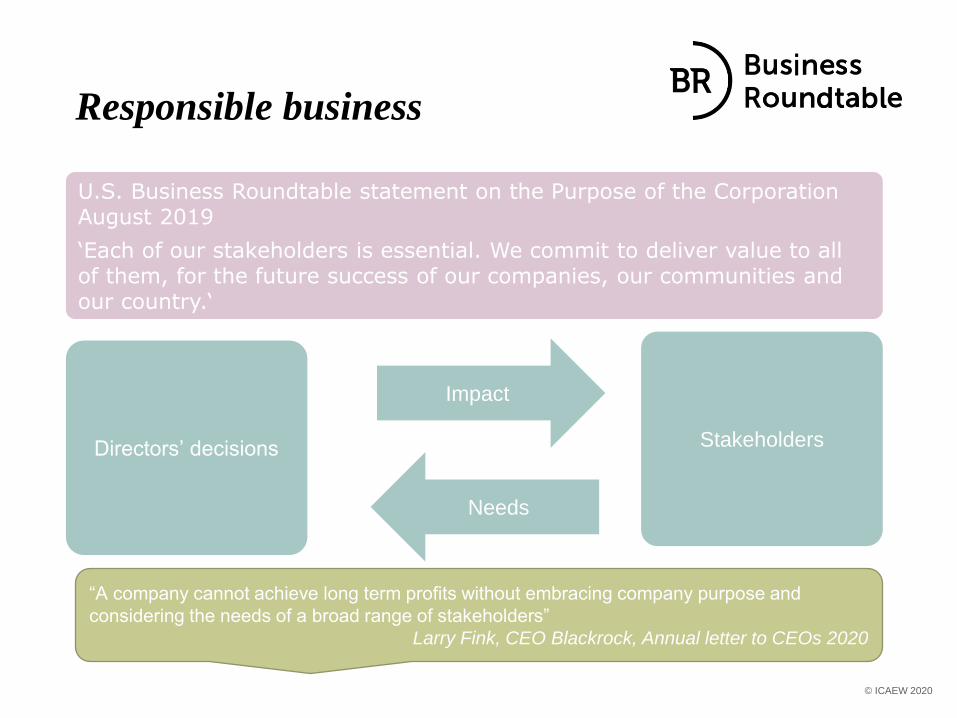

Responsible business

© ICAEW 2020

Impact

Directors’ decisions Stakeholders

Needs

U.S. Business Roundtable statement on the Purpose of the Corporation August 2019

‘Each of our stakeholders is essential. We commit to deliver value to all of them, for the future success of our companies, our communities and our country.‘

“A company cannot achieve long term profits without embracing company purpose and

considering the needs of a broad range of stakeholders”

Larry Fink, CEO Blackrock, Annual letter to CEOs 2020

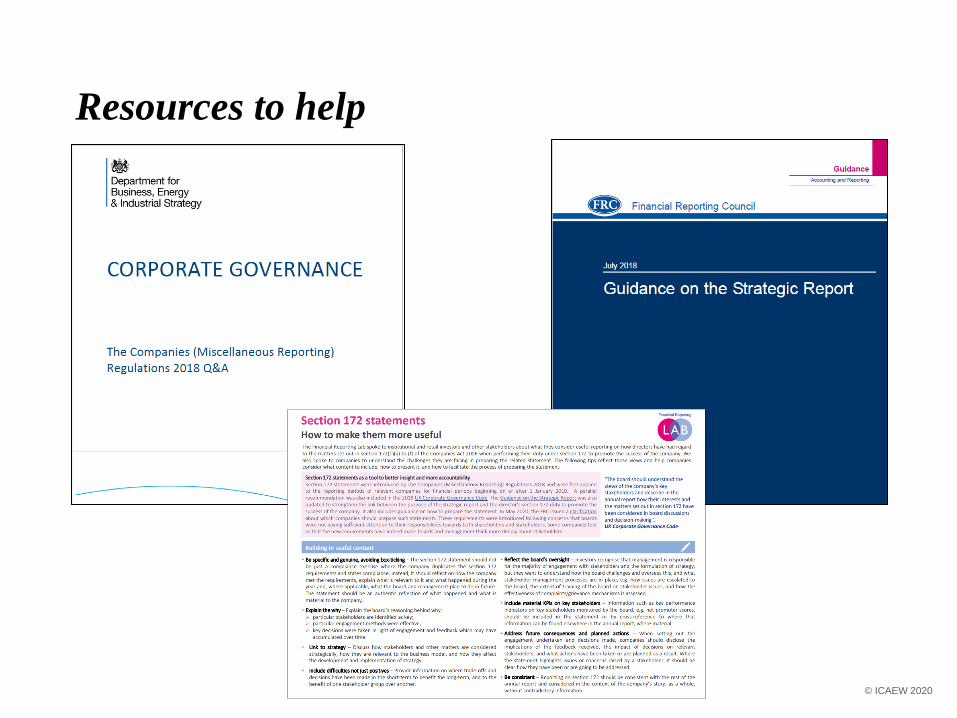

Resources to help

© ICAEW 2020

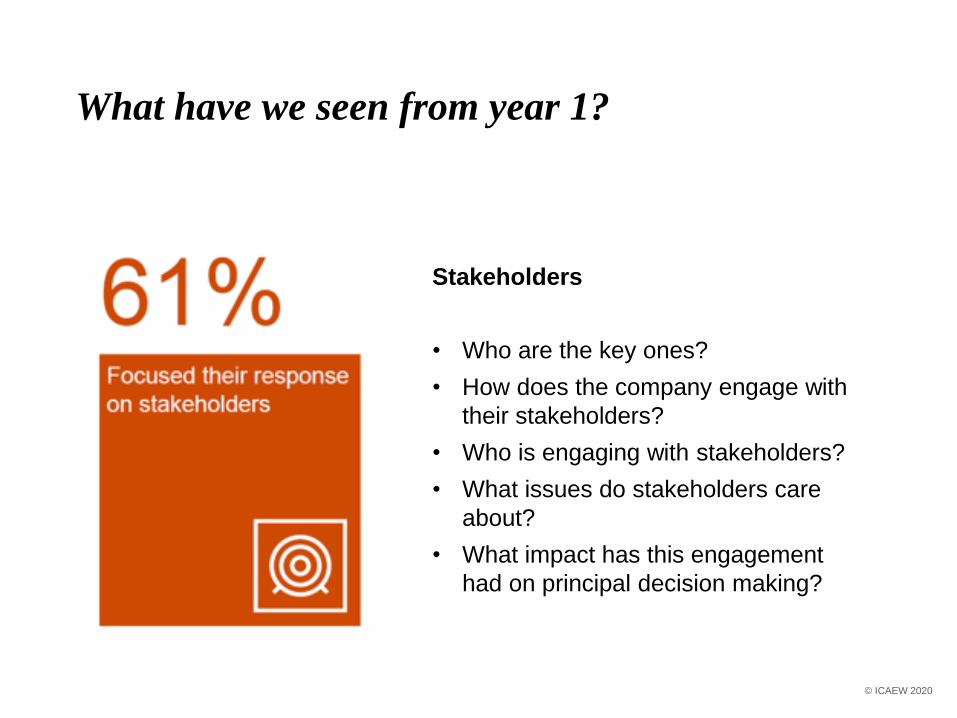

What have we seen from year 1?

© ICAEW 2020

Stakeholders

• Who are the key ones?

• How does the company engage with

their stakeholders?

• Who is engaging with stakeholders?

• What issues do stakeholders care

about?

• What impact has this engagement

had on principal decision making?

Example of stakeholder engagement

© ICAEW 2020

Serco

Annual Report &

Accounts 2019

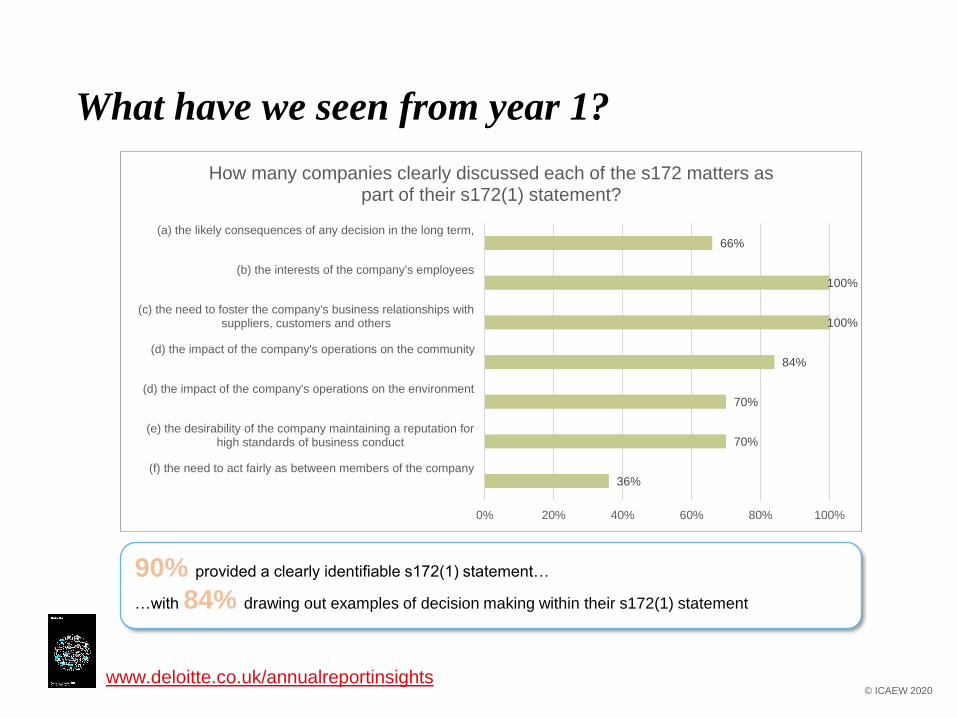

What have we seen from year 1?

© ICAEW 2020

90% provided a clearly identifiable s172(1) statement…

…with 84% drawing out examples of decision making within their s172(1) statement

36%

70%

70%

84%

100%

100%

66%

0% 20% 40% 60% 80% 100%

(f) the need to act fairly as between members of the company

(e) the desirability of the company maintaining a reputation forhigh standards of business conduct

(d) the impact of the company's operations on the environment

(d) the impact of the company's operations on the community

(c) the need to foster the company's business relationships withsuppliers, customers and others

(b) the interests of the company's employees

(a) the likely consequences of any decision in the long term,

How many companies clearly discussed each of the s172 matters as part of their s172(1) statement?

www.deloitte.co.uk/annualreportinsights

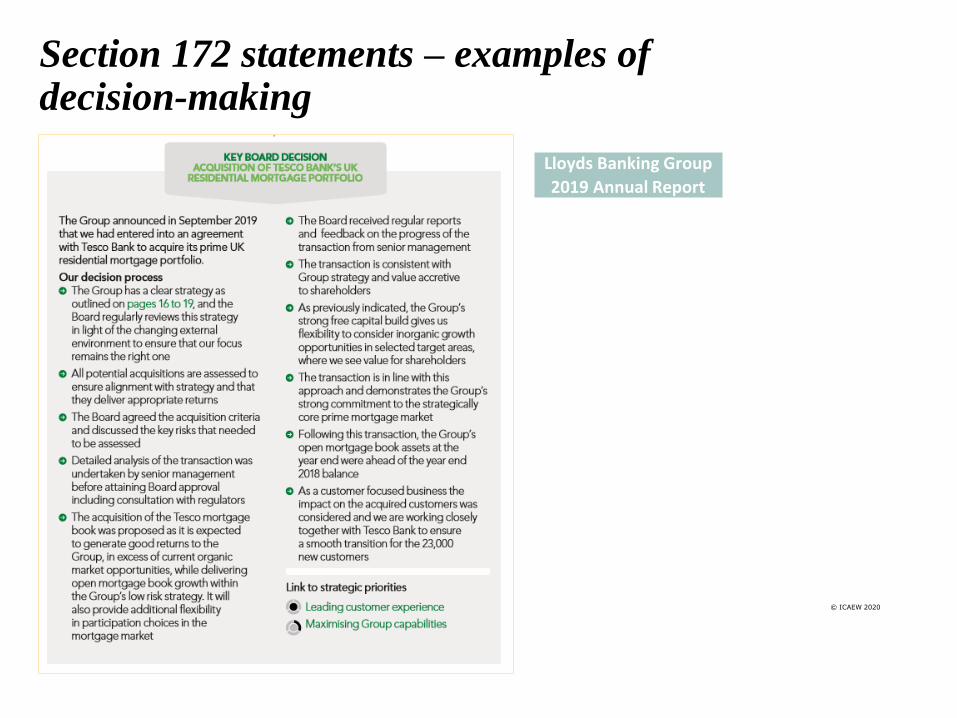

Section 172 statements – examples of decision-making

© ICAEW 2020

Lloyds Banking Group

2019 Annual Report

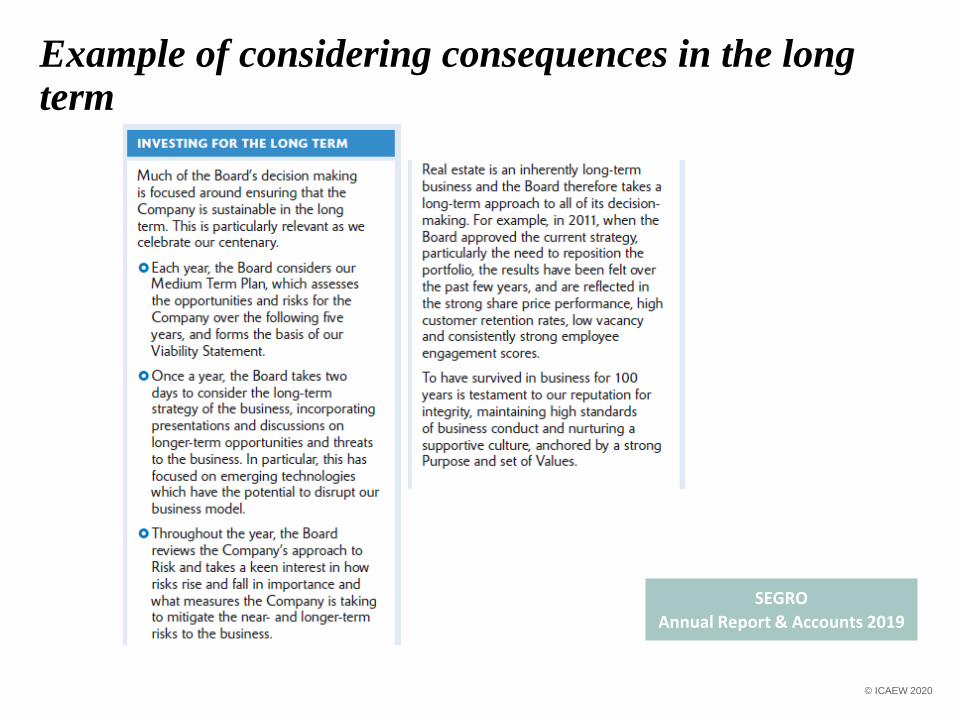

Example of considering consequences in the long term

SEGRO

Annual Report & Accounts 2019

© ICAEW 2020

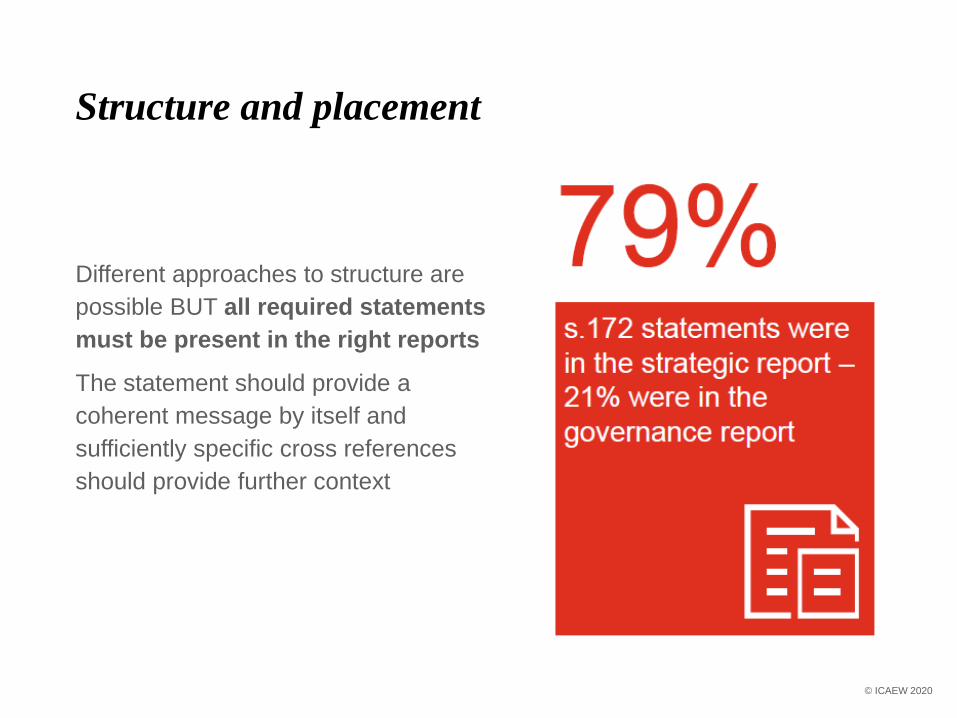

Structure and placement

Different approaches to structure are

possible BUT all required statements

must be present in the right reports

The statement should provide a

coherent message by itself and

sufficiently specific cross references

should provide further context

© ICAEW 2020

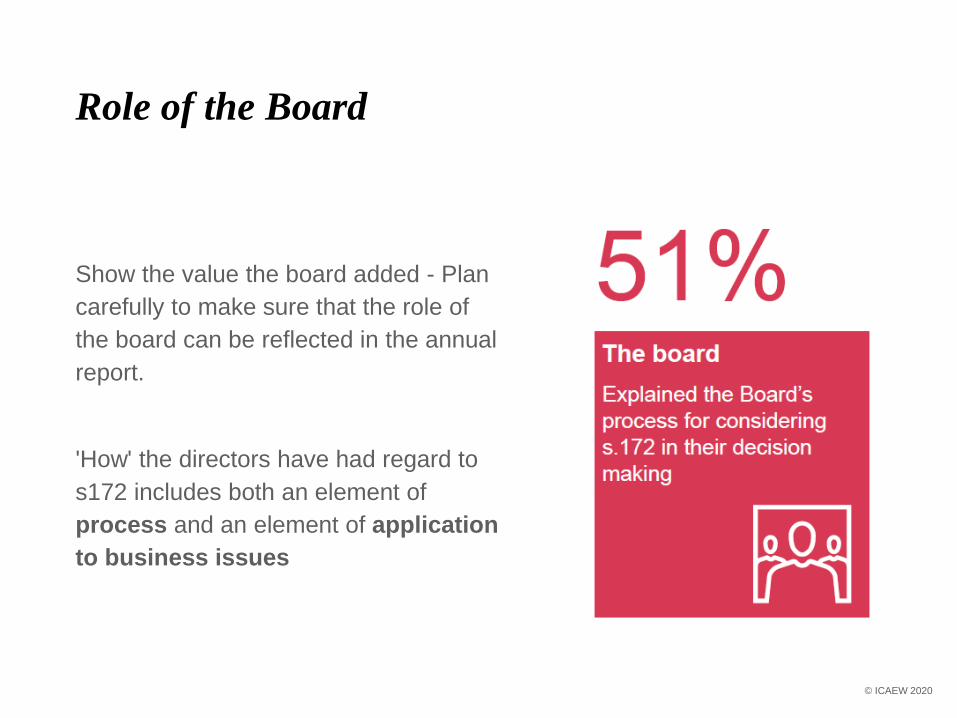

Role of the Board

Show the value the board added - Plan

carefully to make sure that the role of

the board can be reflected in the annual

report.

'How' the directors have had regard to

s172 includes both an element of

process and an element of application

to business issues

© ICAEW 2020

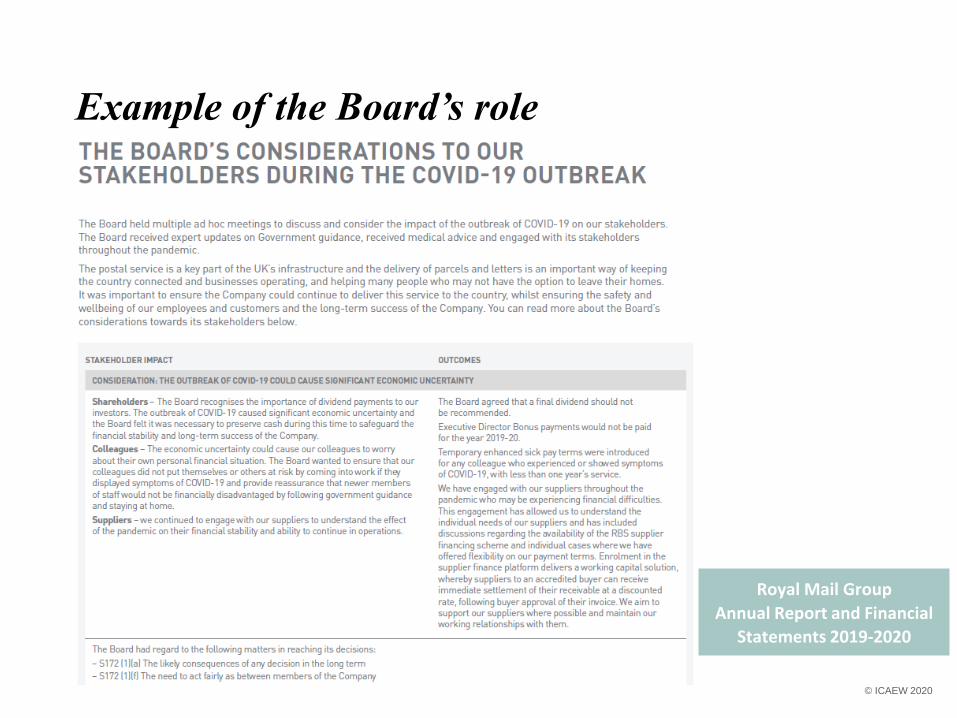

Example of the Board’s role

© ICAEW 2020

Royal Mail Group

Annual Report and Financial

Statements 2019-2020

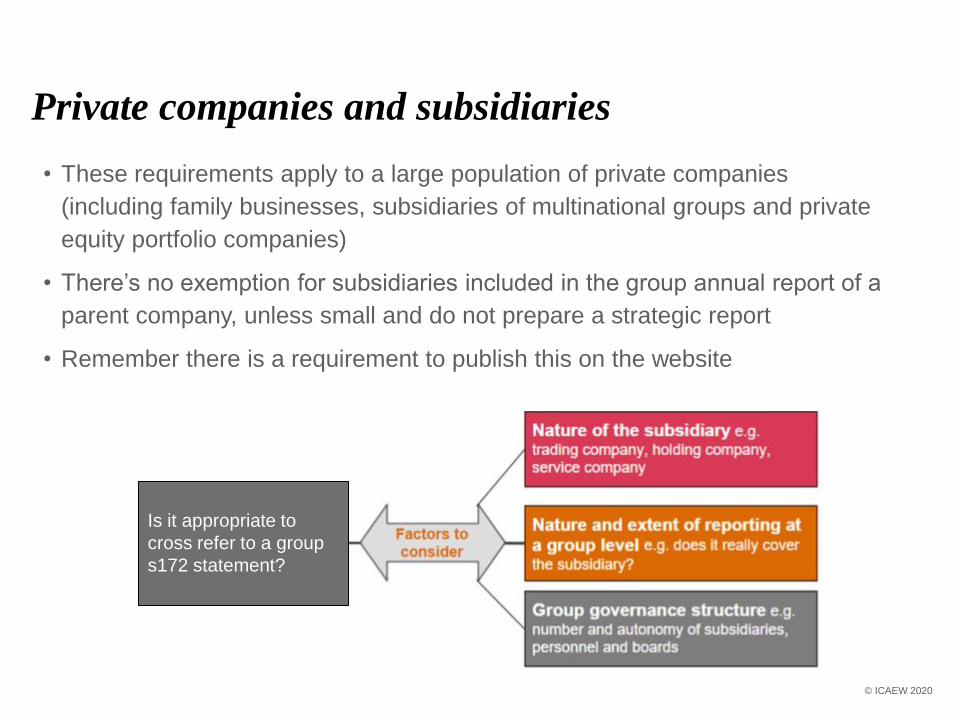

Private companies and subsidiaries

VAT Changes in 2015

• These requirements apply to a large population of private companies

(including family businesses, subsidiaries of multinational groups and private

equity portfolio companies)

• There’s no exemption for subsidiaries included in the group annual report of a

parent company, unless small and do not prepare a strategic report

• Remember there is a requirement to publish this on the website

Is it appropriate to

cross refer to a group

s172 statement?

© ICAEW 2020

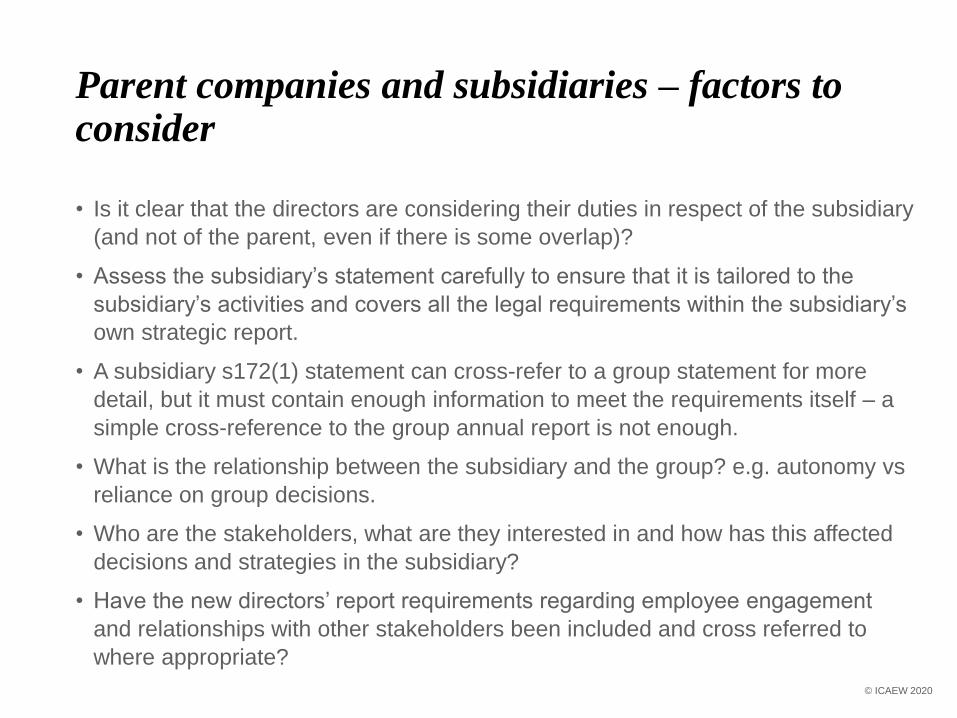

Parent companies and subsidiaries – factors to consider

• Is it clear that the directors are considering their duties in respect of the subsidiary

(and not of the parent, even if there is some overlap)?

• Assess the subsidiary’s statement carefully to ensure that it is tailored to the

subsidiary’s activities and covers all the legal requirements within the subsidiary’s

own strategic report.

• A subsidiary s172(1) statement can cross-refer to a group statement for more

detail, but it must contain enough information to meet the requirements itself – a

simple cross-reference to the group annual report is not enough.

• What is the relationship between the subsidiary and the group? e.g. autonomy vs

reliance on group decisions.

• Who are the stakeholders, what are they interested in and how has this affected

decisions and strategies in the subsidiary?

• Have the new directors’ report requirements regarding employee engagement

and relationships with other stakeholders been included and cross referred to

where appropriate?

© ICAEW 2020

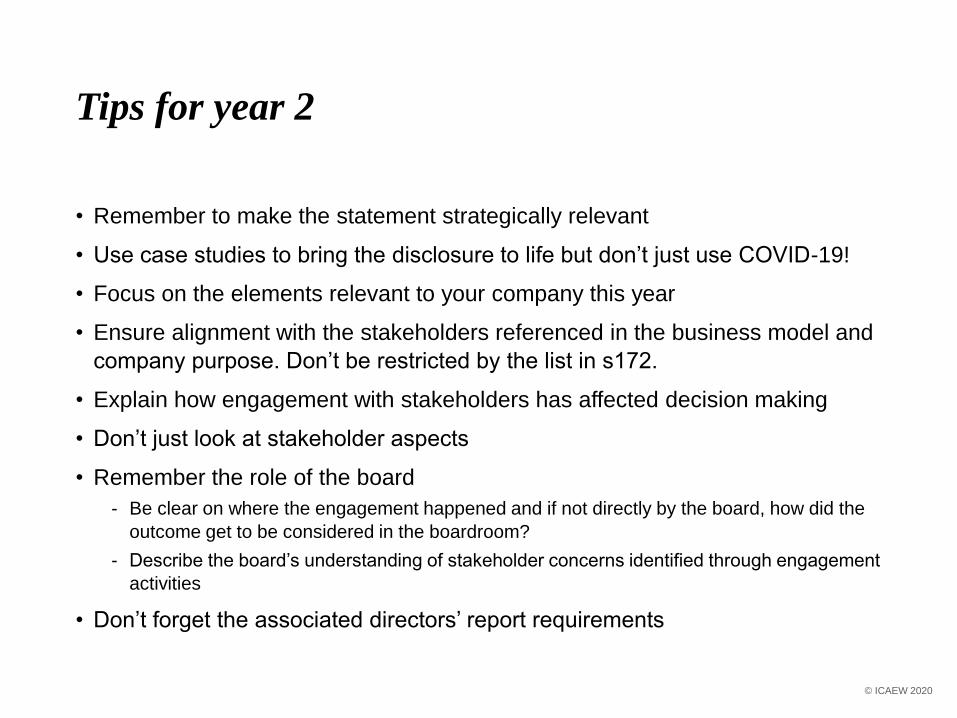

Tips for year 2

• Remember to make the statement strategically relevant

• Use case studies to bring the disclosure to life but don’t just use COVID-19!

• Focus on the elements relevant to your company this year

• Ensure alignment with the stakeholders referenced in the business model and

company purpose. Don’t be restricted by the list in s172.

• Explain how engagement with stakeholders has affected decision making

• Don’t just look at stakeholder aspects

• Remember the role of the board

- Be clear on where the engagement happened and if not directly by the board, how did the

outcome get to be considered in the boardroom?

- Describe the board’s understanding of stakeholder concerns identified through engagement

activities

• Don’t forget the associated directors’ report requirements

© ICAEW 2020

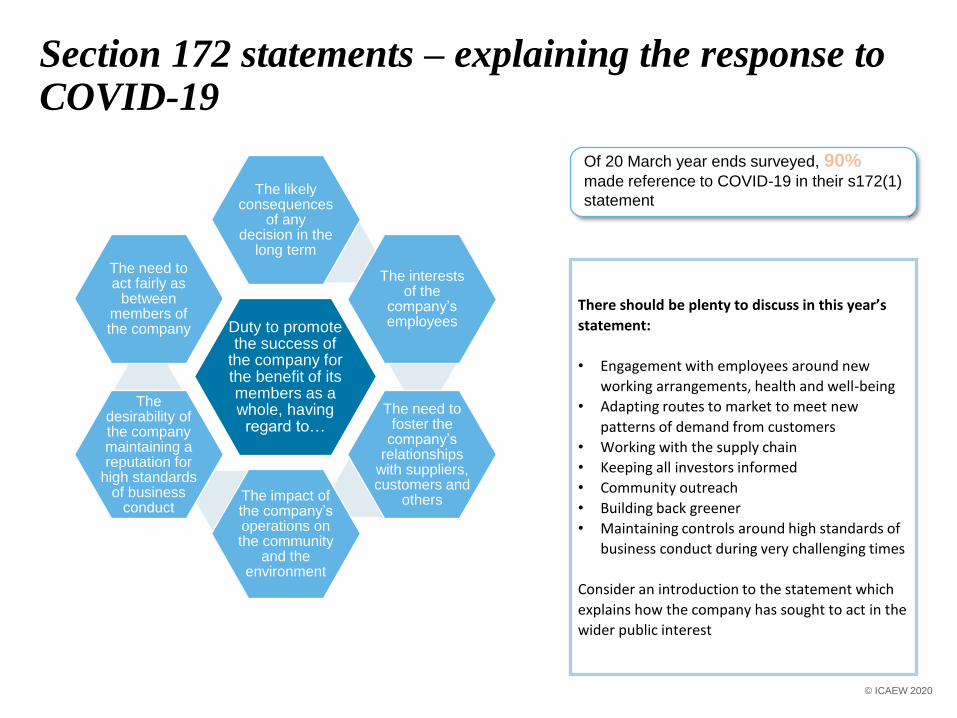

Section 172 statements – explaining the response to COVID-19

Duty to promote the success of

the company for the benefit of its members as a whole, having regard to…

The likely consequences

of any decision in the

long term

The interests of the

company’s employees

The need to foster the

company’s relationships

with suppliers, customers and

othersThe impact of the company’s operations on the community

and the environment

The desirability of the company maintaining a reputation for

high standards of business

conduct

The need to act fairly as

between members of the company

There should be plenty to discuss in this year’s

statement:

• Engagement with employees around new

working arrangements, health and well-being

• Adapting routes to market to meet new

patterns of demand from customers

• Working with the supply chain

• Keeping all investors informed

• Community outreach

• Building back greener

• Maintaining controls around high standards of

business conduct during very challenging times

Consider an introduction to the statement which

explains how the company has sought to act in the

wider public interest

Of 20 March year ends surveyed, 90% made reference to COVID-19 in their s172(1)

statement

© ICAEW 2020

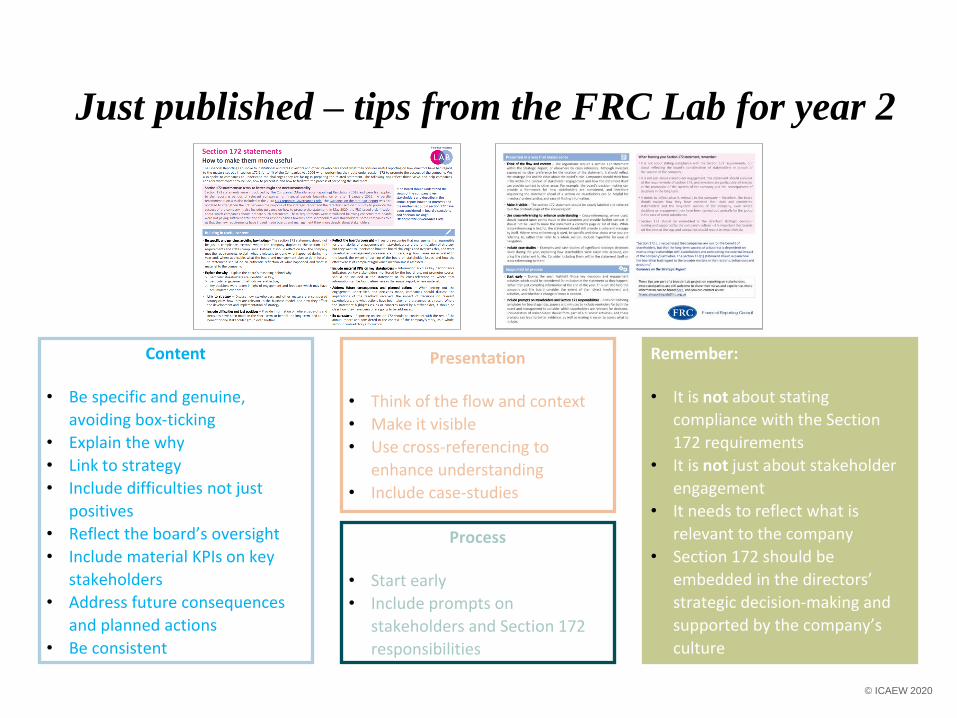

Just published – tips from the FRC Lab for year 2

© ICAEW 2020

Content

• Be specific and genuine,

avoiding box-ticking

• Explain the why

• Link to strategy

• Include difficulties not just

positives

• Reflect the board’s oversight

• Include material KPIs on key

stakeholders

• Address future consequences

and planned actions

• Be consistent

Presentation

• Think of the flow and context

• Make it visible

• Use cross-referencing to

enhance understanding

• Include case-studies

Process

• Start early

• Include prompts on

stakeholders and Section 172

responsibilities

Remember:

• It is not about stating

compliance with the Section

172 requirements

• It is not just about stakeholder

engagement

• It needs to reflect what is

relevant to the company

• Section 172 should be

embedded in the directors’

strategic decision-making and

supported by the company’s

culture

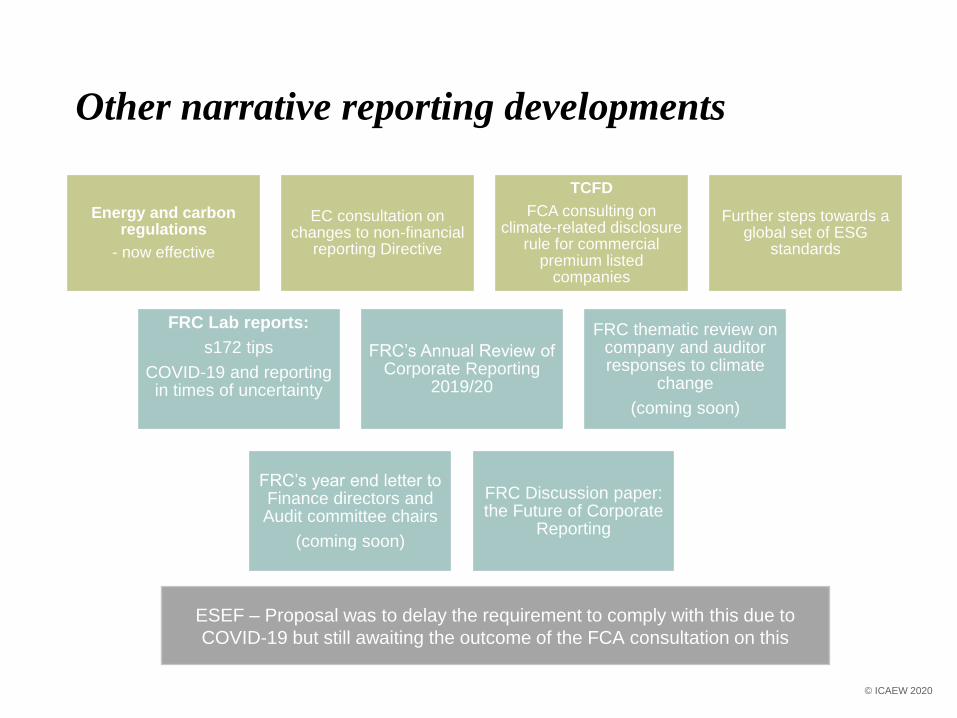

Other narrative reporting developments

© ICAEW 2020

Energy and carbon regulations

- now effective

EC consultation on changes to non-financial

reporting Directive

TCFD

FCA consulting on climate-related disclosure

rule for commercial premium listed

companies

Further steps towards a global set of ESG

standards

ESEF – Proposal was to delay the requirement to comply with this due to

COVID-19 but still awaiting the outcome of the FCA consultation on this

FRC Lab reports:

s172 tips

COVID-19 and reporting in times of uncertainty

FRC’s Annual Review of Corporate Reporting

2019/20

FRC thematic review on company and auditor responses to climate

change

(coming soon)

FRC’s year end letter to Finance directors and Audit committee chairs

(coming soon)

FRC Discussion paper: the Future of Corporate

Reporting

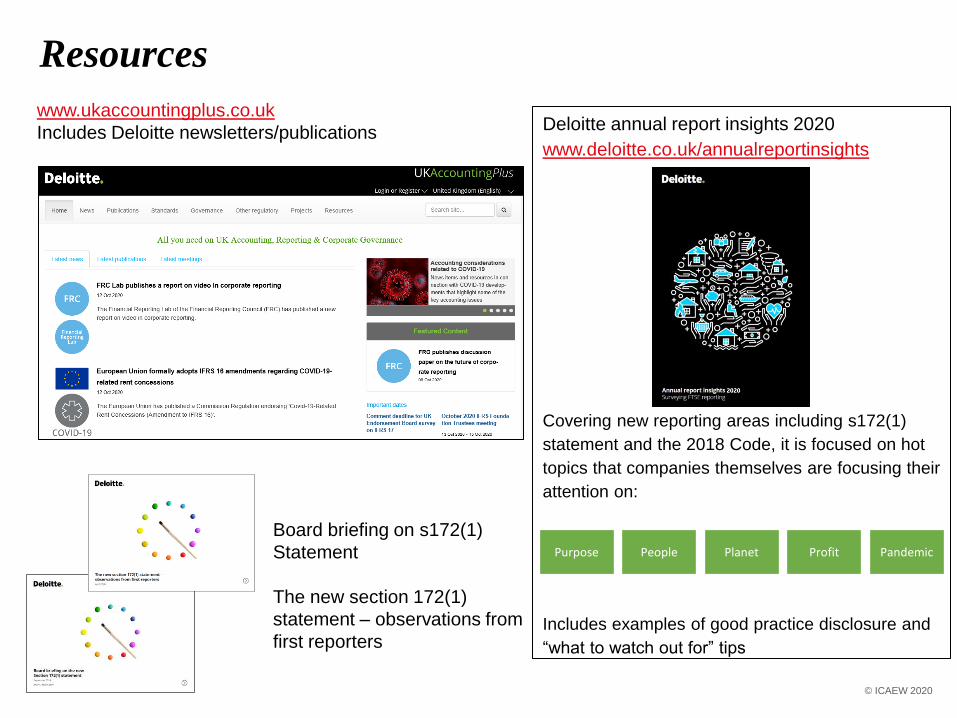

Deloitte annual report insights 2020

www.deloitte.co.uk/annualreportinsights

Covering new reporting areas including s172(1)

statement and the 2018 Code, it is focused on hot

topics that companies themselves are focusing their

attention on:

Includes examples of good practice disclosure and

“what to watch out for” tips

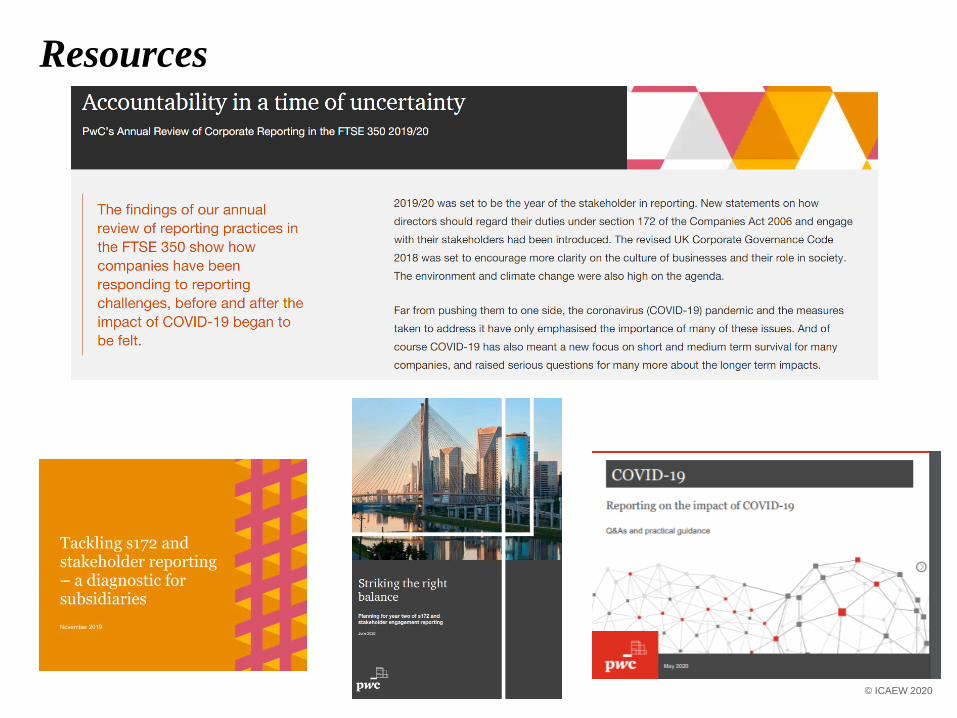

Resources

www.ukaccountingplus.co.uk

Includes Deloitte newsletters/publications

Board briefing on s172(1)

Statement

The new section 172(1)

statement – observations from

first reporters

Purpose People Planet Profit Pandemic

© ICAEW 2020

Resources

© ICAEW 2020

Ask a question

VAT Changes in 2015

Ask a question

Type your question into the box,

then click submit.

© ICAEW 2020

Faculty resources

icaew.com/ukregulation

• Factsheet

- UK Regulation for Company Accounts

• Webinars icaew.com/frfwebinars

- Narrative reporting (part 1) (January 2019)

- Narrative reporting (part 2) (October 2019)

• By All Accounts icaew.com/byallaccounts

- Energy and carbon reporting (July 2020)

- S172(1) reporting: a co-ordinated effort (July

2020)

- Engaging stakeholders (January 2020)

© ICAEW 2020

Future events

For details, please visit icaew.com/frfevents

Bitesize Briefings

COVID-19 series

Webinars

17 November: IFRS 17 Insurance Contracts for non-insurers

2020 Members’ event – recordings available

Going concern and resilience: lessons learned from COVID-19

© ICAEW 2020

We are committed to providing members with practical

help in today's complex world of financial reporting.

Visit icaew.com/financialreporting for more information.

You can also follow us @ICAEW_FRF

to keep up-to-date with the latest financial reporting

developments and breaking faculty news.

Discover the latest news and insights in financial

reporting with articles from ICAEW’s Financial

Reporting Faculty.

Financial reporting at your fingertips

© ICAEW 2020

Questions

Vicki Tibbitts

Senior Manager

Deloitte

Elaine Forrest

Senior Manager

PwC

© ICAEW 2020

Thank you for attending

Financial Reporting at your fingertips

icaew.com/frf

@ICAEW_FRF

Contact the Financial Reporting Faculty

+44 (0)20 7920 8533

© ICAEW 2020

ICAEW will not be liable for any reliance you place on the information in this presentation. You should seek independent advice.

© ICAEW 2020