najam final

DESCRIPTION

DASFADFTRANSCRIPT

Vision & Mission Statements

VisionTo be a leading national enterprise with global aspirations, effectivelyPursuing multiple growth opportunities, maximizing returns to the stakeholders, remaining socially and ethically responsible.MissionTo provide our customers with premium quality products in a safe, reliable, Efficient and environmentally sound manner, deliver exceptional services and customer support, maximizing returns to the shareholders through core business and diversification, providing a dynamic and challenging environment for our employees.

Introduction to prtoject

Pakistan‟s economy is an agricultural based and its importance is well established in the country. It plays an important

and vital role in the growth of the economy, its activity, generating revenues/foreign exchange and in the development of

the industrial sector of the country. It provides raw material to the industrial sector of the country like sugar, cotton,

textile, foods, jute, tobacco and other industries and regarded as a backbone of the Pakistan‟s economic activity. It is

contributed almost 21% of the Pakistan‟s GDP and employs about 41% of the total labor force. Fertilizers have played an

important role in the growth and development of the agricultural sector especially to meet the growing demand of the food

and to achieve the self sufficiency level. Keeping the importance of fertilizer sector in my mind, I have choosen fuiji

fertilizer company for my project of financial Ratio Analysis.

Introduction of the company:

FAUJI FERTILIZER CO. LTD. Fauji Fertilizer Company Limited (FFC) is Pakistan's leading urea manufacturing

company with over 60% market share. It is principally engaged in the production, purchasing, and marketing of fertilizers

and chemicals. It offers ammonia/urea under the brand name „Sona‟, as well as nitrogen, phosphate, and potash based

fertilizers with a vision to acquire self - sufficiency in fertilizer production in the country, FFC was incorporated in 1978

as a private limited company. This was a joint venture between Fauji Foundation (a leading charitable trust in Pakistan)

and Haldor Topsoe A/S of Denmark. The initial share capital of the company was 813.9 Million Rupees. The present

share capital of the company stands above Rs. 8.48 Billion.

Introduction to Problem:

Stock investing and consistency in financial performance requires careful analysis of financial data to find out the

company's true worth. This is generally done by examining the company's profit and loss account, balance sheet and cash

flow statement. This can be time-consuming and cumbersome. An easier way to find out about a company's performance

is to look at its financial ratios.

Research question

Whether company’s performance is consistent to make investment in the company?

Objective:

Ratio analysis is an integral part of the financial statement analysis and it is most widely and powerful tool used to analyze

the company’s financial statements. The main objective of ratio analysis is to deeply analyze the information provided in

the financial statements and present meaningful results in terms of liquidity, solvency, activity and profitability of the

company in a relative form.

Hence, the main objective of the project is to facilitate all the stakeholders especially the investors and bankers to evaluate

the ability that how effectively and efficiently it manages its operations and resources/assets and to know the activity

position of the selected company. This Project will also state the reasons that why the company are able and not able to

manage their assets effectively. The Project will also enable the investors and the other stakeholders to make the decision

to invest.

Significance

The project will provide very significant, rich and valuable information for all the stakeholders, financial analysts and the

students as well. Study of the project will become enable to identify the company‟ past and current performance with

respect to the management of their resources and further will lead them to paint the future growth of the company on the

bases of the facts, figures and analysis provided in the project within the limit of financial ratio. This project will give

them solid analysis in a graphical and tabular form with an interpretation and conclusion drawn on bases of facts and

figures and allow them to take decision whether it is better to invest.

Data Source

Data Collection Sources

This project is based upon the primary sources of data and logic is that annual reports or company statements are treated

as secondary source of data and the whole project is based on company’s annual reports and financial statements.

Secondary Sources Company’s annual accounts report and their official sites has been consulted and used as a secondary

source to collect the basic and necessary information like financial statements, company profile, introduction, business

activity, and their vision and mission statements. Articles, books, stock exchange, brokers and different sites has also been

considered as secondary source available on the internet or in a physical form to collect the raw data and information as

much as possible on the topic selected in order to get a nice and comprehensive shape of the project.

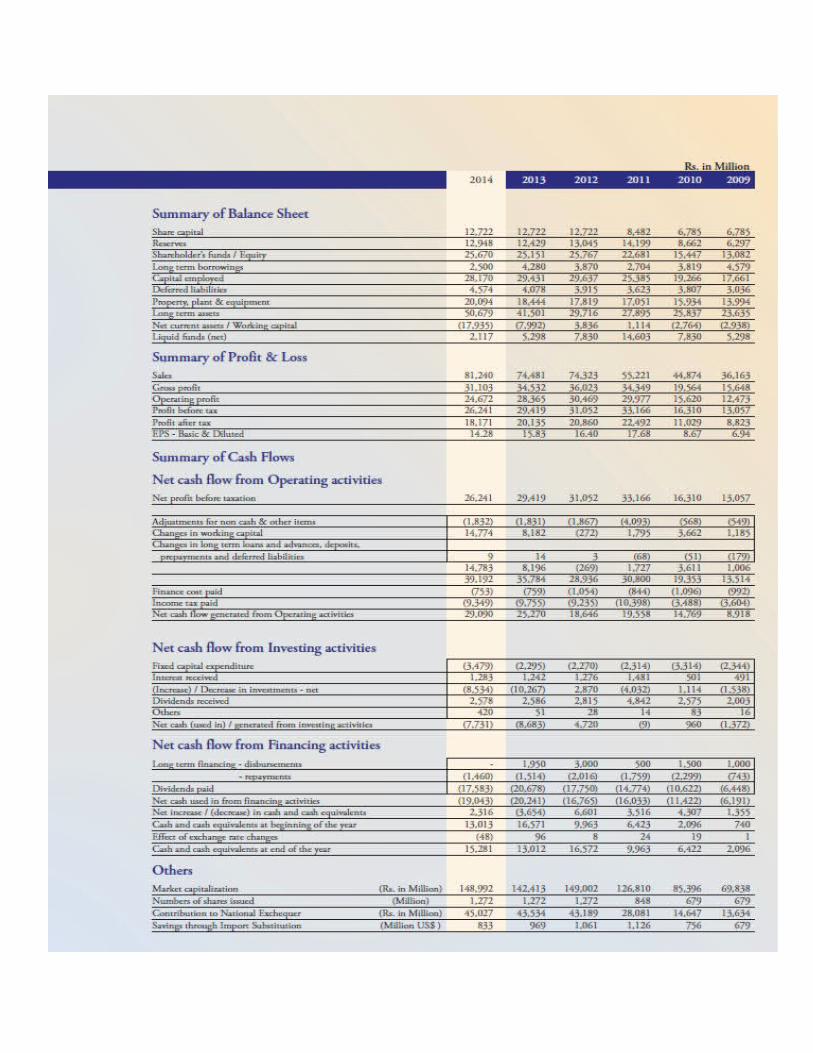

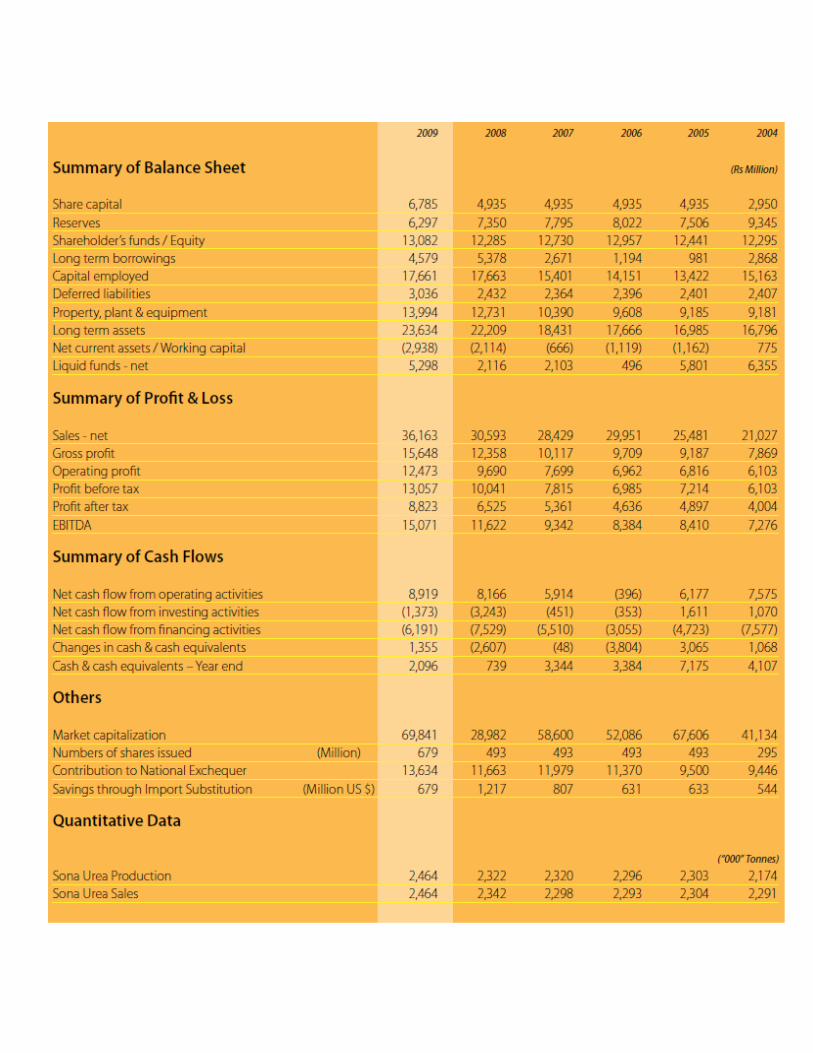

Increase in Assets Current assets include trade debts, stock,short term investments and cash & bank balances. With an aggregate balance of Rs.35.88 billion at the end of 2014, the assets recorded an increase of Rs. 20.97 billion since 2009, mainly on account of increase in short term investments, under Company policy for placement of surplus funds in term deposits for generation of incremental.

Current liabilities

Current liabilities of the Company increased from Rs. 17.86 billion in 2009 to Rs. 53.82billion in 2014, primarily on account of retained GIDC obligations, increase in short term borrowings and customer advances which is fairly in line with the Company’s growth and changes in its operating cycle.

Non-current liabilities

Total non-current liabilities comprising of long term loans, deferred taxation and long term portion of compensated leave absences, have remained fairly constant during the past 6 years. Long term loans reduced by Rs. 1.78 billion during the year on account of repayment ,while deferred liabilities increased by 12% compared to 2013. Long term financing has been utilized for asset

.

Methodology

Ratios simply mean a number expressed in terms of another. A ratio is a statistical yardstick by mean of which relationship between two or various figures can be compared or measured. Thus Ratio Analysis shows the relationship between accounting data. Ratio can be found out by dividing on number by another number. Ratio analysis is an important and age old technique of financial analysis. Following are some of the advantages of ratio analysis.

Advantages:· It simplifies the comprehension of financial statements.· Ratios tell the whole story of changes in the financial condition of the business.· It provides data for inter-company comparison. Makes inter-company comparison possible· Ratio analysis also makes possible comparison of the performance of different divisions of the company. The ratios are helpful in deciding about their efficiency or otherwise in the past and likely performance in the future.· Ratios highlight the factors associated with successful and unsuccessful company. They also reveal strong companies and weak company’s, over-valued under-valued companies.· It helps in planning and forecasting. Ratios can assist management, in its function of forecasting, planning, co-ordination, control and communications.· It helps in investment decisions in the case of investors and lending decisions in the case of investors and lending decisions in the case of bankers’ etc.

Parameters used for Financial Analysis

The parameters used for financial analysis are the ratios of five different categories.

1. Profitability Ratio I. Gross Profit Ratio

II. Net profit ratioIII. Pre Tax margin ratioIV. EBITDA( Earnings before Interest,Tax,Depreciation and Amortization) Margin to SalesV. Return on Equity

VI. Return on Capital EmployedVII. Return on Assets

2. Liquidity Ratios

I. Current RatioII. Quick Ratio

III. Cash flow from operation to salesIV. Cash to Current liabilities

3. Activity and turnover ratioI. Inventory turnover ratios

II. No of days in inventoryIII. Debtors to turn over ratiosIV. No of Days in receivableV. Creditors Turnover Ratios

VI. No of Days in payablesVII. Fixed Asset Turnover ratio

4. Investment Ratio/Market RatioI. Earnings per Share Ratio

II. Dividend yield RatioIII. Market Value per shareIV. Breakup value per shareV. Cash dividend per Share

VI. Bonus shares issued

5. Capital Structure RatiosI. Debt to equity Ratio

II. Interest coverage Ratio

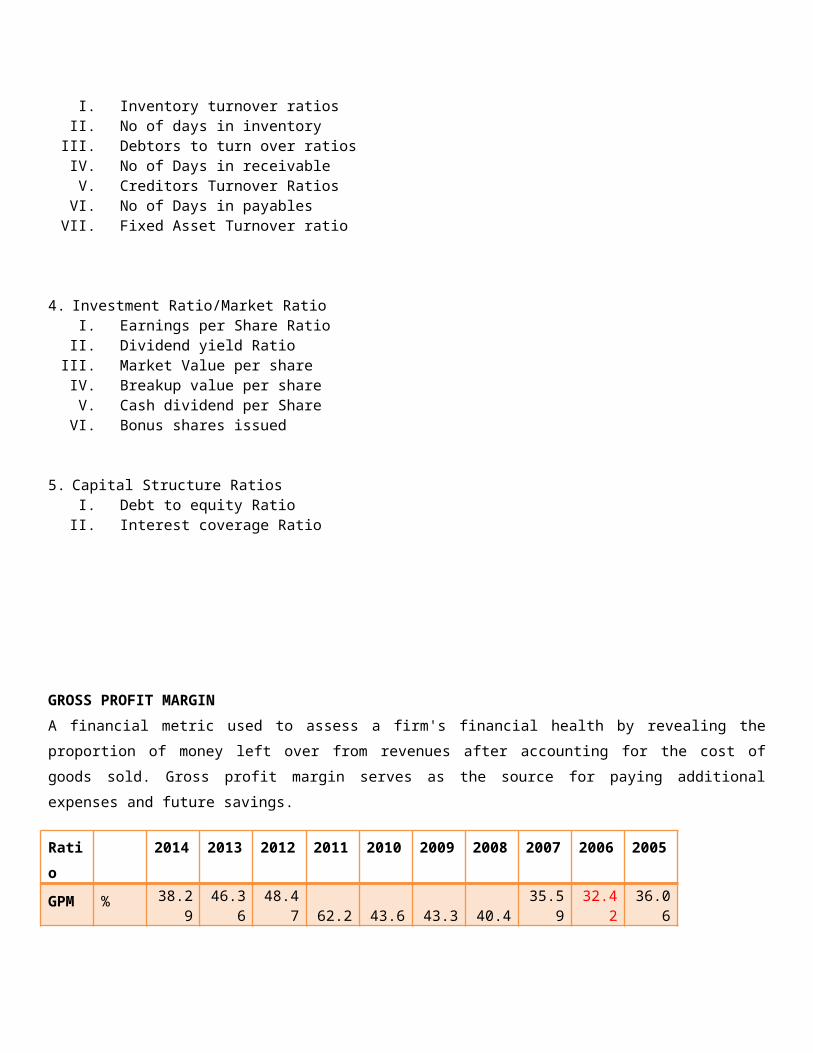

GROSS PROFIT MARGIN

A financial metric used to assess a firm's financial health by revealing the proportion of money left over from revenues

after accounting for the cost of goods sold. Gross profit margin serves as the source for paying additional expenses and

future savings.

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

GPM % 38.29 46.36 48.47 62.2 43.6 43.3 40.4 35.59 32.42 36.06

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

10

20

30

40

50

60

70

38.29

46.3648.47

62.2

43.6 43.2740.4

35.5932.42

36.06

Series1

The gross margin is not an exact estimate of the company's pricing strategy but it does give a good indication of financial

health. Without an adequate gross margin, a company will be unable to pay its operating and other expenses and build for

the future. In general, a company's gross profit margin should be stable. It should not fluctuate much from one period to

another, unless the industry it is in has been undergoing drastic changes which will affect the costs of goods sold or

pricing policies.

Ways to improve Gross Profit Margin Ratio

Reducing Cost of Goods Sold

Cheaper Raw material

Selecting low price suppliers

Modern technology to reduce Labour cost

Increase selling price

Net Profit Margin (NPM)

A ratio of profitability calculated as net income divided by revenues, or net profits divided by sales. It measures how

much out of every dollar of sales a company actually keeps in earnings.

Net Profit Margin =Net ProfitNet Sales

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

NPM % 22.37 27.03 28.07 40.73 24.58 24.4 21.33 18.86 15.48 19.22

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

5

10

15

20

25

30

35

40

45

22.37

27.03 28.07

40.73

24.58 24.421.33

18.86

15.48

19.22 Series1

Net Profit margin is very useful when comparing companies in similar industries. A higher profit margin indicates a more

profitable company that has better control over its costs compared to its competitors.

Ways to improve Net Profit Margin Ratio

Reducing Cost of Goods Sold

Cheaper Raw material

Selecting low price suppliers

Modern technology to reduce Labour cost

Increase selling price

Reduce unnecessary administrative expenses

Reducing finance cost

Rise in cost of sales owing to increased raw material cost and GIDC resulted in a reduction in gross and net profit margins for2014, depicting a decrease of 8% and 5% respectively from last year. Consequently, return on equity (post tax) and capital employed were also lower by 9% and 4% respectively in comparison with 2013.

Pre Tax Margin

The financial ratio pretax margin is a measure of the operating efficiency of a company. Pretax margin only requires two

inputs from the income statement: revenues and income before taxes.

Pretax Margin (%) = (Income before Taxes / Revenues) x 100

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

PTM % 32.3 39.5 41.78 60.06 36.35 36.11 32.82 27.49 23.26 28.31

Higher pretax margins are desirable and indicative of management's ability to keep operating costs low. Investors and analysts typically evaluate a company's pretax margin over time, looking for an increase in the measure. When drawing conclusions about the relative performance of a company, benchmark comparisons should be made with competitors in the same industry.

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

10

20

30

40

50

60

70

PTM

PTM

Earnings before Interest, Tax, Depreciation and Amortization margin to sales

An EBITDA margin is a measurement of a company's earnings before interest, taxes, depreciation, and amortization as a percentage of its total revenue. The formula for EBITDA margin is:

EBITDA Margin = EBITDA/Total Revenue

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

EBITDA % 35.61 42.74 44.99 63.64 41.43 41.68 37.99 32.36 27.99 33.00

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

10

20

30

40

50

60

70

Series1

Return on Equity – ROE

The amount of net income returned as a percentage of shareholders equity. Return on equity measures a corporation's profitability by revealing how much profit a company generates with the money shareholders have invested.

Return on Equity = Net Income/Shareholder's Equity

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

20

40

60

80

100

120

70.79

80.05 80.96

99.17

71.467.44

53.11

42.1135.78

39.36

Series1

Shareholder's equity does not include preferred shares. Widely used by investors, the ROE ratio is an important measure

of a company's earnings performance. The ROE tells common shareholders how effectively their money is being

employed. In general, financial analysts consider return on equity ratios in the 15-20% range as representing attractive

levels of investment quality.

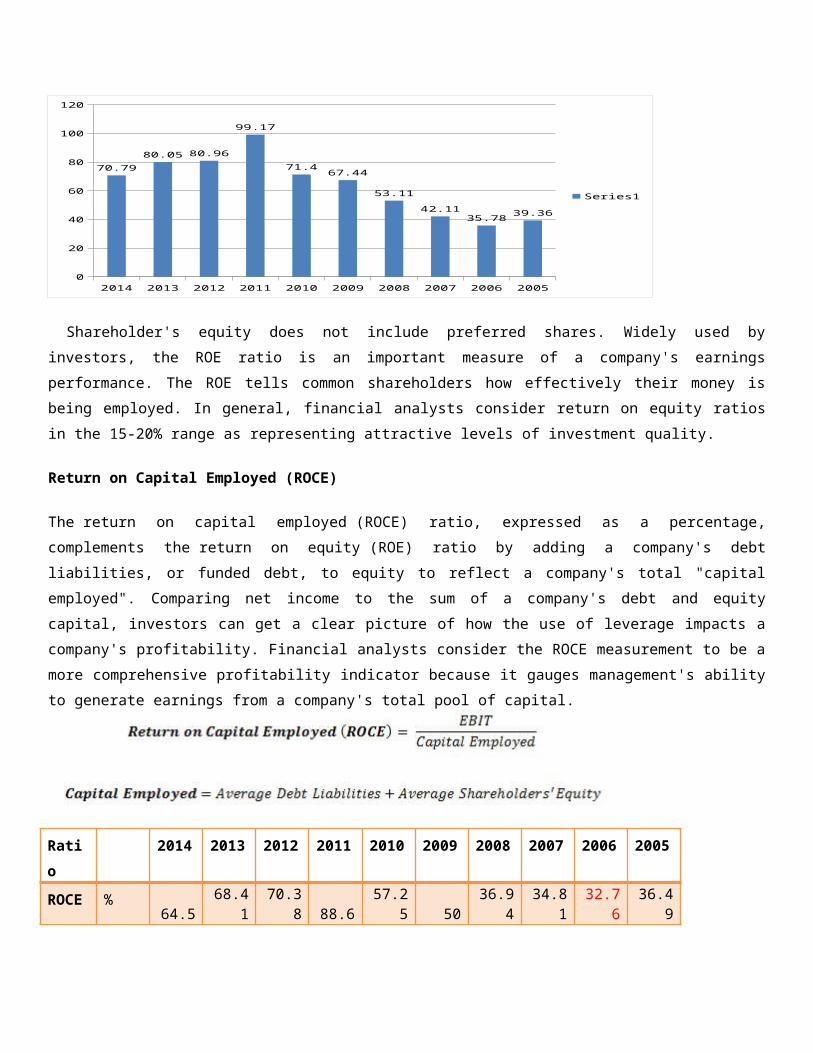

Return on Capital Employed (ROCE)

The return on capital employed (ROCE) ratio, expressed as a percentage, complements the return on equity (ROE) ratio

by adding a company's debt liabilities, or funded debt, to equity to reflect a company's total "capital employed".

Comparing net income to the sum of a company's debt and equity capital, investors can get a clear picture of how the use

of leverage impacts a company's profitability. Financial analysts consider the ROCE measurement to be a more

comprehensive profitability indicator because it gauges management's ability to generate earnings from a company's total

pool of capital.

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

ROE % 70.79 80.05 80.96 99.17 71.4 67.4 53.11 42.11 35.78 39.36

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

10

20

30

40

50

60

70

80

90

Series1

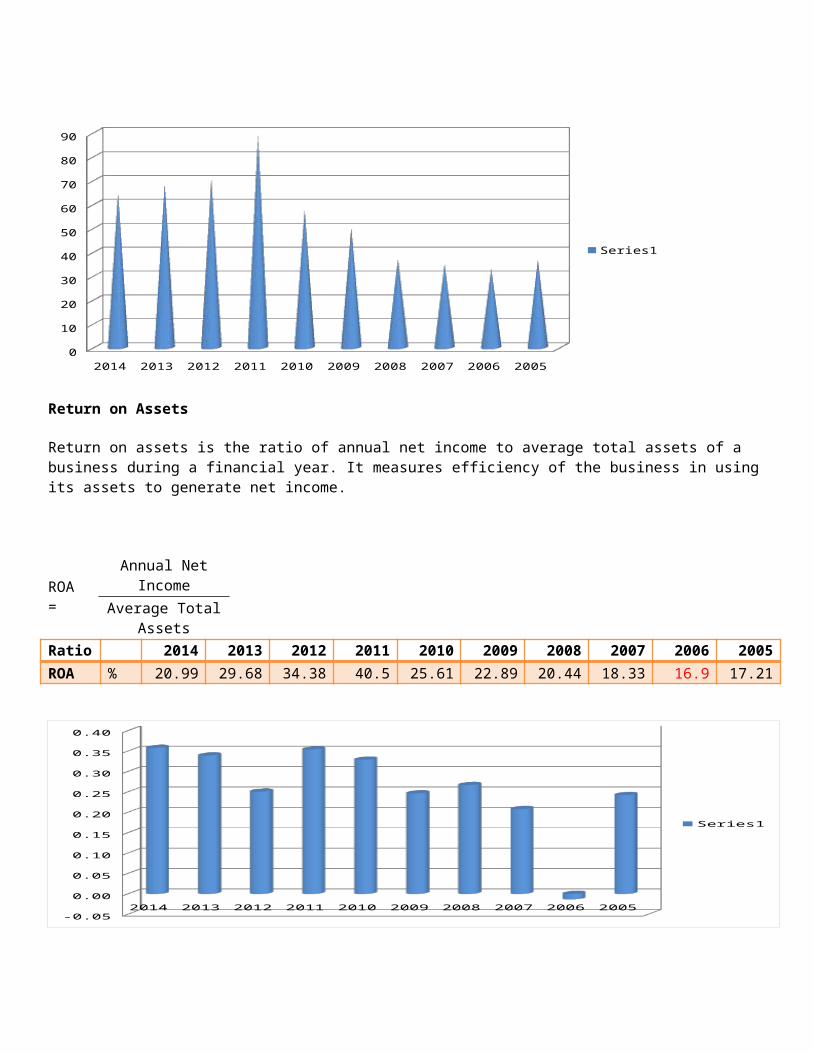

Return on Assets

Return on assets is the ratio of annual net income to average total assets of a business during a financial year. It measures efficiency of the business in using its assets to generate net income.

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

ROA % 20.99 29.68 34.38 40.5 25.61 22.89 20.44 18.33 16.9 17.21

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

ROCE % 64.5 68.41 70.38 88.6 57.25 50 36.94 34.81 32.76 36.49

ROA = Annual Net Income

Average Total Assets

2014 2013 2012 2011 2010 2009 2008 2007 2006 2005-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

Series1

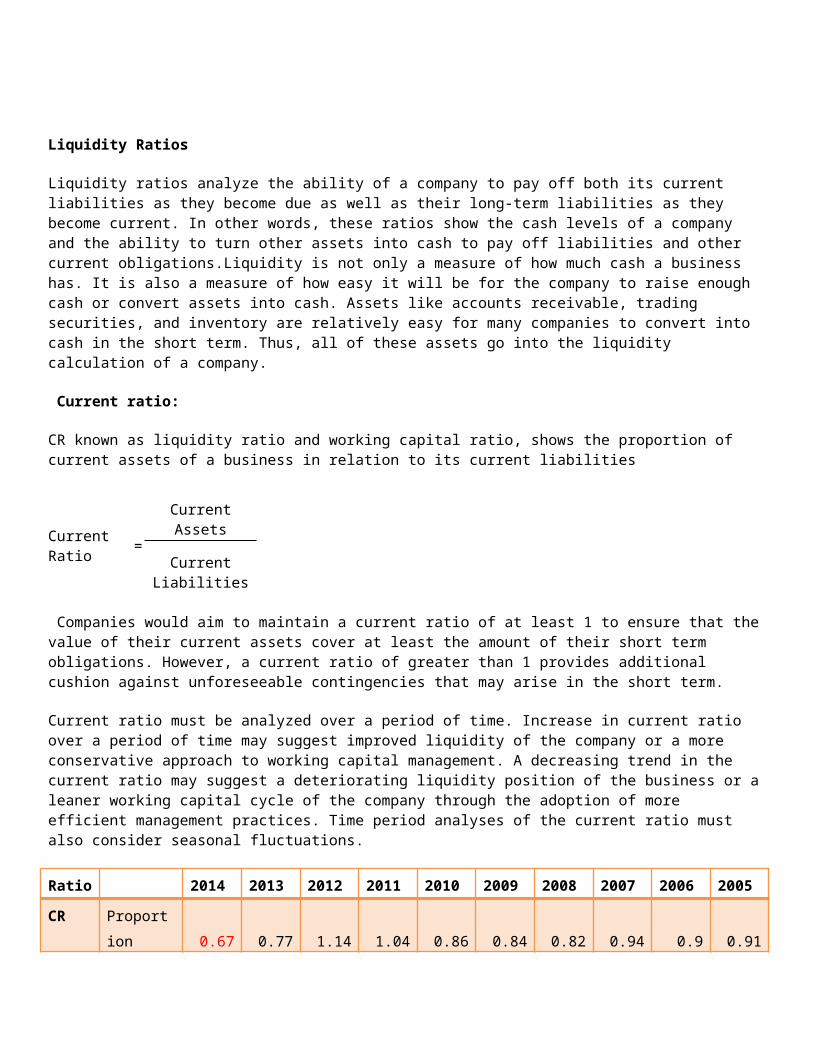

Liquidity Ratios

Liquidity ratios analyze the ability of a company to pay off both its current liabilities as they become due as well as their long-term liabilities as they become current. In other words, these ratios show the cash levels of a company and the ability to turn other assets into cash to pay off liabilities and other current obligations.Liquidity is not only a measure of how much cash a business has. It is also a measure of how easy it will be for the company to raise enough cash or convert assets into cash. Assets like accounts receivable, trading securities, and inventory are relatively easy for many companies to convert into cash in the short term. Thus, all of these assets go into the liquidity calculation of a company.

Current ratio:

CR known as liquidity ratio and working capital ratio, shows the proportion of current assets of a business in relation to its current liabilities

Current Ratio =Current Assets

Current Liabilities

Companies would aim to maintain a current ratio of at least 1 to ensure that the value of their current assets cover at least the amount of their short term obligations. However, a current ratio of greater than 1 provides additional cushion against unforeseeable contingencies that may arise in the short term.

Current ratio must be analyzed over a period of time. Increase in current ratio over a period of time may suggest improved liquidity of the company or a more conservative approach to working capital management. A decreasing trend in the current ratio may suggest a deteriorating liquidity position of the business or a leaner working capital cycle of the company through the adoption of more efficient management practices. Time period analyses of the current ratio must also consider seasonal fluctuations.

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

CR Proportion 0.67 0.77 1.14 1.04 0.86 0.84 0.82 0.94 0.9 0.91

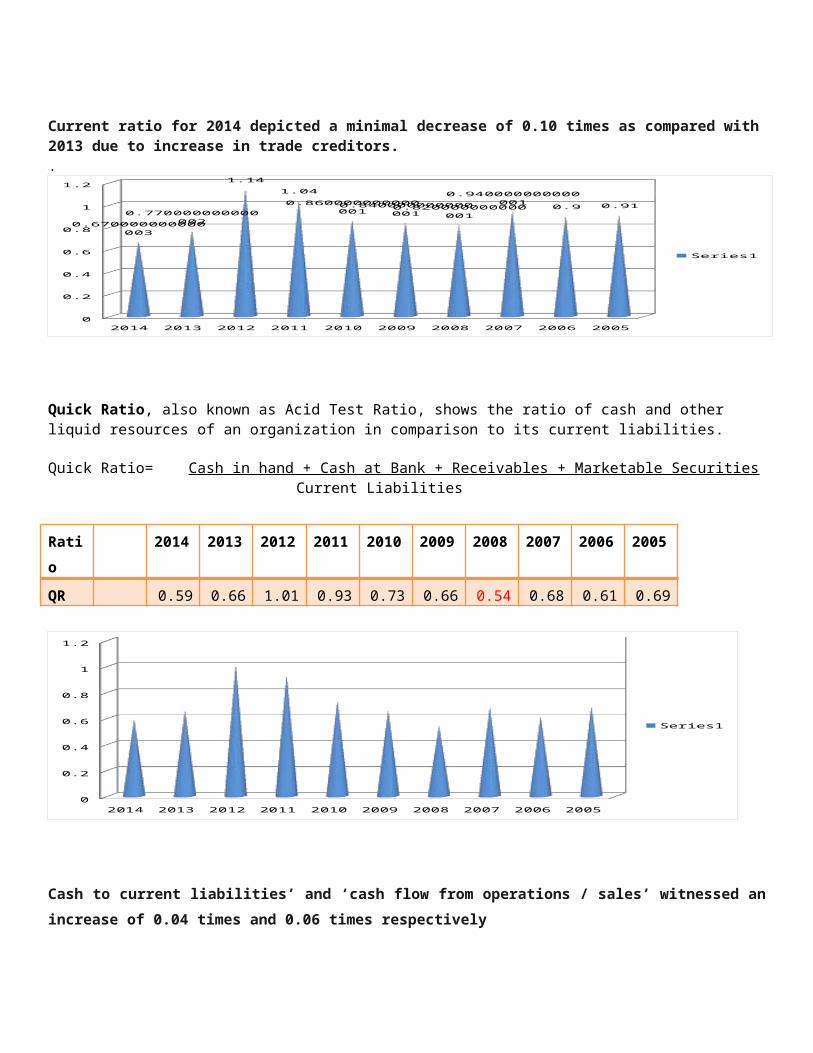

Current ratio for 2014 depicted a minimal decrease of 0.10 times as compared with 2013 due to increase in trade creditors..

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

0.2

0.4

0.6

0.8

1

1.2

0.670000000000003

0.770000000000002

1.14

1.04

0.860000000000001

0.840000000000001

0.820000000000001

0.940000000000001

0.9 0.91

Series1

Quick Ratio, also known as Acid Test Ratio, shows the ratio of cash and other liquid resources of an organization in comparison to its current liabilities.

Quick Ratio= Cash in hand + Cash at Bank + Receivables + Marketable Securities Current Liabilities

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

QR 0.59 0.66 1.01 0.93 0.73 0.66 0.54 0.68 0.61 0.69

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

0.2

0.4

0.6

0.8

1

1.2

Series1

Cash to current liabilities’ and ‘cash flow from operations / sales’ witnessed an increase of 0.04 times and 0.06

times respectively

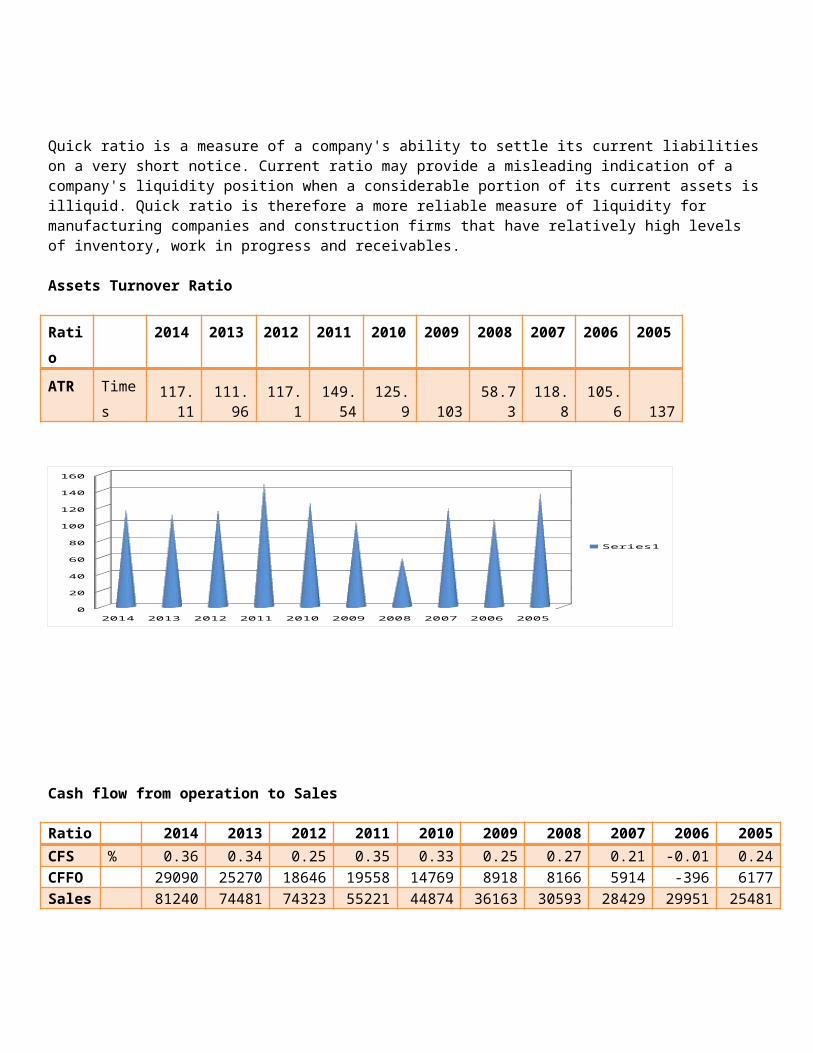

Quick ratio is a measure of a company's ability to settle its current liabilities on a very short notice. Current ratio may provide a misleading indication of a company's liquidity position when a considerable portion of its current assets is

illiquid. Quick ratio is therefore a more reliable measure of liquidity for manufacturing companies and construction firms that have relatively high levels of inventory, work in progress and receivables.

Assets Turnover Ratio

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

ATR Times117.11

111.96 117.1 149.54 125.9 103 58.73 118.8 105.6 137

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

20

40

60

80

100

120

140

160

Series1

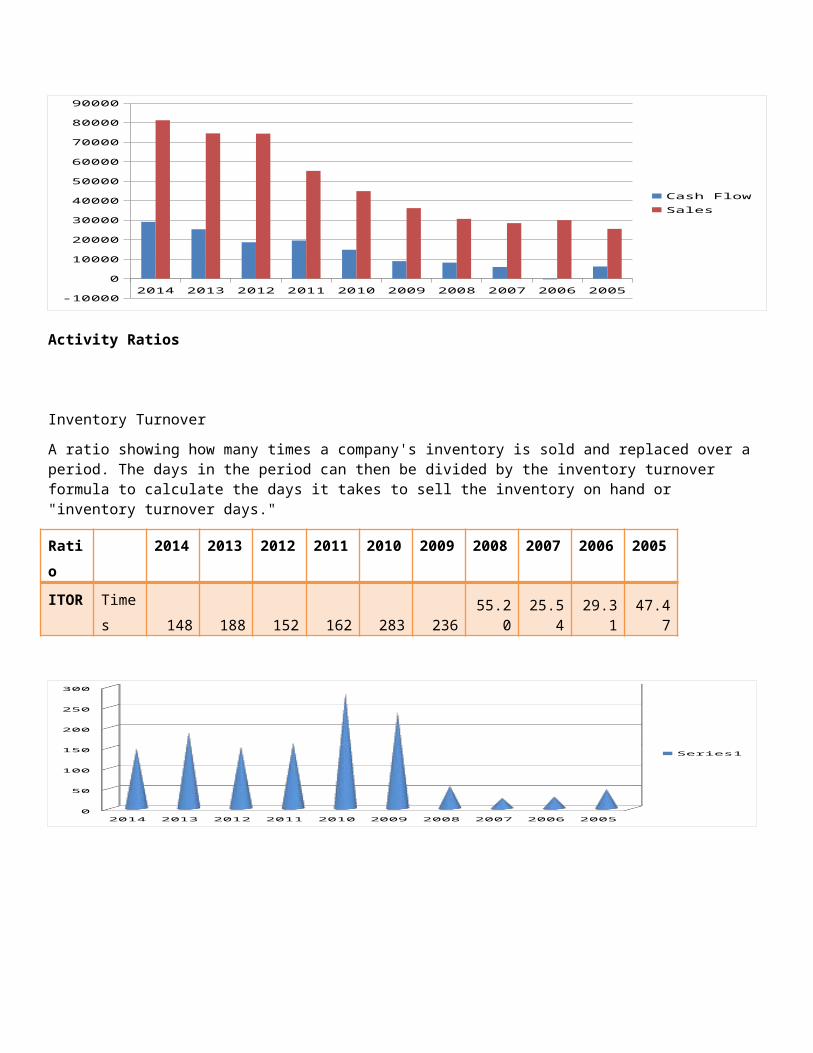

Cash flow from operation to Sales

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

CFS % 0.36 0.34 0.25 0.35 0.33 0.25 0.27 0.21 -0.01 0.24CFFO 29090 25270 18646 19558 14769 8918 8166 5914 -396 6177Sales 81240 74481 74323 55221 44874 36163 30593 28429 29951 25481

2014 2013 2012 2011 2010 2009 2008 2007 2006 2005-10000

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

Cash FlowSales

Activity Ratios

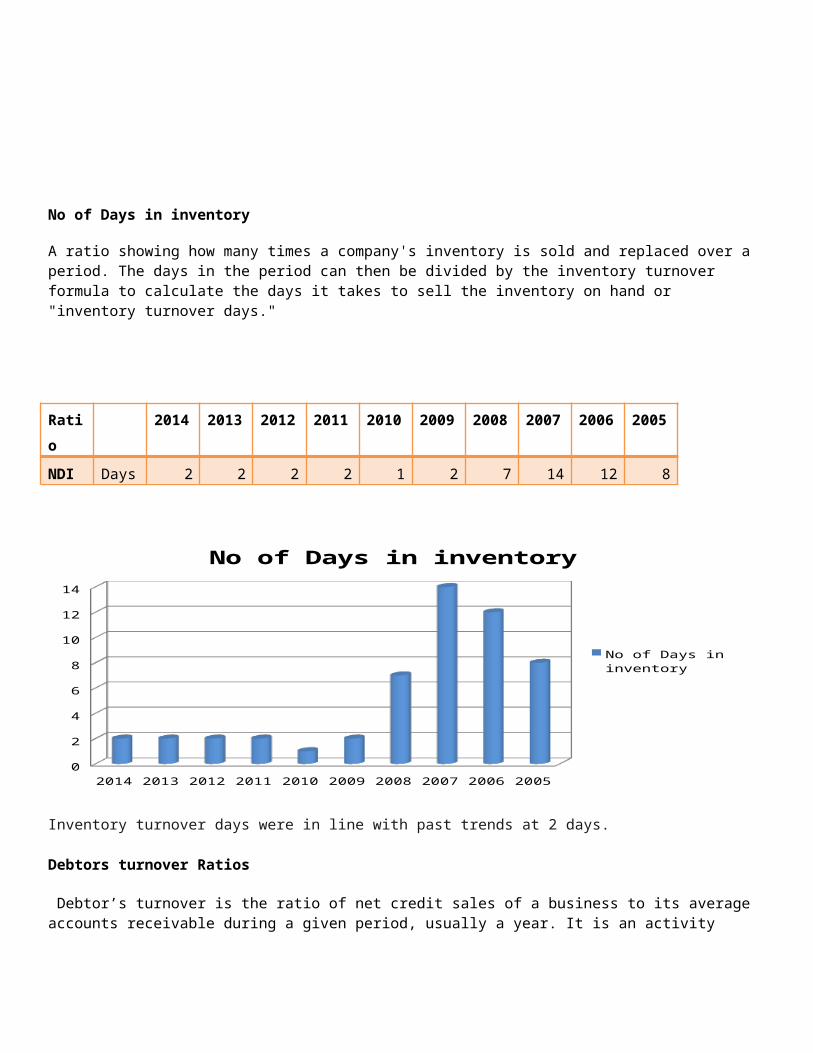

Inventory Turnover

A ratio showing how many times a company's inventory is sold and replaced over a period. The days in the period can then be divided by the inventory turnover formula to calculate the days it takes to sell the inventory on hand or "inventory turnover days."

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

ITOR Times 148 188 152 162 283 236 55.20 25.54 29.31 47.47

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

50

100

150

200

250

300

Series1

No of Days in inventory

A ratio showing how many times a company's inventory is sold and replaced over a period. The days in the period can then be divided by the inventory turnover formula to calculate the days it takes to sell the inventory on hand or "inventory turnover days."

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

NDI Days 2 2 2 2 1 2 7 14 12 8

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

2

4

6

8

10

12

14

No of Days in inventory

No of Days in inventory

Inventory turnover days were in line with past trends at 2 days.

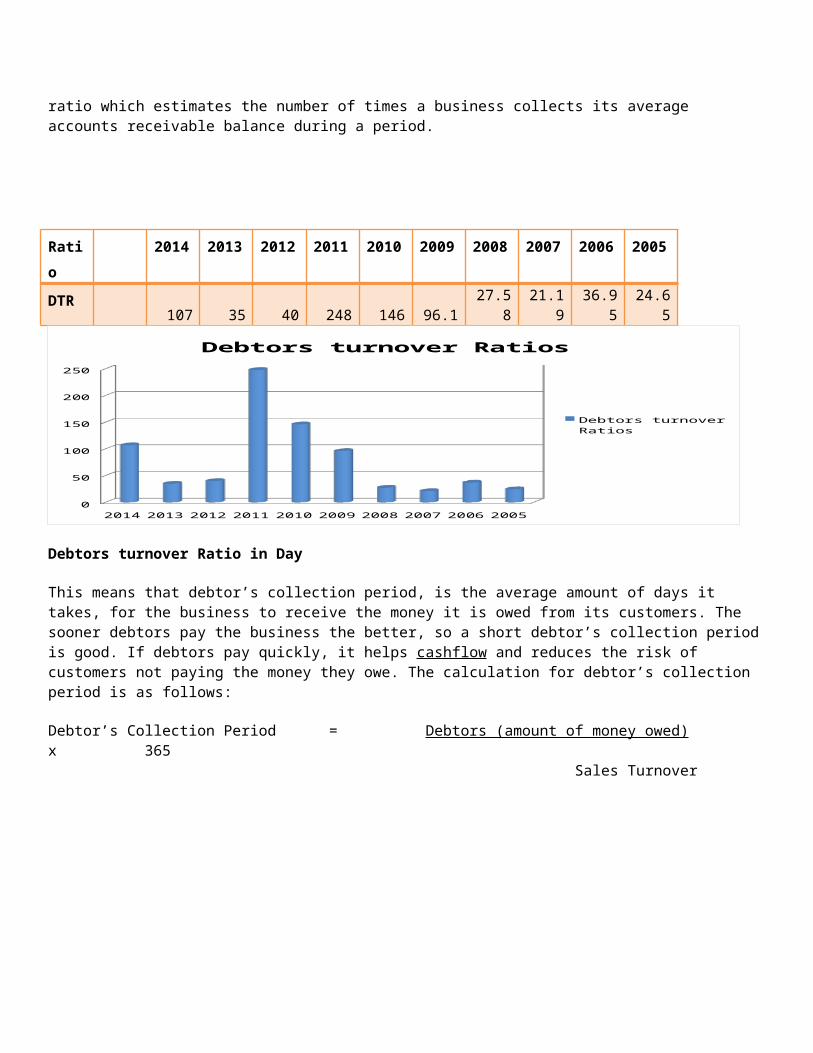

Debtors turnover Ratios

Debtor’s turnover is the ratio of net credit sales of a business to its average accounts receivable during a given period, usually a year. It is an activity ratio which estimates the number of times a business collects its average accounts receivable balance during a period.

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

DTR 107 35 40 248 146 96.1 27.58 21.19 36.95 24.65

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

50

100

150

200

250

Debtors turnover Ratios

Debtors turnover Ratios

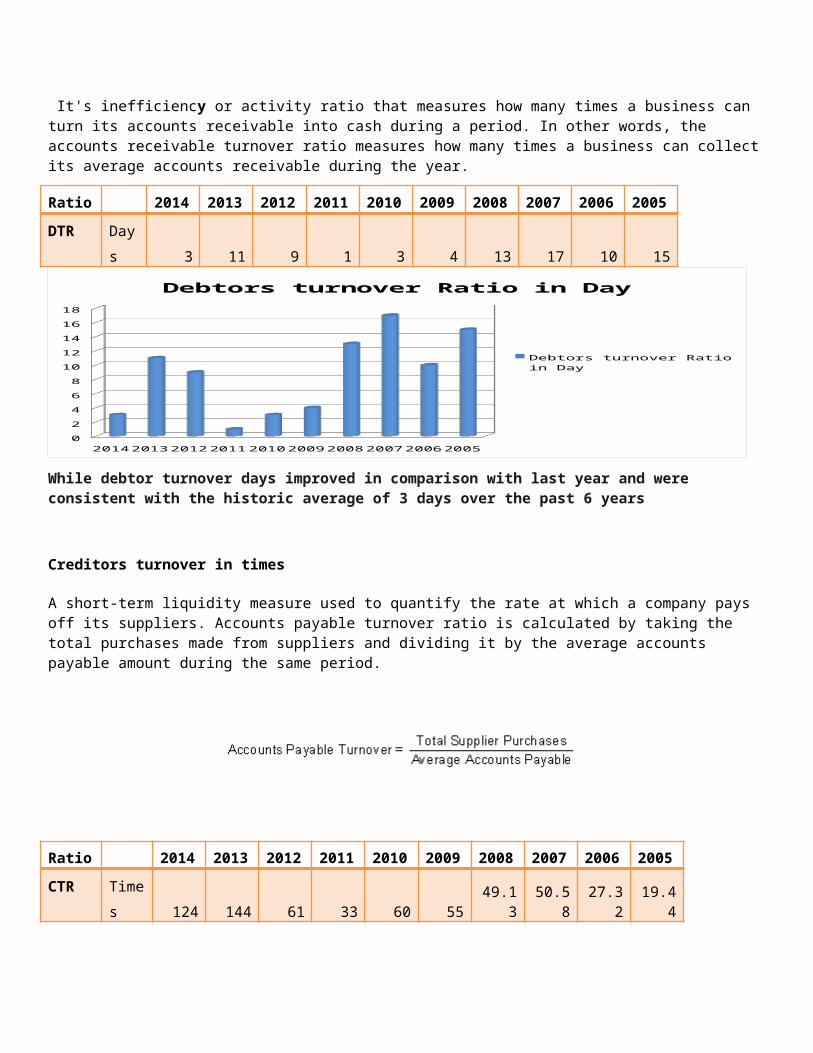

Debtors turnover Ratio in Day

This means that debtor’s collection period, is the average amount of days it takes, for the business to receive the money it is owed from its customers. The sooner debtors pay the business the better, so a short debtor’s collection period is good. If debtors pay quickly, it helps cashflow and reduces the risk of customers not paying the money they owe. The calculation for debtor’s collection period is as follows:

Debtor’s Collection Period = Debtors (amount of money owed) x 365 Sales Turnover

It's inefficiency or activity ratio that measures how many times a business can turn its accounts receivable into cash during a period. In other words, the accounts receivable turnover ratio measures how many times a business can collect its average accounts receivable during the year.

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

DTR Days 3 11 9 1 3 4 13 17 10 15

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

2

4

6

8

10

12

14

16

18

Debtors turnover Ratio in Day

Debtors turnover Ratio in Day

While debtor turnover days improved in comparison with last year and were consistent with the historic average of 3 days over the past 6 years

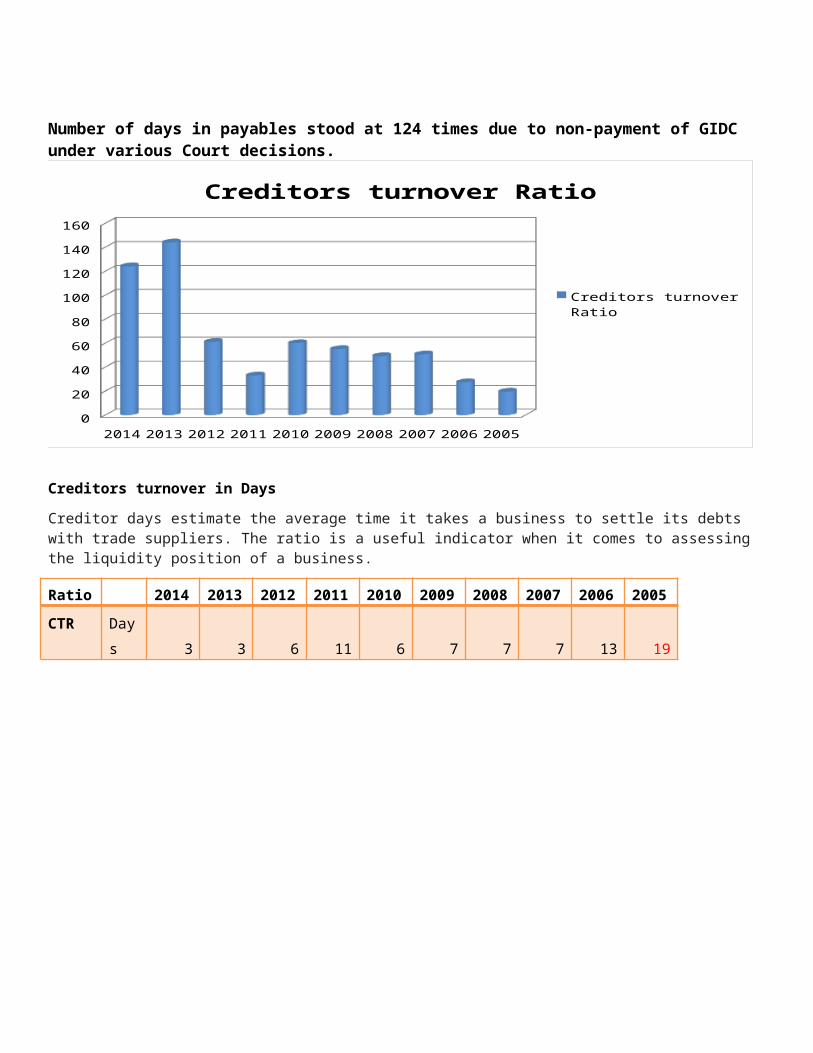

Creditors turnover in times

A short-term liquidity measure used to quantify the rate at which a company pays off its suppliers. Accounts payable turnover ratio is calculated by taking the total purchases made from suppliers and dividing it by the average accounts payable amount during the same period.

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

CTR Times 124 144 61 33 60 55 49.13 50.58 27.32 19.44

Number of days in payables stood at 124 times due to non-payment of GIDC under various Court decisions.

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

20

40

60

80

100

120

140

160

Creditors turnover Ratio

Creditors turnover Ratio

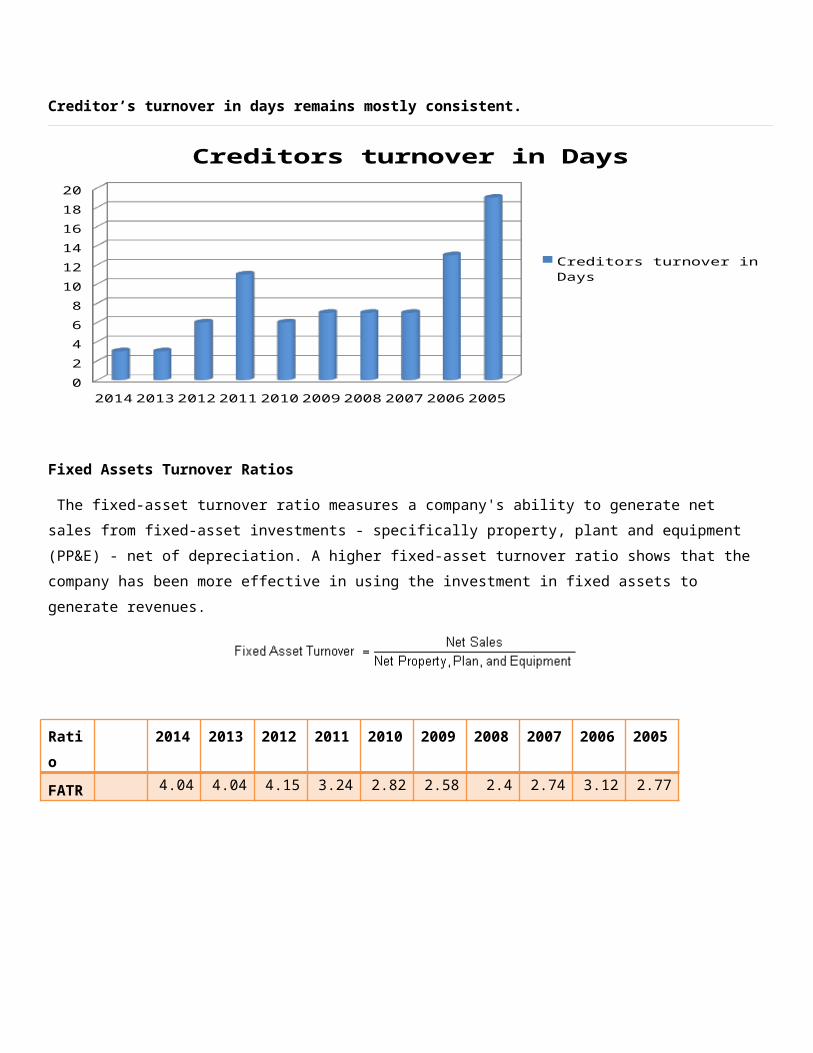

Creditors turnover in Days

Creditor days estimate the average time it takes a business to settle its debts with trade suppliers. The ratio is a useful indicator when it comes to assessing the liquidity position of a business.

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

CTR Days 3 3 6 11 6 7 7 7 13 19

Creditor’s turnover in days remains mostly consistent.

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

2

4

6

8

10

12

14

16

18

20

Creditors turnover in Days

Creditors turnover in Days

Fixed Assets Turnover Ratios

The fixed-asset turnover ratio measures a company's ability to generate net sales from fixed-asset investments -

specifically property, plant and equipment (PP&E) - net of depreciation. A higher fixed-asset turnover ratio shows that the

company has been more effective in using the investment in fixed assets to generate revenues.

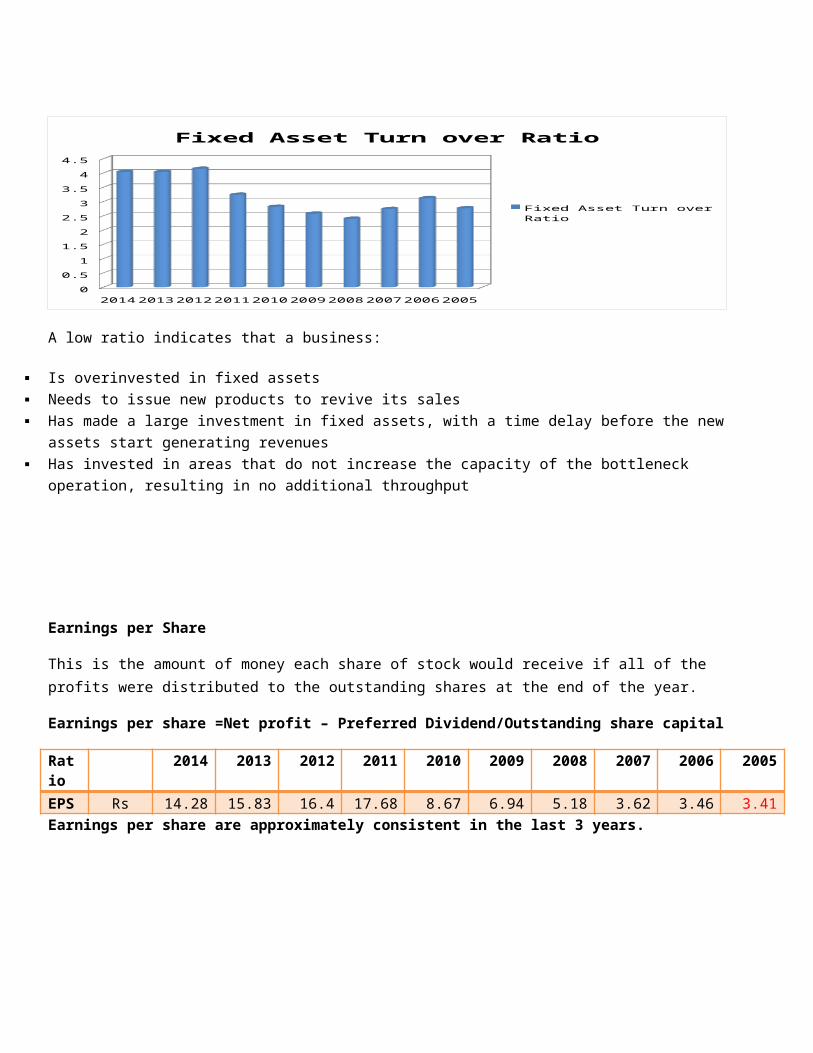

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

FATR4.04 4.04 4.15 3.24 2.82 2.58 2.4 2.74 3.12 2.77

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

0.5

1

1.5

2

2.5

3

3.5

4

4.5

Fixed Asset Turn over Ratio

Fixed Asset Turn over Ratio

A low ratio indicates that a business:

Is overinvested in fixed assets

Needs to issue new products to revive its sales

Has made a large investment in fixed assets, with a time delay before the new assets start generating revenues

Has invested in areas that do not increase the capacity of the bottleneck operation, resulting in no additional throughput

Earnings per Share

This is the amount of money each share of stock would receive if all of the profits were distributed to the outstanding shares at the end of the year.

Earnings per share =Net profit – Preferred Dividend/Outstanding share capital

Ratio

2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

EPS Rs 14.28 15.83 16.4 17.68 8.67 6.94 5.18 3.62 3.46 3.41Earnings per share are approximately consistent in the last 3 years.

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

2

4

6

8

10

12

14

16

18

Earnings Per Share

Earnings Per Share

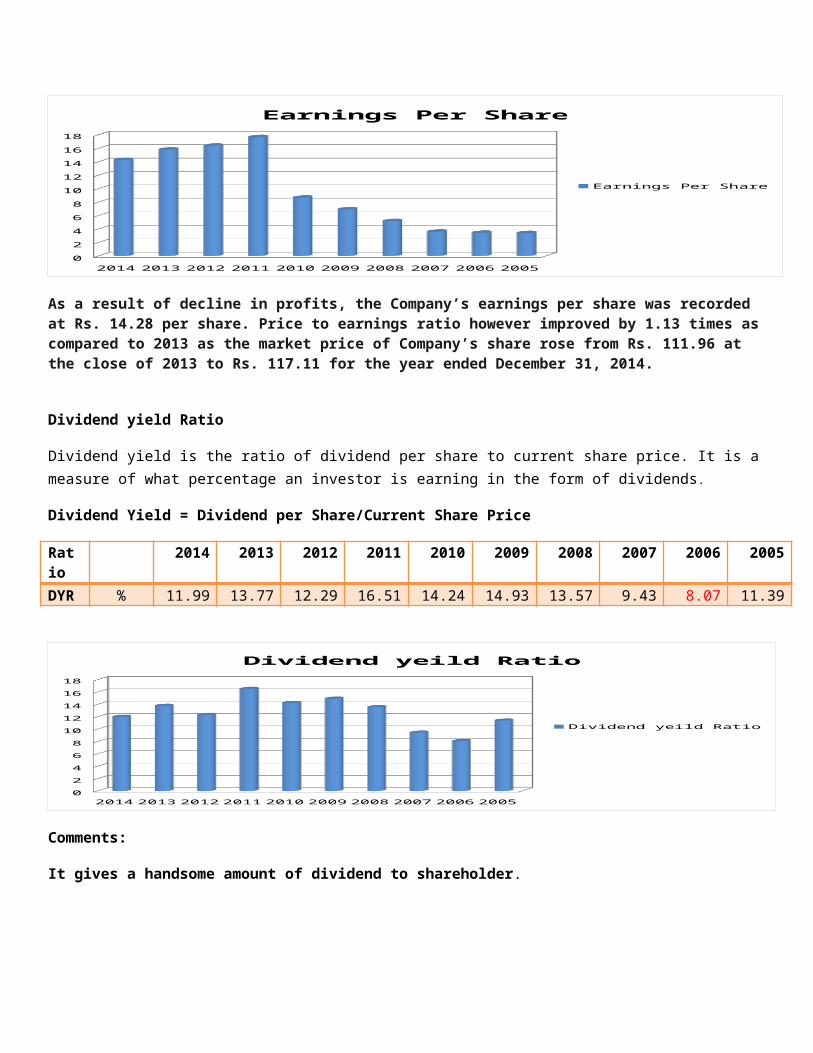

As a result of decline in profits, the Company’s earnings per share was recorded at Rs. 14.28 per share. Price to earnings ratio however improved by 1.13 times as compared to 2013 as the market price of Company’s share rose from Rs. 111.96 at the close of 2013 to Rs. 117.11 for the year ended December 31, 2014.

Dividend yield Ratio

Dividend yield is the ratio of dividend per share to current share price. It is a measure of what percentage an investor is earning in the form of dividends.

Dividend Yield = Dividend per Share/Current Share Price

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

DYR % 11.99 13.77 12.29 16.51 14.24 14.93 13.57 9.43 8.07 11.39

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

2

4

6

8

10

12

14

16

18

Dividend yeild Ratio

Dividend yeild Ratio

Comments:

It gives a handsome amount of dividend to shareholder.

Market value per share

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

MVS Rs 117.11 111.96 117.14 149.54 125.86 102.93 58.73 118.75 105.55 137

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

20

40

60

80

100

120

140

160

Market Value per Share

Market Value per Share

Cash Dividend per share

The sum of declared dividends for every ordinary share issued. Dividend per share (DPS) is the total dividends paid out over an entire year (including interim dividends but not including special dividends) divided by the number of outstanding ordinary shares issued.

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

CDPS Rs 13.65 15.35 15.5 20 13 13.15 13.75 11 10 12

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

2

4

6

8

10

12

14

16

18

20

Cash dividedn per share

Cash dividedn per share

Bonus Share

A bonus share is a free share of stock given to current shareholders in a company, based upon the number of shares that the shareholder already owns While the issue of bonus shares increases the total number ofshares issued and owned, it does not change the value of the company.

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

BS % - - - 50 25 10 - - 40 -

Capital Structure Ratios

Debt to Equity Ratio

The debt-to-equity ratio shows the proportion of equity and debt a firm is using to finance its assets, and the ability for

shareholder equity to fulfill obligations to creditors in the event of a business decline

Debt-to-equity ratio = total liabilities / total shareholders' equity

Ratio

2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

DER % 4/9 2/3 3/5 ½ ¼ 1/3 3/7 ¾ 2/5 1/3

A low debt-to-equity ratio indicates lower risk, since debt holders have fewer claims on the company's assets. A higher

debt-to-equity ratio, on the other hand, shows that a company has been aggressive in financing its growth with debt, and

there may be a greater potential for financial distress if earnings do not exceed the cost of borrowed funds.

INTEREST COVERAGE RATIO

A ratio used to determine how easily a company can pay interest on outstanding debt. The interest coverage ratio is

calculated by dividing a company's earnings before interest and taxes (EBIT) of one period by the company's interest

expenses of the same period:

Ratio 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

EBIT 31.91 39.91 32.08 43.2 16 14.82 15.44 12.1 14.94 23.13

2014 2013 2012 2011 2010 2009 2008 2007 2006 20050

5

10

15

20

25

30

35

40

45

Interest coverage ratio

Interest coverage ratio

Comments:

Financial leverage ratio of 0.62 times for2014 is consistent with the average for the past 6 years. Debt to equity ratio improved to 9:91 indicating the lowest amount of long-term debt in the last 6 years. Company’s interest cover ratio doubled to 32 times in comparison with 15 times in 2009 as result of lower finance cost to profitability ratio.

Conclusion

So,in the light of all the details given above about the financial analysis of FFC i.e Debt to equity, Liquidity and profitability of FFC, we come to know that FFC has performed well even in shortage of Gas supply in the country. It is consistently growing and paying higher rate of return to investor.