nada: 2013 dealers’ outlook/media/others/events/2013/automotive... · nada: 2013 dealers’...

TRANSCRIPT

NADA: 2013 Dealers’ Outlook

20th Annual Automotive Outlook Symposium Federal Reserve Bank of Chicago-Detroit Branch May 31, 2013

Jonathan Banks Executive Automotive Analyst NADA Used Car Guide

Angela Lisulo Economist NADA Industry Analysis Division

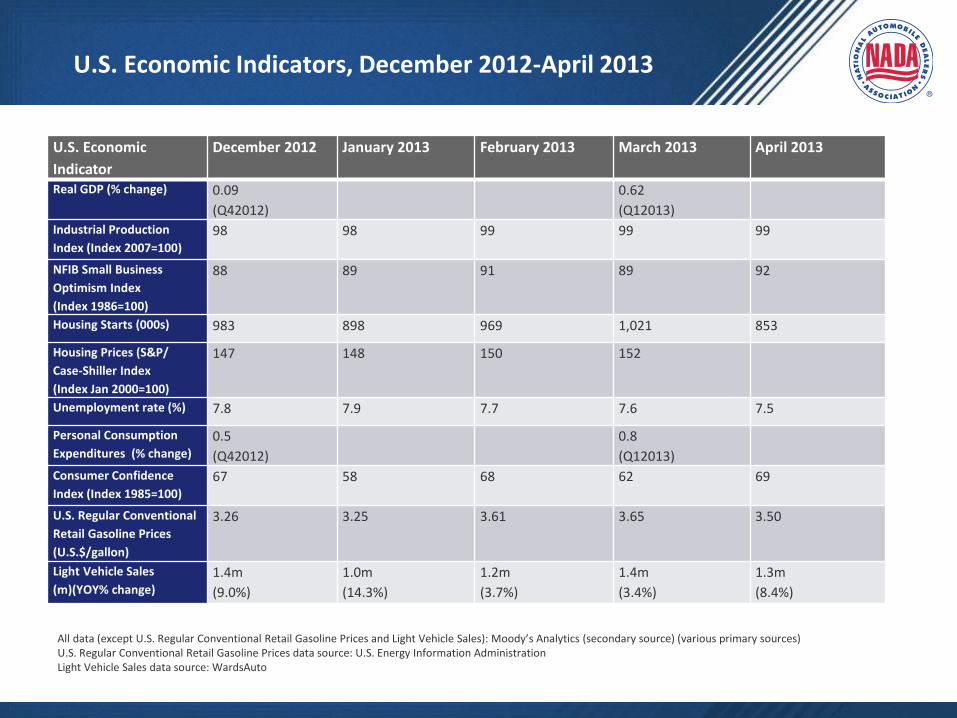

U.S. Economic Indicators, December 2012-April 2013

U.S. Economic

Indicator

December 2012 January 2013 February 2013 March 2013 April 2013

Real GDP (% change) 0.09

(Q42012)

0.62

(Q12013)

Industrial Production

Index (Index 2007=100)

98 98 99 99 99

NFIB Small Business

Optimism Index

(Index 1986=100)

88 89 91 89 92

Housing Starts (000s) 983 898 969 1,021 853

Housing Prices (S&P/

Case-Shiller Index

(Index Jan 2000=100)

147 148 150 152

Unemployment rate (%) 7.8 7.9 7.7 7.6 7.5

Personal Consumption

Expenditures (% change)

0.5

(Q42012)

0.8

(Q12013)

Consumer Confidence

Index (Index 1985=100)

67 58 68 62 69

U.S. Regular Conventional

Retail Gasoline Prices

(U.S.$/gallon)

3.26 3.25 3.61 3.65 3.50

Light Vehicle Sales

(m)(YOY% change)

1.4m

(9.0%)

1.0m

(14.3%)

1.2m

(3.7%)

1.4m

(3.4%)

1.3m

(8.4%)

All data (except U.S. Regular Conventional Retail Gasoline Prices and Light Vehicle Sales): Moody’s Analytics (secondary source) (various primary sources) U.S. Regular Conventional Retail Gasoline Prices data source: U.S. Energy Information Administration Light Vehicle Sales data source: WardsAuto

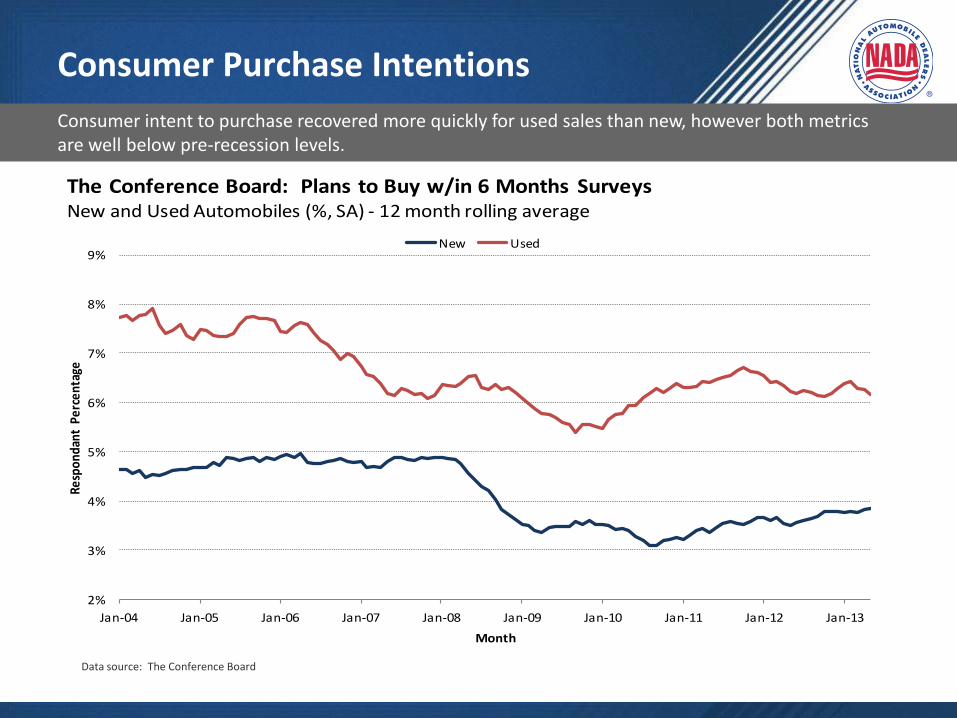

Consumer Purchase Intentions

2%

3%

4%

5%

6%

7%

8%

9%

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

Resp

onda

nt P

erce

ntag

e

Month

The Conference Board: Plans to Buy w/in 6 Months SurveysNew and Used Automobiles (%, SA) - 12 month rolling average

New Used

Source: The Conference Board

Consumer intent to purchase recovered more quickly for used sales than new, however both metrics are well below pre-recession levels.

Data source: The Conference Board

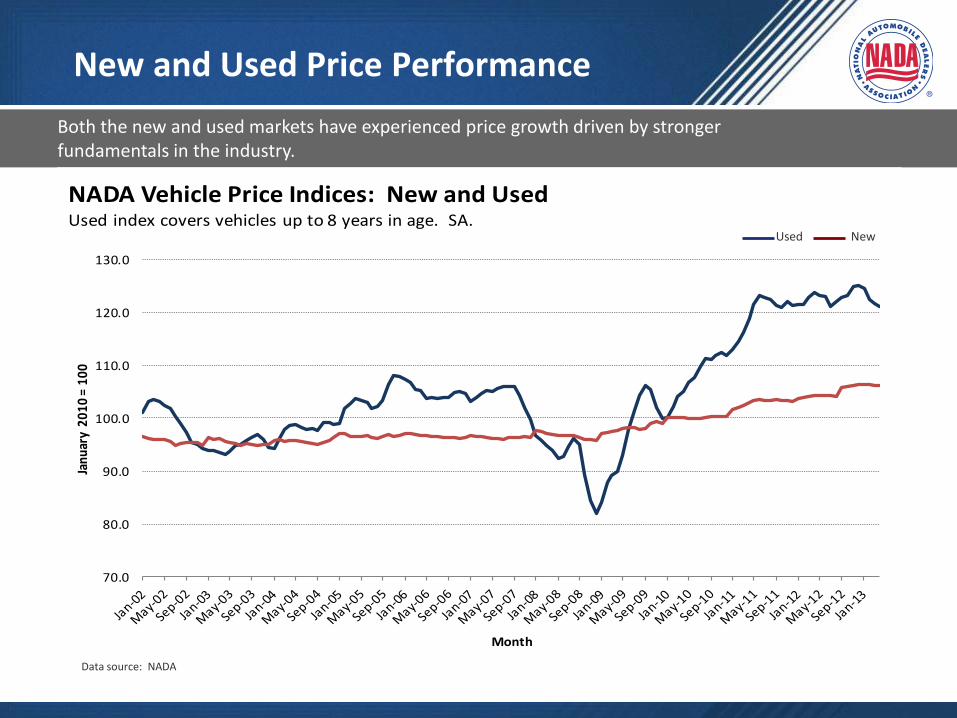

New and Used Price Performance

Both the new and used markets have experienced price growth driven by stronger fundamentals in the industry.

70.0

80.0

90.0

100.0

110.0

120.0

130.0

Janu

ary

2010

= 1

00

Month

NADA Vehicle Price Indices: New and UsedUsed index covers vehicles up to 8 years in age. SA.

Source: NADA

Used New

Data source: NADA

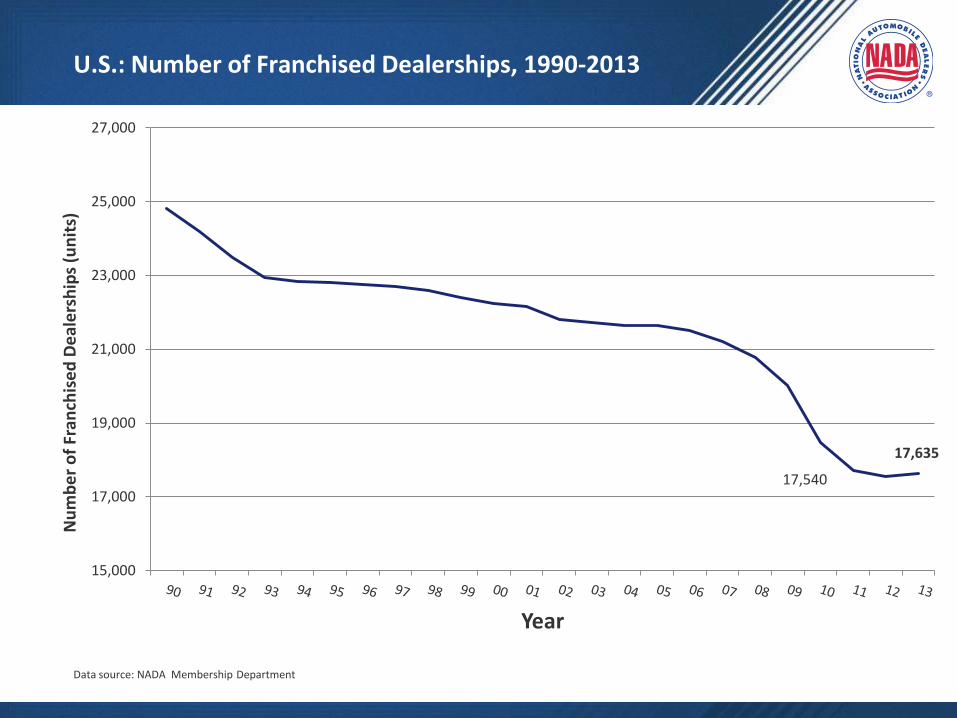

U.S.: Number of Franchised Dealerships, 1990-2013

Data source: NADA Membership Department

17,540

17,635

15,000

17,000

19,000

21,000

23,000

25,000

27,000

Nu

mb

er

of

Fran

chis

ed

De

ale

rsh

ips

(un

its)

Year

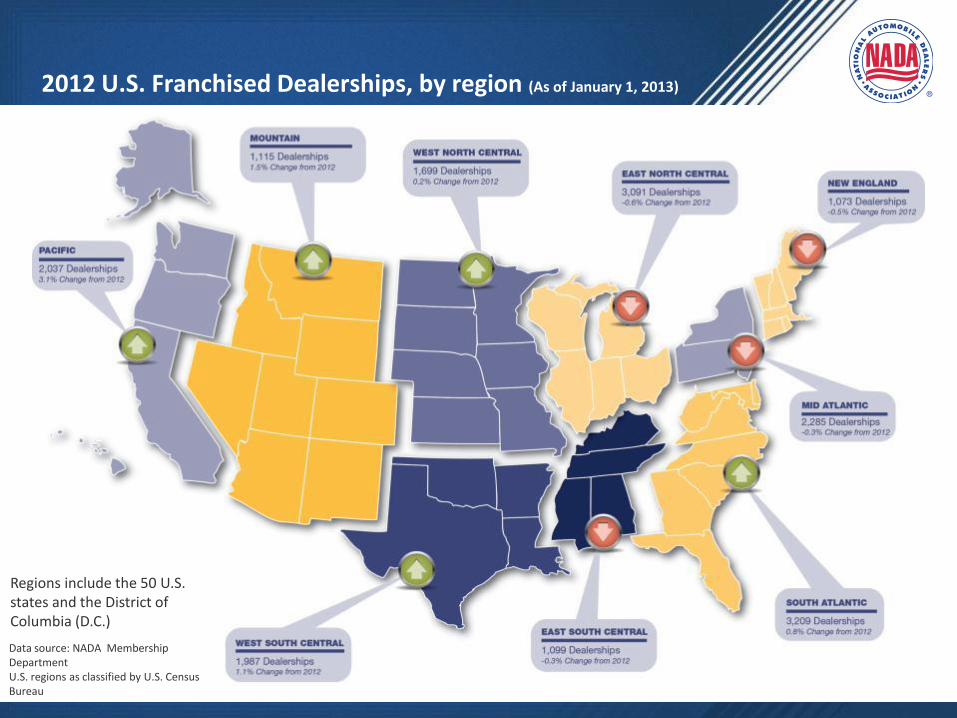

Regions include the 50 U.S. states and the District of Columbia (D.C.)

Data source: NADA Membership Department U.S. regions as classified by U.S. Census Bureau

2012 U.S. Franchised Dealerships, by region (As of January 1, 2013)

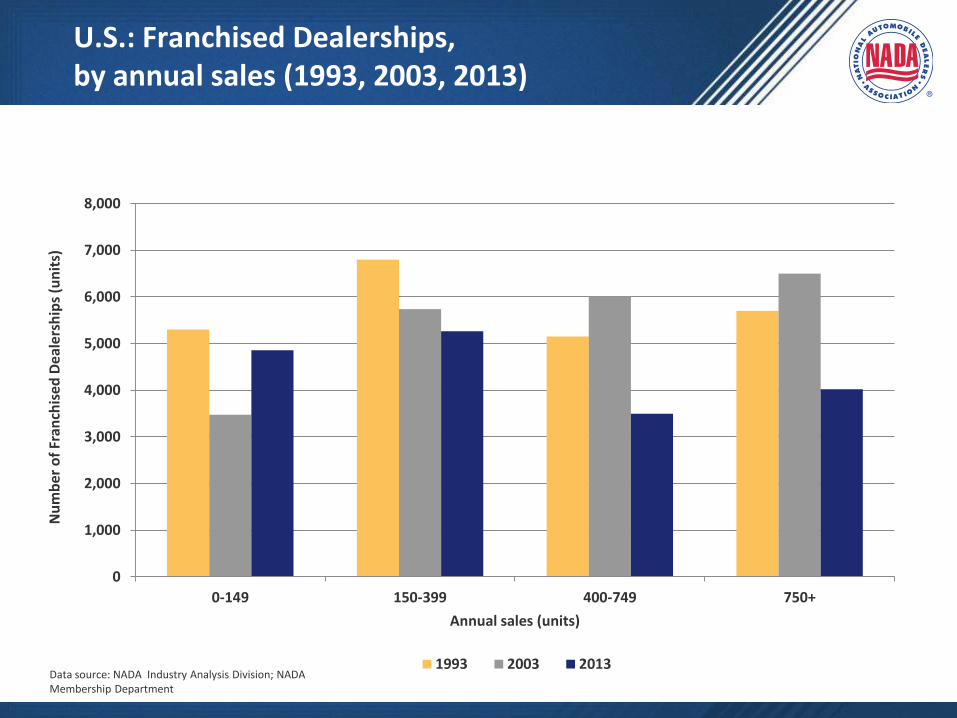

U.S.: Franchised Dealerships, by annual sales (1993, 2003, 2013)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

0-149 150-399 400-749 750+

Nu

mb

er o

f Fr

anch

ise

d D

eal

ersh

ips

(un

its)

Annual sales (units)

1993 2003 2013Data source: NADA Industry Analysis Division; NADA Membership Department

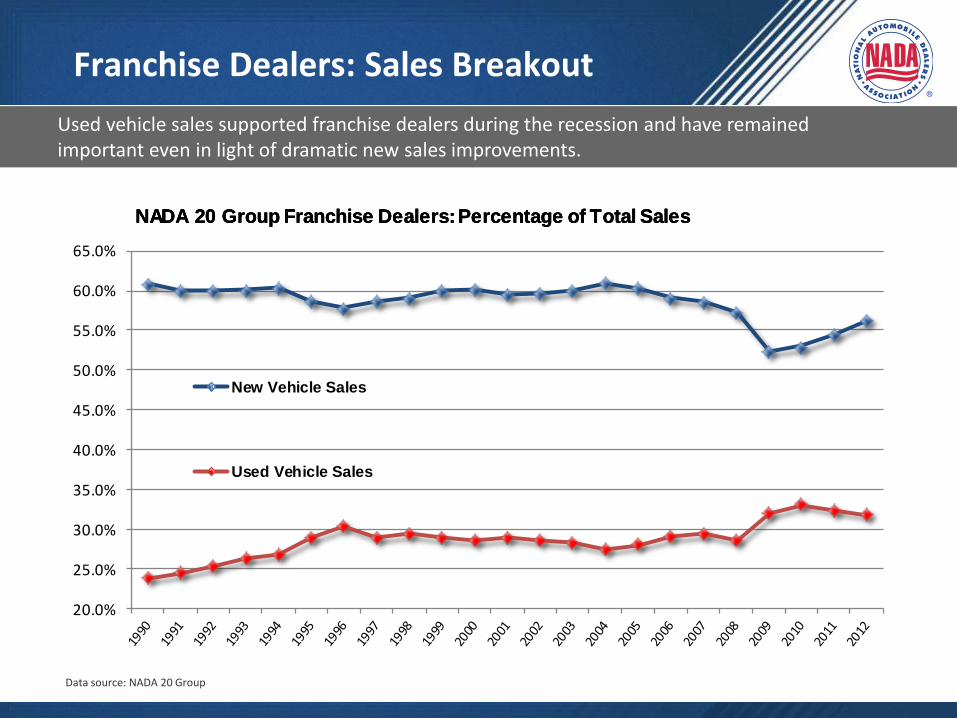

Franchise Dealers: Sales Breakout

Dealership sales have quickly recovered from the trough in 2009 and have reached record levels from our sample.

Data source: NADA 20 Group

$0

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$25,000,000

$30,000,000

$35,000,000

$40,000,000

NADA 20 Group Franchise Dealers: Total Dealership Sales in Dollars

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

55.0%

60.0%

65.0%

New Vehicle Sales

Used Vehicle Sales

NADA 20 Group Franchise Dealers: Percentage of Total SalesNADA 20 Group Franchise Dealers: Percentage of Total SalesNADA 20 Group Franchise Dealers: Percentage of Total Sales

Franchise Dealers: Sales Breakout

Used vehicle sales supported franchise dealers during the recession and have remained important even in light of dramatic new sales improvements.

Data source: NADA 20 Group

Franchise Dealers: Gross Profits

The viability of maintaining a strong used vehicle program is evident in the strong gross profit between the two channels.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

New Vehicle Sales

Used Vehicle Sales

NADA 20 Group Franchise Dealers: Gross Profit

Data source: NADA 20 Group

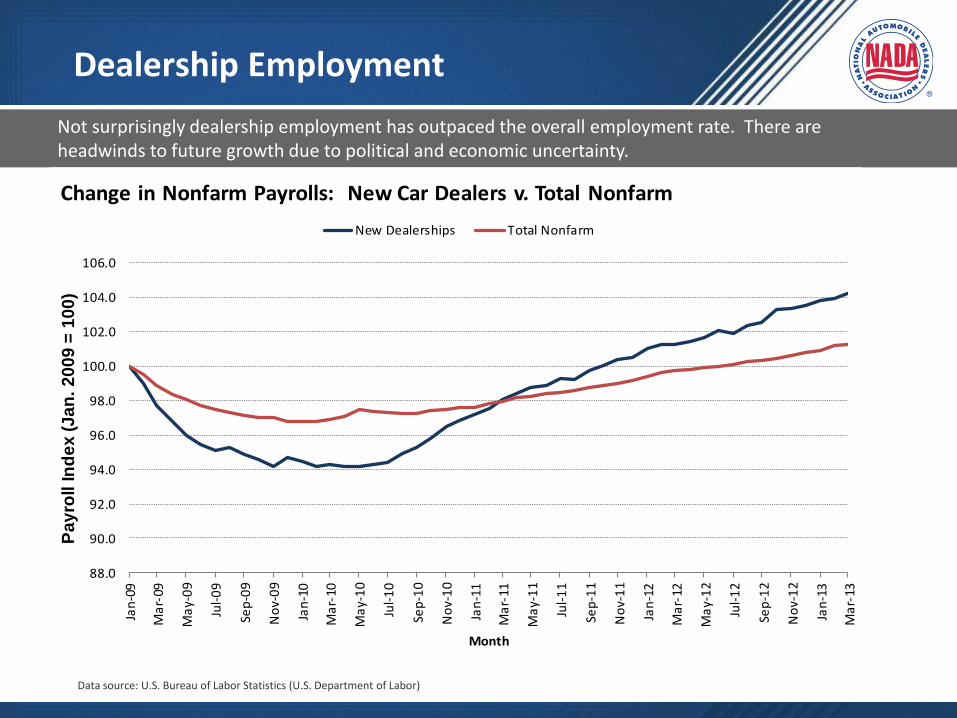

Dealership Employment

Not surprisingly dealership employment has outpaced the overall employment rate. There are headwinds to future growth due to political and economic uncertainty.

88.0

90.0

92.0

94.0

96.0

98.0

100.0

102.0

104.0

106.0

Jan

-09

Ma

r-09

Ma

y-0

9

Jul-

09

Sep

-09

No

v-0

9

Jan

-10

Ma

r-10

Ma

y-1

0

Jul-

10

Sep

-10

No

v-1

0

Jan

-11

Ma

r-11

Ma

y-1

1

Jul-

11

Sep

-11

No

v-1

1

Jan

-12

Ma

r-12

Ma

y-1

2

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Ma

r-13

Pa

yro

ll I

nd

ex

(J

an

. 2

00

9 =

10

0)

Month

Change in Nonfarm Payrolls: New Car Dealers v. Total Nonfarm

New Dealerships Total Nonfarm

Source: BLSData source: U.S. Bureau of Labor Statistics (U.S. Department of Labor)

Public Dealership Groups

“We continue to expect industry new vehicle sales to be approximately mid-15 million units in 2013.”

~ Mike Jackson, Chairman/CEO, April 19, 2013

“Business environment continues to be favorable to retail automotive.”

~ April 23, 2013

“Expect revenue to grow by more than 10% (in 2013) through a combination of same-store growth and acquisitions.”

~ April 29, 2013

All four of the nation’s top dealer groups reported record earnings from continuing operations for Q1 2013. Many of the public groups emphasized the importance of used vehicle sales as a contributor to their high profitability.

• Pent-up demand has increased and consumers still intend to buy

• Used vehicle prices remain robust – Helps consumers in terms of trade-in values;

allows for more aggressive leasing

~ May 2, 2013

AutoNation:

Penske Automotive:

Sonic Automotive:

Group 1 Automotive:

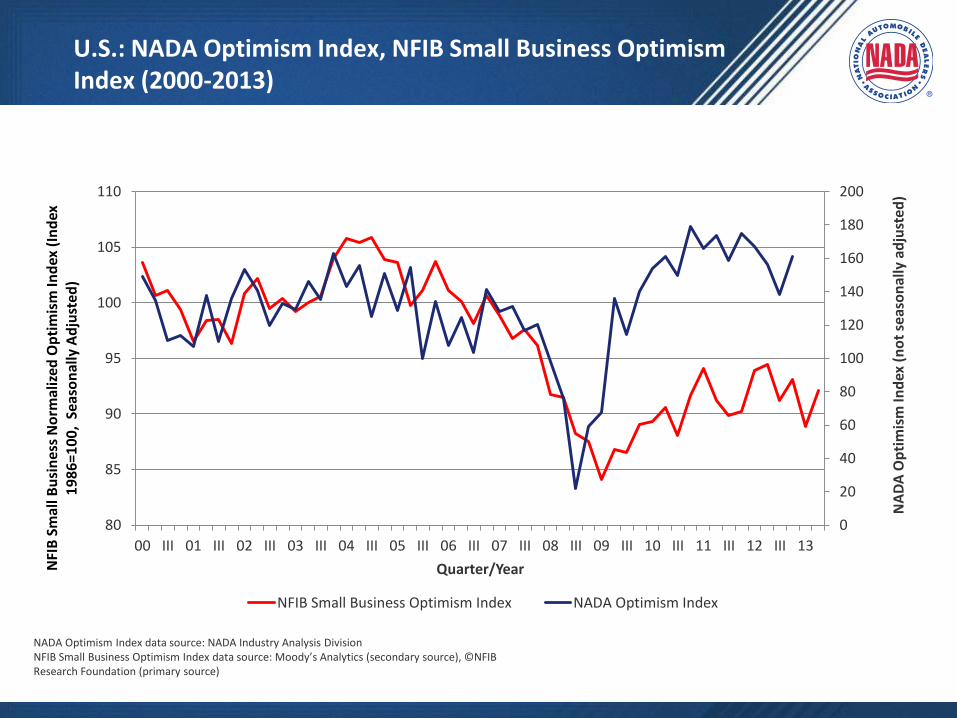

U.S.: NADA Optimism Index, NFIB Small Business Optimism Index (2000-2013)

NADA Optimism Index data source: NADA Industry Analysis Division NFIB Small Business Optimism Index data source: Moody’s Analytics (secondary source), ©NFIB Research Foundation (primary source)

0

20

40

60

80

100

120

140

160

180

200

80

85

90

95

100

105

110

00 III 01 III 02 III 03 III 04 III 05 III 06 III 07 III 08 III 09 III 10 III 11 III 12 III 13

NA

DA

Op

tim

ism

Ind

ex (

no

t se

aso

nal

ly a

dju

sted

)

NFI

B S

mal

l Bu

sin

ess

No

rmal

ized

Op

tim

ism

Ind

ex (

Ind

ex

19

86

=10

0,

Seas

on

ally

Ad

just

ed)

Quarter/Year

NFIB Small Business Optimism Index NADA Optimism Index

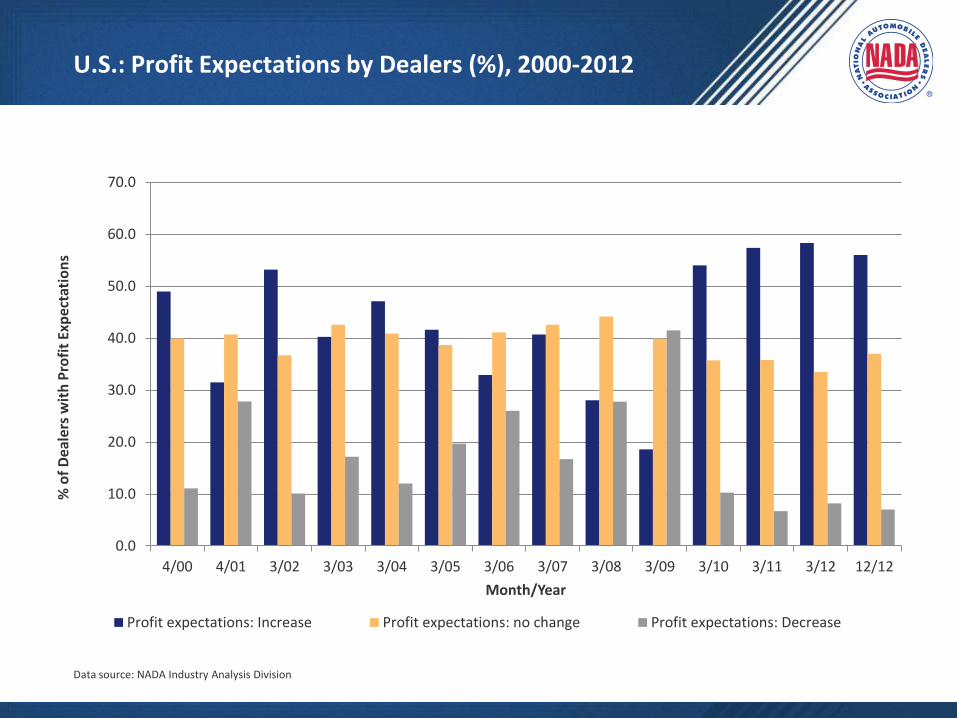

U.S.: Profit Expectations by Dealers (%), 2000-2012

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

4/00 4/01 3/02 3/03 3/04 3/05 3/06 3/07 3/08 3/09 3/10 3/11 3/12 12/12

% o

f D

eale

rs w

ith

Pro

fit

Exp

ecta

tio

ns

Month/Year

Profit expectations: Increase Profit expectations: no change Profit expectations: Decrease

Data source: NADA Industry Analysis Division