money, credit and finance

DESCRIPTION

Money, credit and financeTRANSCRIPT

Money, Credit and Finance

Outline

1. The main claims of the post-Keynesian views on money, credit and finance

2. PK monetary theory in historical perspective. 3. The horizontalist and structuralist

controversies. 4. New developments in monetary policy

implementation. 5. Open-economy monetary economics. 6. The integration of PK monetary economics

into PK macroeconomics

Part I

Post-Keynesian monetary sub-schools

Post-KeynesianMonetary

Economics

Structuralists HorizontalistsAccommodationists

Circuit theory

Paris and Naples

Emissions theoryDijon

Free University of

Berlin School

ChartalistsUKCM school

Neoclassical monetary sub-schools

Neoclassical monetary schools

Monetarists IS/LM

New ParadigmKeynesian

(StiglitzGreenwald)

WicksellianNew Consensus

M

i

Horizontalists(New Consensus)

MonetaristsIS/LMVerticalists

Structuralists(New Paradigm)

Ms

Ms Ms

A simplified overviewof endogenous money

Endogenous money supply: A PK claim now accepted by many schools

Post-Keynesians Neo-Austrians New Keynesians

(New consensus authors), Woodford, Taylor, Roemer, Meyer

(New Paradigm Keynesians, focus on credit) Stiglitz, Greenwald, Bernanke

Real business cycle theorists Barro, McCallum

Goodhart

Main features in monetary economicsFeatures PK school Neoclassical

Money Has counterpart entries

Falls from an helicopter

Money is seen As a flow and as a stock

A stock

Money is tied to Production Exchange

The supply of money is

Endogenous Exogenous

Main concern with Debts, credits Assets, money

Causality Reversed: credits make deposits

Reserves allow deposits

Credit rationing due to Lack of confidence Asymetric information

Main features, interest rates

Features PK School Neoclassical

Interest rates Are distribution variables

Arise from market laws

Liquidity preference Determines the differential relative to base rate

Determines the interest rate

Base rates Are set by the central bank

Are influenced by market forces

The natural rate Takes multiple values or does not exist

Is unique, based on thrift and productivity

Main features, macro implications

Features PK School Neoclassical

A restrictive monetary policy

Has negative effects in short and long run

Has negative effects only in the short run

Schumpeter’s distinction

Monetary analysis

(monetized production economy)

Real analysis

(money neutrality,

inessential veil)

Macro causality Investment determines saving

Saving determines investment

Inflation The growth in money stock aggregates is caused by the growth in output and prices

Price inflation is caused by an excess supply of money

Two kinds of financial systems, according to Hicks 1974

The overdraft financial system

Firms are in debt towards commercial banks

Commercial banks are in debt towards the central bank

The auto or asset-based financial system

Firms finance investment with retained earnings

Commercial banks have large amounts of T-bills in assets

Overdraft vs Asset-based systems

Overdraft systems 90% or more of the world

financial systems (including the pre-euro Bundesbank)

Ignored by textbooks No control on HPM, except

through credit control Clarifies how the monetary

system functions In a sense, all systems are of

the overdraft type: no central bank controls directly the supply of money

Asset-based systems Only in some anglo-saxon

countries Described by mainstream

textbooks Based on open-market

operations; is said to be efficient in controlling the money stock

Puts a veil on the operating procedures of monetary systems

Simplified neoclassical view

Central bank balance sheet

Assets Liabilities

Foreign reserves Banknotes

Domestic T-bills Reserves of commercial banks

Simplified PK view

Central bank balance sheet

Assets Liabilities

Foreign reserves Banknotes

Domestic T-bills Reserves of commercial banks

Loans to domestic banks Government deposits

(Central bank bills)

Part II

PK monetary theory in historical perspective

Cambridge proverbs

« Highbrow opinion is like a hunted hare; if you stand in the same place or nearly in the same place it can be relied upon to come round to you in circle. » (D.H. Robertson 1956)

« Economic ideas move in circles: stand in one place long enough, and you will see discarded ideas come round again. » (A.B. Cramp 1970)

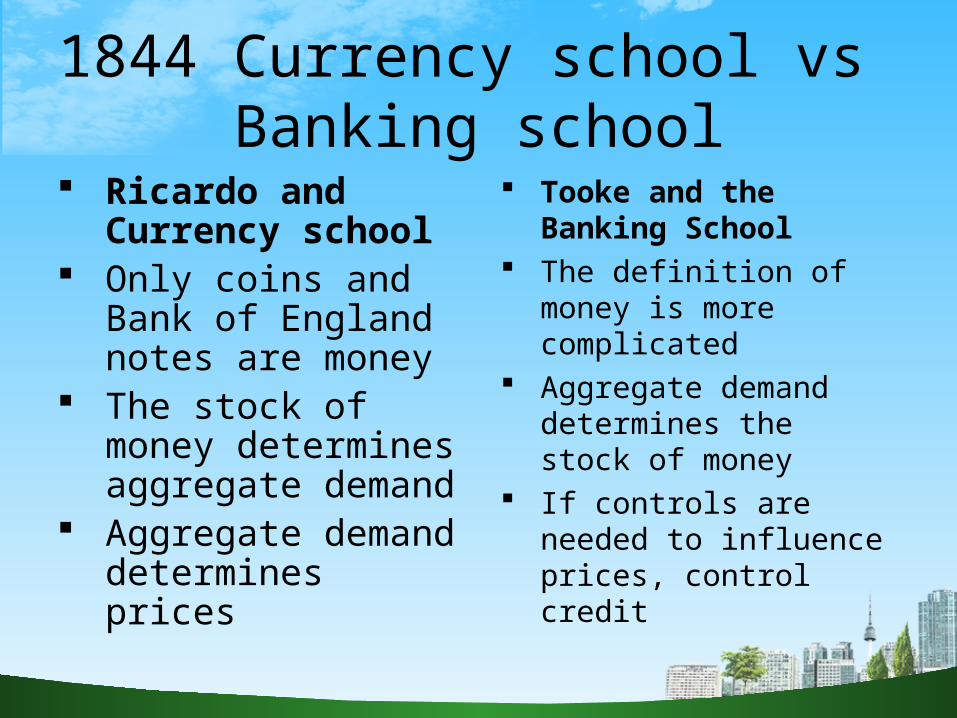

1844 Currency school vs Banking school

Ricardo and Currency school

Only coins and Bank of England notes are money

The stock of money determines aggregate demand

Aggregate demand determines prices

Tooke and the Banking School

The definition of money is more complicated

Aggregate demand determines the stock of money

If controls are needed to influence prices, control credit

Most of modern monetary controversies can be brought back to the Currency school and

Banking school debates Definitions of money Stability of the velocity of money Stability of the deposit multiplier Money versus credit The operational target: the supply of high

powered money or interest rates? Endogenous or exogenous money (reversed

causality) Inflation through excess money growth or

excess wage growth

An additional complexity

An author can be found in two different camps at a time. This is often the case of creative authors. Wicksell (who pretends to support the Quantity

Theory, while throwing it back into question) Keynes (who pretends to attack the Quantity

Theory, while barely modifying it)

Hence it is difficult or even impossible to classify some authors

Keynes, a proto Monetarist?

« We are all Keynesians now, says Friedman, at the height of the IS/LM frenzy.

This can be better understood by reading Kaldor (1982), according to whom Keynes’s 1936 monetary theory is « a modification of the quantity theory of money, not its abandomnent».

Keynes 1930 (The Treatise on Money), despite some of its innovations and some indications about money endogeneity, is still very much in the Quantity tradition: He objects to those who believe that interest rate ought to be the main

operational target of central banks; He approves of the money multiplier (Phillips 1920); He supports the use of quantitative instruments for the conduct of monetary

policy: open market operations and changes in reserve coefficients, which, at that time, were only advocated by Americans and the Fed.

Two different viewpoints, already well identified in 1959

« There are two opposing viewpoints concerning the relationship between the supply of and the demand for money. On the one hand – for the quantity theorists and Keynes – the quantity theory of money is believed to be fixed independently by the banking system…. The opposing view – held by the Banking school and Wicksell – is that the banks set not a quantity but a price. The banking system fixes a rate (or a set of rates) for the money market and then lends however much borrowers ask for, provided that they can offer satisfactory collaterals». Jacques Le Bourva 1959 (1992).

Back to the future?

« The quantity theory of money is dying. The most banal criticisms lodged against it, and long since accepted as truths by all, concern the instability of the velocity of circulation of money …. The principal criticism of the theory, however, rests on the determination of the money supply. It is essential to the validity of the quantity theory that the quantity of money be a variable that is independent of national income and the current economic situation. This implies tha the bankers fix the amount of the money supply by some sovereign act dictated from the heights of their own secret Olympus. This is precisely the premise of the quantity theory that is no longer accepted in France today, and so the Banking school and Wicksell prevail. » Le Bourva 1962 (1992)

Quantity theory of money (Academics) vs the Radcliffe Commission 1959 (Central bankers and

Kaldor and Kahn)

Quantity theory Control of the money

supply, in particular reserves, by central banks

The velocity of money and the money multiplier are quasi constants

Causality runs from money to prices

Radcliffe Commission The central bank controls

interest rates, but very indirectly only money aggregates

The velocity of money is unstable (many substitutes): « general liquidity » concept

Monetary policy only has a moderate effect on inflation, which depends on many other factors

Credit controls?

The 1960s and 1970s The quantity theory and Monetarism gradually take

over.. The Radcliffe view is strongly criticized by Old

Keynesians, who consider it dépassé: « There still do exist in England men whose minds were

fromed in 1939, and who haven’t changed a thought since that time, and who … say money doesn’t matter. They have embalmed their views in the Radcliffe Committee, one of the most sterile operations of all time» Samuelson 1969

With the oil shocks of the 1970s and the productivity slowdown, inflation rises.

Monetarism and monetary targets flourish.

The scourge of monetarism induces a post-Keynesian reaction

Until 1970, even 1980, the PK monetary theory is unclear. Its best exposition can be found in Joan Robinson’s 1956 book, The Accumulation of Capital, but it is towards the end of the book, after a complex exposition of growth theory and value theory, so that hardly anybody pays attention to her monetary theory.

Before 1970, the main criticisms against the quantity theory are based on the instability of the velocity of money or that of the money multiplier (Kaldor 1958, Minsky 1957). Only Robinson and Kahn have a proper understanding of the crucial issue

Starting in 1970, the more essential issue of reversed causality is brought to the forefront by a number of authors.

Reverse causality: three groups of authors

Researchers at the Fed (Holmes 1969, Lombra, Torto, Kaufman, Feige+McGee)

Post-Keynesians Cramp 1970, Kaldor 1970 and 1980, Robinson 1970 Davidson and Weintraub 1973, Moore 1979)

Iconoclasts: Le Bourva 1959 and 1962, F.A. Lutz 1971

The supply of money is not independent; it is determined by demand.

Credits make deposits; deposits make reserves. Short-term interest rates are the exogenous variable. The money/price causality is reversed. We are back to the Banking School and current PKE!

Part III

The Structuralist vs Horizontalist PK controversies

“A storm in a tea cup” (Moore 2001) ?

The first exponents of money endogeneity were mainly “horizontalists”: Robinson, Kahn, Le Bourva, Kaldor, Moore, and the French “circuitists”.

The main “structuralist” critics were Le Héron, Dow, Wray, Howells, Pollin, and Palley, many of which got their inspiration from Minsky.

As Fontana (2003) puts it, “structuralists took over where the accommodationists had stopped”.They brought some clarifications and provided new details. For instance, they insisted that spreads between interest rates could quickly vary, due to assessed default risks or changes in liquidity confidence. Sometimes, however, they constructed a “horizontal strawman” in an effort to highlight the originality of their contributions.

To a large extent, the controversy has petered out, for reasons that will soon be given (although Rochon has rekinkled some excitement by editing a forthcoming book on the topic!).

The horizontalist claims

1. The supply curve of money (or high powered money) can best be represented as a flat curve, at a given interest rate. The short-term interest rate can be viewed as exogenous, under the control of the central bank, within a reasonable range.

2. There can never be an excess supply of money. 3. The supply curve curve of credit can best be

represented as flat curves, at a given interest rate (or set of interest rates).

4. Central banks cannot exert quantity constraints on the reserves of banks.

The structuralist points 1a. What about the reaction function of the central bank? [Chick

1977, Rousseas 1986, Palley 1991, Musella and Panico 1995] 1b. Long-term and other market-determined rates “cause” the

overnight rate [Pollin 1991] 2. If loans create deposits, how do we know that households wish

to hold these deposits? [Howells 1995] 3a. What about credit rationing (shape of credit supply curve)?

[Dow2 1989] 3b. What about borrower’s risk? [Minsky 1975, Dow and Earl 1982] 3c. and lender’s risk (liquidity preference of banks)? [Dow2, Wray

1989, Chick and Dow] 4a. Surely the central bank does not always “accommodate” and

hence exerts quantity constraints on bank reserves. [Pollin 1991] 4b. What about changes in the velocity of money and liability

management, which are the main sources of money endogeneity [Pollin 1991, Palley 1994]

The horizontalist answers I

1. On the horizontal supply of HPM: New operating procedures, based on a target overnight

rate, show clearly that central banks control the overnight rate and can set it at will; recent events also show that the central bank reaction function has a large discretionary component. Thus, we can still see the target overnight rate as an exogenous variable, under the full control of the central bank.

Of course, if, in general, higher economic activity is accompanied by higher inflation rates, then, through the central bank reaction function, higher interest rates are likely to accompany higher economic activity, and thus the supply of money or HPM will appear to be upward-sloping through time.

Horizontalist answers II

2. On the impossibility of excess money: The main argument is the “reflux principle”. The stock-flow consistent models of Godley have shown

that, despite the presence of an apparently independent money demand function and the presence of a supply of money function based on the supply of loans, flow-of-funds accounting is such that deposits must equate loans despite no such condition being inserted into the model.

In more sophisticated models, changes in liquidity preference by households will induce changes in relative rates; but this was never denied by Horizontalists.

Horizontalist answers III

3. On the horizontal supply of credit: It has been shown by Wolfson (1996) that there is no incompatibility

between credit rationing and horizontalism. It is now clearly established that higher economic activity does not

necessarily entail higher debt ratio for firms (contradicting the essence of Minsky’s financial fragility hypothesis). This is now recognized by Wray, a student of Minsky.

But of course, as firms move from one risk class to another, they will trigger higher interest rates.

The remaining issue is lender’s risk: recent events have shown that banks have no clue what their lender’s risk is, and so it cannot be ascertained that banks will raise interest rates if their balance sheet expands.

Loans

Interest rate

Notional demandCredit-

worthy demandi2

A N i1

Credit rationing when there is a reduction in bank confidence(Credit-worthy demand: demand with appropriate collateral:Cf. De Soto, and Heinsohn and Steiger)

A’

Horizontalist answers IV

4. On quantity restraints on bank reserves: There is no incompatibility between

horizontalism and bank innovations or liability management.

New central bank operating procedures clearly show what was hidden before: central banks passively try to provide the reserves being demanded by the banking system.

Conclusion

The original horizontalist depiction, that of Kaldor and Moore, is the most appropriate. Structuralists have helped to fill in some details. As Wray (2006) concludes:

“There cannot be any automatic and necessary impact

of spending on interest rates because loans and deposits can and normally do increase as spending rises. The overnight rate will change only if and when the central bank decides to allow it to do so. Short-term loan and deposit retail rates can be taken as a somewhat variable mark-up and mark-down from the overnight rate.

Part IV

New developments in monetary policy implementation by central

banks

New operationg procedures and horizontalism

Central banks have new operating procedures, although they are not that much different from what they used to be. They bring central banks closer to the « overdraft economy», and further away from the «asset-based econonomy» as defined by Hicks.

The procedures of some central banks are more transparent (than they were and than those of other central banks), so the horizontalist story is more obvious: Canada, Australia, Sweden

The procedures of other central banks are less transparent; but when interpreted in light of horizontalism, we can see that their operational logic is identical to that of the more transparent central banks (like the Fed).

The new operating procedures put in place in Canada and other such countries are fully compatible with the

PK monetary theory

Central banks set a target overnight rate, and a band around it

Commercial banks can borrow as much as they can at the discount rate

There are no compulsory reserves and no free reserves (zero net settlement balances)

The target rate is (nearly) achieved every day Central banks only pursue defensive operations, trying

to achieve zero net balances. When there are tensions, as during the recent subprime

financial crisis, they try their best to supply the extra amount of balances demanded by direct clearers (mainly banks)

Settlementbalances

Overnight rate

0 + (surplus)- (overdraft)

Target rate TR

Bank rate = TR+25pts

Rate on positive balances = TR-25pts

The Bank of Canada channel system

Two different justifications for the current interest rate procedures ?

Post-Keynesians Based on a

microeconomic justification

Tied to the inner functioning of the clearing and settlement system

Linked to the day-by-day, hour-per-hour, operations of central banks

New Consensus Based on the 1970 Poole

article A macroeconomic

justification If the IS curve is the most

unstable, use monetary targeting

If the LM curve is unstable (money demand is unstable), use interest rate targets

Poole 1970

Interest rate

OutputA

IS

LM

MT IT

LM

A = IT MT

IS

Investment is unstable:Use monetary targeting MTLess variability in output

Demand for money is unstable:Use interest rate targetingNo variability in output

ITIT

The microeconomic justification for interest rate targeting

Central bank interventions are essentially « defensive ». Their purpose is to compensate the flows of payments between the central bank and the banking sector.

These flows arise from: a) collected taxes and government expenditures; b) interventions on foreign exchange markets; c) purchases or sales of government securities, or repurchase of securities arrriving at maturity; d) provision of banknotes to private banks by the central bank.

Without these defensive interventions, bank reserves or clearing balances would fluctuate enormously from day to day, or even within an hour. The overnight rate would fluctuate wildly.

Authors who support the microeconomic explanation

Several central bank economists Bindseil 2004 ECB, Clinton 1991 BofC, Lombra

1974 and Whitesell 2003 Fed

Some post-Keynesian authors Eichner 1985, Mosler 1997-98, Wray 1998 and

neo-chartalists in general

Institutionalists Fullwiler 2003 et 2006

Bank of Sweden: overdraft system

« Lending to the banking system currently comprises a significant part of the Riksbank’s assets….

Stage 1 involves a forecast of … how much liquidity needs to be supplied or absorbed for the banks to be able to avoid using the deposit and lending facilities during the coming week …. Stage 3 involves executing open market operations to parry the daily fluctuations in the banking system’s current payments so the banking system will not need to utilise the facilities » Mitlind and Vesterlund, Bank of Sweden Economic Review, 2001

The Fed never tried to constaint reserves !

“The primary objective of the Desk’s open market operations has never been to ‘increase/decrease reserves to provide for expansion/contraction of the money supply’ but rather to maintain the integrity of the payments system through provision of sufficient quantities of Fed balances such that the targeted funds rate is achieved”. Fullwiler (2003)

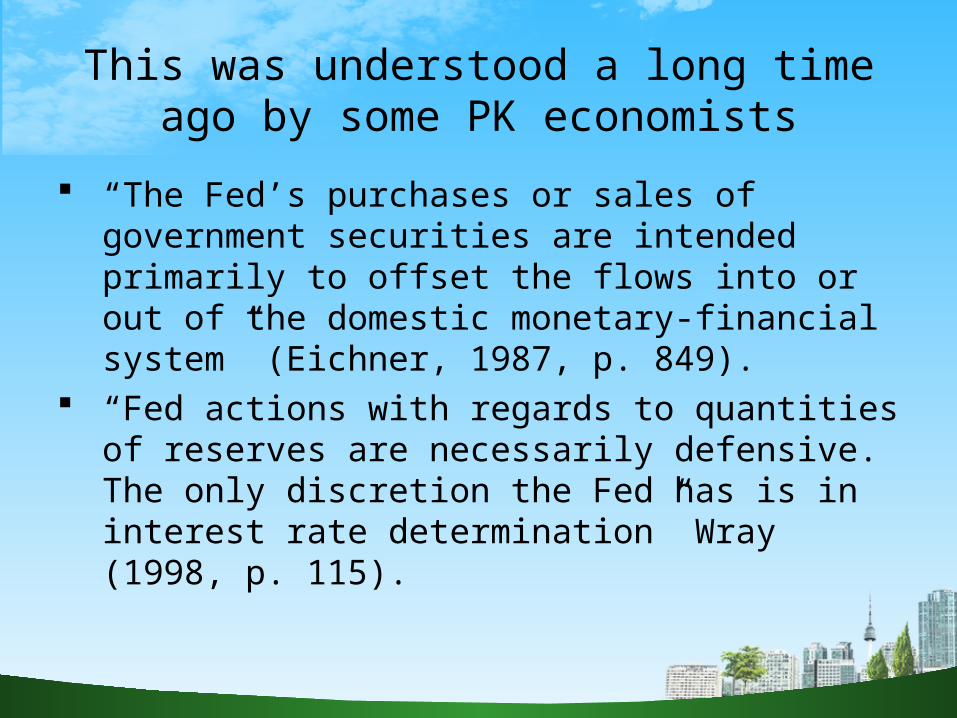

This was understood a long time ago by some PK economists

“The Fed’s purchases or sales of government securities are intended primarily to offset the flows into or out of the domestic monetary-financial system” (Eichner, 1987, p. 849).

“Fed actions with regards to quantities of reserves are necessarily defensive. The only discretion the Fed has is in interest rate determination” Wray (1998, p. 115).

There is no relationship between open market operations and bank reserves

“No matter what additional variables were included in the estimated equation, or how the equation was specified (e.g., first differences, growth rates, etc.), it proved impossible to obtain an R2 greater than zero when regressing the change in the commercial banking system’s nonborrowed reserves against the change in the Federal Reserve System’s holdings of government securities ....”(Eichner, 1985, pp. 100, 111).

Cf Poole in 1982, JMCB

«The old procedures [before 1979-1982] are best characterized as an adjustable federal funds rate peg system ….The new system [1979-1982] is qualitatively similar to the old ….The vast bulk of speculation about Fed intentions by money market participants concerns Fed attitudes toward interest rates…. The issue is always one of when and how hard the Fed will push rates ….»

Why is the federal funds rate sometimes different from the target rate ?

In Canada, the Bank is able to know with perfect certainty the demand for settlement (clearing) balances.

In the States, the Fed forecasts the net demand. Without reserve averaging, the federal funds rate would fluctuate widely between zero and the discount rate, as the set daily supply would be different from the given demand (two vertical curves).

With reserve averaging, banks can speculate on future values of the federal funds rate, and get extra reserves when the rate turns out to be low. The daily supply is still fixed, but the demand is interest elastic.

Problems with no tunnel and a not so credible target: central bank needs to be very precise in its daily forecast of reserves demand (Whitesell 2003)

Reserves

Expected Fed funds rate

Lending rate

Deposit rate

Demand for reserves

S S’

TargetFed rate

And it is the same for the ECB !

‘The logic of the ECB’s liquidity management ... can be summarised very roughly as follows: The ECB attempts to provide liquidity through its open market operations in a way that, after taking into account the effects of autonomous liquidity factors, counter-parties can fulfil their reserve requirements as an average over the reserve maintenance period. If the ECB provides more (less) liquidity than this benchmark, counterparties will use on aggregate the deposit (marginal lending) facility’ Bindseil and Seitz 2001

The case of the ECB: reserve averaging with a tunnel/corridor

Reserves

Target rate

Lending rate

Deposit rateDemand for reserves

SS’

The Cambridgian hare!

« Today’s views and practice on monetary policy implementation and in particular on the choice of the operational target have returned to what economists considered adequate 100 years ago, namely to target short-term interest rates » Ulrich Bindseil 2004, ECB, formerly from the Bundesbank

Part V

Open-economy monetary economics

Exogenous interest rates in open economies?

Wray 2006 argues that interest rates are clearly exogenous in flexible exchange regimes and endogenous in fixed exchange regimes, because the central bank must protect its reserves; but what about China!)

My position and that of Godley (The PK horizontalist position ?) is that interest rates are exogenous both in flexible and in fixed exchange rate regimes.

By contrast sophisticated neoclassical authors argue that interest rates are exogenous in neither flexible nor fixed exchange rate regimes.

Or, within the Mundell-Fleming model, IS/LM neoclassical authors argue that monetary policy is effective in a flexible exchange rate regime, but powerless in a fixed exchange rate regime, because the supply of money is then endogenous, as it varies in line with the balance of payments.

A critique of the Mundell-Fleming model in fixed exchange regime

In the Mundell-Fleming model, the supply of money is endogenous, but still supply-led; demand must adjust to it.

In PKE, the supply of money is endogenous, but it is demand-led, as in a close economy. Any increase in foreign reserves will be compensated by a decrease in another asset of the central bank, or will be compensated by an increase in some liability of the central bank.

This is the compensation thesis, or the thesis of endogenous sterilization (Godley and Lavoie 2005-06).

Simplified PK view

Central bank balance sheet

Assets Liabilities

Foreign reserves Banknotes

Domestic T-bills Reserves of commercial banks

Loans to domestic banks Government deposits

(Central bank bills)

A critique of the sophisticated neoclassical model in flexible exchange regimes

The neoclassical argument is that changes in expected future spot exchange rates determine the forward rate relative to the spot rate.

This differential, through the covered interest parity condition, which is known to hold at all times, determines the domestic interest rate relative to world rates.

The answer to this claim is, once again, reverse causality (Smithin 1994, Lavoie 2000). It is the differential between domestic and world interest rates that determines, nearly as an identity, the differential between the forward and the spot exchange rates. The forward rate has nothing to do with the expected spot rate. Forward rates in no way predict future spot rates (Moosa 2004).

Part V

The integration of PK monetary economics into PK macroeconomics

The integration of PK monetary economics into PK macroeconomics

(a) in PK models competing with New Consensus models, Rochon and Setterfield 2007, Hein and Stockhammer (see lecture on Friday)

(b) in PK growth and distribution models; (c) through the stock-flow consistent

approach (SFC) tied to flow-of-funds analysis.

The integration of PK monetary economics into PK models of growth and distribution

Very early on, it was pointed out that neo-Keynesian models of growth were neglecting monetary factors (Kregel 1985, “Hamlet without the Prince”).

For instance, Davidson (1972) pointed out that the famous neo-Pasinetti model of Kaldor (1966), which, in a very astute way, introduced stock market equities in a neo-Keynesian model, was omitting money balances.

The same drawback hurt early Kaleckian growth models.

The situation started to change only in the early 1990s, when the impact of interest rates was considered explicity, and when debt ratios also got introduced, along with cash-flow issues or interest payments relative to profits.

The case of the Kaleckian model

The canonical Kaleckian growth model is made up of three equations: an investment function, a saving function, and a pricing function.

Obviously the interest rate can be introduced into the investment function.

Should it be the real interest rate (higher opportunity costs) or the nominal interest rate (lower cash flow, lower retained earnings)?

But if so, an increase in the interest rate also has an impact on the saving function (reducing the overall saving rate).

And the interest rate may also have an impact on the normal profit rate (the Banking School argument, picked up by Sraffians), thus having an impact on the markup.

And all these will have an impact on the debt ratio, and hence may have a feedback effect on the investment function.

Things quickly get more complicated. Despite assuming short-run stability, there may not be long-run stability (the debt ratio may explode in the long run).

What if we introduce inflation and unemployment. More complications! [See Hein’s book 2008]

The Stock-flow consistent approach

The Holy Grail of PKE has always been the full integration of monetary and real macroeconomic analysis, i.e., provide a true “Monetary” analysis in the Schumpeter sense.

Until recently, this seemed like a rather impossible task. Godley (1996, 1999) has now done it, under the name of SFC.

[Other authors, around W. Semmler, also achieve something nearly similar]

Portfolio and liquidity preference issues, along with banking and financial stocks of assets and liabilities, are now tied with flows of production, income, and expenditures. Deflated and monetary variables can also be carefully distinguished.

The method is presented in Godley and Lavoie (2007). In my view, the method is particularly appropriate to model the

interaction between (Minsky) financial crises and real crises. The lecture this evening will give a simple example of SFC.