module 9 business deductions. module topics n statutory scheme for deductions n §162 business...

TRANSCRIPT

Module 9 Business DeductionsBusiness Deductions

Module Topics

Statutory Scheme for DeductionsStatutory Scheme for Deductions §162 Business Deductions: The Basic §162 Business Deductions: The Basic

RequirementsRequirements Prohibited DeductionsProhibited Deductions Deductions Common to Most BusinessesDeductions Common to Most Businesses Special Deductions for CorporationsSpecial Deductions for Corporations Capitalization IssuesCapitalization Issues

Statutory Scheme for Deductions

Key Learning ObjectiveKey Learning Objective

Apply the three-tier expense deduction Apply the three-tier expense deduction classification schemeclassification scheme

Tax Concept

No expenditure is deductible unless allowed No expenditure is deductible unless allowed by a provision in the tax lawby a provision in the tax law Specifically authorized by the Code, orSpecifically authorized by the Code, or Satisfies general criteriaSatisfies general criteria

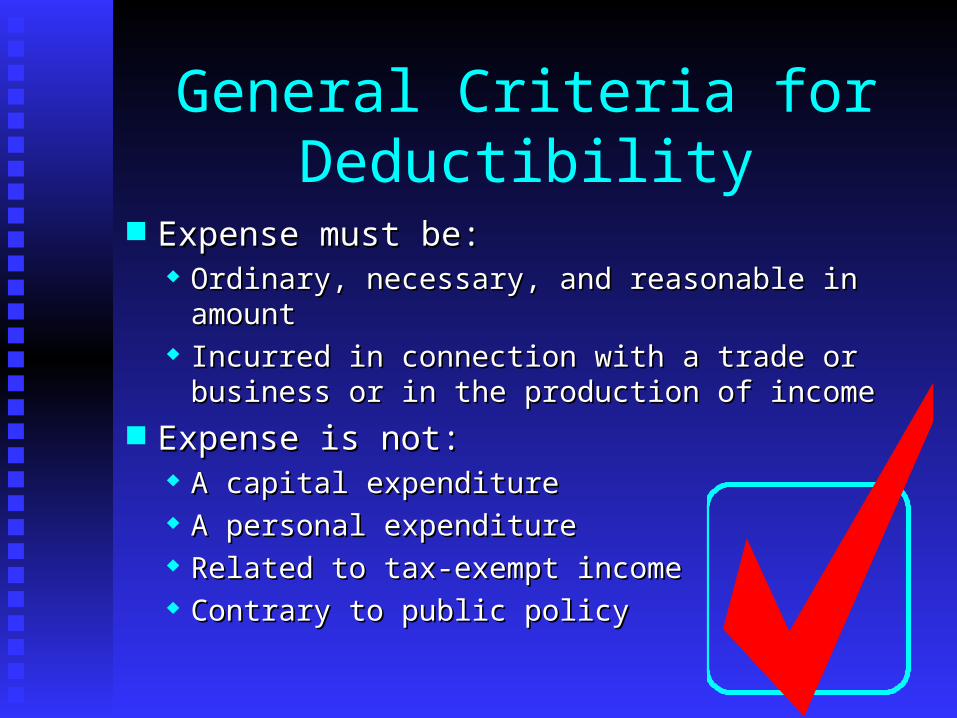

General Criteria for Deductibility

Expense must be:Expense must be: Ordinary, necessary, and reasonable in amountOrdinary, necessary, and reasonable in amount Incurred in connection with a trade or business or in Incurred in connection with a trade or business or in

the production of incomethe production of income Expense is not:Expense is not:

A capital expenditureA capital expenditure A personal expenditureA personal expenditure Related to tax-exempt incomeRelated to tax-exempt income Contrary to public policyContrary to public policy

Deduction Classification Scheme

Trade or business deductions--§162Trade or business deductions--§162 Production of income deductions--§212Production of income deductions--§212 Statutory personal deductionsStatutory personal deductions

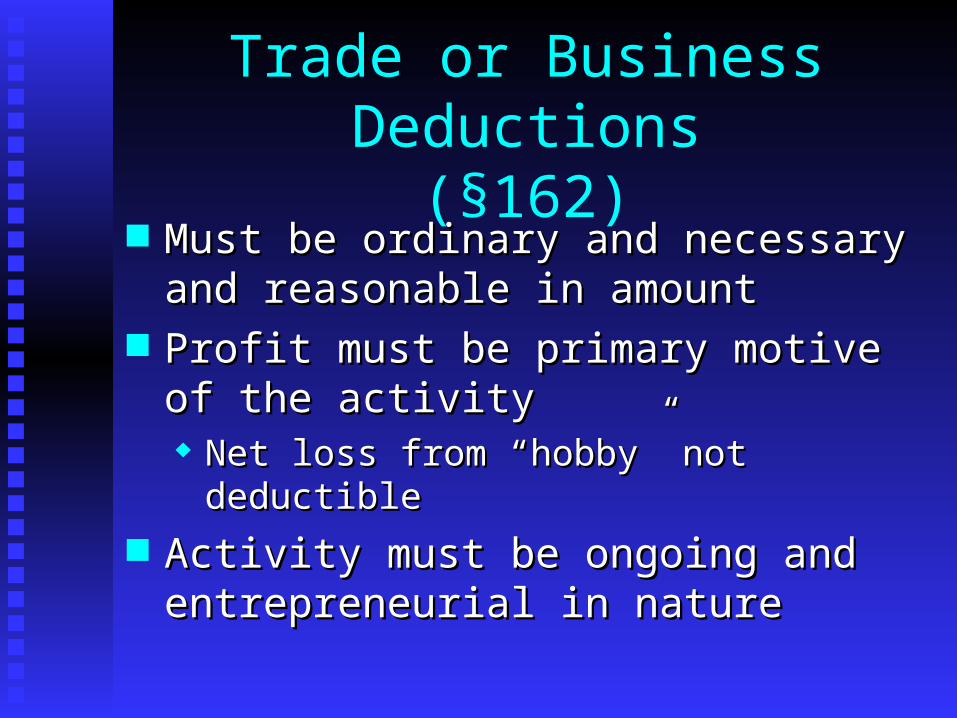

Trade or Business Deductions(§162)

Must be ordinary and necessary and Must be ordinary and necessary and reasonable in amountreasonable in amount

Profit must be primary motive of the Profit must be primary motive of the activityactivity Net loss from “hobby” not deductibleNet loss from “hobby” not deductible

Activity must be ongoing and Activity must be ongoing and entrepreneurial in natureentrepreneurial in nature

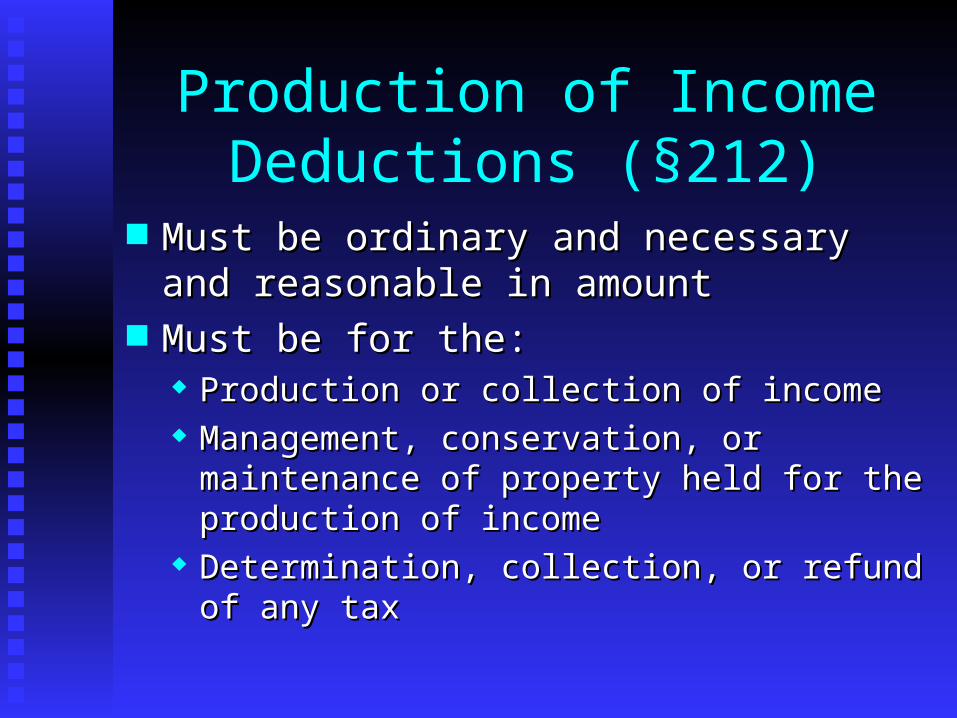

Production of Income Deductions (§212)

Must be ordinary and necessary and Must be ordinary and necessary and reasonable in amountreasonable in amount

Must be for the:Must be for the: Production or collection of incomeProduction or collection of income Management, conservation, or maintenance of Management, conservation, or maintenance of

property held for the production of incomeproperty held for the production of income Determination, collection, or refund of any taxDetermination, collection, or refund of any tax

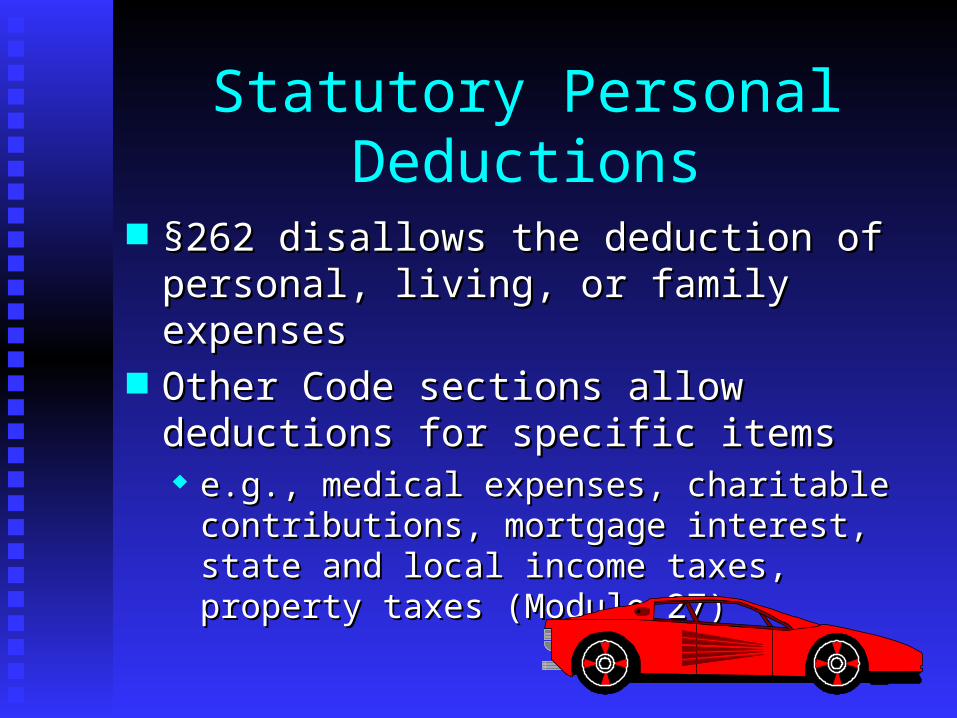

Statutory Personal Deductions

§262 disallows the deduction of personal, §262 disallows the deduction of personal, living, or family expensesliving, or family expenses

Other Code sections allow deductions for Other Code sections allow deductions for specific itemsspecific items e.g., medical expenses, charitable contributions, e.g., medical expenses, charitable contributions,

mortgage interest, state and local income taxes, mortgage interest, state and local income taxes, property taxes (Module 27)property taxes (Module 27)

§162 Business Deductions: The Basic Requirements

Key Learning ObjectiveKey Learning Objective

Apply the ordinary, necessary, and Apply the ordinary, necessary, and reasonableness requirements for business reasonableness requirements for business deductionsdeductions

Basic Requirements

OrdinaryOrdinary Acceptable, given the circumstancesAcceptable, given the circumstances

NecessaryNecessary Appropriate when incurredAppropriate when incurred

ReasonableReasonable Not lavishNot lavish

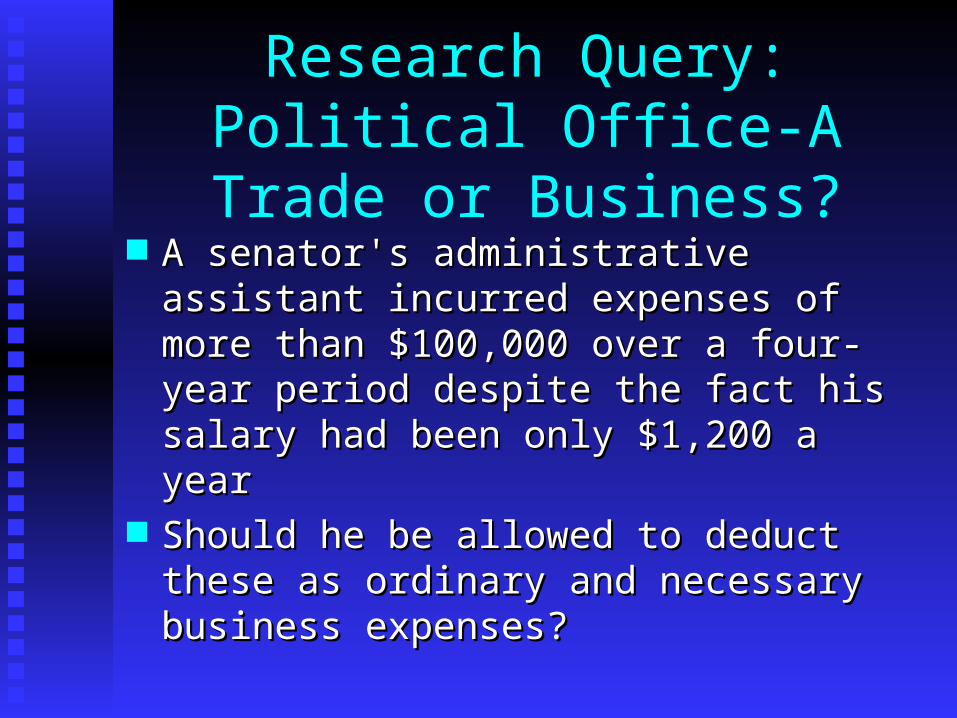

Research Query: Political Office-A Trade or Business?

A senator's administrative assistant incurred A senator's administrative assistant incurred expenses of more than $100,000 over a expenses of more than $100,000 over a four- year period despite the fact his salary four- year period despite the fact his salary had been only $1,200 a yearhad been only $1,200 a year

Should he be allowed to deduct these as Should he be allowed to deduct these as ordinary and necessary business expenses?ordinary and necessary business expenses?

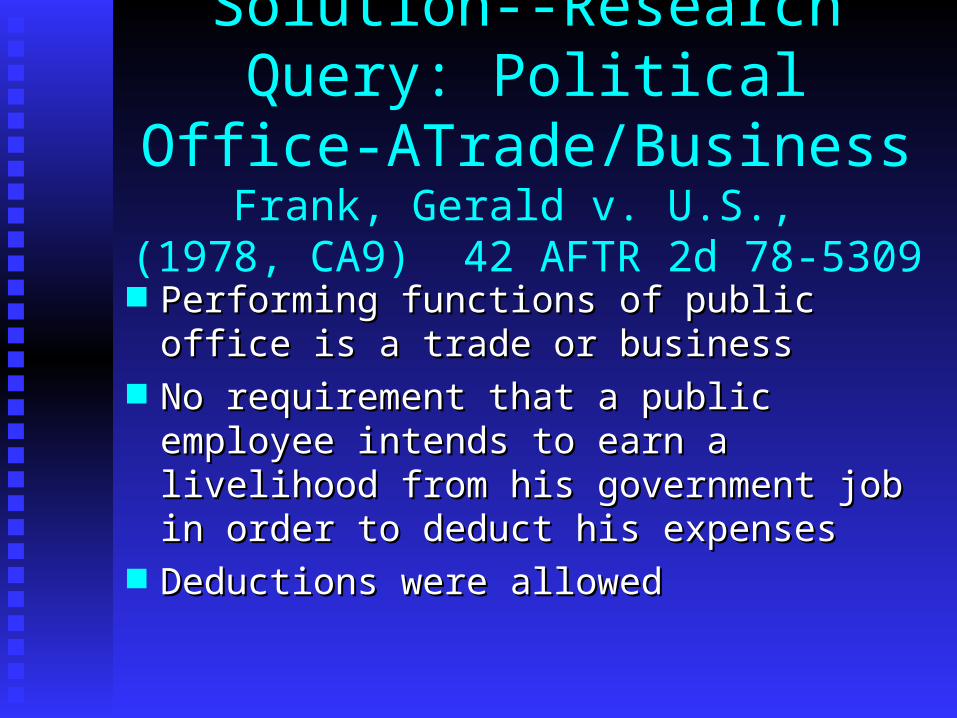

Solution--Research Query: Political Office-ATrade/Business

Frank, Gerald v. U.S., (1978, CA9) 42 AFTR 2d 78-5309

Performing functions of public office is a Performing functions of public office is a trade or businesstrade or business

No requirement that a public employee No requirement that a public employee intends to earn a livelihood from his intends to earn a livelihood from his government job in order to deduct his government job in order to deduct his expensesexpenses

Deductions were allowedDeductions were allowed

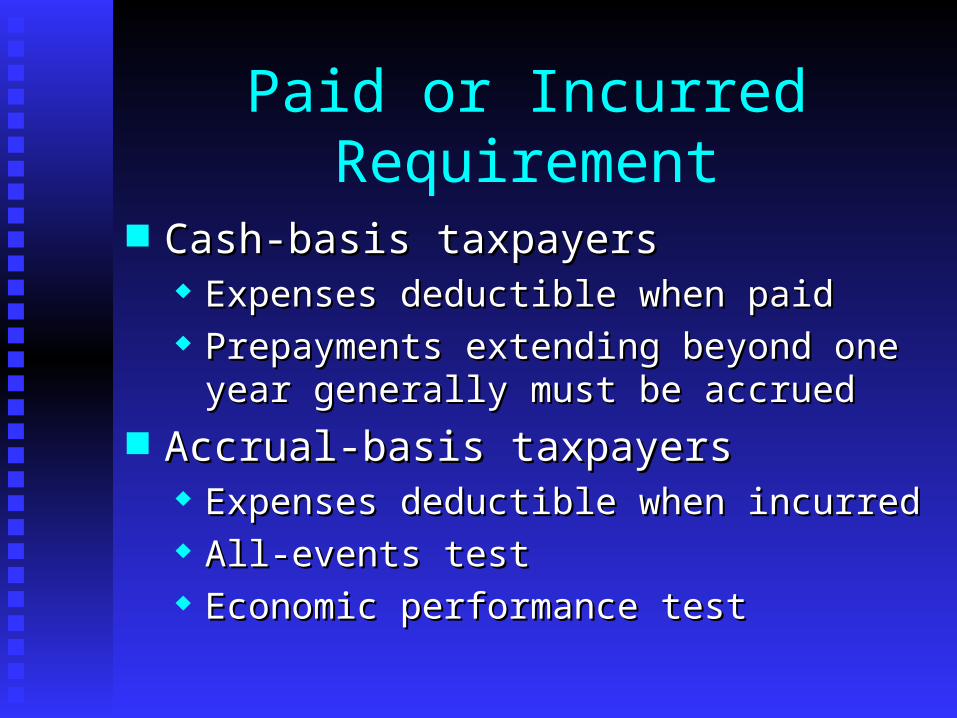

Paid or Incurred Requirement

Cash-basis taxpayersCash-basis taxpayers Expenses deductible when paidExpenses deductible when paid Prepayments extending beyond one year Prepayments extending beyond one year

generally must be accruedgenerally must be accrued Accrual-basis taxpayersAccrual-basis taxpayers

Expenses deductible when incurredExpenses deductible when incurred All-events testAll-events test Economic performance testEconomic performance test

Prohibited Deductions

Key Learning ObjectiveKey Learning Objective

Distinguish between allowable deductions Distinguish between allowable deductions and those which are prohibitedand those which are prohibited

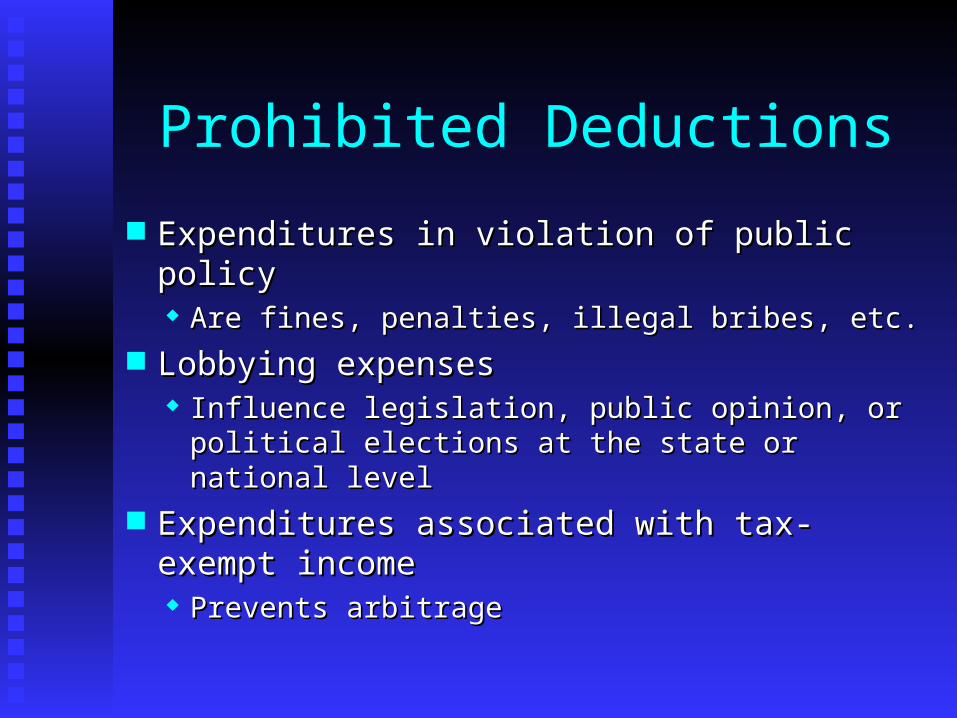

Prohibited Deductions

Expenditures in violation of public policyExpenditures in violation of public policy Are fines, penalties, illegal bribes, etc.Are fines, penalties, illegal bribes, etc.

Lobbying expensesLobbying expenses Influence legislation, public opinion, or Influence legislation, public opinion, or

political elections at the state or national levelpolitical elections at the state or national level Expenditures associated with tax-exempt Expenditures associated with tax-exempt

incomeincome Prevents arbitragePrevents arbitrage

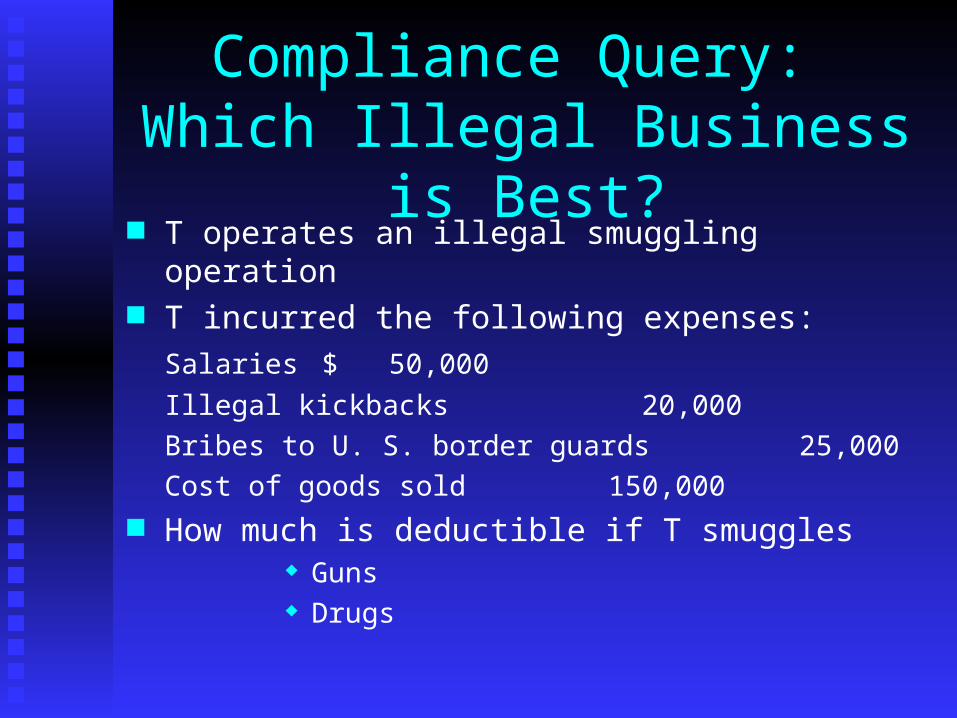

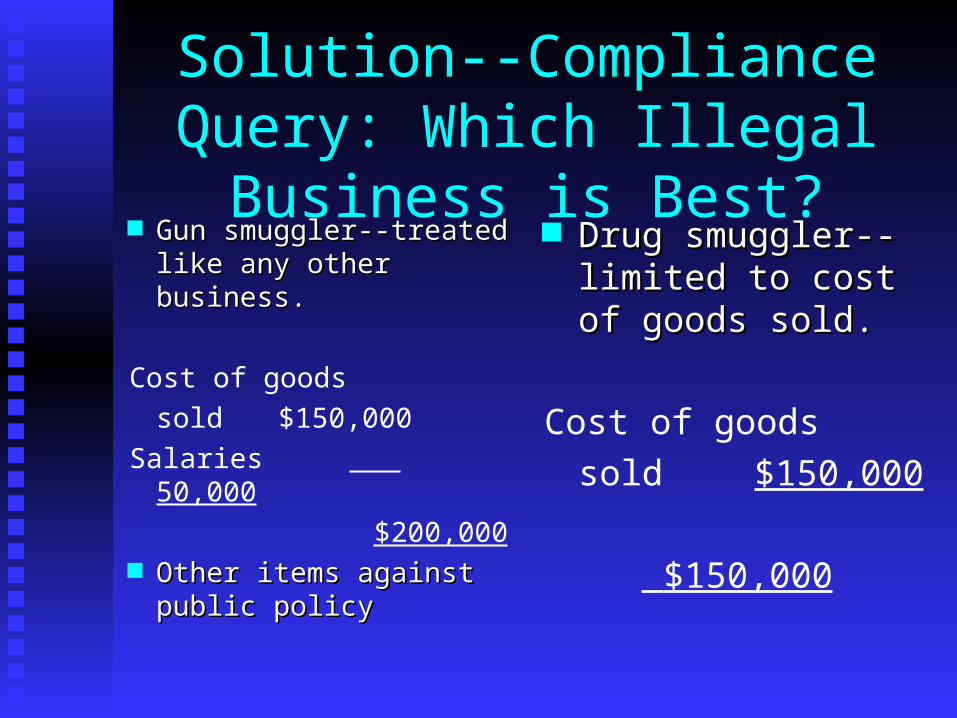

Compliance Query: Which Illegal Business is Best?

T operates an illegal smuggling operation T incurred the following expenses:

Salaries $ 50,000

Illegal kickbacks 20,000

Bribes to U. S. border guards 25,000

Cost of goods sold 150,000 How much is deductible if T smuggles

Guns Drugs

Solution--Compliance Query: Which Illegal Business is Best?

Gun smuggler--treated Gun smuggler--treated like any other business.like any other business.

Cost of goods

sold $150,000

Salaries 50,000

$200,000 Other items against Other items against

public policypublic policy

Drug smuggler--limited Drug smuggler--limited to cost of goods sold.to cost of goods sold.

Cost of goods

sold $150,000

$150,000

Deductions Common to Most Businesses

Key Learning ObjectiveKey Learning Objective

Identify and compute common business Identify and compute common business deductionsdeductions

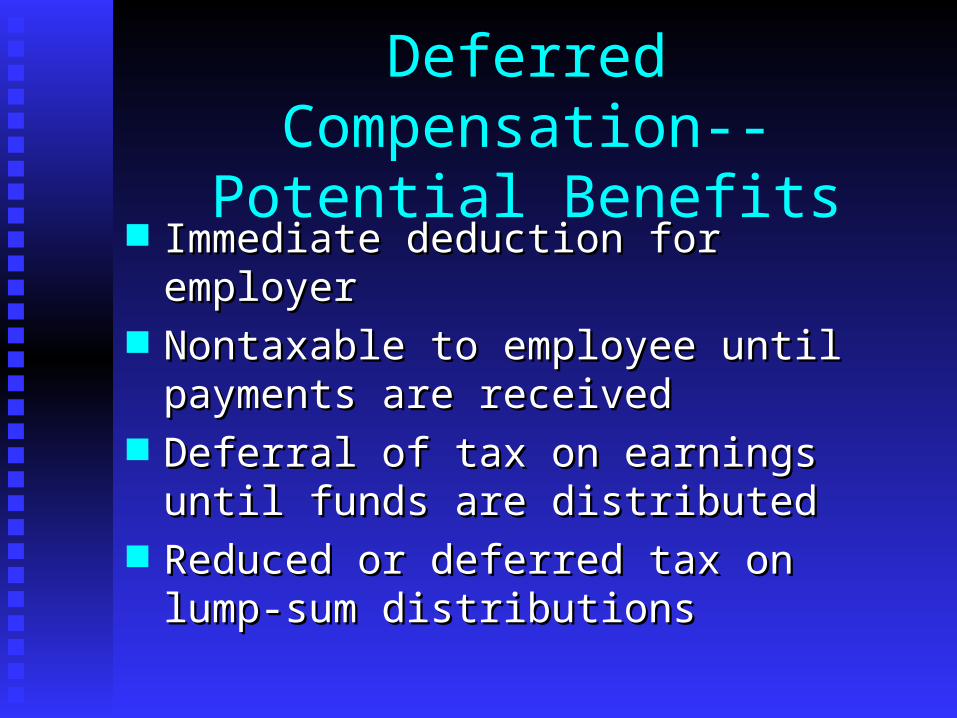

Deferred Compensation-- Potential Benefits

Immediate deduction for employerImmediate deduction for employer Nontaxable to employee until payments are Nontaxable to employee until payments are

receivedreceived Deferral of tax on earnings until funds are Deferral of tax on earnings until funds are

distributeddistributed Reduced or deferred tax on lump-sum Reduced or deferred tax on lump-sum

distributionsdistributions

Deferred Compensation--Types(covered in later modules)

Qualified pension plansQualified pension plans Nonqualified plansNonqualified plans

Fewer potential benefits Fewer potential benefits Keogh plansKeogh plans SEPsSEPs IRAsIRAs

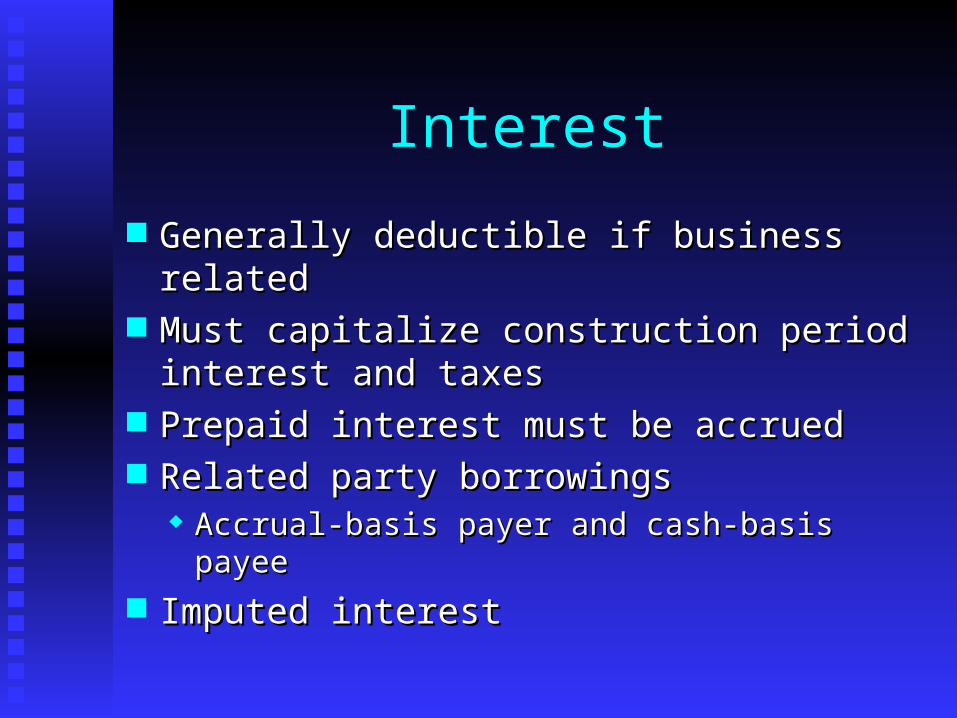

Interest

Generally deductible if business relatedGenerally deductible if business related Must capitalize construction period interest Must capitalize construction period interest

and taxesand taxes Prepaid interest must be accruedPrepaid interest must be accrued Related party borrowingsRelated party borrowings

Accrual-basis payer and cash-basis payeeAccrual-basis payer and cash-basis payee Imputed interestImputed interest

Taxes

Generally deductible if business relatedGenerally deductible if business related Sales taxes capitalized as part of costSales taxes capitalized as part of cost Employer portion of payroll taxes Employer portion of payroll taxes

deductibledeductible Federal income taxes not deductibleFederal income taxes not deductible

Charitable Contributions

Deductible by corporations subject to 10% Deductible by corporations subject to 10% limitlimit 5-year carryover for unused deductions5-year carryover for unused deductions

Amount deductible (basis or FMV) depends Amount deductible (basis or FMV) depends on type of property donatedon type of property donated ““Ordinary income” or “capital gain” propertyOrdinary income” or “capital gain” property Special rules for certain inventory, scientific Special rules for certain inventory, scientific

equipment, and tangible personal propertyequipment, and tangible personal property

Business Gifts

Limited to $25 per donee per yearLimited to $25 per donee per year Special rules for safety or length of service Special rules for safety or length of service

awards to employeesawards to employees

Travel

Generally deductible if business relatedGenerally deductible if business related Includes incidental expensesIncludes incidental expenses ““Away from home” requirement for meals Away from home” requirement for meals

and lodgingand lodging 50% limit for meals50% limit for meals

Strict substantiation requirementsStrict substantiation requirements

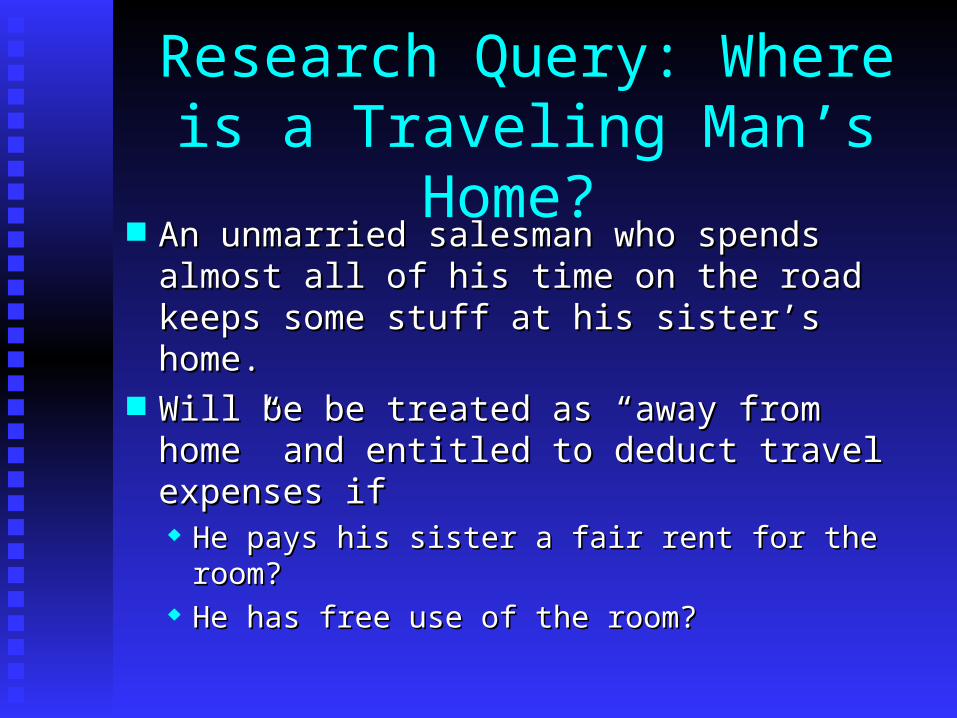

Research Query: Where is a Traveling Man’s Home?

An unmarried salesman who spends almost An unmarried salesman who spends almost all of his time on the road keeps some stuff all of his time on the road keeps some stuff at his sister’s home. at his sister’s home.

Will be be treated as “away from home” Will be be treated as “away from home” and entitled to deduct travel expenses ifand entitled to deduct travel expenses if He pays his sister a fair rent for the room?He pays his sister a fair rent for the room? He has free use of the room?He has free use of the room?

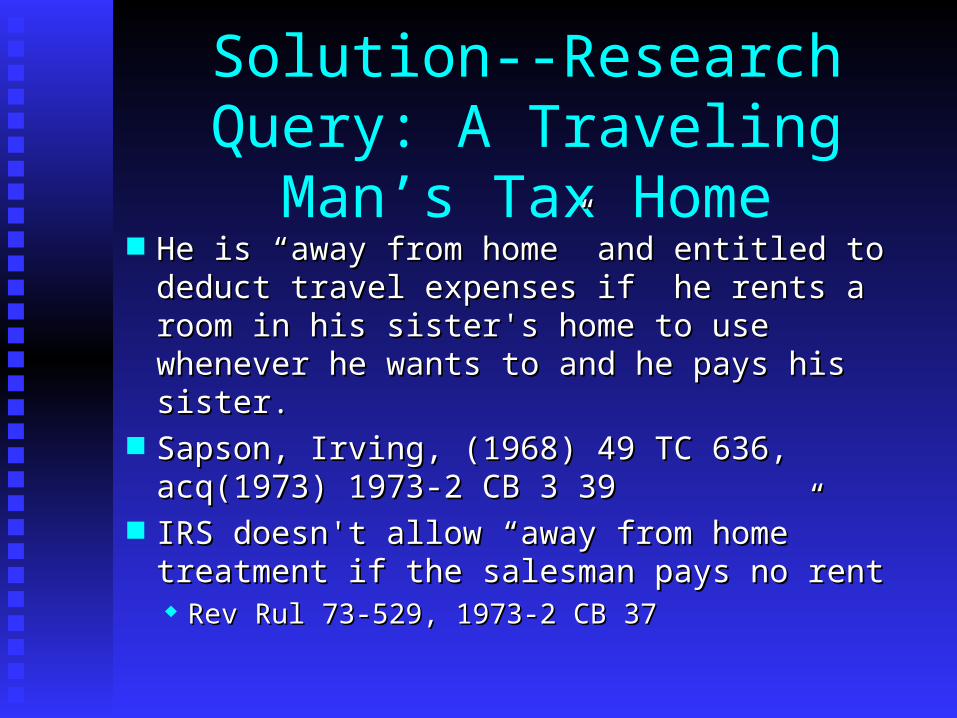

Solution--Research Query: A Traveling Man’s Tax Home

He is “away from home” and entitled to deduct He is “away from home” and entitled to deduct travel expenses if he rents a room in his sister's travel expenses if he rents a room in his sister's home to use whenever he wants to and he pays his home to use whenever he wants to and he pays his sister. sister.

Sapson, Irving, (1968) 49 TC 636, acq(1973) 1973-Sapson, Irving, (1968) 49 TC 636, acq(1973) 1973-2 CB 3 39 2 CB 3 39

IRS doesn't allow “away from home” treatment if IRS doesn't allow “away from home” treatment if the salesman pays no rent the salesman pays no rent Rev Rul 73-529, 1973-2 CB 37Rev Rul 73-529, 1973-2 CB 37

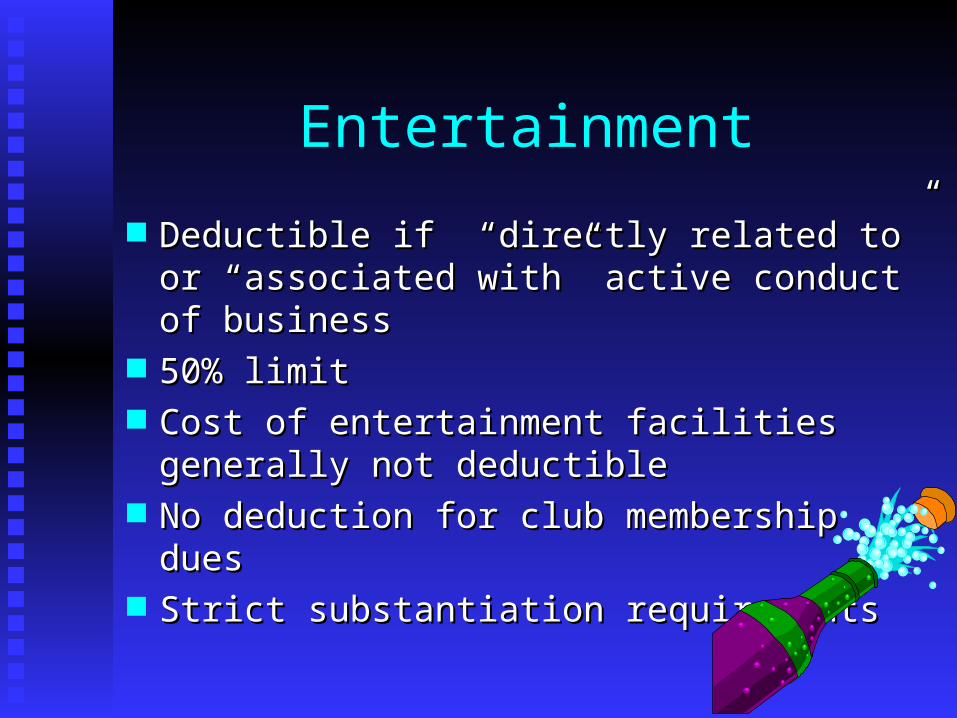

Entertainment

Deductible if “directly related to” or Deductible if “directly related to” or “associated with” active conduct of business“associated with” active conduct of business

50% limit50% limit Cost of entertainment facilities generally not Cost of entertainment facilities generally not

deductibledeductible No deduction for club membership duesNo deduction for club membership dues Strict substantiation requirementsStrict substantiation requirements

Special Deductions for Corporations

Key Learning ObjectiveKey Learning Objective

Calculate deductions for corporate Calculate deductions for corporate organizational costs and dividends receivedorganizational costs and dividends received

Organization Costs

Includes first year attorney, accountant, and Includes first year attorney, accountant, and filing fees, etc., related to corporate filing fees, etc., related to corporate formationformation

Does not include costs of issuing stockDoes not include costs of issuing stock Not currently deductibleNot currently deductible Can capitalize and amortize over 60 monthsCan capitalize and amortize over 60 months

Must make electionMust make election

Dividend Received Deduction

Mitigates triple taxationMitigates triple taxation Applies generally to dividends from Applies generally to dividends from

domestic corporationsdomestic corporations Percent deductible (70%; 80%; 100%) Percent deductible (70%; 80%; 100%)

depends on ownership percentagedepends on ownership percentage Taxable income limitation may applyTaxable income limitation may apply

Capitalization Issues

Key Learning ObjectiveKey Learning Objective

Classify expenditures that contain both Classify expenditures that contain both repair and capitalization attributesrepair and capitalization attributes

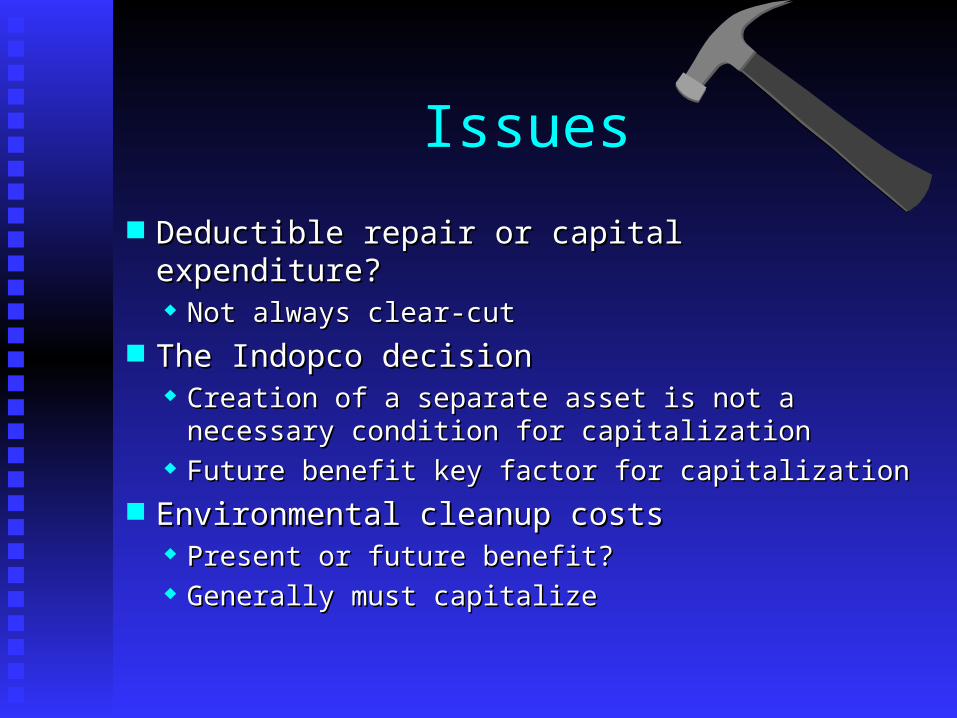

Issues

Deductible repair or capital expenditure?Deductible repair or capital expenditure? Not always clear-cutNot always clear-cut

The Indopco decisionThe Indopco decision Creation of a separate asset is not a necessary Creation of a separate asset is not a necessary

condition for capitalizationcondition for capitalization Future benefit key factor for capitalizationFuture benefit key factor for capitalization

Environmental cleanup costsEnvironmental cleanup costs Present or future benefit?Present or future benefit? Generally must capitalizeGenerally must capitalize

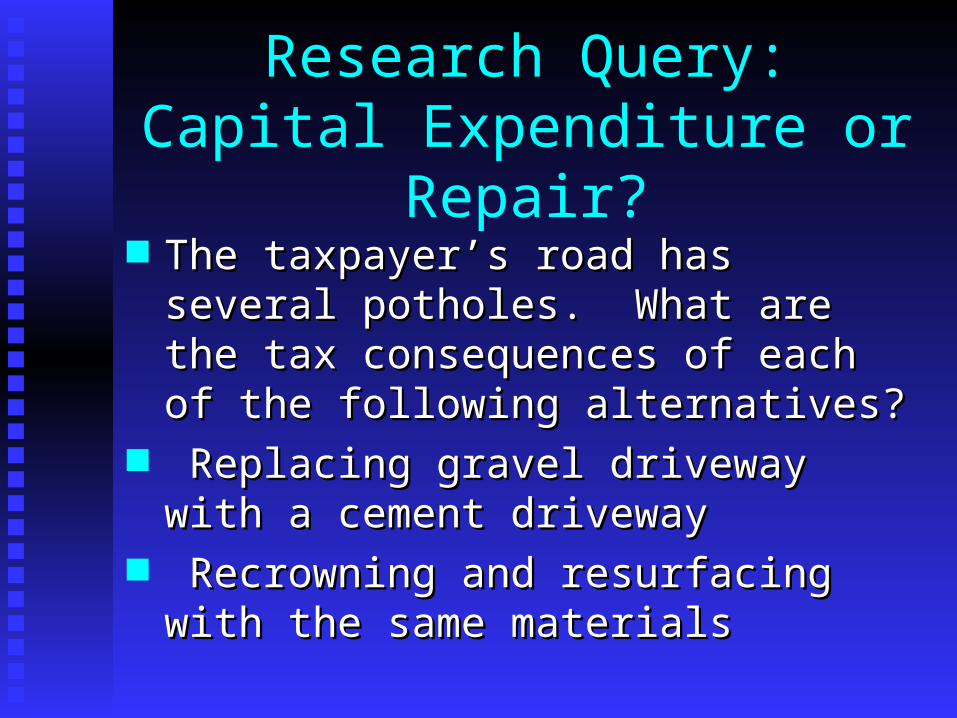

Research Query:Capital Expenditure or Repair?

The taxpayer’s road has several potholes. The taxpayer’s road has several potholes. What are the tax consequences of each of What are the tax consequences of each of the following alternatives?the following alternatives?

Replacing gravel driveway with a cement Replacing gravel driveway with a cement drivewaydriveway

Recrowning and resurfacing with the same Recrowning and resurfacing with the same materialsmaterials

Solution--Research Query: Capital Expenditure or Repair?

Replacing gravel driveway with a cement Replacing gravel driveway with a cement driveway will be treated as a capital driveway will be treated as a capital expenditure.expenditure. Jones, A. Raymond, (1956) 25 TC 1100Jones, A. Raymond, (1956) 25 TC 1100

Recrowning and resurfacing with the same Recrowning and resurfacing with the same materials should be a deductible repair.materials should be a deductible repair. Pennock Plantation Inc, (1951) Pennock Plantation Inc, (1951)

PH TCM ¶51341PH TCM ¶51341