modern entrepeneur and entrepeneurship

TRANSCRIPT

MODERN ENTREPRENEUR AND

ENTREPRENEURSHIP (Theory, Process and Practice)

MODERN ENTREPRENEUR AND

ENTREPRENEURSHIP (Theory, Process and Practice)

H.S. KUMAWAT

SUNRISE , PUBLISHERS & DISTRIBUTORS

E-566, Vaishali Nagar, Jaipur - 302021 (Raj.)

Published by: SUNRISE PUBLISHERS & DISTRIBUTORS E-566, Vaishali Nagar, Jaipur - 302021 (Raj.) Ph.:9413156675,9772299149 Email: [email protected]

First Published - 2009

©Reserved

ISBN: 978-93-80207-01-8

All rights reserved. No part of this book may be reproduced in any form or by any mean without permission in writing from the publisher.

Printed at: Jaipur

CONTENTS

• Preface v

1. Decision by Modern Entrepreneur 1

2. Methods for Comparing Investment Alternatives 10

3. Replacement Analysis 32

4. Farm Management 44

5. Pre-Fabricated Irrigation Channels 61

6. Purchasing Methods 74

7. Stores Control 86

8. Credit System 106

9. Kinds of Credit 124

10. Treasury Bill Market 138

11. Office Machines 160

12. Production Control 182

13. Typical Production-control Procedure 203 •

14. Decision-Making Framework for Export Operation 217

15. Privatisation 225

16. Industrial Sickness 247

17. Service Sector and Modern Entrepreneur 266

18. Commercial Banks 283

19. Insurance 292

20. Warehousing 313

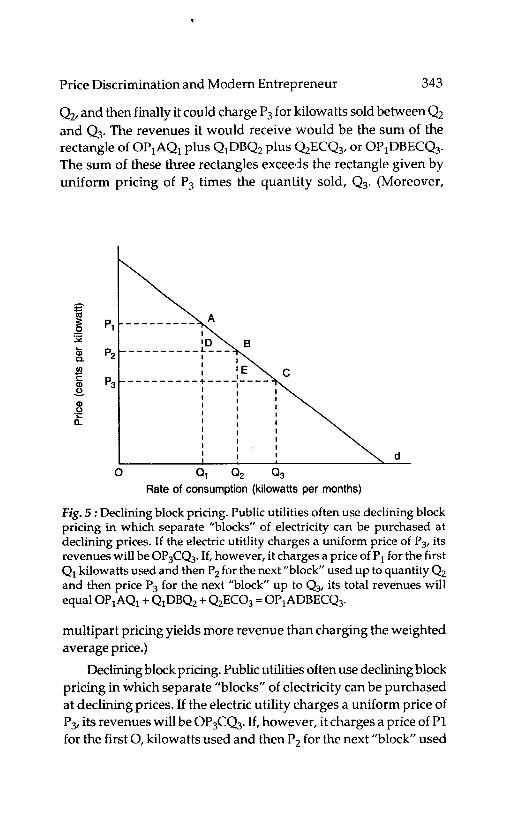

21. Price Discrimination and Modem Entrepreneur 325

22. Leadership in Modem Entrepreneur 352

23. Organisation of Foreign Trade by Modem Entrepreneur 374

24. Import Decisions by Modem Entrepreneur 385

25. Bilateral Trade and Rupee Payment Agreements 398

26. Export Trade 405

PREFACE

The book has been written to meet the requirements of the syllabus prescribed for B.Com., B.B.A., M.Com., and M.B.A. courses of Indian Universities. The book is exhaustive in every sense and cover a large spectrum of subject. In the present economic conditions Entrepreneurship is a subject with wide connotation. The present book deals with the subject matter which is changing which have acquired a critical significance at national and intemationallevel.

I hope the book would receive an overwhelming response from the students, professors and other professionals and they will find it an invaluable text. It will also serve as an excellent reference for practising managers in their day-to-day application and understanding of the subject.

Inspite of all efforts some errors might have crept in, for which I will be grateful to the teachers and students, if same are brought to my notice. Suggestions for further improvement of the book will be gratefully acknowledged.

Author

Chapter

1

** DECISIONS BY MODERN

ENTREPRENEUR

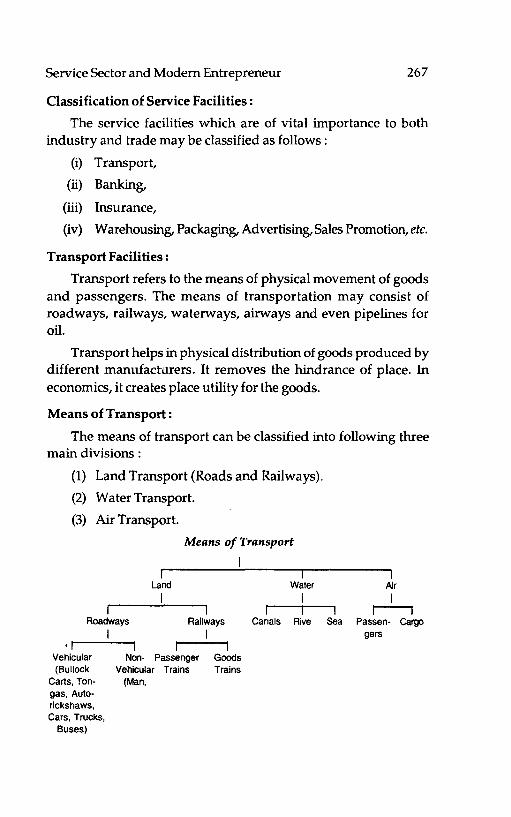

Every business organisation big or small has to invest huge capital for installation of the plant as well as during the process of manufacturing the product or service. The decisions regarding capital expenditures have far reaching consequences on the performance of the business organisation, e.g., capital hired/ acquired on long term credit creates a continuing liability to the business organisation. Capital investments can be divided into folluwing three major categories:

Capital investments

I Fixed Assets Operational Expenses Replacement/innovation

expenses.

(i) Investment on Fixed Assets: These are the expenditures on men, material and machine/ equipment required for manufacturing. The planning of this type of expenditure is to be done either before the installation of the plant or before the start of actual production. One important feature of such expenditures is that once acquired, the capital assets cannot be disposed off without any loss. Similarly if additional assets does not adequately increase the earnings, then these may adversely affect the financial obligations of the company. It is observed that for producing any type of goods the company can

2 Decisions by Modem Entrepreneur

use varying amounts and kinds of input, i.e., man, machine and material. Thus, there are a number of alternatives in which the capital expenditure can be made.

(ii) Expenditures during course of production: This is also known as cost of production. It is a running expenditure and its magnitude depends on the nature of inputs. Wrong capital investment and misuse may result in increasing operating costs and proportionate decrease in return on investments. Thus, balancing expenditures against expected saving in future operating costs need proper analysis of various financial aspects of the operations of a company. This expenditure can also be done in a number of alternative ways.

(iii) Replacement/Innovation Expenses : It is a natural phenomenon that in every system the efficiency of various factors of production deteriorates with time or sometimes the plant or machinery fails completely. Thus, adversely affecting the whole system. In such cases either the plant or machinery is to be replaced completely or there is a need of some remedial measure, i.e. maintenance, to restore the level of efficiency at the desired level. Replacement investments may be desired due to innovations in production technology i.e. for the modernisation of the production system.

The capital expenditure may also relate to:

(a) cost reduction by (i) replacement of machinery and equipment (ii) plant rearrangement programme or mechanisation of the production process.

(b) providing facilities to manufacture £Omponents which are currently purchased.

(c) installation of new plant and machinery for taking up a new product on product lihes.

In view of many uncertainties, scientific and systematic planning and control of capital expenditure is of great significance in modem management. The process of capital expenditure involves planning the availability and controlling the allocation and expenditure of long-term investment funds by determining:

Decisions by Modem Entrepreneur 3

(i) How much money is needed for the capital expenditure in future period?

(ii) How much money will be available with the organisation for investment?

(iii) How the funds available will be allocated to the projects under consideration?

The most common feature of all these expenditures is that there are a number of alternative ways to plan these expenditures to get the desired result and every company wants to formulate an investment policy which is most efficient and economic to the organisation as a whole. Thus, the study of entrepreneurship is a procedure to select the most profitable investment or replacement strategy.

In this chapter a number of techniques for selecting the most appropriate investment/replacement alternative in different situations have been discussed in detailed manner.

Present Value Concept:

Every capital expenditure made today has some opportunity cost associated with it i.e. there will be some return available on it depending upon the period of return. Alternately, whenever some capital expenditures are made, then the arrangement for these is done either through borrowing from some agencies and paying interest on that or paying it from one's savings which otherwise could have fetched some interest. Thus in each case some return in monetary terms is associated with each investment. This return depends on the amount of investment as well as the period for which the money is to be invested. The money borrowed or invested from savings is known as principal and the money paid as interest or loss of return on savings due to investment is known as interest.

The sum of Principal (P) and Interest (I) is known as amount (A). Mathematically, the relationship between the three can be written as:

Amount

A

=

=

Principal

P

+ Interest

+ (1)

4 Decisions by Modern Entrepreneur

Thus, the present value of a sum to be spent within a given period depends on the rate of interest and the period within which the amount is to be repaid.

There are two methods of paying interest (i) Simple interest and (ii) Compound interest.

(a) Simple interest: It is amount paid yearly or some other specified period on the principal amount e.g. if an amount P is borrowed at a fixed interest rate r per rupee per year, then in one year the interest will be iP. next year also the interest will be iP, and in rth year again the interest will be iP. So if total investment is to be paid back in r years, then the total interest paid in r years will be

I = iP + iP + ..... iP r times

= riP

Thus putting the value of / from (2) in (1), we get

A=P+riP

= P(l + ri)

... (2)

... (3)

Note: Generally interest rate is specified in percentage i.e. t% per year.

t r= - peryear

100 ... (4)

It is evident from (3), that the amount A increases progressively in arithmetic progression.

(b) Compound Interest: In this case, the whole amount A is to be paid at the end of the period. Here every year the interest accrued is also added to the Principal amount of previous year to get the new principal for next year i.e. at the end of first year the new principal will be

PI = P + iP = P(l + i)

at the end of second year the principal will be

P2=P1 +iP1 =P1(1+i)

P(l +i) (1 +i) = P (1 +i)2

and at the end of r th year the principal will become

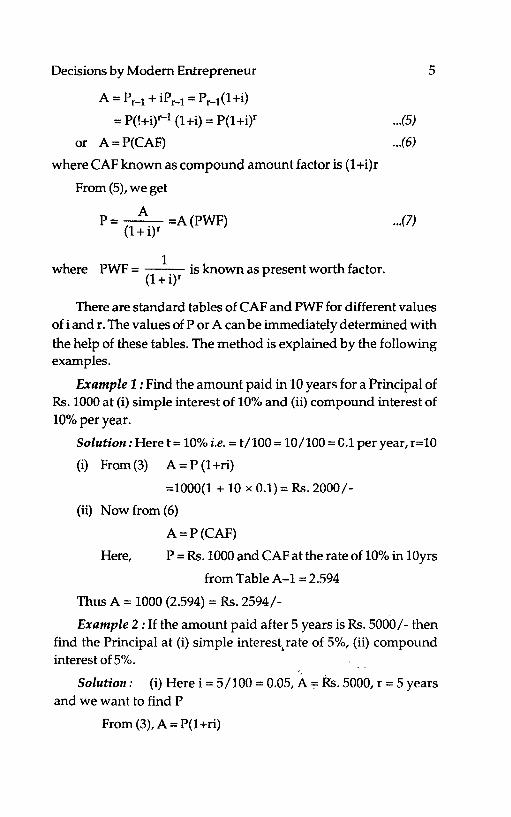

Decisions by Modem Entrepreneur

A = Pr- 1 + iPr- 1 = Pr_1(1+i)

= P(!+W-1 (1 +i) = P(l +i)f

or A=P(CAF)

where CAF known as compound amount factor is (1 +i)r

From (5), we get

A P = -- =A (PWF)

(l+W

where PWF = _1_ is known as present worth factor. (l+W

... (5)

.. .(6)

... (7)

5

There are standard tables of CAF and PWF for different values of i and r. The values of P or A can be immediately determined with

the help of these tables. The method is explained by the following examples.

Example 1: Find the amount paid in 10 years for a Principal of Rs. 1000 at (i) simple interest of 10% and (ii) compound interest of 10% per year.

Solution: Here t= 10% i.e. = t/100 = 10/100 =C.1 per year, r=10

(i) From (3) A = P (1 Hi)

=1000(1 + 10 x 0.1)= Rs. 2000/

(ii) Now from (6)

A=P(CAF)

Here, P = Rs. 1000 and CAF at the rate of 10% in 10yrs

from Table A-I = 2.594

Thus A = 1000 (2.594) = Rs. 2594/-

Example 2 : If the amount paid after 5 years is Rs. 5000/- then find the Principal at (i) simple interest, rate of 5%, (ii) compound interest of 5%.

Solution: (i) Here i = 5/100 = 0.05, A ~ Rs. 5000, r = 5 years and we want to find P

From (3), A = P(1 Hi)

6 Decisions by Modern Entrepreneur

i.e. 5000 = P[l + 5 (0.05)} = P [1.251

P = (5000/1.25) = Rs. 4000

(ii) From (7), P = A (PWF)

(From Table A-2 for 1= 5% and r=5, PWF= 0.7835)

= 5000 x 0.7835 = Rs. 3917.50

(iii) There are some situations, where the borrower agrees to

repay some fixed amount at fixed intervals of time i.e. the money is repaid in fixed installments. If the total amount A accrued in r years is paid in r, installments of Rs. K, then

A = K[(l +W -l]/i = K(CAFS) ... (8)

where CAPS =[(1+i)f-1J/i is known as uniform annual series compound amount factor.

Now, knowing A, we can write

K = (Ai) j [(1+i)f-1] = A(SFF) where SFF=ij[(l+i)f~l)) ... (9)

K= [P(1+W.i)j[(1+i)f-1] is Sinking Fund Factor

= P(CRF) ... (10)

where CRF = [i(1+i)r]![(1+i)f-1] is known as Capital Recovery Factor.

or P = [K(1+W-1)j[(1+W.i)] = K(PWFS) ... (11)

where PWFS = [K(l+i)f -I]! [(1 +W. i] is known as uniform annual series present worth factor.

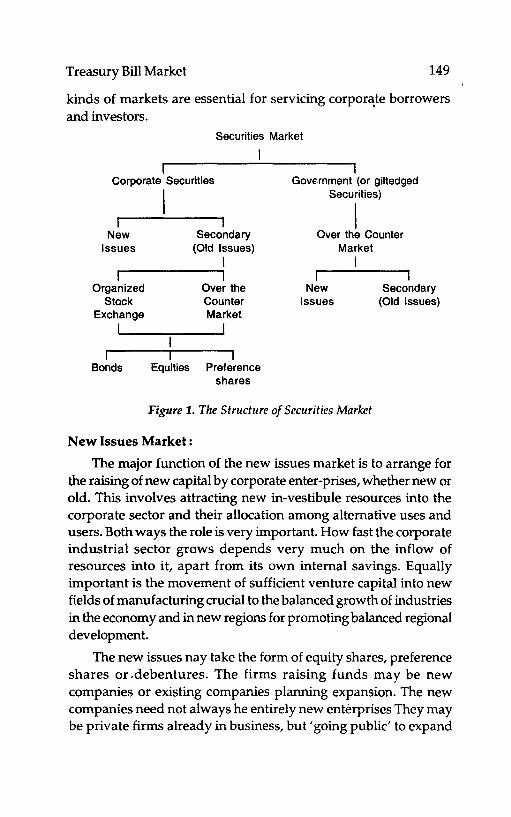

Standard values of CAFS, SFF, CRF and PWFS (for given i and r) are respectively given in Tables.

The use of Tables is illustrated with the following examples:

Example 3 : Mr. X deposits Rs. 500 j ~ every year at an interest rate of 10% for 5 years. Find the total amount at the end of 5 years.

Solution: From (8), A = K(CAFS)

Here, K = Rs. 500, CAFS for 10% and r = 5 from Table A-3 is

equal to 6.105.

Hence A = 500 (6.105) = Rs. 3052.50

Decisions by Modem Entrepreneur 7

Example 4 : A person wants to have Rs. 10,000 in his account after a period of 5 years. The interest rate is 4%. Find his annual installment.

Solution: From (9), K = A (SFF)

Here A = Rs.I0000 and SFF at4% and r=5 from table A-4 = 0.18463.

Hence K = 10000 (0.18463)

= Rs. 1846.30

Example 5 : Mohan wants to borrow a sum of Rs. 20000 and desires to pay it in 10 equal installments. The annual interest rate is 5%. Find the" size of the installment.

Solution: Here P = 20,000, r = 10 and t = 5%.

Now from (10), K = P(CRF)

From A-5, CRF for r=10 and t = 5% = 0.12950

Henct! K = 20000 (0.12950) = Rs. 2590.00 per year.

Example 6: There is an opportunity to invest some money with an assurance to get back Rs. 6000/- after 10 years. The investor wants to earn an interest of 1% per year. How much he should invest?

Solution: Here the following things are known:

t = 15% per year, r = 10 years, and A = Rs. 6000/

From (7) we get, P = A (Pwf)

and from A-2, Pwf for r = 10 and and t = 15% = 0.2394.

Hence, P = 6000 x 0.2394 = Rs. 1436.40

Example 7 :A company sets aside for a reserve fund the sum of Rs. 20,000 annually to enable it to payoff a debenture issue of Rs. 2,39,000 at the end of 10 years. Assuming that the reserve accumulates at 5% per annum compound, find the surplus after paying off the debenture stock.

Solution: Here K = Rs. 20,000, r = 10 years, and t = 5%

From (8), A = K (CAFS) CAFS from table A-3 for r = 10 and

8 Decisions by Modem Entrepreneur

t = 5% = 12.578

A = 20000 x 12.578 - Rs. 251560

Thus the surplus after paying Rs. 2,39,000 will be

Rs. 251560 - Rs. 239000 = Rs. 12560.

Example 8 : On his 48th birthday a man decides to make a gift of Rs. 5000 to a hospital on his 60th birthday. He decides to save this amount by making annual installments up to and including his 60th birthday to a fund which gives 35% compound interest, the first payment being made at once. Calculate the amount of each annual payment.

Solution: Here t = 31.5%, r = 12 years and, A = 5000

Now from (9), K = A(SFF)

From Table A-4 we interpolate the value of SFF for r = 12 and

t = 3.5% = 0.068505

K = SOOO (0.068505) = Rs. 342.525 928.

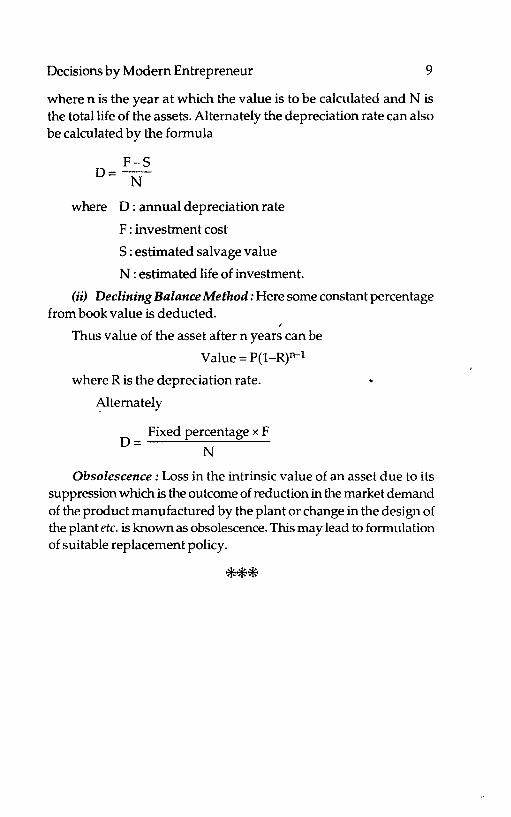

The Loss Value of a Plant:

The plant installed today start immediately to loose its value due to following two main reasons namely, Depreciation and Obsolescence.

Depreciation: The production capacity introduced by some Capital investment tends to decline with time. There is also diminution in the intrinsic value of an asset due to use as well as with passage of time. This diminution may also be due to bad handling, poor maintenance, accidents etc. This decline in the value of investment is known as Depreciation. Depreciation rate can be calculated in two ways:

(i) Straight line method : Here we assume that there is a constant rate of decline during an aS,set's life. Thus same absolute value is deducted from the value of the asset's for each period of use.

P(n -1) i.e. Value = P - N

Decisions by Modern Entrepreneur 9

where n is the year at which the value is to be calculated and N is the total life of the assets. Alternately the depreciation rate can also be calculated by the formula

F-S D=--

N

where D: annual depreciation rate

F : investment cost

5: estimated salvage value

N : estimated life of investment.

(ii) Declining Balance Method: Here some constant percentage from book value is deducted. ,

Thus value of the asset after n years can be

Value = p(l_R)n-l

where R is the depreciation rate.

~lternately

Fixed percentage x F D= N

Obsolescence: Loss in the intrinsic value of an asset due to its suppression which is the outcome of reduction in the market demand of the product manufactured by the plant or change in the design of the plant etc. is known as obsolescence. This may lead to formulation of suitable replacement policy.

***

Chapter

2

** METHODS FOR COMPARING INVESTMENT ALTERNATIVES

In plax;ming any production strategy one very often faces a situation when decisions on investment and replacement proposals are to be taken. There are a number of alternatives, each involving huge capital expenditure. Evidently for making an appropriate decision an economic analysis is more useful for differentiating between various alternatives. The basic steps involved for critical appraisal of different alternatives are:

(i) To evaluate the cost of products and other investment capital requirements i.e. how much money is needed for desired expenditure during the period under consideration.

(ii) Determination of anticipated returns and life of the invested capital.

(iii) Timing of the investment in relation to anticipated requirements.

(iv) How much money can be made available for the purpose and what will be the sources and expenditure for these funds? The funds can be generated in different ways. Some of these can be:

(a) Hire-purcJzase: Contracts can be negotiated for long periods with the interest tied to the bank rate.ln some

Methods for Comparing Investment Alternatives 11

cases payments can fluctuate with a known seasonal variation in output.

(b) Leasing: Here the user never accurately owns the machinery leased. The use of the plant is considered to be more important than its ownership.

(c) Hiring: In fact this is some sort of leasing but in it a maintenance contract is also implied or required.

Methods to compare alternative proposals can be divided into following two main categories:

Present Value Approach:

(a) Present value basis.

(b) Uniform annual value basis.

(c) Last basis.

(d) Discounted cash flow method.

Annual Cost Approach:

(a) Pay-back period

(b) Return on investment.

Present value Approach:

(a) Present Value Basis: In this method, investment in capital expenditure decisions are based on the amount by which the present value of a projected income stream exceeds the cost of an investment. Here both the streams of inflows and outflows are discounted at a calculated rate. The basic assumption behind all discounting is that the cash inflows are re-invested at the discounting rate in net projects as soon as they arise.

Thus in this approach present values of all future expenditures and revenues are calculated for different alternatives and the Net present value of total cost is compared. The alternative with minimum net present value is considered to be most appropriate.

Case (i) In the absence of any annual income:

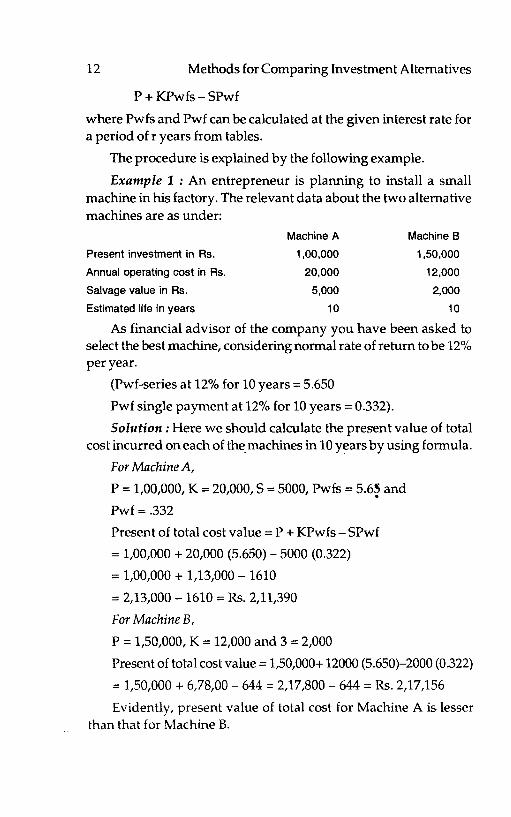

If there is an initial investment of P rupees with a recurring expenditure of K rupees per year for r years and at the end of r years the salvage value is 5, then the present value of total cost is given by

12 Methods for Comparing Investment Alternatives

P + KPwfs - SPwf

where Pwfs and Pwf can be calculated at the given interest rate for a period of r years from tables.

The procedure is explained by the following example.

Example 1 : An entrepreneur is planning to install a small machine in his factory. The relevant data about the two alternative machines are as under:

Machine A Machine B

Present investment in Rs. 1,00,000 1,50,000

Annual operating cost in Rs. 20,000 12,000

Salvage value in Rs. 5,000 2,000

Estimated life in years 10 10

As financial advisor of the company you have been asked to select the best machine, considering normal rate of return to be 12% per year.

(Pwf-series at 12% for 10 years = 5.650

Pwf single payment at 12% for 10 years = 0.332).

Solution: Here we should calculate the present value of total cost incurred on each of the. machines in 10 years by using formula.

For Machine A,

P = 1,00,000, K = 20,000,5 = 5000, Pwfs = 5.6~ and

Pwf= .332

Present of total cost value = P + KPwfs - SPwf

= 1,00,000 + 20,000 (5.650) - 5000 (0.322)

= 1,00,000 + 1,13,000 - 1610

= 2,13,000 -1610 = Rs. 2,11,390

For Machine B,

P = 1,50,000, K = 12,000 and 3 = 2,000

Present of total cost value = 1,50,000+ 12000 (5.650)-2000 (0.322)

= 1,50,000 + 6,78,00 - 644 = 2,17,800 - 644 = Rs. 2,17,156

Evidently, present value of total cost for Machine A is lesser than that for Machine B.

Methods for Comparing Investment Alternatives

Hence the company should select machine A.

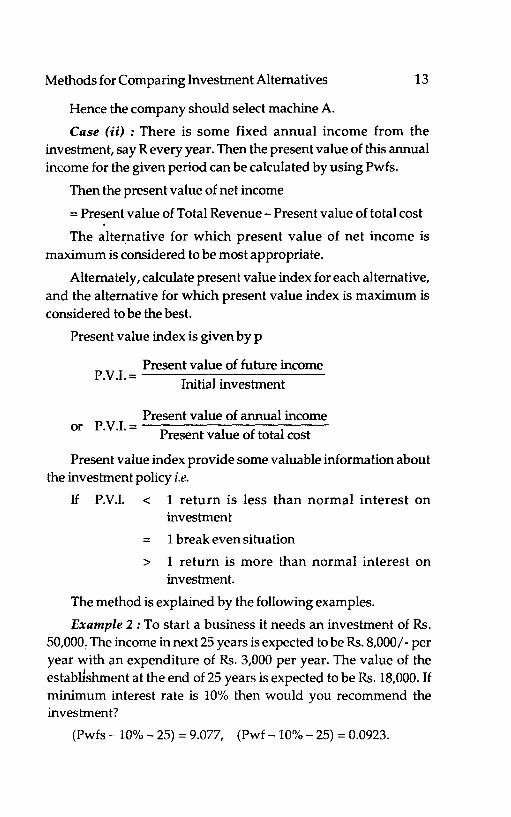

13

Case (ii) : There is some fixed annual income from the investment, say R every year. Then the present value of this annual income for the given period can be calculated by using Pwfs.

Then the present value of net income

= Present value of Total Revenue - Present value of total cost

The alternative for which present value of net income is maximum is considered to be most appropriate.

Alternately, calculate present value index for each alternative, and the alternative for which present value index is maximum is considered to be the best.

Present value index is given by p

Present value of future income P.V.1. = ---I-ru-.t-i-al-in-v-es-tm-e-n-t---

Present value of annual income or P.V.1. = P 1 f 1 resent va ue 0 tota cost

Present value index provide some valuable information about the investment policy i.e.

lf P.V.!. < 1 return is less than normal interest on investment

= 1 break even situation

> 1 return is more than normal interest on investment.

The method is explained by the following examples.

Example 2: To start a business it needs an investment of Rs. 50,000: The income in next 25 years is expected to be Rs. 8,000/ - per year with an expenditure of Rs. 3,000 per year. The value of the establlshment at the end of 25 years is expected to be Rs. 18,000. If minimum interest rate is 10% then would you recommend the investment?

(Pwfs - 10% - 25) = 9.077, (Pwf - 10% - 25) = 0.0923.

14 Methods for Comparing Investment Alternatives

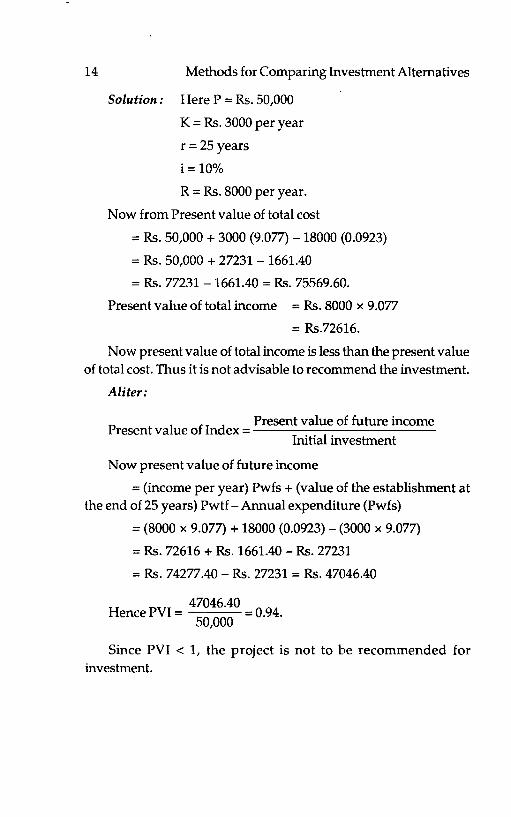

Solution: Here P = Rs. 50,000

K = Rs. 3000 per year

r = 25 years

i=lO%

R = Rs. 8000 per year.

Now from Present value of total cost

= Rs. 50,000 + 3000 (9.077) - 18000 (0.0923)

= Rs. 50,000 + 27231 - 1661.40

= Rs. 77231 - 1661.40 = Rs. 75569.60.

Present value of total income = Rs. 8000 x 9.077

= Rs.72616.

Now present value of total income is less than the present value of total cost. Thus it is not advisable to recommend the investment.

Aliter:

P 1 f I d Present value of future income

resent va ue 0 n ex = I Initia investment

Now present value of future income

= (income per year) Pwfs + (value of the establishment at the end of 25 years) Pwtf - Annual expenditure (Pwfs)

= (8000 x 9.077) + 18000 (0.0923) - (3000 x 9.077)

= Rs. 72616 + Rs. 1661.40 - Rs. 27231

= Rs. 74277.40 - Rs. 27231 = Rs. 47046.40

47046.40 Hence PVI = ---= 094.

50,000 .

Since PVI < 1, the project is not to be recommended for investment.

Methods for Comparing Investment Alternatives 15

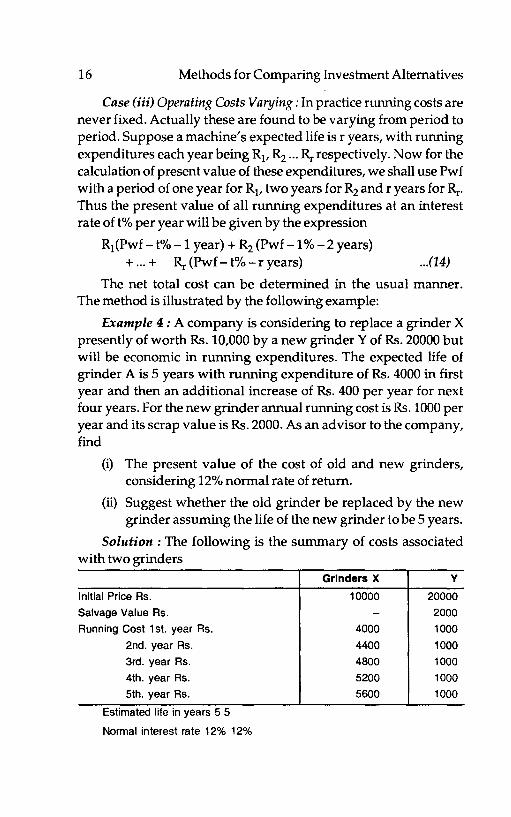

Example 3 : A company is considering to purchase a new grinder. The cost data of alternative grinders are as follows:

Grinders

A B C

Present value in Rs. 20,000 15,000 17,000

Annual operating cost in As. 2,000 1,500 1,400

Annual repair cost in As. 1,000 1,100 1,100

Scrap value after 12 yrs. Rs. 2,000 - 1,000

Estimated life in years 12 12 12

Recommend the grinder to be purchased when the minimum rate of return is 8%.

Solution: Total annual expenditure on each grinder can be calculated by Annual operating cost + Annual repair costs. Thus for the three grinders this cost will be Rs. 3000 for A, Rs. 2600 for B and Rs. 2500 for C. Now present value of total cost for each grinder can be calculated from (12). It is

P.V. = P +K(Pwfs -8%-12) -S (Pwf-8%-12)

Pwf single payment at 12% for 10 years = 0.332).

Now for Grinder A

P.V.= 20000 + 3000 (7.536) - 2000 (0.3971)

= 20000 + 22608 - 794.20

= Rs. 41813.80

For Grinder B

= 15000 + 2600 (7.536) - 0 (0.3971)

= Rs. 34593.60.

For Grinder C

P.V.= 17000 + 2500 (7.536) - 1000 (0.3971)

= 17000 + 18840.00 - 397.10

= Rs. 35442.90

The present value of total cost is minimum for grinder B. Hence grinder B should be purchased.

16 Methods for Comparing Investment Alternatives

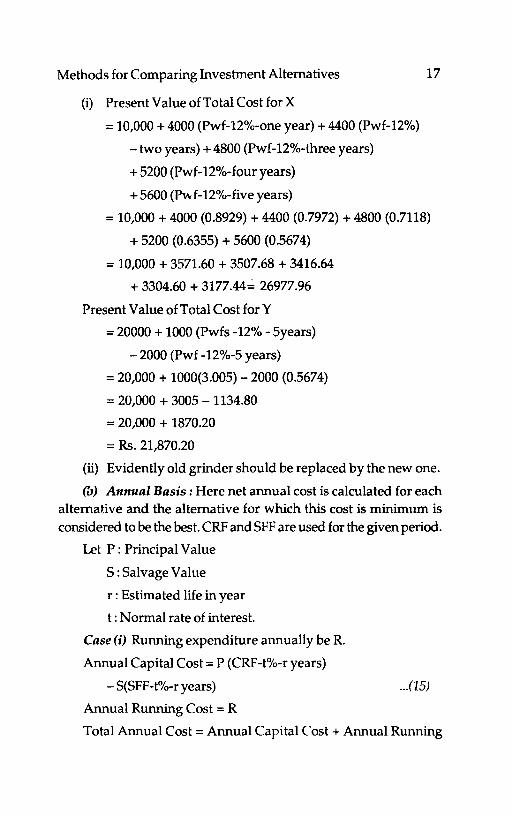

Case (iii) Operating Costs Varying: In practice running costs are never fixed. Actually these are found to be varying from period to period. Suppose a machine's expected life is r years, with running expenditures each year being Rl1 R2 ... Rr respectively. Now for the calculation of present value of these expenditures, we shall use Pwf with a period of one year for R1, two years for R2 and r years for Rr. Thus the present value of all running expenditures at an interest rate of t% per year will be given by the expression

R1(pwf - t% -1 year) + R2 (Pwf -1 % - 2 years) + ... + Rr (Pwf - t% - r years) ... (14)

The net total cost can be determined in the usual manner. The method is illustrated by the following example:

Example 4 : A company is considering to replace a grinder X presently of worth Rs. 10,000 by a new grinder Y of Rs. 20000 but will be economic in running expenditures. The expected life of grinder A is 5 years with running expenditure of Rs. 4000 in first year and then an additional increase of Rs. 400 per year for next four years. For the new grinder annual running cost is Rs. 1000 per year and its scrap value is Rs. 2000. As an advisor to the company, find

(i) The present value of the cost of old and new grinders, considering 12% normal rate of return.

(ii) Suggest whether the old grinder be replaced by the new grinder assuming the life of the new grinder to be 5 years.

Solution: The following is the summary of costs associated with two grinders

Grinders X V

Initial Price Rs. 10000 20000

Salvage Value Rs. 2000

Running Cost 1 st. year Rs. 4000 1000

2nd. year Rs. 4400 1000

3rd. year Rs. 4800 1000

4th. year Rs. 5200 1000

5th. year Rs. 5600 1000

Estimated life in years 5 5

Normal interest rate 12% 12%

Methods for Comparing Investment Alternatives

(i) Present Value of Total Cost for X

= 10,000 + 4000 (Pwf-12%-one year) + 4400 (Pwf-12%)

- two years) + 4800 (Pwf-12°/o-three years)

+ 5200 (Pwf-12% -four years)

+ 5600 (PY\. f-12°/o-five years)

17

= 10,000 + 4000 (0.8929) + 4400 (0.7972) + 4800 (0.7118)

+ 5200 (0.6355) + 5600 (0.5674)

= 10,000 + 3571.60 + 3507.68 + 3416.64

+ 3304.60 + 3177.44";' 26977.96

Present Value ofTotal Cost for Y

= 20000 + 1000 (Pwfs -12% - 5years)

- 2000 (Pwf -12%-5 years)

= 20,000 + 1000(3.005) - 2000 (0.5674)

= 20,000 + 3005 -1134.80

= 20,000 + 1870.20

= Rs. 21,870.20

(li) Evidently old grinder should be replaced by the new one.

('IJ) Annual Basis: Here net annual cost is calculated for each alternative and the alternative for which this cost is minimum is considered to be the best. CRF and SFF are used for the given period.

Let P: Principal Value

S : Salvage Value

r: Estimated life in year

t: Normal rate of interest.

Case (i) Running expenditure annually be R.

Annual Capital Cost = P (CRF-t%-r years)

- S(SFF-t%-r years) ... (15)

Annual Running Cost = R

Total Annual Cost = Annual Capital Cost + Annual Running

18 Methods for Comparing Investment Alternatives

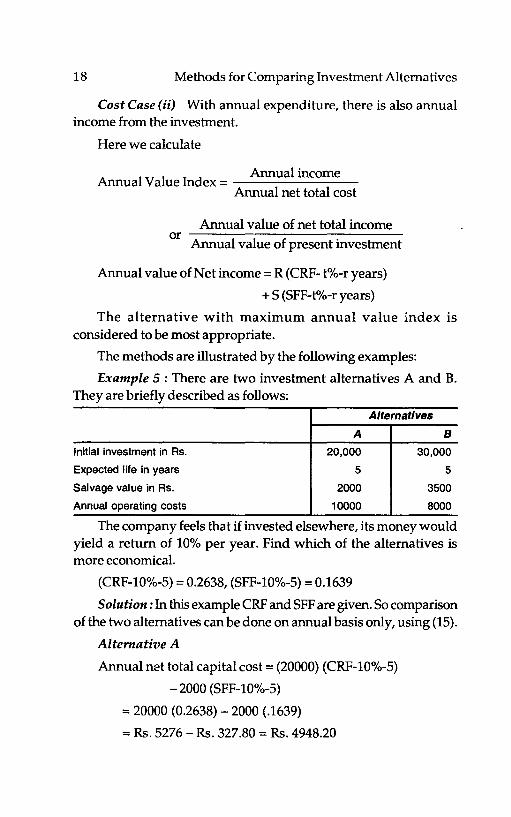

Cost Case (ii) With annual expenditure, there is also annual income from the investment.

Here we calculate

Ann I V I I d Annual income

ua a ue n ex = -------Annual net total cost

Annual value of net total income or

Annual value of present investment

Annual value of Net income = R (CRF- t%-r years)

+ S (SFF-t%-r years)

The alternative with maximum annual value index is considered to be most appropriate.

The methods are illustrated by the following examples:

Example 5 : There are two investment alternatives A and B. They are briefly described as follows:

Alternatives

A B

Initial investment in As. 20,000 30,000

Expected life in years 5 5

Salvage value in As. 2000 3500

Annual operating costs 10000 8000

The company feels that if invested elsewhere, its money would yield a return of 10% per year. Find which of the alternatives is more economical.

(CRF-I0%-5) = 0.2638, (SFF-1O%-5) = 0.1639

Solution: In this example CRF and SFF are given. So comparison of the two alternatives can be done on annual basis only, using (15).

Alternative A

Annual net total capital cost = (20000) (CRF-I0%-5)

- 2000 (SFF-I0%-5)

= 20000 (0.2638) - 2000 (.1639)

= Rs. 5276 - Rs. 327.80 = Rs. 4948.20

Methods for Comparing Investment Alternatives 19

Net Annual Total Cost =Annual Capital Cost +Annual expenditure

= Rs. 4,948.20 + Rs. 10000

= Rs. 14948.20

For alternative B

Annual Capital Cost = 30000 (CRF-10%-5)-3500 (SFF-10%-5)

= Rs. 7340.35

Net Annual Total Cost = Rs. 7340.35 + 8000

= Rs. 15340.35

Evidently alternative A is more economical.

Example 6 : Project X requires at present, investment of Rs. 25000. Estimated annual receipts for 25 years are Rs. 5000 3.nd estimated annual disbursements as Rs. 5000. An alternative project Y requires a present investment of Rs. 35000, estimated annual receipts of Rs. 1000 for 25 years and estimated annual disbursements of Rs. 3000. Each project is estimated to have a salvage value of Rs. 5000 at the end of 25 years. The minimum attractive rate of return is 10%. Which project would you recommend?

Solution: Here annual income for project X is zero (5000-5000=0) Hencefromformula:

Annual Income 0 Annual Value Index = = = 0

Net Annual Cost Net Annual Cost

For Project Y,

Net Annual Income = 1000 - 3000 = - 2000

Net Annual Total Cost = 35000 (CRF-10%-25)

-5000 (SFF-10%-25)

= 35000 (0.11017) - 5000 (0.01017)

= 3805.10

2000 Annual Value Index = = - 0.53

3805.60

Since annual value index for both the projects is less than or,e, none of them is feasible.

20 Methods for Comparing Investment Alternatives

Example 7: If N.K. Ltd. wishes to have a minimum rate of return of 10% per annum on its investment, which of the following two plans should be preferred:

Plan A

Initial cost in As. 40000

Expected life in years 5

Salvage value in As. 4000

Excess of annual receipts over disbursements in As.

1st year 8000

2nd year 8000

3rd year 8000

4th year 8000

5th year 8000

(CAF-10%-5) = 0.26380, (SFF-10%-5) = 0.1638

(Pwf--10%-1) = 0.9091

(Pwf--10%-2) = 0.8264

(Pwf--10%-3) = .7513

Solution: For Plan A

(Pwf-10%-4) = 0.6830

(Pwf-10%-5) = 0.6209

Annual Net income = 8000 + 4000 (SFF-1 0%-5)

= 8000 + 4000(0.1638)

= 8000 + 655.20 = 8655.20

Using formula Annual Value of Present Investment

= 40000 (CRF-1O%-5)

= 40000 (0.2638) = 10,552

Plan B

60000

5

18000

8000

8000

10000

12000

12000

Annual Value Index for Plan A Annual Net Income

=-------Initial Investment

8655.20 = 10,552.00 = 0.8 approx.

PlanB

Present Value of Annual Income

= Rl (Pwf-10%-l) + R2 (Pwf-10%-2) + R3 (Pwf-10%-3) + R4 (Pwf-l 0%-4) + Rs (Pwf-l 0'10-5)

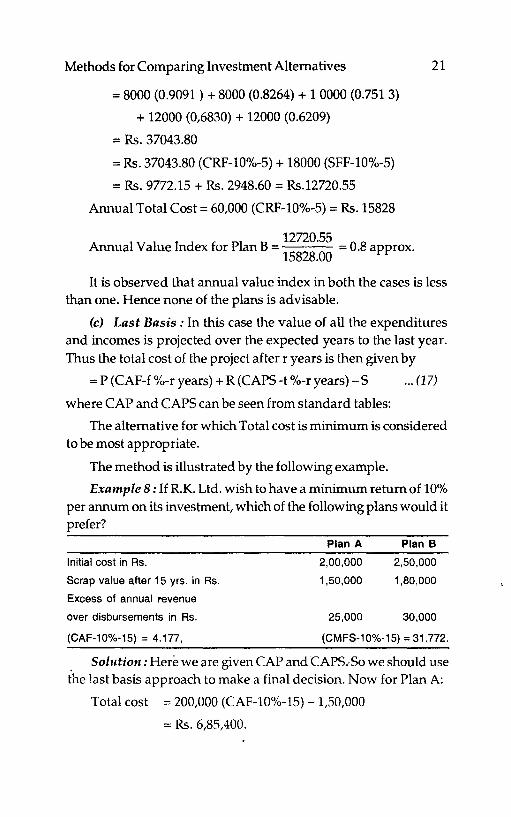

Methods for Comparing Investment Alternatives

= 8000 (0.9091 ) + 8000 (0.8264) + 1 0000 (0.751 3)

+ 12000 (0,6830) + 12000 (0.6209)

= Rs. 37043.80

= Rs. 37043.80 (CRF-10%-5) + 18000 (SFF-10%-5)

= Rs. 9772.15 + Rs. 2948.60 = Rs.12720.55

Annual Total Cost = 60,000 (CRF-10%-5) = Rs. 15828

21

12720.55 Annual Value Index for Plan B = = 0.8 approx.

15828.00

It is observed that annual value index in both the cases is less than one. Hence none of the plans is advisable.

(c) Last Basis: In this case the value of all the expenditures and incomes is projected over the expected years to the last year. Thus the total cost of the project after r years is then given by

= P (CAF-f%-r years) + R(CAPS-t %-ryears) -5 ... (17)

where CAP and CAPS can be seen from standard tables:

The alternative for which Total cost is minimum is considered to be most appropriate.

The method is illustrated by the following example.

Example 8 : If R.K. Ltd. wish to have a minimum return of 10% per annum on its investment, which of the following plans would it prefer?

Plan A Plan B

Initial cost in Rs. 2,00,000 2,50,000

Scrap value after 15 yrs. in Rs. 1,50,000 1,80,000

Excess of annual revenue

over disbursements in Rs. 25,000 30,000

(CAF-10%-15) = 4.177, (CMFS-10%-15) = 31.772.

. Solution: Here we are given CAP and CAPS.·So we should use the last basis approach to make a final decision. Now for Plan A:

Total cost = 200,000 (CAF-1O%-15) -1,50,000

= Rs. 6,85,400.

22 Methods for Comparing Investment Alternatives

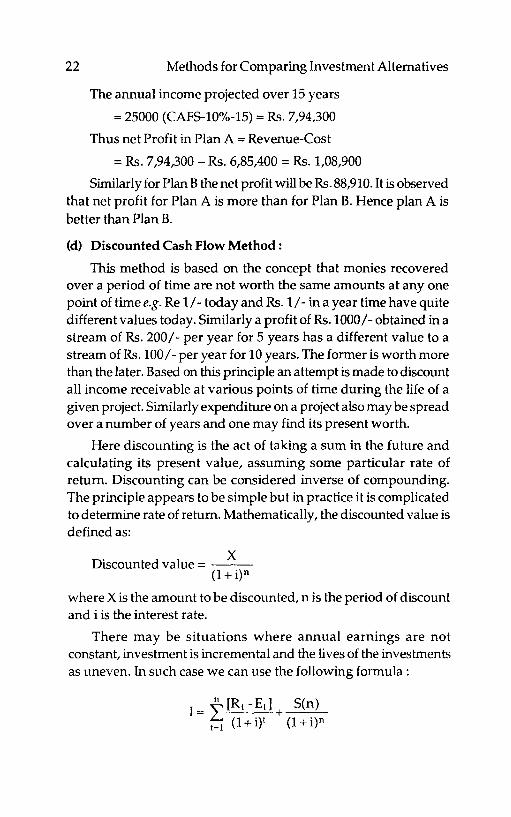

The annual income projected over 15 years

= 25000 (CAFS-1O%-15) = R<;. 7,94,300

Thus net Profit in Plan A = Revenue-Cost

= Rs. 7,94,300 - Rs. 6,85,400 = Rs. 1,08,900

Similarly for Plan B the net profit will be Rs. 88,910. It is observed that net profit for Plan A is more than for Plan B. Hence plan A is better than Plan B.

(d) Discounted Cash Flow Method:

This method is based on the concept that monies recovered over a period of time are not worth the same amounts at anyone point of time e.g. Re 1/- today and Rs. 1/- in a year time have quite different values today. Similarly a profit of Rs. 1000/- obtained in a stream of Rs. 200/- per year for 5 years has a different value to a stream ofRs.100/- per year for 10 years. The former is worth more than the later. Based on this principle an attempt is made to discount all income receivable at various points of time during the life of a given project. Similarly expenditure on a project also may be spread over a number of years and one may find its present worth.

Here discounting is the act of taking a sum in the future and calculating its present value, assuming some particular rate of return. Discounting can be considered inverse of compounding. The principle appears to be simple but in practice it is complicated to determine rate of return. Mathematically, the discounted value is defined as:

X Discounted value = --

(I + i)n

where X is the amount to be discounted, n is the period of discount and i is the interest rate.

There may be situations where annual earnings are not constant, investment is incremental and the lives of the investments as uneven. In such case we can use the following formula:

Methods for Comparing Investment Alternatives

where I investment in Rs.

n economic life in years

time variable

Rt revenue for a given period.

Et expenses for a given period.

S(n): scrap value at the end of the economic life

discount rate.

23

II. Annual Cost Approach: There are two main techniques in this approach, namely

(a) Pay-back method

(b) Rate of return method.

(a) Pay-back method: Whenever any investment is made some amount of return is always expected. Also it is hoped that the investment will be recovered within reasonable period of time. The period of recovery is of great significance for investment decisions. It is commonly known as Pay-back period and is defined to be the period within which the initial investment amount is recovered by net cash inflows. The rationale underlying the use of pay-back method is that the sooner the capital investment can be recovered, the sooner it can be reinvested in revenue producing projects.

In pay-back method, the period of recovery for each alternative investment strategy is calculated and then various alternatives are ranked in terms of recovery period viz. alternative with minimum recovery period is ranked first and so on. Payback period is the time required for each investment to return earnings equal to the cost of investment.

The method is based on the concept of net cash-inflows which is defined to be

Net cash-inflow = [Cash-inflow from earnings-expenditure on operating costs)

Note: Expenditure on operating costs is known as cash outflow. It should include income tax on earnings but should exclude depreciation costs.

24 Methods for Comparing Investment Alternatives

Now cash-inflow can be of two types (i) Even cash flow which is equal for different years and (ii) un-even cash inflow which is not same for different years In this case cumulative sum of cash-inflows is calculated for each year.

The formula for pay-back period is given by

b k . d Amount Invested Pay- ac peno = Ann 1 h ·nfl ua cas 1 ow

... (18)

The method is illustrated by the following example:

Example 9 : In an investment of Rs. 40,000 the organisation expects (i) an even cash flow of Rs. 5000 per year and (ii) uneven cash-inflow of Rs. 8000, Rs. 8000, Rs. 10,000 and Rs. 15,000 for first four years respectively. Find the pay-back period in each case.

Case(i) From (18)

P b k . d Amount Invested 40,000 8 ay- ac peno = Annual cash inflow = 5000 = years

Case (ii) In the case of uneven cash-inflows, we calculate the cumulative cash-inflow year wise to know the year by which the investment amount is likely to be recovered. The calculations can be done in the following tabular form:

Years Cash-inflow Cumulative cash-inflow

8000 8000

2 8000 16,000

3 10,000 26,000

4 15,000 41,000

It can be observed that up to 3rd year only Rs. 26,000 will be recovered. The balance of Rs. 14,000 will be recovered in fourth year. In this case:

Pay back Period in years.

Amount Invested - Amount revmoved upto 3rd year = 3 + (Total cash inflow upto 4th year - Total inflow upto 3rd year)

40,000 - 26,000 41,000 -26,000

= 3 + (14/15) years

Methods for Comparing Investment Alternatives

= 3 years 11 months

The following are the main drawbacks of payback method:

25

(i) Highly profitable projects do not necessarily pay-off in the initial years. Larger gains may occur later.

(ii) It completely ignores the time value of the money received during and after the pay-back period.

(iii) It does nO.t measure the rate of return.

(b) Return on investments method: Here profit is considered as return on investment. For various alternatives, profit is calculated after allowing for depreciation (but before taxation) expressed as a percentage of original investment. Mathematically

Percentage return on investment

Average annual income after depreciation but before taxation = xl00 Annual cash inflow

In this method allowance is made for decrease in the value of the asset due to wear and age and the cost of interest charged is spread uniformly over the projected life of the asset.

These methods may be classified as:

(i) Unadjusted rate of return method.

(ii) Time adjusted rate of return method.

(i) Unadjusted rate of return method: The method is based on certain information's extracted from various financial statements. Here future earnings on investment are not converted to get its present value, that is why it is known as unadjusted return method. The rate of return on investment is calculated for each alternative and the one providing maximum return is considered to be the best. Unadjusted rate of return is given by

Average Annual net income Unadjusted Rate of Return = A . t verage Inves ment

Average ammia cash inflor - Annual depreciation . x 100 .. .(19)

A verage Investment

26 Methods for Comparing Investment Alternatives

Now average investment can be calculated by any of the methods given below, depending upon the nature of the information available.

(a) Average investment =

(uncovered capital in the beginning +uncovered capital at theend)/2

(b) Average investment = (Initial investment + Scrap value)/2

(c) Average investment = [(capital recovered)/2] + Scrap value

... (20)

Example 10 : Rank the investment proposals in order of their profi tability using rate of return method:

Proposal It:lvestment Annual Cash flow Life In years

in Rs. in Rs.

A 25000 3000 10

8 3000 1000 5

C 12000 2000 8

0 20000 4000 10

E 40000 8000 10

Solution: Assuming scrap value to be zero and depreciation rate to be linear, we can find depreciation for each proposal by dividing the investment from life in years. The calculations can be done in the following tabular form:

Proposals Average Depreciation Cashin in flow rate of return investment - Depreciation

A 25000 = 12500 25000 = 2500 3000-2500=500 500 = 0.04

2 10 12500

B 3000 = 1500 3000 = 600 2000-600=400 400 = 0.27

2 5 1500

C 12000 = 6000 1200 =1500 2000-1500=500 500 = 0.33

2 8 1500

0 20000 = 10 000 20000 = 2000 4000-2000=2000

2000 = 0.20 ,2 • 10 10,000

E: 40000 = 20,000 40000 = 4000 8000-4000=4000

4000 = 020 2 10 20,000

A 25000 = 12500 25000 = 2500 3000-2500=500 ~=004

2 10 12500

Methods for Comparing Investment Alternatives 27

Thus the ranking of the proposals are C, B, D, E and A.

Example 11 : A limited company is considering the purchase of one of the two machines with following details: Find the best choice by rate of return method:

Machine X Machine Y

Life 3 years 3 years

Capital Cost As. 1,00,000 As. 1,00,000

Earnings after tax

is

1st year As. 80,000 As. 20,000

2nd year As. 60,000 As. 70,000

3rd year As. 40,000 As. 1,00,000

Solution: Now Average annual cash inflow for the two machines

Machine A = 80,000 + 60,000 + 40,000 = Rs. 60,000 3

M h' B - 20,000+70,000+1,00,000 - Rs 3 00 ac me - 3 - . 6 ,3

D .. f A 100,000 3 3 epreclatIon or = 3 3 3 3

. . 100,000 DeprecIatIon for B = = 33333

3 Average investment for both the machines is

RD' . f j\ 100,000 s. epreclatlOn or' = 2 = 50,000.

Hence from (19)

rate of return for A = 60,000 -33333 = 0.53 50,000

rate of return for B = 63300 - 33333 = 0.60 50,000

(b) Time Adjllsted rate of return method: According to National Association of Accountants, America, "Time adjusted rate of rehlrn is the maximum rate of interest that could be paid for the capital employed over the life of an .investment without loss on the project."

28 Methods for Comparing Investment Alternatives

There are many other names of this method viz. Discounted rate of return method, Internal rate of return method etc. This method is particularly useful when the rate of return on investments is not known exactly.

The method consists of following steps:

(i) Find the ratio of cost of investment and annual cash-in flow.

(ii) For the value obtained in (i), find present value factor from Pwfs table for the given period.

In the case of uneven cash-inflows, trial and error method can be used.

The method is illustrated by the following examples:

Example 12 : An investment of Rs. 12000 provides the annual cash inflows of Rs. 2000, Rs. 3000, Rs. 5000 and Rs. 6000 respectively in 1st, 2nd, 3rd and 4th years. Find Time adjusted rate of return.

Solution: Here there is an uneven cash inflow. So we shall apply trial and error method to find time adjusted rate of return.

First of all we find average annual cash-inflow

= 2000 + 3000 + 5000 + 6000 = 4000 4

Hence

present value factor = Investment = 12000 = 3.0 A verage cash inflow 4000

In Pwfs table, we find that in the row of fourth year, the value 3.0 lie in the column of 12%. Hence at first iteration the time adjusted rate of return is found to be 12%. Now at this rate of return, we can calculate the present value of cash- infllows for different years in the following tabular form:

Year Cash inflow Pwf at 12% Present Value in Rs.

1 2000 0.8929 1785.80

2 3000 0.7972 2391.60

3 5000 0.7118 3559.00

4 6000 0.6355 3813.00

Total 11549.40

Methods for Comparing Investment Alternatives 29

It can be seen that with rate of return to be 12% the total amount recovered in 4 years is Rs. 1 1549.40, which is less than the total investment of Rs. 12000. So the time adjusted rate of return should

be somewhere between 12% and 13%.

The following are the drawbacks of rate of return method:

(i) It fails to give full effect to the time value of money, especially in cases where investments are made at different periods of time or

when income from investments is not likely to accrue at a uniform rate.

(ii) The method does not recognize the true return on capital investments.

In both these techniques no account is taken of the time at which the earnings are made.

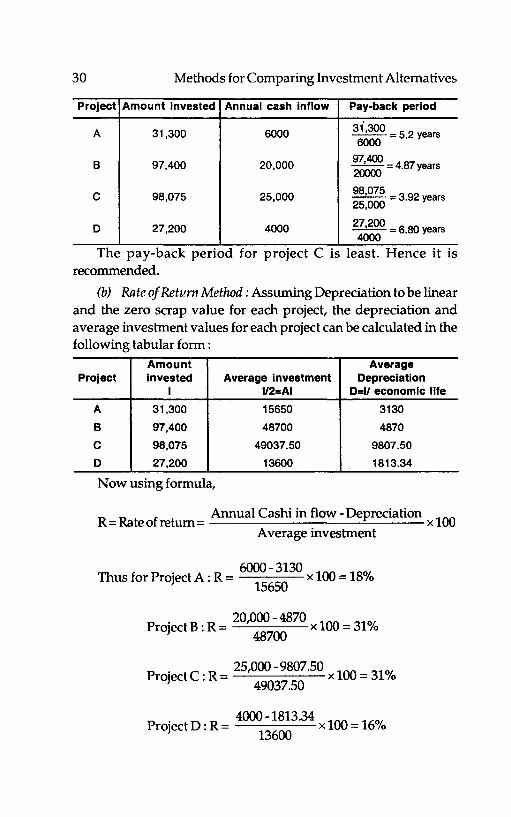

Example 13 : Bajaj Auto Parts Ltd. is screening projects for capital expenditure. They have only Rs. 1,00,000 for investment. The following proposals have been submitted:

to:

Project Investment Cash Flow EconomiC life

Rs. Rs. years

A 31,300 6,000 10

B 97,400 20,000 20

C 98,075 25,000 10

D 27,200 4,000 15

If cost of capital is 20%, please recommend projects according

(a) Pay-back period method

(b) Rate of return meth'Od

(c) Present value index method. Solution:

(a) Pay-back Period method:

Amount investment Pay back period = Annual Cash inflow

The pay-back period for each project can be calculated in the following tabular form:

30 Methods for Comparing Investment Altemativeb

Project Amount invested Annual cash inflow Pay-back period

A 31,300 6000 3(300 --=52 years

6000 .

B 97,400 20,000 97400 ~ = 4.87 years

C 98,075 25,000 98075 25:000 = 3.92 years

0 27,200 4000 27,200 --= 6.80 years

4000

The pay-back penod for project C 1S least. Hence 1t 1S recommended.

(b) Rate o/Return Method: Assuming Depreciation to be linear and the zero scrap value for each project, the depreciation and average investment values for each project can be calculated in the following tabular form :

Amount Average Project invested Average investment Depreciation

I 1/2=AI D=II economic life

A 31,300 15650 3130

B 97,400 48700 4870

C 98,075 49037.50 9807.50

0 27,200 13600 1813.34

Now using formula,

R Ra f Annual Cashi in flow - Depreciation 100

= teo retum= x Average investment

6000-3130 Thus for Project A : R = x 100 = 18%

15650

20,000 - 4870 Project B : R = x 100 = 31%

48700

Pr' C· = 25,000-9807.50 xl00=31% oJect . R 49037.50

4000 -1813.34 Project D : R = x 100 = 16%

13600

Methods for Comparing Investment Alternatives 31

The rate of return is same for Project Band C being 31 %. Any of these can be recommended.

(c) Present value index method:

From formula,

1 I d Present value of future income

Present va ue n ex = al Initi investment

Here salvage value is assumed to be zero. The present value of future income

= Cash inflow (Pwfs -t%-r)

P.V.1. for Project A 6000 (Pwfs-20%-10)

= 31300

= 6000 x 4.1925 = 0.80 31300

20000 (Pwfs - 20% - 20) P.V.1. for Project B = --~-~--~

97400

= 20000 x 4.8696 = 0.99 97400

P V I f p. C 25000 (Pwfs-20%-10) . . . or rOJect = 98075

= 25000 x 4.1925 = 1.07 98075

4000 (Pwfs - 20% -15) P.V. I. for Project D = 27200

= 4000 x 4.6755 = 0.69 27200

The present value index of future income is maximum for project C . Hence it should be recommended.

***

Chapter

3

** REPLACEMENT ANALYSIS

The problem of replacement is an everyday phenomena. It is experienced in systems where machines, individuals or capital assets are the main job performing units. It is a common phenomena that performance / efficiency of a fixed asset in a system deteriorates with time. The remedy is either to replace the fixed asset with some new fixed asset or to restore the level of performance by some sort of maintenance. Also, there comes a stage where maintenance of any fixed asset becomes so much expensive that it is more profitable to replace the fixed asset. Thus there is a necessity to formulate a most economic replacement policy which is in the best interest of the system.

The major reasons for replacement are:

(i) Deterioration: Decline in performance due to wear and tear indicated by increase in maintenance costs; reduction in product quality and rate of production, increase in labour costs, loss of operating time etc.

(ii) Obsolescence: It may be due to advancement in technology. This reduces profits, impairs competition, causes loss in the value of machinery.

(iii) Inadequacy: Equipment's capacity may not be sufficient to meet the demand or it is not able to increase the production rate to desired level.

Replacement Analysis 33

(iv) Working conditions: Causing unsafety to workers and leading to accidents, making the environment noisy and smoky etc.

(v) Economy: The existing units have outlived their effective life and it is not economical to continue with them.

(vi) The existing units breakdown, perished or destroyed all of a sudden.

Some special characteristics of replacement are:

(i) replacement reduces maintenance costs but it involves a high average capital cost.

(ii) many people feel that an equipment should not be replaced until it is physically worn out. But this attitude is never in the interest of the organisation. On the contrary the equipment's must be constantly reviewed and updated, otherwise these may become obsolete.

Replacement Models and Their Solutions:

The study of replacement is some kind of application mostly concerning comparison of alternative replacement policies. The various factors relevant to replacement analysis can be divided into two main categories; namely,

(i) Technical: Deterioration, Obsolescence, Inadequacy.

(ii) Financial: Initial cost; operating costs; labour costs, material costs; maintenance costs, salvage value, insurance etc.

A well designed replacement policy should compare thoroughly an existing equipment with its possible replacement. In order to make a sound economic comparison strategy all the factors should be converted into costs.

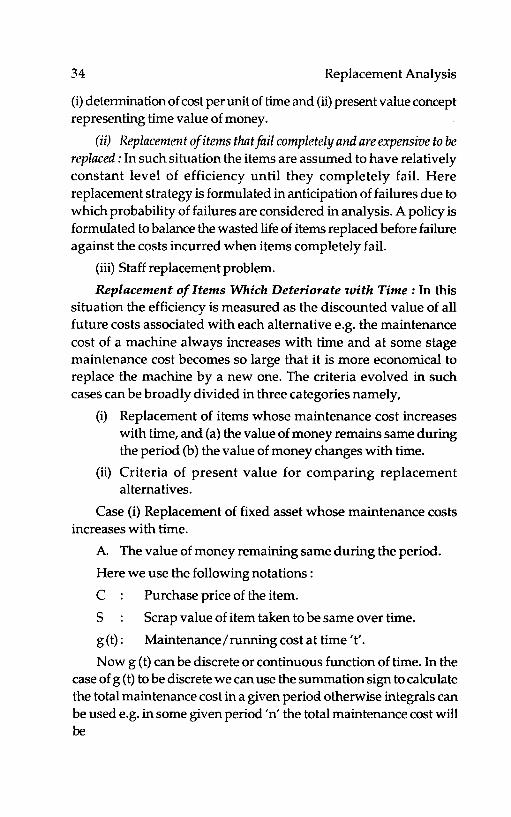

The different types of replacement problems can be broadly classified in following situations:

(i) Replacement of Items Whose Efficiency Deteriorates with Time: The simplest replacement model in such cases is one where the deterioration rate is predictable in terms of increasing maintenance costs and decrease in salvage value with time. The expenditure on replacement items is considered here as cost of replenishment in inventory analysis and maintenance costs are like holding costs. There are two methods to find appropriate solution in this case viz.

34 Replacement Analysis

(i) delermination of cost per unit of time and (ii) present value concept representing time value of money.

(ii) Replacement of items that fail completely and are expensive to be replaced: In such situation the items are assumed to have relatively constant level of efficiency until they completely fail. Here replacement strategy is formulated in anticipation of failures due to which probability of failures are considered in analysis. A policy is formulated to balance the wasted life of items replaced before failure against the costs incurred when items completely fail.

(iii) Staff replacement problem.

Replacement of Items Which Deteriorate with Time: In this situation the efficiency is measured as the discounted value of all future costs associated with each alternative e.g. the maintenance cost of a machine always increases with time and at some stage maintenance cost becomes so large that it is more economical to replace the machine by a new one. The criteria evolved in such cases can be broadly divided in three categories namely,

(i) Replacement of items whose maintenance cost increases with time, and (a) the value of money remains same during the period (b) the value of money changes with time.

(ii) Criteria of present value for comparing replacement alternatives.

Case (i) Replacement of fixed asset whose maintenance costs increases with time.

A. The value of money remaining same during the period.

Here we use the following notations :

C Purchase price of the item.

S Scrap value of item taken to be same over time.

g (t) : Maintenance / running cost at time '1'.

Now g (t) can be discrete or continuous ftmction of time. In the case of g (t) to be discrete we can use the summation sign to calculate the total maintenance cost in a given perioa otherwise integrals can be used e.g. in some given period 'n' the total maintenance cost will be

Replacement Analysis

n

M(n) = L g(t), when t is discrete t=O

and Jong(t) dt, when t is continuous.

35

Thus the total cost incurred on the item in some period n is given by

Total cost = cost of the item + total maintenance cost in period 'n'

- scrap value = C + M(n) - 5

Thus the average cost incurred per year on the item is given by

C+M(n)-S G(n) = ----'-~

n

Now it is advisable to replace the item when G (n) is maximum. Without going into the mathematical treatment it can be seen that G (n) will be minimum when

and

9(n) <

G(n) <

G(n-1)

g(n+1)

So we get the following replacement criteria in this case. Do not replace the item if the next year maintenance cost is less than the average cost of the previous year and replace the item if next years average cost is less than the maintenance cost of next year i.e. when Average Cost is least.

The method is explained by the follOWing examples:

Example 1 : The cost of a machine is Rs. 6100 and its scrap value is Rs. 100. The maintenance costs are found to be :

Year 1 2 3 4 5 6 7 8 Maintenance

Cost in Rs. 100 250 400 600 900 1200 1600 2000

When should the machine be replaced?

Solution: Here C = 6100, 5 = 100 and the maintenance costs are given at discrete values of time~ The total average costs in different years can be calculated in the following tabular form:

36 Replacement Analysis

Cumulative value of (2)

Year g(n) M(n) C + M(n)-S G(n) = C+M(n)-S

n (n) i.e. col. (4)/col(1)

(1 ) (2) (3) (4) (5)

1 100 100 6100 6100

2 250 350 6350 3175

3 400 750 6750 2250

4 600 1350 7350 1837.50

5 900 2250 8250 1650.00

6 1200 3450 9450 1575.00'

7 1600 5050 11050 1578.57

8 2000 7050 13050 1631.25

"Average cost is minimum. Hence the machine should be replaced at the end of the sixth year.

Example Z: A manufacturer finds from his past records that the costs per year associated with a machine with purchase price of Rs. 5000 are as given below:

Year(n) 2 3 4 5 6 7 8 Running

cost g(n) 1500 1600 1800 2100 2500 2900 3400 4000

Scrap S(n) 3500 2500 1700 1200 1000 500 500 500

Determine the optimal replacement policy:

Solution: Here C = 5000 and 5 (n) = scrap value is decreasing with time. So the value of C - 5 will change with time in this case. The calculations can be done in the following tabular form.

Year S(n) C-S(n) g(n) Cumula- Col(3)+(5) G (n)

(n) tive C+M(n) col(6)/(1)

g(n) = - S(n)

M(n)

(1 ) (2) (3) (4) (5) (6) (7)

1 3500 1500 1500 1500 3000 3000

2 2500 2500 1600 3100 5600 2800 . 3 1700 3300 1800 4900 8200 2733

4 1200 3800 2100 7000 10800 2700

Replacement Analysis 37

5 1000 4000 2500 8500 13500 2700

6 500 4500 2900 12400 16900 2816

7 500 4500 3400 15800 20300 2900

8 500 4500 4000 19800 24300 3037

'minimum

The average cost G (n) is minimum in 5th year. Hence 5 years is the optimal replacement interval.

Example 3 : A truck owner has three trucks, two of which are two years old and the third is one year old. The cost price, operating costs and resale value of these trucks are same as given below: Year Running 1 2 3 4 5 6 7 8

cost 1000 1200 1400 1800 2300 2800 3400 3400

Resale 3000 1500 750 375 200 200 200 200 Value

The cost price is Rs. 6000/-.

He is considering a new type of truck with 50% more capacity than one of the old ones at an unit price of Rs. 8000/- . He estimates that the running costs and resale price for the new truck will be:

Year 2 3 4 5 6 7 8

Running costs 1200 1500 1800 2400 3100 4000 5000 6100

Resale price 4000 2000 1000 500 300 300 300 300

Assuming that the loss of flexibility due to fewer trucks is of no significance, and that he will continue to have sufficient work for three of the old trucks, what should his policy be?

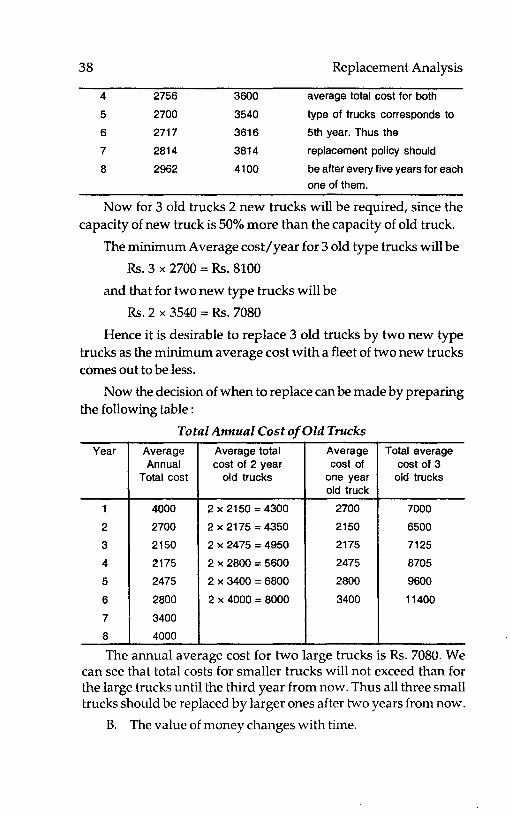

Solution: First of all we have to calculate average total cost for each of the two types of trucks.

On the basis of the calculations as illustrated in Example 23 the average total cost for each of the category will be

Years Average Cost New Type (n) for Type I

4000 5200 The following observations

2 3350 4350 are made from these

3 2950 3833 calculations. (i) The minimum

38 Replacement Analysis

4 2756 3600 average total cost for both

5 2700 3540 type of trucks corresponds to

6 2717 3616 5th year. Thus the

7 2814 3814 replacement policy should

8 2962 4100 be after every five years for each

one of them.

Now for 3 old trucks 2 new trucks will be required, since the capacity of new truck is 50% more than the capacity of old truck.

The minimum Average cost/year for 3 old type trucks will be

Rs.3 x 2700 = Rs. 8100

and that for two new type trucks will be

Rs. 2 x 3540 = Rs. 7080

Hence it is desirable to replace 3 old trucks by two new type trucks as the minimum average cost with a fleet of two new trucks comes out to be less.

Now the decision of when to replace can be made by preparing the following table:

Total Annual Cost of Old Trucks

Year Average Average total Average Total average Annual cost of 2 year cost of cost of 3

Total cost old trucks one year old trucks old truck

1 4000 2 x 2150 = 4300 2700 7000

2 2700 2 x 2175 = 4350 2150 6500

3 2150 2 x 2475 = 4950 2175 7125

4 2175 2 x 2800 = 5600 2475 8705

5 2475 2 x 3400 = 6800 2800 9600

6 2800 2 x 4000 = 8000 3400 11400

7 3400

8 4000

The annual average cost for two large trucks is Rs. 7080. We can see that total costs for smaller trucks will not exceed than for the large trucks until the third year from now. Thus all three small trucks should be replaced by larger ones after two years from now.

B. The value of money changes with time.

Replacement Analysis 39

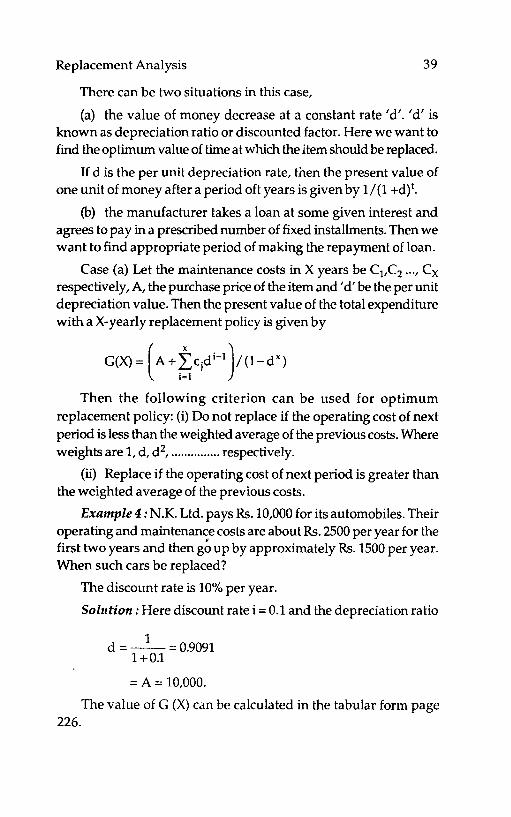

There can be two situations in this case,

(a) the value of money decrease at a constant rate 'd'. 'd' is known as depreciation ratio or discounted factor. Here we want to find the optimum value of time at which the item should be replaced.

If d is the per unit depreciation rate, t.hen the present value of one unit of money after a period oft years is given by 1/(1 +dt

(b) the manufacturer takes a loan at some given interest and agrees to pay in a prescribed number of fixed installments. Then we want to find appropriate period of making the repayment of loan.

Case (a) Let the maintenance costs in X years be C1,C2 ... , Cx respectively, A, the purchase price of the item and' d' be the per unit depreciation value. Then the present value of the total expenditure with a X-yearly replacement policy is given by

G(X) = (A + ~Cjdi-l)/ (l-d X)

Then the following criterion can be used for optimum replacement policy: (i) Do not replace if the operating cost of next period is less than the weighted average of the previous costs. Where weights are 1, d, d 2, ........•••••.. respectively.

(ii) Replace if the operating cost of next period is greater than the weighted average of the previous costs.

Example 4 : N.K. Ltd. pays Rs. 10,000 for its automobiles. Their operating and maintenance costs are about Rs. 2500 per year for the first two years and then g~ up by approximately Rs. 1500 per year. When such cars be replaced?

The discount rate is 10% per year.

Solution: Here discount rate i = 0.1 and the depreciation ratio

d =_1_=0.9091 1 +0.1

= A = 10,000.

The value of G (X) can be calculated in the tabular form page 226.

40 Replacement Analysis

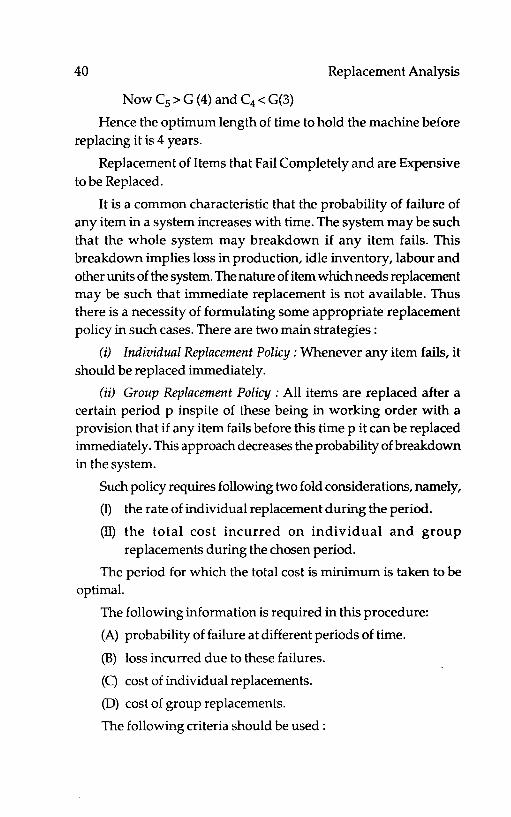

Now Cs > G (4) and C4 < G(3)

Hence the optimum length of time to hold the machine before replacing it is 4 years.

Replacement of Items that Fail Completely and are Expensive to be Replaced.

It is a common characteristic that the probability of failure of any item in a system increases with time. The system may be such that the whole system may breakdown if any item fails. This breakdown implies loss in production, idle inventory, labour and other units of the system. The nature of item which needs replacement may be such that immediate replacement is not available. Thus there is a necessity of formulating some appropriate replacement policy in such cases. There are two main strategies:

(i) Individual Replacement Policy: Whenever any item fails, it should be replaced immediately.

(ii) Group Replacement Policy: All items are replaced after a certain period p inspite of these being in working order with a provision that if any item fails before this time p it can be replaced immediately. This approach decreases the probability of breakdown in the system.

Such policy requires following two fold considerations, namely,

(1) the rate of individual replacement during the period.

(ll) the total cost incurred on individual and group replacements during the chosen period.

The period for which the total cost is minimum is taken to be optimal.

The following information is required in this procedure:

(A) probability of failure at different periods of time.

(B) loss incurred due to these failures.

(C) cost of individual replacements.

(0) cost of group replacements.

The following criteria should be used:

Replacement Analysis 41

Group replacement should be made at the end of tth period if the cost of individual replacement for tth period is greater than average cost per period by the end of period t and one should not adopt a group replacement policy if the cost of individual replacement at the end of (t-1)th period is not less than the average cos t per period through time (t -1).

Example 5 : A Computer contains 10,000 resistors. When any resistor fails, it is replaced. The cost of replacing a resistor individually is Rs. 1/- only. If all the resistors are replaced at the same time, the cost per resistor would be reduced to 15 paise. The percent surviving say S (t) at the end of month and P(t) the probability of failure during the month tare t 0123456

S(t) 100 97 90 70 30 15 0

P{t) 0.03 0.07 0.20 0.40 0.15 0.15

What is the optimum replacement plan?

Solution: The whole problem can be divided into two parts.

1. There is a policy of individual replacement.

2. There is a policy of group replacement.

It should be noted that no resistor survives for more than 6 months. Thus a resistor which has survived for 5 months is sure to fail during sixth month. We assume that the resistors failing during a month are replaced just at the end of the month.

Let Ni denote the number of resistors replaced at the end of ith month.

The different values of Ni can be calculated in the following way:

No = Number of resistors in the beginning = 10,000.

N} = Number of resistors being repliiced by the end of 1st month.

= Number of resistors during the 1st month X probability that a resistor fails during 1st month of its installation.

= 10,000 x 0.03

300.

42 Replacement Analysis

N2 Number of resistors replaced by the end of second month.

N3

N4

Ns

= (Number of resistors in beginning X probability that these fail in 2nd month) + (Number of resistors replaced in first month X Probability that these will fail during second month)

= =

= = -

= =

NOP2+NIPI 10,000 x 0.07 + 300 x 0.03

709

NOP3 + NIPI + N2PI 10,000 x 0.20 + 300 x 0.07 + 709 x 0.03

2042

NoPs + N IP3 + N2P2 + N4PI

10,000 x 0.40 + 300 x 0.20 + 709 x 0.07 + 2042 x 0.03

4171

NoPs + N IP4 + N2P3 + N3P2+N4PI 10,000 x 0.15 + 300 x 0.40 + 709 x 0.20 + 2042 x 0.07 + 4171x 0.03

= 2030

N6 = NoP 6 + NIPS + N2P 4 + N3P3 + N4P2 + NSPI = 10,000 x 0.15 + 300 x 0.15 + 709 x 0.40 + 2042 x 0.20

+ 4171 x 0.07 + 2030 x 0.03

= 2590

It can be seen from above calculations that Nj increases up to fourth month and then qecreases. It can also be seen that Nj will later tend to increase and the value of Nj will oscillate till the system acquires a steady state.

The expected life of each resistor is

= ~~Pi' where "t is the month and Pi is the corresponding

probability of failure.

= 1 x 0.03 + 2 x 0.07 + 3 x 0.20 + 4 x 0.40 + 5 x 0.15

Replacement Analysis 43

+ 6 x 0.15

= 4.02 months

Average number of replacements every month

N 10000 (mean age) 4.02

= 2487.5 -~488-resistors.

Hence average cost of monthly individual replacement- policy = Rs. 2488/-(the cost being Rs. II - per resistor).

Now let us consider the policy of group replacement. End of Total cost of group replacement Cost/month month in Rs. in Rs.

300 x 1 + 10,000 x 0.35 3800.00

= 3800

2 (300 + 709) x 1 + 10,000 x 0.35 = 4509 2254.50

3 (300 + 709 + 2042) x 1 + 10,000 x 0.35 = 6551 2183.66

4 (300 + 709 + 2042 + 4171) x 1 + 10,000 x 0.35 =10722 2680.50

5 (300 + 709 + 2042 + 4171 + 2030) x 1 + 10,000

x 0.35 = 12752 2550.40

6 15442 2557.00

Hence the minimum cost per month is obtained by group replacement of all resistors after three months with an average cost of Rs. 2183.66 per month.

***

Chapter

4

** FARM MANAGEMENT

With the advent of green revolution in India, there has been shift from the traditional system of subsistence type of farming to the new market oriented commercial type of agriculture. The change is being brought about by the employment of scientific and technological advances. Some of the seed are seed of high yielding varieties, fertilizers, plant protection chemicals, new implements and equipment's, improved cropping system, improved water management and use etc. The changes in input use entail the expenditure of larger sums of money to purchase the inputs and consequently have increased the demands for additional funds and sources of credit to finance the agricultural operations. Farming is changing from a way of life to a business-oriented agriculture.

With this change, farmers are favoured with new opportunities and possibilities but are faced with more complex problems of farm organization and operation and are in need of greater management skills to cope with the changes.

Farmers need information on various physical and biological relationship involved in crops and livestock production and also need information on price trends, credit availability and government programmes and policies.

Farm Management 45

Farm Management Deals with Managerial Input:

With the increasing need of managerial input for modern agriculture, 'Farm management' as a subject has gained immense importance among the subjects related to agricultural production.

Although the farm is an economic and social institution developed over many centuries, the scientific management of farm as a business is relatively new. Because of its recent origin, the term farm-management is understood in various ways by different people. There are many definitions of farm management but to understand as to what this term actually means there can be expression as blow:

"Farm management is the science which deals with rational decisions on the use of scarce farm resources, having alternative uses to obtain the maximum profit and family satisfaction on a continuous basis from the farm as a whole and under sound farming programmes."

Farm management science as compared with other fields of agricultural science has many important features. This is a practical and integrating science which is profitability oriented and has macro:approach considering farm unit as a whole. Farmmanagement is the field of agriculture science which is primarily and basically related to human being and its concern with crops and livestock is only secondary.

For successful farm management there is need on the part of farmEr to possess ability and capacity to make correct decisions. Nielson has elaborated the decision making process by proposing following eight functions.

1. Formulation of goals or objective of the farm;

2. Recognition and definition of a problem or opportunity;

3. Obtaining information-observation of relevant facts;

4. Specification and analysis of alternatives;

5. Decision making-choosing an alternative;

6. Taking action;

46 Farm Management

7. Bearing responsibility for the decision or action taken.

8. Evaluating the outcome.

Farm Planning an Effective Tool to Help Farmer make Better Production Decision:

At the micro-level efforts have been directed primarily to extending new inputs, such as fertilizer, irrigation, improved seeds and new techniques of production viz, improved methods of sowing, manuring, fertilizing and irrigation to the farmer. Very little has been done to improve the managerial ability of the farmer. In other words, there has been greater emphasis on providing farm people with new information and inputs rather than m helping them apply these to their own situations. Farm planning aims at providing such help to the farmer.

Farm Planning as Related to Credit :

In under-developed conditions "farm planning" is considered to provide a method by which the farmer with limited available assets can be made credit worthy and thus be able to obtain the needed production supplied and other capital needs In other words, the farm plan provides the farmer with the technical possibility of achieving additional yield and eventually guarantees additional incomes. This additional income forms a source of credit which enables the farmer to borrow funds from institutions to buy mater also needed for production increase. In this case, the plan is regarded as planned repaying capacity for loans.

Concept of Farm Planning:

In farm planning the fundamental concept is to look at the farm as a single operating unit. The kit of the farm planner should include the micro-economic principle, technical knowledge pertaining to different aspects of agricultural science, and information relating to the farm and farmer. The job of a farm planner is to use these information's to help the farmer to ~ake changes in the:

(i) Crop and livestock enterprises on the farm-selection of a product-mix,

(ii) inputs used on the farm-selection on an input complex,

Farm Management 47

(iii) techniques of production-choice as to how to produce and

(iv) marketing procedures choice as to when, where and how to market farm products and purchase farm inputs.

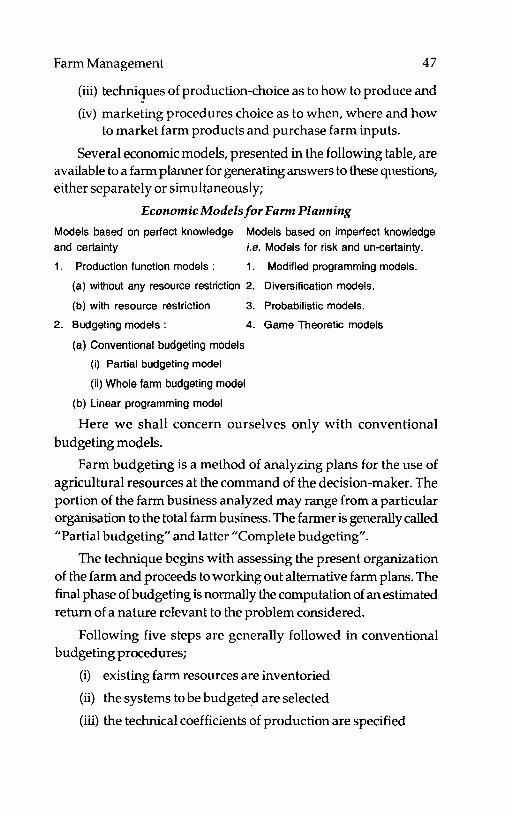

Several economic models, presented in the following table, are available to a farm planner for generating answers to these questions, either separately or simultaneously;

Economic Models for Farm Planning

Models based on perfect knowledge Models based on imperfect knowledge and certainty

1. Production function models:

i.e. Models for risk and un-certainty.

1. Modified programming models.

(a) without any resource restriction 2. Diversification models.

(b) with resource restriction

2. Budgeting models:

(a) Conventional budgeting models

(i) Partial budgeting model

(ii) Whole farm budgeting model

(b) Linear programming model

3. Probabilistic models.

4. Game Theoretic models

Here we shall concern ourselves only with conventional budgeting models.

Farm budgeting is a method of analyzing plans for the use of agricultural resources at the command of the decision-maker. The portion of the farm business analyzed may range from a particular organisation to the total farm business. The farmer is generally called "Partial budgeting" and latter "Complete budgeting".

The technique begins with assessing the present organization of the farm and proceeds to working out alternative farm plans. The final phase of budgeting is normally the computation of an estimated return of a nature relevant to the problem considered.

Following five steps are generally followed in conventional budgeting procedures;

(i) existing farm resources are inventoried

(ii) the systems to be budgete,d are selected

(iii) the technical coefficients of production are specified

48 Farm Management

(iv) prices for inputs and products are specified and

(v) costs and returns are calculated.

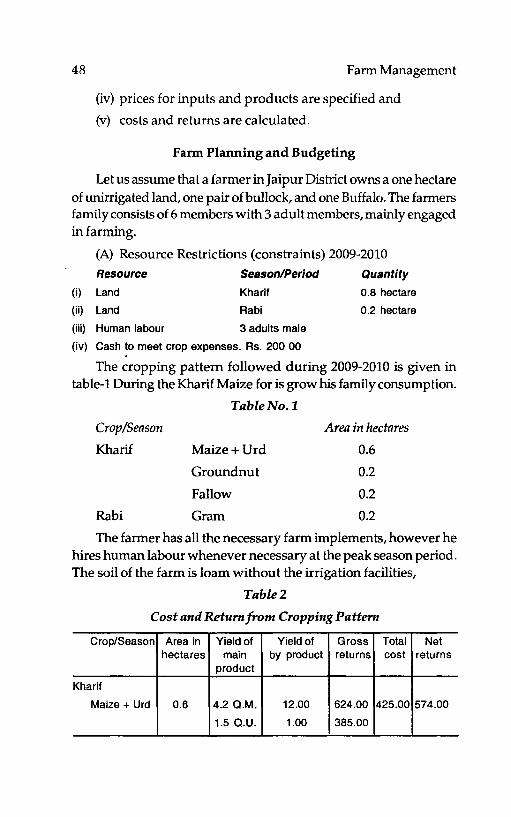

Farm Planning and Budgeting

Let us assume that a farmer in Jaipur District owns a one hectare of unirrigated land, one pair of bullock, and one Buffalo. The farmers family consists of 6 members with 3 adult members, mainly engaged in farming.

(A) Resource Restrictions (constraints) 2009-2010 Resource

(i) Land

(ii) Land

Season/Period

Kharif

Rabi

(iii) Human labour 3 adults male

(iv) Cash to meet crop expenses. Rs. 200 00

Quantity

0.8 hectare

0.2 hectare

The cropping pattern followed during 2009-2010 is given in table-1 During the Kharif Maize for is grow his family consumption.

Crop/Season

Kharif

Rabi

Table No. 1

Maize + Urd

Groundnut

Fallow

Gram

Area in hectares

0.6

0.2

0.2

0.2

The farmer has all the necessary farm implements, however he hires human labour whenever necessary at the peak season period. The soil of the farm is loam without the irrigation facilities,

Table 2

Cost and Return from Cropping Pattern

Crop/Season Area in Yield of Yield of Gross Total Net hectares main by product returns cost returns

product

Kharif

Maize + Urd 0.6 4.2 Q.M. 12.00 624.00 425.00 574.00

1.5 Q.U. 1.00 385.00

Farm Management 49

1009.00

Groundnut 0.2 1.6 1.5 335.00 256.00 79.00

Fallow 0.2 - - - - -Aabi

. Gram 0.2 1.5 1.5 285.00 119.00 166.00

1.00 1629.00 800.00 819.00

In the month of May, 81 the farmer constructed a pacca well on his farm which can command only 0.9 hectares of land. The water quality is good and adequate water is in the well. The farmer has also purchased necessary equipment's for irrigation purpose.

Selection of Activities:

Keeping in mind the resource constraints given in table-I, the land acreage is to be allocated on the basis of maximum net returns, per unit area from different crops.

Physical Norms for Important Crop of the Region

Table-3

Items

1. Fertilizer if' (Kg)

N

P

K

2 Plant protection in (Rs.

3 Seed in (Kg)

4. Human labour in

man days

5. Bullock pair days

6 Yield of main products

in aIls

Price of inputs (As.)

N@As. 3/- Kg.

P@As. 2/- Kg.

Crop Varieties

Maize Maize Groundnut Groundnllt Wheat Local Hybrid Local Improved Hybrid

28 60 - 20 80

- 40 - 60 40

- - - - -

- 100.00 - 12000 100.00

30 20 100 100 100

70 110 50 90 120

19 30 11 12 30

7.00 30.00 800 1500 3500

Price of Inputs and Output Output prices (As.)

Wheat@As. 125/- quintal

Gram@As. 170/- quintal

Gram Hybrid

20

40

-130.00

75

64

16

1500

50 Farm Management

Seed: Maize@Rs. 120/- quintal

Maize local @ 1.5/Kg. Urd@Rs. 250/- quintal

Maize Hybrid @4.00/Kg. Groundnut@Rs. 200/- quintal

Groundnut local @2/- Kg.

Groundnut improved @4/ Kg.

Urd local @3 5/Kg.

Enterprize Budget

Table 4

(in Rupees)

item of Maize •• Maize Groundnut Groundnut Kharif Wheat Grar.1 expenditure Local Hybrid Local Improved pulses HYV Improved

(Urd)

•• With one Improved practice

Fertilizer

N 84 100 60.00 60.00 240.00 60.00

P III 120.00 0000 00.00 00.00

K

Planet Protection 100 120.00 10000 130.00

Seed 45 III 200 400.00 70.00 250.00 150.00

Human labour 350 550 250 450.00 165.00 600.00 320.00

Bullock 228 360 132 144.00 120.00 36000 192.00

Total 707 1350 5lI2 1294.00 49500 1630.00 93200

Interest on working .. 3535 6750 29.10 74.50 24.75 81.50 4660 caprtal @ 1 0% for 6 months

Total cash expenditure 742.35 1417.50 611.10 136850 519.75 171150 978.60

Yield of main products 840.00 3600.00 1600.00 300000 2000.00 437500 2550.00

Yield of by products 28000 1200.00 00.00 520.00 150.00

Gross return 1120.00 480000 1600.00 3000.00 200000 4895.00 2700.00

Net returns 377.65 238300 98900 2632.00 1570.00 3184.00 1722.00

Plan for 0.9 hectare of Irrigated Farm 2010-2011

In his alternative plan for the year 2010-2011, the farmer would like to grow 6.00 quintals of maize and quintals gram 1.5 for his family consumption in kharif and rabi seasons respectively. These activities are called predetermined activities, which the farmers plan to undertake irrespective of their profitability.

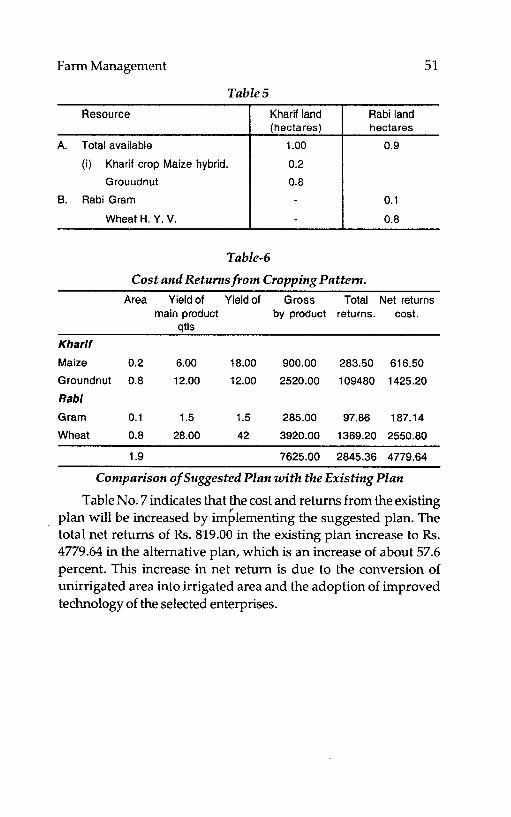

Farm Management

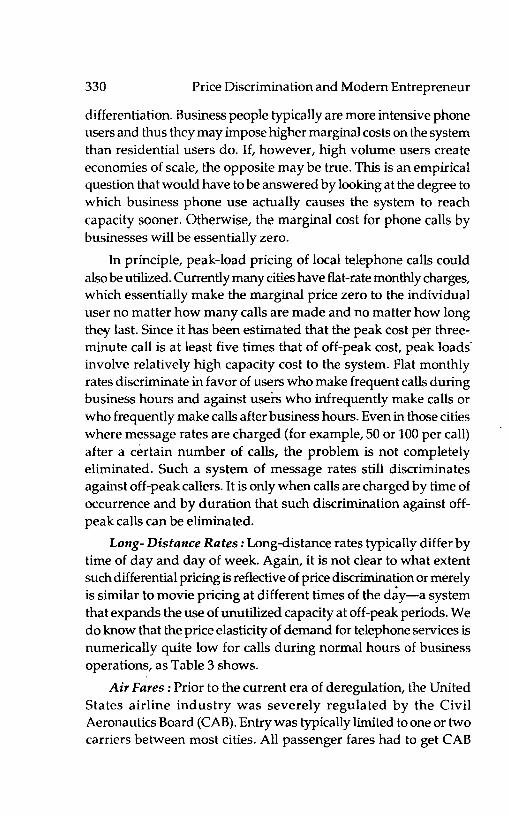

TableS

Resource

A. Total available

(i) Kharif crop Maize hybrid.

Grouudnut

B. Rabi Gram

Wheat H. Y. V.

Table-6

Kharif land (hectares)

1.00

0.2

0.8

Rabi land hectares

0.9

0.1

0.8

51

Cost and Returns from Cropping Pattern.