mining monitor (february 2017) - bk.mufg.jp · impact on chinese coal miners’ output. however,...

TRANSCRIPT

Mining Monitor (February 2017)

Strategic Research Division,

Corporate Research Office

7 February 2017

The Bank of Tokyo-Mitsubishi UFJ, Ltd.

MUFG Union Bank, N.A.

Table of Contents

1. Overview 3

2. Iron Ore 5

3. Coal 8

4. Copper 11

5. Aluminum 14

Mining Monitor | 7 February 2017 2

6. Nickel 17

7. Zinc 20

8. Gold 23

Appendix 26

1. Overview

Mining Monitor | 7 February 2017 3

Takuya Eto

Strategic Research Division,

Corporate Research Office

THE BANK OF TOKYO-MITSUBISHI UFJ, LTD.

Mining Monitor | 7 February 2017 4

Mined Commodity Price Trends

The prices of mined commodities were by and large solid in January 2017 related with growing demand or short

supply mainly in China. Prices of some commodities were affected by government decisions or speculative factors.

1. Overview

Mined Commodity Price Trends

In January 2017, the prices of mined

commodities were stable and solid

except coking coal, thermal coal, and

nickel.

The prices of coking coal and thermal

coal followed the downtrend as the

global supply tightness has relieved.

In respect to nickel, price was coming

down due to the decision from

Indonesian government to relax a

nickel ore export ban.

Conversely, iron ore and copper prices

were positive supported by China’s

growing demand. As aluminum and

zinc were expected to be deficit, those

prices increased as well.

In addition, speculative factors made

influences on some commodities

including gold.

Meanwhile, inventories of some

commodities increased because

trading activities slowed ahead of

Chinese New Year Holiday. It will be

necessary to monitor the movement of

inventories and prices closely.

2016 2017

Yr Avg Jul Aug Sep Oct Nov Dec Jan

Iron Ore ($/t) 58 57 61 57 59 73 80 81

MoM - 11% 6% -6% 3% 23% 10% 1%

YoY 5% 10% 9% 0% 11% 56% 98% 92%

Coking Coal ($/t) 142 96 114 189 232 300 267 185

MoM - 7% 19% 66% 22% 29% -11% -31%

YoY 58% 11% 35% 131% 191% 299% 245% 141%

Thermal Coal ($/t) 65 63 67 72 92 97 85 84

MoM - 16% 7% 8% 27% 6% -12% -2%

YoY 12% 6% 15% 26% 74% 83% 63% 66%

Copper ($/t) 4,866 4,869 4,767 4,731 4,748 5,414 5,667 5,753

MoM - 5% -2% -1% 0% 14% 5% 2%

YoY -11% -11% -6% -9% -9% 13% 22% 29%

Aluminum ($/t) 1,605 1,629 1,639 1,575 1,666 1,737 1,728 1,791

MoM - 2% 1% -4% 6% 4% -1% 4%

YoY -4% -3% 4% -2% 8% 17% 16% 21%

Nickel ($/t) 9,605 10,263 10,336 10,093 10,260 11,126 10,972 9,971

MoM - 15% 1% -2% 2% 8% -1% -9%

YoY -19% -10% -1% 1% -1% 20% 26% 17%

Zinc ($/t) 2,091 2,183 2,279 2,292 2,312 2,566 2,665 2,715

MoM - 8% 4% 1% 1% 11% 4% 2%

YoY 8% 9% 26% 33% 34% 62% 74% 79%

Gold ($/oz) 1,250 1,339 1,338 1,326 1,266 1,237 1,151 1,194

MoM - 5% 0% -1% -5% -2% -7% 4%

YoY 8% 18% 20% 18% 9% 14% 8% 9%

Source: Bloomberg, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

2016

Chloe Lim

Strategic Research Division (Singapore)

THE BANK OF TOKYO-MITSUBISHI UFJ, LTD.

2. Iron Ore

Mining Monitor | 7 February 2017 5

January marked the fourth

consecutive rise (up 1% MoM) in

average monthly iron ore price which

reached US$81/t.

Prices were supported by sustained

imports by Chinese buyers as iron

ore inventory at China ports

indicated no signs of easing and rose

to record high in the month.

As trading activity slowed ahead of

Chinese New Year holiday, prices

were stable towards end-January at

US$83/t.

In the meantime, iron ore pricing is

expected to be sticky on the back of

speculative trade positions.

6

Iron Ore Prices and Inventories

Prices were supported above US$80/t mark as China’s imports remained robust.

2. Iron Ore

1) Price Trends

Mining Monitor | 7 February 2017

0

40

80

120

160

200

0

50

100

150

200

250

Apr-

10

Jul-1

0

Oct-

10

Jan-1

1

Apr-

11

Jul-1

1

Oct-

11

Jan-1

2

Apr-

12

Jul-1

2

Oct-

12

Jan-1

3

Apr-

13

Jul-1

3

Oct-

13

Jan-1

4

Apr-

14

Jul-1

4

Oct-

14

Jan-1

5

Apr-

15

Jul-1

5

Oct-

15

Jan-1

6

Apr-

16

Jul-1

6

Oct-

16

Jan-1

7

China Iron Ore Port Inventory (RHS) Iron Ore Fines 62%, CFR China Import Spot Price (LHS)

($/t) (Mt)

Source: Bloomberg, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

Fortescue Metals Group (“FMG”) 2Q’FY17 result: steady shipment, lower cost and debt – 30 January, 2017

The fourth largest iron ore exporter’s shipment in 2Q’FY17 was firm at 42 million tons and grew 2% to 86 million tons in 1H’FY17. Despite rising oil

prices, its C1 cash cost continued to trend lower to US$12.54/wet metric ton (“wmt”), down -4% QoQ. Higher realised iron ore prices and reduction in

C1 cash cost were sufficient to allow FMG to report a lower net debt level from US$5 billion to US$4 billion in 1H’FY17.

The company looks set to achieve its full-year FY2017 guidance of 165-170 million tons shipment at C1 cash cost of US$12-13/wmt.

Brockman Mining secured port access for the first stage of its Marillana mine in West Australia – 27 January, 2017

Australia’s junior miner, Brockman Mining secured port access at Port Hedland for the first phase of its Marillana iron ore m ine in Pilbara. Known as

Project Maverick, this first phase development is expected to be a 2.5-3 million ton operation and will pave the way for its Marillana mine with an annual

operational capacity of 20 million tons. Marillana mine has an estimated reserve of 1 billion tons.

Construction is targeted in second quarter this year, and commissioning is slated for the first quarter of 2018.

New Zealand’s private conglomerate Todd Corporation plans new A$5 billion project in Pilbara – 22 January, 2017

Todd Corporation signed a state agreement with Western Australian government and laid out the framework for its proposed Balla Balla infrastructure

project in Pilbara region. The A$5.6 billion (US$4.3 billion) development is expected to include a 160km railway network and a trans-shipping port, with

the entire operation capable of exporting about 50 million tons of iron ore annually. Rail construction is likely to start in 2018.

While BBI Group, a subsidiary of Todd Corporation, owns a magnetite iron ore deposit near the proposed port site located between Karratha and Port

Hedland, it is not feasible to develop at current prices. However, the company is confident it can strike an agreement with ASX-listed Flinders Mines and

other existing miners in the vicinity. Todd Corporation is Flinders’ largest shareholder with a 53% stake.

China posted record iron ore imports in 2016 – 12 January, 2017

According to General Administration of Customs, China imported 89 million tons of iron ore in December, down -3% from November. For the full year,

the country’s imports hit an all-time high, posting 8% growth to 1 billion tons in 2016.

The driving factor for Chinese iron ore import growth in 2016 was due to a -6% YoY decline in domestic production, which reached a six-year low of 1.3

billion tons in 2016, based on National Bureau of Statistics.

Mining Monitor | 7 February 2017 7

2. Iron Ore

2) News Flow

Source: Various sources, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

William Cheung

Strategic Research Division (Hong Kong)

THE BANK OF TOKYO-MITSUBISHI UFJ, H.K.

3. Coal

Mining Monitor | 7 February 2017 8

Global coking coal price continued to

fall in January. The average price for

January was $185/ton, down 30.7%

from the previous month.

The price decrease was because

supply tightness has relieved, after

China’s decision to ease production

restrictions and overturn supply

disruptions last year. Besides, supply

disruptions in Australian mines have

been resolved, putting downward

pressure on the coking coal price.

Global thermal coal price followed

the downtrend of coking coal. The

average price fell to $84/ton in

January, mainly because China

eased restrictions on coal mine

operation. However, the pace of

decline was moderating as the

majority of coal mines in China

stopped production during the Spring

Festival holidays from late January to

early February.

Mining Monitor | 7 February 2017 9

Coal Prices

The coking and thermal coal prices continued to fall after the global supply tightness has relieved.

3. Coal

1) Price Trends

0

50

100

150

200

250

300

350

Apr-

10

Jul-1

0

Oct-

10

Jan-1

1

Apr-

11

Jul-1

1

Oct-

11

Jan-1

2

Apr-

12

Jul-1

2

Oct-

12

Jan-1

3

Apr-

13

Jul-1

3

Oct-

13

Jan-1

4

Apr-

14

Jul-1

4

Oct-

14

Jan-1

5

Apr-

15

Jul-1

5

Oct-

15

Jan-1

6

Apr-

16

Jul-1

6

Oct-

16

Jan-1

7

Spot Price (Coking Coal) Spot Price (Thermal Coal)($/t)

Source: Bloomberg, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

Thermal coal price falls with the shift in Chinese policy – 31 January, 2017

The global spot price for thermal coal continued to fall to around $82t/ton in mid-January 2017, down more than 20% from the recent high in November

last year. The major reason was that China eased restrictions on coal mine operation in September last year. Then, coal output in China began to

recover from November and subsequently put downward pressure on the thermal coal spot price to below $90/ton. On the other hand, price showed

little volatility during the Spring Festival holidays in late January 2017, as the majority of coal mines in China will stop production until the first week of

February. However, the thermal coal price may continue to fall after the Spring Festival holidays when coal mines resumes operation.

China coal industry 2016 profits more than triple on year-on-year – 26 January, 2017

According to the latest data released by the National Bureau of Statistics of China, the sales revenue of coal mining industry in China decreased slightly

by 1.6% year-on-year to $338 billion in 2016, because China’s production cut policy and supply disruption caused by abnormal rainfall have negative

impact on Chinese coal miners’ output. However, profits of the industry rose by 223.6% year-on-year to $15.9 billion for the same period, driven by the

improvement in product margin as a result of coal price rally in the second half of last year. Overall, coal miners and processors (i.e. steel mills and oil

refiners) in China saw remarkable improvement in performance, compared with firms in other industries.

Coal capacity cut will continue in China in 2017 – 24 January, 2017

According to the China National Coal Association, the Chinese government will continue its efforts to remove excess capacity in coal industry this year.

The capacity reduction target in 2017 could be lower than last year’s target of 250 million tons. The major reason is that the government is going to

remove excess capacity at operating coal mines, rather than halted or half-halted mines in 2016. The government could face greater difficulties such as

employee resettlement in carrying out the de-capacity task this year. The national target for cutting coal capacity in 2017 is pending the State Council for

final approval and is set to be announced soon.

Coking coal price still falling – 20 January, 2017

The global spot price for coking coal has decreased by around 23% in the first three weeks of 2017 to $173/ton after the supply tightness has relieved.

This could be largely attributable to China’s decision to ease production restrictions and overturn many supply disruptions that caused the price to rally

in 2016. Besides, most of the supply interruptions that hit Australian mines in mid-2016 have been resolved. Looking ahead, many coking coal

producers in US, Australia and Canada such as Warrior Met Coal, Rosebud Mining, Ramaco, South32, Anglo American and Conuma are planning to

increase production in 2017. Against this backdrop, the global coking coal price is likely to fall to $143/ton, according to the market consensus forecast.

Mining Monitor | 7 February 2017 10

3. Coal

2) News Flow

Source: Various sources, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

Satoshi Kondo

Strategic Research (NY)

MUFG UNION BANK, N.A.

4. Copper

Mining Monitor | 7 February 2017 11

Copper price in January 2017

increased 7.4% m-o-m to $5,930/t,

reversing a downward trend seen

in the last month.

On the demand side, anticipation of

demand growth in US and China

bolstered prices. Particularly in

China, imports of copper

concentrate increased 12.8% y-o-y

in December 2016, indicating

expectation of recovery in copper

demand.

On the supply side, tough labor

negotiations in a Chilean mine and

forecast of shipment delays from

Indonesia created upward

pressures on prices.

Inventories at LME declined while

SHFE warehouses increased

ahead of the Chinese New Year.

Mining Monitor | 7 February 2017 12

Copper Prices and Inventories

Copper prices continued to be higher in January given forecast of growing demand in major consumption countries

and supply concerns of major production countries.

4. Copper

1) Price Trends

0

125

250

375

500

625

750

875

1,000

0

2,000

4,000

6,000

8,000

10,000

12,000

Jan-0

9

Apr-

09

Jul-0

9

Oct-

09

Jan-1

0

Apr-

10

Jul-1

0

Oct-

10

Jan-1

1

Apr-

11

Jul-1

1

Oct-

11

Jan-1

2

Apr-

12

Jul-1

2

Oct-

12

Jan-1

3

Apr-

13

Jul-1

3

Oct-

13

Jan-1

4

Apr-

14

Jul-1

4

Oct-

14

Jan-1

5

Apr-

15

Jul-1

5

Oct-

15

Jan-1

6

Apr-

16

Jul-1

6

Oct-

16

Jan-1

7

LME Inventory (RHS) SHFE Inventory (RHS) LME Spot Price (LHS)

($/t) (Kt)

Source: Bloomberg, MUFG Union Bank, Strategic Research

Labor union votes for strike at Chile’s Escondida copper mine – 1 February, 2017

The labor union representing workers at Escondida, the world’s largest copper mine in Chile (2015 production was nearly 6% of global total) voted in

favor of a strike, after a-month-long talks and rejecting a new wage contract which offered no increase in pay and benefit cuts. The owners could

request government mediation, and the strike could begin around the middle of February. The mine is owned by BHP Billiton (57.5%), Rio Tinto (30%),

and Mitsubishi-JECO (12.5%). BHP Billiton commented that the offer “maintained almost all of the benefits of the current contract, adjusting it to the

current reality of the company, industry and country.” The union stated that “the strength of the vote closes the door to any attempt by the company to

introduce its disastrous plans to lower costs through making the workforce cheaper,” and “it will pave the way for other companies to do the same.”

Labor negotiations at Escondida are regarded as a benchmark for the copper industry. During the last contract negotiations held four years ago, copper

prices were much higher, and the mine workers won the highest ever offered bonus of $49,000 per worker.

Freeport may be temporarily exempt from Indonesian export ban – 31 January, 2017

The Indonesian government said that it may issue a temporary permit which could allow Freeport-McMoRan to resume exports of copper concentrate.

The shipment of the metal has been halted since a new rule took effect on January 12, 2017. As part of its efforts to boost domestic industries,

Indonesia is demanding foreign miners to divest 51% of their stakes to local owners by their 10th year of operation, and requiring Freeport’s local

operation, PT-FI, to change operating terms to allow exports by converting Contract to Work to a special mining license. Under the current contract,

Freeport “is not required to pay export duties on concentrate or to conduct further divestments”. Freeport has rejected Indonesia’s demand since it

would eliminate the “legal and fiscal” certainty” provided by the existing contract, unless it is accompanied by a “stability agreement providing the same

rights and the same level of legal and fiscal certainty provided under its contract of work.”

BHP Billiton downgrades FY2017 copper guidance; Rio Tinto 2016 production below estimates – 31 January, 2017

BHP Billion downwardly revised FY2017 copper guidance by 40,000t, due to disruptions in operations from power outages in Southern Australia at the

Olympic Dam as well as unplanned maintenance of the operation’s refinery n 3Q-4Q’16. The FY guidance for Escondida is unchanged at 1.07mt, which

indicates that the company plans to produce 618,000t of copper during 1H 2017.

Rio Tinto’s copper production increased 4% y-o-y to 523,000t in 2016, but 10% below guidance of 575,000 - 625,000t, due mainly to operational

difficulties at the Grasberg mine and lower-than-expected output from the Kennecott mine. The 2017 copper production guidance is 525,000 - 665,000t.

Growth forecasted for copper production in Chile and Peru in 2017 – 24 January, 2017

According to Cochilco, the state copper commission, copper production in Chile is expected to increase 4.3% y-o-y in 2017 to 5.79mt, after declining

3.9% y-o-y to 5.55mt in 2016, as higher output is expected from the Escondida mine owned by BHP Billiton. Production at some plants at Escondida

was suspended during 2016 for upgrading the facilities. The forecast for 2018 is an increase by 3.4% y-o-y to 6.0mt.

According to the Peruvian government, copper production in Peru is expected to increase 20% y-o-y in 2017 to 2.60 – 2.70mt, surpassing estimated

2016 production of 2.20mt. Copper production in Peru surged 42% reaching a record 2.15mt during the period from January to November in 2016 y-o-

y, attributable primarily to higher output from the Las Bambas copper mine owned by China’s MMG and expansion of Cerro Verde mine by Freeport-

McMoRan.

Mining Monitor | 7 February 2017 13

4. Copper

2) News Flow

Source: Various sources, MUFG Union Bank, Strategic Research

Tom Haddon

Strategic Research Division (London)

THE BANK OF TOKYO-MITSUBISHI UFJ, LTD.

5. Aluminum

Mining Monitor | 7 February 2017 14

Prices performed strongly gaining 7%

by month end to finish at over $1,800.

This was in defiance of fundamentals as

although production data for January is

unknown, LME inventories gained 3%.

This was likely down to continued

strong Chinese output as SHFE stocks

grew even faster, peaking during the

month 25% higher than year end 2016.

Therefore it would appear price gains

are speculation driven, based on the

rumour that the Chinese government is

poised to enforce capacity cut backs.

It is estimated by Metal Bulletin that in

China 7Mtpa of inactive capacity built

up during 2016 and the market has

reacted very positively to possible

lasting removal.

However the price gains partially

reversed during the last week of

January as LME inventories remained

high, showing that fundamentals still

hold influence on price.

Mining Monitor | 7 February 2017 15

Aluminum Prices and Inventories

Prices managed to rally during January despite growing inventories. This appeared to be driven by expectations that

the Chinese government may act to address smelter overcapacity in the country.

5. Aluminum

1) Price Trends

0

2,000

4,000

6,000

8,000

0

1,000

2,000

3,000

4,000

Jan-0

9A

pr-

09

Jul-0

9

Oct-

09

Jan-1

0A

pr-

10

Jul-1

0

Oct-

10

Jan-1

1A

pr-

11

Jul-1

1

Oct-

11

Jan-1

2

Apr-

12

Jul-1

2

Oct-

12

Jan-1

3A

pr-

13

Jul-1

3

Oct-

13

Jan-1

4A

pr-

14

Jul-1

4

Oct-

14

Jan-1

5A

pr-

15

Jul-1

5

Oct-

15

Jan-1

6

Apr-

16

Jul-1

6

Oct-

16

Jan-1

7

LME Inventory (RHS) LME Spot Price (LHS)($/t) (Kt)

Source: Bloomberg, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

China's war on smog not seen as a game-changer for aluminum market – 2 February, 2017

Top aluminum producer China's battle against pollution has raised the prospect of output cuts, causing prices to rise to 20-month highs, but the rally

might have gone too far as oversupply remains a problem. The market excitement was sparked by a Chinese government document proposing that

about a third of aluminum capacity in the provinces of Shandong, Henan, Hebei and Shanxi should be shut over the winter months. However it is

thought that the only time production cuts really happened in China was when the economics of the smelters didn’t work. An example of this came in

November 2015 when prices crashed to 6-1/2 year lows below $1,440 a ton and Chinese smelters cut about 3.6 million tonnes of capacity, according to

analysts.

Rio Tinto's 2016 bauxite, alumina, aluminum output exceed expectations – 17 January, 2017

Rio Tinto produced more bauxite, alumina and aluminum than anticipated in 2016, the group said in a production report. Its bauxite yield came in at 47.7

million mt, above guidance of 47 million mt given last October, and up 9% from 2015. Aluminum production was 10% higher than 2015 at 3.65 million

mt, helped by record annual production at 10 smelters, notably at the revamped Kitimat smelter in Canada, which has produced at nameplate capacity

since April 2016. Rio Tinto Tuesday put its 2017 guidance for bauxite at 48 million-50 million mt, with alumina output anticipated at 8 million-8.2 million

mt and aluminum at 3.5 million-3.7 million mt.

Alcoa revenue tops estimates, sees higher aluminum demand – 15 January, 2017

Alcoa reported higher-than-expected revenue in its first quarterly results after the metals company split into two in November, helped partly by a rise in

alumina prices. The producer of aluminum, alumina and bauxite said it expects a 4 percent growth in global aluminum demand in 2017. Alcoa said it

expects bauxite and alumina markets to be relatively balanced in 2017 and "a modest" global aluminum surplus of 400,000-800,000 metric tons.

Mining Monitor | 7 February 2017 16

5. Aluminum

2) News Flow

Source: The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

Tom Haddon

Strategic Research Division (London)

THE BANK OF TOKYO-MITSUBISHI UFJ, LTD.

6. Nickel

Mining Monitor | 7 February 2017 17

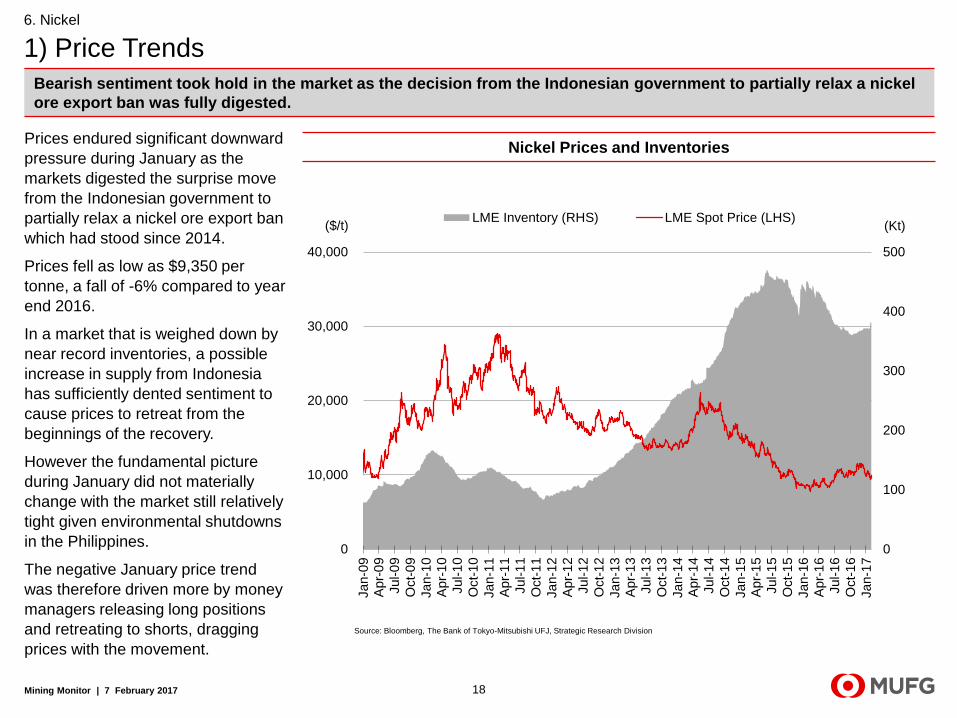

Prices endured significant downward

pressure during January as the

markets digested the surprise move

from the Indonesian government to

partially relax a nickel ore export ban

which had stood since 2014.

Prices fell as low as $9,350 per

tonne, a fall of -6% compared to year

end 2016.

In a market that is weighed down by

near record inventories, a possible

increase in supply from Indonesia

has sufficiently dented sentiment to

cause prices to retreat from the

beginnings of the recovery.

However the fundamental picture

during January did not materially

change with the market still relatively

tight given environmental shutdowns

in the Philippines.

The negative January price trend

was therefore driven more by money

managers releasing long positions

and retreating to shorts, dragging

prices with the movement.

Mining Monitor | 7 February 2017 18

Nickel Prices and Inventories

Bearish sentiment took hold in the market as the decision from the Indonesian government to partially relax a nickel

ore export ban was fully digested.

6. Nickel

1) Price Trends

0

100

200

300

400

500

0

10,000

20,000

30,000

40,000

Jan-0

9A

pr-

09

Jul-0

9

Oct-

09

Jan-1

0A

pr-

10

Jul-1

0

Oct-

10

Jan-1

1A

pr-

11

Jul-1

1

Oct-

11

Jan-1

2

Apr-

12

Jul-1

2

Oct-

12

Jan-1

3A

pr-

13

Jul-1

3

Oct-

13

Jan-1

4A

pr-

14

Jul-1

4

Oct-

14

Jan-1

5A

pr-

15

Jul-1

5

Oct-

15

Jan-1

6

Apr-

16

Jul-1

6

Oct-

16

Jan-1

7

LME Inventory (RHS) LME Spot Price (LHS)($/t) (Kt)

Source: Bloomberg, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

Philippines to shut half of mines, mostly nickel, in environmental clampdown – 3 February, 2017

The Philippines ordered the closure on Thursday of 23 mines, mainly nickel producers that account for about half of output in the world's top nickel ore

supplier, in a government campaign to fight environmental degradation by the industry. News of the mine closures sent global nickel prices higher and

followed the earlier suspension of some operations amid an audit of the country's 41 mines that began shortly after outspoken President Rodrigo

Duterte took office last June. Lopez said the nickel mines ordered to shut account for about 50 percent of the country's annual output, which analysts

estimate at about 10 percent of world supply.

Global Stainless Steel production set for new high in 2017 – 2 February, 2017

Annual global crude stainless steel production for 2016 is estimated to have totalled an all-time high of around 45.5 million tons, which represents a

year-on-year increase of 9.5 percent. MEPS (a market analytics agency) forecasts a further rise in worldwide out-turn of around 4 percent, in 2017, to a

new peak of 47.3 million tons. Recently-issued, official Chinese output figures were significantly higher than earlier expectations, despite reports of plant

closures. In Japan and South Korea, last year’s production is estimated to have fallen slightly below the 2015 totals. Moderate increases are forecast,

for both countries, in 2017. Output in the European Union, in 2016, was approximately 2 percent more than the year earlier figure. A further, marginal

expansion is expected, this year.

Nickel price picked as 2017 winner – 31 January, 2017

Nickel rallied to more than $11,700 by mid-November only to fall back nearly 20% to trade at a six-month low in January. However in a new report

Capital Economics, a London-based independent research house, believes of all industrial metals, the nickel price has the best prospects to improve

adding that "the market is tightening [following years of underinvestment in new mines] and it is still too soon to say what the partial lifting of Indonesia’s

ban on ore exports will mean for supply. Capital Economics sees the price of nickel climbing to $11,500 per tonne by the end of the year (that's a 20%

jump from today's price), with further upside predicted in 2018. That makes nickel the metal Capital Economics is by far the most bullish about.

Mining Monitor | 7 February 2017 19

6. Nickel

2) News Flow

Source: The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

7. Zinc

Mining Monitor | 7 February 2017 20

Tom Haddon

Strategic Research Division (London)

THE BANK OF TOKYO-MITSUBISHI UFJ, LTD.

Zinc prices enjoyed a fantastic month

finishing 14% higher than year end

2016, hitting $2,852 – close to push

through the multiyear high of $2,886

seen in November.

The price rise is driven by the

continued perception of tightening

underlying fundamentals – which is

backed up by LME inventories

dipping below 400kt for only the

second time since 2009.

Bullish price sentiment was also

buoyed by trade statistics showing

that China’s zinc concentrate imports

were down 13% year on year in

December due to lack of availability

rather than decreasing demand as

galvanized steel production was

stable.

However in China, SHFE stocks

marginally increased during January,

providing early indications that

domestic supply may be responding

to the price environment, although it

will take a few more months of stable

or increasing inventories to be sure.

Mining Monitor | 7 February 2017 21

Zinc Prices and Inventories

With the market still in deficit due to mine closures in 2016, the underlying fundamentals have led to bullish

sentiment driving prices close to multiyear highs.

7. Zinc

1) Price Trends

0

500

1,000

1,500

2,000

0

1,000

2,000

3,000

4,000

Jan-0

9A

pr-

09

Jul-0

9

Oct-

09

Jan-1

0A

pr-

10

Jul-1

0

Oct-

10

Jan-1

1A

pr-

11

Jul-1

1

Oct-

11

Jan-1

2

Apr-

12

Jul-1

2

Oct-

12

Jan-1

3A

pr-

13

Jul-1

3

Oct-

13

Jan-1

4A

pr-

14

Jul-1

4

Oct-

14

Jan-1

5A

pr-

15

Jul-1

5

Oct-

15

Jan-1

6

Apr-

16

Jul-1

6

Oct-

16

Jan-1

7

LME Inventory (RHS) LME Spot Price (LHS)($/t) (Kt)

Source: Bloomberg, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

Glencore sticks with 2017 production targets – 2 February, 2017

Glencore stuck with its target for broadly higher output in 2017 after reporting falls in copper and zinc which led overall production lower last year. Zinc

prices rallied 60 percent last year, making them the best performing metal on the London Metals Exchange in 2016, helped partly by Glencore's

production cuts. The company has said capacity for zinc will stay shut until market conditions allow for extra supply without pushing down prices.

MMK ships record volume of galvanized steel – 1 February, 2017

OJSC Magnitogorsk Iron and Steel Works ("MMK“) shipped 1,135,500 tonnes of galvanized steel to its consumers in 2016, the most in the Company’s

history. The previous record of 1,115,700 tonnes was achieved in 2014. During the past 15 years, MMK has sustainably grown its galvanized steel

output. Currently, another continuous hot-dip galvanizing line with annual capacity of 360,000 tonnes is under construction at sheet-rolling shop 11, with

launch scheduled for July 2017.

Global refined zinc market ends in deficit during Jan-Nov ‘16 – 17 January, 2017

The latest statistics published by the International Lead and Zinc Study Group (ILZSG) indicates that global refined zinc market was in deficit of 263,000

tons during the initial eleven-month period of 2016. The total reported zinc inventories declined by 72,000 tons during this period. The zinc mine output

declined considerably in major producing countries including Australia, India, Ireland and Peru. Overall, the zinc mine output declined by 1.2% during

the initial eleven-month period in 2016 when compared with the corresponding period last year. This is despite sharp increase in mine output by China.

The global demand for refined zinc metal increased modestly to 12.795 million tons during January to November last year, as compared with 12.358

million tons during the same period last year.

Mining Monitor | 7 February 2017 22

7. Zinc

2) News Flow

Source: The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

Satoshi Kondo

Strategic Research (NY)

MUFG UNION BANK, N.A.

8. Gold

Mining Monitor | 7 February 2017 23

Mining Monitor | 7 February 2017 24

Gold Prices, ETF Holdings, and 10Yr US TIPS Yield

After the sell-off related to Mr. Trump election in November, gold price turned positive on uncertainties over the

policies of the new US administration.

8. Gold

1) Price Trends

After the sell-off due to concern of

higher US inflation and stronger USD,

all which related to the unexpected

Mr. Trump election in November, gold

prices turned higher in January, up

5.5% in the month.

Factors behind the price gain are

reversal of factors which have been

pressuring gold prices downward. In

other words, lower stock prices and

weaker dollar on the back of

uncertainties over the policies of the

new US administration, which in turn

made risk-averse investors to

purchase gold, a safe-haven asset.

Money manager net length at the

COMEX which have been

plummeting over the trailing three-

month period, turned positive in

January 2017. Gold ETF holdings

were relatively lower (-0.5% m-o-m).

600

900

1,200

1,500

1,800

2,100

2,400

2,700

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Jan-0

9A

pr-

09

Jul-0

9O

ct-

09

Jan-1

0A

pr-

10

Jul-1

0O

ct-

10

Jan-1

1A

pr-

11

Jul-1

1

Oct-

11

Jan-1

2A

pr-

12

Jul-1

2O

ct-

12

Jan-1

3A

pr-

13

Jul-1

3O

ct-

13

Jan-1

4A

pr-

14

Jul-1

4O

ct-

14

Jan-1

5A

pr-

15

Jul-1

5

Oct-

15

Jan-1

6A

pr-

16

Jul-1

6O

ct-

16

Jan-1

7

(t) ETF Holdings (RHS) Gold Price (LHS)($/oz)

Source: World Gold Council, GFMS, Bloomberg, MUFG Union Bank, Strategic Research

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

10Yr US TIPS Yield (%)

Mining Monitor | 7 February 2017 25

8. Gold

2) News Flow

Egypt opened international tender offer for gold exploration rights – 24 January, 2017

Egypt started accepting bids for its first gold exploration rights since 2009 on January 15, 2017. The offer covers five concession areas and remains

open until April 20, 2017. Currently the country has one commercial gold mine, Sukari, operated by Centamin, with production of 551,036 ounces in

2016. The terms of the tender offer include a 6% royalty payment, partial cost-recovery before the beginning of production-sharing, and three bonus

payments to EMRA, Egypt’s mining agency, including one of at least $1 million. Companies will also be required to share at least 50% of any gold

revenues with the government. Miners commented that the international norm for a royalty and tax regime is for the government to take a small royalty

fee from production revenues, a model which has created booming industries in countries such as Chile and Ethiopia. Egypt’s three main foreign miners

(Centamin, Aton Resources, and Thani Stratex Resources) are not planning to bid on current terms, but EMRA expects a “beyond excellent” turnout.

Strike ends at Yamana’s Chilean mine – 18 January, 2017

Workers at Chile’s El Peñon mine and its owner, Canada’s Yamana Gold, have reached a wage agreement, ending a strike which began on January 7,

2017. The mine is the company’s second largest gold mine by output, producing 164,445 ounces during January – September 2016 (approximately 17%

of company’s total production). The company stated that the interruption has not created a “significant impact” on mine and consolidated production and

expects to recover production from its other operations in the near term and from El Peñon throughout 2017.

Goldcorp announced its growth plan to increase production – 17 January, 2017

Goldcorp, a Canadian gold miner, shared a growth plan to increase production by 20% to approximately 3 million ounces over the coming five years.

The growth is planned to be achieved by boosting capacity at its Cerro Negro mine (Argentina) and the Eleonore mine (Canada). The company

forecasts its gold reserves to increase 20% to 50 million ounces during the same period from existing resources at Century project (Ontario),

Peñasquito mine (Mexico), and Pueblo Viejo mine (Dominican Republic). The Goldcorp Chief Executive David Garofalo commented that world’s major

gold miners should partner to share the risks (e.g., financials) of developing large gold deposits, and “what we are looking to do on the M&A side is find

more of those large resources that are undeveloped right now and do so in partnership with some of our senior peer companies.”

Source: Various sources, MUFG Union Bank, Strategic Research

Mining Monitor | 7 February 2017 26

Appendix : Mined Commodities Price Forecasts by Strategic Research Division as of 27 January 2017

Yr Avg 1Q (f) 2Q (f) 3Q (f) 4Q (f) 1H (f) 2H (f) 1H (f) 2H (f)

Iron Ore ($/t) 58 77 72 66 63 60 55 56 52

YoY 5% 60% 29% 12% -11% -20% -14% -6% -5%

QoQ - 9% -6% -9% -4% - - - -

Coking Coal ($/t) 142 179 158 140 128 117 112 107 103

YoY 58% 65% 75% 66% 65% -30% -17% -9% -8%

QoQ - 131% -12% -11% -9% - - - -

Thermal Coal ($/t) 65 81 73 68 66 65 65 64 64

YoY 12% 29% 25% 17% 25% -15% -3% -1% -1%

QoQ - 53% -10% -6% -3% - - - -

Copper ($/t) 4,866 5,119 4,763 4,668 4,617 4,617 4,726 4,904 5,132

YoY -11% 9% 1% -2% -13% -7% 2% 6% 9%

QoQ - -3% -7% -2% -1% - - - -

Aluminum ($/t) 1,605 1,654 1,603 1,584 1,576 1,595 1,644 1,724 1,798

YoY -4% 9% 1% -2% -8% -2% 4% 8% 9%

QoQ - -3% -3% -1% -1% - - - -

Nickel ($/t) 9,605 10,103 9,901 9,852 10,050 10,565 11,101 11,637 11,990

YoY -19% 18% 12% -4% -7% 6% 12% 10% 8%

QoQ - -6% -2% -1% 2% - - - -

Zinc ($/t) 2,091 2,665 2,718 2,746 2,691 2,651 2,611 2,540 2,465

YoY 8% 59% 41% 22% 7% -2% -4% -4% -6%

QoQ - 6% 2% 1% -2% - - - -

Gold ($/oz) 1,250 1,153 1,159 1,168 1,181 1,205 1,223 1,238 1,249

YoY 8% -3% -8% -12% -3% 4% 4% 3% 2%

QoQ - -5% 1% 1% 1% - - - -Source: Bloomberg, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division, MUFG Union Bank, Strategic Research

2016 2017 2018 2019

Disclaimer

Mining Monitor | 7 February 2017 27

This report is intended only for information purposes and is not intended to constitute an offer or solicitation to buy or sell securities or any

other products. Contents of the report are information as at publish date and are subject to change without notice. This report has not been

prepared to provide legal, taxational, financial, market-judgmental, or any other advises on propriety of any transactions. In taking any

action, each reader is requested to act on the basis of his or her own judgment upon consulting certified lawyers, accountants or other

professionals regarding the accuracy, validity and reliability of information appeared in this report.

Bank of Tokyo-Mitsubishi UFJ is regulated by the Financial Services Authority.

No part of this publication may be reproduced, stored in a retrieval system or transmitted without the prior written permission of The Bank

of Tokyo-Mitsubishi UFJ Limited.

Copyright© 2017 The Bank of Tokyo-Mitsubishi UFJ, Ltd. All rights reserved.

Publisher:The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division (Corporate Research Office)

2-7-1, Marunouchi, Chiyoda-ku, Tokyo 100-8388, Japan

Contact details for inquiries : Kouichi Akimoto

(TEL:03-3240-5386、e-mail:[email protected])