migration and remittances during the global financial...

TRANSCRIPT

Migration and Remittances during the Global Financial Crisis and Beyond

Ibrahim Sirkeci

Jeffrey H. Cohen

Dilip Ratha

Editors

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Migration and Remittances during the Global Financial Crisis and Beyond

Migration and Remittances during the Global Financial Crisis and Beyond

Edited by

Ibrahim Sirkeci

Jeffrey H. Cohen

Dilip Ratha

Washington, D.C.

© 2012 International Bank for Reconstruction and Development / International Development

Association or Th e World Bank

1818 H Street NW

Washington DC 20433

Telephone: 202-473-1000

Internet: www.worldbank.org

1 2 3 4 15 14 13 12

Th is volume is a product of the staff of Th e World Bank with external contributions. Th e

fi ndings, interpretations, and conclusions expressed in this volume do not necessarily refl ect the

views of Th e World Bank, its Board of Executive Directors, or the governments they represent.

Th e World Bank does not guarantee the accuracy of the data included in this work.

Th e boundaries, colors, denominations, and other information shown on any map in this work

do not imply any judgment on the part of Th e World Bank concerning the legal status of any

territory or the endorsement or acceptance of such boundaries.

Rights and Permissions

Th e material in this work is subject to copyright. Because Th e World Bank encourages

dissemination of its knowledge, this work may be reproduced, in whole or in part, for

noncommercial purposes as long as full attribution to the work is given.

For permission to reproduce any part of this work for commercial purposes, please

send a request with complete information to the Copyright Clearance Center Inc., 222

Rosewood Drive, Danvers, MA 01923, USA; telephone: 978-750-8400; fax: 978-750-4470;

Internet: www.copyright.com.

All other queries on rights and licenses, including subsidiary rights, should be

addressed to the Offi ce of the Publisher, Th e World Bank, 1818 H Street NW, Washington, DC

20433, USA; fax: 202-522-2422; e-mail: [email protected].

ISBN (paper): 978-0-8213-8826-6

ISBN (electronic): 978-0-8213-8827-3

DOI: 10.1596/978-0-8213-8826-6

Library of Congress Cataloging-in-Publication Data

Migration and remittances during the global fi nancial crisis and beyond / edited by Ibrahim

Sirkeci, Jeff rey H. Cohen and Dilip Ratha.

p. cm.

Includes bibliographical references and index.

ISBN 978-0-8213-8826-6 — ISBN 978-0-8213-8827-3 (electronic)

1. Emigration and immigration—Economic aspects. 2. Global Financial Crisis, 2008-2009.

3. Immigrants—Economic aspects. 4. Emigrant remittances—Cross-cultural studies. I. Sirkeci,

Ibrahim. II. Cohen, Jeff rey H. (Jeff rey Harris) III. Ratha, Dilip.

JV6217.M545 2011

332’.04246090511—dc23

2011032374

Cover image: Diana Ong/Superstock by Getty Images

Cover design: Critical Stages

v

Contents

Foreword ............................................................................................................................xvOtaviano Canuto and Hans Timmer

Acknowledgments ........................................................................................................... xvii

Contributors ......................................................................................................................xix

Abbreviations ................................................................................................................. xxvii

Introduction: Remittance Flows and Practices during the Crisis ...................................... 1Ibrahim Sirkeci, Jeff rey H. Cohen, and Dilip Ratha

PART I

Chapter 1. Theoretical Appraisal: Understanding Remittances ...................................... 15Jeff rey H. Cohen and Ibrahim Sirkeci

Chapter 2. Forecasting Migrant Remittances during the Global Financial Crisis ........... 23Sanket Mohapatra and Dilip Ratha

Chapter 3. Economic Crises and Migration: Learning from the Past and the Present ... 35Tim Green and L. Alan Winters

Chapter 4. Remittance Flow, Working Capital Formation, and Economic Growth ........ 53Gabriela Mundaca

PART II

Chapter 5. The Financial Crisis in the Gulf and Its Impact on South Asian Migration and Remittances .......................................................................... 67

S. Irudaya Rajan and D. Narayana

Chapter 6. Gendered Use of Remittances: The United Arab Emirates–Bangladesh Remittance Corridor ......................................................................................................... 81

Md Mizanur Rahman and Danièle Bélanger

Chapter 7 Trends and Correlates of Remittances to India ............................................. 93Poonam Gupta and Karan Singh

vi l CONTENTS

Chapter 8. Shocks Affecting the Flow and Stability of Workers’ Remittances to India ....................................................................................................... 107

Bhupal Singh

Chapter 9. Migrant Remittances in Nepal: Impact of Global Financial Crisis andPolicy Options ................................................................................................................ 121

Sanket Mohapatra, Dilip Ratha, and Ani Silwal

Chapter 10. Nepal: Migration History and Trends ........................................................ 137Jeevan Raj Sharma

Chapter 11. Resilience of Remittances during the Global Financial Crisis and the Entrenchment of Migration ............................................................................................ 141

Andrea Riester

Chapter 12. Rural-Urban Migration in the Context of Thailand’s Ongoing Uneven Development ................................................................................................................. 149

Gregory S. Gullette

Chapter 13. Migration and Remittances in Bangladesh and Pakistan: Evidence from Two Host Countries ............................................................................... 153

Guntur Sugiyarto, Carlos Vargas-Silva, and Shikha Jha

Chapter 14. Impacts of the Crisis on Migrants and Their Families: A Case Study from Bangladesh ...................................................................................... 171

Guntur Sugiyarto, Selim Raihan, Carlos Vargas-Silva, and Shikha Jha

PART III

Chapter 15. The Impact of the Financial Crisis on Remittance Flows: The Case of El Salvador .................................................................................................. 183

Pablo Acosta, Javier Baez, Rodolfo Beazley, and Edmundo Murrugarra

Chapter 16. Remittance Flows to Mexico and Employment and Total Earnings of Mexican Immigrant Workers in the United States ......................................................... 193

Jesús A. Cervantes González and Alejandro Barajas del Pino

PART IV

Chapter 17. The Impact of the Global Economic Downturn on Remittances from the European Union ............................................................................................... 215

Oscar Gómez Lacalle

Chapter 18. Remittances and Evolving Migration Flows from Central and Eastern Europe to the United Kingdom ......................................................................... 227

Simon Pemberton and Lisa Scullion

Chapter 19. Effects of the Global Crisis on Migration and Remittances in Albania .... 237Ilir Gedeshi and Nicolaas de Zwager

Chapter 20. The Impact of the Global Financial Crisis on Migration to and Remittance Flows from Spain ......................................................................................... 255

Marta Roig and Joaquín Recaño-Valverde

PART V

Chapter 21. Forecasting Turkish Workers’ Remittances from Germany during the Financial Crisis .............................................................................................. 273

Şule Akkoyunlu

CONTENTS l vii

Chapter 22. Remittances in an Environment of Human Insecurity: The Kurdish Case ............................................................................................................ 289

Ibrahim Sirkeci

Chapter 23. Financial Crisis and Remittances from Denmark to Turkey ....................... 295Pinar Yazgan and Ibrahim Sirkeci

Chapter 24. Work and Remittance Patterns of Irregular Immigrants in Turkey ............ 303Oğuzhan Ömer Demir and M. Alper Sozer

PART VI

Chapter 25. Labor Migration, Overseas Remittances, and Local Outcomes in the Contemporary Philippines .............................................................................................. 315

Ty Matejowsky

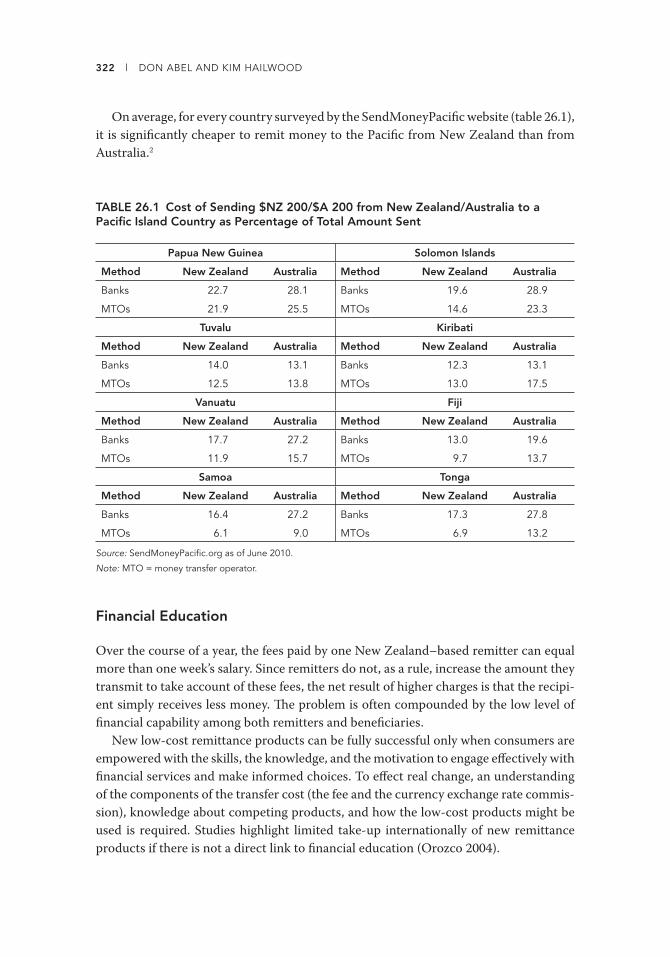

Chapter 26. The New Zealand–Pacifi c Remittance Corridor: Lowering Remittance Costs ............................................................................................ 319

Don Abel and Kim Hailwood

Chapter 27. Role of Trade Openness, Remittances, Capital Infl ows, and Financial Development in Vanuatu ................................................................................................ 325

Ronald R. Kumar

PART VII

Chapter 28. Remittances to Sub-Saharan Africa in the Wake of a Financial Crisis: Source of Resilience or Vulnerability? ............................................................................. 337

Wim Naudé and Henri Bezuidenhout

Chapter 29. From Shock Absorber to Shock Transmitter: Determinants of Remittances in Sub-Saharan Africa...................................................... 349

Raju Jan Singh

Chapter 30. A Comparative Examination of Women’s Remittance Practices in Two Somali Communities: Johannesburg, South Africa, and Columbus, Ohio ............. 359

Marnie Shaff er

PART VIII

Chapter 31. The Global Crisis and Expatriates’ Remittances to Lebanon .................... 365Nassib Ghobril

Chapter 32. Migrant Transfers in the MENA Region: A Two-Way Street in Which Traffi c Is Changing .......................................................................................................... 377

George Naufal and Carlos Vargas-Silva

Bibliography .................................................................................................................... 387

Index ............................................................................................................................... 421

FiguresI.1 Resilience of Remittances Compared to Other Financial Flows to Developing

Countries .........................................................................................................................................2

3.1 Real GDP per Capita with and without the Current Crisis, 1980–2013 ..........................37

3.2 Population of Ireland during the Nineteenth Century ........................................................38

viii l CONTENTS

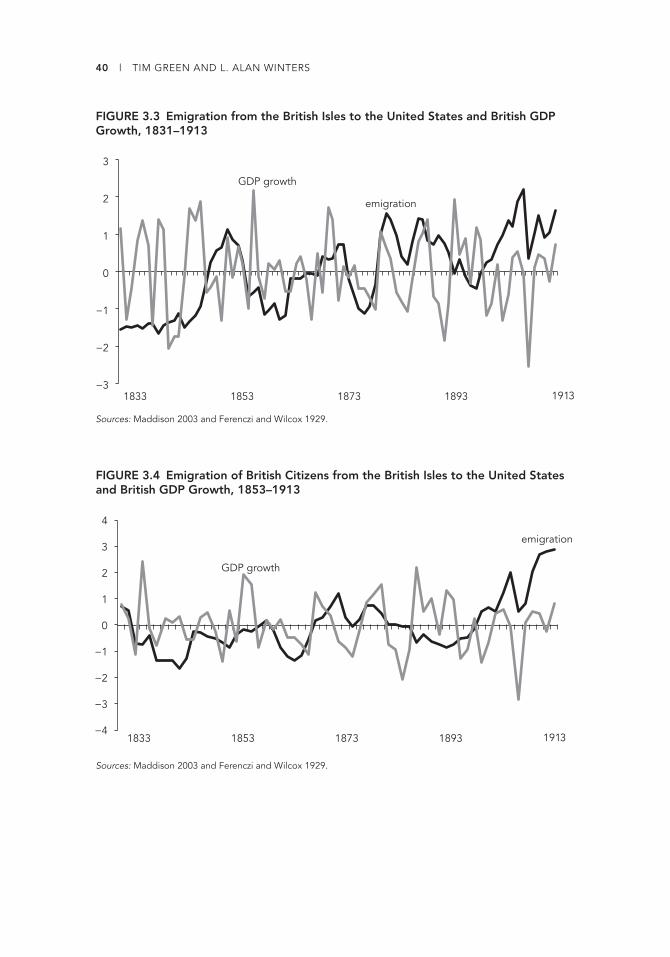

3.3 Emigration from the British Isles to the United States and British GDP Growth,

1831–1913 .....................................................................................................................................40

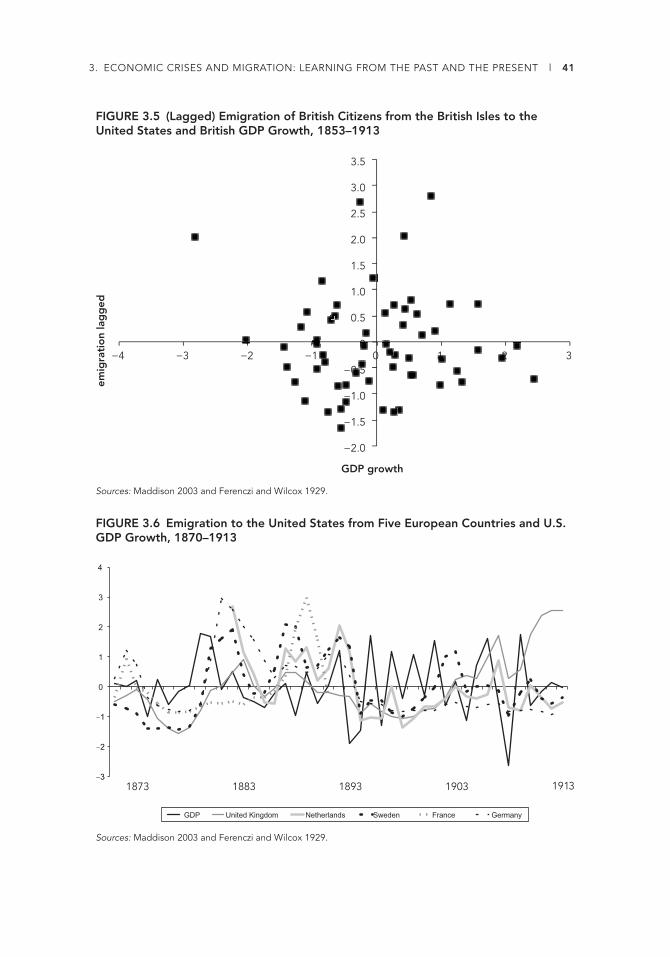

3.4 Emigration of British Citizens from the British Isles to the United States and

British GDP Growth, 1853–1913 .............................................................................................40

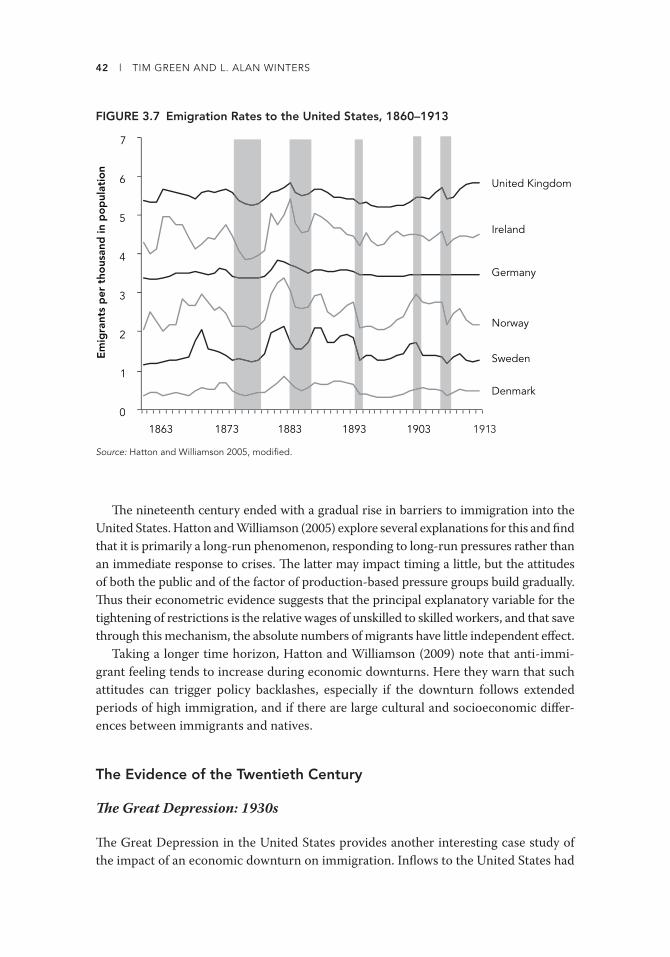

3.5 (Lagged) Emigration of British Citizens from the British Isles to the United States

and British GDP Growth, 1853–1913 .....................................................................................41

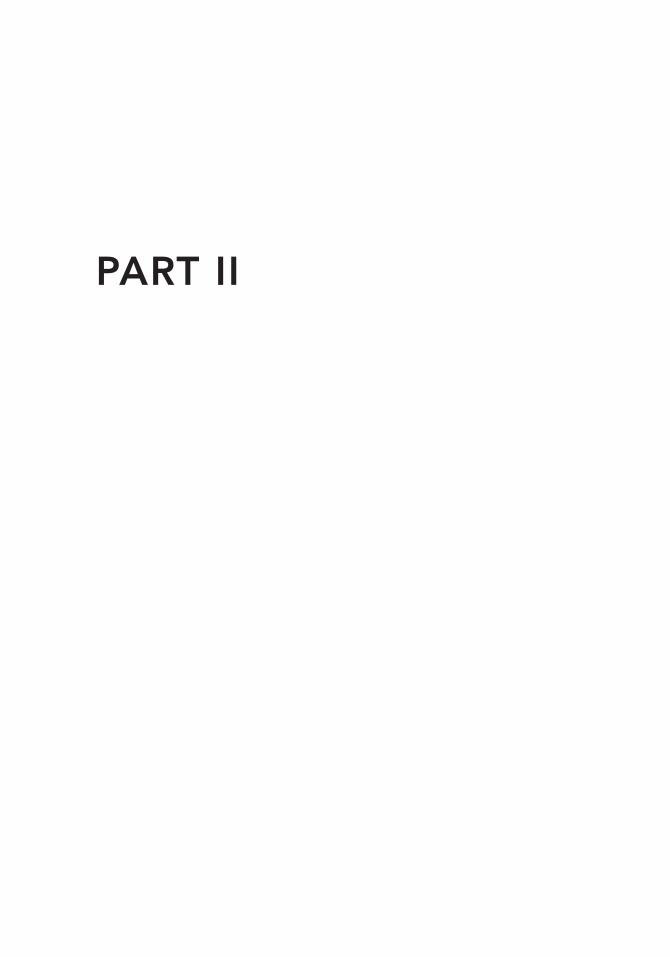

3.6 Emigration to the United States from Five European Countries and U.S. GDP

Growth, 1870–1913 ....................................................................................................................41

3.7 Emigration Rates to the United States, 1860–1913 ..............................................................42

3.8 GDP Growth, Th en and Now ....................................................................................................46

3.9 Change in Unemployment Rates for Native- and Foreign-Born Workers, Selected

OECD Countries, Th ird Quarter 2008 to Th ird Quarter 2009 .........................................51

6.1 Bangladeshi Labor Migration to the United Arab Emirates, 1976–2010 .........................84

6.2 Infl ows of Remittances from the United Arab Emirates to Bangladesh, 1998–2011 ....84

7.1 Remittances to India ...................................................................................................................94

7.2 Current Account Infl ows, 1991–2009 .....................................................................................95

7.3 Net Remittances versus Net Capital Infl ows, 1991–2009 ...................................................96

8.1 Structure of Workers’ Remittances to India, 1975–2010 ................................................. 108

8.2 Impulse Response of Workers’ Remittances to Various Shocks in Model 1 ................ 115

8.3 Impulse Response of Workers’ Remittances to Various Shocks in Model 2 ................ 116

8.4 Annual Growth Rate in Workers’ Remittance Infl ows to India, 1992–2010 ................ 117

9.1 Primary Destinations of Nepalese Migrants, Excluding India,

1999–2000 to 2009–10 ........................................................................................................... 123

9.2 Growth in Remittances and Other Sources of External Finance Sent to Nepal,

1996–2010 .................................................................................................................................. 125

9.3 Remittances to Nepal during the Crisis, April 2007–October 2010 .............................. 127

9.4 Growth in Mobile Phone Subscriptions in Nepal, 2003–08 ............................................ 131

13.1 Remittances to Bangladesh ..................................................................................................... 156

13.2 Remittances to Pakistan .......................................................................................................... 156

13.3 Remittances from the United Kingdom to Bangladesh .................................................... 159

13.4 Remittances from the United States to Bangladesh .......................................................... 159

13.5 Labor Force Participation Rate of Asians in the United States ....................................... 161

13.6 Unemployment Rate of Asians in the United States ......................................................... 161

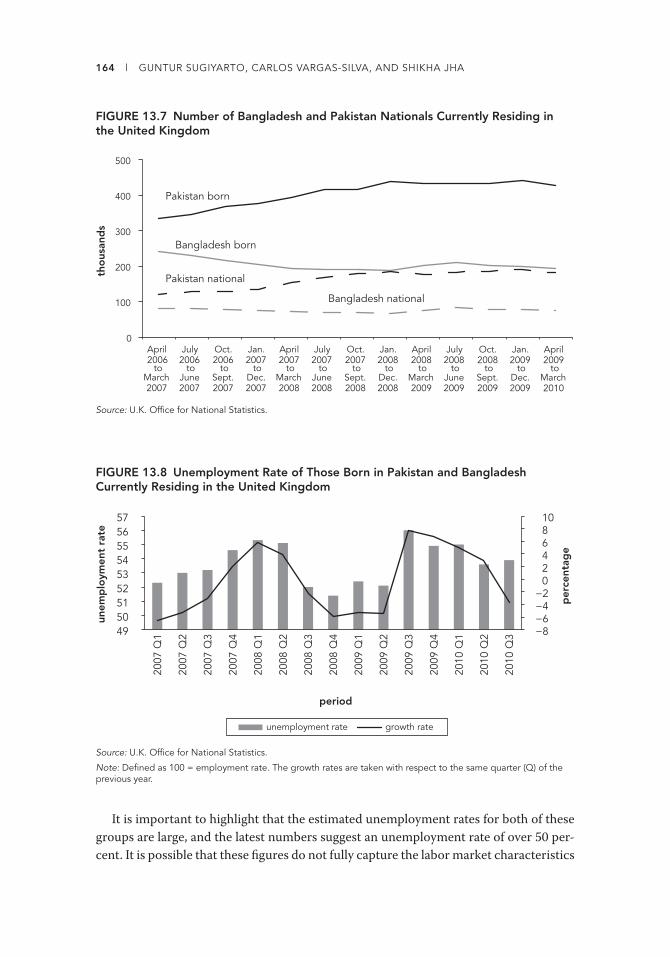

13.7 Number of Bangladesh and Pakistan Nationals Currently Residing in the

United Kingdom ....................................................................................................................... 164

13.8 Unemployment Rate of Th ose Born in Pakistan and Bangladesh Currently

Residing in the United Kingdom ........................................................................................... 164

13.9 Unemployment Rate of Nationals of Pakistan and Bangladesh Currently

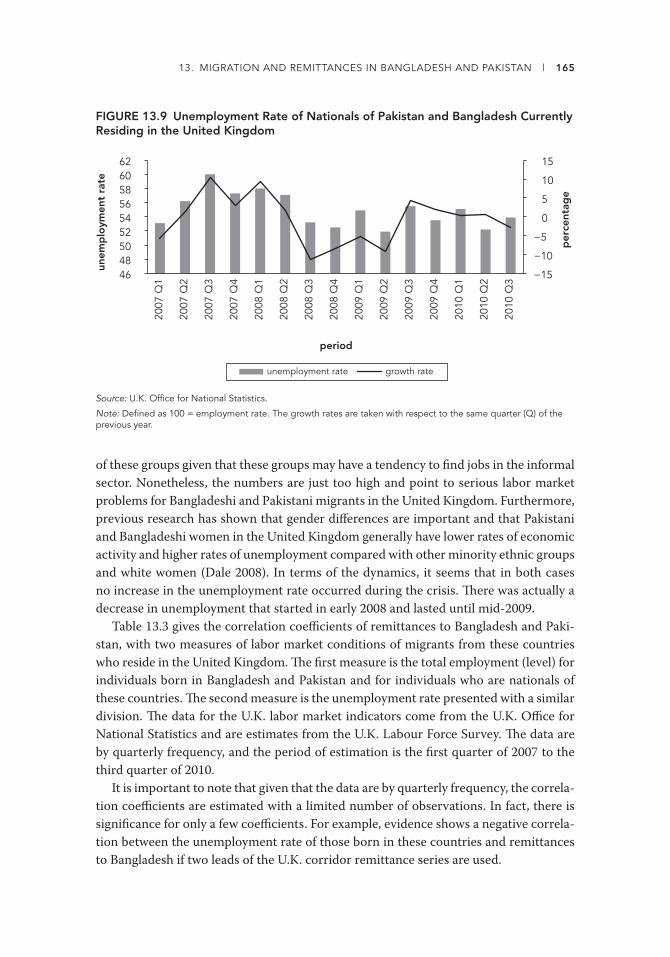

Residing in the United Kingdom ........................................................................................... 165

13.10 U.S. Dollar and U.K. Pound Exchange Rate with Respect to Bangladeshi Taka .......... 168

13.11 U.S. Dollar and U.K. Pound Exchange Rate with Respect to Pakistani Rupee ............. 168

14.1 Knowledge about the Global Financial Crisis .................................................................... 173

14.2 Expected Period of Impact of Global Financial Crisis According to Households

Reporting Relatively or Very Good Knowledge ................................................................. 173

CONTENTS l ix

14.3 Average Number of Family Members Working Abroad before and during the

FInancial Crisis ......................................................................................................................... 174

14.4 Change in Household Income between 2008 and 2009.................................................... 177

15.1 El Salvador: Main Macroeconomic Indicators ................................................................... 184

15.2 Growth in Remittances to El Salvador in Comparison to Growth in U.S. GDP and

Unemployment ......................................................................................................................... 187

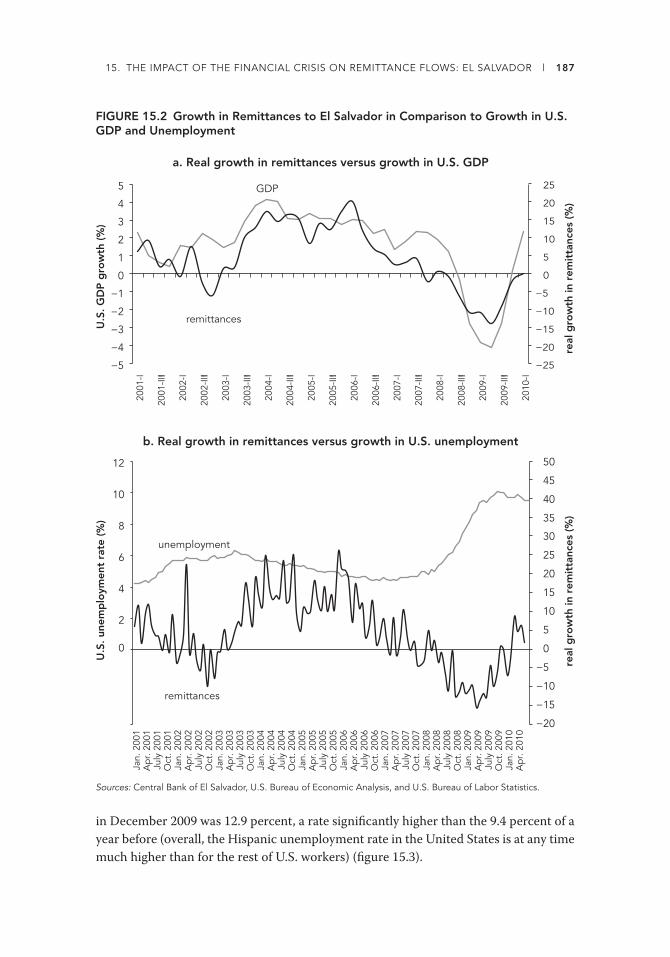

15.3 U.S. Unemployment Rates for Total Population and for Hispanics, 2005–10 ............. 188

15.4 Annual Growth in Remittance Infl ows to El Salvador by Region ................................... 189

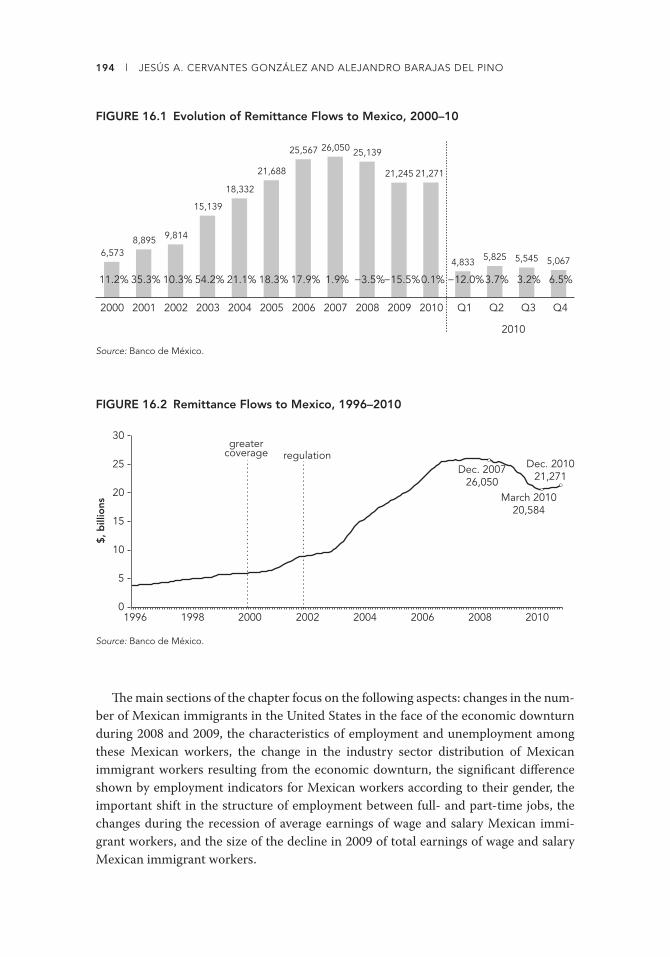

16.1 Evolution of Remittance Flows to Mexico, 2000–10 ......................................................... 194

16.2 Remittance Flows to Mexico, 1996–2010 ............................................................................ 194

16.3 Mexican Immigrants in the United States, 2009 ................................................................ 196

16.4 Unemployment Rate of Mexican Immigrants, Native Population, and

Total Population in the United States ................................................................................... 205

16.5 Annual Percentage Variations of Wage and Salary Mexican Immigrant

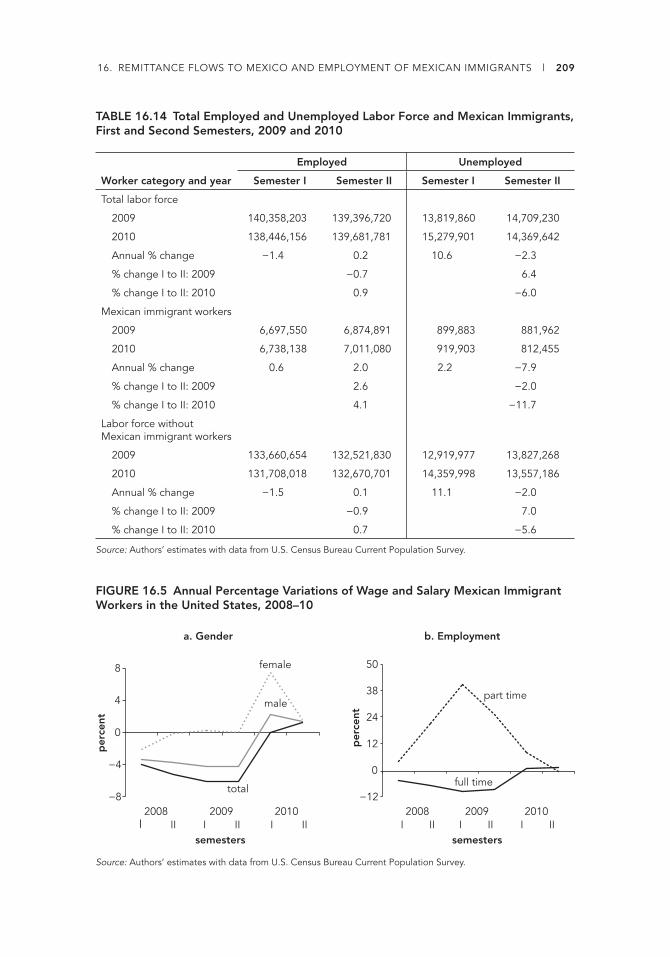

Workers in the United States, 2008–10 ............................................................................... 209

16.6 Proportion of Part-Time Employed among Wage and Salary Mexican

Immigrant Workers, 2007–10 ................................................................................................ 210

16.7 Number of Wage and Salary Mexican Immigrant Workers in the

United States and Th eir Annual Total Earnings, 2007–10 ............................................... 210

17.1 EU Remittances by Destination, 2004–09 ........................................................................... 217

17.2 Workers’ Remittances by Destination, 2004–09 ................................................................ 218

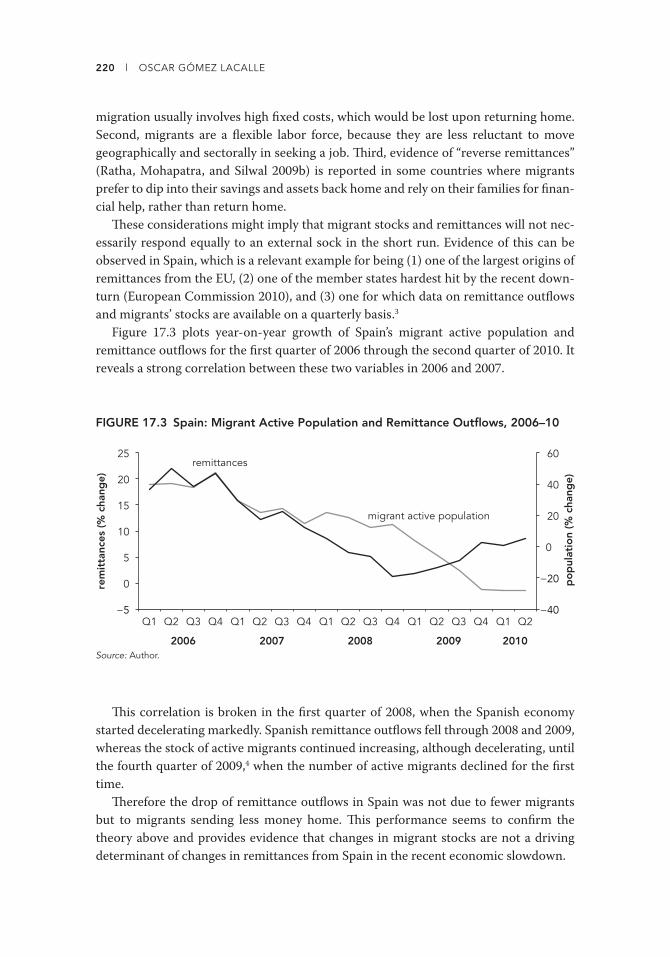

17.3 Spain: Migrant Active Population and Remittance Outfl ows, 2006–10 ....................... 220

17.4 EU: Total Growth in Employment and Remittance Outfl ows, 2006–10 ...................... 221

17.5 Total Employment and Remittance Outfl ows in the European Union, 2004–12 ........ 222

19.1 Employment Sectors of Albanian Migrants in Host Countries, 2009–10 .................... 240

19.2 GDP Growth and Unemployment Rates in Greece and Italy, 1998–2012 .................... 241

19.3 Impact of Economic Crisis on Albanian Households in Migration in 2009 ................ 241

19.4 Months of Unemployment for Albanian Migrants in Greece and Italy, 2009.............. 243

19.5 Rate of Unemployment of Albanian Migrants in Italy and Greece, by Sector,

2009–10 ...................................................................................................................................... 244

19.6 Unemployment Benefi t–Receiving Migrants in Main Host Countries by Gender,

2009–10 ...................................................................................................................................... 244

19.7 Projected Time to Return Home of Respondents Who Are Considering

Th is Option, 2009–10 .............................................................................................................. 252

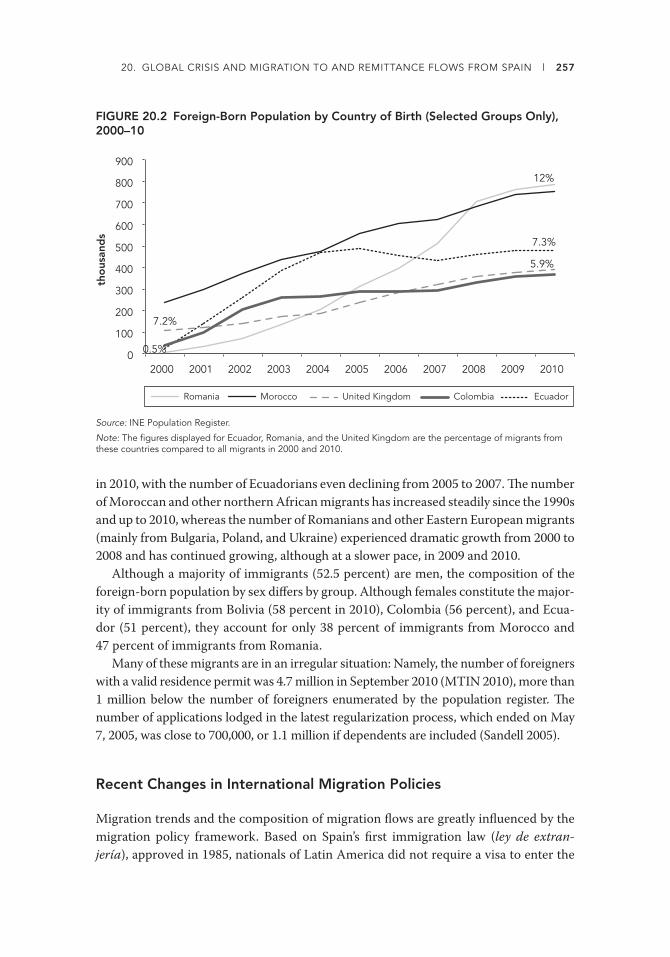

20.1 Infl ow of Foreign-Born Persons by Country of Birth, 2004–09 ...................................... 256

20.2 Foreign-Born Population by Country of Birth (Selected Groups Only), 2000–10 ...... 257

20.3 Outfl ows of Remittances per Quarter, Total and per Foreign-Born Person,

2000–10 ...................................................................................................................................... 259

20.4 Outfl ows of Remittances by Country of Destination, 2004–09 ...................................... 260

20.5 Unemployment by Nationality, 2001–10 ............................................................................. 263

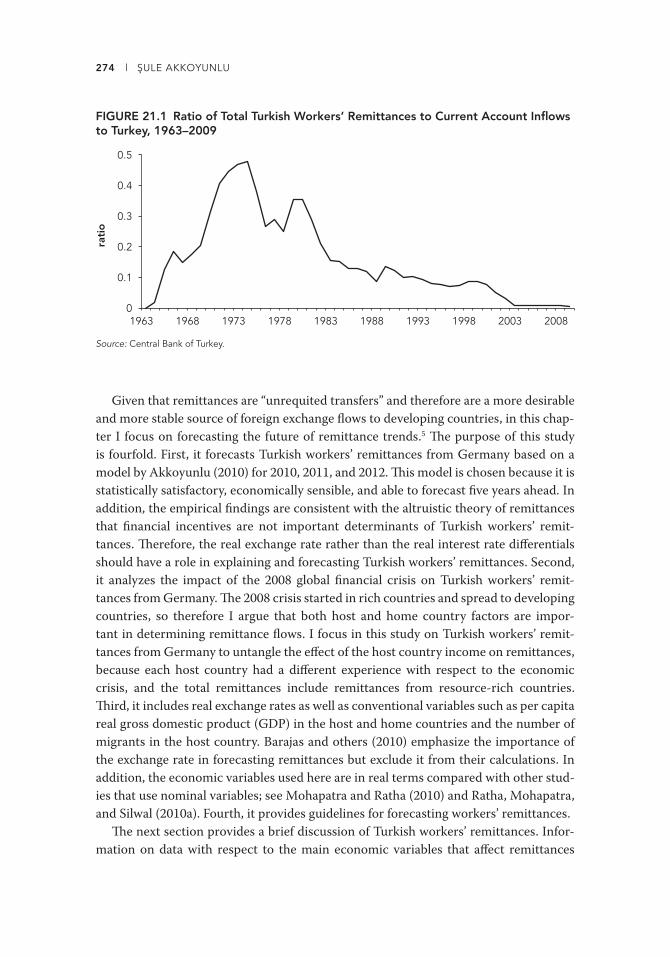

21.1 Ratio of Total Turkish Workers’ Remittances to Current Account Infl ows to

Turkey, 1963–2009 ................................................................................................................... 274

21.2 Turkish Workers’ Remittances Total and from Germany, 1963–2009 .......................... 275

x l CONTENTS

21.3 Turkish Workers’ Remittances from Germany and Other Financial Flows to

Turkey, 1963–2009 ................................................................................................................... 276

21.4 Growth Rates of Real per Capita GDP and Unemployment for Germany and

Turkey ......................................................................................................................................... 277

21.5 Turkish and German Real Short-Term Interest Rates, Th eir Diff erences, and

Turkish Workers’ Remittances from Germany, 1963–2009............................................. 278

21.6 Total and Turkish Employment in Germany, 1991–2009 ................................................ 279

21.7 Turkish Employment in Germany by Sector, 1987–2009 ................................................ 279

21.8 Total and Turkish Unemployment in Germany, 1998–2009 ........................................... 279

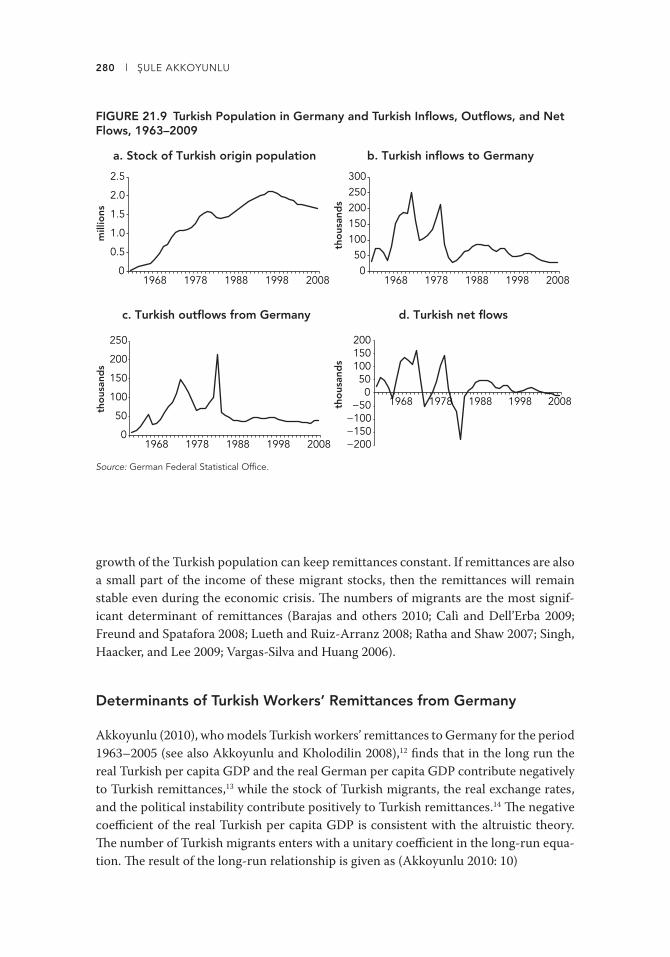

21.9 Turkish Population in Germany and Turkish Infl ows, Outfl ows, and Net Flows,

1963–2009 .................................................................................................................................. 280

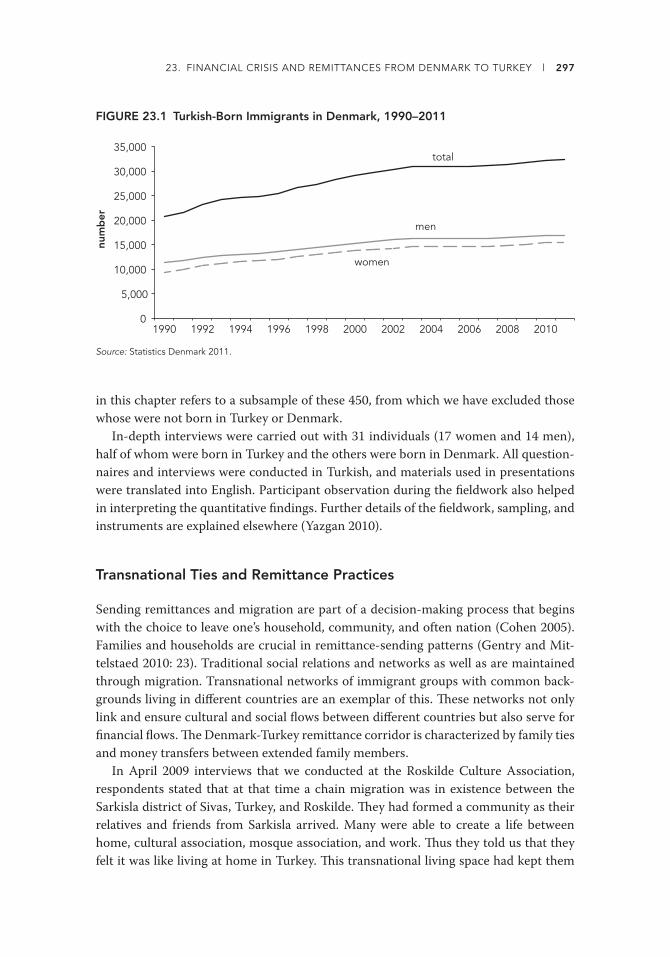

23.1 Turkish-Born Immigrants in Denmark, 1990–2011 ......................................................... 297

23.2 Remittance-Sending Behavior of Danish Turks by Country of Birth, 2010 .................. 298

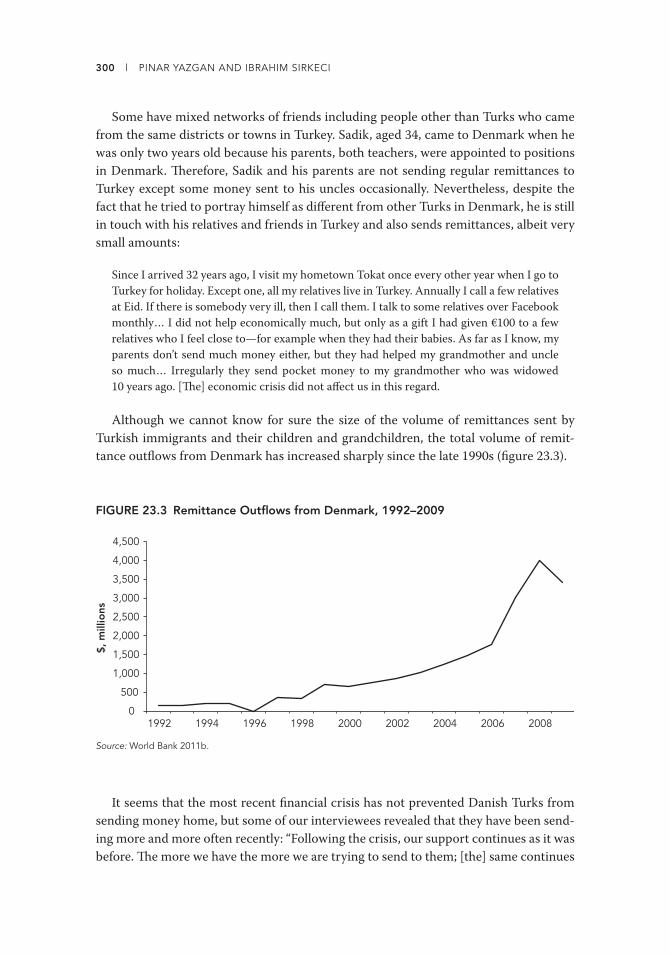

23.3 Remittance Outfl ows from Denmark, 1992–2009 ............................................................ 300

27.1 Remittance and Capital Flows to Developing Countries, 1990–2009 ........................... 326

29.1 Remittances by Major Region ................................................................................................ 350

29.2 Main Recipients of Remittances, 2008 ................................................................................. 351

29.A1 Construction of the Stock of Expatriate Data ..................................................................... 357

31.1 Impact of Crisis on Remittance Infl ows as Percentage of GDP ...................................... 369

31.2 Main Reasons for Emigration from Lebanon, 1992–2007 ............................................... 370

31.3 Main Sources of Electronic Cash Transfers to Lebanon, 2009 ........................................ 372

32.1 Mean Remittance Flows in the MENA Region, 1970–2008 ............................................ 381

32.2 Annual Growth Rate of Remittances from GCC Countries to Bangladesh,

Pakistan, and the Philippines, January 2009–May 2010 ................................................... 383

Tables3.1 Offi cial Estimates of the Total Number of Foreign Workers in Asian Economies,

1996–2000 ....................................................................................................................................45

5.1 Real GDP Growth Rates in Selected Countries .....................................................................70

5.2 Share of Employment across Economic Activities in GCC Countries, 2007 ..................71

5.3 Projects Aff ected by the Crisis in the GCC ............................................................................72

5.4 Government Expenditure in the GCC Countries, 2006–11 ...............................................73

5.5 Estimated Number of Migrants Returning to Kerala Due to Crisis in 2009 ...................74

5.6 Estimates of Emigrants Returning to South Asia from the Gulf Due to Crisis, 2009 ....74

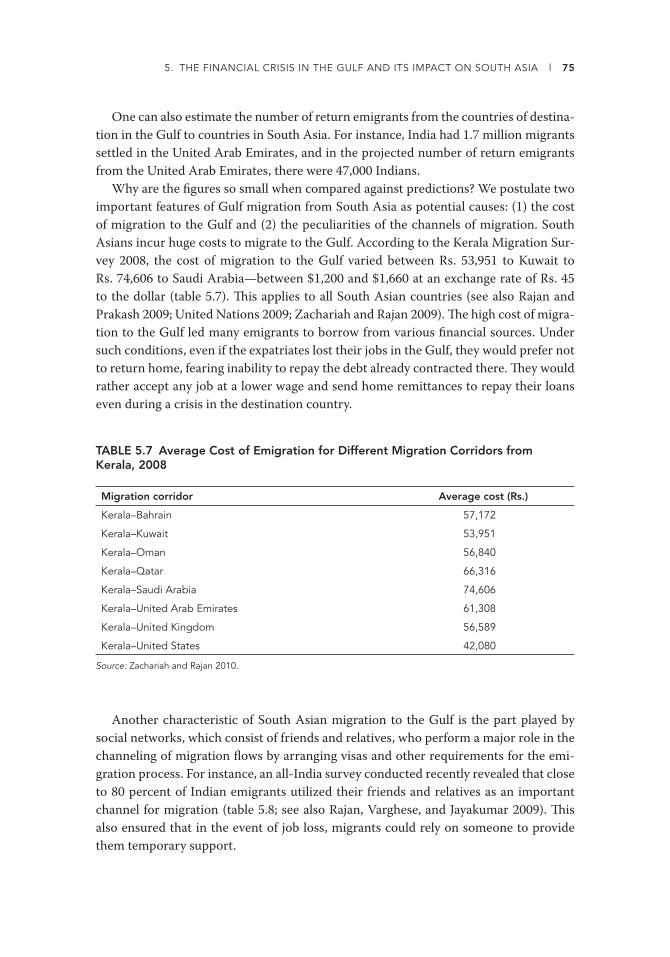

5.7 Average Cost of Emigration for Diff erent Migration Corridors from Kerala, 2008 .......75

5.8 Channels of Migration by Emigrants, 2007 ............................................................................76

5.9 Estimates of Emigrants Who Lost Job in the Gulf but Did Not Return, 2009 ................76

5.10 Flow of Migrant Workers from South Asia to the Gulf, 2005–09 .....................................77

5.11 Inward Remittances to South Asian Countries, 2000–09 ...................................................79

6.1 “Near Past” and “Near Future” Use of Remittances by Gender: Household and

Migrant Worker Surveys, 2009 .................................................................................................88

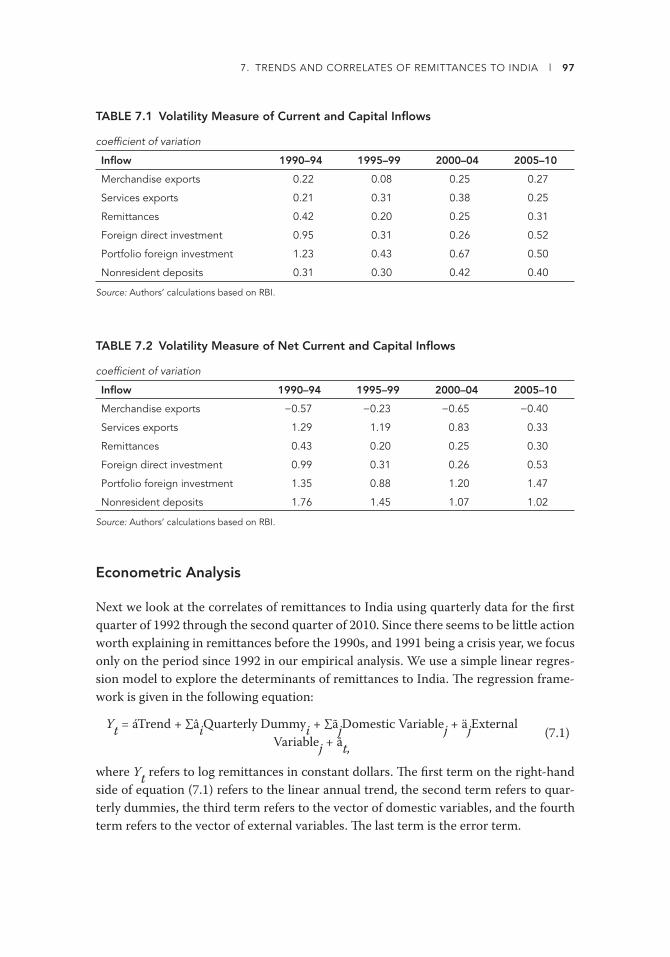

7.1 Volatility Measure of Current and Capital Infl ows ..............................................................97

7.2 Volatility Measure of Net Current and Capital Infl ows ......................................................97

7.3 Trend in Remittances ..................................................................................................................98

CONTENTS l xi

7.4 Correlates of Remittances between 1992 and 2010 ........................................................... 100

7.5 Correlates of Remittances between 1992 and 2003 ........................................................... 101

7.6 Correlates of Remittances between 2004 and 2010 ........................................................... 102

8.1 Source Regions of Workers’ Remittances to India ............................................................. 110

8.2 Relative Volatility of Workers’ Remittance Infl ows to India ............................................ 111

8.3 Volatility in the Components of Workers’ Remittances to India .................................... 112

8.4 Johansen Cointegration Test .................................................................................................. 113

8.5 Long-Run Cointegrating Estimates of Workers’ Remittance Infl ows to India

Based on Vector Error Correction Model ........................................................................... 113

8.6 Error Correction: Short-Run Dynamics ............................................................................. 114

8.7 Variance Decomposition of Workers’ Remittances ........................................................... 116

9.1 Remittance Flows to South Asia and to Nepal Grew at a Slower Rate during the

Global Financial Crisis but Did Not Decline ...................................................................... 126

9.2 Cost of Sending $200 to Nepal, June 2009 .......................................................................... 128

13.1 Remittances to Bangladesh and Pakistan ............................................................................ 158

13.2 Correlation of Remittances and U.S. Labor Market Indicators ...................................... 162

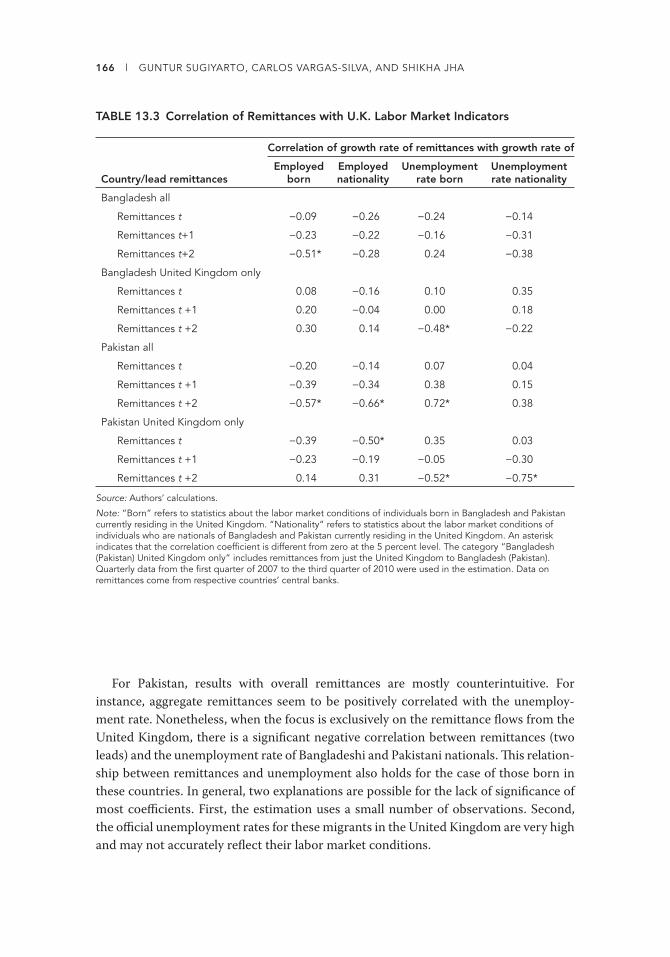

13.3 Correlation of Remittances with U.K. Labor Market Indicators .................................... 166

14.1 Distribution of Samples ........................................................................................................... 172

14.2 Receiving Remittances from Migrants ................................................................................ 175

14.3 Average Amount of Remittances Received ......................................................................... 175

14.4 Frequency of Remittances Received before and during the Crisis ................................. 175

14.5 Channels of Remitting before and during the Crisis ........................................................ 176

14.6 Reasons for the Decrease in Income..................................................................................... 177

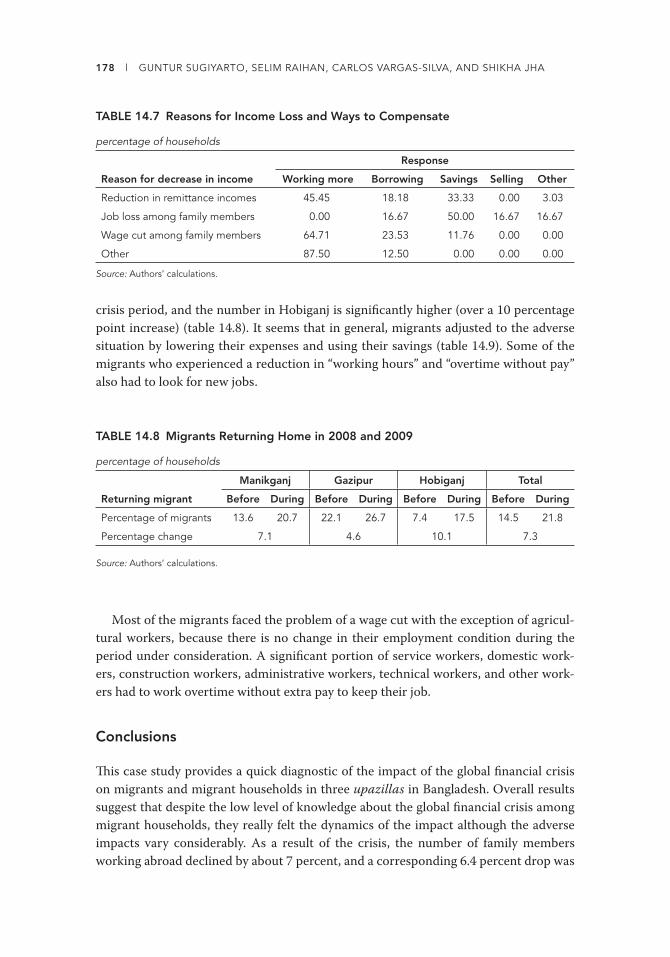

14.7 Reasons for Income Loss and Ways to Compensate ......................................................... 178

14.8 Migrants Returning Home in 2008 and 2009 .................................................................... 178

14.9 Change in Employment Condition and Responses ........................................................... 179

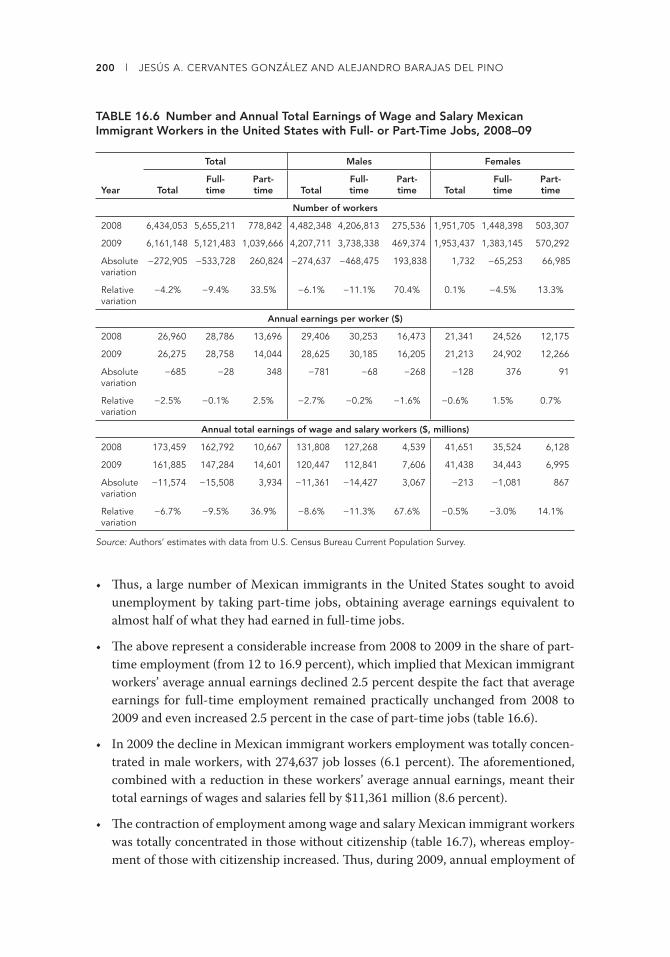

16.1 Population and Immigrants in the United States, 2008–09 ............................................. 195

16.2 Mexican Workers and Immigrants in the United States, 2009 ....................................... 197

16.3 Average Monthly Earnings of Wage and Salary Mexican Immigrant

Workers in the United States, 2008–09 ............................................................................... 197

16.4 Total Earnings of Wage and Salary Workers and of Mexican Immigrants

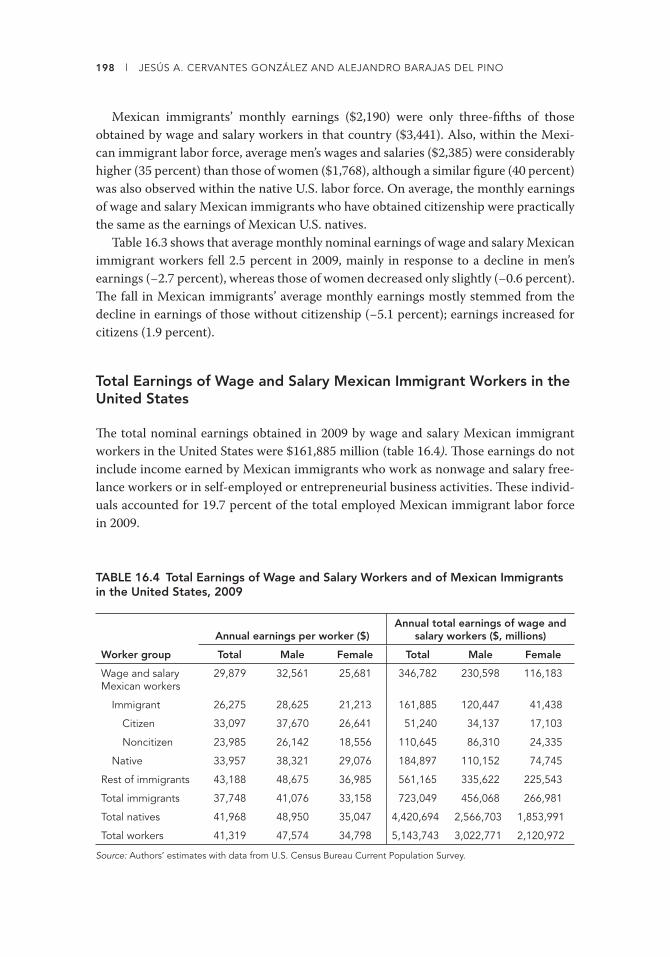

in the United States, 2009 ....................................................................................................... 198

16.5 Variation in the Total Earnings of Wage and Salary Workers and of Mexican

Immigrants in the United States, 2009 ................................................................................. 199

16.6 Number and Annual Total Earnings of Wage and Salary Mexican Immigrant

Workers in the United States with Full- or Part-Time Jobs, 2008–09 ........................... 200

16.7 Number and Annual Total Earnings of Wage and Salary Mexican Immigrant

Workers in the United States by Citizenship Status, 2008–09 ........................................ 201

16.8 Total Employed Labor Force and Mexican Immigrant Workers in the

United States by Industry Sector, 2009 ................................................................................ 202

16.9 Unemployment Rates in the United States, 2006–10 ....................................................... 203

16.10 Years of Education of Mexican Immigrants, 2009 ............................................................. 204

16.11 Educational Attainment among Wage and Salary Mexican Immigrant Workers,

2009 ............................................................................................................................................. 205

xii l CONTENTS

16.12 Variation in Number and Annual Earnings of Wage and Salary Mexican

Immigrant Workers by Educational Attainment, 2009..................................................... 206

16.13 Total Earnings of Wage and Salary Mexican Immigrant Workers by Educational

Attainment, 2009 ...................................................................................................................... 207

16.14 Total Employed and Unemployed Labor Force and Mexican Immigrants,

First and Second Semesters, 2009 and 2010 ....................................................................... 209

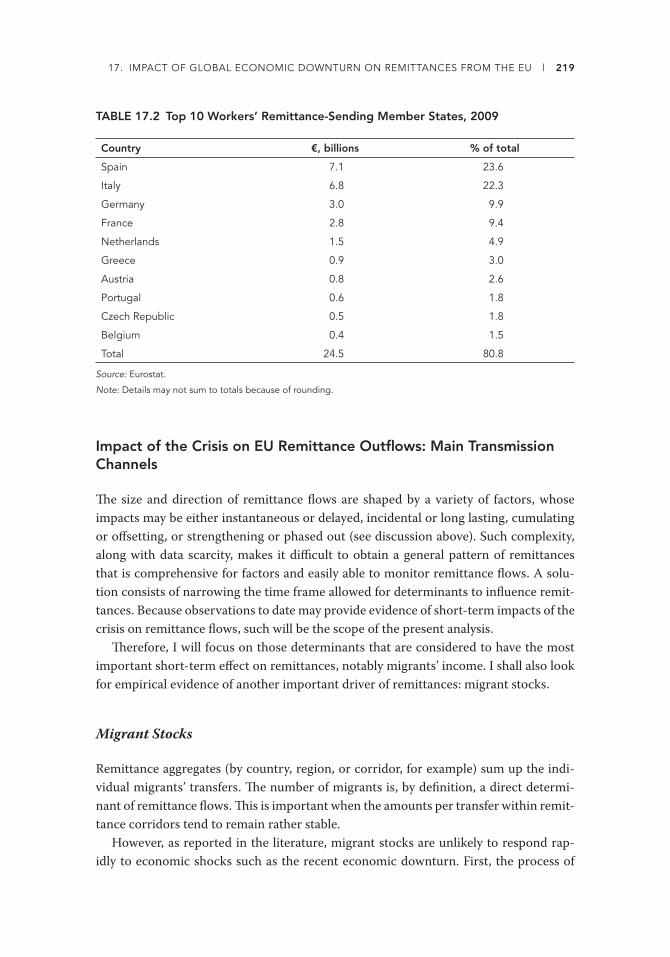

17.1 Top 10 Remittance-Sending Member States, 2009 ............................................................ 218

17.2 Top 10 Workers’ Remittance-Sending Member States, 2009 .......................................... 219

17.3 Selected Member States’ Employment Forecasts, 2009–12 ........................................... 223

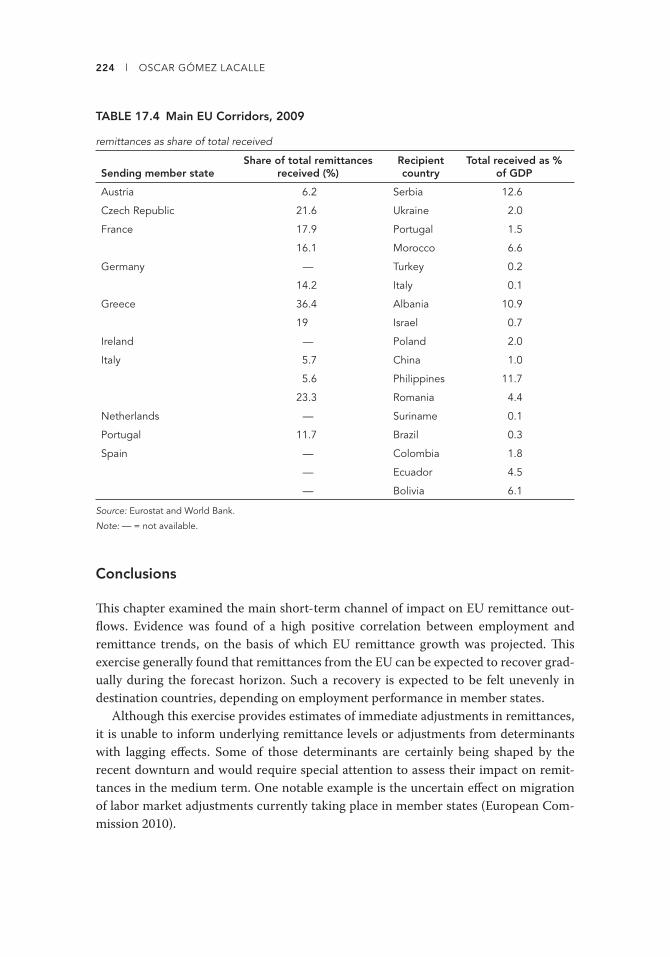

17.4 Main EU Corridors, 2009 ........................................................................................................ 224

19.1 Estimate of Financial Well-Being of Albanian Migrant Households Comparing

2008 and 2009............................................................................................................................ 246

19.2 Comparison of Incomes, Expenses, and Savings of Migrant Households in

Greece in 2008 and 2009 ......................................................................................................... 247

19.3 Savings Levels of Albanian Migrant Households in 2009 ................................................ 247

19.4 Comparison of Estimates of Household Remittance Levels to Albania 2008–09 ....... 249

19.5 Comparison of Migrant Household Remittances in 2008–09 ........................................ 249

19.6 Migrant Household Remittance Amounts Forecasted for 2009–10 .............................. 250

19.7 Planned Strategies for Managing the Eff ects of the Economic Crisis, While in the

Country of Migration............................................................................................................... 251

20.1 Proportion of Women and Children among Migrants Entering Spain by

Country of Origin, 2004–09 ................................................................................................... 261

21.1 Capital Transactions, 2008–10 .............................................................................................. 277

21.2 Summary of Steps ..................................................................................................................... 283

21.3 Forecast Results ........................................................................................................................ 284

21.4 Value of Turkish Workers’ Remittances from Germany .................................................. 284

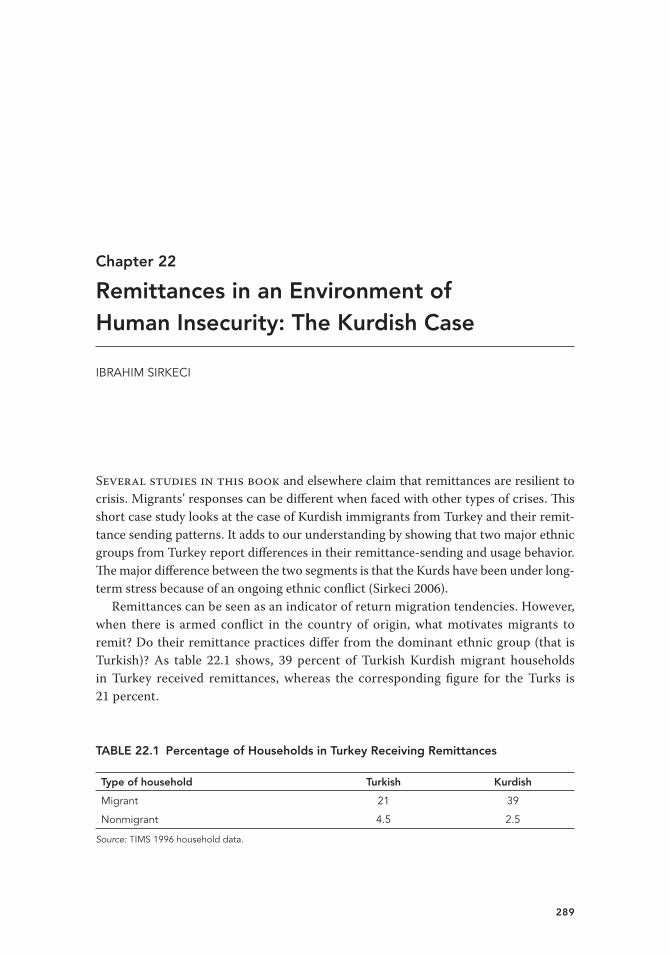

22.1 Percentage of Households in Turkey Receiving Remittances .......................................... 289

22.2 Sources of Remittances for Households in Turkey ............................................................ 290

22.3 Household Goods Received from Migrants ........................................................................ 291

22.4 Use of Most Remittances in Turkey ...................................................................................... 292

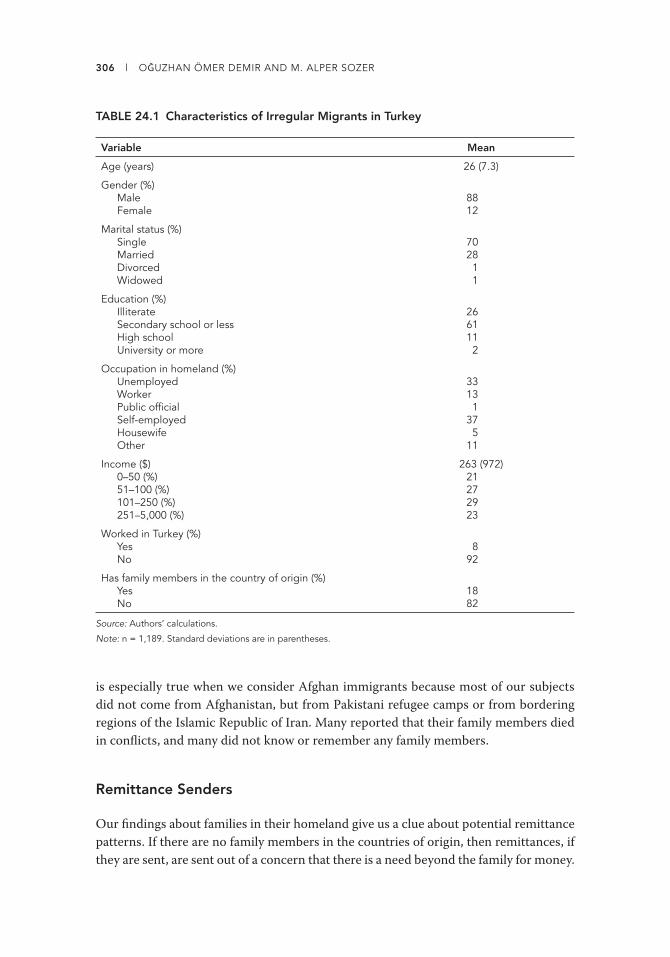

24.1 Characteristics of Irregular Migrants in Turkey ............................................................... 306

24.2 Characteristics of Irregular Migrants in Turkey Who Send Remittances to

Th eir Country of Origin .......................................................................................................... 307

24.3 Work and Remittance Patterns of Irregular Migrants Who Sent Remittances to

Th eir Country of Origin ......................................................................................................... 309

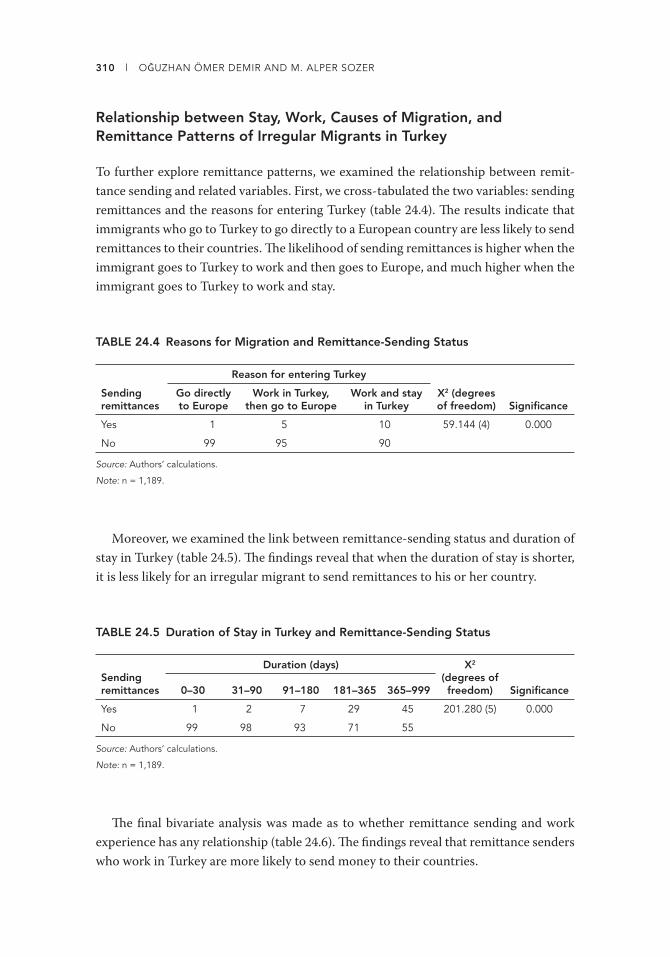

24.4 Reasons for Migration and Remittance-Sending Status ................................................... 310

24.5 Duration of Stay in Turkey and Remittance-Sending Status ........................................... 310

24.6 Employment and Remittance-Sending Status .................................................................... 311

26.1 Cost of Sending $NZ 200/$A 200 from New Zealand/Australia to a Pacifi c Island

Country as Percentage of Total Amount Sent .................................................................... 322

27.1 Vanuatu: Selected Key Indicators .......................................................................................... 327

27.2 Pacifi c Island Countries: Remittances, 1970–2009 ........................................................... 327

27.3 Demographic Profi le of Vanuatu ........................................................................................... 328

27.4 Commercial Financial Institutions in Vanuatu................................................................... 328

CONTENTS l xiii

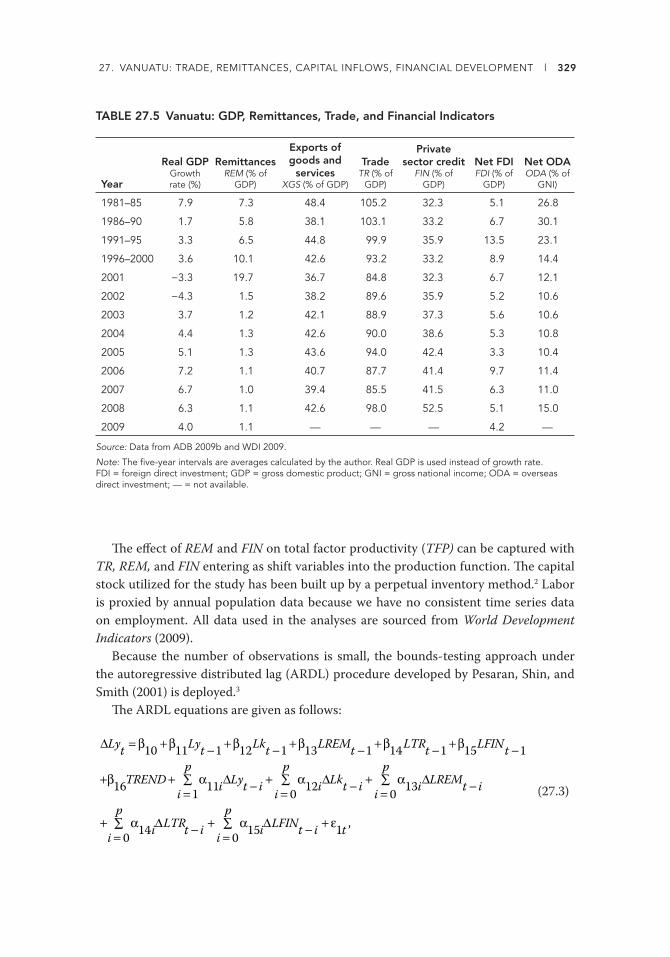

27.5 Vanuatu: GDP, Remittances, Trade, and Financial Indicators ......................................... 329

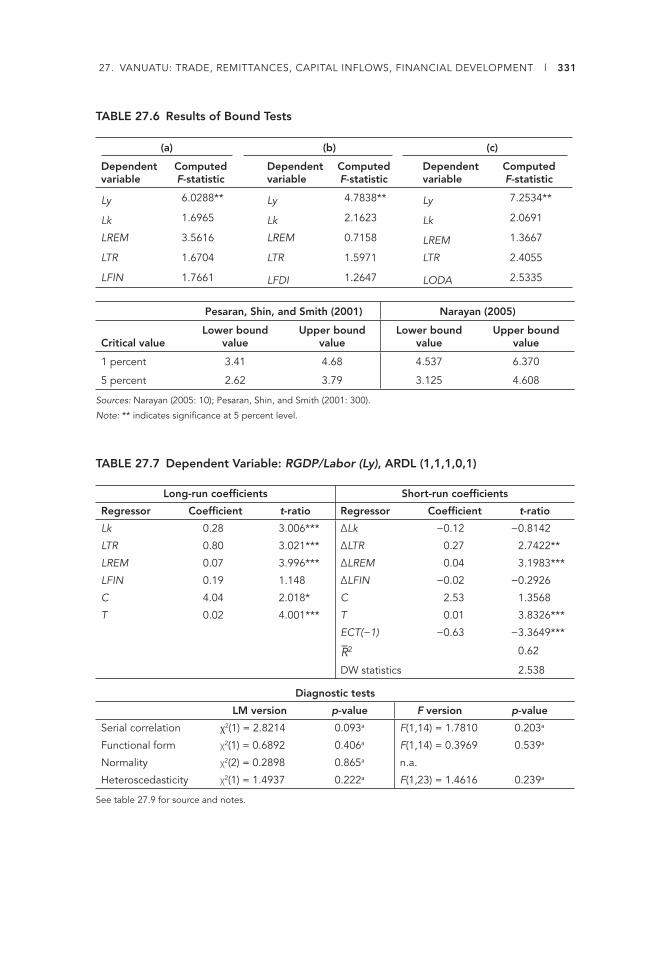

27.6 Results of Bound Tests ............................................................................................................ 331

27.7 Dependent Variable: RGDP/Labor (Ly), ARDL (1,1,1,0,1) ............................................... 331

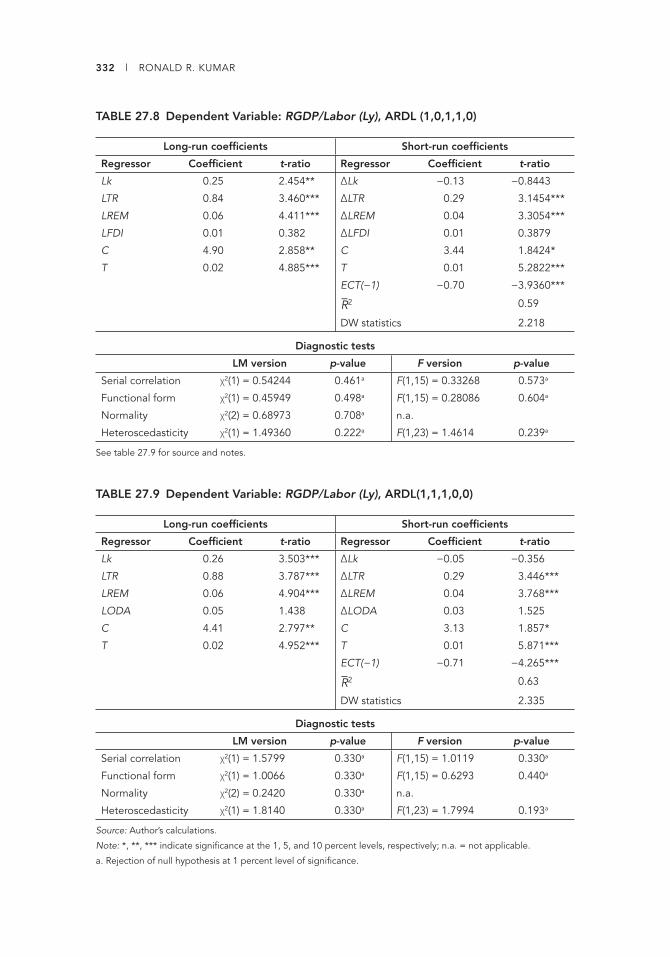

27.8 Dependent Variable: RGDP/Labor (Ly), ARDL (1,0,1,1,0) ............................................... 332

27.9 Dependent Variable: RGDP/Labor (Ly), ARDL(1,1,1,0,0) ................................................ 332

28.1 Summary of Variables and Data Sources ............................................................................. 341

28.2 Remittances, Disasters, and FDI and ODA in the Sample Countries ............................ 343

28.3 Pooled OLS Regression Results (no control variables) ..................................................... 344

28.4 Pooled OLS Regression Results (controls included) ......................................................... 344

28.5 “Diff erence” GMM Dynamic Panel Estimation Results ................................................... 345

29.1 Determinants of Remittances ................................................................................................ 353

31.1 Remittance Infl ows in MENA as Percentage of GDP, 2008–09 ...................................... 368

31.2 Correlation Levels .................................................................................................................... 375

32.1 Top-10 Destinations of Migrants from MENA Countries, 2005 .................................... 379

32.2 Remittance Infl ows and Outfl ows in Selected MENA Countries, 1970–2008 .....................380

32.3 Remittances from GCC to Bangladesh, Pakistan, and the Philippines,

2008 and 2009............................................................................................................................ 382

32.4 Quarterly Remittances Received for 2008, 2009, and 2010.............................................. 385

xv

Foreword

The global financial crisis in 2008–09 served a harsh blow to 215 million

migrants and their families around the world. Migrants faced worsening employment

prospects in destination countries, often coupled with tightening entry regulations

and vicious anti-immigration rhetoric. Meanwhile, migrants’ support to families back

home in the form of remittances was ever more important in the face of the rising

cost of living.

Remittances are the most tangible link between migration and development. At more

than $325 billion per year, remittances sent by migrants to developing countries are

larger than offi cial development assistance as well as private debt and portfolio equity

fl ows. Remittances help families all over the world to pay for food, housing, education,

and health expenses and even invest in small businesses. At the national level, remit-

tances help off set current account defi cits and shore up international reserves.

Th e 49 authors of this volume analyze remittance patterns and practices across the

globe during the recent fi nancial crisis. Some of these studies provide insights into indi-

vidual and household practices, whereas others focus on national and international

fl ows. Evidence shows that remittances fl ows were resilient during this crisis. However,

the cost of money transfers is still very high, and we need to reduce transaction costs to

facilitate remittance fl ows. Studies in this volume also show that remittances are more

than the transfer of money. Gifts, values, skills, and ideas transferred are potentially

crucial for long-term socioeconomic development of developing countries.

Despite the breadth of these studies, readers should be warned of the pitfalls of

migration and remittances data, which are often incomplete. Offi cial fi gures of remit-

tances often underestimate actual fl ows because of the prevalence of informal transfer

channels. Considerably more eff ort is needed to improve the quality of data, reduce

transaction costs, and simplify the process of sending remittances.

xvi l FOREWORD

Th is book is perhaps the fi rst comprehensive study of remittances during the fi nan-

cial crisis and is a timely addition to the literature. It comes at a time when countries

are grappling with the global fi nancial crisis and its aftereff ects. Th e resilience of remit-

tances is good news for developing countries, but leveraging remittances for socio-

economic development remains a key challenge. Th e studies in this book identify and

discuss key patterns observed in remittance practices across the world and possibilities

for the future. We hope this book serves students, researchers, practitioners, and policy

makers around the world as a useful source of reference.

Otaviano Canuto Hans Timmer

Vice President, Poverty Reduction and Director, Development Economics

Economic Management Prospects Group

Th e World Bank Th e World Bank

xvii

Acknowledgments

We would like to acknowledge the support provided by the World Bank. We also

thank Dr. Pinar Yazgan and Dr. Meghan Craig, who assisted in the copyediting and in

the preparation of the bibliography. We are also thankful to our many colleagues who

have contributed to this volume as authors or reviewers. We would like to acknowl-

edge the permission given by Migration Letters to reprint the following papers, which

were fi rst published in a special issue of the journal in October 2010: Mohapatra and

Ratha, “Forecasting Migrant Remittances during the Global Financial Crisis”; Acosta,

Baez, Beazley, and Murrugarra, “Th e Case of El Salvador”; Lacalle, “Th e Impact of the

Global Economic Downturn on Remittances from the European Union”; Singh, “From

Shock Absorber to Shock Transmitter: Sub-Saharan Africa”; and Naufal and Vargas-

Silva, “Migrant Transfers in the MENA Region: A Two-Way Street in Which Traffi c

Is Changing.” We also acknowledge the permission to reprint the paper by Green and

Winters, an earlier version of which was published in Th e World Economy (Vol. 33,

No. 9, pp. 1053–72). We would also like to thank Otaviano Canuto, Sonia Plaza, Hans

Timmer, and Ani Rudra Silwal of the World Bank for encouragement and support at

various stages of the book.

Book design, editing, and production were coordinated by Aziz Gökdemir, Stephen

McGroarty, Stephen Pazdan, and Nora Ridolfi of the World Bank Offi ce of the Pub-

lisher. Nita Congress typeset the book and provided editing, proofreading, and project

management assistance. Bill Pragluski of Critical Stages designed the cover.

xix

Contributors

DON ABEL joined the Reserve Bank of New Zealand in 2004 after a 26-year career

in a large New Zealand–based commercial bank. As Assistant Governor and Head of

Operations, he has a general management function across the Reserve Bank, with par-

ticular responsibility in fi nancial, corporate, commercial, and other internal functions.

He has a liaison role with other central banks in the Pacifi c area. He is a member of the

Bank’s monetary policy and fi nancial stability committees. He has a Ph.D. in geography

from the Victoria University of Wellington.

PABLO ACOSTA works as an Economist in the Social Protection Unit, Latin America

and the Caribbean region, at the World Bank. Before that, he worked as a research

economist in the Andean Development Corporation, at the Ministry of Economy of

Argentina, and as a consultant for the World Bank and the Inter-American Develop-

ment Bank. He holds a Ph.D. in economics from the University of Illinois at Urbana-

Champaign.

ŞULE AKKOYUNLU obtained a B.A. in economics and econometrics from the Uni-

versity of Istanbul, an M.Sc. in economics from the University of London, and a Ph.D.

in economics from Oxford University. She has held teaching and research positions

at the Universities of Oxford, Kent, Bonn, Tel Aviv, California at San Diego, Zurich,

and Neuchatel; and the Swiss Federal Institute of Technology Zurich, OTA, and DIW.

Her research interests include macroeconomics, international economics, economic

history, development economics, econometrics, public economics, political economy,

labor economics, demography, and international migration.

JAVIER BAEZ works as an Economist in the Independent Evaluation Group at the

World Bank. He is also a Research Fellow at the Institute for the Study of Labor and a

Fellow of the Research Network on Population, Reproductive Health, and Economic

Development. He holds a Ph.D. in economics from the Maxwell School of Public Aff airs

at Syracuse University and a master’s in public administration and international devel-

opment from Harvard University.

xx l CONTRIBUTORS

ALEJANDRO BARAJAS DEL PINO is in charge of the Offi ce of Capital Movements

at the Direction for Economic Measurement in Banco de México. He teaches in the Eco-

nomics and Business Faculty of Universidad Anahuac Norte. His undergraduate studies

were at Benemérita Universidad Autónoma de Puebla; his graduate studies were done

at El Colegio de México in México City and at the University of California, Los Angeles.

RODOLFO BEAZLEY is an economist, currently pursuing a master’s degree at the

London School of Economics. Previously, he worked for the Social Protection Unit,

Latin America and the Caribbean region, at the World Bank, and as a researcher for the

Argentine government. He also did consultancies for the International Labour Organi-

zation (ILO) and was a lecturer at the Universidad de Buenos Aires.

DANIÈLE BÉLANGER is Professor of Sociology and Demography at the University

of Western Ontario, London, Canada. She holds the Canada Research Chair in Popula-

tion Gender and Development. She has been conducting research on Asia for 20 years.

Her research interests include gender and migration, marriage migration, labor migra-

tion, and the migration industry. A specialist on Vietnam, she has been involved in

migration-related projects on Bangladesh, Canada, China, India, Japan, the Republic of

Korea, the Philippines, and Taiwan, China.

HENRI BEZUIDENHOUT is Senior Lecturer in International Trade at the North-

West University of South Africa. In 1997, he received a master’s degree in econometrics

from the University of Pretoria and proceeded into development economic consultancy.

In 2007, he earned a Ph.D. in economics from North-West University, after which he

joined the university. Current areas of research include international capital fl ows, for-

eign direct investment risk, investment promotion, and regional integration in Africa.

JEFFREY H. COHEN is Professor of Anthropology at Th e Ohio State University. He

received his Ph.D. from Indiana University. He is coeditor of the Migration Letters jour-

nal and is an offi cer for the Society of Anthropological Sciences. His research focuses

on migration, economic development, and food safety/nutrition. His research has

been supported by the National Science Foundation, National Geographic Society, the

Fulbright program, and the Russell Sage Foundation. His books include Cooperation

and Community: Economy and Society in Oaxaca (1999), Economic Development: An

Anthropological Approach (2002, Alta Mira Press), Th e Culture of Migration in South-

ern Mexico (2004), and Th e Cultures of Migration: Th e Global Nature of Contemporary

Movement (2011, University of Texas Press).

NICOLAAS DE ZWAGER is Founder and Director of the International Agency for

Source Country Information (IASCI), in Vienna. IASCI’s competencies lie in fi eld-

based research/information systems and migration management and development.

Previously, he was the Director for the International Centre for Migration Policy Devel-

opment and served as Chief of Mission for the International Organization for Migration

in Ukraine. He holds a Doctorandus from the University of Amsterdam in the Nether-

lands and a B.A. from the University of Victoria, Canada.

OĞUZHAN ÖMER DEMIR holds M.A. and Ph.D. degrees from Rutgers University.

He is a faculty member at the Turkish National Police Academy, where he also works for

the International Center for Terrorism and Transnational Crime. He is the coeditor of

two books on transnational crime. His academic interests include regular and irregular

migration, transnational crime, and border security.

CONTRIBUTORS l xxi

ILIR GEDESHI is Founder and Director of the Center for Economic and Social Stud-

ies (CESS), an independent think tank specializing in studying economic, social, and

demographic changes, based in Tirana, Albania. CESS has become the main resource

center of Albanian migration issues since its foundation in 1995. Previously, he was the

Director of the Department of Economy at the University of Tirana. He holds a Ph.D. in

economics from the University of Tirana.

NASSIB GHOBRIL is the Chief Economist and Head of the Economic Research and

Analysis Department at the Byblos Bank Group, one of the largest banking and fi nancial

services groups in Lebanon. He is a recipient of the World Lebanese League’s award for

Best Economist in Lebanon and the Diaspora for 2009, and Data Invest and Consult’s

award for Best Sovereign Risk Analyst of 2010. He is a board member of the Lebanese

Transparency Association.

JESÚS A. CERVANTES GONZÁLEZ is Coordinator of Statistical Training and of the

Program for the Application of the General Principles for International Remittances

Services at the Center for Latin American Monetary Studies. Previously, he was Direc-

tor for Economic Measurement at Banco de México. He holds a master of arts degree

and is a Ph.D. candidate at the University of Chicago. He teaches in the Economics and

Business Faculty of Universidad Anahuac Norte.

TIM GREEN is an Economic Advisor at the Department for International Develop-

ment (DFID) in the United Kingdom. After working for the U.K. Financial Services

Authority and as an ODI Fellow in the Ministry of Tourism, Industry, and Commerce

of the government of Guyana, he joined DFID in 2005 and has worked, among other

things, on migration policy in DFID’s Policy Division.

GREGORY S. GULLETTE received his Ph.D. from the University of Georgia in envi-

ronmental anthropology. He has conducted ethnographic fi eldwork in Mexico, New

Zealand, Th ailand, and the United States. He is primarily interested in issues of political

ecology, political economy, development, migration, and transnationalism. His most

recent research in Th ailand centers on the relationships between migration and urban

environmentalism in Bangkok.

POONAM GUPTA is a Professor at ICRIER. She has previously worked at the Inter-

national Monetary Fund and has taught at the Delhi School of Economics. She has

also consulted for the World Bank, the International Monetary Fund, and the Asian

Development Bank. She holds a Ph.D. in economics from the University of Maryland.

Her work has been published in leading academic journals and in collective volumes.

KIM HAILWOOD is the Manager of MoneyPACIFIC, a multiagency project jointly

supported by the Reserve Bank of New Zealand, the New Zealand Ministry of Foreign

Aff airs, and the Ministry of Pacifi c Island Aff airs, in cooperation with the World Bank,

to improve Pacifi c peoples’ fi nancial knowledge and awareness. She completed her

M.A. (1st class honors) in education (fi nancial literacy) in 2007 and is currently working

on a Ph.D. investigating the nature and delivery of fi nancial education in New Zealand.

SHIKHA JHA is a Principal Economist in the Economics and Research Department of

the Asian Development Bank. She holds a Ph.D. in economics from the Indian Statisti-

cal Institute, New Delhi. Her areas of specialization are development economics, public

economics, and agricultural economics. She has published extensively in international

xxii l CONTRIBUTORS

peer-reviewed economics journals and in edited books. Her research and operational

experience covers several countries in South Asia, Southeast Asia, East Asia, and Cen-

tral Asia.

RONALD R. KUMAR is affi liated with the School of Government, Development

and International Aff airs, Faculty of Business and Economics, at the University of the

South Pacifi c, and is a recipient of the Sasakawa Young Leaders Fellowship. His areas

of research include macrolevel studies on factors of economic growth with a particular

focus on developing countries.

OSCAR GÓMEZ LACALLE has worked in the Directorate-General for Economic and

Financial Aff airs of the European Commission since 1998. He is currently a member

of a unit dealing with globalization, trade, and development, including the economic

aspects of migration and fi nancial inclusion. Previously, for the European Commission,

he worked on the Spanish economy. He has a degree in economics from the University

Complutense of Madrid, Spain, and a degree in international and development eco-

nomics from the University of Namur, Belgium.

TY MATEJOWSKY is an Associate Professor with the Department of Anthropology

at the University of Central Florida. He received his Ph.D. in anthropology from Texas

A&M University in 2001. His ongoing research in the Philippines examines numer-

ous issues related to globalization, including fast food, urban development, disaster

responses, and international migration.

SANKET MOHAPATRA is an economist with the Development Prospects Group at

the World Bank. His research interests include international capital fl ows, sovereign

and subsovereign ratings, poverty, inequality and growth, and the development impact

of remittances and migration. He also worked as an economist with the Africa Region

of the International Monetary Fund. He holds a Ph.D. from Columbia University and a

master’s degree from the Delhi School of Economics.

GABRIELA MUNDACA is a faculty member of the Applied Economics Department

at Johns Hopkins University. She has worked in the Economics Department of the Uni-

versity of Oslo, Norway; at the World Bank; and in the Research Department of the

Central Bank of Norway (CBN). She has also advised the policy departments of the

CBN for many years. Her main areas of expertise are fi nancial economics, economet-

rics, and international macroeconomics. She has published articles in refereed interna-

tional journals. She holds a Ph.D. in economics from the State University of New York

at Stony Brook.

EDMUNDO MURRUGARRA is Senior Economist with the Human Development

Department, Latin America and the Caribbean region, World Bank. His areas of interest

are human development in health and education, labor economics, and poverty. He led a

cross-sectoral team involved in streamlining migration issues in analytical and operational

products at the Bank. He has taught at the Pontifi cia Universidad Católica del Perú and the

Central Reserve Bank of Peru, Lima. He is a graduate of the Pontifi cia Universidad Católica

del Perú and holds a Ph.D. from the University of California, Los Angeles.

D. NARAYANA is Professor at the Centre for Development Studies in Kerala, India.

He holds a Ph.D. from the Indian Statistical Institute, Calcutta. He has published exten-

sively in international journals, and was a Fulbright Fellow at Harvard and a Visiting

CONTRIBUTORS l xxiii

Professor at the University of Montreal. His latest book, Safeguarding the Health Sec-

tor in Times of Macroeconomic Instability: Policy Lessons for Low- and Middle-Income

Countries, coedited with Slim Haddad and Enis Bariș, was published by the Africa

World Press (2008).

WIM NAUDÉ is Professor of Development Economics and Entrepreneurship and

Director of Research at the Maastricht School of Management. A graduate of the Uni-

versity of Warwick, United Kingdom, he has been a member of international networks

and advisory bodies including the International Council for Small Business, the Club de

Madrid, and the Households in Confl ict Network. He was a Senior Associate Member

of St. Antony’s College, Oxford, and served on the Faculty of Brown University’s Inter-

national Advanced Research Institutes.

GEORGE NAUFAL is an Assistant Professor of Economics at the American University

of Sharjah and a research fellow at the Institute for the Study of Labor. His primary

research includes migration and its consequences, mainly the impact of remittances on

the remitting countries. His research has focused mostly on the Middle East and North

Africa region, with an emphasis on the Gulf countries.

SIMON PEMBERTON is a Senior Lecturer in Urban Geography and Planning at the

University of Birmingham. His research interests include community planning and liv-

ability, urban resilience and regeneration, the neighborhood impacts of “new” immigra-

tion, and outcomes of state rescaling on urban and rural communities. He has published

widely in all of these areas, including in the Journal of Rural Studies, Urban Studies,

and Regional Studies. He was Director of the Merseyside Social Inclusion Observatory

between 2004 and 2010.

MD MIZANUR RAHMAN is a Research Fellow at the Institute of South Asian Stud-

ies, National University of Singapore. His research interests include gender and migra-

tion, migration and development, remittances, and migrant businesses. He has written

research reports on international migration in Asia for the International Organization

for Migration and the United Nations Development Fund for Women. His work has

appeared in leading migration journals, including International Migration, Population,

Space and Place, Journal of Ethnic and Migration Studies, and Journal of International

Migration and Integration.

SELIM RAIHAN is Associate Professor at the Department of Economics, University

of Dhaka, Bangladesh. He is also the Executive Director, South Asian Network on Eco-

nomic Modelling. His research focuses on international trade and trade policy, poverty

analysis using micro- and macroeconometrics, and applied economics such as linking

trade policies and poverty using computable general equilibrium of single country and

global models. He teaches international trade, economic modeling, quantitative eco-

nomics, econometrics, development economics, and poverty dynamics.

S. IRUDAYA RAJAN is a Chair Professor at the Ministry of Overseas Indian Aff airs

(MOIA), Research Unit on International Migration at the Centre for Development

Studies, Kerala, India. He has extensive research experience in Kerala. He coordinated

fi ve major migration surveys from 1998 to 2009, and has published books and articles

on social, economic, and demographic implications on international migration. He is a

member of the National Migration Policy drafting group appointed by the MOIA. He

edits the annual series India Migration Report published by Routledge.

xxiv l CONTRIBUTORS

DILIP RATHA is the Lead Economist and Manager of the Migration and Remittances

Unit at the World Bank. He is the chair of the advisory group of the Migrating out

of Poverty research consortium and a visiting professor at the University of Sussex.

His expertise includes migration, remittances, and innovative fi nancing. Previously, he

worked at Credit Agricole Indosuez, Singapore; Indian Institute of Management; and

Policy Group, New Delhi. He holds a Ph.D. in economics from the Indian Statistical

Institute, New Delhi.

JOAQUÍN RECAÑOVALVERDE has been a Professor at Universitat Autònoma of

Barcelona since 2003 and a researcher at the Center for Demographic Studies since

1995. From 1989 to 1995, he worked at the Demographic Institute of the Spanish

National Research Council. He has published articles and book chapters on internal

and international migration and on demographic methods of analysis.

ANDREA RIESTER holds a Ph.D. from the Martin Luther University of Halle-Wit-

tenberg and is associated with the Max Planck Institute for Social Anthropology. She

specializes in development, transnationalism, migration, and remittances and works at

the Department for Economic Development and Employment at the German Agency

for International Cooperation (GIZ), based in Eschborn, Germany.

MARTA ROIG is Social Aff airs Offi cer at the Department of Economic and Social

Aff airs of the United Nations. She worked in the Population Division of the United

Nations from 1998 to 2010 and at the United Nations Population Fund from 1996 to

1998. She has authored reports and articles on international and internal migration and

their linkages with development.

LISA SCULLION is a Research Fellow within the Salford Housing and Urban Studies

Unit at the University of Salford, United Kingdom. She has particular research interests

in the needs and experiences of Central and Eastern European migrant workers, female

asylum seekers and refugees, and Gypsy and Traveller communities. She has published

on these issues in journals such as Social Policy and Society and the Community Devel-

opment Journal.

MARNIE SHAFFER worked with Somalis in refugee resettlement before pursuing a

Ph.D. in anthropology at Th e Ohio State University. She is writing her dissertation on

Somali women’s economic lives and gender relations in the Johannesburg community.

She also conducted research in Columbus, Ohio, where she explored the economic

roles of employed Somali women.

JEEVAN RAJ SHARMA is a Senior Researcher at Feinstein International Center and

teaches graduate courses at Friedman School of Nutrition Science and Policy and Fletcher

School of Law and Diplomacy at Tufts University. His current areas of research include

armed confl ict and social transformation, labor mobility and transnationalism, livelihoods

adaptation, international aid policy and practice, research collaboration, and governance

in South Asia. He has a Ph.D. in sociology of South Asia from the University of Edinburgh.

ANI SILWAL has worked at the Washington, D.C., offi ce of the World Bank since April

2008, most recently with the Migration and Remittances Unit. He holds a master’s degree

from the University of Maryland, College Park, and a bachelor’s from Swarthmore Col-

lege. He previously worked as a risk analyst for an energy trading fi rm in Philadelphia.

CONTRIBUTORS l xxv

BHUPAL SINGH is an assistant adviser in the Department of Economic and Policy

Research of the Reserve Bank of India, Mumbai. He has also worked as an economist

in the Bank of England. His research interests include macroeconomics, international

economics, monetary economics, and the fi nancial dimensions of cross-border work-

ers’ remittances. He has been a member of the Luxembourg Group on remittances,

jointly hosted by the IMF and the World Bank with a mandate to improve the recording

of cross-border remittances. He has been the member secretary of the Sub-Group on

Foreign Savings for the Eleventh Five Year Plan (2007–12) set up by the Planning Com-

mission, government of India, in 2006.

KARAN SINGH is an economic specialist with eight years of experience in research

and analytics. For his research on global public bads, he was invited to the Global

Governance School, German Development Institute, Bonn. He has been a lecturer of

applied econometrics for postgraduates at Delhi University, South Campus. He has

authored several research papers in global governance, development economics, mac-

roeconomics, market integration, and applied econometrics. Currently he is a consul-

tant at ICRIER.

RAJU JAN SINGH is the Lead Economist for Central Africa, based in Yaoundé, Cam-

eroon. Prior to joining the World Bank, he held positions at the International Monetary

Fund in Washington, D.C.; at the Swiss Ministry of Finance in Bern; and at Lombard

Odier & Cie (private banking) in Geneva. He was also a consultant for the Swiss Agency

for Development and Cooperation, working with the central banks of Rwanda and Tan-

zania, and taught at the Graduate Institute of International Studies in Geneva. He holds

a Ph.D. from the Graduate Institute of International Studies.

IBRAHIM SIRKECI is Professor of Transnational Studies and Marketing at Regent’s

College, London, U.K. He is also the Director of the Regent’s Centre for Transnational

Studies. Previously, he worked at the University of Bristol. His recent research focuses

on human mobility, confl ict, human insecurity, remittances, segregation, segmentation,

marketing of business schools, and transnational mobile consumers. Most recently,

with Jeff rey Cohen, he coauthored Cultures of Migration (University of Texas Press,

2011). He is the editor of Migration Letters and Transnational Marketing Journal.

MEHMET ALPER SOZER received his Ph.D. from Indiana University of Pennsylva-

nia. He is the author and editor of several books. He is currently working at the Interna-

tional Center for Terrorism and Transnational Crime in Turkey. His research interests

are terrorism, crime prevention, transnational crime, and community policing.

GUNTUR SUGIYARTO is a Senior Economist, Economics and Research Department,

Asian Development Bank. He received his M.Sc. and Ph.D. from the School of Econom-

ics, University of Warwick and Nottingham, United Kingdom. His publications include

books, journal articles, and papers on key development issues, including competitive-

ness, tourism economics and impacts, the labor market, underemployment, the mini-

mum wage, poverty mapping, poverty impact analysis, trade liberalization, optimum

taxation, oil and commodity prices, and migration and remittances.

CARLOS VARGASSILVA is a senior researcher at the University of Oxford, where

he is part of the team establishing the new Migration Observatory. His research inter-

ests include the economic impact of immigration on receiving countries and the link

xxvi l CONTRIBUTORS

between migration and economic development in sending countries, with a special

focus on the role of migrants’ remittances. He has been a consultant for the Asian

Development Bank, the Inter-American Development Bank, the World Bank, and the

United Nations.

L. ALAN WINTERS is a Professor of Economics at the University of Sussex. He is a

Research Fellow at the Centre for Economic Policy Research in London and a Fellow of

the Institute for the Study of Labor in Munich. He previously worked at the Universities

of Cambridge, Bristol, Wales, and Birmingham. He has been editor of the World Bank

Economic Review and associate editor of the Economic Journal, and he serves on several

editorial boards.

PINAR YAZGAN is an Assistant Professor of Sociology at Sakarya University, Turkey.

Her recent research focused on the sense of identity and belonging among migrants

from Turkey in Denmark. She is a research grant recipient from the Scientifi c and Tech-

nological Research Council of Turkey. Between 2007 and 2009, she conducted fi eldwork

in Denmark while serving as a visiting researcher at the Danish National Research Cen-

ter for Social Sciences.

xxvii

Abbreviations

A8 Accession 8 (countries)

ADB Asian Development Bank

AML anti–money laundering

BOP balance of payments

BOPSY Balance of Payments Statistics Yearbook

CAGR compound annual growth rate

CEE Central and Eastern European

CFT countering the fi nancing of terrorism

CIGEM Centre for Migration Information and Management

CPI consumer price index

CSO Central Statistical Offi ce

EEA European Economic Area

EU European Union

FDI foreign direct investment

GCC Gulf Cooperation Council

GDP gross domestic product

GMM generalized method of moments

GNI gross national income

GTZ German Development Cooperation (Deutsche Gesellschaft für

Internationale Zusammenarbeit)

ICRG International Country Risk Guide

ID identifi cation

IEC international education consultancy

IFAD International Fund for Aid and Development

IFS Indian Foreign Service

IMF International Monetary Fund

LCU local currency unit

LIBOR London Interbank Off ered Rate

M2 money and quasi-money

xxviii l ABBREVIATIONS

MENA Middle East and North Africa

MTO money transfer operator

NRI nonresident Indian

ODA offi cial development assistance

ODI overseas direct investment

OFW overseas Filipino worker

OLS ordinary least squares

ONS Offi ce for National Statistics

PATI Programa de Ayuda Temporal al Ingreso

PBS points-based system

PGA Programa General Anti-Crisis

PIC Pacifi c island country

RBI Reserve Bank of India

SSA Sub-Saharan Africa

WDI World Development Indicators

WEO World Economic Outlook

WRS Worker Registration Scheme

All dollar amounts are U.S. dollars unless otherwise indicated.

1

Introduction: Remittance Flows and Practices during the Crisis

IBRAHIM SIRKECI, JEFFREY H. COHEN, AND DILIP RATHA

Immigrants tend to be more negatively aff ected by economic crisis than natives,

particularly when governments apply strict immigration controls. With the onset of

the fi nancial crisis in the latter half of 2008, there were widespread concerns: would

migrants return to sending countries and communities in large numbers, adding fur-

ther economic woes to countries already facing diffi culties? Would remittance fl ows

slow and potentially cease? Th e literature off ers little guidance on these questions. It

is always a challenge to collect data, analyze, interpret, and make recommendations as

the phenomenon under study is still unfolding to reveal new turns and twists. Th e most

recent fi nancial crisis and its repercussions are yet to be completed, and scholars have

only begun processing the event. Th is volume is an eff ort to bring together in one place

fresh thinking and evidence from around the world on the outcomes of mobility in the

context of global fi nancial crisis.

Crises are a part and parcel of the global economic system. In the crisis-aff ected

developed countries, migrants were challenged in their new homes as jobs began to

disappear. Also there was a rapid growth in anti-immigrant sentiment and rhetoric:

where they formerly were often left alone, they now faced discrimination and intimida-

tion and perhaps jail and deportation. In fact, it became easier to scapegoat immigrants

during crises.

Although the latest crisis originated in the United States and around fi nancial sys-

tems in high-income countries, it has had an important and in some places catastrophic

impact on developing nations and migrants. Like political or environmental catastro-

phes, the global fi nancial crisis contributed to an environment of human insecurity,

2 l IBRAHIM SIRKECI, JEFFREY H. COHEN, AND DILIP RATHA

and migration was one strategic response. To avoid the crisis and to survive its impacts,

those who could aff ord to cross borders became international movers; others moved to

domestic destinations; while many simply stayed put and turned to remittances to help

weather the storm. In such situations, remittances are critical to the overall survival of

the sending nation that struggles with ecological disasters disrupting lives, economic

collapse, job market declines, and rising infl ation rates (see, for example, the earthquake

in Haiti in 2010, the Asian crisis of the 1990s, or the crises that plagued Latin America

through the 1980s and 1990s).

Migrant remittances provide a measurable benefi t—a lifeline—for sending commu-

nities, and they contribute directly and indirectly to the income of sending households

(Ratha and Sirkeci 2010: 125). Overall, cash fl ows, increasing expenditures, and (lim-

ited) investments caused by remittances have a substantial impact on the social action

and economic health of movers and nonmovers alike.1 In many parts of the world, par-

ticularly in developing countries, the volume of remittances has increased at a tremen-

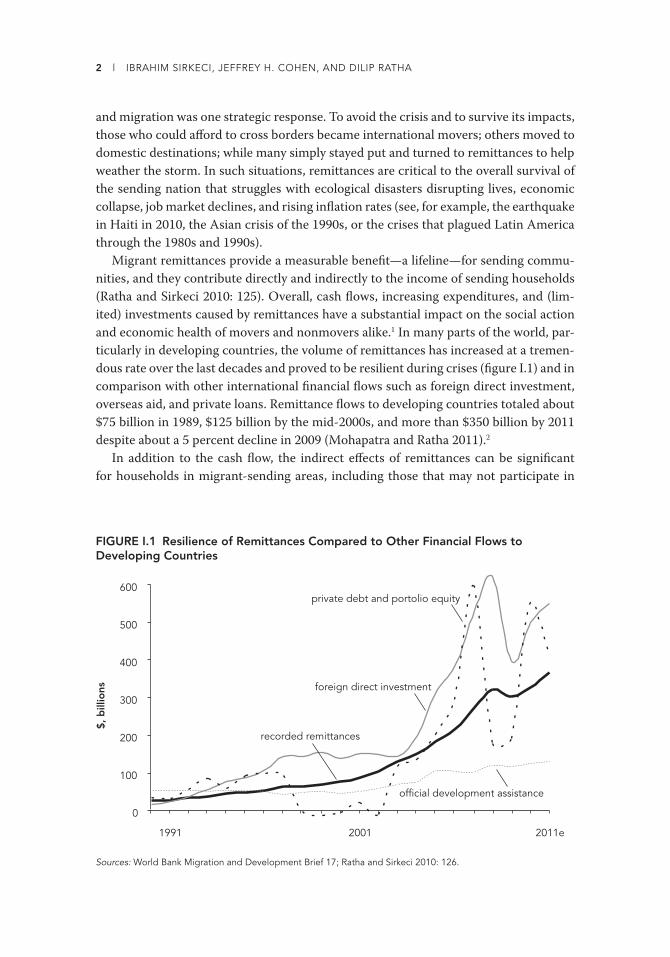

dous rate over the last decades and proved to be resilient during crises (fi gure I.1) and in

comparison with other international fi nancial fl ows such as foreign direct investment,

overseas aid, and private loans. Remittance fl ows to developing countries totaled about

$75 billion in 1989, $125 billion by the mid-2000s, and more than $350 billion by 2011

despite about a 5 percent decline in 2009 (Mohapatra and Ratha 2011).2

In addition to the cash fl ow, the indirect eff ects of remittances can be signifi cant

for households in migrant-sending areas, including those that may not participate in

FIGURE I.1 Resilience of Remittances Compared to Other Financial Flows to Developing Countries

private debt and portolio equity

foreign direct investment

recorded remittances

$, b

illio

ns

0

100

200

300

400

500

600

1991 2001

official development assistance

2011e

Sources: World Bank Migration and Development Brief 17; Ratha and Sirkeci 2010: 126.

INTRODUCTION: REMITTANCE FLOWS AND PRACTICES DURING THE CRISIS l 3

international migration. Massey and Taylor (2004: 157) argue that “the vast majority of

research on migrant remittances and savings ignores their indirect eff ects on migrant-

sending economies. As a result, many studies paint a negative picture of remittances

and savings for development.” According to their assessment, the problem lies in the

fact that many studies fail to recognize the eff ects of nonremittance income and the link

between migrants and nonmigrants.

Remittances remain one of the less volatile sources of foreign exchange earnings for

developing countries. Th e literature has indicated for some time that migrant remit-

tances tend to be stable or even countercyclical in response to economic hardship—

be it a fi nancial crisis, natural disaster, or political confl ict—in a remittance-recipient

country (Ratha 2003; World Bank 2006a). Th is time the crisis began in the United States

and Europe, remittance-source countries. Some early literature (for example, Swamy

1981) argued that source country factors are a major determinant of remittance fl ows.

Th e economic crisis in a major migrant destination country was expected to adversely

aff ect migrants’ income and employment opportunities and hence the willingness and

ability of migrants to stay in their host countries and continue to remit funds. To an

extent, this expectation was realized as remittance fl ows registered a decline in 2009

for the fi rst time in recent memory. Nevertheless, it was also remarkable that remit-

tance fl ows to developing countries fell only 5.2 percent in 2009, proving to be signifi -

cantly more resilient than private capital fl ows, which declined precipitously (Ratha and

Sirkeci 2010: 126).

Remittance receipts at the global level signifi cantly exceed the aid from advanced

economies to developing countries. Th e debate over the impact of remittances on social

and economic inequalities is ongoing. Although some observers argue that remittance

patterns are dependent on the motivations that drive migration (these are not economic

in all cases), others argue that remittances reduce poverty.

Seddon, Adhikari, and Gurung (2002) argue that redressing inequalities is beyond

the concern of migrant remittances. An abundance of evidence is provided by a mul-

titude of studies that confi dently argue that remittances are often used for household

maintenance and for purchase of consumer goods. Remittances are particularly impor-

tant for dependent members of households left behind. Orozco (2006), for example,

argues that remittances are means to ensure social protection as well as capital accumu-

lation (see also Cohen and Rodriguez 2005). Eckstein (2010) argues that remittances are

linked to transnational family social capital and are building blocks for the reproduction

of social networks and connections. Evidence is also found that migrant remittances are

used to support local community projects and events (Cohen 2004). A separate litera-

ture focusing on the role of remittances in relation to confl icts and disasters has also

grown in recent years (Fagen and Bump 2006; Justino and Shemyakina 2010; Mohapa-

tra, Joseph, and Ratha forthcoming). Many of these studies focus on natural disasters

such as the earthquake in Pakistan or tsunamis in the Pacifi c; others look at the implica-

tions of confl icts in African countries. In these examples, remittances appear as insur-

ance for households as they cope with the shocks of confl ict (Davies 2007). Fagen and

4 l IBRAHIM SIRKECI, JEFFREY H. COHEN, AND DILIP RATHA