mew kuwait

TRANSCRIPT

SUSTAINABLE ENERGY SUSTAINABLE ENERGY

POLICY FOR KUWAITPOLICY FOR KUWAIT

MEW - Kuwait

5th Annual Middle East District Cooling Summit November 2013

CONTENTSCONTENTS

Concerns

Power and water demands forecast

Savings Potential

Policy principals

CONCERNSCONCERNS

Major threats to National Sustainability which cannot be ignored:

Real economic diversification is small, the Economy is almost entirely dependant on oil revenue.

Fiscal price could reach real price by 2017.

Fiscal margins necessary to withstand price volatility and to develop the Future Generations income.

By 2030 about 700,000- 900,000 barrels of oil per day will burned to generate electricity and desalinate water.

KUWAIT FISCAL BREAK EVEN KUWAIT FISCAL BREAK EVEN

Break Even

OIL PRICEOIL PRICE

Euro-zone remains in crisis, Asian demand is affected

Oil prices are increasingly volatile to political instability and uncertain supplier policies Coordinated

world emergency action on Climate Change will accelerate conservation and further reduce demand

Makes alternative sources by other producers, Shale oil with technology and production is already a major contributor.

Development of alternative technologies & fuels (Advanced hybrids, Batteries & Hydrogen) will increasingly replace oil in transport fuel role.

SUMMARYSUMMARY

QUOTA (not Related to population)

Social Spending

OPEC forced to maintain High Prices

Accelerates conservation Reduces subsidies in consumer Nations

Makes Shale Oil, Arctic Deepwater Economic

Recovering Producers (Iraq, Libya)

National Development Plans

INCREASING FISCAL

OIL PRICES

WORLD DEMAND OECD stagnant, growing EU crisis ASIA – High Growth (BUT affected by world economy conservation )

QUOTA Reductions MEDIUM TERM PROBABLE LONG TERM CERTAIN LONG TERM

Decisive Climate Change action

Alternative Transport Fuels

Demand reduction

OIL MARKET

Competing Supply

Demand reduction

Competing Supply

Quota Reductions Probable in Medium Term , Certain in Long Term

POWER AND WATER POWER AND WATER

DEMANDDEMAND

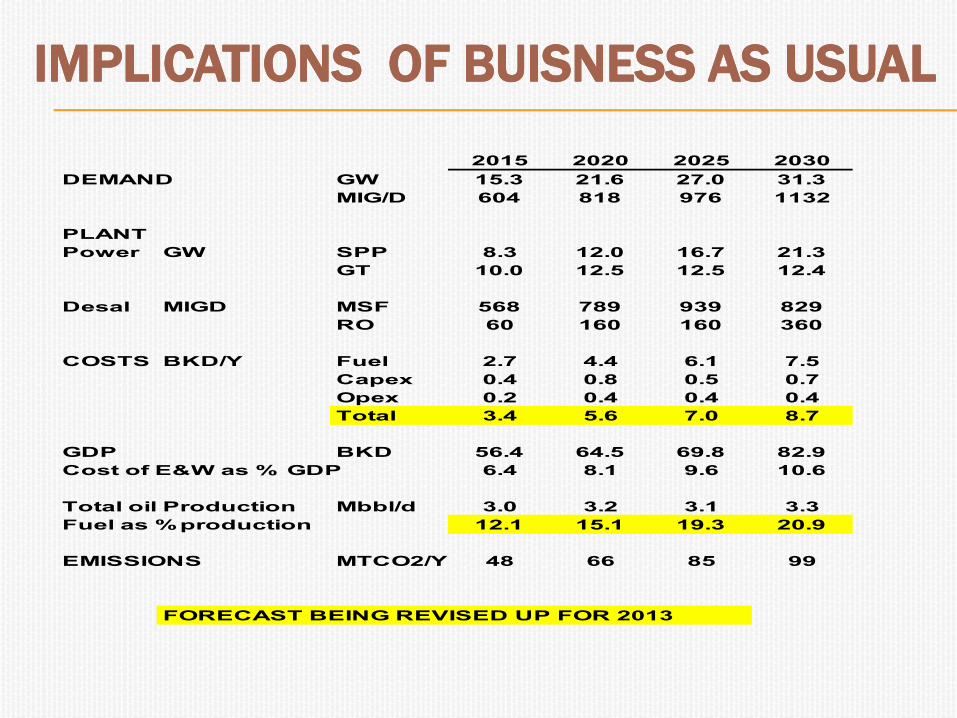

IMPLICATIONS OF BUISNESS AS USUALIMPLICATIONS OF BUISNESS AS USUALSUMMARY OF MEW 2012 FORECAST

2015 2020 2025 2030

DEMAND GW 15.3 21.6 27.0 31.3

MIG/D 604 818 976 1132

PLANT

Power GW SPP 8.3 12.0 16.7 21.3

GT 10.0 12.5 12.5 12.4

Desal MIGD MSF 568 789 939 829

RO 60 160 160 360

COSTS BKD/Y Fuel 2.7 4.4 6.1 7.5

Capex 0.4 0.8 0.5 0.7

Opex 0.2 0.4 0.4 0.4

Total 3.4 5.6 7.0 8.7

GDP BKD 56.4 64.5 69.8 82.9

Cost of E&W as % GDP 6.4 8.1 9.6 10.6

Total oil Production Mbbl/d 3.0 3.2 3.1 3.3

Fuel as %production 12.1 15.1 19.3 20.9

EMISSIONS MTCO2/Y 48 66 85 99

FORECAST BEING REVISED UP FOR 2013

FUEL SUPPLY & DEMAND

0

200

400

600

800

1000

1200

1400

1600

2013 2016 2019 2022 2025 2028

TBTU

HFO Domestic Gas

Total Fuel Demand

DOMESTIC DEMAND DOMESTIC DEMAND -- BUSINESS AS USUALBUSINESS AS USUAL-- DEMANDS

PER CAPITA

PEAK ELECTRICAL (GW)

0

5

10

15

20

25

30

35

1998 2002 2006 2010 2014 2018 2022 2026 2030

Actual

Const Per

Capita

Forecast

PEAK WATER (MIG/D)

0

250

500

750

1000

1250

1998 2002 2006 2010 2014 2018 2022 2026 2030

PEAK ELECTRICAL (KW)

0

1

2

3

4

5

6

1998 2002 2006 2010 2014 2018 2022 2026 2030

PEAK WATER (G/D)

0

50

100

150

200

1998 2002 2006 2010 2014 2018 2022 2026 2030

Efffect of National

Development Plans

Population 6.2 M in 2030

PLANT AND FUEL REQUIREMENTSPLANT AND FUEL REQUIREMENTS

FUEL SUPPLY & DEMAND

(MBoe)

Available

HFO

Avalable

Gas

Crude

LNG &

Gas Oil

0

50

100

150

200

250

300

2013 2017 2021 2025 2029

POWERPLANT REQUIRED

(GW)

0

5

10

15

20

25

30

35

2013 2017 2021 2025 2029

2012 Estimate

2013 Estimate

DESALINATION

(MIGD)

0

250

500

750

1000

1250

2013 2017 2021 2025 2029

2012 Estimate

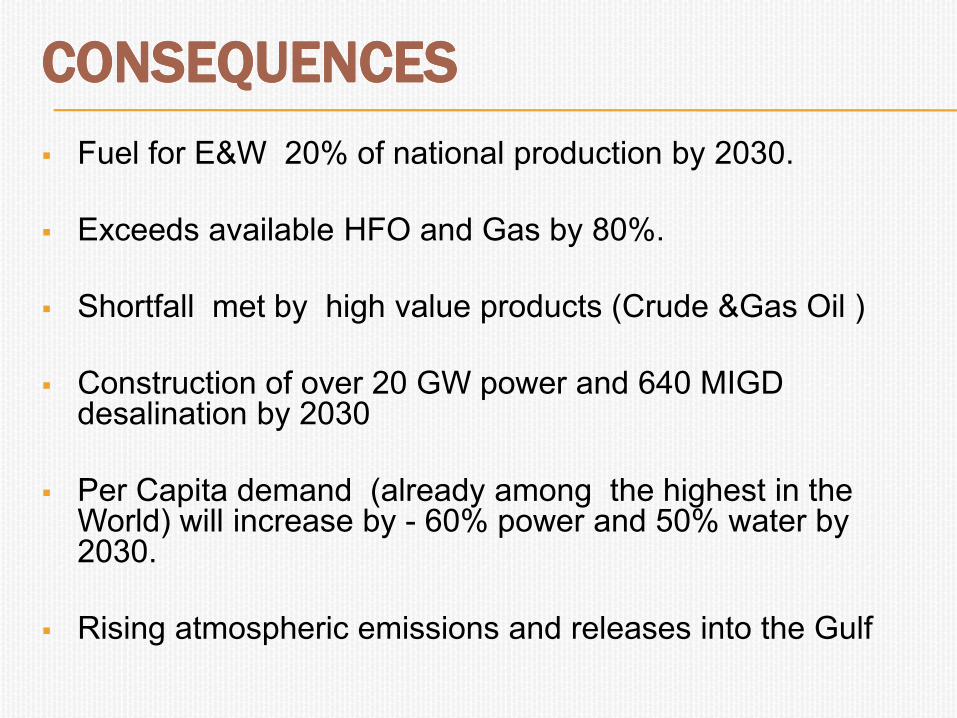

CONSEQUENCESCONSEQUENCES

Fuel for E&W 20% of national production by 2030.

Exceeds available HFO and Gas by 80%.

Shortfall met by high value products (Crude &Gas Oil )

Construction of over 20 GW power and 640 MIGD desalination by 2030

Per Capita demand (already among the highest in the World) will increase by - 60% power and 50% water by 2030.

Rising atmospheric emissions and releases into the Gulf

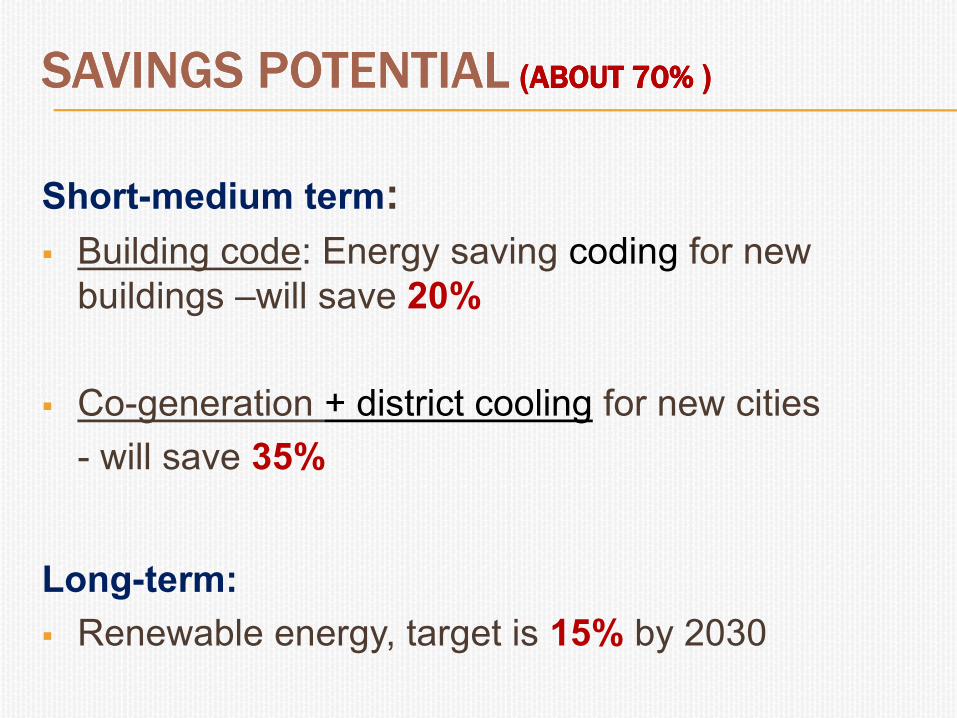

((ABOUT ABOUT 7070% % )) SAVINGS POTENTIALSAVINGS POTENTIAL

Short-medium term:

Building code: Energy saving coding for new

buildings –will save 20%

Co-generation + district cooling for new cities

- will save 35%

Long-term:

Renewable energy, target is 15% by 2030

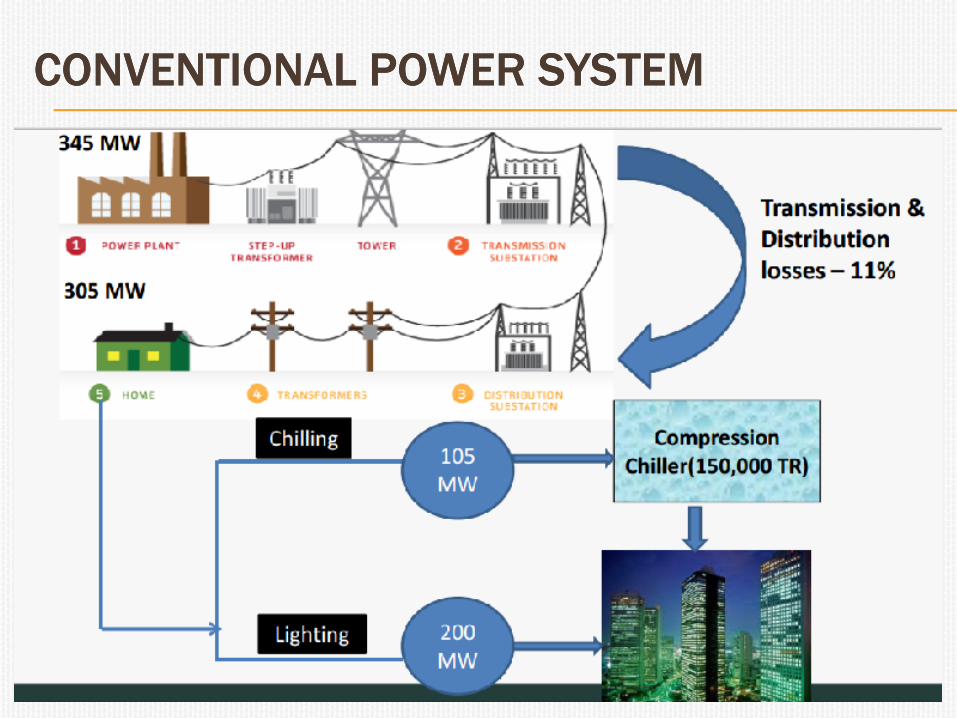

CONVENTIONAL POWER SYSTEMCONVENTIONAL POWER SYSTEM

COCO--GENERATION & DISTRICT COOLINGGENERATION & DISTRICT COOLING

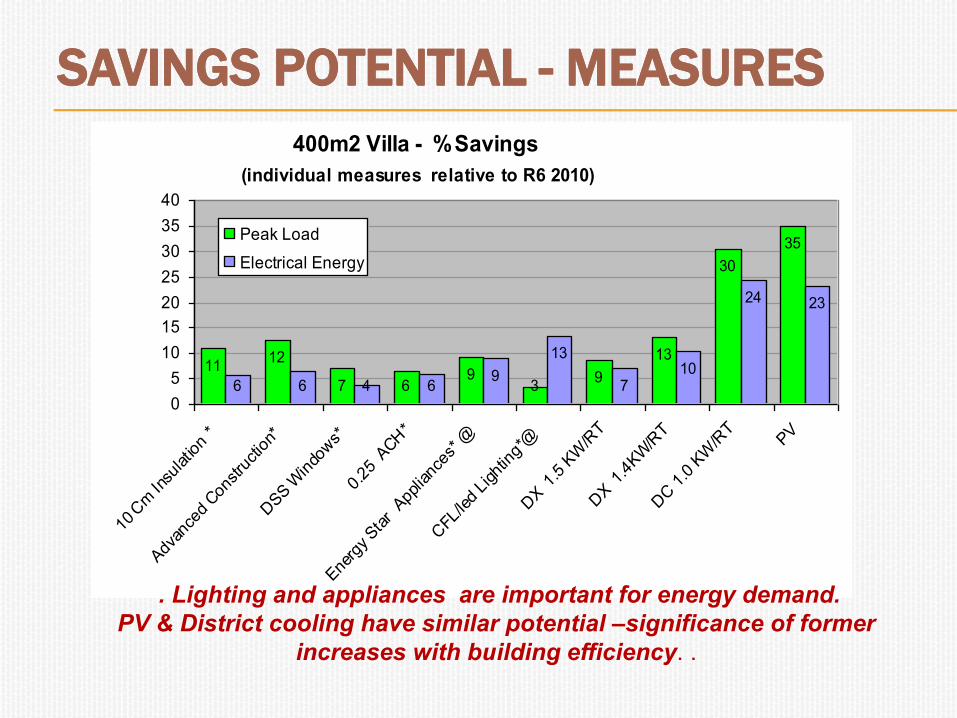

SAVINGS POTENTIAL SAVINGS POTENTIAL -- MEASURESMEASURES

400m2 Villa - %Savings

(individual measures relative to R6 2010)

12

7 69

39

13

30

35

6 6 4 69

13

710

24 23

11

0

5

10

15

20

25

30

35

40

10 C

m In

sulatio

n *

Adv

ance

d Con

stru

ctio

n*

DSS W

indo

ws*

0.25

ACH*

Ene

rgy Sta

r A

pplia

nces

* @

CFL

/led

Ligh

ting*

@

DX 1

.5 K

W/R

T

DX 1

.4KW

/RT

DC 1

.0 K

W/R

TPV

Peak Load

Electrical Energy

. Lighting and appliances are important for energy demand.

PV & District cooling have similar potential –significance of former

increases with building efficiency. .

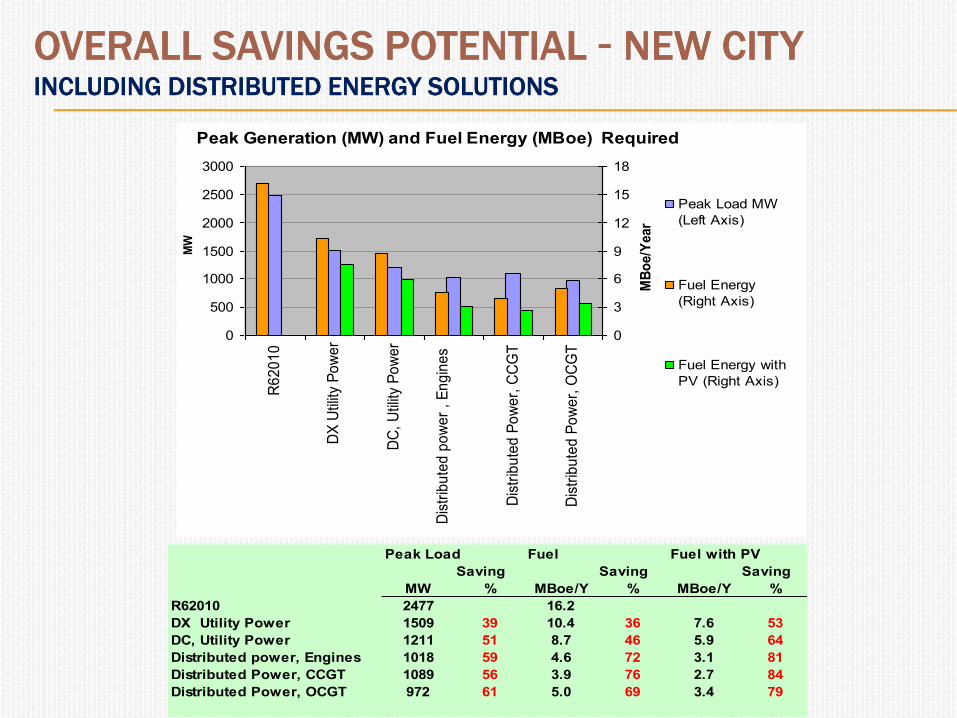

NEW CITYNEW CITY--OVERALL SAVINGS POTENTIAL OVERALL SAVINGS POTENTIAL INCLUDING DISTRIBUTED ENERGY SOLUTIONSINCLUDING DISTRIBUTED ENERGY SOLUTIONS

Peak Load Fuel Fuel with PV

Saving Saving Saving

MW % MBoe/Y % MBoe/Y %

R62010 2477 16.2

DX Utility Power 1509 39 10.4 36 7.6 53

DC, Utility Power 1211 51 8.7 46 5.9 64

Distributed power, Engines 1018 59 4.6 72 3.1 81

Distributed Power, CCGT 1089 56 3.9 76 2.7 84

Distributed Power, OCGT 972 61 5.0 69 3.4 79

Peak Generation (MW) and Fuel Energy (MBoe) Required

0

500

1000

1500

2000

2500

3000

R6

20

10

DX

Util

ity P

ow

er

DC

, U

tility

Po

we

r

Dis

trib

ute

d p

ow

er

, E

ng

ine

s

Dis

trib

ute

d P

ow

er,

CC

GT

Dis

trib

ute

d P

ow

er,

OC

GT

MW

0

3

6

9

12

15

18

MB

oe/Y

ear

Peak Load MW

(Left Axis)

Fuel Energy

(Right Axis)

Fuel Energy with

PV (Right Axis)

RENEWABLE ENERGY POTENTIAL RENEWABLE ENERGY POTENTIAL

17

PV costs reducing rapidly, dominated by Chinese manufacture

Wind and probably Rooftop and Utility PV competitive with RHSPP now

Depends on local conditions, and intermittency , now being confirmed

by pilot projects.

STEAM TURBINES AND GAS TURBINES

0

5

10

15

20

25

70 90 110 130

Crude Price $/Bbl

LC

OE

CK

Wh

r

RH SPP

" F" CCGT

SOLAR & WIND

0

5

10

15

20

25

2015 2020 2025 2030

Wind

CSP

UPV

ENERGY SAVINGS POTENTIAL ENERGY SAVINGS POTENTIAL

0

200

400

600

800

1000

1200

1400

1600

TB

TU

/Y

FUEL ENERGY SUPPLY & DEMAND - SAVINGS POTENTIAL

Building & AC Efficiency (including District Cooling )

Building applied PV

Resultant Demand

Domestic Gas

HFO

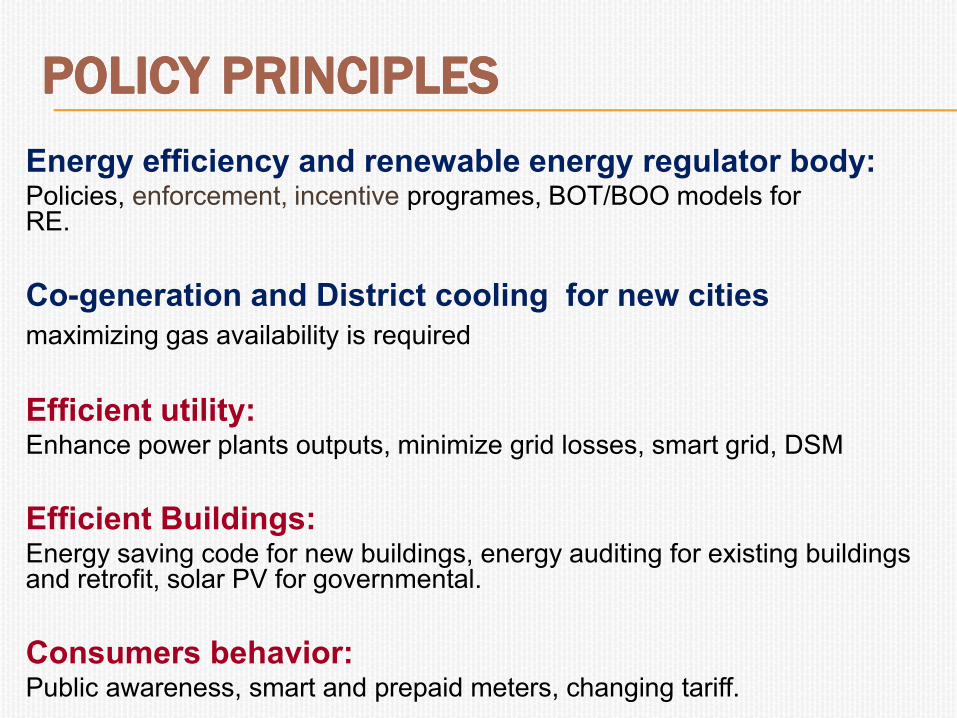

POLICY PRINCIPLESPOLICY PRINCIPLES

Energy efficiency and renewable energy regulator body: Policies, enforcement, incentive programes, BOT/BOO models for RE.

Co-generation and District cooling for new cities

maximizing gas availability is required

Efficient utility:Enhance power plants outputs, minimize grid losses, smart grid, DSM

Efficient Buildings:Energy saving code for new buildings, energy auditing for existing buildings and retrofit, solar PV for governmental.

Consumers behavior:.Public awareness, smart and prepaid meters, changing tariff

THANKSTHANKS

BACKUP BACKUP

FOR QUESTIONS

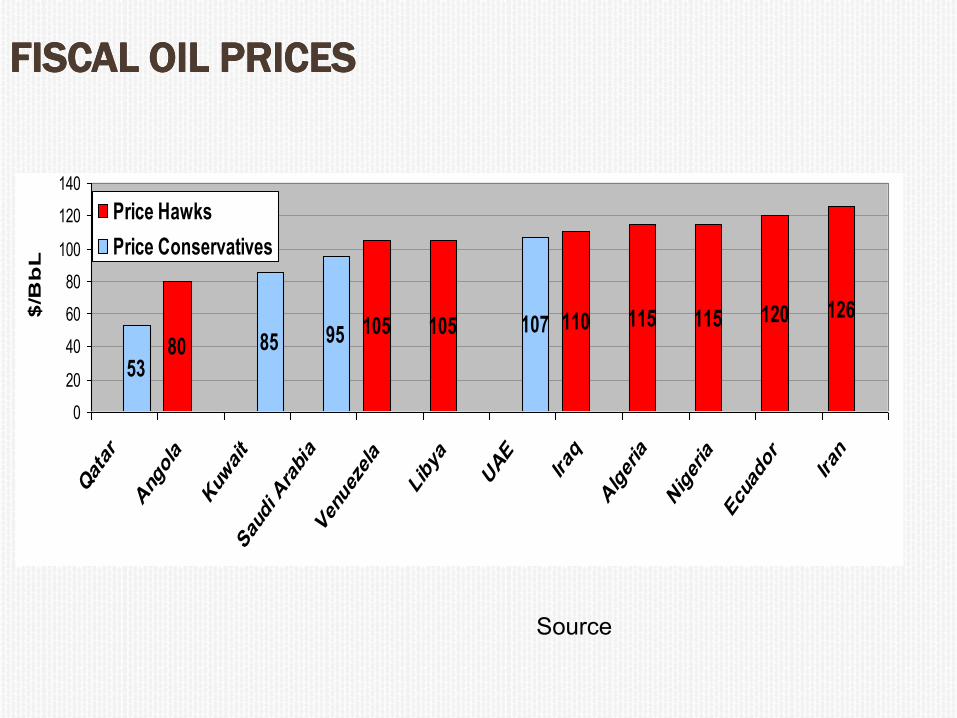

FISCAL OIL PRICESFISCAL OIL PRICES

Price HawksPrice Conservatives

Qatar 53

Angola 80

Kuwait 85

Saudi Arabia 95

Venuezela 105

Libya 105

UAE 107

Iraq 110

Algeria 115

Nigeria 115

Ecuador 120

Iran 126

Esimated Fiscal Oil Price

80105 105 110 115 115 120 126

5385

10795

0

20

40

60

80

100

120

140

Qatar

Ang

ola

Kuw

ait

Sau

di A

rabia

Ven

uez

ela

Libya

UAE

Iraq

Algeria

Nigeria

Ecu

ador

Iran

$/B

bL

Price Hawks

Price Conservatives

Source

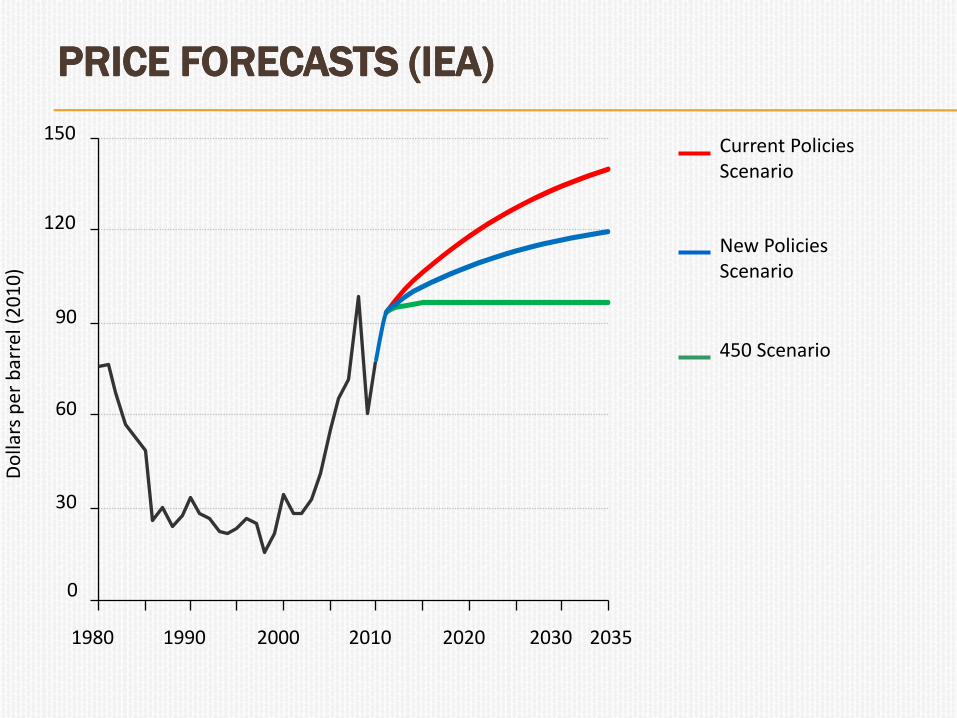

PRICE FORECASTS (IEA)PRICE FORECASTS (IEA)

Current PoliciesScenario

New Policies Scenario

450 Scenario

0

30

60

90

120

150

1980 1990 2000 2010 2020 2030 2035

Do

llars

per

bar

rel (

20

10

)

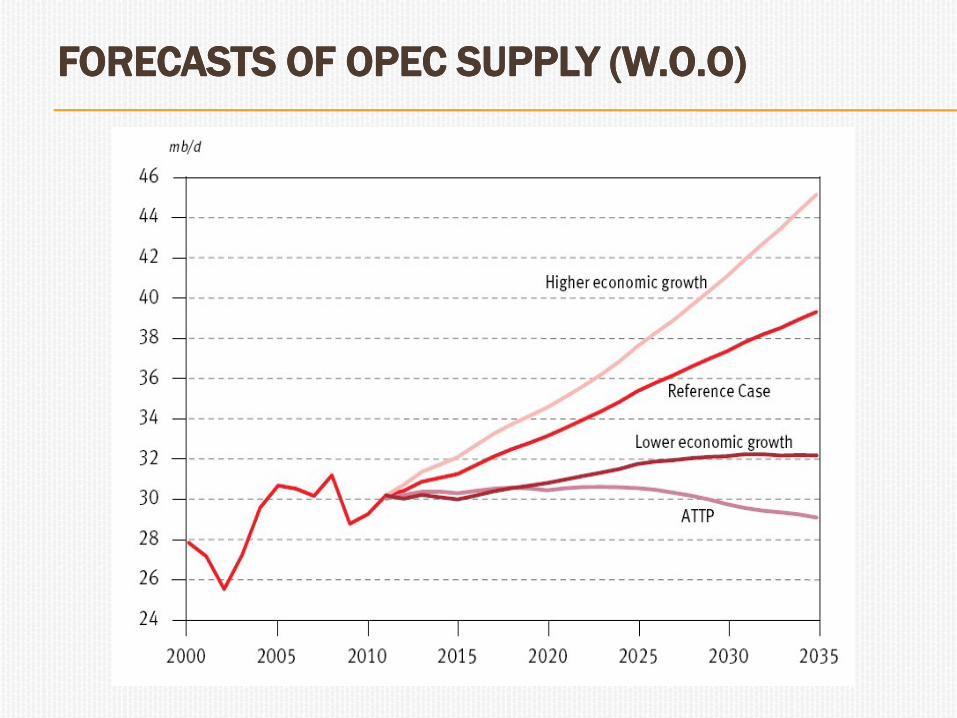

FORECASTS OF OPEC SUPPLY (W.O.O)FORECASTS OF OPEC SUPPLY (W.O.O)

ILLUSTRATION OF EFFECTS ON KUWAITILLUSTRATION OF EFFECTS ON KUWAIT

Production & Exports (MBls/day)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2013

2015

2017

2019

2021

2023

2025

2027

2029

KPC Planned Production

Domestic Consumption

(Petrochem & Transport)

Domestic Consumption

(Power & Water)

Exports with Reduced

Quota

Possible Reduced Quota

Due to Alternative Supplies

Exports @ Planned

Capacity

Fiscal Oil Price $/Bbl

80

100

120

140

160

180

200

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

KPC planned production

with sustainable energy

policy

Assumed OPEC Quota

Reduction

with sustainable energy

policy

Assumptions – quota restriction to 2.5 Mbls/day , 10% contribution to FGF

26

ACTION REQUIREDACTION REQUIRED

Economic and Industrial diversification particularly to petrochemical and new materials uses of oil

Minimise social employment & spending, increase private sector employment over complete jobs spectrum

Continued development of Oil resources to retain swing producer position.

Maximum refining to clean fuels to increase export value

Minimize Loss of Revenue due to Domestic Oil Consumption

Development of gas resources to substitute oil firing

NATIONAL SUSTAINABLE ENERGY POLICY

.

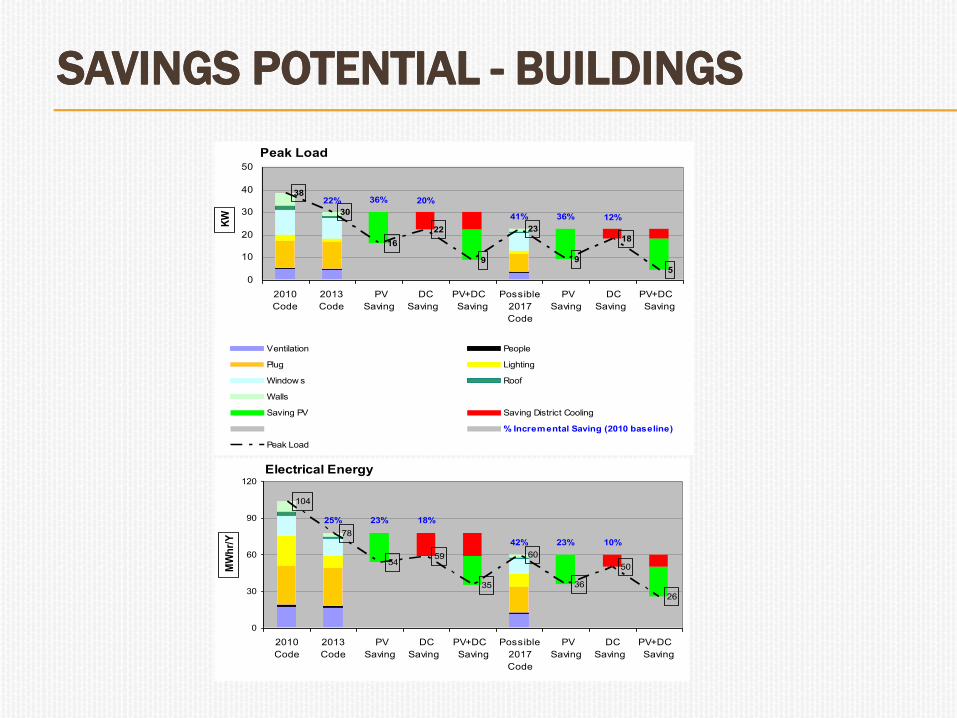

SAVINGS POTENTIAL SAVINGS POTENTIAL -- BUILDINGSBUILDINGS

Peak Load

22% 36% 20%

41% 36% 12%

38

30

16

22

9

23

9

18

5

0

10

20

30

40

50

2010

Code

2013

Code

PV

Saving

DC

Saving

PV+DC

Saving

Possible

2017

Code

PV

Saving

DC

Saving

PV+DC

Saving

KW

Ventilation People

Plug Lighting

Window s Roof

Walls

Saving PV Saving District Cooling

Series12 % Incremental Saving (2010 baseline)

Peak Load

Electrical Energy

25% 23%

42% 23% 10%

18%

104

78

5459

35

60

36

50

26

0

30

60

90

120

2010

Code

2013

Code

PV

Saving

DC

Saving

PV+DC

Saving

Possible

2017

Code

PV

Saving

DC

Saving

PV+DC

Saving

MW

hr/

Y

TARGETSTARGETS

To be the highest technically and economically justifiable.

To be periodically revised according to the technical and cost evolution of applicable measures

Setting and revision by the National Energy Council

Possible values are:

Building Energy Intensities Alternative Generation

2020 2030 2020 2030

New % Application 100 100 % Total 2 10

KWhr/M2/Y 160 130

Existing % Application 20 50

KWhr/M2/Y 200 160