mcgraw-hill/irwin © the mcgraw-hill companies, inc., 2005 18-1 acct 102 financial accounting...

TRANSCRIPT

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-1

ACCT 102

FinancialAccounting

Overview of F/S(Chap 1,2,3,4)

Cash Flows Statement(Chap 16)

Investing activities(Chap 10,15)

Operating activities(Chap 5,6,9,10,11)

Financing activities(Chap 13,14)

ManagementAccounting

Cost Accounting(Chap 18,19,20)

Cost-Volume-Profit Analysis(Chap 22)

Operating Budgets(Chap 23)

Capital Budgets(Chap 25)

Managerial Decision(Chap 25)

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-2

Managerial Accounting Concepts and Principles

Chapter

1818

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-3

Learning objectivesLearning objectives

1. Managerial Accounting Basics2. Managerial Cost Concepts3. Reporting Manufacturing Activities

• Balance Sheet• Income Statement• Flow of Manufacturing Activities• Manufacturing Statement

4. Decision analysis: • Unit Contribution Margin • Contribution Margin Ratio

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-4

Managerial accountingprovides informationfor managers of anorganization whoplan and controlits operations.

Financial accountingprovides information

to stockholders,creditors and others

who are outsidethe organization.

1. Managerial Accounting Basics - Purpose Managerial Accounting

1. Managerial Accounting Basics - Purpose Managerial Accounting

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-5

PlanningFormulating Long- and

Short-Term Plans

Controlling1. Measuring Actual

Performance

Implementing PlansDirecting

andMotivating

Controlling2. Evaluating ActualPerformance versus

Planned Performance

BeginF

EE

DBACK

MONI

TO

RIN

G

Planning and ControlPlanning and Control

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-6

Financial Accounting Managerial Accounting

1. Users Investors, creditors and Managers, employees and other external users other internal users

2. Purpose of Making investment, credit Planning, decision information and other decisions making and control

3. Flexibility Structured and often Relatively flexible of practice controlled by GAAP (no GAAP)

4. Timeliness of Often available only Available quickly without information after audit is complete need to wait for audit

5. Time dimension Historical information Many projections with some predictions and estimates

6. Focus of Emphasis on Projects, processes and information whole organization segments of an organization

7. Nature of Monetary Monetary and information information nonmonetary information

1. Managerial Accounting Basics - Nature of Managerial Accounting1. Managerial Accounting Basics - Nature of Managerial Accounting

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-7

1. Managerial Accounting Basics - Increased Relevance of Managerial Accounting

1. Managerial Accounting Basics - Increased Relevance of Managerial Accounting

Customer Orientation

GlobalEconomy

LeanBusiness

Model

Eliminationof Waste

Satisfy theCustomer

PositiveReturn

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-8

Lean PracticesLean Practices

CustomerOrientationin a GlobalEconomy

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-9

on

Quality throughoutthe production process.

Rewards for employeeswho find defects.

Employees encouragedto try new methodsto improve quality.

Company emphasizesvalue of quality through

quality awards.

Total Quality ManagementTotal Quality Management

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-10

Complete productsjust in time to

ship to customers.

Complete partsjust in time for

assembly into products.

Receive materialsjust in time for

production.

Scheduleproduction.

Receivecustomer

orders.

Just-In-Time (JIT) ManufacturingJust-In-Time (JIT) Manufacturing

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-11

New ways to improve

operations

Continuous ImprovementContinuous Improvement

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-12

LaborCosts

Variable Costs

Use ofTechnology Automation Overhead

FixedCosts

Increase

Decrease

1. Managerial Accounting Basics - Implications for Manufacturing Accounting

1. Managerial Accounting Basics - Implications for Manufacturing Accounting

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-13

Behavior

Traceability

Controllability

Relevance

Function

2. Managerial Cost Concept - Cost Classification2. Managerial Cost Concept - Cost Classification

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-14

Cost behavior means how a cost will react to changes in the level of business activity. Total fixed costs do

not change when activity changes.

Total variable costs change in proportionto activity changes.

Classification by BehaviorClassification by Behavior

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-15

Activity

Cos

t

Activity

Cos

tClassification by BehaviorClassification by Behavior

Cost behavior means how a cost will react to changes in the level of business activity. Total fixed costs do

not change when activity changes.

Total variable costs change in proportionto activity changes.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-16

Direct costs Costs incurred for the

benefit of one specific cost object.

Examples: material and labor cost for a product.

Indirect costs Costs incurred for the

benefit of more than one cost object.

Example: maintenance expenditures benefiting two or more departments.

Classification by TraceabilityClassification by Traceability

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-17

The degree of control depends on thelevel of management in the organization.

More C

ontrolM

ore

Con

trol

Very little control

Classification by ControllabilityClassification by Controllability

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-18

The potential benefit that is given up when one alternative is selected over another. Example: If you were

not attending college,you could be earning$20,000 per year. Your opportunity costof attending college for one year is $20,000.

Classification by Relevance: Opportunity CostsClassification by Relevance: Opportunity Costs

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-19

All costs incurred in the past that cannot be changed by any decision made now or in the future.

Sunk costs should not be considered in decisions.

Example: You bought an automobile that cost $15,000 two years ago. The $15,000 cost is sunk because whether you drive it, park it, trade it, or sell it, you cannot change the $15,000 cost.

Classification by Relevance:Sunk CostsClassification by Relevance:Sunk Costs

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-20

TheProduct

Classification by Function:Product CostsClassification by Function:Product Costs

DirectLabor

DirectMaterial

Manufacturing Overhead

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-21

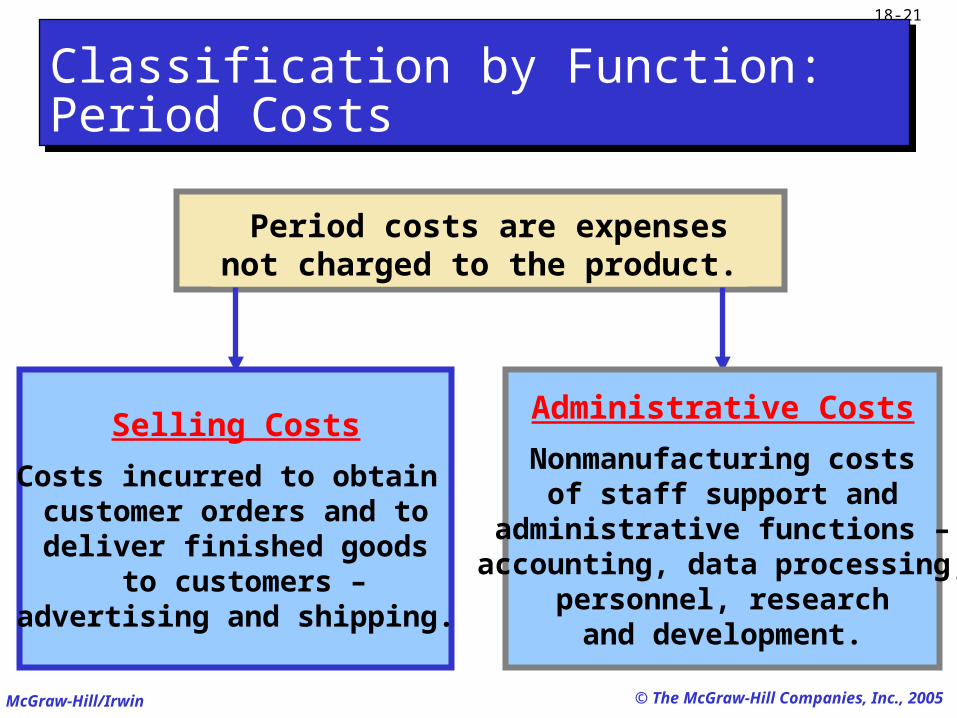

Period costs are expensesnot charged to the product.

Classification by Function:Period CostsClassification by Function:Period Costs

Administrative Costs

Nonmanufacturing costsof staff support and

administrative functions –accounting, data processing,

personnel, researchand development.

Selling Costs

Costs incurred to obtain customer orders and todeliver finished goods

to customers –advertising and shipping.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-22

Period Costs(Expenses)

Product Costs(Inventory)

Inventory Not Sold in 2005

OperatingExpenses

Cost ofGoods Sold

Raw MaterialsGoods in ProcessFinished Goods

Cost ofGoods Sold

2005 CostsIncurred

2005 IncomeStatement

2006 IncomeStatement

2005 BalanceSheet Inventory

InventorySold in 2005

Period and Product Costsin Financial StatementsPeriod and Product Costsin Financial Statements

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-23

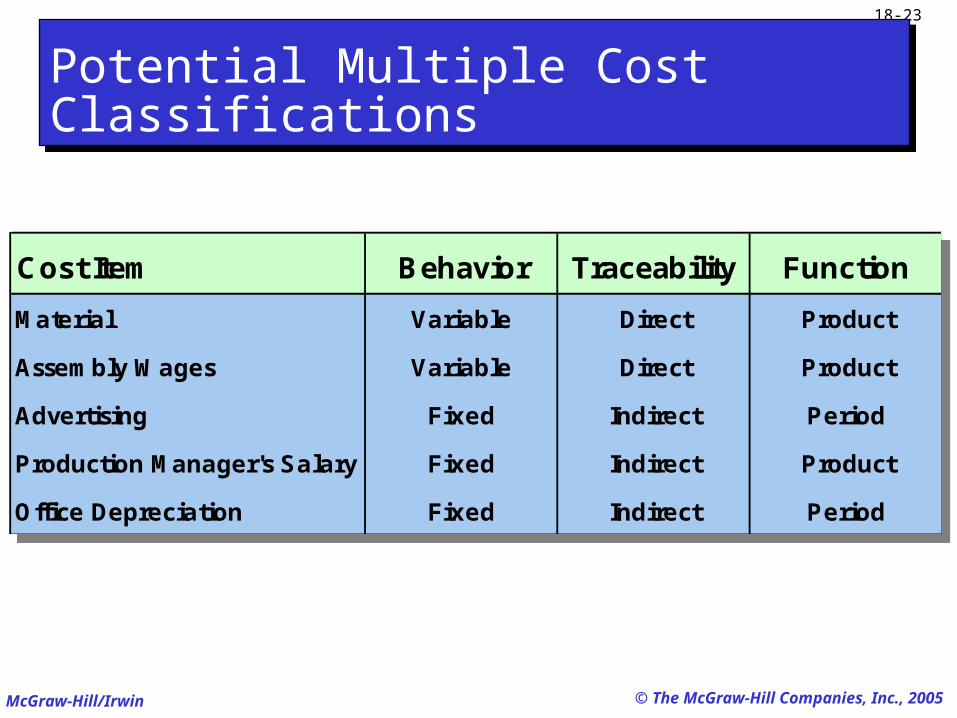

Cost Item Behavior Traceability Function

Material Variable Direct Product

Assembly Wages Variable Direct Product

Advertising Fixed Indirect Period

Production Manager's Salary Fixed Indirect Product

Office Depreciation Fixed Indirect Period

Cost Item Behavior Traceability Function

Material Variable Direct Product

Assembly Wages Variable Direct Product

Advertising Fixed Indirect Period

Production Manager's Salary Fixed Indirect Product

Office Depreciation Fixed Indirect Period

Potential Multiple Cost ClassificationsPotential Multiple Cost Classifications

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-24

I suppose these samecost concepts apply to

service companies.

Cost Concepts for Service CompaniesCost Concepts for Service Companies

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-25

Merchandisers . . .Buy finished goods.

Sell finished goods.

SaleMart

Manufacturers . . .Buy raw materials.

Produce and sell finished goods.

3. Reporting Manufacturing Activities3. Reporting Manufacturing Activities

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-26

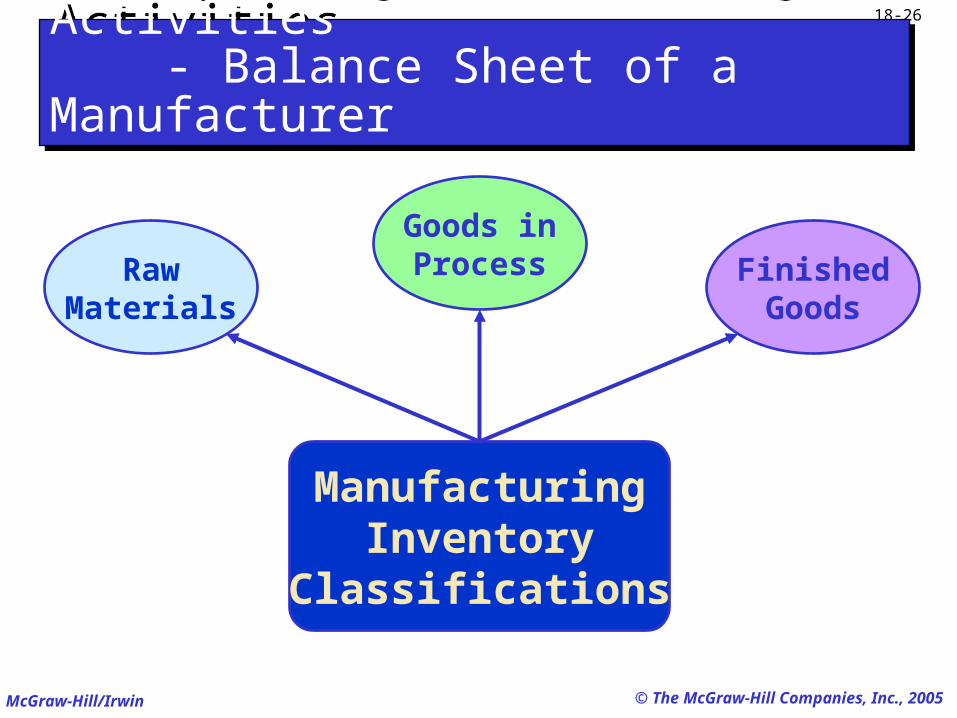

ManufacturingInventory

Classifications

3. Reporting Manufacturing Activities - Balance Sheet of a Manufacturer3. Reporting Manufacturing Activities - Balance Sheet of a Manufacturer

RawMaterials

FinishedGoods

Goods inProcess

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-27

Completedproductsfor sale.

Materialswaiting to beprocessed.

Partially completeproducts.

Material to whichsome labor and/or

overhead havebeen added.

Balance Sheet of a ManufacturerBalance Sheet of a Manufacturer

RawMaterials

FinishedGoods

Goods inProcess

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

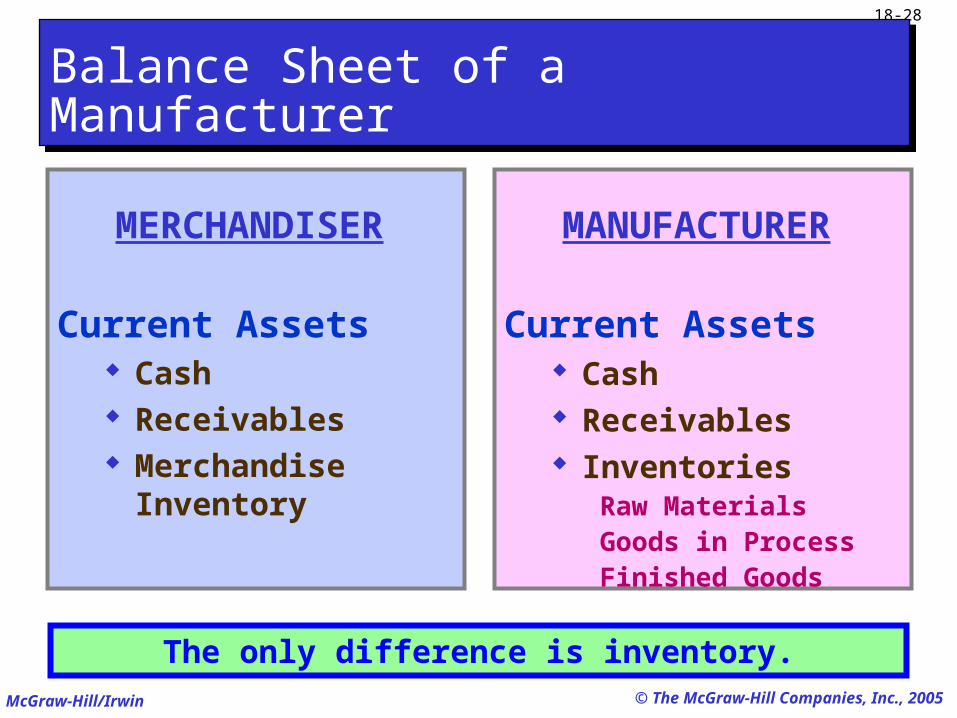

18-28

MERCHANDISER

Current Assets Cash Receivables Merchandise

Inventory

MANUFACTURER

Current Assets Cash Receivables Inventories

Raw MaterialsGoods in ProcessFinished Goods

The only difference is inventory.

Balance Sheet of a ManufacturerBalance Sheet of a Manufacturer

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-29

Beginning Merchandise

Inventory

Beginning Finished Goods

Inventory

Cost of Goods Purchased

Cost of GoodsManufactured

Ending Merchandise

Inventory

EndingFinished Goods

Inventory

Cost of Goods Sold

Merchandiser Manufacturer

+

_

+

==

_

The major difference

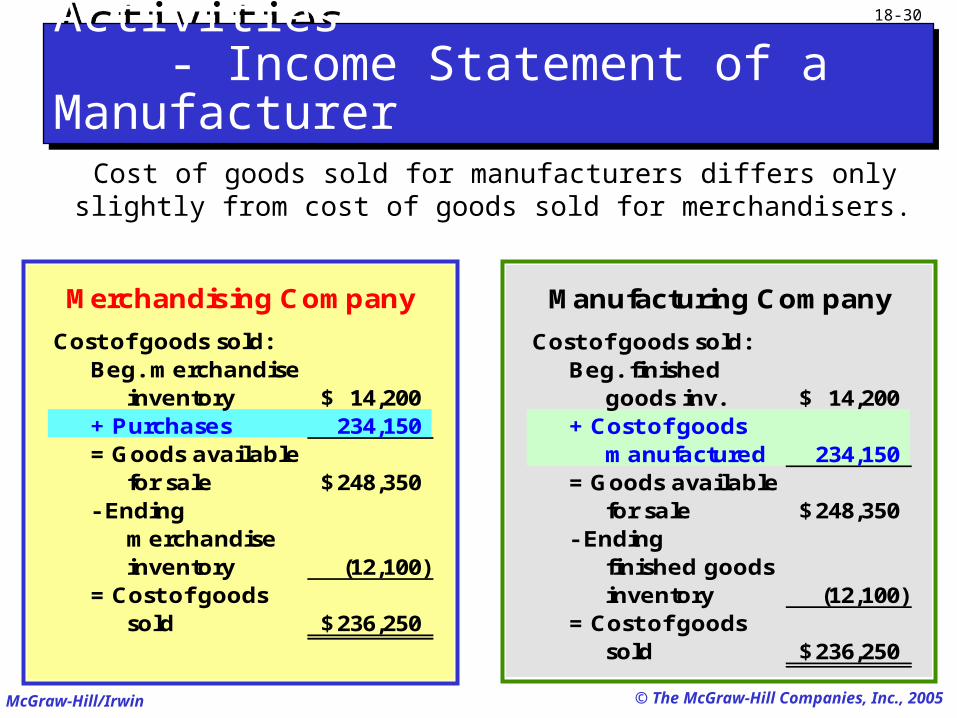

3. Reporting Manufacturing Activities - Income Statement of a Manufacturer3. Reporting Manufacturing Activities - Income Statement of a Manufacturer

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-30

Manufacturing Company

Cost of goods sold: Beg. finished goods inv. 14,200$ + Cost of goods manufactured 234,150 = Goods available for sale 248,350$ - Ending finished goods inventory (12,100) = Cost of goods sold 236,250$

Merchandising Company

Cost of goods sold: Beg. merchandise inventory 14,200$ + Purchases 234,150 = Goods available for sale 248,350$ - Ending merchandise inventory (12,100) = Cost of goods sold 236,250$

Cost of goods sold for manufacturers differs only slightly from cost of goods sold for merchandisers.

3. Reporting Manufacturing Activities - Income Statement of a Manufacturer3. Reporting Manufacturing Activities - Income Statement of a Manufacturer

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-31

Direct Materials

Materials that are clearly and easilyidentified with a particular product.

Direct Materials

Materials that are clearly and easilyidentified with a particular product.

Example:Steel used tomanufacture

the automobile.

Example:Steel used tomanufacture

the automobile.

Income Statement of a ManufacturerIncome Statement of a Manufacturer

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-32

Direct Labor

Labor costs that are clearly traceable to, or readily identifiable with, the

finished product.

Direct Labor

Labor costs that are clearly traceable to, or readily identifiable with, the

finished product.

Example:Wages paid to an

automobile assemblyworker.

Example:Wages paid to an

automobile assemblyworker.

Income Statement of a ManufacturerIncome Statement of a Manufacturer

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-33

Factory Overhead

All factory costs exceptdirect material and direct labor.

Factory costs that cannot betraced directly to specific units produced.

Factory Overhead

All factory costs exceptdirect material and direct labor.

Factory costs that cannot betraced directly to specific units produced.

Examples:Indirect labor – maintenance

Indirect material – cleaning suppliesFactory utility costsSupervisory costs

Income Statement of a ManufacturerIncome Statement of a Manufacturer

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

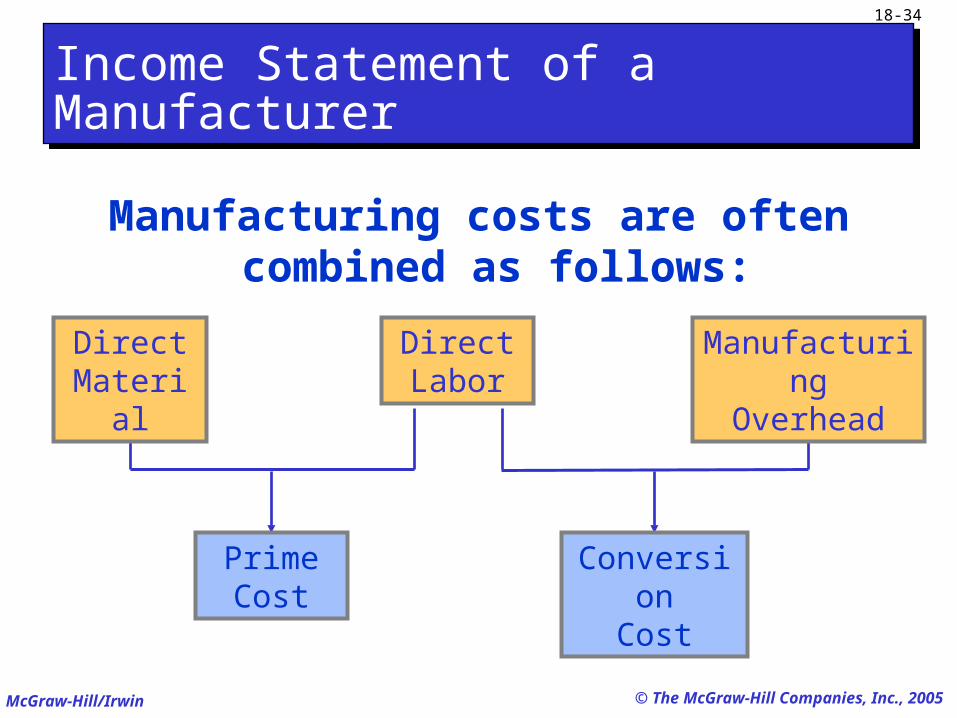

18-34

DirectMaterial

DirectLabor

ManufacturingOverhead

PrimeCost

ConversionCost

Manufacturing costs are oftencombined as follows:

Income Statement of a ManufacturerIncome Statement of a Manufacturer

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-35

QuestionQuestion

What type of account is the manufacturing goods in process account?

a. Income statement expense account.

b. Balance sheet inventory account.

c. Temporary clearing account for direct material and direct labor.

d. Holding account for manufacturing overhead and direct labor.

What type of account is the manufacturing goods in process account?

a. Income statement expense account.

b. Balance sheet inventory account.

c. Temporary clearing account for direct material and direct labor.

d. Holding account for manufacturing overhead and direct labor.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-36

What type of account is the manufacturing goods in process account?

a. Income statement expense account.

b. Balance sheet inventory account.

c. Temporary clearing account for direct material and direct labor.

d. Holding account for manufacturing overhead and direct labor.

What type of account is the manufacturing goods in process account?

a. Income statement expense account.

b. Balance sheet inventory account.

c. Temporary clearing account for direct material and direct labor.

d. Holding account for manufacturing overhead and direct labor.

Question

QuestionQuestion

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-37

QuestionQuestion

The primary distinction between product and period costs is . . .

a. Product costs are expensed in the period incurred.

b. Product costs are directly traceable to product units.

c. Product costs are inventoriable.

d. Period costs are inventoriable.

The primary distinction between product and period costs is . . .

a. Product costs are expensed in the period incurred.

b. Product costs are directly traceable to product units.

c. Product costs are inventoriable.

d. Period costs are inventoriable.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-38

The primary distinction between product and period costs is . . .

a. Product costs are expensed in the period incurred.

b. Product costs are directly traceable to product units.

c. Product costs are inventoriable.

d. Period costs are inventoriable.

The primary distinction between product and period costs is . . .

a. Product costs are expensed in the period incurred.

b. Product costs are directly traceable to product units.

c. Product costs are inventoriable.

d. Period costs are inventoriable.

Question

QuestionQuestion

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-39

Finished GoodsBeginning Inventory

Cost of GoodsManufactured

FinishedGoodsEnding

Inventory

RawMaterialsBeginningInventory

RawMaterials

Purchases

Raw MaterialsEnding Inventory

Costof

GoodsSold

Goods in ProcessBeginning Inventory

Direct Labor

FactoryOverhead

Raw MaterialsUsed

Sales activityProduction activityMaterialsactivity

3. Reporting Manufacturing Activities - Flow of Manufacturing Activities3. Reporting Manufacturing Activities - Flow of Manufacturing Activities

Goods in ProcessEnding Inventory

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-40

Cost of all goods completed and transferred from goods in process to finished goods during a

reporting period.

Direct Materials Used + Direct Labor + Factory Overhead = Total Manufacturing Costs + Beginning Work in Process – Ending Work in Process = Cost of Goods Manufactured

3. Reporting Manufacturing Activities - Manufacturing Statement3. Reporting Manufacturing Activities - Manufacturing Statement

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-41

Let’s take a look at Rocky

Mountain Bikes’ Manufacturing

Statement.

Manufacturing StatementManufacturing Statement

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-42

ROCKY MOUNTAIN BIKES

Manufacturing Statement

For Year Ended December 31, 2005

Direct materials used in production 85,500$

Direct labor 60,000

Total factory overhead costs 30,000

Total manufacturing costs for the period 175,500$

Add: Beginning goods in process inventory 2,500

Total cost of goods in process 178,000$

Deduct: Ending goods in process inventory 7,500

Cost of goods manufactured 170,500$

Manufacturing StatementManufacturing Statement

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-43

ROCKY MOUNTAIN BIKES

Manufacturing Statement

For Year Ended December 31, 2005

Direct materials used in production 85,500$

Direct labor 60,000

Total factory overhead costs 30,000

Total manufacturing costs for the period 175,500$

Add: Beginning goods in process inventory 2,500

Total cost of goods in process 178,000$

Deduct: Ending goods in process inventory 7,500

Cost of goods manufactured 170,500$

Manufacturing StatementManufacturing Statement Exh. 18-16

Computation of Cost of Direct Material Used

Beginning raw materials inventory 8,000$

Add: Purchases of raw materials 86,500

Cost of raw materials available for use 94,500$

Deduct: Ending raw materials inventory 9,000

Cost of direct materials used in production 85,500$

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-44

ROCKY MOUNTAIN BIKES

Manufacturing Statement

For Year Ended December 31, 2005

Direct materials used in production 85,500$

Direct labor 60,000

Total factory overhead costs 30,000

Total manufacturing costs for the period 175,500$

Add: Beginning goods in process inventory 2,500

Total cost of goods in process 178,000$

Deduct: Ending goods in process inventory 7,500

Cost of goods manufactured 170,500$

Include all direct labor costs incurred during the

current period.

Manufacturing StatementManufacturing Statement

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-45

ROCKY MOUNTAIN BIKES

Manufacturing Statement

For Year Ended December 31, 2005

Direct materials used in production 85,500$

Direct labor 60,000

Total factory overhead costs 30,000

Total manufacturing costs for the period 175,500$

Add: Beginning goods in process inventory 2,500

Total cost of goods in process 178,000$

Deduct: Ending goods in process inventory 7,500

Cost of goods manufactured 170,500$

Manufacturing StatementManufacturing Statement Exh. 18-16

Computation of Total Manufacturing Overhead

Indirect labor 9,000$

Factory supervision 6,000

Factory utilities 2,600

Property taxes, factory building 1,900

Factory supplies used 600

Factory insurance expired 1,100

Depreciation, building and equipment 5,300

Other factory overhead 3,500

Total factory overhead costs 30,000$

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

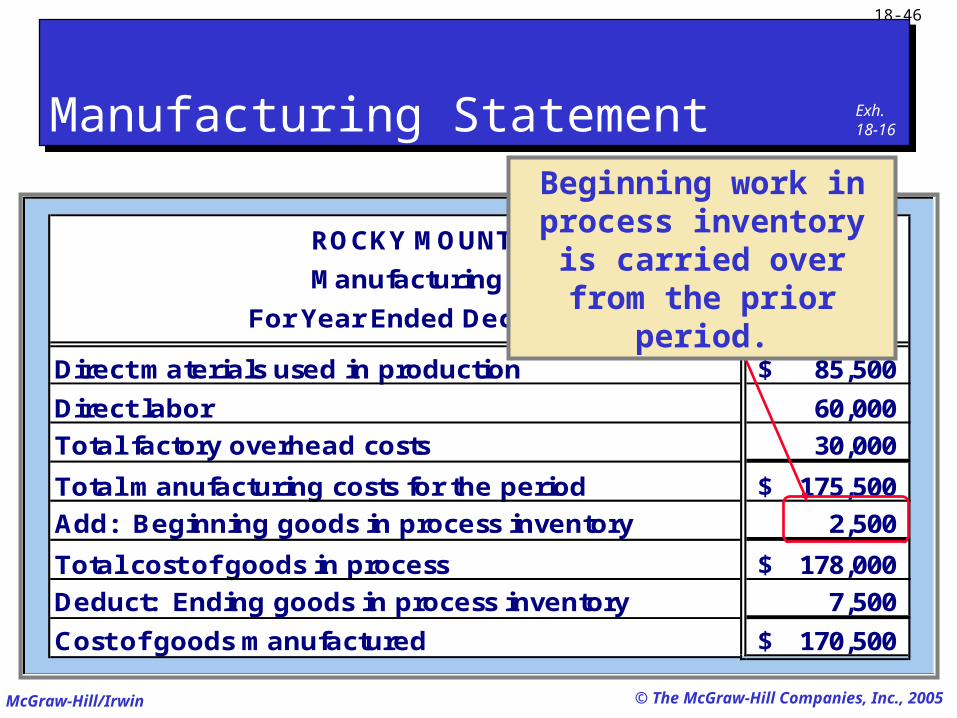

18-46

ROCKY MOUNTAIN BIKES

Manufacturing Statement

For Year Ended December 31, 2005

Direct materials used in production 85,500$

Direct labor 60,000

Total factory overhead costs 30,000

Total manufacturing costs for the period 175,500$

Add: Beginning goods in process inventory 2,500

Total cost of goods in process 178,000$

Deduct: Ending goods in process inventory 7,500

Cost of goods manufactured 170,500$

Beginning work in process inventory is carried over from the

prior period.

Manufacturing StatementManufacturing Statement Exh. 18-16

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-47

ROCKY MOUNTAIN BIKES

Manufacturing Statement

For Year Ended December 31, 2005

Direct materials used in production 85,500$

Direct labor 60,000

Total factory overhead costs 30,000

Total manufacturing costs for the period 175,500$

Add: Beginning goods in process inventory 2,500

Total cost of goods in process 178,000$

Deduct: Ending goods in process inventory 7,500

Cost of goods manufactured 170,500$

Ending work in process inventory contains the cost of unfinished

goods, and is reported in the current assets section of the balance sheet.

Manufacturing StatementManufacturing Statement Exh. 18-16

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-48

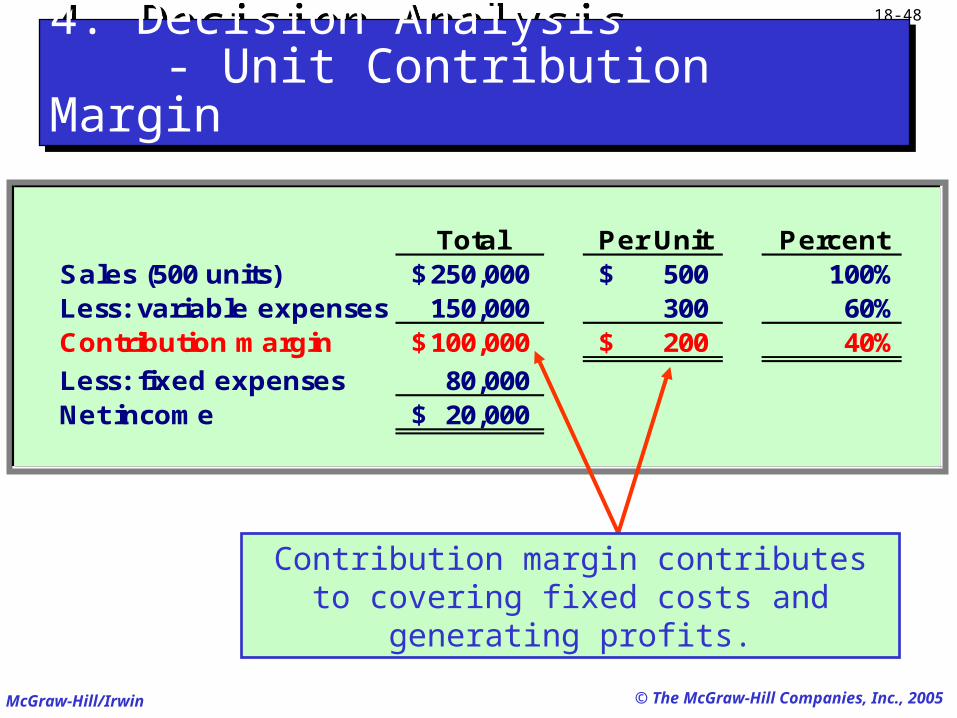

Total Per Unit PercentSales (500 units) 250,000$ 500$ 100%Less: variable expenses 150,000 300 60%Contribution margin 100,000$ 200$ 40%

Less: fixed expenses 80,000 Net income 20,000$

4. Decision Analysis - Unit Contribution Margin4. Decision Analysis - Unit Contribution Margin

Contribution margin contributes to covering fixed costs and generating profits.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-49

Unit Contribution MarginUnit Contribution Margin

Total Per Unit PercentSales (500 units) 250,000$ 500$ 100%Less: variable expenses 150,000 300 60%Contribution margin 100,000$ 200$ 40%

Less: fixed expenses 80,000 Net income 20,000$

Contribution margin ratio is the portion of each sales dollar remaining after deducting total unit variable cost.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005

18-50

End of Chapter 18End of Chapter 18