may 2014 journal of sustainable - cornerstone capital...

TRANSCRIPT

©Pakmor/CrystalGraphics

Journal of Sustainable Finance & BankingSM

May 2014

Global Sector Research Introducing the Global Sector Strategy … Financial Impediments to Job Creation by Start-Ups and Small Firms Michael Geraghty … p.17 and p.25

Valuation & Accounting Making the Case for Crowdfunding Rules Janet Pegg … p.33

Featured Editorial The Global Entreneurship Revolution Shelly Porges … p.35

The Work of an Entreprenuer: Dream Maker – Dream Killer David Lubin … p.37

Where Angels Fear to Tread…. Robert Lamb, Sadika Hameed … p.40

Regional Imperatives MingJian, Testing for Safe Quality Products in China James Feldkamp … p.42

“Exit Left:” A Reflection about VC Investing… Camillo Sicherle … p.44

Open Source Excellence Creating an Ecosystem of Entrepreneurship to Drive Business and Social Value Lauren Moore … p.46

Fans, Flavors and Failure: Innovation from Cow to Cone Jostein Solheim … p.48

Why Compliance Programs Work Like Pushing a Rope… Dan Ostergaard, Michael Fuerst … p.50

Enhanced Analytics Measurement Systems at the Product Level Kara Hurst … p.53

Where Should “Human Capital” Fit Laurie Bassi … p.56

Accelerating Impact Reimagining Impact, Reimagining ROI Bob Harrison, Bulbul Gupta … p.59

Sustainable Standout PIP’n Good Wendy Gordon … p.61

“I Bought the Farm!” Jennifer Grossman … p.65

CEOs Letter on Sustainable Finance & Banking

Erika Karp Founder and Chief Executive Officer of Cornerstone Capital Inc. and Former Head of Global Sector Research at UBS Investment Bank

This month in the Cornerstone Journal of Sustainable Finance & Banking (JSFB), global markets took comfort from easing tensions in the Ukraine, robust US growth dynamics, and the Chinese government’s stimulative intentions. Also, much attention has been paid to the leadership of the European Commission, and corporate M&A activities from GE and Siemen’s respective intent to win Alsthom’s power business, to Pfizer’s failed bid for AstraZeneca, where jobs and the value of intellectual property remain key aspects of negotiations. All the while, debates about the genesis and path of income inequality and corporate governance rage on. These latter issues bring us to a discussion of “legacy.” An important legacy is one of the greatest hopes of entrepreneurs. Entrepreneurs are the greatest hope for capitalism.

This month’s edition of the JSFB explores “Entrepreneurship” from many angles. We begin with our featured domain, “BuildTheLadder.net,” where we celebrate the creative, inspired, dauntless innovators and force-of-will they employ to leverage ideas and relationships toward a successful vision. Some of these leaders would agree with the great American poet Maya Angelou, who passed away this week. In an extraordinary life of lending inspiration to others, Angelou stated that “People will forget what you said, and people will forget what you did, but people will never forget how you made them feel." As this group of entrepreneurs share the feelings they’ve experienced along their journeys, we applaud their efforts as the economy’s single best source of job creation.

Further this month, Cornerstone Capital’s Global Markets Strategist Michael Geraghty takes a more granular look at “Financial Impediments to Job Creation by Start-ups and Small Firms.” This snapshot of bank lending and the IPO market reminds us of the importance of policy efforts, such as the JOBS Act. Janet Pegg, our Head of Valuation & Acccounting, walks us further through this law in “Making the Case for Crowd Funding Rules.” As the SEC eyes this “evolving method to raise money via the internet,” we note the challenges and necessities in validating crowd funding as a viable investment and capital formation tool with transparent and understandable risks.

This month we also introduce the Cornerstone Capital Global Sector Strategy Model where Michael Geraghty ranks the 10 GICS in the MSCI All Country World Index employing our quantitative multi-factor methodology. We generate sector recommendations using our proprietary measures of valuation and earnings (momentum, revisions and margins), while weaving in considerations of Environmental, Social and Governance metrics. While we are expecting our model and processes to evolve, our conscious consideration of the most material ESG factors by sector offers another lens by which to analyze our allocations. Currently, we take a somewhat pro-cyclical stance of being overweight in the Information Technology and Consumer Discretionary sectors, and underweight in Consumer Staples and Materials.

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 2

As Michael notes, the extent to which a weighting in the Materials sector needs to coincide with a Regional Strategy call, we turn to our “Regional Imperatives” section with two entrepreneurial perspectives from China and Brazil offering insights that can be applied globally. James Feldkamp demonstrates that necessity is indeed the mother of invention in the mission of “MingJian: Testing for Safe Quality Products in China,” and Camillo Sicherle in Brazil addresses a structural question of financing new businesses in “Exit Left: A Reflection about VC Investing” -- a mindset that can, at times, undermine the highest purposes of entrepreneurship and capitalism.

In “Open Source Excellence,” we feature three of the world’s leading companies working to articulate a vision for private sector excellence. Lauren Moore of eBay discusses “Creating an Ecosystem of Entrepreneurship to Drive Business and Social Value.” Jostein Solheim of Ben & Jerry’s talks about “Fans, Flavors and Failure: Innovation from Cow to Cone.” And Michael Fuerst of Novartis with Dan Ostergaard of Integrity by Design stress that when “Building a Culture of Integrity” traditional compliance can only go so far. Rather, what is critical from the outset are clear expectations and widespread awareness combined with checks and balances.

Digging deeper into this month’s theme of Entrepreneurship, we learn from expert perspectives across disciplines. In “The Other Revolution,” Shelly Porges showcases the extraordinary prospects for unleashing human potential at a time when “Talent is universal, but opportunity is not” (as stated by Hillary Clinton.) David Lubin brings his years of experience and valuable pragmatic frameworks for success to herald “The Work of an Entrepreneur: Dream Maker – Dream Killer.” And finally, Bob Lamb and Sadika Hameed suggest we can find lessons in surprising places “Where Angels Fear to Tread, Entrepreneurs Rush in – But Investors Usually Don’t.”

Investors do need a world of “Enhanced Analytics” and here we look to Kara Hurst, who argues that sustainable investors are “Going Deep: Seeking Measurement Systems at the Product Level,” while Dr. Laurie Bassi asks “When Should “Human Capital” Fit into the Sustainability Agenda?” In both cases, we find a more robust understanding of the true “food chain” of the capital markets. Finally, this month, we feature “Sustainable Standouts” in the world of social entrepreneurship (3P Partners and FarmCo New York), a summary of the outstanding 2014 Ceres Annual Conference, a review of sustainable eyeglass maker Warby Parker, and a call-to-action from the Clinton Global Initiative that drives explicit commitments for those who wish to “Accelerate Impact” throughout the global capital markets.

My sincere regards, Erika

Erika Karp Chief Executive Officer

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 3

Table of Contents

CEOs Letter on Sustainable Finance and Banking p. 2

Market Summary Overview Market & Global Sector Performance, Monetary Policy & ESG Data

p. 6p. 7

Featured Domain BuildTheLadder.net Erika Karp CEO & Founder,

Cornerstone Capital p.15

Global Sector Strategy Introducing the Cornerstone Capital Sector Strategy Michael Geraghty Global Markets Strategist,

Cornerstone Capital Inc. p.17

The Cornerstone Global Regional Strategy Update Michael Geraghty Global Markets Strategist, Cornerstone Capital Inc.

p.23

Financial Impediments to Job Creation by Start-Ups and Small Firms

Michael Geraghty Global Markets Strategist, Cornerstone Capital Inc.

p.25

Corporate Governance Insights Good Governance: A Cornerstone of Entrepreneurism

Follow the Leader? Follow the Money Sustainable Entrepreneurship in Banking — The Equator Principles

John Wilson

Cindy Motz, CFA

Head of Corporate Governance, Engagement & Research, Cornerstone

Capital Inc.

Independent Research Analyst & Global Advisory Council Member to Cornerstone Capital Inc.

p.29

p.31

Valuation & Accounting Making the Case for Crowdfunding Rules Janet Pegg, CPA Head of Valuation &

Accounting, Cornerstone Capital Inc.

p.33

Featured Editorial The Other Revolution: The Global Entrepreneurship Revolution

The Work of an Entrepreneur: Dream Maker – Dream Killer

Where Angels Fear to Tread: Entrepreneurs Rush In, But Investors Don’t

Shelly Porges

David Lubin

Robert D. Lamb

Sadika Hameed

Global Entrepreneurship Advocate

Managing Director of S3

Senior Fellow & Director for Program on Crisis,

Conflict and Cooperation, CSIS

Fellow, Program on Crisis, Conflict and Cooperation,

CSIS

p.35

p.37

p.40

Regional Imperatives MingJian, Testing for Safe Quality Products in China

“Exit Left:” A Reflection about VC Investing & Entrepreneurship

James Feldkamp

Camillo Sicherle

Co-Founder and CEO, MingJian

Attorney, São Paulo, Brazil

p.42

p.44

Open Source Excellence Creating an Ecosystem of Entreneurship to Drive Business and Social Value

Lauren Moore Head of Global Social Innovation, eBay Inc.

p.46

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 4

Fans, Flavors and Failure: Innovation from Cow to Cone

Why Compliance Programs Work Like Pushing a Rope and How Leaders Can Impact Behaviour

Jostein Solheim

Dan Ostergaard

Dr. Michael Fuerst

CEO, Ben & Jerry’s, a Unilever

Company

Managing Partner, Integrity by Design

Senior Manager, Novartis

p.48

p.50

Enhanced Analytics Going Deep: Measurement Systems at the Product Level

When Should “Human Capital” Fit in the Sustainability Agenda?

Kara Hurst

Dr. Laurie Bassi

CEO, The Sustainability Consortium

CEO, McBassi & Company

p.53

p.56

Accelerating Impact Reimagining Impact, Reimagining ROI Bob Harrison

Bulbul Gupta

CEO, Clinton Global Initiative

Head of Market-Based Approaches, Clinton

Global Initiatives

p.59

Sustainable Standout PIP’n Good Wendy Gordon Co-Founder and CEO, 3P

Partners p.61

“I Bought the Farm!” Jennifer Grossman Founder & President, FarmCo New York

p.65

Sustainable Product Review Warby Parker Michael Shavel, CFA Research & Business

Analyst, Cornerstone Capital Inc.

p.68

Virtual Attendance Ceres Conference 2014 Tanya Khotin Head of Institutional

Business Development, Cornerstone Capital Inc.

p.71

Upcoming Events Global ESG Calendar p.72

Journal of Sustainable Finance & Banking Subscription Form Articles Cornerstone Capital Team

p.73

p.75p.76

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 5

Market Summary

Overview

With earnings season in the rear-view mirror, the global investment narrative remains largely unchanged and most of the major indices are up modestly for the year. Volatility has remained subdued, though there has been more movement under the surface as we’ve witnessed rotation out of growth and into value stocks. This has not coincided with a rotation into defensive sectors, however, implying that investors remain encouraged by economic data and are optimistic on global growth.

In the U.S., economic data is rebounding from the “winter slump” and investors are pushing the Dow Jones and S&P 500 to fresh highs. The Institute for Supply Management’s (ISM) Index rose to 54.9 from 53.7 and the employment component posted a strong gain as well. On the employment front, the closely followed BLS Employment report showed a better-than-expected 288k jobs added in April, bringing the unemployment rate down to 6.3%. After plodding along at uninspiring rate since the GFC, corporate sentiment seems to be on the mend as M&A activity is grabbing headlines and companies are increasing capital expenditure plans. The optimism isn’t contained to large companies; the NFIB small business confidence index is breaking to a new cycle high as well. Despite the positive economic data, the action in the bond market has been counter-intuitive with the 10-year Treasury yield declining. We have seen a few plausible explanations for this, but it is deservedly being closely monitored.

Elsewhere abroad, other developed markets are presenting investors with varying degrees of positive news – though not enough to stave off political routs in fresh elections across the continent. The economic recovery in the UK is well entrenched with employment growing faster than expected and spare capacity falling. The recovery in the Euro zone has been more subdued with GDP growth disappointing (except Germany) and inflation, although slightly improved, remaining precariously low. In Japan, buying ahead of the consumption tax increase in April lifted annualized GDP to a higher than expected 5.9%,

though this effect is likely to dampen economic growth in the second quarter.

Turning to emerging markets, China continues to attract investors’ attention, particularly as it pertains to the slowdown in their property market where sales (by volume) declined 19% vs. the prior year. Still, industrial production and retail sales jumped 8.7% YoY and 11.9% YoY in April, respectively, indicating that the slowdown isn’t reverberating throughout the economy. Meanwhile, Indian markets have outperformed on the overwhelming victory for the Bharatiya Janata Party (BJP) and in hope of economic reforms. In a rally also related to politics, Brazilian investors cheered early polls showing declining voter support for incumbent President Dilma Rouseff.

On a one-month trailing basis, the MSCI Emerging Markets index outperformed the MSCI World index (developed market proxy) by approximately 1.7%, and now are outperforming on a year-to-date basis by about 75 basis points. In a continuation of the more recent trend of underperformance, small cap equities trailed their large cap counterparts by a considerable 4.4% over the last month, bringing YTD underperformance to about 7%. From a sector perspective, performance was mixed between cyclicals and defensives. In the MSCI ACWI (broad index for both developed and emerging equities), energy and consumer staples outperformed while consumer discretionary and industrials lagged.

With first quarter earnings season nearing an end, approximately 75% of S&P 500 companies posted a positive earnings surprise, in line with the prior quarter's results. Topline results weren't as impressive, with only 53% reporting a positive sales surprise relative to 61% in the prior quarter. The technology sector had the highest percentage of earnings beats at 86%, while the energy, industrials and utilities sectors also saw over 80% of their constituents beating earnings estimates. Conversely, telecom and consumer staples delivered weaker results, with only 60% of the companies beating earnings estimates.

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 6

Market Summary

Market and Global Sector Performance

MARKET / INDEX PERFORMANCE As of 5/22/14 (local currency) T1M (%) T3M (%) YTD (%) 2014E P/E 2014E P/B Div. Yield

US Equity Indices

DJIA 0.50 3.33 0.79 14.8 2.7 2.3

S&P 500 0.93 3.60 3.25 16.0 2.5 2.1

Nasdaq 0.01 -2.25 -0.02 20.5 3.2 1.2

Russell 2000 -3.50 -4.00 -3.83 25.4 1.9 1.3

Developed International Indices

Euro STOXX 50 3.89 3.94 4.99 14.4 1.5 3.6

FTSE 100 2.71 1.09 2.94 14.1 1.9 3.7

CAC 40 1.53 4.14 6.23 15.1 1.5 3.2

DAX 1.26 0.66 1.77 13.5 1.7 2.9

Nikkei 225 -0.35 -2.76 -11.27 16.2 1.4 1.8

ASX 200 0.62 2.34 4.35 15.4 2.0 4.4

Emerging Market Indices

IBOVESPA 1.60 11.45 2.52 10.8 1.3 4.1

Shanghai Comp -2.36 -4.24 -3.50 8.0 1.1 3.7

KOSPI 0.57 2.95 0.22 10.9 1.1 1.2

SENSEX 7.20 17.93 15.50 15.4 2.5 1.7

Global Market Indices

MSCI World 0.73 2.63 2.84 15.4 2.0 2.6

MSCI All-Country World 0.92 3.20 2.92 14.8 1.9 2.6

MSCI EAFE 0.77 1.77 2.49 14.5 1.6 3.3

MSCI Emerging Markets 2.47 8.17 3.60 11.1 1.4 2.9

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 7

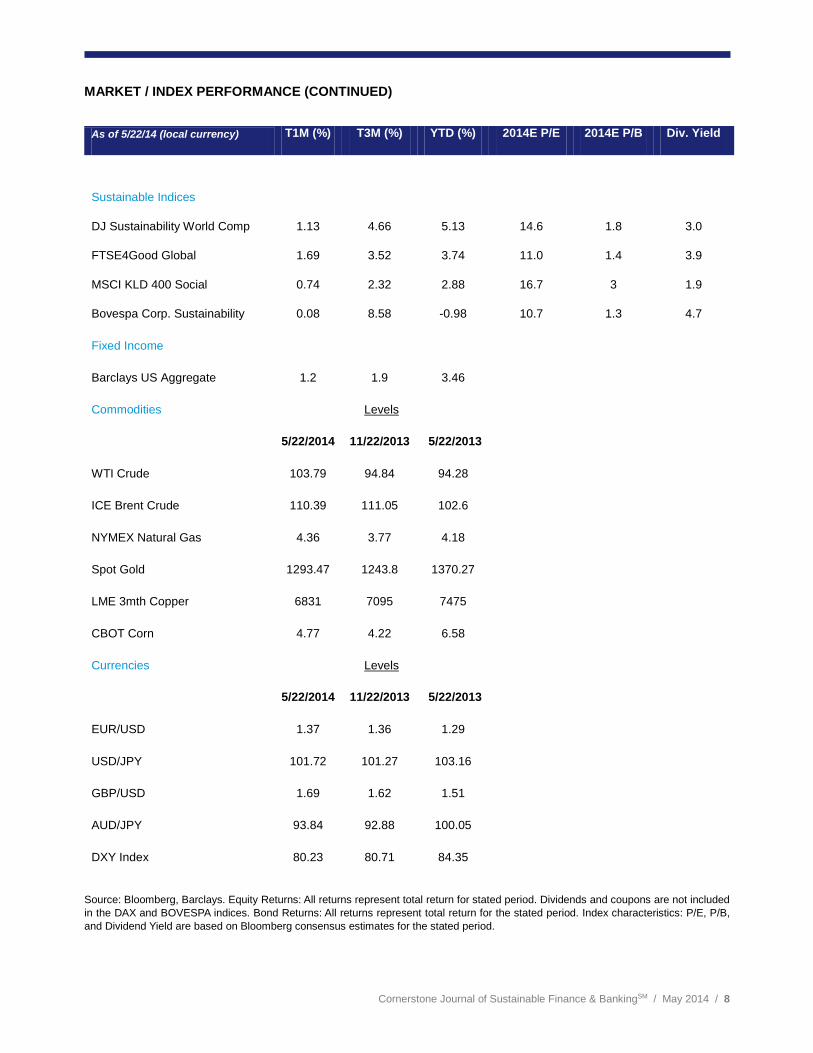

MARKET / INDEX PERFORMANCE (CONTINUED)

As of 5/22/14 (local currency) T1M (%) T3M (%) YTD (%) 2014E P/E 2014E P/B Div. Yield

Sustainable Indices

DJ Sustainability World Comp 1.13 4.66 5.13 14.6 1.8 3.0

FTSE4Good Global 1.69 3.52 3.74 11.0 1.4 3.9

MSCI KLD 400 Social 0.74 2.32 2.88 16.7 3 1.9

Bovespa Corp. Sustainability 0.08 8.58 -0.98 10.7 1.3 4.7

Fixed Income

Barclays US Aggregate 1.2 1.9 3.46

Commodities Levels

5/22/2014 11/22/2013 5/22/2013

WTI Crude 103.79 94.84 94.28

ICE Brent Crude 110.39 111.05 102.6

NYMEX Natural Gas 4.36 3.77 4.18

Spot Gold 1293.47 1243.8 1370.27

LME 3mth Copper 6831 7095 7475

CBOT Corn 4.77 4.22 6.58

Currencies Levels

5/22/2014 11/22/2013 5/22/2013

EUR/USD 1.37 1.36 1.29

USD/JPY 101.72 101.27 103.16

GBP/USD 1.69 1.62 1.51

AUD/JPY 93.84 92.88 100.05

DXY Index 80.23 80.71 84.35

Source: Bloomberg, Barclays. Equity Returns: All returns represent total return for stated period. Dividends and coupons are not included in the DAX and BOVESPA indices. Bond Returns: All returns represent total return for the stated period. Index characteristics: P/E, P/B, and Dividend Yield are based on Bloomberg consensus estimates for the stated period.

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 8

MSCI ACWI SECTOR PERFORMANCE

as of 5/21/14

1 Month Price Return (%)

Source: Bloomberg. Sector returns are based on GICS methodology. MSCI ACWI is a free-float weighted equity index that includes both emerging and developed world markets.

YTD Price Return (%)

Source: Bloomberg. Sector returns are based on GICS methodology. MSCI ACWI is a free-float weighted equity index that includes both emerging and developed world markets.

U.S. EQUITY STYLE PERFORMANCE

Style box returns are based on Russell Indices with the exception of the Large-Cap Blend box, which reflects the S&P 500 Index. All values are cumulative total return for the stated period including the reinvestment of dividends. The index used from left to right, top to bottom are: Russell 1000 Value Index, S&P 500 Index, Russell 1000 Growth Index, Russell Midcap Value Index, Russell Midcap Index, Russell Midcap Growth Index, Russell 2000 Value Index, Russell 2000 Index and Russell 2000 Growth Index.

1 Month

Source: Bloomberg

Year to Date

Source: Bloomberg

Value Growth Blend

0.5

-3.1

0.1

0.9

-3.5

0.1

1.0

-3.9

0.0 Mid

La

rge

Smal

l

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 9

SECTOR SNAPSHOT – TOP 5 COMPANIES BY MARKET CAP as of 5/22/14

Company Name Ticker Industry

Mkt Cap (US$ Bn)

Price (Local)

Total Return YTD % (local)

P/E 2014E

EV/EBITDA 2014E

Div Yield % 2014E

Consumer Disc. Toyota Motor Corp 7203.JP Automobiles 187.2 5526.00 -12.4 8.9 8.9 3.0 The Walt Disney Co DIS Media 142.9 82.52 8.0 19.8 11.3 1.0 Amazon AMZN Internet & Catalog

Retail 140.3 304.91 -23.5 88.8 20.9 N/A

Comcast Corp CMCSA Media 134.3 51.73 0.0 17.7 7.8 1.7 Volkswagen VOW3.GR Automobiles 120.6 190.85 -4.5 8.7 7.4 2.1 Consumer Staples Nestle NESN.VX Food Products 253.4 70.30 11.1 20.2 13.7 3.1 Wal-Mart Stores WMT Food & Staples

Retailing 243.3 75.39 -3.0 14.5 8.0 2.5

Procter & Gamble PG Household Products 218.1 80.60 0.6 19.2 12.7 3.2 The Coca-Cola Co KO Beverages 178.4 40.58 -1.0 19.5 14.9 3.0 Anheuser-Busch Inbev ABI.BB Beverages 178.1 81.13 7.0 21.0 11.7 3.6 Energy Exxon Mobil XOM Oil, Gas & Consumable

Fuels 436.5 101.65 1.8 13.1 6.0 2.7

Royal Dutch Shell RDSA.LN Oil, Gas & Consumable Fuels

258.3 2368.50 12.2 11.0 4.9 4.7

Chevron Corp CVX Oil, Gas & Consumable Fuels

235.6 123.76 0.8 11.5 4.6 3.5

Petrochina Co 857.HK Oil, Gas & Consumable Fuels

224.2 9.47 11.4 10.5 5.3 4.2

Total SA FP.FP Oil, Gas & Consumable Fuels

169.0 52.05 18.4 10.9 3.5 4.6

Financials Berkshire Hathaway- CL B

BRK/B Diversified Financial Services

313.2 127.01 7.1 19.2 N/A N/A

Wells Fargo & Co WFC Banks 263.4 50.01 11.7 12.2 N/A 2.8 JPMorgan Chase JPM Banks 206.6 54.58 -5.5 10.0 N/A 2.9

Ind & Comm Bank of China

1398.HK Banks 204.2 4.97 -5.2 5.1 N/A 6.5

HSBC Holdings HSBA.LN Banks 198.0 616.10 -4.3 11.1 N/A 5.4

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 10

SECTOR SNAPSHOT – TOP 5 COMPANIES BY MARKET CAP (CONTINUED) as of 5/22/14

Company Name Ticker Industry

Mkt Cap (US$ Bn)

Price (Local)

Total Return YTD % (local)

P/E 2014E

EV/EBITDA 2014E

Div Yield % 2014E

Health Care

Johnson & Johnson JNJ Pharmaceuticals 285.2 100.80 11.6 17.1 10.9 2.8

Roche Holdings ROG.VX Pharmaceuticals 258.2 268.50 10.9 17.9 12.0 2.9

Novartis AG NOVN.VX Pharmaceuticals 243.2 80.40 16.7 17.0 15.2 3.0

Pfizer PFE Pharmaceuticals 189.5 29.75 -1.2 13.3 8.3 3.5

Merck & Co MRK Pharmaceuticals 165.2 56.52 13.8 16.3 10.9 3.1

Industrials

General Electric Co GE Industrial Conglomerates

266.4 26.57 -4.4 15.7 12.3 3.3

Siemens AG SIE.GR Industrial Conglomerates

114.4 95.15 -1.1 14.4 9.6 3.2

United Technologies UTX Aerospace & Defense 105.6 115.16 2.2 16.8 10.1 2.0

The Boeing Co BA Aerospace & Defense 96.3 132.11 -2.1 17.9 10.0 2.2

UPS UPS Air Freight & Logistics 93.5 101.66 -1.9 20.0 10.3 2.6

Info Tech

Apple AAPL Technology Hardware, Storage &

524.0 608.33 9.7 13.8 6.5 2.2

Google GOOGL Internet Software & Services

370.9 555.45 -1.0 20.8 12.1 N/A

Microsoft Corp MSFT Software 332.0 40.19 9.0 14.9 8.3 2.8

Samsung Electronics 005930.KS Semiconductors & Semiconductor

204.9 1426000.00 3.9 N/A 3.3 1.0

IBM IBM IT Services 187.9 186 0.1 10.4 8.3 2.4

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 11

SECTOR SNAPSHOT – TOP 5 COMPANIES BY MARKET CAP (CONTINUED)

as of 5/22/14

Company Name Ticker Country Industry Mkt Cap (US$ Bn)

Price (Local)

Total Return YTD % (local)

P/E 2013E

EV/EBITDA 2013E

Div Yield % 2013E

Telecom

Verizon Communications VZ Diversified Telecommunication

204.8 49.45 2.8 14.0 6.9 4.3

China Mobile 941.HK Wireless Telecommunication Ser

203.7 78.00 -3.0 12.0 3.7 4.2

AT&T T Diversified Telecommunication

183.6 35.38 3.3 13.1 6.0 5.2

Vodafone Group VOD.LN Wireless Telecommunication Ser

91.0 204.15 -20.8 24.0 5.5 6.0

Softbank Corp 9984.JP Wireless Telecommunication Ser

82.6 7004.00 -23.7 18.3 7.6 0.6

Utilities

EDF EDF.FP Electric Utilities 69.3 27.31 6.3 13.4 5.4 4.6

GDF Suez GSZ.FP Multi-Utilities 66.9 20.31 23.2 14.9 6.8 5.8

National Grid NG/ LN Multi-Utilities 55.5 881.00 11.8 16.0 10.0 5.3

Enel SpA ENEL.IM Electric Utilities 50.9 3.96 24.9 12.6 6.7 3.3

Duke Energy DUK Electric Utilities 49.9 70.52 4.4 15.4 10.3 4.4

Source: Bloomberg. The securities in each sector represent the largest companies by market cap in the MSCI ACWI in their respective sectors. Sector classification is based on GICS methodology. Equity characteristics: P/E, EV/EBITDA and Dividend Yield are based on Bloomberg consensus estimates for stated period.

GDP / CONSUMER PRICE INFLATION / RATES

Source: Bloomberg. Estimates are composite of Bloomberg contributor estimates. *Italicized text represents actual data.** India fiscal year runs to March 31. Therefore, 2013E is India's FY13 GDP.

Region/Countries 2013E 2014E 2015E 2013E 2014E 2015E 2013E 2014E 2015E 2013E 2014E 2015EUnited States 1.9 2.5 3.1 1.5 1.7 2.1 0.25 0.25 - 3.0 3.2 -Euro Area -0.4 1.1 1.5 1.3 0.8 1.3 0.25 0.10 - 1.9 - -Japan 1.6 1.4 1.3 0.4 2.6 1.7 0.10 0.10 - 0.7 0.8 -UK 1.7 2.9 2.5 2.6 1.8 2.0 0.50 0.50 - 3.0 3.2 -Australia 2.4 2.8 2.9 2.5 2.8 2.7 2.50 2.60 - 4.2 4.5 -China 7.7 7.3 7.2 2.6 2.6 3.0 6.00 6.00 - 4.6 4.3 -Brazil 2.3 1.8 2.0 6.2 6.3 5.9 10.00 11.10 - 10.9 - -**India 4.6 4.7 5.3 10.9 9.5 7.8 7.75 8.00 - 9.2 8.6 -

Real GDP (% YoY) CPI (% YoY) Official Rates Long Rates

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 12

MONETARY POLICY May-14 Nov-13 May-13

Monetary Base growth (YoY) 26.5% 39.2% 20.1%

M-2 growth (YoY) 6.6% 6.0% 7.0%

Money multiplier (M-2/mon base) 2.9 3.0 3.5

4Q13 4Q12 4Q11

Velocity of money (GDP/M-2) 1.56 1.59 1.65

Source: Federal Reserve Bank of St. Louis ESG DATA

2013 2012 2011 2010 Total Global Wind Installations (MW) 318,137.0 283,048.0 238,050.0 197,637.0

Annual World PV New Build (MW) 37007 29,865.0

30,282.0

17,107.0

1Q13 4Q11 4Q10

Global Aggregate % of Women on Boards 11.0 10.5 9.8

ESG DISCLOSURE SCORES OF LARGEST ECONOMIES (2013)

HIGHEST ESG DISCLOSURE SCORES

Source: ESG Disclosure scores are sourced from Bloomberg ESG data which is collected from company sourced filings such as CSR reports, annual reports, company websites and a proprietary Bloomberg survey that requests corporate data directly. Source: Bloomberg, GMI Ratings

Composite Environ Social Governance1. United States 14.4 18.1 15.7 48.9 2. China 17.5 9.9 20.7 43.8 3. Japan 21.2 26.3 20.6 45.0 4. Germany 25.8 28.9 37.3 38.0 5. France 35.9 34.2 46.9 52.2 6. Brazil 32.5 30.4 51.2 37.8 7. U.K. 28.1 20.4 32.4 52.8 8. Russia 17.7 20.9 29.8 39.7 9. Italy 32.6 34.8 44.9 42.0 10. India 14.5 14.9 18.1 44.8

Composite Environ Social GovernanceSpain 40.8 45.9 56.3 46.3 Finland 36.8 33.7 38.5 55.8 France 35.9 34.2 46.9 52.2 Sri Lanka 34.8 33.2 39.9 56.5 Portugal 33.9 35.5 37.2 45.4 Sweden 33.2 26.0 38.9 53.3 Italy 32.6 34.8 44.9 42.0 Brazil 32.5 30.4 51.2 37.8 Greece 32.1 40.7 48.4 45.1 South Africa 31.4 24.7 42.1 55.8

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 13

KEY ECONOMIC CHARTS

C&I Loan Growth (%)

Source: Bloomberg

University of Michigan Survey of Consumer Sentiment

Source: Bloomberg

NFIM Small Business Optimism Index

Source: Bloomberg

ISM Manufacturing Purchasing Managers Index

Source: Bloomberg

U.S. Treasury Yield Curve

Source: Bloomberg

U.S. Initial Jobless Claims

Source: Bloomberg

-25-20-15-10-505

1015202530

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

% Y

oY

50

60

70

80

90

100

110

120

1978

1980

1983

1985

1987

1989

1991

1993

1996

1998

2000

2002

2004

2006

2009

2011

2013

707580859095

100105110

1974

1977

1979

1981

1983

1986

1988

1990

1992

1995

1997

1999

2001

2004

2006

2008

2010

2013

20

30

40

50

60

70

80

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1997

2000

2003

2006

2009

2012

0.000.501.001.502.002.503.003.504.004.50

1M 3M 6M 1Y 2Y 3Y 5Y 7Y 10Y 30Y

%

5/22/2014 11/22/2013 5/22/2013

100

200

300

400

500

600

700

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

(000

s)

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 14

Featured Domain

BuildTheLadder.net

By Erika Karp, Founder & CEO, Cornerstone Capital Inc.

Each month in the Cornerstone Journal of Sustainable Finance & Banking (JSFB), we will offer thoughts on a “Featured Domain,” which is selected from our proprietary “Sustainable Domain Bank.” The Cornerstone “Sustainable Domain Bank” contains 2,000+ addresses on the Internet, which are an articulation of business processes, business practices and aspirations for a more regenerative form of capitalism. Many of these domain names have the potential to be developed into business plans reflecting a robust interpretation of sustainable capitalism and finance. In particular, each “Sustainable Domain” captures a principle, or reflects a value inherent in the systematic understanding of the Environmental, Social and Governance (ESG) imperatives facing businesses and the economy today. Each Domain is intended to facilitate dialogue across functions and sectors of the capital markets; and each is available for collaborative partnership, purchase or transfer should it have particular appeal to Cornerstone clients and colleagues.

Are you “just the right amount of crazy” to start a new business? Do you know that entrepreneurship is like “jumping out of a plane and building the parachute on the way down?” Are you prepared to put enough capital? To put in that same amount in again? And then again? Are you prepared to function without a powerful organizational infrastructure standing around you? Can you tolerate the astonishing speed of the swings between a manic soaring sense of opportunity and optimism, and the panicky middle-of-the-night sweats with your mind racing? Sure, no problem.

And, despite all those worries, it’s worth it. It’s worth going through it all so that you can “Build the Ladder” rather than continue to climb a corporate ladder built by others. It’s worth it all to be able to combine vision with execution, strategy with tactics, and managerial skill with operational excellence. This is the view from a group of successful entrepreneurs, each of whom had a great deal of big corporate experience.

In this month’s edition of the “Cornerstone Journal of Sustainable Finance & Banking” (JSFB), we select “BuildTheLadder.net” as our “Featured Domain.” We honor the entrepreneurs. We celebrate the creative, inspired, dauntless, innovative thought-leaders ... especially those who have managed to instill in their organizations a sense of purpose. In surveying the landscape of these leaders, we also highlight the

©Bruce Rolff/Shutterstock

extent to which they are conscious of the impact they have on the world around them. It is the start-ups among the universe of small and medium-sized enterprises (SMEs) that are creating the vast majority of new jobs in an economy. And it’s often the start-ups that have figured out innovations that can then be scaled to meet the needs of a changing world.

It is this sheer force of will to address an unmet need that is the genesis of economic growth and prosperity. Entrepreneurs recognize the security they may have given up in leaving big companies. But they highlight an extraordinarily deep sense of accomplishment too. They welcome the unparalleled sense of responsibility for their own fate and that of their employees. And, they experience greater

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 15

empathy and respect for those founders around them. At the same time, they have less empathy for those people and institutions that waste time and energy. They have less tolerance for those executives in larger institutions who have the resources and platforms to implement constructive change and progress, but do not. They have even less comfort with the status quo than they did in their former lives.

So in this month’s JSFB, we applaud the awesome innovators who are building the latter and devising solutions to problems ranging from urban transportation nightmares (think Waze and Uber) to absurdly expensive broadband services (think Aero) to eyewear that’s stylish yet doesn’t break the bank (think Warby Parker). We also applaud the executives inside major corporations who have figured out how to create a culture of innovation.

We argue that it is also those companies which can embrace disruptive innovation and not be paralyzed by fears of cannibalization that will truly find sustainable, competitive advantage.

These companies embrace the economist Joseph Schumpeter’s notion of “creative destruction” and somehow manage to embrace change and innovation for the long-term good of capitalism … notwithstanding the sometimes painful journey. These leaders have the entrepreneurial spirit to which we can all aspire.

Erika Karp is the Founder & Chief Executive Officer of Cornerstone Capital Inc. and the former Head of Global Sector Research at UBS Investment Bank.

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 16

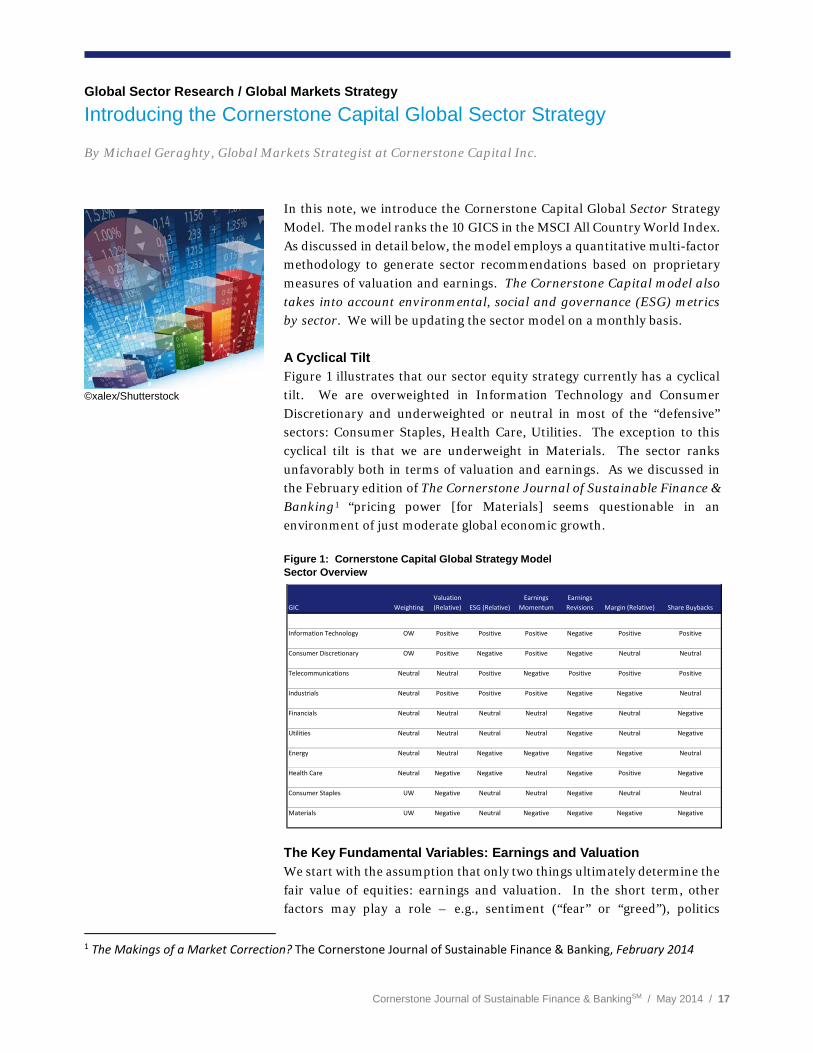

Global Sector Research / Global Markets Strategy

Introducing the Cornerstone Capital Global Sector Strategy

By Michael Geraghty, Global Markets Strategist at Cornerstone Capital Inc.

©xalex/Shutterstock

In this note, we introduce the Cornerstone Capital Global Sector Strategy Model. The model ranks the 10 GICS in the MSCI All Country World Index. As discussed in detail below, the model employs a quantitative multi-factor methodology to generate sector recommendations based on proprietary measures of valuation and earnings. The Cornerstone Capital model also takes into account environmental, social and governance (ESG) metrics by sector. We will be updating the sector model on a monthly basis.

A Cyclical Tilt Figure 1 illustrates that our sector equity strategy currently has a cyclical tilt. We are overweighted in Information Technology and Consumer Discretionary and underweighted or neutral in most of the “defensive” sectors: Consumer Staples, Health Care, Utilities. The exception to this cyclical tilt is that we are underweight in Materials. The sector ranks unfavorably both in terms of valuation and earnings. As we discussed in the February edition of The Cornerstone Journal of Sustainable Finance & Banking1 “pricing power [for Materials] seems questionable in an environment of just moderate global economic growth.

Figure 1: Cornerstone Capital Global Strategy Model Sector Overview

The Key Fundamental Variables: Earnings and Valuation We start with the assumption that only two things ultimately determine the fair value of equities: earnings and valuation. In the short term, other factors may play a role – e.g., sentiment (“fear” or “greed”), politics

1 The Makings of a Market Correction? The Cornerstone Journal of Sustainable Finance & Banking, February 2014

GIC WeightingValuation (Relative) ESG (Relative)

Earnings Momentum

Earnings Revisions Margin (Relative) Share Buybacks

Information Technology OW Positive Positive Positive Negative Positive Positive

Consumer Discretionary OW Positive Negative Positive Negative Neutral Neutral

Telecommunications Neutral Neutral Positive Negative Positive Positive Positive

Industrials Neutral Positive Positive Positive Negative Negative Neutral

Financials Neutral Neutral Neutral Neutral Negative Neutral Negative

Utilities Neutral Neutral Neutral Neutral Negative Neutral Negative

Energy Neutral Neutral Negative Negative Negative Negative Neutral

Health Care Neutral Negative Negative Neutral Negative Positive Negative

Consumer Staples UW Negative Neutral Neutral Negative Neutral Neutral

Materials UW Negative Neutral Negative Negative Negative Negative

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 17

Michael Geraghty is the Global Markets Strategist at Cornerstone Capital Inc. He has over three decades of experience in the financial services industry including working as an investment strategist at UBS and Citi.

(including geopolitical issues), macroeconomic variables (e.g., Central Bank tightening or easing) etc. – but, in the long run, we believe it all comes down to earnings and the valuation of those earnings. A number of factors drive valuation multiples at any point in time, including perceptions of ESG issues.

This is a dynamic model, with factors and factor weightings reviewed on a monthly basis for relevance. The key measures of valuation and earnings are also updated monthly; they can be updated more frequently (e.g., weekly) although a risk here is short-term “noise” in the data that does not persist for a longer period of time. A variation of this model has been in use for a number of years, and has added value in the investment decision process.

The Weighting of Regions versus Sectors The Cornerstone Capital Global Strategy Model is comprised of a regional element and a sector element. The sectors are the 10 GICS in the MSCI All Country World Index (ACWI). Figure 2 illustrates the sector weights in the MSCI ACWI – currently and in recent years. Note that the weight of the Information Technology sector increased dramatically during the TMT “bubble” of the 1990s, while the weight of the Financials sector increased during the sub-prime bubble that burst in 2007. While our strategy model is tactical in nature, in subsequent research reports we will address optimal strategic sector allocations.

Figure 2: Sector Weights in MSCI ACWI

The primary difference between the regional and sector models is the weighting assigned to the valuation and earnings factors. The sector model gives a heavier weighting to earnings while, in the regional model, valuation and earnings have roughly similar weights. The reason for this is that, in our experience, investors look for sectors that primarily offer relatively strong earnings momentum, and for regions that offer a combination of attractive valuations and earnings momentum.

So, for example, an investor may choose to overweight Japan and be underweight Latin America primarily because of the relative valuations of the two markets. To be sure, however, a region (e.g., Japan) that has a heavy weighting of a sector with strong earnings momentum (e.g., Consumer Discretionary) will likely be overweight, while a region (e.g.,

4/30/2014 2007 2006 2005 2000 1999 1998Consumer Discretionary 11% 9% 11% 11% 12% 14% 13%Consumer Staples 10% 8% 8% 8% 7% 6% 9%Energy 10% 12% 10% 9% 6% 5% 5%Financials 21% 22% 26% 25% 21% 17% 20%Health Care 11% 8% 9% 10% 12% 8% 11%Industrials 11% 11% 10% 10% 10% 10% 10%Information Technology 13% 11% 11% 12% 16% 21% 12%Materials 6% 8% 7% 6% 4% 5% 5%Telecom 4% 6% 5% 5% 8% 11% 9%Utilities 3% 5% 4% 4% 4% 3% 5%

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 18

Latin America) with a heavy weighting of a sector with weak earnings momentum (e.g., Materials) will likely be underweight. This is indeed the case – we are overweight Consumer Discretionary and Japan, and we are underweight Materials and Latin America – so that the sector and regional models are consistent.

Sector Valuation Factors In terms of the valuation of a sector, several factors are measured in order to come up with numerical values, which we label “positive,” “neutral,” or “negative” in Figure 1.

These factors include: • P/E relative to other sectors;• P/E relative to the historical average for the sector;• P/E on a “normalized” basis i.e., excluding cyclical peaks and

troughs;• The potential for P/E expansion or contraction.

The first three factors are self-explanatory, while the fourth factor is based on a number of momentum indicators.

Sector ESG Metrics As we noted above, a number of factors drive valuation multiples at any point in time, including perceptions of ESG issues. We also pointed out that this is a dynamic model, with factors and factor weightings being reviewed frequently.

In this first iteration of the sector equity strategy model, we utilize ESG metrics calculated by MSCI. MSCI ESG Intangible Value Assessment (IVA) provides analysis of over 5,000 global companies' financially material risks and opportunities arising from environmental, social, and governance factors. At a security level, an Environment Score, Social Score and Governance score are calculated on a 0-10 scale, with 10 being the best in terms of companies’ opportunity or risk exposure and ability to manage that exposure.

Figure 3 on the following page illustrates that, according to a Deutsche Bank analysis,2 Environmental factors are particularly important in the Utilities and Materials sectors, Social factors are particularly important in the Health Care sector and Governance factors are particularly important in the Telecom and Financials sectors.

2 The Socially Responsible Quant, Deutsche Bank Markets Research, April 24, 2013

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 19

Figure 3:Sector ESG Scores by Weighting

To arrive at a final rating – see Figure 43 - the weighted averages of the scores are aggregated and companies’ scores are normalized by their industries.

Figure 4: MSCI Sector ESG Scores Highest Score is Best

Sector Earnings Factors Turning to the earnings of a sector, the model aggregates a number of measures under four broad headings:

Earnings momentum: Relative to the MSCI All Country World Index, we calculate if the earnings momentum of a sector has been accelerating, stable or decelerating. We then look at the earnings momentum of one sector relative to another. The resulting numerical values are labeled in Figure 1 as “positive” (accelerating momentum), “neutral” (stable momentum) or “negative” (decelerating momentum).

Earnings revisions: For each of the companies in a sector, we look at the recent trend in earnings revisions by calculating the difference between the number of upward and downward estimate revisions. The data are

3 The Socially Responsible Quant, Deutsche Bank Markets Research, April 24, 2013

0%

20%

40%

60%

80%

Con Disc Con Staples Energy Financials Health Industrials Info Tech Materials Telecom Utilities

Environmental Weight Social Weight Governance Weight

Consumer Discretionary 4.8Consumer Staples 5.2Energy 4.7Financials 5.3Health Care 4.8Industrials 6.3Information Technology 6.5Materials 5.7Telecommunication Services 5.9Utilities 5.4

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 20

aggregated, and the resulting numerical values are summarized. A high ratio of upward-to-downward revisions is considered “positive” for a sector; conversely a high ratio of downward-to-upward revisions is considered “negative.”

Margins: We look at the margins of each of the companies in a sector – both actual and estimated – and aggregate the data. We assume that relatively high and sustainable margins are “positive” in that they should support earnings growth, while volatile margins are a “negative.” In recent years, margins in the (knowledge-intensive) Information Technology and Telecom sectors have been consistently high, while margins in the (commoditized) Energy sector have been quite volatile. Consequently, Information Technology and Telecom get a higher score for Margins in Figure 1 than Energy.

Share buybacks: Given that corporate earnings are reported on a per share basis, we take into account the amount of net share buybacks that have occurred over the past twelve months in each sector. Once again, we aggregate data from the company level. A large amount of net share buybacks is “positive” for earnings per share growth in a sector, while the opposite (i.e., share issuance) is “negative.”

Ranking Sectors by Weighting Valuation, Earnings and ESG Scores The values derived from the various measures of valuation, earnings and ESG are weighted, and the sectors are then ranked on the basis of their total “score.” Sectors that are at the very top or very bottom of the distribution are typically ranked “overweight” or “underweight” respectively, while sectors that fall in the middle are typically ranked “neutral.”

Given the quantitative underpinnings of the model, we can look at the dispersion of the “scores” in order to decide on the relative weightings. In other words, a sector’s score might be so high relative to the others in a given month that it is the sole overweight while, in another month, the scores of a number of sectors are closely clustered and they are all assigned the same weighting (e.g., “neutral”).

Combining the Sector and Regional Models Combining our sector and regional models, Figure 5 on the following page illustrates select sector over- and under-weights by region.

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 21

Figure 5: Regional and Sector Overview

We are overweight Information Technology in Japan, Emerging Asia and the U.S.; we are overweight Consumer Discretionary in Japan and the U.S. We are underweight Materials and Consumer Staples in the majority of regions

Japan EM Asia U.K. U.S. CEEMEA Europe ex. U.K. Latin America

Information Technology OW OW OW

Consumer Discretionary OW OW

Telecom

Industrials

Financials

Utilities

Energy

Health Care

Consumer Staples UW UW UW UW

Materials UW UW UW UW UW

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 22

Global Sector Research / Global Markets Strategy

The Cornerstone Capital Regional Strategy Update By Michael Geraghty, Global Markets Strategist at Cornerstone Capital Inc.

©MSEN/Crystal Graphics

In the April edition of The Cornerstone Journal of Sustainable Finance & Banking we introduced the Cornerstone Capital Regional Strategy Model. Table 1 illustrates that, after updating the inputs, there is no change in our regional over- and under-weights.

In terms of performance, Latin America, which is ranked underweight, has been relatively strong, gaining about 2% in the past month, at the same time the MSCI All Country World Index was up around 1%. There has been no change in the fundamental outlook – Latin America still ranks unfavorably both in terms of earnings and valuation.

Brazil is by far the most important country in the region, accounting for 58% of the MSCI Emerging Markets Latin America Index. The MSCI Brazil Index is up about 2% in the past month. It would seem that the rally has been driven by some investors betting on the failure of President Dilma Rousseff’s re-election bid. The hope is that, after the October election, a new administration will usher in new policies - since President Rousseff took office in 2011, the pace of Brazil’s economic growth has been only 2% annually on average. Meanwhile, economists expect Brazil’s inflation to reach 6.5% in 2014, which corresponds to the upper level of the official range set by the government.

Table 1: Cornerstone Capital Global Markets Equity Strategy Model Regional Overview

Region/ Major Economy Weighting

Valuation (Relative)

Governance (Relative)

Earnings Momentum

Earnings Revisions

Margin (Relative)

Share Buybacks

Japan OW Positive Neutral Positive Neutral Negative Neutral

EM Asia OW Positive Negative Neutral Neutral Negative Negative

U.K. Neutral Neutral Positive Negative Neutral Negative Negative

U.S. Neutral Negative Positive Positive Negative Neutral Positive

CEEMEA Neutral Positive Negative Negative Negative Positive Negative

Europe ex. U.K.

UW Negative Neutral Negative Neutral Neutral Negative

Latin America

UW Negative Negative Negative Negative Positive Negative

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 23

Michael Geraghty is the Global Markets Strategist at Cornerstone Capital Inc. He has over three decades of experience in the financial services industry including working as an investment strategist at UBS and Citi.

Uncertainty about the election aside, the fundamental outlook for a weak economy and a likely inflation-driven interest rate hike suggests that the risk-reward scenario in Brazilian equities remains unfavorable.

Our other underweight, Europe excluding the U.K., was a relatively poor performer, remaining virtually unchanged during the month.

In terms of overweight regions, Japanese equities were roughly flat in the past month. Weighing on stock prices was a strong yen driven, in part, by geopolitical tension centered on the Ukraine, which prompted Japanese investors to sell large amounts of euro-denominated bonds. Strength in the yen has pressured Japanese exports. However, many economists expect that the Bank of Japan will engage in additional monetary easing policies later this year, which should support equities as a lower yen benefits corporate profits.

Our other overweight region, Emerging Asia rose about 2% last month, less than the roughly 6% gain in the CEEMEA region. The bearish consensus in emerging markets has reversed in recent weeks, with some of the more troubled markets (most notably Russia) outperforming those with stronger fundamentals. A number of factors are likely behind this shift in sentiment on emerging markets, including reduced geopolitical tension over Ukraine. In addition, market observers have also pointed to: (i) lower U.S. bond yields; (ii) prospective monetary easing by the European Central Bank; (iii) growing expectations of stimulus from the Chinese authorities.

Reflecting attractive valuations in Emerging Asia and the potential for stimulus measures in China, we remain overweight the Emerging Asia region, while staying neutral on CEEMEA given a weak fundamental outlook.

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 24

Global Sector Research / Global Markets Strategy

Financial Impediments to Job Creation by Start-Ups and Small Firms

By Michael Geraghty, Global Markets Strategist at Cornerstone Capital Inc.

©Frank Peters/Crystal Graphics

Start-ups are a significant source of job creation in the U.S. Separately, mature small firms account for a large portion of employment levels. Bank lending and initial public offerings (IPOs) are important forms of financing for start-ups and mature small firms. However, both types of financing have yet to fully recover from the financial crisis of 2008-09. This is cause for concern because available financing is key to start-up formation and business sustainability which, in turn, fuel job growth.

Start-Ups: A Significant Source of Job Creation While older firms are important with regard to employment levels, it is new and young businesses (i.e., less than one year old) that are a key source of job growth. The U.S. economy is comprised of more than 6 million establishments with paid employees. The status of these businesses is constantly churning — some grow, others decline, and yet others close. New businesses replenish the pool of establishments with paid employees; since 1977, newly born companies created 3 million jobs per year on average. As we discuss below, these 3 million new jobs exceed total average annual job growth overall, reflecting job destruction by mature firms.

In recent years, however, the rate of start-up formation has slowed sharply. After declining from 667,000 in 2006 to 507,000 in 2010, the number of startups rose in 2013 for the third consecutive year, albeit only to 628,000 — well below their 2006 peak. As for employment growth, the rate of job creation at start-up companies was steady in the 1980s and 1990s at 11 start-up jobs per 1,000 people (i.e., among every 1,000 Americans, 11 were newly hired at a company begun that year). Not surprisingly, the start-up jobs rate declined along with the rate of start-up formation (to just 8 start-up jobs per 1,000 people in 2009), and improved modestly to 9 per 1,000 in 2013.

As for where start-ups have been predominant in the economy, Figure 1 shows the sectors that accounted for the largest number of jobs created by start-ups in the period from 1994–2013. Note that the Information Technology sector appears relatively unimportant in terms of start-up job formation during this period, accounting for just 3% of jobs created by new young firms (included in “Other”) This is somewhat misleading, however, as it doesn’t take into account the critical issues of (1) survival rates and (ii) net employment growth rates.

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 25

Michael Geraghty is the Global Markets Strategist at Cornerstone Capital Inc. He has over three decades of experience in the financial services industry including working as an investment strategist at UBS and Citi.

Figure 1: Jobs Created in U.S. Establishments <1 Year Old by Sector, 1994-2013

So, for example, a lot of pizza restaurants that fall under the “Accommodation & Food Services” category may open each year after hiring cooks and serving/delivery personnel, but their survival rates are often low. By contrast, far fewer tech firms may set up shop each year with just a handful of employees but, if they successfully develop a product, they survive and often go on to add many more employees. This suggests that some sectors are better than others in creating sustainable jobs.

Small Firms: Big Employers The World Economic Forum has noted that “most young firms start small, but most small firms are not start-ups.1” Almost half of U.S. private sector employment is in firms with fewer than 250 employees; the proportion has been relatively stable over the past two decades, suggesting that small firms consistently account for a large portion of employment levels.

Existing firms create significantly more new jobs than start-ups. Given the very large share of activity accounted for by mature firms, it is not surprising that, in terms of sheer numbers, older firms create and eliminate the largest number of jobs. On average since 1977:

• 10 million new jobs have been created each year at existingfirms (e.g., a Starbucks corporate headquarters);

• 3 million new jobs have been created each year at newestablishments of existing firms (e.g., a new Starbuckssomewhere in the U.S.)

1 Not All SMEs Are Created Equal, World Economic Forum Global Agenda Council on Financing & Capital, 2014

Accommodation & Food Services17%

Retail Trade15%

Office Support Services9%

Health Care9%

Professional Business Services8%

Construction8%

Manufacturing6%

Finance and Insurance5%

Other23%

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 26

• 14 million jobs have been eliminated each year by existingfirms (e.g., “mom and pop” coffee shops closing locationswhen Starbucks enters a new market).

In aggregate, existing employers averaged net job losses of 1 million workers per year, at the same time that newly born companies created 3 million jobs per year on average. So, what matters most, in aggregate, is creating new jobs and holding on to existing jobs.

Less Bank Lending to Small Businesses As per the aforementioned World Economic Forum study, most lending to small and medium-sized enterprises (SMEs) in the U.S. is by the largest banks. Around 85% of all commercial and industrial loans of $100,000 or less were made by banks with more than $1 billion in assets (the largest size bucket reported by the FDIC). Although small banks might lend more to SMEs as a fraction of their asset size, the asset base of large banks is so much larger that their lending to SMEs dwarfs that of smaller banks.

Policies that were enacted in the aftermath of the financial crisis of 2008-09 may have had unintended negative consequences for lending to SMEs. Among the most notable of these policies is the Dodd-Frank Wall Street Reform and Consumer Protection Act intended, in part, to govern the behavior of large banks by making them “less risky.” Risk aversion may have adversely impacted SME lending— the dollar value of commercial and industrial loans to small businesses in 2013 was 15% below 2008 levels (i.e., five years later and with nominal GDP in 2013 14% above 2008 levels.)

Fewer IPOs Stock market IPOs are another important source of funds for young and/or small firms, often functioning as a key rite of passage for many entrepreneurial firms, and allows founders and financial backers to begin cashing out. Furthermore, venture capital and private equity firms are typically contractually mandated by their limited partners to exit their portfolio companies within a certain number of years after the initial investment, and thus are motivated to either sell out or take a company public.

From 1980–2000, an average of 311 firms went public in the United States each year, but in 2001–2011, this number fell to an average of only 99 per year. The drop in IPO activity was most severe among small firms – one study2 documented that the average number of small-company IPOs per year in the period between 2001 and 2009 fell by more than 80% relative to the annual average number of small-company IPOs in the period between 1980 and 2000.

2 Where Have All the IPOs Gone?, Gao, Ritter & Zhu, 2012

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 27

A number of explanations for the prolonged drought in IPOs have been advanced. For example, it has been argued that the Sarbanes Oxley Act of 2002 (SOX) imposed additional compliance costs on publicly traded firms. As a percentage of revenue, these costs have been especially onerous for small firms. Consistent with the SOX explanation for the decline in IPO activity and, as noted above, the decline in IPOs has been most pronounced among small firms. Other observers have attributed the drop in small company IPO volume in the U.S. to a decline in the “ecosystem” of underwriters that focus on smaller firms and provide analyst coverage only after a company has gone public. Policy Implications The drop in IPO activity generated concern among policymakers given that, as outlined above, a big source of job creation is by young, fast-growing firms. Consequently, the Jumpstart Our Business Startups (JOBS) Act was signed into law by President Barack Obama in April 2012 with an explicit goal of encouraging start-ups. Whether attributable to the stimulus provided by the Act or not, the number of IPOs in 2013 rose to over 200, but still well below the 1980-2000 average of 311. It’s undoubtedly a negative for job creation by start-ups and mature small firms that IPOs — and bank lending too — have yet to fully recover from the financial crisis of 2008-09. In addition, there is anecdotal evidence that the U.S. policy environment has made entrepreneurial employment growth more difficult to achieve. At the federal level, the dominant factor here may be new regulations on labor. So for example, the passage of the Affordable Care Act is creating a sweeping alteration of the regulatory environment that directly changes how employers engage their workforces. So in summary, this brief analysis gives a bit more granularity to the extent to which start-ups are a significant source of job creation in the U.S. and mature small firms account for a large portion of employment levels. Further, given that bank lending and IPOs are important forms of financing for start-ups and mature small firms, it seems clear that a greater degree of confidence in the power of capitalism is needed to further stimulate economic growth. In a number of the articles in this month’s edition of the Cornerstone JSFB, we argue that greater transparency and improved corporate governance, can indeed begin to rebuild this confidence...and thus help stimulate the financing that is needed to restart the entrepreneurial jobs engine.

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 28

Corporate Governance Insights

Good Governance: A Cornerstone of Entrepreneurism

By John Wilson, Head of Corporate Governance, Engagement & Research at Cornerstone Capital Inc. “Corporate Governance.” Perhaps the term seems out of place in a journal devoted to entrepreneurship? Entrepreneurship, whether found in a start-up or an established company, implies innovation, strategy and corporate renewal. Corporate Governance, by contrast, is seen as a “soft” form of corporate regulation that restricts and perhaps confines management. Moreover, decades of studies of different corporate governance approaches have not produced a consensus on whether and how corporate governance matters for corporate performance. On the other hand, as Ken Bertsch, the former head of the Society of Corporate Secretaries, once pointed out, “How could it not?” In fact, effective corporate governance is essential for creating entrepreneurial organizations that are built to thrive. Corporate governance describes the relationship between all stakeholders that determines the strategic direction of the organization. Understanding the systems by which the company makes strategic decisions, executes its business plans, and holds management accountable offers insights about whether the firm has the capacity to innovate, execute, and create long-term value. Historically, companies’ governance has been judged according to the formal rules, such as board structure, compensation plans and voting rights – what some call the “hardware” of corporate governance. The virtue of studying “hardware” is that precise and comparable information is available from the company’s regulatory filings. While there is value in this approach, there are limitations as well. Apparently well-designed governance structures can mask deep conflicts of interest, as in the well-known cases of Enron and Lehman Brothers, or less dramatic

1 Fogel, Kathy and Ma, Liping and Morck, Randall, Powerful Independent Directors (January 9, 2014). European Corporate Governance Institute (ECGI) - Finance Working Paper No. 404/2014. Available at SSRN.

but nevertheless significant weaknesses that may signal a long-term risk to shareholder value. Corporate governance "hardware” matters to the extent that it facilitates quality interactions among corporate stakeholders – the “software” of corporate governance. But the tools to evaluate “software” have until recently eluded researchers because outsiders lack a robust perspective on the discussions that take place among managers, boards, and shareholders — much less the company’s engagement with employees, customers, communities and regulators. However, an emerging body of studies are beginning to address this limitation by assessing the quality of the firm’s relationships and its impact on performance. Here we consider a few recent studies that shed light on what makes good corporate governance. Although listing standards and most investors expect that boards include a majority of independent directors, the literature has not definitively linked independence to higher shareholder value. Listing standards consider directors “independent” if they lack conflicts of interest arising from an employment, familial or business relationship with the company. Formal independence does not guarantee that a director will be capable of providing independent perspectives or judgment necessary for effective board leadership. A recent working paper from the European Corporate Governance Institute1 considered individual directors’ relationships more broadly, including their professional, educational and social networks. The paper found that boards that directors with stronger social networks were associated with higher firm valuations. The study posited that these “powerful”

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 29

directors’ external relationships made them better informed, more able to avoid groupthink and more willing to dissent. In other words, it was not enough to be legally independent; directors add value to the company when they are in a position to behave independently. Another important aspect of corporate governance is the firm’s relationship with its external stakeholders, including employees, regulators, communities, and the environment, which can all exert significant influence on a firm’s key strategic decisions. Many advocates of corporate social responsibility claim that good relations with stakeholders can be seen as a proxy for good management. A recent study2 provided direct evidence for this hypothesis by examining the relationship between high quality management and corporate social responsibility practices. The study used a dataset of company responses to a survey about the use of 18 management techniques that had been shown to correlate with strong firm performance. The study found that companies whose top executives use these best management practices are more likely to invest in positive social responsibility practices as well. These studies complement the research of shareholder engagement and firm performance. Some institutional shareholders engage directly with portfolio companies to advocate action on corporate social and environmental impact. The effectiveness of these engagements has been difficult to track because these dialogues tend to be confidential. However, two

2 “A Good Horse Never Lacks a Saddle: Management Quality Practices and Corporate Social Responsibility,”Najah Attig,Associate Professor, Canada Research Chair in Finance Saint Mary‘s University, Halifax, Canada, February 07, 2012 3 Dimson, Elroy and Karakaş, Oğuzhan and Li, Xi, Active Ownership, June 4, 2013, (available at SSRN) and Flammer, Caroline, Does Corporate Social Responsibility Lead to Superior Financial Performance? A Regression Discontinuity Approach, October 2013 (available at SSRN.)

recent studies3 have begun to shed light on this practice. The Dimson, et al, study considered the results of thousands of individual cases of shareholder dialogue, while Flammer looked specifically at shareholder proposals that received majority support. Both studies demonstrate that successful shareholder engagements (either because they receive majority shareholder support, or because they result in policy change) are associated with improved operating and financial performance. Historically, investors have inferred corporate governance practices from formal board structures that may or may not accurately signal the quality of firm decision-making. Together, these studies begin to open the “black box” of corporate governance, suggesting ways that investors may be better able to evaluate a firm’s capacity for long term value-creation by more directly understanding the quality of a company’s management practices and relationships with their stakeholders. It only with an infrastructure of trust and material transparency that today’s innovators can realize the true promise of entrepreneurship.

John Wilson is the Head of Corporate Governance, Engagement & Research at Cornerstone Capital Inc. Prior to Cornerstone, he was the Director of Corporate Governance at TIAA-CREF and the Director of Socially Responsible Investing at the Christian Brothers Investment Services. He is also an Adjunct Assistant Professor at the Columbia University Graduate School of Business.

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 30

Corporate Governance Insights

Follow the Leader, Follow the Money Sustainable Entrepreneurship in Banking — The Equator Principles

By Cindy Motz, Independent Research Analyst & Global Advisory Council Member, Cornerstone Capital “This is where the entrepreneurs come in … Just look at the opportunities, dream up a couple of ideas and work on them.” — Sir Richard Branson1 While images of Branson or Elon Musk may come to mind upon hearing the term “social entrepreneur,” one does not require a huge public presence, a revolutionary new idea, or even billions of dollars to make a positive impact in meeting societal needs. Throughout the world, sustainability professionals are working on effecting lasting change within the banking and project finance sector every day, by having their organizations participate in “The Equator Principles.” The Equator Principles Established on June 4, 2003 by several banks, including ABN Amro, Barclays, Citibank, Westpac, and others, the Equator Principles have now been adopted by 78 financial institutions across 34 countries.2 A voluntary risk management framework designed to take into account environmental and social responsibilities, the Equator Principles are intended to set minimum due diligence standards for member financial institutions participating across all industry sector project finance transactions, including advisory, corporate and bridge loans. Having undergone several revisions since its inception almost

1 Richard Branson, “Richard Branson on the Business of Sustainability,” Entrepreneur, October 10, 2011, http://www.entrepreneur.com/article/220496. 2 Equator Principles, http://www.equator-principles.com/index.php/members-reporting. 3 The Equator Principles 2013, http://www.equator-principles.com/resources/equator_principles_III.pdf. 4 Rainforest Action Network, “Shifting the Paradigm,” http://ran.org/shifting-paradigm.

11 years ago, the most recent framework, the EP III, was established in 2013 for project finance transactions over $10 million beginning in 2014. The provisions now also include a focus on protecting human rights (original transaction threshold was $50 million, and focus was more on environmental rights). Although most of the reporting is qualitative, there are ten principles which the signatories have agreed to track, incorporating categorization and monitoring of risks, greenhouse gas (GHG) reporting, grievances, loan covenants and independent auditing of the principles.3 Sometimes, Opportunity Walks Up and Knocks—on Your Boss’s Door Back in 2000, then Citgroup Chairman and CEO, Sandy Weill, had likely never thought much about the Rainforest Action Network.4 But the situation changed when the NGO began showing up — at his home, office and elsewhere — attempting to pressure Citi, then the world’s largest bank, into thinking about the social and environmental implications associated with some of its project financing transactions. “They realized they needed some standards, a framework,” said Shawn Miller, who was working in 2003 as a Social Development Specialist at the IFC when banks approached the private sector investment division of the World Bank seeking answers. Soon after the initial standards were drafted, Miller joined Citi in 2004, where his first goal was to broaden the bank’s environmental and social risk management

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 31

policy, and then, set up the transaction review process that included implementation of the Equator Principles (which he co-authored in 2006, and are based on IFC guidelines). Eventually, Miller and his team went on to set a 10% GHG reduction target, and Citibank launched a $50 billion, 10-year climate investment initiative that was recently achieved this year, three years earlier than expected.5 Now, Managing Director and Head of Environmental and Social Risk Management at Citibank, Miller served as Chair of the Equator Principle Steering Committee (2010-12), and also helped to draft the recent third iteration of the 2013 Equator Principles.

Stakeholders Follow the Money — Take Them Seriously If You Want to Keep More of Yours

“If any of our clients’ projects do not apply strict standards, they will inevitably suffer from opposition and delays … The cost of these avoidable setbacks can easily run into the billions of dollars,”6 Miller stated in the journal CFI.co.

Throughout his career, Miller has increasingly observed stakeholders “following the money,” essentially focusing on those who financially back projects that may have adverse social or environmental impacts. In addition to the rising trend in shareholder resolutions regarding ESG issues, pressure is now coming from a variety of

different stakeholder sources, all of whom should be taken seriously.7 Miller notes that most clients recognize the value of the Equator Principles and its review processes, understanding that having stakeholder approval and a “social license to operate” are integral to any project’s success. Working with companies to develop action plans and road maps to achieving more sustainable projects, Miller’s group reviews hundreds of projects each year. Globally, 90% of project financings are being handled by financial institutions who are signatories to the Equator Principles.8

Managing Director at Citibank — Sustainable Entrepreneur?

Miller’s ESRM title may not immediately shout “Rachel Carson” at you, but Shawn Miller has been a pioneer in sustainable finance for more than 17 years. While there is more work to be done here, and authoring/implementing the Equator Principles may not be as “sustainably sexy” as Silent Spring or a Model S, sustainable entrepreneurs, like Miller, have seized an opportunity and are working to effect sustainable change both at their own institutions, as well as client organizations, one project at a time.

Cindy Motz is an Independent Research Analyst & Global Advisory Council Member, Cornerstone Capital. She is a former II & WSJ All Star Analyst.

5 http://blog.citigroup.com/2014/04/50-billion-climate-change-investment-initiative.shtml. 6 Shawn Miller, Cfi.co, “Banking on Sustainability,” August 2013, http://cfi.co/asia/2013/08/the-equator-principles-banking-on-sustainability/ 7 Eric J. Hespenheide and Dr. Dinah A. Koehler, “Drivers of Long-Term Business Value,” Deloitte University Press, July 2013, http://dupress.com/articles/drivers-of-long-term-business-value/. 8 Shawn Miller, “Managing Risk, Enhancing Reputation: Discussion on Social and Environmental Performance in the Finance Sector” Lecture, New York, April 29, 2014.

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 32

Valuation & Accounting

Making the Case for Crowdfunding Rules

By Janet Pegg, CPA, Head of Valuation & Accounting at Cornerstone Capital Inc. and former Managing Director and Analyst of U.S. Accounting Research at UBS Investment Bank Start-up companies and investors eagerly await SEC final rules implementing the JOBS Act’s crowdfunding provisions. The SEC, however, must ensure investors are adequately protected. Achieving this goal will help validate crowdfunding as a viable investment and capital raising tool. The Jumpstart Our Business Startups Act (“JOBS Act”, or “the Act”), enacted on April 5, 2012, made significant changes to the ways small companies can raise capital. Title III of the JOBS Act provides for an exemption from regular securities registration in specific circumstance, referred to as crowdfunding. The passage of these provisions has created a great deal of excitement for potential funding for new start-up companies. But the new regulatory exemption doesn’t become effective until the Securities and Exchange Commission issues final rules implementing Title III. Although the Act directed the SEC to issue the rules not later than 270 days after enactment, because of the complexity of the provision and the need to ensure investor protection, proposed rules weren’t issued until October 23, 2013. A comment period closed on February 3, 2014. Although eagerly awaited, there is no set timetable for when the SEC might issue final rules. The concept of crowdfunding is explained in the introduction to the SEC’s proposed rules: Crowdfunding is a new and evolving method to raise money using the Internet. Crowdfunding serves as an alternative source of capital to support a wide range of ideas and ventures. An entity or individual raising funds through crowdfunding typically seeks small individual contributions from a large number of people. A crowdfunding campaign generally has a specified target amount for funds to be raised, or goal, and an identified use of the funds. (SEC Release Nos. 33-9470; 34-70742; File No. S7-09-13)

©LuMaxArt/Crystal Graphics

The JOBS Act included rules and restrictions on the use of the crowdfunding regulatory exemption, directed at the issuers, investors, and intermediaries connecting issuers with investors, and the issuers. The more notable of these rules include: • An issuer cannot issue more than $1 million in any

12-month period and must comply with specific rules.

• Companies issuing securities under the crowdfunding provisions must provide specified information to the SEC and meet other specified rules, must be organized within the U.S. and cannot be existing reporting filers with the SEC. Required disclosures would range from tax returns and financial statements certified by the principal executive officer for issuers offering 100,000 or less, to audited financial statements for issuers offering more than $500,000 in a 12-month period.

• Limitations are placed on the amount an investor can purchase from an issuer in any one-year period. Under the original JOBS Act the limits ranged from $2,000 for the smallest of investors

Cornerstone Journal of Sustainable Finance & BankingSM / May 2014 / 33

to $100,000 for investor’s with annual income or net worth equal to or greater than $100,000.

• An investor cannot transfer acquired securities for one year except in limited circumstances.

• Transactions must be conducted through qualifying brokers or funding portals that follow specific requirements.