matteson retail report

DESCRIPTION

Retail & shopping feasibilityTRANSCRIPT

RETAIL MARKET FEASIBILITY STUDY LINCOLN MALL AREA LINCOLN HIGHWAY, CICERO AVENUE & INTERSTATE 57 MATTESON, ILLINOIS PREPARED FOR VILLAGE OF MATTESON MATTESON, ILLINOIS JUNE 2006

TABLE OF CONTENTS

Section Number Title Page Number I. ASSIGNMENT 1 Study Assumptions 2 II. EXECUTIVE SUMMARY 3 General Findings 3 Conclusions 3

Recommended Actions 11 Estimated Retail Sales by Retail Category 11 Prospective Major Retailers 15 Lifestyle Tenants in Lifestyle Center – Not in Lincoln Mall 15 Matteson’s Shopping Centers 16

III. METHODOLOGY AND DEFINITIONS 20 Methodology 20 Definitions 23 IV. LINCOLN MALL AREA’S RETAIL CONCENTRATION 26 Matteson’s Retail Sales 26 Comparison of Lincoln Mall to Eight Other Malls 27 Comparison of Lincoln Mall to Four Lifestyle Centers 29 Matteson Shopping Centers - Part of the Lincoln Mall Area 31 V. RETAIL TRENDS 32 National Trends 32 Chicagoland Retail Situation 33 Retail Development and Vacancy 34 Big Box Discount Department Stores and Supercenters 35 Department Stores 36

Supermarkets and Warehouse Stores 37 Drug Stores 38 Electronics Stores 38 Furniture Stores 38 Home Improvement Stores 39 Restaurant & Quick Service Casual Facilities 39 VI. RETAIL MARKET ANALYSIS 41 Site/Location 41 Accessibility 41 Traffic Counts 42 Driving Time Analysis 43

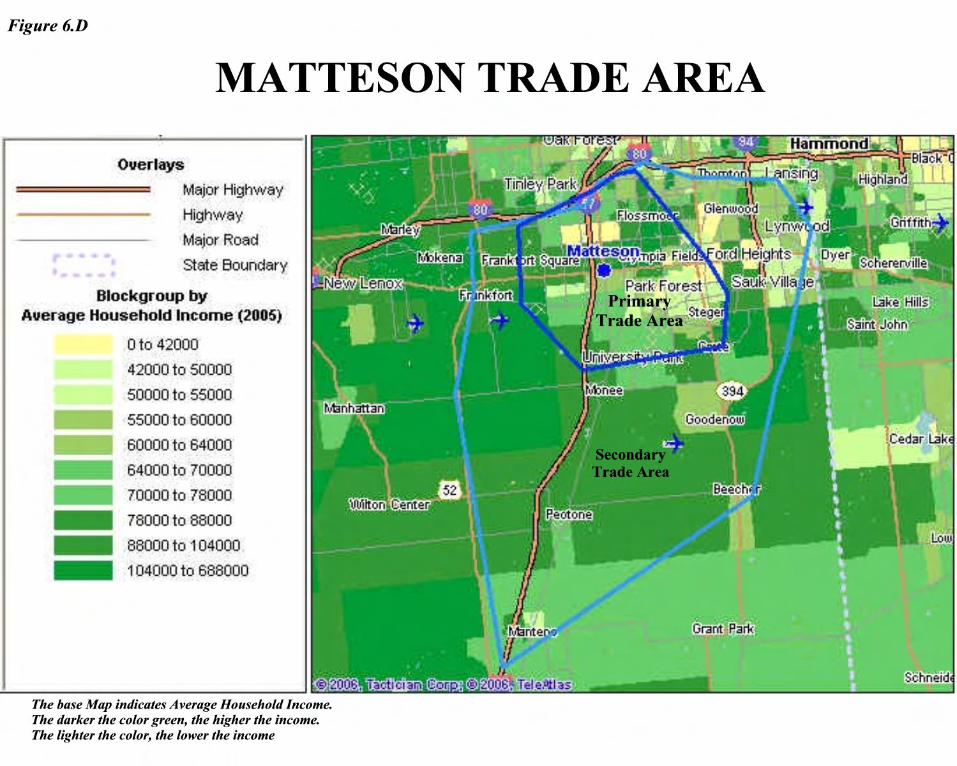

Trade Area Delineation 44 Trade Area Market Support Factors 44

TABLE OF CONTENTS (Continued)

Section Number Title Page Number VI. RETAIL MARKET ANALYSIS (Continued) Competitive Environment 48 Orland Park 49 Homewood/Glenwood 51 Tinley Park 52 Crestwood 52 Country Club Hills 52 Calumet City 52 Planned and Proposed Shopping Facilities 53 Retail Expenditure Patterns 53 Market Penetration 60 Estimated Retail Sales by Retail Category 63 Home Improvement 63 General Merchandise 63 Food Stores 64 Furniture & Home Furnishings 64 Electronics & Appliances 64 Eating & Drinking 65 Drug and Miscellaneous 65 Prospective Major Retailers 66 Lifestyle Tenants not located in Lincoln Mall 66 Matteson’s Shopping Centers near Lincoln Mall 68 Introduction to Melaniphy & Associates, Inc. Addenda

LIST OF TABLES

Number Title Page Number 2.1 Market Support Factors, Matteson Trade Area 6 2.1 Market Support Factors, Matteson Trade Area (Continued) 7 2.2 2006 Retail Sales and Market Penetration – Matteson, Illinois 8 2.3 Estimated Retail Expenditures, Market Penetration, & Matteson Estimated Retail Sales, 2006, 2010, & 2015 19 4.1 Matteson Retail & Foodservice Sales 2002 – 2005 27 4.2 Comparison of Chicagoland Selected Malls to Matteson’s Lincoln Mall 28 4.3 Comparison of Chicago Lifestyle Center Demographics 30 6.1 Market Support Factors – Lincoln Mall Area Trade Area 46 - 47

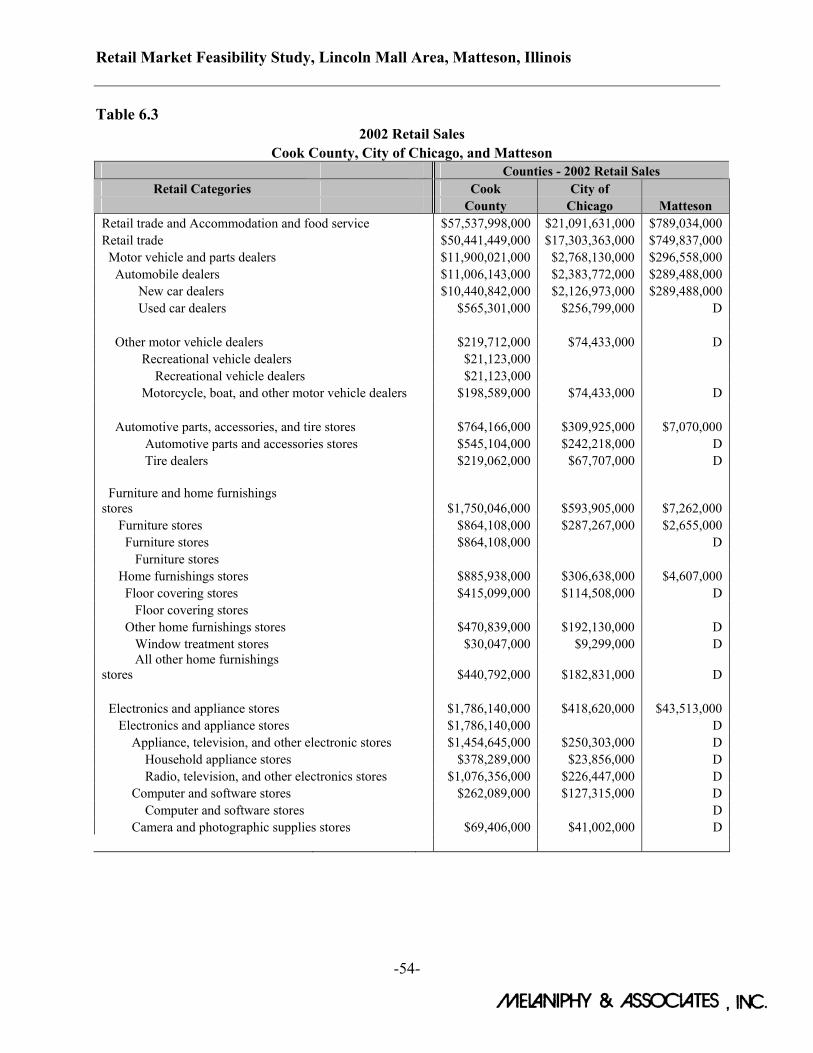

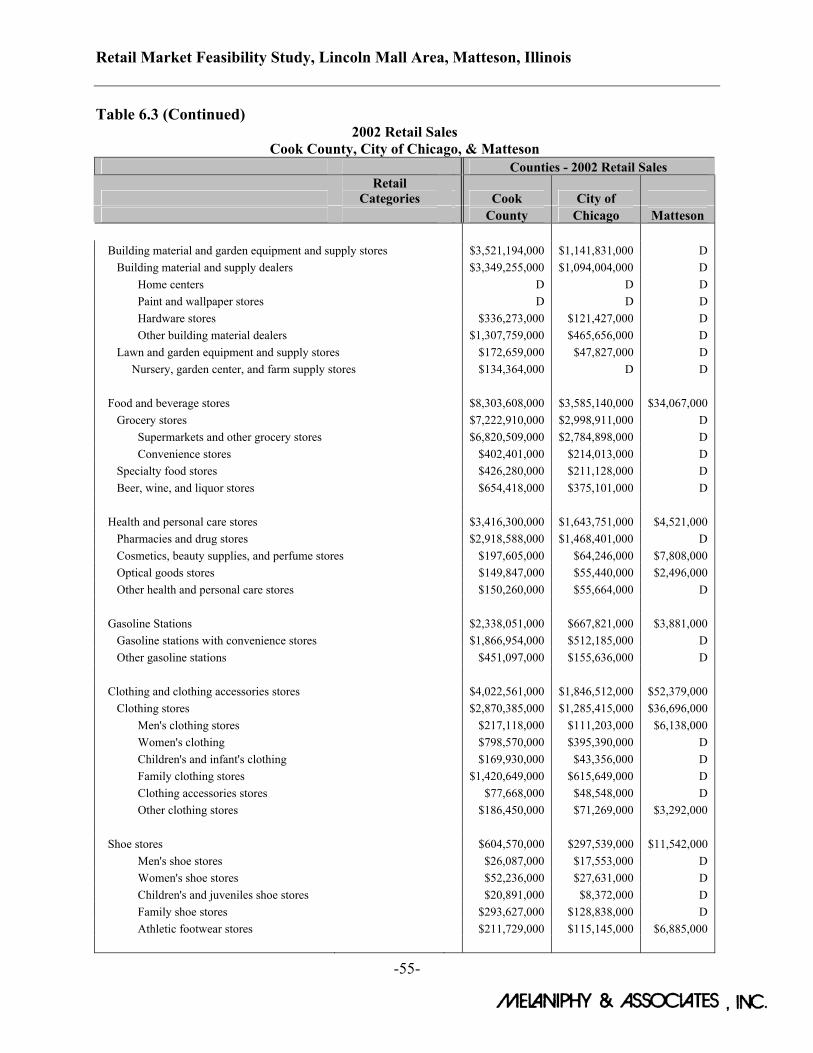

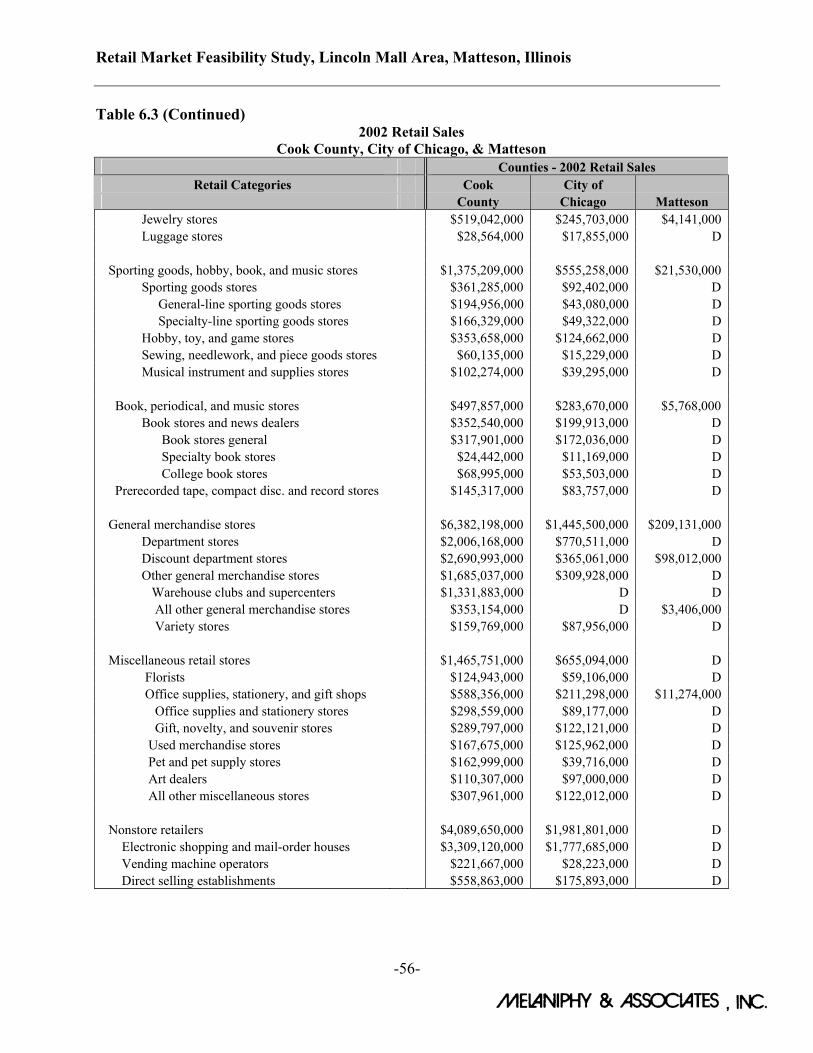

6.2 Competitive Retail Facilities 50 6.3 2002 Retail Sales, Cook County, City of Chicago, and Matteson 54 - 57 6.4 Retail Sales by County, Chicago Metropolitan Area, 2003 - 2005 58 6.5 Matteson Retail & Foodservice Sales – 2002 – 2005 58 6.6 Per Capita Retail Expenditures by Retail Category, 2006, 2010, & 2015 60 6.7 Matteson’s Estimated Retail Expenditures by Retail Categories,

2006, 2010, & 2015 61 6.8 Estimated Retail Expenditures, Market Penetration, & Matteson Estimated Retail Sales, 2006, 2010, & 2015 62

LIST OF FIGURES

Figure Page Number Description Number 2.A Matteson Trade Area 4 4.A Lincoln Mall Redevelopment, Matteson, Illinois 26 6.A Aerial View, the Lincoln Highway and Cicero Avenue Interchange Adjacent to Interstate the Interstate 67 Interchange 41 6.B Traffic Counts for Major State and Federal Roads, Illinois Department of Transportation, Matteson, Illinois 42 6.C Driving Time Analysis – 10 & 20 Minutes, Lincoln Mall Area 43 6.D Matteson Trade Area Map 45 6.E 10 Mile Radius Map, Lincoln Mall, Matteson, Illinois Showing Position of Orland Square Mall & River Oaks Center 51

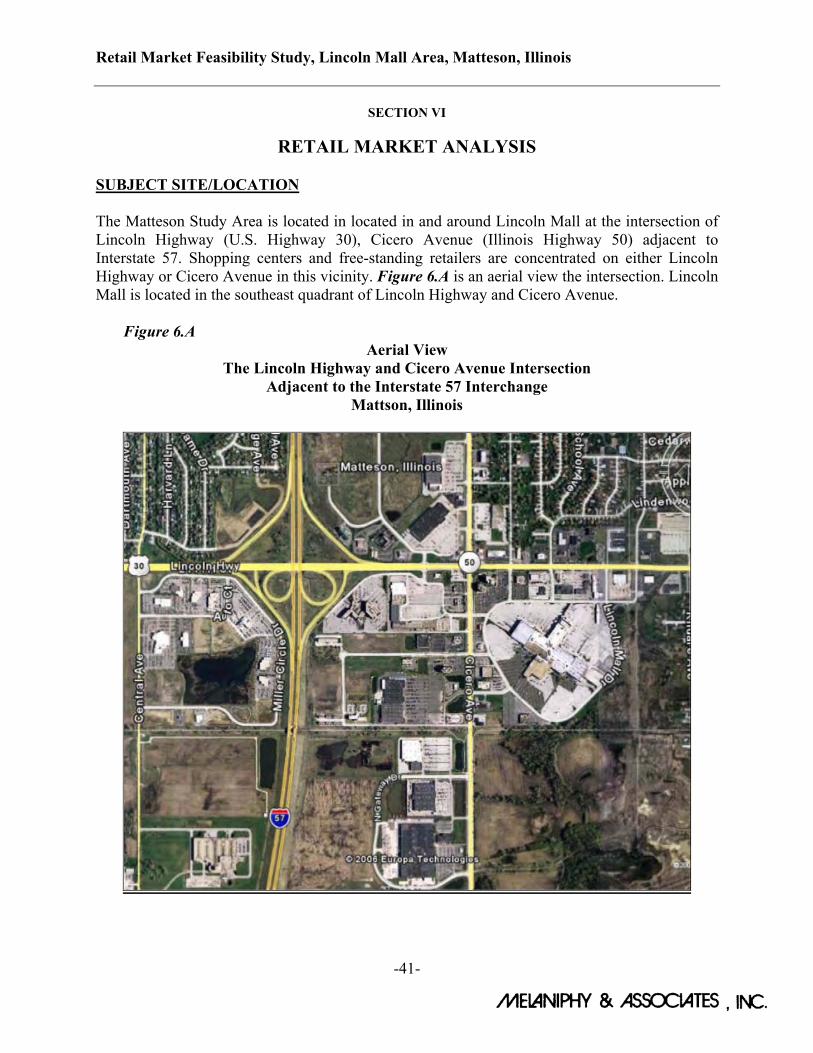

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-1-

SECTION I

ASSIGNMENT

Our assignment has been to undertake a Retail Market Feasibility Study in and around Lincoln Mall at the intersection of Lincoln Highway (U.S. Highway 30), Cicero Avenue (Illinois Highway 50), and Interstate 57 in Matteson, Illinois. Our study included the following: A. Preparation of a Market Feasibility Analysis which determined the extent of the current and

future retail market in and around Lincoln Mall. B. A review of the issue of the “dying Lincoln Mall” image. C. Investigation of the realty of the retail redlining issue, along with actions to eliminate the

issue. D. Determination of Matteson’s overall market penetration and by major retail categories. E. Identification of prospective stores that should be in the Lincoln Mall area retail

concentration. F. Preparation of action recommendations to address the image, market, and prospective new

tenants and big box retailers that can flourish and improve retailing and sales tax revenue in the Village

STUDY ASSUMPTIONS The project was carried out under the following assumptions: 1. No major malls, shopping centers, or major big box competitors, other than those identified

in this report will be constructed within the Primary or Secondary portions of the Trade Area. Any such development would require a reassessment of the conclusions and recommendations contained herein.

2. The economy of the United States will not experience another major recession or inflation

that would result in a significant adjustment in consumer spending or buying attitudes. 3. Gasoline prices will not consistently exceed $3.50 per gallon for an extended period of time.

If this occurs, significant changes may occur in shopping and spending patterns. 4. The United States will not expand the current war on terrorism or escalate military operations

overseas, nor will the United States experience any major catastrophe or terrorist act that would interrupt shopping, driving, mail delivery, or spending patterns.

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-2-

5. A considerable amount of data has been gathered, sorted, and analyzed. Much of the data

has come from agencies of federal, state, county, and the Village of Matteson, along with local real estate companies. Additionally, secondary sources have been utilized, where pertinent. Where possible, our staff has examined the information for its validity and authenticity. Since we have no way of controlling the development of these data sources, we take no responsibility for any inaccuracy. During the course of the study program we have utilized standard statistical techniques involving both subjective and objective judgments in order to arrive at the conclusions and recommendations.

6. We certify that we have no present of prospective interest in the properties in the Matteson

area that are the subject of this report and we have no personal interest or bias with respect to the parties involved. Our compensation is not contingent upon any action or event resulting from this analysis, opinions, or conclusions, in or use of this report.

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-3-

SECTION II

EXECUTIVE SUMMARY The conclusions and recommendations resulting from this market study are contained throughout this report. However, for convenience, this section of the report summarizes our findings. GENERAL FINDINGS 1. Matteson is a dynamic retail Chicagoland suburb. While Matteson only has a population

of approximately 15,000 people, the Community’s retail sales are the 16th largest in the metropolitan area. In 1998, Matteson was in the 21st position with sales of $440 million. In 2005, Matteson’s retail sales amounted to approximately $804.7 million. The sales were down slightly from the 2004 sales of $804.8, but up from the 2003 retail sales of $789.9 million according to the Illinois Department of Revenue, Sale Tax Receipt reports.

2. Matteson has over 2,700,000 square feet of retail space, including Lincoln Mall, numerous

other shopping centers, and large big box stores. 3. Matteson’s population size has been more of a limiting factor in retail sales growth,

than retailer store interest. The Village has a population of approximately 15,000 and a Primary Trade Area population of 151,534 persons. Most major mall areas have higher population numbers. More population growth in Matteson and its adjacent suburbs will have a positive impact upon retail sales.

4. The Lincoln Mall Area has excellent access. Lincoln Highway (U.S. 30) is a major east-

west traffic artery extending from the Indiana-Illinois state line to Frankfort, Illinois and beyond. .Cicero Avenue (Illinois 50) is a major north-south artery that traverses most of the Chicagoland area. Interstate 57 connects the City of Chicago with Memphis, Tennessee and beyond. All of these routes contribute to the importance of retailing in Matteson.

5. Matteson’s current Average Household Income is estimated at approximately $72,500.

By 2010, Average Household Income is expected to rise to approximately $80,000. 6. The planned third Chicagoland Airport, should it be built, will add to the Matteson’s area

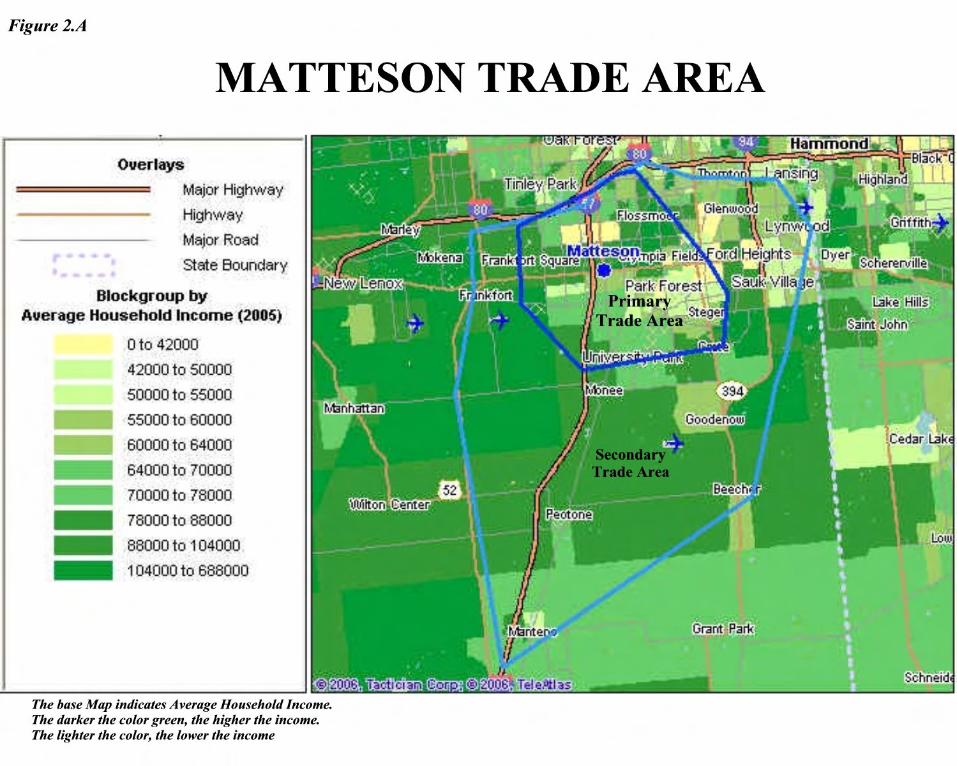

dynamics with new housing, jobs, and increased retail sales. CONCLUSIONS 1. Matteson’s Trade Area extends northward to Interstate 80, eastward to just beyond

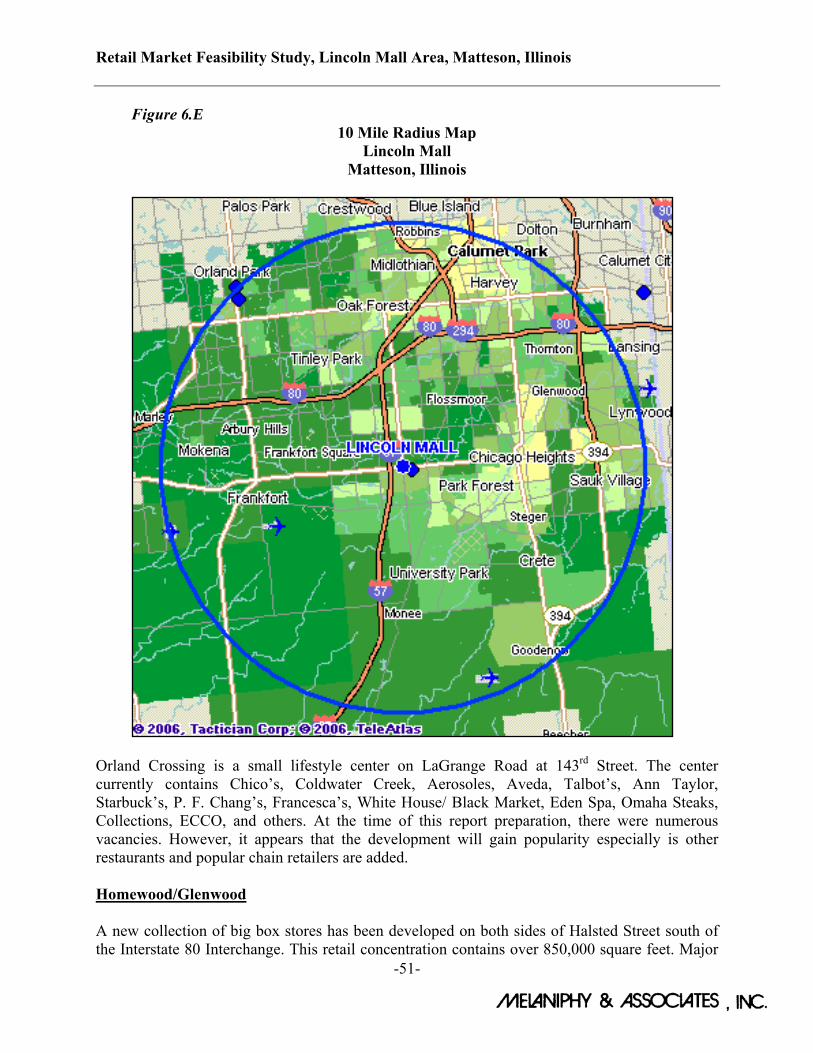

Illinois Highway 1, southward to Manteno, and westward to Frankfort. Matteson’s Trade Area is proscribed by major malls and retail concentrations in Orland Park, Homewood, Tinley, Park, Crestwood, Calumet City, and developing retail concentrations in Frankfort and Kankakee. Figure 2.A depicts the Total Trade Area of the Matteson retail concentration emanating from Lincoln Highway, Cicero Avenue and Interstate 57.

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-5-

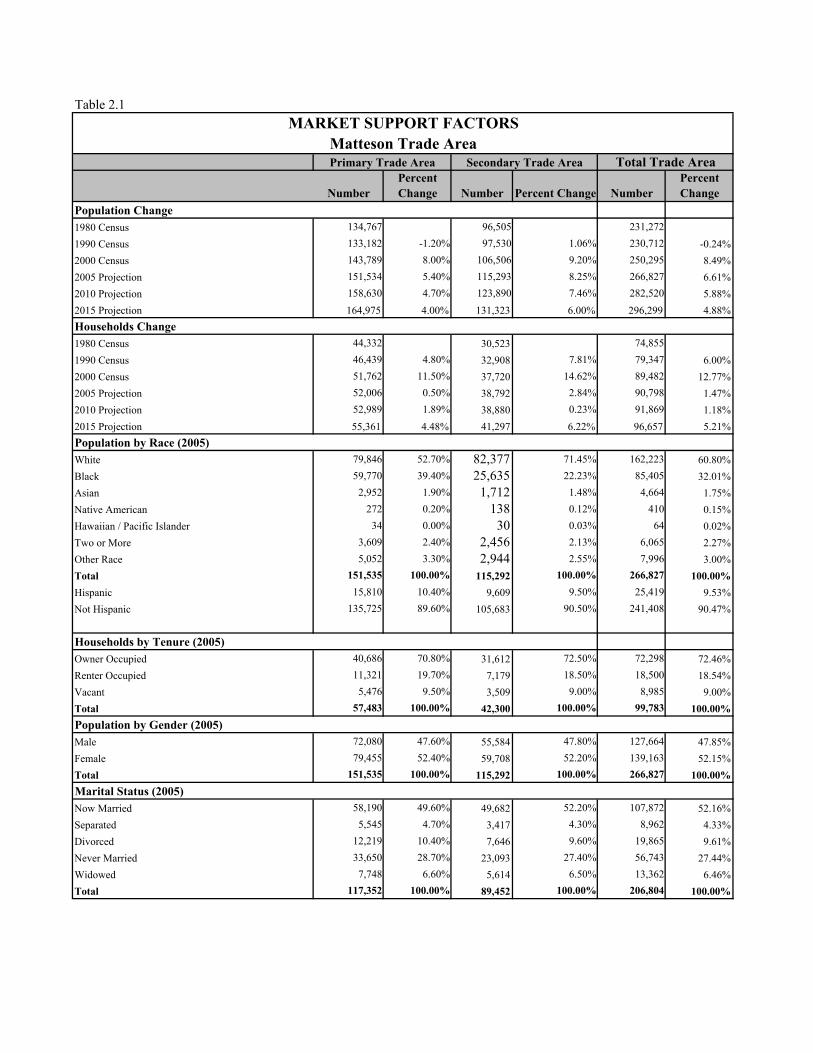

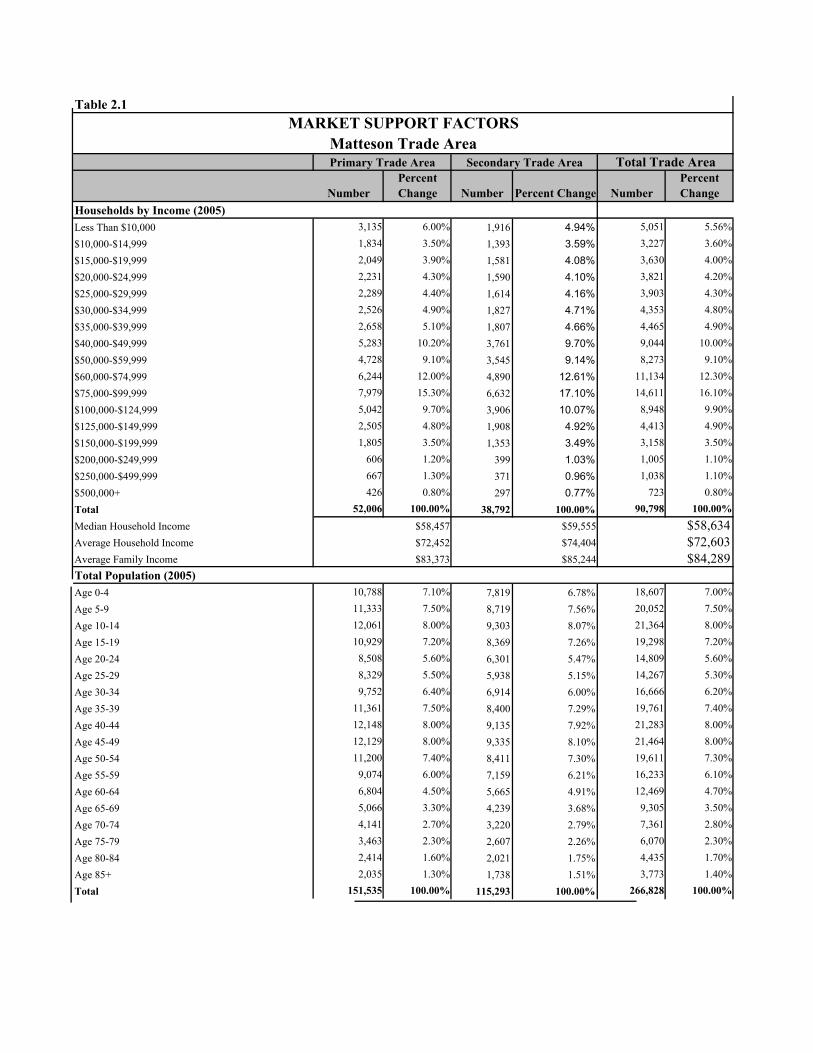

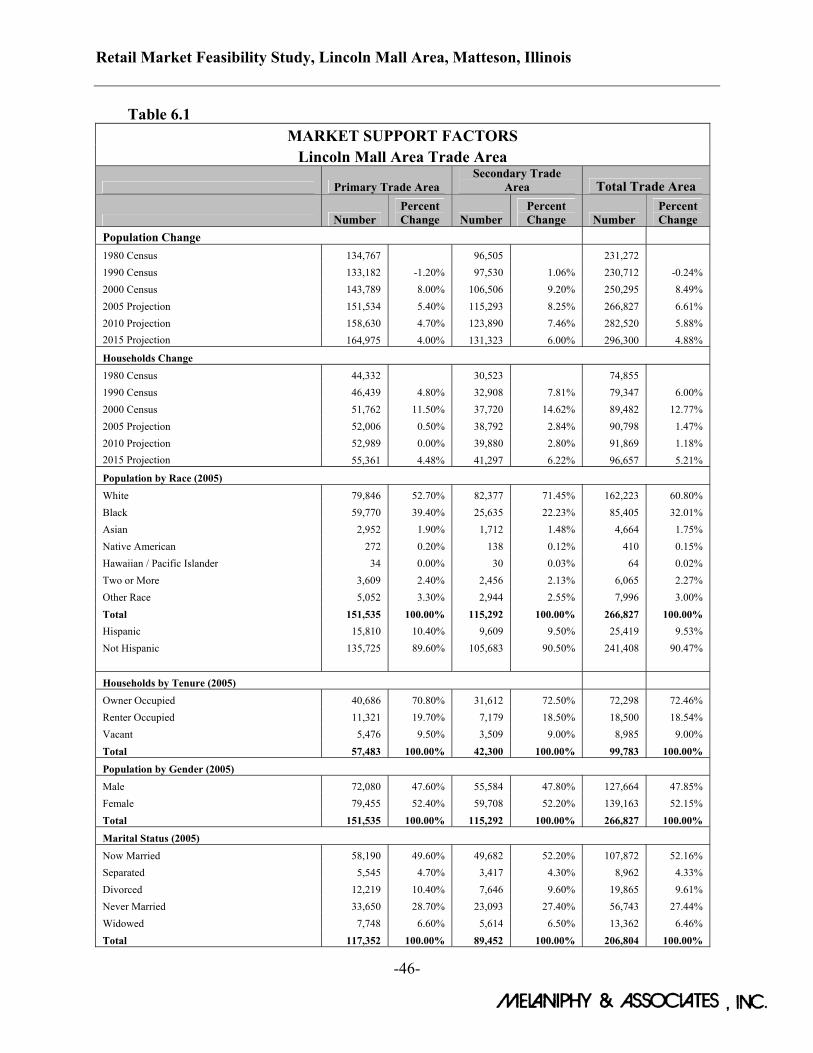

2. The Primary Trade Area, the segment from which the most frequent customers originate, has a current estimated population of 151,534 persons in 52,006 households. The Average Household Income is estimated at $72,452. By 2010, population of the Primary Trade Area is expected to rise to 158,630 persons in 51,989 households. Average Household Income is expected to rise to approximately $80,000. Table 2.1, entitled, Market Support Factors, provides demographic details for the Trade Area.

The Secondary Trade Area, represents that trade area segment where less frequent shoppers originate, contains a population of 115,293 persons in 38,792 households. The population is forecast to 123,890 persons by 2010 and 131,323 persons by 2015. The median age is moderately younger than the Primary Trade Area amounting to an estimated 36.2 years. The average annual household income within the Secondary Trade Area is slightly higher than the Primary Trade Area amounting to an estimated $74,404. Average household is expected to increase to an estimated $83,383 by 2010. The Total Trade Area, including both trade area segments, contains an estimated population of 266,827 persons in 90,798 households. By 2010, the population within the Total Trade Area is forecast to rise to 282,520 persons in 91,869 households, and by 2015 the population is forecast to rise to 296,300 persons in 96,657 households. The median age is 37.1 years.

3. Lincoln Mall, is not a dying Mall, rather it has been impacted by ever changing retail patterns. Like so many other malls, it had become too large for today’s consumer demand. The Mall has eliminated two department stores and is creating a power center along its newly designed internal roadway. Target will reportedly be the first major big box to relocate to the corner of Cicero Avenue and the Mall Road. Other smaller boxes will follow. The internal Mall Road connects Lincoln Highway at Kostner Avenue and extends along the south side of the Mall to Cicero Avenue.

The following major regional shopping centers have lost department stores and have had to adjust or downsize: Yorktown Center, Hawthorn Center, Old Orchard Center, Stratford Square, The Plaza, Gurnee Mills, Oak Brook Center, Northbrook Court, Charlestown Mall, Randhurst Center, North Riverside Park, Lincolnwood Towne Center, Lakehurst Mall (closed), Fax Valley Mall, Orland Park Place, Stratford Square Mall, and Chicago Ridge Mall. Thus, 16 out of the top 20 malls have had to replace at least one department store. Some have been more successful that others.

4. The Automobile category produces the highest retail sales and sales tax revenues in Matteson. In 2005, Automobile category sales amounted to $285.7 million out of total retail sales of $804.7 million. In 2004, Automotive category sales were $276.2 million.

Table 2.1MARKET SUPPORT FACTORS

Matteson Trade AreaTotal Trade Area

NumberPercent Change Number Percent Change Number

Percent Change

1980 Census 134,767 96,505 231,2721990 Census 133,182 -1.20% 97,530 1.06% 230,712 -0.24%2000 Census 143,789 8.00% 106,506 9.20% 250,295 8.49%2005 Projection 151,534 5.40% 115,293 8.25% 266,827 6.61%2010 Projection 158,630 4.70% 123,890 7.46% 282,520 5.88%2015 Projection 164,975 4.00% 131,323 6.00% 296,299 4.88%

1980 Census 44,332 30,523 74,8551990 Census 46,439 4.80% 32,908 7.81% 79,347 6.00%2000 Census 51,762 11.50% 37,720 14.62% 89,482 12.77%2005 Projection 52,006 0.50% 38,792 2.84% 90,798 1.47%2010 Projection 52,989 1.89% 38,880 0.23% 91,869 1.18%2015 Projection 55,361 4.48% 41,297 6.22% 96,657 5.21%

White 79,846 52.70% 82,377 71.45% 162,223 60.80%Black 59,770 39.40% 25,635 22.23% 85,405 32.01%Asian 2,952 1.90% 1,712 1.48% 4,664 1.75%Native American 272 0.20% 138 0.12% 410 0.15%Hawaiian / Pacific Islander 34 0.00% 30 0.03% 64 0.02%Two or More 3,609 2.40% 2,456 2.13% 6,065 2.27%Other Race 5,052 3.30% 2,944 2.55% 7,996 3.00%Total 151,535 100.00% 115,292 100.00% 266,827 100.00%Hispanic 15,810 10.40% 9,609 9.50% 25,419 9.53%Not Hispanic 135,725 89.60% 105,683 90.50% 241,408 90.47%

Owner Occupied 40,686 70.80% 31,612 72.50% 72,298 72.46%Renter Occupied 11,321 19.70% 7,179 18.50% 18,500 18.54%Vacant 5,476 9.50% 3,509 9.00% 8,985 9.00%Total 57,483 100.00% 42,300 100.00% 99,783 100.00%

Male 72,080 47.60% 55,584 47.80% 127,664 47.85%Female 79,455 52.40% 59,708 52.20% 139,163 52.15%Total 151,535 100.00% 115,292 100.00% 266,827 100.00%

Now Married 58,190 49.60% 49,682 52.20% 107,872 52.16%Separated 5,545 4.70% 3,417 4.30% 8,962 4.33%Divorced 12,219 10.40% 7,646 9.60% 19,865 9.61%Never Married 33,650 28.70% 23,093 27.40% 56,743 27.44%Widowed 7,748 6.60% 5,614 6.50% 13,362 6.46%Total 117,352 100.00% 89,452 100.00% 206,804 100.00%

Marital Status (2005)

Households by Tenure (2005)

Population by Gender (2005)

Households Change

Population by Race (2005)

Population Change

Primary Trade Area Secondary Trade Area

Table 2.1MARKET SUPPORT FACTORS

Matteson Trade AreaTotal Trade Area

NumberPercent Change Number Percent Change Number

Percent Change

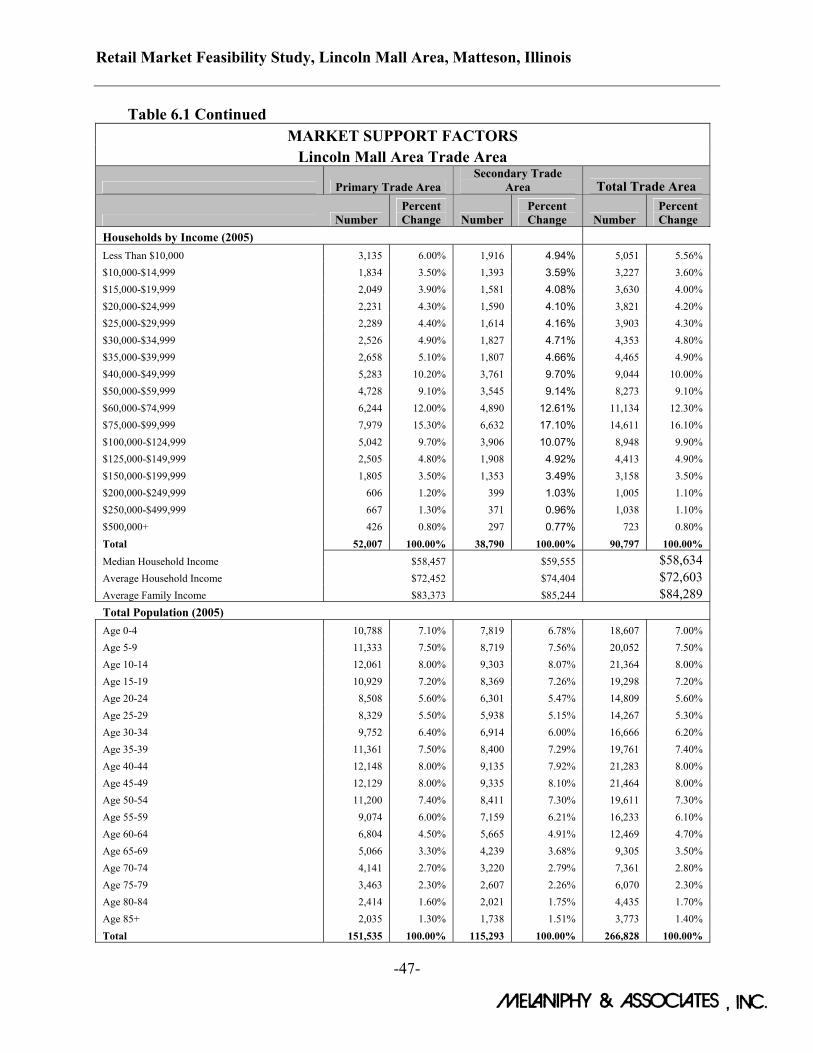

Less Than $10,000 3,135 6.00% 1,916 4.94% 5,051 5.56%$10,000-$14,999 1,834 3.50% 1,393 3.59% 3,227 3.60%$15,000-$19,999 2,049 3.90% 1,581 4.08% 3,630 4.00%$20,000-$24,999 2,231 4.30% 1,590 4.10% 3,821 4.20%$25,000-$29,999 2,289 4.40% 1,614 4.16% 3,903 4.30%$30,000-$34,999 2,526 4.90% 1,827 4.71% 4,353 4.80%$35,000-$39,999 2,658 5.10% 1,807 4.66% 4,465 4.90%$40,000-$49,999 5,283 10.20% 3,761 9.70% 9,044 10.00%$50,000-$59,999 4,728 9.10% 3,545 9.14% 8,273 9.10%$60,000-$74,999 6,244 12.00% 4,890 12.61% 11,134 12.30%$75,000-$99,999 7,979 15.30% 6,632 17.10% 14,611 16.10%$100,000-$124,999 5,042 9.70% 3,906 10.07% 8,948 9.90%$125,000-$149,999 2,505 4.80% 1,908 4.92% 4,413 4.90%$150,000-$199,999 1,805 3.50% 1,353 3.49% 3,158 3.50%$200,000-$249,999 606 1.20% 399 1.03% 1,005 1.10%$250,000-$499,999 667 1.30% 371 0.96% 1,038 1.10%$500,000+ 426 0.80% 297 0.77% 723 0.80%Total 52,006 100.00% 38,792 100.00% 90,798 100.00%

Median Household Income $58,634Average Household Income $72,603Average Family Income $84,289

Age 0-4 10,788 7.10% 7,819 6.78% 18,607 7.00%Age 5-9 11,333 7.50% 8,719 7.56% 20,052 7.50%Age 10-14 12,061 8.00% 9,303 8.07% 21,364 8.00%Age 15-19 10,929 7.20% 8,369 7.26% 19,298 7.20%Age 20-24 8,508 5.60% 6,301 5.47% 14,809 5.60%Age 25-29 8,329 5.50% 5,938 5.15% 14,267 5.30%Age 30-34 9,752 6.40% 6,914 6.00% 16,666 6.20%Age 35-39 11,361 7.50% 8,400 7.29% 19,761 7.40%Age 40-44 12,148 8.00% 9,135 7.92% 21,283 8.00%Age 45-49 12,129 8.00% 9,335 8.10% 21,464 8.00%Age 50-54 11,200 7.40% 8,411 7.30% 19,611 7.30%Age 55-59 9,074 6.00% 7,159 6.21% 16,233 6.10%Age 60-64 6,804 4.50% 5,665 4.91% 12,469 4.70%Age 65-69 5,066 3.30% 4,239 3.68% 9,305 3.50%Age 70-74 4,141 2.70% 3,220 2.79% 7,361 2.80%Age 75-79 3,463 2.30% 2,607 2.26% 6,070 2.30%Age 80-84 2,414 1.60% 2,021 1.75% 4,435 1.70%Age 85+ 2,035 1.30% 1,738 1.51% 3,773 1.40%Total 151,535 100.00% 115,293 100.00% 266,828 100.00%

Total Population (2005)$83,373 $85,244

$58,457 $59,555 $72,452 $74,404

Households by Income (2005)

Primary Trade Area Secondary Trade Area

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-8-

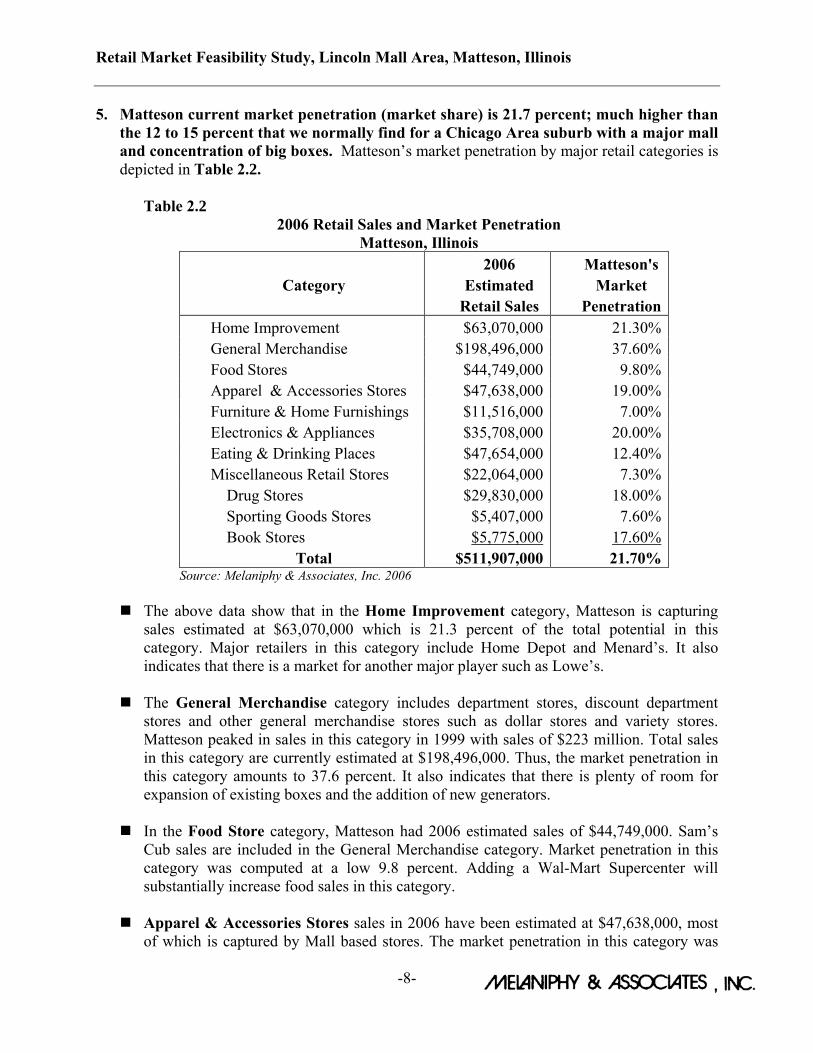

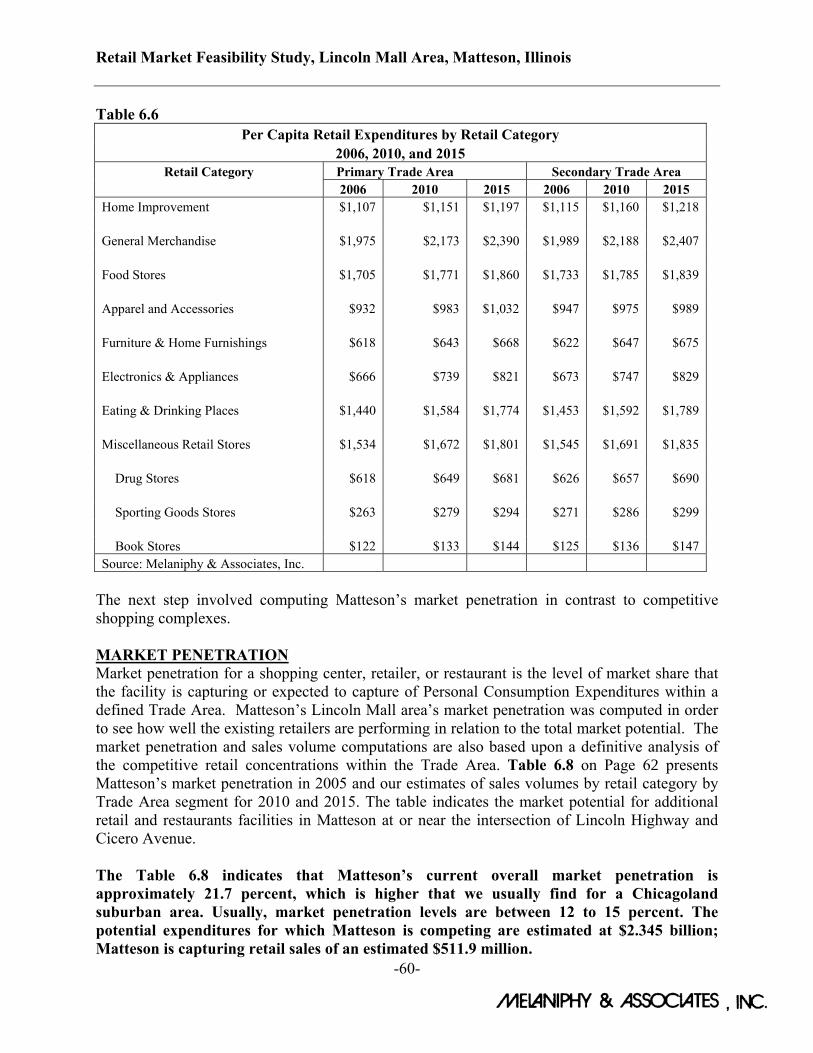

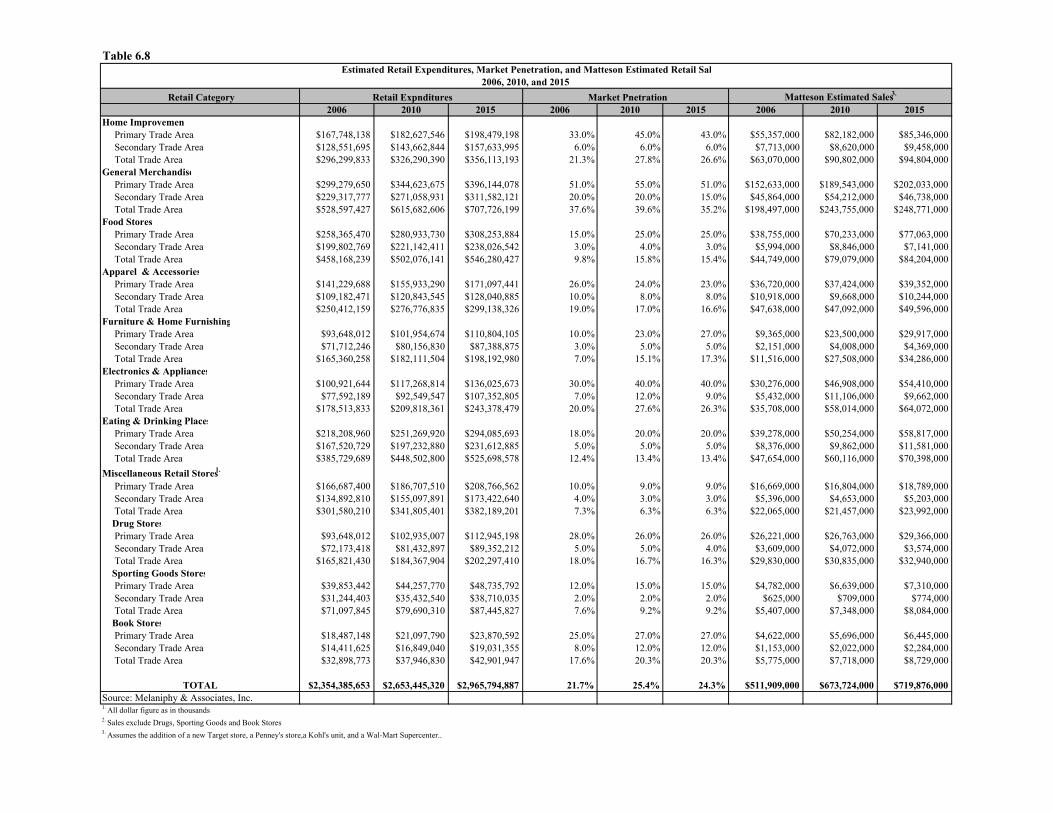

5. Matteson current market penetration (market share) is 21.7 percent; much higher than the 12 to 15 percent that we normally find for a Chicago Area suburb with a major mall and concentration of big boxes. Matteson’s market penetration by major retail categories is depicted in Table 2.2.

Table 2.2

2006 Retail Sales and Market Penetration Matteson, Illinois

2006 Matteson's Category Estimated Market

Retail Sales PenetrationHome Improvement $63,070,000 21.30%General Merchandise $198,496,000 37.60%Food Stores $44,749,000 9.80%Apparel & Accessories Stores $47,638,000 19.00%Furniture & Home Furnishings $11,516,000 7.00%Electronics & Appliances $35,708,000 20.00%Eating & Drinking Places $47,654,000 12.40%Miscellaneous Retail Stores $22,064,000 7.30% Drug Stores $29,830,000 18.00% Sporting Goods Stores $5,407,000 7.60% Book Stores $5,775,000 17.60%

Total $511,907,000 21.70% Source: Melaniphy & Associates, Inc. 2006

The above data show that in the Home Improvement category, Matteson is capturing

sales estimated at $63,070,000 which is 21.3 percent of the total potential in this category. Major retailers in this category include Home Depot and Menard’s. It also indicates that there is a market for another major player such as Lowe’s.

The General Merchandise category includes department stores, discount department stores and other general merchandise stores such as dollar stores and variety stores. Matteson peaked in sales in this category in 1999 with sales of $223 million. Total sales in this category are currently estimated at $198,496,000. Thus, the market penetration in this category amounts to 37.6 percent. It also indicates that there is plenty of room for expansion of existing boxes and the addition of new generators.

In the Food Store category, Matteson had 2006 estimated sales of $44,749,000. Sam’s

Cub sales are included in the General Merchandise category. Market penetration in this category was computed at a low 9.8 percent. Adding a Wal-Mart Supercenter will substantially increase food sales in this category.

Apparel & Accessories Stores sales in 2006 have been estimated at $47,638,000, most

of which is captured by Mall based stores. The market penetration in this category was

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-9-

computed at 19.0 percent. Today, a considerable portion of this category’s sales are captured by big box retailers.

The Furniture & Household Furnishings category had estimated 2006 sales of

$11,516,000 and a market penetration level of 7.0 percent. There is ample room in this category for additional stores. We have talked to Wickes Furniture regarding a new store in Matteson, and they have shown considerable interest doing so.

In the Electronics & Appliances category, we have estimated sales at $35,708,000,

which given both Best Buy and Circuit City in Matteson is low performance. The current level of market penetration is computed at 20.0 percent. One or both of the stores need to expand to capture a larger share of the potential sales.

The Eating & Drinking category has estimated sales captured by Matteson restaurants

and quick service facilities amounting to $47,654,000. This category’s market penetration is computed at 12.4 percent. We expect that there will be additional demand for new restaurants in Matteson, especially with the development of new major big boxes.

In the Miscellaneous Retail Stores category sales have been currently estimated at

$22,064,000. Stores in this category are normally concentrated in the Mall. Market penetration ahs been computed at 7.3 percent. There is a market for additional stores, however, it will not be met until the Mall has completed both external and internal improvements.

Sales in the Drug Store category are estimated at $29,830,000. Market penetration has been computed at 18.0 percent. Some of this market is picked up by Target and Wal-Mart.

In the Sporting Goods category sales have been estimated at $5,407,000. The market

penetration in this category has been computed at 7.60 percent.

Book Stores sales have been estimated at $5,775,000. Market penetration has been computed at 17.6 percent of potential in the Book Store category.

6. Matteson’s principal competition is located in Orland Park with Orland Square Mall,

plus every major big box with the exception of Ikea, Meijer, Costco, and a Wal-Mart Supercenter. Costco is seeking approval for a new store at 159th and LaGrange Road and Wal-Mart is seeking a Supercenter location in Orland Park. Meijer’s has a site ready to go at 143rd Street and Bell Road in Homer Glen, just west of Orland Park. In 2005, retailers in Orland Park captured retail sales exceeding $1.777 billion, up from $1.709 billion in 2004. General Merchandise sales in 2005 amounted to $258.2 million, down from $290.4 million in 2004, for a decrease of $32.2 million. Orland Park contains close to 6,000,000 square feet of retail space.

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-10-

7. A collection of big box retailers has been developed in Homewood and Glenwood on Halsted Street just north of Interstate 80. Boxes include Kohl’s, Target, Wal-Mart, Best Buy, Home Depot, Menard’s, Bed Bath & Beyond, Petco, JoAnn Fabrics, T.J. Maxx, and others. Homewood’s total retail sales in 2005 amounted to $377.2 million up slightly from $363.8 million in 2004.

8. A lifestyle center is currently being leased in Orland Park on LaGrange Road at

approximately 143rd Street. Lifestyle centers are a collection of popular specialty retailers and restaurants that together generate customers on a frequent basis, usually without department stores. Known as Orland Crossing, the center has the beginnings of a lifestyle center featuring Talbot’s, Coldwater Creek, Ann Taylor, Chico’s, Aveda, Aerosoles, along with Starbuck’s, P. F. Chang’s, Francesca’s, White House/ Black Market, Eden Spa, Omaha Steaks, Collections, ECCO, and others. There are numerous vacancies. Lifestyle centers generally require average household incomes above $80,000.

9. Matteson has more retail square feet in some categories than the market can support.

For example, the Apparel and Accessories category has had declining sales since 2002. Unfortunately, there is no simple solution to shifting consumer demand. Consumers are buying more of their apparel in big box stores and less in the Mall. The shift to casual attire has impacted many of these stores. The Miscellaneous Stores Category has also shown weakness. Since most of the stores in this category are located in the Mall, the center has been affected by stores leaving the Mall. The Mall needs to continue with its aggressive marketing plans to attract new stores, as well as improve the facility both in an out to make it more attractive.

10. There is an excess of small vacant retail and service store spaces in Matteson. The slow

down of Mall customer generation has had an impact upon small retailers. More retail dollars are being captured by big box retailers and fewer overall Personal Consumption Expenditures being captured by small retail shops. The market has shifted to services and foodservice. Furthermore, the focus of the market is shifted to Cicero Avenue from Lincoln Highway. Improvement to the Mall and increased retail sales will eliminate some, but not all of the vacancy.

11. Retailer redlining is not ethnic issue; rather it is a reaction to department store closings and the loss of some customer generation. Retailers that we talked to indicated that the market was smaller than other mall areas. Also, Penney’s closing bothered them. Nonetheless, most are interested to see what happens with the Mall redevelopment and new store additions. Matteson’s income is too high and there are too many stores planning expansion or new units to be redlining issue. It is important to get the message out the Matteson is an excellent market. Certainly, the big boxes are moving forward based upon their own experiences. The issue will become moot, as soon as Target opens its new store, Wickes opens a new store, and Wal-Mart announces and builds a Supercenter.

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-11-

RECOMMENDED ACTIONS 1. Lincoln Mall should continue to implement the power center development. When the

current redevelopment plans are complete, the Mall should implement a lifestyle component on the northeast side of the mall. Here, a cinema, restaurants, specialty stores, and entertainment should be added to create excitement. The Mall needs to renovate both the interior and exterior of the Mall. Added improvement in the area will help attract additional merchants.

2. We recommend that Matteson permit big box retailers to expand or build new stores,

such as Wal-Mart, Sam’s Club, and Menard’s, and generally assist in implementing new development plans. Also, encourage Penney’s, Kohl’s, Lowe’s, and Wickes to build new stores.

3. Either Best Buy or Circuit City needs a larger store. As the market penetration indicates one or both need to expand to increase sales. On a combined basis they are only capturing approximately 20 percent of the market in the Electronics & Appliance category.

4. We understand that a user is negotiating to buy the former Builders Square store on Lincoln Highway. We encourage the Village to assist in implementing this action. It will remove a large vacant store, add a viable user, and help to increase activity near many of the smaller shopping centers on Lincoln Highway.

5. Matteson needs to work on its retail image. Regular announcements regarding additions and improvements in Matteson should be communicated to the Chicago area new media. Also, the retail and shopping center media should be informed including Shopping Center Today, Shopping Center Business, Chain Store Age (Shopping Center Addition), Retail Traffic, Heartland Real Estate, Globe Street.Com, and others. Articles should be written regarding Matteson’s dynamics, Mall improvement, market penetration, and retail changes. The issues should be directed toward retailers, making them aware of Matteson’s pro-retailing environment.

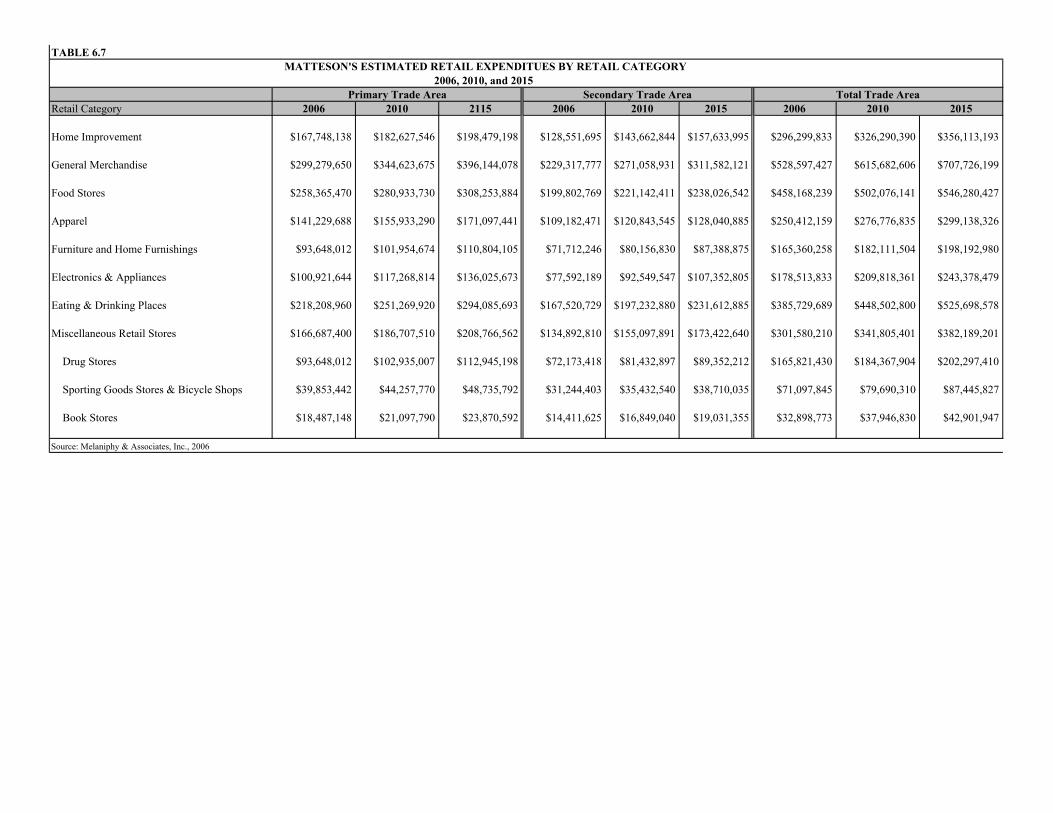

Estimated Retail Sales By Retail Category We have estimated retail sales by major retail category and compared the data to the sales actually being captured in the Village. Next, we simulated alternative retail store development scenarios to determine what was realistic. Finally, we estimated the retail sales that are likely should certain actions take place. These are discussed below by retail category. Table 2.3 at the end of Section II presents the potential expenditures by year, trade area segment, major retail category, market penetration percentages, and the estimated retail sales for 2010 and 2015. Home Improvement Matteson’s 2005 retail sales in this category were approximately $63 million. This results in a market penetration in this category estimated at 33 percent for the Primary Trade Area and

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-12-

21.3 percent for the Total Trade Area in relation to Home Improvement expenditures of $296.3 million. Menard’s and Home Depot are the major retailers in this category. Menard’s apparently would like to build a new larger store and it is very likely that Lowe’s will also want to enter this market. In 2010, the potential in this category is forecast to increase to $326.3 million. We forecast that the market penetration should rise to an estimated 27.8 percent, resulting in a sales potential in this category for the existing and added retailers amounting to $90.8 million. By 2015, sales are estimated to rise to approximately $94.8 million. General Merchandise The General Merchandise category includes department stores such as Carson’s and Sears and big box discounters including Wal-Mart, Target, and Value City. These stores generated sales of over $197.4 million in 2005 and are now estimated at $198.5 million. The market penetration in this category amounts to 37.6 percent. Target is planning to build a new store, Wal-Mart would like to build a Supercenter, Penney’s is looking in the market, and Kohl’s may eventually wish to be in this market segment. Our forecasts indicate that the market potential in 2010 in this category will amount to an estimated $615.7 million. We estimate the stores in this category can capture approximately 39.6 percent, resulting in estimated sales of $243.8 million. This assumes the both Sears and Carson’s continue to operate stores in the Mall. By 2015, the potential in General Merchandise is forecast to rise to $707.7 million. We estimate that the General Merchandise stores in Matteson can expect to capture approximately 35.2 percent of the potential, or sales amounting to an estimated $248.8 million. This assumes that Penney’s and Kohl’s enter the market segment and Target and Wal-Mart build new stores. Food Stores The current market penetration in the Food Store category is a low 9.8 percent. Sales in this category in 2005 were $43.4 million, or about $834,000 a week. That is the equivalent of two strong supermarkets. The potential in this category currently amounts to $458.2 million annually. It should be pointed out the Sam’s Club sales are included by the government in the General Merchandise category, so this category is understated. Wal-Mart would like to build a Supercenter which features food. We recommend that they be allowed to do so. The market potential in 2010 is estimated at $502.1 million. We estimate Matteson’s market penetration rise to 15.8 percent, resulting in Food sales of an estimated $79.1 million. By 2015, Food Store sales are estimated at $84.2 million with a market penetration of 15.4 percent.

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-13-

Apparel & Accessories Stores In 2005, Matteson captured retail sales in this category of $47.4 million. We estimate sales currently at $47.6 million, resulting in a market penetration of 19.0 percent. The majority of sales in this category are captured by Lincoln Mall. We have assumed that both Mall department stores will remain and improve their attraction. However, this category has had a difficult time throughout the country. Many stores in this category are affected by big box competition. In 2010, we estimate that sales in this category will be about the same at $47.1 million resulting in a market penetration of 17.0 percent. By 2015, we estimate that sales in this category will be approximately $49.5 million with a market penetration of 16.6 percent. Furniture & Home Furnishings Sales in this category in 2005 amounted to an estimated $11.0 million. The current potential in this category is estimated at $165.4 million, resulting in a current market penetration of 7.0 percent. The data indicate that there is a market in this category for one or two new furniture stores. In 2010, the market potential will increase to an estimated $182.1 million. Furniture stores in this market segment should be capable of capturing a market penetration of 15.1 percent, resulting in estimated retail sales of $27.5 million. By 2015, we estimate that the potential should rise to an estimated $198.2 million and with a market share of 17.3 percent; sales are estimated at $34.3 million. Wickes has already shown an interest in locating a new store in this area. Electronics and Appliances Sales in this category in 2005 amounted to approximately $35.0 million. Given a market potential in this category of an estimated $178.5 million, the market penetration currently amounts to an estimated 20.0 percent. The potential in this category in 2010 amounts to an estimated $209.8 million. We expect either Best Buy or Circuit to expand at there curren location or build a new store in this market area. Sales in this category are estimated at $58.0 million in 2010. In 2015, we expect sales to rise to $64.1 million based upon a market penetration of 26.3 percent. Eating & Drinking This category includes both restaurants and quick service food units (formerly fast-food). Sales in 2005 in this category amounted to $44.9 million. We currently estimate sales at $47.7 million for a market penetration of 12.4 percent based upon a market potential of $385.7 million. In 2010, we estimate that the market potential in this category will rise to an estimated $448.5 million. A considerable portion of these potential dollars are spent where people work and in restaurants outside the Matteson area. Nonetheless, we estimate that Matteson will have a market penetration in 2010 of approximately 13.4 percent, resulting in estimated sales of $60.1 million. By 2015, we estimate that market potential will rise to an estimated $552.7 million and Matteson facilities will capture approximately 13.4 percent, or $70.4 million.

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-14-

Drug Store and Miscellaneous Stores In 2005, this category had retail sales of $65.8 million, up over $10 million from 2004. In our analysis, we have separated the Drug store, Sporting Goods, Book, and Miscellaneous sales from the total category to better see current and future opportunities. Each will be discussed separately.

Drug Stores We estimate that Drug Stores are currently capturing sale amounting to approximately $29.8 million. The market potential in this category amounts to approximately $165.8 million, resulting in a market penetration of 18.0 percent. In the Primary Trade Area the market penetration amounts to 28 percent. By 2010, the potential in this category is forecast to rise to an estimated $184.4 million. Market penetration is expected to decline to 16.7 percent because of additional discount competition, resulting in estimated sales of $30.8 million. In 2015, our estimate of potential sales in this category amounts to $202.3 million, with Matteson capturing sales of 16.3 percent for sales of $32.9 million.

Sporting Goods Sales in this category are currently estimated at $5.4 million. Total market potential in the Sporting Goods category is estimated at $71.1 million, resulting in a market penetration of 7.6 percent. In 2010, we estimate that the market potential will rise to an estimated $79.7 million and with a market share of 9.2 percent; sales will rise to $7.3 million. In 2015, we estimate that the market potential will rise to $87.4 million and with a market share of 9.2 percent; stores in this category should capture sales of an estimated $8.1 million.

Book Stores Currently, we estimate that sales in this category are approximately $5.6 million. With a market potential of $32.9 million, the estimated market penetration is estimated at 17.6 percent. In 2010, we estimate that the market potential will rise to $37.9 million and with a market penetration of 20.3 percent will result in estimated sales of $7.7 million. In 2015, we estimate that the market potential will increase to $42.9 million and with a market penetration of an estimated 20.3 percent; sales are estimated to rise to $8.7 million.

Miscellaneous Retail Stores Sales in this category are currently estimated at $32.1 million of the potential of $301.6 million, resulting in a market penetration of 7.3 percent. By 2010, we estimate the market penetration will decline to approximately 6.3 percent because of big box competition, but potential will rise to $341.8 million because of growth and rising income. Thus, sales in this category are estimated at $21.5 million. By 2015, market potential is forecast to an estimated $382.2 million, resulting in estimated sales of $24.0 million with a market penetration of 6.3 percent.

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-15-

PROSPECTIVE MAJOR RETAILERS

We have evaluated the market potential and the opportunities for retailers not currently in the Matteson portion of the Chicago Metropolitan Area. Listed below are a suggest list of potential retailers.

Barnes & Noble Costco DSW Shoes Ashley Furniture Kohl’s Lowe’s Home Improvement Penney’s new free-standing stores Wickes Furniture Woodman’s Warehouse Foods Wal-Mart Supercenter

LIFESTYLE TENANTS IN LIFESTYLE CENTERS IN THE CHICAGO AREA WHO ARE NOT IN LINCOLN MALL

Lincoln Mall has contacted many of these retailers in an attempt to secure them for the Mall. Usually it takes three interested retailers or restaurants at the same time to get the attention of others. We encourage repeated attempts to obtain some lifestyle tenants. It will be necessary to create and environment that appeals to their objectives. Redevelopment of the former department store at the east end of the Mall into a lifestyle component featuring lifestyle retailers, restaurants, cinema, and entertainment segment would have a positive impact upon the Mall. Some of the lifestyle tenants normally found in lifestyle centers are as follows.

Lifestyle Tenants Abercrombie & Fitch American Eagle Outfitters Ann Taylor and Ann Taylor Loft Anthropologie April Cornell Banana Republic Barnes and Noble Bombay & Bombay Kids Build-A-Bear Chico’s Coach Coldwater Creek Crate & Barrel Eddie Bauer Gap, Baby Gap, Gap Kids Dick’s Sporting Goods H & M

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-16-

Lifestyle Tenants (Continued) Hollister Co. Hot Topic’s J Crew Jos. A. Bank Pottery Barn and Pottery Barn Kids Restoration Hardware Smith & Hawken Steve Madden Talbot's, Talbot's Petites, Talbot's Woman Tommy Bahama Trader Joe’s Williams-Sonoma Yankee Candle Company Z Gallerie Cinema’s

Lifestyle Restaurants The Cheesecake Factory Brio Tuscan Grille P. F. Chang’s China Bistro California Pizza Kitchen Claddagh Irish Pub Cold Stone Creamery Noodles & Company Corner Bakery Café Big Bowl Asian Kitchen Maggiano’s Little Italy Potbelly Sandwich Works Romano’s Macaroni Grill Rockfish Seafood Grill Bar Louis Max & Irma’s

MATTESON’S SHOPPING CENTERS The following are a list of Matteson area shopping centers located principally on Lincoln Highway. They vary in size and condition. Some are aggressive and others are passive, simply waiting for a retailer or service store to call. In this environment, one cannot sit and wait; one must be aggressive a go after retailers. Below is a brief discussion of centers in Matteson other than Lincoln Mall.

Matteson Towncenter is located in the southwest quadrant of Cicero Ave & Lincoln Highway containing 229,041 square feet. The shopping center currently contains Pets Mart,

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-17-

Office Max, Fashion Bug, Old Country Buffet and others. Toys R Us is a separate property, as is Applebee’s and Fuddruckers. A site fronting on Cicero Avenue at the center’s traffic light is being readied for development. The shopping center owner is preparing a redevelopment plan for the shopping center which includes a realigned internal roadway. When complete, it will be submitted to the Village. We encourage Village assistance for this strategic location at the Interstate 57, the Matteson Gateway.

Century Tile Plaza at 20909 S. Cicero Avenue on the east side of Cicero Avenue contains

approximately 49,600 square feet. The primary tenant is Century Tile and a medical office. The vacancies are small store spaces which today are difficult to lease. The owners current focus should be toward service stores and small offices. The supply of small retailers is limited are they are more oriented toward Lincoln Highway. Also, seeing that traffic on Cicero Avenue north of Lincoln Highway is often oriented toward Home Depot, retail stores and service shops that are more men oriented would be best. Furthermore, northbound shoppers who are not destined for Home Depot are leaving the shopping area. Service oriented shops that can be on the back-side of a shopping trip should be considered.

Matteson Town Center is located on the northwest corner of Lincoln Highway and Cicero

Avenue. The center contains approximately 157,885 square feet. Tenants include Border’s Books, Sportmart, Linens ‘N Things, Marshalls, Mattress World, Harris Bank, Panera Bread Company, and others.

Liberty Plaza is located at 4555 Lincoln Highway and contains approximately 64,600

square feet. The center fronts on the south side of Lincoln Highway in front of the Mall and has access to the Mall parking lot. Chernin’s Shoes is the principal retail generator. Ownership has an approximately 22,500 square foot site for development. This is a difficult size for individual retailers and will probably necessitate dividing the space for two or more users. The expansion of Wal-Mart and Menards and the relocation of Target, as well as other retail change should have a positive affect upon this shopping center. Moreover, ownership is focused upon addressing the vacancy and development opportunity.

Matteson Plaza, located in the southwest quadrant of Lincoln Highway and Governor’s

Highway at 4243 Lincoln Highway, contains approximately 280,000 square feet. Major tenants include Dominick’s Finer Foods, Michaels, and Value City Department Store. The center was adversely affected by Safeway’s acquisition of Dominick’s and the changes which they instituted which adversely affected the consumer. Value City has not provided the customer generation expected. They are being affected by Wal-Mart. There are considerable vacancies in the center.

Centel Plaza is located on Lincoln Highway at 4331 W. 211th Street and contains

approximately 23,000 square feet. The principal tenant is Hancock Fabricas. There are approximately 9,000 square feet vacant. As with many of the other centers, filling the small spaces is difficult. The market is primarily for service uses and some small retailers who are not competing directly with the big box retailers. Furthermore, many small centers are avoided because of difficult access. Finally, the vacant former Builder’s Square has been an

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-18-

eyesore. It is our understanding that there may be a buyer and user for the Builder’s Square building. If so, it would have a positive impact upon this area and this center.

The Marketplace Plaza is located on the north side of Lincoln Highway at 4200 211th Street

and contains approximately 309,800 square feet. Principal tenants include Cub Foods, Burlington Coat Factory, A. J. Wright, Aronson’s Furniture, and others. This center has had some retail turnover even though that it has some generative retailers. This is a reflection of the excessive amount of vacant small retail space in Matteson. The market for small spaces is over built. Nonetheless, the amount of traffic on Lincoln Highway will continue to increase and offer opportunities for other retailers and service stores.

Lincoln Square shopping center is located at 4431 W. 211th Street in Matteson and contains

approximately 25,000 square feet. The largest store of approximately 8,000 square feet is currently vacant. Pepe’s Mexican Restaurant is the second largest store. The are other small store vacancies. Here again, the market is producing a limited number of small store retail and service tenants. The focus should be on service and foodservice. That is where the most possibilities will occur.

Rose Plaza is located at 4700 W. 211th in Matteson and contains approximately 25,000

square feet with no vacancies. Should vacancies occur, the focus should be toward retail and service.

The Former Builder’s Square on the north side of Lincoln Highway has remained vacant for several years. The unit contains approximately 90,000 square feet and 450 parking spaces. One of the problems of this property is access. The site does not have a traffic light making it difficult to get out of the property. Also, because of the Creek/Retention Area at the frontage of the property the entry is steep, making it more difficult to enter and exit the property. It is our understanding that a user has expressed an interest in the property. The Village should encourage the redevelopment of the property.

The Village staff should continue to participate in International Council of Shopping Centers

(ICSC) meetings and other development and redevelopment workshops and seminars to develop contacts, networking, and identifying possible retailers for Matteson. Also, to carry the message of how well Matteson is doing with its dynamic market.

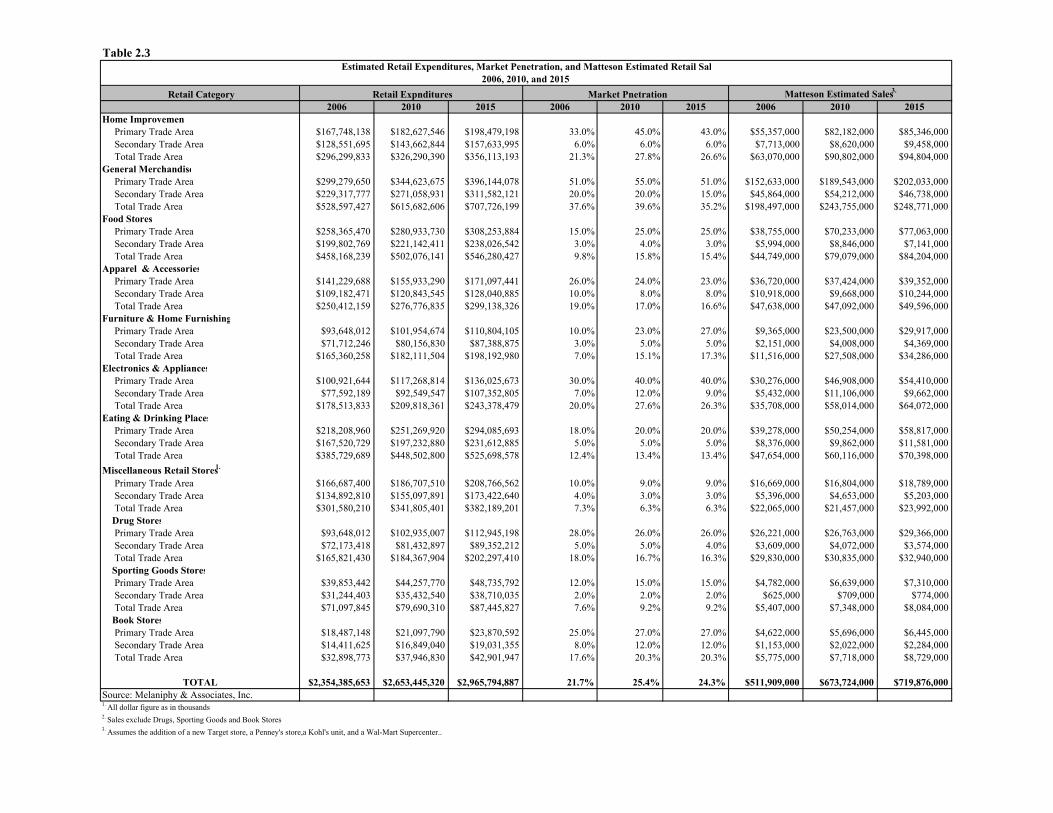

Table 2.3Estimated Retail Expenditures, Market Penetration, and Matteson Estimated Retail Sal

2006, 2010, and 2015

Retail Category Retail Expnditures Market Pnetration Matteson Estimated Sales3.

2006 2010 2015 2006 2010 2015 2006 2010 2015Home Improvemen Primary Trade Area $167,748,138 $182,627,546 $198,479,198 33.0% 45.0% 43.0% $55,357,000 $82,182,000 $85,346,000 Secondary Trade Area $128,551,695 $143,662,844 $157,633,995 6.0% 6.0% 6.0% $7,713,000 $8,620,000 $9,458,000 Total Trade Area $296,299,833 $326,290,390 $356,113,193 21.3% 27.8% 26.6% $63,070,000 $90,802,000 $94,804,000General Merchandise Primary Trade Area $299,279,650 $344,623,675 $396,144,078 51.0% 55.0% 51.0% $152,633,000 $189,543,000 $202,033,000 Secondary Trade Area $229,317,777 $271,058,931 $311,582,121 20.0% 20.0% 15.0% $45,864,000 $54,212,000 $46,738,000 Total Trade Area $528,597,427 $615,682,606 $707,726,199 37.6% 39.6% 35.2% $198,497,000 $243,755,000 $248,771,000Food Stores Primary Trade Area $258,365,470 $280,933,730 $308,253,884 15.0% 25.0% 25.0% $38,755,000 $70,233,000 $77,063,000 Secondary Trade Area $199,802,769 $221,142,411 $238,026,542 3.0% 4.0% 3.0% $5,994,000 $8,846,000 $7,141,000 Total Trade Area $458,168,239 $502,076,141 $546,280,427 9.8% 15.8% 15.4% $44,749,000 $79,079,000 $84,204,000Apparel & Accessories Primary Trade Area $141,229,688 $155,933,290 $171,097,441 26.0% 24.0% 23.0% $36,720,000 $37,424,000 $39,352,000 Secondary Trade Area $109,182,471 $120,843,545 $128,040,885 10.0% 8.0% 8.0% $10,918,000 $9,668,000 $10,244,000 Total Trade Area $250,412,159 $276,776,835 $299,138,326 19.0% 17.0% 16.6% $47,638,000 $47,092,000 $49,596,000Furniture & Home Furnishing Primary Trade Area $93,648,012 $101,954,674 $110,804,105 10.0% 23.0% 27.0% $9,365,000 $23,500,000 $29,917,000 Secondary Trade Area $71,712,246 $80,156,830 $87,388,875 3.0% 5.0% 5.0% $2,151,000 $4,008,000 $4,369,000 Total Trade Area $165,360,258 $182,111,504 $198,192,980 7.0% 15.1% 17.3% $11,516,000 $27,508,000 $34,286,000Electronics & Appliances Primary Trade Area $100,921,644 $117,268,814 $136,025,673 30.0% 40.0% 40.0% $30,276,000 $46,908,000 $54,410,000 Secondary Trade Area $77,592,189 $92,549,547 $107,352,805 7.0% 12.0% 9.0% $5,432,000 $11,106,000 $9,662,000 Total Trade Area $178,513,833 $209,818,361 $243,378,479 20.0% 27.6% 26.3% $35,708,000 $58,014,000 $64,072,000Eating & Drinking Places Primary Trade Area $218,208,960 $251,269,920 $294,085,693 18.0% 20.0% 20.0% $39,278,000 $50,254,000 $58,817,000 Secondary Trade Area $167,520,729 $197,232,880 $231,612,885 5.0% 5.0% 5.0% $8,376,000 $9,862,000 $11,581,000 Total Trade Area $385,729,689 $448,502,800 $525,698,578 12.4% 13.4% 13.4% $47,654,000 $60,116,000 $70,398,000

Miscellaneous Retail Stores1. Primary Trade Area $166,687,400 $186,707,510 $208,766,562 10.0% 9.0% 9.0% $16,669,000 $16,804,000 $18,789,000 Secondary Trade Area $134,892,810 $155,097,891 $173,422,640 4.0% 3.0% 3.0% $5,396,000 $4,653,000 $5,203,000 Total Trade Area $301,580,210 $341,805,401 $382,189,201 7.3% 6.3% 6.3% $22,065,000 $21,457,000 $23,992,000 Drug Stores Primary Trade Area $93,648,012 $102,935,007 $112,945,198 28.0% 26.0% 26.0% $26,221,000 $26,763,000 $29,366,000 Secondary Trade Area $72,173,418 $81,432,897 $89,352,212 5.0% 5.0% 4.0% $3,609,000 $4,072,000 $3,574,000 Total Trade Area $165,821,430 $184,367,904 $202,297,410 18.0% 16.7% 16.3% $29,830,000 $30,835,000 $32,940,000 Sporting Goods Stores Primary Trade Area $39,853,442 $44,257,770 $48,735,792 12.0% 15.0% 15.0% $4,782,000 $6,639,000 $7,310,000 Secondary Trade Area $31,244,403 $35,432,540 $38,710,035 2.0% 2.0% 2.0% $625,000 $709,000 $774,000 Total Trade Area $71,097,845 $79,690,310 $87,445,827 7.6% 9.2% 9.2% $5,407,000 $7,348,000 $8,084,000 Book Stores Primary Trade Area $18,487,148 $21,097,790 $23,870,592 25.0% 27.0% 27.0% $4,622,000 $5,696,000 $6,445,000 Secondary Trade Area $14,411,625 $16,849,040 $19,031,355 8.0% 12.0% 12.0% $1,153,000 $2,022,000 $2,284,000 Total Trade Area $32,898,773 $37,946,830 $42,901,947 17.6% 20.3% 20.3% $5,775,000 $7,718,000 $8,729,000

TOTAL $2,354,385,653 $2,653,445,320 $2,965,794,887 21.7% 25.4% 24.3% $511,909,000 $673,724,000 $719,876,000Source: Melaniphy & Associates, Inc.1. All dollar figure as in thousands2. Sales exclude Drugs, Sporting Goods and Book Stores 3. Assumes the addition of a new Target store, a Penney's store,a Kohl's unit, and a Wal-Mart Supercenter..

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-20-

SECTION III

METHODOLOGY

Our basic approach has been to identify the forces of supply and demand that either directly or indirectly affect retail market potential in Matteson in and around Lincoln Mall over the projection period. The market forces include population, population change, households, age structure, family size, household income, employment, shopping habits and patterns, retail sales, existing and proposed competitive facilities, directional growth patterns, accessibility within the market area, consumer expenditure dynamics, and finally, the share of the market that Matteson might capture overall and by major retail categories. In order to arrive at a determination of the retail market potential, we have carried out a number of research steps. They are summarized below: 1. An analysis was undertaken of trends taking place in retailing and consumer patterns

nationally, regionally, and, more specifically, in the Matteson area. 2. A search was conducted of published and unpublished data regarding population, population

projections, income, housing, employment, expenditures, retail sales, traffic counts, competition, shopping habits and patterns, consumer preferences, and other data pertinent to this analysis. Sources included:

United States Department of Commerce; Bureau of the Census, Census of Population:

1990 and 2000 United States Department of Commerce; Census of Retail Trade and Foodservice, 1997

and 2002 State of Illinois - Department of Revenue, Annual Sales Tax Receipt Reports – 2000

through 2005 State of Illinois - Department of Transportation (IDOT) State of Illinois - Department of Employment Security (IDES) Northeastern Illinois Regional Planning Commission (NIPC) Matteson Area Chamber of Commerce (MACC) Matteson Department of Economic Development Chicago Southland Chamber of Commerce Chicago Southland Convention and Visitors Bureau Cook County Planning Department Cook County Division of Transportation Chicagoland Retail Guide International Council of Shopping Centers (ICSC) Mid America Real Estate – Annual Shopping Center Development Report CB Richard Ellis Retail report Forrester Research Shopping Centers Today Shopping Center Business

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-21-

Crain’s Chicago Business Chicago Tribune The Daily Herald www.Globest.com The Melaniphy Commercial Newsletters Claritas, Inc. Tactician, Inc.

3. Members of our staff visited the Subject Area and toured the Village of Matteson and

surrounding communities. We also drove all of the major and many of the minor traffic arteries in and around the Village. Notes were taken regarding housing, schools, parks, commercial facilities, socio-economic levels, employers, and general physical conditions.

4. A senior member of our staff met with Lincoln Mall representatives to discuss the Mall and

the current redevelopment efforts. Mall ownership was helpful in providing performance data, customer characteristics, and trade area coverage.

5. Lincoln Mall executives provided us with a zip code distribution of the Mall’s trade area

determined from an analysis of the department stores sales activity. We obtained additional confidential trade area from other retailers with the provision that we keep their data confidential. We utilized the trade area data within the parameters of confidentially in determining the future trade area of the entire Lincoln Mall, Cicero Avenue, Lincoln Highway, and Interstate 57 interchange retail concentration.

6. Members of our staff either met or discussed via telephone with many of the owners or

managers of existing shopping centers in Matteson. 7. Accessibility was analyzed in terms of ingress and egress to the intersection, Lincoln Mall,

and many of the shopping centers in the area. Also, we reviewed traffic flow and driving times.

8. A Driving Time Analysis was conducted from the Subject Site for 20 minutes in all

directions by 5 minute intervals. The locations reached were recorded and plotted on maps to simulate the experience that shoppers would have in driving to the Study Area. Generally, speed limits were observed except where all traffic was moving beyond the posted speed limits. The objective was to simulate distances to competitive facilities, experience any physical or psychological barriers, and to better understand the overall market area.

9. The socioeconomic characteristics of the Matteson area were evaluated and the changes

which have taken place, determined. The 2000 Census of Population was evaluated. The socioeconomic characteristics include: population, population growth, age structure, household characteristics, income dynamics, ethnic mix, employment, employment change, housing values, retail expenditure potential, and retail sales trends.

10. Members of our staff inventoried the existing and proposed competitive retail facilities that

affect the market at the Subject Site. The evaluation identified the characteristics of shopping

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-22-

centers within the Trade Area including their location, size, tenant mix, degree of success, and general impact of competitive facilities. We also identified proposed retail facilities. This includes proposed shopping centers and freestanding retailers including their location, size, timing, major anchors, and anchor sizes.

11. We delineated the Trade Area for the Subject Intersection on the basis of the 2000 Population

and Housing Census, estimated 2005 demographic characteristics, the existing and proposed retail facilities, the road network, physical and psychological barriers, the detailed driving time analysis, consumer orientation, and our over 40 years of experience in evaluating projects throughout the world.

12. Once the Trade Area was delineated, we evaluated the 2000 Census of Population and

Housing to determine the level of market support available within the Trade Area. Next, we examined the population data and projections from two computer demographic services ─ Claritias, and Tactician. Finally, based upon our local demographic findings, we forecast the demographics of the Trade Area and its subsectors for 2005, 2010, and 2015. Demographics include population, age structure, population growth, households, household size, household income, and other pertinent elements.

13. We analyzed current household income, along with the changes which have taken place since

the 1990 and 2000 Census. Moreover, household income was forecast for 2005, 2010, and 2015.

14. Retail sales data was obtained and studied. The initial data included the Census of Retail

Trade and Foodservice for Matteson for 1997 and 2002 (the latest Census data available). Next, we analyzed the Illinois Department of Revenue Sales Tax Receipt data for Matteson, by retail category from 2003 to 2005. This assisted in determining the changes that had taken place both in total retail sales and major retail categories. Next, we converted the data to a per capita basis and applied our findings to determine the total retail market potential for the Trade Area in 2005, 2010, and 2015. This process permitted us to identify retail categories which represent a future development opportunity for the Village.

15. We calculated the Trade Area resident's Personal Consumption Expenditures by retail store

category. These data were forecast for the projection years. Personal Consumption Expenditures include General Merchandise (including Department stores and big box discounters), Food Stores, Eating and Drinking Places, Women’s Apparel and Accessories, Men’s Apparel and Accessories, Family Apparel, Children’s Apparel, Furniture and Household Furnishings, Appliances including TV and Electronics, Home Improvement, Drugs and Miscellaneous stores, and others. These data represent the dollars spent by Trade Area residents in retail facilities in and around the Matteson Area and were computed for 2005, 2010, and 2015.

16. Based upon the potential expenditures for the projection years, we first determined

Matteson’s current market penetration for the various retail categories within the Trade Area segments. Next, we forecast potential expenditures for the projection years and estimated the market penetration that the Village might capture if the recommended improvements and

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-23-

retailer additions are implemented. The market penetration or capture rates, when applied to the retail sales potential by retail category, provide sales projections by retail category for the Subject Site for 2010 and 2015.

17. Once the expenditure potential and market penetration by individual retail categories were

computed, our staff identified the retail categories which represent an opportunity for the Village. The objective was to identify market opportunities in individual retail categories and then consider specific retailers that "could fill the void". This included an evaluation of the current placement of major retailers in the Trade Area and their respective locations in relation to the Subject Site.

18. We determined the market for retail development in Matteson. Our staff analyzed present and

future trends affecting retail development in Matteson and the likelihood of attracting new retail businesses to the Subject Area.

19. A simulation of alternative retail development improvements was undertaken. This involved

simulating possible market capture rates for varying types of retail development on the Subject Site.

20. Finally, action recommendations were prepared for the Village as a guide to improving the

market for retail, restaurant, and shopping center development. This included the type of development that the market will support; possible phasing of the development; the sales that can be expected in 2006, 2010, and 2015; the types of stores that can be supported; and some of the retailers who should be the center of focus.

DEFINITIONS The following definitions have been gathered from the International Council of Shopping Centers, the National Retail Federation, The Selection of Retail Locations, Market Research for Shopping Centers, Restaurant and Fast Food Site Selection, The Restaurant Site Selection Guidebook, Urban Land Institute’s, The Dollars and Cents of Shopping Centers, the International Council of Shopping Centers’ Dictionary of Shopping Center Terms, and from our own experience over the past 40 years of evaluating markets for retailers and shopping center developers.

A Major Mall or Center can be either open or enclosed and contains at least two department stores anchoring the addition of numerous specialty stores. Malls usually range in size between 400,000 and 1,500,000 square feet. Lincoln Mall falls into this category.

A Super Regional Mall or Center usually range between 1,500,000 and 1,750,000 square

feet with four or more department stores with over 150 specialty stores, food court operators, and restaurants.

Lifestyle Centers usually are a collection of apparel, home, accessory, entertainment, and

other specialty stores located in upper middle or upper income areas along with both quick service and full service restaurants ranging in size from 200,000 to 800,000 square feet.

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-24-

Most do not contain department stores. Presently, there are no lifestyle centers in the South Bend area.

Community Centers are usually older centers with an old Kmart or some other major retail

generator along with a mix of retail stores and service shops. They range in size from 100,000 to 350,000 square feet. Many however have either been converted to Power Centers or have considerable vacancies.

Power Centers or Power Towns are usually a collection of Big Box retailers including

discounters, home improvement, book stores, appliance stores, pet stores, supermarkets, warehouse and club stores, linen stores, sporting goods, computer stores, restaurants, and other box retailers. Stores in this category include Wal-Mart, Wal-Mart Supercenters, Super Target, Target, Meijer, Kohl’s, Home Depot, Lowe’s, Menards, Best Buy, Circuit City, Barnes & Noble, Borders Books, Bed Bath & Beyond, Linens ‘n Things, Ross Dress for Less, The Sports Authority, Dick’s Sporting Goods, Big Kmart, and others. They can range from approximately 300,000 to 1,000,000 square feet.

Outlet Centers usually are a combination of manufacturing company stores and off-price

retailers normally located at an Interstate interchange usually on a highway which connects vacation concentrations with urban areas. There are some very large examples of Outlet Centers on the edge of major metropolitan areas. Gurnee Mill in Gurnee fall into this category.

Big Box Retailers include almost any large retailer such as Wal-Mart, Target, Kohl’s, Home

Depot, Lowe’s, Rooms to Go, Bass Pro Shop, Best Buy, Cabela’s, Circuit City, Barnes & Noble, Border’s Books, Bed Bath & Beyond, Linens ‘n Things, Ross Dress for Less, The Sports Authority, Dick’s Sporting Goods, Kmart, Martin’s, Kroger, Walgreens, CVS, Rite-Aid, Office Max, Office Depot, Staples, Theaters, and others. They can be either part of a power center or freestanding. They normally range in size from 20,000 square feet to over 200,000 square feet. Super Big Box retailers include Cabela’s and Ikea, generate a significant customer base from wide area attraction and operate stores ranging from 200,000 to over 400,000 square feet.

Neighborhood Convenience Centers are usually anchored by a supermarket, a supermarket

combination unit with a drug store, or a major drug store, along with a collection of convenience and service oriented stores, ranging in size from 30,000 square feet up to 150,000 square feet.

Downtown is usually an older part of an urban area where the city first started to grow. It

usually contains a concentration of office, financial, retail, government, restaurants, and civic uses surrounded by a combination of residential, industrial, and some small retail uses.

Strip Service Centers are very small shopping centers typically with a convenience food

mart and other convenience and service shops ranging in size between 7,000 to 20,000 square feet.

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-25-

Convenience Goods and Service Stores are stores directed toward the convenience of the shoppers. These include supermarkets, food marts, drug stores, hardware, stores, liquor shops, video shop, meat markets, fish markets, fast food shops, restaurants, cleaners, laundry, currency exchange, and other shops serving a narrow market. These stores are shopped on a highly frequent basis to meet local everyday needs.

Shopper Goods Stores are stores selling durable goods such as apparel for every member of

the family, shoes, accessories, jewelry, appliances, furniture, home furnishings, toys, books, bedding, office goods, and others durable goods.

Entertainment includes cinemas, comedy clubs, family entertainment centers, bowling,

laser tag, electronic games, electronic sports, and other indoor entertainment venues.

A Trade Area represents that portion of a market area where a retailer or retail concentration can expect to capture between 80 and 90 percent of its customers. Because of driving patterns, visitors, employment, and infrequent shopping visitors, it is difficult, if not impractical, to define a Trade Area more precisely. As more distance is added, the area covered grows geometrically making the assessment beyond 90 percent usually uneconomic.

o Primary Convenience Trade Area is that area from which the most frequent customers

to convenience goods stores originate. o Primary Shoppers Trade Area is that area from which the most frequent customers

originate to purchase shoppers goods items.

o Secondary Trade Area is generally the area from which less frequent customers originate to make purchases.

o Tertiary Trade Area is used with very large and dynamic projects which attract

customers from a very wide area. The Tertiary Trade Area usually defines the area from which very infrequent customers will originate.

Market Penetration, sometimes referred to as “Market Share,” is the percentage of capture

that a retailer, shopping center, or retail complex has of the potential expenditures within its respective Trade Area.

Personal Consumption Expenditures represent the dollars available for the purchase of

goods and services during a year. They usually represent approximately 30 to 40 percent of a household’s income.

Travel or Driving Time Analysis represents the distance that one can drive at five-minute

intervals during normal shopping periods following either posted speed limits or keeping up with traffic. Driving times are usually conducted for 20 minutes in each direction from an area of interest.

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-26-

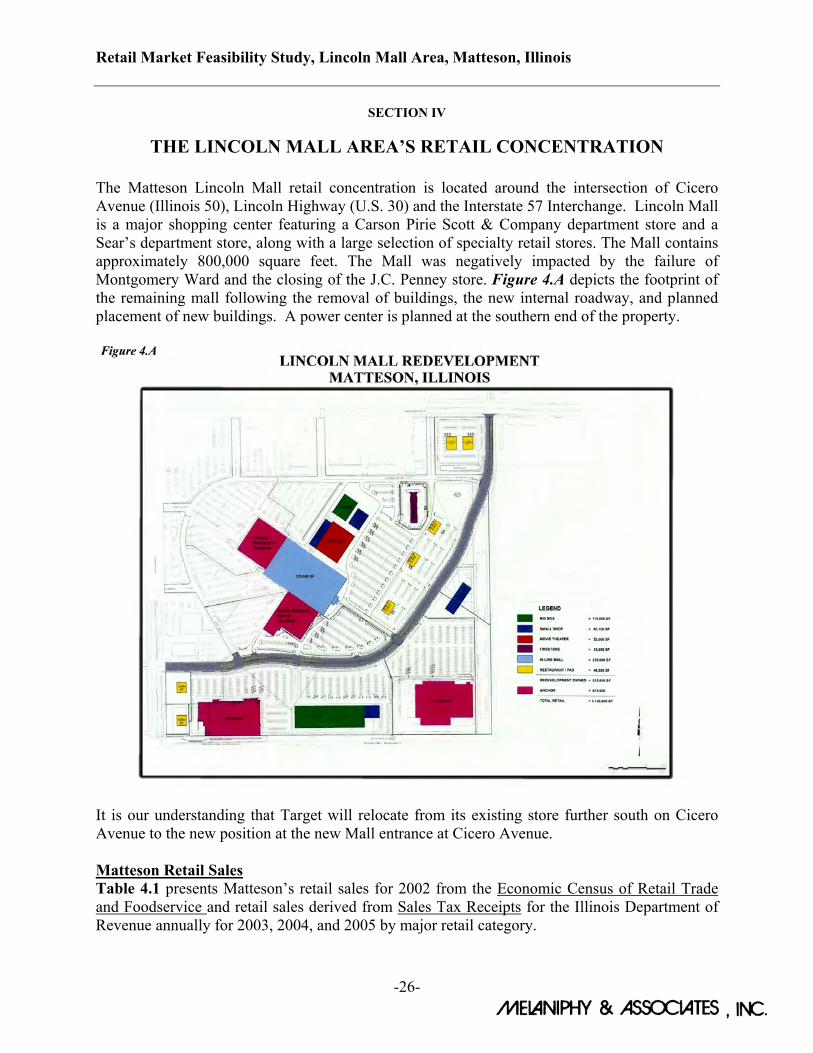

SECTION IV

THE LINCOLN MALL AREA’S RETAIL CONCENTRATION

The Matteson Lincoln Mall retail concentration is located around the intersection of Cicero Avenue (Illinois 50), Lincoln Highway (U.S. 30) and the Interstate 57 Interchange. Lincoln Mall is a major shopping center featuring a Carson Pirie Scott & Company department store and a Sear’s department store, along with a large selection of specialty retail stores. The Mall contains approximately 800,000 square feet. The Mall was negatively impacted by the failure of Montgomery Ward and the closing of the J.C. Penney store. Figure 4.A depicts the footprint of the remaining mall following the removal of buildings, the new internal roadway, and planned placement of new buildings. A power center is planned at the southern end of the property.

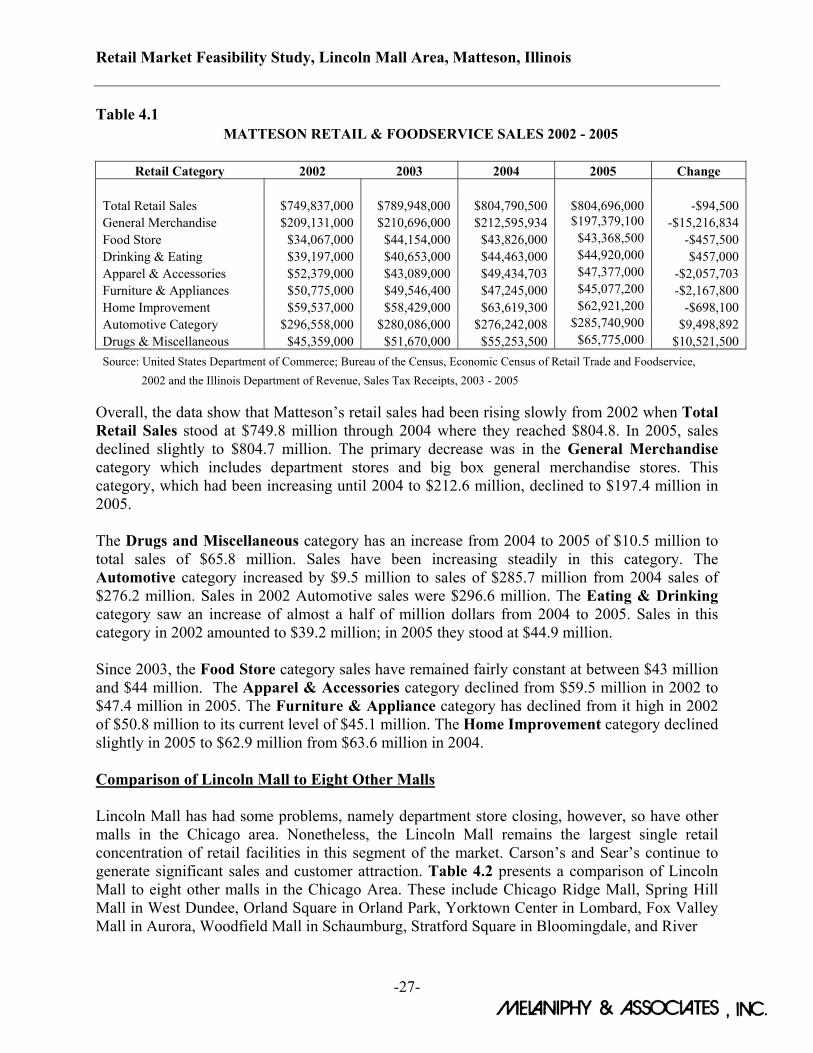

It is our understanding that Target will relocate from its existing store further south on Cicero Avenue to the new position at the new Mall entrance at Cicero Avenue. Matteson Retail Sales Table 4.1 presents Matteson’s retail sales for 2002 from the Economic Census of Retail Trade and Foodservice and retail sales derived from Sales Tax Receipts for the Illinois Department of Revenue annually for 2003, 2004, and 2005 by major retail category.

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-27-

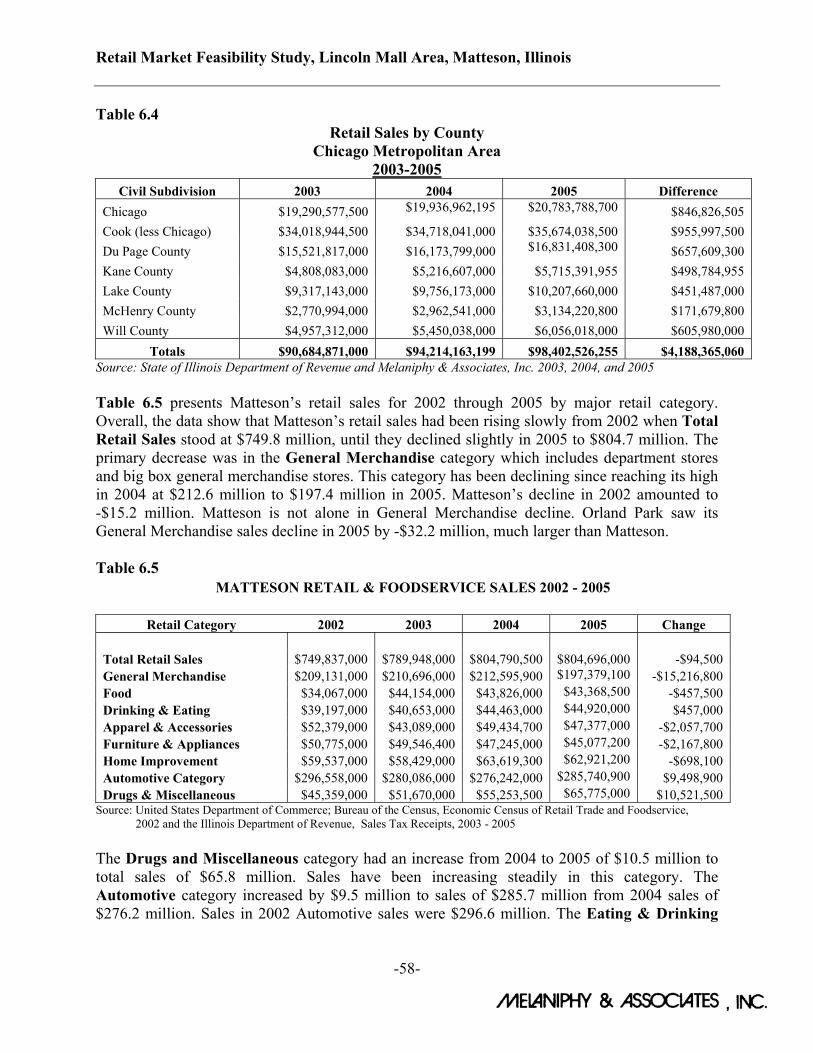

Table 4.1 MATTESON RETAIL & FOODSERVICE SALES 2002 - 2005

Retail Category 2002 2003 2004 2005 Change

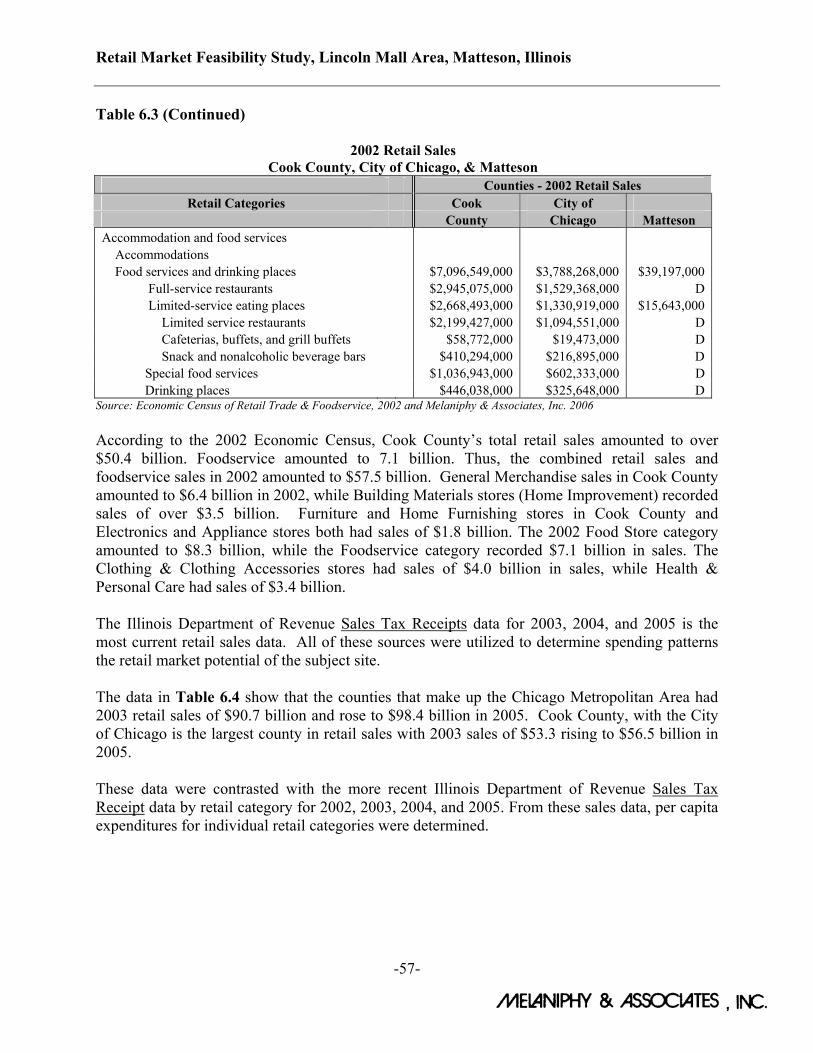

Total Retail Sales $749,837,000 $789,948,000 $804,790,500 $804,696,000 -$94,500 General Merchandise $209,131,000 $210,696,000 $212,595,934 $197,379,100 -$15,216,834 Food Store $34,067,000 $44,154,000 $43,826,000 $43,368,500 -$457,500 Drinking & Eating $39,197,000 $40,653,000 $44,463,000 $44,920,000 $457,000 Apparel & Accessories $52,379,000 $43,089,000 $49,434,703 $47,377,000 -$2,057,703 Furniture & Appliances $50,775,000 $49,546,400 $47,245,000 $45,077,200 -$2,167,800 Home Improvement $59,537,000 $58,429,000 $63,619,300 $62,921,200 -$698,100 Automotive Category $296,558,000 $280,086,000 $276,242,008 $285,740,900 $9,498,892 Drugs & Miscellaneous $45,359,000 $51,670,000 $55,253,500 $65,775,000 $10,521,500 Source: United States Department of Commerce; Bureau of the Census, Economic Census of Retail Trade and Foodservice, 2002 and the Illinois Department of Revenue, Sales Tax Receipts, 2003 - 2005

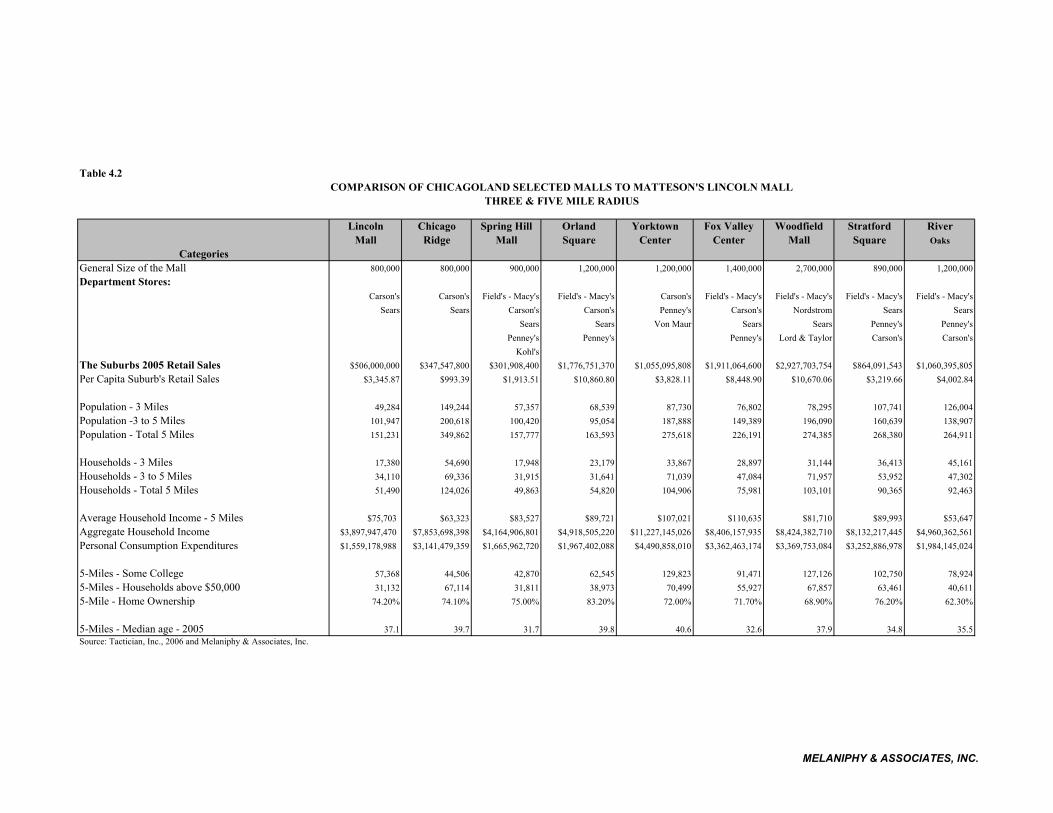

Overall, the data show that Matteson’s retail sales had been rising slowly from 2002 when Total Retail Sales stood at $749.8 million through 2004 where they reached $804.8. In 2005, sales declined slightly to $804.7 million. The primary decrease was in the General Merchandise category which includes department stores and big box general merchandise stores. This category, which had been increasing until 2004 to $212.6 million, declined to $197.4 million in 2005. The Drugs and Miscellaneous category has an increase from 2004 to 2005 of $10.5 million to total sales of $65.8 million. Sales have been increasing steadily in this category. The Automotive category increased by $9.5 million to sales of $285.7 million from 2004 sales of $276.2 million. Sales in 2002 Automotive sales were $296.6 million. The Eating & Drinking category saw an increase of almost a half of million dollars from 2004 to 2005. Sales in this category in 2002 amounted to $39.2 million; in 2005 they stood at $44.9 million. Since 2003, the Food Store category sales have remained fairly constant at between $43 million and $44 million. The Apparel & Accessories category declined from $59.5 million in 2002 to $47.4 million in 2005. The Furniture & Appliance category has declined from it high in 2002 of $50.8 million to its current level of $45.1 million. The Home Improvement category declined slightly in 2005 to $62.9 million from $63.6 million in 2004. Comparison of Lincoln Mall to Eight Other Malls Lincoln Mall has had some problems, namely department store closing, however, so have other malls in the Chicago area. Nonetheless, the Lincoln Mall remains the largest single retail concentration of retail facilities in this segment of the market. Carson’s and Sear’s continue to generate significant sales and customer attraction. Table 4.2 presents a comparison of Lincoln Mall to eight other malls in the Chicago Area. These include Chicago Ridge Mall, Spring Hill Mall in West Dundee, Orland Square in Orland Park, Yorktown Center in Lombard, Fox Valley Mall in Aurora, Woodfield Mall in Schaumburg, Stratford Square in Bloomingdale, and River

Table 4.2COMPARISON OF CHICAGOLAND SELECTED MALLS TO MATTESON'S LINCOLN MALL

THREE & FIVE MILE RADIUS

Lincoln Chicago Spring Hill Orland Yorktown Fox Valley Woodfield Stratford River Mall Ridge Mall Square Center Center Mall Square Oaks

CategoriesGeneral Size of the Mall 800,000 800,000 900,000 1,200,000 1,200,000 1,400,000 2,700,000 890,000 1,200,000Department Stores:

Carson's Carson's Field's - Macy's Field's - Macy's Carson's Field's - Macy's Field's - Macy's Field's - Macy's Field's - Macy'sSears Sears Carson's Carson's Penney's Carson's Nordstrom Sears Sears

Sears Sears Von Maur Sears Sears Penney's Penney's Penney's Penney's Penney's Lord & Taylor Carson's Carson's

Kohl'sThe Suburbs 2005 Retail Sales $506,000,000 $347,547,800 $301,908,400 $1,776,751,370 $1,055,095,808 $1,911,064,600 $2,927,703,754 $864,091,543 $1,060,395,805Per Capita Suburb's Retail Sales $3,345.87 $993.39 $1,913.51 $10,860.80 $3,828.11 $8,448.90 $10,670.06 $3,219.66 $4,002.84

Population - 3 Miles 49,284 149,244 57,357 68,539 87,730 76,802 78,295 107,741 126,004Population -3 to 5 Miles 101,947 200,618 100,420 95,054 187,888 149,389 196,090 160,639 138,907Population - Total 5 Miles 151,231 349,862 157,777 163,593 275,618 226,191 274,385 268,380 264,911

Households - 3 Miles 17,380 54,690 17,948 23,179 33,867 28,897 31,144 36,413 45,161Households - 3 to 5 Miles 34,110 69,336 31,915 31,641 71,039 47,084 71,957 53,952 47,302Households - Total 5 Miles 51,490 124,026 49,863 54,820 104,906 75,981 103,101 90,365 92,463

Average Household Income - 5 Miles $75,703 $63,323 $83,527 $89,721 $107,021 $110,635 $81,710 $89,993 $53,647Aggregate Household Income $3,897,947,470 $7,853,698,398 $4,164,906,801 $4,918,505,220 $11,227,145,026 $8,406,157,935 $8,424,382,710 $8,132,217,445 $4,960,362,561Personal Consumption Expenditures $1,559,178,988 $3,141,479,359 $1,665,962,720 $1,967,402,088 $4,490,858,010 $3,362,463,174 $3,369,753,084 $3,252,886,978 $1,984,145,024

5-Miles - Some College 57,368 44,506 42,870 62,545 129,823 91,471 127,126 102,750 78,9245-Miles - Households above $50,000 31,132 67,114 31,811 38,973 70,499 55,927 67,857 63,461 40,6115-Mile - Home Ownership 74.20% 74.10% 75.00% 83.20% 72.00% 71.70% 68.90% 76.20% 62.30%

5-Miles - Median age - 2005 37.1 39.7 31.7 39.8 40.6 32.6 37.9 34.8 35.5Source: Tactician, Inc., 2006 and Melaniphy & Associates, Inc.

MELANIPHY & ASSOCIATES, INC.

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-29-

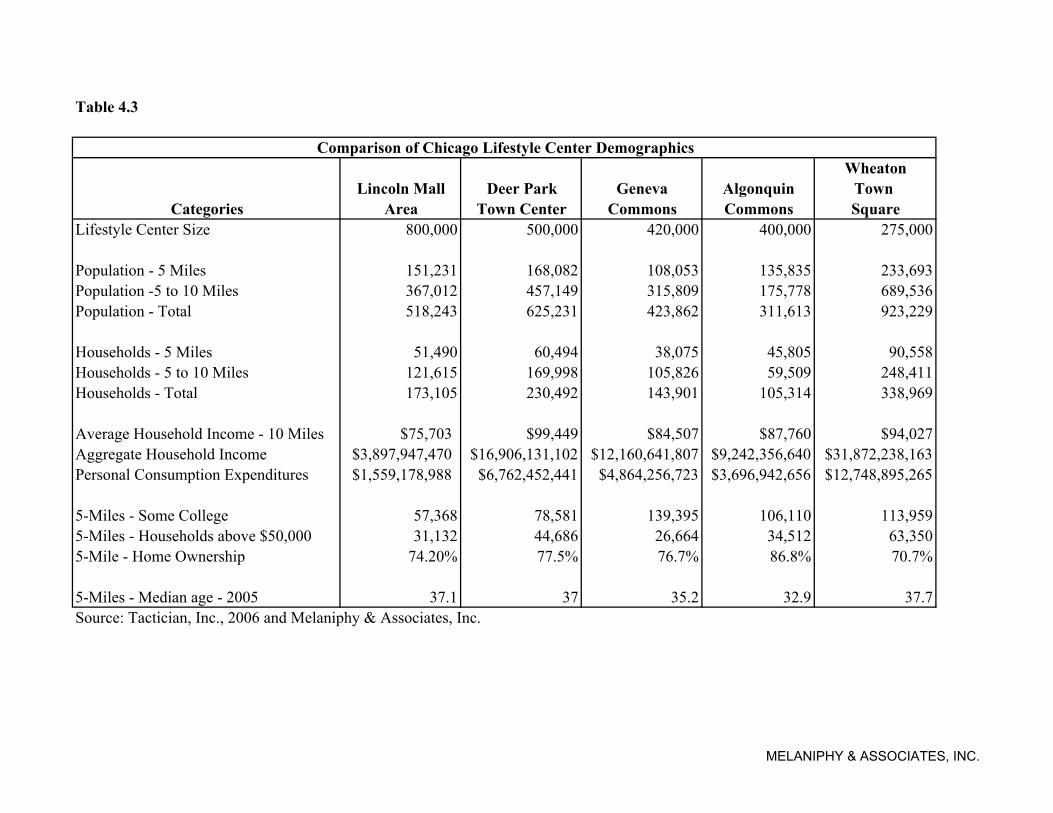

Oaks Center in Calumet City, Some have lost department stores, while others have not. Woodfield Mall has the highest sales of any of these malls. Only Lincoln Mall and Chicago Ridge Mall have two department stores, all of the others have three or four. Matteson had 2005 retail sales of over $804.7 million, while Chicago Ridge had sales of $347.5 million. West Dundee, including Spring Hill Mall with five department stores, had sales of $301.9 million. All of the other communities and malls had sales larger than Matteson. Yorktown Center in Lombard, Stratford Square in Bloomingdale, and River Oaks Center in Calumet City all had sales over a billion dollars. Orland Park, with Orland Square Mall, had 2005 sales of $1.78 billion, while Aurora, with Fox Valley Mall, had 2005 sales of $1.9 billion. Schaumburg, with Woodfield Mall, was clearly the winner with sales of $2.93 billion. Every one of the Table 4.2 examples has a larger Personal Consumption Expenditures within five miles than Matteson. Personal Consumption Expenditures include what households spend for goods and services such as food, drugs, paint and hardware, general merchandise, home improvement, apparel and accessories, furniture, electronics and appliances, sporting goods, jewelry, office supplies, books, eating and drinking, and numerous other retail goods. Services include cleaners, shoe repair, household equipment repair, banking, cinemas, bowling, theater, amusement, and others. Matteson stood at approximately $1.559 billion while all of the others are higher. The closest to Matteson was Spring Hill Mall in West Dundee with five department stores. Finally, Matteson had a Average Household Income estimated at $75,703 within five miles compared to River Oaks’s $53,647 and Chicago Ridge’s $63,323. Orland Park, Matteson’s closest major competitor, had Average Household income within five miles of $89,721. Comparison of Lifestyle Centers We compared Lincoln Mall’s 5 and 10 mile radii with the four existing lifestyle center’s in the Chicago area. A lifestyle center is a collection of popular apparel and accessory stores, specialty shops, home furnishing stores, sporting goods, shoe stores, foodservice facilities, and others. They normally do not contain department stores. The four existing lifestyle centers include Deer Park Town Center in Deer Park, Geneva Commons on Randall Road in Geneva, Algonquin Commons in Algonquin, and Wheaton Town Square in Wheaton. Wheaton Town Center was one of the first lifestyle centers built in the United States. Table 4.3 presents the comparison. Matteson (Lincoln Mall) has a five mile population estimated at 151,231 and a 10 mile population estimated at 518,243. This compares favorably with most of the four lifestyle centers. Matteson (Lincoln Mall) has more people within five miles than Geneva Commons, and more people within 10 miles that Geneva Commons and Algonquin Commons. Wheaton Town Square has the most people within 10 miles with an estimated population of 923,229 persons. Deer Park Town Center also has a larger population with an estimated population within 10 miles of 625,231 persons.

Table 4.3

Comparison of Chicago Lifestyle Center Demographics Wheaton

Lincoln Mall Deer Park Geneva Algonquin Town Categories Area Town Center Commons Commons Square

Lifestyle Center Size 800,000 500,000 420,000 400,000 275,000

Population - 5 Miles 151,231 168,082 108,053 135,835 233,693Population -5 to 10 Miles 367,012 457,149 315,809 175,778 689,536Population - Total 518,243 625,231 423,862 311,613 923,229

Households - 5 Miles 51,490 60,494 38,075 45,805 90,558Households - 5 to 10 Miles 121,615 169,998 105,826 59,509 248,411Households - Total 173,105 230,492 143,901 105,314 338,969

Average Household Income - 10 Miles $75,703 $99,449 $84,507 $87,760 $94,027Aggregate Household Income $3,897,947,470 $16,906,131,102 $12,160,641,807 $9,242,356,640 $31,872,238,163Personal Consumption Expenditures $1,559,178,988 $6,762,452,441 $4,864,256,723 $3,696,942,656 $12,748,895,265

5-Miles - Some College 57,368 78,581 139,395 106,110 113,9595-Miles - Households above $50,000 31,132 44,686 26,664 34,512 63,3505-Mile - Home Ownership 74.20% 77.5% 76.7% 86.8% 70.7%

5-Miles - Median age - 2005 37.1 37 35.2 32.9 37.7Source: Tactician, Inc., 2006 and Melaniphy & Associates, Inc.

MELANIPHY & ASSOCIATES, INC.

Retail Market Feasibility Study, Lincoln Mall Area, Matteson, Illinois

-31-