master thesis maurits kruithof

DESCRIPTION

Basel III Capital Requirements: Impact of Higher Capital Requirements on Bank Funding CostsMaster Business Economics, Finance (University of Amsterdam)TRANSCRIPT

Basel III Capital Requirements

Impact of Higher Capital Requirements on Bank Funding Costs

Maurits J. H. Kruithof Master’s Thesis

Business Economics, Finance Track

Date: March 14, 2013 Student Number: 5603404 Supervisor: Professor Arnoud W. A. Boot Second Examiner: Dr. Jeroen E. Ligterink

University of Amsterdam, Faculty of Economics and Business

[this page intentionally left blank]

Basel III Capital Requirements

Impact of Higher Capital Requirements on Bank Funding Costs

Abstract

This thesis analyzes the impact of higher capital requirements on bank funding costs.

Often is claimed that capital is an expensive form of funding. An extensive literature

review of theoretical insights points out that this is not necessarily the case. The

foundation of capital structure research is the Modigliani-Miller theorem. The question is

whether this theorem holds in practice and is applicable to banks. It proves to be a

useful theorem to identify relevant frictions and distortive policies. This thesis scrutinizes

the public policies that favor debt financing over equity financing, because the corporate

tax system and implicit government guarantees create a significant lower cost of debt

funding. The Basel III capital requirements should therefore be complemented with tax

policy reforms and recapitalization of the banking system with the use of a contingent

capital (CoCo) requirement.

JEL classifications: G21, G28, G32, G38, H25

Keywords: Banking Regulation, Basel III, Capital Requirements, Capital Structure,

Funding Costs, Government Guarantee, Lending Spread, Leverage, Modigliani-Miller

Theorem, Tax Shield.

Table of Contents

1. Introduction.…………………………………………………………………………………………… 7 PART I Theory and Empirics

2. Higher Capital Requirements: Theoretical Insights.……………………… 10 2.1 Modigliani and Miller (1958)..…………………………………………………………………… 10 2.2 Modigliani-Miller Theorem versus CAPM.…………………………………………………… 12 2.3 Having More Equity Capital: Steady State.……………………………………………… 15 2.3.1 Cost of Capital Fallacy.……………………………………………………………………………… 15 2.3.2 The Role of Subsidies on Debt in New Equilibrium……………………………………… 16 2.4 Raising More Equity Capital: Transition Phase………………………………………… 17 2.4.1 Information Asymmetry.…………………………………………………………………………… 17 2.4.2 Debt Overhang………………………………………………………………………………………… 18 2.5 Conclusion.………………………………………………………………………………………………… 20

3. Empirical Studies on Higher Capital Requirements..……………………… 21 3.1 Kashyap, Stein and Hanson (2010).………………………………………………………… 21 3.2 King (2010).……………………………………………………………………………………………… 22 3.3 Angelini et al. (2011)..……………………………………………………………………………… 24 3.4 Cosimano and Hakura (2011)..………………………………………………………………… 27 3.5 Santos and Elliott (2012).………………………………………………………………………… 29 3.6 Conclusion.………………………………………………………………………………………………… 30 PART II Tax Shield, Government Guarantee and Policy Reforms 4. Tax Shield on Debt………………………………………………………………………………… 32 4.1 The Methodology of Debt Tax Shield Calculation.…………………………………… 32 4.2 The Size of the Dutch Bank Tax Shield.…………………………………………………… 33 4.3 The Future of the Tax Shield.…………………………………………………………………… 37 5. Government Guarantees and Recapitalization..……………………………… 39 5.1 Impact and Consequences of Government Guarantees.………………………… 39 5.2 The Size of the Dutch Government Guarantee..……………………………………… 40 5.3 Recapitalization of the Banking System..………………………………………………… 44 6. Summary and Conclusion.…………………………………………………………………… 46 List of Abbreviations.…………………………………………………………………………………………………… 48 Bibliography…………………………………………………………………………………………………………………… 49 Other References, Sources and Data..……………………………………………………………………… 53 Appendices..…………………………………………………………………………………………………………………… 54

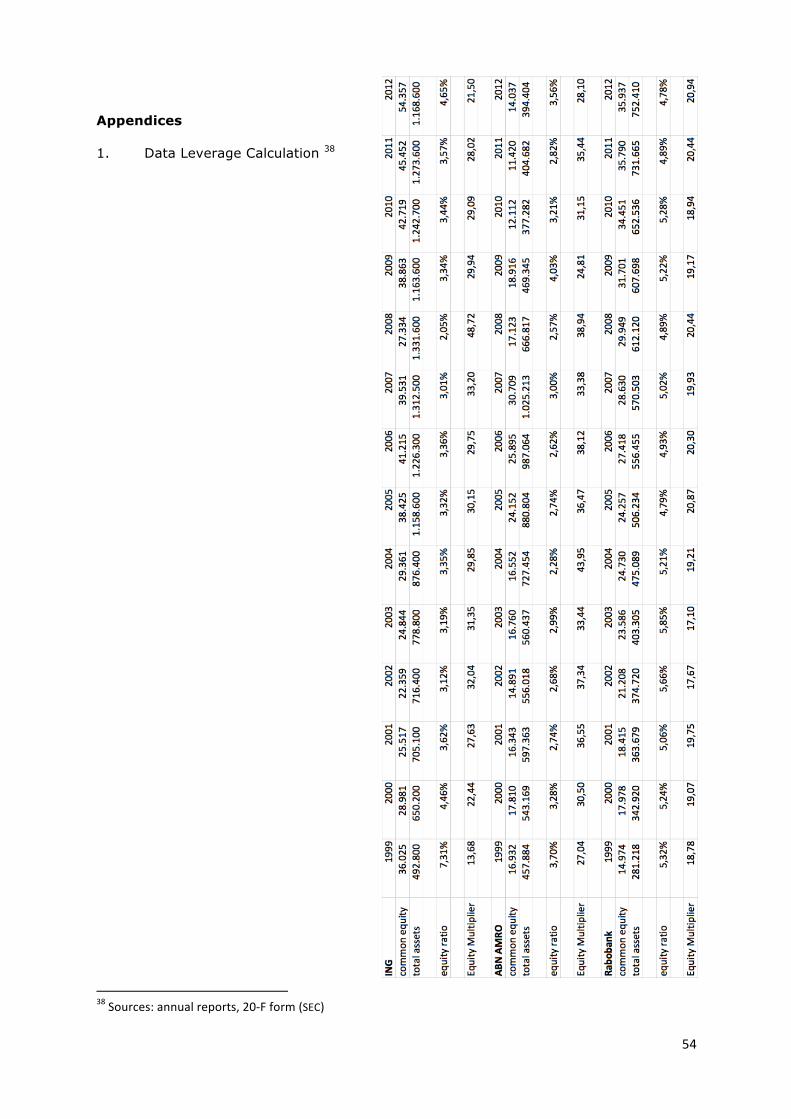

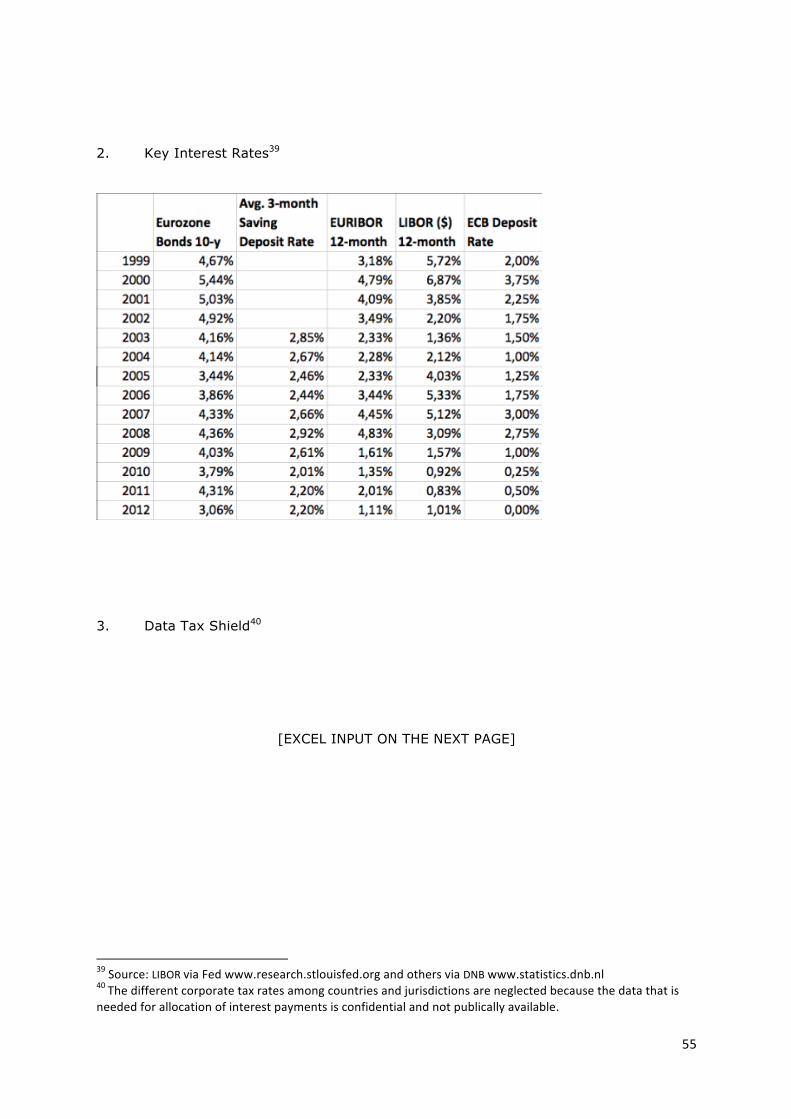

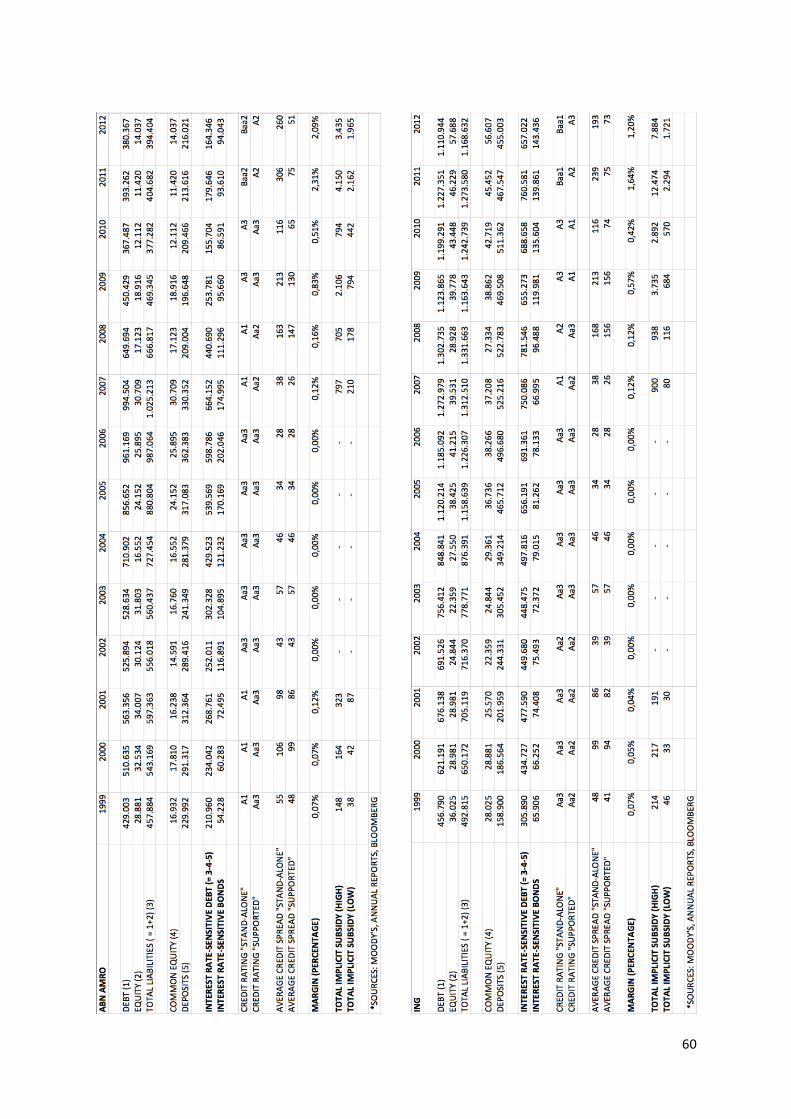

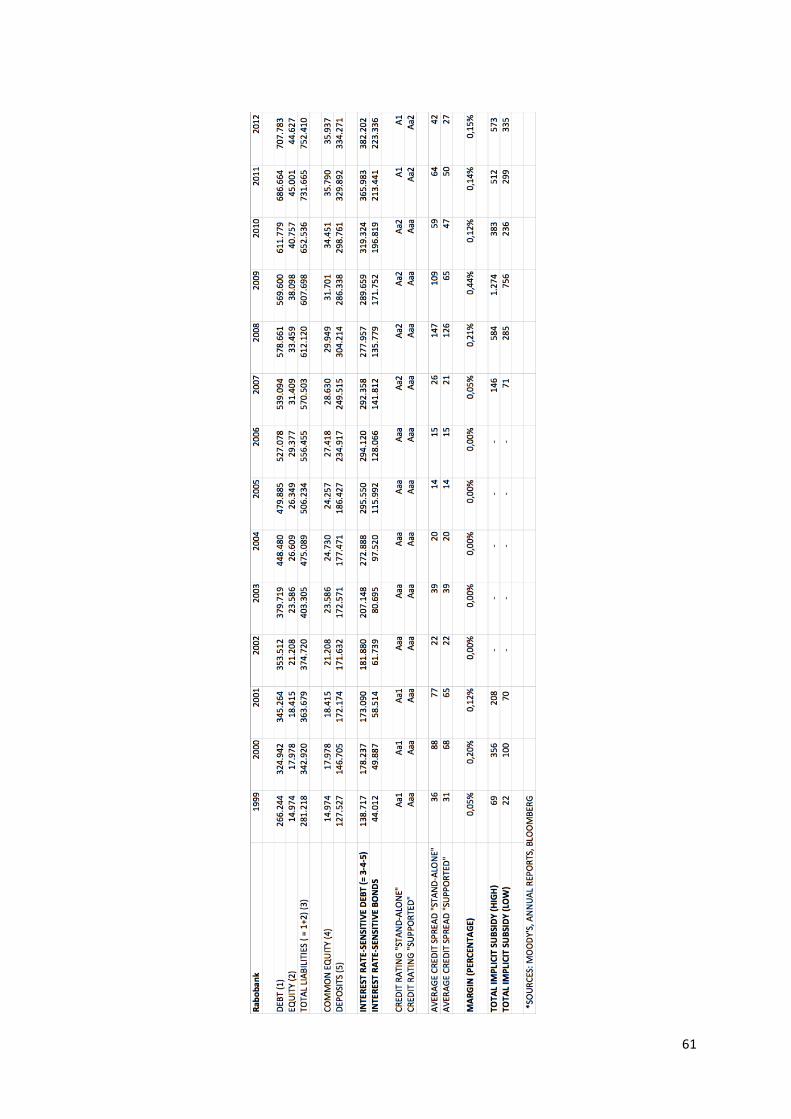

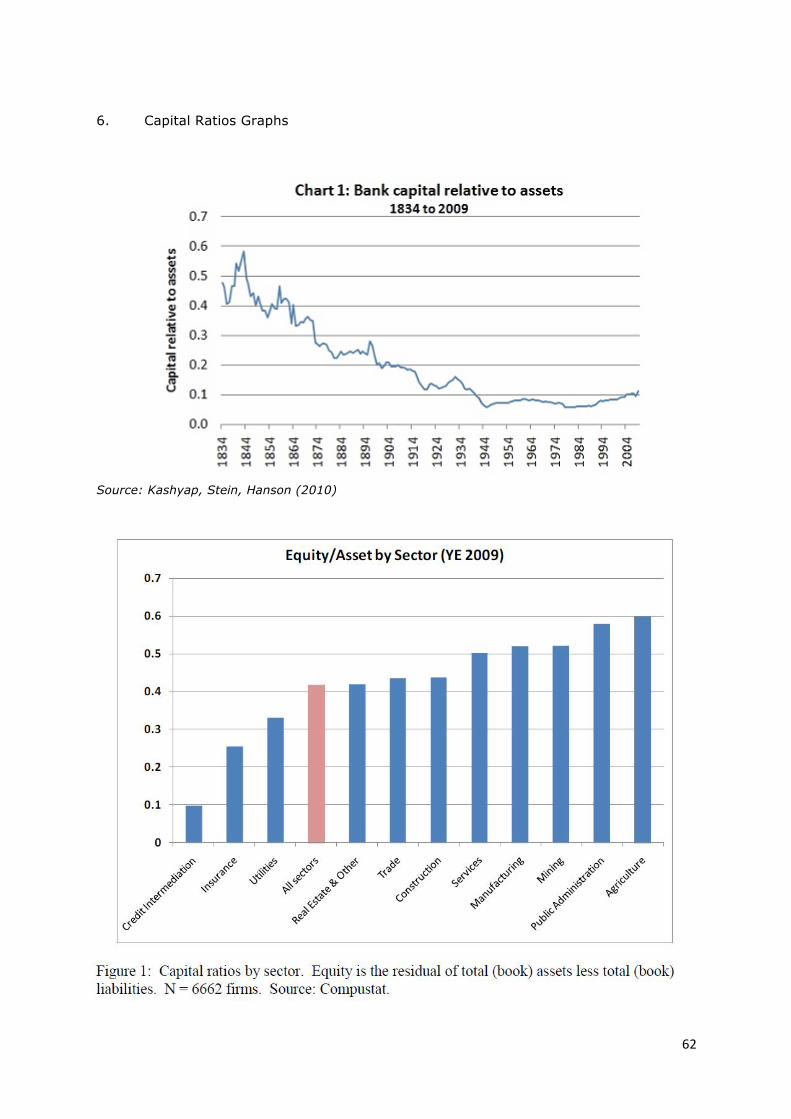

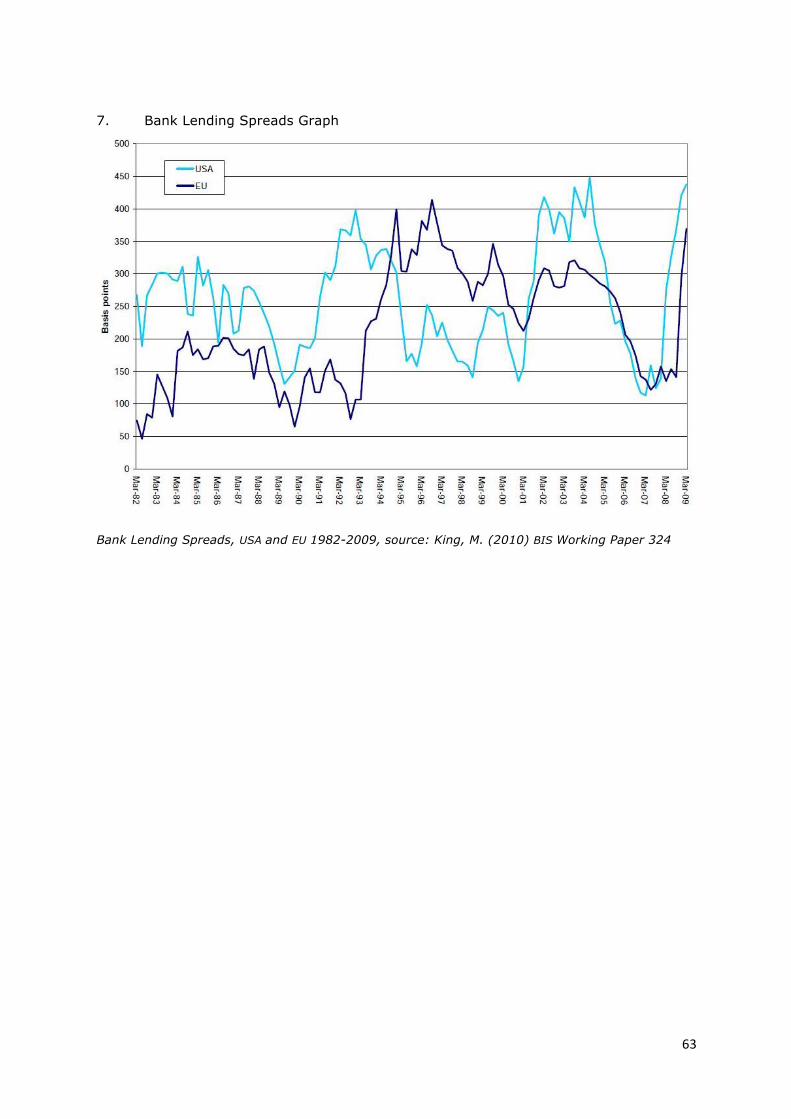

List of boxes, figures and tables Box 2.1: Roles of Capital.………………………………………………………………………………………… 10 Figure 1.1: Process Display of the Statement.…………………………………………………………… 7 Figure 2.1: Alternative Responses to Increased Capital Requirements.…………………… 19 Figure 3.1: Alternative Responses to Increased Capital Requirements.…………………… 26 Figure 4.1: Leverage (Equity Multipliers) of Three Largest Dutch Banks.………………… 34 Figure 4.2: Key Interest Rates.…………………………………………………………………………………… 35 Figure 4.3: Tax Shield on Debt (in EUR millions).……………………………………………………… 36 Figure 4.4: Tax Shield as a Percentage of Total Assets.…………………………………………… 36 Figure 4.5: Fee Income as a Percentage of Total Interest and Fee Income..…………… 37 Figure 5.1: Notches Between “Stand-Alone” and “Supported” Credit Ratings.………… 41 Table 4.1: Profit and Loss Account, Tax Shield………………………………………………………… 32 Table 4.2: Corporate Tax Rate in the Netherlands…………………………………………………… 33 Table 4.3: Leverage (Equity Multipliers) of Three Largest Dutch Banks.………………… 34 Table 5.1: Implicit Subsidy High (In Millions) 1999-2012..……………………………………… 42 Table 5.2: Implicit Subsidy Low (In Millions) 1999-2012………………………………………… 42 Appendices 1. Data Leverage Calculation…………………………………………………………………………………… 54 2. Key Interest Rates..……………………………………………………………………………………………… 55 3. Data Tax Shield.…………………………………………………………………………………………………… 56 4. Net Interest and Fee Income.……………………………………………………………………………… 57 5. Data and Calculations Implicit Government Guarantee……………………………………… 58 6. Capital Ratios Graphs…………………………………………………………………………………………… 62 7. Bank Lending Spreads Graph.……………………………………………………………………………… 63

Preface

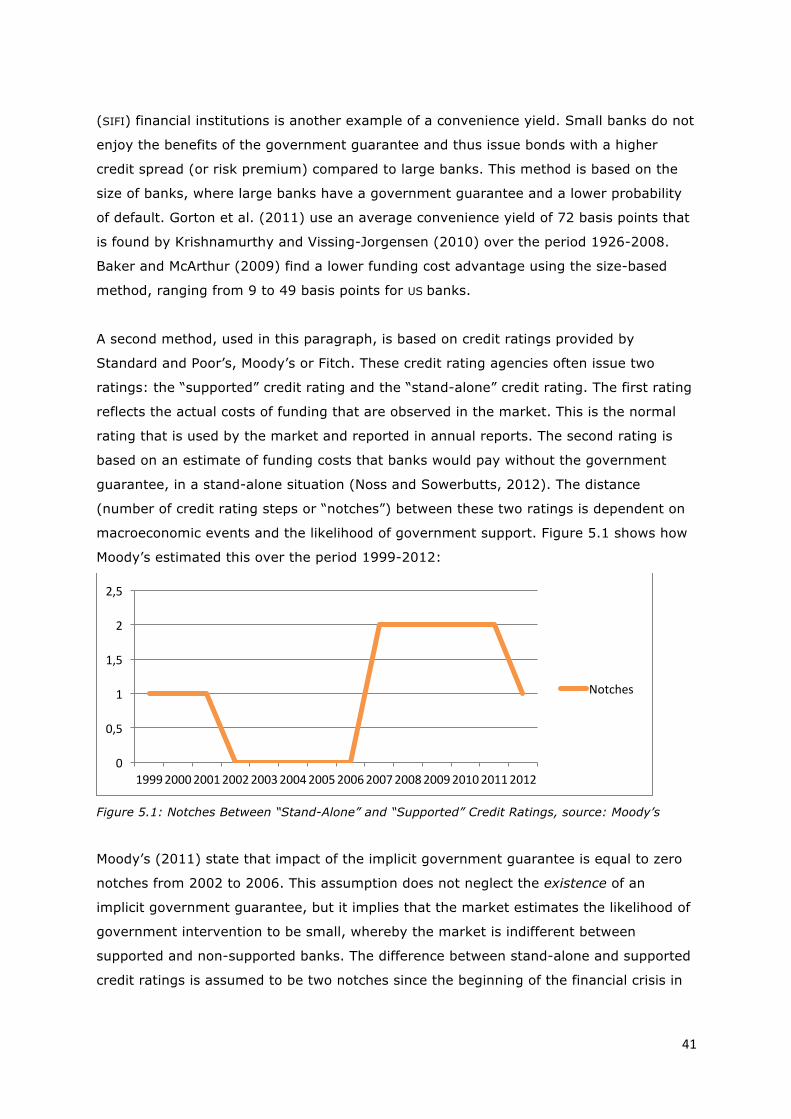

After a difficult start, where I’ve spent several months reading all sorts of papers that

were very interesting but totally not relevant, I finally got the spirit during my first

extensive meeting with professor Boot in his office. I’m very thankful for his support,

advice and time he spent with me on my thesis. I also think that this is the right place to

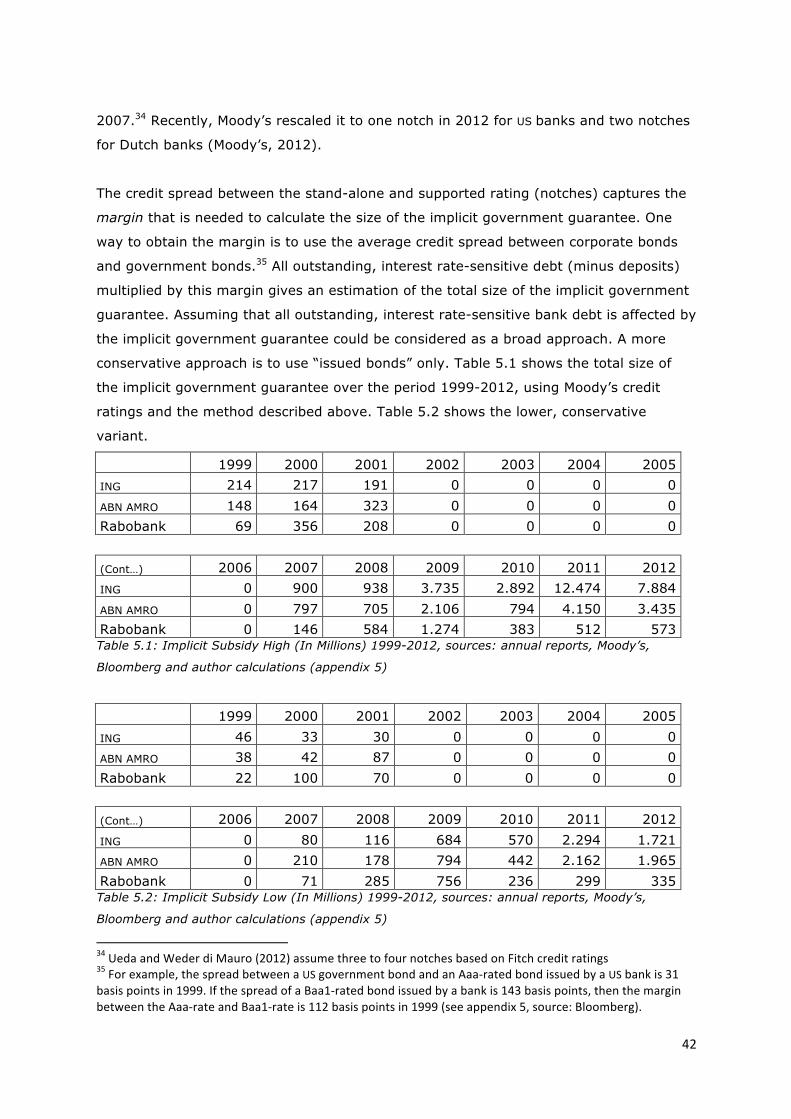

express my gratitude to him for all he has done to help Room for Discussion achieve

success. It happens rarely these days that a mentor-student relationship is possible

when so many students are pursuing their ambitions. I was privileged to have such a

great mentor.

I also want to thank my parents for their ongoing support and interest during my studies

and work for Room for Discussion. They’ve helped me creating the circumstances in

which I could do all the things I needed to do, for that I’m very grateful.

After all the interviews and debates I did for Room for Discussion, I certainly knew that

my thesis had to be about banks and the financial sector. During one of my preparations

for a debate I found a speech by Thomas Huertas, which was written before the collapse

of Lehman Brothers. It contained the following quote1: ‘Capital is the cornerstone of

banking. Capital is the foundation on which banks take risks and achieve rewards, and

capital is ultimately what protects deposits.’ If capital really is the cornerstone of banking,

why were banks so poorly capitalized that the banking crisis of 2007-2009 could happen?

Well, I’ve tried to find an answer and that ultimately resulted in this Master’s thesis.

Maurits Kruithof

Amsterdam, March 2013

1 Derived from a speech by Thomas Huertas, FSA United Kingdom, June 26th 2008, via www.fsa.gov.uk. * I thank my friends Richard Evers and Gerben Smit for their useful comments and suggestions. I also thank the banks, accountancy and consultancy firms with whom I’ve had several informal meetings for their time, advices, comments, criticism and willingness to spar with me.

7

1. Introduction

The recent financial crisis of 2007-2009 shows that the ability of the banking sector to

deal with major shocks must be strengthened. The assets that are held by the banking

sector are too risky or high priced compared to the amount of capital on the liability side

of the balance sheet. The sector is not capable to absorb losses on their own positions,

portfolios and loans provided to companies and households. In 2008 and 2009

governments across the world had to recapitalize banks and guarantee bank debt.

To prevent recurrence of such problems in the long run the Basel Committee presents

reforms to strengthen global capital and liquidity rules, henceforth Basel III (BCBS,

2010a). This should improve the resilience of individual institutions, but also contribute

to greater stability of the financial system as a whole. The measures of Basel III

intervene in the capital structure of banks. The banking sector has to acquire more

capital and of higher quality. Banks’ balance sheets and capital structures will be

different after the implementation of Basel III. Many bankers argue that equity capital is

expensive and higher capital requirements increase the total cost of funding and the

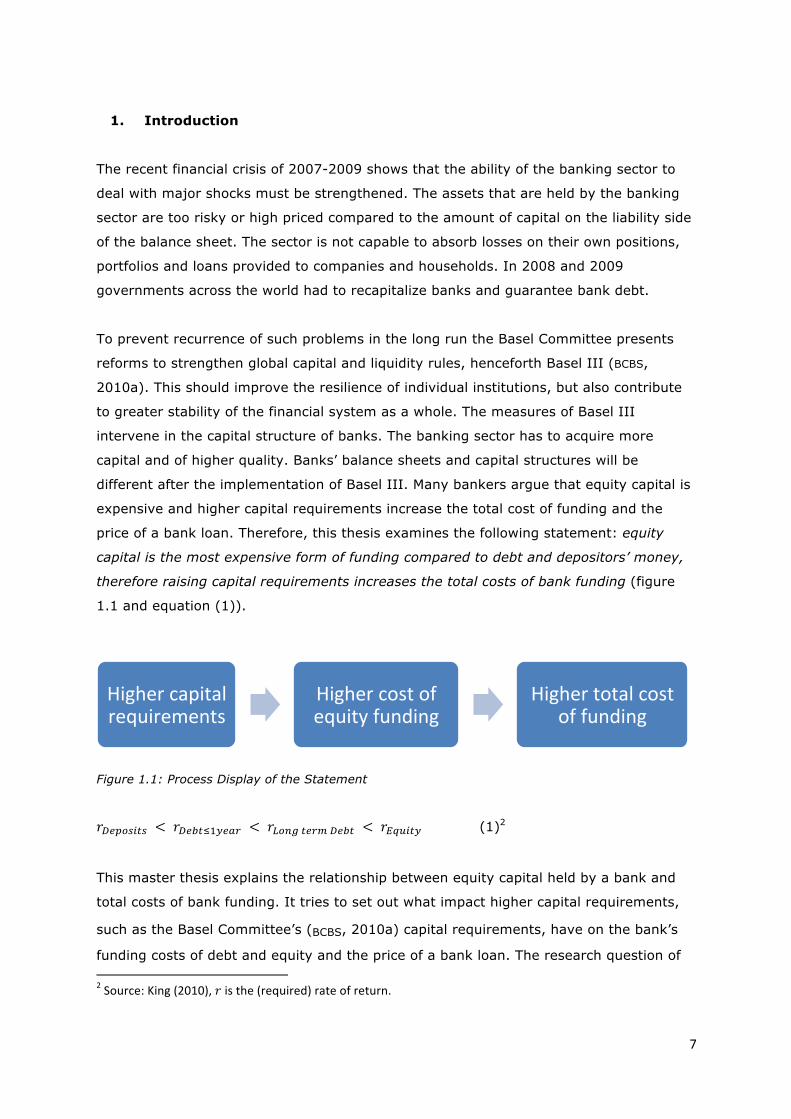

price of a bank loan. Therefore, this thesis examines the following statement: equity

capital is the most expensive form of funding compared to debt and depositors’ money,

therefore raising capital requirements increases the total costs of bank funding (figure

1.1 and equation (1)).

Figure 1.1: Process Display of the Statement

𝑟!"#$%&'% < 𝑟!"#$!!!"#$ < 𝑟!"#$ !"#$ !"#$ < 𝑟!"#$%& (1)2

This master thesis explains the relationship between equity capital held by a bank and

total costs of bank funding. It tries to set out what impact higher capital requirements,

such as the Basel Committee’s (BCBS, 2010a) capital requirements, have on the bank’s

funding costs of debt and equity and the price of a bank loan. The research question of 2 Source: King (2010), 𝑟 is the (required) rate of return.

Higher capital requirements

Higher cost of equity funding

Higher total cost of funding

8

this thesis is: What impact have higher capital requirements on the cost of equity capital

and total funding costs? This study reviews important theoretical literature that is

available on the impact of higher capital requirements. It also analyzes recent papers

that empirically tested the effects of higher capital requirements on total funding costs

and prices of bank loans. The assumptions of these empirical studies are compared to

the fundamental and theoretical insights, including those from Admati et al.’s (2011) key

paper. Analyzing higher capital requirements demands a clear distinction between having

more equity capital (steady state) and raising more equity capital (transition phase). The

dynamics of a steady state and transition phase analysis are rather different.

Based on the Modigliani-Miller capital structure theory (1958), Admati et al. (2011) state

that bank capital is not expensive and that many arguments are fallacious (steady state).

Though, not a few other authors question the applicability of the Modigliani-Miller

theorem on banking. Banks have a certain “special” role, which is to provide liquidity to

the economy and debt is the instrument that banks need to fulfill this role. However, it

turns out that public policy creates distortions in the funding costs of debt and equity,

mainly due to fiscal incentives and government guarantees. The high leverage ratio of

the financial sector is partly explained by these policies that subsidize debt. Higher

capital requirements mean that banks can make less use of these implicit subsidies.

These distortions can be resolved, since they are part of public policy.

This thesis is relevant to financial policy makers, people working in the financial sector

and those engaged in scientific research into capital regulation. It should lead to a better

understanding and awareness of the importance of correct and sufficient capital

regulation in relationship with capital structure. It provides a discussion of “state of art”

theories and concepts written in fundamental papers about capital regulation, capital

structures and bank lending. This thesis explains that public policy favors debt financing

and gives proposals of how policies on taxation and government guarantees can be

reformed, or at least which direction new policies should have to reduce the incentives

for debt financing. It also provides a notion of recapitalization, which reduces the

government guarantee and debt overhang problem. The system has to be robust and

able to absorb losses, while less dependent on government guarantees.

This thesis proceeds as follows. The first part of this thesis focuses on theoretical and

empirical studies of higher capital requirements and funding costs. Starting with chapter

two, it discusses the theoretical insights related to higher capital requirements, the

difference between raising and having more equity capital and what kind of impact this

9

has on banks’ funding costs. Chapter three compares assumptions and results of

empirical studies with the theoretical insights of chapter two. The result of this analysis

emerges two main distortive policies in the discussion of higher capital requirements,

namely corporate tax rules and governments guarantees that implicitly favor debt

financing. These two distortions will be at the center of the second part of this thesis,

respectively chapters four and five. Chapter four elaborates the tax shield methodology,

provides a calculation of the Dutch size of the tax shield and proposes tax policy reforms.

Chapter five sets forth the implicit government guarantee, estimates the size of the

Dutch guarantee and proposes efficient recapitalization in relationship with government

guarantees. This thesis ends with a summary and conclusion in chapter six.

10

PART I Theory and Empirics 2. Higher Capital Requirements: Theoretical Insights

This chapter discusses theoretical concepts and insights related to the capital structure

of banks, banks’ funding costs and higher capital requirements. The basic theory of

capital structure composed by Modigliani and Miller (1958) is the starting point of this

chapter. Many arguments that are put forward by Admati, DeMarzo, Hellwig and

Pfleiderer (2011) are based on this theory of corporate finance. Admati et al. (2011)

explain why bank equity is not expensive and refute many fallacious, irrelevant and/or

very weak arguments. But the academic literature is ambivalent in thinking about the

Modigliani-Miller theorem and its applicability to banks. This chapter also explains

important distinctions between raising more equity capital (transition phase) and having

more equity capital (steady state). The dynamics of raising and having more equity

capital are quite different. Raising more equity capital implies debt overhang problems

and creates information asymmetry problems. Having a higher equity capital ratio in a

new, steady state, equilibrium affects e.g. the benefits of the tax shield and implicit or

explicit government guarantees. This chapter ends with a brief summary and conclusion.

2.1 Modigliani and Miller (1958)

Modigliani and Miller (1958), who wrote a fundamental paper about capital structure,

state that under certain assumptions a firm’s capital structure is irrelevant for I) its value

and II) weighted average cost of capital (WACC). These are known as the Modigliani and

Miller Propositions I and II. The four assumptions made in the frictionless Modigliani and

Miller world are severe; they include no information asymmetry, taxes, financial distress

costs and transaction costs.

Box 2.1 Roles of Capital

Capital is one of the most fundamental concepts in economics. Wherever there is entrepreneurial

activity, investments made and clients served, capital plays an essential role in businesses. It

provides funding, receives profits and is the only mechanism on the balance sheet to absorb

losses. The role of capital can roughly been split into three main characteristics3: 1) as a technical

instrument on balance sheets, 2) as a governance tool and 3) as a systemic buffer.

The first role of capital is technical. The amount of capital relative to the amount of debt is crucial

in this wide debate on the role of capital. The extent to which capital is risky or costly relies on the

leverage of a firm (Modigliani and Miller, 1958) and the riskiness of the assets. The second 3 Inspired by Modigliani and Miller (1958, p. 261) who viewed their main question “what is the cost of capital?” through three perspectives, the one of the corporate finance specialist (technical), the manager (governance) and macroeconomist (systemic level).

11

important and fundamental function of capital is that it monitors the management and distributes

risk among its shareholders. Shareholders are more or less the owners of the company and they

use their voting rights to control or influence management decisions. The agency theory explains

the moral hazard and adverse selection problems (Jensen, 1986). Third, capital provides as a

buffer for the system as a whole to absorb losses. The first and second roles of capital are

important for individual firms, while the systemic role of capital matters the economy as a whole.

Frequently, the systemic role of capital is wrongly separated from the individual interests of a firm

(Admati et al., 2011). Some argue that capital is too expensive and that cheaper debt finance is

preferable (Gorton, 2010). However, this may not be the case if welfare costs of high leverage

ratios are included (Admati et al., 2011). Berger (1995) states that regulators use capital

requirements to create safety nets and to protect the economy from negative externalities. In this

way, the systemic role of capital is taken into account for individual financial institutions.

A second misunderstanding that is important to mention here is that capital is not something to

keep idle or that must be set aside (Admati et al., 2011). Cochrane (2013) states: “capital is a

source of money, not a use of money.” There is a difference between capital requirements and

liquidity or reserve requirements. Capital requirements prescribe banks how to fund themselves

with debt or equity (leverage ratio), while liquidity or reserve requirements relate to the type of

assets and asset mix banks must hold (Admati et al., 2011). Capital requirements address the

right-hand side of the balance sheet and liquidity or reserve requirements the left-hand side.

However, there is a link between capital requirements and assets, because of the Risk Weighted

Assets (RWA) rule that is included in all Basel Accords.4 Nevertheless, once a bank meets reserve or

liquidity requirements, all capital can be used for new loans and investments.5

An important proposition to discuss is whether the Modigliani-Miller theorem is applicable

to banks, under the same assumptions mentioned above. Bank balance sheets and

operations are fundamentally different compared to non-bank firms. For example, banks

produce financial debt instruments such as deposits, short-term commercial paper and

repurchase agreements to provide liquidity to the economy, while non-bank firms do not

fulfill this function. Admati et al. (2011) conclude that, based on the framework of

Modigliani and Miller, higher capital requirements have no significant, long-term,

negative consequences for the economy that offset the benefits. This only concerns the

new equilibrium (steady state), thus after the equity capital is acquired. Miller (1995)

states that the Modigliani-Miller theorem is only applicable ex ante, when equity capital

ratios can be fully anticipated in an equilibrium (at t=0 or t=1). The theorem is not

applicable during the transition phase, the time between t=0 and t=1. The interest rates

on debt do not reflect the new equity capital infusion between t=0 and t=1, simply

4 Each asset that a bank holds is risk-‐adjusted, which means that high risk assets require a higher capital ratio. 5 More about capital and bank lending, see Cebenoyan Strahan (2004) Fabi et al. (2005) Gambacorta, Mistrulli (2004) Inderst, Mueller (2008) Thakor (1996) Elliott (2010a).

12

because most of the debt is already in place and terms and conditions cannot be

renegotiated. However, there is an extensive collection of literature available that

discusses the applicability and relevance of the Modigliani-Miller theorem on banking in

the steady state (the equilibrium of today at t=0). If the Modigliani-Miller theorem does

not hold on banking in its pure form, could increasing capital requirements have

significant consequences for bank’s overall cost of capital and eventually their lending

spreads in the new equilibrium (steady state at t=1)?

The applicability of the Modigliani-Miller theorem is questioned in a paper by Gorton,

Lewellen and Metrick (2011). They argue that bank debt is information-insensitive6

similar to government debt. According to Gorton et al. (2011) and Gorton (2010), bank

debt is immune to adverse selection in trading because agents do not want to acquire

private information about the current health of the bank, since acquiring or generating

information is costly. Gorton et al. (2011) regress the fraction of financial liabilities in the

economy against the fraction of government liabilities in the economy and find that

government and financial liabilities are viewed as acceptable substitutes by investors.

Gorton et al. (2011) argue that bank debt therefore may contain a convenience yield,

like government debt. A convenience yield is a yield below what might be expected

according to standard fixed income calculations7. In other words, investors in bank debt

are willing to accept a lower rate of return due to the implicit or explicit government

guarantee. Gorton et al. (2011) use an average convenience yield of 70 basis points. In

a world with such implicit government guarantees the Modigliani-Miller theorem no

longer holds. Implicit and explicit government guarantees are therefore a distortion in

the pricing of banks’ funding costs. Paragraph 2.3 and chapter five will elaborate on the

distortive effects of implicit government guarantees.

2.2 Modigliani-Miller Theorem versus CAPM

A widely debated consequence of higher capital requirements is that more equity capital

should lower the Return On Equity (ROE). Although many bankers claim that equity

capital is expensive and consider the ROE as fixed, basic corporate finance theory shows

that these propositions are inconsistent. The ROE increases both by more asset risk

and/or more leverage and vice versa. The proposition that more equity capital decreases

the ROE can be interpreted on the basis of two theories. First, the Modigliani-Miller

theorem state that the distribution of total asset risk among more shareholders lowers

6 Note from the author: the definition ‘information-‐insensitive’ seems a contradictio in terminis, like ‘risk-‐free’ is too. 7 For example, the Dutch State has recently issued short-‐term debt with negative interest rates.

13

the ROE, while total funding costs of the bank remain unchanged (proposition II). Admati

et al. (2011) rely heavily on this theorem and proposition. Second, the Capital Asset

Pricing Model (CAPM) calculates the required rate of return of a security (in this case a

bank stock, thus the return on equity) in relation to its risk (𝛽!"#$%& ). The risk (𝛽!"#$%& ) is

dependent on leverage (!!!!

). The CAPM formula states that the ROE (𝑅!"#$%& ) equals the

risk-free rate (𝑅!) plus a risk premium (𝑅!) multiplied by the risk factor (𝛽!"#$%& ):

𝑅!"#$%& = 𝑅! + 𝛽!"#$%& 𝑅! (2)

This model is independent of the Modigliani-Miller theorem and is using different

assumptions. But, since both the Modigliani-Miller theorem and CAPM calculate the ROE,

Gorton et al. (2011) and Miles, Yang, Marcheggiano (2012) find it useful to examine

their relationship. Does the Modigliani-Miller theorem holds simultaneously with CAPM?

Gorton et al. (2011) state that if a bank satisfies the minimum capital requirements it

can produce information-insensitive debt with a convenience yield. Banks that do not

satisfy the minimum capital requirements are considered insolvent: their debt will

become information-sensitive. The existence of a convenience yield on debt breaks the

basic corporate finance theory on capital structure, risk and return. Holding asset risk

and return on assets unchanged, existing shareholders benefit from cheaper debt at the

expense of debt holders (and at the expense of taxpayers when a bail-out is needed).

The implicit government guarantee enables shareholders to receive a higher return. If

banks would follow the corporate finance theory, the advantage of the convenience yield

must result in lower interest rates charged on loans. Because banks can obtain cheaper

debt, they are able to offer loans with lower interest rates. This would imply that the

relationship between the Modigliani-Miller theorem and CAPM does not hold. According to

Gorton et al. (2011), either one of the following two statements can be true:

I. The ROE of banks exceeds their cost of capital under the CAPM. In this case, the

Modigliani-Miller theorem still holds, but CAPM no longer holds (= higher return

on equity with no significant change of risk).

II. Because of the existence of a convenience yield, banks can lower their return

on assets (interest rates charged on loans), leaving the returns on equity and

debt unchanged. Now, the CAPM holds, but Modigliani-Miller Proposition II no

longer holds.8

Gorton et al. (2011) regress bank equity returns against the market portfolio to test

whether statement I is true and banks earn a significant higher equity return given their

8 The required return on assets is independent of the firm’s capital structure.

14

level of risk. They find no abnormal equity return relative to the CAPM, which means

statement II is most likely the case and statement I is not true (Gorton et al., 2011).

Because the counterfactual of statement II is not directly observable, Gorton et al. (2011)

cannot test this statement. However, they assume that the convenience yield influences

the interest rate that banks charge on loans. Banks are driven by competition and will

therefore lower their interest rates charged on loans to gain as much clients as possible.

Gorton et al. (2011) argue that non-bank firms don’t issue similar debt with a

convenience yield, because these firms are able to obtain the same gain as a borrower

by taking out a bank loan with a lower interest rate.

Miles et al. (2012) state that the Modigliani-Miller theorem is unlikely to hold exactly and

use the theorem to assess its relevance for measuring the social costs of more equity

financed lending by banks. They refer to key questions such as how the probability of

crisis falls when banks hold more capital and to what extent the ROE lowers when banks

hold more capital and reduce the risk of that capital. Miles et al. (2012) mention the tax

and guarantee distortions as important factors that influence financial structure. As

mentioned earlier, these distortions ensure that Modigliani-Miller theorem does not hold

completely. Miles et al. (2012) use data on UK banks to test this empirically (chapter 3).

Similar to Gorton et al. (2011), Miles et al. (2012) use the CAPM to test if bank leverage

and risk/return are correlated. The risk of bank assets (𝛽!""#$") is distributed among debt

and equity holders. Therefore, 𝛽!""#$" can be written as follows:

𝛽!""#$" = 𝛽𝑒𝑞𝑢𝑖𝑡𝑦!

!!!+ 𝛽!"#$

!!!!

(3)

(D=debt, E=equity and 𝛽!"#$=risk of debt)

Assuming that debt is riskless (𝛽!"#$ = 0), this equation implies:

𝛽!"#$%& =!!!!𝛽!""#$ (4)

Equation (4) shows the similarity of the CAPM and Modigliani-Miller theorem (Miles et al.,

2012), namely a linear relationship between risk and leverage. Under the assumption of

riskless debt, which is more or less the same as a convenience yield, the ROE depends on

leverage. More equity capital results in a decrease of risk and return on equity.

Miles et al. (2012) regress equation (4) to test the linear relationship between risk and

leverage. Will the CAPM and Modigliani-Miller theorem hold if banks halve their leverage?

This implies that equity risk (𝛽!"#$%& ) is reduced by 50%. Their results show that the

relationship between the Modigliani-Miller theorem and the CAPM does not hold.9 The

9 Gorton et al. (2011) draw the same conclusion.

15

equity risk is not linearly related to leverage because externalities influence the return

on equity.10 However, they use the test results (the coefficients that Miles et al. (2012)

found of the CAPM formula 𝑅!"#$%& = 𝑅! + (𝑎 + 𝑏 leverage)𝑅!) to estimate the weighted

average cost of capital (WACC) assuming that the cost of debt is fixed (risk-free rate)

while leverage halves. As mentioned earlier, the second proposition of the Modigliani-

Miller theorem states that the WACC is irrelevant to the capital structure, therefore the

WACC should not change. Miles et al. (2012) find an increase of the WACC and estimate

that the rise in WACC is only about 55% of what it would be in the absence of the

Modigliani-Miller theorem. In other words, there is a Modigliani-Miller effect and the

theorem holds for approximately 45% of the full extent.

2.3 Having More Equity Capital: Steady State

As the previous paragraphs have shown, the theoretical consequences of higher capital

requirements are ambiguous. This paragraph discusses the dynamics of having more

equity capital on the balance sheet in a new steady state. How can poorly capitalized

banks of today be compared with banks that have a low financial leverage in the new

equilibrium when all banks are better capitalized? Important to mention here is that, ex

ante, the new equilibrium is hard to predict. Today it is unknown how banks’ assets or

liabilities must be priced in the future. However, could bank capital be an attractive and

safe asset class with lower required returns on equity in the new equilibrium?

2.3.1 Cost of Capital Fallacy

The cost of capital fallacy, namely that equity capital is expensive and the return on

equity is fixed at a high level, creates a vicious circle. Once a bank has a capital surplus,

i.e. any “available” equity capital above the minimum capital requirement, it tends to

economize on capital to increase ROE by engaging in certain activities.11 According to

Boot (2013), “putting capital to use” increases the cost of this capital and may not create

value at all. Boot (2013) states that shareholders and other market participants foresee

that banks will economize on capital and thus raise their required return on equity. This

confirms the belief of banks that equity capital is expensive and that the best response

to higher capital requirements is to increase risk on the short-term to realize the

required return in the future. Stating that the cost of capital is also expensive in a new

equilibrium and that the ROE will be (or must be) fixed in a new equilibrium is

fundamentally flawed and misleading, since they do not adjust for risk (Admati et al.,

2011). As a caveat, this belief of banks suggests that the new equilibrium consists of

10 E.g. corporate tax system, government guarantees, capital regulation and market sentiment. 11 E.g. proprietary trading.

16

many more risky assets and activities, which would be the opposite of what higher

capital requirements are meant for.

Despite of this self-fulfilling belief (or vicious circle), Admati et al. (2011) advocate a

banking system with more equity capital. They argue that if the asset risk remains

constant, i.e. no significant change on the left side of the balance sheet, an increase in

capital requirements lowers the ROE due to less leverage. Note that this applies to the

new equilibrium (steady state at t=1). By assuming that asset risk remains constant,

Admati et al.’s (2011) statement is correct: more equity capital distributes risk.

Substantial more equity capital reduces the total per unit risk that is borne by the equity

holder, which should result in lower required rates of return. Thus, holding a bank share

could be an attractive and safe asset class in the new equilibrium when all banks have

more equity capital on their balance sheets and asset risk remains constant.

2.3.2 The Role of Subsidies on Debt in New Equilibrium

The impact of having more equity capital in a new equilibrium is that today’s subsidies

on debt can be less used in the future. On the one hand, more equity capital distributes

risk and lowers the required returns on equity. On the other hand, the implicit

government guarantee and tax shield play a smaller role because there is less debt on

the balance sheet. This could increase the cost of debt. As mentioned earlier, Gorton et

al.’s (2011) analysis indicates that when banks have less information-insensitive debt on

their balance sheet, the benefit from the convenience yield decreases in the new

equilibrium. This also applies to the benefits of the tax shield. The corporate tax system

gives a fiscal incentive to finance with debt, because interest payments on debt are tax

deductible. When there is less debt on the balance sheet, this fiscal advantage of debt

disappears. These reductions of debt-financing advantages increase the total cost of

funding, which according to Gorton et al. (2011) results in higher prices for a bank loan.

Chapters four and five elaborate the tax shield and implicit government guarantees in

more detail and propose some reforms that can be applicable to the new equilibrium and

transition phase.

Following the theory of Admati et al. (2011), Gorton et al.’s (2011) assumptions suffer

from a neglect of external costs and misaligned incentives. Gorton et al. (2011) and

Gorton (2010) argue that banks produce debt, which distinguishes banks from other

companies and makes them “special”. They also state that the economy needs debt and

it is socially desirable that banks produce liquid securities, e.g. securitization of individual

mortgages or short-term commercial paper. Although debt is a useful instrument for the

17

economy, this observation does not imply that banks should be highly leveraged. Admati

et al. (2011) state that investors do not always need those liquid securities in the form

of short-term debt. Bank capital can be a safe and attractive asset class (in a new

equilibrium) for long-term investors that are now holding long-term and senior debt.

Admati et al. (2011) argue that the attractiveness of short-term debt is enhanced when

banks are better capitalized, while investors with longer time horizons hold more equity

capital.

Given the huge costs of the system’s breakdown in the 2007-2009 financial crisis,

Admati et al. (2011) see strong reasons to question the social value of much of this debt

creation that Gorton et al. (2011) advocate.12 The call for more equity capital and the

use of less debt suggest a long-term transition to a banking landscape that is much

different than that of today and hard to predict upfront.

2.4 Raising More Equity Capital: Transition Phase

The road leading to higher capital levels entails other sorts of issues, such as debt

overhang, information asymmetry and stigmatization problems (“new-issuance costs” or

flow costs). Kashyap, Stein and Hanson (2010) explain that there is a crucial distinction

to make when discussing costs of capital in relation to acquiring more equity capital.

First, if a poorly capitalized bank is trying to attract more equity capital from the market,

it could face debt overhang problems while better-capitalized banks do not. Second,

costs associated with information asymmetry also play a bigger role when the bank in

dispute is highly leveraged. Kashyap et al. (2010) state that the frictions of raising more

equity capital are more severe than the “ongoing costs” of holding more equity capital.

2.4.1 Information Asymmetry

An important contribution to the information asymmetry discussion is the flow-cost

theory, which is set up by Myers and Majluf (1984). They explain the difference between

more and less information available for respectively firm management and outside

investors. Assuming that management acts on behalf of existing shareholders, then an

equity issue will be taken as a negative signal, since management prefers to sell shares

when they think shares are overvalued. This is also known as the signaling effect (or

stigmatization) and share issues will tend to be associated with negative share-price

impacts. Because management knows that there is a negative impact of this

12 Admati et al. (2011) state that the financial crisis is due to high leverage ratios and that if the equity cushion was big enough, the crisis did not occur. On the other hand, Gorton et al. (2011) argue that the conversion of information-‐insensitivity debt into information-‐sensitivity debt (e.g. repo) is the cause of the financial crisis and not necessarily the level of debt (leverage).

18

stigmatization, they will postpone or not propose an equity capital issuance. This

disturbs the leverage reduction during the transition phase.

If a bank faces higher capital requirements, it might not be raising new external equity

and instead prefers to shrink its assets and stop lending. Kashyap et al. (2010) conclude

that, in the sense of the Myers-Majluf model and empirical work they have surveyed,

new capital requirements should be phased-in sufficiently, in order to reduce the

information asymmetry problem and to give banks time to generate the necessary

additional capital largely out of retained earnings and maintain lending activities

normally.

On the other hand, Admati et al. (2011) argue that if the share issue decision is not

taken by the management, but required by the regulator, the negative signaling effect

can be neutralized. They refer to the Troubled Asset Relief Program (TARP) in 2009,

where banks didn’t have a choice whether to accept government intervention or not, and

the information asymmetry was not an issue. If new capital requirements are

accompanied by regulation mandating all banks to issue new shares at a pre-specified

scheme, the negative signaling effect would be removed, and banks have no reason to

reduce lending in order to meet the new capital requirements during the transition phase

(Admati et al., 2011). Also Admati et al. (2011) recommend regulators to postpone

dividend payments by banks for a period of time, and use the retained earnings to build

up bank capital. Again, if done under force of regulation, this will not lead to a negative

signaling effect on the health of any particular bank (Admati et al., 2011).

2.4.2 Debt Overhang

In addition to the information asymmetry problem, poorly capitalized banks face debt

overhang problems. Myers (1977) was the first to describe the problem of debt overhang.

For a firm with outstanding debt, equity capital issuance reduces leverage. Leverage

reduction of these firms benefits existing debt holders and providers of debt guarantees.

For each unit of equity capital that is added to the balance sheet, debt becomes safer

and a transfer of value takes place from shareholders to existing debt holders (“dilution”)

during the transition phase. This transfer of value leads to underinvestment; new (partial

equity financed) projects are not carried out, because dilution will occur (Myers, 1977).

In a paper about debt overhang in relation to banks, Admati, DeMarzo, Hellwig and

Pfleiderer (2012) state that shareholders do not want to reduce the leverage even if the

reduction would not change the total value of the bank. In some cases, new equity

19

capital that is invested in good assets (loans with positive NPV) might increase the total

value of the bank. Due to debt overhang and the “addiction” to leverage new loans are

not provided (Admati et al., 2012). During financial crises, when the probability of

default is significantly higher, debt overhang problems partly explain the credit rationing.

Repayments of existing loans are used to strengthen the banks’ balance sheets.

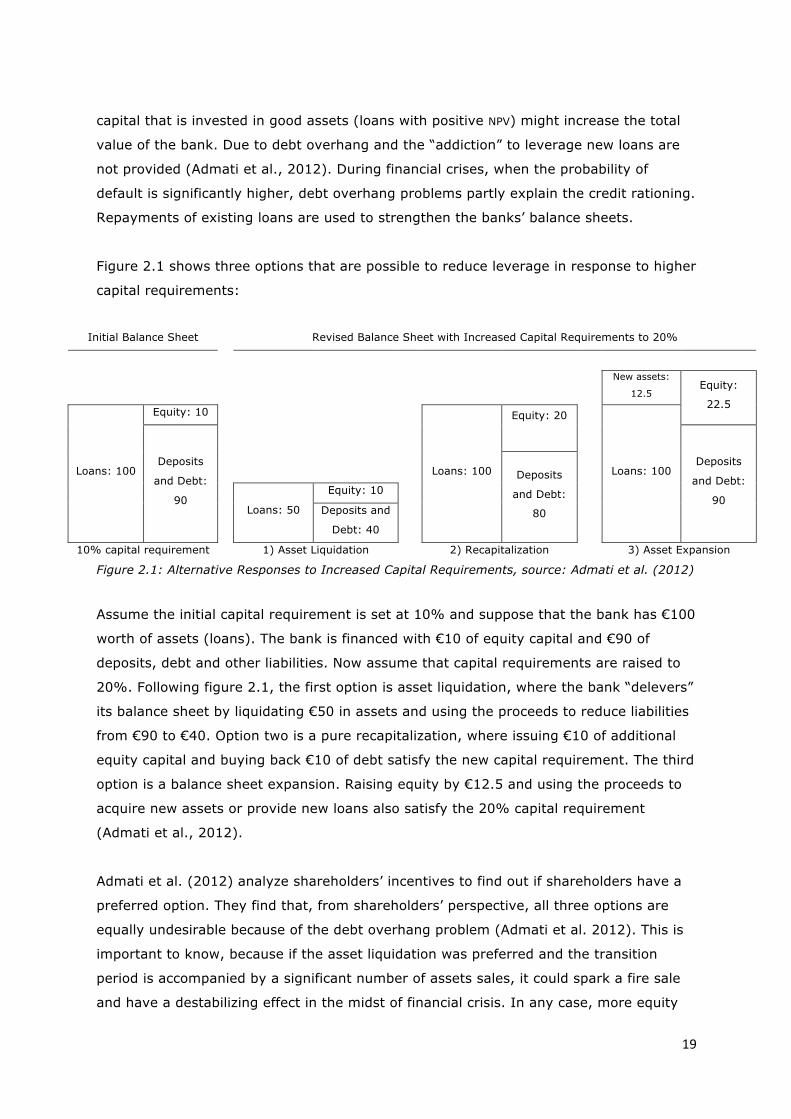

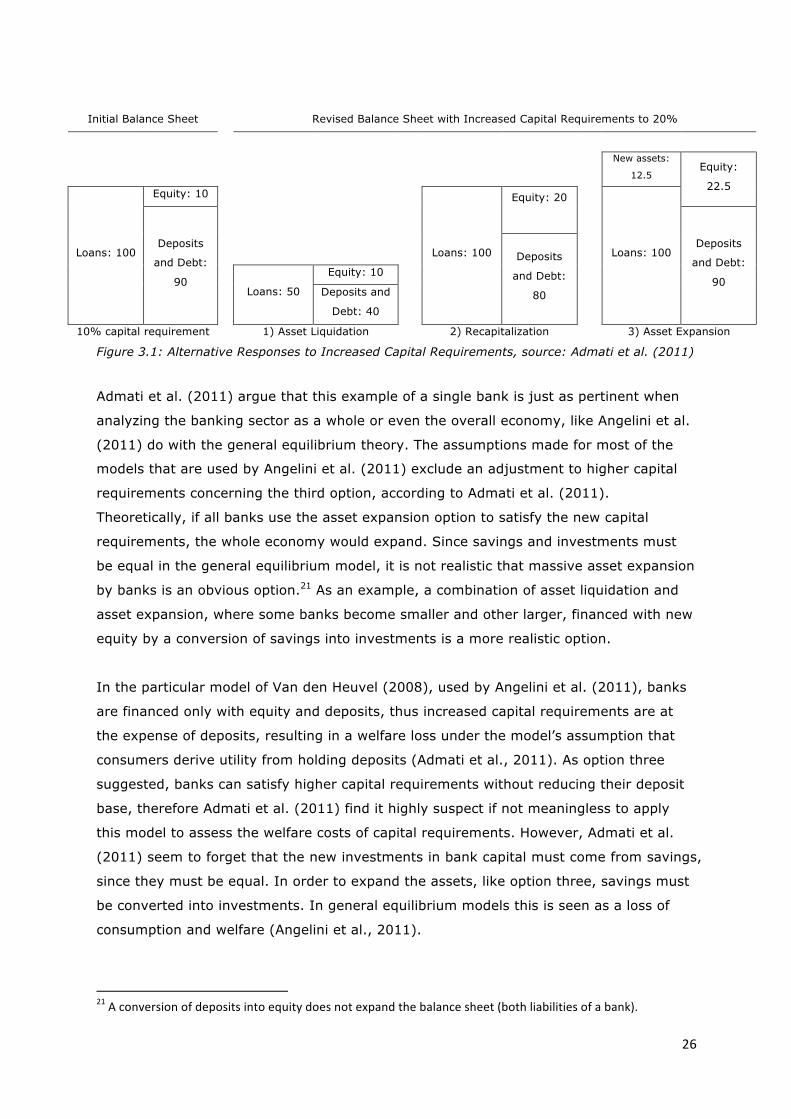

Figure 2.1 shows three options that are possible to reduce leverage in response to higher

capital requirements:

Initial Balance Sheet Revised Balance Sheet with Increased Capital Requirements to 20%

New assets:

12.5 Equity:

22.5

Loans: 100

Equity: 10

Loans: 100

Equity: 20

Loans: 100 Deposits

and Debt:

90

Deposits

and Debt:

90

Deposits

and Debt:

80

Loans: 50

Equity: 10

Deposits and

Debt: 40

10% capital requirement 1) Asset Liquidation 2) Recapitalization 3) Asset Expansion

Figure 2.1: Alternative Responses to Increased Capital Requirements, source: Admati et al. (2012)

Assume the initial capital requirement is set at 10% and suppose that the bank has €100

worth of assets (loans). The bank is financed with €10 of equity capital and €90 of

deposits, debt and other liabilities. Now assume that capital requirements are raised to

20%. Following figure 2.1, the first option is asset liquidation, where the bank “delevers”

its balance sheet by liquidating €50 in assets and using the proceeds to reduce liabilities

from €90 to €40. Option two is a pure recapitalization, where issuing €10 of additional

equity capital and buying back €10 of debt satisfy the new capital requirement. The third

option is a balance sheet expansion. Raising equity by €12.5 and using the proceeds to

acquire new assets or provide new loans also satisfy the 20% capital requirement

(Admati et al., 2012).

Admati et al. (2012) analyze shareholders’ incentives to find out if shareholders have a

preferred option. They find that, from shareholders’ perspective, all three options are

equally undesirable because of the debt overhang problem (Admati et al. 2012). This is

important to know, because if the asset liquidation was preferred and the transition

period is accompanied by a significant number of assets sales, it could spark a fire sale

and have a destabilizing effect in the midst of financial crisis. In any case, more equity

20

capital increases debt holders’ safety and value. Admati et al. (2012) emphasize that

these problems would be less significant when the banking system is better capitalized.

2.5 Conclusion

This chapter discussed important insights and concepts related to capital structure of

banks, banks’ cost of funding and higher capital requirements. In conclusion, banks are

“special” and have some unique dynamics on their balance sheets (e.g. deposits).

However, some important corporate finance insights are applicable to banks and should

be taken into account when discussing the capital structure of banks. The Modigliani-

Miller theorem holds partially and is independent of CAPM. The theorem is also useful to

expose and identify frictions and distortions. The impact of higher capital requirements

on the total cost of funding is negatively affected mainly by two externalities. First,

implicit and explicit government guarantees affect the banks’ cost of funding due to a

discount on the interest rates on debt: the convenience yield. Second, the tax shield is

also subsidizing debt and makes the total cost of funding cheaper. These problems, and

many more issues, play a minor role when the banking system is better capitalized;

hence higher capital requirements are necessary to reduce frictions and distortions.

The theoretical analysis of discussing and implementing higher capital requirements

must be segregated in two ways, namely having more equity capital and raising more

equity capital. The self-fulfilling beliefs of banks that having more equity capital is

expensive and the ROE is fixed are fundamentally flawed. Having more equity capital

reduces the required return on equity, since risk is distributed among more shareholders.

It is therefore misleading if banks engage in risky activities to remain their ROE constant.

In the new equilibrium (steady state, when all banks are better capitalized), bank capital

can be an attractive and safe asset class to hold in the portfolio, with a low risk profile

and a reduced required return on equity.

Raising more equity capital could transfer value from shareholders to existing debt

holders. This so-called debt overhang problem makes the decision to acquire more

equity capital difficult for banks’ shareholders and managers. Along with information

asymmetry problems, high leverage ratios are hard to breach by raising more equity

capital. The combination of these two problems demands that higher capital

requirements should be phased in gradually. However, these problems can be alleviated

if the regulator requires banks to postpone dividend payouts and to issue new equity

capital on short notice under force of that same regulator.

21

3. Empirical Studies on Higher Capital Requirements

This chapter surveys five recently published, empirical-based papers and publications on

the effect of higher capital requirements on loan growth and bank lending spreads. In

chronological order of publication it discusses Kashyap, Stein and Hanson (2010), King

(2010), Angelini et al. (2011), Cosimano and Hakura (2011) and Santos and Elliot

(2012). The assumptions and results of these studies are compared with the theoretical

concepts and insights discussed in chapter two. These five studies empirically test the

long-run impact of higher capital requirements. Their results relate to a new, steady

state, equilibrium. Some of these papers mention the transition phase briefly by

explaining debt overhang and asymmetry information problems. These problems are not

involved in their empirical parts, with the exception of Santos and Elliott (2012). In some

cases, chapter two will be complemented with other insights and arguments. A summary

and conclusion form the end of the chapter.

3.1 Kashyap, Stein and Hanson (2010)

Kashyap, Stein and Hanson (2010) examine the impact of “substantially heightened”

capital requirements on large financial institutions, and on their customers. They begin

their empirical study by validating the Modigliani-Miller theorem. A large sample of banks

is used to test if the 𝛽!"#$%& halves when the equity capital ratio is doubled (similar to

Miles et al. (2012)). The regression results are roughly in line with what is predicted

upfront. There is some empirical evidence that justifies the use of the Modigliani-Miller

theorem for further calibrations. Note that Kashyap et al. (2010) assume, for simplicity

matters, that debt is risk-free (𝛽!"#$), which implies the existence of a convenience yield.

Their baseline regression results are not corrected for the loss of subsidized debt when

the equity capital ratio is doubled. Thus, the Modigliani-Miller effect must be dampened.

The second conclusion Kashyap, Stein and Hanson (2010) draw is that if the minimum

capital ratio is raised by ten percentage points, the loan rates will increase by 25-45

basis points13 according to their methodology. This applies to the new equilibrium

(steady state). They qualify this as a minor change in loan rates and small in absolute

terms. The outcomes are only as good as the model that underlies them and the main

assumption of the model is the loss of the tax shield when debt is replaced with equity.

They assume the cost of long-term debt is 7% and the corporate tax rate is 35%. Thus a

ten percentage points increase of the capital ratio would raise the lending spread with 25

basis points (=10% x 7% x 35%). Kashyap et al. (2010) correct for the loss of 13 100 basis points = 1 percent.

22

subsidized debt in an aggressive case (violation of the Modigliani-Miller theorem) and

find an increase of the lending spread by 45 basis points.

There is an incentive for banks to be highly leveraged, because of these benefits

provided by a convenience yield and the tax shield. Admati et al. (2011) explain that

when debt has indeed a tax advantage over equity, this assumption is correct, but

irrelevant to capital regulation. Both capital regulation and tax rules are matters of public

policy. Tax policy should aim at discouraging behavior that generates negative

externalities, such as increases in leverage ratios. High leverage ratios raise the

probability of bank failures and weaken the financial system. The probability of

government intervention, using public funds, is also increased (Admati et al., 2011).

The final conclusion of Kashyap, Stein and Hanson (2010) is that intense competition

drives the banks in the direction of high leverage. The most competitive advantage that

banks have is the ability to fund themselves cheaply (i.e. short-term debt or “repo”14).

Even the smallest increase in cost of funding relative to direct competitors can lead to

the loss of much business (Kashyap, Stein and Hanson, 2010). They also argue that

substantially heightened capital requirements will lead to greater banking activity within

the so-called “shadow banking” sector due to these competition forces. This

phenomenon is also known as regulatory arbitrage. Kashyap et al. (2010) find empirical

evidence that large banks in particular tend to hold less capital and are able to exploit

regulatory arbitrage. Admati et al. (2011) point out that most activities and entities in

the “shadow banking system” relied on commitments made by regulated entities, and

thus were within regulators’ reach. They believe it is unhelpful in the context of the

capital regulation discussion to refer to the “shadow banking system” like that. Capital

regulation is focused on reducing excessive leverage and regulators should be able to

assess the true leverage of banks. This includes banks’ contribution to the entities within

“shadow banking system” that are being used to hide leverage and exposures (Admati et

al., 2011). Obligations to the shadow banking system could be higher than expected.

3.2 King (2010)

The second paper, a BIS working paper by King (2010), outlines a methodology for

mapping the increases in capital and liquidity requirements proposed under Basel III to

bank lending spreads. He finds that a one-percentage point increase (steady state) in

the capital ratio can be recovered by increasing lending spreads by 15 basis points. This

is a bigger change in the lending spread compared to the figures Kashyap, Stein and 14 For the role of repo financing, see Gorton (2010) and Gorton and Metrick (2010).

23

Hanson (2010) estimated with their methodology. King’s (2010) most important

assumption is that the return on equity (ROE) and the cost of debt are unchanged when

more equity capital is acquired. He argues that theoretically both the cost of debt and

the cost of equity should decline as leverage decreases and the risk of default becomes

smaller, but it is not evident that these theories hold in practice (King, 2010). According

to King, this is due to implicit government guarantees on bank debt, which reduce the

risk of default, leading shareholders to expect a lower ROE. At the same time King (2010)

mentions the implicit subsidy on cost of deposits due to the deposit insurance schemes,

lowering the cost of wholesale funding compared to firms with similar leverage ratios. As

mentioned in chapter two, bankers argue that higher capital requirements will increase

funding costs, since indeed more equity capital will reduce banks’ ability to benefit from

these guarantees and subsidies. Following this reasoning, capital is indeed expensive.

Admati et al. (2011) argue that this is not a legitimate reason for regulators not to

propose new capital requirements. The existence of these subsidies cannot be neglected,

but that does not justify high leverage ratios. Admati et al. (2011) find it paradoxical

that the government subsidizes the leverage of banks at the same time that it

recognizes that this leverage is socially very costly and considers imposing higher capital

requirements to prevent the banks from taking advantage of this subsidy.

Admati et al. (2011) make a clear distinction between private costs and social costs,

which is important to do when empirically testing higher capital requirements. King

(2010) seems to neglect this. Similar to the case of the tax advantage of debt,

government guarantees on debt concern private costs of bank capital. Admati et al.

(2011) take into account the default risks borne by the taxpayer and the costs of these

risks to taxpayers as social costs. Once these costs are included, there is a strong case

for requiring banks to have more equity capital. Equity cushions are valuable, as they

reduce the likelihood and cost of the guarantees (Admati et al., 2011). Note that this

refers to the new equilibrium (steady state).

King (2010) holds the ROE and the cost of debt constant while calculating the effects of

new capital requirements. This is contrary of what should happen according to the

Modigliani-Miller theorem, as extensively stated in chapter two. Raising the amount of

capital should reduce risk per unit of capital and thus lower the ROE. King (2010)

mentions that it is possible to empirically identify an inverse relationship between bank

24

capital ratios and historical ROEs, with lower returns for more highly capitalized banks.15

Because there is a lack of data on secondary market prices for bank debt, the empirical

relationship between bank capital ratios and the cost of wholesale funding is less clear

(King, 2010). Therefore, King (2010) argues that it is reasonable to assume that ROE and

cost of debt are unchanged despite new higher capital levels. This is false, since ROE does

not adjust for risk. King’s (2010) reasoning shows a misunderstanding of the way in

which risks must be taken into account when calculating the cost of funding. Referring to

chapter two, the required return on equity is higher than the required return on debt and

this difference reflects the greater riskiness of equity relative to debt. Reducing the

amount of capital (increasing leverage) has an effect on the riskiness of debt and equity

and, therefore, on the required expected return on equity.

Modigliani and Miller (1958) state that, with or without tax advantages and public

subsidies to debt and deposits, increasing the amount of equity simply re-distributes the

total risk that is borne by investors in the bank, the right side of the balance sheet. The

total risk of the bank is given by the risks that are inherent in the bank’s asset return,

the left side of the balance sheet (Admati et al., 2011). According to the Modigliani-Miller

theorem, changing the capital structure must affect the return on equity and cost of debt,

therefore King’s (2010) assumption cannot hold. King’s (2010) calculations and test

results are incomplete, since previous mentioned arguments are not taken into account.

3.3 Angelini et al. (2011)

The third paper, a NY Fed Staff Report by Angelini et al. (2011), assesses the long-term

economic impact of the new regulatory standards (the Basel III reform). In line with

Kashyap et al. (2010) and King (2010), this third study also examines the steady state

(new equilibrium). However, Angelini et al.’s (2011) method is a completely different

approach compared to Kashyap et al. (2010) and King (2010), which have studied the

new capital requirements at the level of banks’ balance sheets and used partial

equilibrium models.16 Angelini et al. (2011) address the impact of the new capital

requirements on economic performance and fluctuations. They also discuss the adaption

of countercyclical capital buffers on economic fluctuations. When the economy is

booming (shrinking), capital ratios should be increasing (decreasing). Angelini et al.

(2011) use different general equilibrium models to calculate output17, welfare18 and

consumption. The general equilibrium theory assumes that investments and savings are 15 This is similar to the Modigliani-‐Miller effect mentioned in chapter two. 16 Assuming other sectors are not affected due to the change in the banking sector, hence ceteris paribus. 17 Output is the volatility of macroeconomic variables. 18 The welfare-‐model of Van den Heuvel (2008) is a well-‐known example.

25

in equilibrium and equal, therefore savings are needed when capital investments

increase across different sectors. A conversion of savings into investments in the

financial sector changes the equilibrium of welfare, consumption and economic output for

all sectors. Angelini et al.’s (2011) focus is on the costs of the new regulation and how

these costs affect the behavior of supply and demand in the whole economy. A highly

stylized version of the new scenario (higher capital requirements, conversion of savings

into investments) is translated into model inputs and different variables. The results, or

the model output, are steady state values and volatility of key macroeconomic variables,

which determine the new general (macro) equilibrium (Angelini et al., 2011).

Angelini et al. (2011) derive three results about long-term economic performance,

fluctuations and countercyclical capital buffers. The first result is that a one-percentage

point increase in the capital ratio translates into a 0.09 percent output loss relative to

the level that would have prevailed in the absence of capital tightening. Their

interpretation of this figure is that the impact on long-term economic performance is

modest, which is in line with results obtained in similar studies19 (Angelini et al., 2011).

The second estimate is about the impact of higher capital requirements on economic

fluctuations. According to Angelini et al. (2011), higher capital requirements should

dampen output volatility (the magnitude of economic shocks). Their used models

estimate that a one-percentage point increase in the capital-to-asset ratio reduces the

standard deviation of output by 1.0 per cent, which they opine as a modest result.

Angelini et al. (2011) also find that a one per cent increase in capital raises the lending

spread with 13 basis points20. The final result of Angelini et al. (2011) is that a

countercyclical capital buffer could have a more sizeable dampening effect on output

volatility. The equity capital buffers that are accumulated in good times reduce the

downward impact of an economy in recession.

A modest loss of welfare, as Angelini et al. (2011) estimated, could suggest that

increasing capital requirements reduces the ability of banks to provide loans or hold

deposits, which can be consumed. Admati et al. (2011) claim that increasing capital

requirements do not have to lead to a decline of welfare. Figure 2.1 from chapter two

provides three options that are possible to reduce leverage. The third response, asset

expansion, gives a bank the opportunity to increase the equity capital ratio, while at the

same time providing new loans to the economy.

19 MAG (2010b), BCBS (2010b). 20 King (2010) estimates a comparable increase.

26

Initial Balance Sheet Revised Balance Sheet with Increased Capital Requirements to 20%

New assets:

12.5 Equity:

22.5

Loans: 100

Equity: 10

Loans: 100

Equity: 20

Loans: 100 Deposits

and Debt:

90

Deposits

and Debt:

90

Deposits

and Debt:

80

Loans: 50

Equity: 10

Deposits and

Debt: 40

10% capital requirement 1) Asset Liquidation 2) Recapitalization 3) Asset Expansion

Figure 3.1: Alternative Responses to Increased Capital Requirements, source: Admati et al. (2011)

Admati et al. (2011) argue that this example of a single bank is just as pertinent when

analyzing the banking sector as a whole or even the overall economy, like Angelini et al.

(2011) do with the general equilibrium theory. The assumptions made for most of the

models that are used by Angelini et al. (2011) exclude an adjustment to higher capital

requirements concerning the third option, according to Admati et al. (2011).

Theoretically, if all banks use the asset expansion option to satisfy the new capital

requirements, the whole economy would expand. Since savings and investments must

be equal in the general equilibrium model, it is not realistic that massive asset expansion

by banks is an obvious option.21 As an example, a combination of asset liquidation and

asset expansion, where some banks become smaller and other larger, financed with new

equity by a conversion of savings into investments is a more realistic option.

In the particular model of Van den Heuvel (2008), used by Angelini et al. (2011), banks

are financed only with equity and deposits, thus increased capital requirements are at

the expense of deposits, resulting in a welfare loss under the model’s assumption that

consumers derive utility from holding deposits (Admati et al., 2011). As option three

suggested, banks can satisfy higher capital requirements without reducing their deposit

base, therefore Admati et al. (2011) find it highly suspect if not meaningless to apply

this model to assess the welfare costs of capital requirements. However, Admati et al.

(2011) seem to forget that the new investments in bank capital must come from savings,

since they must be equal. In order to expand the assets, like option three, savings must

be converted into investments. In general equilibrium models this is seen as a loss of

consumption and welfare (Angelini et al., 2011).

21 A conversion of deposits into equity does not expand the balance sheet (both liabilities of a bank).

27

Concluding, Angelini et al. (2011) seem to neglect the social costs that arose from

misalignments and distortions underlying the system’s breakdown in the crisis. Angelini

et al. (2011) focuses on costs in terms of the loss of welfare and consumption. In 2008,

Van den Heuvel concluded that capital requirements were too high and he estimated that

one upper bound for the cost of a one-percentage point increase in capital requirements

is $1.8 billion per year. Given these facts, Admati et al. (2011) find it remarkable that

Van den Heuvel’s (2008) welfare-model is used by Angelini et al. (2011). The loss of

output, consumption or welfare due to higher capital requirements is significantly smaller

than the costs of the financial crisis (Admati et al., 2011). If more equity capital reduces

the costs of financial crises, than equity capital should be taken into account as a benefit.

3.4 Cosimano and Hakura (2011)

The fourth paper that is discussed, an IMF Working Paper by Cosimano and Hakura

(2011), investigates the impact of the new capital requirements of Basel III on bank

lending rates and loan growth (steady state, new equilibrium). The method used by

Cosimano and Hakura (2011) models three variables simultaneously; the generalized

method of moments (GMM). The first variable that Cosimano and Hakura (2011) regress

is the choice of capital, depending on the capital requirement, interest rate on deposits,

noninterest costs of loans and total assets (Cosimano and Hakura, 2011). The second

regression variable is the loan rate, which is dependent of the first variable plus interest

rate on deposits, costs of loans and economic activity. The last step they examine is the

elasticity of bank loans, for which they use the loan rate from the second regression. The

elasticity of bank loans indicates the effect of higher capital requirements and loan rates

on loan growth. Cosimano and Hakura (2011) assume that higher capital requirements

raise banks’ marginal cost of funding, which leads to higher lending rates. They also

assume that the ROE is fixed, which means that all costs of increasing capital are

reflected by a higher loan rate. This is a violation of the Modigliani-Miller theorem, as

mentioned earlier. The last assumption is that bank liabilities consist only of equity and

deposits (Cosimano and Hakura, 2011). Three different groupings of banks are (cross-

country) analyzed: 1) the 100 largest banks worldwide; 2) commercial banks or bank

holding companies (BHC’s) in advanced economies that experienced the 2007-2009 crisis;

and 3) commercial banks or BHC’s that did not experience the 2007-2009 crisis.

The first finding of Cosimano and Hakura (2011) is that a one percent increase in the

capital requirement (equity-to-asset ratio) raises the loan rate for the 100 largest banks

with 12 basis points. For the second group, banks that faced the 2007-2009 crisis, a one

percent increase is associated with a 9 basis points average increase in the loan rate.

28

The banks that did not experience the 2007-2009 crisis have a 13 basis point average

increase. Cosimano and Hakura (2011) also find a 12 basis point increase in marginal

cost of equity relative to the marginal cost of deposits, which is evidence against the

Modigliani-Miller theorem. Chapter two explained that there is a Modigliani-Miller effect,

thus not all assumptions hold in their pure form. A higher level of equity would reduce

the riskiness of the bank equity such that the ROE declines. However, Cosimano and

Hakura (2011) refer to the government guarantees and subsidies as a possible source of

the higher cost of equity. Since there is less room for subsidized debt, as stated in

chapter two, total cost of funding becomes higher and thus raising equity capital is

expensive. It is therefore not surprising that they find these increases.

Cosimano and Hakura (2011) use the increases in loan rates to estimate the loan

demand or elasticity for the three groups and different countries. The 100 largest banks

estimations imply a reduction in the volume of loans by on average 1.3 percent in the

long run when Basel III is in force (1.3 percent increase of equity-to-asset ratio).

Cosimano and Hakura (2011) use 2007 data as baseline scenario, which is outdated (see

paragraph 2.5). For banks in countries that experienced the 2007-2009 crisis,

implementing Basel III would reduce loan growth with 4.6 percent on average and 14.8

percent for banks in countries that did not experience the 2007-2009 crisis (Cosimano

and Hakura, 2011). According to Cosimano and Hakura (2011), the wide variance in the

results of loan rate increases and loan demand decreases reflects the differences

between countries’ interest elasticity of loan demand and bank’s net cost of raising

equity.22

Admati et al. (2011) state that highly leveraged banks are generally subject to

distortions in their lending decisions, such as frictions23 associated with governance and

information. This may lead to worse lending decisions compared to a better-capitalized

bank. If shareholders and management of a highly leveraged bank work on the basis of

ROE, they have incentives to make excessively risky investments, especially when

governments guarantee debt. The upward potential, a high ROE, is intended for

shareholders and managers, while the downward potential is shifted to taxpayers.

Cosimano and Hakura (2011) show that higher capital requirements raise lending rates

and reduce loan growth. Admati et al. (2011) would see this as a social benefit, since

excessive lending is reduced. The reduce in loan growth is not a necessity as is shown in

22 Differences in cost of capital are due to different tax policies and ex-‐ and/or implicit government guarantees on debt and deposits across countries. 23 i.e. agency theory, moral hazard, asymmetric information, debt overhang.

29

figure 3.1, thus there should be no concern with any negative impact on the economy of

increased equity capital requirements (Admati et al., 2011). However, this argument is

questionable when a general equilibrium method from Angelini et al.’s (2011) paper is

used where savings and investments are assumed to be equal.

3.5 Santos and Elliott (2012)

As stated in the introduction of this thesis, the first reason for higher capital

requirements is to strengthen the resilience of banks and the banking sector (BCBS,

2010). The previous four studies showed that, with or without correct and justified

assumptions, higher capital requirements result in higher cost of funding and ultimately

higher loan rates in a new equilibrium. In addition to higher loan rates due to the loss of

tax advantage and government guarantees, Santos and Elliott (2012) compose three

extensions of methodologies used by Kashyap et al. (2010), King (2010), Angelini et al.

(2011) and Cosimano and Hakura (2011). These extensions lead to substantially lower

net economic costs and are more in line with arguments of Admati et al. (2011). Santos

and Elliott (2012) state that financial reform comes at a price and that higher capital

requirements do add operating costs for banks that result in higher loan rates. However,

Santos and Elliott (2012) estimate in their study that loan rate increases will likely be

significantly smaller compared to King (2010) and Angelini et al. (2011).24

The first extension of Santos and Elliott (2012) is that market forces demand banks to

have greater safety margins above the minimum capital requirement. They state that

simply comparing the new Basel capital requirements with the old misses the crucial

point that banks hold capital on top of the minimum requirements, as a result of their

own desire to operate safely and because of pressure from the markets and rating

agencies (Santos and Elliott, 2012). Therefore, Santos and Elliott (2012) use the end-

2010 levels as baseline for their estimates, which are higher than the Basel II capital

requirements. The distance between end-2010 levels and Basel III is smaller.

The second extension of Santos and Elliott (2012) assumes that banks will cut costs and

take other measures to reduce the effect on loan rates and remain competitive. This

accounts for an average reduction of 14 basis points on the lending rate (end-2010

24 In the IMF Staff Discussion Note by Santos and Elliott (2012), the estimates are mainly compared to official BIS, IIF and OECD studies.

30

levels versus Basel III capital requirements). Santos and Elliott (2012) mention eight

different bank responses to cost increases which they have included in their study.25

The final extension is more in line with Admati et al. (2011), namely investors will lower

their required rate of return on bank equity when the bank reduces its leverage and

improves safety (Santos and Elliott, 2012). Holding the ROE fixed at a high level is

misleading, as explained in chapter two. With these three extensions taken into account,

Santos and Elliott (2012) estimate that average loan rates increase by 28 basis points in

the United States, 17 basis point in Europe and 8 basis points in Japan in the long term

because of the new capital requirements. Santos and Elliott (2012) mention by

comparison that the smallest step by which central banks change the interest rate is 25

basis points, which has no dramatic effect on the economy. Note that Santos and Elliott

(2012) assume that during the transition phase many permanent cost-saving measures

are implemented.

3.6 Conclusion

This chapter analyzed five empirical-based studies that researched the impact of higher

capital requirements on bank funding costs. The assumptions made in these studies are

compared with the theory of chapter two. The first four studies mainly examined the cost

side of higher capital requirements in a new equilibrium, the steady state. Overall, some

benefits of higher capital requirements are mentioned, but generally not taken into

account in the empirical tests and calculations. King (2010), Angelini et al. (2011) and

Cosimano and Hakura (2012) find substantial increases of funding costs when higher

capital requirements are implemented. The figures are in the range of 12 to 15 basis

points for each percentage point that equity capital increases. However, under the

assumption of fixed and high-level ROE’s and neglecting social benefits of a better-

capitalized banking system, these conclusions are misleading, flawed and/or incomplete.

Admati et al. (2011) and Miles et al. (2012) advocate an empirical analysis of the impact

of higher capital requirements that considers not only costs, but also benefits of

increased equity capital ratios. Such an analysis requires a clear distinction between

costs and benefits to individual banks (private costs and benefits) and overall economic

or social costs and benefits. The empirical studies discussed in this chapter show that

private costs of banks may rise. The loss of subsidized debt on the balance sheet when

more equity capital is acquired cannot be ignored. On the other hand, private benefits

25 See Santos and Elliott (2012, p. 8). Many costs savings can be realized due to increased safety and lower volatility. Admati et al. (2011) mention these effects as the largest benefit of increased capital requirements.

31

are difficult to quantify when the ROE is assumed to be fixed. Therefore the outcomes are

biased to the cost side of higher capital requirements. For a more balanced empirical test

of a new equilibrium, the following four factors should be included (Miles et al., (2012)):

1) Changes in required return on debt and equity as capital structure changes.

2) Changes in weighted average cost of capital (WACC) due to a different capital

structure and tax treatments of debt and equity. 26

3) A lower probability of banking problems as equity buffers rise (safety net).

4) Economic costs generated when banking sector problems arise (bailouts).

The empirical parts of the studies by Santos and Elliott (2012) and Miles et al. (2012) do

take into account these beneficial factors and find significantly lower increases of steady

state funding costs. Furthermore, Miles et al. (2012) even find that the optimal level of

bank capital relative to the proportion of GDP is between 8 and 10 percent of total bank

assets.27 This estimation is twice the capital requirement of Basel III.

The five papers discussed in this chapter generally agree that public policies, such as the

corporate tax system and implicit government guarantees, create subsidized debt. The

main conclusion that can be derived from the empirical studies is that most of the

increase of funding costs due to higher capital requirements is caused by the loss of this

subsidized debt on the balance sheet (steady state). This subsidized debt creates an

incentive for banks to prefer debt financing and to be highly leveraged. The transition

towards a better-capitalized banking system is easier when these negative externalities

are removed. Therefore, higher capital requirements should be complemented with

reforms of policies concerning the corporate tax system and implicit government

guarantees.

26 Note that all analyzes discussed in this chapter assume that asset risk and return are unchanged in a new equilibrium (for simplicity matters). As stated in chapter two, the self-‐fulfilling belief that equity capital is expensive may cause risk-‐seeking bank managers during the transition phase. Santos and Elliott (2012) add to this that banks will cut operational costs to increase equity capital buffers and remain competitive. 27 The capital must be explicitly loss absorbing.

32

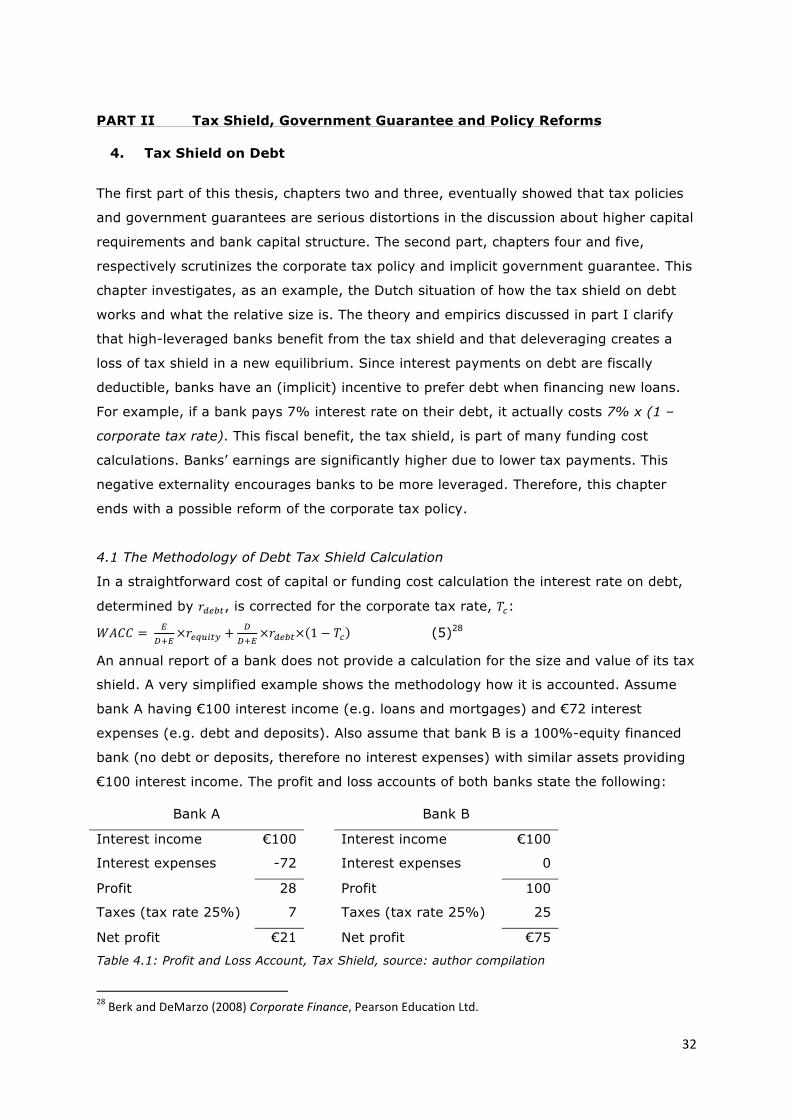

PART II Tax Shield, Government Guarantee and Policy Reforms 4. Tax Shield on Debt

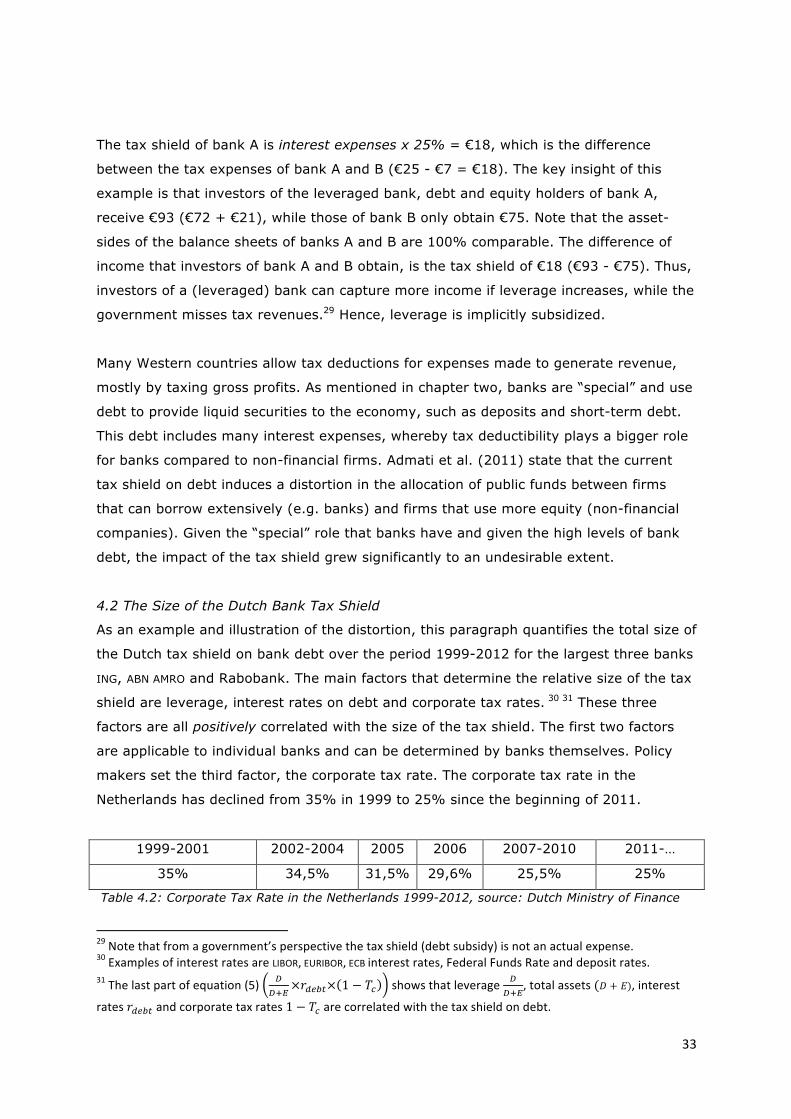

The first part of this thesis, chapters two and three, eventually showed that tax policies