marketing simulation; examples

TRANSCRIPT

Case Studies A sample of applications of Concentric software

Simulate Your Market

© Concentric, Inc. 2014. All rights reserved.

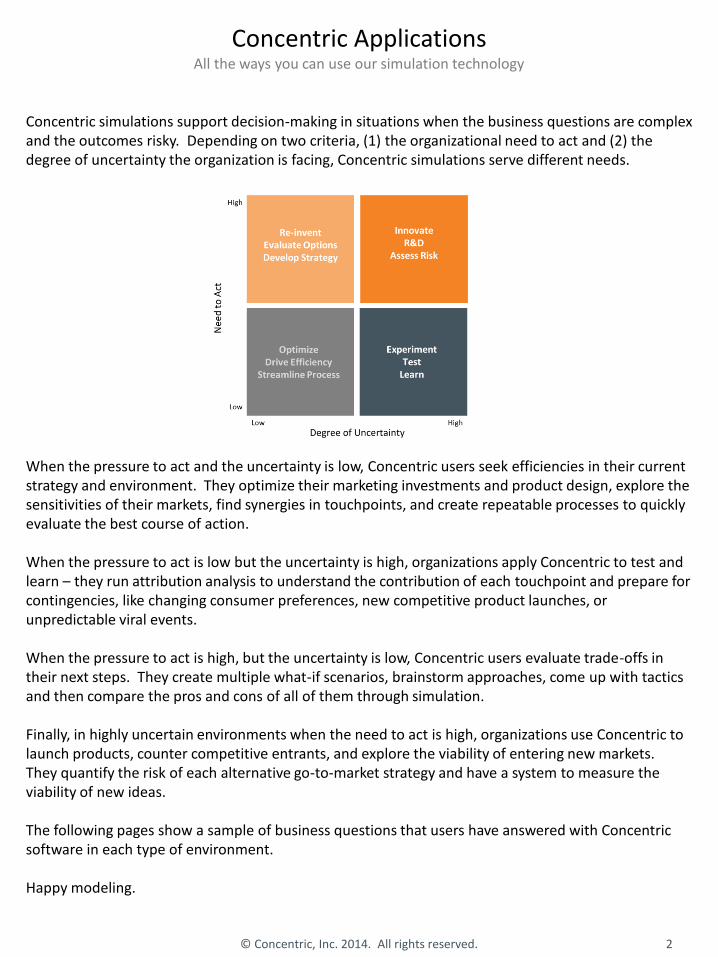

Concentric Applications All the ways you can use our simulation technology

Concentric simulations support decision-making in situations when the business questions are complex and the outcomes risky. Depending on two criteria, (1) the organizational need to act and (2) the degree of uncertainty the organization is facing, Concentric simulations serve different needs. When the pressure to act and the uncertainty is low, Concentric users seek efficiencies in their current strategy and environment. They optimize their marketing investments and product design, explore the sensitivities of their markets, find synergies in touchpoints, and create repeatable processes to quickly evaluate the best course of action. When the pressure to act is low but the uncertainty is high, organizations apply Concentric to test and learn – they run attribution analysis to understand the contribution of each touchpoint and prepare for contingencies, like changing consumer preferences, new competitive product launches, or unpredictable viral events. When the pressure to act is high, but the uncertainty is low, Concentric users evaluate trade-offs in their next steps. They create multiple what-if scenarios, brainstorm approaches, come up with tactics and then compare the pros and cons of all of them through simulation. Finally, in highly uncertain environments when the need to act is high, organizations use Concentric to launch products, counter competitive entrants, and explore the viability of entering new markets. They quantify the risk of each alternative go-to-market strategy and have a system to measure the viability of new ideas. The following pages show a sample of business questions that users have answered with Concentric software in each type of environment. Happy modeling.

© Concentric, Inc. 2014. All rights reserved. 2

Contents A sample of applications

© Concentric, Inc. 2014. All rights reserved. 3

5 Streaming Video What media allocation maximizes subscriptions?

7 Banking What portfolio allocation reaches our targets?

9 Automotive What marketing investment maximizes web traffic?

11 Pre-paid Wireless Which strategy for which region?

13 Coffee Maker Invest in product or in-store marketing?

15 Soup Would promotions increase sales?

17 Telecom How does sentiment move market share?

19 Vitamin Supplement What channels and what timing for a new message?

21 Luxury Perfume What is the impact of earned media?

22 Airline How do we minimize the effect of negative word of mouth?

24 Credit Card What is the trade-off between profit and reputation?

26 Internet TV Network What is the risk of competitive pricing moves?

27 Magazine How do we make our brand more engaging?

29 Pharma Which launch strategy reaches our sales target?

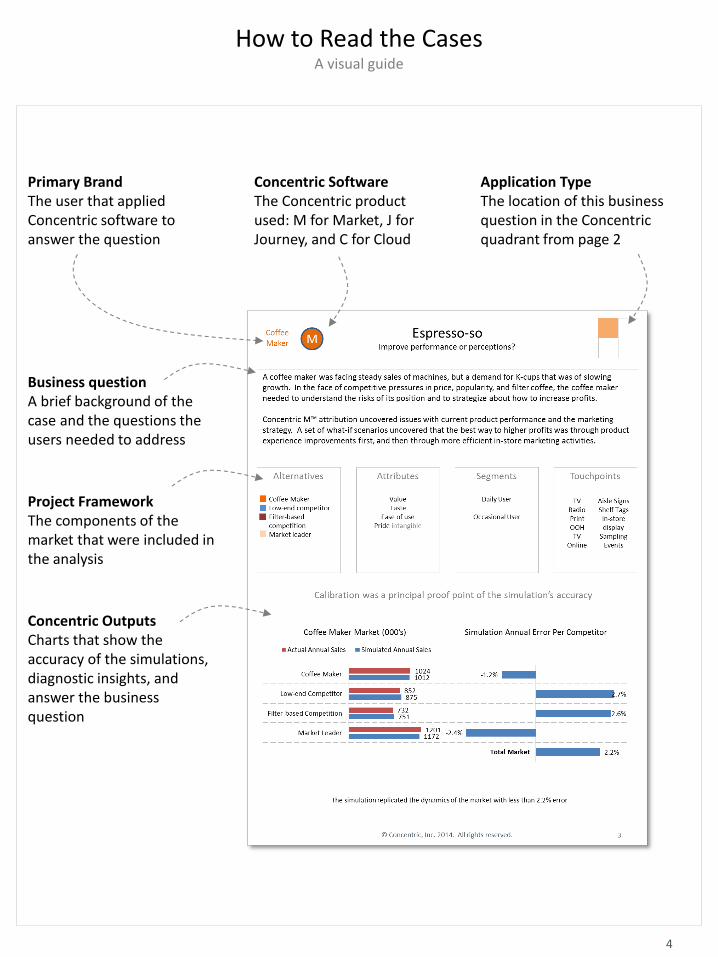

How to Read the Cases A visual guide

Business question A brief background of the case and the questions the users needed to address

Primary Brand The user that applied Concentric software to answer the question

Concentric Software The Concentric product used: M for Market, J for Journey, and C for Cloud

Application Type The location of this business question in the Concentric quadrant from page 2

Project Framework The components of the market that were included in the analysis

Concentric Outputs Charts that show the accuracy of the simulations, diagnostic insights, and answer the business question

4

-

10

20

30

40

50

Sub

scri

ber

ship

(m

illio

ns)

2012 Validation

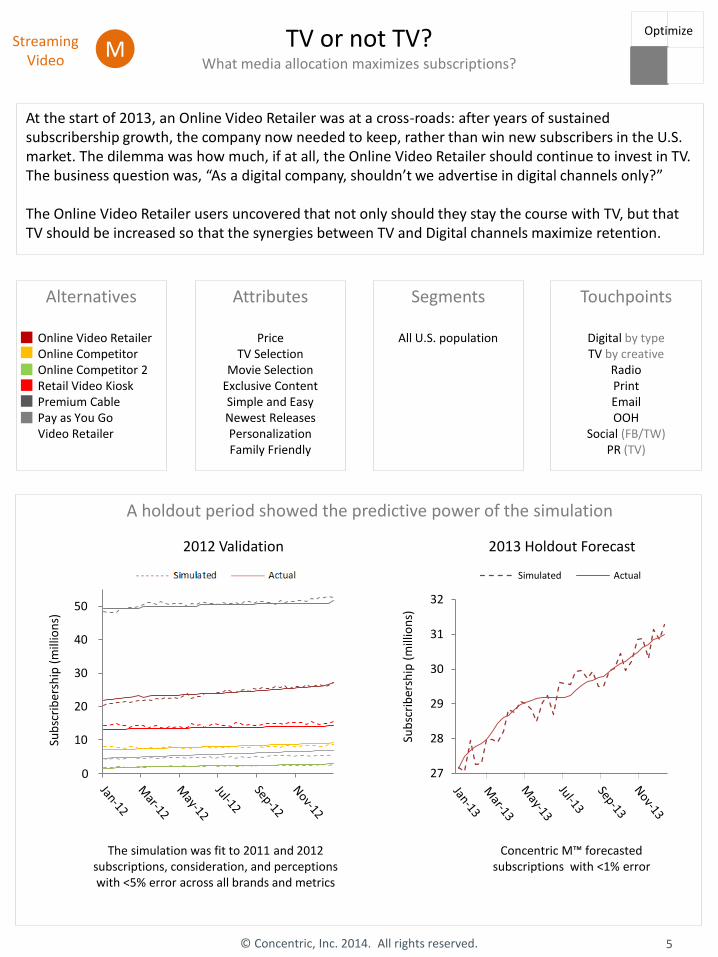

TV or not TV? What media allocation maximizes subscriptions?

At the start of 2013, an Online Video Retailer was at a cross-roads: after years of sustained subscribership growth, the company now needed to keep, rather than win new subscribers in the U.S. market. The dilemma was how much, if at all, the Online Video Retailer should continue to invest in TV. The business question was, “As a digital company, shouldn’t we advertise in digital channels only?” The Online Video Retailer users uncovered that not only should they stay the course with TV, but that TV should be increased so that the synergies between TV and Digital channels maximize retention.

Alternatives

Online Video Retailer Online Competitor Online Competitor 2 Retail Video Kiosk Premium Cable Pay as You Go Video Retailer

Attributes

Price TV Selection

Movie Selection Exclusive Content Simple and Easy Newest Releases Personalization Family Friendly

Segments

All U.S. population

Touchpoints

Digital by type TV by creative

Radio Print Email OOH

Social (FB/TW) PR (TV)

A holdout period showed the predictive power of the simulation

The simulation was fit to 2011 and 2012 subscriptions, consideration, and perceptions with <5% error across all brands and metrics

Concentric M™ forecasted subscriptions with <1% error

27

28

29

30

31

32

Sub

scri

ber

ship

(m

illio

ns)

2013 Holdout Forecast

Simulated Actual

M

5 © Concentric, Inc. 2014. All rights reserved.

Streaming Video

Optimize

0

TV or not TV? What media allocation maximizes subscriptions?

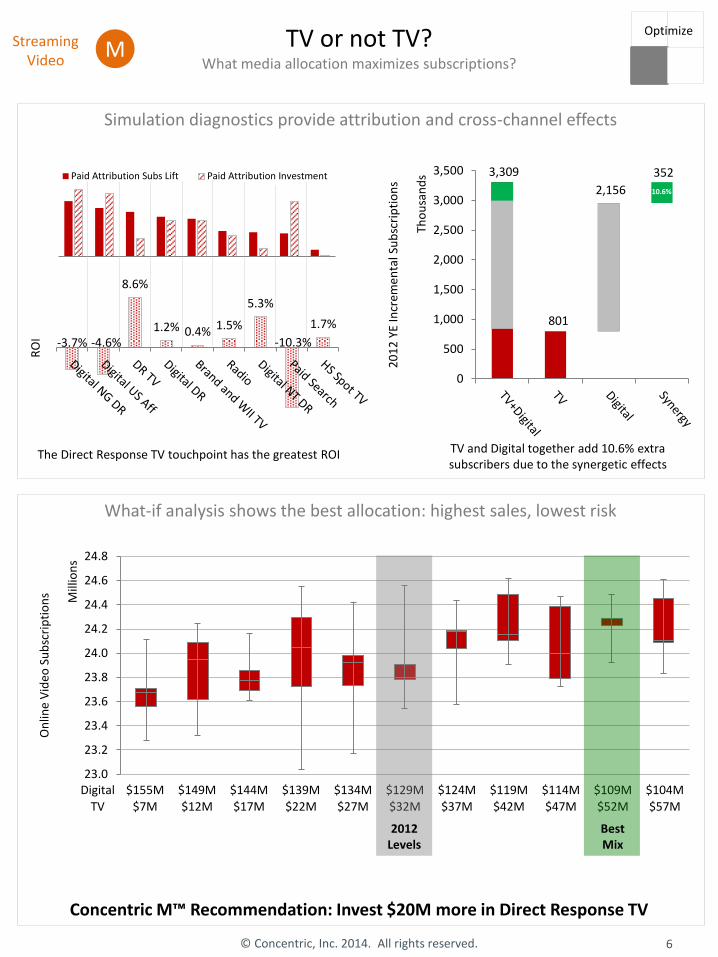

Simulation diagnostics provide attribution and cross-channel effects

What-if analysis shows the best allocation: highest sales, lowest risk

Paid Attribution Subs Lift Paid Attribution Investment

The Direct Response TV touchpoint has the greatest ROI

3,309

801

2,156

352

0

500

1,000

1,500

2,000

2,500

3,000

3,500

20

12

YE

Incr

emen

tal S

ub

scri

pti

on

s

Tho

usa

nd

s

10.6%

TV and Digital together add 10.6% extra subscribers due to the synergetic effects

23.0

23.2

23.4

23.6

23.8

24.0

24.2

24.4

24.6

24.8

On

line

Vid

eo S

ub

scri

pti

on

s Mill

ion

s

Digital $155M $149M $144M $139M $134M $129M $124M $119M $114M $109M $104M

TV $7M $12M $17M $22M $27M $32M $37M $42M $47M $52M $57M

2012 Levels

Best Mix

-3.7% -4.6%

8.6%

1.2% 0.4% 1.5%

5.3%

-10.3%

1.7%

RO

I

Concentric M™ Recommendation: Invest $20M more in Direct Response TV

Streaming Video

M

6 © Concentric, Inc. 2014. All rights reserved.

Optimize

-

20,000

40,000

60,000

80,000

100,000

120,000

Mem

ber

s

Auto - Simulation

Auto - Actual

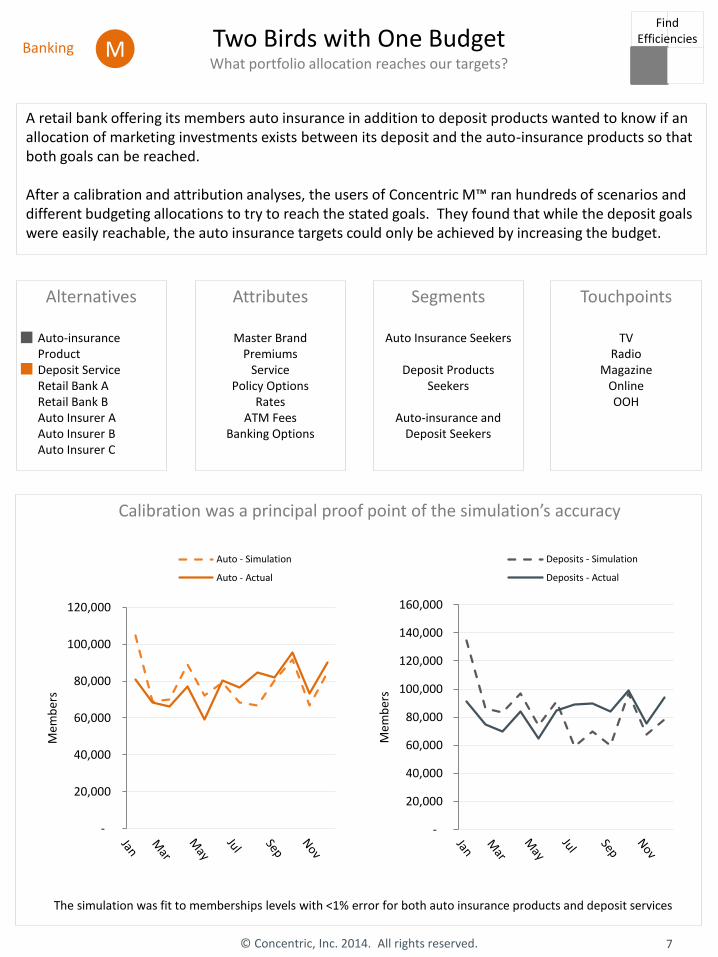

Two Birds with One Budget What portfolio allocation reaches our targets?

A retail bank offering its members auto insurance in addition to deposit products wanted to know if an allocation of marketing investments exists between its deposit and the auto-insurance products so that both goals can be reached. After a calibration and attribution analyses, the users of Concentric M™ ran hundreds of scenarios and different budgeting allocations to try to reach the stated goals. They found that while the deposit goals were easily reachable, the auto insurance targets could only be achieved by increasing the budget.

Alternatives

Auto-insurance Product Deposit Service Retail Bank A Retail Bank B Auto Insurer A Auto Insurer B Auto Insurer C

Attributes

Master Brand Premiums

Service Policy Options

Rates ATM Fees

Banking Options

Segments

Auto Insurance Seekers

Deposit Products Seekers

Auto-insurance and

Deposit Seekers

Touchpoints

TV Radio

Magazine Online OOH

Calibration was a principal proof point of the simulation’s accuracy

The simulation was fit to memberships levels with <1% error for both auto insurance products and deposit services

Banking M

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

Mem

ber

s

Deposits - Simulation

Deposits - Actual

7 © Concentric, Inc. 2014. All rights reserved.

Find Efficiencies

Base, 817,500

Media, 230,000

Base, 952,500

Media, 70,000

Two Birds with One Budget What portfolio allocation reaches our targets?

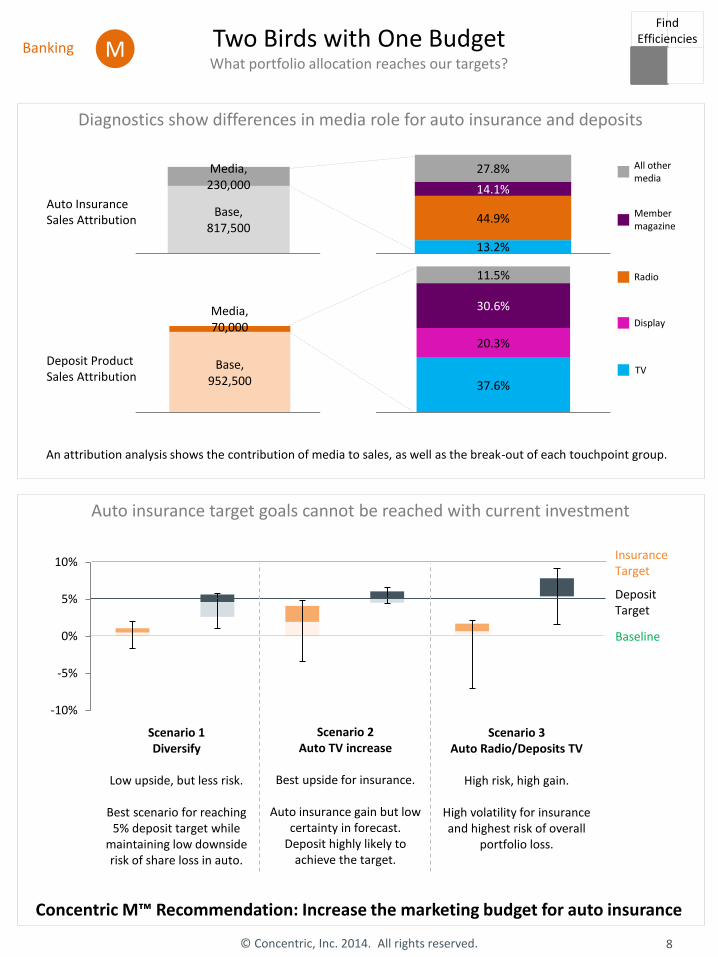

Diagnostics show differences in media role for auto insurance and deposits

Auto insurance target goals cannot be reached with current investment

M

-10%

-5%

0%

5%

10%

Scenario 1 Diversify

Low upside, but less risk.

Best scenario for reaching

5% deposit target while maintaining low downside risk of share loss in auto.

Scenario 2 Auto TV increase

Best upside for insurance.

Auto insurance gain but low

certainty in forecast. Deposit highly likely to

achieve the target.

Scenario 3 Auto Radio/Deposits TV

High risk, high gain.

High volatility for insurance and highest risk of overall

portfolio loss.

Deposit Target

Insurance Target

Baseline

Concentric M™ Recommendation: Increase the marketing budget for auto insurance

13.2%

44.9%

14.1%

27.8%

An attribution analysis shows the contribution of media to sales, as well as the break-out of each touchpoint group.

37.6%

20.3%

30.6%

11.5%

Auto Insurance Sales Attribution

Deposit Product Sales Attribution

All other media

Member magazine

Radio

Display

TV

8 © Concentric, Inc. 2014. All rights reserved.

Banking

Find Efficiencies

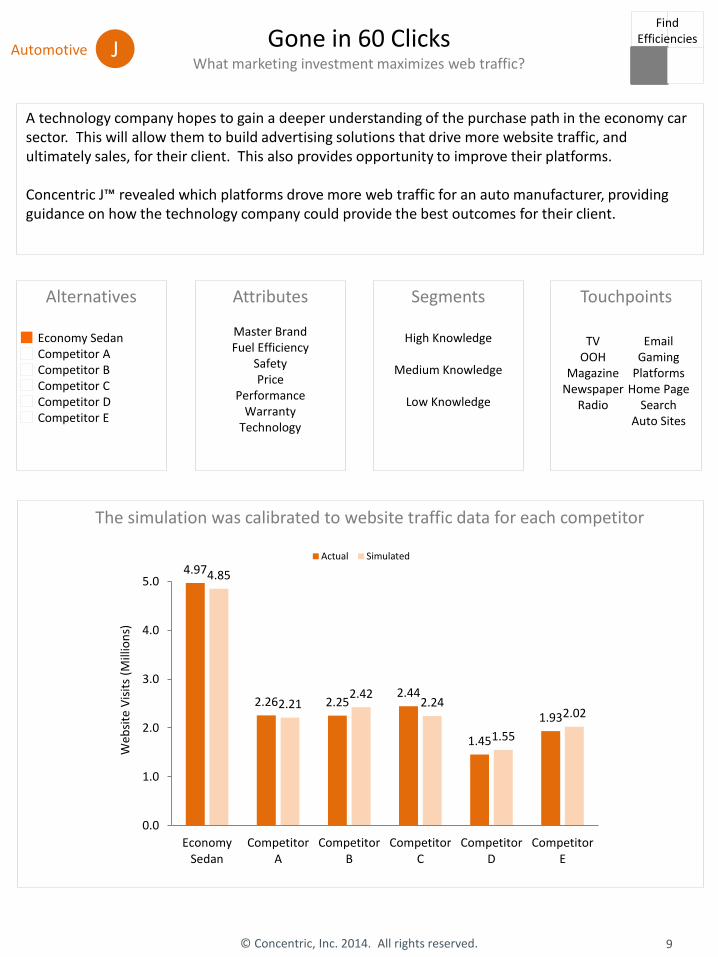

Gone in 60 Clicks What marketing investment maximizes web traffic?

A technology company hopes to gain a deeper understanding of the purchase path in the economy car sector. This will allow them to build advertising solutions that drive more website traffic, and ultimately sales, for their client. This also provides opportunity to improve their platforms. Concentric J™ revealed which platforms drove more web traffic for an auto manufacturer, providing guidance on how the technology company could provide the best outcomes for their client.

Alternatives

Economy Sedan Competitor A Competitor B Competitor C Competitor D Competitor E

Attributes

Master Brand Fuel Efficiency

Safety Price

Performance Warranty

Technology

Segments

High Knowledge

Medium Knowledge

Low Knowledge

Touchpoints

J

TV OOH

Magazine Newspaper

Radio

Email Gaming

Platforms Home Page

Search Auto Sites

The simulation was calibrated to website traffic data for each competitor

4.97

2.26 2.25 2.44

1.45

1.93

4.85

2.21 2.42

2.24

1.55

2.02

0.0

1.0

2.0

3.0

4.0

5.0

EconomySedan

CompetitorA

CompetitorB

CompetitorC

CompetitorD

CompetitorE

Web

site

Vis

its

(Mill

ion

s)

Actual Simulated

9 © Concentric, Inc. 2014. All rights reserved.

Automotive

Find Efficiencies

Gone in 60 Clicks What marketing investment maximizes web traffic?

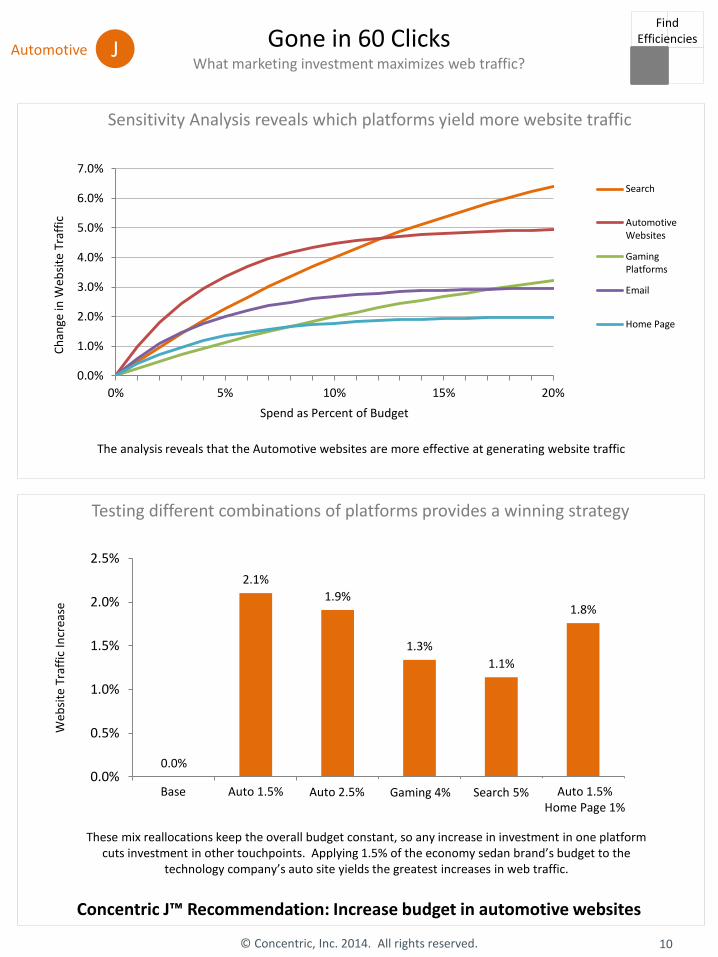

Testing different combinations of platforms provides a winning strategy

Concentric J™ Recommendation: Increase budget in automotive websites

10 © Concentric, Inc. 2014. All rights reserved.

Automotive J

0.0%

2.1%

1.9%

1.3%

1.1%

1.8%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Base MS Auto 1.5 MS Auto 2.5 MS Windows 4 MS Bing 5 Auto 1.5 +Windows 1

Web

site

Tra

ffic

In

crea

se

Sensitivity Analysis reveals which platforms yield more website traffic

Auto 1.5% Auto 2.5% Search 5% Auto 1.5% Home Page 1%

Base Gaming 4%

These mix reallocations keep the overall budget constant, so any increase in investment in one platform cuts investment in other touchpoints. Applying 1.5% of the economy sedan brand’s budget to the

technology company’s auto site yields the greatest increases in web traffic.

The analysis reveals that the Automotive websites are more effective at generating website traffic

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0% 5% 10% 15% 20%

Ch

ange

in W

ebsi

te T

raff

ic

Spend as Percent of Budget

Search

AutomotiveWebsites

GamingPlatforms

Home Page

Find Efficiencies

165

69

155

71

35

106

194

73

170

78

33

127

Gro

ss A

dd

s (0

00

)

Forecast Data

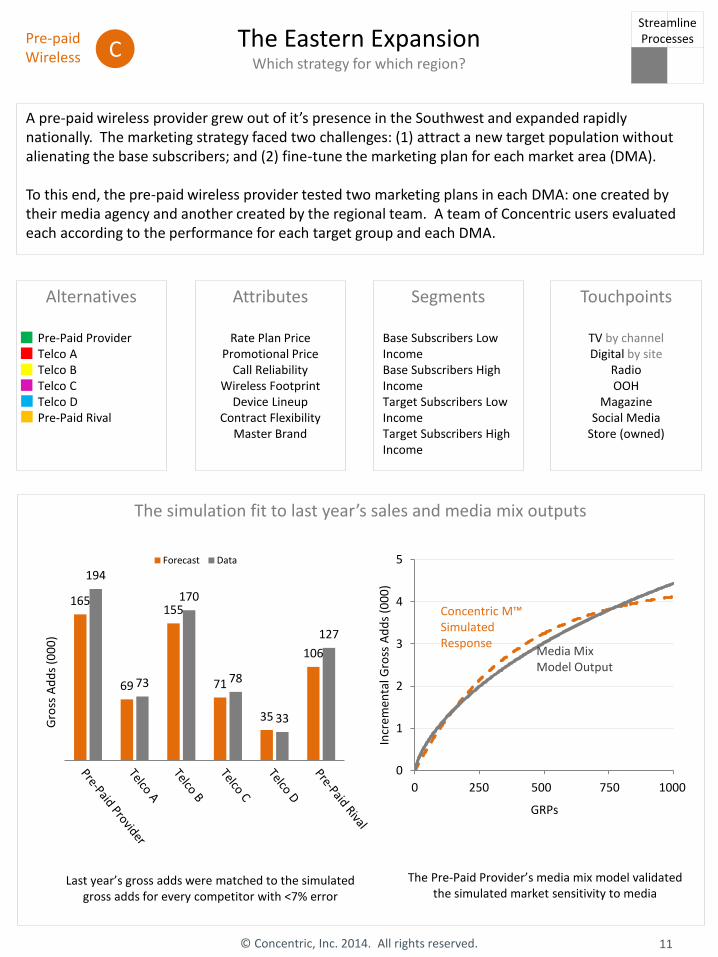

The Eastern Expansion Which strategy for which region?

The simulation fit to last year’s sales and media mix outputs

Last year’s gross adds were matched to the simulated gross adds for every competitor with <7% error

Pre-paid Wireless

A pre-paid wireless provider grew out of it’s presence in the Southwest and expanded rapidly nationally. The marketing strategy faced two challenges: (1) attract a new target population without alienating the base subscribers; and (2) fine-tune the marketing plan for each market area (DMA). To this end, the pre-paid wireless provider tested two marketing plans in each DMA: one created by their media agency and another created by the regional team. A team of Concentric users evaluated each according to the performance for each target group and each DMA.

Alternatives

Pre-Paid Provider Telco A Telco B Telco C Telco D Pre-Paid Rival

Attributes

Rate Plan Price Promotional Price

Call Reliability Wireless Footprint

Device Lineup Contract Flexibility

Master Brand

Segments

Base Subscribers Low Income Base Subscribers High Income Target Subscribers Low Income Target Subscribers High Income

Touchpoints

TV by channel Digital by site

Radio OOH

Magazine Social Media

Store (owned)

C

0

1

2

3

4

5

1 251 501 751 1001

Incr

emen

tal G

ross

Ad

ds

(00

0)

GRPs

Concentric M™ Simulated Response

Media Mix Model Output

The Pre-Paid Provider’s media mix model validated the simulated market sensitivity to media

11 © Concentric, Inc. 2014. All rights reserved.

Streamline Processes

0 250 500 750 1000 GRPs

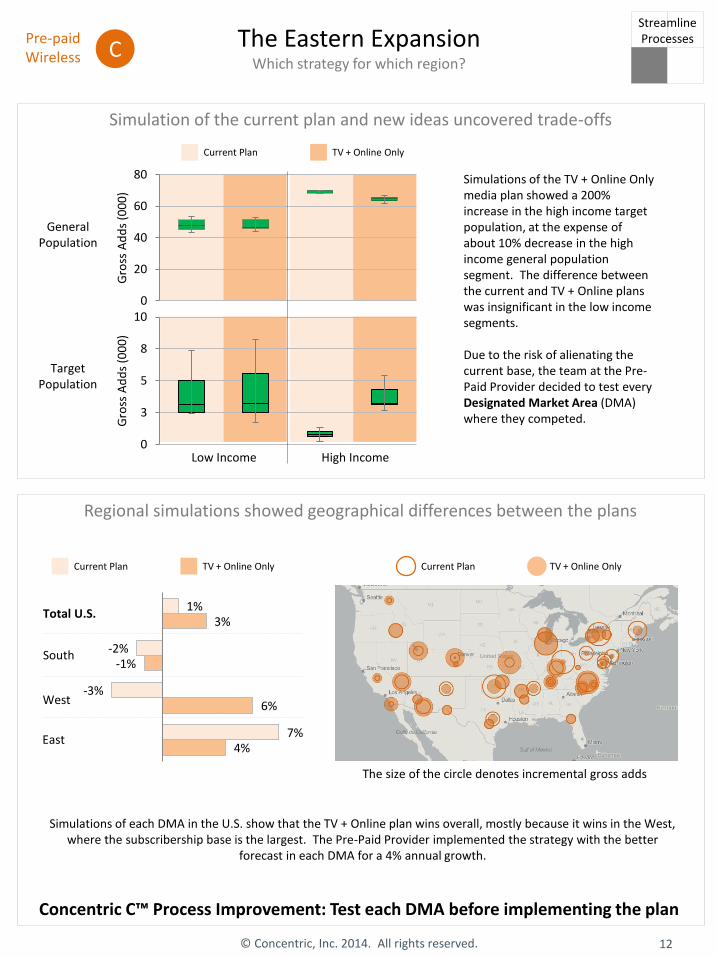

Simulation of the current plan and new ideas uncovered trade-offs

The Eastern Expansion Which strategy for which region?

Regional simulations showed geographical differences between the plans

Concentric C™ Process Improvement: Test each DMA before implementing the plan

Simulations of each DMA in the U.S. show that the TV + Online plan wins overall, mostly because it wins in the West, where the subscribership base is the largest. The Pre-Paid Provider implemented the strategy with the better

forecast in each DMA for a 4% annual growth.

Pre-paid Wireless C

4%

6%

-1%

3%

7%

-3%

-2%

1% Total U.S.

South

West

East

Current Plan TV + Online Only

Low Income 0

3

5

8

10

Gro

ss A

dd

s (0

00

)

0

20

40

60

80

Gro

ss A

dd

s (0

00

)

High Income

General Population

Target Population

Simulations of the TV + Online Only media plan showed a 200% increase in the high income target population, at the expense of about 10% decrease in the high income general population segment. The difference between the current and TV + Online plans was insignificant in the low income segments. Due to the risk of alienating the current base, the team at the Pre-Paid Provider decided to test every Designated Market Area (DMA) where they competed.

The size of the circle denotes incremental gross adds

12 © Concentric, Inc. 2014. All rights reserved.

Streamline Processes

Current Plan TV + Online Only Current Plan TV + Online Only

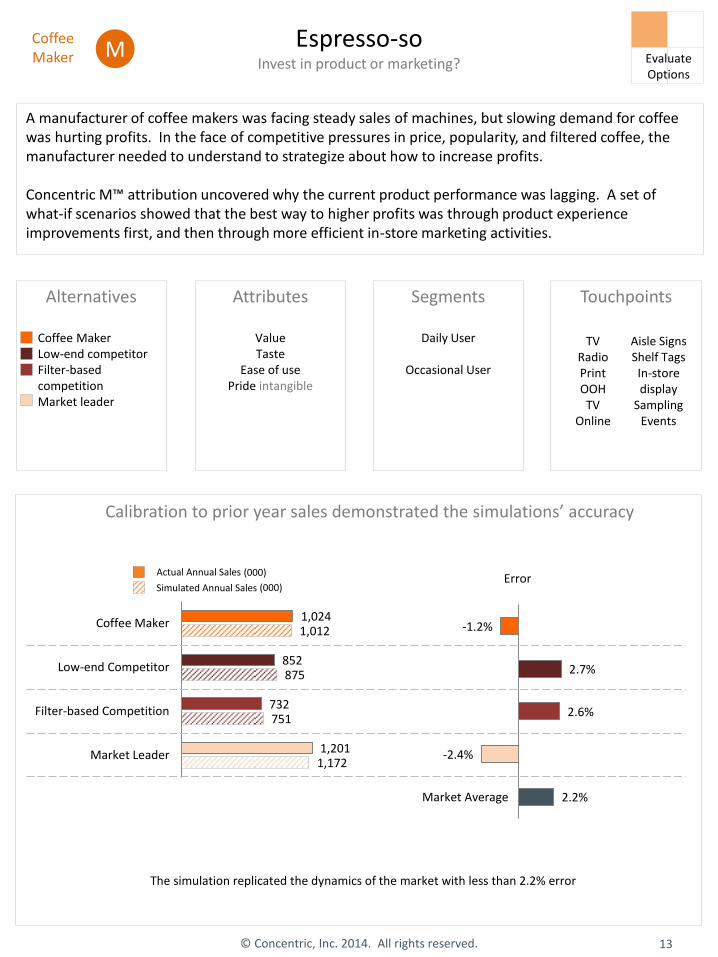

Espresso-so Invest in product or marketing?

A manufacturer of coffee makers was facing steady sales of machines, but slowing demand for coffee was hurting profits. In the face of competitive pressures in price, popularity, and filtered coffee, the manufacturer needed to understand to strategize about how to increase profits. Concentric M™ attribution uncovered why the current product performance was lagging. A set of what-if scenarios showed that the best way to higher profits was through product experience improvements first, and then through more efficient in-store marketing activities.

Alternatives

Coffee Maker Low-end competitor Filter-based competition Market leader

Attributes

Value Taste

Ease of use Pride intangible

Segments

Daily User

Occasional User

Touchpoints

Calibration to prior year sales demonstrated the simulations’ accuracy

The simulation replicated the dynamics of the market with less than 2.2% error

Coffee Maker M

TV Radio Print OOH TV

Online

Aisle Signs Shelf Tags In-store display

Sampling Events

1,172

751

875

1,012

1,201

732

852

1,024

Market Leader

Filter-based Competition

Low-end Competitor

Coffee Maker

Actual Annual Sales

Simulated Annual Sales

2.2%

-2.4%

2.6%

2.7%

-1.2%

Market Average

13 © Concentric, Inc. 2014. All rights reserved.

Evaluate Options

(000) Error

(000)

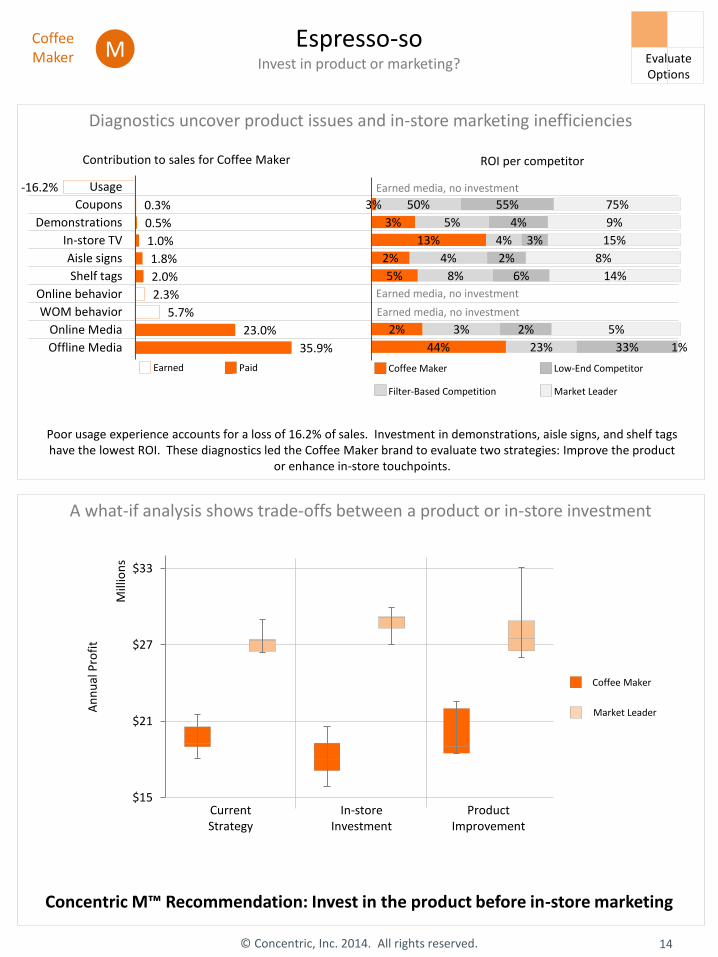

Espresso-so Invest in product or marketing?

Diagnostics uncover product issues and in-store marketing inefficiencies

A what-if analysis shows trade-offs between a product or in-store investment

Coffee Maker M

Concentric M™ Recommendation: Invest in the product before in-store marketing

35.9%

23.0%

5.7%

2.3%

2.0%

1.8%

1.0%

0.5%

0.3%

-16.2%

Offline Media

Online Media

WOM behavior

Online behavior

Shelf tags

Aisle signs

In-store TV

Demonstrations

Coupons

Usage

Contribution to sales for Coffee Maker

44%

2%

5%

2%

13%

3%

3%

23%

3%

8%

4%

4%

5%

50%

33%

2%

6%

2%

3%

4%

55%

1%

5%

14%

8%

15%

9%

75%

ROI per competitor

Coffee Maker Low-End Competitor

Filter-Based Competition Market Leader

Earned media, no investment

Earned media, no investment

Earned media, no investment

$15

$21

$27

$33

An

nu

al P

rofi

t

Mill

ion

s

Earned Paid

Poor usage experience accounts for a loss of 16.2% of sales. Investment in demonstrations, aisle signs, and shelf tags have the lowest ROI. These diagnostics led the Coffee Maker brand to evaluate two strategies: Improve the product

or enhance in-store touchpoints.

Current Strategy

In-store Investment

Product Improvement

14 © Concentric, Inc. 2014. All rights reserved.

Evaluate Options

Market Leader

Coffee Maker

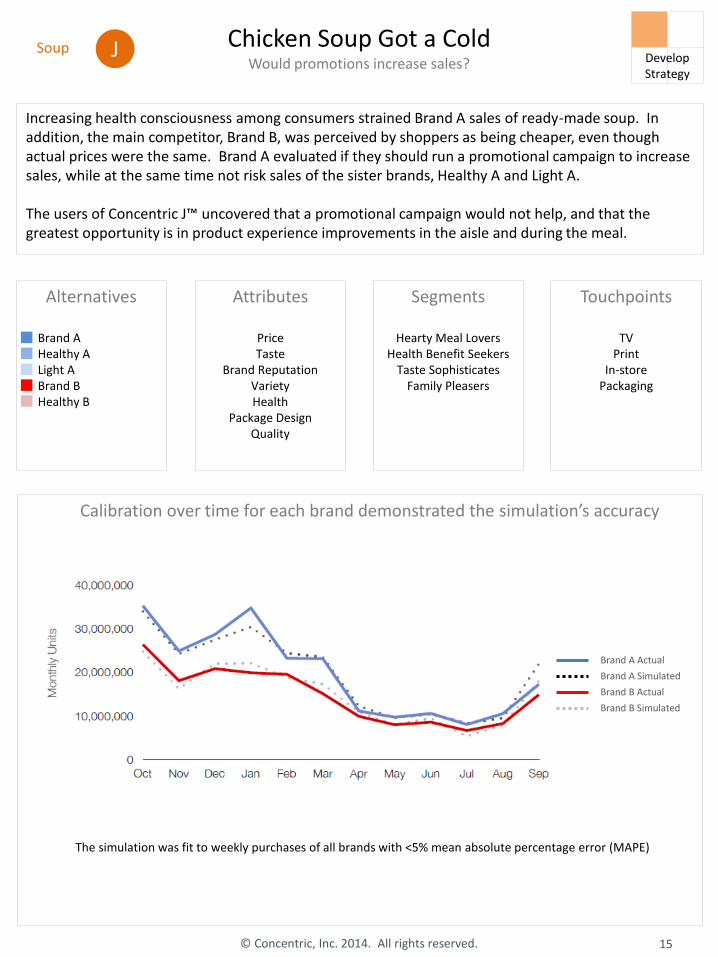

Chicken Soup Got a Cold Would promotions increase sales?

Increasing health consciousness among consumers strained Brand A sales of ready-made soup. In addition, the main competitor, Brand B, was perceived by shoppers as being cheaper, even though actual prices were the same. Brand A evaluated if they should run a promotional campaign to increase sales, while at the same time not risk sales of the sister brands, Healthy A and Light A. The users of Concentric J™ uncovered that a promotional campaign would not help, and that the greatest opportunity is in product experience improvements in the aisle and during the meal.

Alternatives

Brand A Healthy A Light A Brand B Healthy B

Attributes

Price Taste

Brand Reputation Variety Health

Package Design Quality

Segments

Hearty Meal Lovers Health Benefit Seekers

Taste Sophisticates Family Pleasers

Touchpoints

TV Print

In-store Packaging

Calibration over time for each brand demonstrated the simulation’s accuracy

The simulation was fit to weekly purchases of all brands with <5% mean absolute percentage error (MAPE)

Soup

Brand A Actual

Brand A Simulated

Brand B Actual

Brand B Simulated

J

15 © Concentric, Inc. 2014. All rights reserved.

Develop Strategy

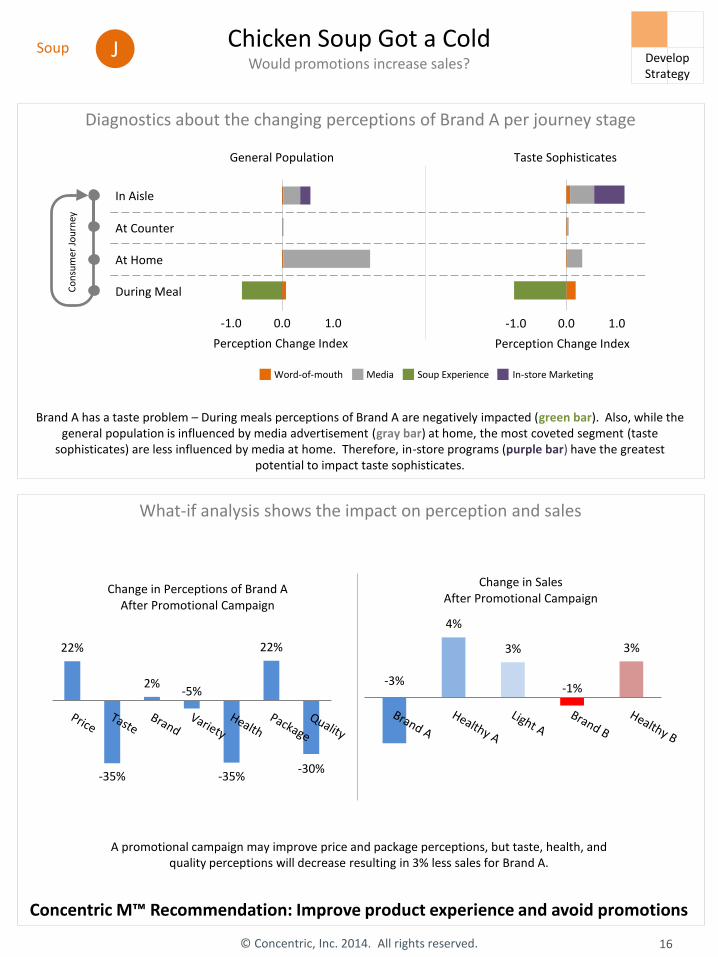

Chicken Soup Got a Cold Would promotions increase sales?

Diagnostics about the changing perceptions of Brand A per journey stage

What-if analysis shows the impact on perception and sales

Brand A has a taste problem – During meals perceptions of Brand A are negatively impacted (green bar). Also, while the general population is influenced by media advertisement (gray bar) at home, the most coveted segment (taste

sophisticates) are less influenced by media at home. Therefore, in-store programs (purple bar) have the greatest potential to impact taste sophisticates.

Concentric M™ Recommendation: Improve product experience and avoid promotions

-2.0 -1.0 0.0 1.0 2.0

Perception Change Index

-2.0 -1.0 0.0 1.0 2.0

Perception Change Index

General Population Taste Sophisticates

In Aisle

At Counter

At Home

During Meal Co

nsu

mer

Jo

urn

ey

Word-of-mouth Media Soup Experience In-store Marketing

22%

-35%

2% -5%

-35%

22%

-30%

Change in Perceptions of Brand A After Promotional Campaign

-3%

4%

3%

-1%

3%

Change in Sales After Promotional Campaign

A promotional campaign may improve price and package perceptions, but taste, health, and quality perceptions will decrease resulting in 3% less sales for Brand A.

Soup J

16 © Concentric, Inc. 2014. All rights reserved.

Develop Strategy

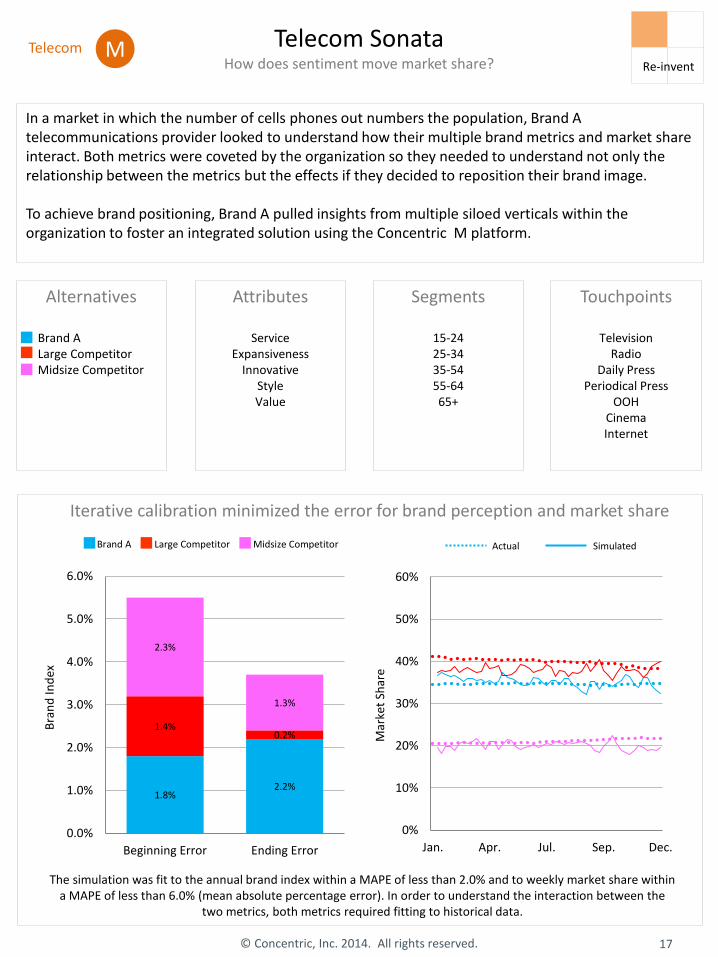

In a market in which the number of cells phones out numbers the population, Brand A telecommunications provider looked to understand how their multiple brand metrics and market share interact. Both metrics were coveted by the organization so they needed to understand not only the relationship between the metrics but the effects if they decided to reposition their brand image. To achieve brand positioning, Brand A pulled insights from multiple siloed verticals within the organization to foster an integrated solution using the Concentric M platform.

Alternatives

Brand A Large Competitor Midsize Competitor

Attributes

Service Expansiveness

Innovative Style Value

Segments

15-24 25-34 35-54 55-64 65+

Touchpoints

Television Radio

Daily Press Periodical Press

OOH Cinema Internet

Iterative calibration minimized the error for brand perception and market share

The simulation was fit to the annual brand index within a MAPE of less than 2.0% and to weekly market share within a MAPE of less than 6.0% (mean absolute percentage error). In order to understand the interaction between the

two metrics, both metrics required fitting to historical data.

17 © Concentric, Inc. 2014. All rights reserved.

Telecom Sonata How does sentiment move market share? Re-invent

Telecom M

0%

10%

20%

30%

40%

50%

60%

Jan. Apr. Jul. Sep. Dec.

Mar

ket

Shar

e

Actual Simulated

1.8% 2.2%

1.4% 0.2%

2.3%

1.3%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Beginning Error Ending Error

Bra

nd

Ind

ex

Brand A Large Competitor Midsize Competitor

Different campaigns impact brand equity and market share differently

-1.1%

1.0%

0.6%

-0.5%

-0.8%

Market Share

-0.5%

0.9%

0.6%

-0.7%

-2.5%

Brand Index

Diagnostics showed correlation between sentiment and market share.

Each of the brand metrics included in the simulation were tested overall and by individual components to see if there was a correlation between them. Tests indicate that not all brand metrics included were correlated. As a part of this analysis, the brand looked to adopt only one brand tracking metric to stream line their insights for clearer information and continuous feeds into their simulation. Further analysis in the form of what-if scenarios were conducted in order to see how the market responded to repositioning their brand image.

Concentric M™ Recommendation: Invest in the Service Campaign

18 © Concentric, Inc. 2014. All rights reserved.

Telecom Sonata How does sentiment move market share? Re-invent

Telecom M

34.2%

34.5%

34.8%

35.1%

4.4

4.5

4.6

4.7

4.8

Jan. April July Nov. Dec.

Brand Index Market Share

0%

3%

0%

1%

0% 0%

1%

0%

0% 0%

-2.0%

0.0%

2.0%

4.0%C

han

ge

Service

Innovation

Style

Value

Brand

Market Sh

are Se

nti

men

t

Campaign

1.5%

-2.4%

-2.5%

0.1%

-0.2%

2.5%

Error

A Vitamin a Day Keeps the Doctor Away What channels and what timing for a new message?

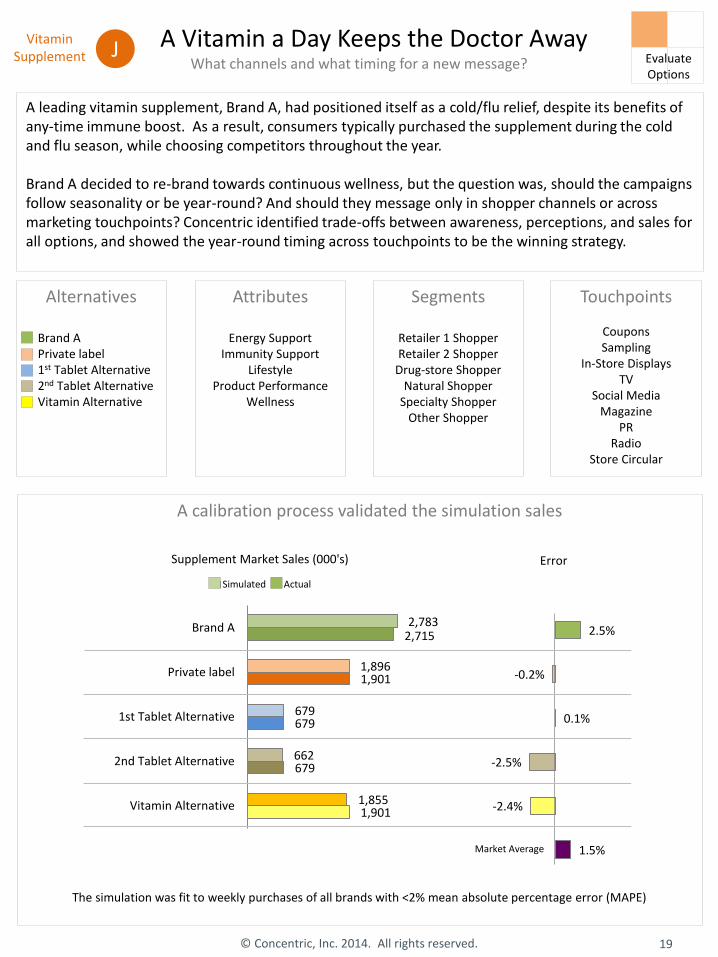

A leading vitamin supplement, Brand A, had positioned itself as a cold/flu relief, despite its benefits of any-time immune boost. As a result, consumers typically purchased the supplement during the cold and flu season, while choosing competitors throughout the year. Brand A decided to re-brand towards continuous wellness, but the question was, should the campaigns follow seasonality or be year-round? And should they message only in shopper channels or across marketing touchpoints? Concentric identified trade-offs between awareness, perceptions, and sales for all options, and showed the year-round timing across touchpoints to be the winning strategy.

Alternatives

Brand A Private label 1st Tablet Alternative 2nd Tablet Alternative Vitamin Alternative

Attributes

Energy Support Immunity Support

Lifestyle Product Performance

Wellness

Segments

Retailer 1 Shopper Retailer 2 Shopper

Drug-store Shopper Natural Shopper

Specialty Shopper Other Shopper

Touchpoints

Coupons Sampling

In-Store Displays TV

Social Media Magazine

PR Radio

Store Circular

© Concentric, Inc. 2014. All rights reserved.

Vitamin Supplement J Evaluate

Options

A calibration process validated the simulation sales

The simulation was fit to weekly purchases of all brands with <2% mean absolute percentage error (MAPE)

1,901

679

679

1,901

2,715

1,855

662

679

1,896

2,783

Vitamin Alternative

2nd Tablet Alternative

1st Tablet Alternative

Private label

Brand A

Supplement Market Sales (000's)

Simulated Actual

Market Average

19

What-if scenario analysis shows big trade-offs between the strategies

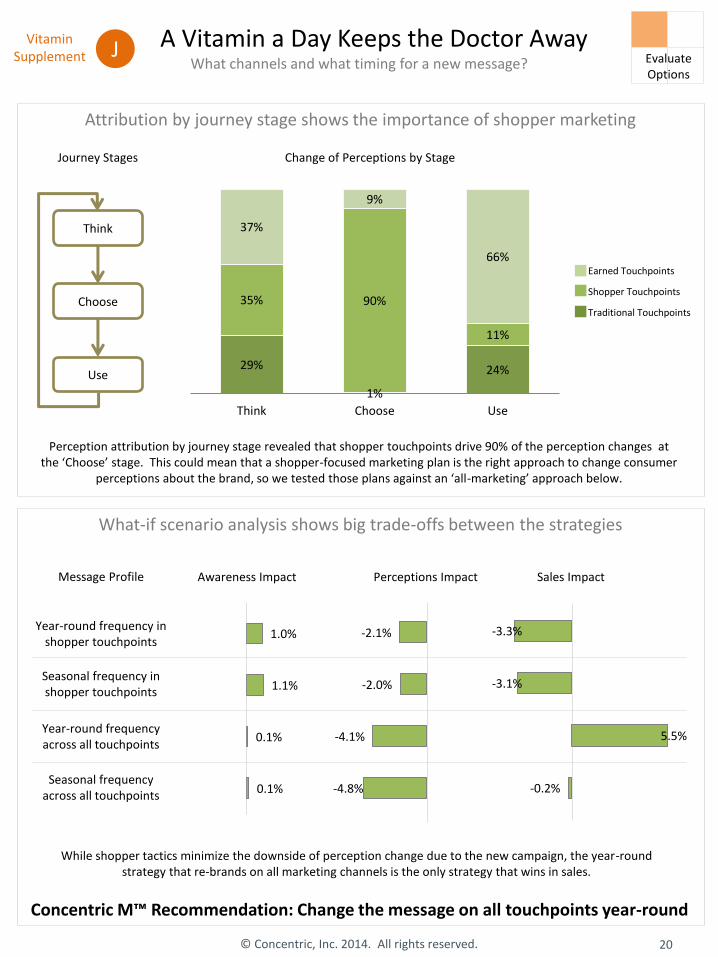

Attribution by journey stage shows the importance of shopper marketing

Concentric M™ Recommendation: Change the message on all touchpoints year-round

Perception attribution by journey stage revealed that shopper touchpoints drive 90% of the perception changes at the ‘Choose’ stage. This could mean that a shopper-focused marketing plan is the right approach to change consumer

perceptions about the brand, so we tested those plans against an ‘all-marketing’ approach below.

20 © Concentric, Inc. 2014. All rights reserved.

A Vitamin a Day Keeps the Doctor Away What channels and what timing for a new message?

Vitamin Supplement Evaluate

Options

29%

1%

24%

35% 90%

11%

37%

9%

66%

Think Choose Use

Change of Perceptions by Stage

Earned Touchpoints

Shopper Touchpoints

Traditional Touchpoints

While shopper tactics minimize the downside of perception change due to the new campaign, the year-round strategy that re-brands on all marketing channels is the only strategy that wins in sales.

-0.2%

5.5%

-3.1%

-3.3% Year-round frequency in shopper touchpoints

Sales Impact

0.1%

0.1%

1.1%

1.0%

Awareness Impact

-4.8%

-4.1%

-2.0%

-2.1%

Perceptions Impact

Seasonal frequency in shopper touchpoints

Year-round frequency across all touchpoints

Seasonal frequency across all touchpoints

Message Profile

Journey Stages

Think

Choose

Use

J

Scent of a Brand What is the impact of earned media?

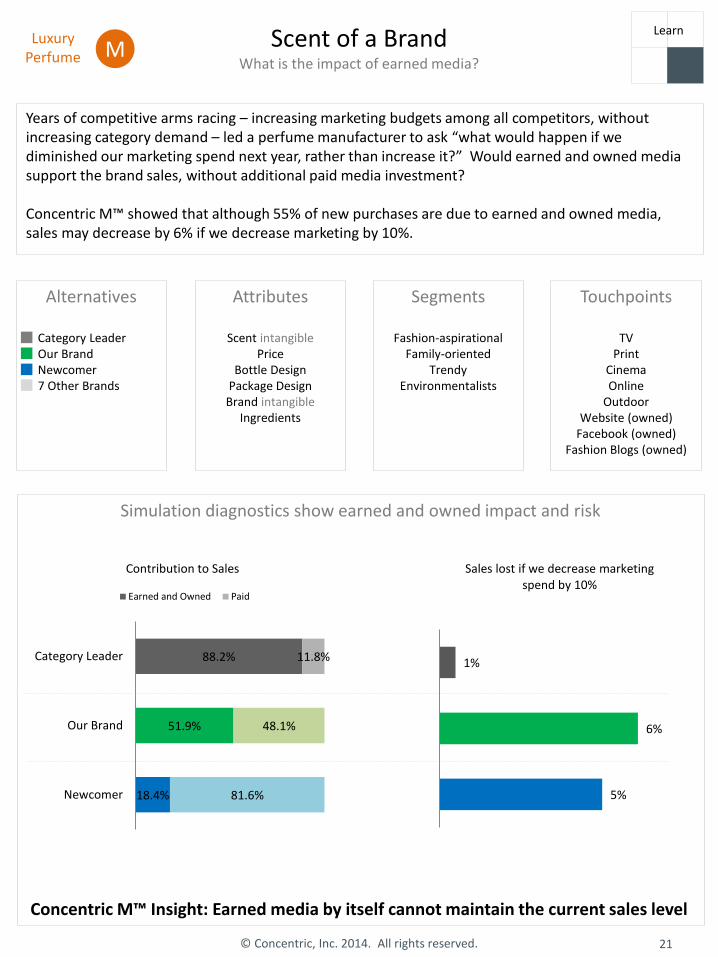

Simulation diagnostics show earned and owned impact and risk

Concentric M™ Insight: Earned media by itself cannot maintain the current sales level

Luxury Perfume

Years of competitive arms racing – increasing marketing budgets among all competitors, without increasing category demand – led a perfume manufacturer to ask “what would happen if we diminished our marketing spend next year, rather than increase it?” Would earned and owned media support the brand sales, without additional paid media investment? Concentric M™ showed that although 55% of new purchases are due to earned and owned media, sales may decrease by 6% if we decrease marketing by 10%.

Alternatives

Category Leader Our Brand Newcomer 7 Other Brands

Attributes

Scent intangible Price

Bottle Design Package Design

Brand intangible Ingredients

Segments

Fashion-aspirational Family-oriented

Trendy Environmentalists

Touchpoints

TV Print

Cinema Online

Outdoor Website (owned)

Facebook (owned) Fashion Blogs (owned)

18.4%

51.9%

88.2%

81.6%

48.1%

11.8%

Newcomer

Our Brand

Category Leader

Contribution to Sales

Earned and Owned Paid

5%

6%

1%

Sales lost if we decrease marketing spend by 10%

M

21 © Concentric, Inc. 2014. All rights reserved.

Learn

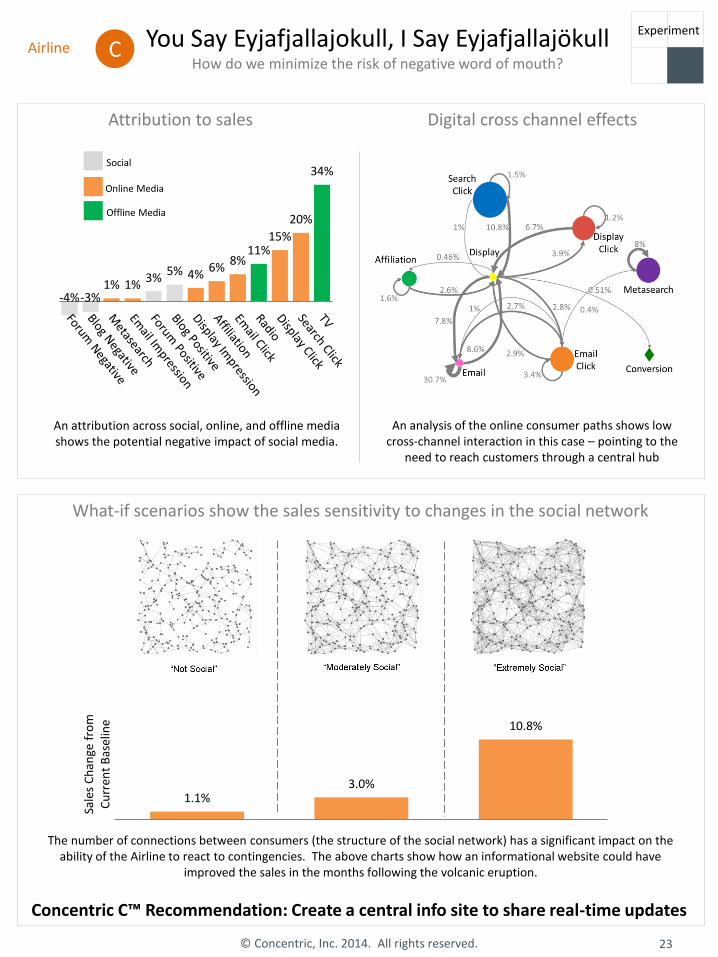

You Say Eyjafjallajokull, I Say Eyjafjallajökull How do we minimize the risk of negative word of mouth?

The simulation recreated the level of observed events and behaviors

Airline

In April 2010, an Icelandic volcano covered northern Europe with an ash cloud that grounded flights for weeks and stranded passengers – most of whom went to social media for information and to share. One airline decided to analyze the terabytes of attitudinal, behavioral, and transactional data of the months before and after the disruption to understand how they can react better to large social media events that may impact the future sales and brand engagement among their customer base. They turned to Concentric C™ for answers and found them in the analysis of their passengers social network structure.

Alternatives

Airline Competitor A Competitor B Competitor C

Attributes

Price Service

Experience Customer Service

Destinations

Segments

Elite Members Frequent Fliers

Occasional Passengers

Touchpoints

C

22 © Concentric, Inc. 2014. All rights reserved.

299

12

2,451

1,020

12

746

289

7

2,273

1,319

23

749

Conversion Affiliation Search Email Metasearch Display Click

Simulation Median Real Values

608,000

626,000

Co

nve

rsio

ns

(00

0)

Display Imp.

Weighted Absolute Percentage Error (WAPE): 2.93%

TV Radio Blog

Forum Facebook

Search Email

Metasearch Display

Affiliation Website

Experiment

You Say Eyjafjallajokull, I Say Eyjafjallajökull How do we minimize the risk of negative word of mouth?

What-if scenarios show the sales sensitivity to changes in the social network

Concentric C™ Recommendation: Create a central info site to share real-time updates

The number of connections between consumers (the structure of the social network) has a significant impact on the ability of the Airline to react to contingencies. The above charts show how an informational website could have

improved the sales in the months following the volcanic eruption.

23 © Concentric, Inc. 2014. All rights reserved.

-4% -3% 1% 1%

3% 5% 4%

6% 8%

11% 15%

20%

34% Social

Online Media

Offline Media

An attribution across social, online, and offline media shows the potential negative impact of social media.

Attribution to sales Digital cross channel effects

An analysis of the online consumer paths shows low cross-channel interaction in this case – pointing to the

need to reach customers through a central hub

1.1% 3.0%

10.8%

Sale

s C

han

ge f

rom

C

urr

ent

Bas

elin

e

Airline C Experiment

-12

13

31 33

11

41

-18

11 5

24

43

6

26

-6 -18

13

3

74

5

-5

31 32 26

7 5

-20

-10

0

10

20

30

40

50

60

70

80

Ind

ex o

f P

erce

pti

on

Ch

ange

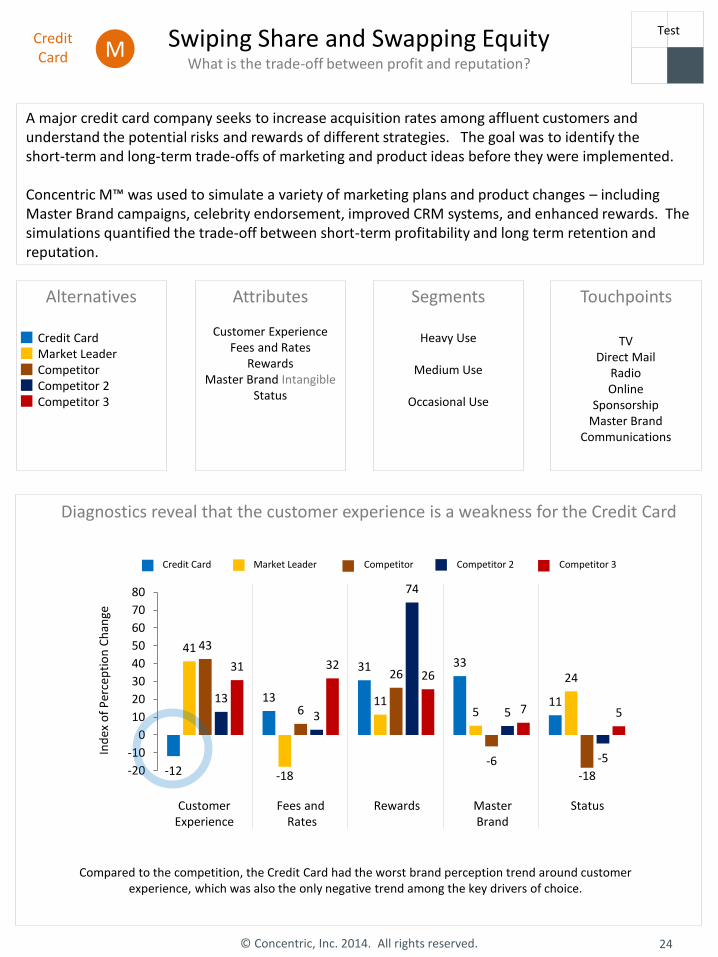

Swiping Share and Swapping Equity What is the trade-off between profit and reputation?

A major credit card company seeks to increase acquisition rates among affluent customers and understand the potential risks and rewards of different strategies. The goal was to identify the short-term and long-term trade-offs of marketing and product ideas before they were implemented. Concentric M™ was used to simulate a variety of marketing plans and product changes – including Master Brand campaigns, celebrity endorsement, improved CRM systems, and enhanced rewards. The simulations quantified the trade-off between short-term profitability and long term retention and reputation.

Alternatives

Credit Card Market Leader Competitor Competitor 2 Competitor 3

Attributes

Customer Experience Fees and Rates

Rewards Master Brand Intangible

Status

Segments

Heavy Use

Medium Use

Occasional Use

Touchpoints

Diagnostics reveal that the customer experience is a weakness for the Credit Card

Credit Card M

TV Direct Mail

Radio Online

Sponsorship Master Brand

Communications

24 © Concentric, Inc. 2014. All rights reserved.

Drive Efficiency

Test

Customer Experience

Fees and Rates

Rewards Master Brand

Status

Competitor 2 Credit Card Market Leader Competitor Competitor 3

Compared to the competition, the Credit Card had the worst brand perception trend around customer experience, which was also the only negative trend among the key drivers of choice.

Swiping Share and Swapping Equity What is the trade-off between profit and reputation?

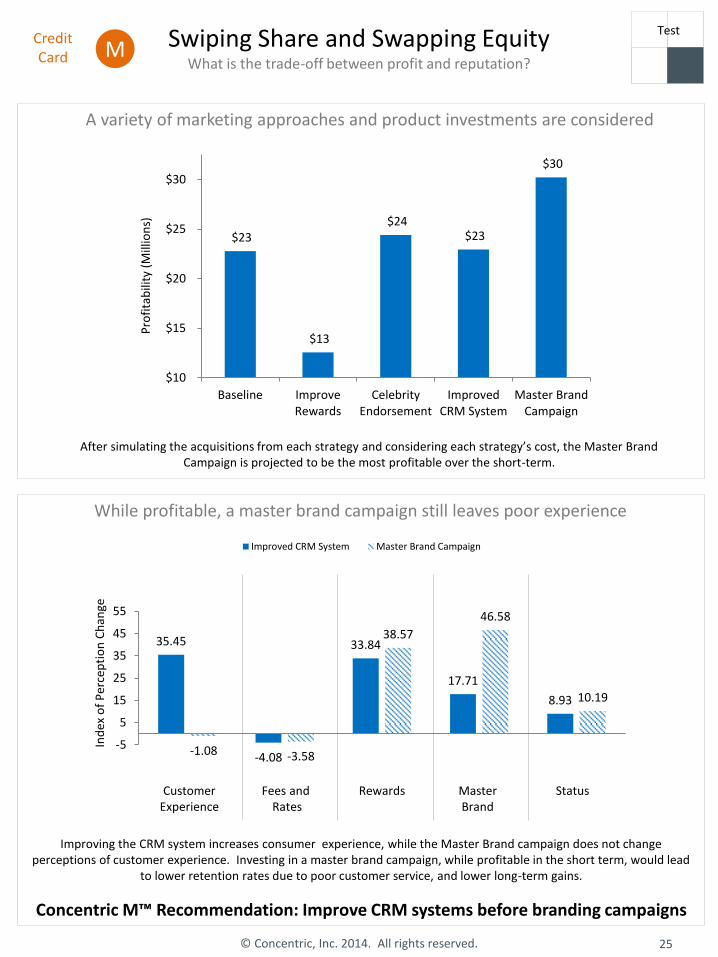

While profitable, a master brand campaign still leaves poor experience

Concentric M™ Recommendation: Improve CRM systems before branding campaigns

25 © Concentric, Inc. 2014. All rights reserved.

Credit Card M

Drive Efficiency

A variety of marketing approaches and product investments are considered

Test

$23

$13

$24 $23

$30

$10

$15

$20

$25

$30

Baseline ImproveRewards

CelebrityEndorsement

ImprovedCRM System

Master BrandCampaign

Pro

fita

bili

ty (

Mill

ion

s)

After simulating the acquisitions from each strategy and considering each strategy’s cost, the Master Brand Campaign is projected to be the most profitable over the short-term.

35.45

-4.08

33.84

17.71

8.93

-1.08 -3.58

38.57

46.58

10.19

-5

5

15

25

35

45

55

Ind

ex o

f P

erce

pti

on

Ch

ange

Improved CRM System Master Brand Campaign

Improving the CRM system increases consumer experience, while the Master Brand campaign does not change perceptions of customer experience. Investing in a master brand campaign, while profitable in the short term, would lead

to lower retention rates due to poor customer service, and lower long-term gains.

Customer Experience

Fees and Rates

Rewards Master Brand

Status

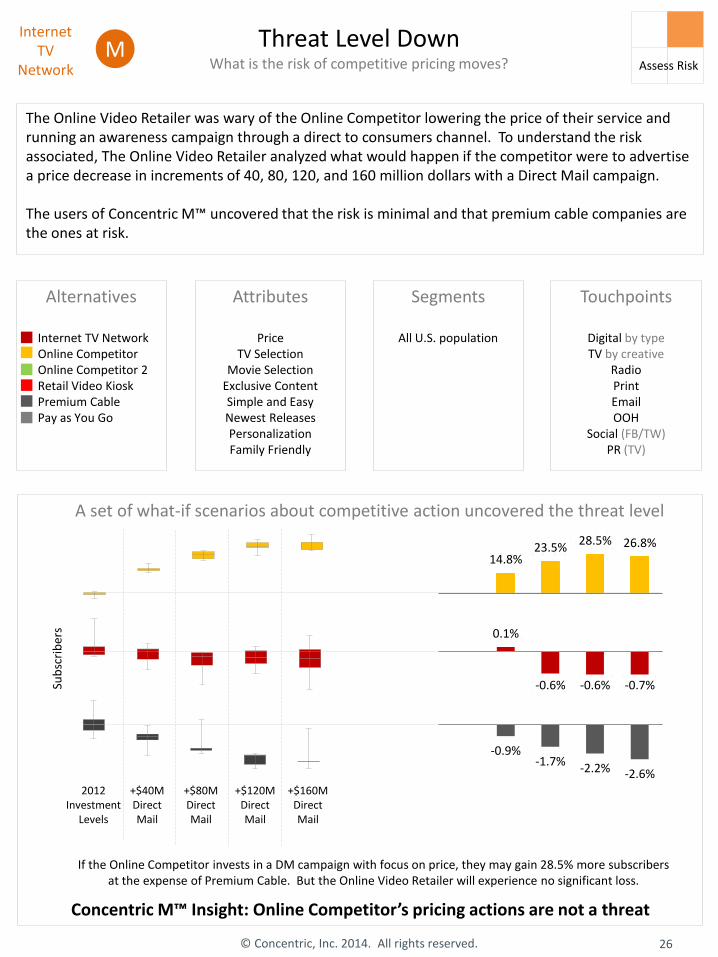

Threat Level Down What is the risk of competitive pricing moves?

The Online Video Retailer was wary of the Online Competitor lowering the price of their service and running an awareness campaign through a direct to consumers channel. To understand the risk associated, The Online Video Retailer analyzed what would happen if the competitor were to advertise a price decrease in increments of 40, 80, 120, and 160 million dollars with a Direct Mail campaign. The users of Concentric M™ uncovered that the risk is minimal and that premium cable companies are the ones at risk.

Alternatives

Internet TV Network Online Competitor Online Competitor 2 Retail Video Kiosk Premium Cable Pay as You Go

Attributes

Price TV Selection

Movie Selection Exclusive Content Simple and Easy Newest Releases Personalization Family Friendly

Segments

All U.S. population

Touchpoints

Digital by type TV by creative

Radio Print Email OOH

Social (FB/TW) PR (TV)

A set of what-if scenarios about competitive action uncovered the threat level

Sub

scri

ber

s 0.1%

-0.6% -0.6% -0.7%

-0.9% -1.7%

-2.2% -2.6%

14.8% 23.5%

28.5% 26.8%

2012 Investment

Levels

Concentric M™ Insight: Online Competitor’s pricing actions are not a threat

+$40M Direct Mail

+$80M Direct Mail

+$120M Direct Mail

+$160M Direct Mail

If the Online Competitor invests in a DM campaign with focus on price, they may gain 28.5% more subscribers at the expense of Premium Cable. But the Online Video Retailer will experience no significant loss.

M

26 © Concentric, Inc. 2014. All rights reserved.

Assess Risk

Internet TV

Network

Rules of Engagement How do we make our brand more engaging?

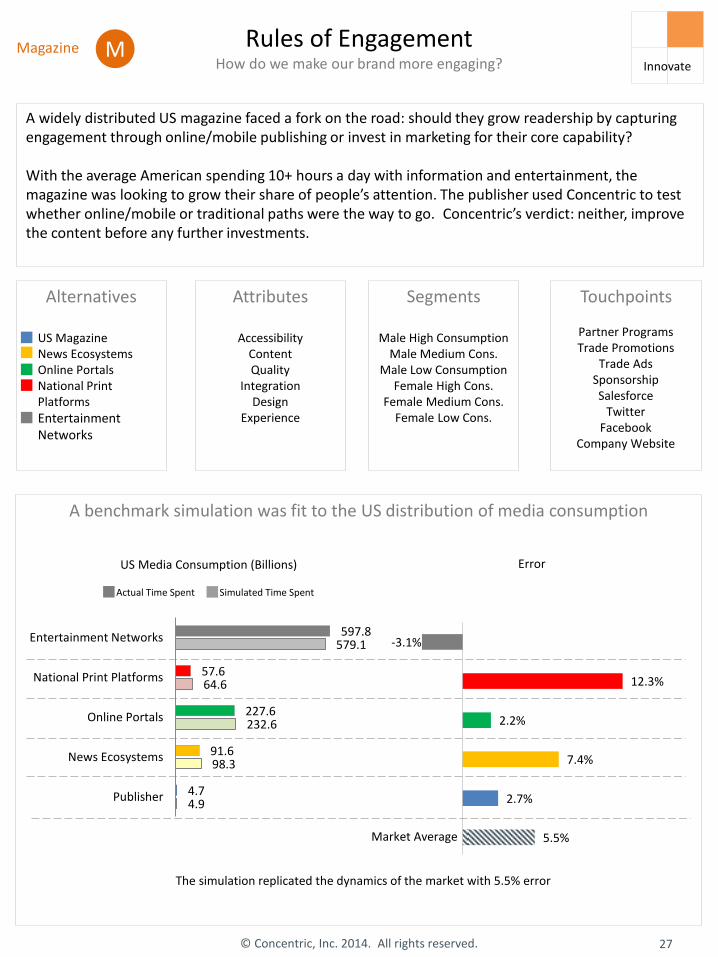

A widely distributed US magazine faced a fork on the road: should they grow readership by capturing engagement through online/mobile publishing or invest in marketing for their core capability? With the average American spending 10+ hours a day with information and entertainment, the magazine was looking to grow their share of people’s attention. The publisher used Concentric to test whether online/mobile or traditional paths were the way to go. Concentric’s verdict: neither, improve the content before any further investments.

Alternatives

US Magazine News Ecosystems Online Portals National Print Platforms

Entertainment Networks

Attributes

Accessibility Content Quality

Integration Design

Experience

Segments

Male High Consumption Male Medium Cons.

Male Low Consumption Female High Cons.

Female Medium Cons. Female Low Cons.

Touchpoints

A benchmark simulation was fit to the US distribution of media consumption

The simulation replicated the dynamics of the market with 5.5% error

Magazine M

Partner Programs Trade Promotions

Trade Ads Sponsorship Salesforce

Twitter Facebook

Company Website

Market Average

27 © Concentric, Inc. 2014. All rights reserved.

Innovate

4.9

98.3

232.6

64.6

579.1

4.7

91.6

227.6

57.6

597.8

Publisher

News Ecosystems

Online Portals

National Print Platforms

Entertainment Networks

US Media Consumption (Billions)

Actual Time Spent Simulated Time Spent

5.5%

2.7%

7.4%

2.2%

12.3%

-3.1%

Error

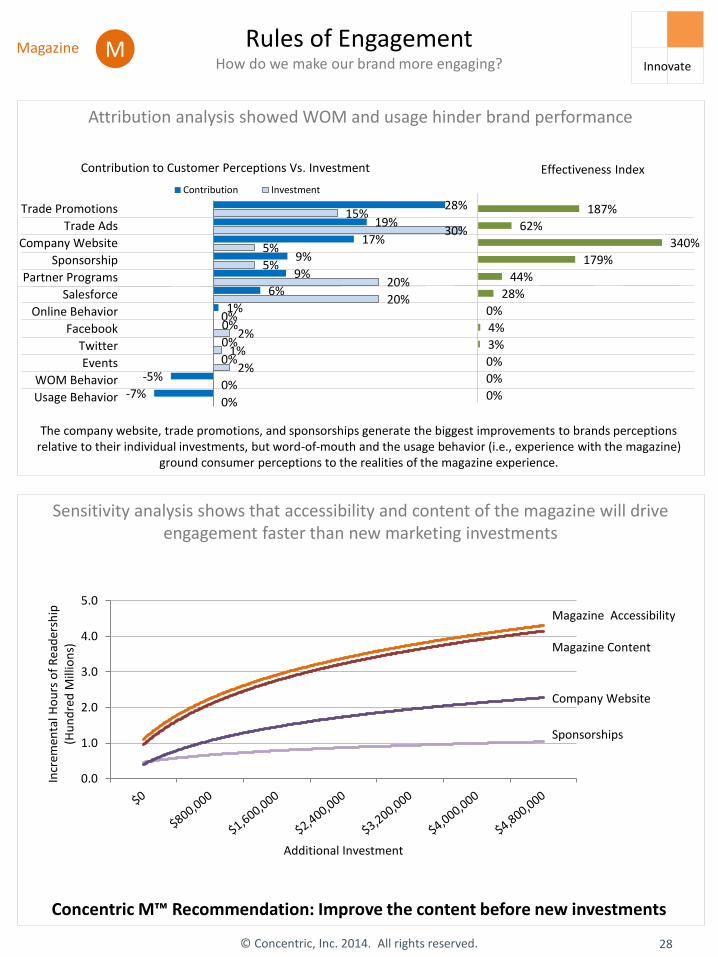

Attribution analysis showed WOM and usage hinder brand performance

0%

0%

2%

1%

2%

0%

20%

20%

5%

5%

30%

15%

-7%

-5%

0%

0%

0%

1%

6%

9%

9%

17%

19%

28%

Usage Behavior

WOM Behavior

Events

Online Behavior

Salesforce

Partner Programs

Sponsorship

Company Website

Trade Ads

Trade Promotions

Contribution to Customer Perceptions Vs. Investment

Contribution Investment

Sensitivity analysis shows that accessibility and content of the magazine will drive engagement faster than new marketing investments

Concentric M™ Recommendation: Improve the content before new investments

The company website, trade promotions, and sponsorships generate the biggest improvements to brands perceptions relative to their individual investments, but word-of-mouth and the usage behavior (i.e., experience with the magazine)

ground consumer perceptions to the realities of the magazine experience.

28 © Concentric, Inc. 2014. All rights reserved.

0.0

1.0

2.0

3.0

4.0

5.0

Incr

emen

tal H

ou

rs o

f R

ead

ersh

ip

(Hu

nd

red

Mill

ion

s)

Additional Investment

Magazine Accessibility

Magazine Content

Company Website

Sponsorships

0%

0%

0%

3%

4%

0%

28%

44%

179%

340%

62%

187%

Effectiveness Index

Rules of Engagement How do we make our brand more engaging?

M Magazine Innovate

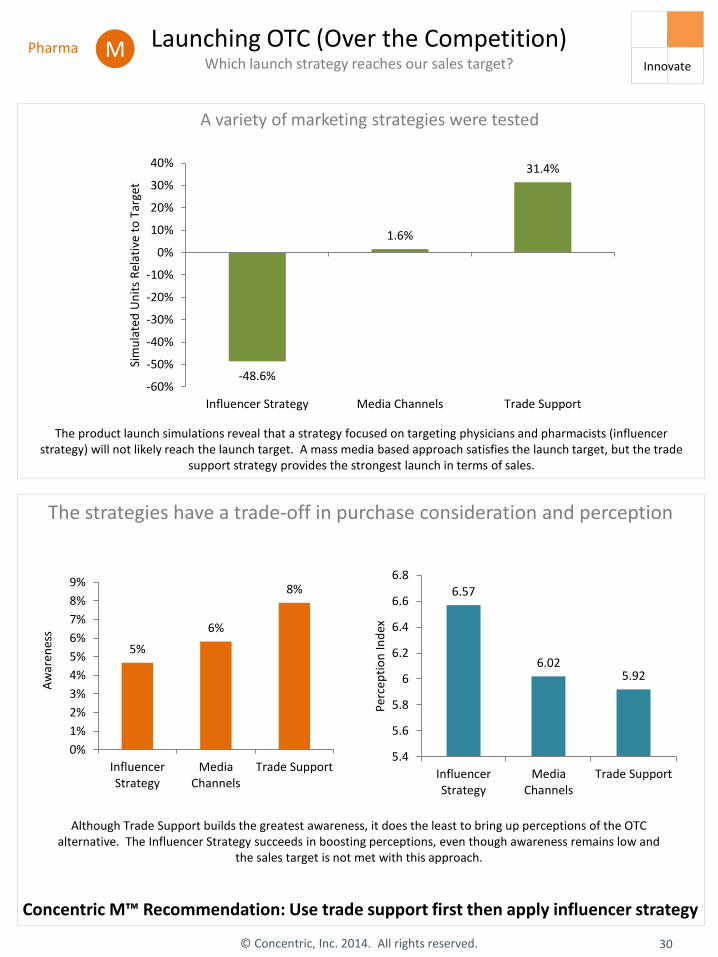

Launching OTC (Over the Competition) Which launch strategy reaches our sales target?

A company was planning to launch an OTC version of an existing prescription drug. The goal was a sales target in the face of heavy competition within the category – from prescription drugs, existing OTC brands, and private label options. Concentric M™ was used to simulate the dynamics of the product launch – including the impact of competitor trade promotions and recommendations from pharmacists and physicians. This recreation of the entire market provided the client with useful insights when planning the OTC launch.

Alternatives

OTC Launch Rx Version Other Rx OTC Leader OTC Private Label

Attributes

Relief Prevention

Price Speed

New Promise

Segments

Heavy Use Moderate Use *Pharmacists *Physicians

*Non-purchasing

influencer segments

Touchpoints

TV Print

Digital FSI

Trade Support PR

Medical Website

The simulation was calibrated to sales with a high degree of accuracy

Pharma M

29 © Concentric, Inc. 2014. All rights reserved.

Drive Efficiency

The Mean Absolute Percent Error (MAPE) for annual sales across the competitors is 2.5% in the calibrated baseline simulation

21.4

76.8

21.0

31.5

22.1

79.4

20.6

31.1

-

10

20

30

40

50

60

70

80

90

Rx Version Other Rx OTC Brand Leader Private Label

Sale

s (M

illio

ns)

Actual Simulated

Innovate

Launching OTC (Over the Competition) Which launch strategy reaches our sales target?

The strategies have a trade-off in purchase consideration and perception

Concentric M™ Recommendation: Use trade support first then apply influencer strategy

30 © Concentric, Inc. 2014. All rights reserved.

Pharma M Drive

Efficiency

A variety of marketing strategies were tested

The product launch simulations reveal that a strategy focused on targeting physicians and pharmacists (influencer strategy) will not likely reach the launch target. A mass media based approach satisfies the launch target, but the trade

support strategy provides the strongest launch in terms of sales.

Although Trade Support builds the greatest awareness, it does the least to bring up perceptions of the OTC alternative. The Influencer Strategy succeeds in boosting perceptions, even though awareness remains low and

the sales target is not met with this approach.

-48.6%

1.6%

31.4%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Influencer Strategy Media Channels Trade Support

Sim

ula

ted

Un

its

Rel

ativ

e to

Tar

get

5%

6%

8%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

InfluencerStrategy

MediaChannels

Trade Support

Aw

aren

ess

6.57

6.02 5.92

5.4

5.6

5.8

6

6.2

6.4

6.6

6.8

InfluencerStrategy

MediaChannels

Trade Support

Per

cep

tio

n In

dex

Innovate

© Concentric, Inc. 2014. All rights reserved.

Simulate Your Market

Visit or call any time!

222 3rd Street, Suite 0142

Cambridge, MA 02142 USA

617-674-5678

www.concentricabm.com