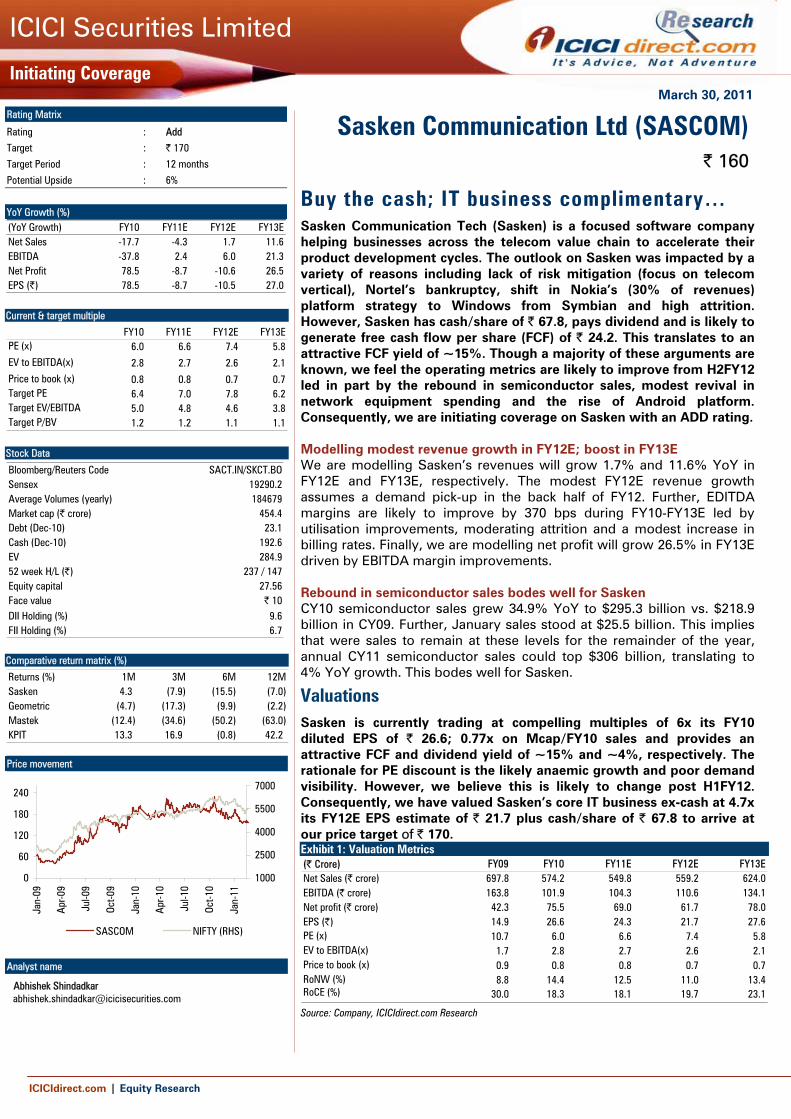

march 30, 2011 sasken communication ltd...

TRANSCRIPT

March 30, 2011

ICICIdirect.com | Equity Research

Initiating Coverage

ICICI Securities Limited

Buy the cash; IT business complimentary… Sasken Communication Tech (Sasken) is a focused software company helping businesses across the telecom value chain to accelerate their product development cycles. The outlook on Sasken was impacted by a variety of reasons including lack of risk mitigation (focus on telecom vertical), Nortel’s bankruptcy, shift in Nokia’s (30% of revenues) platform strategy to Windows from Symbian and high attrition. However, Sasken has cash/share of | 67.8, pays dividend and is likely to generate free cash flow per share (FCF) of | 24.2. This translates to an attractive FCF yield of ~15%. Though a majority of these arguments are known, we feel the operating metrics are likely to improve from H2FY12 led in part by the rebound in semiconductor sales, modest revival in network equipment spending and the rise of Android platform. Consequently, we are initiating coverage on Sasken with an ADD rating. Modelling modest revenue growth in FY12E; boost in FY13E We are modelling Sasken’s revenues will grow 1.7% and 11.6% YoY in FY12E and FY13E, respectively. The modest FY12E revenue growth assumes a demand pick-up in the back half of FY12. Further, EDITDA margins are likely to improve by 370 bps during FY10-FY13E led by utilisation improvements, moderating attrition and a modest increase in billing rates. Finally, we are modelling net profit will grow 26.5% in FY13E driven by EBITDA margin improvements. Rebound in semiconductor sales bodes well for Sasken CY10 semiconductor sales grew 34.9% YoY to $295.3 billion vs. $218.9 billion in CY09. Further, January sales stood at $25.5 billion. This implies that were sales to remain at these levels for the remainder of the year, annual CY11 semiconductor sales could top $306 billion, translating to 4% YoY growth. This bodes well for Sasken.

Valuations Sasken is currently trading at compelling multiples of 6x its FY10 diluted EPS of | 26.6; 0.77x on Mcap/FY10 sales and provides an attractive FCF and dividend yield of ~15% and ~4%, respectively. The rationale for PE discount is the likely anaemic growth and poor demand visibility. However, we believe this is likely to change post H1FY12. Consequently, we have valued Sasken’s core IT business ex-cash at 4.7x its FY12E EPS estimate of | 21.7 plus cash/share of | 67.8 to arrive at our price target of | 170. Exhibit 1: Valuation Metrics (| Crore) FY09 FY10 FY11E FY12E FY13ENet Sales (| crore) 697.8 574.2 549.8 559.2 624.0EBITDA (| crore) 163.8 101.9 104.3 110.6 134.1Net profit (| crore) 42.3 75.5 69.0 61.7 78.0EPS (|) 14.9 26.6 24.3 21.7 27.6PE (x) 10.7 6.0 6.6 7.4 5.8EV to EBITDA(x) 1.7 2.8 2.7 2.6 2.1Price to book (x) 0.9 0.8 0.8 0.7 0.7RoNW (%) 8.8 14.4 12.5 11.0 13.4RoCE (%) 30.0 18.3 18.1 19.7 23.1

Source: Company, ICICIdirect.com Research

Sasken Communication Ltd (SASCOM) | 160

Rating Matrix

Rating : Add

Target : | 170

Target Period : 12 months

Potential Upside : 6%

YoY Growth (%) (YoY Growth) FY10 FY11E FY12E FY13ENet Sales -17.7 -4.3 1.7 11.6EBITDA -37.8 2.4 6.0 21.3Net Profit 78.5 -8.7 -10.6 26.5EPS (|) 78.5 -8.7 -10.5 27.0

Current & target multiple

FY10 FY11E FY12E FY13EPE (x) 6.0 6.6 7.4 5.8EV to EBITDA(x) 2.8 2.7 2.6 2.1Price to book (x) 0.8 0.8 0.7 0.7Target PE 6.4 7.0 7.8 6.2Target EV/EBITDA 5.0 4.8 4.6 3.8Target P/BV 1.2 1.2 1.1 1.1

Stock Data

Bloomberg/Reuters Code SACT.IN/SKCT.BOSensex 19290.2Average Volumes (yearly) 184679Market cap (| crore) 454.4Debt (Dec-10) 23.1Cash (Dec-10) 192.6EV 284.952 week H/L (|) 237 / 147Equity capital 27.56Face value | 10DII Holding (%) 9.6FII Holding (%) 6.7

Comparative return matrix (%)

Returns (%) 1M 3M 6M 12MSasken 4.3 (7.9) (15.5) (7.0) Geometric (4.7) (17.3) (9.9) (2.2) Mastek (12.4) (34.6) (50.2) (63.0) KPIT 13.3 16.9 (0.8) 42.2

Price movement

0

60

120

180

240

Jan-

09

Apr-0

9

Jul-0

9

Oct-0

9

Jan-

10

Apr-1

0

Jul-1

0

Oct-1

0

Jan-

11

1000

2500

4000

5500

7000

SASCOM NIFTY (RHS)

Analyst name

Abhishek Shindadkar [email protected]

ICICIdirect.com | Equity Research Page 2

ICICI Securities Limited

Company background Established in 1989 at San Jose by Rajiv Mody and two other co-founders, Sasken is a focused communications software company helping businesses across the telecom value chain to accelerate their product development cycles. With its deep domain skills, the company provides both research and development (R&D) services and software product solutions using a hybrid model. Sasken provides R&D services in the telecom infrastructure and semiconductor segments while product solutions are for handset manufacturers and include basic communication software along with multimedia codecs and applications software.

Business Description

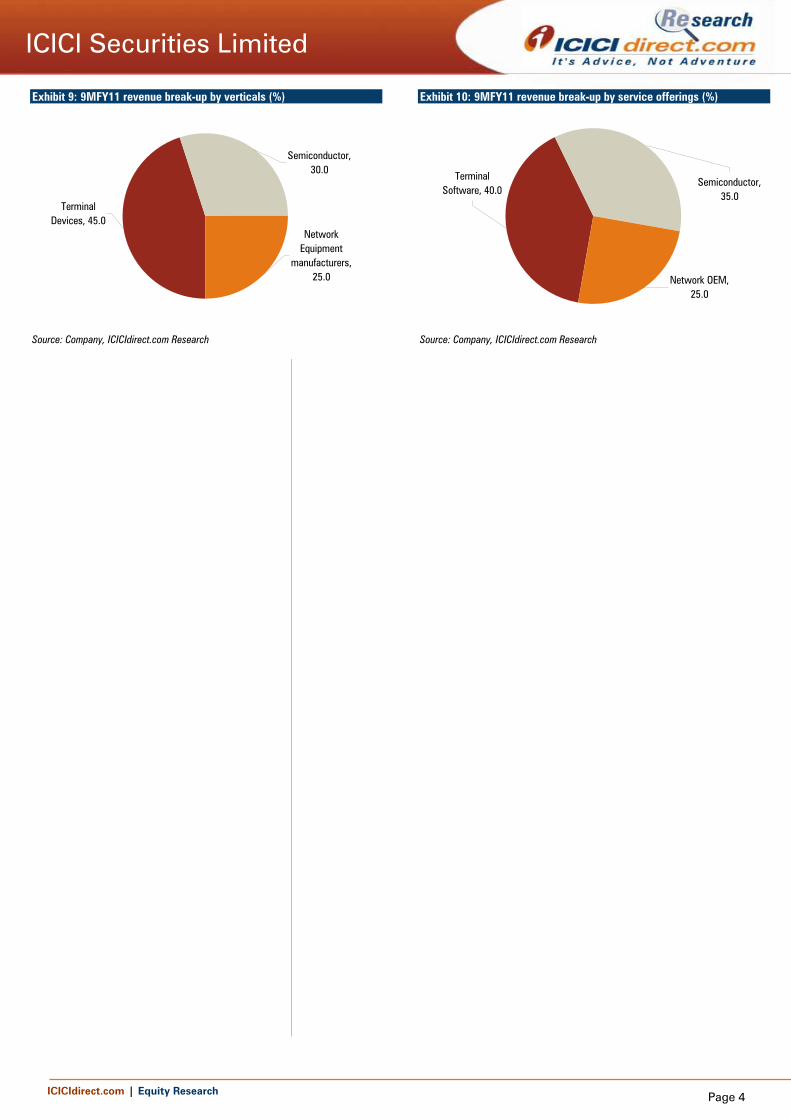

Sasken generates services revenues (88% of 9MFY11 revenues) in three industry segments: 1) network original equipment manufacturers (OEM, ~25% of 9MFY11 revenues), 2) semiconductor vendors (30%) and 3) terminal devices (handset vendors, ~45%).

Network OEMs – Sasken primarily offers R&D services (30% of network revenues) to equipment manufacturers such as Kapsch. Services include 1) radio access network services for 2G and Universal Mobile Telecommunications System (UMTS) technologies, 2) network management - includes element management solution and 3) network engineering services. Typically, R&D spend constitutes 10-15% of OEMs annual revenues of which 10% is outsourced and 25-30% of outsourced is offshored.

Semiconductor vendors – Sasken offers chip design services, OS related software services, multimedia codecs and protocol stacks pre-integrated on semiconductor platforms. The company works with six of the top 10 vendors including, Texas Instruments (TI), Qualcomm, Intel, Infineon, NEC and NXP. R&D budgets typically constitute 10-15% of annual revenues and are likely to remain at elevated levels given the proliferation of open source platforms. Exhibit 2: Semiconductor offerings

Semiconductor Offerings Services % RevenueHardware Design IC design 40.0Software Design chipsets, OS related, multimedia codecs 60.0

Source: Company, ICICIdirect.com Research

Terminal devices - Sasken offers development and testing services for handset manufacturers such as Samsung, LG, Kyocera and Dell as well as integration and porting for the Android and Symbian platform. The terminal devices portfolio was enhanced and complemented by the Botnia acquisition, which brought in radio frequency, hardware and mechanical design services and gave access to Nokia. Exhibit 3: Terminal device offerings

Terminal Devices offerings Services % RevenueHardware Design Mechanical desgin 20.0Software Design Product design, testing, validation and support 80.0

Source: Company, ICICIdirect.com Research

Software products

The products business, 11% of Q3FY11 revenues, offers wireless embedded software with pre-integrated solutions and design flexibility. Sasken’s solution is portable across silicon platforms and operating systems increasing their reusability over phone models through customisation. The company’s key offerings include (1) wireless protocol

Share holding pattern (February 18, 2011)

Shareholder Holding (%)Promoters 28.3Institutional Investors 16.3Other Investors 11.8General Public 43.6

FII & DII holding trend (%)

28.0

27.8

27.6

27.6

28.3

16.9

18.6

20.7

19.1

16.3

0

6

12

18

24

30

FY4Q10 FY1Q11 FY2Q11 FY3Q11 18-Feb-11

(%)

Promoters FII & DII

ICICIdirect.com | Equity Research Page 3

ICICI Securities Limited

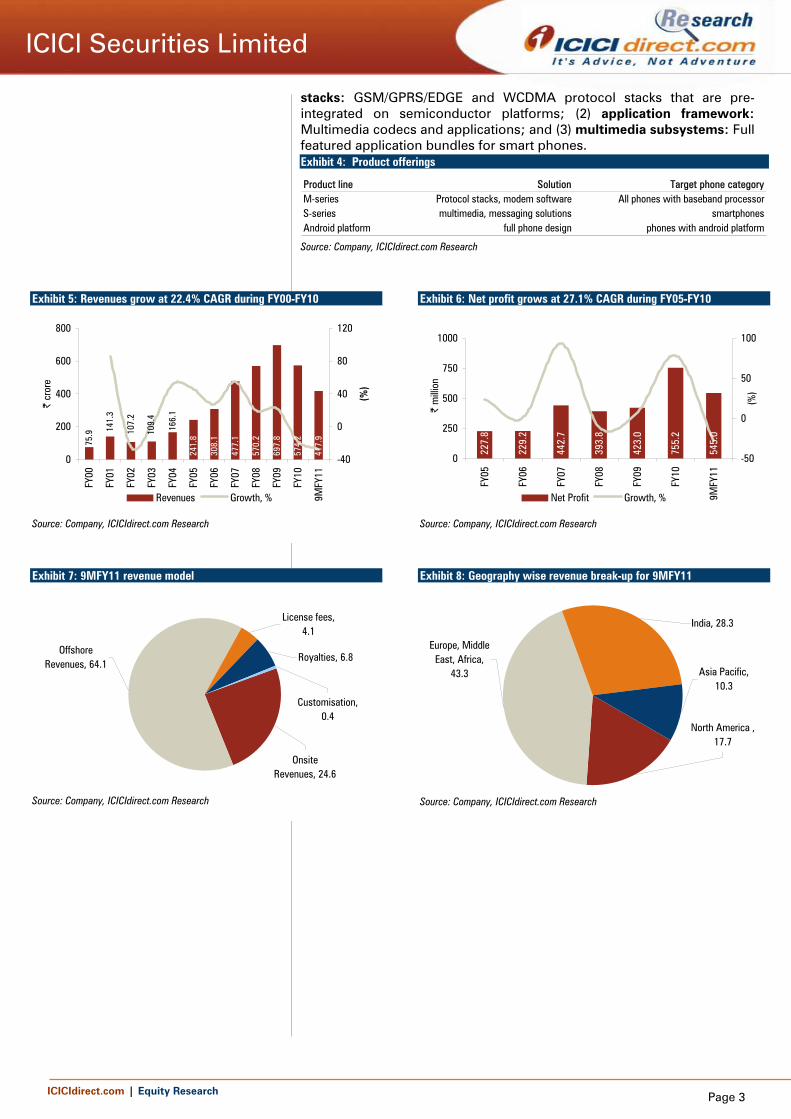

stacks: GSM/GPRS/EDGE and WCDMA protocol stacks that are pre-integrated on semiconductor platforms; (2) application framework: Multimedia codecs and applications; and (3) multimedia subsystems: Full featured application bundles for smart phones. Exhibit 4: Product offerings

Product line Solution Target phone categoryM-series Protocol stacks, modem software All phones with baseband processorS-series multimedia, messaging solutions smartphonesAndroid platform full phone design phones with android platform

Source: Company, ICICIdirect.com Research

Exhibit 5: Revenues grow at 22.4% CAGR during FY00-FY10

308.

1

477.

1

570.

2

697.

8

574.

2

241.

8

166.

1

109.

4

107.

2

141.

3

75.9

417.

9

0

200

400

600

800

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

9MFY

11

| cr

ore

-40

0

40

80

120

(%)

Revenues Growth, %

Source: Company, ICICIdirect.com Research

Exhibit 6: Net profit grows at 27.1% CAGR during FY05-FY10

227.

8

229.

2

442.

7

393.

8

423.

0

755.

2

545.

0

0

250

500

750

1000

FY05

FY06

FY07

FY08

FY09

FY10

9MFY

11

| m

illion

-50

0

50

100

(%)

Net Profit Growth, %

Source: Company, ICICIdirect.com Research

Exhibit 7: 9MFY11 revenue model

Customisation, 0.4

Royalties, 6.8

License fees, 4.1

Offshore Revenues, 64.1

Onsite Revenues, 24.6

Source: Company, ICICIdirect.com Research

Exhibit 8: Geography wise revenue break-up for 9MFY11

North America , 17.7

Europe, Middle East, Africa,

43.3

India, 28.3

Asia Pacific, 10.3

Source: Company, ICICIdirect.com Research

ICICIdirect.com | Equity Research Page 4

ICICI Securities Limited

Exhibit 9: 9MFY11 revenue break-up by verticals (%)

Terminal Devices, 45.0

Semiconductor, 30.0

Network Equipment

manufacturers, 25.0

Source: Company, ICICIdirect.com Research

Exhibit 10: 9MFY11 revenue break-up by service offerings (%)

Network OEM, 25.0

Semiconductor, 35.0

Terminal Software, 40.0

Source: Company, ICICIdirect.com Research

ICICIdirect.com | Equity Research Page 5

5 Error! Reference source not found.

ICICI Securities Limited

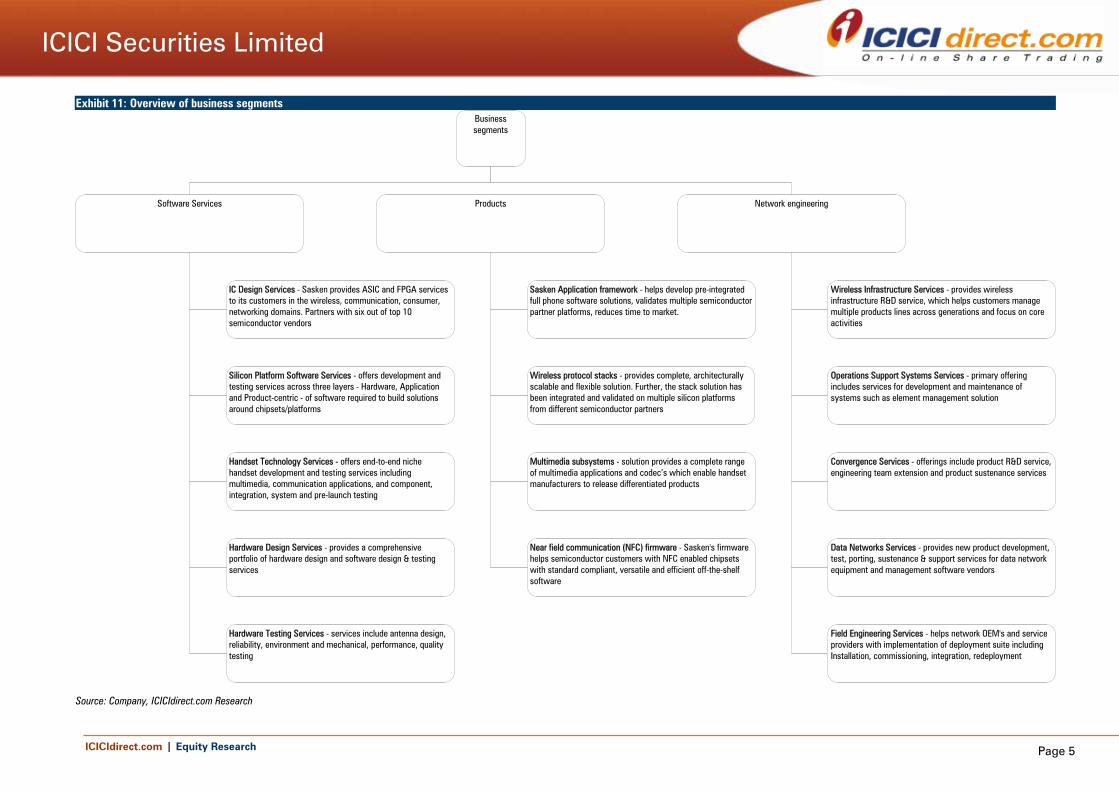

Exhibit 11: Overview of business segments

Source: Company, ICICIdirect.com Research

Business segments

Software Services Products Network engineering

IC Design Services - Sasken provides ASIC and FPGA services to its customers in the wireless, communication, consumer, networking domains. Partners with six out of top 10 semiconductor vendors

Silicon Platform Software Services - offers development and testing services across three layers - Hardware, Application and Product-centric - of software required to build solutions around chipsets/platforms

Handset Technology Services - offers end-to-end niche handset development and testing services including multimedia, communication applications, and component, integration, system and pre-launch testing

Hardware Design Services - provides a comprehensive portfolio of hardware design and software design & testing services

Hardware Testing Services - services include antenna design, reliability, environment and mechanical, performance, quality testing

Sasken Application framework - helps develop pre-integrated full phone software solutions, validates multiple semiconductorpartner platforms, reduces time to market.

Wireless protocol stacks - provides complete, architecturally scalable and flexible solution. Further, the stack solution has been integrated and validated on multiple silicon platforms from different semiconductor partners

Multimedia subsystems - solution provides a complete range of multimedia applications and codec’s which enable handset manufacturers to release differentiated products

Near field communication (NFC) firmware - Sasken's firmware helps semiconductor customers with NFC enabled chipsets with standard compliant, versatile and efficient off-the-shelf software

Wireless Infrastructure Services - provides wireless infrastructure R&D service, which helps customers manage multiple products lines across generations and focus on core activities

Operations Support Systems Services - primary offering includes services for development and maintenance of systems such as element management solution

Convergence Services - offerings include product R&D service, engineering team extension and product sustenance services

Data Networks Services - provides new product development, test, porting, sustenance & support services for data network equipment and management software vendors

Field Engineering Services - helps network OEM's and service providers with implementation of deployment suite including Installation, commissioning, integration, redeployment

ICICIdirect.com | Equity Research Page 6

ICICI Securities Limited

Management profile

Governing council

Rajiv Mody, an industry veteran who co-founded Sasken, continues to be the Chairman and CEO. Rajiv has worked with corporations like AMD, Seattle Tech Inc and VLSI Technology Inc and was awarded Technovator of the year in 2007. He has also served as an executive council member of Nasscom during 2001-2008.

G Venkatesh, CTO head of world wide delivery has been with the company since 1995. He graduated in Electronics from IIT-Madras and was a professor of Computer Science at IIT-Mumbai before joining Sasken. At Sasken, he has served different roles including head of the product division.

Neeta Revankar has been with the company since 1995 and heads the finance, HR and business operations. She is a qualified chartered accountant (CA) and company secretary (CS) and serves as a whole time director on the Sasken board. In 2005, IMA India conferred her with the India CFO award.

Board of directors

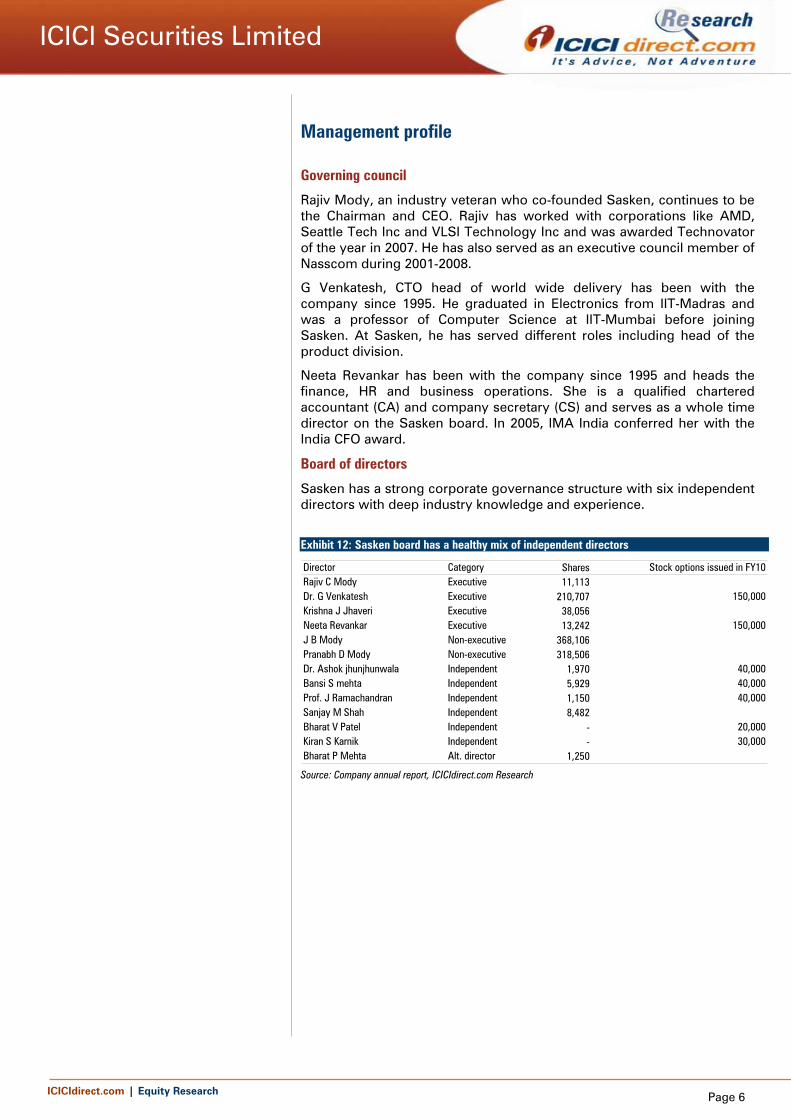

Sasken has a strong corporate governance structure with six independent directors with deep industry knowledge and experience.

Exhibit 12: Sasken board has a healthy mix of independent directors

Director Category Shares Stock options issued in FY10Rajiv C Mody Executive 11,113Dr. G Venkatesh Executive 210,707 150,000Krishna J Jhaveri Executive 38,056Neeta Revankar Executive 13,242 150,000J B Mody Non-executive 368,106Pranabh D Mody Non-executive 318,506Dr. Ashok jhunjhunwala Independent 1,970 40,000Bansi S mehta Independent 5,929 40,000Prof. J Ramachandran Independent 1,150 40,000Sanjay M Shah Independent 8,482Bharat V Patel Independent - 20,000Kiran S Karnik Independent - 30,000Bharat P Mehta Alt. director 1,250

Source: Company annual report, ICICIdirect.com Research

ICICIdirect.com | Equity Research Page 7

ICICI Securities Limited

Investment rationale

We expect a demand pick-up from the semiconductor industry and the rise of the Android platform to be the core contributors for revenue growth. From an operating metric perspective, we expect utilisation to bottom out in H1FY12 while attrition could moderate modestly. Consequently, we are modelling conservative revenue growth of 1.7% and 11.6% YoY in FY12E and FY13E respectively, while EDITDA margins are likely to improve by 370 bps during FY10-FY13E. Finally, our investment thesis acknowledges the attractive valuations at which the stock is available, i.e. at 4.7x its FY12E EPS estimate of | 21.7, coupled with a 4% dividend yield and | 67.8 cash/share.

Semiconductor sales continue to rebound

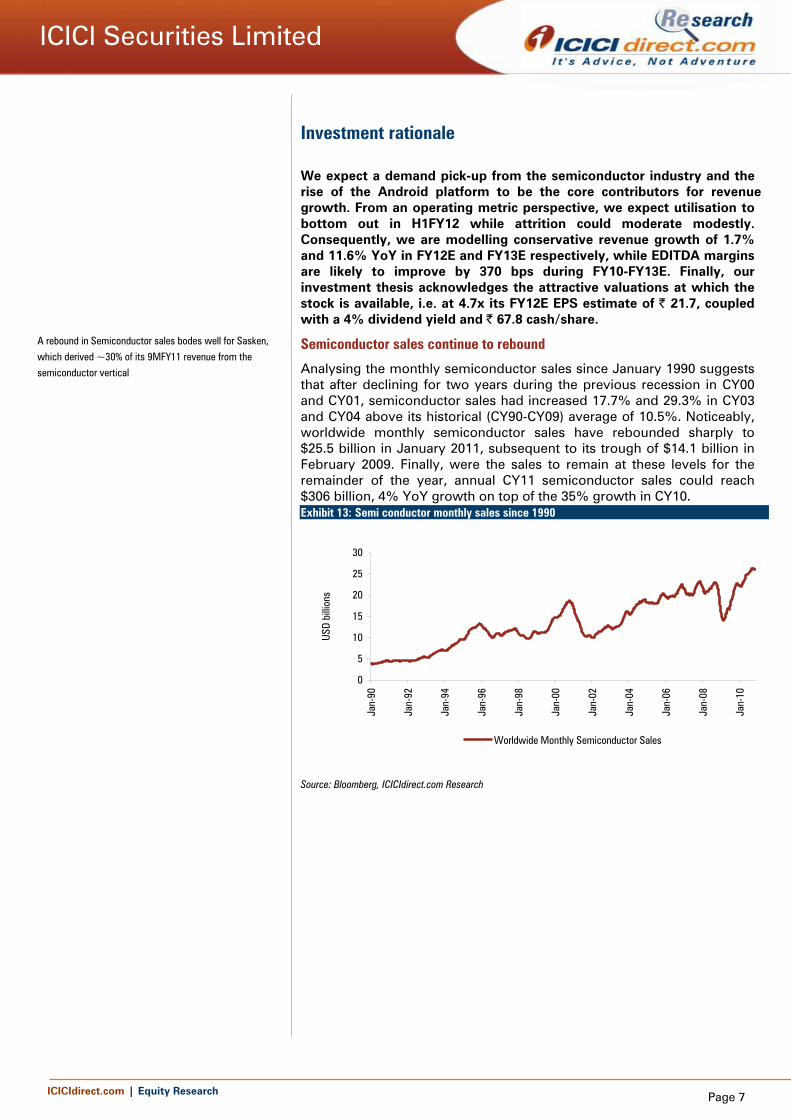

Analysing the monthly semiconductor sales since January 1990 suggests that after declining for two years during the previous recession in CY00 and CY01, semiconductor sales had increased 17.7% and 29.3% in CY03 and CY04 above its historical (CY90-CY09) average of 10.5%. Noticeably, worldwide monthly semiconductor sales have rebounded sharply to $25.5 billion in January 2011, subsequent to its trough of $14.1 billion in February 2009. Finally, were the sales to remain at these levels for the remainder of the year, annual CY11 semiconductor sales could reach $306 billion, 4% YoY growth on top of the 35% growth in CY10. Exhibit 13: Semi conductor monthly sales since 1990

0

5

10

15

20

25

30

Jan-

90

Jan-

92

Jan-

94

Jan-

96

Jan-

98

Jan-

00

Jan-

02

Jan-

04

Jan-

06

Jan-

08

Jan-

10

USD

billi

ons

Worldwide Monthly Semiconductor Sales

Source: Bloomberg, ICICIdirect.com Research

A rebound in Semiconductor sales bodes well for Sasken,

which derived ~30% of its 9MFY11 revenue from the

semiconductor vertical

ICICIdirect.com | Equity Research Page 8

ICICI Securities Limited

Exhibit 14: Semiconductor sales trends

0

70

140

210

280

350

CY19

90

CY19

91

CY19

92

CY19

93

CY19

94

CY19

95

CY19

96

CY19

97

CY19

98

CY19

99

CY20

00

CY20

01

CY20

02

CY20

03

CY20

04

CY20

05

CY20

06

CY20

07

CY20

08

CY20

09

CY20

10E

CY20

11E

$ bi

llions

-45

-30

-15

0

15

30

45

60

%

Worldwide semiconductor sales Growth %, YoY

Source: Bloomberg, ICICIdirect.com Research

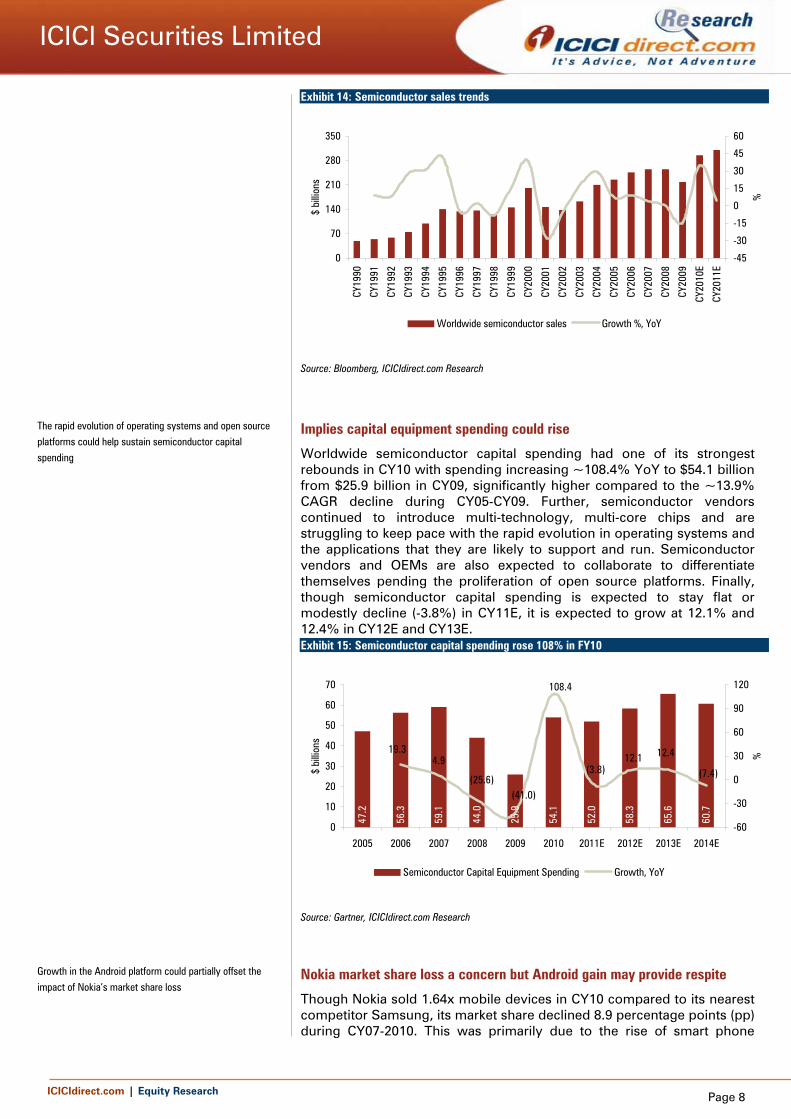

Implies capital equipment spending could rise

Worldwide semiconductor capital spending had one of its strongest rebounds in CY10 with spending increasing ~108.4% YoY to $54.1 billion from $25.9 billion in CY09, significantly higher compared to the ~13.9% CAGR decline during CY05-CY09. Further, semiconductor vendors continued to introduce multi-technology, multi-core chips and are struggling to keep pace with the rapid evolution in operating systems and the applications that they are likely to support and run. Semiconductor vendors and OEMs are also expected to collaborate to differentiate themselves pending the proliferation of open source platforms. Finally, though semiconductor capital spending is expected to stay flat or modestly decline (-3.8%) in CY11E, it is expected to grow at 12.1% and 12.4% in CY12E and CY13E. Exhibit 15: Semiconductor capital spending rose 108% in FY10

47.2

56.3

59.1

44.0

25.9

54.1

52.0

58.3

65.6

60.7

19.34.9

(25.6)(41.0)

(3.8)

108.4

12.1 12.4

(7.4)

0

10

20

30

40

50

60

70

2005 2006 2007 2008 2009 2010 2011E 2012E 2013E 2014E

$ bi

llions

-60

-30

0

30

60

90

120

%

Semiconductor Capital Equipment Spending Growth, YoY

Source: Gartner, ICICIdirect.com Research

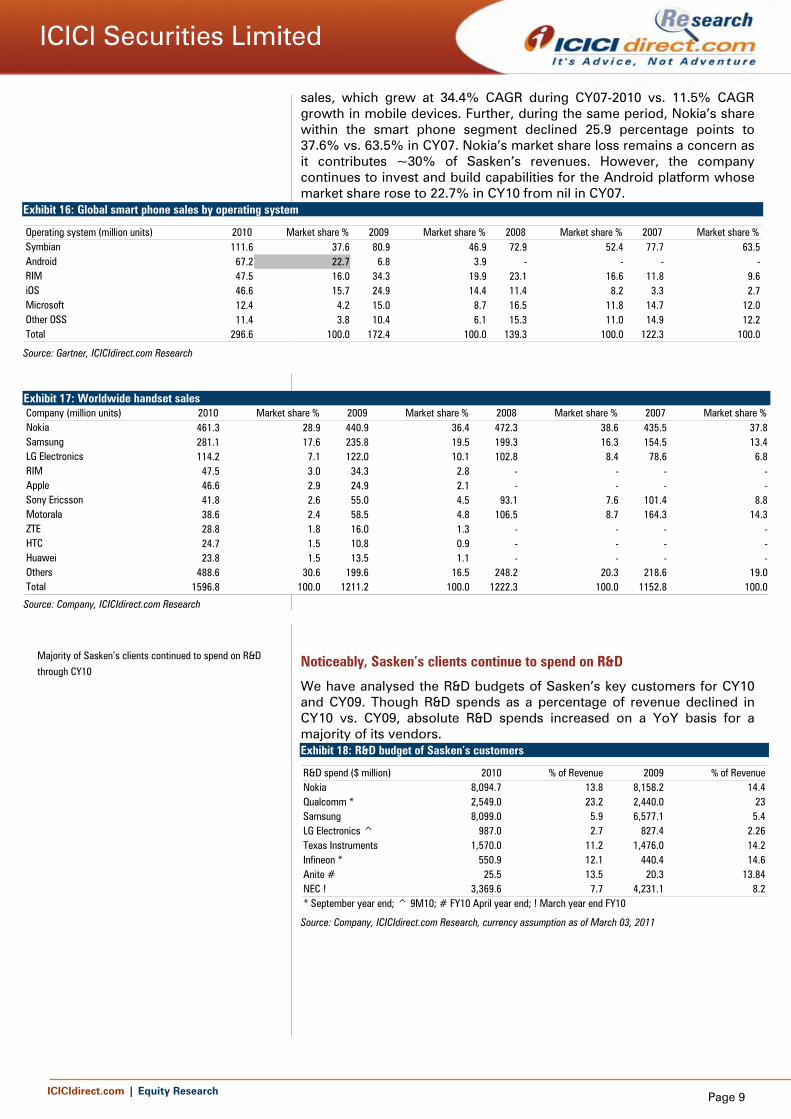

Nokia market share loss a concern but Android gain may provide respite

Though Nokia sold 1.64x mobile devices in CY10 compared to its nearest competitor Samsung, its market share declined 8.9 percentage points (pp) during CY07-2010. This was primarily due to the rise of smart phone

The rapid evolution of operating systems and open source

platforms could help sustain semiconductor capital

spending

Growth in the Android platform could partially offset the

impact of Nokia’s market share loss

ICICIdirect.com | Equity Research Page 9

ICICI Securities Limited

sales, which grew at 34.4% CAGR during CY07-2010 vs. 11.5% CAGR growth in mobile devices. Further, during the same period, Nokia’s share within the smart phone segment declined 25.9 percentage points to 37.6% vs. 63.5% in CY07. Nokia’s market share loss remains a concern as it contributes ~30% of Sasken’s revenues. However, the company continues to invest and build capabilities for the Android platform whose market share rose to 22.7% in CY10 from nil in CY07.

Exhibit 16: Global smart phone sales by operating system

Operating system (million units) 2010 Market share % 2009 Market share % 2008 Market share % 2007 Market share %Symbian 111.6 37.6 80.9 46.9 72.9 52.4 77.7 63.5Android 67.2 22.7 6.8 3.9 - - - -RIM 47.5 16.0 34.3 19.9 23.1 16.6 11.8 9.6iOS 46.6 15.7 24.9 14.4 11.4 8.2 3.3 2.7Microsoft 12.4 4.2 15.0 8.7 16.5 11.8 14.7 12.0Other OSS 11.4 3.8 10.4 6.1 15.3 11.0 14.9 12.2Total 296.6 100.0 172.4 100.0 139.3 100.0 122.3 100.0

Source: Gartner, ICICIdirect.com Research

Exhibit 17: Worldwide handset sales Company (million units) 2010 Market share % 2009 Market share % 2008 Market share % 2007 Market share %Nokia 461.3 28.9 440.9 36.4 472.3 38.6 435.5 37.8Samsung 281.1 17.6 235.8 19.5 199.3 16.3 154.5 13.4LG Electronics 114.2 7.1 122.0 10.1 102.8 8.4 78.6 6.8RIM 47.5 3.0 34.3 2.8 - - - -Apple 46.6 2.9 24.9 2.1 - - - -Sony Ericsson 41.8 2.6 55.0 4.5 93.1 7.6 101.4 8.8Motorala 38.6 2.4 58.5 4.8 106.5 8.7 164.3 14.3ZTE 28.8 1.8 16.0 1.3 - - - -HTC 24.7 1.5 10.8 0.9 - - - -Huawei 23.8 1.5 13.5 1.1 - - - -Others 488.6 30.6 199.6 16.5 248.2 20.3 218.6 19.0Total 1596.8 100.0 1211.2 100.0 1222.3 100.0 1152.8 100.0

Source: Company, ICICIdirect.com Research

Noticeably, Sasken’s clients continue to spend on R&D

We have analysed the R&D budgets of Sasken’s key customers for CY10 and CY09. Though R&D spends as a percentage of revenue declined in CY10 vs. CY09, absolute R&D spends increased on a YoY basis for a majority of its vendors. Exhibit 18: R&D budget of Sasken’s customers

R&D spend ($ million) 2010 % of Revenue 2009 % of RevenueNokia 8,094.7 13.8 8,158.2 14.4Qualcomm * 2,549.0 23.2 2,440.0 23Samsung 8,099.0 5.9 6,577.1 5.4LG Electronics ^ 987.0 2.7 827.4 2.26Texas Instruments 1,570.0 11.2 1,476.0 14.2Infineon * 550.9 12.1 440.4 14.6Anite # 25.5 13.5 20.3 13.84NEC ! 3,369.6 7.7 4,231.1 8.2* September year end; ^ 9M10; # FY10 April year end; ! March year end FY10

Source: Company, ICICIdirect.com Research, currency assumption as of March 03, 2011

Majority of Sasken’s clients continued to spend on R&D

through CY10

ICICIdirect.com | Equity Research Page 10

ICICI Securities Limited

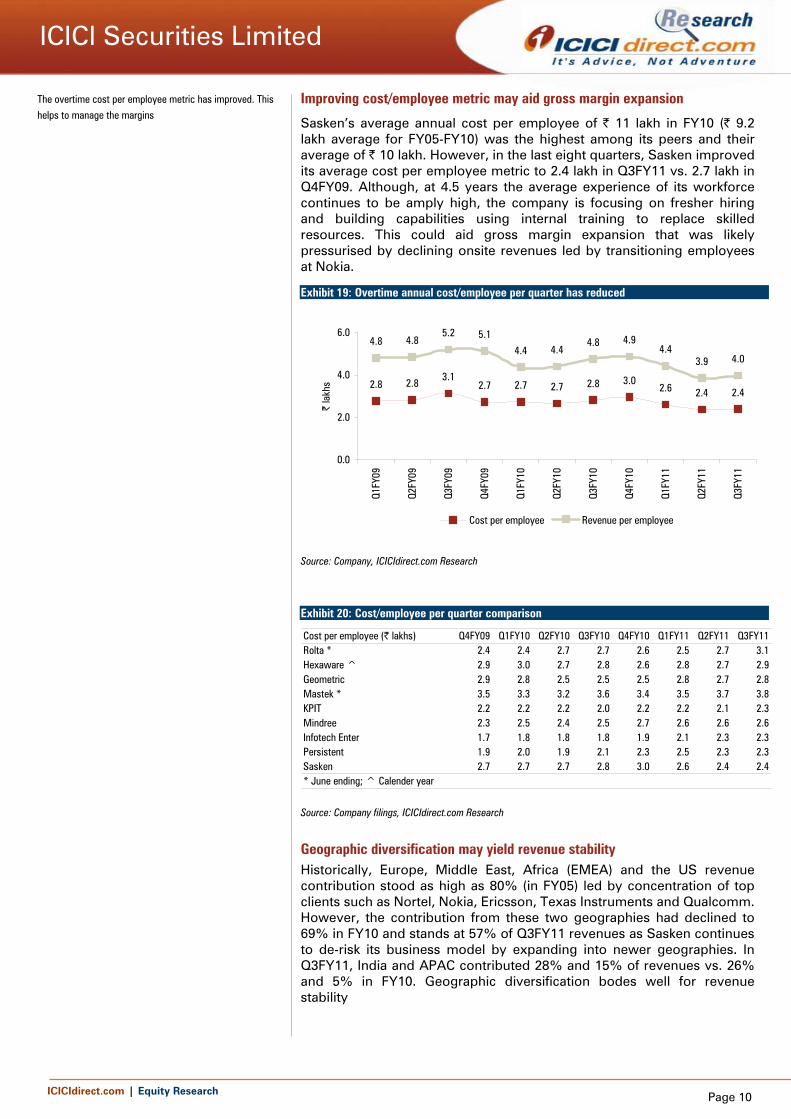

Improving cost/employee metric may aid gross margin expansion

Sasken’s average annual cost per employee of | 11 lakh in FY10 (| 9.2 lakh average for FY05-FY10) was the highest among its peers and their average of | 10 lakh. However, in the last eight quarters, Sasken improved its average cost per employee metric to 2.4 lakh in Q3FY11 vs. 2.7 lakh in Q4FY09. Although, at 4.5 years the average experience of its workforce continues to be amply high, the company is focusing on fresher hiring and building capabilities using internal training to replace skilled resources. This could aid gross margin expansion that was likely pressurised by declining onsite revenues led by transitioning employees at Nokia.

Exhibit 19: Overtime annual cost/employee per quarter has reduced

2.8 2.83.1

2.7 2.7 2.7 2.8 3.02.6 2.4 2.4

4.8 4.85.2 5.1

4.4 4.44.8 4.9

4.43.9 4.0

0.0

2.0

4.0

6.0

Q1FY

09

Q2FY

09

Q3FY

09

Q4FY

09

Q1FY

10

Q2FY

10

Q3FY

10

Q4FY

10

Q1FY

11

Q2FY

11

Q3FY

11

| la

khs

Cost per employee Revenue per employee

Source: Company, ICICIdirect.com Research

Exhibit 20: Cost/employee per quarter comparison

Cost per employee (| lakhs) Q4FY09 Q1FY10 Q2FY10 Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11Rolta * 2.4 2.4 2.7 2.7 2.6 2.5 2.7 3.1Hexaware ^ 2.9 3.0 2.7 2.8 2.6 2.8 2.7 2.9Geometric 2.9 2.8 2.5 2.5 2.5 2.8 2.7 2.8Mastek * 3.5 3.3 3.2 3.6 3.4 3.5 3.7 3.8KPIT 2.2 2.2 2.2 2.0 2.2 2.2 2.1 2.3Mindree 2.3 2.5 2.4 2.5 2.7 2.6 2.6 2.6Infotech Enter 1.7 1.8 1.8 1.8 1.9 2.1 2.3 2.3Persistent 1.9 2.0 1.9 2.1 2.3 2.5 2.3 2.3Sasken 2.7 2.7 2.7 2.8 3.0 2.6 2.4 2.4* June ending; ^ Calender year

Source: Company filings, ICICIdirect.com Research

Geographic diversification may yield revenue stability Historically, Europe, Middle East, Africa (EMEA) and the US revenue contribution stood as high as 80% (in FY05) led by concentration of top clients such as Nortel, Nokia, Ericsson, Texas Instruments and Qualcomm. However, the contribution from these two geographies had declined to 69% in FY10 and stands at 57% of Q3FY11 revenues as Sasken continues to de-risk its business model by expanding into newer geographies. In Q3FY11, India and APAC contributed 28% and 15% of revenues vs. 26% and 5% in FY10. Geographic diversification bodes well for revenue stability

The overtime cost per employee metric has improved. This

helps to manage the margins

ICICIdirect.com | Equity Research Page 11

ICICI Securities Limited

Exhibit 21: Geography wise revenue break-up

34 35 29 28 20 20 19 18 16

47 37 44 5052 49 45 44 41

9 22 21 19 23 26 28 2928

11 7 7 3 5 5 8 8 15

0102030405060708090

100

FY05 FY06 FY07 FY08 FY09 FY10 Q1FY11 Q2FY11 Q3FY11

(%)

North America Europe, Middle East, Africa India Asia Pacific

s

Source: Company operating metric, ICICIdirect.com Research

Buyback should support share price in near term; improve financial ratios over medium term

On October 21, 2010, the Sasken board approved a share buyback through (starting December 2, 2010) open market transactions at a price not exceeding | 260/- per equity share for an amount not exceeding | 34.54 crore. The offer would close either on October 20, 2011 or in case the maximum offer shares (~2.755 million) have been bought. At | 260/share, 13,28,461 shares could have to be bought representing ~4.90% of the paid-up equity share capital. However, the average share price since December 3, 2010 stood at of | 167.08. This suggests, Sasken would acquire ~7,55,023 shares higher compared to what it would have acquired at | 260. This implies that apart from supporting near term share price volatility, the buyback announced would improve its financial ratios upon extinguishing higher number of acquired shares. Finally, till date, the company has spent | 18.6 crore to buy back ~1.2 million shares at an average price of | 155. Exhibit 22: Buyback should support near term price volatility

Buyback DetailsBuyback Amount (| cr) 34.54 Maximum Price (|) 260 Maximum shares bought 1,328,461 Average Share price (|) 165.78 Maximum shares bought 2,083,484 Incremental shares that could be bought 755,023 Shares bought back till date at an average price of |155 1,200,000

Source: Company, ICICIdirect.com Research

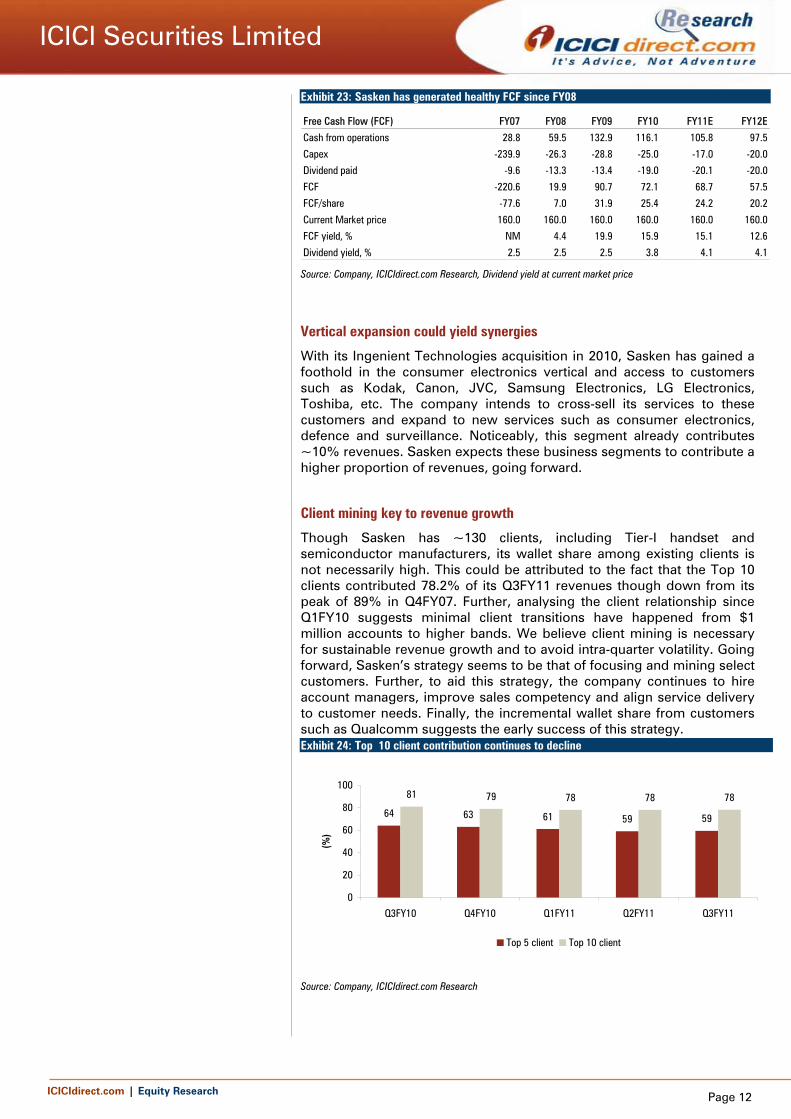

Healthy cash balance & free cash flow yield should comfort investors

Sasken continues to generate healthy operating and free cash flow. In FY10, Sasken generated cash flow from operations (CFO) of | 116.1 crore compared to | 132.9 crore in FY09. Further, we are modelling FY11E and FY12E CFO of | 105.8 crore and |97.5 crore, respectively. Adjusting for capex and dividend payment of | 17 crore and | 20.1 crore in FY11E and | 20 crore each in FY12E yields a free cash flow per share of | 24.2 and | 20.2 or an FCF yield of 15.1% and 12.6% for FY11E and FY12E, respectively. Finally, a healthy cash balance of | 192.6 crore (| 67.8/share) should comfort investors.

The buyback should support near term share price volatility

and improve financial ratios, going forward. Till date,

Sasken has bought back ~12 lakh shares at an average

price of | 155

Sasken has a healthy cash/share of | 67.8 and attractive

FCF yield of 15.1%

ICICIdirect.com | Equity Research Page 12

ICICI Securities Limited

Exhibit 23: Sasken has generated healthy FCF since FY08

Free Cash Flow (FCF) FY07 FY08 FY09 FY10 FY11E FY12E

Cash from operations 28.8 59.5 132.9 116.1 105.8 97.5

Capex -239.9 -26.3 -28.8 -25.0 -17.0 -20.0

Dividend paid -9.6 -13.3 -13.4 -19.0 -20.1 -20.0

FCF -220.6 19.9 90.7 72.1 68.7 57.5

FCF/share -77.6 7.0 31.9 25.4 24.2 20.2

Current Market price 160.0 160.0 160.0 160.0 160.0 160.0

FCF yield, % NM 4.4 19.9 15.9 15.1 12.6

Dividend yield, % 2.5 2.5 2.5 3.8 4.1 4.1

Source: Company, ICICIdirect.com Research, Dividend yield at current market price

Vertical expansion could yield synergies

With its Ingenient Technologies acquisition in 2010, Sasken has gained a foothold in the consumer electronics vertical and access to customers such as Kodak, Canon, JVC, Samsung Electronics, LG Electronics, Toshiba, etc. The company intends to cross-sell its services to these customers and expand to new services such as consumer electronics, defence and surveillance. Noticeably, this segment already contributes ~10% revenues. Sasken expects these business segments to contribute a higher proportion of revenues, going forward.

Client mining key to revenue growth

Though Sasken has ~130 clients, including Tier-I handset and semiconductor manufacturers, its wallet share among existing clients is not necessarily high. This could be attributed to the fact that the Top 10 clients contributed 78.2% of its Q3FY11 revenues though down from its peak of 89% in Q4FY07. Further, analysing the client relationship since Q1FY10 suggests minimal client transitions have happened from $1 million accounts to higher bands. We believe client mining is necessary for sustainable revenue growth and to avoid intra-quarter volatility. Going forward, Sasken’s strategy seems to be that of focusing and mining select customers. Further, to aid this strategy, the company continues to hire account managers, improve sales competency and align service delivery to customer needs. Finally, the incremental wallet share from customers such as Qualcomm suggests the early success of this strategy. Exhibit 24: Top 10 client contribution continues to decline

64 63 61 59 59

81 79 78 78 78

0

20

40

60

80

100

Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11

(%)

Top 5 client Top 10 client

Source: Company, ICICIdirect.com Research

ICICIdirect.com | Equity Research Page 13

ICICI Securities Limited

Exhibit 25: Client mining key to revenue growth

15

17

13

13

15

4

5

5

5

7

5

4

6

6

4

2

2

1

1

1

1

1

1

1

1

0 5 10 15 20 25 30 35

Q3FY10

Q4FY10

Q1FY11

Q2FY11

Q3FY11

< $1mn TTM

$1mn < > $3 million

$3 mn < > $10 million

$10 mn < > $20 million

> $20 million

Source: Company, ICICIdirect.com Research

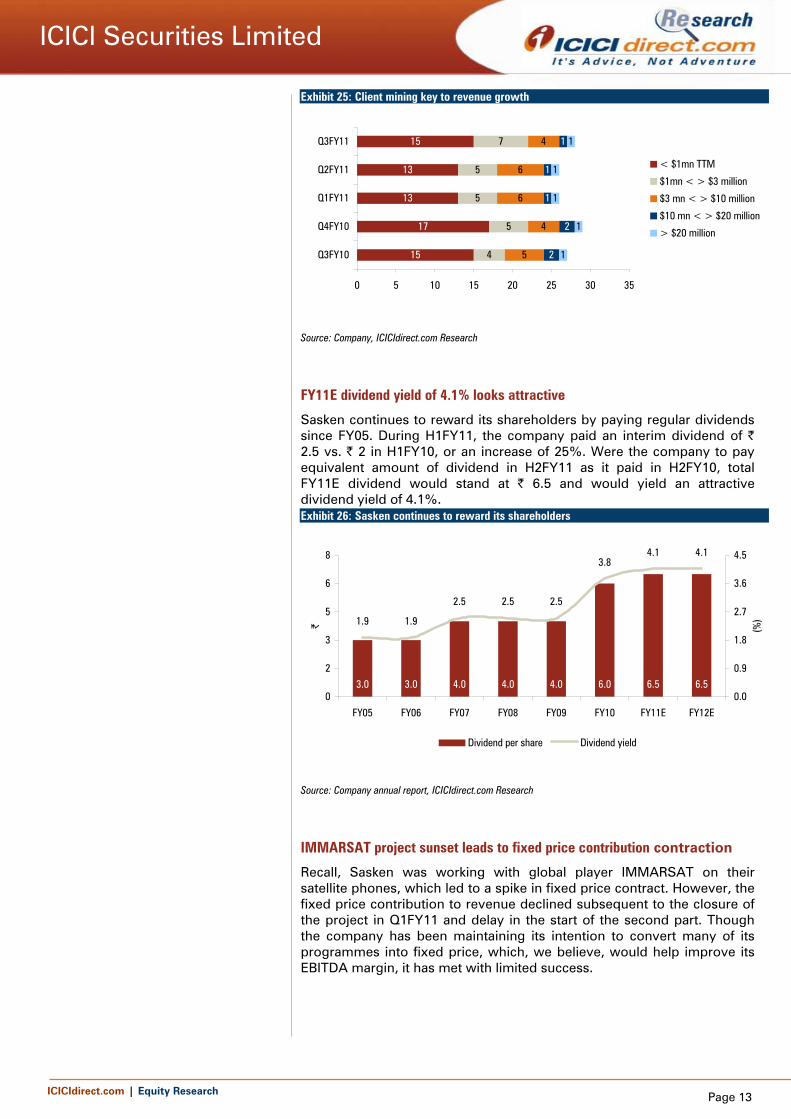

FY11E dividend yield of 4.1% looks attractive

Sasken continues to reward its shareholders by paying regular dividends since FY05. During H1FY11, the company paid an interim dividend of | 2.5 vs. | 2 in H1FY10, or an increase of 25%. Were the company to pay equivalent amount of dividend in H2FY11 as it paid in H2FY10, total FY11E dividend would stand at | 6.5 and would yield an attractive dividend yield of 4.1%. Exhibit 26: Sasken continues to reward its shareholders

3.0 3.0 4.0 4.0 4.0 6.0 6.5 6.5

1.9 1.9

2.5 2.5 2.5

3.84.1 4.1

0

2

3

5

6

8

FY05 FY06 FY07 FY08 FY09 FY10 FY11E FY12E

|

0.0

0.9

1.8

2.7

3.6

4.5

(%)

Dividend per share Dividend yield

Source: Company annual report, ICICIdirect.com Research

IMMARSAT project sunset leads to fixed price contribution contraction

Recall, Sasken was working with global player IMMARSAT on their satellite phones, which led to a spike in fixed price contract. However, the fixed price contribution to revenue declined subsequent to the closure of the project in Q1FY11 and delay in the start of the second part. Though the company has been maintaining its intention to convert many of its programmes into fixed price, which, we believe, would help improve its EBITDA margin, it has met with limited success.

ICICIdirect.com | Equity Research Page 14

ICICI Securities Limited

Exhibit 27: Rise in fixed price contribution should shore up margins

7.3 9.0 14.6 14.2 18.2 22.6 20.2 18.3 15.3

92.7 91.0 85.4 85.8 81.8 77.4 79.8 81.7 84.7

0102030405060708090

100

Q3FY09 Q4FY09 Q1FY10 Q2FY10 Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11

(%)

Fixed price Time and material

Source: Company, ICICIdirect.com Research

Sasken may benefit from vendor rationalisation by handset clients

Discussions with the management suggest handset OEMs continue to rationalise vendors from fragmented landscape currently. We believe this could benefit Sasken given its domain expertise and as it is among top 10 vendors’ list for a majority of its customers. However, Nokia continues to shift work to low cost from high cost locations. Further, offshoring volume ramp-ups are not in the same ratio as onsite ramp-downs.

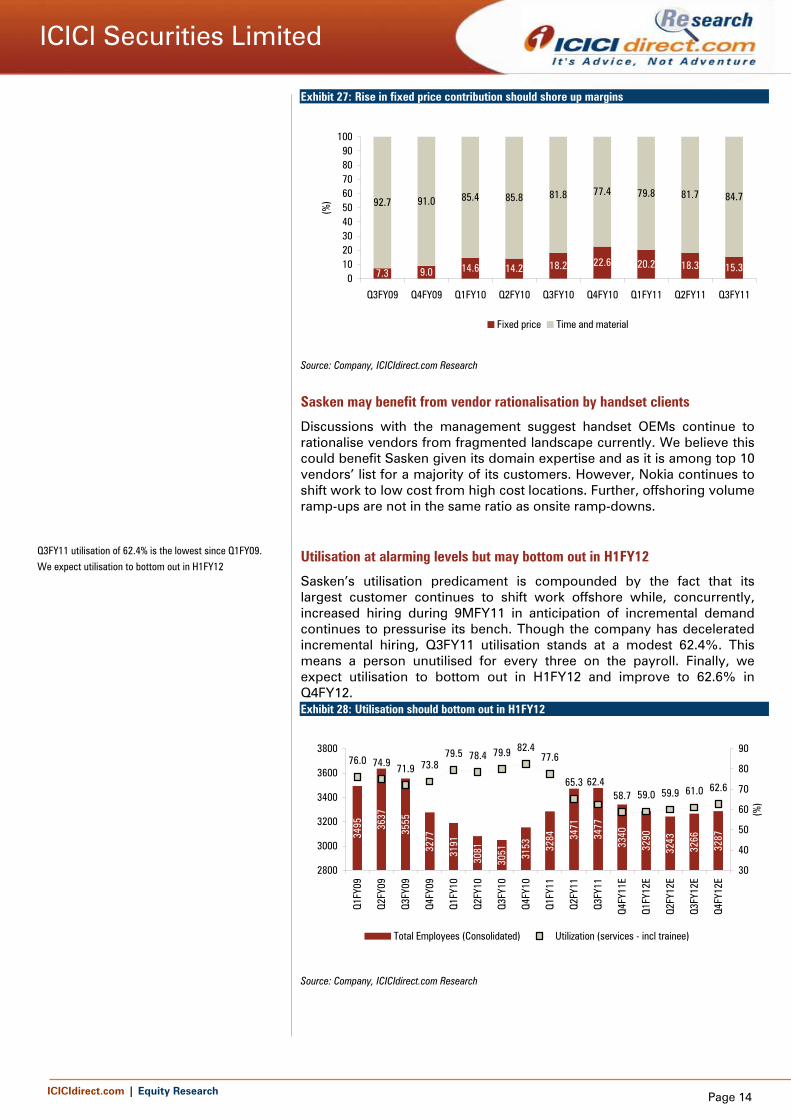

Utilisation at alarming levels but may bottom out in H1FY12

Sasken’s utilisation predicament is compounded by the fact that its largest customer continues to shift work offshore while, concurrently, increased hiring during 9MFY11 in anticipation of incremental demand continues to pressurise its bench. Though the company has decelerated incremental hiring, Q3FY11 utilisation stands at a modest 62.4%. This means a person unutilised for every three on the payroll. Finally, we expect utilisation to bottom out in H1FY12 and improve to 62.6% in Q4FY12. Exhibit 28: Utilisation should bottom out in H1FY12

3495 36

37

3555

3277

3191

3081

3051 31

53 3284 34

71

3477

3340

3290

3243

3266

3287

76.0 74.9 71.9 73.879.5 78.4 79.9 82.4

77.6

65.358.7 59.0 59.9 61.0 62.662.4

2800

3000

3200

3400

3600

3800

Q1FY

09

Q2FY

09

Q3FY

09

Q4FY

09

Q1FY

10

Q2FY

10

Q3FY

10

Q4FY

10

Q1FY

11

Q2FY

11

Q3FY

11

Q4FY

11E

Q1FY

12E

Q2FY

12E

Q3FY

12E

Q4FY

12E

30

40

50

60

70

80

90(%

)

Total Employees (Consolidated) Utilization (services - incl trainee)

Source: Company, ICICIdirect.com Research

Q3FY11 utilisation of 62.4% is the lowest since Q1FY09.

We expect utilisation to bottom out in H1FY12

ICICIdirect.com | Equity Research Page 15

ICICI Securities Limited

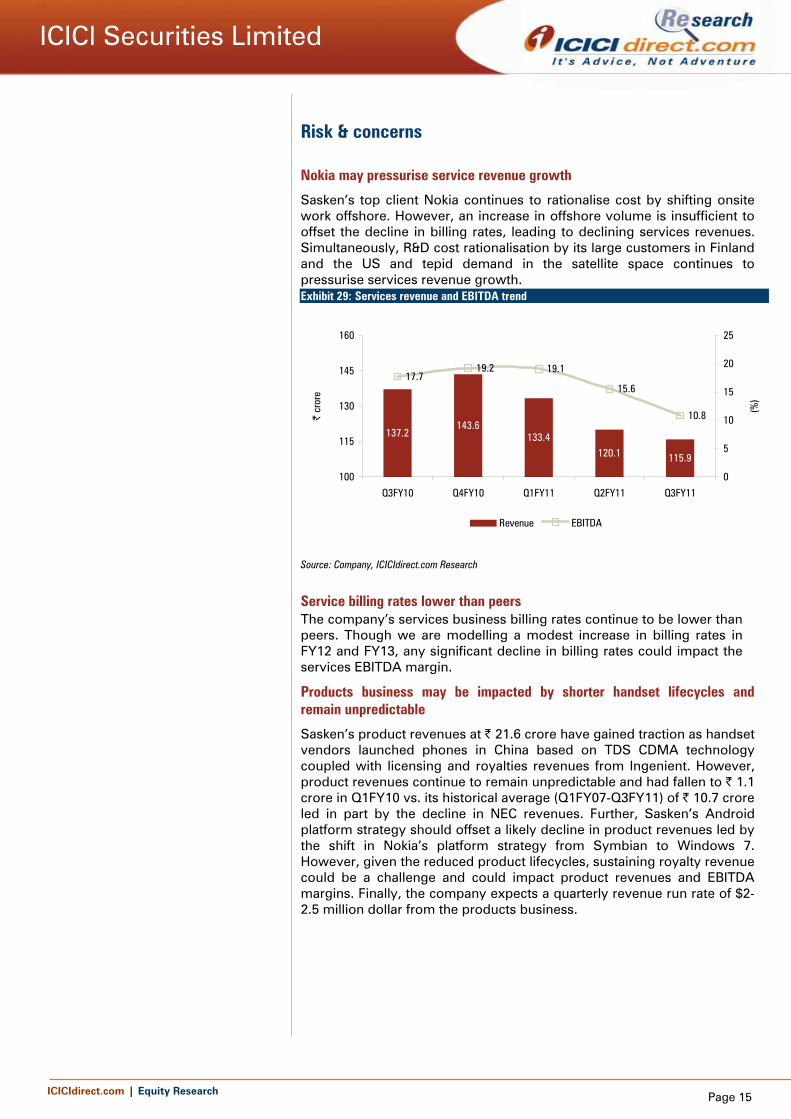

Risk & concerns

Nokia may pressurise service revenue growth

Sasken’s top client Nokia continues to rationalise cost by shifting onsite work offshore. However, an increase in offshore volume is insufficient to offset the decline in billing rates, leading to declining services revenues. Simultaneously, R&D cost rationalisation by its large customers in Finland and the US and tepid demand in the satellite space continues to pressurise services revenue growth. Exhibit 29: Services revenue and EBITDA trend

137.2143.6

133.4120.1 115.9

17.719.2 19.1

15.6

10.8

100

115

130

145

160

Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11

| cr

ore

0

5

10

15

20

25

(%)

Revenue EBITDA

Source: Company, ICICIdirect.com Research

Service billing rates lower than peers The company’s services business billing rates continue to be lower than peers. Though we are modelling a modest increase in billing rates in FY12 and FY13, any significant decline in billing rates could impact the services EBITDA margin.

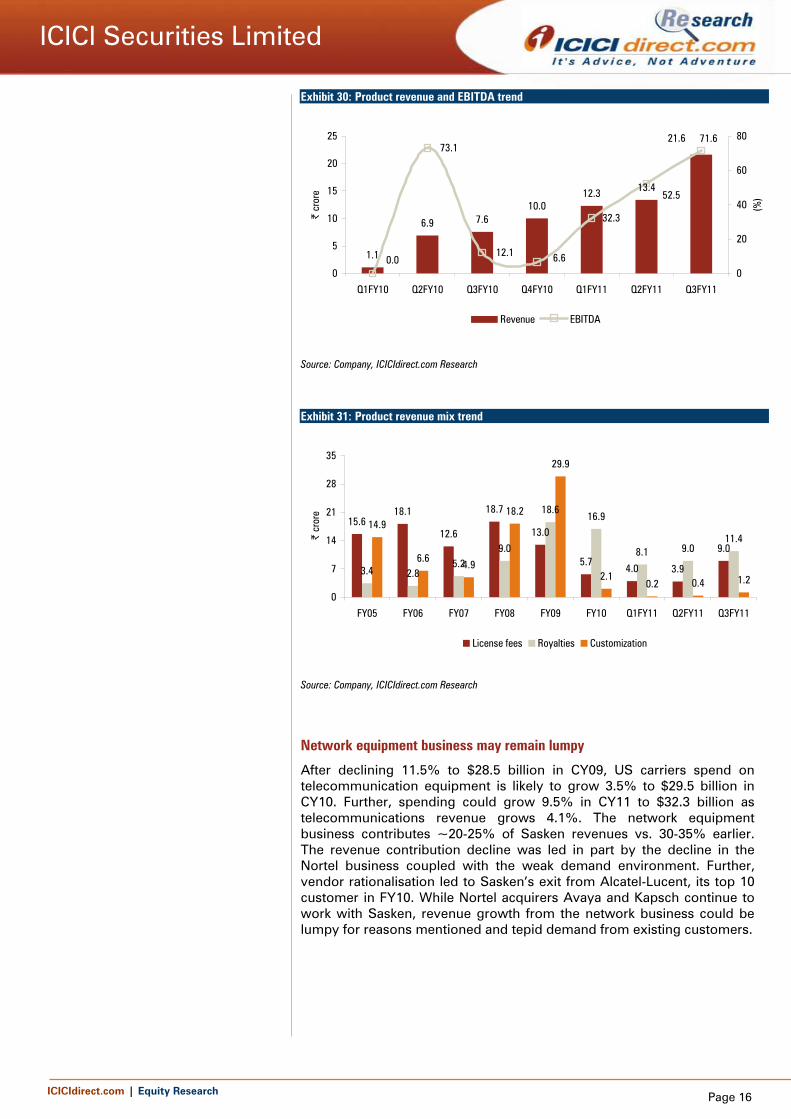

Products business may be impacted by shorter handset lifecycles and remain unpredictable

Sasken’s product revenues at | 21.6 crore have gained traction as handset vendors launched phones in China based on TDS CDMA technology coupled with licensing and royalties revenues from Ingenient. However, product revenues continue to remain unpredictable and had fallen to | 1.1 crore in Q1FY10 vs. its historical average (Q1FY07-Q3FY11) of | 10.7 crore led in part by the decline in NEC revenues. Further, Sasken’s Android platform strategy should offset a likely decline in product revenues led by the shift in Nokia’s platform strategy from Symbian to Windows 7. However, given the reduced product lifecycles, sustaining royalty revenue could be a challenge and could impact product revenues and EBITDA margins. Finally, the company expects a quarterly revenue run rate of $2-2.5 million dollar from the products business.

ICICIdirect.com | Equity Research Page 16

ICICI Securities Limited

Exhibit 30: Product revenue and EBITDA trend

1.1

6.9 7.610.0

12.3 13.4

21.6 71.6

12.1

73.1

0.0

52.5

32.3

6.60

5

10

15

20

25

Q1FY10 Q2FY10 Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11

| cr

ore

0

20

40

60

80

(%)

Revenue EBITDA

Source: Company, ICICIdirect.com Research

Exhibit 31: Product revenue mix trend

15.618.1

12.6

18.7

13.0

5.74.0 3.9

9.0

3.4 2.85.2

9.0

18.616.9

8.1 9.011.4

14.9

6.64.9

18.2

29.9

2.10.2 0.4 1.2

0

7

14

21

28

35

FY05 FY06 FY07 FY08 FY09 FY10 Q1FY11 Q2FY11 Q3FY11

| cr

ore

License fees Royalties Customization

Source: Company, ICICIdirect.com Research

Network equipment business may remain lumpy

After declining 11.5% to $28.5 billion in CY09, US carriers spend on telecommunication equipment is likely to grow 3.5% to $29.5 billion in CY10. Further, spending could grow 9.5% in CY11 to $32.3 billion as telecommunications revenue grows 4.1%. The network equipment business contributes ~20-25% of Sasken revenues vs. 30-35% earlier. The revenue contribution decline was led in part by the decline in the Nortel business coupled with the weak demand environment. Further, vendor rationalisation led to Sasken’s exit from Alcatel-Lucent, its top 10 customer in FY10. While Nortel acquirers Avaya and Kapsch continue to work with Sasken, revenue growth from the network business could be lumpy for reasons mentioned and tepid demand from existing customers.

ICICIdirect.com | Equity Research Page 17

ICICI Securities Limited

Exhibit 32: Telecommunication equipment likely to grow 9.5% in CY11

21.3

22.5

26.4

29.3

30.8

32.2

28.5

29.5

32.3

33.9

35.0

1140.71083.41033.1992.8987.81047.61003.9

921.1837.2

765.8709.5

0

8

16

24

32

40

CY03 CY04 CY05 CY06 CY07 CY08 CY09 CY10E CY11E CY12E CY13E

$, b

illion

s

0

400

800

1200

$, b

illion

s

US carrier spending on telecommunications equipment US telecommunications revenue

Source: Telecommunication Industry Association (TIA), ICICIdirect.com Research

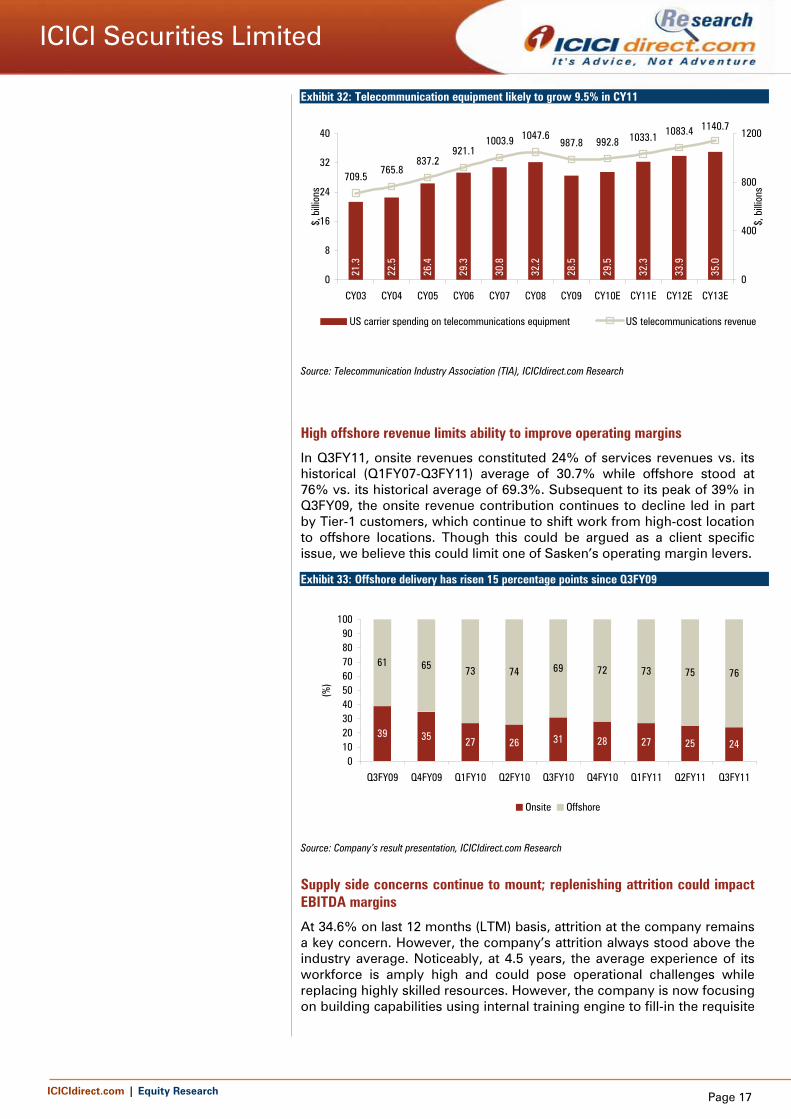

High offshore revenue limits ability to improve operating margins

In Q3FY11, onsite revenues constituted 24% of services revenues vs. its historical (Q1FY07-Q3FY11) average of 30.7% while offshore stood at 76% vs. its historical average of 69.3%. Subsequent to its peak of 39% in Q3FY09, the onsite revenue contribution continues to decline led in part by Tier-1 customers, which continue to shift work from high-cost location to offshore locations. Though this could be argued as a client specific issue, we believe this could limit one of Sasken’s operating margin levers.

Exhibit 33: Offshore delivery has risen 15 percentage points since Q3FY09

39 35 27 26 31 28 27 25 24

61 65 73 74 69 72 73 75 76

0102030405060708090100

Q3FY09 Q4FY09 Q1FY10 Q2FY10 Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11

(%)

Onsite Offshore

Source: Company’s result presentation, ICICIdirect.com Research

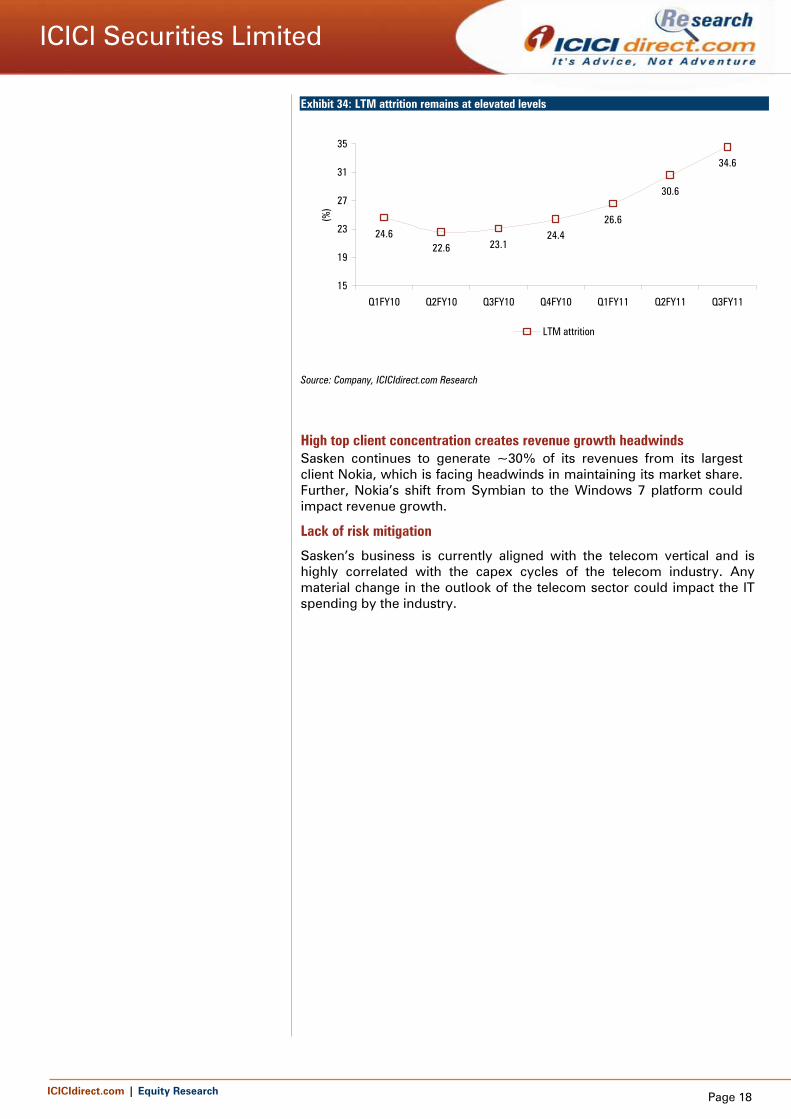

Supply side concerns continue to mount; replenishing attrition could impact EBITDA margins

At 34.6% on last 12 months (LTM) basis, attrition at the company remains a key concern. However, the company’s attrition always stood above the industry average. Noticeably, at 4.5 years, the average experience of its workforce is amply high and could pose operational challenges while replacing highly skilled resources. However, the company is now focusing on building capabilities using internal training engine to fill-in the requisite

ICICIdirect.com | Equity Research Page 18

ICICI Securities Limited

Exhibit 34: LTM attrition remains at elevated levels

24.622.6 23.1

24.426.6

30.6

34.6

15

19

23

27

31

35

Q1FY10 Q2FY10 Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11

(%)

LTM attrition

Source: Company, ICICIdirect.com Research

High top client concentration creates revenue growth headwinds Sasken continues to generate ~30% of its revenues from its largest client Nokia, which is facing headwinds in maintaining its market share. Further, Nokia’s shift from Symbian to the Windows 7 platform could impact revenue growth.

Lack of risk mitigation

Sasken’s business is currently aligned with the telecom vertical and is highly correlated with the capex cycles of the telecom industry. Any material change in the outlook of the telecom sector could impact the IT spending by the industry.

ICICIdirect.com | Equity Research Page 19

ICICI Securities Limited

Financials

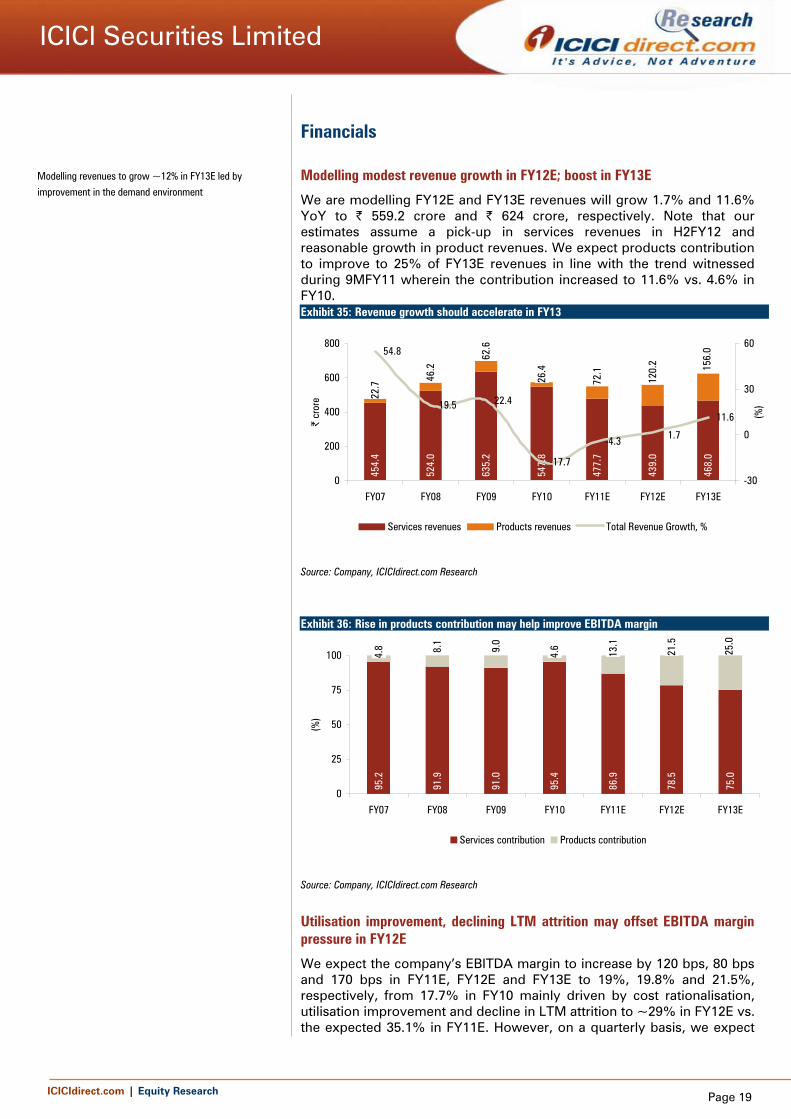

Modelling modest revenue growth in FY12E; boost in FY13E

We are modelling FY12E and FY13E revenues will grow 1.7% and 11.6% YoY to | 559.2 crore and | 624 crore, respectively. Note that our estimates assume a pick-up in services revenues in H2FY12 and reasonable growth in product revenues. We expect products contribution to improve to 25% of FY13E revenues in line with the trend witnessed during 9MFY11 wherein the contribution increased to 11.6% vs. 4.6% in FY10. Exhibit 35: Revenue growth should accelerate in FY13

454.

4

524.

0

635.

2

547.

8

477.

7

439.

0

468.

0

26.4 15

6.0

120.

2

72.1

62.6

46.2

22.7

54.8

19.5 22.4

-17.7

-4.3

11.6

1.7

0

200

400

600

800

FY07 FY08 FY09 FY10 FY11E FY12E FY13E

| cr

ore

-30

0

30

60

(%)

Services revenues Products revenues Total Revenue Growth, %

Source: Company, ICICIdirect.com Research

Exhibit 36: Rise in products contribution may help improve EBITDA margin

95.2

91.9

91.0

95.4

86.9

78.5

75.0

4.6

4.8 8.

1

9.0

13.1

21.5

25.0

0

25

50

75

100

FY07 FY08 FY09 FY10 FY11E FY12E FY13E

(%)

Services contribution Products contribution

Source: Company, ICICIdirect.com Research

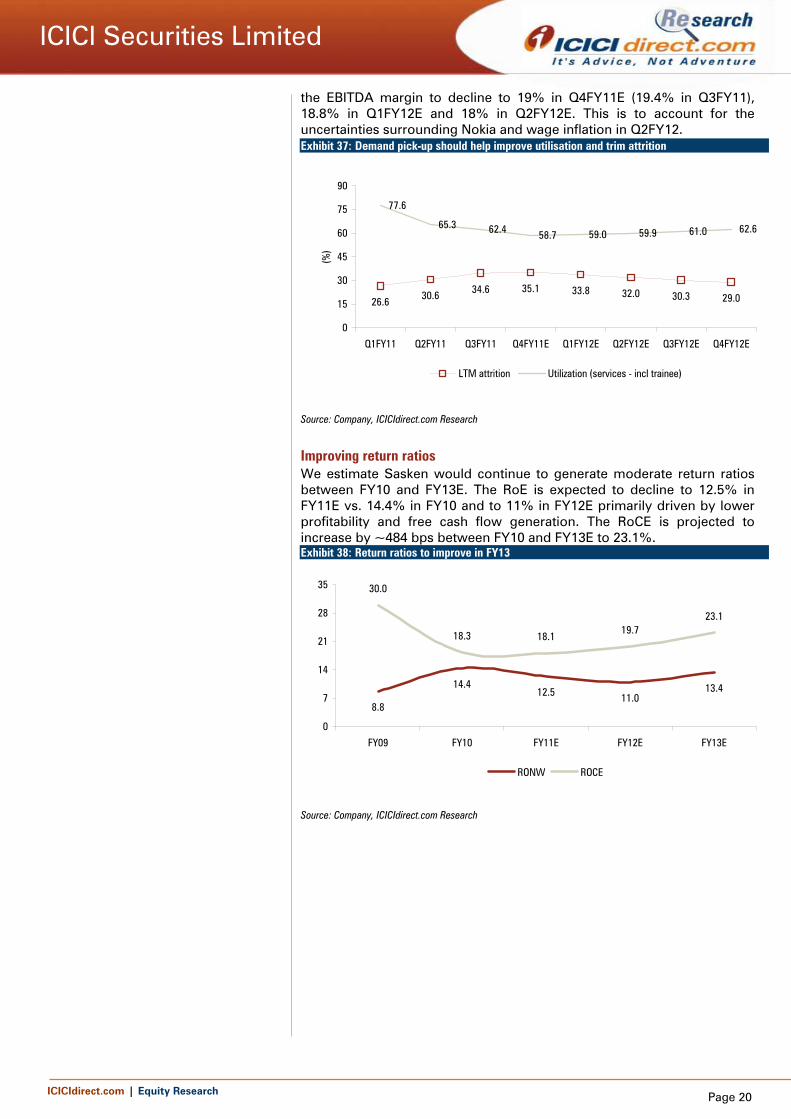

Utilisation improvement, declining LTM attrition may offset EBITDA margin pressure in FY12E

We expect the company’s EBITDA margin to increase by 120 bps, 80 bps and 170 bps in FY11E, FY12E and FY13E to 19%, 19.8% and 21.5%, respectively, from 17.7% in FY10 mainly driven by cost rationalisation, utilisation improvement and decline in LTM attrition to ~29% in FY12E vs. the expected 35.1% in FY11E. However, on a quarterly basis, we expect

Modelling revenues to grow ~12% in FY13E led by

improvement in the demand environment

ICICIdirect.com | Equity Research Page 20

ICICI Securities Limited

the EBITDA margin to decline to 19% in Q4FY11E (19.4% in Q3FY11), 18.8% in Q1FY12E and 18% in Q2FY12E. This is to account for the uncertainties surrounding Nokia and wage inflation in Q2FY12. Exhibit 37: Demand pick-up should help improve utilisation and trim attrition

26.6 30.6 34.6 35.1 33.8 32.0 30.3 29.0

77.6

65.3 62.4 58.7 59.0 59.9 61.0 62.6

0

15

30

45

60

75

90

Q1FY11 Q2FY11 Q3FY11 Q4FY11E Q1FY12E Q2FY12E Q3FY12E Q4FY12E

(%)

LTM attrition Utilization (services - incl trainee)

Source: Company, ICICIdirect.com Research

Improving return ratios We estimate Sasken would continue to generate moderate return ratios between FY10 and FY13E. The RoE is expected to decline to 12.5% in FY11E vs. 14.4% in FY10 and to 11% in FY12E primarily driven by lower profitability and free cash flow generation. The RoCE is projected to increase by ~484 bps between FY10 and FY13E to 23.1%. Exhibit 38: Return ratios to improve in FY13

8.8

14.412.5 11.0

13.4

30.0

18.3 18.119.7

23.1

0

7

14

21

28

35

FY09 FY10 FY11E FY12E FY13E

RONW ROCE

Source: Company, ICICIdirect.com Research

ICICIdirect.com | Equity Research Page 21

ICICI Securities Limited

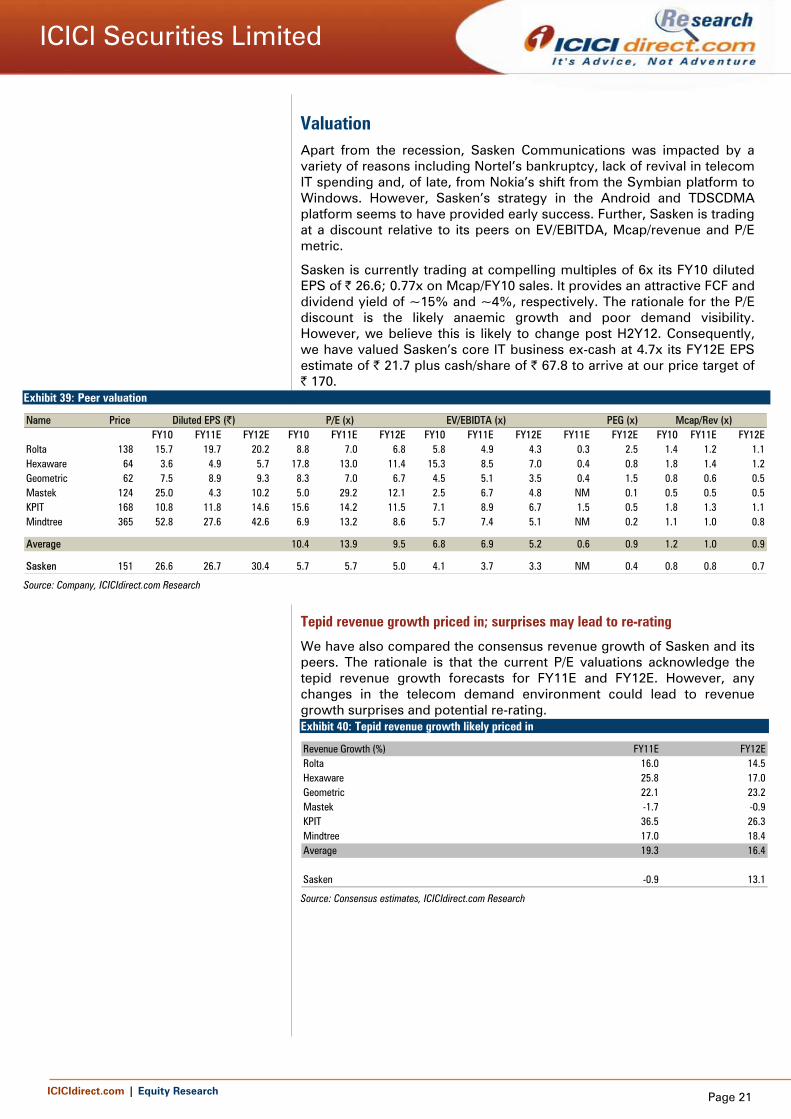

Valuation Apart from the recession, Sasken Communications was impacted by a variety of reasons including Nortel’s bankruptcy, lack of revival in telecom IT spending and, of late, from Nokia’s shift from the Symbian platform to Windows. However, Sasken’s strategy in the Android and TDSCDMA platform seems to have provided early success. Further, Sasken is trading at a discount relative to its peers on EV/EBITDA, Mcap/revenue and P/E metric.

Sasken is currently trading at compelling multiples of 6x its FY10 diluted EPS of | 26.6; 0.77x on Mcap/FY10 sales. It provides an attractive FCF and dividend yield of ~15% and ~4%, respectively. The rationale for the P/E discount is the likely anaemic growth and poor demand visibility. However, we believe this is likely to change post H2Y12. Consequently, we have valued Sasken’s core IT business ex-cash at 4.7x its FY12E EPS estimate of | 21.7 plus cash/share of | 67.8 to arrive at our price target of | 170.

Exhibit 39: Peer valuation

Name Price FY10 FY11E FY12E FY10 FY11E FY12E FY10 FY11E FY12E FY11E FY12E FY10 FY11E FY12E

Rolta 138 15.7 19.7 20.2 8.8 7.0 6.8 5.8 4.9 4.3 0.3 2.5 1.4 1.2 1.1Hexaware 64 3.6 4.9 5.7 17.8 13.0 11.4 15.3 8.5 7.0 0.4 0.8 1.8 1.4 1.2Geometric 62 7.5 8.9 9.3 8.3 7.0 6.7 4.5 5.1 3.5 0.4 1.5 0.8 0.6 0.5Mastek 124 25.0 4.3 10.2 5.0 29.2 12.1 2.5 6.7 4.8 NM 0.1 0.5 0.5 0.5KPIT 168 10.8 11.8 14.6 15.6 14.2 11.5 7.1 8.9 6.7 1.5 0.5 1.8 1.3 1.1Mindtree 365 52.8 27.6 42.6 6.9 13.2 8.6 5.7 7.4 5.1 NM 0.2 1.1 1.0 0.8

Average 10.4 13.9 9.5 6.8 6.9 5.2 0.6 0.9 1.2 1.0 0.9

Sasken 151 26.6 26.7 30.4 5.7 5.7 5.0 4.1 3.7 3.3 NM 0.4 0.8 0.8 0.7

Mcap/Rev (x)Diluted EPS (|) P/E (x) EV/EBIDTA (x) PEG (x)

Source: Company, ICICIdirect.com Research

Tepid revenue growth priced in; surprises may lead to re-rating

We have also compared the consensus revenue growth of Sasken and its peers. The rationale is that the current P/E valuations acknowledge the tepid revenue growth forecasts for FY11E and FY12E. However, any changes in the telecom demand environment could lead to revenue growth surprises and potential re-rating. Exhibit 40: Tepid revenue growth likely priced in

Revenue Growth (%) FY11E FY12ERolta 16.0 14.5Hexaware 25.8 17.0Geometric 22.1 23.2Mastek -1.7 -0.9KPIT 36.5 26.3Mindtree 17.0 18.4Average 19.3 16.4

Sasken -0.9 13.1

Source: Consensus estimates, ICICIdirect.com Research

ICICIdirect.com | Equity Research Page 22

ICICI Securities Limited

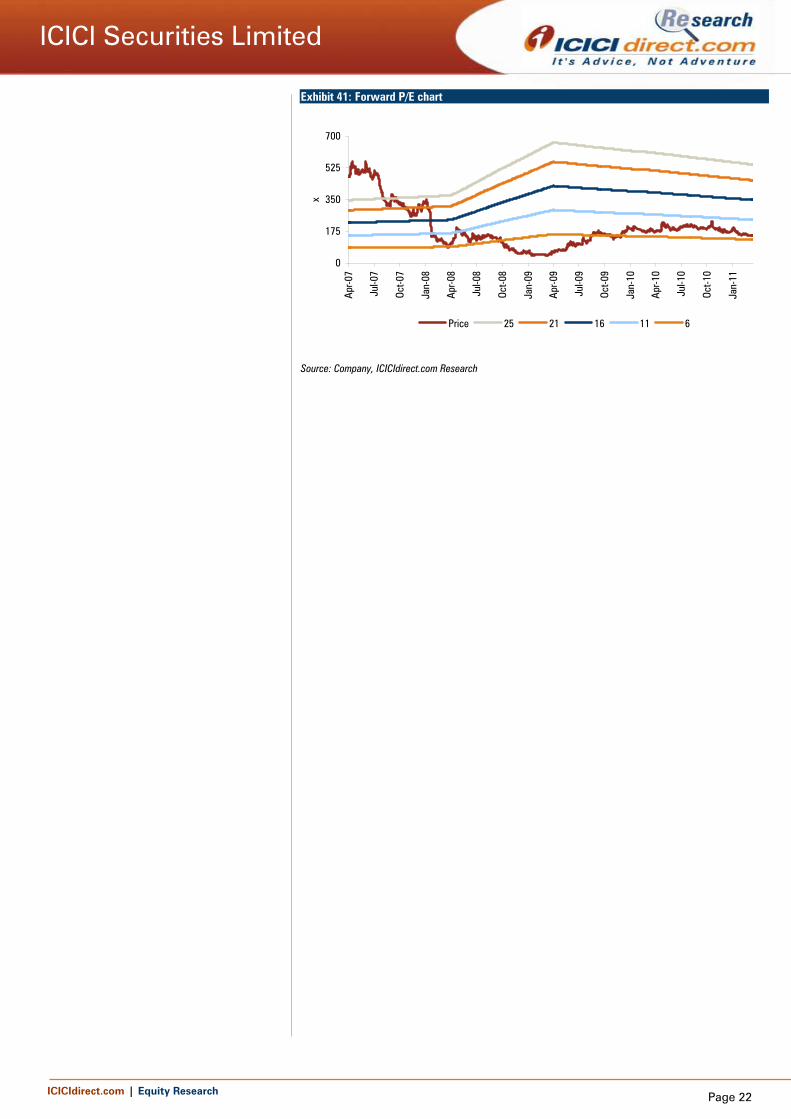

Exhibit 41: Forward P/E chart

0

175

350

525

700

Apr-0

7

Jul-0

7

Oct-0

7

Jan-

08

Apr-0

8

Jul-0

8

Oct-0

8

Jan-

09

Apr-0

9

Jul-0

9

Oct-0

9

Jan-

10

Apr-1

0

Jul-1

0

Oct-1

0

Jan-

11

xPrice 25 21 16 11 6

Source: Company, ICICIdirect.com Research

ICICIdirect.com | Equity Research Page 23

ICICI Securities Limited

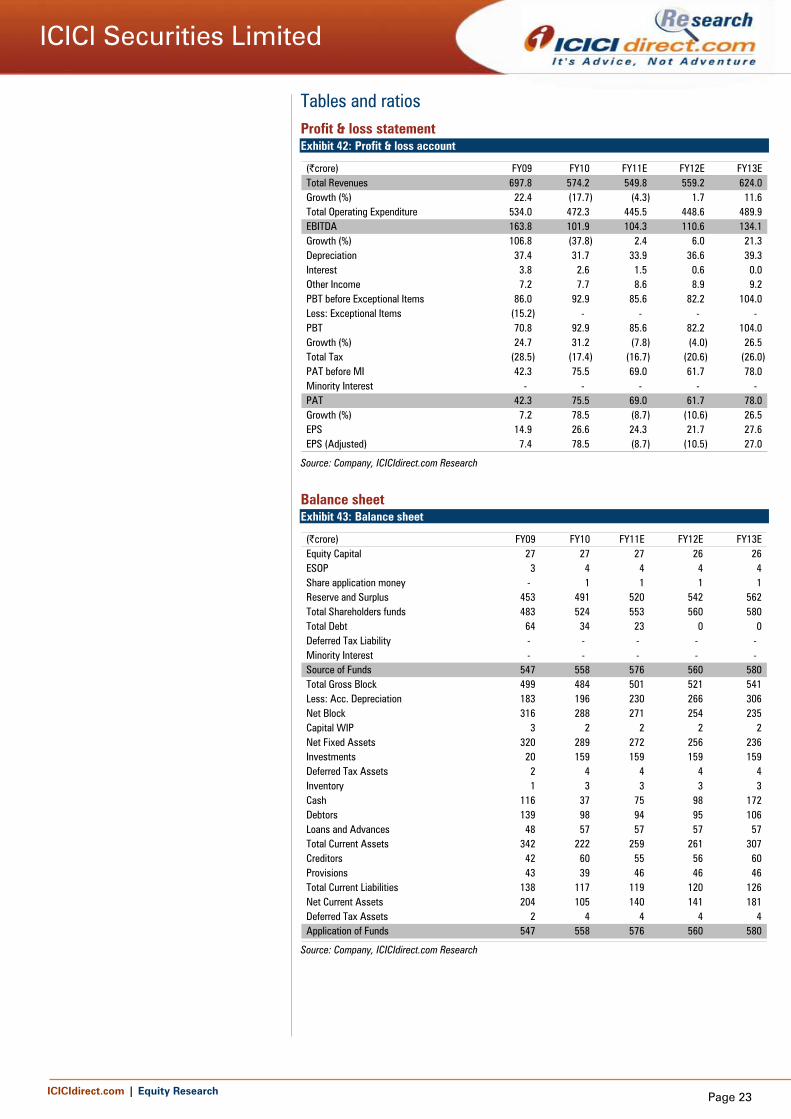

Tables and ratios Profit & loss statement Exhibit 42: Profit & loss account

(|crore) FY09 FY10 FY11E FY12E FY13ETotal Revenues 697.8 574.2 549.8 559.2 624.0 Growth (%) 22.4 (17.7) (4.3) 1.7 11.6 Total Operating Expenditure 534.0 472.3 445.5 448.6 489.9 EBITDA 163.8 101.9 104.3 110.6 134.1 Growth (%) 106.8 (37.8) 2.4 6.0 21.3 Depreciation 37.4 31.7 33.9 36.6 39.3 Interest 3.8 2.6 1.5 0.6 0.0 Other Income 7.2 7.7 8.6 8.9 9.2 PBT before Exceptional Items 86.0 92.9 85.6 82.2 104.0 Less: Exceptional Items (15.2) - - - - PBT 70.8 92.9 85.6 82.2 104.0 Growth (%) 24.7 31.2 (7.8) (4.0) 26.5 Total Tax (28.5) (17.4) (16.7) (20.6) (26.0) PAT before MI 42.3 75.5 69.0 61.7 78.0 Minority Interest - - - - - PAT 42.3 75.5 69.0 61.7 78.0 Growth (%) 7.2 78.5 (8.7) (10.6) 26.5 EPS 14.9 26.6 24.3 21.7 27.6 EPS (Adjusted) 7.4 78.5 (8.7) (10.5) 27.0

Source: Company, ICICIdirect.com Research

Balance sheet Exhibit 43: Balance sheet

(|crore) FY09 FY10 FY11E FY12E FY13EEquity Capital 27 27 27 26 26 ESOP 3 4 4 4 4 Share application money - 1 1 1 1 Reserve and Surplus 453 491 520 542 562 Total Shareholders funds 483 524 553 560 580 Total Debt 64 34 23 0 0 Deferred Tax Liability - - - - - Minority Interest - - - - - Source of Funds 547 558 576 560 580 Total Gross Block 499 484 501 521 541 Less: Acc. Depreciation 183 196 230 266 306 Net Block 316 288 271 254 235 Capital WIP 3 2 2 2 2 Net Fixed Assets 320 289 272 256 236 Investments 20 159 159 159 159 Deferred Tax Assets 2 4 4 4 4 Inventory 1 3 3 3 3 Cash 116 37 75 98 172 Debtors 139 98 94 95 106 Loans and Advances 48 57 57 57 57 Total Current Assets 342 222 259 261 307 Creditors 42 60 55 56 60 Provisions 43 39 46 46 46 Total Current Liabilities 138 117 119 120 126 Net Current Assets 204 105 140 141 181 Deferred Tax Assets 2 4 4 4 4 Application of Funds 547 558 576 560 580

Source: Company, ICICIdirect.com Research

ICICIdirect.com | Equity Research Page 24

ICICI Securities Limited

Cash flow statement Exhibit 44: Cash flow statement

FY09 FY10 FY11E FY12E FY13EProfit after Tax 71 93 86 82 104Depreciation 37 32 34 37 39(inc)/dec in Current Assets -62 120 -37 -2 -46(inc)/dec in current Liabilities 46 -17 -5 1 6CF from operations 133 116 106 97 109Other Investments 3 -1 2 3 5(Purchase)/Sale of Fixed Assets -23 -151 -17 -20 -20CF from investing Activities -20 -151 -15 -17 -15Inc / (Dec) in Equity Capital -15 1 -20 -14 0Inc / (Dec) in sec.loan Funds -27 -23 -11 -23 0Dividend & Divendend tax -13 -19 -20 -20 -20Govt subsidy -net of utilization 0 0 0 0 0Interest paid -4 -1 -2 -1 0CF from Financial Activities -60 -42 -53 -58 -20Cash generating during the year 53 -77 38 23 74Translation effect on bank balance 7 -2 0 0 0Opening cash balance 56 116 37 75 98Closing cash 116 37 75 98 172

Source: Company, ICICIdirect.com Research

Ratios Exhibit 45: Key ratios

FY09 FY10 FY11E FY12E FY13EPer Share Data (|)EPS 14.9 26.6 24.3 21.7 27.6 Cash EPS 28.1 37.7 36.2 34.6 41.3 BV 178.1 193.1 203.1 213.8 221.5 Operating profit per share 57.7 35.9 36.7 38.9 47.2 Operating Ratios (%)EBITDA/Total Revenues 23.5 17.7 19.0 19.8 21.5 PBT/Total Revenues 10.1 16.2 15.6 14.7 16.7 PAT/ Total Revenues 6.1 13.2 12.5 11.0 12.5 Return Ratios (%)RoNW 8.8 14.4 12.5 11.0 13.4 RoCE 30.0 18.3 18.1 19.7 23.1 RoIC 5.3 10.1 8.5 7.4 10.0

FY09 FY10 FY11E FY12E FY13EValuation Ratios (x times)P/E 10.2 5.7 6.3 7.0 5.5 EV / EBITDA 1.6 2.6 2.5 2.4 2.0 Price to Book Value 0.9 0.8 0.7 0.7 0.7 EV/Total Revenues 0.4 0.5 0.5 0.5 0.4 MCap/Total Revenues 0.6 0.8 0.8 0.8 0.7 Total Revenues/ Equity 1.4 1.1 1.0 1.0 1.1 Turnover Ratios (x times)Inventory Turnover - - - - - Debtors Turnover Ratio 5.1 4.9 5.7 5.9 6.2 Creditors Turnover Ratio 0.1 0.1 0.1 0.1 0.1 Fixed Asset Turnover ratio 2.2 1.9 2.0 2.1 2.6 Solvency Ratios (x times)Debt / Equity 0.1 0.1 0.0 0.0 0.0 Current Ratio 2.5 1.9 2.2 2.2 2.4 Quick Ratio 2.5 1.9 2.2 2.2 2.4 Debt / EBITDA 0.4 0.3 0.2 0.0 0.0

Source: Company, ICICIdirect.com Research

ICICIdirect.com | Equity Research Page 25

ICICI Securities Limited

RATING RATIONALE ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns ratings to its stocks according to their notional target price vs. current market price and then categorises them as Strong Buy, Buy, Add, Reduce and Sell. The performance horizon is two years unless specified and the notional target price is defined as the analysts' valuation for a stock. Strong Buy: 20% or more; Buy: Between 10% and 20%; Add: Up to 10%; Reduce: Up to -10% Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk, ICICI Securities Limited, 7th Floor, Akruti Centre Point, MIDC Main Road, Marol Naka, Andheri (East) Mumbai – 400 093

ANALYST CERTIFICATION We /I, Abhishek Shindadkar research analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our personal views about any and all of the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. Analysts aren't registered as research analysts by FINRA and might not be an associated person of the ICICI Securities Inc.

Disclosures: ICICI Securities Limited (ICICI Securities) and its affiliates are a full-service, integrated investment banking, investment management and brokerage and financing group. We along with affiliates are leading underwriter of securities and participate in virtually all securities trading markets in India. We and our affiliates have investment banking and other business relationship with a significant percentage of companies covered by our Investment Research Department. Our research professionals provide important input into our investment banking and other business selection processes. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their dependent family members from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on reasonable basis, ICICI Securities, its subsidiaries and associated companies, their directors and employees (“ICICI Securities and affiliates”) are under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities is acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return of investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities and affiliates accept no liabilities for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities and its affiliates might have managed or co-managed a public offering for the subject company in the preceding twelve months. ICICI Securities and affiliates might have received compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of public offerings, corporate finance, investment banking or other advisory services in a merger or specific transaction. ICICI Securities and affiliates expect to receive compensation from the companies mentioned in the report within a period of three months following the date of publication of the research report for services in respect of public offerings, corporate finance, investment banking or other advisory services in a merger or specific transaction. It is confirmed that Abhishek Shindadkar research analysts and the authors of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months. Our research professionals are paid in part based on the profitability of ICICI Securities, which include earnings from Investment Banking and other business.

ICICI Securities or its subsidiaries collectively do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of the research report.

It is confirmed that Abhishek Shindadkar research analysts and the authors of this report or any of their family members does not serve as an officer, director or advisory board member of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. ICICI Securities and affiliates may act upon or make use of information contained in the report prior to the publication thereof.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.