macroeconomic & political dynamics agenda • economic and demand trends for 2016 • us...

TRANSCRIPT

Macroeconomic & Political Dynamics

Peter Morris, Chief Economist, Ascend

Macro Economics and Political Dynamics - 2016

Peter Morris Chief Economist Aviation Frontiers 2016 Dublin January 2016

3

Agenda • Economic and Demand Trends for 2016 • US Domestic Trends • Oil price and effects on the market • Aircraft orders • Global Risks 2015/16

4

Western Europe likely to see the weakest growth, Asia the strongest

5

Majority of regions expect slight improvement in 2016

EIU Dec 2015

6

Tourism - 2015 slightly better than 2014, with some significant regional variances

7

World Trade sees continued slow growth in 2015

Source: WTO

8

Overall, OECD lead indicators suggest stability. US a concern?

Source: OECD 2016

9

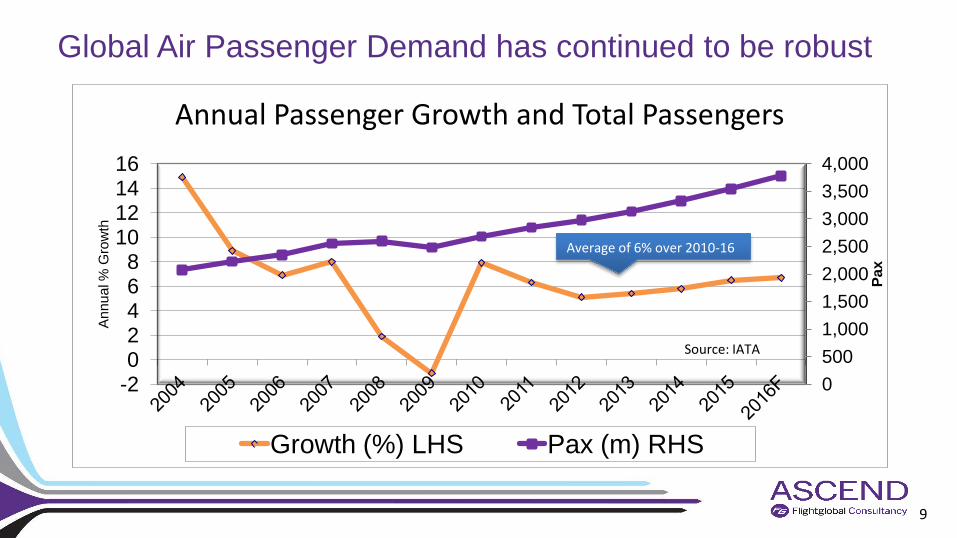

Global Air Passenger Demand has continued to be robust

0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000

-2 0 2 4 6 8

10 12 14 16

Pax

Annu

al %

Gro

wth

Annual Passenger Growth and Total Passengers

Growth (%) LHS Pax (m) RHS

Source: IATA

Average of 6% over 2010-16

10

Overall industry profits, margins solid since 2010

-1 0 1 2 3 4 5 6 7 8 9

-10 0

10 20 30 40 50 60 70

% M

argi

n

$Bn

Global Airline Profits and % (EBIT) Margin

Profit ($Bn) % margin

Source: IATA

11

Asia-Pacific (APAC) and Middle East (ME) continued to lead demand growth globally in 2015

Source – IATA, Year to Date to end November 2015, IATA Dec Forecast

0%

2%

4%

6%

8%

10%

12%

14%

16%

Africa Asia-Pacific Middle East Latin America North America

Europe Global 2015

Pre

dict

ed /

Actu

al G

row

th

Predicted Traffic Growth Predicted Capacity Growth Year to Date Traffic Year to Date Capacity

12

Traffic and Capacity expected to grow by 6-7% globally in 2016

Source – IATA

0%

2%

4%

6%

8%

10%

12%

14%

Africa Asia-Pacific Middle East Latin America North America

Europe Global

2016

Pre

dict

ed G

row

th

Predicted Traffic Growth Predicted Capacity Growth

13

The changing face of the industry – U.S. Consolidation

0

20

40

60

80

100

Airlines Flights(*10^4) Seats(*10^6) O-D pairs(*10)

Changes in the US Domestic Market 2005-2015

Aug-05 Aug-15

14

60 + airports lost domestic service

0

50

100

150

200

250

300

350

400

450

No flights < 10 flights 10-50 flights 50-100 flights 100-200 flights

200-350 flights

350-700 flights

700-1000 flights

> 1000 Fllights

Airp

orts

Distribution of US scheduled daily flight departures by airport 2005 vs 2015 (August)

2005 2015

In a decade, 21% fewer flights, and some major US airports have lost 50%+ of domestic service

Change in monthly departing scheduled flights (Top 10) 2015 vs 2005

SFO 3455 SEA 2812 DAL 2181 JFK 1855 CLT 1738 AUS 743 LAX 702 LKE 700 DCA 584 MIA 554

IAH -4173 -21% MSP -4414 -22% PIT -4702 -49% SLC -5090 -34%

DTW -5276 -26% ATL -5281 -13% CLE -5689 -57%

MEM -6456 -72% IAD -9595 -54% CVG -15606 -79%

Growth Decline

August Schedules, Innovata

16

How have oil prices played through?

•Dramatically falling oil price since 2014Q2

•Falling expectations on future oil prices

•Additional supply on horizon

Oil

•GDP stimulus for oil import countries, and overall

•Reduced inflation •Losers among ‘oil rent’

economies

GDP •Reduction in ticket price possible

•Hedging a factor •Exchange rate effects vs. $ •Competition level drives

speed of price change?

Price

•Increases in travel and

aircraft demand •Could be +2%/+4% extra

under certain scenarios •Big benefit for previously

marginal airlines •6.7% RPK growth 2015

Air Travel

17

A view from 2008

History lesson? There were dire predictions of the impact of fuel price on demand in 2008. While it was still a huge challenge, demand proved more robust, and supply costs more flexible than expected

19

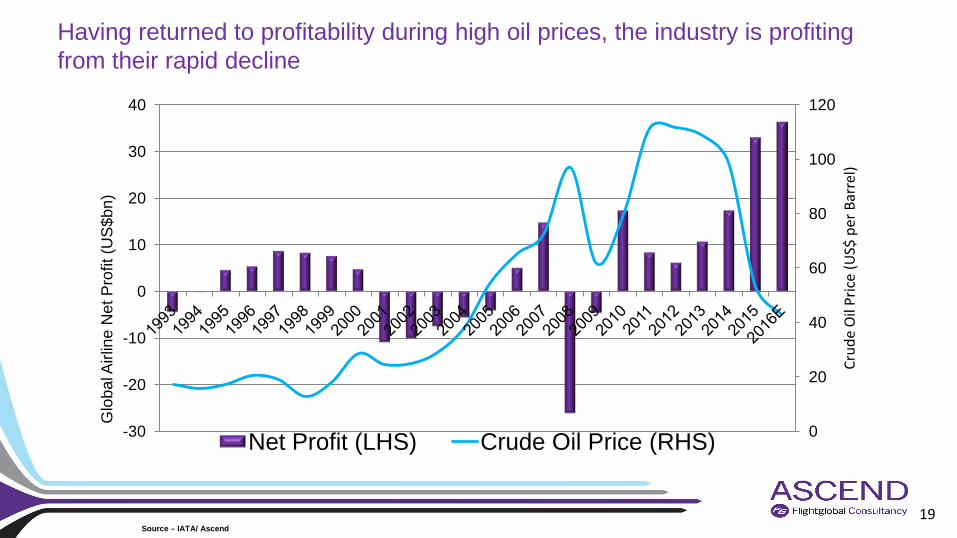

Having returned to profitability during high oil prices, the industry is profiting from their rapid decline

0

20

40

60

80

100

120

-30

-20

-10

0

10

20

30

40

Crud

e O

il Pr

ice

(US$

per

Bar

rel)

Glo

bal A

irlin

e N

et P

rofit

(US$

bn)

Net Profit (LHS) Crude Oil Price (RHS)

Source – IATA/ Ascend

20

70%+ Collapse of oil price in 18 months

21

Oil ‘Futures’ prices suggests only slow rebound - and have reduced dramatically since last year

Source: Barchart

0

20

40

60

80

100

Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 Jan-20

Future Brent Crude Price ($/Barrel) for Delivery 2016-20

At Jan 2015 At Jan 2016

22

Next generation lease rate premiums are sensitive to fuel price

23

Next generation fuel burn environmentally more efficient

Source – Ascend analysis of Airbus and Boeing data, 3,000nm sector

0

10

20

30

40

50

60

70

80

90

767-300ER 787-8 A330-300 A330-900neo

CO

2 em

issi

ons

(g p

er p

ax-k

m) -13%

-14%

24

Order volumes continue to be high

Source: Flightglobal Fleets Analyzer – orders for commercial customers only

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Com

mer

cial

jet o

rder

s

Jet Gross Orders Jet Net Orders

$123bn

$209bn

25

Commercial jet backlog at record high

Source: Flightglobal Fleets Analyzer & Ascend Values (2016$ Base Full Life Value)

0%

10%

20%

30%

40%

50%

60%

70%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

1990

19

91

1992

19

93

1994

19

95

1996

19

97

1998

19

99

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

11

2012

20

13

2014

20

15

Bac

klog

as

% o

f Fle

et

Com

mer

cial

Jet

Ord

er B

ackl

og

Backlog at Year End Backlog as % of Fleet

Backlog Value Now $960bn

26

Deliveries represent typically 6-8% of the global fleet

Source: Flightglobal Fleets Analyzer & Flightglobal Fleet Forecast

0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11%

0 200 400 600 800

1000 1200 1400 1600 1800 2000 2200

1990

19

91

1992

19

93

1994

19

95

1996

19

97

1998

19

99

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

11

2012

20

13

2014

20

15

2016

20

17

2018

20

19

2020

20

21

2022

20

23

2024

Del

iver

ies

as %

of F

leet

in S

ervi

ce

Pass

enge

r Airl

iner

Del

iver

ies

Deliveries / Forecast Deliveries Deliveries as % of Fleet in Service

27

Comparing take off - Widebody programme

0

200

400

600

800

1,000

1,200

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Year 11

A350 and 787 Cumulative Orders from First Year

787 A350

28

Comparing Take Off - Narrowbody Programmes

0 500

1,000 1,500 2,000 2,500 3,000 3,500 4,000

Year 1 Year 2 Year 3 Year 4 Year 5

A320neo and 737 Max Cumulative Orders from First Year

A320neo 737 Max

29

Trying to categorise and assess Global Risk

Source: World Economic Forum

30

Ratings for Likelihood and Impact of Global Risks

Source: Global Risks Survey 2015 World Economic Forum

31

Significant variance in risk factors by region

32

Heightened concerns on geopolitical issues and terrorism

Source: McKinsey, Dec 15

33

Caution in Developing Markets

Source: McKinsey, Dec 15

Summary

GDP growth continues (if weak) and cost structures under control Oil price continuing fall is a big plus for industry, and continues (for five years?) Global Traffic Demand 2016 will likely be higher than previously forecast, with local exceptions Various stakeholders will bid for a share of the ‘new’ profitability Aircraft demand strong, with a few ‘widows and orphans’ Current orders seem robust and younger/mid life aircraft more attractive Wider demand risk factors continue to fission

A final thought, after analysing the industry for 30 years

• Positive GDP Growth • Profitable Industry • Full Order Books • Possible 50% (and more) fuel cost decline • New aircraft technology coming on stream

36

Flightglobal and Ascend – Aviation Connected

Peter Morris Chief Economist +44 (0)20 8564 6790 [email protected]

The information contained in our databases and used in this presentation has been assembled from many sources, and whilst reasonable care has been taken to ensure accuracy, the information is supplied on the understanding that no legal liability whatsoever shall attach to Ascend Advisory, its offices, or employees in respect of any error or omission that may have occurred.