macro financial modeling: a private sector perspective on ... · private sector perspective on...

TRANSCRIPT

© 2016 CME Group. All rights reserved.

Macro Financial Modeling: A

Private Sector Perspective on

Research Challenges

Blu Putnam, Chief Economist & Managing Director,

CME Group, Inc.

June 2016

© 2016 CME Group. All rights reserved.

Investment advice is neither given nor intended

The research views

expressed herein

are those of the

author and do not

necessarily

represent the views

of CME Group or its

affiliates.

All examples in this

presentation are

hypothetical

interpretations of

situations and are

used for

explanation

purposes only.

This report and the

information herein

should not be

considered

investment advice

or the results of

actual market

experience.

2

© 2016 CME Group. All rights reserved.

Futures trading is not suitable for all investors, and involves the risk of loss. Futures are a leveraged investment, and because only a percentage of

a contract’s value is required to trade, it is possible to lose more than the amount of money deposited for a futures position. Therefore, traders

should only use funds that they can afford to lose without affecting their lifestyles. And only a portion of those funds should be devoted to any one

trade because they cannot expect to profit on every trade. All references to options refer to options on futures.

Swaps trading is not suitable for all investors, involves the risk of loss and should only be undertaken by investors who are ECPs within the

meaning of section 1(a)12 of the Commodity Exchange Act. Swaps are a leveraged investment, and because only a percentage of a contract’s

value is required to trade, it is possible to lose more than the amount of money deposited for a swaps position. Therefore, traders should only use

funds that they can afford to lose without affecting their lifestyles. And only a portion of those funds should be devoted to any one trade because

they cannot expect to profit on every trade.

Any research views expressed are those of the individual author and do not necessarily represent the views of the CME Group or its affiliates.

CME Group is a trademark of CME Group Inc. The Globe Logo, CME, Globex and Chicago Mercantile Exchange are trademarks of Chicago

Mercantile Exchange Inc. CBOT and the Chicago Board of Trade are trademarks of the Board of Trade of the City of Chicago, Inc. NYMEX, New

York Mercantile Exchange and ClearPort are registered trademarks of New York Mercantile Exchange, Inc. COMEX is a trademark of Commodity

Exchange, Inc. KCBOT, KCBT and Kansas City Board of Trade are trademarks of The Board of Trade of Kansas City, Missouri, Inc. All other

trademarks are the property of their respective owners.

The information within this presentation has been compiled by CME Group for general purposes only. CME Group assumes no responsibility for

any errors or omissions. Additionally, all examples in this presentation are hypothetical situations, used for explanation purposes only, and should

not be considered investment advice or the results of actual market experience.

All matters pertaining to rules and specifications herein are made subject to and are superseded by official Exchange rules. Current rules should be

consulted in all cases concerning contract specifications.

Copyright © 2015 CME Group. All rights reserved.

Disclaimer

© 2016 CME Group. All rights reserved.

Macro Financial Modeling: A Private Sector

Perspective on Research Challenges

Two Market-Based Case Studies

Interest Rates:

Why has unconventional monetary policy

failed to create inflation?

Does market liquidity matter for growth?

Energy:

What are the challenges when the dynamics

of supply and demand are being driven by

ever-changing technologies?

Weather matters, too.

© 2016 CME Group. All rights reserved.

Rates:

Why has unconventional Monetary Policy failed to create inflation

and

Does market liquidity matter for economic growth?

© 2016 CME Group. All rights reserved. 6

$0

$1

$2

$3

$4

$5

US$

Tri

llio

ns

Source: Federal Reserve Bank of St. Louis FRED Database

Composition of Federal Reserve Assets

Long-Term Treasuries

Short & Medium Term

Mortgage-BackedSecurities

Other

© 2016 CME Group. All rights reserved. 7

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1999 2001 2004 2006 2009 2011 2014

Euro

Bill

ion

s

Source: European Central Bank Monthly Bulletins, obtained through the Bloomberg Professional.

European Central Bank Assets

Securities & Govt Debt

Loans

Other

FX and Gold

© 2016 CME Group. All rights reserved. 8

¥0

¥50

¥100

¥150

¥200

¥250

¥300

¥350

¥400

¥450

Trill

ion

s o

f Ja

pan

ese

Ye

n

Source: Bank of Japan (www.boj.or.jp)

Bank of Japan Assets

Japanese Government Securities

Loans

© 2016 CME Group. All rights reserved. 9

-2%

-1%

0%

1%

2%

3%

4%

5%

Smo

oth

ed

(ex

po

ne

nta

il la

g) o

f Ye

ar-o

ver-

Year

Ge

ne

ral

Co

nsu

me

r P

rice

Infl

atio

n (

incl

ud

ing

sale

s ta

x in

cre

ase

s,

foo

d, e

ne

rgy,

etc

.)

Source: Bloomberg Professional (GRCP2000, JCPNGEN, CPI INDX)

Inflation Trends (Smoothed):US, Germany, and Japan

Japan

Germany

US

© 2016 CME Group. All rights reserved. 10

-3%

0%

3%

6%

9%

12%

19

49

19

53

19

57

19

61

19

65

19

69

19

73

19

77

19

81

19

85

19

89

19

93

19

97

20

01

20

05

20

09

20

13

20

17

Year

-ove

r-Ye

ar P

erc

en

tage

Ch

ange

Source: Federal Reserve Bank of St. Louis FRED Database (PCE, PCELFE). Estimates for Q2/16 - Q4/17 by CME Economics.

US Personal Consumption (PCE) Inflation

Since 1994, Core PCE Inflation has been between 1.0% and 2.4%, averaging 1.7%.

© 2016 CME Group. All rights reserved. 11

-2%

0%

2%

4%

6%

8%

10%

Source: Bloomberg Professional (GJGB10,USGG10YR,

10-Year Government Bond Yields

USGermany

Japan

© 2016 CME Group. All rights reserved. 12

-6%

-4%

-2%

0%

2%

4%

6%

-4% -2% 0% 2% 4% 6% 8%

De

gre

e o

f St

imu

lus

Nominal Interest Rate (Assuming 2% Inflation)

Source: CME Group, Strategic Intelligence & Analytics

Different Interpretations of Negative Rates

Negative Rates are a tax, discourage economic activity, and may be interpreted as a tigher policy -- Non-Linear Thinking

The more negative the nominal rates, the more the stimulus -- Linear Thinking

© 2016 CME Group. All rights reserved. 13

100

105

110

115

120

125

130

Jap

ane

se y

en

pe

r U

S d

olla

r

Source: Reuters (Japanese yen per USD spot FX).

Japanese Yen (vs USD) and the Bank of Japan's Negative Interest Rate Policy

The BoJ's negative rate surprise hit the yen for only 24 hours,then the yen strengthened.

Lower values indicate the yen is appreciating versus the US dollar.

© 2016 CME Group. All rights reserved. 14

0.90

1.00

1.10

1.20

US

do

llar

pe

r Eu

ro

Source: Reuters (USD per Euro Spot FX).

Euro and the European Central Bank's Negative Interest Rate Policy

The ECB's expansion of negative rates resulted in a stronger Euro vs USD.

Higher values indicate the Euro is appreciating versus the US dollar.

© 2016 CME Group. All rights reserved.

Citations Related to Quantitative Easing

Putnam, Bluford H. "Essential concepts necessary to consider when evaluating the efficacy of quantitative easing." Review of Financial Economics 22.1 (2013): 1-7.

Putnam, Bluford H., and Samantha Azzarello. "A Bayesian interpretation of the Federal Reserve's dual mandate and the Taylor Rule." Review of Financial Economics 21.3 (2012): 111-119.

Phillips, Susan M., and Putnam, Bluford H. “A Historical Perspective on the Different Origins of U.S. Financial Market Regulators, Journal of Financial Transformation, May 2016, pp. 86-91.

Putnam, Bluford H., “Evaluating different approaches to quantitative easing: lessons for the future of central banking”, Journal of Financial Perspectives, July 2014 | Volume 2 – Issue 2.

© 2016 CME Group. All rights reserved.

Energy:

What are the challenges when the dynamics of supply and demand are

being driven by ever-changing technologies and weather?

© 2016 CME Group. All rights reserved. 17

0

20

40

60

80

100

120

Pri

ces

Ind

exe

d t

o 3

0 J

un

e 2

01

5 =

10

0

Source: Bloomberg Professional (CL, HG, IO, Most Active Contract Prices)

Oil, Copper, Iron Ore:Finding Trading Ranges in H1/16;

Fears of Ever Lower Prices Dissipating?

Iron Ore

Copper

Oil

© 2016 CME Group. All rights reserved. 18

$0

$30

$60

$90

$120

$150

US$

Pri

ce p

er

Bar

rel

Source: Bloomberg Professional (CLA, COA)

WTI and Brent Crude Oil Prices

Brent

WTI

© 2016 CME Group. All rights reserved. 19

-$20

-$10

$0

$10

$20

$30

$40

US$

pe

r B

arre

l of

Cru

de

Oil

Source: Bloomberg Professional(Brent = EUCRBRDT, WTI = USCRWTIC)

Brent minus WTI Spot Price Spread

© 2016 CME Group. All rights reserved. 20

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

BTU

s o

f En

erg

y p

er

1 U

S D

olla

r

Source: Bloomberg Professional for prices (CL1, NG1), CME Economics Research for BTU conversion.

BTUs per US$1 by US Energy Source

US WTI Crude Oil

US Natural Gas

© 2016 CME Group. All rights reserved. 21

-1.00

-0.75

-0.50

-0.25

0.00

0.25

0.50

0.75

1.00

90

-day

Ro

llin

g C

orr

ela

tio

n o

f D

aily

Ret

urn

s

Source: Bloomberg Profressional.

Crude Oil vs Equities Rolling 90-Day Correlation

© 2016 CME Group. All rights reserved. 22

$0

$30

$60

$90

$120

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35

US$

pe

r b

arre

l of

Oil

Futures Price Number of Months into the FutureSource: Bloomberg Professional (CL <Comdty>)

WTI Crude Oil Futures Maturity Curves

30 June 2014

11 October 2014

31 December 2014

30 October 2015

26 February 2016

© 2016 CME Group. All rights reserved.

There was no El Niño back in February 2015

© 2016 CME Group. All rights reserved.

El Niño built quickly and peaked in Q3 2015

© 2016 CME Group. All rights reserved.

El Niño started to fade – March 2016

© 2016 CME Group. All rights reserved.

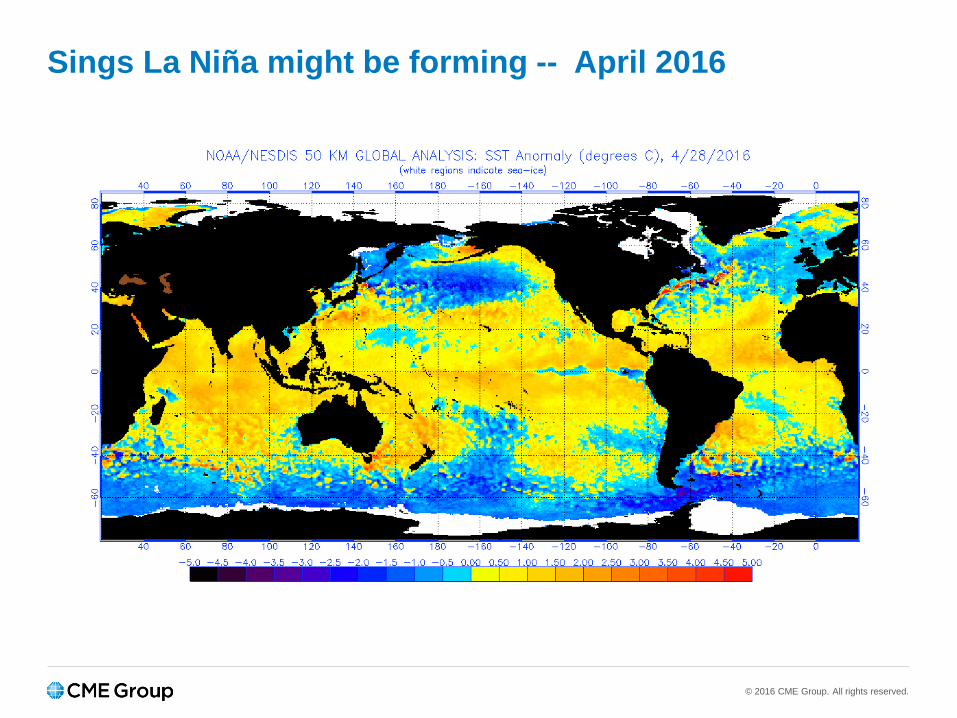

Sings La Niña might be forming -- April 2016

© 2016 CME Group. All rights reserved.

La Niña appears to be forming -- June 2016

© 2016 CME Group. All rights reserved. 28

-1500

-1000

-500

0

500

1000

1500

52

We

ek

Ch

ange

Bill

ion

s o

f C

ub

ic F

eet

Natural Gas Storage: Year on Year Change

Source: Bloomberg Professional (DOENUST1) with CME Group Economic Research Calculations

1997-98 El Niño Inventory Build

1999-00 La Niña Inventory Drawdown

2015-16 El Niño Inventory Build

© 2016 CME Group. All rights reserved. 29

0

2

4

6

8

10

12

Jan-99 Apr-99 Jul-99 Oct-99 Jan-00 Apr-00 Jul-00 Oct-00

USD

/ M

MB

tuNatural Gas: 1st Nearby Contract Price

Source: Bloomberg Professional (NG1)

© 2016 CME Group. All rights reserved.

Observations from the Practitioner Perspective

Forecasting or Hypothesis Testing:

Practitioners cannot mix past with future data

Pattern Instability:

Dynamic, time-varying probabilistic tools required

When long-term evolution intersects

short-run dynamics -- demographics

Big Data, Small Data, Limited Data:

Appropriate statistical tools for data frequency

Robust theoretical foundation:

Assumptions matter

Institutions and regulations matter

Judgment with quantitative discipline (JQD)

© 2016 CME Group. All rights reserved.

Citations Related to Dynamic Portfolio Risk

Assessment & Portfolio Construction

Quintana, Jose M., and Putnam, Bluford H. “Multivariate Dynamic Models for Financial Time Series: Is the Whole Greater than the Sum of its Parts?”, American Statistical Association 1997 Proceedings of the Section on Bayesian Statistical Science. 1997, pp. 245-250.

Putnam, Bluford H. "Volatility expectations in an era of dissonance", Review of Futures Markets. 2012. March.

Putnam, Bluford H., Global Commodities Applied Research Digest, "Oil Market Dynamics and 2016 Outlook," Research Council Corner, Vol. 1, No. 1, Spring, 2016.