looking to the future - tisa - tax incentivised … · looking to the future 10th june 2009 1...

TRANSCRIPT

Looking to the Future 10th June 2009

1

Looking to the Future

“My Personal View of the Range of Impacts”Robert Gardner, Founder & Co‐CEO

29

10th June 2009

Looking to the Future

The Three Pillars of Pension Provision

State

• Social Security systems

Final Salary

• Employer‐sponsored

Personal

• Additional voluntarySocial Security systems provided through government taxes. This can either be on a funded basis (where funds are ring‐fenced to pay out future benefits) or on a pay‐as‐you‐go basis where benefits are paid for using

Employer sponsored defined benefit and defined contribution schemes. Typically, employers will make some contributions in the form of ‘deferred salary’. In some countries employer contributions may be

Additional voluntary contributions may be amassed through the growth of defined contribution schemes. These plans typically provide some tax benefits of contributions. Important implications

30

are paid for using current tax revenues. Benefits will be subject to a minimum retirement age.

contributions may be mandatory.

Important implications for individuals in managing these assets (i.e. investment risk and longevity risk).

Looking to the Future 10th June 2009

2

“Isn't it interesting that the same people who laugh at science fiction listen to weather forecasts and economists?” – Kelvin Throop III

Looking to the Future

Timeline: 1997‐2009

“Under this Government,

"I believe that the general growth in large [fi i l] i tit ti

“These problems...are unprecedented We

1997/1998

Asian Crisis

Russian Financial

Crisis

1995-2001

Dotcom Bubble

2000-2003

Dotcom Bubble Crash

2003-2007

Steady Growth

2007-2008

Credit Crunch

2009-

Go e e ,Britain will not return to the boom and bust of the past.” –HM Treasury, Budget 2000

[financial] institutions have occurred in...markets in which many of the larger risks are dramatically -- I should say, fully --hedged.“ – Alan Greenspan, Chairman of the Federal Reserve (2000)

unprecedented… We will not and must not relax our efforts to move this economy through the downturn back to a period of growth.” – Gordon Brown, Prime Minister (2009)

Looking into the Future

Final Salary in Long‐Term Run‐Off

2 June 2009

32

Looking to the Future 10th June 2009

3

“New Perspectives on Investment & Longevity”

Risks Facing Pensions Schemes

Sponsor Covenant

Risks

Asset Risks

• Equity Market Risk

Liability Risks

33

• Duration Mis‐Match• Credit• Property• Liquidity•Reinvestment• Counterparty

• Interest Rates

• Inflation

• Longevity/Mortality

Looking to the Future

Risks Facing Pensions Schemes

• VaR provides a single amount (the value) which

• How well equipped (or not) a portfolio may be to

• Determines how a portfolio rises or falls with respect toamount (the value) which

one might expect to lose (at risk) in a reasonable “worst case” scenario, i.e. in one year’s time.

portfolio may be to withstand sudden and severe jolts or sustained market dislocations.

rises or falls with respect to micro and macro changes in long term interest rates and long term inflation expectations.

34

Looking to the Future 10th June 2009

4

Example ALM Risk Management

Risk Telescope

40000

Cashflow Structure for Pensioner

10000

15000

20000

25000

30000

35000

Annual Pension Paym

ent (£)

Inflation Risk

?Longevity

35

0

5000

2009 2012 2015 2018 2021 2024 2027 2030

Nominal Inflation

Risk

Example ALM Risk Management

Risk Telescope

80

lions

Cashflow Structure for Pension Scheme by Member Type

20

30

40

50

60

70

£ M

ill

36

0

10

20

2009 2019 2029 2039 2049 2059 2069 2079 2089 2099

Actives Deferreds Pensioners

Looking to the Future 10th June 2009

5

Example ALM Risk Management

Risk Telescope

140

Millions

Cashflow Structure for Pension Scheme under Different Inflation Assumptions

40

60

80

100

120

£

Inflation Risk

37

0

20

2009 2019 2029 2039 2049 2059 2069 2079 2089 2099 2109

Inflation 5% inflation 4% Inflation 3%

Example ALM Risk Management

Risk Telescope

30000

Cashflow Structure for PPP/PFI

Inflation

5000

10000

15000

20000

25000

Annual Cashflow (£ million)

Nominal Matching Pension liability Cashflow

38

0

1 4 7 10 13 16 19 22 25

Lease

Looking to the Future 10th June 2009

6

Example ALM Risk Management

Risk Telescope

Existing Mechanism 2005‐2008

PPP / PFI 20000

25000

30000

(£ million)

Cashflow Structure for PPP/PFI

Inflation

Nominal LDI FundRPI

Fixed/Projects

0

5000

10000

15000

1 4 7 10 13 16 19 22 25

Annua

l Cashflow (

Lease

Financing

Pension Fund

Fixed

Libor

Fixed

Swap out RPIConsortium of Banks

39

Receive Fixed

Example ALM Risk Management

Risk Telescope

New Model?

15000

20000

25000

30000

hflow (£

million)

Cashflow Structure for PPP/PFI

Inflation

Nominal

Benefits to Pension

Fund:PPP / PFI P j t

0

5000

10000

1 4 7 10 13 16 19 22 25

Annu

al Cash

Lease

Pension Fund

£ 100m

Finance

• Long dated rates

• Inflation

• Return

• But with credit risk

Issues:

concentration/

Projects

Primary School

Pension Funds

40

£ 100m diversification risk

Fund Gallery

Hospital

Pension Funds

Funds

Pension Funds

Looking to the Future 10th June 2009

7

Longevity Facts

• Life expectancy is increasing 5 hours a day. 25

Increase in Life Expectancy65 year old in England & Wales

Looking to the Future

Risks Facing Pensions Schemes

• The average life expectancy used by FTSE100 DB pension schemes for a 60 yr old man is 15.5 years.

• The Pension Protection Fund (PPF)’s latest S143 and S179 valuation assumptions set life expectancy for a 60yr old man as 16.8 years.

• “Each year of extra life adds about 3‐4% to i h li biliti ”

0

5

10

15

20

Lif

e E

xpec

tan

cypension scheme liabilities.” (TPR 2006 Norgrovespeech)

0

1920 1940 1960 1980 2000

Male Female

41

What is Longevity Risk?

• Jeanne Louise Calment is the oldest person on record, living for 122 years and 164 days. (Feb. 21, 1875 – Aug. 4, 1997)

Introduction to Longevity

Facts

Jeanne Louise Calmenton her 119th birthday.

• At the age of 90, Jeanne signed a deal to sell her apartment to a man named Raffray, then aged 47, who agreed to pay a monthly sum until she died (reverse mortgage).

• Big mistake by Raffray. Jeane Calment refused to die and he had to make mortgage payments for 30 years. He never moved into the apartment.

• Raffray himself died in Dec 1995, leaving his widow to continue the

Source: The New York Times

payments for twenty more months.

• That is Longevity Risk.

42

Looking to the Future 10th June 2009

8

2000

• In 2007 the Anniversaries Office sent almost 50002031

Introduction to Longevity

Facts

What is Longevity Risk?

1917 King George V sends the first centenarian

telegram.

1952 Queen Elizabeth II sends out her first

telegram

2000 Queen Mother

receives telegram from her daughter

VS

sent almost 5000 birthday cards to centenarians.

• It is estimated that by 2031 there will be 40,000 people turning 100 years old.

• 2031 ‐Will the Queen be issuing a

1977 Queen Elizabeth II Silver Jubilee. More than 1000 telegrams are being sent

every year

2031

40,000+

Queen be issuing a letter to Prince Charles when he is 100 years old?

24 250+ 1000+3600+

43

Alec Holden’s Hedge

• Mr. Alec Holden placed a bet of £100 for himself to live older than 100 on 10 December 1997 when he was 90 years old.

Alternative Solutions

Longevity Hedging Solutions

y

• The bookmaker William Hill accepted the bet and gave him an odds of 250/1.

• On 24th April 2007, he celebrated his 100thbirthday with a cheque for £25,000 (tax‐free) and a birthday card from the Queen.

“The first 1000‐year‐old is probably only ~ 10 years younger than the first 150‐year‐old”

‐‐‐‐‐Aubrey de Grey

44

Looking to the Future 10th June 2009

9

• Governance 2 0

Looking to the Future

Upgrade Governance

• Community

• Governance 1.0

• Governance 2.0

45

The Future of Retirement

'It's Time to Prepare'

“The world’s population of over 65s set to increase from 550 milliontoday to over 1.4 billion by 2050”

This material shows the type of analysis which Redington can undertake to monitor a schemes assets and liabilities. You should not rely upon any of the calculations or numbers shown in this presentation as they are for illustration purposes only.

46

Source: HSBC Insurance 2009

Looking to the Future 10th June 2009

10

Future of Retirement

'It's Time to Prepare'

47

Source: HSBC Insurance 2009

Future of Retirement

'It's Time to Prepare'

Increase Contributions

Reduce Eligibility

Reduce the value of the pension benefits

Work longer/phased retirement

Tax more

Save more

The Future of Retirement findings show that families in Europe and North America prefer to save

The Future of Retirement findings show that families in Asian societies prefer to work longer (i.e.

48

benefits America prefer to save more (i.e. increase their contributions). There is relatively little support to increase contributionsthrough tax‐funded means.

reduce their entitlements).

Source: HSBC Insurance 2009

Looking to the Future 10th June 2009

11

Longevity

Generation Y

This material shows the type of analysis which Redington can undertake to monitor a schemes assets and liabilities. You should not rely upon any of the calculations or numbers shown in this presentation as they are for illustration purposes only.

49

Who is… What is… Generation Y?

Living Longer – at What Price?

Generation Y

50

Looking to the Future 10th June 2009

12

“Generation Y is the generation born between 1981 and 2000. They are the largest of the four generations currently in the workforce, and they

Understanding Generation Y

The Basics

g y , yhave been tagged as the next “civic” generation –poised to be the next great institution builders.

“The media often paints Generation Y in a negative light – citing high job turnover and impatience with paying dues as negative Gen Y traits. But we know better. We know that Generation Y does not want to job‐hop every two years; we know that Generation Y will be the most productive generation in the history of the workforce and we know that the single best wayworkforce, and we know that the single best way to connect with Generation Y is to meet them on their turf – online.”

51

Generational traits at work and home

Boomer Gen X Gen Y

Living Longer – at What Price?

Generation Y

Born 1946‐1961

• Now aged 47‐62

• Idealistic, career‐orientated, consumerist

• Promoted ‘young’ and propped

Born 1961‐1976

•Now aged 32‐47

•Realists, cynical

•Held back by “old fart log‐jam”

• Peak income earning 2006‐2021

Born 1976‐1991

•Now aged 17‐32

• Experiential, ethicists, uncommitted to career, relationships

•Helicopter kids; KIPPERS*

• Peak income earning 2021

Boomer Gen X Gen Y

• Peak income earning 1991‐2005

• Succession planning, advisory boards, non‐exec. directors.

2021

•Resentful of Boomer focus on Ys in the office; sandwich gen.

•Must deal with baby boomers in retirement.

• Peak income earning 2021‐2036

• Technology savvy; global thinking

• Inherit boomer wealth.

• *‘Kippers’ stands for ‘Kids In Parents Pockets Eroding Retirement Savings’.

Source: KPMG 52

Looking to the Future 10th June 2009

13

Changing life expectancy creates the concept of a ‘working life’ followed by ‘retirement’

Gen Y ‘Wealth’

Living Longer – at What Price?

Generation Y

Source: UN Statistics Division; KPMG 53

Average annual income per person by single year in UK

Living Longer – at What Price?

Generation Y

Source: HM Revenue and Customs Statistics, Survey of Personal Incomes 2004/5; KPMG

54

Looking to the Future 10th June 2009

14

Is Retirement a 20th Century Concept?

As life expectancy continues to increase, so too does the demand for a funded retirement. A pension plan developed from youth and nurtured throughout middle age must support a lifestyle for up to 20 years beyond retirement

Living Longer – at What Price?

Generation Y

Life Expectancy at birth (years)

Japan 81.9

Hong Kong 81.5

Switzerland 80.5

Australia 80.2

A Japanese child born in 2005 can expect (ceteris paribus) a lifespan of 81.9 years: 78 for men and 85 for woman.

for up to 20 years beyond retirement.

Source: KPMG: ‘Generation Y – beyond the baby boomers’

Sweden 80.1

Source: UN Population Database, 2007

55

Lifestyle Trend Reshaped by Demographic Change

Top five shift in age at first marriage (years)

• “First time” marriages postponed – average age in theUK is now approaching 30.

Living Longer – at What Price?

Generation Y

(years)

1980 2005 Change

United Kingdom 22.9 29.5 6.6

New Zealand 21.7 28.1 6.4

Germany 23.2 29.6 6.4

Australia 21.9 28.0 6.1

France 23.0 29.1 6.1

• The postponement of marriage is matched in manydeveloped countries by a scaling back in the number ofchildren per couple.

• This has had a “knock on” effect on the transition intothe types of financial responsibilities associated withasset and family protection:

• Purchase and insurance of property• Pension plan (DB/DC)• Pension plan (DB/DC).

Source: KPMG: ‘Generation Y – beyond the baby boomers’

Source: UN Population Database, 2007

56

Looking to the Future 10th June 2009

15

Top five fall in fertility rate

Lifestyle Trend Reshaped by Demographic Change

• In the latter decades of the 20th century fertility rates have declined in most countries.

Living Longer – at What Price?

Generation Y

Top five fall in fertility rate (number of children per woman)

1975 2005

Singapore 2.6 1.4

Italy 2.3 1.3

New Zealand 2.8 2

Japan 2.1 1.3

Australia 2.5 1.8

• An exception to this is in the US, where fertility is on the rise due in part to the values of the Latino population.

• Women and men are marrying later in life and having fewer children (in most developed nations).

Source: UN Population Database 2007

• This shift has changed the experience of 20‐something youth between the boomer and Gen Y.

Source: KPMG: ‘Generation Y – beyond the baby boomers’

Source: UN Population Database, 2007 • The boomers required commitment to support relationships and households

• Gen Y are freed of these commitments in their youth.

57

Is Retirement a 20th Century Concept?

Living Longer – at What Price?

Implications of Generation Y

• Life expectancy in the UK exceeded 65 for the first time in 1946.

The Voice of Generation Y

• By 2005 those aged 65 in that year could expect to live a further 18.7 years.

• It was assumed that expenditure in retirement would be lower .

• Between 1971 and 2000, the average age of first births for married couples increased from 24 to nearly 30.

• Parents are still be receiving calls/texts

58

• Parents are still be receiving calls/texts from their children for a ‘spare £100 for a windsurfing course’ well into their sixties.

• The investment implications are only now starting to sink in.

Source: KPMG

Looking to the Future 10th June 2009

16

Is Retirement a 20th Century Concept?

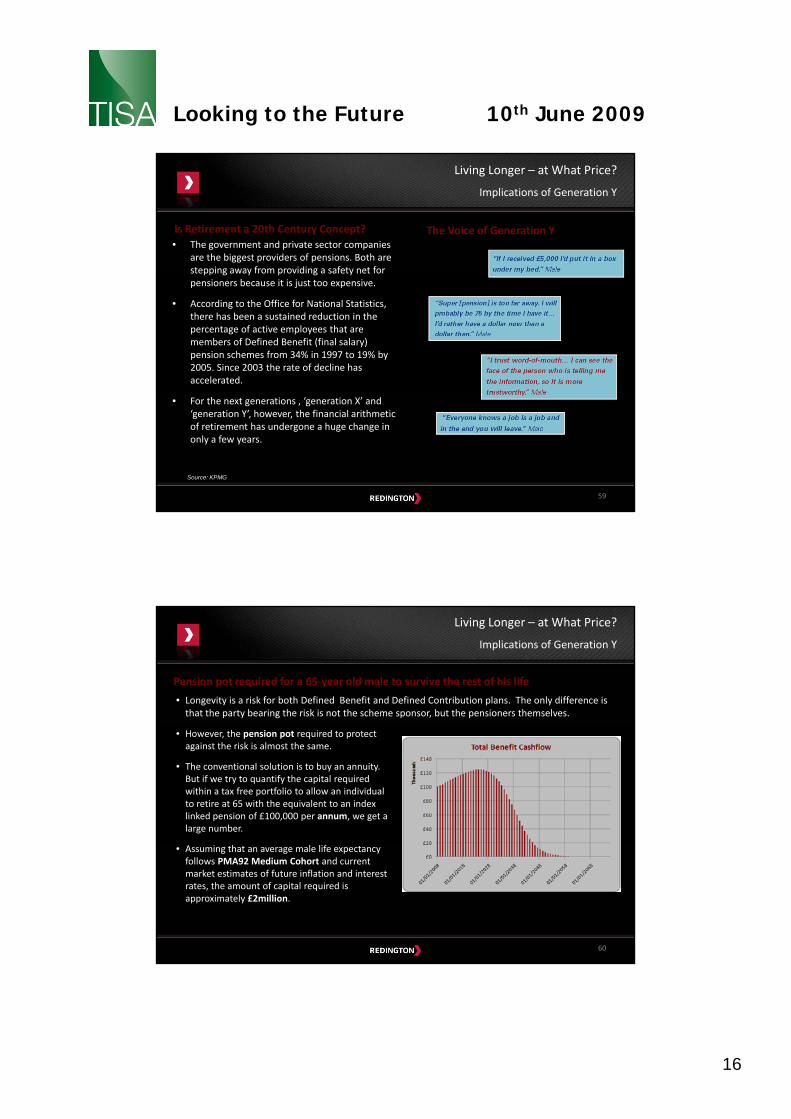

• The government and private sector companies are the biggest providers of pensions. Both are stepping away from providing a safety net for

Living Longer – at What Price?

Implications of Generation Y

The Voice of Generation Y

stepping away from providing a safety net for pensioners because it is just too expensive.

• According to the Office for National Statistics, there has been a sustained reduction in the percentage of active employees that are members of Defined Benefit (final salary) pension schemes from 34% in 1997 to 19% by 2005. Since 2003 the rate of decline has accelerated.

• For the next generations , ‘generation X’ and ‘generation Y’, however, the financial arithmetic of retirement has undergone a huge change in only a few years.

59

Source: KPMG

Pension pot required for a 65‐year old male to survive the rest of his life

Living Longer – at What Price?

Implications of Generation Y

• Longevity is a risk for both Defined Benefit and Defined Contribution plans. The only difference is that the party bearing the risk is not the scheme sponsor, but the pensioners themselves.

• However, the pension pot required to protect against the risk is almost the same.

• The conventional solution is to buy an annuity. But if we try to quantify the capital required within a tax free portfolio to allow an individual to retire at 65 with the equivalent to an index linked pension of £100,000 per annum, we get a large number.

• Assuming that an average male life expectancy follows PMA92 Medium Cohort and current market estimates of future inflation and interest rates, the amount of capital required is approximately £2million.

60

Looking to the Future 10th June 2009

17

Is Retirement a 20th Century Concept?

• The implications for investment policy are clear:

• Long term planning and a concerted effort to

Living Longer – at What Price?

Implications of Generation Y

save will be required in order to create a reserve capable of generating sufficient revenue to maintain living standards.

• Continued investment is needed for growth of capital and income for many years past retirement.

• With the increase in longevity, this means that risk should be reduced over a 20‐30 year period and not just at 65period and not just at 65.

• A new approach is needed with respect to asset allocation based around “Life Styling”.

61

“Falling markets have left some investments in defined contribution schemes worth less than the cash contributions made into them, PricewaterhouseCoopers says.”

‐Professional Pensions, 4 March 2009

• Japanese children taught about pensions and saving

Living Longer – at What Price?

Early Years Education

It is never too young to start learning

about pensions and saving for retirement from an early age (11 – 18)

• Lessons given by local municipality officials under Personal Health and Social Education (PHSE)

• Sessions not limited to schoolchildren

• All nationals between 20 –59 are required to en‐roll in the national pension plan.

Looking to the Future 10th June 2009

18

Direct Line: +44 (0) 20 7250 3416Telephone: +44 (0) 20 7250 3331

Redington13-15 Mallow StreetLondon EC1Y 8RD

Looking to the Future

My Personal view of the range of impacts

Disclaimer For professional investors only. Not suitable for private customers.

The information herein was obtained from various sources. We do not guarantee every aspect of its accuracy. The information is for your private information and is for discussionpurposes only. A variety of market factors and assumptions may affect this analysis, and this analysis does not reflect all possible loss scenarios. There is no certainty that theparameters and assumptions used in this analysis can be duplicated with actual trades. Any historical exchange rates, interest rates or other reference rates or prices which appear

Robert GardnerFounder &Co-CEO

THE DESTINATION FOR ASSET & LIABILITY MANAGEMENT

parameters and assumptions used in this analysis can be duplicated with actual trades. Any historical exchange rates, interest rates or other reference rates or prices which appearabove are not necessarily indicative of future exchange rates, interest rates, or other reference rates or prices. Neither the information, recommendations or opinions expressedherein constitutes an offer to buy or sell any securities, futures, options, or investment products on your behalf. Unless otherwise stated, any pricing information in this message isindicative only, is subject to change and is not an offer to transact. Where relevant, the price quoted is exclusive of tax and delivery costs. Any reference to the terms of executedtransactions should be treated as preliminary and subject to further due diligence .

Please note, the accurate calculation of the liability profile used as the basis for implementing any capital markets transactions is the sole responsibility of the Trustees' actuarialadvisors. Redington Ltd will estimate the liabilities if required but will not be held responsible for any loss or damage howsoever sustained as a result of inaccuracies in thatestimation. Additionally, the client recognizes that Redington Ltd does not owe any party a duty of care in this respect.

Redington Ltd are investment consultants regulated by the Financial Services Authority. We do not advise on all implications of the transactions described herein. This informationis for discussion purposes and prior to undertaking any trade, you should also discuss with your professional tax, accounting and / or other relevant advisers how such particulartrade(s) affect you. All analysis (whether in respect of tax, accounting, law or of any other nature), should be treated as illustrative only and not relied upon as accurate.