literature review on corporate social responsibility 1980-2014 literature review 1980 to... ·...

TRANSCRIPT

Literature Review on

Corporate Social Responsibility

1980-2014

School of Accounting and Finance

1

Scope of Review

• I did a survey on the articles published in the top 15 journals and

related 5 top-ranked journals whose title or keywords contain the

word “corporate social responsibility (CSR)” during 1980 to March

2015.

• I also collected articles which are relevant to this topic through

“citation pearl growing” method.

• Literature Collection:

• Identify a set of core references as initial.

• Based on these first wave of searches looks for articles where this core

literature has been cited.

• The next wave looks for articles where those indentified and included

from the first wave have been cited.

2

Scope of Review

• Corporate social responsibility related articles appear most in

management journals, for example, there have been about

310 papers on CSR(included in title) in Journal of Business

Ethics since 1982, 90% of which were published after 2000.

• Key methods and findings of each typical paper (selected) are

highlighted in one slide, with an objective to uncover critical

knowledge gaps, understand research trends and provide

clear and specific directions for future research.

3

Scope of Review

4

Selected Journals Used for Article Search

Accounting Journal Finance Journal Management and

Economics Journal Other Journals

Accounting Review Journal of Finance Management Science

Accounting,

Organization, and

Society

Journal of Accounting

and Economics

Journal of Financial

Economics

American Economic

Review

Journal of Accounting,

Auditing, and Finance

Journal of Accounting

Research

Journal of Financial

and Quantitative

Analysis

Quarterly Journal of

Economics

Journal of Accounting

and Public Policy

Contemporary

Accounting Research

Review of Financial

Studies

Journal of Political

Economy

Journal of Business

Ethics

Review of Accounting

Studies

Journal of Corporate

Finance

Review of Economic

Studies

Journal of Banking

&Finance

5

Distribution of published papers by journal

0

2

4

6

8

10

12

14

16

18

6

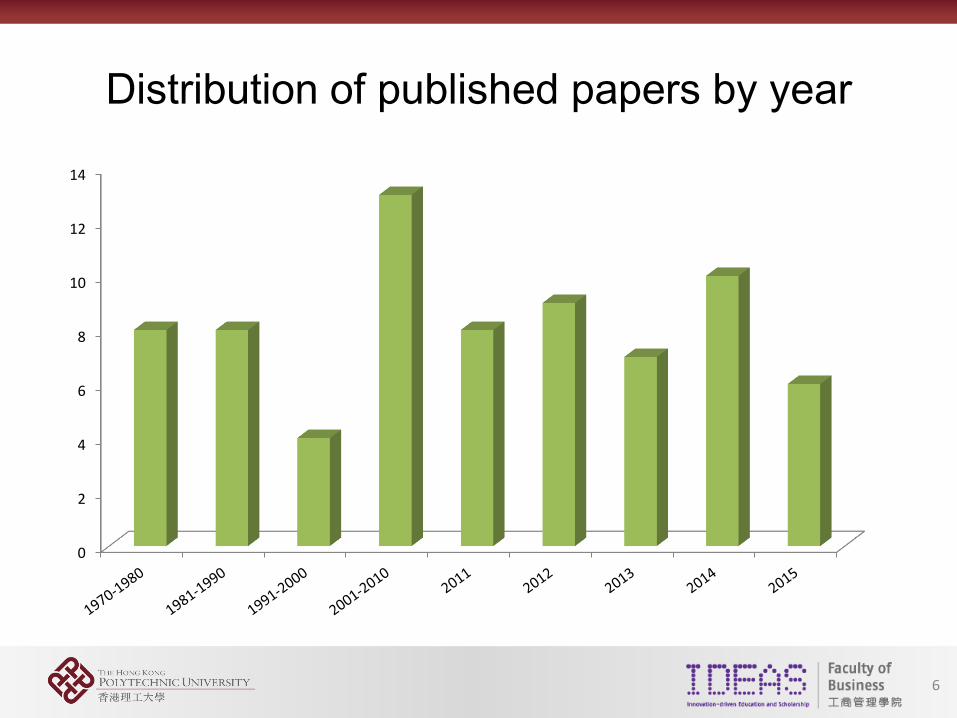

Distribution of published papers by year

0

2

4

6

8

10

12

14

7

Distribution of published papers in JBE by year

0

5

10

15

20

25

30

35

40

45

The Accounting Review

8

9

• Concentrate on developing a theoretical framework consisting of a proposed set of

social accounting objectives, concepts, measurement methods and reporting

standards.

• Objectives of corporate social accounting: identify and measure the periodic net

social contribution of an individual firm; help determine whether an individual firm’s

strategies and practices are consistent with social priorities and legitimate aspirations;

make relevant information in an optimal manner to all social constituents.

10

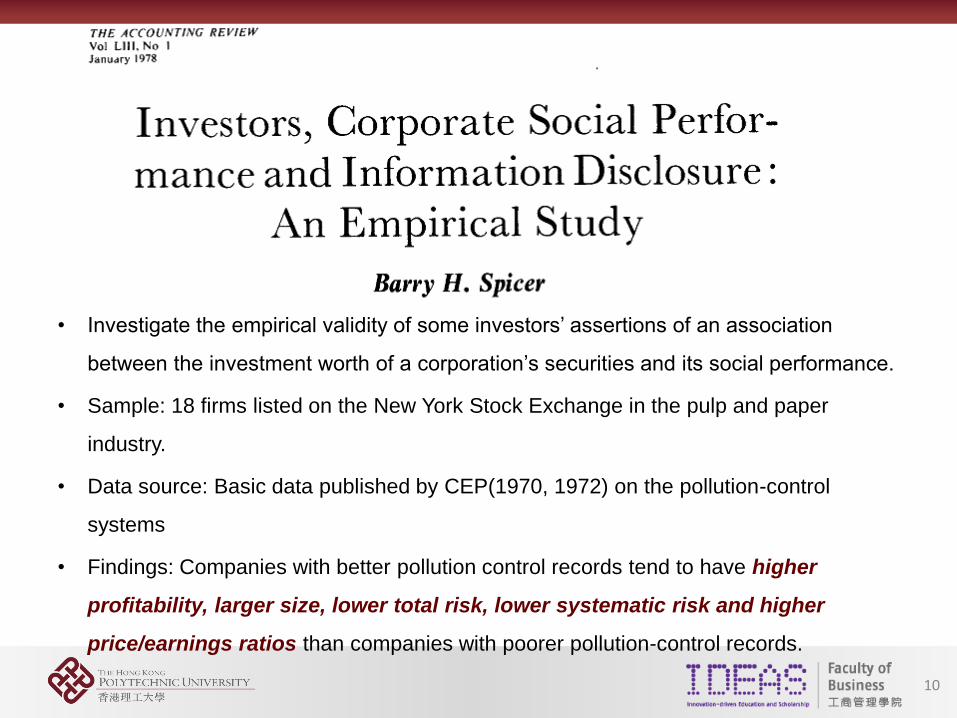

• Investigate the empirical validity of some investors’ assertions of an association

between the investment worth of a corporation’s securities and its social performance.

• Sample: 18 firms listed on the New York Stock Exchange in the pulp and paper

industry.

• Data source: Basic data published by CEP(1970, 1972) on the pollution-control

systems

• Findings: Companies with better pollution control records tend to have higher

profitability, larger size, lower total risk, lower systematic risk and higher

price/earnings ratios than companies with poorer pollution-control records.

11

• Examine potential demand by university investors for information on corporate

activities in nine selected areas of social concern through mailing a questionnaire to a

random sample of 500 university CFO.

• Nine social items of information: Improper or illegal business or political practices,

Equal opportunity employment practices, Sale of tobacco or alcoholic beverages,

Sales of products potentially hazardous to human health or safety, Pollution of the

environment, Business activities in countries with limited civil rights, Nonpollution-

related environmental issues, Sale of military equipment and Charitable contributions.

• Findings: The university investor may not be a strong source of demand for

information about social responsibility.

12

• Analyze the impact on the capital markets of voluntary social disclosure.

• Social disclosure: A firm’s community involvement, human resource, environmental

impact, and product/service contributions.

• Research Method: Based on CAPM, they form the equivalent (systematic) risk

portfolios using the common equity securities of socially disclosing firms and the

common equity securities of non-disclosing firms. The mean returns of the portfolios

are then compared over two six-month periods (pre- and post-fiscal-year-end).

• Sample: 1972 annual reports of Fortune 500 firms whose common equity securities

are traded on the New York Stock Exchange. Finally, 201 disclosing and 113 non-

disclosing firms satisfied.

• Findings: Social disclosure has information content and that the market values this

disclosure positively.

13

• Investigate whether security price movements are associated with the release of externally

produced information about companies’ performances in the pollution area.

• The source of the externally produced information is the Council on Economic

Priorities(CEP) , and the sample firms were included in both the initial and follow-up

reports of the eight studies conducted by CEP from 1970 to 1977 in four industries in the

U.S.

• Findings: (1) CEP firms experienced relatively large negative abnormal returns on the two

days immediately prior to newspaper reports on the release of the CEP studies. (2)

Investors use the information to discriminate between companies with different pollution-

control performance records.

14

• Explore why companies producing sustainability reports have this information voluntarily

assured and their choice of assurance provider.

• Sustainability reports are collected from Corporate Register covering the period 2002-

2004 across 31 countries.

• A sequential logit model: Assurance/Provider=f(legal, industry, stakeholder, control

variables)

• Findings: (1)The incidence of assurance of sustainability reports is higher for companies

with a greater need to enhance credibility. (2) The companies in stakeholder countries

are more likely to have their sustainability reports assured. (3) Companies from

stakeholder-orientated countries being more likely to choose a member of the auditing

profession as their assurance provider.

Roger Simnett, Ann Vanstraelen, and Wai Fong Chua

15

• Examine a potential benefit associated with the initiation of voluntary disclosure of corporate

social responsibility CSR activities: a reduction in firms’ cost of equity capital.

• Employ a sample of firms that intersect two CSR data sources: (1) a comprehensive list of

firms releasing electronic or hard-copy standalone CSR reports since 1993, collected from

various sources on the Internet; and (2) the KLD STATS database that provides detailed CSR

performance ratings for individual firms.

• Findings: (1)Firms with a high cost of equity capital in the previous year tend to initiate

disclosure of CSR activities in the current year and that initiating firms with superior social

responsibility performance enjoy a subsequent reduction in the cost of equity capital. (2)

Initiating firms are more likely than non-initiating firms to raise equity capital following the

initiations; among firms raising equity capital, initiating firms raise a significantly larger amount

than do non-initiating firms.

Dan S. Dhaliwal, Oliver Zhen Li, Albert Tsang, and Yong George Yang

16

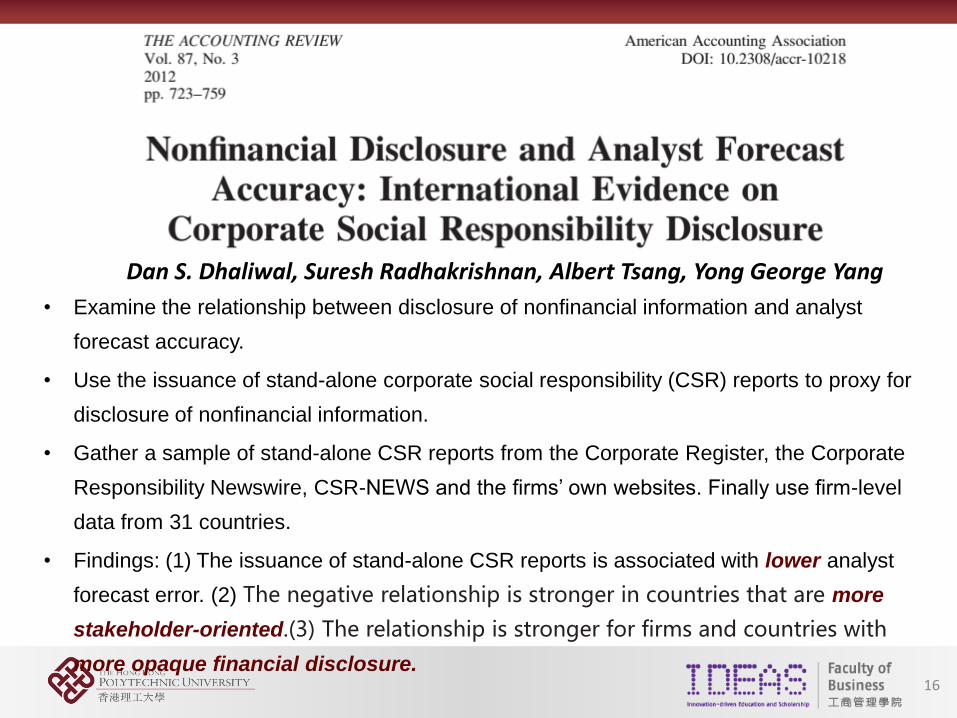

• Examine the relationship between disclosure of nonfinancial information and analyst

forecast accuracy.

• Use the issuance of stand-alone corporate social responsibility (CSR) reports to proxy for

disclosure of nonfinancial information.

• Gather a sample of stand-alone CSR reports from the Corporate Register, the Corporate

Responsibility Newswire, CSR-NEWS and the firms’ own websites. Finally use firm-level

data from 31 countries.

• Findings: (1) The issuance of stand-alone CSR reports is associated with lower analyst

forecast error. (2) The negative relationship is stronger in countries that are more

stakeholder-oriented.(3) The relationship is stronger for firms and countries with

more opaque financial disclosure.

Dan S. Dhaliwal, Suresh Radhakrishnan, Albert Tsang, Yong George Yang

17

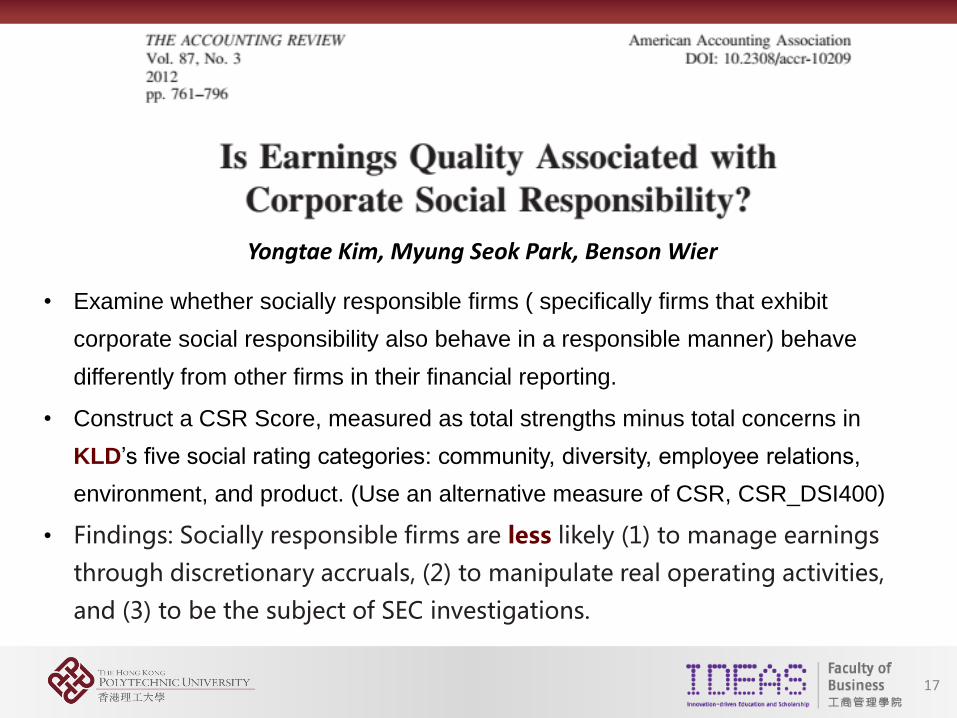

• Examine whether socially responsible firms ( specifically firms that exhibit

corporate social responsibility also behave in a responsible manner) behave

differently from other firms in their financial reporting.

• Construct a CSR Score, measured as total strengths minus total concerns in

KLD’s five social rating categories: community, diversity, employee relations,

environment, and product. (Use an alternative measure of CSR, CSR_DSI400)

• Findings: Socially responsible firms are less likely (1) to manage earnings

through discretionary accruals, (2) to manipulate real operating activities,

and (3) to be the subject of SEC investigations.

Yongtae Kim, Myung Seok Park, Benson Wier

18

• Summative paper.

• Consider two broad perspectives on CSR: (1) Companies will or should only engage in

socially responsible activities when doing so maximizes shareholder value. (2) Companies

might also make investments that benefit society even when doing so decreases shareholder

value.

• State the two papers (Dhaliwal et al. 2012; Kim et al. 2012) that aligns with the perspective

that CSR activities and disclosures are primarily a response to shareholder demand.

• Suggestions: CSR research in accounting could benefit significantly if accounting researchers

were more open to (1) the possibility that CSR activities and related disclosures are driven by

both shareholders and non-shareholder constituents, and (2) the use of experiments to

answer important CSR questions that are difficult to answer with currently available archival

data.

19

Chun Keung Hoi, Qiang Wu, Hao Zhang

• Examine the empirical association between corporate social responsibility (CSR) and tax

avoidance.

• Aggressive tax avoidance: Wilson’s (2009) tax-sheltering probability measure, the permanent

book-tax differences (Frank et al. 2009), and the discretionary book-tax differences (Desai

and Dharmapala 2006).

• Irresponsible CSR activities: Negative social ratings obtained from KLD Research &

Analytics.

• Use a sample of 2620 U.S. public firms over the period 2003–2009.

• Findings: Firms with excessive irresponsible CSR activities have a higher likelihood of

engaging in tax-sheltering activities and greater discretionary/permanent book-tax

differences.

• Implication: Corporate culture affects tax avoidance.

20

Jivas Chakravarthy, Ed deHaan, Shivaram Rajgopal

• Review firms’ press releases and identify 1,765 reputation-building actions taken by: (1) 94

restating firms in the periods before and after their restatement; and (2) a set of matched

control firms during contemporaneous periods.

• Sample: The set of firms identified by Hennes et al. (2008) to have had a restatement

involving irregularities between January 1997 and July 2006 and the authors randomly

select a sample of 94 of 188 restatements for investigation.

• Findings: (1)The frequency of, and stock returns to, reputation-building actions are greater

for restating firms in the period after their restatement than for the control groups. (2) Firm

characteristics predict the types of stakeholders targeted by firms. (3) Actions targeted at

both capital providers and other stakeholders are associated with improvements in the

restating firm’s financial reporting credibility.

21

W. Brooke Elliott, Kevin E. Jackson, Mark E. Peecher, Brian J. White

• Experimental paper.

• Examine the unintended, causal relation between Corporate Social Responsibility (CSR)

performance and investors’ estimates of fundamental value that can be attenuated by

investors’ explicit assessment of CSR performance.

• Conduct an experiment that uses a 2*2 + control between-subjects design, , with CSR

performance and explicit assessment of CSR performance as manipulated independent

factors.

• Main Finding: Investors’ estimates of fundamental value depend jointly on a firm’s

corporate social responsibility (CSR) performance and on explicit assessment of such

performance during their investment analysis.

22

Ella Mae Matsumura, Rachna Prakash, Sandra C. Vera-Munoz

• Examine the effects on firm value of carbon emissions and of the act of voluntarily

disclosing carbon emissions.

Sample: All S&P 500 firms for the three-year period 2006 to 2008.

• Hand-collect carbon emissions data from 2006 to 2008 from the CDP database.

• Findings: (1) For every additional thousand metric tons of carbon emissions, firm value

decreases by $212,000 on average, where the median emissions for the disclosing firms

in our sample are 1.07 million metric tons. (2) The median value of firms that disclose their

carbon emissions is about $2.3 billion higher than that of comparable non-disclosing

firms.

• Implication: The markets penalize all firms for their carbon emissions, but a further penalty

is imposed on firms that do not disclose emissions information.

Journal of Accounting and Economics

23

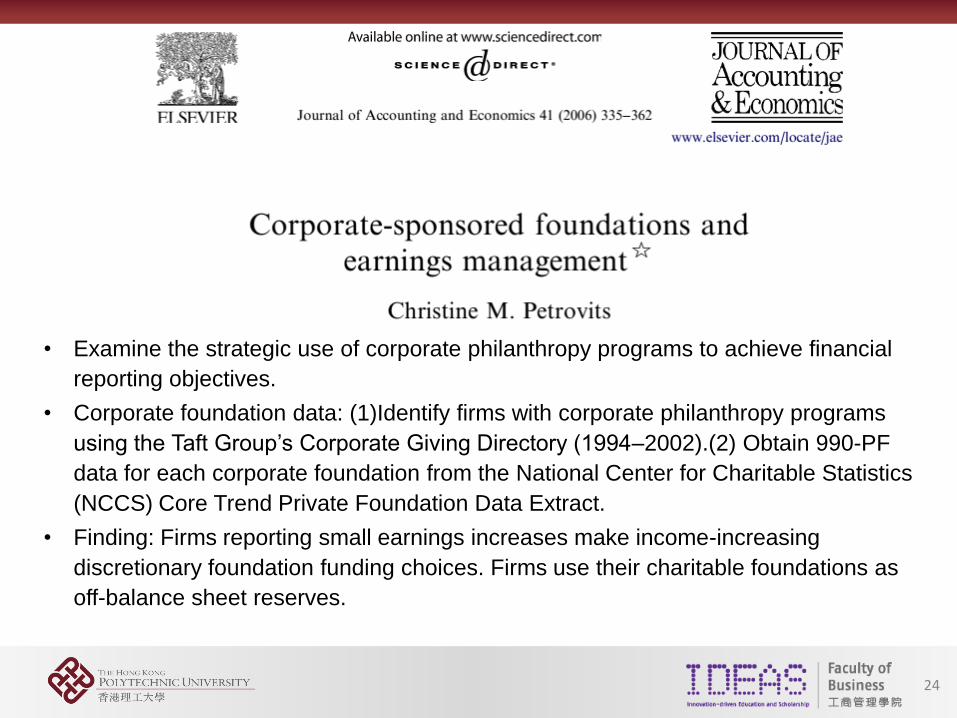

24

• Examine the strategic use of corporate philanthropy programs to achieve financial

reporting objectives.

• Corporate foundation data: (1)Identify firms with corporate philanthropy programs

using the Taft Group’s Corporate Giving Directory (1994–2002).(2) Obtain 990-PF

data for each corporate foundation from the National Center for Charitable Statistics

(NCCS) Core Trend Private Foundation Data Extract.

• Finding: Firms reporting small earnings increases make income-increasing

discretionary foundation funding choices. Firms use their charitable foundations as

off-balance sheet reserves.

25

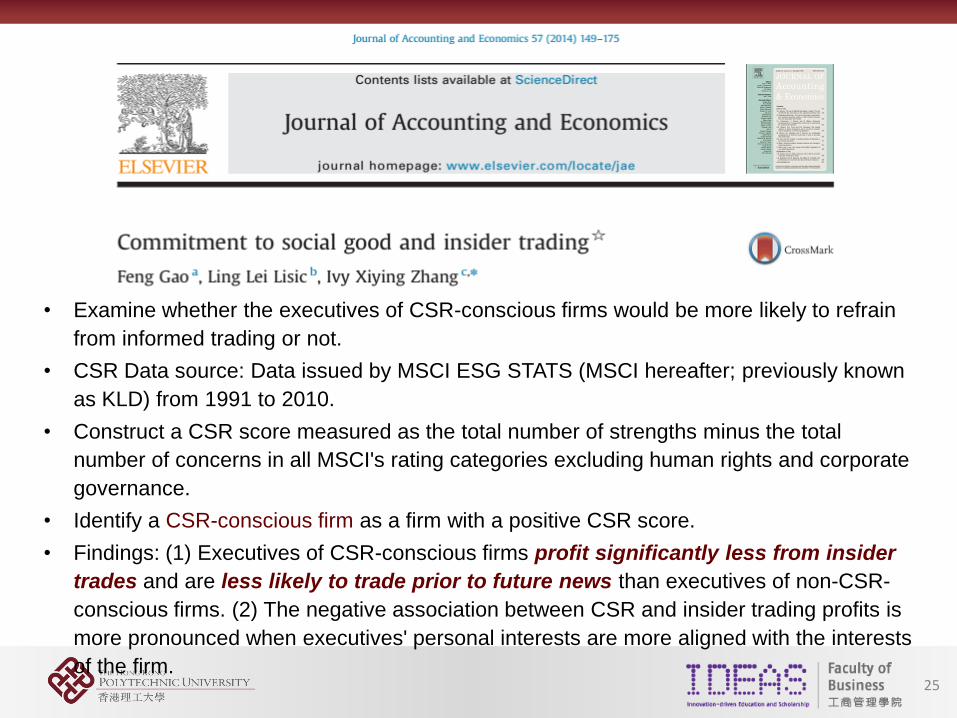

• Examine whether the executives of CSR-conscious firms would be more likely to refrain

from informed trading or not.

• CSR Data source: Data issued by MSCI ESG STATS (MSCI hereafter; previously known

as KLD) from 1991 to 2010.

• Construct a CSR score measured as the total number of strengths minus the total

number of concerns in all MSCI's rating categories excluding human rights and corporate

governance.

• Identify a CSR-conscious firm as a firm with a positive CSR score.

• Findings: (1) Executives of CSR-conscious firms profit significantly less from insider

trades and are less likely to trade prior to future news than executives of non-CSR-

conscious firms. (2) The negative association between CSR and insider trading profits is

more pronounced when executives' personal interests are more aligned with the interests

of the firm.

26

• Examine the relation between corporate social responsibility (“CSR”) expenditures and

firm performance.

• Posit that a firm may undertake a CSR initiative because the firm expects strong future

financial performance, rejecting the underlying assumption that CSR expenditures

lead to improvements in a firm's performance in the previous studies.

• Charity hypothesis & Investment hypothesis & Signaling hypothesis

• Research Methods:

• (1) Establish whether a positive association exists between current CSR expenditures and future

firm performance.(H1)

• (2) Examine the direction of the causality between CSR expenditures and future performance to

identify whether the relation is consistent with either the signaling or investment hypothesis.

(Two-stage approach) (H2&H3)

27

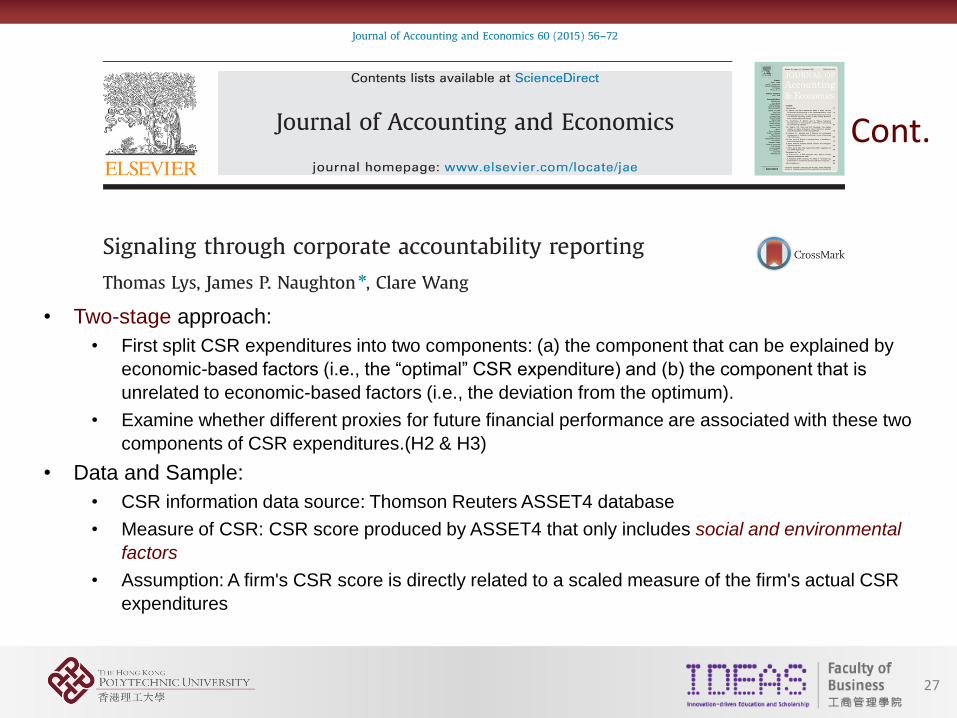

• Two-stage approach:

• First split CSR expenditures into two components: (a) the component that can be explained by

economic-based factors (i.e., the “optimal” CSR expenditure) and (b) the component that is

unrelated to economic-based factors (i.e., the deviation from the optimum).

• Examine whether different proxies for future financial performance are associated with these two

components of CSR expenditures.(H2 & H3)

• Data and Sample:

• CSR information data source: Thomson Reuters ASSET4 database

• Measure of CSR: CSR score produced by ASSET4 that only includes social and environmental

factors

• Assumption: A firm's CSR score is directly related to a scaled measure of the firm's actual CSR

expenditures

Cont.

28

• Findings:

• (1) Corporate social responsibility (“CSR”) expenditures are not a form of corporate

charity nor do they improve future financial performance.

• (2) Firms undertake CSR expenditures in the current period when they anticipate stronger

future financial performance.

• Implication:

• The positive association between CSR expenditures and future firm performance differs

from what is claimed in the vast majority of the literature and that corporate accountability

reporting is another channel through which outsiders may infer insiders’ private

information about firms’ future financial prospects.

Cont.

Journal of Accounting Research

29

30

• Explore the relevance of certain social responsibility disclosures of firms to investors by

empirically assessing their impact on security returns.

• The sample consisted of annual reports of Fortune 500 companies issued for fiscal years

ending between May 1, 1970 and April30, 1976.

• Disclosure categories: environmental, fair business practice, personnel, community

involvement, product.

• The disclosures were partitioned into two groups (monetary and nonmonetary) for each

category.

• Two related empirical tests of information content: (1) Analyze returns for portfolios of

securities selected from a broad spectrum of the market; (2) Investigate the return

performance of specific market segments (Industry, excess earnings, time period).

• Finding: The information content of firms‘ social responsibility disclosures is conditional

upon the market segment with which the firm is identified.

Contemporary Accounting Research

31

32

• It aims to develop the understanding of how assurance practitioners have attempted to

construct the practice of sustainability assurance.

• It seeks to understand how, and the extent to which, these efforts have rendered

sustainability reporting auditable.

• A longitudinal case study conducted in the national headquarters of two Big Four

professional services firms (code-named JIF and TRU for anonymity purposes) in

Western Europe.

• Data source: 36 in-depth interviews with practitioners and diverse documentary sources.

• Innovation in new assurance practices may be constrained by an over-reliance on

traditional financial audit training and techniques and certain internal professional

services firm control procedures.

• Practitioners are shown to have experienced considerable discomfort in their attempts to

construct a stable and legitimate knowledge base for assurance practice.

33

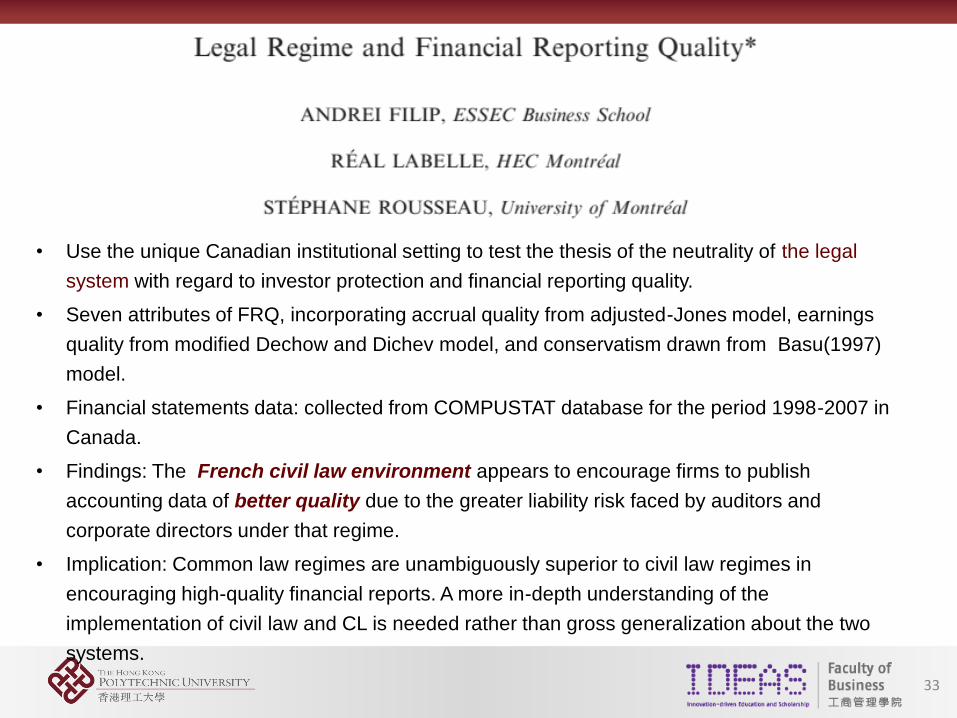

• Use the unique Canadian institutional setting to test the thesis of the neutrality of the legal

system with regard to investor protection and financial reporting quality.

• Seven attributes of FRQ, incorporating accrual quality from adjusted-Jones model, earnings

quality from modified Dechow and Dichev model, and conservatism drawn from Basu(1997)

model.

• Financial statements data: collected from COMPUSTAT database for the period 1998-2007 in

Canada.

• Findings: The French civil law environment appears to encourage firms to publish

accounting data of better quality due to the greater liability risk faced by auditors and

corporate directors under that regime.

• Implication: Common law regimes are unambiguously superior to civil law regimes in

encouraging high-quality financial reports. A more in-depth understanding of the

implementation of civil law and CL is needed rather than gross generalization about the two

systems.

Review of Accounting Studies

34

35

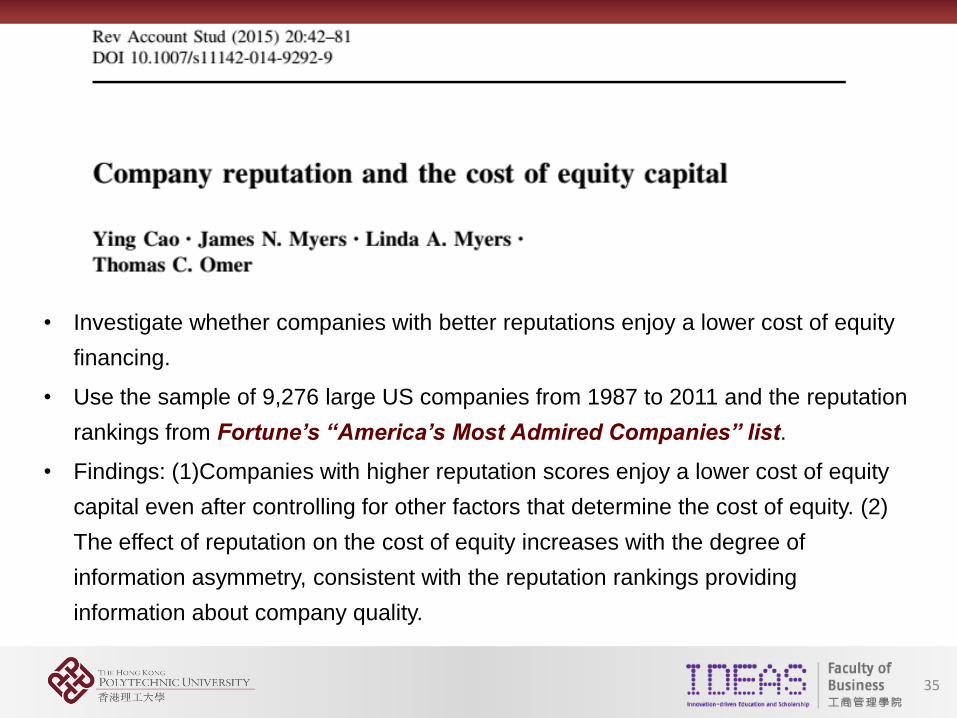

• Investigate whether companies with better reputations enjoy a lower cost of equity

financing.

• Use the sample of 9,276 large US companies from 1987 to 2011 and the reputation

rankings from Fortune’s ‘‘America’s Most Admired Companies’’ list.

• Findings: (1)Companies with higher reputation scores enjoy a lower cost of equity

capital even after controlling for other factors that determine the cost of equity. (2)

The effect of reputation on the cost of equity increases with the degree of

information asymmetry, consistent with the reputation rankings providing

information about company quality.

Journal of Financial Economics

36

37

• Analyze the relationship between employee satisfaction and long-run stock returns.

• My main data source: List of the ‘‘100 Best Companies to Work for in America.’’

• Findings: (1) A value-weighted portfolio of the ‘‘100 Best Companies to Work For in

America’’ earned an annual four-factor alpha of 3.5% from 1984 to 2009, and 2.1%

above industry benchmarks. (2) The Best Companies also exhibited significantly more

positive earnings surprises and announcement returns.

• Implications: (1) Employee satisfaction is positively correlated with shareholder returns

and need not represent managerial slack. (2) The stock market does not fully value

intangibles, even when independently verified by a highly public survey on large firms. (3)

Certain socially responsible investing (SRI) screens may improve investment returns.

38

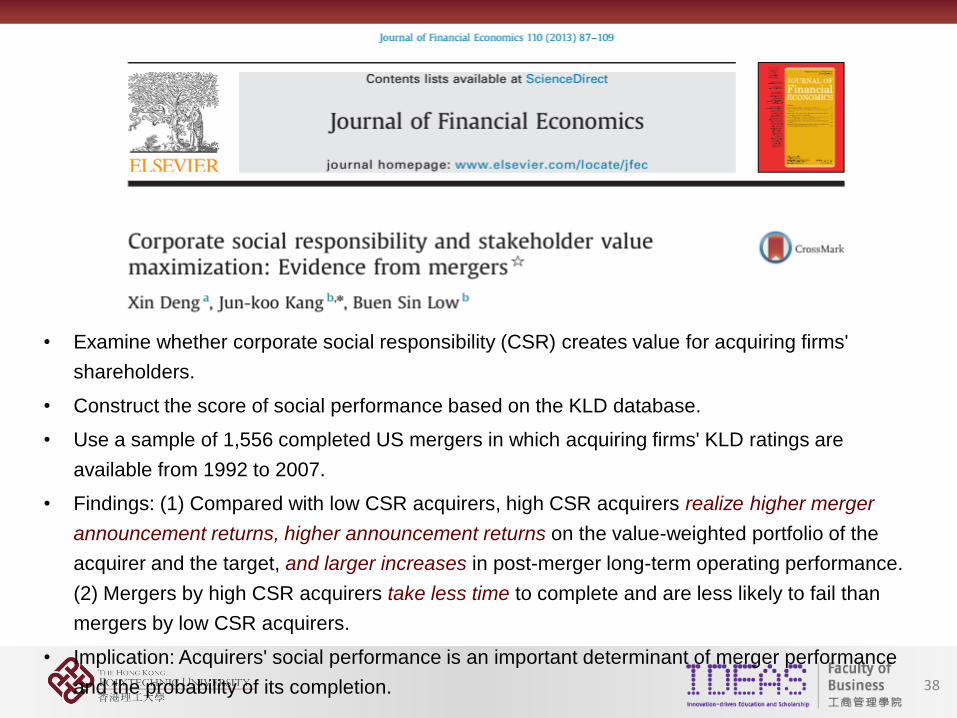

• Examine whether corporate social responsibility (CSR) creates value for acquiring firms'

shareholders.

• Construct the score of social performance based on the KLD database.

• Use a sample of 1,556 completed US mergers in which acquiring firms' KLD ratings are

available from 1992 to 2007.

• Findings: (1) Compared with low CSR acquirers, high CSR acquirers realize higher merger

announcement returns, higher announcement returns on the value-weighted portfolio of the

acquirer and the target, and larger increases in post-merger long-term operating performance.

(2) Mergers by high CSR acquirers take less time to complete and are less likely to fail than

mergers by low CSR acquirers.

• Implication: Acquirers' social performance is an important determinant of merger performance

and the probability of its completion.

39

• Examine the relation between political leaning and CSR performance, moreover, the causal

relation between CSR and firm value.

• Sample: The largest 3,000 publicly traded U.S. companies (Russell 3000) from 2003 to 2009.

• CSR data source: The Kinder, Lydenberg, and Domini (KLD) database (the ratings for 56

different categories including 30 strengths and 26 concerns).

• Findings: (1) Firms score higher on CSR when they have Democratic rather than Republican

founders, CEOs, and directors, and when they are headquartered in Democratic rather than

Republican-leaning states. (2) Democratic-leaning firms spend $20 million more on CSR than

Republican-leaning firms or roughly 10% of net income. (3) Increases in firm CSR ratings are

associated with negative future stock returns and declines in firm ROA, suggesting that any

benefits to stakeholders from social responsibility come at the direct expense of firm value.

40

• Study how stock markets react to positive and negative events concerned with a firm's

corporate social responsibility (CSR).

• Data source: Two different KLD products, namely KLD Socrates and the @KLD newsletters.

• Sample: 2,116 events concerning 745 different firms between 2001 and 2007.

• Apply textual analysis to the event descriptions.

• Findings: (1) Investors respond strongly negatively to negative events and weakly negatively

to positive events.(2) Investors do value “offsetting CSR”, that is positive CSR news

concerning firms with a history of poor stakeholder relations.(3) Investors respond negatively

to positive CSR news which is more likely to result from agency problems. (4) CSR news with

stronger legal and economic information content generates a more pronounced investor

reaction.

Review of Financial Studies

41

42

• Focus on the Fortune 500 companies as of April 17, 2006.

• Hand-collect corporate giving data from the National Directory of Corporate Giving.

• Collect data on corporate contributions to charities and foundations using all directories

between 1997 and 2007 to construct a database that spans the 1996–2006 period. Then

add these amounts to obtain total firm contributions.

• Hand-match firm-level contributions data with PERMNOs and GVKEYs.

• Findings: Corporate giving is positively (negatively) associated with CEO charity

preferences (CEO shareholdings and corporate governance quality). Corporate

donations advance CEO interests and suggests misuses of corporate resources that

reduce firm value.

Journal of Corporate Finance

43

44

• Focus on firm-specific giving practices and evaluate both an “agency cost” theory, which

postulates that managers and board members increase their own utility through corporate

philanthropy, and a “value enhancement” theory, which postulates that philanthropy creates

value for shareholders.

• Examine determinants of corporate giving, including the size and composition of the board

of directors; monitoring by debtholders, blockholders, and institutional investors; state

philanthropy and fiduciary duty laws; and industry settings.

• Sample: All Fortune 500 firms identified in the 1998 issue.

• Giving is defined as the amount the corporation identifies as cash contributions (Direct or

through foundation) to not-for-profit organizations. Charitable data are from 1999 Corporate

Giving Directory(2000).

• Findings: (1)Results provide some support for the theory that giving enhances shareholder

value, as firms in the same industry tend to adopt similar giving practices and firms that

advertise more intensively also give more to charity. (2) Agency costs play a prominent role in

explaining corporate giving.

45

• Investigate the impact of ethics and stakeholder governance on the risk-adjusted performance for

SRI funds across the world.

• Construct a database that contains socially responsible and conventional equity mutual funds

domiciled in 17 countries and three regions, including Europe, North America and Asia-Pacific from

January 1991 (prior to this year the number of SRI mutual funds is small) and ends in December 2003.

• Data source of SRI and conventional funds: Standard & Poor's Fund Service (Micropal), CRSP

Survivor-bias Free Mutual Fund Database, Bloomberg, Datastream “dead” mutual funds research

files.

• Findings: (1) The average SRI funds in the US, the UK, and most continental European and Asia-

Pacific countries strongly underperform their Fama-French-Carhart (FFC) benchmarks.(2) Although

ethical investors are unable to identify the funds that will outperform, there is some fund-selection

ability to identify the ethical funds that will perform poorly. (3) The screening activities and processes

of SRI funds have a significant impact on the risk-adjusted returns. (4) While fund size erodes the

returns of conventional funds, there is no such effect for SRI funds.

46

• Investigate whether firms’ corporate social performance (CSP) ratings impact their

performance (cost of capital) and risk.

• Detailed proprietary ESG ratings data (both general and industry-specific ESG factors)

from Sustainability Asset Management Group GmbH (SAM) for the period 2002 to 2010.

• Select the 256 companies that comprise the UK component of SAM's database.

• Findings: (1) There is no significant difference in the risk-adjusted performance of

portfolios with high and low CSP. (2) CSP does not seem to impact aggregate

unsystematic risk. (3) There is a positive relation between CSP and firm size.

• Implication: Investors and managers are able to implement a CSP investment or

business strategy without incurring any significant financial cost (or benefit) in terms of

risk or return.

47

• Focus on firms that use auditor-provided tax services and analyze the impact of tax

management fees and CSR, including corporate governance, community and diversity

on effective tax rates.

• Measurement of tax avoidance: GAAP tax expense to pretax accounting income (GAAP

ETR) and taxes paid to pretax accounting income (Cash ETR)

• Measurement of CSR: sum of strengths and concerns on CG, community and diversity.

Data source: KLD STATS.

• Sample: S&P 500 firms

• Findings: The interaction of community concerns with tax management fees positively

affects both GAAP and Cash ETR, while the interaction of negatively affects Cash ETR.

• The first paper to empirically relate tax avoidance, tax management and CSR.

48

• Investigate the various factors (firm-level and CEO-level characteristics, media

scrutiny) that motivate firm managers to make socially responsible investments.

• CSR Data source: KLD Research & Analytics (Community, Diversity, Employee,

Environment, Humanitarian, and Product)

• Sample: 11711 firm years from 1992 to 2006.

• Findings: (1)Larger firms, firms with greater free cash flow, and higher advertising outlays

demonstrate higher levels of corporate social responsibility(CSR). (2)Companies with

stronger institutional ownership are less likely to invest in CSR. (3) Female CEOs,

younger CEOs, and managers who donate to both Republican and Democratic parties

are significantly more likely to invest in CSR. (4) There is a strong positive connection

between the level of media scrutiny surrounding the firm and its CEO, and the level of

CSR investment.

49

• Explore the impact that environmental, social and governance (ESG) corporate practice

disclosure has on equity financing.

• Present a framed field experiment with Private Equity investors (including both venture capital and

buyouts specialists) and infer from their expertise explicit measures of over

and underperformance in terms of corporate social responsibility practice disclosure, formalized

as ESG factors.

• Findings: (1)Firm valuations and investment decisions are both impacted by the factor (ESG), sign

(socially responsible/good or socially irresponsible/bad) and quality (hard or soft) of disclosed

corporate practices.(2)There is an asymmetric effect of non-financial performance disclosure,

investors reacting more to bad than to good ESG news.

• Implication: Irresponsible corporate policies might both prevent equity financing and increase its

cost, the disclosure of ESG performance thus consisting in a defensive strategy to protect firm

value and equity access.

Management Science

50

51

• Aim to understand the conditions under which a brand’s CSR actions can serve as effective

instruments of competitive strategy, helping it compete with a formidable market leader.

• Premise: The success of such a macrolevel strategic objective depends, ultimately, on the

microlevel actions of individual consumers.

• Qualitative focus group study

• Field study

• The efficacy of a challenger’s CSR initiative in helping the challenger gain customers from the

market leader hinges interactively on two key factors: consumers’ participation in (versus awareness

of) the initiative and their affective trust in both the challenger and the leader.

• Findings: (1)The challenger can reap superior business returns among consumers who had

participated in its CSR initiative, relative to those who were merely aware of the initiative. (2)

Participant consumers demonstrate the desired business returns in favor of the challenger,

regardless of their affective trust in the leader, whereas aware consumers’ reactions become less

favorable as their affective trust in the leader increases.

52

• Explore an indirect link between CSR and firm value, particularly the channel through

which CSR affect firm value.

• Focus on the key stakeholder—consumers, due to the insights that the impact of CSR on

firm value depends on the ability of CSR to influence stakeholders in the firm.

• Employ the KLD Stats database over the period 1991–2005 (Firms in S&P 500, Russell

1000, Russell 2000).

• Measure of CSR (Indices): Narrow measure of CSR(five categories covering community,

diversity, employment, environment, human rights) ;Broad measure of CSR(seven

categories covering narrow ones and product, industry), both from KLD.

• Measure of performance: Tobin’s q

• Measure of consumer awareness: Advertising spending

• Measure of reputation for being responsible citizen: Fortune’s rating on the list of

“America’s Most Admired Companies.” (Removing financial halo effect)

53

• Findings:

• CSR activities can enhance firm value for firms with high public awareness, as proxied by

advertising intensity. However, firms with high public awareness are also penalized more when

there are CSR concerns.

• Second, for firms with low public awareness, the impact of CSR activities on firm value is

either insignificant or negative.

• Third, advertising has a negative impact on the CSR–value relation if there is an inconsistency

between the firm’s CSR efforts and the company’s overall reputation.

• Fourth, after including firm fixed effects there is no direct relation between CSR and firm value.

• Implications: (1) Advertising creates awareness about the company and its activities,

which creates more “goodwill” on the part of customers. (2) There are no enough

evidences to suggest that CSR is employed to signal product quality.

Cont.

54

• Explore the organizational and performance implications for organizations that integrate social and environmental

issues into their processes through the adoption of corporate policies.

• Such organizations represent an alternative and distinct way of competing for the modern corporation, characterized by

a governance structure that in addition to financial performance,accounts for the environmental and social impact of the

company, a long-term approach toward maximizing intertemporal profits, an active stakeholder management process,

and more developed measurement and reporting systems.

• Main Data Source: Thomson Reuters ASSET4 database (corporate policies related to the environment, employees,

community, products, and customers)

• Findings:

• Corporate governance: The boards of directors of high sustainability companies are more likely to be formally

responsible for sustainability, and top executive compensation incentives are more likely to be a function of sustainability

metrics.

• Stakeholder engagement/ Time horizon/ Measurement and disclosure: High sustainability companies are more likely

to have established processes for stakeholder engagement, to be more long-term oriented, and to exhibit higher

measurement and disclosure of nonfinancial information.

• Corporate performance: High sustainability companies significantly outperform their counterparts over the long term,

both in terms of stock market and accounting performance.

55

Quarterly Journal of Economics

56

• Develop a laboratory product market in which low-cost production creates a negative

externality for third parties, but where alternative production with higher costs mitigates

the externality.

• Report two laboratory studies that explore the extent to which socially responsible

market behavior can mitigate the problem of negative external effects.

• First study: Conducted in Switzerland, reveals a persistent preference among many

consumers and firms for avoiding negative social impact in the market, reflected both in

the composition of product types and in a price premium for socially responsible

products.

• Second study: Investigate whether market social responsibility varies across societies by

comparing market behavior in Switzerland and China. Low-cost production that creates

negative externalities is significantly more prevalent in markets in China.

Accounting, Organizations and Society

57

58

• Aim to determine (1) whether the funds’ investment policies considered corporate

activities in nine selected areas of social concern and (2) the respondents’ perceptions of

the relative importance and availability of information related to the nine areas.

• Mail a questionnaire(covering three topic areas) to a random sample of 250 mutual fund

presidents from the 1974 edition of Investment Companies, Mutual Funds and Other

Types published by Wissenberger Services, Inc.

• Nine areas of social concern: Environmental pollution; Other nonpollution related

environmental damage; Fails to contribute to charitable causes; Equal opportunity

employment practices of the firm, etc.

• Findings: (1) A majority of the funds had investment policies which considered some, but

not all of the nine social activities. (2) The relative importance of information on eight of

the nine social activities was less than that for six selected financial items of information,

and the availability of information on the nine social areas was perceived to be low.

59

• Analytical paper.

• Evaluate the degree of institutional reform, designed to empower stakeholders, and

thereby enhance corporate accountability, accompanying these voluntary initiatives,

together with that potentially ensuing from proposed regulations, later rescinded, for

mandatory publication of an Operating and Financial Review by UK quoted companies.

• Methods: Draw upon a number of reports short-listed for the Social and

Sustainability categories of the 2003 ACCA UK Sustainability Reporting Awards

Scheme, together with an analysis of the somewhat long drawn out processes which

led to the publication of the Department of Trade and Industry’s OFR draft regulations.

• Findings: Both forms of disclosure offer little in the way of opportunity for facilitating

action on the part of organizational stakeholders, and cannot therefore be viewed as

exercises in accountability.

60

• Draw on stakeholder theory to evaluate the relationship between perceived

stakeholder influences and organizations’ use of different types of environmental audits

(no audit, internal audits only, external audits only, and a combination of both internal and

external audits).

• Sample: Both large and small organizations in manufacturing sectors operating in seven

different countries (Canada, France, Germany, Hungary, Japan, Norway and the US) .

• Data source: An international survey developed and administered by the Organization for

Economic Co-Operation and Development (OECD) Environment Directorate and

academic researchers from Canada, France, Germany, Hungary, Japan, Norway and the

US.

• Findings: There are significant variations in the use of environmental audits are

associated with differences in stakeholder influences, and that a more nuanced

treatment is needed when evaluating these audits.

61

• Investigate whether there are self-serving biases present in the language and verbal

tone in corporations’ environmental disclosures as a tool for managing stakeholder

impressions

• H1:Firm environmental performance “optimism” exhibited in environmental

disclosures ;Optimism—language endorsing some person, group, concept, or event,

or highlighting their positive entailments

• H2:Firm environmental performance “certainty” exhibited in environmental

disclosures ;Certainty—language that indicates resoluteness, inflexibility,

completeness, and a tendency to speak ex cathedra

• Sample: A cross-sectional sample (190 firms) of corporate environmental disclosures

contained in US 10-K annual reports.

• Environmental Disclosures: Content analysis (using software DICTION);

• Environmental Performance: Environmental concern ratings from KLD Research

and Associates, Inc.

-

+

62

• Findings: (1) Worse environmental performance is associated with the use of

more optimistic language in our test companies’ disclosures. (2) Environmental

performance measure is negatively related to the certainty scale of the disclosure.

• Implications: The language and verbal tone used in corporate environmental

disclosures, in addition to their amount and thematic content, must be considered

when investigating the relation between corporate disclosure and performance.

Cont.

63

• Explore the relations between environmental performance, environmental disclosure,

membership in the DJSI, and perceptions of corporate environmental reputation.

• (1) Investigate the extent to which firms’ environmental performance is reflected in

perceptions of their environmental reputation and whether environmental disclosure serves

to mediate the negative aspects of poorer environmental performance associated with

those assessments.

• (2) Examine whether differences in environmental performance and environmental

disclosure appear to be associated with membership selection to the Dow Jones

Sustainability Index (DJSI).

• Sample: A cross-sectional sample of 92 US firms from environmentally sensitive industries.

• Data Source: Firms from the basic materials, oil and gas, and utility industries in Newsweek

magazine’s ranking of 500 large US companies.

• Method: Path analysis model

64

Cont.

• (1) Environmental performance measured using Trucost environmental

performance scores is negatively related to both reputation scores and

membership in the DJSI.

• (2) The extent of voluntary environmental disclosure included in annual

financial reports and, where issued, stand-alone

corporate social responsibility (CSR) reports is negatively

related to environmental performance.

• (3) There is a significant positive relation between environmental

disclosure and both the environmental reputation measures and DJSI

membership.

• (4) The DJSI designation positively influences perceptions of corporate

reputation, membership in the Index appears to be related more

to what companies say than what they do.

• Implications: (1) Voluntary environmental disclosure appears to mediate the effect of poor environmental performance

on environmental reputation. (2) The DJSI may be reducing the incentives for companies included as members to

improve their future environmental performance.

Journal of Accounting, Auditing & Finance

65

66

• Identify determinants of corporate environmental reporting by Canadian firms subject to

water pollution compliance regulations during the 1986-I993 period.

• Use a cost-benefit framework:

• Information Costs: Volatility or perceived firm risk (market Beta); Reliance on capital markets;

Trading volume; Control by a single shareholder, individual or family; Subsidiary of another firm.

• Financial Condition: Accounting-based performance(ROA); Stock market performance; Leverage.

• Environmental Performance.

• Sample: 33 firms are selected from water pollution compliance surveys published by the

Canadian, Ontario, and Quebec environmental departments from 1986 to 1993.

• Finding: Information costs and a firm’s financial condition are key determinants of

environmental disclosure. Firm size, the regulatory regime governing corporate

disclosure and industry, also contribute to explaining environmental disclosure.

Journal of Accounting and Public Policy

67

68

• Aim to explore the potential effects of culture and corporate governance on social

disclosures.

• Culture: The ethnic background of directors and shareholders (boards dominated by Malay

directors, a Malay Finance Director, Malay shareholders)

• Corporate governance: Board composition, multiple directorships and type of shareholders

(boards dominated by non-executive directors, a chairman having multiple directorships,

dominated by foreign shareholders)

• Social disclosures: Disclosure in annual reports of Malaysian corporations, measured by an

index score as well as in terms of number of words

• Findings: There is a significant relationship between corporate social disclosure and boards

dominated by Malay directors, boards dominated by executive directors, chair with multiple

directorships and foreign share ownership.

69

• Examine the influence of social responsibility ratings on market returns to Arthur Andersen

(AA) clients following the Enron audit failure.

• CSR information data source: The Kinder, Lynderberg, Domini Research and Analytics

Inc. (KLD) database.

• Measurement of CSR: Construct a measure of aggregate social responsibility by totaling

each of the sub-category strengths and each of the sub-category concerns.

• Sample: (1) Begin with all AA firms included in the KLD data; (2) Match each AA firm to a

non-AA firm from the KLD database based on industry, size and ‘‘Big 5” auditor.

• Findings: There is no evidence that social responsibility mitigated the negative returns to

AA clients following the Enron audit failure. The results are inconsistent with claims that

social responsibility can burnish a firm’s reputation in a time of crisis.

70

• Experimental study.

• Examine the impact of corporate social disclosure (CSD) on investment behavior in the US, Japan,

France, and Sweden using stakeholder theory as the underlying framework for the analysis.

• Arguments: The role of a corporation in society and the perception of the relative importance of its

stakeholders are influenced by a country’s unique cultural heritage. Further, a country’s stakeholder

orientation affects the way in which investors react to CSD.

• Participants Sample: Graduate business students from the US, France, Sweden, and Japan.

• Measurement of stakeholder orientation: develop a stakeholder scale.

• Findings: (1) CSD does impact investment behavior within each of the countries in the sample and that

the extent of this impact is influenced by their stakeholder orientation. (2) There is a significant

difference in investors’ reactions to CSD across countries and the reactions of investors are related to

the investors’ stakeholder orientation.

• Implication: There are systematic, cross-national differences in the investment response to CSD and

that the stakeholder concept is useful in explaining this variation.

71

• Examine the association between corporate social responsibility (CSR) and corporate tax

aggressiveness.

• Sample: 408 publicly listed Australian corporations for the 2008/2009 financial year

• Corporate tax aggressiveness based on ETRs (two different measures of ETRs) collected from the

Aspect-Huntley financial database

• Income tax expense currently payable divided by book income

• Income tax expense currently payable divided by operating cash flows

• CSR: Take CSR disclosure as an indicator of CSR performance and developed a broad-based CSR

disclosure index (CSRDISC)

• Findings: (1) The higher the level of CSR disclosure of a corporation, the lower is the level of

corporate tax aggressiveness. Thus more socially responsible corporations are likely to be less tax

aggressive in nature. (2) The social investment commitment and CSR strategy (including the ethics and

business conduct) of a corporation are important elements of CSR activities that have a negative

impact on tax aggressiveness.

72

• Examine the relation between specific aspects of governance and media coverage and the

quality of voluntary environmental disclosure (VED).

• Use a sample of 127 firms over a 6-year period (2000–2005) from five industries (chemical, oil

and gas, electrical utilities, pharmaceutical and biotech, food and beverage)

• Voluntary environmental disclosures: the quantitative and qualitative measures related to firm-

specific environmental issues

• The quality of VED: use both the substance and form of environmental indicators reported by a

firm.

• Environmental legitimacy: media coverage from the Wall Street Journal for environmental

disclosures

• Findings: (1) VED quality is positively associated with environmental media coverage, negative

environmental media and board attributes of independence, diversity, and expertise. (2)

Institutional investors exert influence over managerial decisions on environmental reporting only

in the face of negative environmental media.

73

• (1) Investigate whether CSR performance affects information asymmetry. (2) Investigate the

effect of informed (institutional investors) on the CSR performance-asymmetry relation.

• Measure of CSR performance: social performance rating scores from KLD STAT

• Measure of information asymmetry: Bid-ask spread—Annually averaging the ratio of the daily

bid-ask spread to the closing price from the CRSP daily stock file.

• Sample: 17555 firm-year observations, spanning 7 years from 2003 to 2009, from Compustat

and CRSP.

• Findings: (1) Both positive and negative CSR performance reduce information asymmetry. (2)

The influence of negative CSR performance is much stronger than that of positive CSR

performance in reducing information asymmetry. (3) The negative association between CSR

performance and bid-ask spread decreases for firms with a high level of institutional investors

compared to those with a low level of institutional investors.

• Implication: CSR performance plays a positive role for investors by reducing information

asymmetry and that regulatory action may be appropriate to mitigate the adverse selection

problem faced by less-informed investors.

74

• Examine the benefits associated with corporate social responsibility (CSR) disclosure in an

international setting covering 31 countries.

• Use variables such as the legal status of labor protection, CSR disclosure requirements, and

public awareness of and attitudes toward CSR issues, then divide countries into more and

less stakeholder-oriented groups.

• Collect standalone CSR reports from various internet-based sources, including the Corporate

Register, Corporate Responsibility Newswire, CSR News, and firms’ own websites.

• CSR reporting indicator (NONFIN). An indicator variable that takes the value of 1 if a firm

issues a standalone CSR report during the year, and 0 otherwise.

• Findings: (1) There is a negative association between CSR disclosure and the cost of equity

capital; this relationship is more pronounced in stakeholder-oriented countries. (2) Financial

and CSR disclosures act as substitutes for each other in reducing the cost of equity capital.

Journal of Business Ethics

75

76

• Review paper.

• Examine the status of CSR research from its beginning especially after 1970 to year 2008

in leading academic journals and reports to assess the focus areas of research on CSR

so far.

• Compare and contrast various kinds of research articles, methodologies, and research

designs used in various researches in literature.

• Examine the academic literature on Corporate Social Responsibility and Performance

using a paradigmatic and methodological lens.

• Parameters for methodological review——nature and types of articles; research design and

approach; nature of research design; sources and nature of data; data testing and data analysis

techniques.

• Paradigmatic shift review

• Relational analysis——Changing meaning, definition, and models of CSR; Factors

determining CSR initiatives; CSR in actions; Impact of CSR on stakeholders and financial

performance; Impact of CSR on stakeholders and financial performance.

77

• Review paper.

• Review and synthesize the contemporary business literature that focuses on the role of

corporate social responsibility (CSR) to enhance firm value published in top-ranked

finance, accounting, and management journals, as well as other select journals that focus

exclusively on CSR research.

• Domains of CSR literature in this review: firm performance, capital market returns,

cost of capital, financial reporting, corporate governance, employee benefits,

executive compensation, product market advantages, determinants and

informational contents of CSR disclosures, and auditability of CSR disclosures.

• Definition and Measurement of CSR

• Value-Enhancing Capabilities of CSR (The Concept and Measurements of Firm Value/ Sources of

Value-Enhancing Capabilities/ CSR and Firm Performance/ CSR and Capital Market Benefits/ CSR and

Capital Market Benefits/ CSR, Executive Compensation, and Employment Market Benefits/ CSR and

M&A-Market Benefits/……)

78

Cont.

79

• Examine whether corporate social responsibility performance is associated with corporate

tax avoidance.

• Tax Avoidance: A Social Irresponsibility

• Employ a matched sample of 434 firm-year observations (i.e., 217 tax-avoidant and 217

non-tax-avoidant firm-year observations) from the Kinder, Lydenberg, and Domini

database over the period 2003–2009

• Findings: (1)The higher the level of CSR performance of a firm, the lower the likelihood of

tax avoidance. (2) The CSR categories community relations and diversity represent

particularly important elements of CSR performance that reduce tax avoidance.

Journal of Banking & Finance

80

81

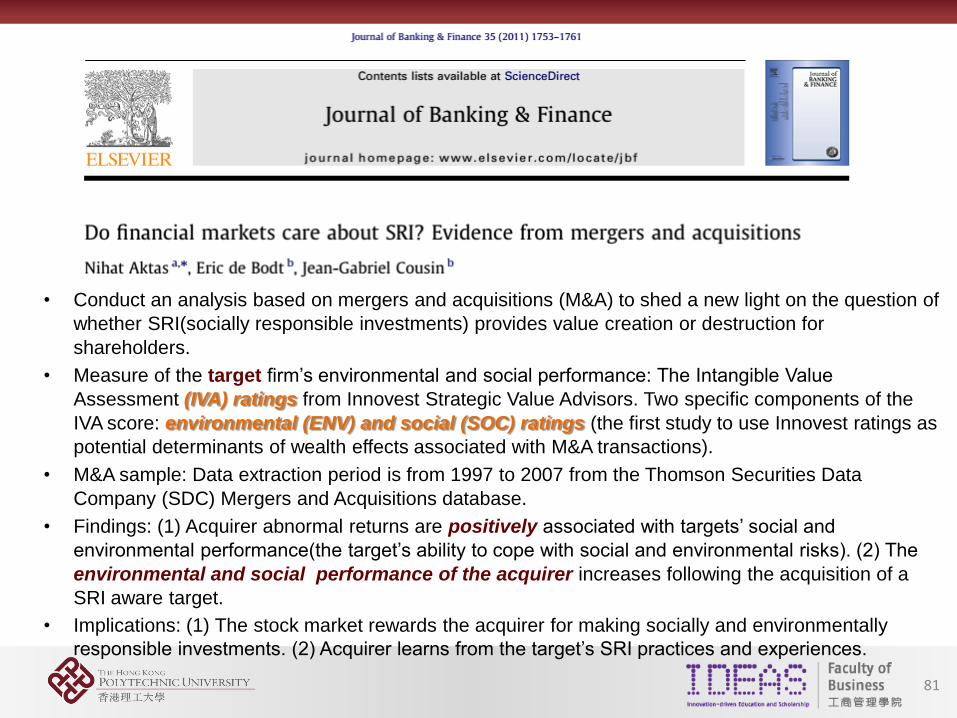

• Conduct an analysis based on mergers and acquisitions (M&A) to shed a new light on the question of

whether SRI(socially responsible investments) provides value creation or destruction for

shareholders.

• Measure of the target firm’s environmental and social performance: The Intangible Value

Assessment (IVA) ratings from Innovest Strategic Value Advisors. Two specific components of the

IVA score: environmental (ENV) and social (SOC) ratings (the first study to use Innovest ratings as

potential determinants of wealth effects associated with M&A transactions).

• M&A sample: Data extraction period is from 1997 to 2007 from the Thomson Securities Data

Company (SDC) Mergers and Acquisitions database.

• Findings: (1) Acquirer abnormal returns are positively associated with targets’ social and

environmental performance(the target’s ability to cope with social and environmental risks). (2) The

environmental and social performance of the acquirer increases following the acquisition of a

SRI aware target.

• Implications: (1) The stock market rewards the acquirer for making socially and environmentally

responsible investments. (2) Acquirer learns from the target’s SRI practices and experiences.

82

• Seek to advance the understanding of the CSR-financial performance relationship by examining

whether CSR performance affects firms’ costs of equity capital for a large sample of US firms.

• Relative size of a firm’s investor base: Low CSR firms tend to have smaller investor base due

to investor preferences and information asymmetry.

• A firm’s perceived risk: Investors perceive socially irresponsible firms as having a higher level of

risk which cannot be easily diversified away in an investor’s portfolio..

• Estimate firms’ ex ante cost of equity implied in analyst earnings forecasts and stock prices.

• Sample: 12,915 US firm-year observations from 1992 to 2007.

• Data source of CSR: KLD STATS.

• Findings: (1) Firms with better CSR scores exhibit cheaper equity financing. (2) Investment in

improving responsible employee relations, environmental policies, and product strategies

contributes substantially to reducing firms’ cost of equity. (3) Participation in the two industries—

tobacco and nuclear power, increases firms’ cost of equity.

• Implication: Firms with socially responsible practices have higher valuation and lower risk.

83

• Examine the link between corporate social responsibility (CSR) and bank debt.

• Assume that banks have no social agenda to promote but rather are interested solely in the ability

of the borrower to repay its loan obligations.

• The risk mitigation view & The overinvestment view

• Use a sample of 3996 loans extended to 1265 US firms over the period from 1991 to 2006.

• Data source of CSR: KLD STATS from KLD Research and Analytics Inc.

• Dependent variable: Log-spread (Logarithm of initial all-indrawn spread over LIBOR)

• Findings: (1) Firms with social responsibility concerns pay between 7 and 18 basis points more

than firms that are more responsible. (2) Lenders are more sensitive to CSR concerns in the

absence of security. (3) Low-quality borrowers that engage in discretionary CSR spending face

higher loan spreads and shorter maturities, but lenders are indifferent to CSR investments by

high-quality borrowers.

84

• Investigate the relationship between corporate social responsibility (CSR) and I/B/E/S analysts’

earnings per share (EPS) forecasts using a large sample of US firms for 1992–2011.

• Four factors of CSR effect : Accounting opacity, corporate governance, stakeholder risk, and

overinvestment.

• Data source: The Kinder, Lydenberg, and Domini Research & Analytics, Inc. (RiskMetrics-KLD)

rating.

• Findings: (1) All of the four factors significantly affect both the absolute forecast error on EPS and

its standard deviation controlling for forecast horizon; number of analysts and forecasts; and year,

industry, and broker house effects. (2) Overinvestment, stakeholder risk, and accounting opacity

have a positive effect, increasing both dependent variables, while corporate governance quality

has a negative effect. (3) Unbiasedness is generally met in the subsample of the Top CSR quality

companies and markedly violated in the subsample of the Bottom CSR companies.

85

• Set up a theoretical model of banking profit function considering three motives (altruism, strategic

choices, and greenwashing) pertaining to the ways that CSR affects financial performance.

• Bank profit function:

• Aggregate CSR index: cover all the CSR activities of each bank, where the data of activities come from

the EIRIS database.

• Use global banking data from 2003 to 2009 from 22 countries (the U.S., Canada, Austria, UK, Hong

Kong, etc.)

• Findings: (1) CSR positively associates with financial performance in terms of return on assets, return on

equity, net interest income, and non-interest income. (2) CSR negatively associates with non-performing

loans.

• Implication: Strategic choice is the primary motive of banks to engage in CSR

86

• Investigate whether corporate social responsibility (CSR) mitigates or contributes to stock price crash

risk.

• Crash risk, defined as the conditional skewness of return distribution, captures asymmetry in risk and is

important for investment decisions and risk management.

• Corporate social ratings data source: The MSCI ESG database, formerly known as the Kinder,

Lyndenberg, and Domini Research and Analytics Inc. (KLD) database (from 1994 to 2008).

• Measure of CSR: An aggregate CSR score to capture firm-level social responsibility based on five areas

(community, diversity, employee relations, environment, and product)of strength/concern ratings MSCI

ESG assigns to each company.

• Findings: (1) If socially responsible firms commit to a high standard of transparency and engage in less

bad news hoarding, they would have lower crash risk. (2) If managers engage in CSR to cover up bad

news and divert shareholder scrutiny, CSR would be associated with higher crash risk. (3) Firms’ CSR

performance is negatively associated with future crash risk after controlling for other predictors of crash

risk, and the association is more pronounced when firms have less effective corporate governance or a

lower level of institutional ownership.

• Implication: Firms that actively engage in CSR also refrain from bad news hoarding behavior, thus

reducing crash risk, supporting the mitigating effect of CSR on crash risk.

Other journals

87

88

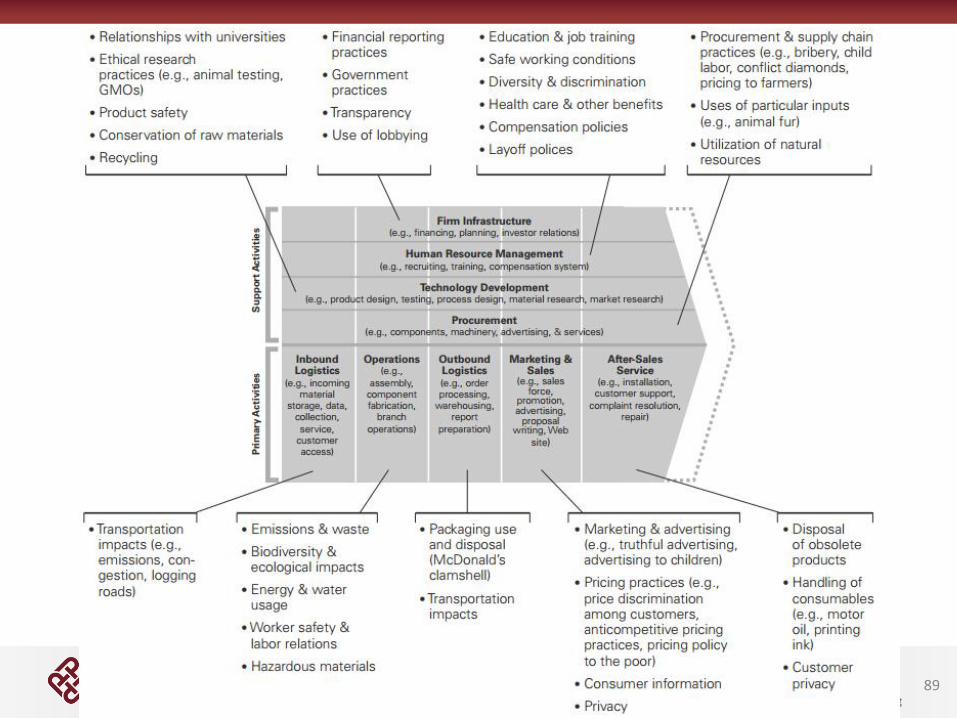

• Michael E. Porter and Mark R. Kramer. 2006. Strategy and Society: The

link between competitive advantage and Corporate Social Responsibility.

Harvard Business Review.

• The prevailing approaches to CSR are so fragmented and so disconnected from business and

strategy as to obscure many of the greatest opportunities for companies to benefit society.

• Propose a new way to look at the relationship between business and society that does not treat

corporate success and social welfare as a zero-sum game.

• Introduce a framework companies can use to identify all of the effects, both positive and

negative, they have on society; determine which ones to address; and to the AIDS pandemic in

Africa even though it was far removed from their primary product lines and markets.

• An affirmative corporate social agenda moves from mitigating harm to reinforcing

corporate strategy through social progress.

• Mapping the social impact of the value chain:

89

90

• Review paper.

• (1) Outline which CSR activities and outcomes have been included in previous research.

• Activities

• Philanthropy: cause-related marketing, donations of cash, community involvement, employee

volunteerism, promotion of a social issue, donations of products, licensing, event sponsorship,

customer donations and non-specific support for charities.

• Business practices: environmental protection practices, etc.

• Product-related: products that generate fewer pollutants, product quality, organic products,

biodegradability.

• (2) Synthesize the means by which CSR activities can add value for consumers and how

these have been represented in CSR literature.

• Propose that different CSR activities (and their associated forms of value) impact marketing

outcomes and subsequent firm financial performance through distinct value propositions for

stakeholders.

• (3) Present a research agenda for future research.

Concluding Remarks • The majority of CSR-related research has been published in the

management literature. The management literature tends to highlight the

meaning, obligations and expectations of CSR, as well as the impact of

different CSR issues on firm performance.

• Studies pertaining to CSR found in management literature are primarily

descriptive or qualitative in nature.

• The accounting literature began to emphasize CSR issues around the year

2000. Accounting research has focused primarily on firms’ CSR as well as

CSR disclosure, and the association of those two factors with various

accounting and financial variables.

• Only a few CSR studies have been published in the finance literature.

• CSR research that is featured in accounting and finance literature

investigates specific research questions and establishes causal links by

using empirical data.

91

Concluding Remarks • Main data sources of CSR information:

– Survey/ Media publication

– Content analysis of a firm’s reports (financial reports and stand-alone CSR

reports) and other disclosure documents

– Experiments or case studies

– Databases: • The Kinder, Lynderberg, Domini Research, and Analytics Inc. (KLD) database (providing CSR

information for more than 3,000 firms, which accounts for

98 % of the total market value of all public firms in the U.S.)

• The Asset 4 Thomson Reuters database (with CSR information for 4,000 global firms since 2002)

• The Intangible Value Assessment (IVA) ratings from Innovest Strategic Value Advisors.

• The Bloomberg database (with more than 5 years of data for 4,000 global firms)

• The CRD Analytics (with more than 5 years of sustainability investment data for 1,000 global firms)

• The Dow-Jones Sustainability database (which includes sustainable asset management data dating

back to 1999)

• The FTSE4 Global Index Series (social responsibility index data)

• The Carbon Disclosure Project Leadership Index database (which is the largest database of

corporate climate performance scores)

• The web sites CorporateRegister.com and CSRwire.com.(covering Over 40,000 CSR reports for firms

across 125 countries)

• Toxic Release Inventory (TRI) database

92