lexington-fayette urban county government - 2014 … · maturity schedule $24,190,000...

TRANSCRIPT

OFFICIAL STATEMENT DATED OCTOBER 8, 2014

New Issue – Book Entry Only Ratings: Moody’s : "Aa2"S&P: "AA+ "

(See "RATINGS" herein.)

In the opinion of Peck, Shaffer & Williams, a division of Dinsmore & Shohl LLP, Bond Counsel, under existing law (i)interest on the Series 2014A Bonds is excludible from gross income of the holders thereof for purposes of federal incometaxation; (ii) interest on the Series 2014A Bonds is not be a specific item of tax preference for purposes of the federal alternativeminimum tax imposed on individuals and corporations; (iii) interest on the Series 2014B Bonds is not excludible from grossincome of the holders thereof for purposes of federal income taxation; and (iv) interest on the Series 2014 Bonds is exempt fromKentucky income tax and the Series 2014 Bonds are exempt from ad valorem taxation by the Commonwealth of Kentucky and anyof its political subdivisions, all subject to the qualifications described herein under the heading "TAX MATTERS."

$34,600,000LEXINGTON-FAYETTE URBAN COUNTY GOVERNMENT (KENTUCKY)

SEWER SYSTEM REVENUE REFUNDING BONDSSERIES 2014

$24,190,000Tax-Exempt Sewer System

Revenue Refunding Bonds, Series 2014A

$10,410,000Taxable Sewer System

Revenue Refunding Bonds, Series 2014B

Dated: Date of Delivery Due: As Shown on Inside Cover

The above-captioned Series 2014A Bonds and Series 2014B Bonds (together the "Series 2014 Bonds") of theLexington-Fayette Urban County Government (the “Issuer”) were sold pursuant to a competitive sale as provided in the OfficialTerms and Conditions of Bond Sale. The Series 2014 Bonds shall be dated, bear interest at the rates, and mature, all as set forthon the inside cover pages hereof. The Series 2014 Bonds shall bear interest semiannually on each March 1 and September 1 tomaturity, commencing March 1, 2015. The Series 2014 Bonds are subject to redemption prior to maturity as described herein.

The Series 2014 Bonds will be initially issued as fully registered bonds in book entry form in the name of TheDepository Trust Company ("DTC") or its nominee. There will be no distribution of Series 2014 Bonds to owners of book entryinterests. So long as DTC or its nominee is the sole registered owner, DTC will receive all payments of principal and interestwith respect to the Series 2014 Bonds from The Bank of New York Mellon Trust Company, N.A., Louisville, Kentucky, astrustee and paying agent (the "Trustee"). DTC is required by its rules and procedures to remit such payments to participants inDTC for subsequent disbursement to the owners of book entry interests. So long as DTC or its nominee is the registered ownerof the Series 2014 Bonds, references herein to the Bondholders or registered owners (other than under the captions "TAXMATTERS", "LEGAL MATTERS" and "CONTINUING DISCLOSURE") shall mean DTC or its nominee, and not the ownersof book entry interests in the Series 2014 Bonds. The Series 2014 Bonds will be issued in denominations of $5,000 each orintegral multiples thereof.

The Series 2014 Bonds are being issued by the Issuer for the purpose of (i) currently refunding the entire outstandingprincipal amount of its Taxable Sewer Revenue Bonds, Series 2009 (Build America Bonds – Direct Pay); (ii) advance refundingthe entire outstanding principal amount of its Sewer System Revenue Refunding Bonds, Series 2010A; and (iii) paying the costsof issuance of the Series 2014 Bonds. See “PURPOSE AND PLAN OF REFUNDING” herein.

The Series 2014 Bonds will be secured by a Master Trust Agreement, dated as of September 1, 2014, as amended andsupplemented by a First Supplemental Trust Agreement, dated as of the date of the Series 2014 Bonds (together, the “TrustAgreement”), by and between the Trustee and the Issuer. Pursuant to the Trust Agreement, the payment of the Debt ServiceCharges on the Series 2014 Bonds, and any future Additional Bonds to be issued on parity therewith, shall be secured by a pledgeof the Pledged Revenues of the Sewer System of the Issuer, including the Revenue Fund created under the Trust Agreement.

THE SERIES 2014 BONDS ARE SPECIAL AND LIMITED REVENUE OBLIGATIONS OF THE ISSUER ANDDO NOT CONSTITUTE A DEBT, GENERAL OBLIGATION, AN INDEBTEDNESS, OR PLEDGE OF THE FAITH ANDCREDIT OR LIABILITY OF THE ISSUER, THE COMMONWEALTH OF KENTUCKY OR OF ANY AGENCY ORPOLITICAL SUBDIVISION THEREOF WITHIN THE MEANING OF THE CONSTITUTION OR STATUTES OF THECOMMONWEALTH OF KENTUCKY, AND THE SERIES 2014 BONDS ARE PAYABLE SOLELY FROM AND SECUREDBY THE PLEDGED REVENUES OF THE SEWER SYSTEM, INCLUDING THE REVENUE FUND CREATED UNDERTHE TRUST AGREEMENT. NEITHER THE CREDIT NOR THE TAXING POWER OF THE ISSUER, THECOMMONWEALTH OF KENTUCKY OR ANY AGENCY OR POLITICAL SUBDIVISION THEREOF IS PLEDGED TOTHE PAYMENT OF THE PRINCIPAL OF OR INTEREST ON THE SERIES 2014 BONDS.

The Series 2014 Bonds are offered when, as and if issued, subject to the approval of legality and tax treatment by Peck,Shaffer & Williams, a division of Dinsmore & Shohl LLP, Bond Counsel, Lexington, Kentucky. The Series 2014 Bonds areexpected to be available for delivery on or about October 23, 2014.

THIS COVER PAGE CONTAINS CERTAIN INFORMATION FOR QUICK REFERENCE ONLY. IT IS NOT ASUMMARY OF THIS ISSUE. INVESTORS MUST READ THE ENTIRE OFFICIAL STATEMENT TO OBTAININFORMATION ESSENTIAL TO THE MAKING OF AN INFORMED INVESTMENT DECISION.

HUTCHINSON, SHOCKEY, ERLEY & CO.(Series 2014A Bonds)

CITIGROUP(Series 2014B Bonds

MATURITY SCHEDULE

$24,190,000

Lexington-Fayette Urban County Government (Kentucky)

Tax-Exempt Sewer System Revenue Refunding Bonds

Series 2014A

Year

(September 1)

Amount

Interest

Rate

Price

Yield

CUSIP†

2018 $ 500,000 5.000% 115.707 0.850% 528902 JF7

2019 1,800,000 5.000% 117.922 1.190% 528902 JG5 2020 2,945,000 5.000% 119.796 1.460% 528902 JH3 2021 3,095,000 5.000% 121.051 1.730% 528902 JJ9 2022 1,490,000 5.000% 121.949 1.970% 528902 JK6 2023 1,560,000 4.000% 115.278 2.100% 528902 JL4 2024 1,630,000 5.000% 124.885 2.180% 528902 JM2 2025 1,695,000 3.000% 104.788

* 2.450% 528902 JN0

2026 1,755,000 4.000% 113.215* 2.480% 528902 JP5

2027 1,825,000 4.000% 112.563* 2.550% 528902 JQ3

2028 1,895,000 3.000% 99.000 3.089% 528902 JR1 2029 1,960,000 4.000% 111.180

* 2.700% 528902 JS9

2030 2,040,000 4.000% 110.633* 2.760% 528902 JT7

TOTAL $24,190,000

______

*Priced to the September 1, 2024 call date.

$10,410,000

Lexington-Fayette Urban County Government (Kentucky)

Taxable Sewer System Revenue Refunding Bonds

Series 2014B

Year

(September 1)

Amount

Interest

Rate

Price

Yield

CUSIP†

2015 $2,290,000 5.000% 104.030 0.280% 528902 JU4

2016 2,410,000 5.000% 108.009 0.650% 528902 JV2 2017 2,540,000 5.000% 110.932 1.100% 528902 JW0 2018 2,165,000 5.000% 113.062 1.500% 528902 JX8 2019 1,005,000 5.000% 114.561 1.850% 528902 JY6

TOTAL $10,410,000

† Copyright 2014, CUSIP Global Services. CUSIP is a registered trademark of the American Bankers Association.

CUSIP Global Services is managed on behalf of the American Bankers Association by Standard & Poor’s. CUSIP

data herein are provided by Standard & Poor’s, CUSIP Service Bureau, a Division of The McGraw-Hill Companies,

Inc. The CUSIP numbers listed are being provided solely for the convenience of the holders only at the time of

issuance of the Series 2014 Bonds, and the Lexington-Fayette Urban County Government does not make any

representations with respect to such numbers or undertake any responsibility for their accuracy now or at any time in

the future. The CUSIP number for a specific maturity is subject to being changed after the issuance of the Series

2014 Bonds as a result of various subsequent actions, including, but not limited to, a refunding in whole or in part of

such maturity or as a result of the procurement of secondary market portfolio insurance or other similar

enhancement by investors that is applicable to all or a portion of certain maturities of the Series 2014 Bonds.

REGARDING THIS OFFICIAL STATEMENT

This Official Statement does not constitute an offering of any security other than theoriginal offering of the Series 2014 Bonds of the Lexington-Fayette Urban County Government(the “Issuer”). No dealer, broker, salesman or other person has been authorized by the Issuer togive any information or to make any representation, other than those contained in this OfficialStatement, and, if given or made, such other information or representations must not be reliedupon as having been authorized by the Issuer. This Official Statement does not constitute anoffer to sell or the solicitation of an offer to buy, nor shall there be any sale of the Series 2014Bonds by any person in any jurisdiction in which it is unlawful for such person to make suchoffer, solicitation or sale.

The information and expressions of opinion herein are subject to change without notice.Neither the delivery of this Official Statement nor any sale made hereunder shall, under anycircumstances, create any implication that there has been no change in the affairs of the Issuersince the date hereof.

Upon issuance, the Series 2014 Bonds will not be registered by the Issuer under anyfederal or state securities law, and will not be listed on any stock or other securities exchange.Neither the Securities and Exchange Commission nor any other federal, state, municipal or othergovernmental entity or agency except the Issuer will have, at the request of the Issuer, passedupon the accuracy or adequacy of this Official Statement or approved the Series 2014 Bonds forsale.

All financial and other information presented in this Official Statement has been providedby the Issuer from its records, except for information expressly attributed to other sources. Thepresentation of information, including tables of receipts from taxes and other sources, is intendedto show recent historic information, and is not intended to indicate future or continuing trends inthe financial position or other affairs of the Issuer. No representation is made that pastexperience, as is shown by that financial and other information, will necessarily continue or berepeated in the future.

Insofar as the statements contained in this Official Statement involve matters of opinionor estimates, even if not expressly stated as such, such statements are made as such and not asrepresentations of fact or certainty, no representation is made that any of such statements havebeen or will be realized, and such statements should be regarded as suggesting independentinvestigation or consultation of other sources prior to the making of investment decisions.Certain information may not be current; however, attempts were made to date and documentsources of information. Neither this Official Statement nor any oral or written representations byor on behalf of the Issuer preliminary to sale of the Series 2014 Bonds should be regarded as partof the contract of the Issuer with the successful bidder or the holders from time to time of theSeries 2014 Bonds.

References herein to provisions of Kentucky law, whether codified in the KentuckyRevised Statutes ("KRS") or uncodified, or to the provisions of the Kentucky Constitution or theordinances or resolutions of the Issuer, are references to such provisions as they presently exist.Any of these provisions may from time to time be amended, repealed or supplemented.

ii

As used in this Official Statement, "debt service" means principal of, interest and anypremium on, the obligations referred to; and "State" or "Kentucky" means the Commonwealth ofKentucky.

[Remainder of page intentionally left blank]

iii

LEXINGTON-FAYETTE URBAN COUNTY GOVERNMENT

MayorJim Gray

Council Members at LargeLinda Gorton (Vice Mayor)

Chuck Ellinger IISteve Kay

Council Members by District

1st DistrictChris Ford

5th DistrictBill Farmer, Jr.

9th DistrictJennifer Mossotti

2nd DistrictShevawn Akers

6th DistrictKevin O. Stinnett

10th DistrictHarry Clarke

3rd DistrictDiane Lawless

7th DistrictJennifer Scutchfield

11th DistrictPeggy Henson

4th DistrictJulian Beard

8th DistrictGeorge Myers

12th DistrictEd Lane

Commissioner of FinanceWilliam O'Mara

Clerk of the Lexington-Fayette Urban County CouncilMeredith Nelson

Division of Water QualityCharles H. Martin, P.E., Director

TRUSTEEThe Bank of New York Mellon Trust Company, N.A.

Louisville, Kentucky

FINANCIAL ADVISORRaymond James & Associates, Inc.

Lexington, Kentucky

BOND COUNSELPeck, Shaffer & Williams, a division of Dinsmore & Shohl LLP

Lexington, Kentucky

iv

TABLE OF CONTENTS

REGARDING THIS OFFICIAL STATEMENT ............................................................................ I

INTRODUCTION .......................................................................................................................... 1

The Issuer.................................................................................................................................. 1Purpose of the Series 2014 Bonds ............................................................................................ 1Original Issuance of the Series 2009 Bonds as Build America Bonds ..................................... 2Security and Source of Payment for the Series 2014 Bonds as Parity Bonds .......................... 3Parties to the Issuance of the Series 2014 Bonds...................................................................... 3Authority for Issuance............................................................................................................... 3Description of the Series 2014 Bonds....................................................................................... 4Tax Matters ............................................................................................................................... 4Offering and Delivery of the Series 2014 Bonds...................................................................... 5Disclosure Information ............................................................................................................. 5Additional Information ............................................................................................................. 5

DESCRIPTION OF THE SERIES 2014 BONDS.......................................................................... 6

General ...................................................................................................................................... 6Redemption Provisions ............................................................................................................. 7Book-Entry-Only System.......................................................................................................... 8

SECURITY AND SOURCE OF PAYMENT FOR THE SERIES 2014 BONDS....................... 11

General .................................................................................................................................... 11Rate Covenant......................................................................................................................... 11Historical Debt Service Coverage........................................................................................... 12Additional Bonds and Borrowing Plans ................................................................................. 13

PURPOSE OF THE SERIES 2014 BONDS AND PLAN OF REFUNDING............................. 14

Purpose of the Series 2014 Bonds .......................................................................................... 14Issuance of the Prior Bonds .................................................................................................... 14Redemption of the Series 2009 Bonds as Build America Bonds............................................ 15Plan of Refunding ................................................................................................................... 15Verification of Mathematical Accuracy.................................................................................. 18Sources and Uses of Funds ..................................................................................................... 18

PRINCIPAL AND INTEREST REQUIREMENTS ON THE SERIES 2014 BONDS ANDCURRENT OUTSTANDING OBLIGATIONS .......................................................................... 19

Prior Bonds ............................................................................................................................. 19Principal and Interest Requirements with respect to the Series 2014 Bonds.......................... 19Other Sewer System Obligations ............................................................................................ 20Estimated Principal and Interest Requirements with respect to the Series 2014 Bonds and theOther Sewer System Obligations ............................................................................................ 21

INVESTMENT CONSIDERATIONS ......................................................................................... 22

THE ISSUER................................................................................................................................ 22

THE SEWER SYSTEM ............................................................................................................... 23

v

General .................................................................................................................................... 23Consent Decree ....................................................................................................................... 24Administration and Management of the Sewer System.......................................................... 25The Service Area..................................................................................................................... 30Customer History.................................................................................................................... 31Waste Water Treatment Plants................................................................................................ 32Blue Sky Wastewater Treatment Plant ................................................................................... 33Pump Stations ......................................................................................................................... 34Rates and Charges................................................................................................................... 34

TAX MATTERS........................................................................................................................... 37

Series 2014A Bonds................................................................................................................ 37Series 2014B Bonds................................................................................................................ 39

CONTINUING DISCLOSURE.................................................................................................... 40

Corrective Action Related to Certain Disclosure Requirements ............................................ 40

UNDERWRITING ....................................................................................................................... 41

LEGAL MATTERS...................................................................................................................... 41

RATINGS ..................................................................................................................................... 42

FINANCIAL ADVISOR .............................................................................................................. 43

MISCELLANEOUS ..................................................................................................................... 44

Appendices

APPENDIX A Summary of Certain DefinitionsAPPENDIX B Summary of Certain Provisions of the Trust Agreement and First

Supplemental Trust AgreementAPPENDIX C Certain Operating Data Regarding the Sewer SystemAPPENDIX D Comprehensive Annual Financial Report for the Fiscal Year Ended

June 30, 2013APPENDIX E-1 Form of Legal Approving Opinion of Bond Counsel (Series 2014A

Bonds)APPENDIX E-2 Form of Legal Approving Opinion of Bond Counsel (Series 2014B Bonds)APPENDIX F Form of Continuing Disclosure Certificate

INTRODUCTION

The purpose of this Official Statement, which includes the cover page and appendiceshereto, is to provide certain information with respect to the issuance of $34,600,000 aggregateprincipal amount of Sewer System Revenue Bonds by the Lexington-Fayette Urban CountyGovernment (the “Issuer”), consisting of the following:

(a) $24,190,000 Tax-Exempt Sewer System Revenue Refunding Bonds,Series 2014A (the "Series 2014A Bonds"); and

(b) $10,410,000 Taxable Sewer System Revenue Refunding Bonds, Series2014B (the "Series 2014B Bonds" and together with the Series 2014A Bonds, the "Series2014 Bonds").

This introduction is not a summary of this Official Statement. It is only a briefdescription of and guide to, and is qualified by, more complete and detailed informationcontained in the entire Official Statement, including the cover page and appendices hereto, andthe documents summarized or described herein. A full review should be made of the entireOfficial Statement. The offering of the Series 2014 Bonds to potential investors is made only bymeans of the entire Official Statement.

Terms used, but not defined, in this Official Statement are used as defined in the MasterTrust Agreement, dated as of September 1, 2014 (the “Master Trust Agreement”), as amendedand supplemented by a First Supplemental Trust Agreement, dated as of the date of issuance ofthe Series 2014 Bonds (the “First Supplement” and together, with the Master Trust Agreement,the “Trust Agreement”), by and between the Issuer and The Bank of New York Mellon TrustCompany, N.A., Louisville, Kentucky, as trustee (the “Trustee”). A summary of such definitionsis provided in Appendix A – “SUMMARY OF CERTAIN DEFINITIONS.”

The Issuer

The Series 2014 Bonds are being issued by the Lexington-Fayette Urban CountyGovernment, a political subdivision of the Commonwealth of Kentucky created on April 15,1974 by the merger of the City of Lexington with the County of Fayette. It exists as the singleunit of general local government exercising jurisdiction throughout the geographical boundariesof Fayette County, Kentucky. The Issuer owns and operates a sanitary sewer system (the “SewerSystem”), the services of which are, and are to be, supplied to persons and corporations withinthe jurisdiction of the Sewer System.

Purpose of the Series 2014 Bonds

The proceeds from the sale of the Series 2014 Bonds will be used to:

(i) currently refund the entire outstanding principal amount of the Lexington-Fayette Urban County Government Taxable Sewer Revenue Bonds, Series 2009 (BuildAmerica Bonds - Direct Pay), dated October 22, 2009, issued in the original principalamount of $35,960,000 and currently outstanding in the principal amount of $30,280,000(the “Series 2009 Bonds”);

2

(ii) advance refund the entire outstanding principal amount of the Lexington-Fayette Urban County Government Sewer System Revenue Refunding Bonds, Series2010A, dated May 13, 2010, issued in the original principal amount of $13,860,000, andcurrently outstanding in the principal amount of $11,740,000 (the “Series 2010 Bonds”and together with the Series 2009 Bonds, the “Prior Bonds”); and

(iii) paying the costs of issuance of the Series 2014 Bonds,

all as further described herein under the heading “PURPOSE AND PLAN OF REFUNDING.”

Original Issuance of the Series 2009 Bonds as Build America Bonds

Pursuant to Sections 54AA(g) and 6431 of the Internal Revenue Code of 1986, asamended (the “Code”) (added to the Code by the American Recovery and Reinvestment Act of2009), the Series 2009 Bonds were issued as taxable Build America Bonds (Direct Pay) tofinance capital expenditures. In connection with such issuance, the Issuer elected to receivepayments (the “BAB Interest Subsidy Payments”) directly from the United States Treasury in anamount equal to 35% of the corresponding interest payable on such Series 2009 Bonds on eachinterest payment date.

As provided in Ordinance No. 221-2009, adopted by the Lexington-Fayette UrbanCounty Council (the “Legislative Authority”) on October 15, 2009, authorizing the Series 2009Bonds (the “Series 2009 Bond Ordinance”) and the Official Statement with respect to the Series2009 Bonds, in the event that the United States Treasury or any agency of the United States ofAmerica should at any time cease to remit to the Issuer all or any part of the BAB InterestSubsidy Payments payable with respect to the Series 2009 Bonds, then the Issuer has the right toredeem and retire all or any part of the principal amount of the Series 2009 Bonds thenoutstanding.

As set forth in the 2014 Bond Legislation, based on a reduction in the BAB InterestSubsidy Payments related to the interest payment dates commencing July 1, 2013, the Issuer hasdetermined to exercise its right to redeem all or a portion of the Series 2009 Bonds, provided thatthe federal government has not announced its intention to pay the balance of the reduced BABInterest Subsidy Payments prior to the date of the execution of the Series 2014A Certificate ofAward and the Series 2014B Certificate of Award, following the sale of the Series 2014 Bonds(the “Sale Date”).

See “PURPOSE AND PLAN OF REFUNDING – Redemption of the Series 2009 Bondsas Build America Bonds.”

3

Security and Source of Payment for the Series 2014 Bonds as Parity Bonds

Pursuant to the Trust Agreement, Bond Service Charges on the Series 2014 Bonds will bepaid from the Bond Account created under such Trust Agreement and held by the Trustee. Tosecure payment of Bond Service Charges, the Issuer will assign to the Trustee the PledgedRevenues of the Sewer System, including the Revenue Fund. As further defined in Appendix Ahereto, the Pledged Revenues include the Gross Revenues of the Sewer System and the RevenueFund (as further defined in Appendix A hereto). (See "SECURITY AND SOURCE OFPAYMENT FOR THE SERIES 2014 BONDS" herein.)

THE SERIES 2014 BONDS ARE SPECIAL AND LIMITED REVENUEOBLIGATIONS OF THE ISSUER AND DO NOT CONSTITUTE A DEBT, GENERALOBLIGATION, AN INDEBTEDNESS, OR PLEDGE OF THE FAITH AND CREDIT ORLIABILITY OF THE ISSUER, THE COMMONWEALTH OF KENTUCKY OR OF ANYAGENCY OR POLITICAL SUBDIVISION THEREOF WITHIN THE MEANING OF THECONSTITUTION OR STATUTES OF THE COMMONWEALTH OF KENTUCKY, ANDTHE SERIES 2014 BONDS ARE PAYABLE SOLELY FROM AND SECURED BY THEPLEDGED REVENUES OF THE SEWER SYSTEM, INCLUDING THE REVENUE FUNDCREATED UNDER THE TRUST AGREEMENT. NEITHER THE CREDIT NOR THETAXING POWER OF THE ISSUER, THE COMMONWEALTH OF KENTUCKY OR ANYAGENCY OR POLITICAL SUBDIVISION THEREOF IS PLEDGED TO THE PAYMENT OFTHE PRINCIPAL OF OR INTEREST ON THE SERIES 2014 BONDS.

Parties to the Issuance of the Series 2014 Bonds

The Bank of New York Mellon Trust Company, N.A., Louisville, Kentucky, will serve asthe trustee, bond registrar, paying agent, payee bank, and transfer agent, with respect to theSeries 2014 Bonds (the "Trustee"). Legal matters incident to the issuance of the Series 2014Bonds and with regard to the tax treatment of the interest thereon are subject to the approvinglegal opinion of Peck, Shaffer & Williams, a division of Dinsmore & Shohl LLP, Lexington,Kentucky, as bond counsel (“Bond Counsel”). The Underwriter or Underwriters will be listed onthe cover page of the final Official Statement. The Financial Advisor to the Issuer is RaymondJames & Associates, Inc. (the “Financial Advisor”).

Authority for Issuance

The Series 2014 Bonds will be issued pursuant to (i) Sections 58.010 through 58.140,inclusive, 67A.060 and 82.082 of the Kentucky Revised Statutes (collectively, the “Act”); (ii)Ordinance No. 118-2014 adopted by the Legislative Authority on September 25, 2014,authorizing the Master Trust Agreement (the “General Bond Ordinance”); (iii) Ordinance No.119-2014 adopted by the Legislative Authority on September 25, 2014 authorizing the issuanceof the Series 2014 Bonds (together items (ii), and (iii) are referred to herein as the “2014 BondLegislation”); and (iv) the Trust Agreement.

4

Description of the Series 2014 Bonds

General. The Series 2014 Bonds shall be dated their date of delivery and bear interest atthe rates set forth on the inside cover pages hereof. The Series 2014 Bonds are issuable only asfully registered bonds, without coupons, in the denominations of $5,000 or any integral multiplethereof. Interest on the Series 2014 Bonds shall be payable semi-annually on March 1 andSeptember 1 commencing March 1, 2015. The record dates for March 1 and September 1interest payment dates shall be the preceding February 15 and August 15, respectively (each a“Regular Record Date”).

Book-Entry. The Series 2014 Bonds, when issued, will be registered in the name ofCede & Co., as nominee of The Depository Trust Company, New York, New York (“DTC”),which will act as securities depository for the Series 2014 Bonds. Purchasers will not receivecertificates representing their ownership interest in the Series 2014 Bonds purchased. Principaland any redemption premium related thereto is payable to the registered owner at the designatedcorporate trust office of the Trustee. Interest will be payable by electronic transfer or check ordraft sent by the Trustee to the person who is the registered owner as of the Regular Record Dateimmediately preceding the month of the applicable interest payment date. So long as DTC or itsnominee is the registered owner of the Series 2014 Bonds, payments of the principal of andinterest due on the Series 2014 Bonds will be made directly to DTC by the Trustee. (See"DESCRIPTION OF THE SERIES 2014 BONDS – Book-Entry-Only System" herein.)

Redemption

Optional Redemption. The Series 2014A Bonds maturing on or after September1, 2025 shall be subject to optional redemption prior to maturity on any date on or afterSeptember 1, 2024. (See "DESCRIPTION OF THE SERIES 2014 BONDS -Redemption Provisions - Optional Redemption" herein).

The Series 2014B Bonds are not subject to optional redemption prior to maturity.

Redemption Procedures. The procedures for redemption are set forth hereinunder “DESCRIPTION OF THE SERIES 2014 BONDS - Redemption Provisions –Redemption Procedures.”

Tax Matters

Series 2014A Bonds. In the opinion of Peck, Shaffer & Williams, a division of Dinsmore& Shohl LLP, Bond Counsel, under existing law, interest on the Series 2014A Bonds isexcludible from gross income of the holders thereof for purposes of federal income taxation,pursuant to the Internal Revenue Code of 1986, as amended (the "Code"). Furthermore, intereston the Series 2014A Bonds will not be treated as a specific item of tax preference, under Section57(a)(5) of the Code, in computing the alternative minimum tax for individuals and corporations.In rendering the opinions in this paragraph, Bond Counsel has assumed continuing compliancewith certain covenants designed to meet the requirements of Section 103 of the Code. The Issuerhas not designated the Series 2014 Bonds as "qualified tax-exempt obligations" with respect tocertain financial institutions under Section 265 of the Code. See Appendix E-1 hereto for the

5

form of the opinion that Bond Counsel proposes to deliver in connection with the Series 2014ABonds.

Series 2014B Bonds. In the opinion of Bond Counsel, under existing law, interest on theSeries 2014B Bonds is not excludible from gross income of the holders thereof for purposes offederal income taxation. See Appendix E-2 hereto for the form of the opinion that Bond Counselproposes to deliver in connection with the Series 2014B Bonds.

Kentucky Taxation. Interest on the Series 2014 Bonds is exempt from Kentucky incometaxation and the Series 2014 Bonds are exempt from ad valorem taxation by the Commonwealthof Kentucky and any of its political subdivisions.

*****************************

Bond Counsel expresses no other opinion as to the federal tax consequences ofpurchasing, holding, or disposing of the Series 2014 Bonds.

See “TAX MATTERS” herein.

Offering and Delivery of the Series 2014 Bonds

The Series 2014 Bonds are offered when, as and if issued by the Issuer. The Series 2014Bonds will be delivered on or about October 23, 2014 in New York, New York through theDepository Trust Company (DTC) or by virtue of a “fast close” through DTC.

Disclosure Information

This Official Statement speaks only as of its date, and the information contained herein issubject to change. This Official Statement and continuing disclosure documents of the Issuer areintended to be made available through a continuing disclosure service of the MunicipalSecurities Rulemaking Board’s ("MSRB"), Electronic Municipal Market Access system("EMMA"). Copies of the basic documentation relating to the Series 2014 Bonds, including the2014 Bond Legislation are available from the Issuer.

The Issuer deems this Official Statement to be final for the purposes of Securities andExchange Commission Rule 15c2-12(b)(3) (the "Rule").

Additional Information

Additional information concerning this Official Statement, as well as copies of the basicdocumentation relating to the Series 2014 Bonds, is available from Raymond James &Associates, Inc., 489 East Main Street, Lexington, Kentucky 40507, telephone (859) 232-8211 or(859) 232-8249, Attn: Bob Pennington or Kristen Millard.

6

DESCRIPTION OF THE SERIES 2014 BONDS

General

The Series 2014 Bonds will be dated as of the date of their delivery, will bear interestpayable at the rates and time and will mature on dates set forth on the inside cover pages of thisOfficial Statement. The Series 2014 Bonds will be issuable only in fully registered form indenomination of $5,000 each, or any integral multiple thereof. The Series 2014 Bonds shall bedelivered to and initially registered in the name of Cede and Co., as registered owner andnominee for the Depository Trust Company, New York, New York (“DTC”). See"DESCRIPTION OF THE SERIES 2014 BONDS – Book-Entry Only System" herein.

Interest accruing on the Series 2014 Bonds shall be payable semiannually on March 1 andSeptember 1 of each year (commencing March 1, 2015). The interest installment on each Series2014 Bond will be paid to the person who is the registered owner thereof as of the close ofbusiness on the Regular Record Date for such interest installment, which Record Date shall bethe close of business on February 15 or August 15, as the case may be, next preceding theapplicable Interest Payment Date (whether or not a business day). Payment of interest shall bemade by electronic transfer or check or draft mailed to the person who is the registered owner onthe applicable Record Date at the address of such owner as it appears on the books of theTrustee. Principal shall be paid when due upon delivery of a matured Series 2014 Bond forpayment at the designated corporate trust office of the Trustee. So long as DTC or its nominee,Cede & Co., is the registered owner of the Series 2014 Bonds, such payments will be madedirectly to Cede & Co. See "DESCRIPTION OF THE SERIES 2014 BONDS – Book-EntryOnly System" herein.

The Series 2014 Bonds are transferable by the registered owner hereof in person or byhis/her attorney duly authorized in writing, at the designated corporate trust office of the Trustee,but only in the manner and subject to the limitations provided in the 2014 Bond Legislation, andupon surrender and cancellation of the applicable Series 2014 Bond(s), duly endorsed for transferor accompanied by an assignment duly executed by the registered owners or his/her authorizedrepresentative.

[Remainder of page intentionally left blank]

7

Redemption Provisions

Optional Redemption. The Series 2014A Bonds maturing on and after September 1,2025 are subject to redemption, in the manner provided in the Trust Agreement, at the option ofthe Issuer, either in whole or in part, in inverse order of their maturity dates or on any date, on orafter September 1, 2024, from any legally available funds, at a redemption price equal to theprincipal amount of the Series 2014A Bonds called for redemption, plus accrued interest withrespect thereto to the date fixed for redemption.

The Series 2014B Bonds are not subject to optional redemption prior to maturity.

Redemption Procedures. The Issuer shall give written notice to the Registrar and theTrustee of its election to redeem in the manner provided in and in accordance with the applicableBond Legislation, of the places where the amounts due upon such redemption are payable, and ofthe redemption date and of the principal amount of each maturity of each series of redeemableSeries 2014 Bonds to be redeemed, which notice shall be given at least 45 days prior to theredemption date or such shorter period as shall be acceptable to the Trustee.

Unless waived by any Holder of Series 2014 Bonds to be redeemed, notice of any suchredemption shall be given by the Registrar and the Trustee, on behalf of the Issuer, by mailing acopy of an official redemption notice by first class mail, postage prepaid, or by sending aconfirmed facsimile, at least 30 days prior to the date fixed for redemption to the registeredHolder or Holders of the Series 2014 Bond or Bonds at the address shown on the Register or atsuch other address as is furnished in writing by such registered Holder to the Registrar and theTrustee; provided that, if less than all of an outstanding Series 2014 Bond of one maturity in abook entry system is to be called for redemption, the Registrar and the Trustee shall give noticeto the Depository or the nominee of the Depository that is the Holder of such Series 2014 Bond,and the selection of the beneficial interests in that Series 2014 Bond to be redeemed shall be atthe sole discretion of the Depository and its participants; provided further, that, in connectionwith any optional redemption, the Registrar and the Trustee may, at the written request of theIssuer, provide for conditional notice of optional redemption to the registered Holder or Holdersof a Series 2014 Bond or Bonds so long as any revocation of such notice is sent by first classmail, postage prepaid or sent by facsimile (immediately followed by written confirmation ofreceipt of such facsimile transmission) to the registered Holder of a Series 2014 Bond or Bondsat least ten Business Days prior to the redemption date.

All official notices of redemption shall be dated and shall state:

(a) the redemption date,

(b) the redemption price,

(c) that on the redemption date, the redemption price will become due andpayable upon each Series 2014 Bond, and that interest thereon shall cease to accrue fromand after said date, and

8

(d) the place where such Series 2014 Bonds are to be surrendered for paymentof the redemption price, which place of payment shall be the designated office of theTrustee.

Prior to any redemption date, the Issuer shall deposit with the Trustee an amount ofmoney sufficient to pay the redemption price of all the Series 2014 Bonds which are to beredeemed on that date, provided, however, no such deposit need be made if a conditional noticeis being sent.

Failure to receive notice by mailing or any defect in that notice regarding any Series 2014Bond, however, shall not affect the validity of the proceedings for the redemption of any Series2014 Bonds.

Notice of any redemption hereunder with respect to Series 2014 Bonds held under a bookentry system shall be given by the Trustee only to the Depository, or its nominee, as the Holderof such Series 2014 Bonds. Selection of book entry interests in the Series 2014 Bonds called forredemption is the responsibility of the Depository and any failure of such Depository to notifythe book entry interest owners of any such notice and its contents or effect will not affect thevalidity of such notice of any proceedings for the redemption of such Series 2014 Bonds.

Book-Entry-Only System

The following information concerning DTC and DTC’s book-entry-only system has beenobtained from DTC and contains statements that are believed to describe accurately DTC, themethod of effecting book-entry transfers of securities distributed through DTC and certainrelated matters, but neither the Issuer nor the Trustee takes any responsibility for the accuracy ofsuch statements.

The Depository Trust Company ("DTC"), New York, NY, will act as securitiesdepository for the Series 2014 Bonds (the "Securities"). The Securities will be issued as fully-registered securities registered in the name of Cede & Co. (DTC’s partnership nominee) or suchother name as may be requested by an authorized representative of DTC. One fully-registeredSecurity certificate will be issued for each issue of the Securities, each in the aggregate principalamount of such issue, and will be deposited with DTC.

DTC, the world’s largest securities depository, is a limited-purpose trust companyorganized under the New York Banking Law, a "banking organization" within the meaning ofthe New York Banking Law, a member of the Federal Reserve System, a "clearing corporation"within the meaning of the New York Uniform Commercial Code, and a "clearing agency"registered pursuant to the provisions of Section 17A of the Securities Exchange Act of 1934.DTC holds and provides asset servicing for over 3.5 million issues of U.S. and non-U.S. equityissues, corporate and municipal debt issues, and money market instruments (from over 100countries) that DTC’s participants ("Direct Participants") deposit with DTC. DTC alsofacilitates the post-trade settlement among Direct Participants of sales and other securitiestransactions in deposited securities, through electronic computerized book-entry transfers andpledges between Direct Participants’ accounts. This eliminates the need for physical movementof securities certificates. Direct Participants include both U.S. and non-U.S. securities brokersand dealers, banks, trust companies, clearing corporations, and certain other organizations. DTC

9

is a wholly-owned subsidiary of The Depository Trust & Clearing Corporation ("DTCC").DTCC is the holding company for DTC, National Securities Clearing Corporation and FixedIncome Clearing Corporation, all of which are registered clearing agencies. DTCC is owned bythe users of its regulated subsidiaries. Access to the DTC system is also available to others suchas both U.S. and non-U.S. securities brokers and dealers, banks, trust companies, and clearingcorporations that clear through or maintain a custodial relationship with a Direct Participant,either directly or indirectly ("Indirect Participants"). DTC has a Standard & Poor’s rating ofAA+. The DTC Rules applicable to its Participants are on file with the Securities and ExchangeCommission. More information about DTC can be found at www.dtcc.com.

Purchases of Securities under the DTC system must be made by or through DirectParticipants, which will receive a credit for the Securities on DTC’s records. The ownershipinterest of each actual purchaser of each Security ("Beneficial Owner") is in turn to be recordedon the Direct and Indirect Participants’ records. Beneficial Owners will not receive writtenconfirmation from DTC of their purchase. Beneficial Owners are, however, expected to receivewritten confirmations providing details of the transaction, as well as periodic statements of theirholdings, from the Direct or Indirect Participant through which the Beneficial Owner entered intothe transaction. Transfers of ownership interests in the Securities are to be accomplished byentries made on the books of Direct and Indirect Participants acting on behalf of BeneficialOwners. Beneficial Owners will not receive certificates representing their ownership interests inSecurities, except in the event that use of the book-entry system for the Securities isdiscontinued.

To facilitate subsequent transfers, all Securities deposited by Direct Participants withDTC are registered in the name of DTC’s partnership nominee, Cede & Co., or such other nameas may be requested by an authorized representative of DTC. The deposit of Securities with DTCand their registration in the name of Cede & Co. or such other DTC nominee do not effect anychange in beneficial ownership. DTC has no knowledge of the actual Beneficial Owners of theSecurities; DTC’s records reflect only the identity of the Direct Participants to whose accountssuch Securities are credited, which may or may not be the Beneficial Owners. The Direct andIndirect Participants will remain responsible for keeping account of their holdings on behalf oftheir customers.

Conveyance of notices and other communications by DTC to Direct Participants, byDirect Participants to Indirect Participants, and by Direct Participants and Indirect Participants toBeneficial Owners will be governed by arrangements among them, subject to any statutory orregulatory requirements as may be in effect from time to time. Beneficial Owners of Securitiesmay wish to take certain steps to augment the transmission to them of notices of significantevents with respect to the Securities, such as redemptions, tenders, defaults, and proposedamendments to the Security documents. For example, Beneficial Owners of Securities may wishto ascertain that the nominee holding the Securities for their benefit has agreed to obtain andtransmit notices to Beneficial Owners. In the alternative, Beneficial Owners may wish to providetheir names and addresses to the Trustee and request that copies of notices be provided directlyto them.

10

Redemption notices shall be sent to DTC. If less than all of the Securities within an issueare being redeemed, DTC’s practice is to determine by lot the amount of the interest of eachDirect Participant in such issue to be redeemed.

Neither DTC nor Cede & Co. (nor any other DTC nominee) will consent or vote withrespect to Securities unless authorized by a Direct Participant in accordance with DTC’s MMIProcedures. Under its usual procedures, DTC mails an Omnibus Proxy to the issuer as soon aspossible after the record date. The Omnibus Proxy assigns Cede & Co.’s consenting or votingrights to those Direct Participants to whose accounts Securities are credited on the record date(identified in a listing attached to the Omnibus Proxy).

Redemption proceeds, distributions, and dividend payments on the Securities will bemade to Cede &. Co., or such other nominee as may be requested by an authorized representativeof DTC. DTC’s practice is to credit Direct Participants’ accounts upon DTC’s receipt of fundsand corresponding detail information from the Issuer, on payable date in accordance with theirrespective holdings shown on DTC’s records. Payments by Participants to Beneficial Ownerswill be governed by standing instructions and customary practices, as is the case with securitiesheld for the accounts of customers in bearer form or registered in "street name," and will be theresponsibility of such Participant and not of DTC or the Issuer, subject to any statutory orregulatory requirements as may be in effect from time to time. Payment of redemption proceeds,distributions, and dividend payments to Cede & Co. (or such other nominee as may be requestedby an authorized representative of DTC) is the responsibility of the Issuer, disbursement of suchpayments to Direct Participants will be the responsibility of DTC, and disbursement of suchpayments to the Beneficial Owners will be the responsibility of Direct and Indirect Participants.

DTC may discontinue providing its services as depository with respect to the Securities atany time by giving reasonable notice to the Issuer. Under such circumstances, in the event that asuccessor depository is not obtained, Security certificates are required to be printed anddelivered.

The Issuer may decide to discontinue use of the system of book-entry-only transfersthrough DTC (or a successor securities depository). In that event, Security certificates will beprinted and delivered to DTC.

The Issuer will not have any responsibility or obligations to any Direct Participants orIndirect Participants or the persons for whom they act with respect to (i) the accuracy of anyrecords maintained by DTC or any such Direct Participant or Indirect Participant; (ii) thepayment by any Participant of any amount due to the Beneficial Owner in respect of theprincipal of, premium, if any, or interest on the Series 2014 Bonds; (iii) the delivery by any suchDirect Participant or Indirect Participant of any notice to any Beneficial Owner that is requiredor permitted to be given to owners of the Series 2014 Bonds; (iv) the selection of the BeneficialOwners to receive payments in the event of any partial redemption of the Series 2014 Bonds; or(v) any consent given or other action taken by DTC as Registered Owner.

11

SECURITY AND SOURCE OF PAYMENT FOR THE SERIES 2014 BONDS

General

The Series 2014 Bonds are equally and ratably secured from, and secured by, a pledgeand assignment of the Pledged Revenues to the Trustee, pursuant to the Trust Agreement. Asfurther defined in Appendix A hereto, the Pledged Revenues include the Gross Revenues of theSewer System and the Revenue Fund (as further defined in Appendix A hereto).

THE SERIES 2014 BONDS ARE SPECIAL AND LIMITED REVENUEOBLIGATIONS OF THE ISSUER AND DO NOT CONSTITUTE A DEBT, GENERALOBLIGATION, AN INDEBTEDNESS, OR PLEDGE OF THE FAITH AND CREDIT ORLIABILITY OF THE ISSUER, THE COMMONWEALTH OF KENTUCKY OR OF ANYAGENCY OR POLITICAL SUBDIVISION THEREOF WITHIN THE MEANING OF THECONSTITUTION OR STATUTES OF THE COMMONWEALTH OF KENTUCKY, ANDTHE SERIES 2014 BONDS ARE PAYABLE SOLELY FROM AND SECURED BY THEPLEDGED REVENUES OF THE SEWER SYSTEM, INCLUDING THE REVENUE FUNDCREATED UNDER THE TRUST AGREEMENT. NEITHER THE CREDIT NOR THETAXING POWER OF THE ISSUER, THE COMMONWEALTH OF KENTUCKY OR ANYAGENCY OR POLITICAL SUBDIVISION THEREOF IS PLEDGED TO THE PAYMENT OFTHE PRINCIPAL OF OR INTEREST ON THE SERIES 2014 BONDS.

Rate Covenant

As set forth in the Trust Agreement, the Issuer will at all times prescribe and charge suchrates for the services of the Sewer System, and will so restrict Operating and MaintenanceExpenses, as shall result in Net Revenues at least adequate to provide for (i) the paymentsrequired by the 2014 Bond Legislation to be made into the Revenue Fund; (ii) sufficient funds topay the Principal and Interest Requirements on any General Obligation Bonds and Notes and allother Obligations of the Issuer incurred for Sewer System purposes; (iii) sufficient earningscoverage to permit the issue of the Additional Bonds required for the construction of necessaryor advisable extensions or improvements of the Sewer System; and (iv) to provide for the normalgrowth and sound operation of the Sewer System.

In no event shall the sum of Net Revenues with respect to each Fiscal Year be less than120% of the aggregate amount of Principal and Interest Requirements on the Bonds payableduring such Fiscal Year and the Issuer will be responsible for delivering to the Trustee evidenceof compliance therewith in accordance with the Trust Agreement; provided, however, that therequired deposits are being made to the applicable funds on an ongoing basis; and providedfurther, however, that if Additional Bonds are issued to pay the cost of Improvements, theportion of the Principal and Interest Requirements thereon that shall be included in thecalculation in each Fiscal Year during the estimated construction period of the Improvementsshall equal the portion of the interest on said Additional Bonds payable during that Fiscal Yearthat has not been funded.

[Remainder of page intentionally left blank]

12

Historical Debt Service Coverage

The table set forth below presents historical debt service coverage for Fiscal Years 2009-2014, applying the debt service coverage provisions of the Trust Agreement retroactively to thecalculation of the Net Revenues of the Sewer System available for the payment of debt servicefor the Fiscal Years 2009-2014 on (i) revenue bonds issued for Sewer System purposes(including the Prior Bonds, when applicable, the “Revenue Bonds”) and (ii) General ObligationBonds and Notes and all other Obligations issued for Sewer System purposes (collectively, the“Other Sewer System Obligations” as further described below), all as outstanding at the end ofsuch respective Fiscal Years, as prepared by the Issuer’s Division of Water Quality.

For additional information please see (i) the definition of “Net Revenues” in Appendix B– “SUMMARY OF CERTAIN PROVISIONS OF THE TRUST AGREEMENT – Definitions”and (ii) pages 45-46 of the Comprehensive Annual Financial Report of the Issuer for the FiscalYear Ended June 30, 2013, attached as Appendix D hereto.

ActualFiscal Year

2009

ActualFiscal Year

2010

ActualFiscal Year

2011

ActualFiscal Year

2012

ActualFiscal Year

2013

UnauditedFiscal Year

2014Gross Revenues

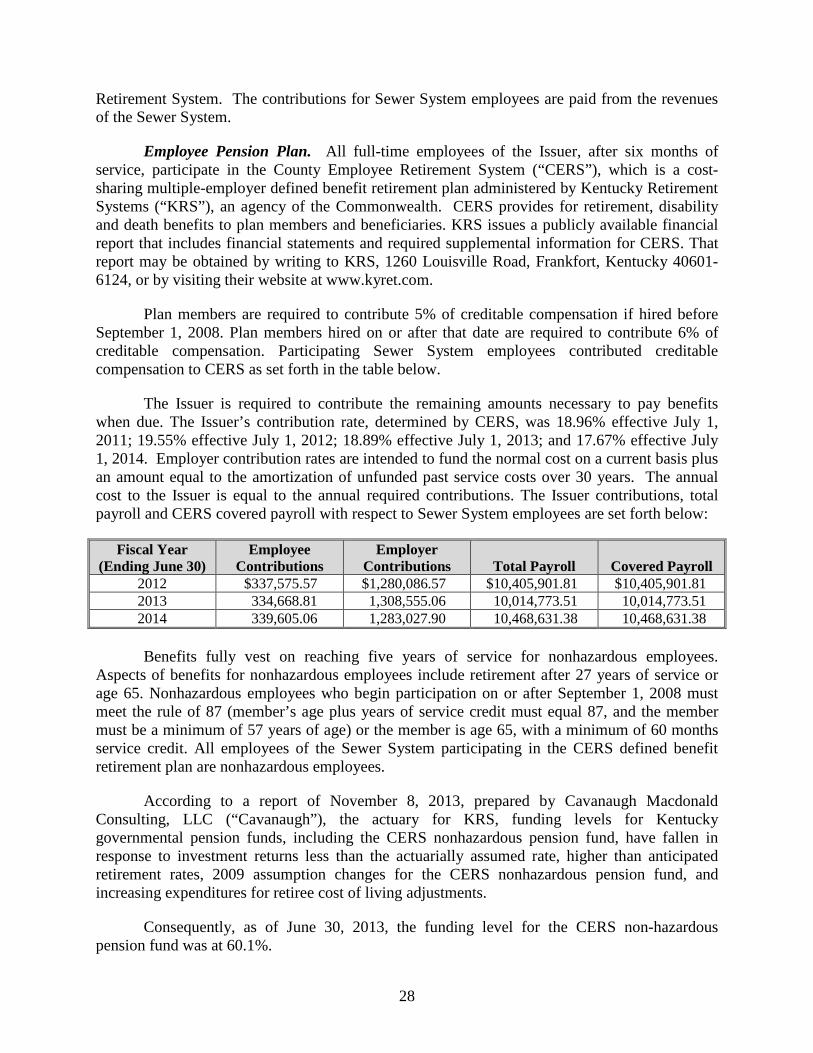

Sewer User Fees $35,144,436 $45,573,537 $45,513,175 $44,305,075 $45,921,141 $46,362,035Tap-on Fees 993,375 928,087 1,528,415 1,768,371 2,202,326 2,017,004Other 217,622 194,770 221,511 260,183 231,417 853,966

Total Revenues $36,355,433 $46,696,393 $47,263,100 46,333,629 $48,354,884 $49,233,005

ExpensesOperating

Personnel $9,760,577 $10,574,004 $11,232,861 $10,405,902 $10,014,774 $10,468,631Operating 13,577,651 16,170,553 14,642,808 13,933,579 13,561,872 16,688,521Insurance 1,275,387 1,181,520 414,125 2,219,282 1,677,387 1,088,430Capital 2,586,981 3,846,550 5,908,141 3,581,321 3,584,770 4,804,830

Total Operating Expenses $27,200,596 $31,772,628 $32,197,937 $30,140,083 $28,838,803 $33,050,413

Operating Income(Net Revenues Available for Debt Service) $9,154,836 $14,923,766 $15,065,164 $16,193,546 $19,516,081 $16,182,592

Debt ServiceRevenue Bonds (Senior) $5,561,138 $5,889,017 $7,118,615 $13,878,356+ $4,957,821 $4,915,285Other Sewer System Obligations 419,264† 856,127† 855,860†

Aggregate Debt Service $5,561,138 $5,889,017 $7,118,615 $14,297,620+ $5,813,948 $5,771,144

Debt Service CoverageDebt Service Coverage Ratio for RevenueBonds (Senior)1 165% 253% 212% 117%+ 394% 329%Aggregate Debt Service Coverage Ratio(Revenue Bonds and Other Sewer SystemObligations)2 165% 253% 212% 113%+ 336% 280%

[NOTES TO THE HISTORICAL DEBT SERVICE COVERAGE TABLE APPEAR ON THE FOLLOWING PAGE]

13

NOTES TO THE HISTORICAL DEBT SERVICE COVERAGE TABLE______+The debt service for FY 2012 reflects accelerated debt payments with respect to the Issuer’s Sewer System Revenue Bonds,Series A of 2001 and Sewer System Refunding Revenue Bonds, Series B of 2001 B due to a timing issue between the scheduleddue date of the debt payments and the fiscal year end.

†See note to table under “PRINCIPAL AND INTEREST REQUIREMENTS ON THE SERIES 2014 BONDS AND CURRENTOUTSTANDING OBLIGATIONS - Other Sewer System Obligations.”

1Equal to Net Revenues divided by Principal and Interest Requirements on the Revenue Bonds which were outstanding at the endof the respective Fiscal Years.

2Equal to Net Revenues divided by Principal and Interest Requirements on the Revenue Bonds and Other Sewer SystemObligations which were outstanding at the end of the respective Fiscal Years.

Additional Bonds and Borrowing Plans

The Issuer may issue Additional Bonds on a parity with the Series 2014 Bonds payablefrom the Pledged Revenues (including without limitation, the Revenue Fund) for the purpose ofmaking additions and improvements to the Sewer System and/or refunding, for any lawfulpurpose, any outstanding Bonds, subject to certain conditions of the Trust Agreement (seeAppendix B - "SUMMARY OF CERTAIN PROVISIONS OF THE TRUST AGREEMENT –Additional Bonds" hereto).

As set forth herein under “THE SEWER SYSTEM – Consent Decree,” the Issueranticipates additional borrowings to comply with a federal consent decree (the “ConsentDecree,” as further defined herein), finalized in January 2011. At the current time, it is estimatedthat the Consent Decree and other capital projects will require an investment of approximately$600 million over approximately 12 years. In order to fully fund the requirements of theConsent Decree and the Trust Agreement, the Issuer anticipates continued rate increases.Anticipated funding for the plan includes a mix of cash funding, Kentucky InfrastructureAuthority State Revolving Fund Loans (subordinate to the Series 2014 Bonds), and additionalBonds. The Issuer has put in place processes to monitor developments and manage costsassociated with the Consent Decree and capital expenditures, including various internalforecasting models which contain a 36-month, rolling monthly forecast and annual forecastthereafter until plan completion. Plan estimates through FY 2019 show capital funding in theamount of approximately $362 million to be funded by approximately $110 million of cash,approximately $127 million of Kentucky Infrastructure Authority State Revolving Fund Loansand approximately $125 million of additional Bonds.

The information on projected capital funding amounts and sources of funds above mayconstitute a "forward looking statement" under federal securities law. Actual revenues,expenses, costs and/or funding amounts could differ materially from those forecasted and therecan be no assurance that such estimates of future results will be achieved. For example, there canbe no assurance that the Legislative Body will approve any new rate schedules, or that theLegislative Body may not from time to time consider amending the rate ordinances related to theSewer System. In general, important factors that could cause actual results to differ materiallyfrom anticipated amounts presently estimated include, but are not limited to, material changes inthe size and composition of the Service Area of the Sewer System, unanticipated changes in law

14

or unanticipated material litigation, efficiency of operations and the capital construction andexpenditure plans and results of the Sewer System.

PURPOSE OF THE SERIES 2014 BONDS AND PLAN OF REFUNDING

Purpose of the Series 2014 Bonds

The proceeds from the sale of the Series 2014 Bonds will be used to:

(i) currently refund the entire outstanding principal amount of the Series 2009Bonds (the “Refunded Series 2009 Bonds,” as further described below), the proceeds ofwhich Series 2009 Bonds were used to finance the construction of major additions,betterment and extensions to the Sewer System, including but not limited to replacementand elimination of various pumping stations, major trunk line rehabilitations and otherrelated facilities, all in accordance with the Capital Plan of the Sewer System;

(ii) advance refund the entire outstanding principal amount of the Series 2010Bonds (the “Refunded Series 2010 Bonds,” as further described below, and together withthe Refunded Series 2009 Bonds, the “Refunded Prior Bonds”), the proceeds of whichSeries 2010 Bonds were used to refund the outstanding principal amount of theLexington-Fayette Urban County Government Sewer System Revenue Bonds, Series Aof 2001; and

(iii) pay the costs of issuance of the Series 2014 Bonds.

Issuance of the Prior Bonds

The financing structure related to the Prior Bonds of the Issuer provided for the issuanceof revenue bonds for the purpose of financing or refinancing improvements to the Sewer Systempursuant to Ordinance No. 96-2001 adopted by Legislative Authority on May 3, 2001 (the“Series 2001 Bond Ordinance”), as amended by the Series 2009 Bond Ordinance. The Series2001 Bond Ordinance also specifically readopted, reapproved, and incorporated by referencecertain designated sections and provisions of Bond Ordinance No. 153-85, adopted by theLegislative Authority on July 25, 1985. The Series 2010 Bonds were issued pursuant to theSeries 2001 Bond Ordinance, as amended by the Series 2009 Bond Ordinance, and OrdinanceNo. 61-2010, adopted by the Legislative Authority on April 29, 2010 (the “Series 2010 BondOrdinance, and collectively with the Series 2001 Bond Ordinance and the Series 2009 BondOrdinance, the “Prior Ordinance”).

Pursuant to the Prior Ordinance, the payment of principal and interest on the Prior Bondsis payable solely from and secured by a pledge of, a fixed portion of the gross income andrevenues of the Sewer System set aside in a sinking fund established under such Prior Ordinanceto pay such principal and interest when due. Upon the deposit of the applicable portions of theproceeds of the Series 2014 Bonds into the Refunded Series 2009 Escrow Fund and theRefunded Series 2010 Escrow Fund (as described below under “PURPOSE AND PLAN OFREFUNDING – Plan of Refunding”), such revenue pledge shall be fully defeased and releasedwithout any further action necessary.

15

Redemption of the Series 2009 Bonds as Build America Bonds

As provided in the Series 2009 Bond Ordinance and the Official Statement with respectto the Series 2009 Bonds, in the event that the United States Treasury or any agency of theUnited States of America should at any time cease to remit to the Issuer all or any part of theBAB Interest Subsidy Payments payable with respect to the Series 2009 Bonds, then the Issuerhas the right to redeem and retire all or any part of the principal amount of Series 2009 Bondsthen outstanding, in any order of maturities (less than all of a single maturity to be selected bylot), on any date upon 30 days’ written notice by regular United States Mail to the holders of theSeries 2009 Bonds upon terms of the principal amount so redeemed plus accrued interest to theredemption date but without premium.

Following a statement by the United States Treasury that interest subsidy payments madeto issuers of direct pay bonds would be reduced, the Issuer received a reduced BAB InterestSubsidy Payment in an amount less than 35% of the corresponding interest due and payable onthe Series 2009 Bonds on July 1, 2013 and has continued to receive reduced BAB InterestSubsidy Payments with respect to the interest payment dates thereafter (the “Reduced BABInterest Subsidy Payments”).

Pursuant to the 2014 Bond Legislation, the Issuer has determined to exercise its right toredeem all or a portion of the Series 2009 Bonds, provided that the federal government has notannounced its intention to pay the balance of the Reduced BAB Interest Subsidy Payments priorto the Sale Date. If such an announcement is made prior to the Sale Date, then the Issuer wouldhave no obligation or authority to redeem all or a portion of the Series 2009 Bonds.

Plan of Refunding

On the date of issuance of the Series 2014 Bonds, a portion of the proceeds thereof willbe applied to the refunding of the entire outstanding principal amount of the Refunded PriorBonds as follows:

(a) A portion of the proceeds of the Series 2014A Bonds (and other monies ofthe Issuer), will be applied to the current refunding, defeasance and legal discharge of theentire outstanding principal amount of the Refunded Series 2009 Bonds through thedeposit thereof in a separate and distinct irrevocable escrow fund for such RefundedSeries 2009 Bonds (the “Refunded Series 2009 Escrow Fund”), to be held by The Bankof New York Mellon Trust Company, N.A., Louisville, Kentucky, as escrow trustee (the"Series 2009 Escrow Trustee") under an Escrow Trust Agreement, dated October 23,2014 (the “Series 2009 Escrow Agreement”), by and between the Issuer and the Series2009 Escrow Trustee. The Series 2009 Escrow Trustee will hold such deposit uninvestedin the Refunded Series 2009 Escrow Fund, to pay the principal of and interest on theRefunded Series 2009 Bonds when due through November 25, 2014 (the "Series 2009Bonds Redemption Date"), and to redeem the Refunded Series 2009 Bonds on suchSeries 2009 Bonds Redemption Date, at a redemption price of 100% of the principalamount thereof, plus accrued interest thereon to the Series 2009 Bonds Redemption Date.See "VERIFICATION OF MATHEMATICAL ACCURACY" herein. Upon the makingof the foregoing deposit with the Series 2009 Escrow Trustee, the Refunded Series 2009

16

Bonds will no longer be deemed to be outstanding under the Series 2009 Bond Ordinanceand the indebtedness with respect thereto will be discharged.

(b) A portion of the proceeds of the Series 2014B Bonds (and other monies ofthe Issuer) will be applied to the advance refunding, defeasance and legal discharge of theentire outstanding principal amount of the Refunded Series 2010 Bonds through thedeposit thereof in a separate and distinct irrevocable escrow fund for such RefundedSeries 2010 Bonds (the “Refunded Series 2010 Escrow Fund”), to be held by The Bankof New York Mellon Trust Company, N.A., Louisville, Kentucky, as escrow trustee (the"Series 2010 Escrow Trustee") under an Escrow Trust Agreement, dated October 23,2014 (the “Series 2010 Escrow Agreement”), by and between the Issuer and the Series2010 Escrow Trustee. The Series 2010 Escrow Trustee will apply a portion of the moneyon deposit in the Refunded Series 2010 Escrow Fund to the purchase of certain directobligations of the United States of America (the "United States Treasury Obligations"),which will earn interest at such rates and mature on such dates so as to provide sufficientfunds, together with any cash held uninvested in the Refunded Series 2010 Escrow Fund,to pay the principal of and interest on the Refunded Series 2010 Bonds as same becomesdue through July 1, 2021, which is the final maturity date of the Series 2010 Bonds. See"VERIFICATION OF MATHEMATICAL ACCURACY" herein. Upon the making ofthe foregoing deposit with the Series 2010 Escrow Trustee, the Refunded Series 2010Bonds will no longer be deemed to be outstanding under the Series 2010 Bond Ordinanceand the indebtedness with respect thereto will be discharged.

Upon the issuance of the Series 2014 Bonds, all Prior Bonds will be fully defeased andthe Series 2014 Bonds will be the only Bonds outstanding under the Trust Agreement.

[Remainder of page intentionally left blank]

17

Refunded Series 2009 Bonds

Maturity Date(July 1)

OutstandingPrincipalAmount Interest Rate Redemption Date

RedemptionPrice

Serial Bonds

2015 $1,490,000 3.750% 11/25/2014 100%2016 1,530,000 4.250% 11/25/2014 100%2017 1,575,000 4.250% 11/25/2014 100%2018 1,620,000 4.375% 11/25/2014 100%2019 1,665,000 4.500% 11/25/2014 100%2025 2,010,000 5.375% 11/25/2014 100%2026 2,085,000 5.500% 11/25/2014 100%2027 2,160,000 5.625% 11/25/2014 100%2028 2,240,000 5.750% 11/25/2014 100%2029 2,330,000 5.750% 11/25/2014 100%2030 2,420,000 5.875% 11/25/2014 100%

Term Bond

20241 9,155,000 4.80% 11/25/2014 100%TOTAL $30,280,000

_______1The entire outstanding principal amount of the Series 2009 Term Bond maturing on July 1, 2024 will be currentlyrefunded.

Refunded Series 2010 Bonds

The Series 2010 Bonds are not subject to optional redemption prior to maturity. Aportion of the proceeds of the Series 2014B Bonds will be used to provide for the defeasance andadvance refunding of the Refunded Series 2010 Bonds by a deposit into the Refunded Series2010 Escrow Fund in the amount required for the payment of principal and interest when due onsuch Refunded Series 2010 Bonds through the final maturity.

Maturity Date(July 1)

OutstandingPrincipalAmount Interest Rate Payment Date

Serial Bonds2015 $1,515,000 2.625% 07/01/20152016 1,560,000 3.000% 07/01/20162017 1,615,000 3.375% 07/01/20172018 1,670,000 3.500% 07/01/20182019 1,730,000 3.500% 07/01/20192020 1,790,000 3.625% 07/01/20202021 1,860,000 3.750% 07/01/2021

TOTAL $11,740,000

18

Verification of Mathematical Accuracy

Grant Thornton LLP (the "Verification Agent") will deliver to the Issuer, on or before thesettlement date of the Series 2014 Bonds, its report indicating that it has examined theinformation and assertions provided by the Issuer and its representatives. Included in the scopeof its examination will be a verification of the mathematical accuracy of (a) the computations ofthe adequacy of the cash and/or the maturing principal of and interest on the defeasancesecurities deposited in the Refunded Series 2009 Escrow Fund to pay, when due, the maturingprincipal, interest, and redemption premium, if any, on the Refunded Series 2009 Bonds on orprior to the Redemption Date; (b) the computations of the adequacy of the cash and/or thematuring principal of and interest on the defeasance securities deposited in the Refunded Series2010 Escrow Fund to pay, when due, the maturing principal and interest due on the RefundedSeries 2010 Bonds through final maturity; and (c) the computations supporting the conclusion ofBond Counsel that the Series 2014A Bonds are not "arbitrage bonds" under the Code and theregulations promulgated thereunder. The Verification Agent has expressed no opinion on theassumptions provided to them, nor as to the exemption from income taxation of interest on theSeries 2014A Bonds.

Sources and Uses of Funds

The following table sets forth the sources and uses of funds by the Issuer in connectionwith the issuance of the Series 2014 Bonds and the refunding of the Prior Bonds:

Sources Series 2014A Series 2014B TotalSeries 2014 Bond Proceeds

Par Amount $24,190,000.00 $10,410,000.00 $34,600,000.00Net Premium 3,566,099.85 992,107.05 4,558,206.90Total Bond Proceeds $27,756,099.85 $11,402,107.05 $39,158,206.90

Other SourcesDeposit from the Debt Service Reserve Fund

with respect to the Prior Bonds 3,470,920.08 1,445,669.92 4,916,590.00

TOTAL SOURCES $31,227,019.93 $12,847,776.97 $44,074,796.90UsesDeposit to respective Escrow Fund

Cash Deposit $30,888,896.00 $ 195.50 $30,889,091.50Purchase of United States Treasury Obligations 0.00 12,732,650.43 12,732,650.43

Bond Issuance Expenses(1) 338,123.93 114,931.04 453,054.97TOTAL USES $31,227,019.93 $12,847,776.97 $44,074,796.90

__________(1) Includes underwriter’s discount, printing costs, rating agency fees, legal fees, fees of the Trustee, fees of theEscrow Agent, and other issuance costs.

[Remainder of page intentionally left blank]

19

PRINCIPAL AND INTEREST REQUIREMENTS ON THE SERIES 2014 BONDSAND CURRENT OUTSTANDING OBLIGATIONS

Prior Bonds

The following Prior Bonds of the Issuer are currently outstanding under the PriorOrdinances, to be refunded in full with a portion of the proceeds of the Series 2014 Bonds.

Date ofOriginal

Issue Description Interest RateFinal

MaturityOriginal

Amount IssuedAmount

Outstanding10/22/2009 Series 2009 Bonds 3.750%-5.875% 07/01/2030 $35,960,000 $30,280,00005/13/2010 Series 2010 Bonds 2.625%-3.750% 07/01/2021 13,860,000 11,740,000TOTAL $49,820,000 $42,020,000

Upon issuance, the Series 2014 Bonds will be the only Outstanding Bonds under theTrust Agreement.

Principal and Interest Requirements with respect to the Series 2014 Bonds

The following table sets forth the Principal and Interest Requirements with respect to theSeries 2014 Bonds.

Series 2014A Bonds Series 2014B BondsPeriodEnding Principal Interest Principal Interest

PeriodDebt Service

Annual DebtService

3/1/2015 $372,017.78 $185,066.67 $ 557,084.45 $ 557,084.45

9/1/2015 523,150.00 $2,290,000 260,250.00 3,073,400.00

3/1/2016 523,150.00 203,000.00 726,150.00 3,799,550.00

9/1/2016 523,150.00 2,410,000 203,000.00 3,136,150.00

3/1/2017 523,150.00 142,750.00 665,900.00 3,802,050.00

9/1/2017 523,150.00 2,540,000 142,750.00 3,205,900.00

3/1/2018 523,150.00 79,250.00 602,400.00 3,808,300.00

9/1/2018 $ 500,000 523,150.00 2,165,000 79,250.00 3,267,400.00

3/1/2019 510,650.00 25,125.00 535,775.00 3,803,175.00

9/1/2019 1,800,000 510,650.00 1,005,000 25,125.00 3,340,775.00

3/1/2020 465,650.00 465,650.00 3,806,425.00

9/1/2020 2,945,000 465,650.00 3,410,650.00

3/1/2021 392,025.00 392,025.00 3,802,675.00

9/1/2021 3,095,000 392,025.00 3,487,025.00

3/1/2022 314,650.00 314,650.00 3,801,675.00

9/1/2022 1,490,000 314,650.00 1,804,650.00

3/1/2023 277,400.00 277,400.00 2,082,050.00

9/1/2023 1,560,000 277,400.00 1,837,400.00

3/1/2024 246,200.00 246,200.00 2,083,600.00

20

Series 2014A Bonds Series 2014B BondsPeriodEnding Principal Interest Principal Interest

PeriodDebt Service

Annual DebtService

9/1/2024 1,630,000 246,200.00 1,876,200.00

3/1/2025 205,450.00 205,450.00 2,081,650.00

9/1/2025 1,695,000 205,450.00 1,900,450.00

3/1/2026 180,025.00 180,025.00 2,080,475.00

9/1/2026 1,755,000 180,025.00 1,935,025.00

3/1/2027 144,925.00 144,925.00 2,079,950.00

9/1/2027 1,825,000 144,925.00 1,969,925.00

3/1/2028 108,425.00 108,425.00 2,078,350.00

9/1/2028 1,895,000 108,425.00 2,003,425.00

3/1/2029 80,000.00 80,000.00 2,083,425.00

9/1/2029 1,960,000 80,000.00 2,040,000.00

3/1/2030 40,800.00 40,800.00 2,080,800.00

9/1/2030 2,040,000 40,800.00 2,080,800.00 2,080,800.00

TOTAL $24,190,000 $9,966,467.78 $10,410,000 $1,345,566.67 $45,912,034.45 $45,912,034.45

Other Sewer System Obligations

Currently there are no outstanding General Obligation Bonds and Notes issued for SewerSystem purposes. The Issuer has the following outstanding Obligations, consisting of KentuckyInfrastructure Authority Loans, which are Subordinate Obligations under the Trust Agreement.

Loan Date DescriptionInterest

RateFinal

Maturity†Original

Amount IssuedAmount

Outstanding06/01/2012 Loan – A9-01 South Elkhorn 2.00% 12/01/2031 $14,045,119.00 $12,584,806.9411/01/2013 Loan – A13-003 East Lake 2.00% N/A 536,778.58 536,778.5801/01/2012 Loan - A10-08 Wolf Run 2.00% N/A 7,972,208.54 7,972,208.5411/01/2013 Loan - A13-18 E2A 2.00% N/A 3,164,636.56 3,164,636.5611/01/2013 Loan - A13-003 Century Hills 2.00% N/A 522,273.75 522,273.7502/01/2014 Loan - A13-002 Bob O Link 2.00% N/A 1,070,057.39 1,070,057.39TOTAL $27,311,073.82 $25,850,761.76

______†Until the remaining balance is requested, the Kentucky Infrastructure Authority does not issue an amortization schedule for theloan nor does the Issuer initiate payment of principal toward the loan. The maturity of the loan is set when the final balance of theloan is requested from the Kentucky Infrastructure Authority. Currently, Loan-A9-01 South Elkhorn (the “South Elkhorn Loan”)is the only such loan for which an amortization schedule has been issued and the loan payments thereunder commenced on June1, 2012. The payments related to the South Elkhorn Loan are the only amounts currently listed in the table in “SECURITY ANDSOURCE OF PAYMENT FOR THE SERIES 2014 BONDS - Historical Debt Service Coverage” under Other Sewer SystemObligations.

21

Estimated Principal and Interest Requirements with respect to the Series 2014 Bonds andthe Other Sewer System Obligations

The following table sets forth the estimated Principal and Interest Requirements withrespect to the Series 2014 Bonds and the Other Sewer System Obligations.

Fiscal Year

Principal andInterest

Requirements forthe Series 2014

Bonds

Principal andInterest

Requirements forOther Sewer System

Obligations†

AggregatePrincipal and InterestRequirements for theSeries 2014 Bonds andOther Sewer System

Obligations2015 $ 557,084.45 $ 988,519.10 $1,545,603.552016 3,799,550.00 1,661,701.98 5,461,251.982017 3,802,050.00 1,661,592.80 5,463,642.802018 3,808,300.00 1,661,481.39 5,469,781.392019 3,803,175.00 1,661,367.78 5,464,542.782020 3,806,425.00 1,661,251.91 5,467,676.912021 3,802,675.00 1,661,133.70 5,463,808.702022 3,801,675.00 1,661,013.11 5,462,688.112023 2,082,050.00 1,660,890.17 3,742,940.172024 2,083,600.00 1,660,764.74 3,744,364.742025 2,081,650.00 1,660,636.79 3,742,286.792026 2,080,475.00 1,660,506.30 3,740,981.302027 2,079,950.00 1,660,373.18 3,740,323.182028 2,078,350.00 1,660,237.42 3,738,587.422029 2,083,425.00 1,660,098.93 3,743,523.932030 2,080,800.00 1,659,957.67 3,740,757.672031 2,080,800.00 1,659,813.58 3,740,613.582032 0.00 1,231,736.86 1,231,736.862033 0.00 803,657.17 803,657.172034 0.00 803,504.27 803,504.272035 0.00 803,348.32 803,348.32

TOTALS $45,912,034.45 $31,203,587.17 $77,115,621.62_________†As stated in the note to the table under “Other Sewer System Obligations” above, the Issuer does not initiate payment ofprincipal toward the Kentucky Infrastructure Authority Loans until the final balance of the loan is requested from the KentuckyInfrastructure Authority. To provide the estimates of Principal and Interest Requirements in this table, debt service with respectto the Kentucky Infrastructure Authority Loans has been estimated based on the following assumptions: level debt service,commencing June 1, 2015, amortized over a 20 year period (as each such loan is referenced above under “Other Sewer SystemObligations”), with the exception of the South Elkhorn Loan, for which an actual amortization schedule has been issued. Debtservice with respect to the Kentucky Infrastructure Authority Loans (actual and estimated) does not include certain annual feesrelated thereto.

22

INVESTMENT CONSIDERATIONS

The Series 2014 Bonds, like all obligations of state and local government, are subject tochanges in value due to changes in the condition of the tax-exempt bond market.

Prospective purchasers of the Series 2014 Bonds may need to consult their own taxadvisors prior to any purchase of the Series 2014 Bonds as to the impact of the Internal RevenueCode of 1986, as amended, upon their acquisition, holding or disposition of the Series 2014Bonds.

With regard to the risks related to a change in status with respect to the BAB InterestSubsidy Payments related to the Refunded Series 2009 Bonds, see “PURPOSE AND PLAN OFREFUNDING – Redemption of the Series 2009 Bonds as Build America Bonds” herein. Withregard to the risk involved in a lowering of the bond rating of the Issuer, see "RATINGS" herein.With regard to creditors’ rights, see "SECURITY AND SOURCE OF PAYMENT FORBONDS" herein.

THE ISSUER