leveraging chile’s strengths to become a preferred ... bell director, global business policy...

TRANSCRIPT

Simon BellDirector, Global Business Policy Council

April 10, 2007

Leveraging Chile’s Strengths to become aPreferred Location for Remote Services

2A.T. Kearney / 2007

Presentation Overview

The Global Remote ServicesOpportunity – and Challenge

Assessing Chile’s Strengths andWeaknesses

Recommendations to Optimize Chile’sCompetitive Position

3A.T. Kearney / 2007

The Global Remote Services Opportunity– and Challenge

4A.T. Kearney / 2007

A confluence of factors has, in the last 10 years, created awhole new industry – the offshoring of services

IncreasingIncreasingTalent Shortage Talent Shortage

in Developed in Developed CountriesCountries

Increasing Increasing Talent Supply Talent Supply in Developing in Developing

CountriesCountries

GlobalGlobalMarket Market

Liberalization Liberalization & Integration& Integration

Shift from Shift from ManufacturingManufacturing

to Servicesto ServicesEconomyEconomy

Technology-Technology-Driven Driven

Innovation Innovation and Productivityand Productivity

Any service orfunction

that does not requirephysical interaction

can now bedelivered remotely

from anywherein the world

5A.T. Kearney / 2007

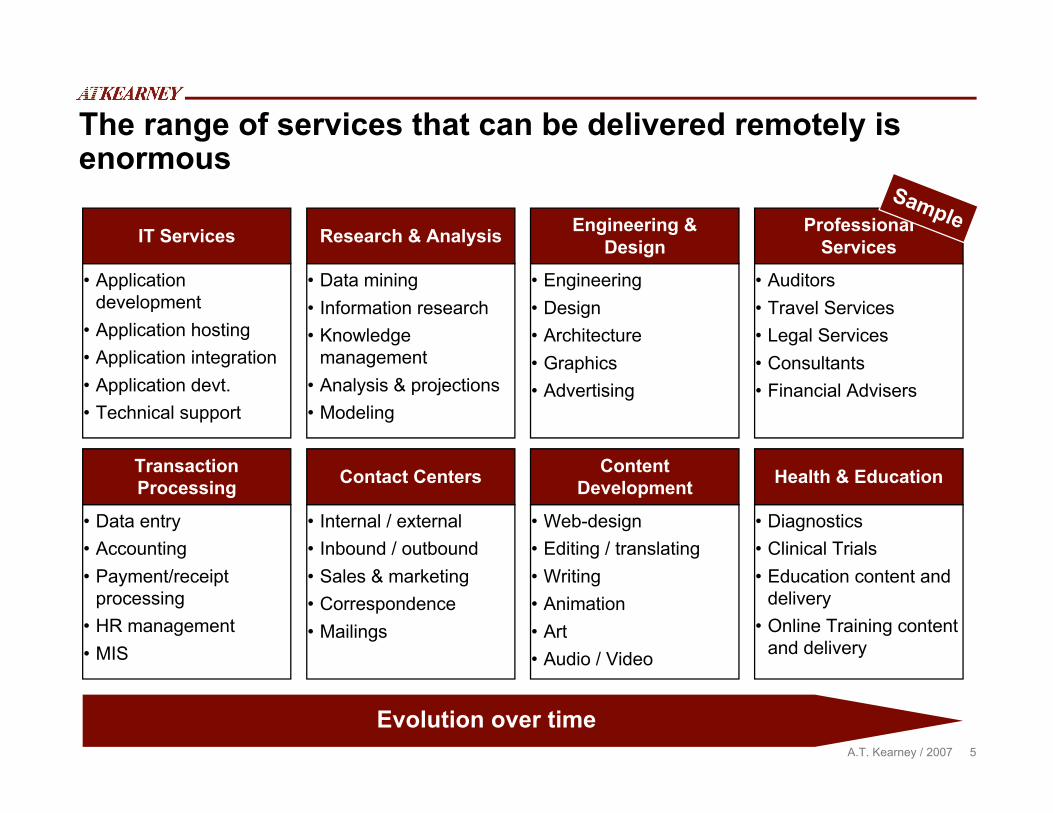

The range of services that can be delivered remotely isenormous

• Applicationdevelopment

• Application hosting• Application integration• Application devt.• Technical support

IT Services

• Data mining• Information research• Knowledge

management• Analysis & projections• Modeling

Research & Analysis

• Engineering• Design• Architecture• Graphics• Advertising

Engineering &Design

• Auditors• Travel Services• Legal Services• Consultants• Financial Advisers

ProfessionalServices

• Diagnostics• Clinical Trials• Education content and

delivery• Online Training content

and delivery

Health & Education

• Web-design• Editing / translating• Writing• Animation• Art• Audio / Video

ContentDevelopment

• Internal / external• Inbound / outbound• Sales & marketing• Correspondence• Mailings

Contact Centers

• Data entry• Accounting• Payment/receipt

processing• HR management• MIS

TransactionProcessing

Evolution over time

Sample

6A.T. Kearney / 2007

39%

66%

62%

50%

61%

71%

73%

66%

76%

70%

87%

79%

Source: A.T. Kearney Foreign Direct Confidence Index, 2003-2005

Interest in offshoring is growing rapidly across all regionsand functional areas

11%

14%

14%

15%

26%

13%

24%

16%

16%

30%

25%

32%

38%

50%

24%

26%

41%

41%

44%

50%

IT Developm’t.& Support

ContactCenters

Logistics/Distribution

Manufacturing

BusinessProcesses

KnowledgeManagement

R&D/Engineering

Major companies planning on offshoring overthe next three years, percent

AsianInvestors

EuropeanInvestors

GlobalInvestors

NorthAmericanInvestors

2005 2004 2003

Major companies planning on offshoringcorporate activities, by function, percent

67%

7A.T. Kearney / 2007

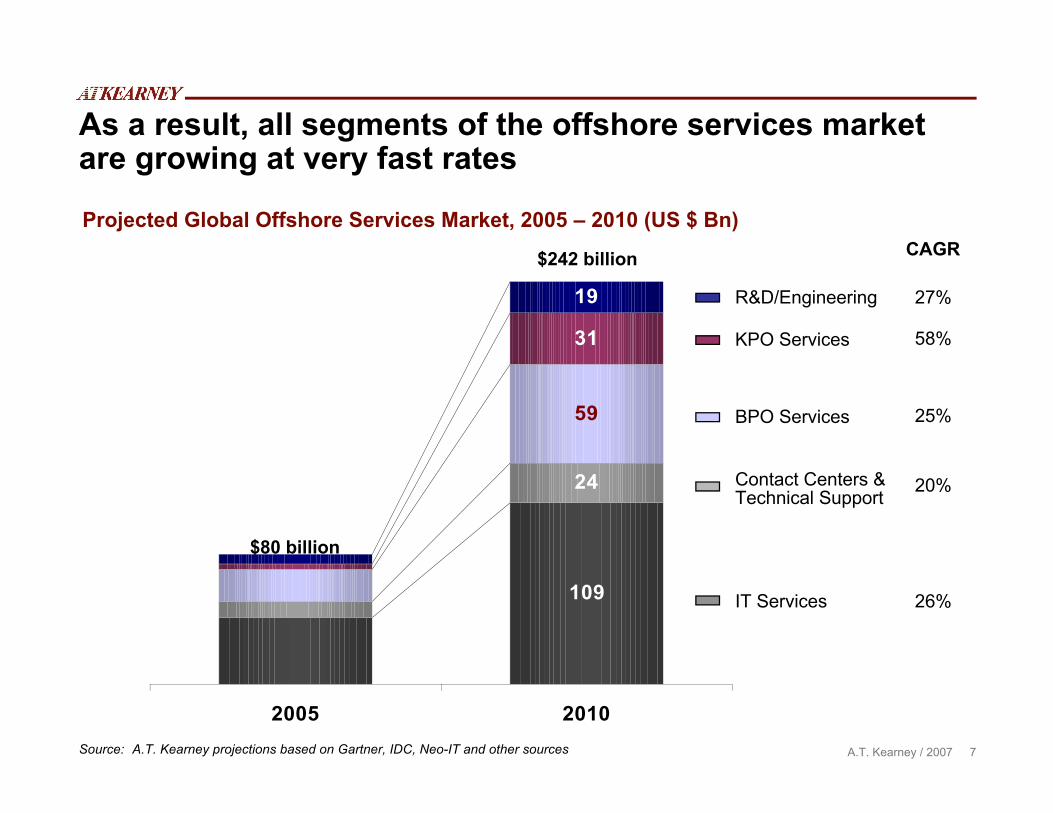

As a result, all segments of the offshore services marketare growing at very fast rates

Source: A.T. Kearney projections based on Gartner, IDC, Neo-IT and other sources

Projected Global Offshore Services Market, 2005 – 2010 (US $ Bn)

109

24

59

31

19

2005 2010

CAGR

R&D/Engineering

26%

Contact Centers &Technical Support

BPO Services

KPO Services

27%

58%

25%

20%

IT Services

$80 billion

$242 billion

8A.T. Kearney / 2007

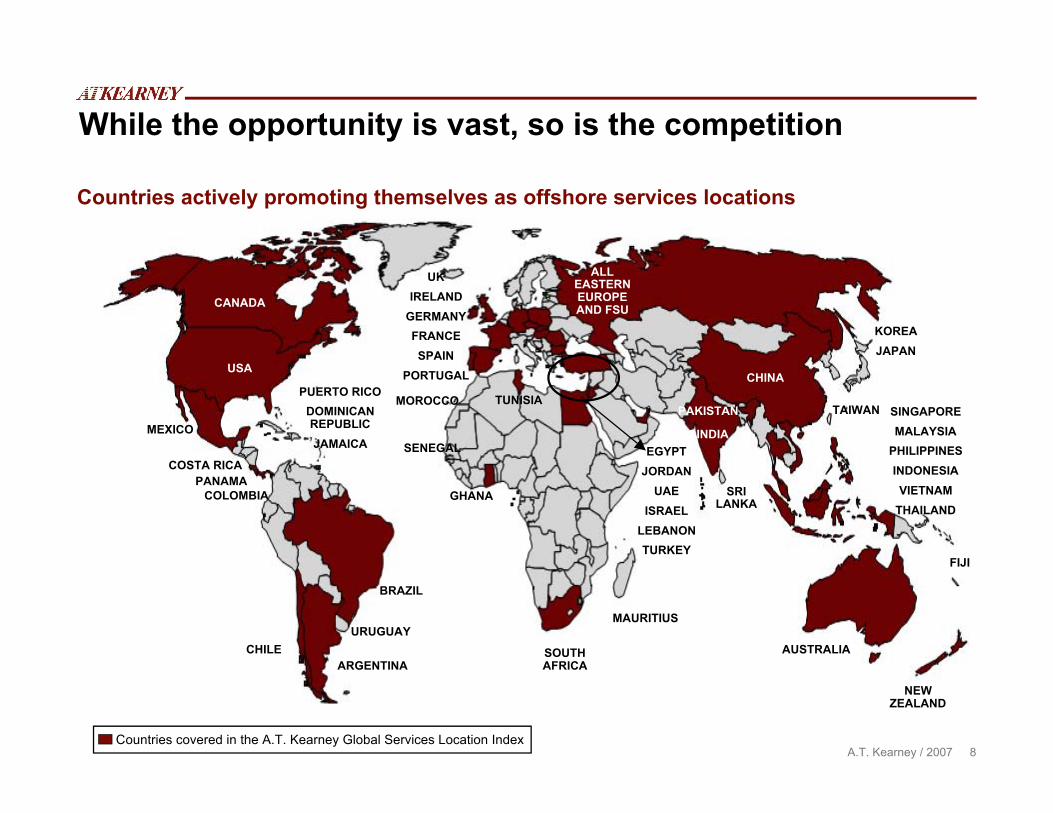

While the opportunity is vast, so is the competition

Countries covered in the A.T. Kearney Global Services Location Index

SENEGAL

AUSTRALIA

NEWZEALAND

SOUTHAFRICA

GHANA SRILANKA

INDIA

PAKISTAN

ALLEASTERNEUROPEAND FSU

EGYPTJORDAN

UAEISRAEL

LEBANONTURKEY

CANADA

USA

MEXICO

MOROCCO TUNISIAPUERTO RICO

DOMINICANREPUBLICJAMAICA

CHILEARGENTINA

BRAZIL

COSTA RICAPANAMA

COLOMBIA

UKIRELAND

GERMANYFRANCESPAIN

PORTUGAL

KOREAJAPAN

SINGAPOREMALAYSIA

PHILIPPINESINDONESIAVIETNAM

THAILAND

CHINA

TAIWAN

FIJI

MAURITIUS

Countries actively promoting themselves as offshore services locations

URUGUAY

9A.T. Kearney / 2007

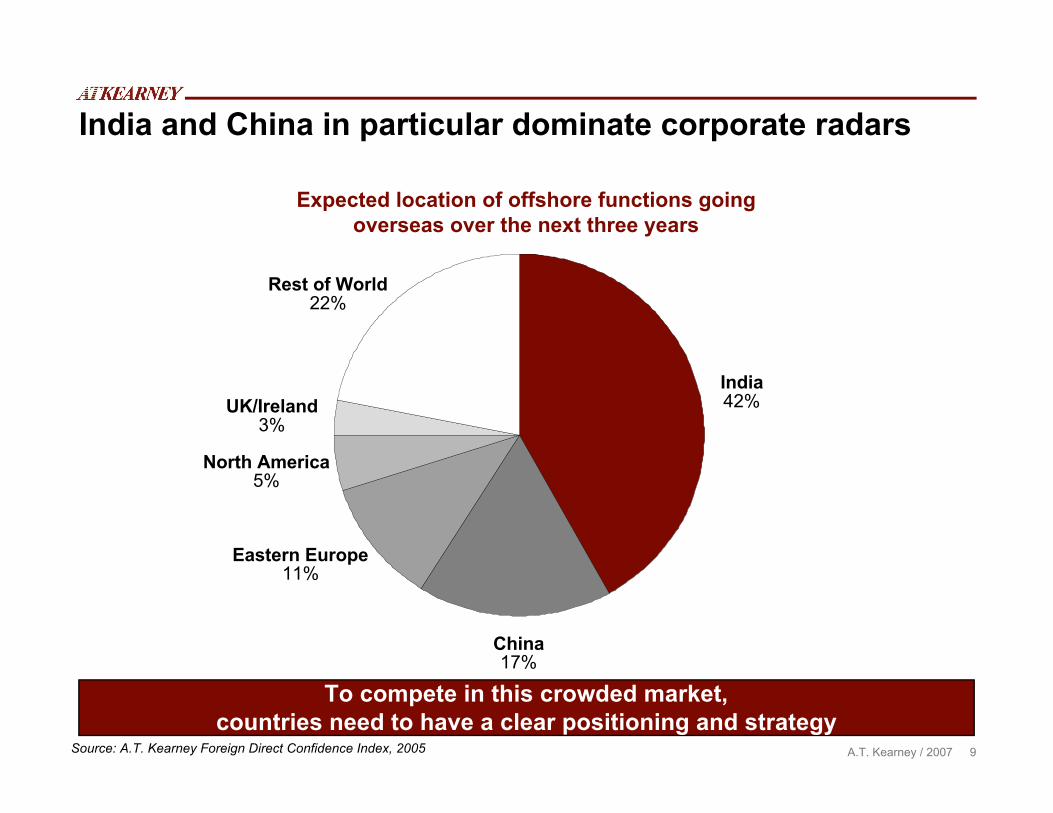

India and China in particular dominate corporate radars

India42%

Eastern Europe11%

China17%

Rest of World22%

UK/Ireland3%

North America5%

Expected location of offshore functions goingoverseas over the next three years

Source: A.T. Kearney Foreign Direct Confidence Index, 2005

To compete in this crowded market,countries need to have a clear positioning and strategy

10A.T. Kearney / 2007

Assessing Chile’s Strengths and Weaknesses

11A.T. Kearney / 2007

Since 2001, A.T. Kearney has produced a Location Index toassist clients in assessing potential service locations

Financial Costs People Skills and Availability Business Environment

40% 30% 30%

Compensation Costs

Infrastructure Costs

Tax and Regulatory Costs

80%

10%

10%

Cumulative IT/ServicesExperience and Skills

Labor Force Availability

Language Skills

Educational Skills

Attrition Risk

40%

20%

15%

15%

10%

Country Environment

Country Infrastructure

Security of IntellectualProperty

Cultural Exposure

60%

20%

10%

10%

Metrics evaluated in the A.T. Kearney Global Services Location Index

Source: A.T. Kearney Global Services Location Index

12A.T. Kearney / 2007

Chile has consistently ranked among the top 10 countriesin the Index

3.2

2.9

2.8

3.2

2.6

3.3

2.7

3.3

3.2

2.6

1.7

2.8

3.2

3.1

2.4

2.4

2.6

2.6

3.3

2.7

0.5

3.0

2.9

2.5

2.8

2.3

2.3

1.3

1.2

1.8

1.5

1.2

1.2

1.0

1.5

1.5

1.0

1.1

1.0

1.0

1.1

0.9

1.2

1.0

0.9

2.7

1.0

1.3

1.0

1.0

1.4

1.4

2.0

1.6

1.5

1.1

1.9

1.3

1.6

1.6

2.5

1.8

1.3

1.5

2.2

2.1

2.0

1.8

1.2

1.9

2.3

1.5

1.3

2.0

1.6

India

ChinaMalaysia

Thailand

BrazilIndonesia

ChilePhilippines

BulgariaMexico

SingaporeSlovakia

Egypt

JordanEstonia

CzechLatvia

PolandVietnam

UAEUSA (Tier II)

Uruguay

ArgentinaHungary

Mauritius

Source: A.T. Kearney Global Services Location Index 2007

Global Services Location Index 2007Ranks 1-25 Ranks 26-50

3.0

3.3

2.6

3.2

3.2

2.5

2.8

2.9

3.0

0.8

2.9

2.6

2.0

3.2

0.5

2.9

0.5

1.2

1.5

0.9

1.6

2.8

0.5

2.1

0.4

0.9

0.9

0.8

1.0

1.0

1.2

1.0

0.9

0.9

2.1

0.9

1.4

1.3

0.8

2.2

0.8

2.2

1.7

1.1

1.7

1.1

1.0

2.1

1.3

1.5

1.5

1.3

2.0

1.2

1.1

1.6

1.5

1.5

1.4

2.3

1.3

1.2

1.9

1.1

2.4

1.4

2.4

2.1

2.3

2.3

2.1

1.1

2.3

1.4

2.3

Tunisia

GhanaLithuaniaSri Lanka

PakistanSouth Africa

Jamaica

RomaniaCosta Rica

Canada

MoroccoRussia

IsraelSenegal

Germany (Tier II)

PanamaUK (Tier II)

Spain

New ZealandAustraliaPortugal

UkraineFrance (Tier II)

Turkey

Ireland

EnvironmentFinancial PeopleCountry score:

13A.T. Kearney / 2007

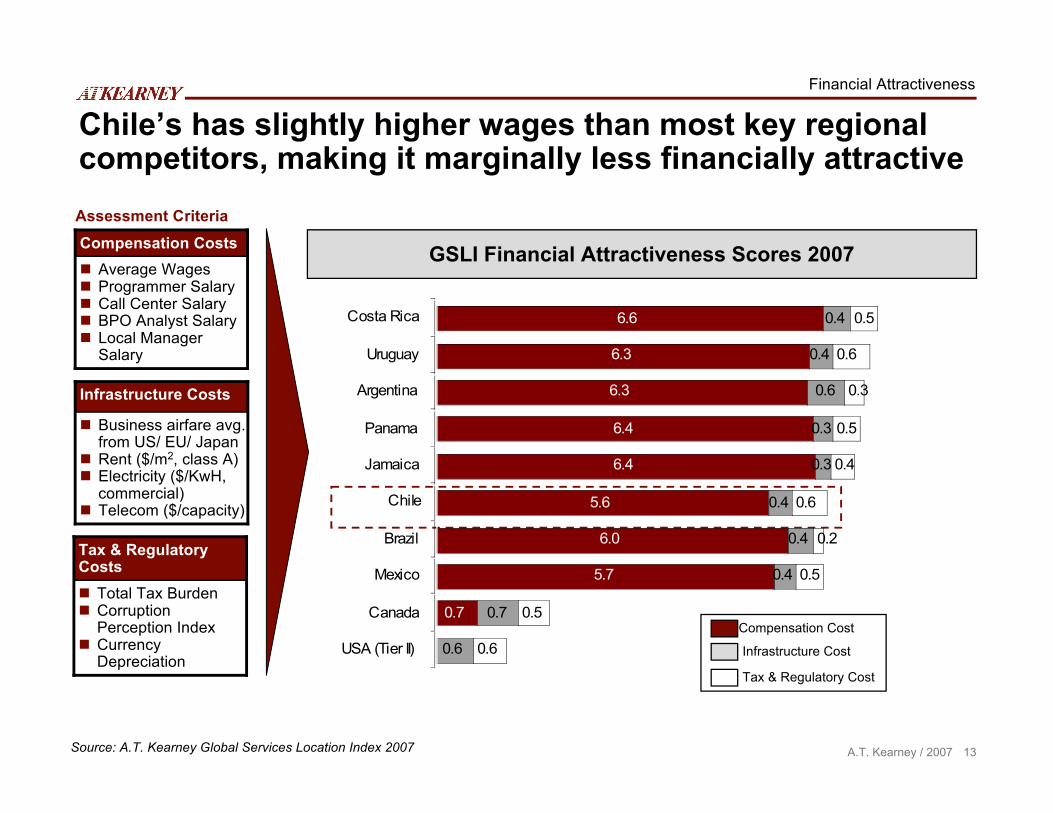

Chile’s has slightly higher wages than most key regionalcompetitors, making it marginally less financially attractive

GSLI Financial Attractiveness Scores 2007

0.7

5.7

6.0

5.6

6.4

6.4

6.3

6.3

6.6

0.6

0.7

0.4

0.4

0.4

0.3

0.3

0.6

0.4

0.4

0.6

0.5

0.5

0.2

0.6

0.4

0.5

0.3

0.5

0.6

USA (Tier II)

Canada

Mexico

Brazil

Chile

Jamaica

Panama

Argentina

Uruguay

Costa Rica

Tax & Regulatory Cost

Compensation Cost

Infrastructure Cost

Business airfare avg.from US/ EU/ Japan

Rent ($/m2, class A) Electricity ($/KwH,

commercial) Telecom ($/capacity)

Infrastructure Costs

Total Tax Burden Corruption

Perception Index Currency

Depreciation

Tax & RegulatoryCosts

Assessment Criteria

Average Wages Programmer Salary Call Center Salary BPO Analyst Salary Local Manager

Salary

Compensation Costs

Source: A.T. Kearney Global Services Location Index 2007

Financial Attractiveness

14A.T. Kearney / 2007

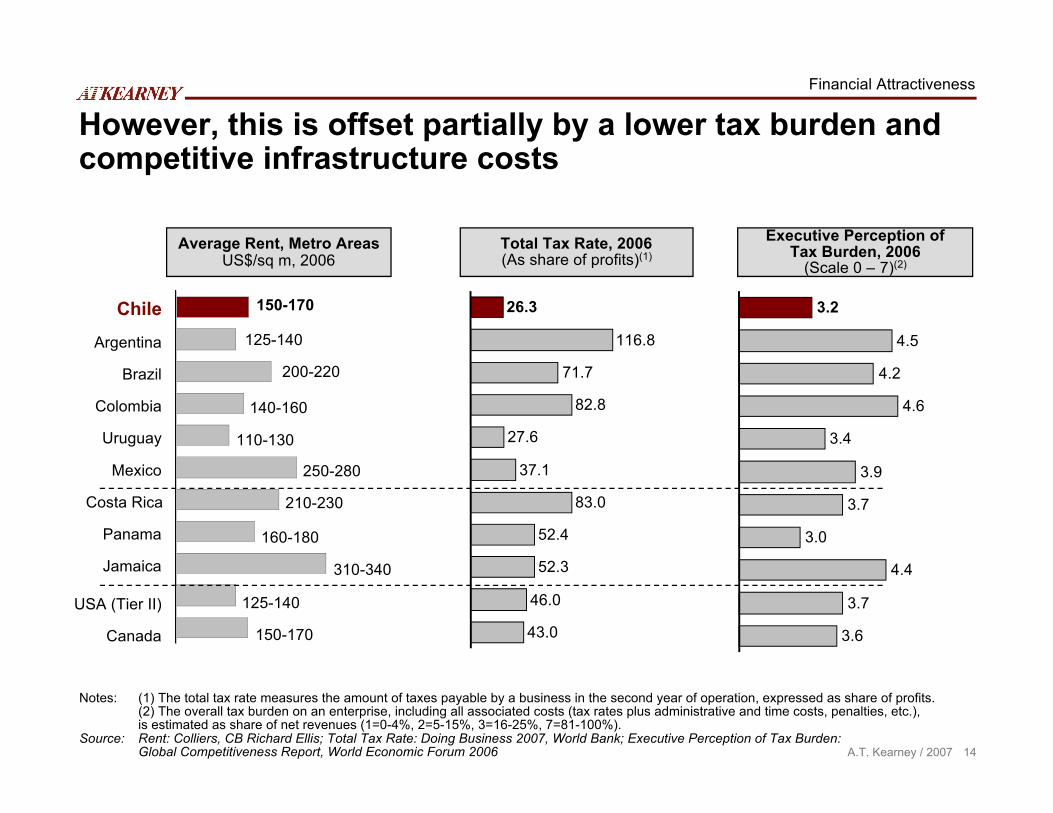

However, this is offset partially by a lower tax burden andcompetitive infrastructure costs

Financial Attractiveness

Chile

Argentina

Brazil

Colombia

Uruguay

Costa Rica

Panama

Jamaica

Mexico

USA (Tier II)

Canada

150-170

125-140

200-220

140-160

110-130

210-230

160-180

310-340

250-280

125-140

150-170

Average Rent, Metro AreasUS$/sq m, 2006

Total Tax Rate, 2006(As share of profits)(1)

Executive Perception ofTax Burden, 2006

(Scale 0 – 7)(2)

Notes: (1) The total tax rate measures the amount of taxes payable by a business in the second year of operation, expressed as share of profits.(2) The overall tax burden on an enterprise, including all associated costs (tax rates plus administrative and time costs, penalties, etc.),is estimated as share of net revenues (1=0-4%, 2=5-15%, 3=16-25%, 7=81-100%).

Source: Rent: Colliers, CB Richard Ellis; Total Tax Rate: Doing Business 2007, World Bank; Executive Perception of Tax Burden:Global Competitiveness Report, World Economic Forum 2006

26.3

116.8

82.8

27.6

37.1

83.0

52.4

46.0

43.0

52.3

71.7

3.2

4.5

4.6

3.4

3.9

3.7

3.0

3.7

3.6

4.4

4.2

15A.T. Kearney / 2007

0.3

0.4

0.3

0.4

1.2

1.3

1.8

2.2

3.4

4.0

0.1

0.4

0.8

1.3

0.3

2.0

1.0

0.7

1.1

1.0

1.0

1.0

1.0

1.3

1.2

1.1

1.2

1.5

1.2

1.2

1.2

1.2

1.5

1.5

0.4

0.2

0.4

0.5

0.3

0.3

0.5

0.5

0.7

1.2

0.6

0.7

Panama

Costa Rica

Jamaica

Uruguay

Chile

Argentina

Mexico

Brazil

Canada

USA (Tier II)

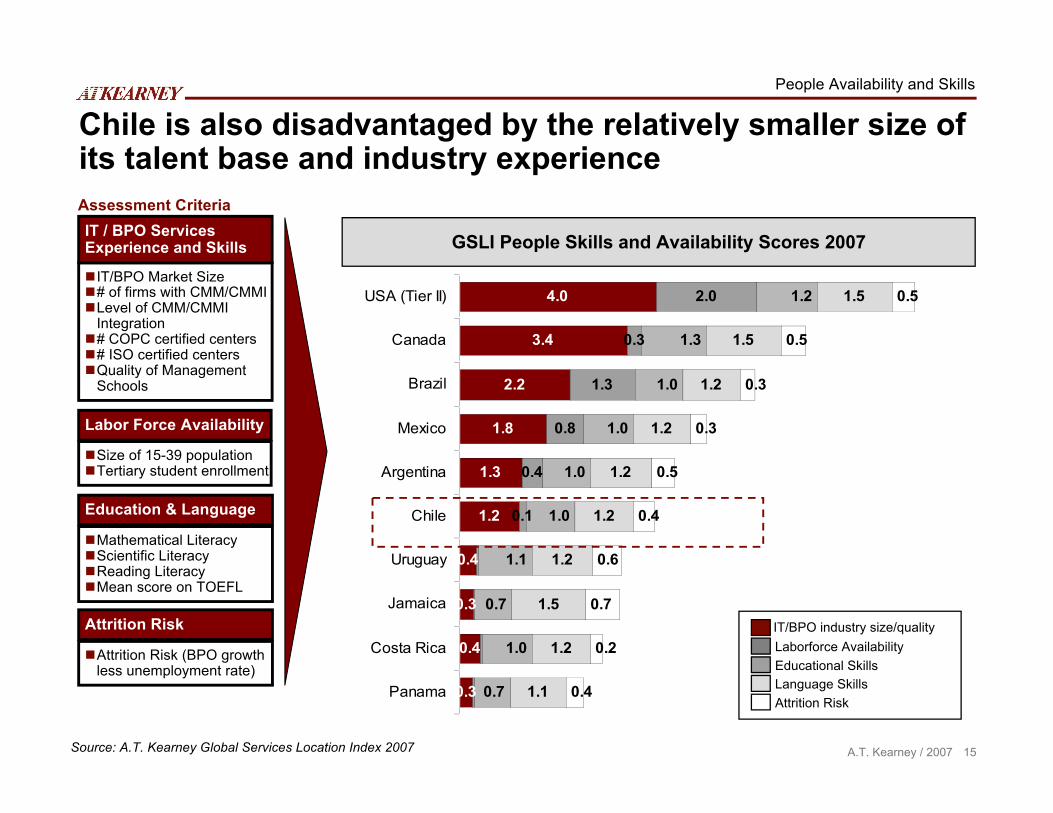

Chile is also disadvantaged by the relatively smaller size ofits talent base and industry experience

GSLI People Skills and Availability Scores 2007

People Availability and Skills

Educational Skills

IT/BPO industry size/qualityLaborforce Availability

Language SkillsAttrition Risk

Size of 15-39 populationTertiary student enrollment

Labor Force Availability

Mathematical LiteracyScientific LiteracyReading LiteracyMean score on TOEFL

Education & Language

IT/BPO Market Size# of firms with CMM/CMMILevel of CMM/CMMI

Integration# COPC certified centers# ISO certified centersQuality of Management

Schools

IT / BPO ServicesExperience and Skills

Attrition Risk (BPO growthless unemployment rate)

Attrition Risk

Assessment Criteria

Source: A.T. Kearney Global Services Location Index 2007

16A.T. Kearney / 2007

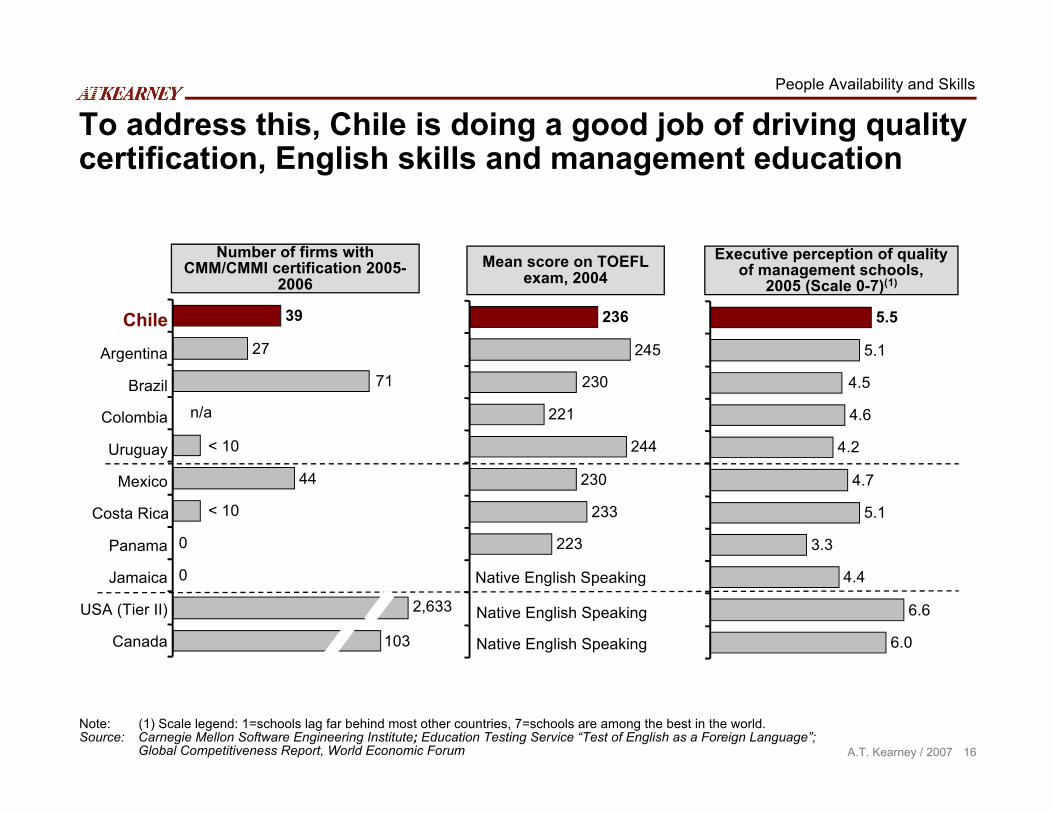

To address this, Chile is doing a good job of driving qualitycertification, English skills and management education

People Availability and Skills

Chile

Argentina

Brazil

Colombia

Uruguay

Costa Rica

Panama

Jamaica

Mexico

USA (Tier II)

Canada

Native English Speaking

Native English Speaking

Native English Speaking

Note: (1) Scale legend: 1=schools lag far behind most other countries, 7=schools are among the best in the world.Source: Carnegie Mellon Software Engineering Institute; Education Testing Service “Test of English as a Foreign Language”;

Global Competitiveness Report, World Economic Forum

Mean score on TOEFLexam, 2004

Executive perception of qualityof management schools,

2005 (Scale 0-7)(1)

2,633

n/a

103

< 10

< 10

Number of firms withCMM/CMMI certification 2005-

2006

39

27

44

0

71

0

5.5

5.1

4.6

4.2

4.7

5.1

3.3

6.6

6.0

4.4

4.5

236

245

221

244

230

233

223

230

17A.T. Kearney / 2007

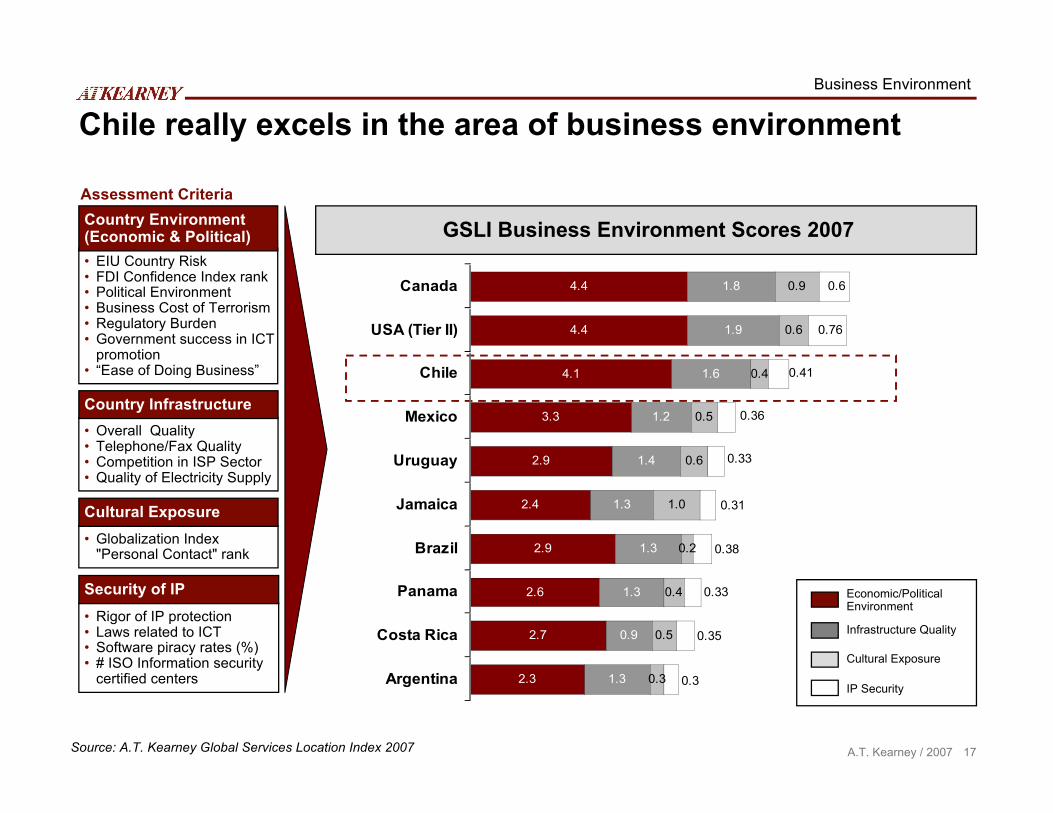

Chile really excels in the area of business environment

• Overall Quality• Telephone/Fax Quality• Competition in ISP Sector• Quality of Electricity Supply

Country Infrastructure

• Globalization Index"Personal Contact" rank

Cultural Exposure

Assessment Criteria

• EIU Country Risk• FDI Confidence Index rank• Political Environment• Business Cost of Terrorism• Regulatory Burden• Government success in ICT

promotion• “Ease of Doing Business”

Country Environment(Economic & Political)

• Rigor of IP protection• Laws related to ICT• Software piracy rates (%)• # ISO Information security

certified centers

Security of IP

Business Environment

2.3

2.7

2.6

2.9

2.4

2.9

3.3

4.1

4.4

4.4

1.3

0.9

1.3

1.3

1.3

1.4

1.2

1.6

1.9

1.8

0.3

0.5

0.4

0.2

1.0

0.6

0.5

0.4

0.76

0.60.9

0.6

0.3

0.35

0.33

0.38

0.31

0.33

0.36

0.41

Argentina

Costa Rica

Panama

Brazil

Jamaica

Uruguay

Mexico

Chile

USA (Tier II)

Canada

GSLI Business Environment Scores 2007

Economic/Political Environment

Infrastructure Quality

Cultural Exposure

IP Security

Source: A.T. Kearney Global Services Location Index 2007

18A.T. Kearney / 2007

Chile offers by far the most stable business-friendlyoperating environment in Latin America

Business Environment

EIU Overall Business Risk2006

100=high risk (lower is better)

Source: Economist Intelligence Unit, Global Competitiveness Report, World Economic Forum; World Bank, Doing Business 2007

Chile

Argentina

Brazil

Colombia

Uruguay

Costa Rica

Panama

Jamaica

Mexico

USA (Tier II)

Canada

World Bank Labor MarketRigidity, 2006

100= Most rigid

Executive Perception ofRegulatory Burden, 2006

Index 1-5 (5 = lowest burden)

3.6

2.4

2.8

2.9

2.5

2.6

2.9

3.4

2.6

2.0

3.6

53

54

21

40

41

40

40

22

20

50

48

24

41

27

31

38

32

56

0

4

4

42

19A.T. Kearney / 2007

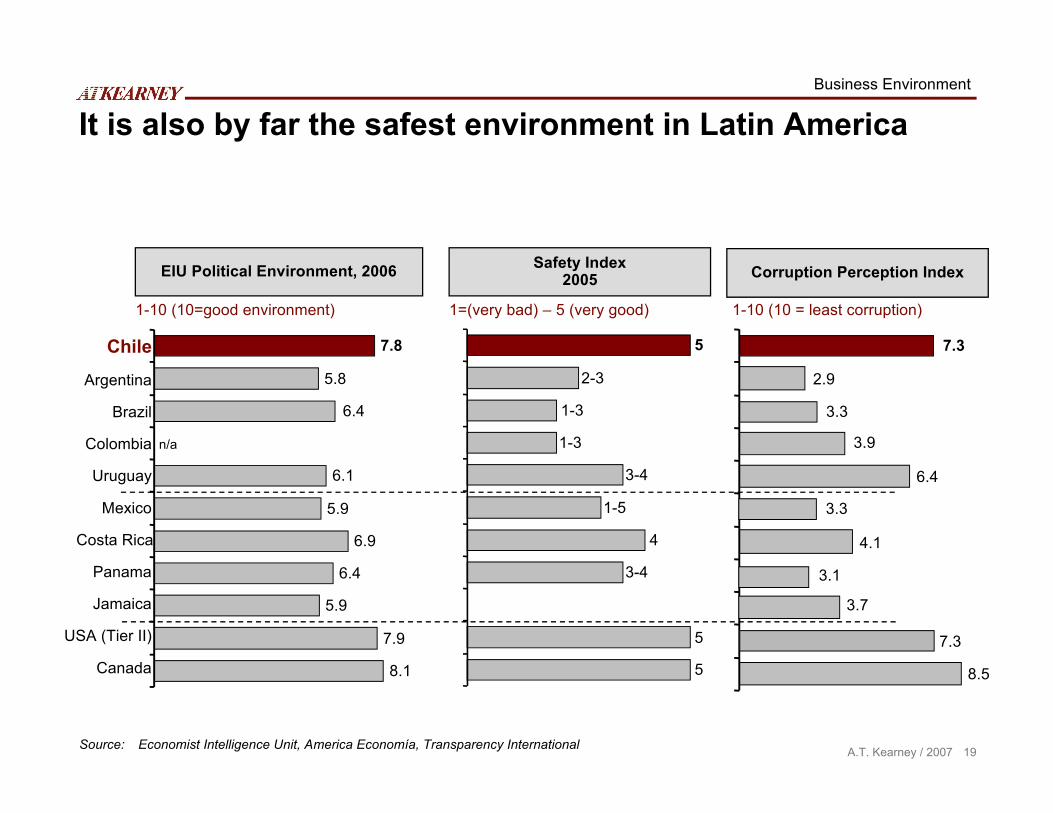

It is also by far the safest environment in Latin AmericaBusiness Environment

n/a

EIU Political Environment, 2006

1-10 (10=good environment)

Source: Economist Intelligence Unit, America Economía, Transparency International

Chile

Argentina

Brazil

Colombia

Uruguay

Costa Rica

Panama

Jamaica

Mexico

USA (Tier II)

Canada

1-10 (10 = least corruption)

Safety Index2005

1=(very bad) – 5 (very good)

Corruption Perception Index

7.3

2.9

3.9

6.4

4.1

3.1

8.5

3.7

3.3

7.3

3.3

5

4

5

5

3-4

1-5

3-4

1-3

2-3

1-3

7.8

5.8

6.1

5.9

6.9

6.4

7.9

8.1

5.9

6.4

20A.T. Kearney / 2007

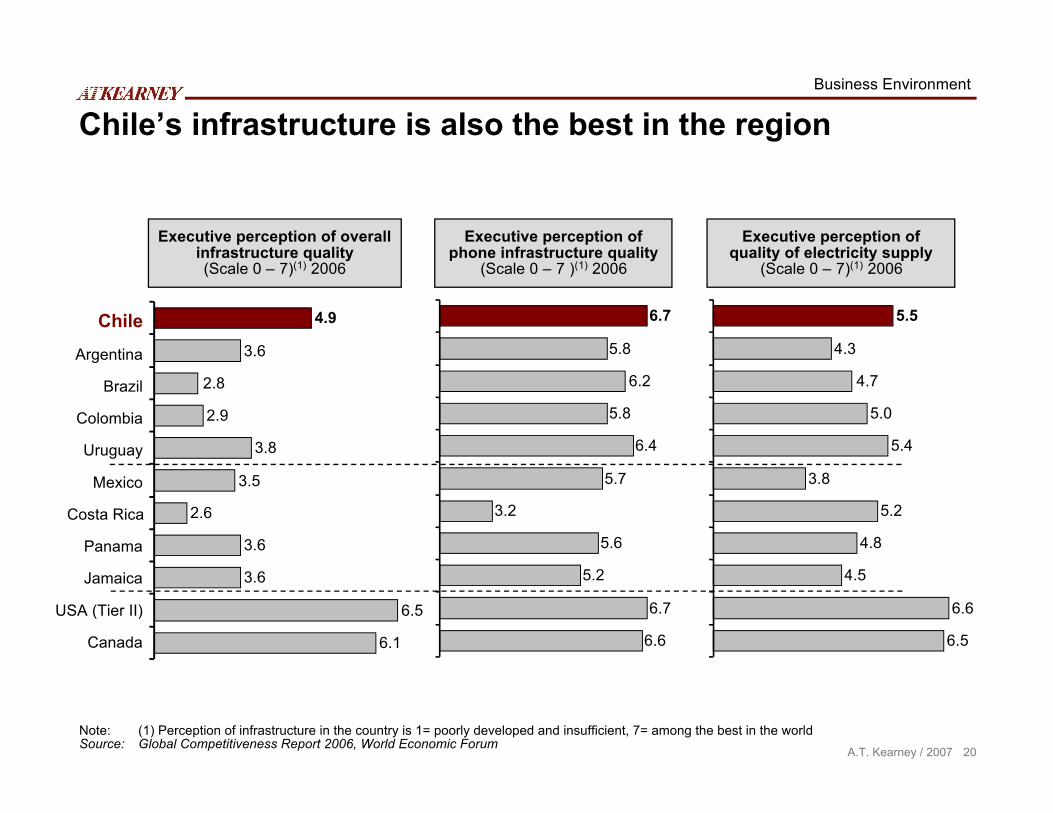

Chile’s infrastructure is also the best in the region

Chile

Argentina

Brazil

Colombia

Uruguay

Costa Rica

Panama

Jamaica

Mexico

USA (Tier II)

Canada

Executive perception of overallinfrastructure quality(Scale 0 – 7)(1) 2006

Note: (1) Perception of infrastructure in the country is 1= poorly developed and insufficient, 7= among the best in the worldSource: Global Competitiveness Report 2006, World Economic Forum

Executive perception ofphone infrastructure quality

(Scale 0 – 7 )(1) 2006

Executive perception ofquality of electricity supply

(Scale 0 – 7)(1) 2006

4.9

3.6

2.9

3.8

3.5

2.6

3.6

6.5

6.1

3.6

2.8

6.7

5.8

5.8

6.4

5.7

3.2

5.6

6.7

6.6

6.2

5.2

5.5

4.3

5.0

5.4

3.8

5.2

4.8

6.6

6.5

4.5

4.7

Business Environment

21A.T. Kearney / 2007

Interviews with industry players inside and outside Chileconfirm broad recognition of Chile’s key strengths …

Political andeconomic stability

• Chile’s political and economic stability is widely recognized• Long term investors, such as multinationals developing captive shared service centers,

consider this a particularly important factor

Transparency andstrength ofinstitutions

• Chile is considered the most transparent location to do business in Latin America• The existence and general enforcement of regulations—as in labor and arbitration—provides

confidence, compared to volatile conditions in Argentina, Colombia or even Brazil.• As one investor said, “one can rest assured that institutions will do their job”

Pro-businessclimate

• Radical demands from labor and other interest groups are much lower than in peer countries• Investors are enthusiastic about the effectiveness and efficiency of government agencies. A recent

investor indicates “visas can be obtained in weeks in Chile rather than months in other countries”

Developedinfrastructure

• Developed telecommunications is mentioned as one of the key country’s strengths• Santiago offers all the amenities of a developed city and has air connections with major world hubs

Specialized talentavailability and

stability

• Investors recognize that Chile’s top talent pool is as strong as any in the world. Non-investorsmention Chile’s reputation for qualified and well educated people

• Unlike locations like Costa Rica, India, and China, salaries are stable, making Chile increasinglyattractive as the cost arbitrage of other locations decreases

Strong supportfrom government

agencies

• Recent investors note this strength more emphatically than other groups• They express that the support received from Chile’s representatives “from the Ambassador to

CORFO” was “professional, proactive and effective in helping us establish in Chile”

Chile’s Key Strengths Identified in Stakeholder Interviews

22A.T. Kearney / 2007

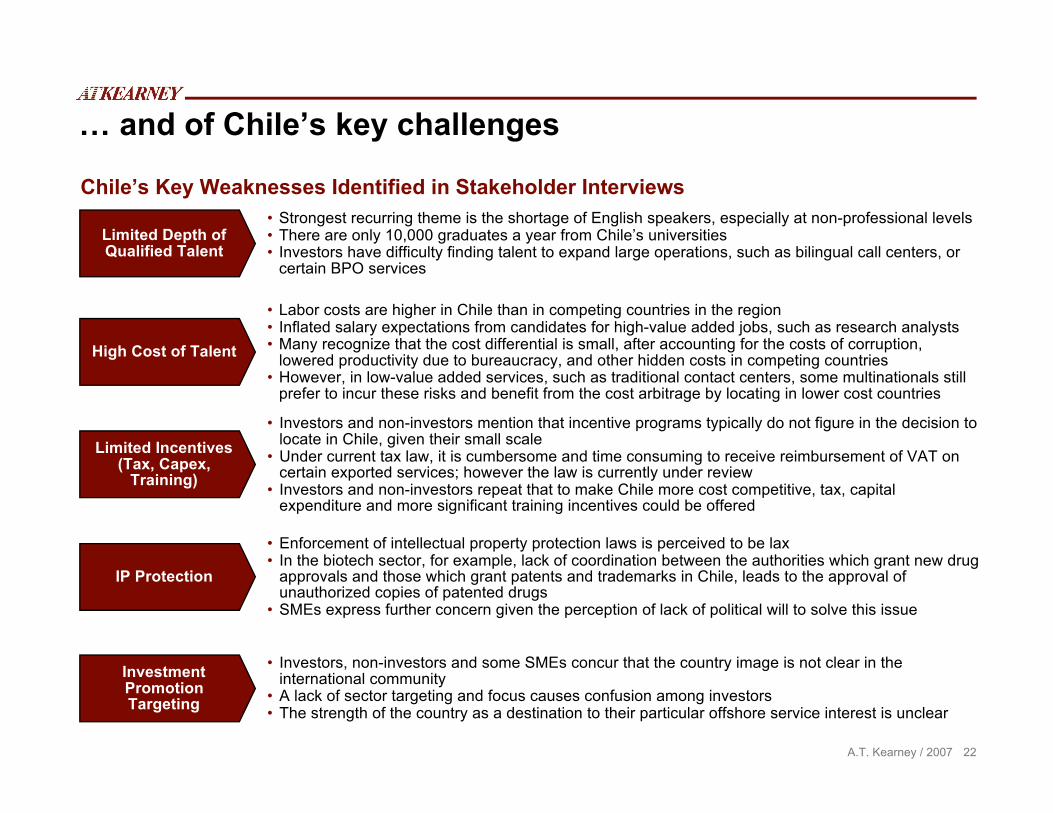

… and of Chile’s key challenges

Limited Depth ofQualified Talent

• Strongest recurring theme is the shortage of English speakers, especially at non-professional levels• There are only 10,000 graduates a year from Chile’s universities• Investors have difficulty finding talent to expand large operations, such as bilingual call centers, or

certain BPO services

High Cost of Talent

• Labor costs are higher in Chile than in competing countries in the region• Inflated salary expectations from candidates for high-value added jobs, such as research analysts• Many recognize that the cost differential is small, after accounting for the costs of corruption,

lowered productivity due to bureaucracy, and other hidden costs in competing countries• However, in low-value added services, such as traditional contact centers, some multinationals still

prefer to incur these risks and benefit from the cost arbitrage by locating in lower cost countries

Limited Incentives(Tax, Capex,

Training)

• Investors and non-investors mention that incentive programs typically do not figure in the decision tolocate in Chile, given their small scale

• Under current tax law, it is cumbersome and time consuming to receive reimbursement of VAT oncertain exported services; however the law is currently under review

• Investors and non-investors repeat that to make Chile more cost competitive, tax, capitalexpenditure and more significant training incentives could be offered

IP Protection

• Enforcement of intellectual property protection laws is perceived to be lax• In the biotech sector, for example, lack of coordination between the authorities which grant new drug

approvals and those which grant patents and trademarks in Chile, leads to the approval ofunauthorized copies of patented drugs

• SMEs express further concern given the perception of lack of political will to solve this issue

InvestmentPromotionTargeting

• Investors, non-investors and some SMEs concur that the country image is not clear in theinternational community

• A lack of sector targeting and focus causes confusion among investors• The strength of the country as a destination to their particular offshore service interest is unclear

Chile’s Key Weaknesses Identified in Stakeholder Interviews

23A.T. Kearney / 2007

Recommendations to OptimizeChile’s Competitive Position

24A.T. Kearney / 2007

Four key themes emerge to optimize Chile’s position as apreferred location for remote services

1. Focus• Given its small size and the competitive environment, Chile can not afford

to compete in all segments of the remote services sector• Chile must focus on those segments where it offers investors a clear value-

proposition

2. TargetedPromotion

• Having identified priority sectors, more targeted promotion is required tospecific sub-segments within these sectors

• This means development and distribution of more specific information onChile’s attributes in key target sectors, as well as prioritization of specificregions, industries and firms to be targeted

3. Skills andCreativity

• The most important key to success in each of the priority sectors is going tobe to expand the quantity and quality of the skill-base eligible to work inthe sector – English language skills, relevant graduation rates, opennessand attractiveness to foreign knowledge workers, and so on

4. BusinessEnvironment

• As this is Chile’s key competitive advantage, like Singapore, Chile mustcontinuously seek to optimize all aspects of its business environment,particularly areas like Intellectual property protection and informationsecurity, infrastructure quality and costs, and regulatory efficiency

Key Recommendations

25A.T. Kearney / 2007

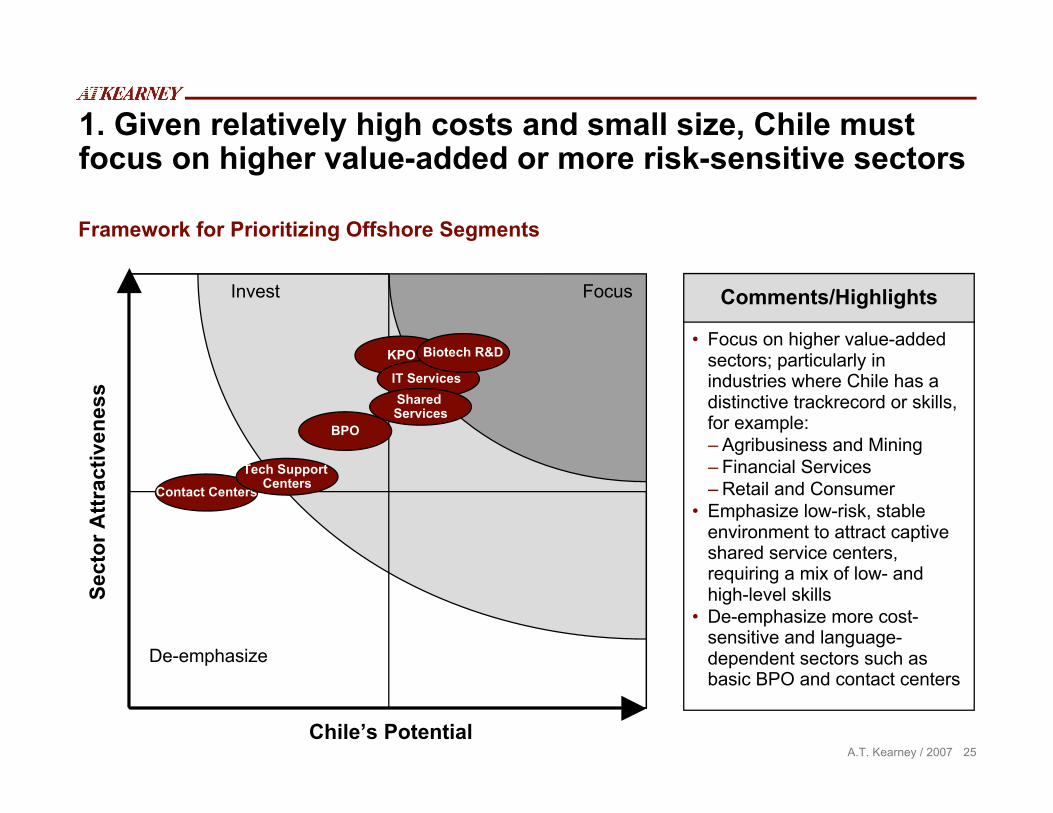

1. Given relatively high costs and small size, Chile mustfocus on higher value-added or more risk-sensitive sectors

KPO

BPO

IT Services

Chile’s Potential

Sect

or A

ttrac

tiven

ess

Focus

De-emphasize

Invest

Biotech R&D

Shared Services

Contact CentersTech Support

Centers

• Focus on higher value-addedsectors; particularly inindustries where Chile has adistinctive trackrecord or skills,for example:– Agribusiness and Mining– Financial Services– Retail and Consumer

• Emphasize low-risk, stableenvironment to attract captiveshared service centers,requiring a mix of low- andhigh-level skills

• De-emphasize more cost-sensitive and language-dependent sectors such asbasic BPO and contact centers

Comments/Highlights

Framework for Prioritizing Offshore Segments

26A.T. Kearney / 2007

2. Within these sectors, a very targeted approach isrequired to promote Chile’s attributes

• For target sectors, develop andmake readily available muchmore specific information onChile’s key attributes:–#/sources of relevant graduates

in relevant disciplines–Special skill development

initiatives (universitypartnerships, etc.)

–Detailed cost information–Fringes and taxes–Specific incentives–Specific policy commitments

(e.g. labor laws for ICT; IP forR&D, etc.)

–Set-up/Approval process/speed

What

• Focus on promoting Chile asR&D, ITO and BPO location toindustries with affinity for Chile orexisting local skill-base:–Agribusiness and Fisheries–Mining, Forestry,–Retail, Consumer–Financial Services

• Focus on countries where Chilehas FTA

• Target specific firms most likelyto be seeking a Latin Americaservice center in the near future

• Identify and leverage Chilenoexpat connections in target firms

Who

• Focus less on advertising, largetrade-shows and broad-brushbrochures; develop customizedpresentations for specific firms,laying out business case andproposition

• Find opportunities for individualdecision-makers visit Chile – tosee for themselves theinfrastructure, stability, quality oflife, etc.

• Mobilize existing investors, localvendors and industryassociations as ambassadors

• Look at overall Chile branding –does not adequately conveyattributes

How

Targeted Promotion Campaign

27A.T. Kearney / 2007

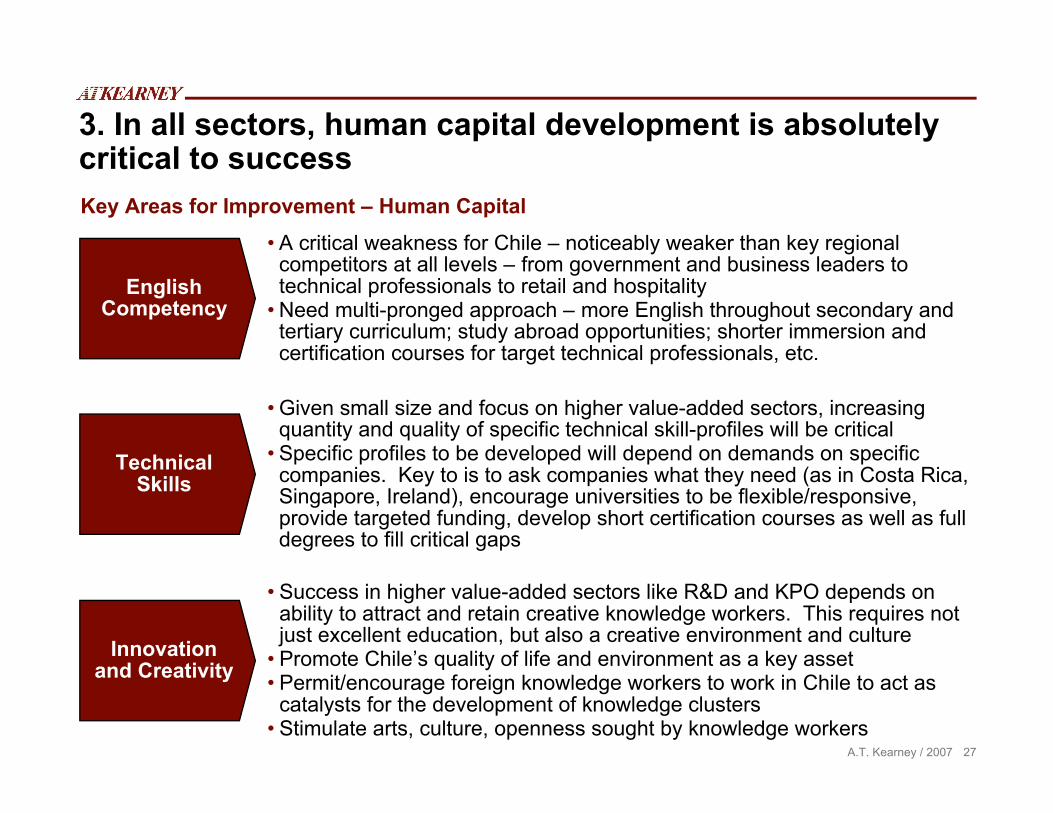

3. In all sectors, human capital development is absolutelycritical to success

EnglishCompetency

• A critical weakness for Chile – noticeably weaker than key regionalcompetitors at all levels – from government and business leaders totechnical professionals to retail and hospitality

• Need multi-pronged approach – more English throughout secondary andtertiary curriculum; study abroad opportunities; shorter immersion andcertification courses for target technical professionals, etc.

TechnicalSkills

• Given small size and focus on higher value-added sectors, increasingquantity and quality of specific technical skill-profiles will be critical

• Specific profiles to be developed will depend on demands on specificcompanies. Key to is to ask companies what they need (as in Costa Rica,Singapore, Ireland), encourage universities to be flexible/responsive,provide targeted funding, develop short certification courses as well as fulldegrees to fill critical gaps

Innovationand Creativity

• Success in higher value-added sectors like R&D and KPO depends onability to attract and retain creative knowledge workers. This requires notjust excellent education, but also a creative environment and culture

• Promote Chile’s quality of life and environment as a key asset• Permit/encourage foreign knowledge workers to work in Chile to act as

catalysts for the development of knowledge clusters• Stimulate arts, culture, openness sought by knowledge workers

Key Areas for Improvement – Human Capital

28A.T. Kearney / 2007

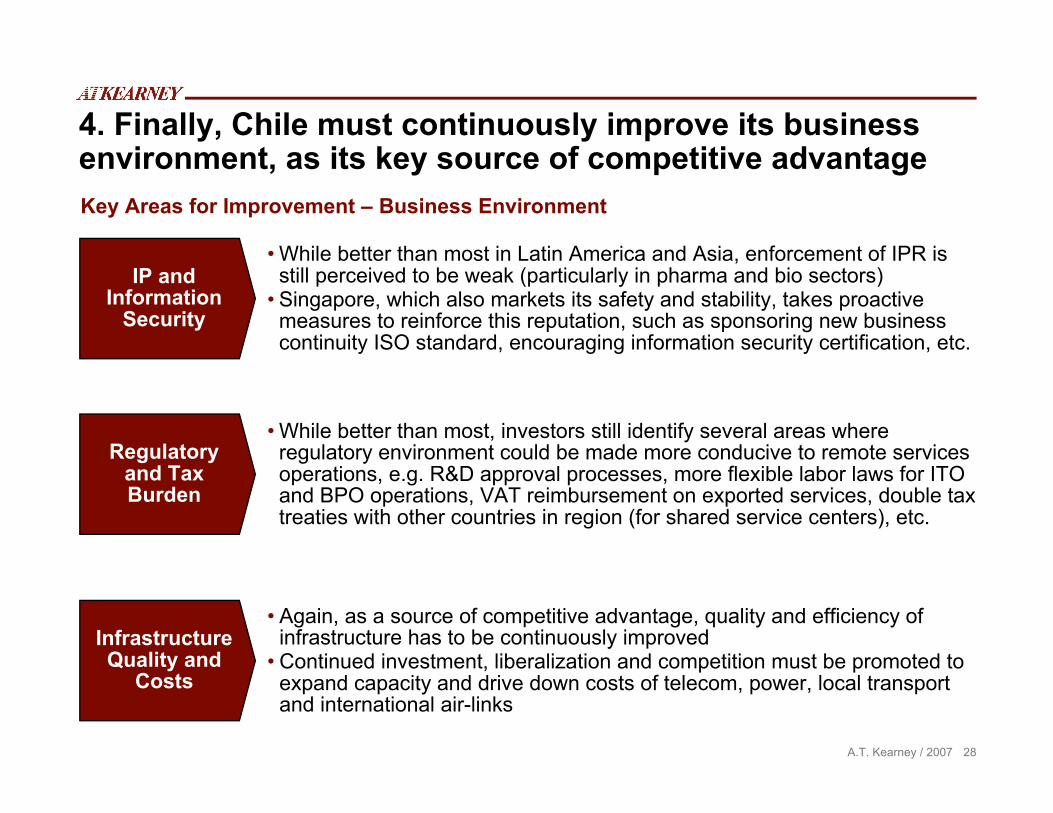

4. Finally, Chile must continuously improve its businessenvironment, as its key source of competitive advantage

IP andInformation

Security

• While better than most in Latin America and Asia, enforcement of IPR isstill perceived to be weak (particularly in pharma and bio sectors)

• Singapore, which also markets its safety and stability, takes proactivemeasures to reinforce this reputation, such as sponsoring new businesscontinuity ISO standard, encouraging information security certification, etc.

Regulatoryand TaxBurden

• While better than most, investors still identify several areas whereregulatory environment could be made more conducive to remote servicesoperations, e.g. R&D approval processes, more flexible labor laws for ITOand BPO operations, VAT reimbursement on exported services, double taxtreaties with other countries in region (for shared service centers), etc.

InfrastructureQuality and

Costs

• Again, as a source of competitive advantage, quality and efficiency ofinfrastructure has to be continuously improved

• Continued investment, liberalization and competition must be promoted toexpand capacity and drive down costs of telecom, power, local transportand international air-links

Key Areas for Improvement – Business Environment

29A.T. Kearney / 2007

Thank you

For further information, please contact:

Simon Bell: [email protected]

or

Chris Callieri: [email protected]