lesson 14-1

DESCRIPTION

LESSON 14-1. Budget Planning. BUDGET FUNCTIONS. page 413. Planning Operational control Department coordination. BUDGET PERIOD. page 413. Long-range budget Annual budget Quarterly budget Monthly budget. SOURCES OF BUDGET INFORMATION. page 414. Company records - PowerPoint PPT PresentationTRANSCRIPT

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 14-1LESSON 14-1

Budget Planning

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

2

LESSON 14-1

BUDGET FUNCTIONSBUDGET FUNCTIONS

Planning Operational control Department coordination

page 413

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

3

LESSON 14-1

BUDGET PERIODBUDGET PERIOD

Long-range budget Annual budget Quarterly budget Monthly budget

page 413

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

4

LESSON 14-1

SOURCES OF BUDGET INFORMATIONSOURCES OF BUDGET INFORMATION

Company records General economic information Company staff and managers Good judgment

page 414

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

5

LESSON 14-1

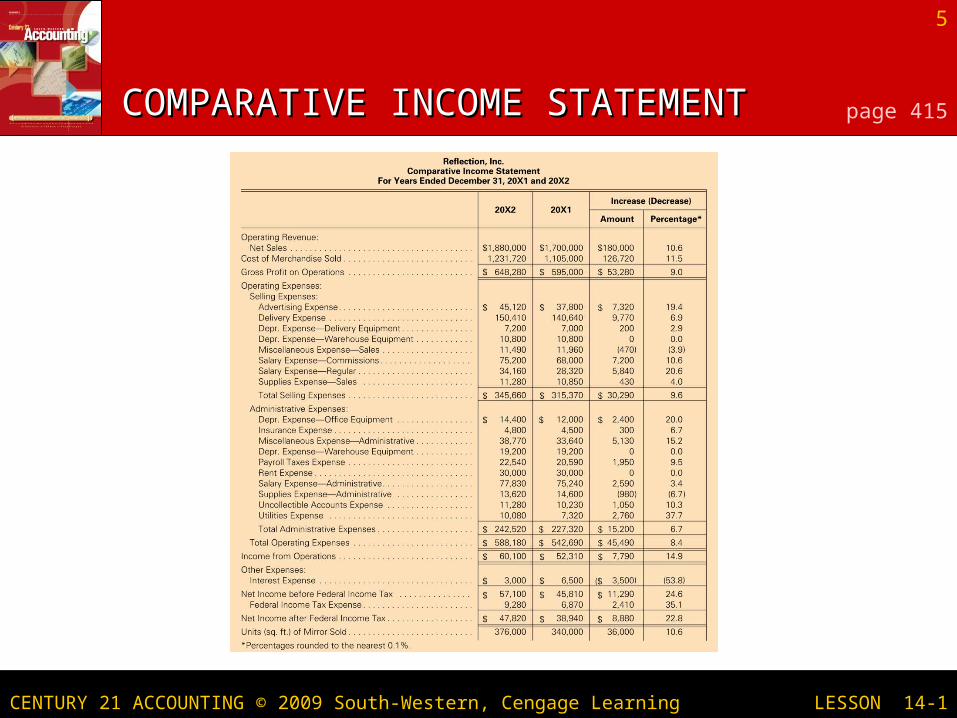

COMPARATIVE INCOME STATEMENTCOMPARATIVE INCOME STATEMENT page 415

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

6

LESSON 14-1

INTERPRETING THE COMPARATIVE INTERPRETING THE COMPARATIVE INCOME STATEMENTINCOME STATEMENT page 416

Compare the percentage change in expenses or costs to the percentage change in sales. Effect on net income

If the % increase in expenses or costs > the % increase in sales, net income decreases.

Unfavorable

If the % increase in expenses or costs < the % increase in sales, net income increases.

Favorable

If the % decrease in expenses or costs > the % decrease in sales, net income increases.

Favorable

If the % decrease in expenses or costs < the % decrease in sales, net income decreases.

Unfavorable

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

7

LESSON 14-1

TERMS REVIEWTERMS REVIEW

budgeting budget budget period comparative income statement

page 417

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 14-2LESSON 14-2

Budgeted Income Statement

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

9

LESSON 14-2

1. Enter actual and projected units.

2. Determine sales percentages.

6. Calculate total net sales.

3. Calculate unit sales volume.

4. Enter unit sales prices.

5. Calculate projected net sales.

SALES BUDGET SCHEDULESALES BUDGET SCHEDULE page 419

11

6633

5544

22

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

10

LESSON 14-2

1. Calculate ending inventory for each quarter.

2. Enter projected unit sales.

3. Determine total units needed.

4. Enter beginning inventory.

6. Enter unit cost.

5. Determine purchases.

7. Determine cost of purchases.

PURCHASES BUDGET SCHEDULEPURCHASES BUDGET SCHEDULE page 420

11

22

33

44

55

77

66

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

11

LESSON 14-2

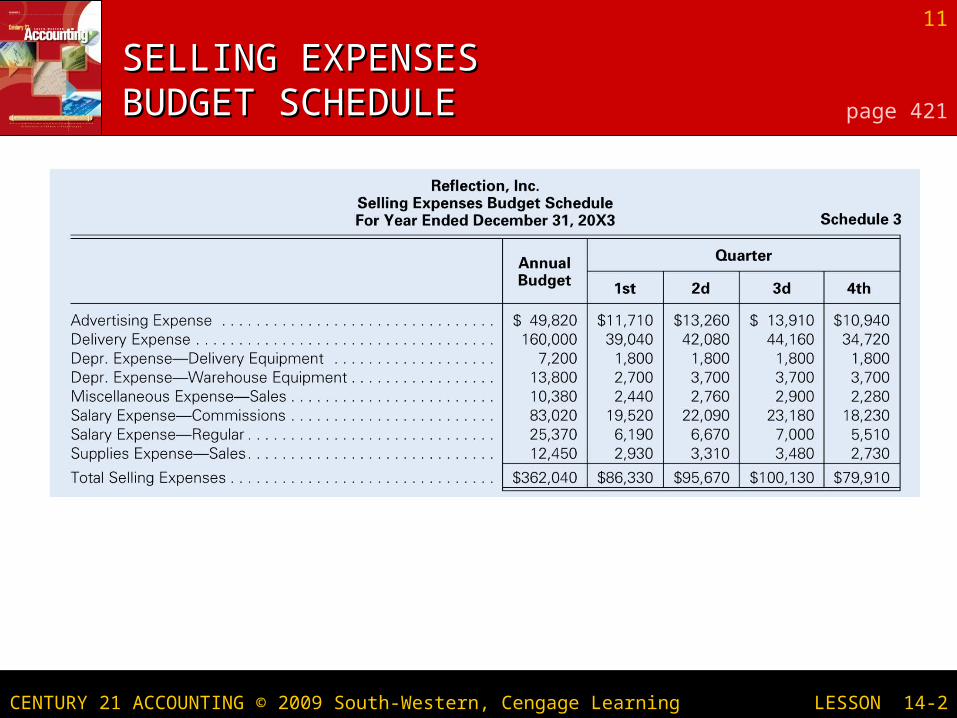

SELLING EXPENSES SELLING EXPENSES BUDGET SCHEDULEBUDGET SCHEDULE page 421

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

12

LESSON 14-2

ADMINISTRATIVE EXPENSESADMINISTRATIVE EXPENSESBUDGET SCHEDULEBUDGET SCHEDULE page 423

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

13

LESSON 14-2

OTHER REVENUE AND EXPENSES OTHER REVENUE AND EXPENSES BUDGET SCHEDULEBUDGET SCHEDULE page 424

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

14

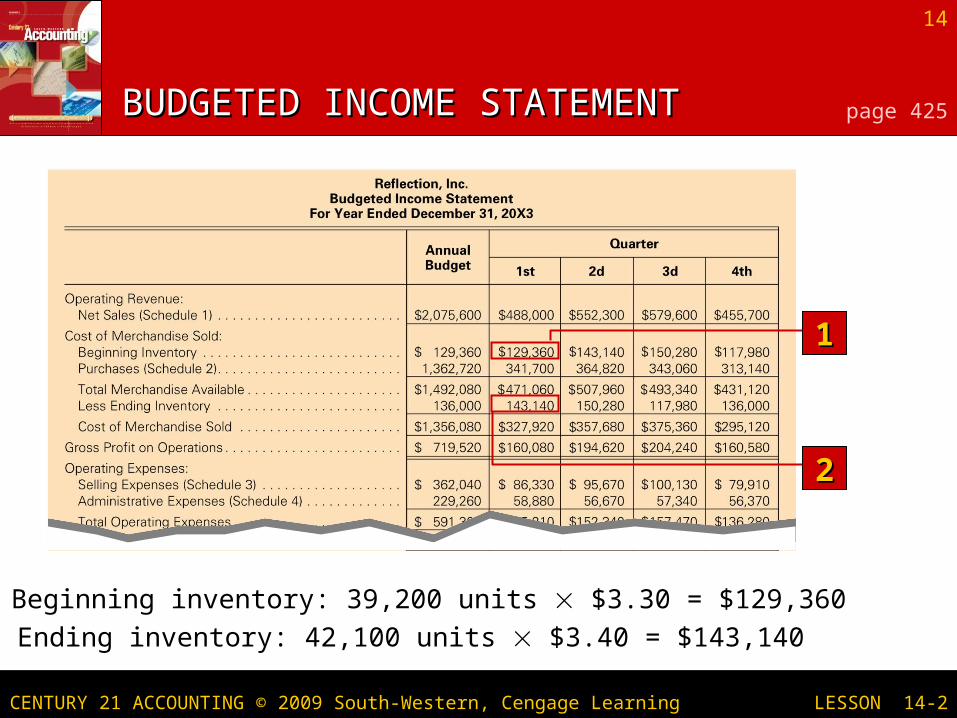

LESSON 14-2

1. Beginning inventory: 39,200 units $3.30 = $129,360

2. Ending inventory: 42,100 units $3.40 = $143,140

BUDGETED INCOME STATEMENTBUDGETED INCOME STATEMENT page 425

11

22

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

15

LESSON 14-2

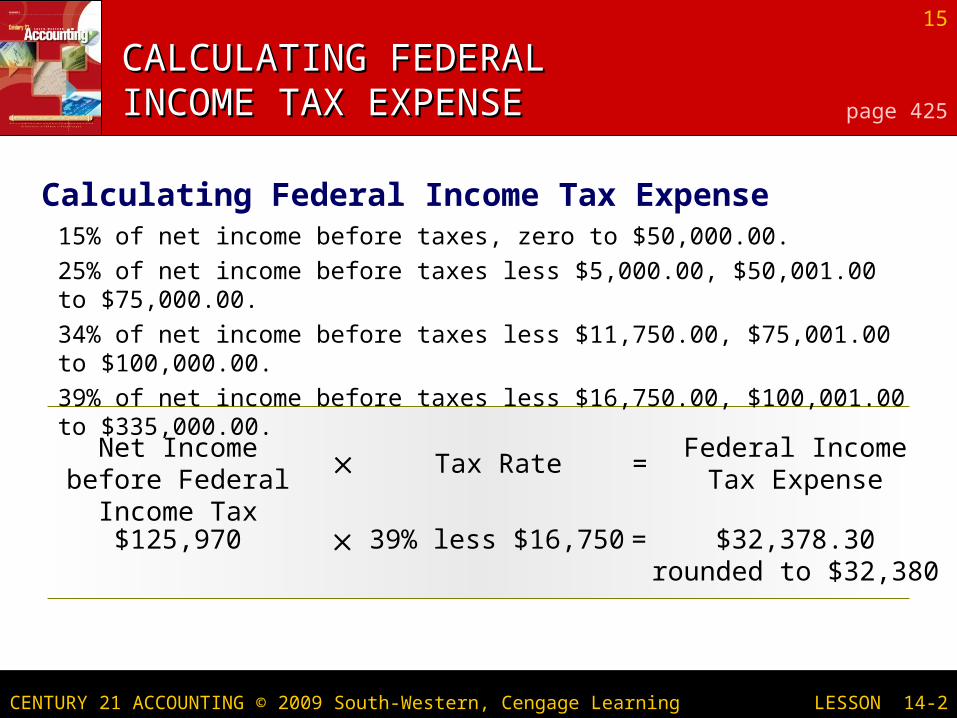

Net Income before Federal Income Tax

Tax Rate =Federal IncomeTax Expense

15% of net income before taxes, zero to $50,000.00.

25% of net income before taxes less $5,000.00, $50,001.00 to $75,000.00.

34% of net income before taxes less $11,750.00, $75,001.00 to $100,000.00.

39% of net income before taxes less $16,750.00, $100,001.00 to $335,000.00.

CALCULATING FEDERAL CALCULATING FEDERAL INCOME TAX EXPENSEINCOME TAX EXPENSE page 425

Calculating Federal Income Tax Expense

$125,970 39% less $16,750 = $32,378.30rounded to $32,380

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

16

LESSON 14-2

TERMS REVIEWTERMS REVIEW

sales budget schedule purchases budget schedule selling expenses budget schedule administrative expenses budget schedule other revenue and expenses budget schedule budgeted income statement

page 426

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 14-3LESSON 14-3

Cash Budgets and Performance Reports

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

18

LESSON 14-3

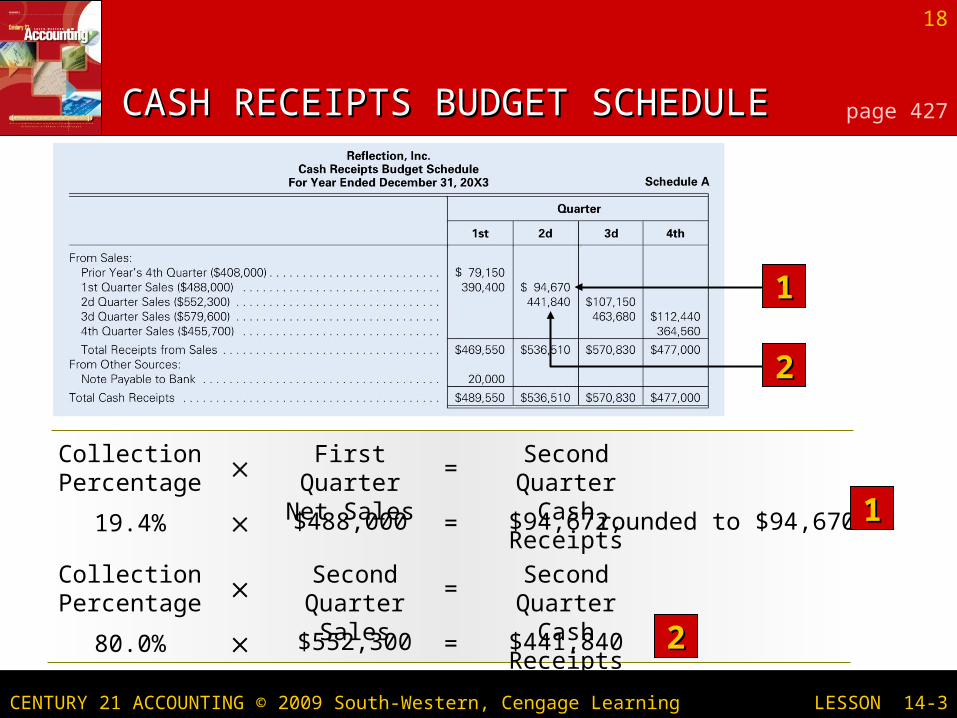

CASH RECEIPTS BUDGET SCHEDULECASH RECEIPTS BUDGET SCHEDULE page 427

Collection Percentage

First QuarterNet Sales

=Second QuarterCash Receipts

19.4% $488,000 = $94,672, rounded to $94,670

Collection Percentage

Second Quarter Sales

=Second QuarterCash Receipts

80.0% $552,300 = $441,840

11

11

22

22

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

19

LESSON 14-3

CASH PAYMENTS BUDGET SCHEDULECASH PAYMENTS BUDGET SCHEDULE page 429

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

20

LESSON 14-3

CASH BUDGETCASH BUDGET page 430

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

21

LESSON 14-3

PERFORMANCE REPORTPERFORMANCE REPORT page 431

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

22

LESSON 14-3

PERFORMANCE REPORTPERFORMANCE REPORT page 431

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

23

LESSON 14-3

TERMS REVIEWTERMS REVIEW

cash receipts budget schedule cash payments budget schedule cash budget performance report

page 433