latin american mobile economy snapshot

TRANSCRIPT

The Global Media Intelligence ReportLatin America

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-1

Latin AmericaThanks to a wealth of natural resources, rising investment and an expanding consumer base, Latin America has been partly sheltered from economic problems elsewhere, such as the financial turmoil in the eurozone. Yet all parts of the region—Central and South America and the Caribbean—are directly exposed to economic conditions in North America, and may see adverse effects if the US is hurt by Europe’s crises or hobbled by further downturns in domestic demand. Real GDP in Latin America rose 4.5% in 2011, according to the July 2012 “Worldwide Economic Outlook Update” prepared by the International Monetary Fund (IMF). The rate of growth is expected to drop slightly, to 3.4% in 2012, before climbing back to 4.2% in 2013.

These solid economic gains mean bigger budgets for many advertisers. Ad spending in Latin America topped $30 billion in 2011, eMarketer estimates, and will reach nearly $35 billion in 2012, a rise of 12%. Growth rates are expected to average about 10% during the next four years and drive spending on measured media to $51.33 billion. Brazil will continue to account for more than half of all ad spending in the region, but Argentina, representing 14% in 2012, is the area’s fastest-growing advertising market and has already overtaken Mexico to occupy second place in ad dollars regionally.

billions

Total Media Ad Spending in Latin America, by Country,2010-2016

$27.41$30.94

$34.65$38.12

$42.69$46.75

$51.33

Brazil Argentina Mexico Other

Note: includes digital (online and mobile), directories, magazines, newspapers, outdoor, radio and TV; numbers may not add up to total due to roundingSource: eMarketer, Sep 2012141858 www.eMarketer.com

20112010 2012 2013 2014 2015 2016

$14.81

$3.17$3.73

$5.69

$16.58

$4.12$4.05

$6.19

$18.46

$4.95

$4.47

$6.77

$20.12

$5.83

$4.85

$7.33

$22.53

$6.87

$5.28

$8.00

$24.78

$7.57

$5.69

$8.70

$27.63

$8.22

$6.08

$9.39

141858

Internet penetration in Latin America is relatively poor, except in urban areas. As a result, fewer than half (42.6%) of the region’s residents, some 255 million people, will be online in 2012. This proportion is rising by several percentage points each year, an encouraging trend when household penetration of broadband is only 30% in 2012. Countries with more robust infrastructure—notably Argentina—will demonstrate levels of web usage well above the regional average.

% of population in each group

Internet User Penetration in Latin America, byCountry, 2011-2016

2011 2012 2013 2014 2015 2016

Argentina 49.8% 54.3% 58.7% 63.0% 66.8% 68.0%

Brazil 39.0% 42.0% 44.0% 46.0% 47.0% 48.0%

Mexico 35.5% 40.5% 44.5% 48.0% 51.1% 53.8%

Other 37.1% 42.1% 46.1% 49.7% 52.9% 55.4%

Latin America 38.4% 42.6% 46.0% 49.0% 51.5% 53.4%Note: individuals of any age who use the internet from any location via anydevice at least once per monthSource: eMarketer, Feb 2012136973 www.eMarketer.com

136973

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-2

Latin America

With internet penetration so low, it is no surprise that digital ads represent a mere fraction of all advertising expenditures. Inevitably, though, that share is climbing. Digital advertising will make up 10.4% of total ad spending in 2012, eMarketer estimates, and will account for 15% by 2016.

billions

Digital Ad Spending in Latin America, by Country,2010-2016

2010 2011 2012 2013 2014 2015 2016

Brazil $1.12 $1.46 $2.05 $2.45 $3.14 $3.61 $4.13

Mexico* $0.28 $0.40 $0.53 $0.70 $0.92 $1.13 $1.34

Argentina $0.22 $0.34 $0.47 $0.59 $0.77 $0.94 $1.11

Other $0.41 $0.48 $0.57 $0.68 $0.84 $1.01 $1.10

Latin America $2.03 $2.67 $3.62 $4.43 $5.67 $6.69 $7.68Note: includes advertising that appears on desktop and laptop computersas well as mobile phones and tablets, and includes all the various formatsof advertising on those platforms; excludes SMS, MMS and P2Pmessaging-based advertising; numbers may not add up to total due torounding; *eMarketer benchmarks its Mexico online ad spendingprojections against the IAB México/PwC data for which the last full yearmeasured was 2011Source: eMarketer, Sep 2012144756 www.eMarketer.com

144756

Latin America boasts far more mobile phone users—nearly 390 million in 2012—than web users. Yet here too there is enormous untapped potential. eMarketer estimates that fewer than two-thirds of the entire population will own a mobile this year, and less than one in four of those individuals will have a smartphone. Across the region, the number of people using a mobile handset to go online in 2012 will reach 100 million.

Despite the slow advance of some technologies, internet users in Latin America have seized many digital opportunities with enthusiasm. For example, the region currently posts some of the world’s most impressive levels of social networking, according to eMarketer calculations. Data from comScore also points to extraordinarily high social networking engagement in early 2012. Brazil is reckoned to have one of the highest proportions of internet users using social networks (74% in 2012) anywhere in the world, eMarketer estimates. Overall, 68.9% of web users in the region will be regular visitors to social sites this year—well above the global average of 61.9%. The regional average will continue to exceed the worldwide average by more than five percentage points through 2014.

% of internet users in each group

Social Network User Penetration Worldwide, byRegion, 2010-2014

2010 2011 2012 2013 2014

Middle East & Africa 55.9% 62.8% 70.2% 76.6% 80.2%

Eastern Europe 65.1% 67.6% 69.0% 71.5% 73.1%

Latin America 60.9% 65.3% 68.9% 72.4% 74.9%

North America 60.0% 63.6% 65.8% 66.9% 68.0%

Asia-Pacific 46.8% 52.3% 58.1% 63.7% 67.9%

Western Europe 44.0% 49.8% 54.2% 57.8% 60.5%

Worldwide 52.2% 57.2% 61.9% 66.4% 69.6%Note: internet users who use a social network site via any device at leastonce per monthSource: eMarketer, Aug 2012143648 www.eMarketer.com

143648

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-3

Argentina ■ The influence of TV in Argentina may be waning, but only minimally. Over 95% of residents ages 12 to 75 watched free-to-air broadcasts at least once a week in 2011, according to TGI Latina’s “2011 Argentina Study, Waves 1–4,” and over 71% were monthly cable or satellite TV viewers. Newspapers and magazines appear to have lost readers in 2011, and attracted smaller audiences than the web. Internet usage is higher than elsewhere in Latin America. But penetration, estimated by eMarketer at 54.3% in 2012, remains far below that of North America, Western Europe or parts of Asia-Pacific.

■ Nearly 23 million consumers in Argentina will go online at least once a month in 2012, eMarketer estimates. This group has been expanding by double digits annually, though growth will drop below 10% in 2013. By 2015, two-thirds of the country’s residents will use the web. Demographically, the online population still reveals a younger, male bias. Over 64% of those online in 2011 were ages 12 to 34, and 52% were male, TGI reported. The company also found that more than one-third of internet users came from the lowest socioeconomic levels, and for the first time, the most affluent consumers accounted for less than 20% of web users.

■ Broadband is finally reaching substantial numbers of residents. The tally of fixed broadband subscriptions in Argentina surged by nearly 45% in 2011, to 7.4 million, and will top 9 million in 2012, according to eMarketer projections. But household penetration will likely not pass 50% until 2014.

■ As TGI noted, only television enjoyed wider reach than mobile phones in 2011. More than 33 million people in Argentina will own a mobile phone in 2012—some 79% of the population, according to eMarketer forecasts. Mobile penetration is expected to hit 84% in 2016, as usage spreads through all age and income brackets. In addition, the pronounced female bias among mobile users reported by TGI Latina in 2010 diminished last year. In 2011, 51.2% of Argentina’s mobile phone users were female, vs. 48.8% male.

■ Despite high mobile phone penetration, smartphones are not widespread. The number of smartphone users will leap 40% in 2012, eMarketer predicts, but will amount to no more than 7.7 million—less than one-quarter of Argentina’s mobile phone users and around 18% of the entire population. The market for advanced mobile handsets is still embryonic, and users display several “early adopter” characteristics. Some 59% of smartphone owners were male in 2011, according to TGI, and 64% were ages 12 to 34.

■ As in many other countries, mobile web usage correlates closely with smartphone ownership. eMarketer estimates that just 8 million residents will go online via mobile at least once per month in 2012. But the outlook for mobile web use is excellent. In 2016, nearly half of Argentina’s mobile phone users—around 17 million people—will use a handset to access the web.

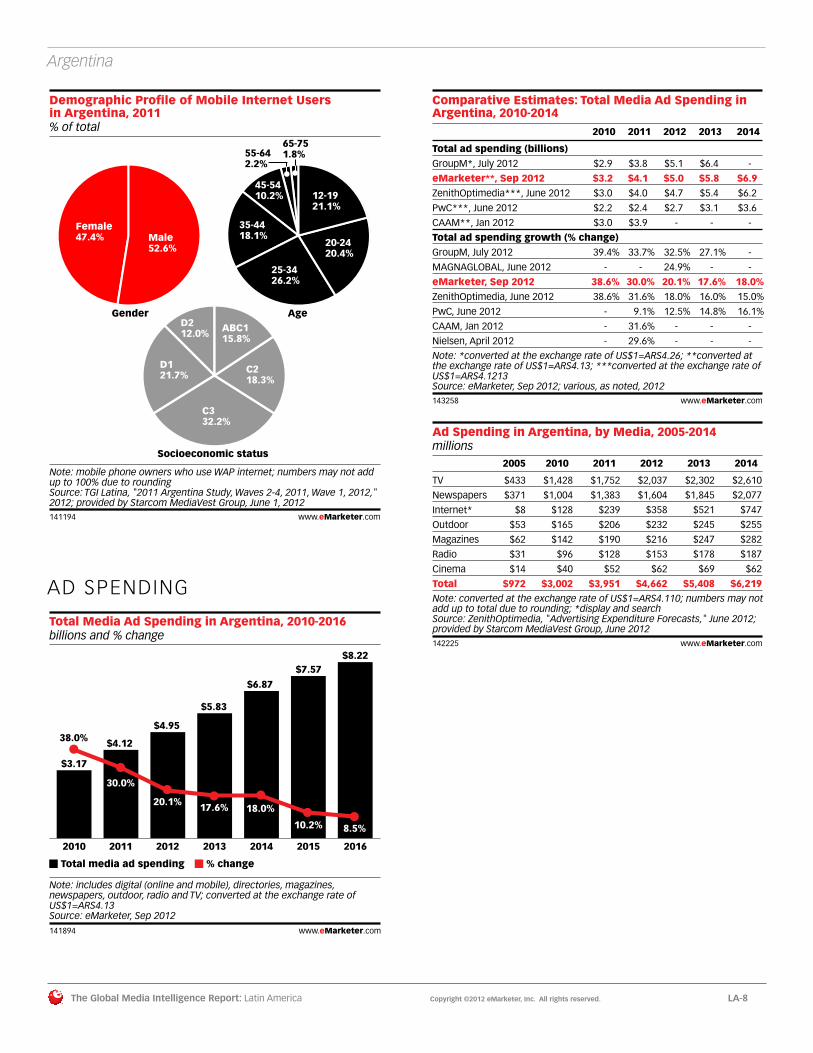

■ Research firms agree that 2011 was a boom year for Argentina’s advertising sector. Spending in all measured media grew by a remarkable 30%, according to eMarketer estimates, to reach $4.1 billion. Most other sources also put 2011 growth at similar levels. Looking to 2012 and beyond, eMarketer has projected slightly higher totals than the majority of other firms, but the variation is not great. The clear outlier is PricewaterhouseCoopers (PwC), whose projected spending figures are substantially lower than all others.

■ Spending on digital ads is rising more quickly than any other category—by 55% in 2011 alone, eMarketer estimates. The internet became Argentina’s third most important media channel for advertising in 2011, according to ZenithOptimedia, and will consolidate that position in coming years. Yet digital spending, including online and mobile formats, will constitute only 9.5% of total ad spending in 2012, eMarketer predicts. The actual value of Argentina’s online ad market is also hotly debated. eMarketer has forecast that digital spending will reach $470 million this year. Other recent estimates of 2012 spending range from $110 million (PwC, June 2012) to $358 million (ZenithOptimedia, June 2012). eMarketer’s figure is higher chiefly because it includes several types of digital advertising, such as email and lead generation, which other firms do not. Mobile advertising will amount to an estimated $11 million this year, a gain of 73% compared to 2011.

■ In October 2011, Cristina Fernández de Kirchner was re-elected to a second four-year term as Argentina’s president. Such continuity has its dangers, however, as Fernández has shown a tendency to ad hoc actions that may undermine financial stability and weaken important institutions. According to the Economist Intelligence Unit (EIU), Argentina’s current legal, economic and regulatory environment makes it “one of the less attractive investment locations” among the world’s emerging economies. As of mid-2012, the EIU also noted that inflation—pegged by numerous analysts between 10% and 22%, the highest in the region—and public unease at wage stagnation were both contributing to a looming crisis of consumer and business confidence. GDP did rise by 8.9% in 2011, but the EIU expected the rate of growth to plummet this year, to just 2.1%, prior to a 2.7% gain in 2013.

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-4

Argentina

POPULATION

millionsPopulation in Argentina, 2010-2020

2010

41.3

50

100

2012

42.2

2014

43.0

2016

43.8

2018

44.6

2020

45.4

Note: population as of July for each yearSource: US Census Bureau, International Data Base, June 27, 2012142190 www.eMarketer.com

142190

MEDIA

% of populationMedia Penetration in Argentina, 2011

TV viewers (1) 95.2%

Mobile phone owners 76.3%

Cable/satellite TV viewers (1) 71.4%

Radio listeners (2) 68.3%

Internet users (3) 53.6%

Newspaper readers (4) 43.2%

Magazine readers (5)21.4%

Mobile internet users (6)7.1%

Note: ages 12-75; (1) viewed in the past week; (2) listened yesterday; (3)used in the past 30 days; (4) read weekday and Sunday publications; (5)read any publication; (6) mobile phone owners who use WAP internetSource: TGI Latina, "2011 Argentina Study, Waves 2-4, 2011, Wave 1, 2012,"2012; provided by Starcom MediaVest Group, June 1, 2012141184 www.eMarketer.com

141184

% of totalDemographic Profile of Media Users in Argentina, 2011

Internet users (1)

Mobile phone owners

TV viewers (2)

Cable/satellite TV viewers (2)

Radio listeners (3)

Magazine readers (4)

Newspaper readers (5)

GenderMale

Female

Age12-19

20-24

25-34

35-44

45-54

55-64

65-75

Socioeconomic statusABC1

C2

C3

D1

D2

52.0%

48.0%

26.0%

16.0%

22.3%

15.6%

11.7%

5.9%

2.5%

19.2%

15.2%

31.0%

21.9%

12.7%

48.8%

51.2%

17.7%

13.4%

21.7%

18.1%

15.1%

9.2%

4.8%

13.9%

11.9%

26.5%

26.8%

21.0%

47.7%

52.3%

18.8%

11.9%

19.2%

16.7%

14.5%

10.2%

8.8%

10.9%

9.8%

24.5%

27.8%

27.0%

49.0%

51.0%

19.3%

11.5%

19.4%

16.1%

14.6%

10.5%

8.6%

14.7%

12.2%

26.4%

26.4%

20.4%

48.9%

51.1%

17.8%

12.1%

19.3%

16.5%

14.1%

10.9%

9.3%

11.3%

10.0%

24.7%

27.9%

26.0%

38.9%

61.1%

18.9%

11.0%

20.2%

17.6%

15.2%

10.2%

6.9%

16.5%

11.7%

25.5%

25.1%

21.2%

50.5%

49.5%

12.3%

11.2%

20.7%

17.6%

17.1%

11.7%

9.3%

16.9%

11.8%

25.2%

25.0%

21.2%

Note: numbers may not add up to 100% due to rounding; (1) used in the past 30 days; (2) viewed in the past week; (3) listened yesterday; (4) read any publication; (5) read weekday and Sunday publicationsSource: TGI Latina, "2011 Argentina Study, Waves 2-4, 2011, Wave 1, 2012," 2012; provided by Starcom MediaVest Group, June 1, 2012141185 www.eMarketer.com

141185

INTERNET

millions, % of population and % changeInternet Users and Penetration in Argentina, 2011-2016

2011

20.8

49.8%

11.1%

2012

22.9

54.3%

10.1%

2013

25.0

58.7%

9.2%

2014

27.1

63.0%

8.4%

2015

29.0

66.8%

7.0%

2016

29.8

68.0%

2.7%

Internet users % of population % change

Note: individuals of any age who use the internet from any location via anydevice at least once per monthSource: eMarketer, Feb 2012136989 www.eMarketer.com

136989

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-5

Argentina

Comparative Estimates: Internet Users andPenetration in Argentina, 2010-2012

2010 2011 2012

Internet users (millions)eMarketer*, Feb 2012 18.7 20.8 22.9comScore Inc.**, May 2012 - 12.9 13.4

Prince & Cooke, Dec 2011 26.5 30.5 -

Internet user penetration (% of population)eMarketer*, Feb 2012 45.3% 49.8% 54.3%TGI Latina***, June 2012 - 53.6% -

ITU, July 2012 - 47.7% -

Note: *individuals of any age who use the internet from any location viaany device at least once per month; **ages 15+; home and work locations;data is for Jan of each year; ***ages 12-75; used in the past 30 daysSource: eMarketer, Feb 2012; various, as noted, 2011 & 2012143240 www.eMarketer.com

143240

Gender Age

Socioeconomic status

% of total

Demographic Profile of Internet Users in Argentina,2011

Male52.0%

Female48.0%

12-1926.0%

20-2416.0%

25-3422.3%

35-4415.6%

45-5411.7%

55-645.9%

65-752.5%

ABC119.2%

C215.2%

C331.0%

D121.9%

D212.7%

Note: used in the past month; numbers may not add up to 100% due toroundingSource: TGI Latina, "2011 Argentina Study, Waves 2-4, 2011, Wave 1, 2012," 2012; provided by Starcom MediaVest Group, June 1, 2012141190 www.eMarketer.com

141190

Fixed Broadband Households and Subscriptions in Argentina, 2010-2016

Households (millions)—% change

—Household penetration

Subscriptions (millions)—% change

2010

4.221.8%

37.5%

5.119.5%

2011

4.814.9%

42.7%

7.444.7%

2012

5.310.4%

46.7%

9.021.4%

2013

5.77.2%

49.6%

10.414.7%

2014

6.05.1%

51.7%

11.38.9%

2015

6.23.6%

53.1%

11.84.8%

2016

6.32.7%

54.1%

12.33.9%

Note: includes connections with permanent access to the internet viacable modem, DSL, fiber and wireless/satellite technologies; excludesmobileSource: eMarketer, April 2012139108 www.eMarketer.com

139108

Comparative Estimates: Fixed Broadband Householdsand Penetration in Argentina, 2010-2012

2010 2011 2012

Fixed broadband households (millions)eMarketer*, April 2012 4.2 4.8 5.3GroupM, April 2012 3.8 4.3 4.7

INDEC**, March 2012 5.1 8.1 -

Fixed broadband household penetration (% of households)PwC, June 2012 43.2% 50.6% 55.6%

eMarketer*, April 2012 37.5% 42.7% 46.7%GroupM, April 2012 33.0% 36.0% 39.0%

Note: *includes connections with permanent access to the internet viacable modem, DSL, fiber and wireless/satellite technologies; excludesmobile; **data is for Dec of each yearSource: eMarketer, April 2012; various, as noted, 2012143241 www.eMarketer.com

143241

Social Network Users and Penetration in Argentina,2010-2014

Social network users (millions)—% change

—% of internet users

—% of population

2010

11.639.4%

61.8%

28.0%

2011

14.122.0%

67.9%

33.8%

2012

15.912.7%

69.5%

37.7%

2013

17.811.5%

71.0%

41.7%

2014

19.59.9%

72.0%

45.4%

Note: internet users who use a social network site via any device at leastonce per monthSource: eMarketer, Aug 2012143662 www.eMarketer.com

143662

% of internet users

Comparative Estimates: Social Network UserPenetration in Argentina, 2011 & 2012

Ipsos*, March 2012

eMarketer, Aug 2012

comScore Inc.**,Dec 2011

Randstad, March 2011

TGI Latina, June 2012

2011

-

67.9%

96.0%

84.0%

64.8%

2012

76.0%

69.5%

-

-

-

Usage

Visited in past 3 months

Use via any device atleast once per month

-

Have a profile

Used in past 30 days

Age

16-64

All ages

15+

18-65

12-75

Note: *includes social network sites, forums or blogs; **home and worklocations; data is for OctSource: eMarketer, Aug 2012; various, as noted, 2011 & 2012143243 www.eMarketer.com

143243

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-6

Argentina

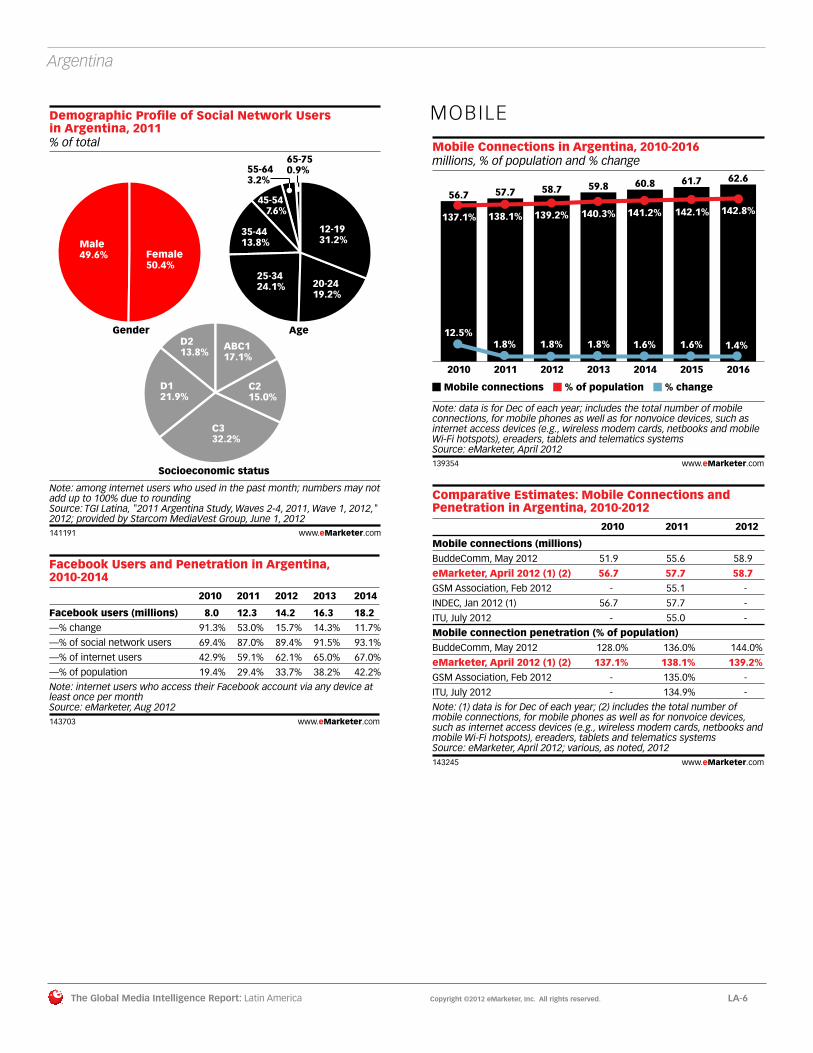

% of total

Demographic Profile of Social Network Usersin Argentina, 2011

Note: among internet users who used in the past month; numbers may notadd up to 100% due to roundingSource: TGI Latina, "2011 Argentina Study, Waves 2-4, 2011, Wave 1, 2012," 2012; provided by Starcom MediaVest Group, June 1, 2012141191 www.eMarketer.com

Gender Age

Socioeconomic status

Female50.4%

Male49.6%

12-1931.2%

20-2419.2%

25-3424.1%

35-4413.8%

45-54 7.6%

55-643.2%

65-750.9%

ABC117.1%

C215.0%

C332.2%

D121.9%

D213.8%

141191

Facebook Users and Penetration in Argentina,2010-2014

2010 2011 2012 2013 2014

Facebook users (millions) 8.0 12.3 14.2 16.3 18.2—% change 91.3% 53.0% 15.7% 14.3% 11.7%

—% of social network users 69.4% 87.0% 89.4% 91.5% 93.1%

—% of internet users 42.9% 59.1% 62.1% 65.0% 67.0%

—% of population 19.4% 29.4% 33.7% 38.2% 42.2%

Note: internet users who access their Facebook account via any device atleast once per monthSource: eMarketer, Aug 2012143703 www.eMarketer.com

143703

MOBILE

millions, % of population and % changeMobile Connections in Argentina, 2010-2016

2010

56.7

137.1%

12.5%

2011

57.7

138.1%

1.8%

2012

58.7

139.2%

1.8%

2013

59.8

140.3%

1.8%

2014

60.8

141.2%

1.6%

2015

61.7

142.1%

1.6%

2016

62.6

142.8%

1.4%

Mobile connections % of population % change

Note: data is for Dec of each year; includes the total number of mobileconnections, for mobile phones as well as for nonvoice devices, such asinternet access devices (e.g., wireless modem cards, netbooks and mobileWi-Fi hotspots), ereaders, tablets and telematics systemsSource: eMarketer, April 2012139354 www.eMarketer.com

139354

Comparative Estimates: Mobile Connections andPenetration in Argentina, 2010-2012

2010 2011 2012

Mobile connections (millions)BuddeComm, May 2012 51.9 55.6 58.9

eMarketer, April 2012 (1) (2) 56.7 57.7 58.7GSM Association, Feb 2012 - 55.1 -

INDEC, Jan 2012 (1) 56.7 57.7 -

ITU, July 2012 - 55.0 -

Mobile connection penetration (% of population)BuddeComm, May 2012 128.0% 136.0% 144.0%

eMarketer, April 2012 (1) (2) 137.1% 138.1% 139.2%GSM Association, Feb 2012 - 135.0% -

ITU, July 2012 - 134.9% -

Note: (1) data is for Dec of each year; (2) includes the total number ofmobile connections, for mobile phones as well as for nonvoice devices,such as internet access devices (e.g., wireless modem cards, netbooks andmobile Wi-Fi hotspots), ereaders, tablets and telematics systemsSource: eMarketer, April 2012; various, as noted, 2012143245 www.eMarketer.com

143245

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-7

Argentina

millions, % of population and % changeMobile Phone Users in Argentina, 2010-2016

2010

31.0

75.0%

6.7%

2011

32.2

77.0%

3.7%

2012

33.3

79.0%

3.6%

2013

34.5

81.0%

3.5%

2014

35.3

82.0%

2.2%

2015

36.0

83.0%

2.2%

2016

36.8

84.0%

2.1%

Mobile phone users % of population % change

Note: mobile phone users are individuals of any age who own at least onemobile phone and use the phone(s) at least once per monthSource: eMarketer, April 2012139312 www.eMarketer.com

139312

% of total

Demographic Profile of Mobile Phone Ownersin Argentina, 2011

Note: numbers may not add up to 100% due to roundingSource: TGI Latina, "2011 Argentina Study, Waves 2-4, 2011, Wave 1, 2012," 2012; provided by Starcom MediaVest Group, June 1, 2012141192 www.eMarketer.com

Gender Age

Socioeconomic status

Female51.2%

Male48.8%

12-1917.7%

20-2413.4%

25-3421.7%

35-4418.1%

45-5415.1%

55-64 9.2%

65-754.8%

ABC113.9%

C211.9%

C326.5%

D126.8%

D221.0%

141192

Smartphone Users and Penetration in Argentina,2010-2016

Smartphoneusers (millions)—% change

—% of mobilephone users

—% of population

2010

2.5

70.8%

8.0%

6.0%

2011

5.5

120.4%

17.0%

13.1%

2012

7.7

40.2%

23.0%

18.2%

2013

10.0

30.6%

29.0%

23.5%

2014

12.3

23.4%

35.0%

28.7%

2015

14.8

19.7%

41.0%

34.0%

2016

16.6

12.1%

45.0%

37.8%

Note: smartphone users are individuals of any age who own at least onesmartphone and use the smartphone(s) at least once per monthSource: eMarketer, April 2012139344 www.eMarketer.com

139344

% of total

Demographic Profile of Smartphone Owners in Argentina, 2011

Note: numbers may not add up to 100% due to roundingSource: TGI Latina, "2011 Argentina Study, Waves 2-4, 2011, Wave 1, 2012," 2012; provided by Starcom MediaVest Group, June 1, 2012141193 www.eMarketer.com

Gender Age

Socioeconomic status

Male59.0%

Female41.0%

12-1922.0%

20-2413.5%

25-3428.5%

35-4420.5%

45-54 8.5%

55-644.5%

65-752.5%

ABC121.9%

C216.3%

C330.7%

D116.3%

D214.9%

141193

Mobile Internet Users and Penetration in Argentina,2010-2016

2016

Mobile internetusers (millions)

16.9

—% change 11.9%

—% of mobilephone users

46.0%

—% of population

2010

2.8

37.2%

9.0%

6.8%

2011

5.8

107.5%

18.0%

13.9%

2012

8.0

38.2%

24.0%

19.0%

2013

10.4

29.4%

30.0%

24.3%

2014

12.7

22.7%

36.0%

29.5%

2015

15.1

19.2%

42.0%

34.9% 38.6%

Note: mobile phone users of any age who access the internet from amobile browser or an installed application at least once per month;excludes SMS, MMS and IMSource: eMarketer, April 2012139327 www.eMarketer.com

139327

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-8

Argentina

% of total

Demographic Profile of Mobile Internet Usersin Argentina, 2011

Note: mobile phone owners who use WAP internet; numbers may not addup to 100% due to roundingSource: TGI Latina, "2011 Argentina Study, Waves 2-4, 2011, Wave 1, 2012," 2012; provided by Starcom MediaVest Group, June 1, 2012141194 www.eMarketer.com

Gender Age

Socioeconomic status

Male52.6%

Female47.4%

12-1921.1%

20-2420.4%

25-3426.2%

35-4418.1%

45-5410.2%

55-642.2%

65-751.8%

ABC115.8%

C218.3%

C332.2%

D121.7%

D212.0%

141194

AD SPENDING

billions and % changeTotal Media Ad Spending in Argentina, 2010-2016

$3.17

38.0% $4.12

30.0%

$4.95

20.1%

$5.83

17.6%

$6.87

18.0%

$7.57

10.2%

$8.22

8.5%

Total media ad spending % change

Note: includes digital (online and mobile), directories, magazines, newspapers, outdoor, radio and TV; converted at the exchange rate of US$1=ARS4.13Source: eMarketer, Sep 2012

141894 www.eMarketer.com

20112010 2012 2013 2014 2015 2016

141894

Comparative Estimates: Total Media Ad Spending inArgentina, 2010-2014

2010 2011 2012 2013 2014

Total ad spending (billions)GroupM*, July 2012 $2.9 $3.8 $5.1 $6.4 -

eMarketer**, Sep 2012 $3.2 $4.1 $5.0 $5.8 $6.9ZenithOptimedia***, June 2012 $3.0 $4.0 $4.7 $5.4 $6.2

PwC***, June 2012 $2.2 $2.4 $2.7 $3.1 $3.6

CAAM**, Jan 2012 $3.0 $3.9 - - -

Total ad spending growth (% change)GroupM, July 2012 39.4% 33.7% 32.5% 27.1% -

MAGNAGLOBAL, June 2012 - - 24.9% - -

eMarketer, Sep 2012 38.6% 30.0% 20.1% 17.6% 18.0%ZenithOptimedia, June 2012 38.6% 31.6% 18.0% 16.0% 15.0%

PwC, June 2012 - 9.1% 12.5% 14.8% 16.1%

CAAM, Jan 2012 - 31.6% - - -

Nielsen, April 2012 - 29.6% - - -

Note: *converted at the exchange rate of US$1=ARS4.26; **converted atthe exchange rate of US$1=ARS4.13; ***converted at the exchange rate ofUS$1=ARS4.1213Source: eMarketer, Sep 2012; various, as noted, 2012143258 www.eMarketer.com

143258

millionsAd Spending in Argentina, by Media, 2005-2014

TV

Newspapers

Internet*

Outdoor

Magazines

Radio

Cinema

Total

2005

$433

$371

$8

$53

$62

$31

$14

$972

2010

$1,428

$1,004

$128

$165

$142

$96

$40

$3,002

2011

$1,752

$1,383

$239

$206

$190

$128

$52

$3,951

2012

$2,037

$1,604

$358

$232

$216

$153

$62

$4,662

2013

$2,302

$1,845

$521

$245

$247

$178

$69

$5,408

2014

$2,610

$2,077

$747

$255

$282

$187

$62

$6,219Note: converted at the exchange rate of US$1=ARS4.110; numbers may notadd up to total due to rounding; *display and searchSource: ZenithOptimedia, "Advertising Expenditure Forecasts," June 2012;provided by Starcom MediaVest Group, June 2012142225 www.eMarketer.com

142225

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-9

Argentina

20112010 2012 2013 2014 2015 2016

billions and % changeDigital Ad Spending in Argentina, 2010-2016

$0.22

44.0%

$0.34

55.1%

$0.47

37.0%$0.59

27.0%

$0.77

30.0%

$0.94

22.0%

$1.11

18.0%

Digital ad spending % change

Note: includes advertising that appears on desktop and laptop computers as well as mobile phones and tablets, and includes all the various formats of advertising on those platforms; excludes SMS, MMS and P2P messaging-based advertising; CAGR (2011-2016)=26.6%; converted at the exchange rate of US$1=ARS4.13Source: eMarketer, Sep 2012141947 www.eMarketer.com

141947

Comparative Estimates: Digital Ad Spending inArgentina, 2010-2014

Digital ad spending (millions)eMarketer, Sep 2012GroupM, July 2012 (1) (2)

ZenithOptimedia, June 2012 (1) (3)

PwC, June 2012 (4)

IAB Argentina, April 2012 (4)

CAAM, Jan 2012 (5)

BCG, March 2012

Digital ad spending growth (% change)ZenithOptimedia, June 2012 (1)

eMarketer, Sep 2012GroupM, July 2012 (1)

PwC, June 2012

IAB Argentina, April 2012

CAAM, Jan 2012

2010

$220.0$124.0

$128.0

$87.0

$127.8

$127.8

$300.0

49.5%

44.0%70.3%

-

-

-

2011

$340.0$269.0

$239.0

$95.0

$277.7

$238.2

-

86.5%

55.1%117.2%

9.2%

117.0%

86.5%

2012

$470.0$363.0

$358.0

$110.0

-

-

-

49.5%

37.0%35.0%

15.8%

-

-

2013

$590.0$491.0

$521.0

$126.0

-

-

-

45.5%

27.0%35.0%

14.5%

-

-

2014

$770.0-

$747.0

$144.0

-

-

-

43.4%

30.0%-

14.3%

-

-

Note: (1) excludes mobile; (2) converted at the exchange rate ofUS$1=ARS4.26; (3) converted at the exchange rate of US$1=ARS4.110; (4)converted at the exchange rate of US$1=ARS4.1213; (5) converted at theexchange rate of US$1=ARS4.13Source: eMarketer, Sep 2012; various, as noted, 2012143259 www.eMarketer.com

143259

millions and % changeMobile Ad Spending in Argentina, 2010-2016

$3.7

58.5%

$6.4

72.0%

$11.0

73.0%

$18.1

65.0%

$32.7

80.3%

$51.0

56.0%

$70.4

38.0%

Mobile ad spending % change

Note: includes display (banners, video and rich media) and search; excludesSMS, MMS and P2P messaging-based advertising; includes ad spending ontablets; converted at the exchange rate of US$1=ARS4.13; CAGR(2011-2016)=61.8%Source: eMarketer, Sep 2012142059 www.eMarketer.com

20112010 2012 2013 2014 2015 2016

142059

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-10

Brazil ■ Brazil was the world’s sixth largest economy in early 2012, and may rise to fifth position by the end of the year, according to “The World Factbook” prepared by the Central Intelligence Agency. But the country is not immune to financial wobbles. Industrial activity and services are gradually gaining on agriculture as sources of national revenue, but weak infrastructure and an overly complex tax regime have been identified by the EIU as major hindrances to business and investment. Brazilian GDP climbed by just 2.7% in 2011, according to the IMF, and the growth rate will dip slightly, to 2.5%, in 2012. But analysts expect a palpable boost in 2013, as the country prepares for the 2014 FIFA World Cup soccer tournament. Annual rises in GDP should remain at or above 4% between 2013 and 2016, the EIU has forecast. Brazil’s increasing population—approaching 200 million this year—is still seen as a plus, providing an ever-larger labor force, rather than a pressure on resources.

■ Even in towns and cities, most Brazilians are beyond the reach of broadband. Fewer than 30% of households will have a fixed broadband internet connection in 2012, eMarketer estimates, and the proportion will likely remain below 40% until 2016. As a result, web usage has been slow to take off, and the market is underdeveloped. eMarketer projects that just 42% of the population will go online at least once per month in 2012. Even in 2016, less than half (48%) of Brazil’s population is expected to use the web. That will amount to an estimated user base of 103 million people, however, compared to 86.4 million in 2012. eMarketer’s calculations of internet user numbers in Brazil are very close to those of other research firms, with the exception of comScore and Nielsen, which evaluate access from home and work locations only. This approach clearly excludes the many people who go online in public places such as libraries and internet cafes.

■ Despite relatively low levels of internet penetration, Brazil has embraced many aspects of the digital lifestyle. One is social networking. Nearly 64 million people—74% of the country’s online population—will use social sites at least monthly in 2012, eMarketer has projected. Moreover, the number of social networkers is growing by more than 13% annually. In less than two years, an estimated 79.3 million web users in Brazil will be regular visitors to virtual communities. The pre-eminence of Facebook, which will attract some 48% of the online population in Brazil in 2012, is less marked than in several other Latin countries, including Argentina and Mexico. But more than 87% of social network users in Brazil are expected to have Facebook accounts in 2014.

■ Brazil hosts a burgeoning mobile community. The number of mobile device connections jumped by nearly 20% in 2011, and will show similar double-digit growth again this year. By the end of 2013, total connections will reach almost 300 million. eMarketer estimates that in 2012, 58% of all residents will have at least one mobile phone. Females outnumbered males among the mobile population in 2011—by 52.8% to 47.2%—but mobile usage was widely distributed among all age and income groups, with the exception of seniors (ages 65 to 75) and the poorest residents. By contrast, use of smartphones and the mobile web was generally associated with younger, more affluent demographic segments in 2011. And the mobile internet, in particular, remains a minority activity. Just 31% of Brazil’s mobile phone users will go online via handset in 2012, according to eMarketer calculations.

■ Research firms generally agree that the Brazilian advertising industry enjoyed a significant lift in 2011, and most predict another growth spurt in 2012. Estimates for total ad spending this year range from $14.6 billion (GroupM, July 2012) to $20.3 billion (Projeto Inter-Meios [PIM], March 2012), though most projections—including eMarketer’s—cluster between $18 billion and $19.5 billion.

■ Estimates of online ad spending differ widely. eMarketer forecasts that online spending will rise 40.2% this year, and pass $2 billion. GroupM, by contrast, has pegged 2012 online spending at just $983 million, about one-third of the $2.78 billion proposed by PIM. Both PwC and ZenithOptimedia anticipate online ad spending growth of 12% to 13% this year, while PIM and GroupM foresee a leap of approximately 39%. Some of these discrepancies likely arise from differences in methodology, but it also seems clear that analysts have divergent views on the short-term strength and potential of the market.

■ Advertisers are rushing to take advantage of an explosion in mobile usage. eMarketer estimates that spending on mobile display and search ads in Brazil will nearly double this year, to $24.6 million. Annual growth rates will remain above 80% in 2013 and 2014. In 2016, mobile ad spending will approach $200 million.

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-11

Brazil

POPULATION

millionsPopulation in Brazil, 2010-2020

Note: population as of July for each yearSource: US Census Bureau, International Data Base, June 27, 2012142195 www.eMarketer.com

2010 2012 2014 2016 2018 2020

200

400

195.8 199.3 202.7 205.8 208.8 211.7

142195

MEDIA

% of populationMedia Penetration in Brazil, 2011

TV viewers (1) 97.3%

Mobile phone owners 81.4%

Internet users (2) 56.5%

Radio listeners (3) 50.3%

Magazine readers (4) 40.2%

Cable/satellite TV viewers (1)34.4%

Newspaper readers (5)33.7%

Mobile internet users (6)10.2%

Note: ages 12-75; (1) viewed in the past week; (2) used in the past 30 days;(3) listened yesterday; (4) read any publication; (5) read weekday andSunday publications; (6) mobile phone owners who use WAP internetSource: TGI Latina, "2011 Brazil Study, Waves 1 & 2," 2012; provided byStarcom MediaVest Group, June 1, 2012141412 www.eMarketer.com

141412

% of totalDemographic Profile of Media Users in Brazil, 2011

GenderMale

Female

Age12-19

20-24

25-34

35-44

45-54

55-64

65-75

Socioeconomic statusAB1

B2

C1

C2

DE

49.0%

51.0%

23.6%

14.6%

25.0%

17.1%

12.1%

5.8%

1.8%

29.6%

24.8%

27.6%

13.4%

4.5%

47.2%

52.8%

15.4%

11.9%

23.5%

19.5%

15.9%

9.5%

4.4%

22.2%

21.0%

29.1%

18.3%

9.5%

47.4%

52.6%

16.9%

10.5%

20.8%

18.5%

16.3%

10.8%

6.2%

18.6%

19.9%

28.9%

20.2%

12.4%

51.0%

49.0%

17.8%

11.3%

21.8%

17.3%

16.7%

10.1%

5.0%

39.1%

24.6%

23.2%

10.3%

2.8%

48.7%

51.3%

16.1%

10.6%

20.9%

19.0%

17.0%

10.7%

5.8%

20.5%

20.0%

27.9%

19.7%

11.9%

39.9%

60.1%

17.4%

10.9%

22.6%

19.9%

15.5%

9.4%

4.4%

31.9%

22.7%

25.7%

14.1%

5.5%

52.4%

47.6%

10.3%

9.3%

23.4%

19.4%

18.3%

12.7%

6.5%

29.4%

21.9%

27.1%

15.3%

6.3%

Note: numbers may not add up to 100% due to rounding; (1) used in the past 30 days; (2) viewed in the past week; (3) listened to AM/FM yesterday; (4) read any publication; (5) read weekday and Sunday publicationsSource: TGI Latina, "2011 Brazil Study, Waves 1 & 2," 2012; provided byStarcom MediaVest Group, June 1, 2012141413 www.eMarketer.com

Internet users (1)

Mobile phone owners

TV viewers (2)

Cable/satellite TV viewers (2)

Radio listeners (3)

Magazine readers (4)

Newspaper readers (5)

141413

INTERNET

millions, % of population and % changeInternet Users and Penetration in Brazil, 2011-2016

2011

79.3

39.0%

9.0%

2012

86.4

42.0%

8.9%

2013

91.5

44.0%

5.9%

2014

96.7

46.0%

5.7%

2015

99.8

47.0%

3.2%

2016

103.0

48.0%

3.2%

Internet users % of population % change

Note: individuals of any age who use the internet from any location via anydevice at least once per monthSource: eMarketer, Feb 2012136990 www.eMarketer.com

136990

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-12

Brazil

Comparative Estimates: Internet Users andPenetration in Brazil, 2010-2012

2010 2011 2012

Internet users (millions)eMarketer, Feb 2012 - 79.3 86.4comScore Inc., May 2012 (1) - 40.5 46.3

BCG, April 2012 - 82.0 -

IBOPE, April 2012 (2) 73.9 79.9 -

F/Nazca Saatchi & Saatchi, Dec 2011 (3) - 78.0 -

Nielsen, Dec 2011 (4) 39.3 44.9 -

Internet user penetration (% of population)eMarketer, Feb 2012 - 39.0% 42.0%TGI Latina, June 2012 (5) - 56.5% -

NIC.BR, May 2012 (6) 48.0% 53.0% -

F/Nazca Saatchi & Saatchi, Aug 2011 (7) 47.0% 51.0% -

ITU, July 2012 - 45.0% -

Note: (1) ages 15+; data is for Jan of each year; (2) data is for Q4; (3) ages12+; data is for Aug; (4) data is for July; includes applications; (5) ages12-75; (6) ages 10+; (7) ages 16+Source: eMarketer, Feb 2012; various, as noted, 2011 & 2012143283 www.eMarketer.com

143283

% of totalDemographic Profile of Internet Users in Brazil, 2011

Note: used in the past month; numbers may not add up to 100% due toroundingSource: TGI Latina, "2011 Brazil Study, Waves 1 & 2," 2012; provided byStarcom MediaVest Group, June 1, 2012141414 www.eMarketer.com

Gender Age

Socioeconomic status

Female51.0%

Male49.0%

12-1923.6%

20-2414.6%

25-3425.0%

35-4417.1%

45-5412.1%

55-645.8%

65-751.8%

AB129.6%

B224.8%

C127.6%

C213.4%

DE4.5%

141414

Fixed Broadband Households and Subscriptions in Brazil, 2010-2016

Households (millions)—% change

—Household penetration

Subscriptions (millions)—% change

2010

12.821.8%

23.0%

13.821.1%

2011

15.017.5%

26.6%

16.116.7%

2012

17.013.0%

29.6%

18.112.4%

2013

18.911.4%

32.5%

20.010.3%

2014

20.89.9%

35.2%

21.68.4%

2015

22.68.9%

37.8%

23.47.9%

2016

24.58.1%

40.3%

25.17.4%

Note: eMarketer benchmarks its Brazil broadband subscription numbersagainst Teleco, for which the last full year measured was 2010; includesconnections with permanent access to the internet via cable modem, DSL,fiber and wireless/satellite technologies; excludes mobileSource: eMarketer, April 2012139109 www.eMarketer.com

139109

Comparative Estimates: Fixed Broadband Householdsand Penetration in Brazil, 2010-2012

2010 2011 2012

Fixed broadband households (millions)eMarketer*, April 2012 12.8 15.0 17.0GroupM, April 2012 12.5 14.3 15.7

Telebrasil, May 2011 17.4 - -

Fixed broadband household penetration (% of households)PwC, June 2012 22.1% 27.6% 34.8%

eMarketer*, April 2012 23.0% 26.6% 29.6%GroupM, April 2012 22.0% 24.0% 26.0%

Ofcom**, Dec 2011 25.0% - -

Note: *includes connections with permanent access to the internet viacable modem, DSL, fiber and wireless/satellite technologies; excludesmobile; **includes business broadband linesSource: eMarketer, April 2012; various, as noted, 2011 & 2012143284 www.eMarketer.com

143284

Social Network Users and Penetration in Brazil,2010-2014

Social network users (millions)—% change

—% of internet users

—% of population

2010

47.316.5%

65.0%

23.5%

2011

56.319.0%

71.0%

27.7%

2012

63.913.5%

74.0%

31.1%

2013

72.313.1%

79.0%

34.8%

2014

79.39.7%

82.0%

37.7%

Note: internet users who use a social network site via any device at leastonce per monthSource: eMarketer, Aug 2012143663 www.eMarketer.com

143663

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-13

Brazil

% of internet users

Comparative Estimates: Social Network UserPenetration in Brazil, 2011 & 2012

Hi-Mídia & M.sense, March2012

eMarketer, Aug 2012

Ipsos, March 2012 (1)

comScore Inc., Dec 2011 (2)

F/Nazca Saatchi & Saatchi,Dec 2011 (3)

InSites Consulting, Sep2011 (4)

UM, Feb 2012

NIC.BR, May 2012

TGI Latina, June 2012

2011

-

71.0%

-

97.4%

93.0%

86.0%

74.3%

69.0%

67.2%

95.0%

2012

74.0%

62.0%

-

-

-

-

-

-

-

Usage

Use

Use via anydevice atleast onceper month

Visited in past3 months

Use

Use

Used in past6 months

Used in past3 months

Used in past30 days

Age

12+

All ages

16-64

15+

12+

15+

16-54

10+

12-75

Note: (1) includes social network sites, forums or blogs; (2) home and worklocations; data is for Oct; (3) data is for Aug; (4) data is for Q2Source: eMarketer, Aug 2012; various, as noted, 2011 & 2012143285 www.eMarketer.com

143285

% of total

Demographic Profile of Social Network Users in Brazil, 2011

Note: respondents are internet users; used virtual community sites in thepast month; numbers may not add up to 100% due to roundingSource: TGI Latina, "2011 Brazil Study, Waves 1 & 2," 2012; provided byStarcom MediaVest Group, June 1, 2012141419 www.eMarketer.com

Gender Age

Socioeconomic status

Female53.9%

Male46.1%

12-1930.6%

20-2417.8%

25-3427.3%

35-4413.7%

45-54 7.3%

55-642.8%

65-750.5%

AB126.2%

B225.0%

C129.6%

C214.6%

DE4.6%

141419

Facebook Users and Penetration in Brazil, 2010-2014

2010 2011 2012 2013 2014

Facebook users (millions) 7.3 28.2 41.5 60.0 69.2—% change 92.4% 288.0% 46.8% 44.7% 15.3%

—% of social network users 15.4% 50.1% 64.9% 83.0% 87.3%

—% of internet users 10.0% 35.6% 48.0% 65.6% 71.6%

—% of population 3.6% 13.9% 20.2% 28.9% 32.9%

Note: internet users who access their Facebook account via any device atleast once per monthSource: eMarketer, Aug 2012143704 www.eMarketer.com

143704

MOBILE

millions, % of population and % changeMobile Connections in Brazil, 2010-2016

2010

202.9

100.9%

16.6%

2011

242.2

119.1%

19.4%

2012

276.1

134.2%

14.0%

2013

295.5

142.1%

7.0%

2014

307.3

146.2%

4.0%

2015

318.0

149.8%

3.5%

2016

327.6

152.7%

3.0%

Mobile connections % of population % change

Note: data is for Dec of each year; includes the total number of mobileconnections, for mobile phones as well as for nonvoice devices, such asinternet access devices (e.g., wireless modem cards, netbooks and mobileWi-Fi hotspots), ereaders, tablets and telematics systemsSource: eMarketer, April 2012139355 www.eMarketer.com

139355

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-14

Brazil

Comparative Estimates: Mobile Connections andPenetration in Brazil, 2010-2012

Mobile connections (millions)BuddeComm, March 2012

eMarketer*, April 2012Anatel*, Jan 2012 (2)

ITU, July 2012

GSM Association, Feb 2012

Mobile connection penetration (% of population)BuddeComm, March 2012

eMarketer*, April 2012Anatel*, Jan 2012

ITU, July 2012

GSM Association, Feb 2012

Pyramid Research, Jan 2012

2010

206.3

202.9202.9

-

-

104.0%

100.9%104.7%

-

-

-

2011

246.4

242.2242.2

242.2

240.1

123.0%

119.1%123.9%

123.2%

123.0%

118.0%

2012

293.0

276.1-

-

-

145.0%

134.2%-

-

-

-

Note: *data is for Dec of each yearSource: eMarketer, April 2012; various, as noted, 2012143286 www.eMarketer.com

143286

millions, % of population and % changeMobile Phone Users in Brazil, 2010-2016

2010

100.6

50.0%

10.0%

2011

109.9

54.0%

9.2%

2012

119.3

58.0%

8.6%

2013

128.9

62.0%

8.1%

2014

137.7

65.5%

6.8%

2015

146.5

69.0%

6.4%

2016

155.5

72.5%

6.1%

Mobile phone users % of population % change

Note: mobile phone users are individuals of any age who own at least onemobile phone and use the phone(s) at least once per monthSource: eMarketer, April 2012139313 www.eMarketer.com

139313

% of total

Demographic Profile of Mobile Phone Owners in Brazil, 2011

Note: numbers may not add up to 100% due to roundingSource: TGI Latina, "2011 Brazil Study, Waves 1 & 2," 2012; provided byStarcom MediaVest Group, June 1, 2012141420 www.eMarketer.com

Gender Age

Socioeconomic status

Female52.8%

Male47.2%

12-1915.4%

20-2411.9%

25-3423.5%

35-4419.5%

45-5415.9%

55-649.5%

65-754.4%

AB122.2%

B221.0%C1

29.1%

C218.3%

DE9.5%

141420

Smartphone Users and Penetration in Brazil,2010-2016

Smartphoneusers (millions)—% change

—% of mobilephone users

—% of population

2010

6.5

78.7%

6.5%

3.3%

2011

20.9

219.3%

19.0%

10.3%

2012

34.6

65.8%

29.0%

16.8%

2013

47.1

36.0%

36.5%

22.6%

2014

63.3

34.6%

46.0%

30.1%

2015

80.6

27.3%

55.0%

38.0%

2016

94.9

17.7%

61.0%

44.2%

Note: smartphone users are individuals of any age who own at least onesmartphone and use the smartphone(s) at least once per monthSource: eMarketer, April 2012139345 www.eMarketer.com

139345

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-15

Brazil

% of total

Demographic Profile of Smartphone Owners in Brazil,2011

Note: numbers may not add up to 100% due to roundingSource: TGI Latina, "2011 Brazil Study, Waves 1 & 2," 2012; provided byStarcom MediaVest Group, June 1, 2012141421 www.eMarketer.com

Gender Age

Socioeconomic status

Male51.8%

Female48.2%

12-1918.2%

20-2414.3%

25-3428.1%

35-4419.6%

45-5412.5%

55-645.5%

65-751.8%

AB135.4%

B221.0%

C126.8%

C29.8%

DE7.0%

141421

Mobile Internet Users and Penetration in Brazil,2010-2016

Mobile internetusers (millions)—% change

—% of mobilephone users

—% of population

2010

8.0

46.7%

8.0%

4.0%

2011

25.3

214.1%

23.0%

12.4%

2012

37.0

46.4%

31.0%

18.0%

2013

49.0

32.5%

38.0%

23.6%

2014

64.7

32.1%

47.0%

30.8%

2015

82.1

26.8%

56.0%

38.6%

2016

96.4

17.5%

62.0%

45.0%

Note: mobile phone users of any age who access the internet from amobile browser or an installed application at least once per month;excludes SMS, MMS and IMSource: eMarketer, April 2012139328 www.eMarketer.com

139328

% of total

Demographic Profile of Mobile Internet Users in Brazil, 2011

Note: mobile phone owners who use WAP internet; numbers may not addup to 100% due to roundingSource: TGI Latina, "2011 Brazil Study, Waves 1 & 2," 2012; provided byStarcom MediaVest Group, June 1, 2012141422 www.eMarketer.com

Gender Age

Socioeconomic status

Male50.9%

Female49.1%

12-1920.7%

20-2417.0%

25-3430.5%

35-4416.8%

45-54 9.2%

55-644.5%

65-751.5%

AB134.7%

B223.2%

C128.2%

C210.0%

DE3.8%

141422

AD SPENDING

20112010 2012 2013 2014 2015 2016

billions and % changeTotal Media Ad Spending in Brazil, 2010-2016

$14.81

11.0%

$16.58

12.0%

$18.46

11.3%

$20.12

9.0%

$22.53

12.0%

$24.78

10.0%

$27.63

11.5%

Total media ad spending % change

Note: includes digital (online and mobile), directories, magazines, newspapers, outdoor, radio and TV; converted at the exchange rate of US$1=BRL1.67Source: eMarketer, Sep 2012

141895 www.eMarketer.com141895

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-16

Brazil

Comparative Estimates: Total Media Ad Spending inBrazil, 2010-2014

2010 2011 2012 2013 2014

Total ad spending (billions)Projeto Inter-Meios*, March 2012 $16.4 $18.2 $20.3 - -

MAGNAGLOBAL, June 2012 - - $19.5 $21.5 -

ZenithOptimedia*, June 2012 $15.5 $16.8 $18.7 $20.3 $22.2

eMarketer*, Sep 2012 $14.8 $16.6 $18.5 $20.1 $22.5PwC, June 2012 $13.8 $14.6 $15.5 $16.5 $20.3

GroupM**, July 2012 $12.3 $13.3 $14.6 $16.0 -

Total ad spending (% change)Projeto Inter-Meios, April 2012 - 10.6% 11.5% - -

eMarketer, Sep 2012 11.0% 12.0% 11.3% 9.0%12.0%ZenithOptimedia, June 2012 18.1% 8.7% 11.0% 8.8% 9.4%

GroupM, July 2012 13.2% 8.2% 10.0% 10.0% -

Carat, March 2012 - 8.1% 10.5% 8.0% -

Warc, Feb 2012 - 7.1% 8.5% - -

PwC, June 2012 - 5.8% 6.2% 6.5% 23.0%

Nielsen, April 2012 - 13.7% - - -

Note: *converted at the exchange rate of US$1=BRL1.67; **converted atthe exchange rate of US$1=BRL2.06Source: eMarketer, Sep 2012; various, as noted, 2012143287 www.eMarketer.com

143287

millionsAd Spending in Brazil, by Media, 2005-2014

TV

Newspapers

Magazines

Online display

Radio

Outdoor

Cinema

Total

2005

$5,907

$1,555

$839

$159

$399

$407

$32

$9,299

2010

$10,468

$1,938

$1,176

$727

$654

$458

$55

$15,476

2011

$11,480

$2,012

$1,217

$870

$676

$513

$52

$16,819

2012

$12,813

$2,195

$1,329

$983

$747

$539

$54

$18,661

2013

$13,909

$2,356

$1,401

$1,189

$795

$596

$58

$20,302

2014

$15,233

$2,523

$1,514

$1,383

$848

$653

$62

$22,216Note: converted at the exchange rate of US$1=BRL1.67; numbers may notadd up to total due to roundingSource: ZenithOptimedia, "Advertising Expenditure Forecasts," June 2012;provided by Starcom MediaVest Group, June 2012142227 www.eMarketer.com

142227

20112010 2012 2013 2014 2015 2016

billions and % changeDigital Ad Spending in Brazil, 2010-2016

$1.12

25.0%

$1.46

30.0%

$2.05

40.2%

$2.45

20.0%

$3.14

28.0%

$3.61

15.0%

$4.13

14.2%

Digital ad spending % change

Note: includes advertising that appears on desktop and laptop computers as well as mobile phones and tablets, and includes all the various formats of advertising on those platforms; excludes SMS, MMS and P2P messaging-based advertising; CAGR (2011-2016)=23.1%; converted at the exchange rate of US$1=BRL1.67Source: eMarketer, Sep 2012141948 www.eMarketer.com

141948

Comparative Estimates: Digital Ad Spending in Brazil,2010-2014

Digital ad spending (millions)

Projeto Inter-Meios,April 2012 (1)

eMarketer,Sep 2012 (1)

PwC, June 2012 (2)

GroupM, July 2012 (3) (4)

BCG, March 2012

Digital ad spending growth (% change)

eMarketer,Sep 2012Projeto Inter-Meios,April 2012GroupM, July 2012 (4)

ZenithOptimedia,June 2012 (4)

PwC, June 2012

2010

$1,455.1

$1,120.0

$864.0

$591.0

$1,700.0

25.0%

-

28.0%

28.0%

-

2011

$2,000.0

$1,460.0

$1,006.0

$707.0

-

30.0%

37.3%

19.6%

19.6%

16.4%

2012

$2,784.4

$2,050.0

$1,128.0

$983.0

-

40.2%

39.1%

38.9%

13.0%

12.1%

2013

-

$3,140.0

$1,274.0

$1,349.0

-

20.0%

-

37.3%

20.9%

12.9%

2014

-

$3,610.0

$1,440.0

-

-

28.0%

-

-

16.3%

13.0%Note: (1) converted at the exchange rate of US$1=BRL1.67; (2) converted atthe exchange rate of US$1=BRL1.6698; (3) converted at the exchange rateof US$1=BRL2.06; (4) excludes mobileSource: eMarketer, Sep 2012; various, as noted, 2012143298 www.eMarketer.com

143298

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-17

Brazil

millions and % changeMobile Ad Spending in Brazil, 2010-2016

$5.4

100.0%

$12.9

140.2%

$24.6

90.4%

$44.4

80.5% $85.2

92.0%$141.4

66.0%

$198.3

40.2%

Mobile ad spending % change

Note: includes display (banners, video and rich media) and search; excludesSMS, MMS and P2P messaging-based advertising; includes ad spending ontablets; converted at the exchange rate of US$1=BRL1.67; CAGR(2011-2016)=72.7%Source: eMarketer, Sep 2012142060 www.eMarketer.com

20112010 2012 2013 2014 2015 2016

142060

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-18

Chile ■ As of Q3 2012, Chile had avoided the worst effects of recent economic turmoil in the region and elsewhere in the world, thanks to healthy levels of investment and sound fiscal policies. According to the EIU, Chilean GDP rose by 6% in 2011 (The IMF is marginally more pessimistic, estimating the 2011 increase at 5.9%). Annual growth rates will drop somewhat, to 5% in 2012 and an average 4.8% between 2013 and 2016, the EIU anticipates. Budget surpluses are likely to continue through 2016. President Sebastián Piñera’s efforts to push through productivity reforms threaten a long-standing status quo and will be opposed by many politicians. Yet his popularity reached a record high in July 2012, following resoundingly positive economic performance in Q2.

■ Around 99% of residents ages 12 and older watched television weekly in 2011, according to TGI Latina’s “2011 Chile Study, Waves 1 & 2.” Radio also remained a powerful media platform, listened to by nearly 73% of the population in the day prior to the study. Penetration of cable and satellite TV were much lower, at 40.3% and 16.5%, respectively. As in other markets, print has suffered as Chilean consumers spend more time with online and mobile options. Females outnumbered males in every media audience except that for newspapers. Newspapers were also the medium with the highest proportion of consumers ages 65 and older (8.3%), and the lowest proportion of users ages 12 to 24 (18.9%).

■ Nearly two-thirds of Chilean residents ages 12 and older had home access to the internet in 2011, TGI reported. Since 2010, females have edged ahead of males in the online population, 52% to 48%. Perhaps surprisingly, the proportion of young people online has not shifted; as in 2010, half of those using the web in 2011 were ages 12 to 34. But the distribution of internet users by income has changed dramatically—and in a direction that should encourage digital advertisers. In 2010, an estimated 67% of those online had a monthly income of less than CLP330,000 ($647). In 2011, that proportion had fallen to 39%.

■ Social networking is a major attraction for younger internet users in Chile. Some 72.6% of those visiting virtual communities in 2011 were ages 12 to 34; less than 12% were ages 45 to 64. Females accounted for 52.8% of social network users last year.

■ Mobile has consolidated its place as the second-ranking media platform by reach. An estimated 88% of Chile’s consumers ages 12 and older owned a mobile phone in 2011, a rise of 5 percentage points compared to 2010,

according to TGI. Smartphone penetration also climbed significantly, from 10.8% to 14.4% of respondents. But mobile internet usage remained startlingly low, engaging just 3.9% of the population. Males accounted for 58.8% of smartphone users and 56.5% of mobile web users.

■ Spending in all measured media in Chile will approach $1.38 billion in 2012, up more than 7% in one year, according to ZenithOptimedia forecasts. TV and newspapers together will claim more than $1 billion of the total. Despite the high penetration of mobile phones, mobile and other digital advertising spending will amount to just $71 million, or less than 5.2% of all ad spending. Online spending is rising more rapidly than investment in any other channel, however, and is predicted to draw level with radio ad spending within two years.

POPULATION

millionsPopulation in Chile, 2010-2020

16.8 17.1 17.4 17.4 17.9 18.2

Note: population as of July for each yearSource: US Census Bureau, International Data Base, June 27, 2012142197 www.eMarketer.com

2010

20

40

2012 2014 2016 2018 2020

142197

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-19

Chile

MEDIA

% of populationMedia Penetration in Chile, 2011

TV viewers (1) 98.7%

Mobile phone owners 87.7%

Radio listeners (2) 72.7%

Internet users (3) 65.6%

Newspaper readers (4) 47.8%

Cable TV viewers 40.3%

Magazine readers (5) 34.7%

Satellite TV viewers16.5%

Smartphone owners14.4%

Mobile internet users (6)3.9%

Note: ages 12+; (1) viewed in the past week; (2) listened to AM/FMyesterday; (3) home access; (4) read weekday and Sunday publications; (5)read any publication; (6) access via feature phone, PDA, Smartphone,iPhone or BlackBerrySource: TGI Latina, "2011 Chile Study, Waves 1 & 2," 2012; provided byStarcom MediaVest Group, June 1, 2012141437 www.eMarketer.com

141437

% of totalDemographic Profile of Media Users in Chile, 2011

GenderMale

Female

Age12-17

18-24

25-34

35-44

45-54

55-64

65+

Monthly income (CLP)<164K

165K-330K

330K-440K

440K-825K

825K-1,100K

1,100K+

48.0%

52.0%

12.8%

16.5%

20.9%

19.1%

17.5%

8.6%

4.6%

2.4%

36.6%

16.6%

26.0%

9.3%

9.1%

48.7%

51.3%

10.8%

15.7%

21.5%

18.5%

17.2%

10.2%

6.2%

5.8%

43.1%

16.3%

21.3%

6.8%

6.8%

47.8%

52.2%

11.3%

14.9%

19.3%

18.1%

17.3%

11.0%

8.1%

7.3%

44.9%

15.7%

19.9%

6.2%

6.0%

48.0%

52.0%

9.5%

13.4%

19.8%

19.9%

18.4%

11.1%

7.8%

6.2%

44.5%

15.4%

21.0%

6.4%

6.5%

43.4%

56.6%

12.1%

13.9%

22.2%

20.0%

17.1%

9.3%

5.5%

4.4%

40.5%

14.2%

23.5%

9.0%

8.4%

50.6%

49.4%

7.5%

11.4%

19.5%

19.0%

21.0%

13.5%

8.3%

4.8%

40.4%

17.4%

21.7%

8.3%

7.4%

Note: (1) home access; (2) viewed in the past week; (3) listened to AM/FMyesterday; (4) read any publication; (5) read weekday and SundaypublicationsSource: TGI Latina, "2011 Chile Study, Waves 1 & 2," 2012; provided byStarcom MediaVest Group, June 1, 2012141438 www.eMarketer.com

Internet users (1)

Mobile phone owners

TV viewers (2)

Radio listeners (3)

Magazine readers (4)

Newspaper readers (5)

141438

INTERNET

% of totalDemographic Profile of Internet Users in Chile, 2011

Note: home internet accessSource: TGI Latina, "2011 Chile Study, Waves 1 & 2," 2012; provided byStarcom MediaVest Group, June 1, 2012141439 www.eMarketer.com

Gender Age

Monthly income (CLP)

Female52.0%

Male48.0%

12-1712.8%

18-2416.5%

25-3420.9%

35-4419.1%

45-5417.5%

55-64 8.6%

65+4.6%

<164K2.4%

165K-330K36.6%

330K-440K16.6%

440K-825K26.0%

825K-1,100K9.3%

1,100K+9.1%

141439

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-20

Chile

% of total

Demographic Profile of Social Network Users in Chile,2011

Note: used a virtual communitySource: TGI Latina, "2011 Chile Study, Waves 1 & 2," 2012; provided byStarcom MediaVest Group, June 1, 2012141440 www.eMarketer.com

Gender Age

Monthly income (CLP)

Female52.8%

Male47.2%

12-1720.6%

18-2424.6%25-34

27.4%

35-4415.0%

45-54 8.2%

55-643.5%

65+0.7%

<164K5.2%

165K-330K36.3%

330K-440K16.6%

440K-825K23.9%

825K-1,100K8.9%

1,100K+9.1%

141440

MOBILE

% of total

Demographic Profile of Mobile Phone Owners in Chile, 2011

Note: numbers may not add up to 100% due to roundingSource: TGI Latina, "2011 Chile Study, Waves 1 & 2," 2012; provided byStarcom MediaVest Group, June 1, 2012141441 www.eMarketer.com

Gender Age

Monthly income (CLP)

Female51.3%

Male48.7%

12-1710.8%

18-2415.7%

25-3421.5%35-44

18.5%

45-5417.2%

55-6410.2%

65+6.2%

<164K5.8%

165K-330K43.1%

330K-440K16.3%

440K-825K21.3%

825K-1,100K6.8%

1,100K+6.6%

141441

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-21

Chile

% of total

Demographic Profile of Smartphone Owners in Chile,2011

Note: numbers may not add up to 100% due to roundingSource: TGI Latina, "2011 Chile Study, Waves 1 & 2," 2012; provided byStarcom MediaVest Group, June 1, 2012141442 www.eMarketer.com

Gender Age

Monthly income (CLP)

Male58.8%

Female41.2%

12-1712.1%

18-2416.6%

25-3428.7%

35-4424.0%

45-5411.3%

55-644.8%

65+2.5%

<164K2.9%

165K-330K30.9%

330K-440K12.9%

440K-825K22.7%

825K-1,100K14.0%

1,100K+16.7%

141442

% of total

Demographic Profile of Mobile Internet Users in Chile,2011

Note: access via feature phone, PDA, smartphone, iPhone or BlackBerry;numbers may not add up to 100% due to roundingSource: TGI Latina, "2011 Chile Study, Waves 1 & 2," 2012; provided byStarcom MediaVest Group, June 1, 2012141443 www.eMarketer.com

Gender Age

Monthly income (CLP)

Male56.5%

Female43.5%

12-179.2%

18-2418.7%

25-3450.1%

35-4414.1%

45-544.9%

55-642.1%

65+0.8%

<164K3.1%

165K-330K25.3%

330K-440K10.6%

440K-825K26.3%

825K-1,100K13.4%

1,100K+21.2%

141443

AD SPENDING

millionsAd Spending in Chile, by Media, 2005-2014

TV

Newspapers

Outdoor

Radio

Internet

Magazines

Cinema

Total

2005

$418

$250

$72

$70

$9

$27

$3

$848

2010

$614

$318

$88

$80

$49

$25

$4

$1,179

2011

$663

$350

$97

$86

$59

$27

$5

$1,287

2012

$703

$375

$105

$91

$71

$28

$5

$1,378

2013

$738

$401

$112

$96

$83

$29

$6

$1,465

2014

$770

$425

$121

$99

$99

$31

$6

$1,552Note: converted at the exchange rate of US$1=CLP483.67; numbers maynot add up to total due to roundingSource: ZenithOptimedia, "Advertising Expenditure Forecasts," June 2012;provided by Starcom MediaVest Group, June 2012142229 www.eMarketer.com

142229

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-22

Colombia ■ According to the EIU, Colombia’s GDP registered 5.9% growth in 2011—exceeding earlier forecasts—but prospects for 2012 are somewhat dimmer, at less than 4.5%. The rate of growth is expected to pick up beginning in 2013. The strong economy, founded chiefly on the exploitation of large oil and coal reserves, has boosted the popularity of the current government, headed by President Juan Manuel Santos. Fiscal reforms passed in 2011 should gradually trim the federal deficit between now and 2016. But most of the country‘s residents are poor by the standards of advanced economies. Colombia’s population is rising by around 1 million each year, and will pass 45 million in 2012.

■ Colombia’s advertising industry will continue to benefit from an encouraging financial environment. According to ZenithOptimedia, total media ad spending will outpace the country’s economy, rising 5.5% in 2012, and passing $1.44 billion. Nearly half (49%) of that will go to TV. Spending on newspaper ads will be virtually stagnant, at $259 million. This reflects a dwindling readership; fewer than one-third of TGI respondents said they had read a newspaper in the week before polling. The web, which drew $60 million in advertising in 2011, is expected to post a 53% gain, and attract $92 million this year.

■ Nearly two-thirds of Colombia’s residents ages 12 and older are now online. TGI Latina’s “2011 Colombia Study” reported that 63% used the internet at least monthly in 2011, compared to 57% in 2010. Increasing engagement with the web has not yet led to more usage among older residents, however. The proportion of internet users older than age 54 actually dropped in 2011, according to TGI, from 5% to 4.7%. The social networking population is also overwhelmingly young; nearly 73% of those using social sites in 2011 were ages 12 to 34. But social networking appears equally attractive to both sexes; social media users were divided almost precisely between male and female in 2011.

■ Mobile remains a headline media story in Colombia. Penetration of mobile phones among residents ages 12 and older reached a landmark 90% in 2011, and—as in 2010—surpassed that of any other media channel. The audience for free-to-air TV rose by 3 percentage points, to 88%, but penetration of paid-for cable and satellite television fell marginally, to 70% from 73% in 2010.

■ Females outnumbered males in the mobile population in 2011, by 52% to 48%. Mobile phone ownership was distributed quite evenly across young and old age groups, with the exception of seniors ages 65 and older, who accounted for just 3.7% of mobile users. Far more striking

was the tiny proportion of well-to-do residents with mobile phones; in 2011, the top two income brackets accounted for less than 12% of Colombia’s mobile audience.

■ The estimated penetration of smartphones in Colombia more than doubled between 2010 and 2011, from 5.6% to 12%. In this group, males were the stronger presence, accounting for nearly 55% of smartphone owners. Predictably, too, affluent consumers were more numerous here than in the wider mobile population. Some 52.5% of people with smartphones in 2011 were middle or high earners, according to TGI.

■ Colombia’s mobile web audience also displayed a strong bias toward younger, male and more affluent users. Around 71% of those in Colombia who went online via mobile in 2011 were ages 12 to 34. Over 56% were male, and a similar percentage came from middle- or high-income households.

POPULATION

millionsPopulation in Colombia, 2010-2020

44.2 45.2 46.2 47.2 48.2 49.1

Note: population as of July for each yearSource: US Census Bureau, International Data Base, June 27, 2012142200 www.eMarketer.com

2010

50

100

2012 2014 2016 2018 2020

142200

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-23

Colombia

MEDIA

% of populationMedia Penetration in Colombia, 2011

Mobile phone owners 90%

TV viewers (1) 85%

Pay-TV subscribers (2) 70%

Radio listeners (1) 68%

Internet users (3) 63%

Social media users (4) 51%

Magazine readers (5) 40%

Newspaper readers (6)32%

Smartphone owners12%

Note: ages 12+; (1) used yesterday; (2) subscribe to cable or satellite; (3)used in the past 30 days; (4) visited a blog, virtual community (Facebook,hi5, Myspace), shared photo or used IM in the past 30 days; (5) read anypublication in the past 6 months; (6) read any publication in the past weekSource: TGI Latina, "2011 Colombia Study," 2012; provided by StarcomMediaVest Group, June 1, 2012141363 www.eMarketer.com

141363

% of totalDemographic Profile of Media Users in Colombia, 2011

GenderMale

Female

Age12-17

18-24

25-34

35-44

45-54

55-64

65+

Socioeconomic statusA

B

C

D

E

52.5%

47.5%

20.5%

21.8%

27.6%

14.8%

10.6%

3.9%

0.8%

6.4%

9.3%

20.0%

35.7%

28.7%

48.0%

52.0%

12.3%

16.5%

22.8%

19.2%

16.5%

9.0%

3.7%

4.3%

7.1%

14.9%

38.0%

35.7%

47.0%

53.0%

13.0%

15.7%

21.6%

18.6%

17.0%

9.6%

4.6%

3.8%

6.6%

14.0%

37.9%

37.7%

50.4%

49.6%

13.4%

16.6%

22.6%

17.7%

16.0%

9.7%

4.0%

3.7%

7.4%

16.1%

38.8%

33.9%

47.3%

52.7%

14.5%

16.5%

20.9%

17.8%

16.6%

9.4%

4.5%

4.3%

6.6%

14.4%

36.2%

38.6%

42.1%

57.9%

13.4%

16.1%

24.8%

19.0%

15.3%

8.0%

3.4%

6.8%

9.3%

17.6%

35.5%

30.9%

53.2%

46.8%

9.5%

13.9%

22.4%

21.3%

18.4%

10.7%

3.8%

7.2%

10.3%

17.7%

34.7%

30.0%

Note: numbers may not add up to 100% due to rounding; (1) used in thepast 30 days; (2) used yesterday; (3) subscribe to cable or satellite; (4) readany publication in the past 6 months; (5) read any publication in the pastweekSource: TGI Latina, "2011 Colombia Study," 2012; provided by StarcomMediaVest Group, June 1, 2012141364 www.eMarketer.com

Internet users (1)

Mobile phone owners

TV viewers (2)

Pay-TV subscribers (3)

Radio listeners (2)

Magazine readers (4)

Newspaper readers (5)

141364

INTERNET

Gender Age

Socioeconomic status

% of total

Demographic Pro�le of Internet Users in Colombia,2011

Male52.5%

Female47.5%

12-1720.5%

18-2421.8%

25-3427.6%

35-4414.8%

45-5410.6%

55-643.9%

65+0.8%

A6.4%

B9.3%

C20.0%

D35.7%

E28.7%

Note: used in the past 30 days; numbers may not add up to 100% due toroundingSource: TGI Latina, "2011 Colombia Study," 2012; provided by StarcomMediaVest Group, June 1, 2012141372 www.eMarketer.com

141372

The Global Media Intelligence Report: Latin America Copyright ©2012 eMarketer, Inc. All rights reserved. LA-24

Colombia

% of total

Demographic Profile of Social Media Users in Colombia, 2011

Note: visited a blog or virtual community (Facebook, hi5, Myspace), sharedphotos or used IM in the past 30 days; numbers may not add up to 100%due to roundingSource: TGI Latina, "2011 Colombia Study," 2012; provided by StarcomMediaVest Group, June 1, 2012141373 www.eMarketer.com

Gender Age

Socioeconomic status

Male50.2%

Female49.8%

12-1721.4%

18-2423.2%25-34

28.2%

35-4415.0%

45-54 8.2%

55-643.3%

65+0.6%

A6.2%

B9.3%

C19.1%

D34.4%

E30.9%

141373

MOBILE

% of total

Demographic Pro�le of Mobile Phone Ownersin Colombia, 2011

Note: numbers may not add up to 100% due to roundingSource: TGI Latina, "2011 Colombia Study," 2012; provided by StarcomMediaVest Group, June 1, 2012141374 www.eMarketer.com

Gender Age

Socioeconomic status

Female52.0%

Male48.0%

12-1712.3%

18-2416.5%

25-3422.8%