l-3 analyzing aggregate demand - bi.go.id · increased uncertainty about future income higher...

TRANSCRIPT

L-3

Analyzing Aggregate Demand

PresenterNatan Epstein

Deputy Director, STI

This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF courses. Any reuse requires the permission of the IMF.

IMF − Singapore Regional Training InstituteOT 18.52 Macroeconomic Diagnostics February 26 – March 2, 2018

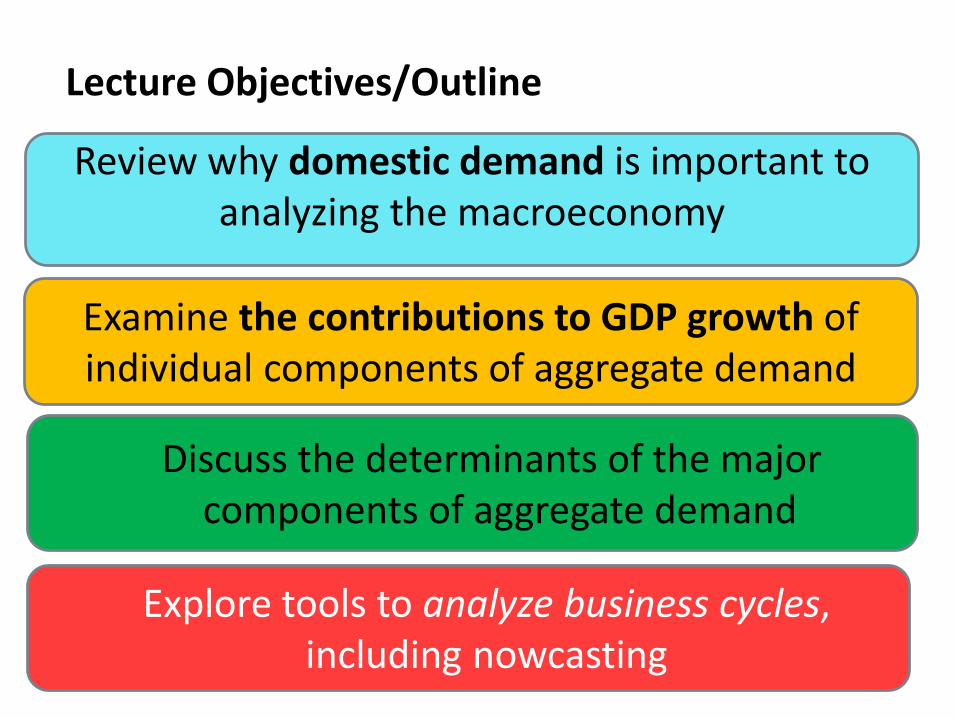

Lecture Objectives/Outline

Review why domestic demand is important to analyzing the macroeconomy

Examine the contributions to GDP growth of individual components of aggregate demand

Discuss the determinants of the major components of aggregate demand

Explore tools to analyze business cycles, including nowcasting

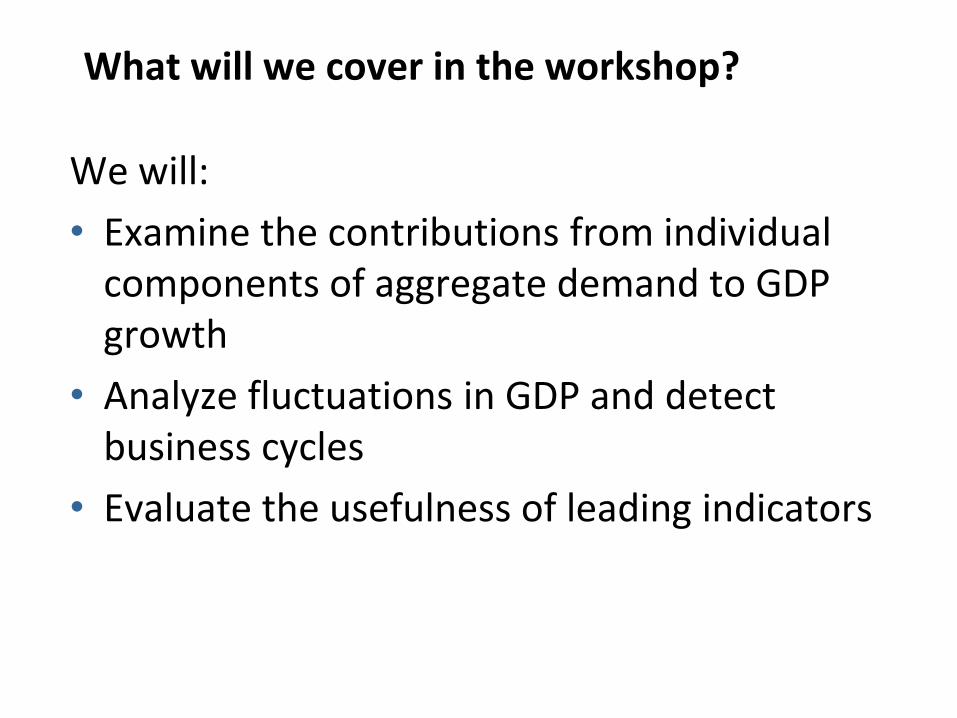

What will we cover in the workshop?

We will:

• Examine the contributions from individual components of aggregate demand to GDP growth

• Analyze fluctuations in GDP and detect business cycles

• Evaluate the usefulness of leading indicators

Why do we analyze domestic demand?

• Fluctuations in domestic demand (DD) play an important role in economic cycles

• DD impacts inflation, fiscal, and monetary policy

And is affected by these factors

• Domestic demand relative to national income determines the external current account and the exchange rate

• Consumption/saving and investment have important implications for current and future economic welfare and macro stability

Investment -> Capital accumulation -> future production capacity

Aggregate Demand and Aggregate Supply

• AD illustrates the relationship between prices and output demanded

• Many factors can cause demand to shift such as increase in money supply, investment, government consumption or decrease in taxes

• When aggregate demand increases there is a movement along the supply curve.

P

Real GDP

AS

AD1

AD2

P2

P1

Y1 Y2

I. Short-term analysis of AD

The expenditure approach to GDP

GDP = Final Consumption (Cp + Cg) + Investment (Ip+ Ig+ DS)

+ exports (X) – imports (M) of goods & services

= Domestic absorption (A) + Net Exports (X-M)

• Note that domestic absorption includes both public and private consumption (Cp and Cg) and investment (Ip and Ig), and the change in inventory investment (DS).

• Understanding the behavior of these key components is important to understanding the behavior of the economy.

What are the sources of growth?

( ( ))

( )

( ) ( )

( )

GDP C I X M

GDP GDP

C I X M

GDP GDP GDP

C C I I X M X M

C GDP I GDP X M GDP

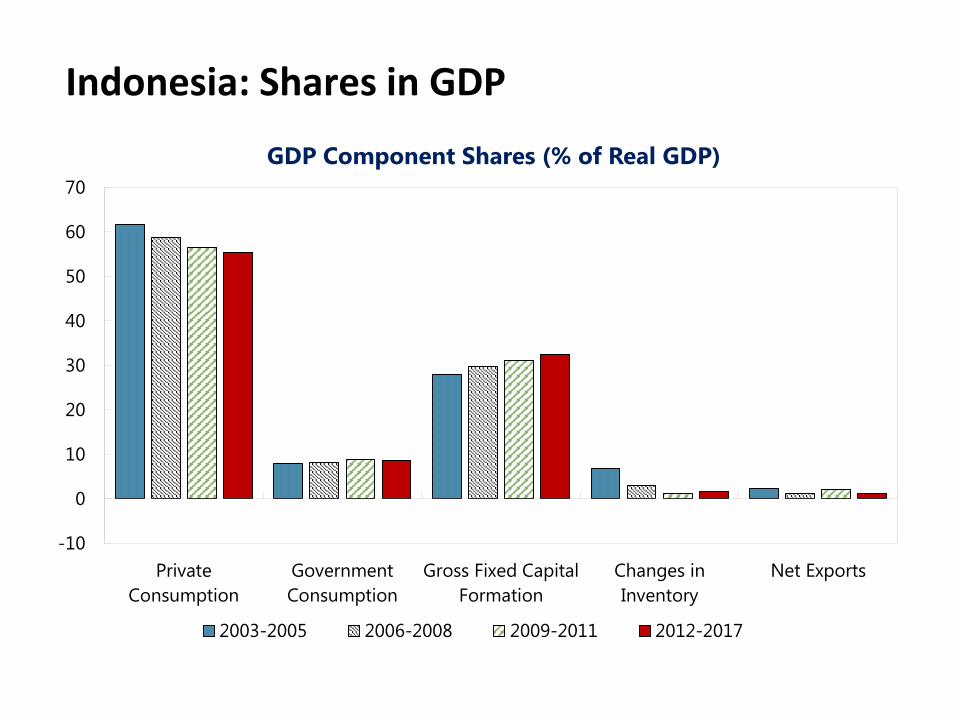

Indonesia: Shares in GDP

-10

0

10

20

30

40

50

60

70

Private

Consumption

Government

Consumption

Gross Fixed Capital

Formation

Changes in

Inventory

Net Exports

GDP Component Shares (% of Real GDP)

2003-2005 2006-2008 2009-2011 2012-2017

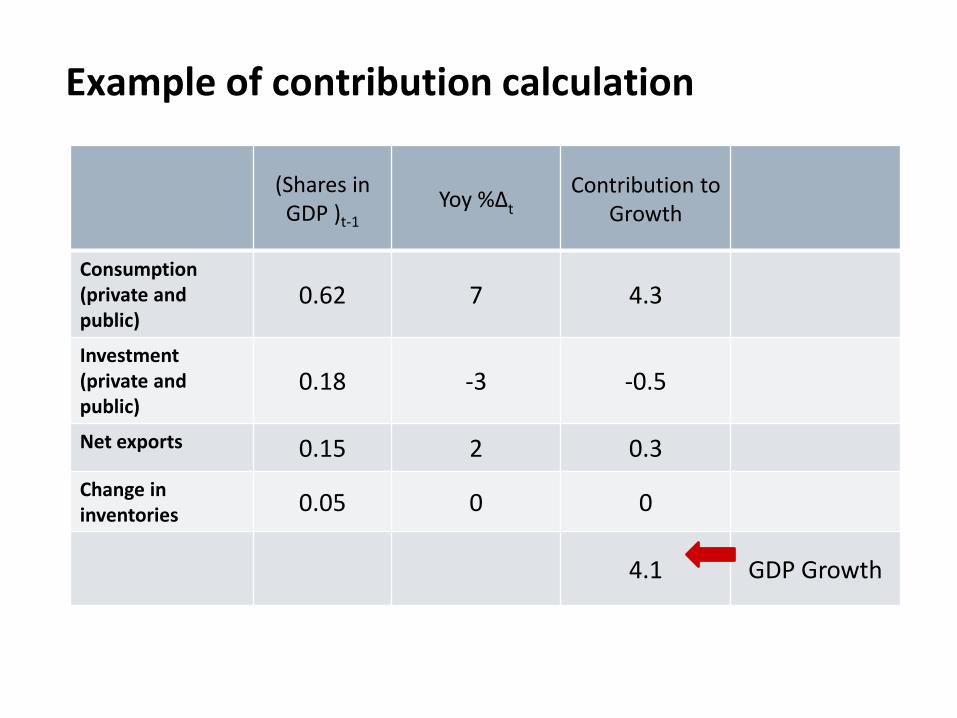

Example of contribution calculation

(Shares in GDP )t-1

Yoy %∆t

Contribution to Growth

Consumption (private and public)

0.62 7 4.3

Investment (private and public)

0.18 -3 -0.5

Net exports 0.15 2 0.3

Change in inventories 0.05 0 0

4.1 GDP Growth

-8

-6

-4

-2

0

2

4

6

8

10

12

14

Q1-2008 Q1-2010 Q1-2012 Q1-2014 Q1-2016

Indonesia: Sources of Growth (Contributions to Real GDP Growth YoY)

Private Consumption Public Consumption Public Investment

Private Investment Change In Inventory Net Exports

Statistical Discrepencies Real GDP Growth %Δ Year-over-Year

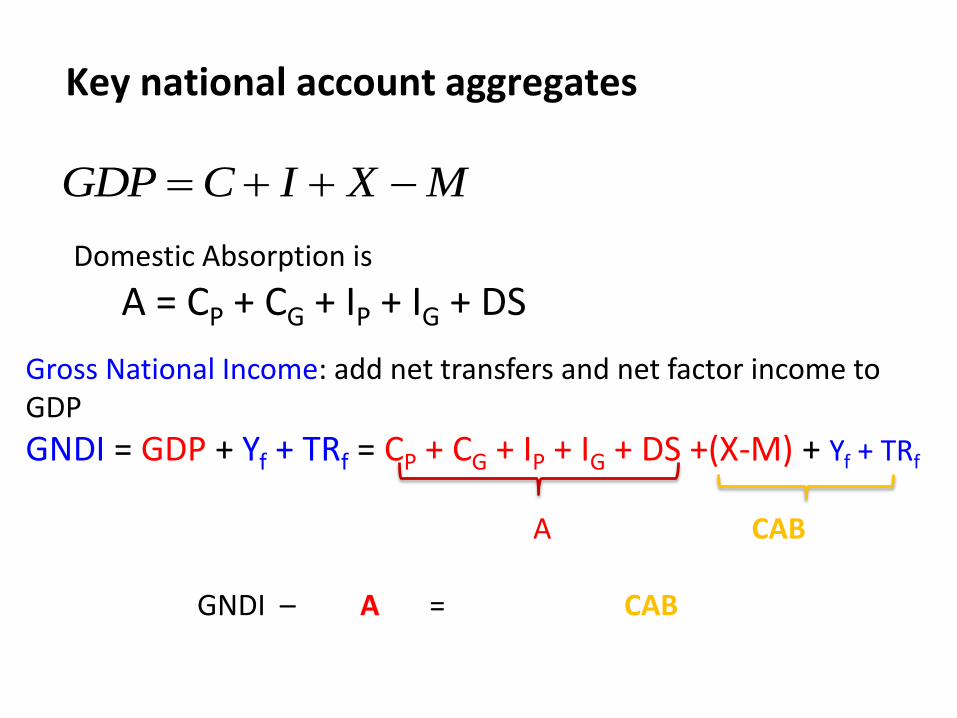

A = CP + CG + IP + IG + DS

Gross National Income: add net transfers and net factor income to GDP

GNDI = GDP + Yf + TRf = CP + CG + IP + IG + DS +(X-M) + Yf + TRf

A CAB

GNDI – A = CAB

Key national account aggregates

GDP C I X M

Domestic Absorption is

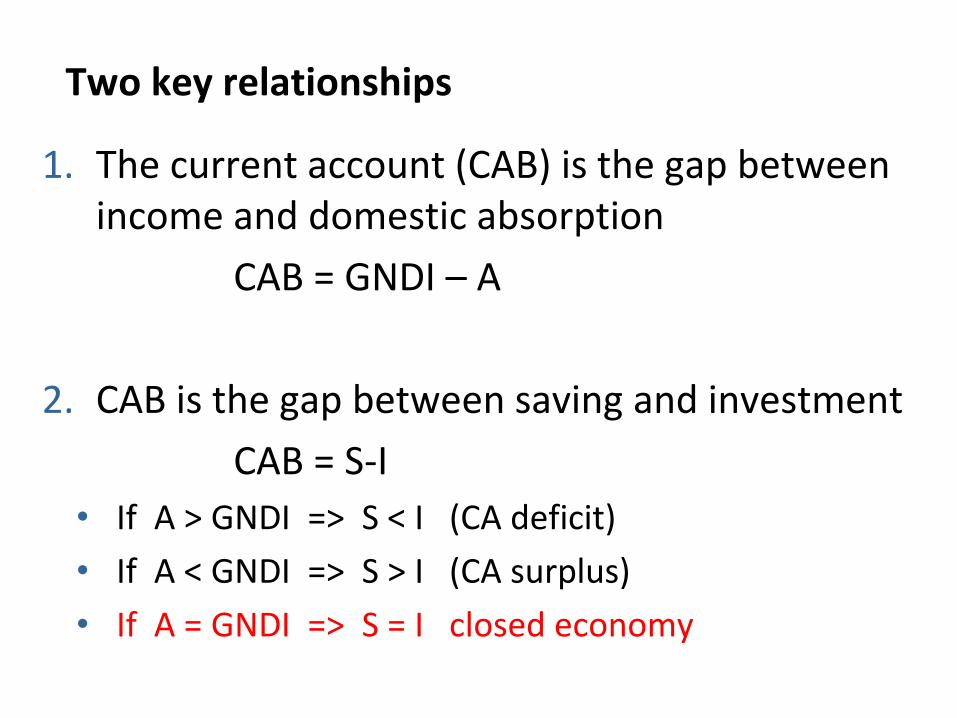

Two key relationships

1. The current account (CAB) is the gap between income and domestic absorption

CAB = GNDI – A

2. CAB is the gap between saving and investment

CAB = S-I

• If A > GNDI => S < I (CA deficit)

• If A < GNDI => S > I (CA surplus)

• If A = GNDI => S = I closed economy

II. Analysis of the key components:

Consumption

Why analyze spending components?

• By far, C and I are the most important components of GDP

• The behavior of C and I have significant implications for

current and future economic growth

• Fluctuations in domestic demand (household consumption,

government consumption, private investment and public

investment) play important role in economic cycles

• The behavior of domestic demand (domestic absorption)

relative to national income determines the external current

account, which is important for assessing external

sustainability.

Durables• Examples: motor vehicles, furniture and household equipment• Tend to be highly cyclical

Non-durables• Examples: food, clothing and shoes, fuel• Not very cyclical because they are necessities for the most part; these

purchases generally track population growth

Services• Examples: housing services, transportation• May include imputed items• Not very cyclical because they are necessities for the most part; these

purchases generally track population growth• Fast growing countries relatively ask for more services

What are the key components of consumption?

Consumers distribute consumption throughout their lives so as to maximize lifetime utility, taking account of:

• Current disposable incomeHigher current income higher current consumption, higher saving

• Expected future incomeHigher future income higher current consumption, lower saving

• UncertaintyIncreased uncertainty about future income higher saving (in the face of risk aversion and imperfect financial markets)

• WealthHigher wealth higher current consumption, lower saving

• Expected real interest rateHigher real interest rate saving could go up or down

Analyzing Consumption

Other determinants of consumption

Government borrowing may constrain private consumption through Ricardian equivalence:

• If the government has a large debt, consumers would expect an increase in taxes down the road even if they reduce taxes now

• Consumers would then consume less today and save more to smooth consumption over their lifecycle (significant offset of private and public saving).

III. Analysis of the key components:

Investment

What are the key components of investment?

Private fixed investment

• Nonresidential structures, e.g., commercial buildings, industrial plants, farm buildings

• Producers’ durable equipment, e.g., ICT equipment, transportation equipment

• Residential structures, i.e., housing

Inventory investment

• Change in inventories from the previous period

• Not level of inventories

Government investment

Private investment (IP) includes spending by businesses and households on fixed assets.

IP is much more volatile than consumption

• substantially contributes to fluctuations in GDP.

Driving factors:

• Rate of return

• Expected future income

• Cost of finance

• Access to financing

• Uncertainty

Analyzing Private Investment

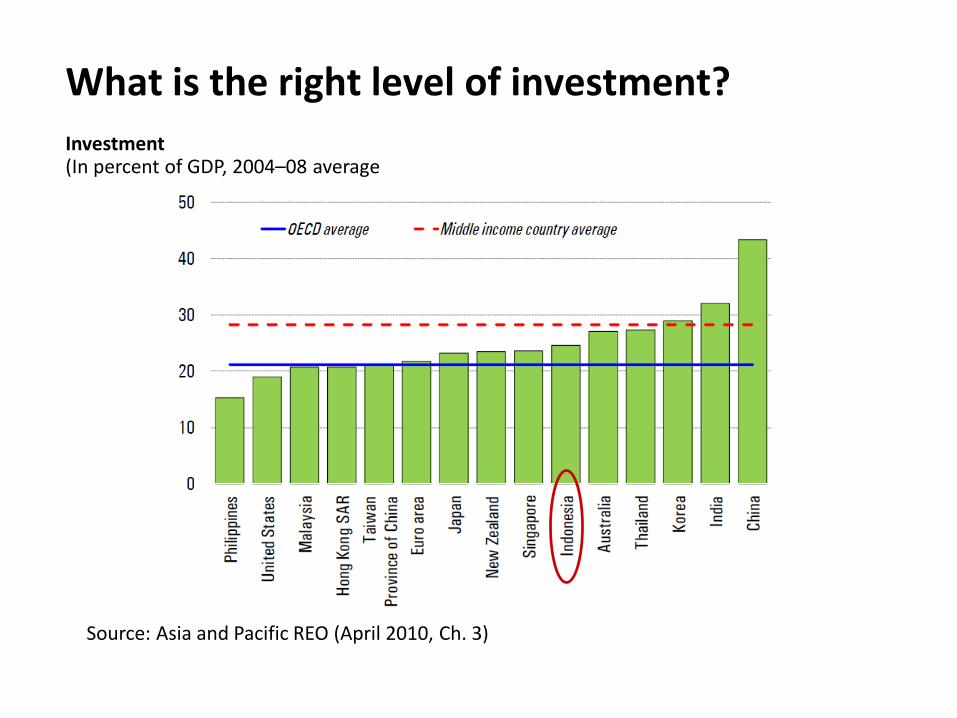

What is the right level of investment?

Investment(In percent of GDP, 2004–08 average

Source: Asia and Pacific REO (April 2010, Ch. 3)

III. Business cycles, indicators, and nowcasting

What is a business cycle?

Business cycle:

• Repeated sequence of economic expansion followed by temporary decline, then recovery.

• Temporary deviation from the economy’s normal growth path. Part of the output losses and gains that occur during a

business cycle may become permanent.

• No two business cycles are alike but they often have common features These features can be very helpful in understanding

and diagnosing the state of the economy.

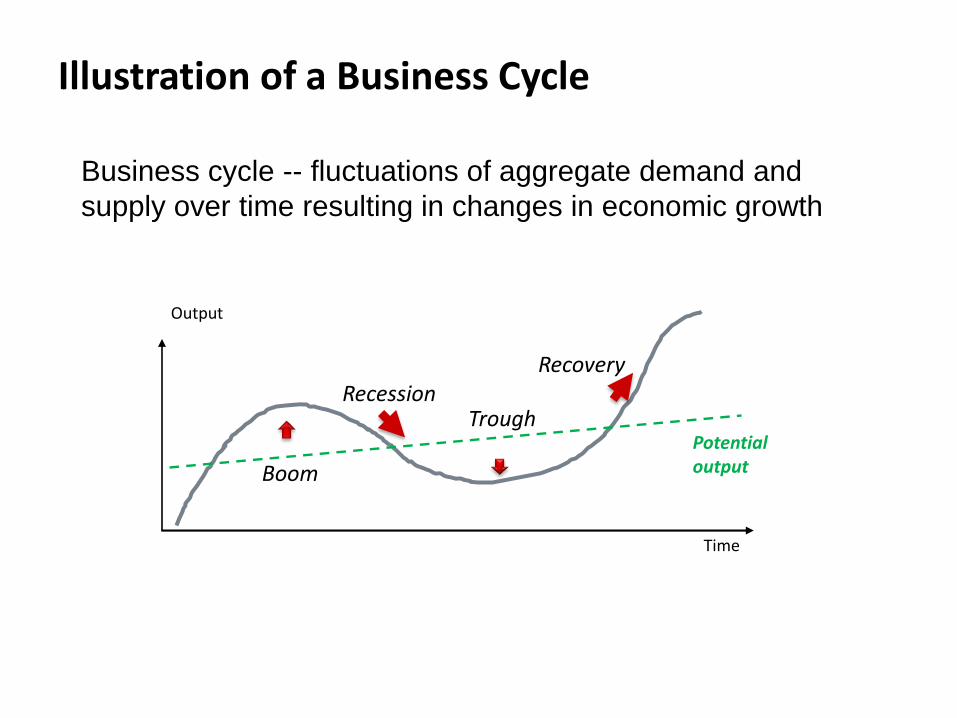

Business cycle -- fluctuations of aggregate demand and

supply over time resulting in changes in economic growth

Illustration of a Business Cycle

Output

Time

Boom

TroughRecession

Recovery

Potential output

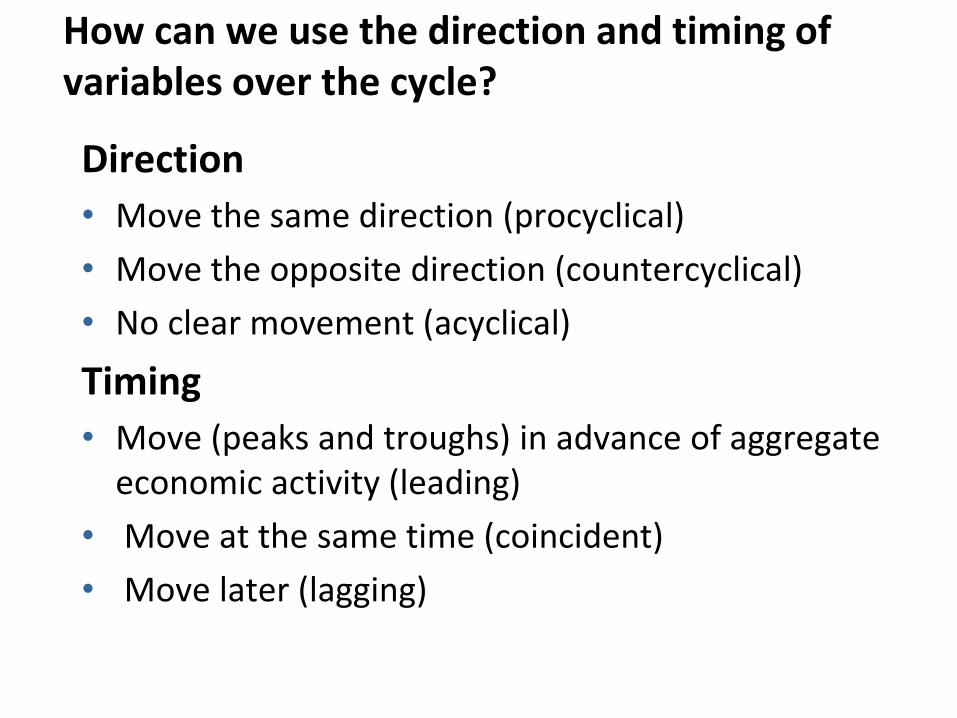

How can we use the direction and timing of variables over the cycle?

Direction

• Move the same direction (procyclical)

• Move the opposite direction (countercyclical)

• No clear movement (acyclical)

Timing

• Move (peaks and troughs) in advance of aggregate economic activity (leading)

• Move at the same time (coincident)

• Move later (lagging)

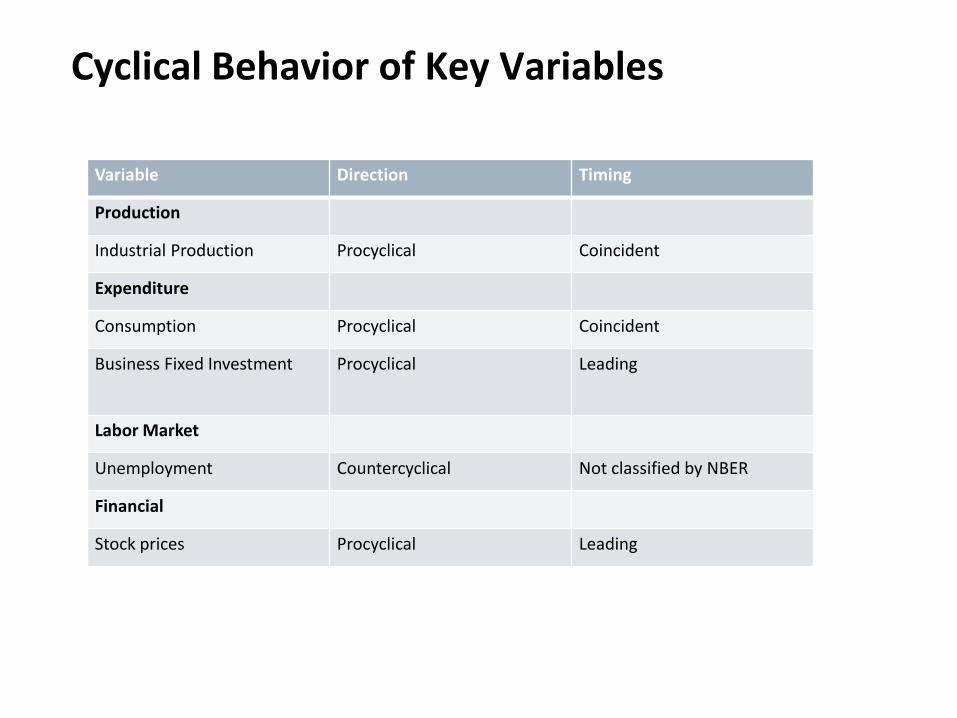

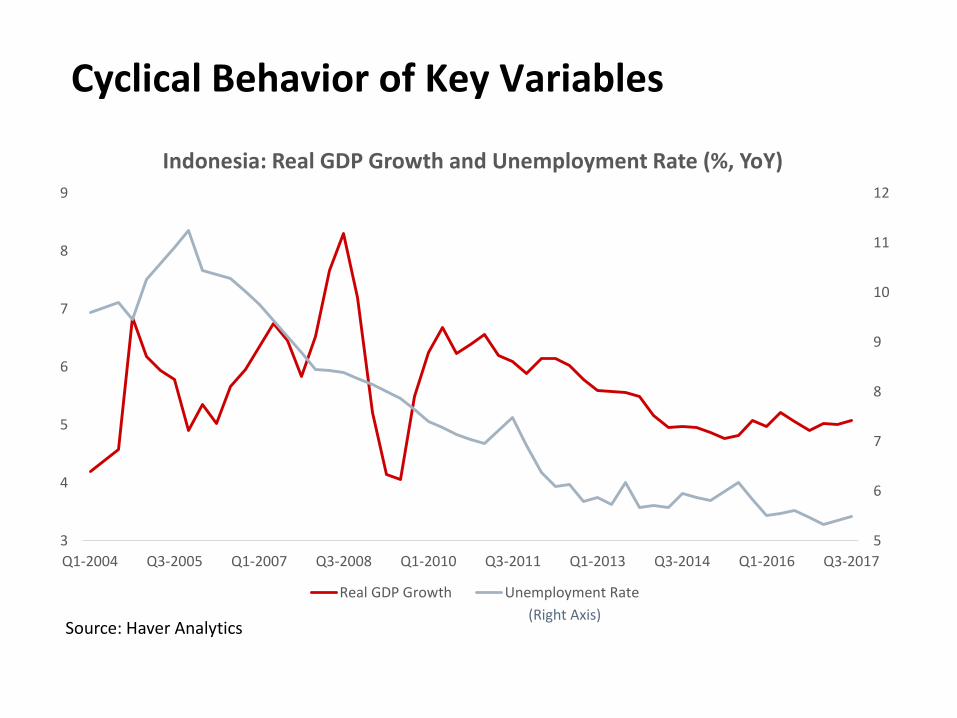

Cyclical Behavior of Key Variables

Variable Direction Timing

Production

Industrial Production Procyclical Coincident

Expenditure

Consumption Procyclical Coincident

Business Fixed Investment Procyclical Leading

Labor Market

Unemployment Countercyclical Not classified by NBER

Financial

Stock prices Procyclical Leading

Cyclical Behavior of Key Variables

5

6

7

8

9

10

11

12

3

4

5

6

7

8

9

Q1-2004 Q3-2005 Q1-2007 Q3-2008 Q1-2010 Q3-2011 Q1-2013 Q3-2014 Q1-2016 Q3-2017

Indonesia: Real GDP Growth and Unemployment Rate (%, YoY)

Real GDP Growth Unemployment Rate

Source: Haver Analytics(Right Axis)

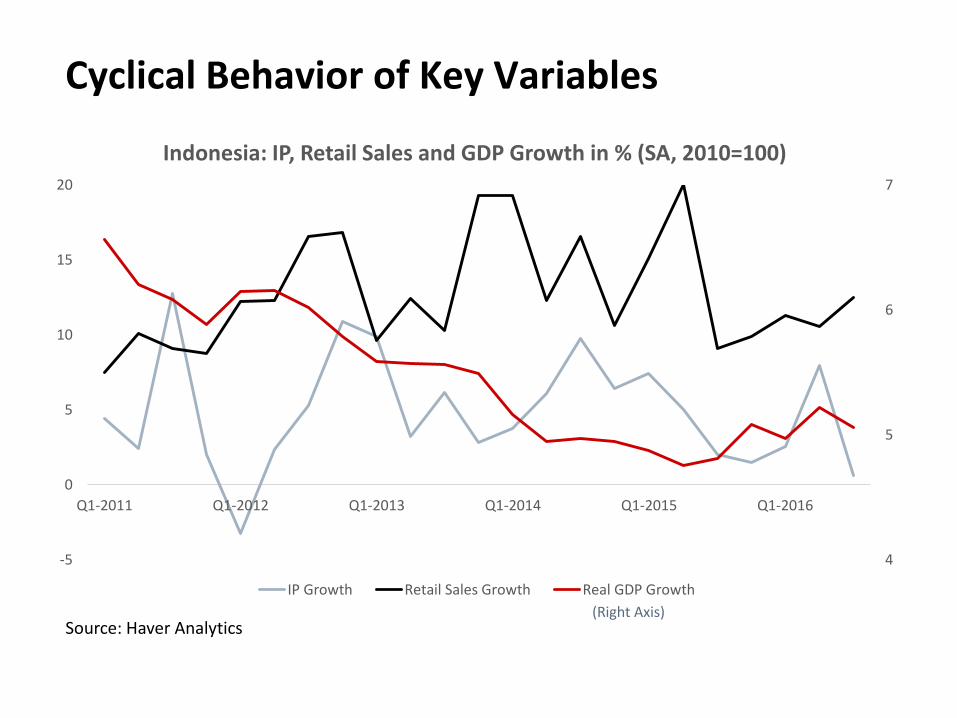

Cyclical Behavior of Key Variables

Source: Haver Analytics

4

5

6

7

-5

0

5

10

15

20

Q1-2011 Q1-2012 Q1-2013 Q1-2014 Q1-2015 Q1-2016

Indonesia: IP, Retail Sales and GDP Growth in % (SA, 2010=100)

IP Growth Retail Sales Growth Real GDP Growth

(Right Axis)

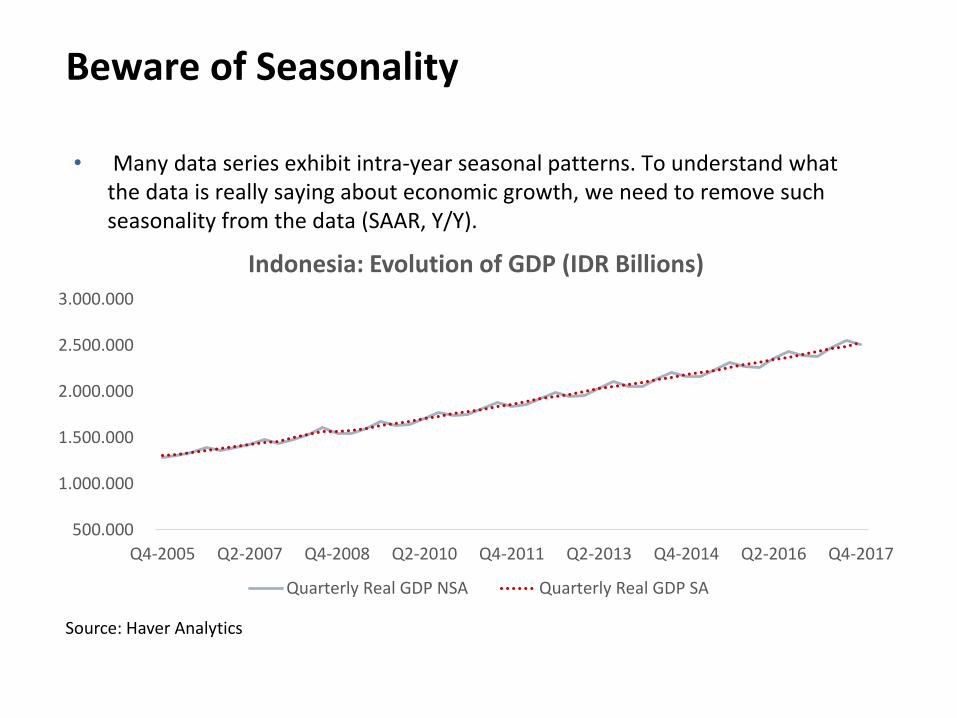

Beware of Seasonality

• Many data series exhibit intra-year seasonal patterns. To understand what the data is really saying about economic growth, we need to remove such seasonality from the data (SAAR, Y/Y).

Source: Haver Analytics

500.000

1.000.000

1.500.000

2.000.000

2.500.000

3.000.000

Q4-2005 Q2-2007 Q4-2008 Q2-2010 Q4-2011 Q2-2013 Q4-2014 Q2-2016 Q4-2017

Indonesia: Evolution of GDP (IDR Billions)

Quarterly Real GDP NSA Quarterly Real GDP SA

Business Cycle Indicators and Nowcasting

• Some of the economic indicators which co-move with GDP happen to be available at higher frequency than GDP—IP, retail sales, electricity…

• High frequency indicators can be used to now-cast GDP (Stock and Watson (1991)).

• The Federal Reserve Bank of New York (FRBNY) updates a nowcast of GDP growth by weighing in news releases relative to employment, international trade, retail and consumption, etc.

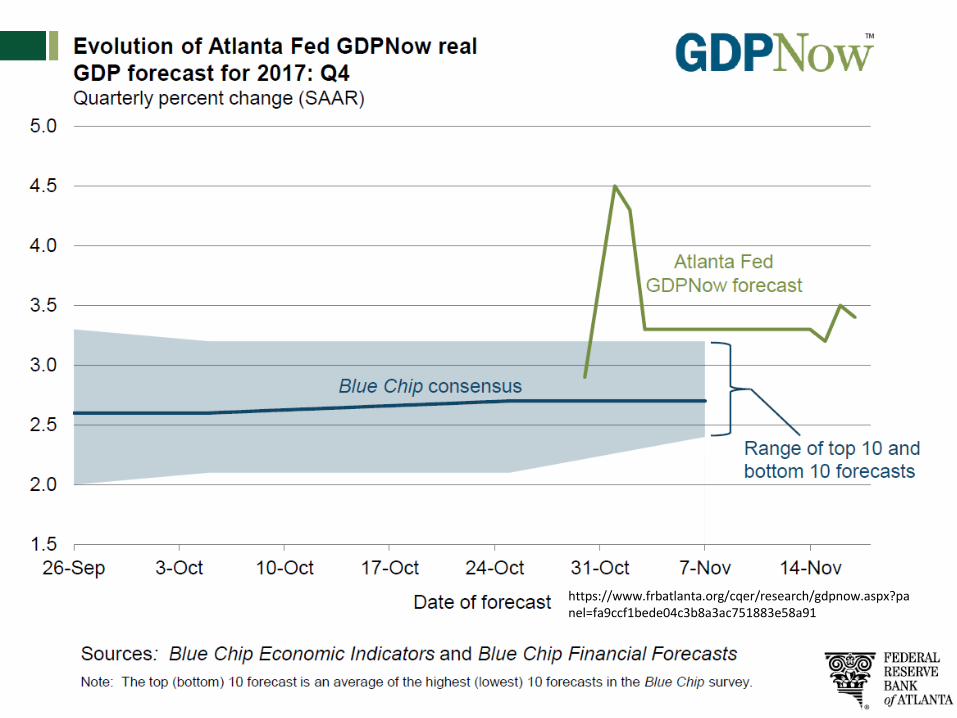

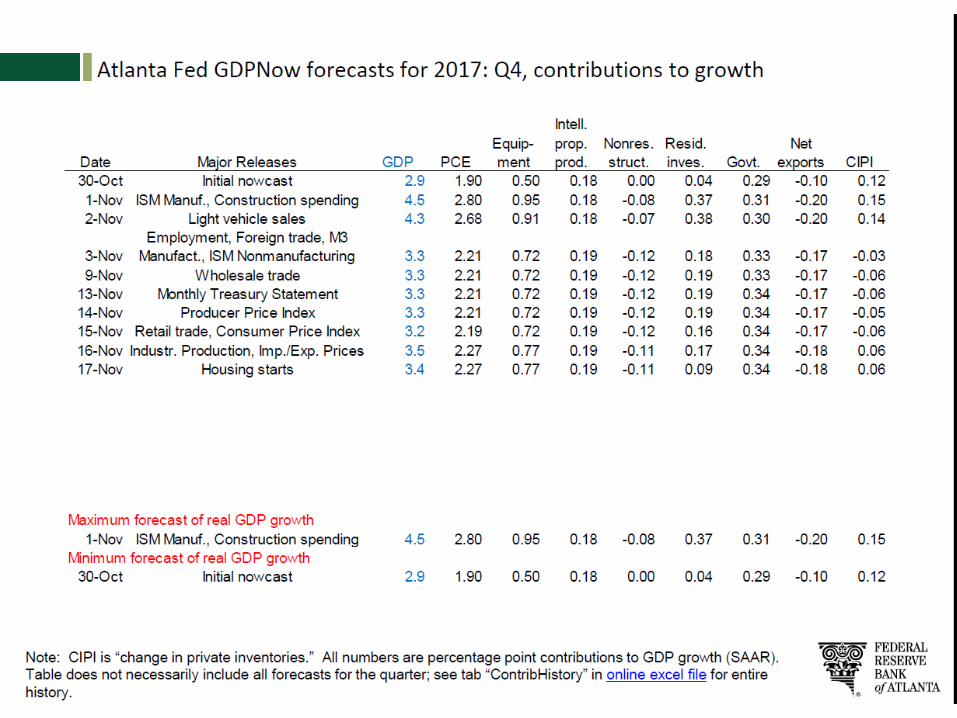

Nowcasting: An Example from the FRBNY

https://www.frbatlanta.org/cqer/research/gdpnow.aspx?panel=fa9ccf1bede04c3b8a3ac751883e58a91

Business cycle analysis

• Familiarity with cyclical patterns of key macro variables can help detect when the economy may be off track

• Very helpful in pinning down the causes

• Provide insights into what is going on during the current quarter / year

• Standard measures to assess the current state of the economy are often available with lags and revisions

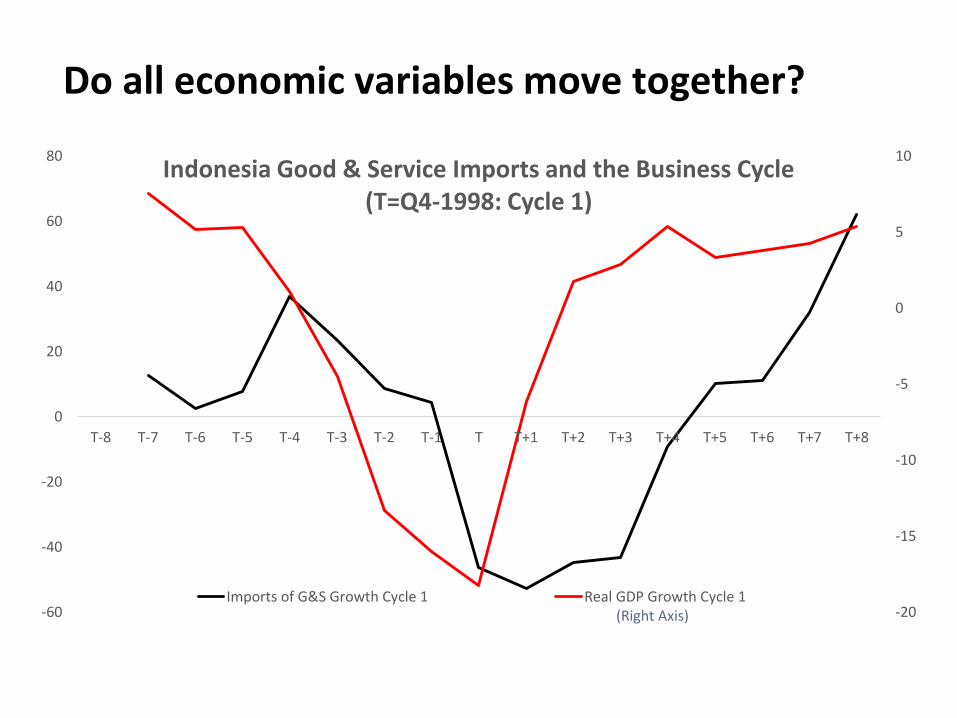

Do all economic variables move together?

-20

-15

-10

-5

0

5

10

-60

-40

-20

0

20

40

60

80

T-8 T-7 T-6 T-5 T-4 T-3 T-2 T-1 T T+1 T+2 T+3 T+4 T+5 T+6 T+7 T+8

Indonesia Good & Service Imports and the Business Cycle (T=Q4-1998: Cycle 1)

Imports of G&S Growth Cycle 1 Real GDP Growth Cycle 1(Right Axis)

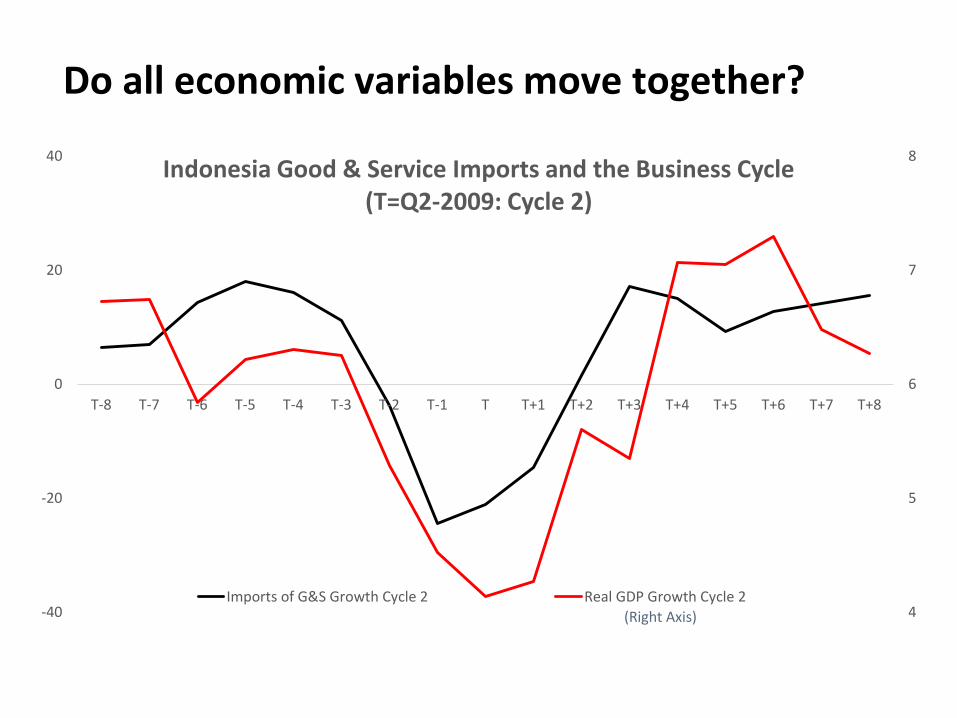

Do all economic variables move together?

(Right Axis) 4

5

6

7

8

-40

-20

0

20

40

T-8 T-7 T-6 T-5 T-4 T-3 T-2 T-1 T T+1 T+2 T+3 T+4 T+5 T+6 T+7 T+8

Indonesia Good & Service Imports and the Business Cycle (T=Q2-2009: Cycle 2)

Imports of G&S Growth Cycle 2 Real GDP Growth Cycle 2

What does IP say about GDP growth?

2

3

4

5

6

7

8

-6

-4

-2

0

2

4

6

8

10

12

14

T-8 T-7 T-6 T-5 T-4 T-3 T-2 T-1 T T+1 T+2 T+3 T+4 T+5 T+6 T+7 T+8

Indonesia IP and the Business Cycle (T=Q2-2009: Cycle 2)

IP Growth Real GDP Growth

(Right Axis)

Key takeaways

• Potential output estimation tools include time series filters and theory based-methods (production function approach), all have limits and should be used complementarily

• Analysis of domestic demand requires high quality data on GDP and its components, especially consumption and investment

• Understanding the underlying drivers of consumption and investment is key to diagnosing the state of the economy

• Business cycle provides information on the current state of the economy and the short run direction it might be moving in

Thank You

Appendix

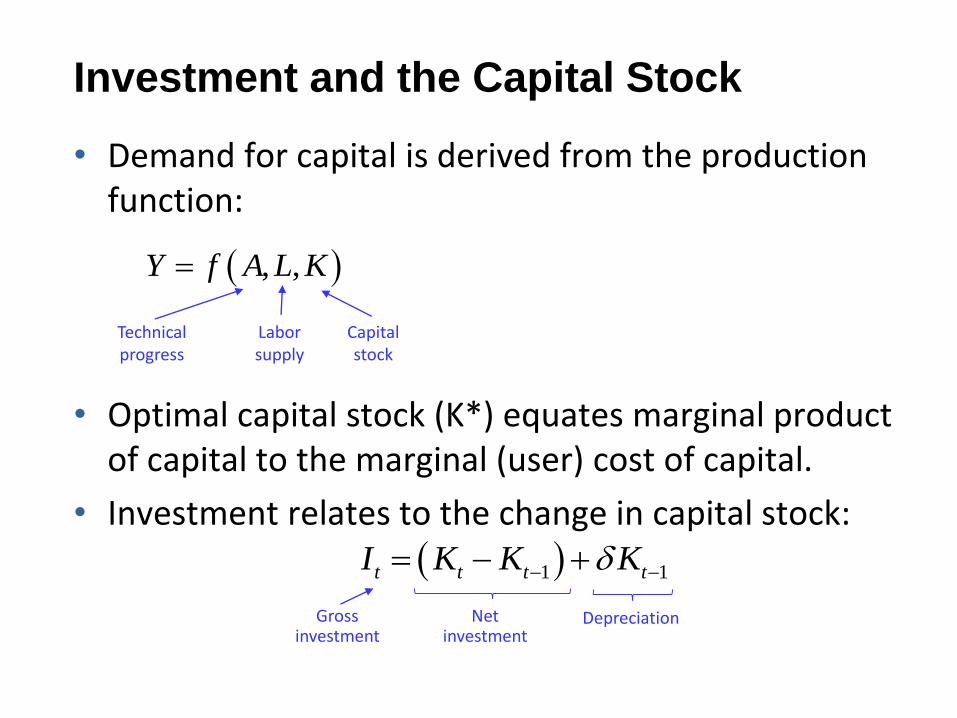

Investment and the Capital Stock

• Demand for capital is derived from the production function:

• Optimal capital stock (K*) equates marginal product of capital to the marginal (user) cost of capital.

• Investment relates to the change in capital stock:

, ,Y f A L K

1 1t t t tI K K K

Gross investment

Net investment

Depreciation

Technical progress

Capital stock

Labor supply