kantoor of koffiebar. alain swolfs.pdf · source: capgemini financial services analysis, 2015; 2015...

TRANSCRIPT

Kantoor of Koffiebar

Alain SwolfsMarket Unit Leader Banking & Insurance

Bessenveldstraat

Brussels, Belgium

Mobile:+32 (0)494 32 13 85

>> 0 >> 1 >> 2 >> 3 >> 4 >>

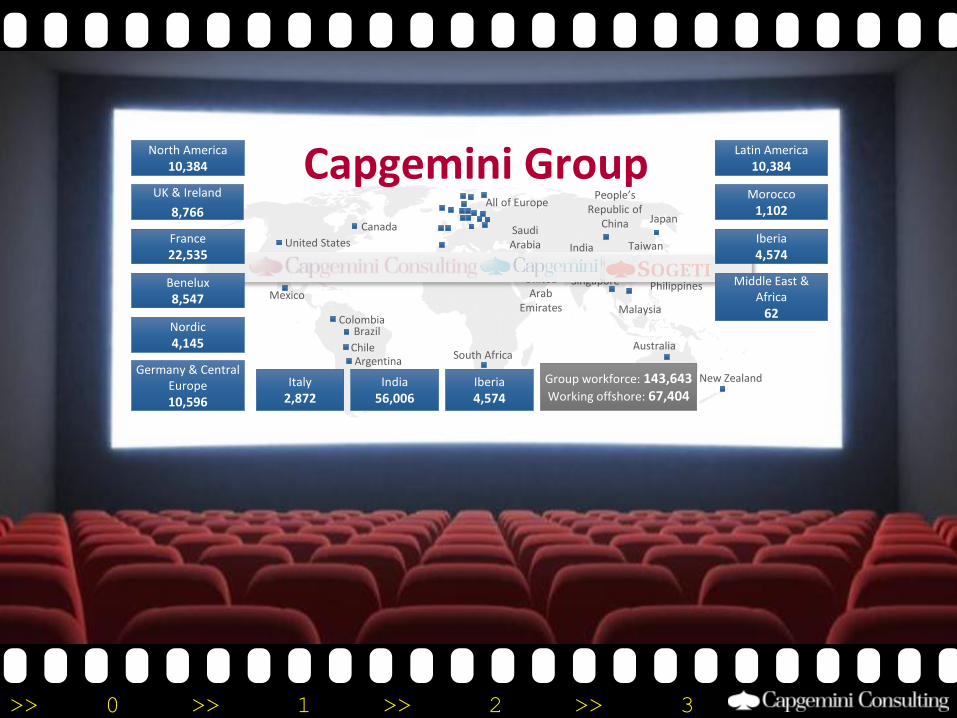

Japan

Taiwan

Philippines

Malaysia

Singapore

VietnamIndia

People’s Republic of

China

United Arab

Emirates

Saudi Arabia

All of Europe

Morocco

South AfricaArgentina

Chile

BrazilColombia

Guatemala

Mexico

United States

Canada

Capgemini Group

Australia

New Zealand

North America

10,384

UK & Ireland

8,766

Nordic

4,145

Germany & Central Europe

10,596

Latin America

10,384

Morocco

1,102

Iberia

4,574India

56,006Italy

2,872

Group workforce: 143,643Working offshore: 67,404

France

22,535

Benelux

8,547

Iberia

4,574

Middle East & Africa

62

>> 0 >> 1 >> 2 >> 3 >> 4 >>

>> 0 >> 1 >> 2 >> 3 >> 4 >>

>> 0 >> 1 >> 2 >> 3 >> 4 >>

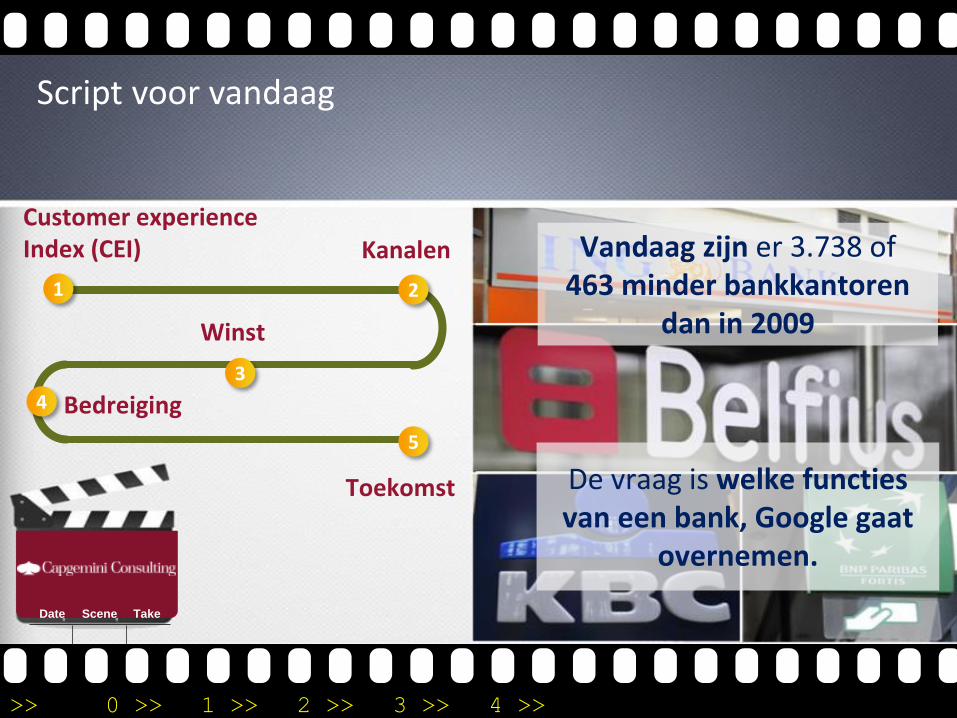

Script voor vandaag

Date Scene Take

De vraag is welke functies van een bank, Google gaat

overnemen.

Vandaag zijn er 3.738 of 463 minder bankkantoren

dan in 2009

Customer experience Index (CEI) Kanalen

Winst

Bedreiging

Toekomst

1 2

3

4

5

>> 0 >> 1 >> 2 >> 3 >> 4 >>

>> 0 >> 1 >> 2 >> 3 >> 4 >>

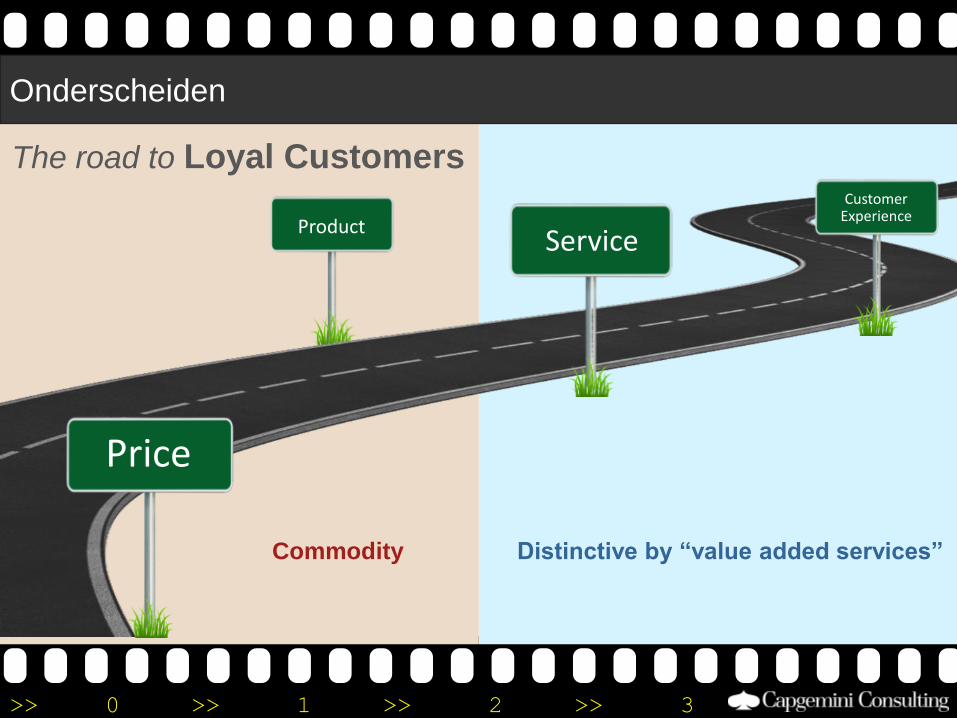

Onderscheiden

The road to Loyal Customers

Price

ServiceProduct

Customer Experience

Distinctive by “value added services”Commodity

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Thought Leadership

>> 0 >> 1 >> 2 >> 3 >> 4 >>

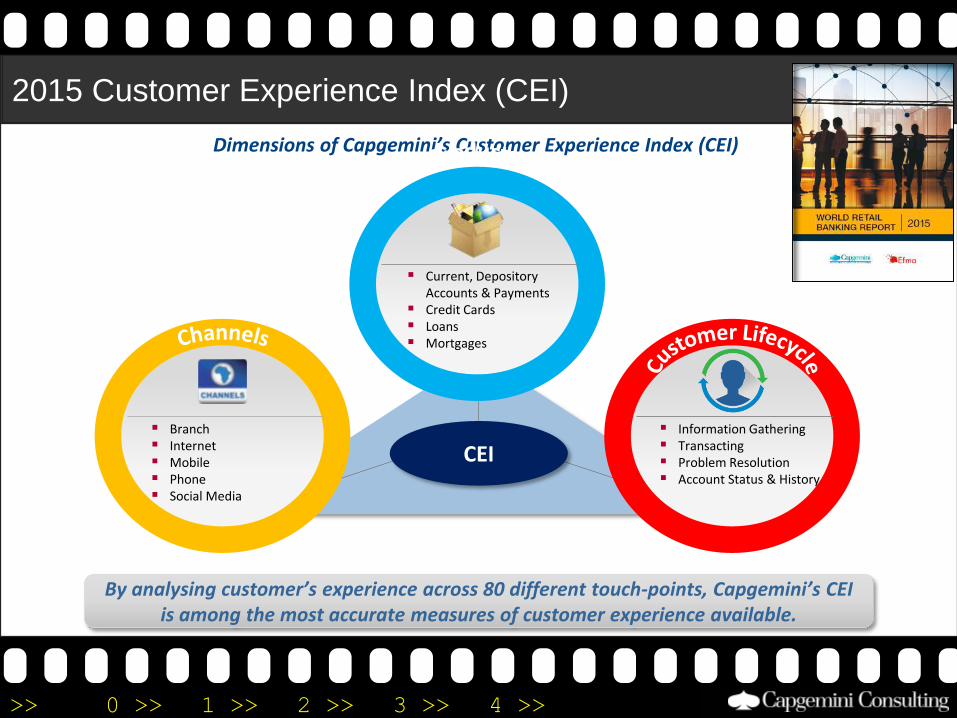

By analysing customer’s experience across 80 different touch-points, Capgemini’s CEI is among the most accurate measures of customer experience available.

Dimensions of Capgemini’s Customer Experience Index (CEI)

CEI

Current, Depository Accounts & Payments

Credit Cards Loans Mortgages

Information Gathering Transacting Problem Resolution Account Status & History

Branch Internet Mobile Phone Social Media

2015 Customer Experience Index (CEI)

>> 0 >> 1 >> 2 >> 3 >> 4 >>

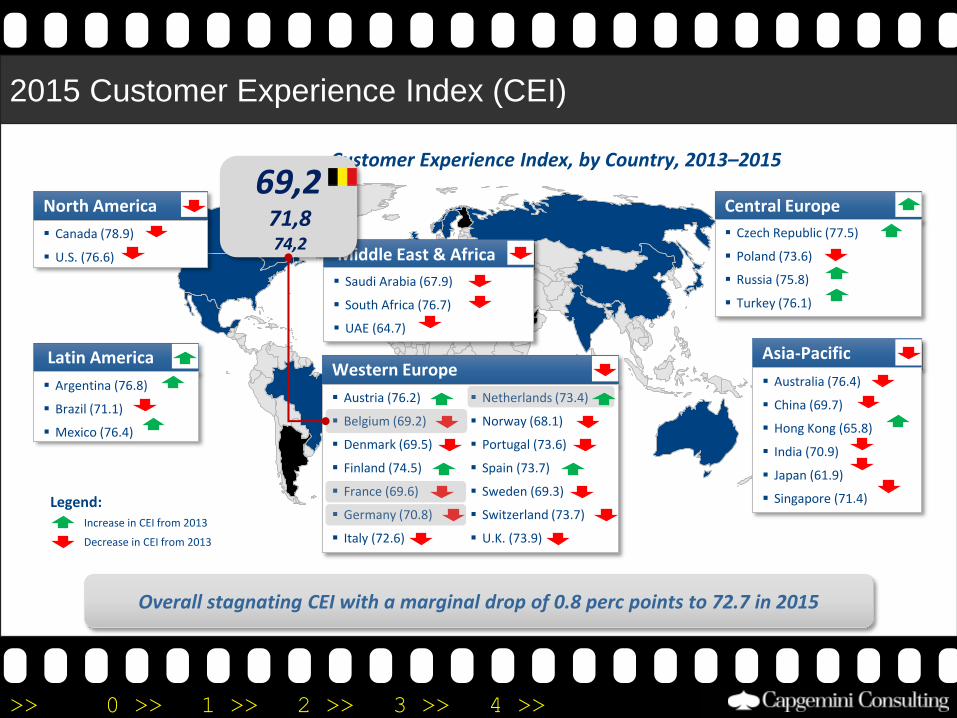

2015 Customer Experience Index (CEI)

Western Europe

Austria (76.2)

Belgium (69.2)

Denmark (69.5)

Finland (74.5)

France (69.6)

Germany (70.8)

Italy (72.6)

Netherlands (73.4)

Norway (68.1)

Portugal (73.6)

Spain (73.7)

Sweden (69.3)

Switzerland (73.7)

U.K. (73.9)

Middle East & Africa

Saudi Arabia (67.9)

South Africa (76.7)

UAE (64.7)

Increase in CEI from 2013

Legend:

Decrease in CEI from 2013

Latin America

Argentina (76.8)

Brazil (71.1)

Mexico (76.4)

North America

Canada (78.9)

U.S. (76.6)

Asia-Pacific

Australia (76.4)

China (69.7)

Hong Kong (65.8)

India (70.9)

Japan (61.9)

Singapore (71.4)

Central Europe

Czech Republic (77.5)

Poland (73.6)

Russia (75.8)

Turkey (76.1)

Overall stagnating CEI with a marginal drop of 0.8 perc points to 72.7 in 2015

Customer Experience Index, by Country, 2013–2015

69,271,874,2

>> 0 >> 1 >> 2 >> 3 >> 4 >>

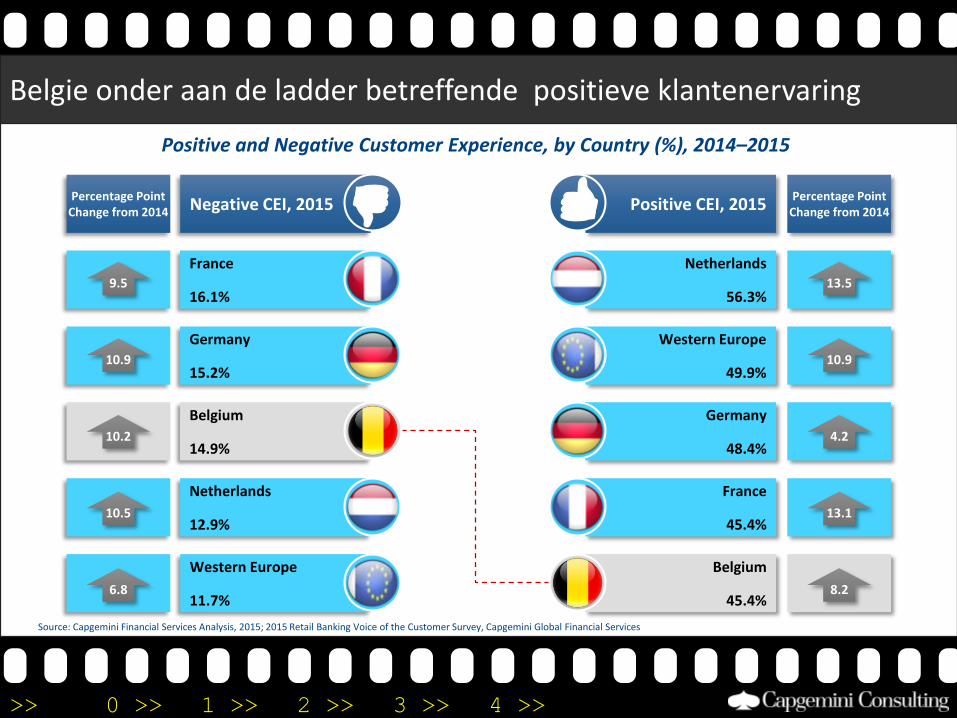

Percentage Point Change from 2014

Netherlands

56.3%

Germany

48.4%

France

45.4%

Positive CEI, 2015

Western Europe

49.9%

Western Europe

11.7%

Netherlands

12.9%

Germany

15.2%

France

16.1%

Negative CEI, 2015

9.5

10.9

10.2

10.5

6.8

13.5

10.9

4.2

13.1

8.2

Percentage Point Change from 2014

Belgie onder aan de ladder betreffende positieve klantenervaring

Source: Capgemini Financial Services Analysis, 2015; 2015 Retail Banking Voice of the Customer Survey, Capgemini Global Financial Services

Positive and Negative Customer Experience, by Country (%), 2014–2015

Belgium

14.9%

Belgium

45.4%

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Generation Y (18-34 jarigen)

206 Bones

207th Bone

>> 0 >> 1 >> 2 >> 3 >> 4 >>

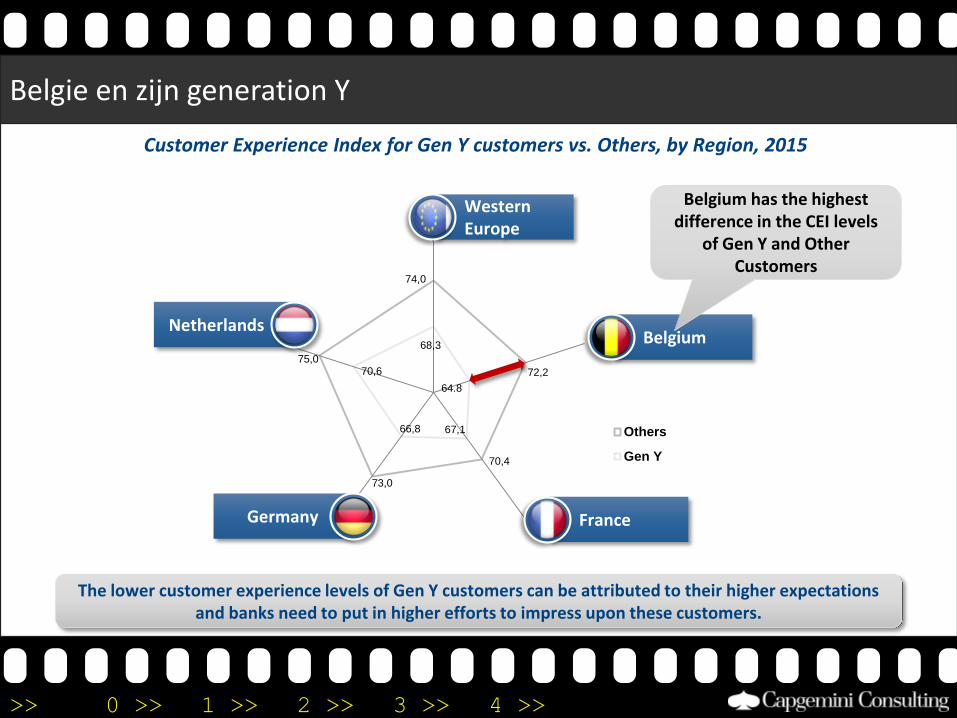

74,0

72,2

70,4

73,0

75,0

68,3

67,166,8

70,6

Others

Gen Y

Belgie en zijn generation Y

BelgiumNetherlands

Germany France

WesternEurope

The lower customer experience levels of Gen Y customers can be attributed to their higher expectations and banks need to put in higher efforts to impress upon these customers.

Belgium has the highest difference in the CEI levels

of Gen Y and Other Customers

Customer Experience Index for Gen Y customers vs. Others, by Region, 2015

64.8

>> 0 >> 1 >> 2 >> 3 >> 4 >>

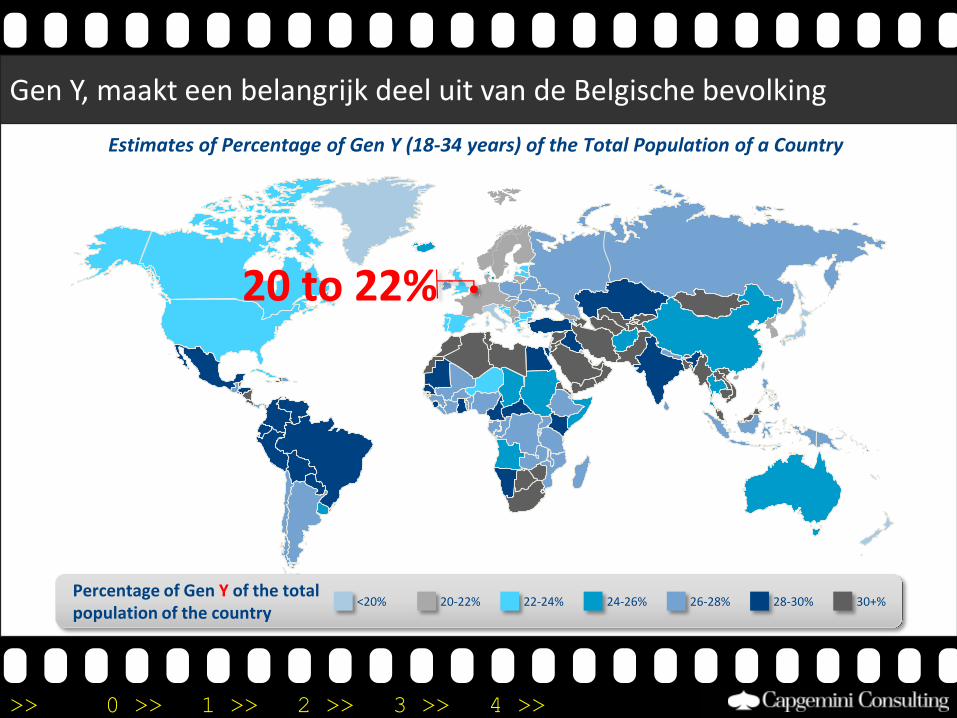

Gen Y, maakt een belangrijk deel uit van de Belgische bevolking

Percentage of Gen Y of the total population of the country

28-30%24-26%<20% 20-22% 22-24% 26-28% 30+%

Estimates of Percentage of Gen Y (18-34 years) of the Total Population of a Country

20 to 22%

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Kanaal voorkeur van de klant

Branches Digital Channels

>> 0 >> 1 >> 2 >> 3 >> 4 >>

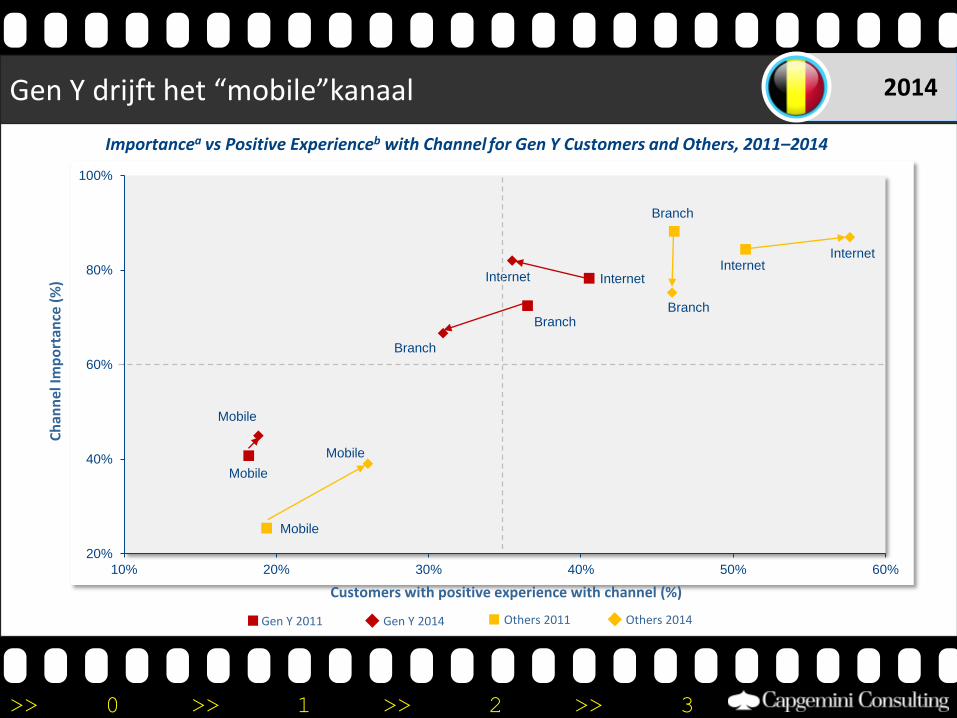

Gen Y drijft het “mobile”kanaal 2014

Branch

Internet

Mobile

Branch

Internet

Mobile

Branch

Internet

Mobile

Branch

Internet

Mobile

20%

40%

60%

80%

100%

10% 20% 30% 40% 50% 60%

Importancea vs Positive Experienceb with Channel for Gen Y Customers and Others, 2011–2014

Customers with positive experience with channel (%)

Ch

ann

el Im

po

rtan

ce (

%)

Gen Y 2014 Others 2014Gen Y 2011 Others 2011

>> 0 >> 1 >> 2 >> 3 >> 4 >>

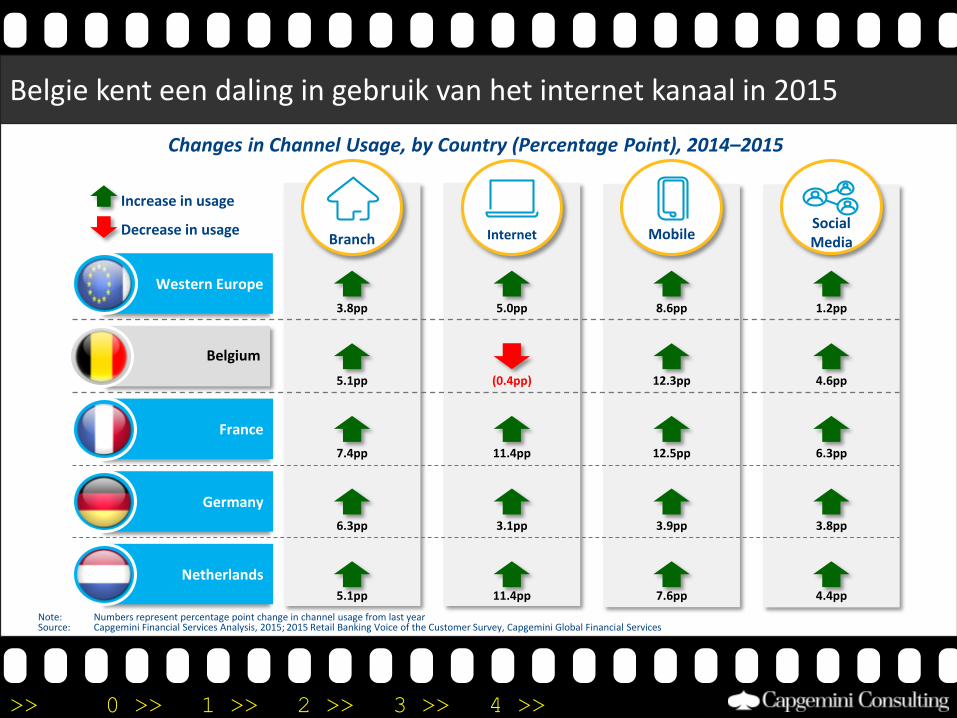

Belgie kent een daling in gebruik van het internet kanaal in 2015

Branch

3.8pp

5.1pp

7.4pp

6.3pp

5.1pp

Internet

5.0pp

(0.4pp)

11.4pp

3.1pp

11.4pp

Mobile

8.6pp

12.3pp

12.5pp

3.9pp

7.6pp

Social Media

1.2pp

4.6pp

6.3pp

3.8pp

4.4pp

Germany

France

Western Europe

Netherlands

Changes in Channel Usage, by Country (Percentage Point), 2014–2015

Increase in usage

Decrease in usage

Note: Numbers represent percentage point change in channel usage from last yearSource: Capgemini Financial Services Analysis, 2015; 2015 Retail Banking Voice of the Customer Survey, Capgemini Global Financial Services

Belgium

>> 0 >> 1 >> 2 >> 3 >> 4 >>

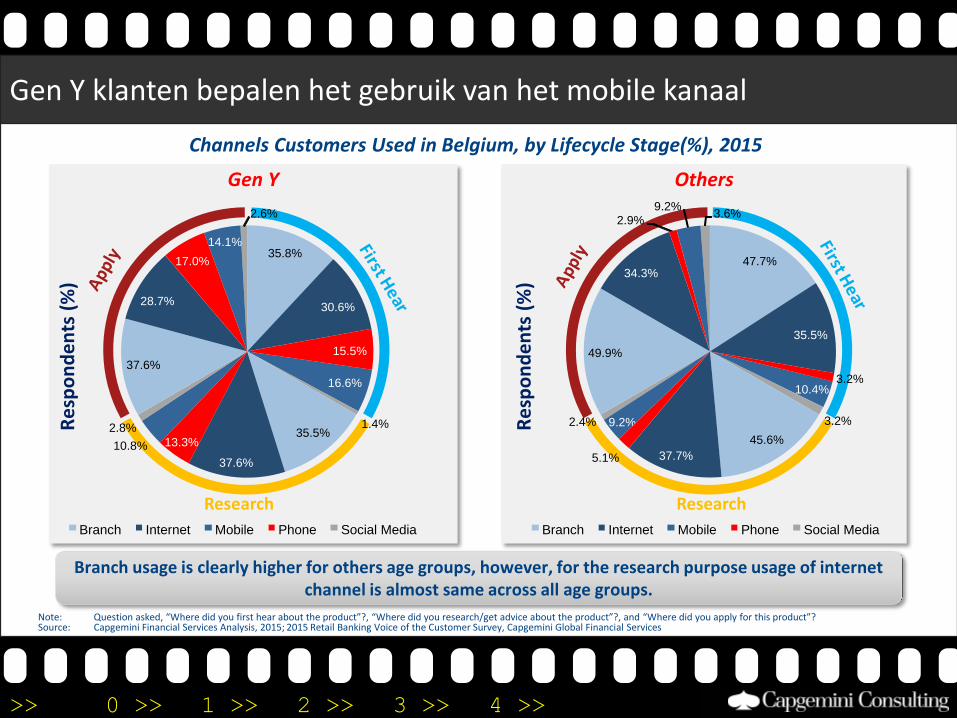

Gen Y klanten bepalen het gebruik van het mobile kanaal

Gen Y Others

Re

spo

nd

en

ts (

%)

Re

spo

nd

en

ts (

%)

Branch usage is clearly higher for others age groups, however, for the research purpose usage of internet channel is almost same across all age groups.

Note: Question asked, “Where did you first hear about the product”?, “Where did you research/get advice about the product”?, and “Where did you apply for this product”? Source: Capgemini Financial Services Analysis, 2015; 2015 Retail Banking Voice of the Customer Survey, Capgemini Global Financial Services

Channels Customers Used in Belgium, by Lifecycle Stage(%), 2015

47.7%

35.5%

3.2%

45.6%

37.7%

2.4%

49.9%

34.3%

3.6%

Branch Internet Mobile Phone Social Media

Research

35.8%

30.6%

1.4%35.5%

37.6%

2.8%

37.6%

28.7%

2.6%

Branch Internet Mobile Phone Social Media

Research

16.6%

10.8%

10.4%

9.2%

9.2%

14.1%

3.2%

5.1%

2.9%

15.5%

13.3%

17.0%

>> 0 >> 1 >> 2 >> 3 >> 4 >>

De Impact van klanten gedrag op de winstgevendheid

>> 0 >> 1 >> 2 >> 3 >> 4 >>

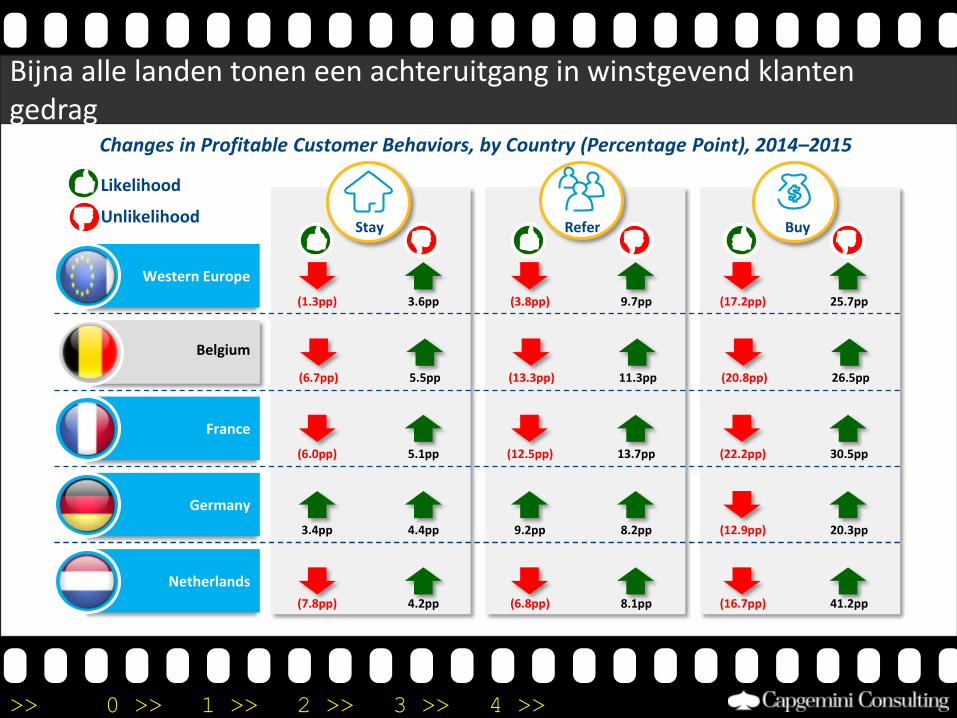

Bijna alle landen tonen een achteruitgang in winstgevend klanten gedrag

Stay Refer Buy

Likelihood

Unlikelihood

(6.7pp) 5.5pp (13.3pp) 11.3pp (20.8pp) 26.5pp

(6.0pp) 5.1pp (12.5pp) 13.7pp (22.2pp) 30.5pp

Germany

France

Western Europe

Netherlands

3.4pp 4.4pp 9.2pp 8.2pp (12.9pp) 20.3pp

(7.8pp) 4.2pp (6.8pp) 8.1pp (16.7pp) 41.2pp

(1.3pp) 3.6pp (3.8pp) 9.7pp (17.2pp) 25.7pp

Changes in Profitable Customer Behaviors, by Country (Percentage Point), 2014–2015

Belgium

>> 0 >> 1 >> 2 >> 3 >> 4 >>

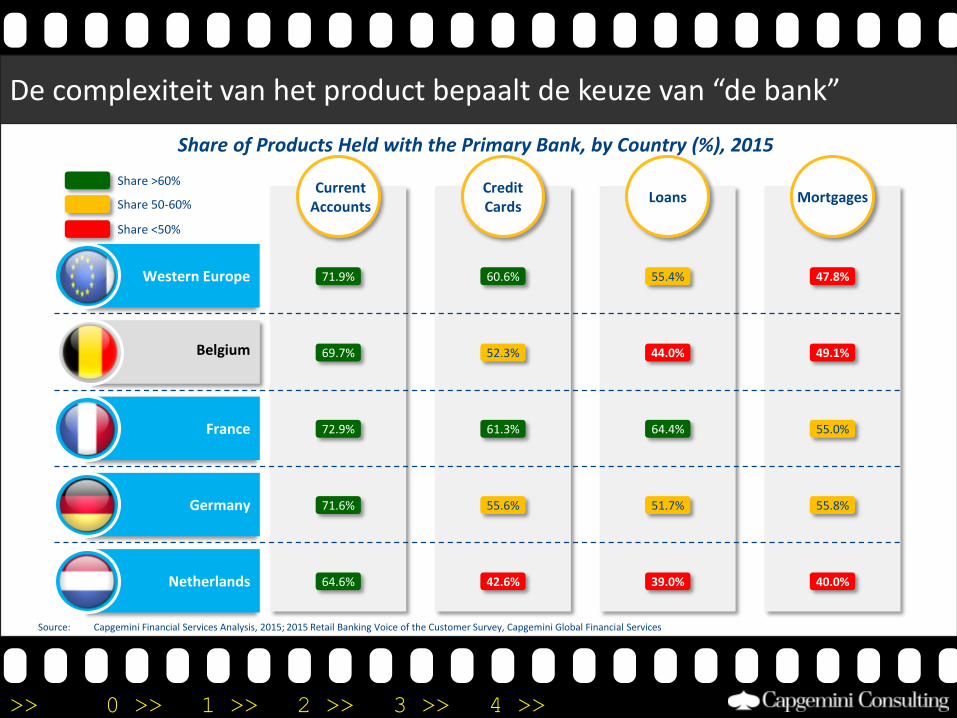

De complexiteit van het product bepaalt de keuze van “de bank”

71.9%

Current Accounts

MortgagesCredit Cards

Loans

60.6% 55.4% 47.8%

52.3% 44.0% 49.1%

72.9% 61.3% 64.4% 55.0%

71.6% 55.6% 51.7% 55.8%

64.6% 42.6% 39.0% 40.0%

69.7%

Share >60%

Share 50-60%

Share <50%

Share of Products Held with the Primary Bank, by Country (%), 2015

Germany

France

Western Europe

Netherlands

Source: Capgemini Financial Services Analysis, 2015; 2015 Retail Banking Voice of the Customer Survey, Capgemini Global Financial Services

Belgium

>> 0 >> 1 >> 2 >> 3 >> 4 >>

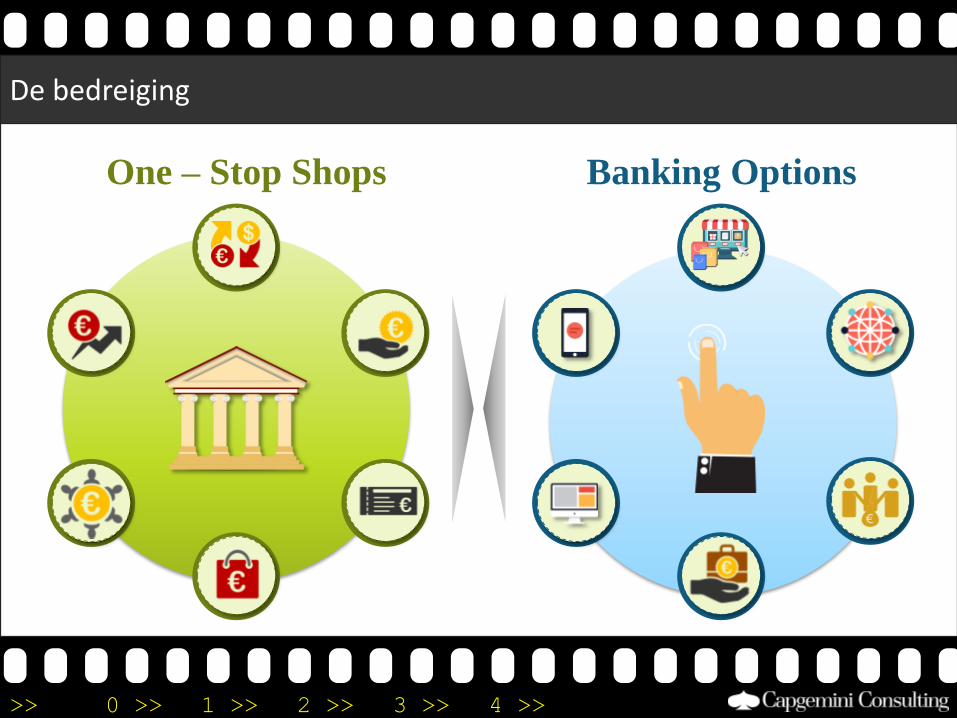

Banking Options

De bedreiging

One – Stop Shops

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Brett King

BANK 3.0

Why Banking is no longer

somewhere you GO, But

Something you DO

>> 0 >> 1 >> 2 >> 3 >> 4 >>

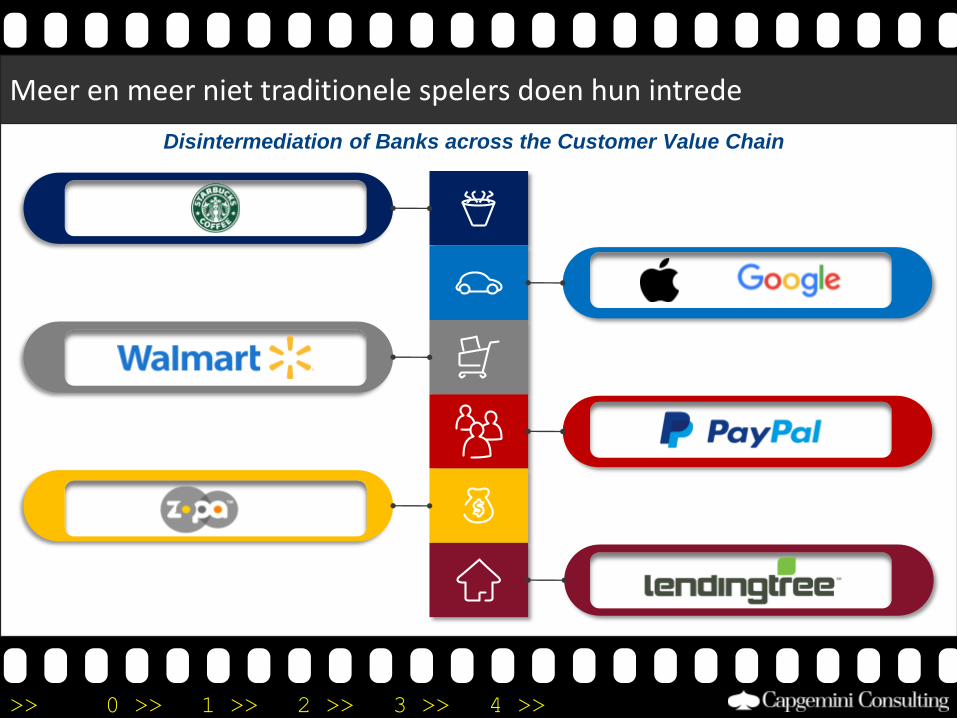

Meer en meer niet traditionele spelers doen hun intrede

Disintermediation of Banks across the Customer Value Chain

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Customer sees multiple touch points as part of the same brand.

Single view but banks operate in functional silo’s

Customer sees multiple touch points independently

Channels are functional & technical silo’s.

Totaal ervaring

Single Channel Multi Channel Cross Channel All Channel experience

ATM Call CentreOnline Banking Internet Banking Video Banking Virtual BankingMobile Banking

1967 1980 1990 2000 201? 201?2010

Single Channel

Customers experience single touchpoint

Banks have a single type of touchpoint

Inside Out Paradigma Shift Outside InInside Out Paradigma Shift Outside InInside Out Paradigma Shift Outside In

Multi Channel Cross Channel All Channel experience

Customer experience a brand, not a channel within a brand

>> 0 >> 1 >> 2 >> 3 >> 4 >>

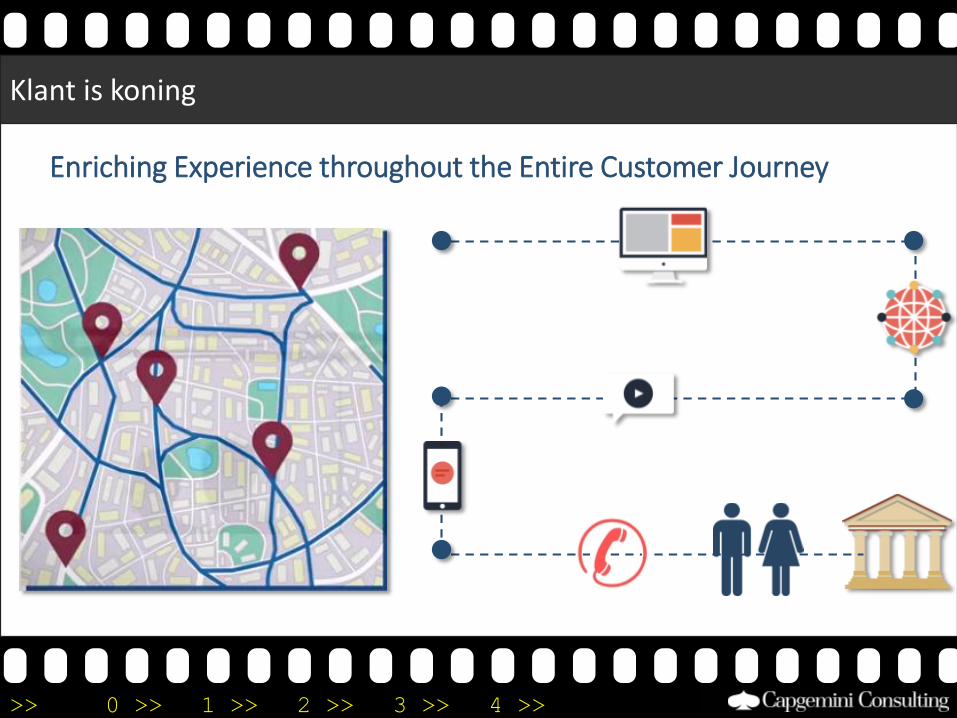

Klant is koning

Enriching Experience throughout the Entire Customer Journey

>> 0 >> 1 >> 2 >> 3 >> 4 >>

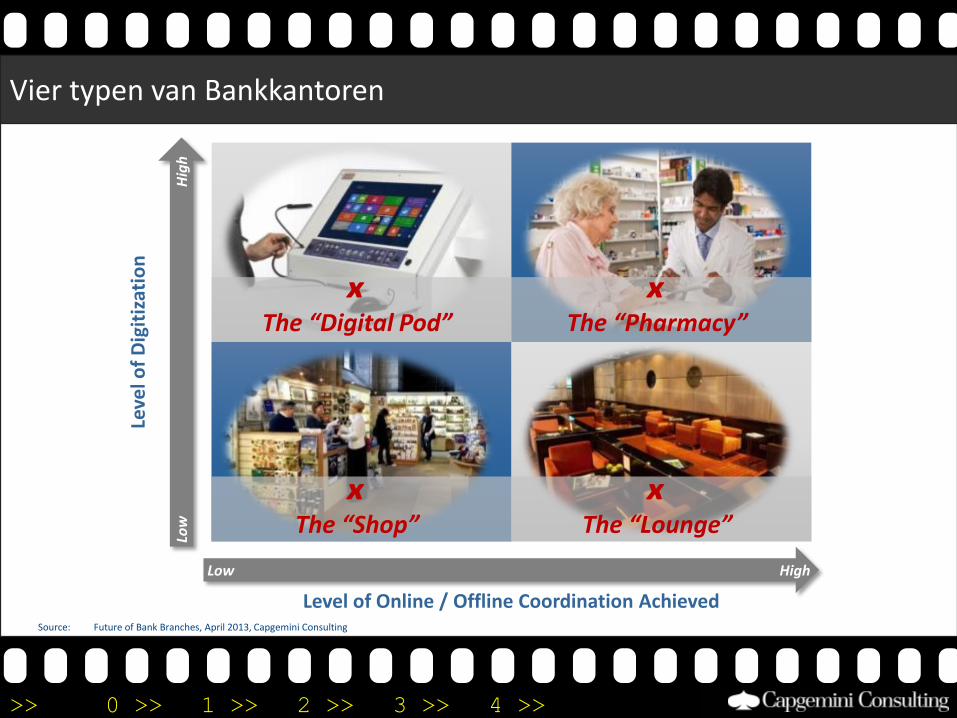

Source: Future of Bank Branches, April 2013, Capgemini Consulting

Leve

l of

Dig

itiz

atio

n

Hig

hLo

w

Low High

Level of Online / Offline Coordination Achieved

ₓThe “Shop”

ₓThe “Digital Pod”

ₓThe “Pharmacy”

ₓThe “Lounge”

Vier typen van Bankkantoren

>> 0 >> 1 >> 2 >> 3 >> 4 >>

“Digital Pod”: Gericht op een

vooruitstrevende en overweldigende

digital experience

Level of Customer Intimacy Level of Advice ComplexityBranch Format

The Digital Pod

>> 0 >> 1 >> 2 >> 3 >> 4 >>

“Pharmacy”: Zeer goede coordinatie tussen

kanalen, zowel fysiek als digitaal

Level of Customer Intimacy Level of Advice Complexity

The Pharmacy

Branch Format

>> 0 >> 1 >> 2 >> 3 >> 4 >>

“Shop”: Ideaal voor studenten, nieuwe – en

bestaande klanten met standaard

behoeften

Level of Customer Intimacy Level of Advice ComplexityBranch Format

The Shop

>> 0 >> 1 >> 2 >> 3 >> 4 >>

“Lounge”: Vooral gericht op het bouwen van

duurzame relaties met klanten

Level of Customer Intimacy Level of Advice ComplexityBranch Format

The Lounge

>> 0 >> 1 >> 2 >> 3 >> 4 >>

JA... DIT IS EEN BANKKANTOOR

>> 0 >> 1 >> 2 >> 3 >> 4 >>

May The

Force

Be With You