jollibee foods corporation doing business under the name ...… · jollibee group’s acquisitions...

TRANSCRIPT

Jollibee Foods CorporationDoing business under the name andstyle of Jollibee(formerly Jollibee Foods Corporation)and Subsidiaries

Consolidated Financial StatementsDecember 31, 2018 and 2017and Years Ended December 31, 2018,2017 and 2016

and

Independent Auditor’s Report

*SGVFS034434*

INDEPENDENT AUDITOR’S REPORT

The Stockholders and the Board of DirectorsJollibee Foods CorporationDoing business under the name and style of Jollibee(formerly Jollibee Foods Corporation) and Subsidiaries

Opinion

We have audited the consolidated financial statements of Jollibee Foods Corporation Doing businessunder the name and style of Jollibee (formerly Jollibee Foods Corporation) (the Parent Company) and itssubsidiaries (the Jollibee Group), which comprise the consolidated statements of financial position as atDecember 31, 2018 and 2017, and the consolidated statements of comprehensive income, consolidatedstatements of changes in equity and consolidated statements of cash flows for each of the three years inthe period ended December 31, 2018, and notes to the consolidated financial statements, including asummary of significant accounting policies.

In our opinion, the accompanying consolidated financial statements present fairly, in all material respects,the financial position of the Jollibee Group as at December 31, 2018 and 2017, and its consolidatedfinancial performance and its consolidated cash flows for each of the three years in the period endedDecember 31, 2018 in accordance with Philippine Financial Reporting Standards (PFRSs).

Basis for Opinion

We conducted our audits in accordance with Philippine Standards on Auditing (PSAs). Ourresponsibilities under those standards are further described in the Auditor’s Responsibilities for the Auditof the Consolidated Financial Statements section of our report. We are independent of the Jollibee Groupin accordance with the Code of Ethics for Professional Accountants in the Philippines (Code of Ethics)together with the ethical requirements that are relevant to our audit of the consolidated financialstatements in the Philippines, and we have fulfilled our other ethical responsibilities in accordance withthese requirements and the Code of Ethics. We believe that the audit evidence we have obtained issufficient and appropriate to provide a basis for our opinion.

Key Audit Matters

Key audit matters are those matters that, in our professional judgment, were of most significance in ouraudit of the consolidated financial statements of the current period. These matters were addressed in thecontext of our audit of the consolidated financial statements as a whole, and in forming our opinionthereon, and we do not provide a separate opinion on these matters. For each matter below, ourdescription of how our audit addressed the matter is provided in that context.

SyCip Gorres Velayo & Co.6760 Ayala Avenue1226 Makati CityPhilippines

Tel: (632) 891 0307Fax: (632) 819 0872ey.com/ph

BOA/PRC Reg. No. 0001, October 4, 2018, valid until August 24, 2021SEC Accreditation No. 0012-FR-5 (Group A), November 6, 2018, valid until November 5, 2021

A member firm of Ernst & Young Global Limited

*SGVFS034434*

- 2 -

We have fulfilled the responsibilities described in the Auditor’s Responsibilities for the Audit of theConsolidated Financial Statements section of our report, including in relation to these matters.Accordingly, our audit included the performance of procedures designed to respond to our assessment ofthe risks of material misstatement of the consolidated financial statements. The results of our auditprocedures, including the procedures performed to address the matters below, provide the basis for ouraudit opinion on the accompanying consolidated financial statements.

Accounting for Business Combination – Acquisition of SJBF LLC

On April 17, 2018, the Jollibee Group, through its wholly owned subsidiary, Bee Good! Inc., obtained45% additional interest over SJBF LLC resulting in 85% controlling interest. The Jollibee Grouprecognized goodwill of P=5,345.5 million and trademark and favourable leases of P=10,782.4 million basedon the purchase price allocation performed. We considered the accounting for this acquisition to be a keyaudit matter because it required significant amount of management judgment and estimation inidentifying the underlying acquired assets and liabilities and in determining their fair values, specificallythe acquired property and equipment, trademark and favourable leases.

The disclosures in relation to the acquisition of SJBF LLC are included in Notes 4 and 11 to theconsolidated financial statements.

Audit Response

We evaluated the competence, capabilities and objectivity of the external appraiser who prepared theappraisal report for the property and equipment and the external valuation specialist who valued thetrademark and favourable leases by considering their qualifications, relevant experience and reportingresponsibilities. We involved our internal specialist in the review of the methodologies and assumptionsused in arriving at the fair values of the property and equipment, trademark and favourable leases. Wecompared the key assumptions used such as the list prices and adjustment factors by reference to relevantmarket data for the valuation of property and equipment and favourable leases. We also compared thekey assumptions in the valuation of trademark such as revenue growth rate, long-term growth rate androyalty rate by reference to existing contractual terms, historical trends and relevant external information.We tested the parameters used in determining the discount rate against market data. We reviewed thepresentation and disclosures in the consolidated financial statements.

Recoverability of Goodwill and Trademarks with Indefinite Life

Goodwill and trademarks with indefinite life account for 27.2% of the Jollibee Group’s consolidated totalassets as at December 31, 2018. Goodwill relate to several cash generating units (CGUs) mainly fromJollibee Group’s acquisitions in the Philippines, the People’s Republic of China, Vietnam and the UnitedStates of America. Under Philippine Accounting Standard (PAS) 36, Impairment of Assets, the JollibeeGroup is required to perform an annual impairment test on the amount of goodwill and trademarks withindefinite life. These annual impairment tests are significant to our audit because the amounts arematerial to the consolidated financial statements. In addition, the determination of the recoverableamount of the CGUs to which the goodwill belongs and the trademarks with indefinite life involvessignificant assumptions about the future results of business such as discount rates which are applied to thecash flow or net sales forecasts, long-term revenue growth rates, and earnings before interest, taxes,depreciation and amortization (EBITDA).

Refer to Notes 4 and 14 to the consolidated financial statements for the details on trademarks andgoodwill and the assumptions used in the forecasts.

A member firm of Ernst & Young Global Limited

*SGVFS034434*

- 3 -

Audit Response

We involved our internal specialist in evaluating the methodologies and the assumptions used indetermining the recoverable amounts of the CGUs for goodwill and the trademarks with indefinite life.These assumptions include the discount rates, long-term revenue growth rates and EBITDA. Wecompared the forecasted long-term revenue growth rates, forecasted net sales and EBITDA against thehistorical data of the CGUs and inquired from management and operations personnel about the plans tosupport the forecast.

Furthermore, we tested the parameters used in the determination of discount rate against market data. Wereviewed the weighted average cost of capital (WACC) used in the impairment test by comparing it withthe WACC of comparable companies where the CGUs operate. We also reviewed the Jollibee Group’sdisclosures about those assumptions to which the outcome of the impairment test is most sensitive,specifically those that have the most significant effect on the determination of the recoverable amount ofgoodwill and trademarks with indefinite life.

Provisions and Contingencies

The Jollibee Group is involved in litigations, claims and disputes which are normal to its business. Thismatter is significant to our audit because the estimation of the potential liability resulting from theselitigations, claims and disputes requires significant management judgment. The inherent uncertainty overthe outcome of these matters is brought about by the differences in the interpretation and application oflaws and rulings.

Refer to Notes 4 and 17 for the disclosures about provisions and Note 29 for the disclosures aboutcontingencies of the Jollibee Group.

Audit Response

We involved our internal specialist in evaluating management’s assessment on whether provisions on thecontingencies should be recognized, and the estimation of such amount. We also discussed the status ofthe litigations, claims and disputes with management. In addition, we read correspondences with therelevant government agencies, obtained replies from third party legal counsels, and any relevant laws andrulings on similar matters. We evaluated the position of the Jollibee Group by considering the relevantlaws, rulings and jurisprudence.

Recoverability of Deferred Income Tax Assets

The Parent Company and certain subsidiaries (foreign and local) have recognized deferred tax assetsamounting to P=4,842.8 million as at December 31, 2018. Of that amount, around 24.0% relates to netoperating loss carryover and excess minimum corporate income tax over regular corporate income tax.Management estimated the recoverability of these deferred tax assets based on the forecasted taxableincome taking into account the period in which they can be claimed in the Philippines, the People’sRepublic of China and the United States of America. The analysis of the recoverability of deferred taxassets is significant to our audit because the assessment process requires use of management judgment. Itis also based on assumptions of future revenues and expenses as well as management’s plans andstrategies of the relevant taxable entities, including the Parent Company and certain subsidiaries.

A member firm of Ernst & Young Global Limited

*SGVFS034434*

- 4 -

Refer to Note 24 to the consolidated financial statements for the details of the deferred tax assets andNote 4 for the discussion of management’s judgments and estimates.

Audit Response

We obtained an understanding of the Parent Company and its subsidiaries’ deferred income taxcalculation process and, together with our internal specialist, the applicable tax rules and regulations. Wereviewed management’s assessment on the availability of future taxable income in reference to financialforecasts and tax strategies. We evaluated management’s forecast by comparing forecasts of futuretaxable income against approved budgets, historical performance of the relevant entities like past growthrates and with relevant external market information such as inflation. We also reviewed the timing of thereversal of future taxable and deductible temporary differences.

Adoption of PFRS 15, Revenue from Contracts with Customers

Effective January 1, 2018, the Jollibee Group adopted the new revenue recognition standard, PFRS 15,Revenue from Contracts with Customers, using the full retrospective method of adoption. The adoptionof PFRS 15 resulted in significant changes in the Group’s revenue recognition policies, process, andprocedures. The adoption of PFRS 15 is significant to our audit because this involves application ofsignificant management judgment and estimation in the following areas: (1) assessment whether allpromises in the franchise agreement meet the definition of distinct performance obligations;(2) determination of the transaction price of the franchise agreement; (3) assessment of the timing ofrevenue recognition; and (4) presentation of the Jollibee Group’s share in advertising expense arisingfrom the franchise agreement.

The disclosures related to the adoption of PFRS 15 are included in Note 2 to the consolidated financialstatements.

Audit Response

We obtained an understanding of the Jollibee Group’s process in implementing the new revenuerecognition standard, including revenue streams identification and scoping. We reviewed the PFRS 15adoption papers and accounting policies prepared by management. For significant revenue streams, weobtained sample contracts and reviewed whether the accounting policies considered the five-step modeland cost requirements of PFRS 15.

In relation to franchise fees, we reviewed sample franchise contracts focusing on the identification of theperformance obligations, determination of the transaction price, and the timing of revenue recognition.We reviewed management’s assessment on whether the activities being performed prior to opening offranchise store are distinct performance obligations.

In relation to reimbursements of system-wide advertising fees arising from franchise agreements, wereviewed and checked management’s assessment on whether the promises within these agreements meetthe definition of distinct performance obligations. We also reviewed management’s assessment indetermining that the Jollibee Group is acting as a principal for the system-wide advertising fees stated inthe franchise agreements and the presentation of these share in the system-wide advertising fees in theconsolidated statement of comprehensive income. We test computed the transition adjustments andreviewed the disclosures on the adoption of PFRS 15 in notes to the consolidated financial statements.

A member firm of Ernst & Young Global Limited

*SGVFS034434*

- 5 -

Other Information

Management is responsible for the other information. The other information comprises the informationincluded in the SEC Form 20-IS (Definitive Information Statement), SEC Form 17-A and Annual Reportfor the year ended December 31, 2018, but does not include the consolidated financial statements and ourauditor’s report thereon. The SEC Form 20-IS (Definitive Information Statement), SEC Form 17-A andAnnual Report for the year ended December 31, 2018 are expected to be made available to us after thedate of this auditor’s report.

Our opinion on the consolidated financial statements does not cover the other information and we will notexpress any form of assurance conclusion thereon.

In connection with our audits of the consolidated financial statements, our responsibility is to read theother information identified above when it becomes available and, in doing so, consider whether the otherinformation is materially inconsistent with the consolidated financial statements or our knowledgeobtained in the audits, or otherwise appears to be materially misstated.

Responsibilities of Management and Those Charged with Governance for the ConsolidatedFinancial Statements

Management is responsible for the preparation and fair presentation of the consolidated financialstatements in accordance with PFRSs, and for such internal control as management determines isnecessary to enable the preparation of consolidated financial statements that are free from materialmisstatement, whether due to fraud or error.

In preparing the consolidated financial statements, management is responsible for assessing the JollibeeGroup’s ability to continue as a going concern, disclosing, as applicable, matters related to going concernand using the going concern basis of accounting unless management either intends to liquidate theJollibee Group or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Jollibee Group’s financial reportingprocess.

Auditor’s Responsibilities for the Audit of the Consolidated Financial Statements

Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as awhole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s reportthat includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that anaudit conducted in accordance with PSAs will always detect a material misstatement when it exists.Misstatements can arise from fraud or error and are considered material if, individually or in theaggregate, they could reasonably be expected to influence the economic decisions of users taken on thebasis of these consolidated financial statements.

As part of an audit in accordance with PSAs, we exercise professional judgment and maintainprofessional skepticism throughout the audit. We also:

∂ Identify and assess the risks of material misstatement of the consolidated financial statements,whether due to fraud or error, design and perform audit procedures responsive to those risks, andobtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of

A member firm of Ernst & Young Global Limited

*SGVFS034434*

- 6 -

not detecting a material misstatement resulting from fraud is higher than for one resulting from error,as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override ofinternal control.

∂ Obtain an understanding of internal control relevant to the audit in order to design audit proceduresthat are appropriate in the circumstances, but not for the purpose of expressing an opinion on theeffectiveness of the Jollibee Group’s internal control.

∂ Evaluate the appropriateness of accounting policies used and the reasonableness of accountingestimates and related disclosures made by management.

∂ Conclude on the appropriateness of management’s use of the going concern basis of accounting and,based on the audit evidence obtained, whether a material uncertainty exists related to events orconditions that may cast significant doubt on the Jollibee Group’s ability to continue as a goingconcern. If we conclude that a material uncertainty exists, we are required to draw attention in ourauditor’s report to the related disclosures in the consolidated financial statements or, if suchdisclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidenceobtained up to the date of our auditor’s report. However, future events or conditions may cause theJollibee Group to cease to continue as a going concern.

∂ Evaluate the overall presentation, structure and content of the consolidated financial statements,including the disclosures, and whether the consolidated financial statements represent the underlyingtransactions and events in a manner that achieves fair presentation.

∂ Obtain sufficient appropriate audit evidence regarding the financial information of the entities orbusiness activities within the Jollibee Group to express an opinion on the consolidated financialstatements. We are responsible for the direction, supervision and performance of the audit. Weremain solely responsible for our audit opinion.

We communicate with those charged with governance regarding, among other matters, the planned scopeand timing of the audit and significant audit findings, including any significant deficiencies in internalcontrol that we identify during our audit.

We also provide those charged with governance with a statement that we have complied with relevantethical requirements regarding independence, and to communicate with them all relationships and othermatters that may reasonably be thought to bear on our independence, and where applicable, relatedsafeguards.

From the matters communicated with those charged with governance, we determine those matters thatwere of most significance in the audit of the consolidated financial statements of the current period andare therefore the key audit matters. We describe these matters in our auditor’s report unless law orregulation precludes public disclosure about the matter or when, in extremely rare circumstances, wedetermine that a matter should not be communicated in our report because the adverse consequences ofdoing so would reasonably be expected to outweigh the public interest benefits of such communication.

A member firm of Ernst & Young Global Limited

*SGVFS034434*

- 7 -

The engagement partner on the audit resulting in this independent auditor’s report isMariecris N. Barbaso.

SYCIP GORRES VELAYO & CO.

Mariecris N. BarbasoPartnerCPA Certificate No. 97101SEC Accreditation No. 1513-AR-1 (Group A), November 16, 2018, valid until November 15, 2021Tax Identification No. 202-065-716BIR Accreditation No. 08-001998-108-2018, February 14, 2018, valid until February 13, 2021PTR No. 7332526, January 3, 2019, Makati City

April 8, 2019

A member firm of Ernst & Young Global Limited

*SGVFS034434*

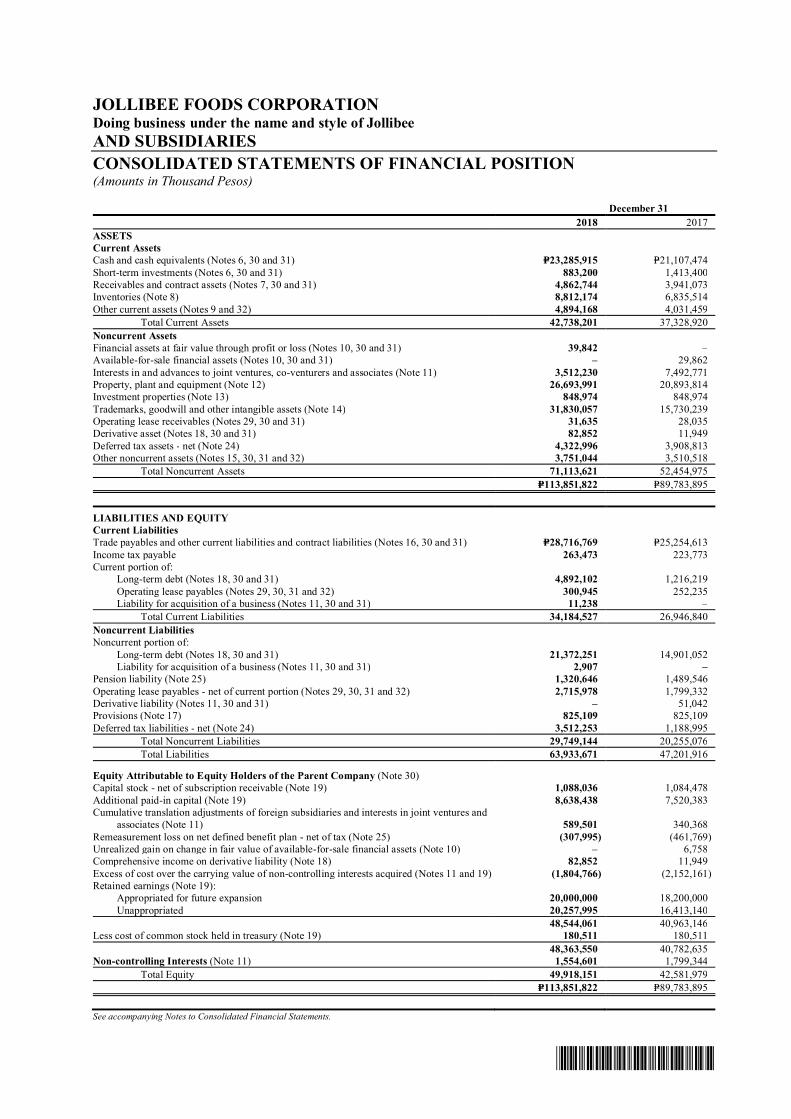

JOLLIBEE FOODS CORPORATIONDoing business under the name and style of JollibeeAND SUBSIDIARIESCONSOLIDATED STATEMENTS OF FINANCIAL POSITION(Amounts in Thousand Pesos)

December 312018 2017

ASSETSCurrent AssetsCash and cash equivalents (Notes 6, 30 and 31) P=23,285,915 P=21,107,474Short-term investments (Notes 6, 30 and 31) 883,200 1,413,400Receivables and contract assets (Notes 7, 30 and 31) 4,862,744 3,941,073Inventories (Note 8) 8,812,174 6,835,514Other current assets (Notes 9 and 32) 4,894,168 4,031,459

Total Current Assets 42,738,201 37,328,920Noncurrent AssetsFinancial assets at fair value through profit or loss (Notes 10, 30 and 31) 39,842 –Available-for-sale financial assets (Notes 10, 30 and 31) – 29,862Interests in and advances to joint ventures, co-venturers and associates (Note 11) 3,512,230 7,492,771Property, plant and equipment (Note 12) 26,693,991 20,893,814Investment properties (Note 13) 848,974 848,974Trademarks, goodwill and other intangible assets (Note 14) 31,830,057 15,730,239Operating lease receivables (Notes 29, 30 and 31) 31,635 28,035Derivative asset (Notes 18, 30 and 31) 82,852 11,949Deferred tax assets - net (Note 24) 4,322,996 3,908,813Other noncurrent assets (Notes 15, 30, 31 and 32) 3,751,044 3,510,518

Total Noncurrent Assets 71,113,621 52,454,975P=113,851,822 P=89,783,895

LIABILITIES AND EQUITYCurrent LiabilitiesTrade payables and other current liabilities and contract liabilities (Notes 16, 30 and 31) P=28,716,769 P=25,254,613Income tax payable 263,473 223,773Current portion of:

Long-term debt (Notes 18, 30 and 31) 4,892,102 1,216,219Operating lease payables (Notes 29, 30, 31 and 32) 300,945 252,235Liability for acquisition of a business (Notes 11, 30 and 31) 11,238 –

Total Current Liabilities 34,184,527 26,946,840Noncurrent LiabilitiesNoncurrent portion of:

Long-term debt (Notes 18, 30 and 31) 21,372,251 14,901,052Liability for acquisition of a business (Notes 11, 30 and 31) 2,907 –

Pension liability (Note 25) 1,320,646 1,489,546Operating lease payables - net of current portion (Notes 29, 30, 31 and 32) 2,715,978 1,799,332Derivative liability (Notes 11, 30 and 31) – 51,042Provisions (Note 17) 825,109 825,109Deferred tax liabilities - net (Note 24) 3,512,253 1,188,995

Total Noncurrent Liabilities 29,749,144 20,255,076Total Liabilities 63,933,671 47,201,916

Equity Attributable to Equity Holders of the Parent Company (Note 30)Capital stock - net of subscription receivable (Note 19) 1,088,036 1,084,478Additional paid-in capital (Note 19) 8,638,438 7,520,383Cumulative translation adjustments of foreign subsidiaries and interests in joint ventures and

associates (Note 11) 589,501 340,368Remeasurement loss on net defined benefit plan - net of tax (Note 25) (307,995) (461,769)Unrealized gain on change in fair value of available-for-sale financial assets (Note 10) – 6,758Comprehensive income on derivative liability (Note 18) 82,852 11,949Excess of cost over the carrying value of non-controlling interests acquired (Notes 11 and 19) (1,804,766) (2,152,161)Retained earnings (Note 19):

Appropriated for future expansion 20,000,000 18,200,000Unappropriated 20,257,995 16,413,140

48,544,061 40,963,146Less cost of common stock held in treasury (Note 19) 180,511 180,511

48,363,550 40,782,635Non-controlling Interests (Note 11) 1,554,601 1,799,344

Total Equity 49,918,151 42,581,979P=113,851,822 P=89,783,895

See accompanying Notes to Consolidated Financial Statements.

*SGVFS034434*

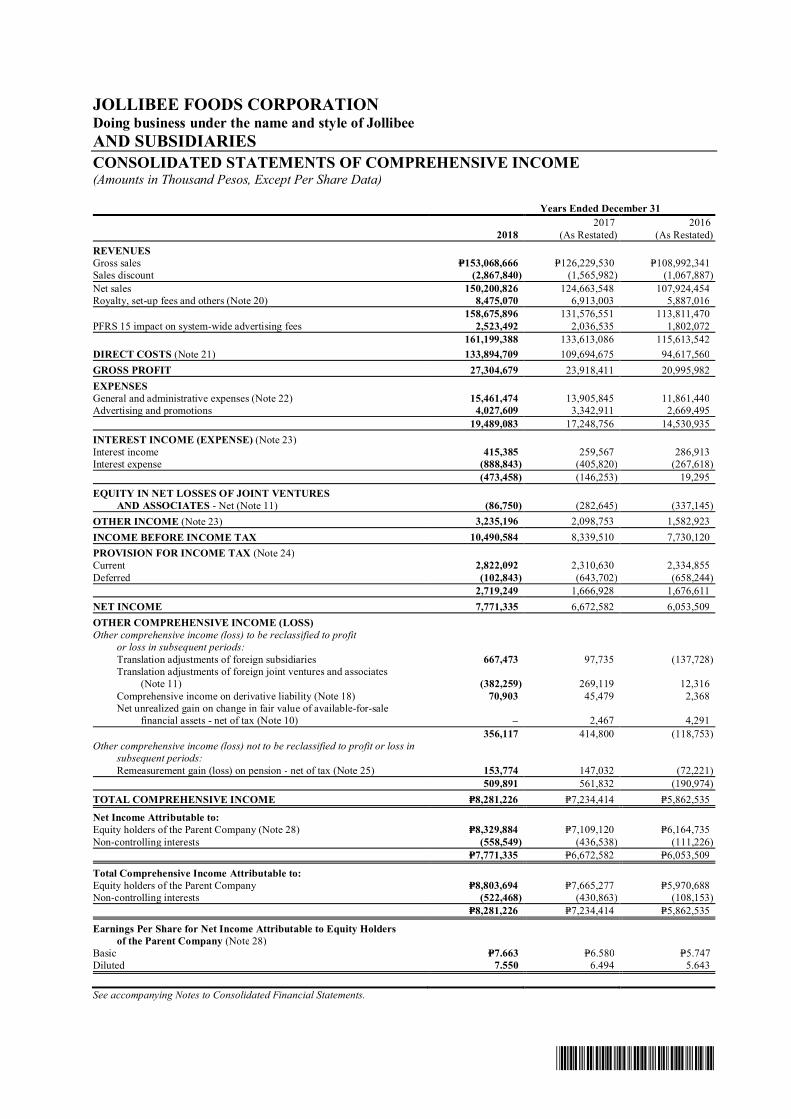

JOLLIBEE FOODS CORPORATIONDoing business under the name and style of JollibeeAND SUBSIDIARIESCONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME(Amounts in Thousand Pesos, Except Per Share Data)

Years Ended December 31

20182017

(As Restated)2016

(As Restated)REVENUESGross sales P=153,068,666 P=126,229,530 P=108,992,341Sales discount (2,867,840) (1,565,982) (1,067,887)Net sales 150,200,826 124,663,548 107,924,454Royalty, set-up fees and others (Note 20) 8,475,070 6,913,003 5,887,016

158,675,896 131,576,551 113,811,470PFRS 15 impact on system-wide advertising fees 2,523,492 2,036,535 1,802,072

161,199,388 133,613,086 115,613,542DIRECT COSTS (Note 21) 133,894,709 109,694,675 94,617,560GROSS PROFIT 27,304,679 23,918,411 20,995,982EXPENSESGeneral and administrative expenses (Note 22) 15,461,474 13,905,845 11,861,440Advertising and promotions 4,027,609 3,342,911 2,669,495

19,489,083 17,248,756 14,530,935INTEREST INCOME (EXPENSE) (Note 23)Interest income 415,385 259,567 286,913Interest expense (888,843) (405,820) (267,618)

(473,458) (146,253) 19,295EQUITY IN NET LOSSES OF JOINT VENTURES

AND ASSOCIATES - Net (Note 11) (86,750) (282,645) (337,145)OTHER INCOME (Note 23) 3,235,196 2,098,753 1,582,923INCOME BEFORE INCOME TAX 10,490,584 8,339,510 7,730,120PROVISION FOR INCOME TAX (Note 24)Current 2,822,092 2,310,630 2,334,855Deferred (102,843) (643,702) (658,244)

2,719,249 1,666,928 1,676,611NET INCOME 7,771,335 6,672,582 6,053,509OTHER COMPREHENSIVE INCOME (LOSS)Other comprehensive income (loss) to be reclassified to profit

or loss in subsequent periods:Translation adjustments of foreign subsidiaries 667,473 97,735 (137,728)Translation adjustments of foreign joint ventures and associates

(Note 11) (382,259) 269,119 12,316Comprehensive income on derivative liability (Note 18) 70,903 45,479 2,368Net unrealized gain on change in fair value of available-for-sale

financial assets - net of tax (Note 10) – 2,467 4,291356,117 414,800 (118,753)

Other comprehensive income (loss) not to be reclassified to profit or loss insubsequent periods:Remeasurement gain (loss) on pension - net of tax (Note 25) 153,774 147,032 (72,221)

509,891 561,832 (190,974)TOTAL COMPREHENSIVE INCOME P=8,281,226 P=7,234,414 P=5,862,535

Net Income Attributable to:Equity holders of the Parent Company (Note 28) P=8,329,884 P=7,109,120 P=6,164,735Non-controlling interests (558,549) (436,538) (111,226)

P=7,771,335 P=6,672,582 P=6,053,509

Total Comprehensive Income Attributable to:Equity holders of the Parent Company P=8,803,694 P=7,665,277 P=5,970,688Non-controlling interests (522,468) (430,863) (108,153)

P=8,281,226 P=7,234,414 P=5,862,535

Earnings Per Share for Net Income Attributable to Equity Holdersof the Parent Company (Note 28)

Basic P=7.663 P=6.580 P=5.747Diluted 7.550 6.494 5.643

See accompanying Notes to Consolidated Financial Statements.

*SGVFS034434*

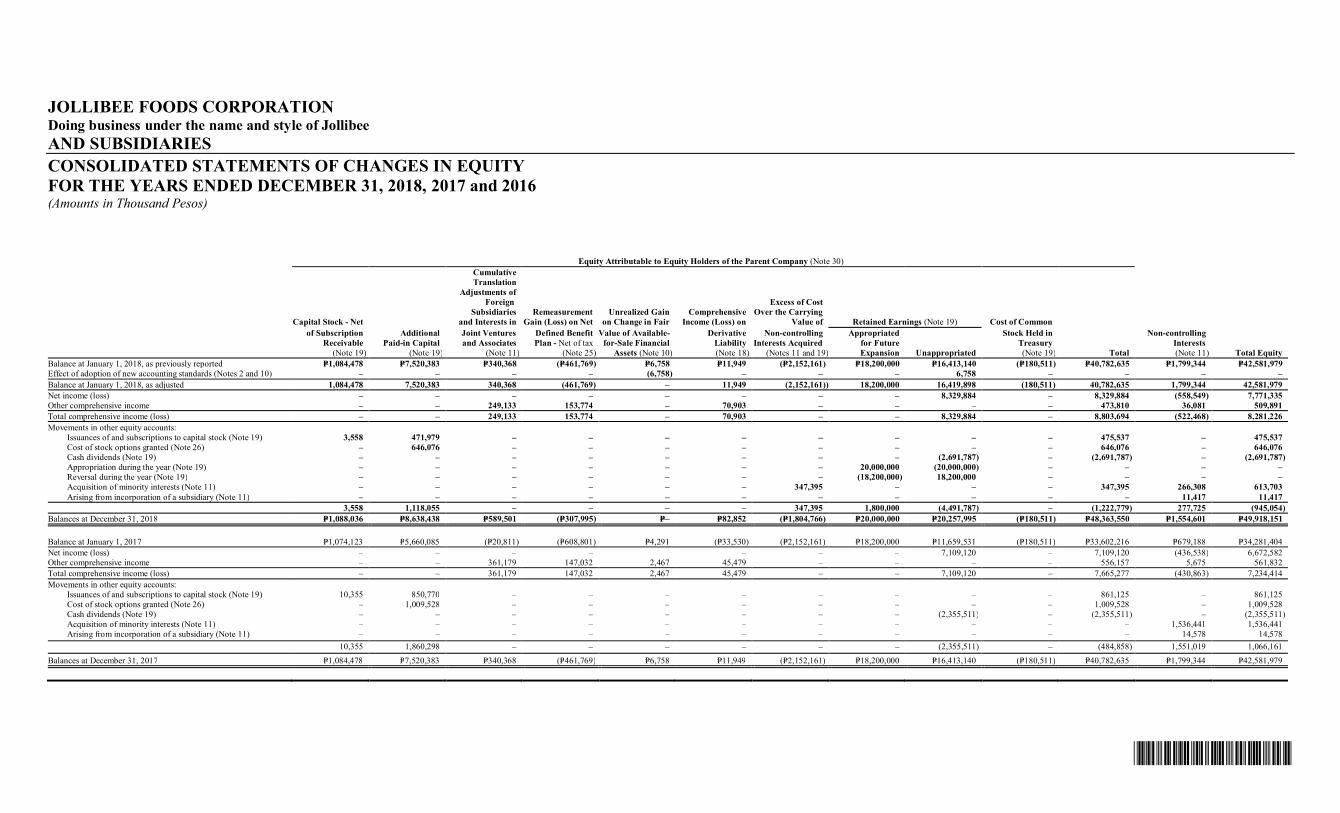

JOLLIBEE FOODS CORPORATIONDoing business under the name and style of JollibeeAND SUBSIDIARIESCONSOLIDATED STATEMENTS OF CHANGES IN EQUITYFOR THE YEARS ENDED DECEMBER 31, 2018, 2017 and 2016(Amounts in Thousand Pesos)

Equity Attributable to Equity Holders of the Parent Company (Note 30)CumulativeTranslation

Adjustments ofForeign Excess of Cost

Subsidiaries Remeasurement Unrealized Gain Comprehensive Over the CarryingCapital Stock - Net and Interests in Gain (Loss) on Net on Change in Fair Income (Loss) on Value of Retained Earnings (Note 19) Cost of Common

of Subscription Additional Joint Ventures Defined Benefit Value of Available- Derivative Non-controlling Appropriated Stock Held in Non-controllingReceivable Paid-in Capital and Associates Plan - Net of tax for-Sale Financial Liability Interests Acquired for Future Treasury Interests

(Note 19) (Note 19) (Note 11) (Note 25) Assets (Note 10) (Note 18) (Notes 11 and 19) Expansion Unappropriated (Note 19) Total (Note 11) Total EquityBalance at January 1, 2018, as previously reported P=1,084,478 P=7,520,383 P=340,368 (P=461,769) P=6,758 P=11,949 (P=2,152,161) P=18,200,000 P=16,413,140 (P=180,511) P=40,782,635 P=1,799,344 P=42,581,979Effect of adoption of new accounting standards (Notes 2 and 10) – – – – (6,758) – – – 6,758 – – – –Balance at January 1, 2018, as adjusted 1,084,478 7,520,383 340,368 (461,769) – 11,949 (2,152,161)) 18,200,000 16,419,898 (180,511) 40,782,635 1,799,344 42,581,979Net income (loss) – – – – – – – – 8,329,884 – 8,329,884 (558,549) 7,771,335Other comprehensive income – – 249,133 153,774 – 70,903 – – – – 473,810 36,081 509,891Total comprehensive income (loss) – – 249,133 153,774 – 70,903 – – 8,329,884 – 8,803,694 (522,468) 8,281,226Movements in other equity accounts:

Issuances of and subscriptions to capital stock (Note 19) 3,558 471,979 – – – – – – – – 475,537 – 475,537Cost of stock options granted (Note 26) – 646,076 – – – – – – – – 646,076 – 646,076Cash dividends (Note 19) – – – – – – – – (2,691,787) – (2,691,787) – (2,691,787)Appropriation during the year (Note 19) – – – – – – – 20,000,000 (20,000,000) – – – –Reversal during the year (Note 19) – – – – – – – (18,200,000) 18,200,000 – – – –Acquisition of minority interests (Note 11) – – – – – – 347,395 – – – 347,395 266,308 613,703Arising from incorporation of a subsidiary (Note 11) – – – – – – – – – – – 11,417 11,417

3,558 1,118,055 – – – – 347,395 1,800,000 (4,491,787) – (1,222,779) 277,725 (945,054)Balances at December 31, 2018 P=1,088,036 P=8,638,438 P=589,501 (P=307,995) P=– P=82,852 (P=1,804,766) P=20,000,000 P=20,257,995 (P=180,511) P=48,363,550 P=1,554,601 P=49,918,151

Balance at January 1, 2017 P=1,074,123 P=5,660,085 (P=20,811) (P=608,801) P=4,291 (P=33,530) (P=2,152,161) P=18,200,000 P=11,659,531 (P=180,511) P=33,602,216 P=679,188 P=34,281,404Net income (loss) – – – – – – – 7,109,120 – 7,109,120 (436,538) 6,672,582Other comprehensive income – – 361,179 147,032 2,467 45,479 – – – – 556,157 5,675 561,832Total comprehensive income (loss) – – 361,179 147,032 2,467 45,479 – – 7,109,120 – 7,665,277 (430,863) 7,234,414Movements in other equity accounts:

Issuances of and subscriptions to capital stock (Note 19) 10,355 850,770 – – – – – – – – 861,125 – 861,125Cost of stock options granted (Note 26) – 1,009,528 – – – – – – – – 1,009,528 – 1,009,528Cash dividends (Note 19) – – – – – – – – (2,355,511) – (2,355,511) – (2,355,511)Acquisition of minority interests (Note 11) – – – – – – – – – – – 1,536,441 1,536,441Arising from incorporation of a subsidiary (Note 11) – – – – – – – – – – – 14,578 14,578

10,355 1,860,298 – – – – – – (2,355,511) – (484,858) 1,551,019 1,066,161Balances at December 31, 2017 P=1,084,478 P=7,520,383 P=340,368 (P=461,769) P=6,758 P=11,949 (P=2,152,161) P=18,200,000 P=16,413,140 (P=180,511) P=40,782,635 P=1,799,344 P=42,581,979

*SGVFS034434*

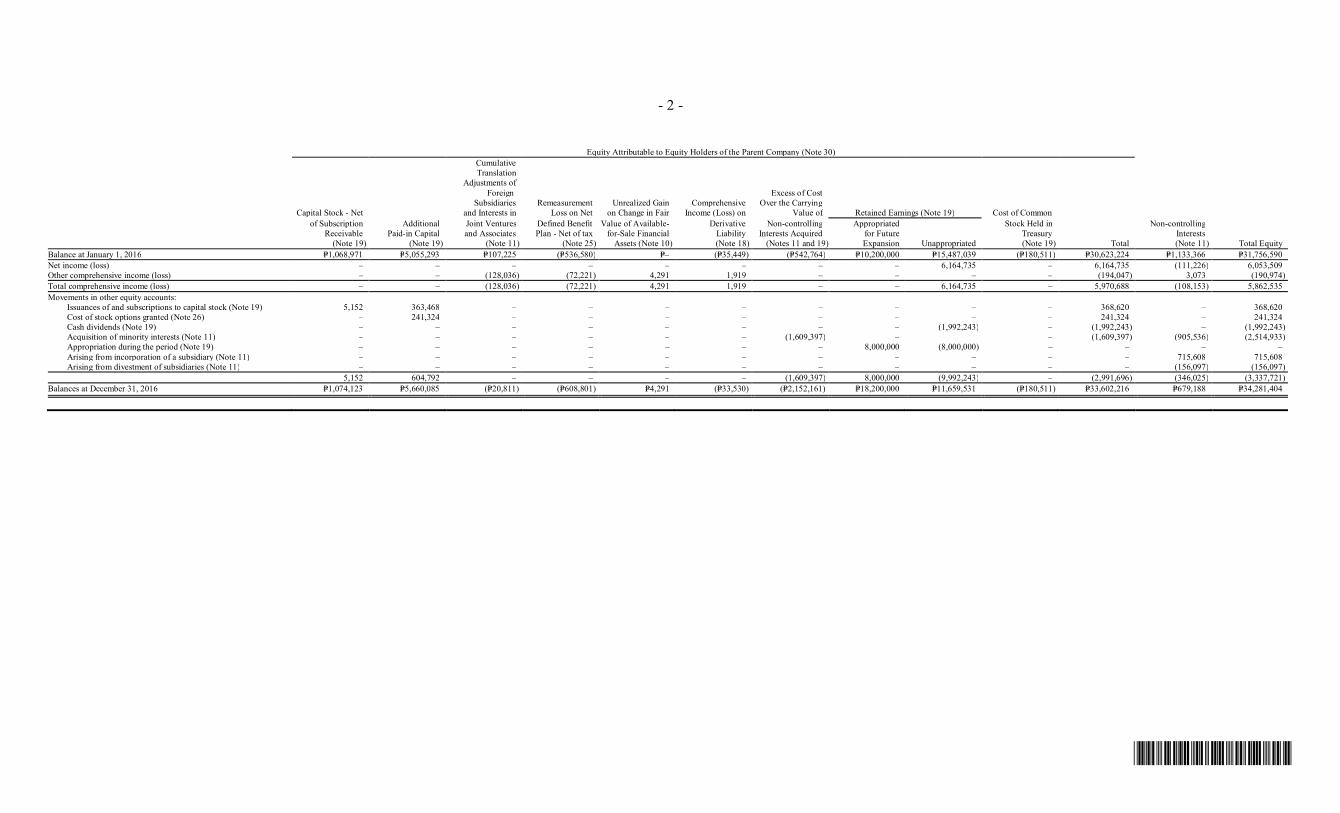

- 2 -

Equity Attributable to Equity Holders of the Parent Company (Note 30)CumulativeTranslation

Adjustments ofForeign Excess of Cost

Subsidiaries Remeasurement Unrealized Gain Comprehensive Over the CarryingCapital Stock - Net and Interests in Loss on Net on Change in Fair Income (Loss) on Value of Retained Earnings (Note 19) Cost of Common

of Subscription Additional Joint Ventures Defined Benefit Value of Available- Derivative Non-controlling Appropriated Stock Held in Non-controllingReceivable Paid-in Capital and Associates Plan - Net of tax for-Sale Financial Liability Interests Acquired for Future Treasury Interests

(Note 19) (Note 19) (Note 11) (Note 25) Assets (Note 10) (Note 18) (Notes 11 and 19) Expansion Unappropriated (Note 19) Total (Note 11) Total EquityBalance at January 1, 2016 P=1,068,971 P=5,055,293 P=107,225 (P=536,580) P=– (P=35,449) (P=542,764) P=10,200,000 P=15,487,039 (P=180,511) P=30,623,224 P=1,133,366 P=31,756,590Net income (loss) – – – – – – – – 6,164,735 – 6,164,735 (111,226) 6,053,509Other comprehensive income (loss) – – (128,036) (72,221) 4,291 1,919 – – – – (194,047) 3,073 (190,974)Total comprehensive income (loss) – – (128,036) (72,221) 4,291 1,919 – – 6,164,735 – 5,970,688 (108,153) 5,862,535Movements in other equity accounts:

Issuances of and subscriptions to capital stock (Note 19) 5,152 363,468 – – – – – – – – 368,620 – 368,620Cost of stock options granted (Note 26) – 241,324 – – – – – – – – 241,324 – 241,324Cash dividends (Note 19) – – – – – – – – (1,992,243) – (1,992,243) – (1,992,243)Acquisition of minority interests (Note 11) – – – – – – (1,609,397) – – (1,609,397) (905,536) (2,514,933)Appropriation during the period (Note 19) – – – – – – – 8,000,000 (8,000,000) – – – –Arising from incorporation of a subsidiary (Note 11) – – – – – – – – – – – 715,608 715,608Arising from divestment of subsidiaries (Note 11) – – – – – – – – – – – (156,097) (156,097)

5,152 604,792 – – – – (1,609,397) 8,000,000 (9,992,243) – (2,991,696) (346,025) (3,337,721)Balances at December 31, 2016 P=1,074,123 P=5,660,085 (P=20,811) (P=608,801) P=4,291 (P=33,530) (P=2,152,161) P=18,200,000 P=11,659,531 (P=180,511) P=33,602,216 P=679,188 P=34,281,404

*SGVFS034434*

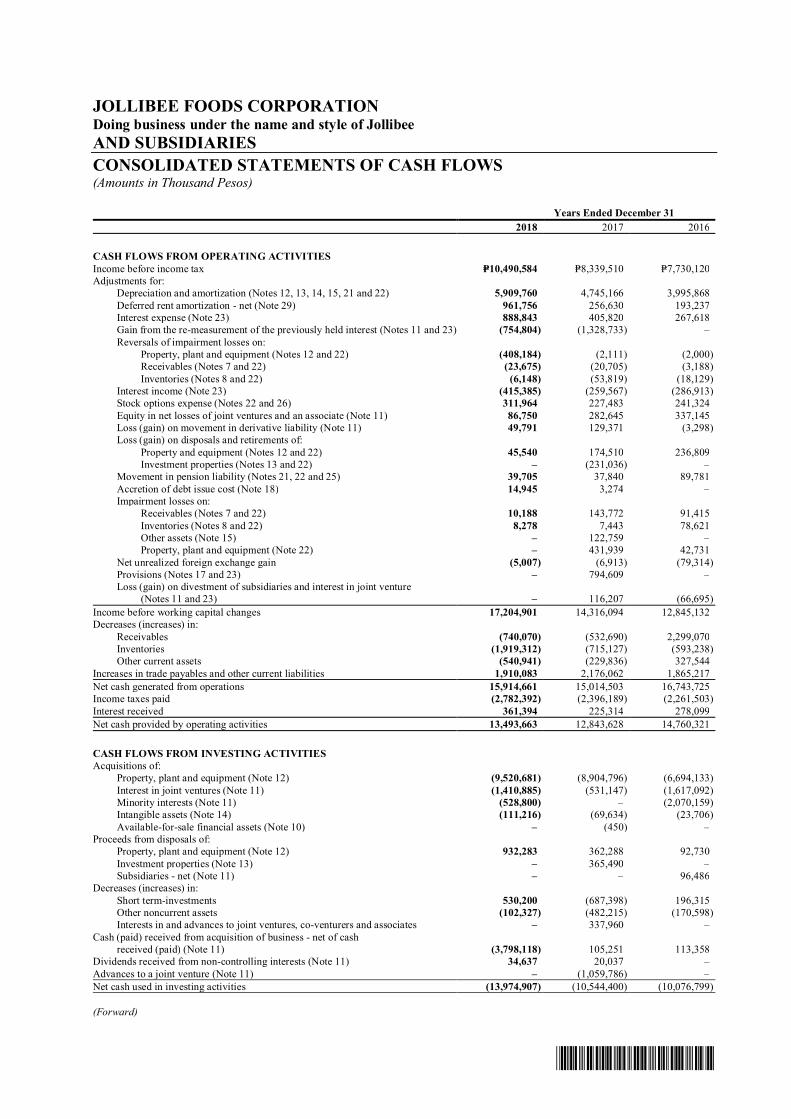

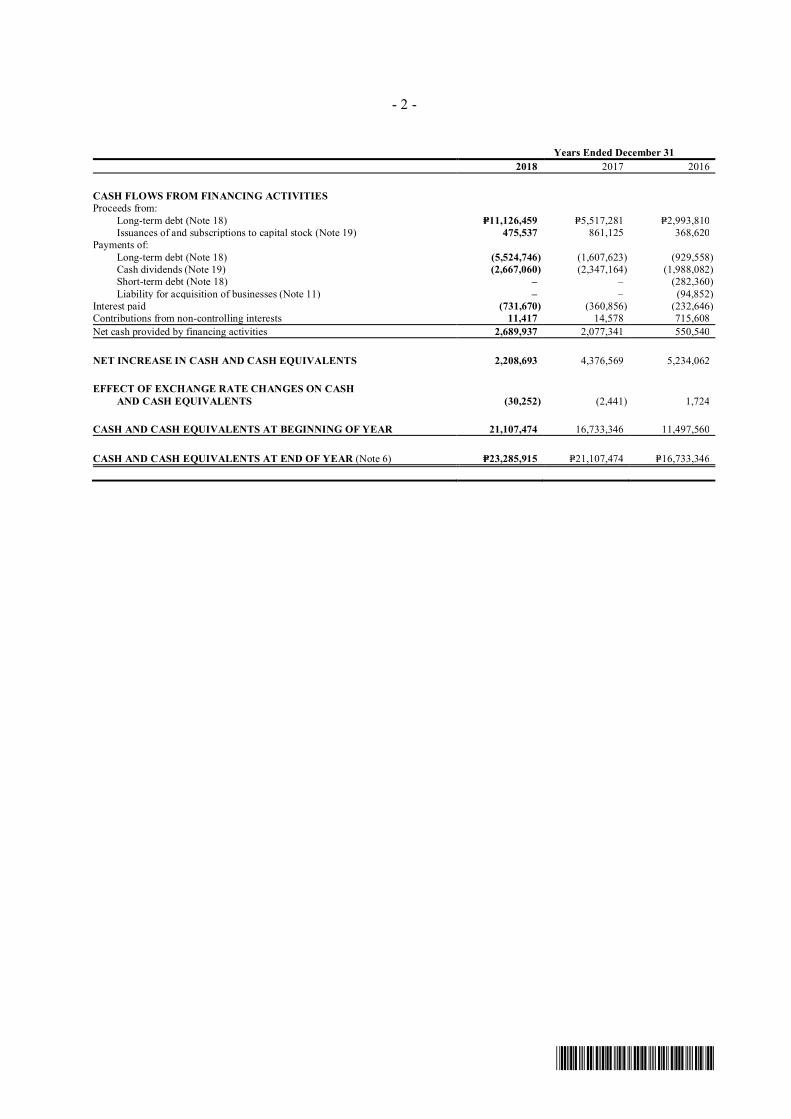

JOLLIBEE FOODS CORPORATIONDoing business under the name and style of JollibeeAND SUBSIDIARIESCONSOLIDATED STATEMENTS OF CASH FLOWS(Amounts in Thousand Pesos)

Years Ended December 312018 2017 2016

CASH FLOWS FROM OPERATING ACTIVITIESIncome before income tax P=10,490,584 P=8,339,510 P=7,730,120Adjustments for:

Depreciation and amortization (Notes 12, 13, 14, 15, 21 and 22) 5,909,760 4,745,166 3,995,868Deferred rent amortization - net (Note 29) 961,756 256,630 193,237Interest expense (Note 23) 888,843 405,820 267,618Gain from the re-measurement of the previously held interest (Notes 11 and 23) (754,804) (1,328,733) –Reversals of impairment losses on:

Property, plant and equipment (Notes 12 and 22) (408,184) (2,111) (2,000)Receivables (Notes 7 and 22) (23,675) (20,705) (3,188)Inventories (Notes 8 and 22) (6,148) (53,819) (18,129)

Interest income (Note 23) (415,385) (259,567) (286,913)Stock options expense (Notes 22 and 26) 311,964 227,483 241,324Equity in net losses of joint ventures and an associate (Note 11) 86,750 282,645 337,145Loss (gain) on movement in derivative liability (Note 11) 49,791 129,371 (3,298)Loss (gain) on disposals and retirements of:

Property and equipment (Notes 12 and 22) 45,540 174,510 236,809Investment properties (Notes 13 and 22) – (231,036) –

Movement in pension liability (Notes 21, 22 and 25) 39,705 37,840 89,781Accretion of debt issue cost (Note 18) 14,945 3,274 –Impairment losses on:

Receivables (Notes 7 and 22) 10,188 143,772 91,415Inventories (Notes 8 and 22) 8,278 7,443 78,621Other assets (Note 15) – 122,759 –Property, plant and equipment (Note 22) – 431,939 42,731

Net unrealized foreign exchange gain (5,007) (6,913) (79,314)Provisions (Notes 17 and 23) – 794,609 –Loss (gain) on divestment of subsidiaries and interest in joint venture

(Notes 11 and 23) – 116,207 (66,695)Income before working capital changes 17,204,901 14,316,094 12,845,132Decreases (increases) in:

Receivables (740,070) (532,690) 2,299,070Inventories (1,919,312) (715,127) (593,238)Other current assets (540,941) (229,836) 327,544

Increases in trade payables and other current liabilities 1,910,083 2,176,062 1,865,217Net cash generated from operations 15,914,661 15,014,503 16,743,725Income taxes paid (2,782,392) (2,396,189) (2,261,503)Interest received 361,394 225,314 278,099Net cash provided by operating activities 13,493,663 12,843,628 14,760,321

CASH FLOWS FROM INVESTING ACTIVITIESAcquisitions of:

Property, plant and equipment (Note 12) (9,520,681) (8,904,796) (6,694,133)Interest in joint ventures (Note 11) (1,410,885) (531,147) (1,617,092)Minority interests (Note 11) (528,800) – (2,070,159)Intangible assets (Note 14) (111,216) (69,634) (23,706)Available-for-sale financial assets (Note 10) – (450) –

Proceeds from disposals of:Property, plant and equipment (Note 12) 932,283 362,288 92,730Investment properties (Note 13) – 365,490 –Subsidiaries - net (Note 11) – – 96,486

Decreases (increases) in:Short term-investments 530,200 (687,398) 196,315Other noncurrent assets (102,327) (482,215) (170,598)Interests in and advances to joint ventures, co-venturers and associates – 337,960 –

Cash (paid) received from acquisition of business - net of cashreceived (paid) (Note 11) (3,798,118) 105,251 113,358

Dividends received from non-controlling interests (Note 11) 34,637 20,037 –Advances to a joint venture (Note 11) – (1,059,786) –Net cash used in investing activities (13,974,907) (10,544,400) (10,076,799)

(Forward)

*SGVFS034434*

- 2 -

Years Ended December 312018 2017 2016

CASH FLOWS FROM FINANCING ACTIVITIESProceeds from:

Long-term debt (Note 18) P=11,126,459 P=5,517,281 P=2,993,810Issuances of and subscriptions to capital stock (Note 19) 475,537 861,125 368,620

Payments of:Long-term debt (Note 18) (5,524,746) (1,607,623) (929,558)Cash dividends (Note 19) (2,667,060) (2,347,164) (1,988,082)Short-term debt (Note 18) – – (282,360)Liability for acquisition of businesses (Note 11) – – (94,852)

Interest paid (731,670) (360,856) (232,646)Contributions from non-controlling interests 11,417 14,578 715,608Net cash provided by financing activities 2,689,937 2,077,341 550,540

NET INCREASE IN CASH AND CASH EQUIVALENTS 2,208,693 4,376,569 5,234,062

EFFECT OF EXCHANGE RATE CHANGES ON CASHAND CASH EQUIVALENTS (30,252) (2,441) 1,724

CASH AND CASH EQUIVALENTS AT BEGINNING OF YEAR 21,107,474 16,733,346 11,497,560

CASH AND CASH EQUIVALENTS AT END OF YEAR (Note 6) P=23,285,915 P=21,107,474 P=16,733,346

*SGVFS034434*

JOLLIBEE FOODS CORPORATIONDoing business under the name and style of JollibeeAND SUBSIDIARIESNOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. Corporate Information

Jollibee Foods Corporation Doing business under the name and style of Jollibee (formerlyJollibee Foods Corporation) was incorporated in the Philippines and registered with the PhilippineSecurities and Exchange Commission (SEC) on January 11, 1978. The Parent Company and itssubsidiaries (collectively referred to as “the Jollibee Group”) and affiliates are involved primarily inthe development, operations and franchising of quick service restaurants (QSRs) under the tradenames “Jollibee”, “Chowking”, “Greenwich”, “Red Ribbon”, “Yong He King”, “Hong ZhuangYuan”, “Mang Inasal”, “Burger King”, “Highlands Coffee”, “Pho24”, “Hard Rock Cafe”, “Dunkin’Donuts”, “Smashburger”, “Tim Ho Wan” and “Tortas Frontera”. The other activities of the JollibeeGroup include manufacturing and property leasing in support of the quick service restaurant systemsand other business activities (see Notes 2 and 5). The corporate life of the Parent Company is fifty(50) years from the date of incorporation or until 2028.

The common shares of the Parent Company are listed and traded in the Philippine Stock Exchange(PSE) beginning July 14, 1993.

The registered office address of the Parent Company is 10/F Jollibee Plaza Building, 10 F. Ortigas Jr.Ave., Ortigas Center, Pasig City.

The consolidated financial statements as at December 31, 2018 and 2017 and for each of the threeyears in the period ended December 31, 2018 were reviewed and recommended for approval by theAudit Committee as well as approved and authorized for issuance by the Board of Directors (BOD)on April 8, 2019.

2. Basis of Preparation, Statement of Compliance, Changes in Accounting Policies and Basis ofConsolidation

Basis of PreparationThe consolidated financial statements of the Jollibee Group have been prepared on a historical costbasis, except for financial assets at fair value through profit or loss (FVTPL) and derivative financialinstruments in 2018 and available-for-sale (AFS) investments and derivative financial instruments in2017, which are measured at fair value. The consolidated financial statements are presented inPhilippine peso, which is the Parent Company’s functional and presentation currency. All values arerounded to the nearest thousand pesos, except par values, per share amounts, number of shares andwhen otherwise indicated.

Statement of ComplianceThe accompanying consolidated financial statements have been prepared in compliance withPhilippine Financial Reporting Standards (PFRS).

Changes in Accounting PoliciesThe accounting policies adopted are consistent with those of the previous financial year, except forthe adoption of the following new accounting pronouncements starting January 1, 2018. Adoption ofthese pronouncements did not have any significant impact on the consolidated statement of financialposition and performance unless otherwise indicated.

- 2 -

*SGVFS034434*

ƒ Amendments to PFRS 2, Share-based Payment, Classification and Measurement of Share-basedPayment Transactions

The amendments to PFRS 2 address three main areas: the effects of vesting conditions on themeasurement of a cash-settled share-based payment transaction; the classification of a share-based payment transaction with net settlement features for withholding tax obligations; and theaccounting where a modification to the terms and conditions of a share-based paymenttransaction changes its classification from cash-settled to equity-settled. Entities are required toapply the amendments to: (1) share-based payment transactions that are unvested or vested butunexercised as at January 1, 2018, (2) share-based payment transactions granted on or afterJanuary 1, 2018 and to (3) modifications of share-based payments that occurred on or afterJanuary 1, 2018. Retrospective application is permitted if elected for all three amendments and ifit is possible to do so without hindsight.

The Jollibee Group’s accounting policy for cash-settled share-based payments is consistent withthe approach clarified in the amendments. In addition, the Jollibee Group has no share-basedpayment transaction with net settlement features for withholding tax obligations and had notmade any modifications to the terms and conditions of its share-based payment transaction.Therefore, these amendments do not have any impact on the Jollibee Group’s consolidatedfinancial statements.

ƒ PFRS 9, Financial Instruments

PFRS 9, replaces Philippine Accounting Standards (PAS) 39, Financial Instruments: Recognitionand Measurement, for annual periods beginning on or January 1, 2018, bringing together all theseaspects of the accounting for financial instruments: classification and measurement; impairment;and hedge accounting.

The Jollibee Group applied PFRS 9 using modified retrospective approach, with an initialapplication date of January 1, 2018. The Jollibee Group has not restated the comparativeinformation, which continues to be reported under PAS 39. Differences arising from the adoptionof PFRS 9 have been recognized directly in retained earnings and net unrealized gain on AFSfinancial assets.

The effect of adopting PFRS 9 follows:

(a) Classification and Measurement

Under PFRS 9, debt instruments are subsequently measured at FVTPL, amortized cost, or fairvalue through other comprehensive income (FVOCI). The classification is based on two criteria:the Jollibee Group’s business model for managing the assets; and whether the instruments’contractual cash flows represent ‘solely payments of principal and interest’ on the principalamount outstanding.

The assessment of the Jollibee Group’s business model was made as of the date of initialapplication, January 1, 2018, and then applied prospectively to those financial assets that were notderecognized before January 1, 2018. The assessment of whether contractual cash flows on debtinstruments are solely comprised of principal and interest was made based on the facts andcircumstances as at the initial recognition of the assets.

- 3 -

*SGVFS034434*

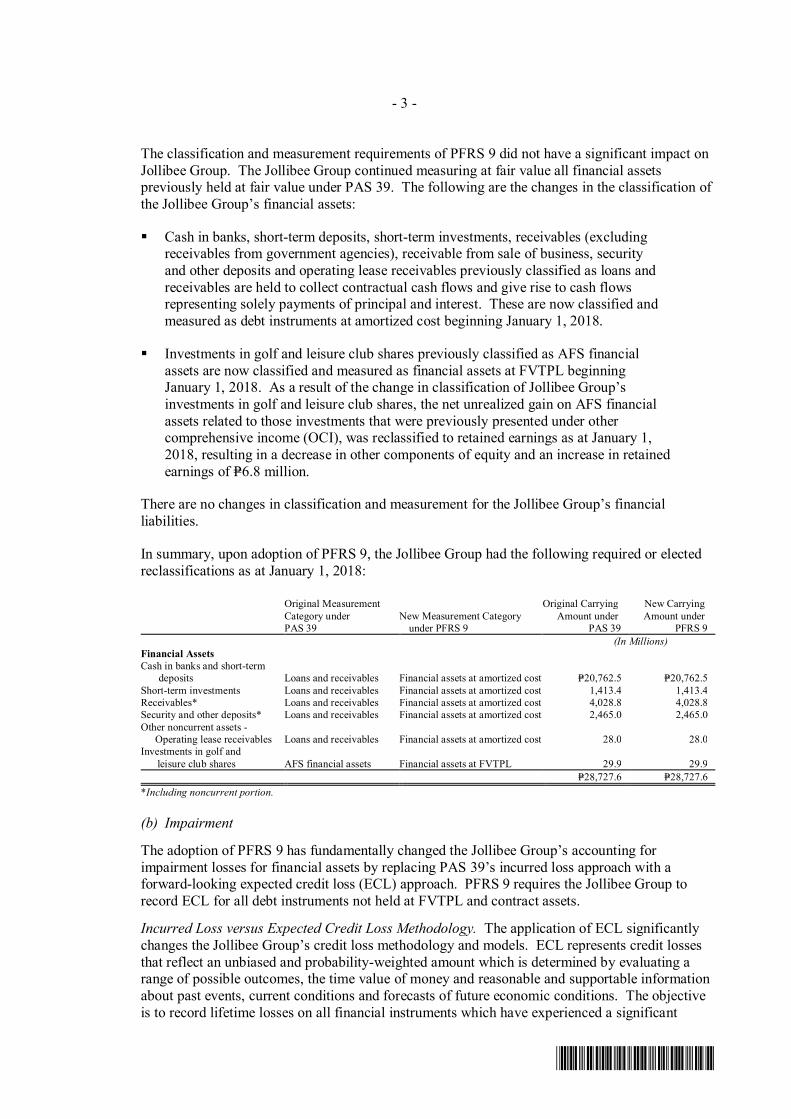

The classification and measurement requirements of PFRS 9 did not have a significant impact onJollibee Group. The Jollibee Group continued measuring at fair value all financial assetspreviously held at fair value under PAS 39. The following are the changes in the classification ofthe Jollibee Group’s financial assets:

ƒ Cash in banks, short-term deposits, short-term investments, receivables (excludingreceivables from government agencies), receivable from sale of business, securityand other deposits and operating lease receivables previously classified as loans andreceivables are held to collect contractual cash flows and give rise to cash flowsrepresenting solely payments of principal and interest. These are now classified andmeasured as debt instruments at amortized cost beginning January 1, 2018.

ƒ Investments in golf and leisure club shares previously classified as AFS financialassets are now classified and measured as financial assets at FVTPL beginningJanuary 1, 2018. As a result of the change in classification of Jollibee Group’sinvestments in golf and leisure club shares, the net unrealized gain on AFS financialassets related to those investments that were previously presented under othercomprehensive income (OCI), was reclassified to retained earnings as at January 1,2018, resulting in a decrease in other components of equity and an increase in retainedearnings of P=6.8 million.

There are no changes in classification and measurement for the Jollibee Group’s financialliabilities.

In summary, upon adoption of PFRS 9, the Jollibee Group had the following required or electedreclassifications as at January 1, 2018:

Original MeasurementCategory underPAS 39

New Measurement Categoryunder PFRS 9

Original CarryingAmount under

PAS 39

New CarryingAmount under

PFRS 9(In Millions)

Financial AssetsCash in banks and short-term

deposits Loans and receivables Financial assets at amortized cost P=20,762.5 P=20,762.5Short-term investments Loans and receivables Financial assets at amortized cost 1,413.4 1,413.4Receivables* Loans and receivables Financial assets at amortized cost 4,028.8 4,028.8Security and other deposits* Loans and receivables Financial assets at amortized cost 2,465.0 2,465.0Other noncurrent assets -

Operating lease receivables Loans and receivables Financial assets at amortized cost 28.0 28.0Investments in golf and

leisure club shares AFS financial assets Financial assets at FVTPL 29.9 29.9P=28,727.6 P=28,727.6

*Including noncurrent portion.

(b) Impairment

The adoption of PFRS 9 has fundamentally changed the Jollibee Group’s accounting forimpairment losses for financial assets by replacing PAS 39’s incurred loss approach with aforward-looking expected credit loss (ECL) approach. PFRS 9 requires the Jollibee Group torecord ECL for all debt instruments not held at FVTPL and contract assets.

Incurred Loss versus Expected Credit Loss Methodology. The application of ECL significantlychanges the Jollibee Group’s credit loss methodology and models. ECL represents credit lossesthat reflect an unbiased and probability-weighted amount which is determined by evaluating arange of possible outcomes, the time value of money and reasonable and supportable informationabout past events, current conditions and forecasts of future economic conditions. The objectiveis to record lifetime losses on all financial instruments which have experienced a significant

- 4 -

*SGVFS034434*

increase in credit risk (SICR) since their initial recognition. As a result, ECL allowances aremeasured at amounts equal to either (i) 12-month ECL or (ii) lifetime ECL for those financialinstruments which have experienced a SICR since initial recognition (General Approach). The12-month ECL is the portion of lifetime ECL that results from default events over the expectedlife of a financial instrument. In comparison, the previous incurred loss model recognizeslifetime credit losses only when there is objective evidence of impairment while ECL modeleliminated the threshold or trigger event required under incurred loss model, and lifetime ECL arerecognized earlier.

Staging Assessment

For non-credit-impaired financial instruments:∂ Stage 1 is comprised of all non-impaired financial instruments which have not experienced a

SICR since initial recognition. The Jollibee Group recognizes a 12-month ECL for Stage 1financial instruments.

∂ Stage 2 is comprised of all non-impaired financial instruments which have experienced aSICR since initial recognition. The Jollibee Group recognizes a lifetime ECL for Stage 2financial instruments.

For credit-impaired financial instruments:

Financial instruments are classified as Stage 3 when there is objective evidence of impairment asa result of one or more loss events that have occurred after initial recognition with a negativeimpact on the estimated future cash flows of a loan or a portfolio of loans. The ECL modelrequires a lifetime ECL for impaired financial instruments.

For cash in banks, short-term deposits, short-term investments, and security and other deposits,the Jollibee Group has applied the General Approach and has calculated ECL based on 12-monthECL. For receivables and contract assets, and operating lease receivables, the Jollibee Groupapplied the simplified approach permitted by PFRS 9, which requires lifetime ECL to berecognized from initial recognition of the receivables. As at January 1, 2018, the Jollibee Groupassessed that there was no SICR related to its financial assets at amortized cost.

The adoption of ECL approach has no significant impact on the allowance for impairment lossesrecognized in the consolidated financial statements.

ƒ Amendments to PFRS 4, Applying PFRS 9 with PFRS 4, Insurance Contracts

The amendments address concerns arising from implementing PFRS 9, the new financialinstruments standard before implementing the new insurance contracts standard.The amendments introduce two options for entities issuing insurance contracts: a temporaryexemption from applying PFRS 9 and an overlay approach. The temporary exemption is firstapplied for reporting periods beginning on or after January 1, 2018. An entity may elect theoverlay approach when it first applies PFRS 9 and apply that approach retrospectively to financialassets designated on transition to PFRS 9. The entity restates comparative information reflectingthe overlay approach if, and only if, the entity restates comparative information when applyingPFRS 9.

The amendments are not applicable to the Jollibee Group since none of the entities within theJollibee Group have activities that are predominantly connected with insurance or issue insurancecontracts.

- 5 -

*SGVFS034434*

ƒ PFRS 15, Revenue from Contracts with Customers

PFRS 15 supersedes PAS 11, Construction Contracts, PAS 18, Revenue, and relatedinterpretations and it applies, with limited exceptions, to all revenue arising from contracts withits customers. PFRS 15 establishes a five-step model to account for revenue arising fromcontracts with customers and requires that revenue be recognized at an amount that reflects theconsideration to which an entity expects to be entitled in exchange for transferring goods orservices to a customer.

PFRS 15 requires entities to exercise judgment, taking into consideration all of the relevant factsand circumstances when applying each step of the model to contracts with their customers.The standard also specifies the accounting for the incremental costs of obtaining a contract andthe costs directly related to fulfilling a contract. In addition, the standard requires extensivedisclosures.

The Jollibee Group adopted PFRS 15 using the full retrospective method of adoption. The effectof the transition on the current period has not been disclosed as the standard provides an optionalpractical expedient. The Jollibee Group did not apply any of the other available optional practicalexpedients.

The adoption of PFRS 15 did not have a material impact to the consolidated statement offinancial position, consolidated statement of changes in equity, on OCI or the Jollibee Group’soperating, investing and financing cash flows.

The effect of adopting PFRS 15 on the consolidated statements of comprehensive income for theyears ended December 31, 2017 and 2016 resulted to an increase in:

2017 2016(in Millions)

REVENUE FROM CONTRACTS WITH CUSTOMERSRevenue from contracts with customers P=2,036.5 P=1,802.1

DIRECT COSTSShare on system-wide advertising fees 2,036.5 1,802.1

NET INCOME P=– P=–

The reason for the above changes in the consolidated statement of comprehensive income for theyears ended December 31, 2017 and 2016 is described below:

ƒ Principal versus Agent Consideration. The Jollibee Group’s agreement with the franchiseeincludes the right to charge the franchisee its share in the Jollibee Group’s nationwideadvertising and marketing efforts as well as fees for the Jollibee Group’s administration ofvarious advertisements, network and media placements. Upon adoption of PFRS 15, theJollibee Group determined that it is acting as principal for the nationwide advertising becauseit is the Jollibee Group who retains the right to direct the service provider of theadvertisements, network and media placements, and has the discretion on how to price theadvertising fee charges.

Before the adoption of PFRS 15, contract asset is not presented separately from receivables whilecontract liabilities are presented as other liabilities. Under PFRS 15, the timing of revenuerecognition, schedule of payment and cash collections results in billed accounts receivable (tradereceivables), accrued receivables (contract assets) and deferred revenue and unearned revenuefrom gift certificates (contract liabilities). Upon adoption of PFRS 15, the Jollibee Group

- 6 -

*SGVFS034434*

reclassified “Trade receivables” to “Contract assets” amounting to P=407.4 million and “Otherliabilities” to “Contract liabilities” amounting to P=2.7 million as at December 31, 2017.

ƒ Amendments to PAS 28, Investments in Associates and Joint Ventures, Measuring an Associateor Joint Venture at Fair Value (Part of Annual Improvements to PFRSs 2014 - 2016 Cycle)

The amendments clarify that an entity that is a venture capital organization, or other qualifyingentity, may elect, at initial recognition on an investment-by-investment basis, to measure itsinvestments in associates and joint ventures at fair value through profit or loss. They also clarifythat if an entity that is not itself an investment entity has an interest in an associate or jointventure that is an investment entity, the entity may, when applying the equity method, elect toretain the fair value measurement applied by that investment entity associate or joint venture tothe investment entity associate’s or joint venture’s interests in subsidiaries. This election is madeseparately for each investment entity associate or joint venture, at the later of the date on which(a) the investment entity associate or joint venture is initially recognized; (b) the associate or jointventure becomes an investment entity; and (c) the investment entity associate or joint venture firstbecomes a parent. Retrospective application is required. The Jollibee Group elected to retain thefair value measurement applied by the investment entity joint venture in accounting for itsinvestment.

ƒ Amendments to PAS 40, Investment Property, Transfers of Investment Property

The amendments clarify when an entity should transfer property, including property underconstruction or development into, or out of investment property. The amendments state that achange in use occurs when the property meets, or ceases to meet, the definition of investmentproperty and there is evidence of the change in use. A mere change in management’s intentionsfor the use of a property does not provide evidence of a change in use. Retrospective applicationof the amendments is not required and is only permitted if this is possible without the use ofhindsight.

Since the Jollibee Group’s current practice is in line with the clarifications issued, the JollibeeGroup does not expect any effect on its consolidated financial statements upon adoption of theseamendments.

ƒ Philippine Interpretation International Financial Reporting Interpretations Committee (IFRIC)-22,Foreign Currency Transactions and Advance Consideration

The interpretation clarifies that, in determining the spot exchange rate to use on initial recognitionof the related asset, expense or income (or part of it) on the derecognition of a non-monetary assetor non-monetary liability relating to advance consideration, the date of the transaction is the dateon which an entity initially recognizes the nonmonetary asset or non-monetary liability arisingfrom the advance consideration. If there are multiple payments or receipts in advance, then theentity must determine the date of the transaction for each payment or receipt of advanceconsideration. Retrospective application of this interpretation is not required.

Since the Jollibee Group’s current practice is in line with the clarifications issued, the JollibeeGroup does not expect any effect on its consolidated financial statements upon adoption of thisinterpretation.

- 7 -

*SGVFS034434*

Future Changes in Accounting PoliciesPronouncements issued but not yet effective are listed below. Unless otherwise indicated, the JollibeeGroup does not expect that the future adoption of the said pronouncements will have a significantimpact on its consolidated financial statements. The Jollibee Group intends to adopt the followingpronouncements when these become effective.

Effective beginning on or after January 1, 2019

ƒ Amendments to PFRS 9, Prepayment Features with Negative Compensation

Under PFRS 9, a debt instrument can be measured at amortized cost or at fair value through othercomprehensive income, provided that the contractual cash flows are ‘solely payments of principaland interest on the principal amount outstanding’ (the SPPI criterion) and the instrument is heldwithin the appropriate business model for that classification. The amendments to PFRS 9 clarifythat a financial asset passes the SPPI criterion regardless of the event or circumstance that causesthe early termination of the contract and irrespective of which party pays or receives reasonablecompensation for the early termination of the contract. The amendments should be appliedretrospectively and are effective from January 1, 2019, with earlier application permitted.

The Jollibee Group has assessed that the adoption of these amendments will not have any impacton the consolidated financial statements.

ƒ PFRS 16, Leases

PFRS 16 sets out the principles for the recognition, measurement, presentation and disclosure ofleases and requires lessees to account for all leases under a single on-balance sheet model similarto the accounting for finance leases under PAS 17, Leases. The standard includes tworecognition exemptions for lessees – leases of ’low-value’ assets (e.g., personal computers) andshort-term leases (i.e., leases with a lease term of 12 months or less). At the commencement dateof a lease, a lessee will recognize a liability to make lease payments (i.e., the lease liability) andan asset representing the right to use the underlying asset during the lease term (i.e., the right-of-use asset). Lessees will be required to separately recognize the interest expense on the leaseliability and the depreciation expense on the right-of-use asset.

Lessees will be also required to remeasure the lease liability upon the occurrence of certain events(e.g., a change in the lease term, a change in future lease payments resulting from a change in anindex or rate used to determine those payments). The lessee will generally recognize the amountof the remeasurement of the lease liability as an adjustment to the right-of-use asset.

Lessor accounting under PFRS 16 is substantially unchanged from today’s accounting underPAS 17. Lessors will continue to classify all leases using the same classification principle as inPAS 17 and distinguish between two types of leases: operating and finance leases.

PFRS 16 also requires lessees and lessors to make more extensive disclosures than under PAS 17.

A lessee can choose to apply the standard using either a full retrospective or a modifiedretrospective approach. The standard’s transition provisions permit certain reliefs.

The Jollibee Group is currently assessing the impact of adopting PFRS 16.

- 8 -

*SGVFS034434*

ƒ Amendments to PAS 19, Employee Benefits, Plan Amendment, Curtailment or Settlement

The amendments to PAS 19 address the accounting when a plan amendment, curtailment orsettlement occurs during a reporting period. The amendments specify that when a planamendment, curtailment or settlement occurs during the annual reporting period, an entity isrequired to:

ƒ Determine current service cost for the remainder of the period after the plan amendment,curtailment or settlement, using the actuarial assumptions used to remeasure the net definedbenefit liability (asset) reflecting the benefits offered under the plan and the plan assets afterthat event.

ƒ Determine net interest for the remainder of the period after the plan amendment, curtailmentor settlement using: the net defined benefit liability (asset) reflecting the benefits offeredunder the plan and the plan assets after that event; and the discount rate used to remeasurethat net defined benefit liability (asset).

The amendments also clarify that an entity first determines any past service cost, or a gain or losson settlement, without considering the effect of the asset ceiling. This amount is recognized inprofit or loss. An entity then determines the effect of the asset ceiling after the plan amendment,curtailment or settlement. Any change in that effect, excluding amounts included in the netinterest, is recognized in other comprehensive income.

The amendments apply to plan amendments, curtailments, or settlements occurring on or after thebeginning of the first annual reporting period that begins on or after January 1, 2019, with earlyapplication permitted. These amendments will apply only to any future plan amendments,curtailments, or settlements of the Jollibee Group.

ƒ Amendments to PAS 28, Long-term Interests in Associates and Joint Ventures

The amendments clarify that an entity applies PFRS 9 to long-term interests in an associate orjoint venture to which the equity method is not applied but that, in substance, form part of the netinvestment in the associate or joint venture (long-term interests). This clarification is relevantbecause it implies that the expected credit loss model in PFRS 9 applies to such long-terminterests.

The amendments also clarified that, in applying PFRS 9, an entity does not take account of anylosses of the associate or joint venture, or any impairment losses on the net investment,recognized as adjustments to the net investment in the associate or joint venture that arise fromapplying PAS 28.

The amendments should be applied retrospectively and are effective from January 1, 2019, withearly application permitted. Since the Jollibee Group does not have such long-term interests in itsassociate and joint venture, the amendments will not have an impact on its consolidated financialstatements.

ƒ Philippine Interpretation IFRIC-23, Uncertainty over Income Tax Treatments

The interpretation addresses the accounting for income taxes when tax treatments involveuncertainty that affects the application of PAS 12, Income Taxes, and does not apply to taxes orlevies outside the scope of PAS 12, nor does it specifically include requirements relating tointerest and penalties associated with uncertain tax treatments.

- 9 -

*SGVFS034434*

The interpretation specifically addresses the following:

ƒ Whether an entity considers uncertain tax treatments separatelyƒ The assumptions an entity makes about the examination of tax treatments by taxation

authoritiesƒ How an entity determines taxable profit (tax loss), tax bases, unused tax losses, unused tax

credits and tax ratesƒ How an entity considers changes in facts and circumstances

An entity must determine whether to consider each uncertain tax treatment separately or togetherwith one or more other uncertain tax treatments. The approach that better predicts the resolutionof the uncertainty should be followed. The Jollibee Group is currently assessing the impact ofadopting this interpretation.

ƒ Annual Improvements to PFRSs 2015-2017 Cycle

ƒ Amendments to PFRS 3, Business Combinations, and PFRS 11, Joint Arrangements,Previously Held Interest in a Joint Operation

The amendments clarify that, when an entity obtains control of a business that is a jointoperation, it applies the requirements for a business combination achieved in stages,including remeasuring previously held interests in the assets and liabilities of the jointoperation at fair value. In doing so, the acquirer remeasures its entire previously held interestin the joint operation.

A party that participates in, but does not have joint control of, a joint operation might obtainjoint control of the joint operation in which the activity of the joint operation constitutes abusiness as defined in PFRS 3. The amendments clarify that the previously held interests inthat joint operation are not remeasured.

An entity applies those amendments to business combinations for which the acquisition dateis on or after the beginning of the first annual reporting period beginning on or afterJanuary 1, 2019 and to transactions in which it obtains joint control on or after the beginningof the first annual reporting period beginning on or after January 1, 2019, with earlyapplication permitted. These amendments are currently not applicable to the Jollibee Groupbut may apply to future transactions.

ƒ Amendments to PAS 12, Income Tax Consequences of Payments on Financial InstrumentsClassified as Equity

The amendments clarify that the income tax consequences of dividends are linked moredirectly to past transactions or events that generated distributable profits than to distributionsto owners. Therefore, an entity recognizes the income tax consequences of dividends inprofit or loss, other comprehensive income or equity according to where the entity originallyrecognized those past transactions or events.

An entity applies those amendments for annual reporting periods beginning on or afterJanuary 1, 2019, with early application is permitted. These amendments are not expected tohave significant impact to the Jollibee Group.

- 10 -

*SGVFS034434*

ƒ Amendments to PAS 23, Borrowing Costs, Borrowing Costs Eligible for Capitalization

The amendments clarify that an entity treats as part of general borrowings any borrowingoriginally made to develop a qualifying asset when substantially all of the activities necessaryto prepare that asset for its intended use or sale are complete.

An entity applies those amendments to borrowing costs incurred on or after the beginning ofthe annual reporting period in which the entity first applies those amendments. An entityapplies those amendments for annual reporting periods beginning on or after January 1, 2019,with early application permitted.

Since the Jollibee Group’s current practice is in line with these amendments, theJollibee Group does not expect any effect on its consolidated financial statements uponadoption.

Effective beginning on or after January 1, 2020

ƒ Amendments to PFRS 3, Definition of a Business

The amendments to PFRS 3 clarify the minimum requirements to be a business, remove theassessment of a market participant’s ability to replace missing elements, and narrow thedefinition of outputs. The amendments also add guidance to assess whether an acquired processis substantive and add illustrative examples. An optional fair value concentration test isintroduced which permits a simplified assessment of whether an acquired set of activities andassets is not a business.

An entity applies those amendments prospectively for annual reporting periods beginning on orafter January 1, 2020, with earlier application permitted.

These amendments will apply on future business combinations of the Jollibee Group.

ƒ Amendments to PAS 1, Presentation of Financial Statements, and PAS 8, Accounting Policies,Changes in Accounting Estimates and Errors, Definition of Material

The amendments refine the definition of material in PAS 1 and align the definitions used acrossPFRSs and other pronouncements. They are intended to improve the understanding of theexisting requirements rather than to significantly impact an entity’s materiality judgements.

An entity applies those amendments prospectively for annual reporting periods beginning on orafter January 1, 2020, with earlier application permitted. The Jollibee Group is currentlyassessing the impact of these amendments.

Effective beginning on or after January 1, 2021

ƒ PFRS 17, Insurance Contracts

PFRS 17 is a comprehensive new accounting standard for insurance contracts coveringrecognition and measurement, presentation and disclosure. Once effective, PFRS 17 will replacePFRS 4. This new standard on insurance contracts applies to all types of insurance contracts (i.e.,life, non-life, direct insurance and re-insurance), regardless of the type of entities that issue them,as well as to certain guarantees and financial instruments with discretionary participation features.A few scope exceptions will apply.

- 11 -

*SGVFS034434*

The overall objective of PFRS 17 is to provide an accounting model for insurance contracts thatis more useful and consistent for insurers. In contrast to the requirements in PFRS 4, which arelargely based on grandfathering previous local accounting policies, PFRS 17 provides acomprehensive model for insurance contracts, covering all relevant accounting aspects. The coreof PFRS 17 is the general model, supplemented by:

ƒ A specific adaptation for contracts with direct participation features (the variable feeapproach)

ƒ A simplified approach (the premium allocation approach) mainly for short-duration contracts

PFRS 17 is effective for reporting periods beginning on or after January 1, 2021, withcomparative figures required. Early application is permitted. Adoption of this standard is notexpected to have any impact to the Jollibee Group.

Deferred Effectivity

ƒ Amendments to PFRS 10 and PAS 28, Sale or Contribution of Assets between an Investor and itsAssociate or Joint Venture

The amendments address the conflict between PFRS 10 and PAS 28 in dealing with the loss ofcontrol of a subsidiary that is sold or contributed to an associate or joint venture. Theamendments clarify that a full gain or loss is recognized when a transfer to an associate or jointventure involves a business as defined in PFRS 3. Any gain or loss resulting from the sale orcontribution of assets that does not constitute a business, however, is recognized only to theextent of unrelated investors’ interests in the associate or joint venture.

On January 13, 2016, the Financial Reporting Standards Council postponed the original effectivedate of January 1, 2016 of the said amendments until the International Accounting StandardsBoard has completed its broader review of the research project on equity accounting that mayresult in the simplification of accounting for such transactions and of other aspects of accountingfor associates and joint ventures.

Basis of ConsolidationThe consolidated financial statements comprise the financial statements of the Parent Company andits subsidiaries as at December 31, 2018 and for each of the three years in the period endedDecember 31, 2018.

Control is achieved when the Jollibee Group is exposed, or has rights, to variable returns from itsinvolvement with the investee and has the ability to affect those returns through its power over theinvestee. Specifically, the Jollibee Group controls an investee if, and only if, the Jollibee Group has:

ƒ Power over the investee (i.e., existing rights that give it the current ability to direct the relevantactivities of the investee);

ƒ Exposure, or rights, to variable returns from its involvement with the investee;ƒ The ability to use its power over the investee to affect its returns.

- 12 -

*SGVFS034434*

There is a general presumption that a majority of voting rights results in control. To support thispresumption when the Jollibee Group has less than a majority of the voting or similar rights of aninvestee, the Jollibee Group considers all relevant facts and circumstances in assessing whether it haspower over an investee, including:

ƒ The contractual arrangement with the other vote holders of the investee.ƒ Rights arising from other contractual arrangements.ƒ The Jollibee Group’s voting rights and potential voting rights.

The Jollibee Group re-assesses whether or not it controls an investee if facts and circumstancesindicate that there are changes to one or more of the three elements of control. Consolidation of asubsidiary begins when the Jollibee Group obtains control over the subsidiary and ceases when theJollibee Group loses control of the subsidiary. Assets, liabilities, income and expenses of a subsidiaryacquired or disposed of during the year are included in the consolidated financial statements from thedate the Jollibee Group gains control until the date the Jollibee Group ceases to control the subsidiary.

Profit or loss and each component of OCI are attributed to the equity holders of the Parent Companyand to the non-controlling interests, even if this results in the non-controlling interests having a deficitbalance. When necessary, adjustments are made to the financial statements of subsidiaries to bringtheir accounting policies in line with the Jollibee Group’s accounting policies. All intra-group assetsand liabilities, equity, income, expenses and cash flows relating to transactions between members ofthe Jollibee Group are eliminated in full on consolidation.

The reporting dates of the Parent Company and the associates or joint ventures are identical and thelatter’s accounting policies conform to those used by the Parent Company for like transactions andevents in similar circumstances.

If the Jollibee Group loses control over a subsidiary, it:

ƒ Derecognizes the assets (including goodwill) and liabilities of the subsidiary;ƒ Derecognizes the carrying amount of any non-controlling interests;ƒ Derecognizes the cumulative translation differences recorded in equity;ƒ Recognizes the fair value of the consideration received;ƒ Recognizes the fair value of any investment retained;ƒ Recognizes any surplus or deficit in profit or loss; and,ƒ Reclassifies the parent’s share of components previously recognized in other comprehensive

income to profit or loss or retained earnings, as appropriate, as would be required if the JollibeeGroup had directly disposed of the related assets or liabilities.

Non-controlling interests represent the interests in the subsidiaries not held by the Parent Company,and are presented separately in the consolidated statement of comprehensive income and consolidatedstatement of financial position, separately from equity attributable to equity holders of theParent Company.

A change in ownership interest in a subsidiary that does not result in a loss of control is accounted foras an equity transaction. The carrying amounts of the controlling and non-controlling interests areadjusted to reflect the changes in the Jollibee Group’s relative interests in the subsidiary. The JollibeeGroup recognizes directly in equity any difference between the amount by which the non-controllinginterests are adjusted and the fair value of the consideration paid or received, and attribute it to theequity holders of the Parent Company. These include acquisitions of non-controlling interests ofGreenwich, Yong He King, Mang Inasal, Happy Bee Foods Processing Pte. Ltd. and Smashburger.In particular cases where the Jollibee Group acquires non-controlling interest in a subsidiary at a

- 13 -

*SGVFS034434*

consideration in excess of its carrying amount, the excess is charged to the “Excess of cost over thecarrying value of non-controlling interests acquired” account under equity. These changes in theownership interest in a subsidiary do not result in the recognition of a gain or loss in profit or loss.

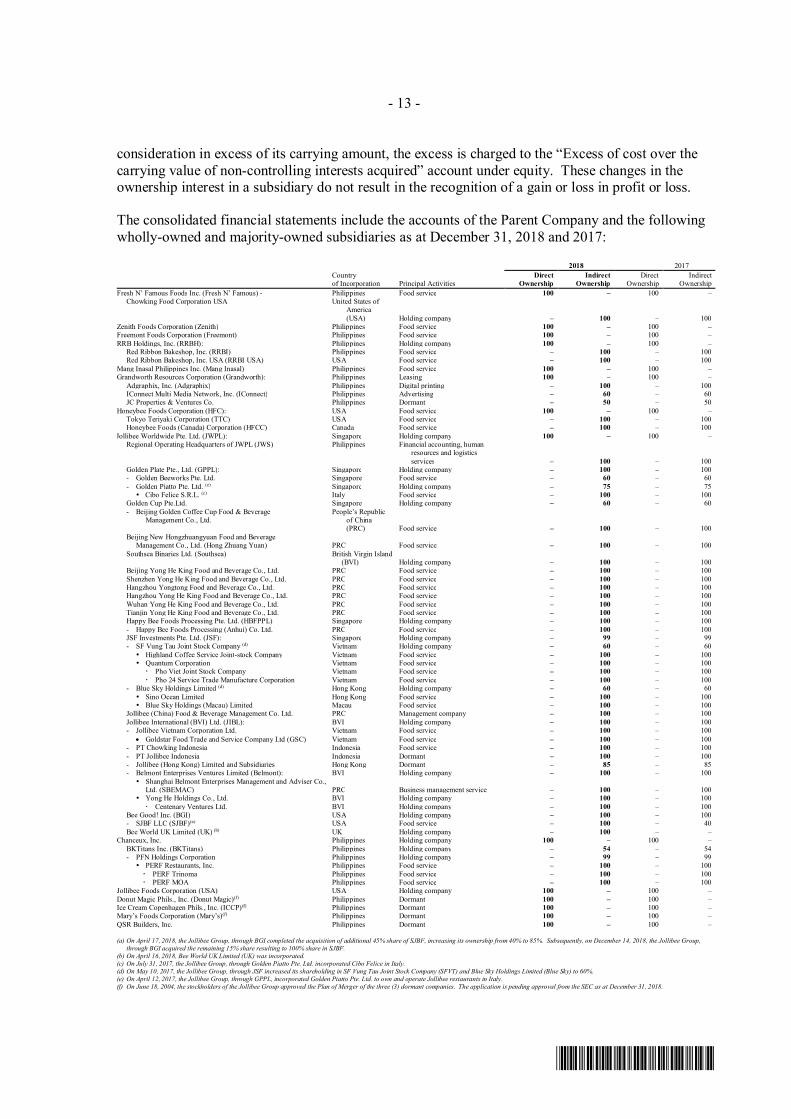

The consolidated financial statements include the accounts of the Parent Company and the followingwholly-owned and majority-owned subsidiaries as at December 31, 2018 and 2017:

Countryof Incorporation

2018 2017

Principal ActivitiesDirect

OwnershipIndirect

OwnershipDirect

OwnershipIndirect

OwnershipFresh N’ Famous Foods Inc. (Fresh N’ Famous) - Philippines Food service 100 – 100 –

Chowking Food Corporation USA United States ofAmerica(USA) Holding company – 100 – 100

Zenith Foods Corporation (Zenith) Philippines Food service 100 – 100 –Freemont Foods Corporation (Freemont) Philippines Food service 100 – 100 –RRB Holdings, Inc. (RRBH): Philippines Holding company 100 – 100 –

Red Ribbon Bakeshop, Inc. (RRBI) Philippines Food service – 100 – 100Red Ribbon Bakeshop, Inc. USA (RRBI USA) USA Food service – 100 – 100

Mang Inasal Philippines Inc. (Mang Inasal) Philippines Food service 100 – 100 –Grandworth Resources Corporation (Grandworth): Philippines Leasing 100 – 100 –

Adgraphix, Inc. (Adgraphix) Philippines Digital printing – 100 – 100IConnect Multi Media Network, Inc. (IConnect) Philippines Advertising – 60 – 60

JC Properties & Ventures Co. Philippines Dormant – 50 – 50Honeybee Foods Corporation (HFC): USA Food service 100 – 100 –

Tokyo Teriyaki Corporation (TTC) USA Food service – 100 – 100Honeybee Foods (Canada) Corporation (HFCC) Canada Food service – 100 – 100

Jollibee Worldwide Pte. Ltd. (JWPL): Singapore Holding company 100 – 100 –Regional Operating Headquarters of JWPL (JWS) Philippines Financial accounting, human

resources and logisticsservices – 100 – 100