job order and process costin accounting

TRANSCRIPT

JOB ORDER AND PROCESS COSTİNG

By: Bahaidr Beadin

Cost Accounting Systems

Gather information to determine the production cost per unit.

Help managers: set selling prices that will lead to profits compute cost of goods sold for the income

statement compute the cost of inventory for the balance

sheet Assign these costs to the company’s product

or service using: Job order costing Process costing

Job Order Costing

Some companies manufacture batches of unique products or provide specialized services. A job order costing system accumulates costs for each batch, or job.

Accounting firms, music studios, health-care providers, building contractors, and furniture manufacturers are examples of companies that use job order costing systems.

For example, Dell makes personal computers based on customer orders.

Process Costing

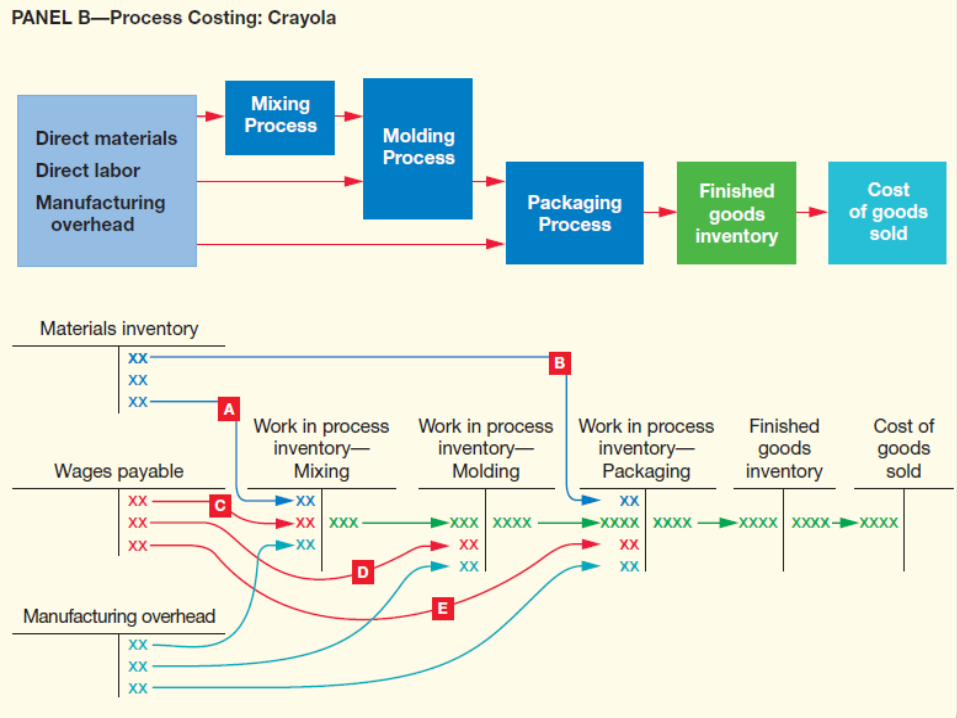

Other companies, such as Procter & Gamble and Coca-Cola produce identical units through a series of production steps or processes. A process costing system accumulates the costs of each process needed to complete the product.

So, for example, Coca-Cola’s process steps may include mixing, bottling, and packaging.

A surfboard manufacturing company’s process steps may include sanding, painting, waxing, and packaging.

A medical equipment manufacturer of a blood glucose meter’s process steps may include soldering, assembly, and testing.

Process costing is used primarily by large producers of similar goods.

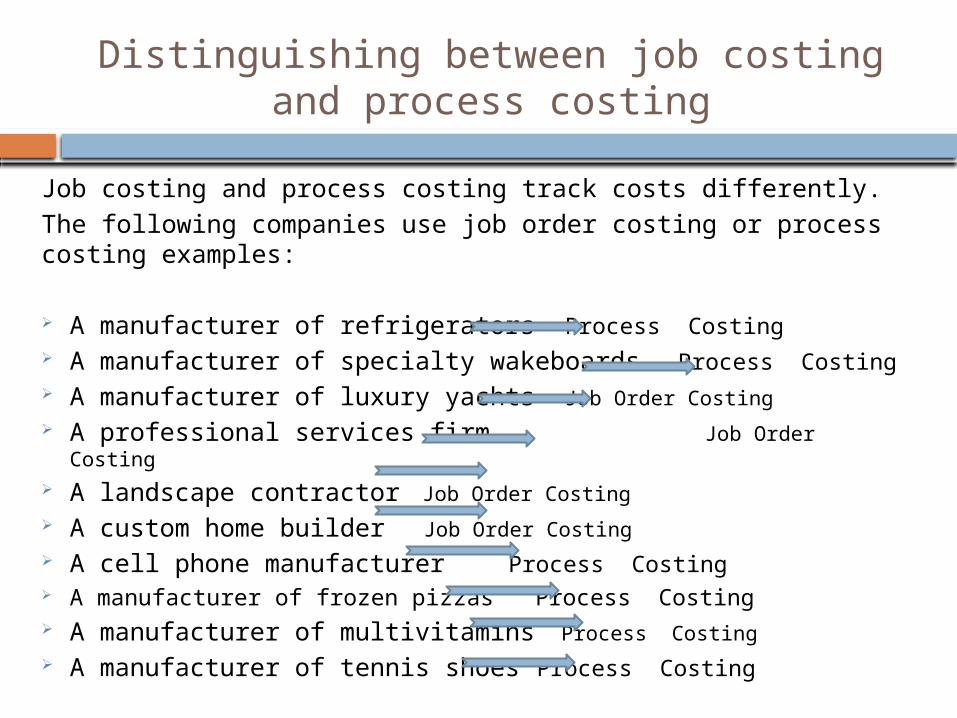

Distinguishing between job costing and process costing

Job costing and process costing track costs differently.The following companies use job order costing or process costing examples:

A manufacturer of refrigerators Process Costing A manufacturer of specialty wakeboards Process Costing A manufacturer of luxury yachts Job Order Costing A professional services firm Job Order Costing A landscape contractor Job Order Costing A custom home builder Job Order Costing A cell phone manufacturer Process Costing A manufacturer of frozen pizzas Process Costing A manufacturer of multivitamins Process Costing A manufacturer of tennis shoes Process Costing

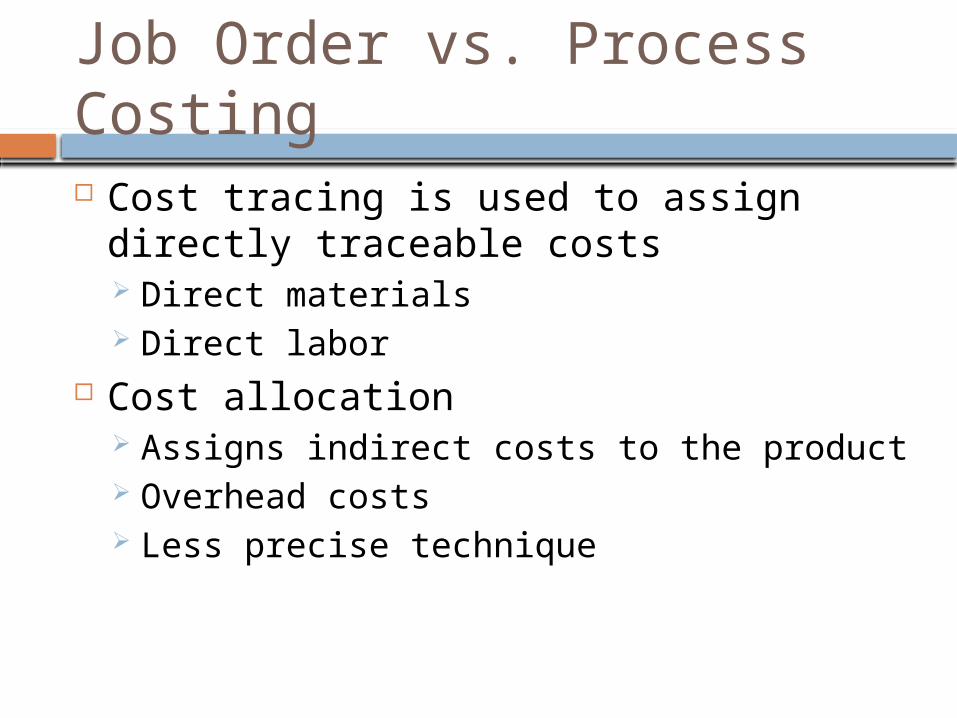

Job Order vs. Process Costing Cost tracing is used to assign directly

traceable costs Direct materials Direct labor

Cost allocation Assigns indirect costs to the product Overhead costs Less precise technique

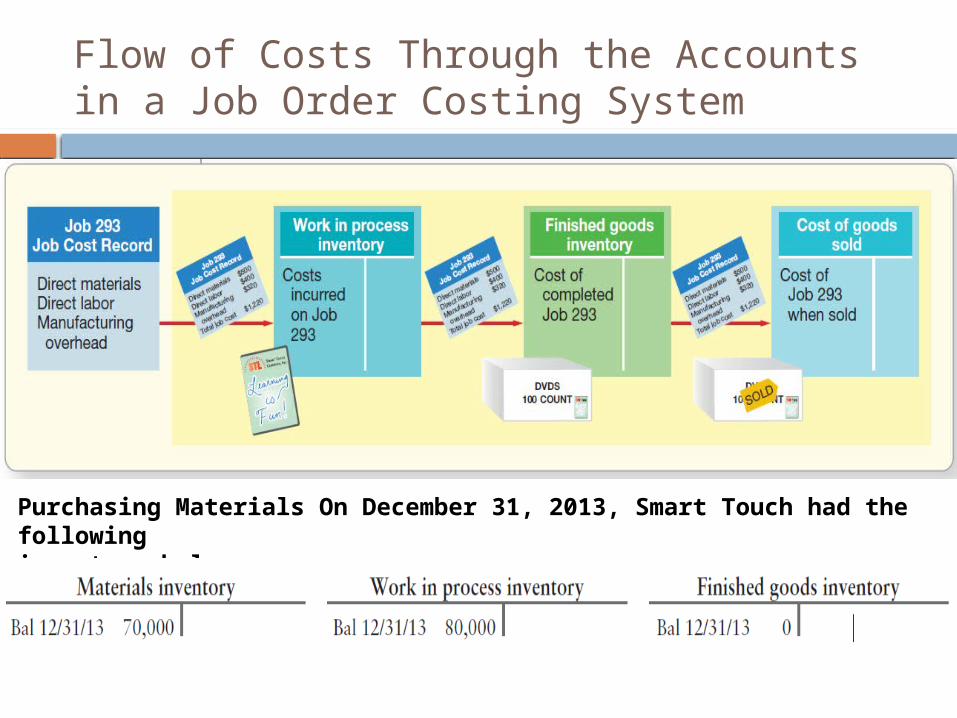

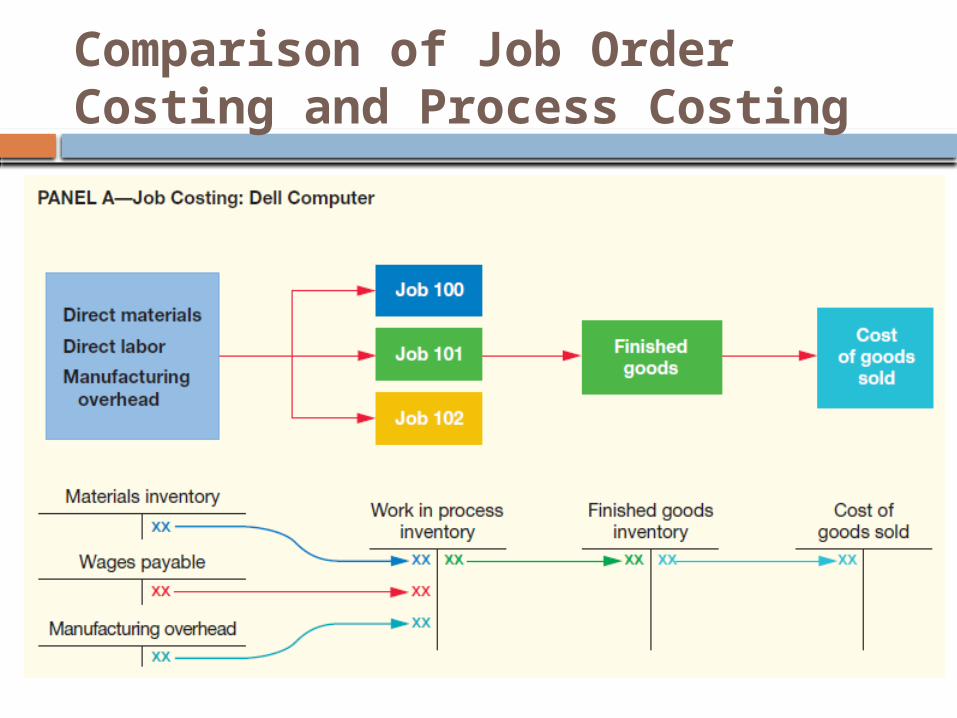

Flow of Costs Through the Accounts in a Job Order Costing System

Purchasing Materials On December 31, 2013, Smart Touch had the followinginventory balances:

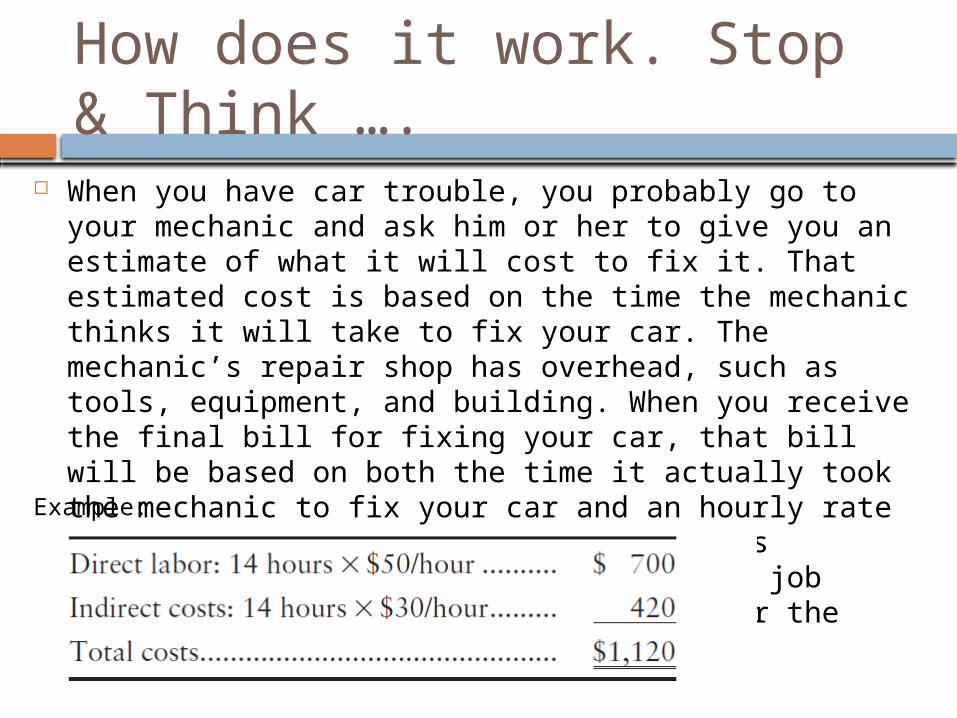

How does it work. Stop & Think ….

When you have car trouble, you probably go to your mechanic and ask him or her to give you an estimate of what it will cost to fix it. That estimated cost is based on the time the mechanic thinks it will take to fix your car. The mechanic’s repair shop has overhead, such as tools, equipment, and building. When you receive the final bill for fixing your car, that bill will be based on both the time it actually took the mechanic to fix your car and an hourly rate that includes the mechanic repair shop’s overhead. This is an example of service job costing. Your car problem is the job for the mechanic.

Example:

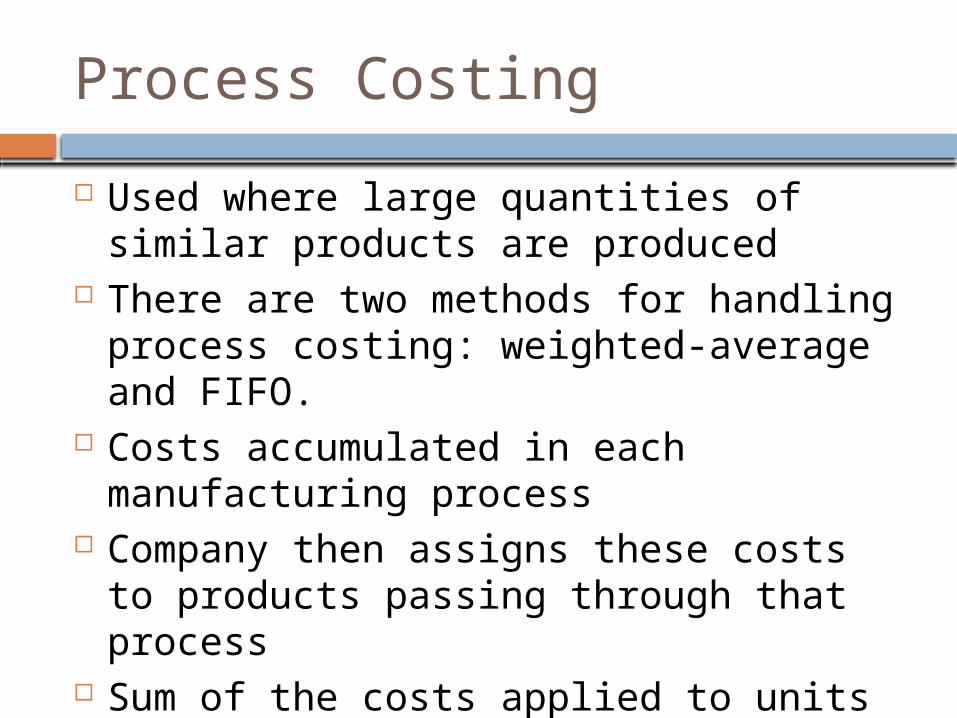

Process Costing

Used where large quantities of similar products are produced

There are two methods for handling process costing: weighted-average and FIFO.

Costs accumulated in each manufacturing process

Company then assigns these costs to products passing through that process

Sum of the costs applied to units produced to determine costs per unit

Exampel

Suppose Crayola’s production costs incurred to make 10,000 crayons and the costs per crayon are as follows:

The total cost to produce 10,000 crayons is the sum of the costs incurred for the three processes. The cost per crayon is the total cost divided by the number of crayons, or

.

Comparison of Job Order Costing and Process Costing

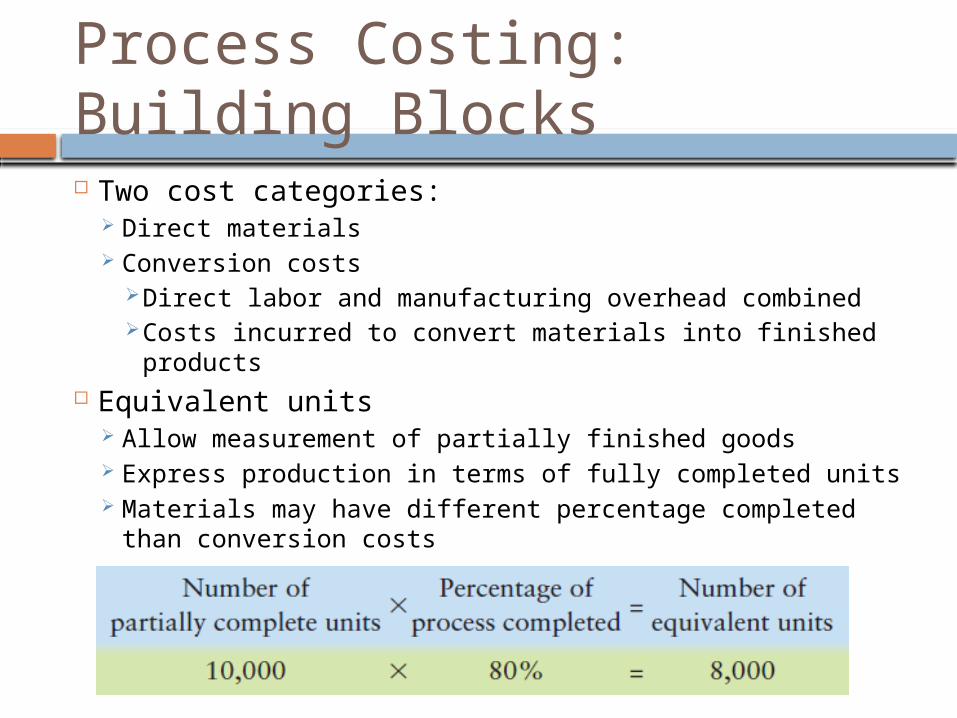

Process Costing: Building Blocks Two cost categories:

Direct materials Conversion costs

Direct labor and manufacturing overhead combined Costs incurred to convert materials into finished

products Equivalent units

Allow measurement of partially finished goods Express production in terms of fully completed units Materials may have different percentage completed than

conversion costs

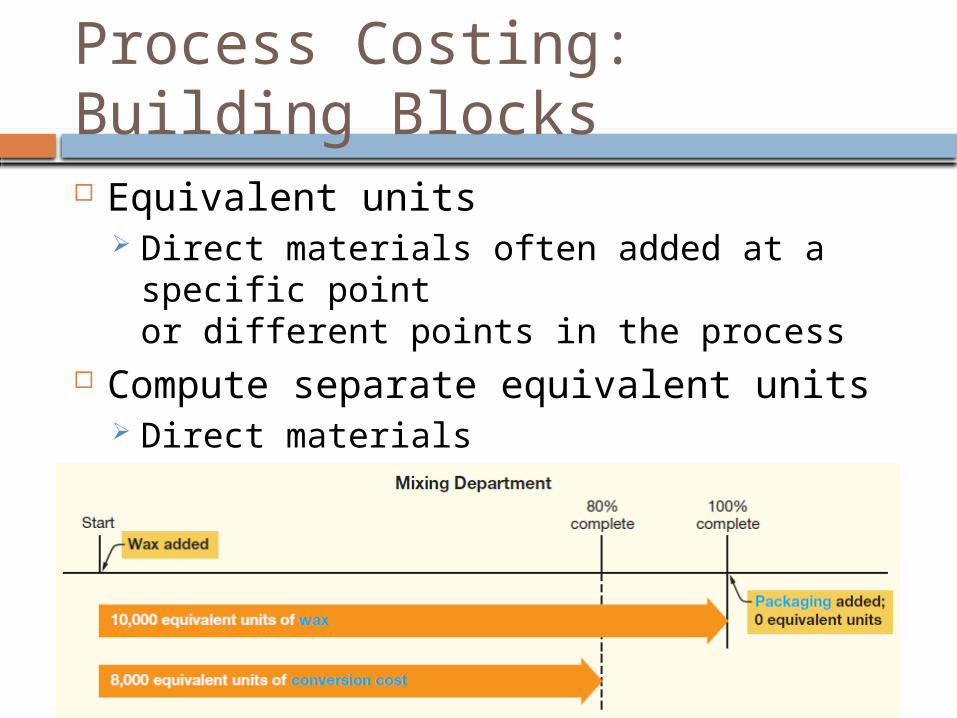

Process Costing: Building Blocks Equivalent units

Direct materials often added at a specific pointor different points in the process

Compute separate equivalent units Direct materials Conversion cost

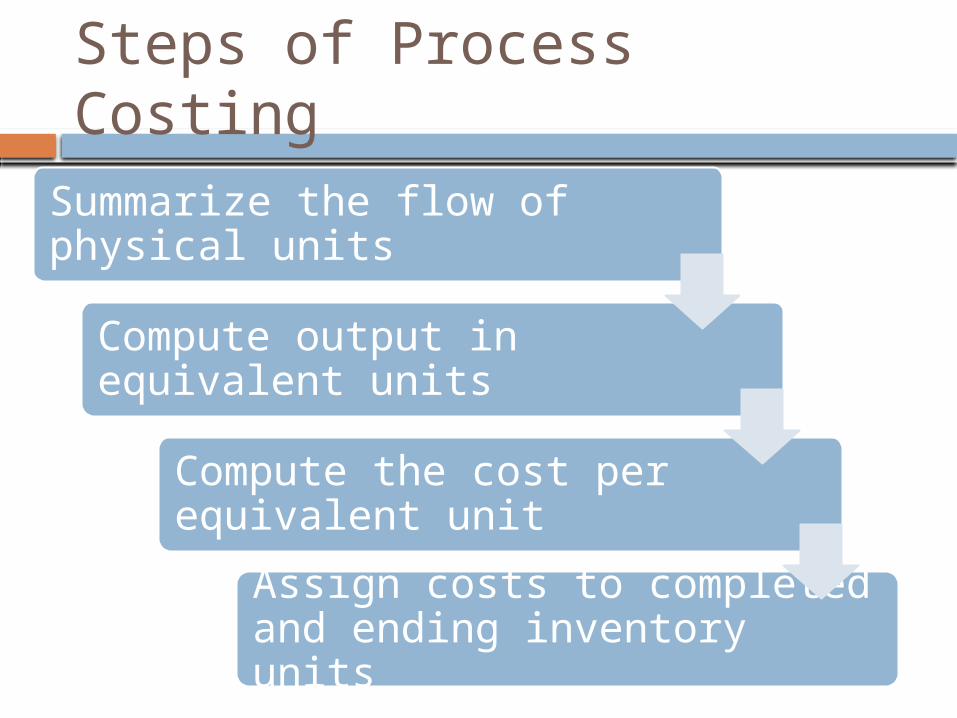

Steps of Process Costing

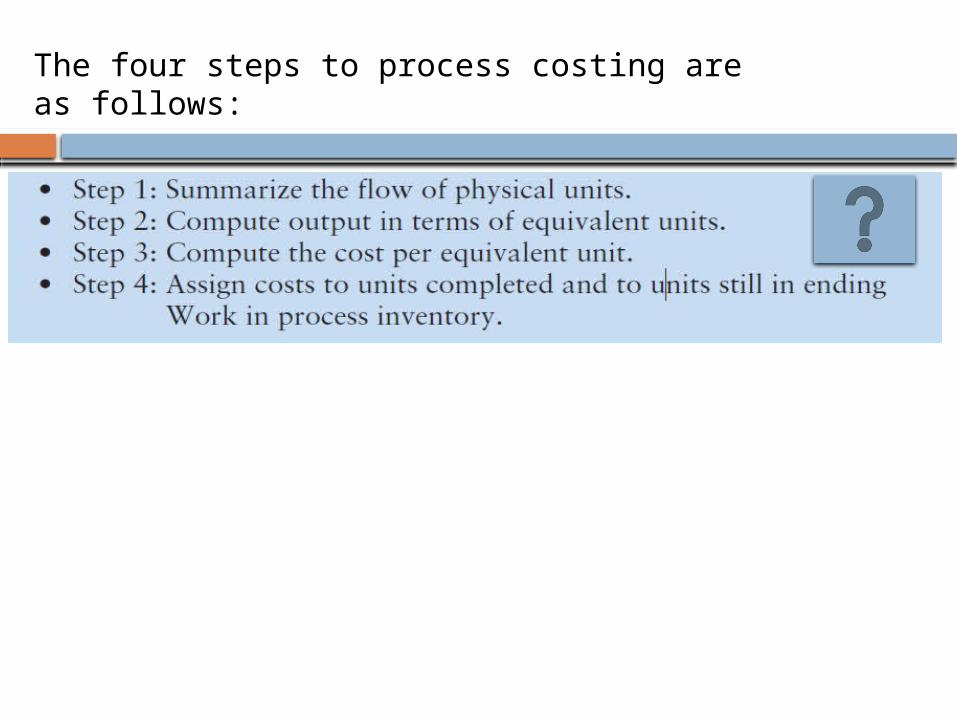

Summarize the flow of physical units

Compute output in equivalent units

Compute the cost per equivalent unit

Assign costs to completed and ending inventory units

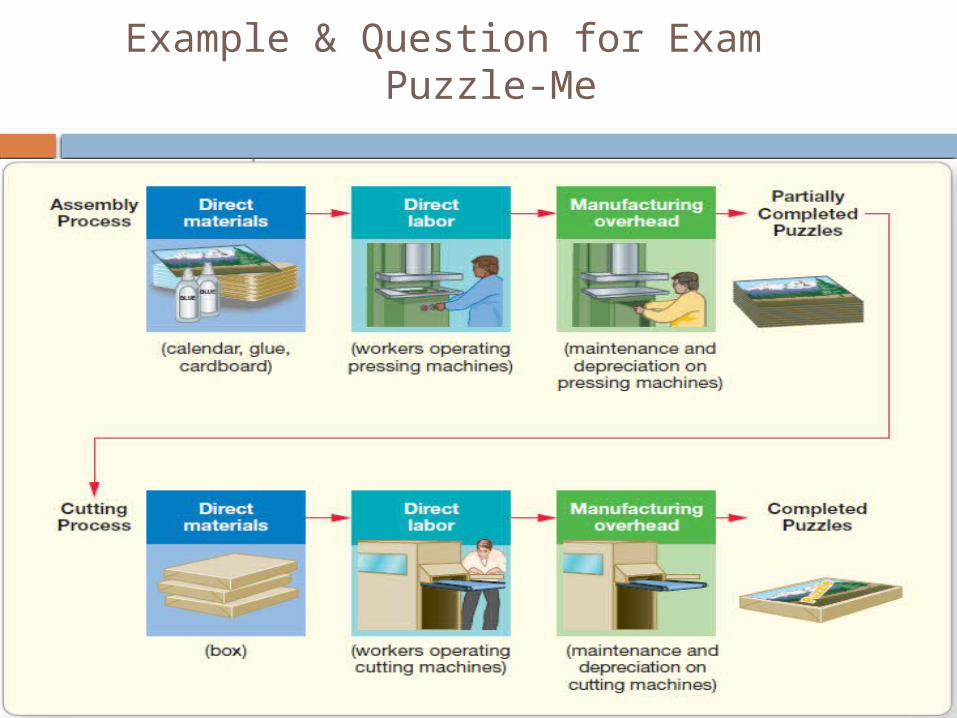

Example & Question for Exam Puzzle-Me

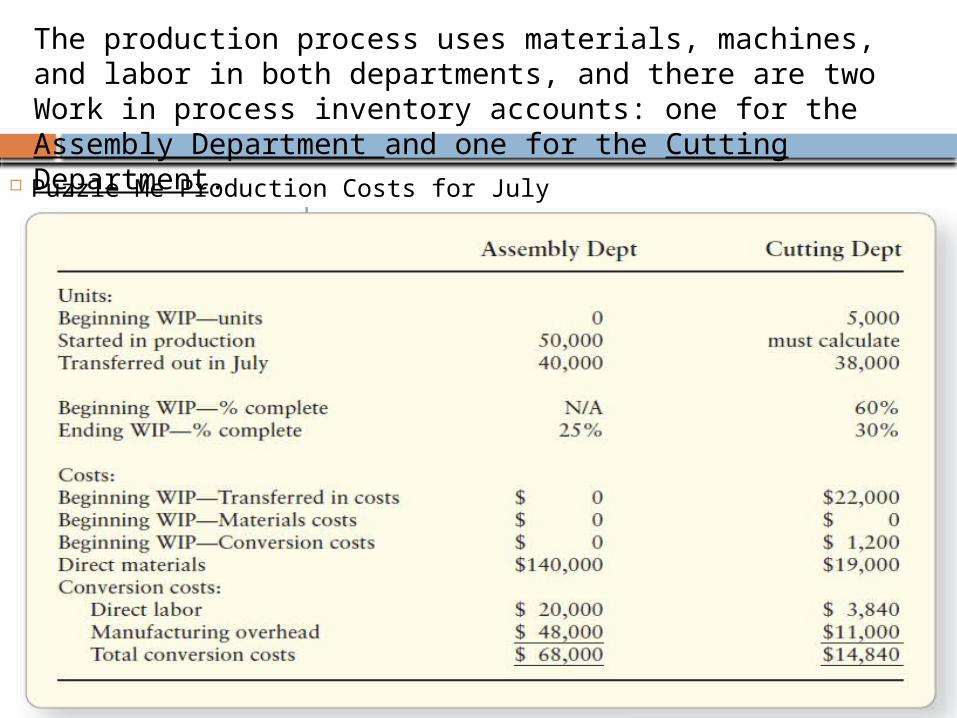

The production process uses materials, machines, and labor in both departments, and there are two Work in process inventory accounts: one for the Assembly Department and one for the Cutting Department.

Puzzle Me Production Costs for July

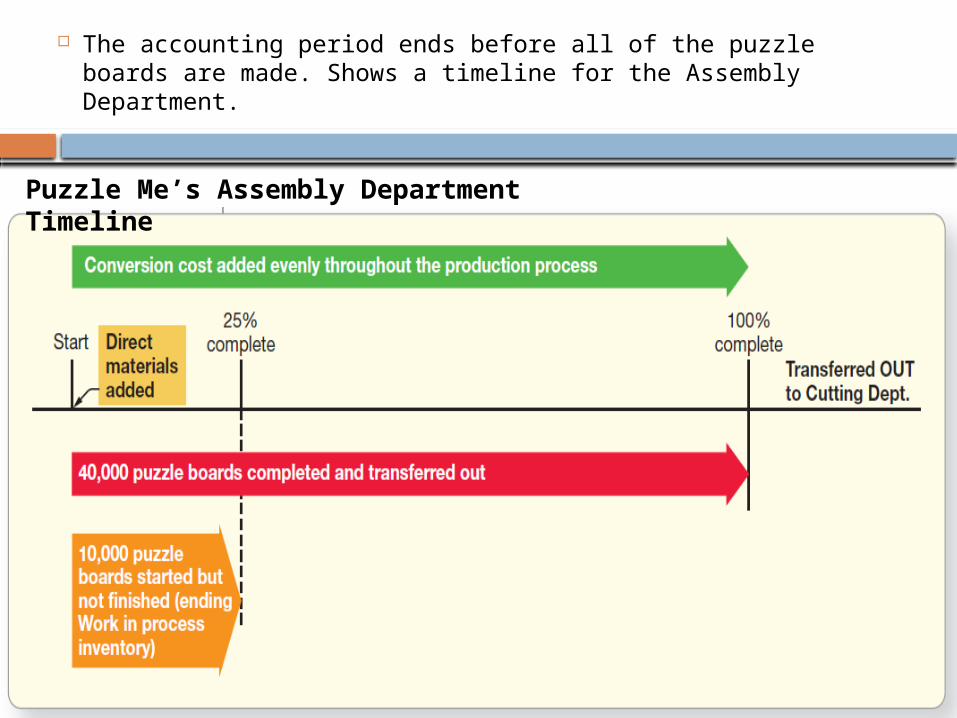

The accounting period ends before all of the puzzle boards are made. Shows a timeline for the Assembly Department.

Puzzle Me’s Assembly Department Timeline

The four steps to process costing are as follows:

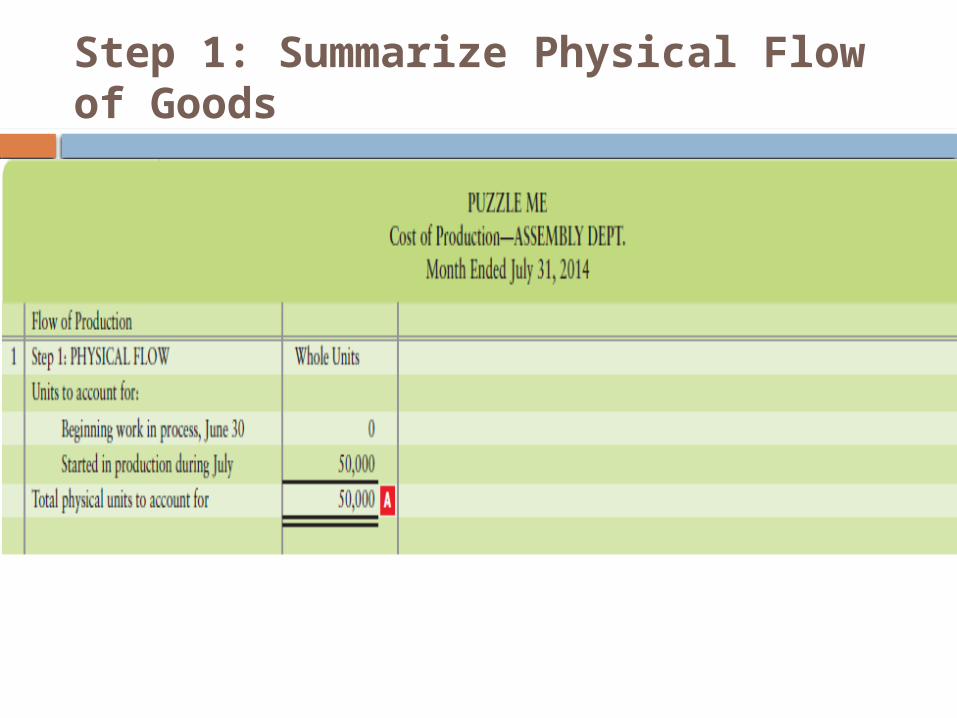

Step 1: Summarize Physical Flow of Goods

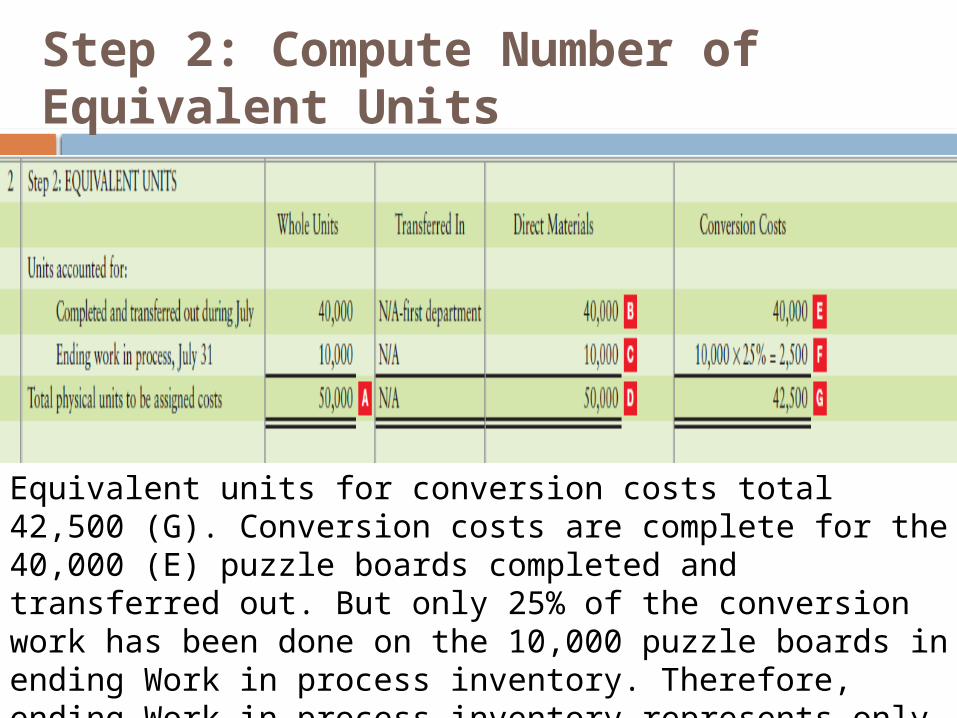

Step 2: Compute Number of Equivalent Units

Equivalent units for conversion costs total 42,500 (G). Conversion costs are complete for the 40,000 (E) puzzle boards completed and transferred out. But only 25% of the conversion work has been done on the 10,000 puzzle boards in ending Work in process inventory. Therefore, ending Work in process inventory represents only 2,500 (F) equivalent units for conversion costs.

Step 3: Compute Cost per Equivalent Unit

We computed equivalent units for direct materials (50,000)(G)) and conversion costs (42,500)(D)). Because the equivalent units differ, we must compute a separate cost per unit for direct materials and for conversion costs. Exhibit shows that the direct materials costs are ($140,000(H+I=J)). Conversion costs are ($68,000(L+M=N)) , which is the sum of direct labor of $20,000 and manufacturing overhead of $48,000. The cost per equivalent unit of material is ($2.80(J/D=K)), and the cost per equivalent unit of conversion cost is ($1.60(N/G=O)) ,as shown

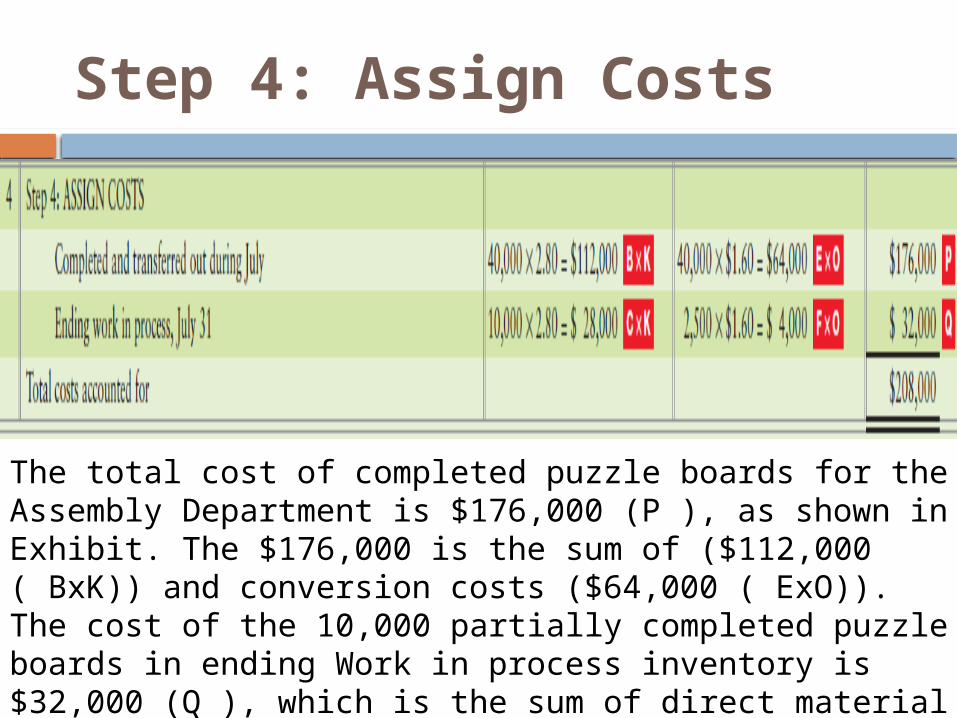

Step 4: Assign Costs

The total cost of completed puzzle boards for the Assembly Department is $176,000 (P ), as shown in Exhibit. The $176,000 is the sum of ($112,000 ( BxK)) and conversion costs ($64,000 ( ExO)). The cost of the 10,000 partially completed puzzle boards in ending Work in process inventory is $32,000 (Q ), which is the sum of direct material costs ($28,000 (CxK)) and conversion costs ($4,000 (FxO)) allocated in Exhibit.

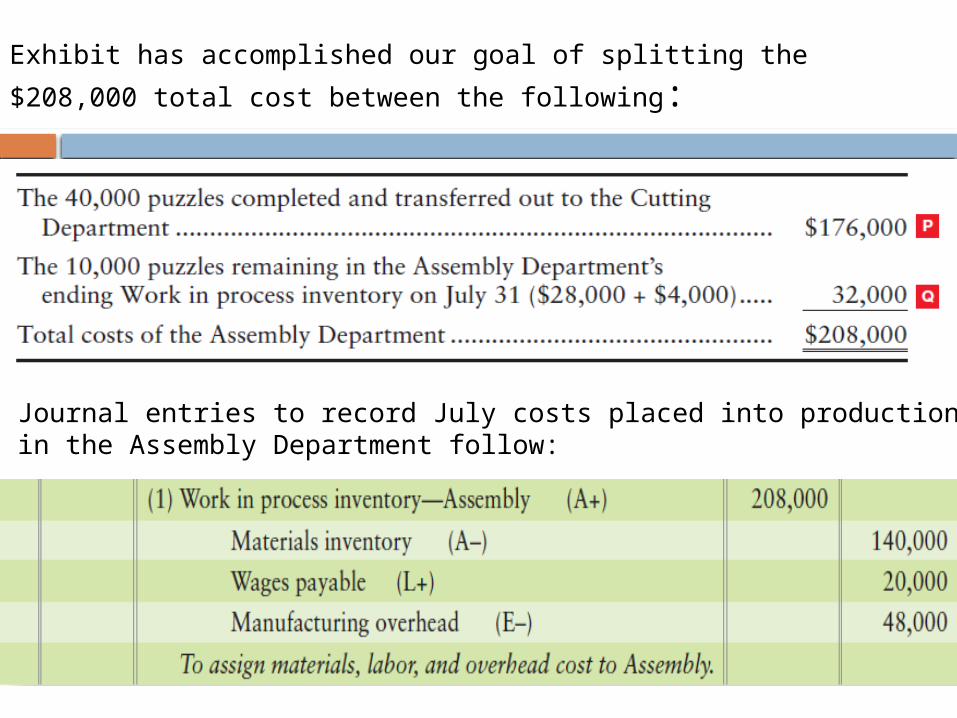

Exhibit has accomplished our goal of splitting the $208,000 total

cost between the following:

Journal entries to record July costs placed into production in the Assembly Department follow:

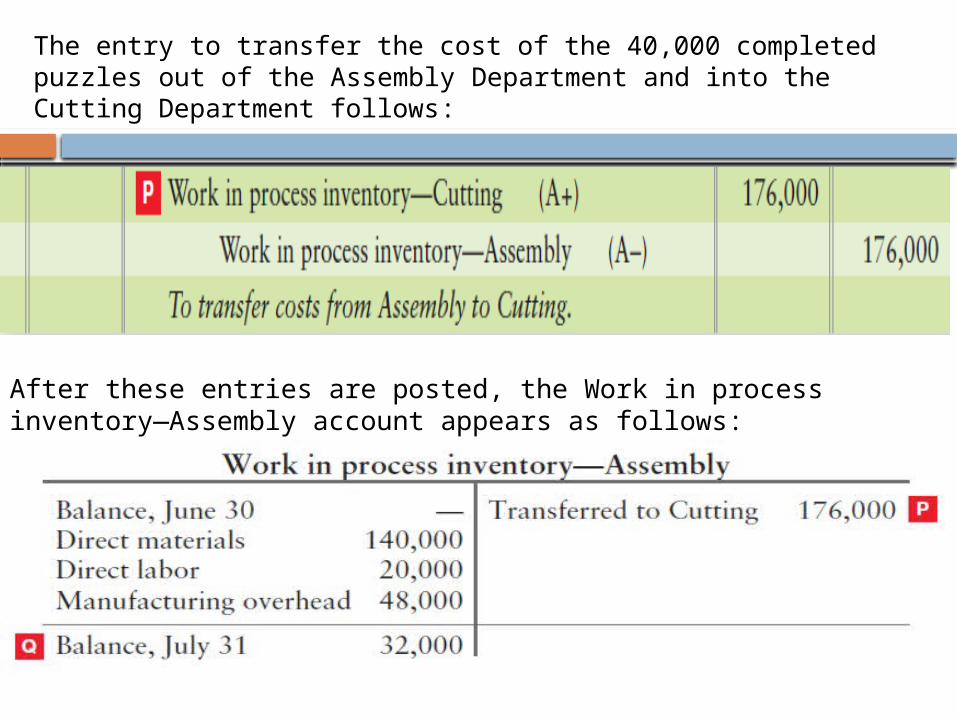

The entry to transfer the cost of the 40,000 completed puzzles out of the Assembly Department and into the Cutting Department follows:

After these entries are posted, the Work in process inventory—Assembly account appears as follows:

Thanks