it governance for enterprise resource planning supported by the delone–mclean model of information...

TRANSCRIPT

Information & Management 45 (2008) 257–269

Contents l is ts ava i lab le at ScienceDirec t

Information & Management

journa l homepage: www.e lsev ier .com/ locate / im

IT governance for enterprise resource planning supported by theDeLone–McLean model of information systems success

Edward W.N. Bernroider *

Vienna University of Economics and Business Administration, Department for Information Business, Augasse 2-6, 1090 Vienna, Austria

A R T I C L E I N F O

Article history:

Received 18 May 2005

Received in revised form 24 August 2007

Accepted 11 November 2007

Available online 1 May 2008

Keywords:

ERP

IT governance

IT success

IT value delivery

Empirical survey

A B S T R A C T

I investigated the role of IT governance in driving the success of ERP projects. The tool for assessing ERP

value was a comprehensive, multivariate and validated model adapted from the widely used Delone and

McLean model of IS success. This showed that ERP investments were more effective in organizations

having an IT governance domain consisting of proactive strategic guidance and participatory team

building. Large enterprises, however, under-performed compared to SMEs and needed specific

performance drivers, such as top management commitment to become effective.

� 2008 Elsevier B.V. All rights reserved.

1. Introduction

Today’s business requirements have moved IT governance intothe focus of attention. The core processes underlying effective andcomprehensive IT governance are the same as those for anenterprise. IT activities are critically important to all aspects of theenterprise. This applies to ERP system applications which are seenas key in supporting business processes in many organizations. ERPinvolves the seamless integration of processes across functionalareas such as finance, human resources, manufacturing andlogistics. They support improved workflow, standardization ofbusiness practices, and improved capabilities. ERP systems includeseveral configurable modules that integrate core business activ-ities into a single environment based on an integrated, shareddatabase. The far-reaching structural changes following an ERPimplementation can be disastrous, as shown by examples [3,5,21].Indeed, it has been reported that 70% of ERP implementations failto achieve their corporate goals. However, most researchconducted on ERP systems has concentrated on issues related tothe implementation phase in large enterprises. There seems to belimited work reported that assesses the value of ERP in amultivariate context focusing on post-implementation stages.

My goal was to analyse empirically the success rates achievedwith ERP investments according to expectations for a multiple

* Tel.: +43 1 31336/5200; fax: +43 1 31336/739.

E-mail address: [email protected].

0378-7206/$ – see front matter � 2008 Elsevier B.V. All rights reserved.

doi:10.1016/j.im.2007.11.004

attributive assessment seeking to embrace all major dimensions ofERP consequences for the organisation. In order to tackle this task,the popular Delone and McLean (D&M) IS success model [8,9] wasadopted with multiple attributes that accounted for ERP as aspecific IS investment. The work went beyond implementing aD&M model specification by applying it as a concrete measure-ment model. A number of questions were developed as hypothesesto analyse the effect of observed IT governance practices on ERPvalue delivery. To support the analysis, I drew on data gatheredfrom an independent, empirical survey undertaken in Austria forsmall to medium and large enterprises in order to include size-specific considerations. The Austrian case can be seen as a goodexample for a well-developed region within the European Union.In this sense, results should be applicable to most of the 25member states.

2. Research background and research hypotheses

2.1. IT governance

The critical role of IT in enterprises has led to the view that ITgovernance must be managed to support or enable businessobjectives and mitigate risks associated with IT implementation[4,23,26]. IT strategic planning has received growing emphasis andis a major component of IT governance [11], which can be seen as aholistic strategic controlling framework for effective and efficientuse of IT. Legacy software and infrastructures must be transformedinto well-defined services to facilitate future business models and

E.W.N. Bernroider / Information & Management 45 (2008) 257–269258

legal needs. Business management needs to trigger organizationalchange, establishing a new organizational structure. Consequently,any ERP initiative can be viewed as a strategic IT decision addingvalue to the firms’ IT/IS infrastructure and that it shouldbe safeguarded by effective IT governance methods. In addition,the legal and regulatory responsibilities of top management areevolving and becoming more complicated.

2.2. A characterisation of ERP

ERP can be viewed from a variety of perspectives: as a softwareproduct, an infrastructure, from a vendor or user viewpoint, etc.Here, ERP is considered to be both a commodity and a managementconcept that seeks to map all major processes and data into acomprehensive integrative structure. It is a software package thatis customizable without much programming effort having pre-configured templates that allow it to target an anonymous market.Typical business processes are generally supported across businessunits and functions in a seamless way. Thus, ERP packages arecomplex software applications having some difficulties in theirimplementation. The operational challenges associated with ERPimplementation and on-going usage can easily dominate the user’sperception of ERP. I focused on a conception-centric view of ERP,rather than a technical or IS oriented one. The ERP implementationmust be based on an understanding of the processes used by thefirm and should provide the basis for future processes.

To assess ERP value or success, a model was developed. An ERPsystem has many stakeholders. Thus, different actors define itssuccess differently [13]:

� F

rom an implementer’s perspective, it entails adherence toprojected resource commitments and developing specificationsfor particular functional objectives. � F rom a vendor’s perspective, the implementer must carefullyconsider follow-up investments.

� F rom an end user’s perspective, the ERP system should improvejob performance while being usable and satisfying.

� F rom a manager’s perspective, it should be effective and efficientin supporting business objectives.

Measurement of ERP success also depends on time spent forimplementation [17]. However, ERP success criteria defined in theearly stages will not capture the entire scope of ERP related successduring use and later periods. Case-based studies have shown thatan ERP implementation claimed to be successful can become afailure [14]. I believed that ERP success was multi-dimensionalcovering aspects related to strategy and business. This businessperception of ERP differed from that of IS in general and proveddifficult to measure.

2.3. DeLone and McLean’s IS success model

The assessment of economic and organizational benefits is adifficult task. Several models have been developed to examine howfirms utilize IT capabilities, e.g. [15,16,29]. These concentrate onthe rationale behind IT adoption, but cannot provide a holisticpicture of adoption success. A widely adopted model of IS successconcentrated on its multi-dimensional and interdependent nature:the Delone and McLean’s (D&M) IS success model. The purpose ofthe original model was to synthesize work involving individualmeasures into a single coherent model. This was based primarilyon work reported in [18,22] and empirical IS related studies. Themodel contained six IS success factors: (1) ‘‘system quality’’, (2)‘‘information quality’’, (3) ‘‘use’’, (4) ‘‘user satisfaction’’, (5)‘‘individual impact’’, and (6) ‘‘organizational impact’’. Based on a

large volume of contributions since the original model waspublished (referenced in nearly 300 articles), the authors revisedtheir model. Quality was considered to be a three-dimensionalconstruct (information, system, and service quality), each mea-sured and controlled separately. Those quality dimensionssingularly or jointly affect intention to use, use, and usersatisfaction. As a result certain net benefits occur.

The purpose of my study was to view ERP success in the usagestage after its implementation. Important social actors of this stageare end users, technical administration, and business and ITmanagement personnel. All of these are involved in the D&M(updated) IS success model. The multi-dimensional approach withsuitable perspectives justified its use.

2.4. Research hypotheses

Whereas the direct influence of management practices on theconfiguration of IT is known, their direct effects on IT utility and firmperformance remain unproven. I focused on the direct link betweenmanagerial practices and ERP value. In general, business manage-ment acquires resources directly or indirectly by finding appropriatepartners, investors, and advisors. Firms with developed and diversemanagement skills can undertake more promising competitiveroles. SMEs often show a relatively unclear distribution ofresponsibilities in management, a lack of formal structure, strategiclimitations due to short-term time frames, and a lack of managerialexperience. Consequently, it is necessary to emphasise theimportance of building management competence in SMEs [12].

I hypothesized that ERP success increased with implementationof key IT governance practices. More specifically, the consideredpractices comprised of the employment of an IT/IS strategy; theachievement of strategic alignment; the development of aselection goal hierarchy based on fundamental strategic objec-tives; management commitment to the whole project; and theinstallation of a participative form of decision making andimplementation that included all major stakeholders. All facetswere considered as managerial key practices in strategic ISdecisions [24,28,30]. Accordingly, I enunciated the followinghypotheses:

Hypothesis A. ERP success increases if firms have an explicitlydefined IT/IS strategy.

Hypothesis B. ERP success increases if companies pursue strategicalignment.

Hypothesis C. ERP success increases if a strategic concept drivesERP evaluation.

Hypothesis D. ERP success increases with top management com-mitment to the whole project.

Hypothesis E. ERP success increases if a participative form ofdecision-making is employed.

Hypothesis F. ERP success decreases if the project team is domi-nated by business management.

Hypothesis A assumes a clear understanding of the strategicgoals of the company. In terms of any major business investment,there must be a clear definition of goals, expectations anddeliverables [1]. The decision maker, controller, and auditors needto know why an ERP system is being implemented and whatcritical business needs it should address. However, the strategicfocus of the firm is often vague or undefined. Consequently, mystudy began by analyzing whether companies with a defined IT/ISstrategy achieved greater ERP success.

E.W.N. Bernroider / Information & Management 45 (2008) 257–269 259

Hypothesis B was constructed because of many reportedfailures of ERP implementations attributed to a lack of alignmentwith business needs [7].

Hypothesis C was postulated because firms show a lack offormal measurement of IT benefits and often fail to recognizemethodologies that consider fundamental decision making goals,in particular strategic needs, in evaluating the ERP strategy or/andsystem alternatives. Consequently, firms can easily fail to utilizeimportant benefits of ERP because of their lack of strategicplanning. Hence, I assumed that a strategic concept was needed toincrease ERP project success.

Hypothesis D repeats the well-known fact that successfulimplementations of any systems needs leadership, commitment,and participation by top management.

Hypothesis E states that participative decision-making is animportant success factor for ERP implementations in a socio-technical perspective. IT governance also needs to consider theway that decision making on IT investments is distributed amongthe stakeholders.

Hypothesis F was intended to prove that ERP projects were toooften dominated by business management: that ERP successdecreases if the project team is dominated by them.

3. Empirical research methodology

3.1. Overview

My work drew on data from an industry independent empiricalsurvey undertaken in the years 2003–2004. The questionnaireconcentrated on ERP success. A comprehensive set of questionswas developed from work performed in a previous ERP relatedstudy [2], plus a review of relevant literature and recommenda-tions of a panel of ERP experts from two universities in Austria andthe UK. The panel was asked to criticize the questionnaire forcontent validity [10]. As a result, the questionnaire was revised andused in pre-testing in both Austria and the UK. The completequestionnaire as shown in Appendix A, started with a generalsection assessing background information on the company and itsperformance. The second part determined the duration andexpended effort in the ERP choice and implementation stages.The subsequent topics were placed in three sections dealing withthe ERP system lifecycle: adoption decision and system acquisi-tion, implementation, and use (including maintenance). However,this paper only considers a sub-set of the wide range of aspects thatwere assessed in the given questionnaire.

3.2. The Sample

The target group consisted of Austrian small-to-medium andlarge enterprises (LEs). To avoid under representing the LEs, astratified and disproportional set of subgroups was selected, basedon company size. The total sample consisted of one thousandrandomly selected firms from a comprehensive database contain-ing financial information on 7 million public and privatecompanies in 38 European countries [6]. This source ensured thatthe sample procedure was repeatable.

3.3. Procedure

Companies were contacted through a multi-staged procedure.A cover letter, the hardcopy questionnaire and a stamped, self-addressed, return envelope were sent to the business managementof each of the companies. The package explained the purpose of thestudy, promoted participation in the survey, assured confidenti-ality of respondents, and offered an ERP-related collection of

material on CD and a summary of the results to participants,together with the opportunity to engage in further activities. Thequestionnaire was also provided in an electronic version. Twoweeks after the initial mailing, follow-up calls were made to allcompanies who had not responded, requesting their participationand, if possible, an email address. Shortly after these calls,reminder/thank you emails were sent out. The next round ofcontact consisted of reminders to 400 randomly selectedcompanies who had not responded; the telephone calls againsupplied address and login information about the online ques-tionnaire.

3.4. Response

Two hundred and nine valid returns were registered, resultingin an above-average response rate (22%). Some companies couldnot be contacted, because they had ceased to exist or they hadmoved, etc. These neutral dropouts (49 companies) wereconsidered in the calculation of the response rate and thereforedid not decrease the return quota. To test for non-response bias,known distributions of three variables available through thecorporate database (legal form, number of employees, number ofsubsidiaries) were assessed. The analysis revealed no significantlydifferent characteristics between non-respondents and respon-dents in terms of all three aspects as measured by chi-square (x2)and two-sample unpaired t tests (see Appendix B).

3.5. Measures

Respondents were asked to assess the questions on differentscales, either dichotomous (yes = 1, no = 0), on metric (e.g., foremployees, sales), or on interval scales (either percentages from 0to 100%, or 5-point Likert scales). To avoid misconceptions, theorientation of the 5-point scales was applied uniformly: Low scoreswere attributed to negative settings, while high scores account forfavourable situations. The data was analysed using a statisticalpackage. To avoid biased estimates, the analysis used an SPSSmodule [Complex Samples] where adjusted tests including x2

were provided. However, since the range of procedures waslimited, analysis was also conducted using sampling weights [20].

4. Adopting D&M’s IS success model

4.1. The a priori ERP success model

The D&M model does not give guidance on the measures to beused or on how to go about the evaluation process [25]. Themeasures I used were based on a goal centric definition of utility.The interviewee stated whether the expectations were met on a 5-point Likert scale, where a 1 was for a very negative and 5 for a verypositive evaluation. These targets were given in terms of a widerange of attributes. In particular, many non-financial factors had tobe assessed, including the most important potential improve-ments. Therefore, the selection of attributes accounted for a widespectrum of ERP impacts. The measurement criteria were drawnfrom a revised and amendment list of ERP selection criteriaidentified in prior research through a Delphi Method involvingstudents, practitioners, and researchers. The list items were splitalong the dimensions of the D&M IS success model.

Fig. 1 shows the resulting a priori ERP success model, whichinterprets the model in its original context. It is a causal-exploratory model of how perceived quality affects use and usersatisfaction, which are direct antecedents of net benefits.

The focus is on assessing net benefits via assessment of thepositive and negative impacts of the system.

Fig. 1. Measures alligned along DeLone and McLean’s updated IS success model.

Table 1Final exploratory factor solution: Varimax rotation

Items NB: net benefits SY: system quality FI: firm level financial impact SE: service quality

Ne6 Business process improvement 0.87 0.10 0.11 0.13

Ne2 Reduced cycle times 0.87 �0.17 0.18 0.22

Ne7 Enabler for desired business processes 0.83 0.15 0.15 0.16

Ne1 Enhanced decision making 0.81 0.05 0.32 �0.12

Ne9 Improved innovation capabilities 0.77 0.00 0.04 0.28

Ne5 System costs 0.67 0.33 �0.17 �0.04

Ne8 Increased organisational flexibility 0.63 0.03 0.10 0.26

Sy1 System flexibility 0.24 0.85 0.14 0.10

Sy4 System functionality �0.05 0.84 0.05 0.35

Sy2 System interoperability 0.01 0.69 0.02 �0.43

Ne10 Revenue after switching to ERP 0.08 0.28 0.92 �0.02

Ne11 Profit after switching to ERP 0.28 �0.09 0.89 0.16

Se2 Availability of IT/IS services 0.23 �0.08 0.18 0.78

Se1 Systems reliability 0.22 0.29 �0.06 0.63

Kaiser–Meyer–Olkin (KMO) sampling adequacy 0.740

Bartlett’s test of sphericity

x2 119.0

d.f. 91

Significance 0.026

E.W.N. Bernroider / Information & Management 45 (2008) 257–269260

4.2. Testing the model for construct validity

The 21 items in the model were included in an exploratoryfactor analysis in testing the model for construct validity with thesingle variable for information quality excluded. The model waspartially validated: of the 21 variables, 7 were dropped and theremaining 14 variables resulted in a more interpretable andparsimonious outcome (see Table 1). All remaining itemsexplained 73.7% of the variance. In the context of my study, ERPcan lead to financial consequences such as higher profit or loss. Thedimension ‘‘Intention to use/use and user satisfaction’’ wasomitted from the model because it is not seen as a fittingdimension of success unless system use is voluntary, which is notthe case for ERP.

Table 2Correlations between general success criteria and dimensions

Variables A B

Correlation p Correlation

NB Net benefits 0.36 0.05 –

SY System quality 0.49 0.01 0.51

FI Financial impact – – –

SE Service quality – – 0.43

DA Dimension average 0.52 0.05 0.78

4.3. Testing the model for dimension validity

To analyse the validity of the four factor items in measuring ITsuccess, the following overall IT success metrics from the surveyinstrument were considered.

A. I

s ERP in general aiding your organisation to gain a competitiveedge? (No or Yes),B. E

fficiency of IT/IS supported processes, C. I T/IS impacts on goal achievement and D. I T/IS reliability.The statements (B–D) were measured on Likert scales from 1(very negative) to 5 (very positive).

C D

p Correlation p Correlation p

– 0.69 0.00 0.60 0.01

0.03 0.40 0.10 0.42 0.08

– – – – –

0.08 – – – –

0.00 0.60 0.01 0.47 0.05

Fig. 2. Final model and measurement dimensions for empirical analysis.

Table 3Firm size and branch distribution according to NAICS

No. of

companies

(rel. in %)

No. of

companies (abs.

unweighted N)

Size

Small to medium sized enterprises (SMEs) 92.8 130

Large enterprises (LEs) 7.2 79

Total 100 209

Branch

Trade (42,44–45) 22.6 58

Manufacturing (31–33) 21.0 60

Construction (23) 20.5 20

Services (54) 15.7 30

Transportation and warehousing (48–49) 7.6 8

Information (51) 4.5 8

Health care and social assistance (62) 1.9 4

Management of companies and enterprises (55) 1.4 8

Other 4.8 12

Total 100 208a

aOne organisation excluded.

E.W.N. Bernroider / Information & Management 45 (2008) 257–269 261

To compute a valid single measure of overall success, DA wascomputed as the average of the four dimensions from factoranalysis. The four variables (A–D) were correlated (Spearman rankcorrelation) with these four dimensions and their average (DA).The extent to which each dimension and their average correlateswith the variable scores was evidence of their validity. This is ofparticular importance since certain follow-up analysis onlyconsidered the four factors scores and their average. Table 2 givesthe results: for net benefits (NB) and system quality (SY) validity issupported, most criterions show large positive correlations withboth dimensions; financial impact (FI) and service quality (SE)apparently only have limited effect on IT success; and DA yields thelargest correlation with all the criteria. Therefore, when combinedthe criteria yield a stronger overall measure of success than thoseof any single dimension.

4.4. Resulting measurement model

The resulting model is shown in Fig. 2. It consists of 14 variablesgrouped by their factors/dimensions, and the single variableInformation Quality.

5. Empirical results

5.1. Sample demographics

Table 3 provides the firm size and branch distribution of thedata. The branch classification was based on codes of the NorthAmerican Industry Classification System (NAICS) [19]. Concor-dance tables can be used to translate the codes into theClassification of Economic Activities in the European Community(NACE) Revision 1.1 and the International Standard IndustrialClassification of all Economic Activities (ISIC) Revision 3.1 [27].

ERP diffusion along the system’s lifecycle stages is shown inTable 4 and Fig. 3. For LEs, ERP did not apply in 23.9% of the cases.For small to medium-sized enterprises the proportion increased to77.5%. While the majority of LEs are currently using, maintaining orextending ERP solutions, only a small minority of small to mediumsized enterprises have so far reached these lifecycle stages. Asexpected, the observed differences between SMEs and LEs arehighly significant (x2, p = 0.00).

Of the 209 data sets, 101 were not concerned with ERP. Theempirical analysis was consequently based on 108 observations(all numbers given in unweighted terms). In terms of usagesuccess, the number of eligible data sets was further reduced to 86.

5.2. IT governance practices

Organisations assessed the IT governance practices theyprovided or undertook when starting their ERP project with sixvariables. Table 5 depicts the managerial practices for allcompanies and subgroups sorted by the size of the company.Where applicable, x2 or correlation analysis were employed to testfor significant dependencies. Managerial functions seemed betterdeveloped in LEs. However, the IT/IS strategy was explicitly definedonly for every second LE. SMEs only have a formal IT/IS strategy in24% of the cases. Strategic alignment took place at some middlelevel. In terms of project team building, the situation alsodepended on company size. While LEs often relied on aparticipative character of their ERP project teams, SMEs more

Table 4ERP diffusion among SMEs and LEs

Stage All companies Small-to-medium enterprises Large enterprises

% Cum. % % Cum. % Unweight. N % Cum. % Unweight. N

Consideration 6.6 6.6 6.6 6.6 7 6.4 6.4 3

Evaluation 0.5 7.1 0.3 6.9 1 2.0 8.4 2

Implementation 1.2 8.3 0.4 7.3 2 10.5 18.9 7

Stabilisation 1.8 10.1 1.8 9.1 2 2.0 20.9 2

Usage and maintenance 13.4 23.5 11.4 20.5 27 39.0 59.9 32

Extension 2.9 26.4 1.9 22.4 7 16.1 76 16

No ERP 73.6 100 77.5 100 84 23.9 100 17

Total 100 – 100 – 130 100 – 79

Fig. 3. ERP diffusion among SMEs and LEs.

Fig. 4. Mean ERP success rates of the five measurement model dimensions.

E.W.N. Bernroider / Information & Management 45 (2008) 257–269262

often choose a central and business management oriented teamstructure. Generally, management commitment to the ERP projectwas present, but not pronounced.

5.3. IT value delivery

Fig. 4 gives the mean scores for every dimension of the appliedmeasurement model for all companies as well as for separatecompany size classes. It can be seen that ERP success according toexpectations is achieved. The mean values are all greater than 3,which can be seen as the threshold between positive and negativeeffects. In relative terms, net benefits and financial impact are lessdeveloped than quality. In the causal-explanatory view of the D&Mmodel, the quality dimensions should have an effect on NB and FI.Expectations of managers of SMEs were met at a higher level thanthose in LEs. The most pronounced difference can be seen forsystem quality. Statistical analysis revealed a correlation coeffi-cient of �0.38 with a minor significance ( p = 0.056).

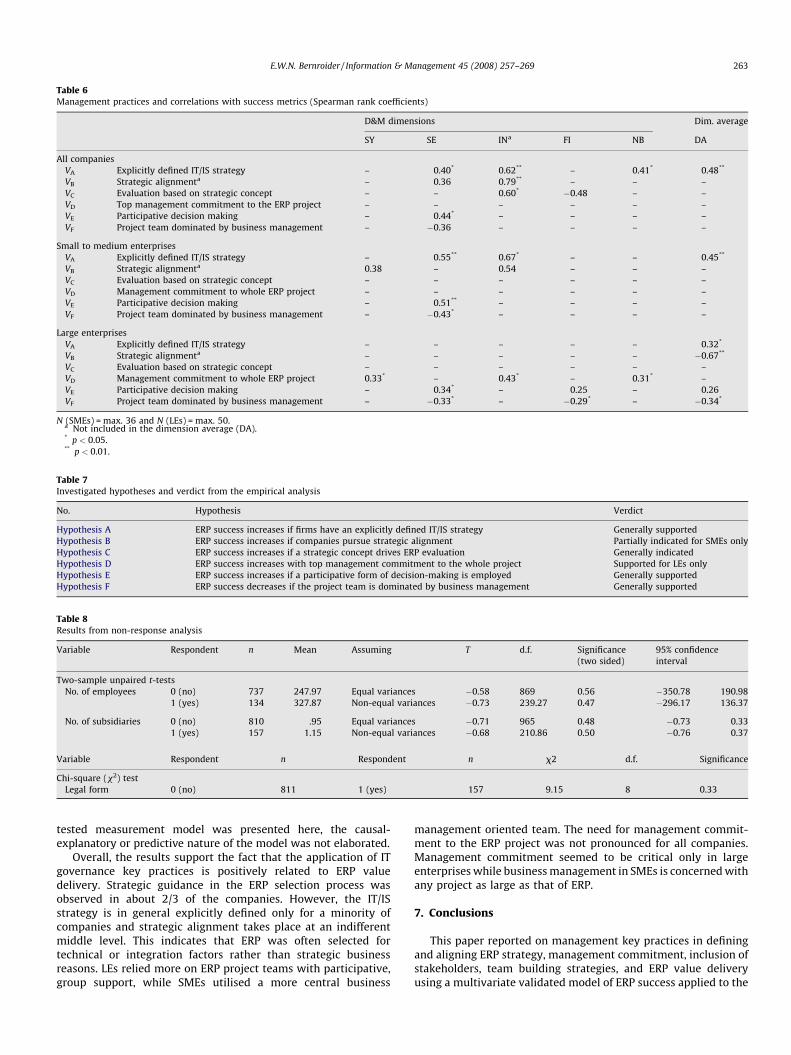

5.4. IT governance and value delivery

Table 6 gives the results of analysing the hypotheses based onpotential relationships between the management practice variableand the success metrics. The results cover correlations between thevariables and dimensions of the ERP success model: systemquality, service quality, information quality (IN), financial impact,and net benefits. The DA provides an overall metric covering alldimensions apart from information quality. Table 7 shows the

Table 5IT governance practices for all enterprises, SMEs, and LEs

Variable All

VA Explicitly defined IT/IS strategy 25.8%

VB Strategic alignmenta 3.13

VC Evaluation based on strategic concept 65.3%

VD Top management commitment to the ERP projecta 3.73

VE Participative decision making 15.2%

VF Project team dominated by business management 36.9%

a Rated on a scale between 1 (very poor) and 5 (very strong); N (SMEs) = max. 36, N

result for each hypothesis. The analysis was conducted for threedifferent samples of organisational size (all, LEs, and SMEs). Ahypothesis was attributed as generally supported, if it could beaccepted for every sample. It is partially supported, if therelationship is accepted for one sample, e.g., for LEs only. In allother respects, the hypotheses were rejected. However, analysisalso considered a slightly increased significance level ( p < 0.1).

ERP success rates seem to be higher in organisations with anexplicitly defined IT/IS strategy and for firms employing aparticipative form of decision making which includes all majorstakeholders rather than a more centric or commanding type.Furthermore, if the project team is dominated by businessmanagement members, a less successful implementation of ERPoccurs. The importance of top management commitment to thewhole project was only apparent for LEs.

6. Discussion

The D&M IS success model was well suited to design an a prioriERP success model. The model was analysed and revised by testingfor construct and dimension validity. A new dimension (‘‘netbenefits’’) was introduced to account for the financial consequencesof ERP. The model was empirically tested for dimension validity. Thegeneral success dimensions were consistent and, when combined,seemed to yield a single valid measure of ERP success. Although a

SMEs LEs x2 Correlation

23.8% 48.2% 0.00 –

3.11 3.51 0.04 –

63.7% 76.9% – –

3.76 3.60 0.02 –

8.1% 35.6% 0.00 –

41.0% 25.2% – –

(LEs) = max. 50; N = 0, Y = 1.

Table 6Management practices and correlations with success metrics (Spearman rank coefficients)

D&M dimensions Dim. average

SY SE INa FI NB DA

All companies

VA Explicitly defined IT/IS strategy – 0.40* 0.62** – 0.41* 0.48**

VB Strategic alignmenta – 0.36 0.79** – – –

VC Evaluation based on strategic concept – – 0.60* �0.48 – –

VD Top management commitment to the ERP project – – – – – –

VE Participative decision making – 0.44* – – – –

VF Project team dominated by business management – �0.36 – – – –

Small to medium enterprises

VA Explicitly defined IT/IS strategy – 0.55** 0.67* – – 0.45**

VB Strategic alignmenta 0.38 – 0.54 – – –

VC Evaluation based on strategic concept – – – – – –

VD Management commitment to whole ERP project – – – – – –

VE Participative decision making – 0.51** – – – –

VF Project team dominated by business management – �0.43* – – – –

Large enterprises

VA Explicitly defined IT/IS strategy – – – – – 0.32*

VB Strategic alignmenta – – – – – �0.67**

VC Evaluation based on strategic concept – – – – – –

VD Management commitment to whole ERP project 0.33* – 0.43* – 0.31* –

VE Participative decision making – 0.34* – 0.25 – 0.26

VF Project team dominated by business management – �0.33* – �0.29* – �0.34*

N (SMEs) = max. 36 and N (LEs) = max. 50.a Not included in the dimension average (DA).* p < 0.05.** p < 0.01.

Table 8Results from non-response analysis

Variable Respondent n Mean Assuming T d.f. Significance

(two sided)

95% confidence

interval

Two-sample unpaired t-tests

No. of employees 0 (no) 737 247.97 Equal variances �0.58 869 0.56 �350.78 190.98

1 (yes) 134 327.87 Non-equal variances �0.73 239.27 0.47 �296.17 136.37

No. of subsidiaries 0 (no) 810 .95 Equal variances �0.71 965 0.48 �0.73 0.33

1 (yes) 157 1.15 Non-equal variances �0.68 210.86 0.50 �0.76 0.37

Variable Respondent n Respondent n x2 d.f. Significance

Chi-square (x2) test

Legal form 0 (no) 811 1 (yes) 157 9.15 8 0.33

Table 7Investigated hypotheses and verdict from the empirical analysis

No. Hypothesis Verdict

Hypothesis A ERP success increases if firms have an explicitly defined IT/IS strategy Generally supported

Hypothesis B ERP success increases if companies pursue strategic alignment Partially indicated for SMEs only

Hypothesis C ERP success increases if a strategic concept drives ERP evaluation Generally indicated

Hypothesis D ERP success increases with top management commitment to the whole project Supported for LEs only

Hypothesis E ERP success increases if a participative form of decision-making is employed Generally supported

Hypothesis F ERP success decreases if the project team is dominated by business management Generally supported

E.W.N. Bernroider / Information & Management 45 (2008) 257–269 263

tested measurement model was presented here, the causal-explanatory or predictive nature of the model was not elaborated.

Overall, the results support the fact that the application of ITgovernance key practices is positively related to ERP valuedelivery. Strategic guidance in the ERP selection process wasobserved in about 2/3 of the companies. However, the IT/ISstrategy is in general explicitly defined only for a minority ofcompanies and strategic alignment takes place at an indifferentmiddle level. This indicates that ERP was often selected fortechnical or integration factors rather than strategic businessreasons. LEs relied more on ERP project teams with participative,group support, while SMEs utilised a more central business

management oriented team. The need for management commit-ment to the ERP project was not pronounced for all companies.Management commitment seemed to be critical only in largeenterprises while business management in SMEs is concerned withany project as large as that of ERP.

7. Conclusions

This paper reported on management key practices in definingand aligning ERP strategy, management commitment, inclusion ofstakeholders, team building strategies, and ERP value deliveryusing a multivariate validated model of ERP success applied to the

E.W.N. Bernroider / Information & Management 45 (2008) 257–269264

operational/usage stage of the ERP system lifecycle. The ERP valuemeasurement model was used to analyse ERP success levelsaccording to expectations and results. An effective IT governancemechanism seems to facilitate ERP success rates. Overall, most ERP

Appendix A. (The complete ERP questionnaire)

adopters were found to be content with their decision to adopt, ERPstrategies were successful, meeting expectations. SMEs weregenerally more pleased with their ERP systems than LEs, inparticular in terms of perceived system quality.

E.W.N. Bernroider / Information & Management 45 (2008) 257–269 265

E.W.N. Bernroider / Information & Management 45 (2008) 257–269266

E.W.N. Bernroider / Information & Management 45 (2008) 257–269 267

E.W.N. Bernroider / Information & Management 45 (2008) 257–269268

Appendix B. (Tests for non-response bias)

Table 8 shows the results from non-response analysis based onunpaired (two sample) t tests (‘‘number of employees’’, ‘‘number ofsubsidiaries’’) and a chi-square (x2) test (‘‘legal form’’). Nosignificant differences were observed between non-respondentsand respondents in terms of all three considered variables.

References

[1] I. Ansoff, Corporate Strategy, Penguin Books, London, 1988.[2] E.W.N. Bernroider, S. Koch, ERP selection process in midsize and large

organizations, Business Process Management Journal 7 (3) (2001) 251–257.

[3] P. Bingi, M. Sharma, J. Godla, Critical issues affecting an ERP implementation,Information Systems Management Decision 16 (3) (1999) 7–14.

E.W.N. Bernroider / Information & Management 45 (2008) 257–269 269

[4] P.L. Bowen, M.-Y.D. Cheung, F.H. Rohde, Enhancing IT governance practices: amodel and case study of an organization’s efforts, International Journal ofAccounting Information Systems 8 (3) (2007) 191–221.

[5] S. Buckhout, E. Frey, J. Nemec Jr., Making ERP succeed. Turning fear into promise,IEEE Transactions of Engineering Management 27 (3) (1999) 116–123.

[6] Bureau-van-Dijk Analyse MAjor Databases from EUropean Sources (AMADEUS),Bureau van Dijk Electronic Publishing (BvDEP), 2003.

[7] T.H. Davenport, Putting the enterprise into the enterprise system, Harvard Busi-ness Review (1998) 121–131.

[8] W.D. DeLone, E.R. McLean, The DeLone and McLean model of information systemssuccess: a ten-year update, Journal of Management Information Systems 19 (4)(2003) 9–30.

[9] W.H. DeLone, E.R. McLean, Information systems success: the quest for thedependent variable, Information Systems Research 3 (1) (1992) 60–95.

[10] D.A. Dillman, Mail and telephone surveys: the total design method, John Wileyand Sons, New York, 1978.

[11] S. Hamaker, A. Hutton, Principles of IT governance, Information Systems ControlJournal (2) (2004) 1–4.

[12] A. Hughes, Innovation and business performance: small entrepreneurial firms inthe UK and the EU, New Economy 8 (3) (2001) 157–163.

[13] H. Klaus, M. Rosemann, G.G. Gable, What is ERP? Information Systems Frontiers 2(2) (2000) 141–162.

[14] M.A. Larsen, M.D. Myers, When success turns into failure: a package-drivenbusiness process re-engineering project in the financial services industry, TheJournal of Strategic Information Systems 8 (4) (1999) 395–417.

[15] M. Levy, P. Powell, Exploring SME internet adoption: towards a contingent model,Electronic Markets 13 (2) (2003) 173–181.

[16] M. Levy, P. Powell, P. Yetton, SMEs: aligning IS and the strategic context, Journal ofInformation Technology 16 (3) (2001) 133–144.

[17] M.L. Markus, S. Axline, D. Petrie, C. Tanis, Learning from adopters’ experienceswith ERP: problems encountered and success achieved, Journal of InformationTechnology 15 (4) (2000) 245–265.

[18] R.O. Mason, Measuring information output: a communication systems approach,Information & Management 1 (5) (1978) 219–234.

[19] NAICS-Association NAICS-North American Industry Classification System, 1997.[20] S. Purdon, K. Pickering The use of sampling weights in the analysis of the 1998

Workplace Employee Relations Survey, National Centre for Social Research, 2001,pp. 1–21.

[21] J.E. Scott, The FoxMeyer drugs’ bankruptcy: was it a failure of ERP? in: FifthAmericas Conference on Information Systems, Milwaukee, WI, (1999), pp. 223–225.

[22] C.E. Shannon, W. Weaver, The Mathematical Theory of Communication, Uni-versity of Illinois Press, Urbana, IL, 1949.

[23] A.S. Sohal, P. Fitzpatrick, IT governance and management in large Australian orga-nisations, International Journal of Production Economics 75 (1/2) (2002) 97–112.

[24] T.M. Somers, K.G. Nelson, The impact of strategy and integration mechanisms onenterprise system value: empirical evidence from manufacturing firms, EuropeanJournal of Operational Research 146 (2) (2003) 315–338.

[25] R. Stockdale, C. Standing, An interpretive approach to evaluating informationsystems: a content, context, process framework, European Journal of OperationalResearch 173 (3) (2006) 1090–1102.

[26] G. Trites, Director responsibility for IT governance, International Journal ofAccounting Information Systems 5 (2) (2004) 89–99.

[27] U.S.-Census-Bureau Concordances between Industry Classification Systems,2006.

[28] E.J. Umble, R.R. Haft, M.M. Umble, Enterprise resource planning: implementationprocedures and critical success factors, European Journal of Operational Research146 (2) (2003) 241–257.

[29] N. Venkatraman, IT-induced business reconfiguration, in: M. Scott-Morton (Ed.),The Corporation of the 1990s, Oxford University Press, New York, 1991, pp. 122–158.

[30] H.R. Yen, C. Sheu, Aligning ERP implementation with competitive priorities ofmanufacturing firms: an exploratory study, International Journal of ProductionEconomics 92 (3) (2004) 207–220.

Edward W.N. Bernroider received a MS degree in

applied informatics (1997) from the University of

Salzburg and a doctoral degree in business admin-

istration and information systems (2001) from the

Vienna University of Economics and Business

Administration. He worked as assistant professor

for seven years and after gaining the Austrian

Habilitation degree (tenure track decision, 2005) as

associate professor for another two years at the

Vienna University of Economics and BA. His current

research interests include governance, risk and

compliance with active model support applied to

IT service management and other service systems.

Output from his research activities appeared in over 50 international publications

covering different refereed journals, conferences and books.