islamic investment funds

TRANSCRIPT

IN THE NAME OF ALLAH THE MOST BENEFICENT AND THE MOST MERIFUL

ISLAMIC BANKING

“FUUAST ISLAMABAD”

Group members:Saad Iftikhar Wani

Raja Kamran Gul.

Muhammad Ayub

Asif Miraj

Usman Ali

ISLAMIC INVESTMENT FUNDS

Presented by :

RAJA KAMRAN GUL

THE TERM "ISLAMIC INVESTMENT FUND" MEANS.

Islamic Investment Funds are joint pool of funds wherein the

investors contribute their surplus money for the purpose of its

investment to earn halal profits in strict conformity with the

principles of Islamic Shariah

Principles of Islamic Investment funds

Subscribers of funds receive a document may be

called a certificate, a unit, a share or any other name

representing the value and will earn pro rated profits

on it.

Management can share in the profits or can charge a

fee for their services on monthly or annual basis.

Principles of Islamic Investment funds

Returns are tied up with the actual profits earned or

losses suffered.

In case of loss caused by the negligence on the part of

management, compensation will be provided by the

management.

Funds raised must be invested in Shariah approved

businesses.

Funds being Operated in the Market

UBL Sharia stock fund

United Islamic income fund

HBL Islamic money market fund

HBL Islamic stock fund

Al- Meezan Mutual fund Ltd.

Askari Islamic asset allocation fund

…………………

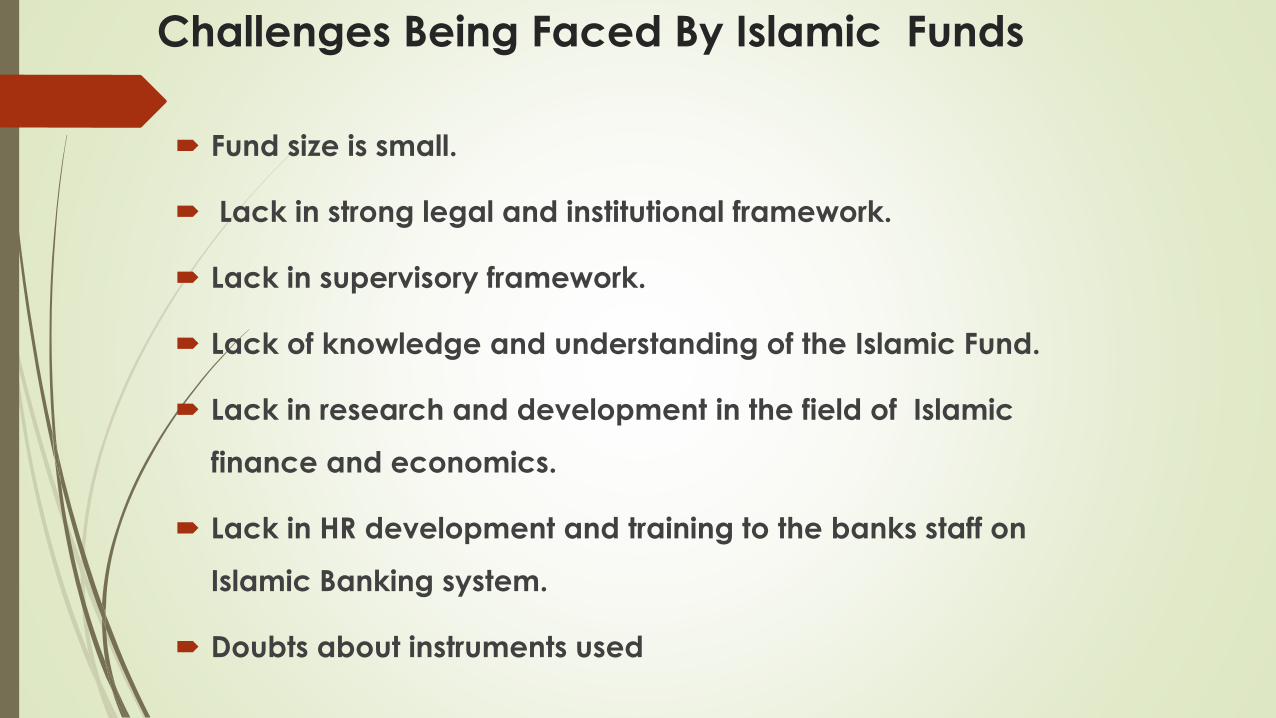

Challenges Being Faced By Islamic Funds

Fund size is small.

Lack in strong legal and institutional framework.

Lack in supervisory framework.

Lack of knowledge and understanding of the Islamic Fund.

Lack in research and development in the field of Islamic

finance and economics.

Lack in HR development and training to the banks staff on

Islamic Banking system.

Doubts about instruments used

EQUITY FUND

Presented by :

ASIF MAIRAJ

What Is an equity fund ?

CONTEMPORARY SHARIAH

contemporary Shariah experts are almost unanimous

on the point that if all the transactions of a company

are in full conformity with Shariah,

NOT LAWFUL IN TERMS OF SHARIAH

If the main business of a company is not lawful in terms

of Shariah, it is not allowed for an Islamic Fund to

purchase, hold or sell its shares,

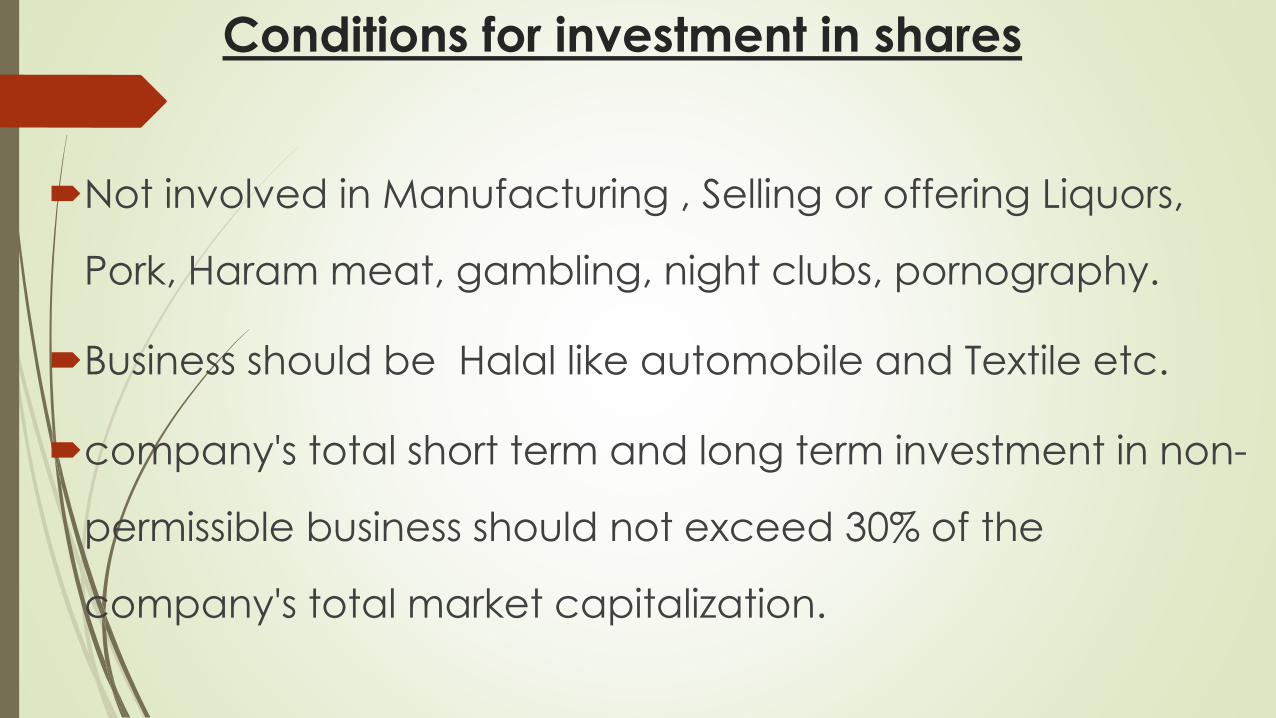

Conditions for investment in shares

Not involved in Manufacturing , Selling or offering Liquors,

Pork, Haram meat, gambling, night clubs, pornography.

Business should be Halal like automobile and Textile etc.

company's total short term and long term investment in non-

permissible business should not exceed 30% of the

company's total market capitalization.

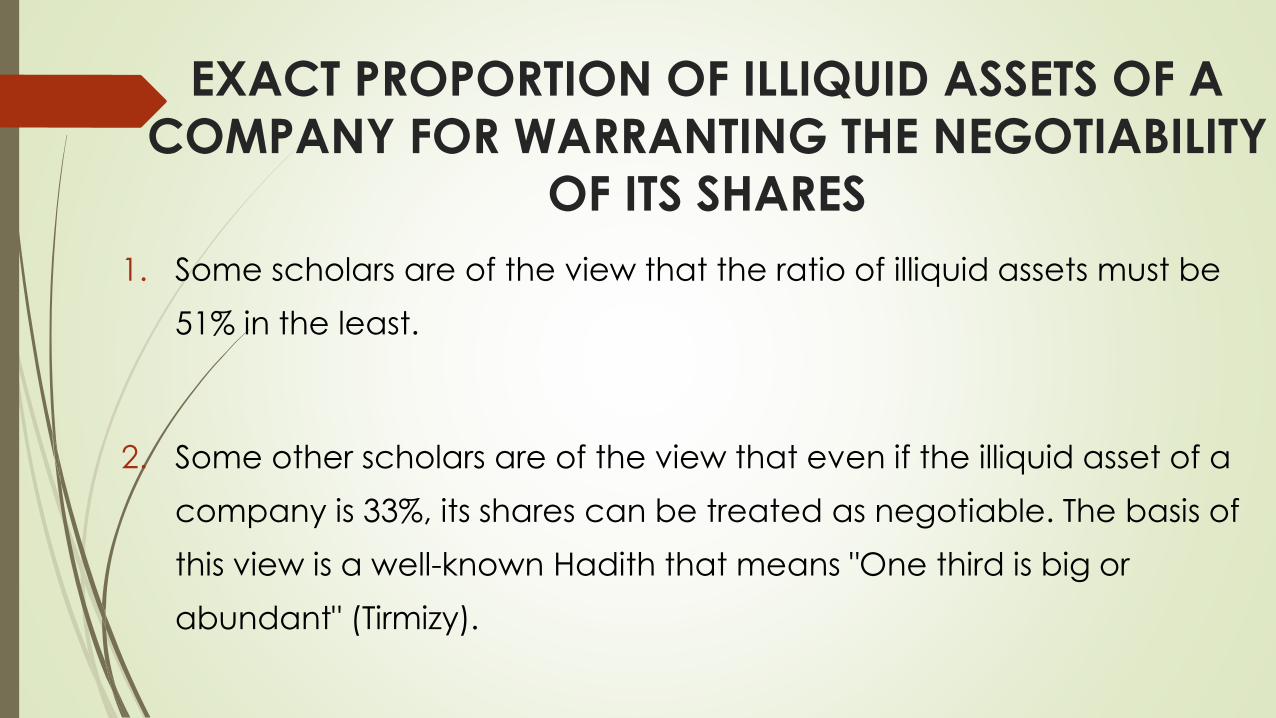

EXACT PROPORTION OF ILLIQUID ASSETS OF A

COMPANY FOR WARRANTING THE NEGOTIABILITY

OF ITS SHARES

1. Some scholars are of the view that the ratio of illiquid assets must be

51% in the least.

2. Some other scholars are of the view that even if the illiquid asset of a

company is 33%, its shares can be treated as negotiable. The basis of

this view is a well-known Hadith that means "One third is big or

abundant" (Tirmizy).

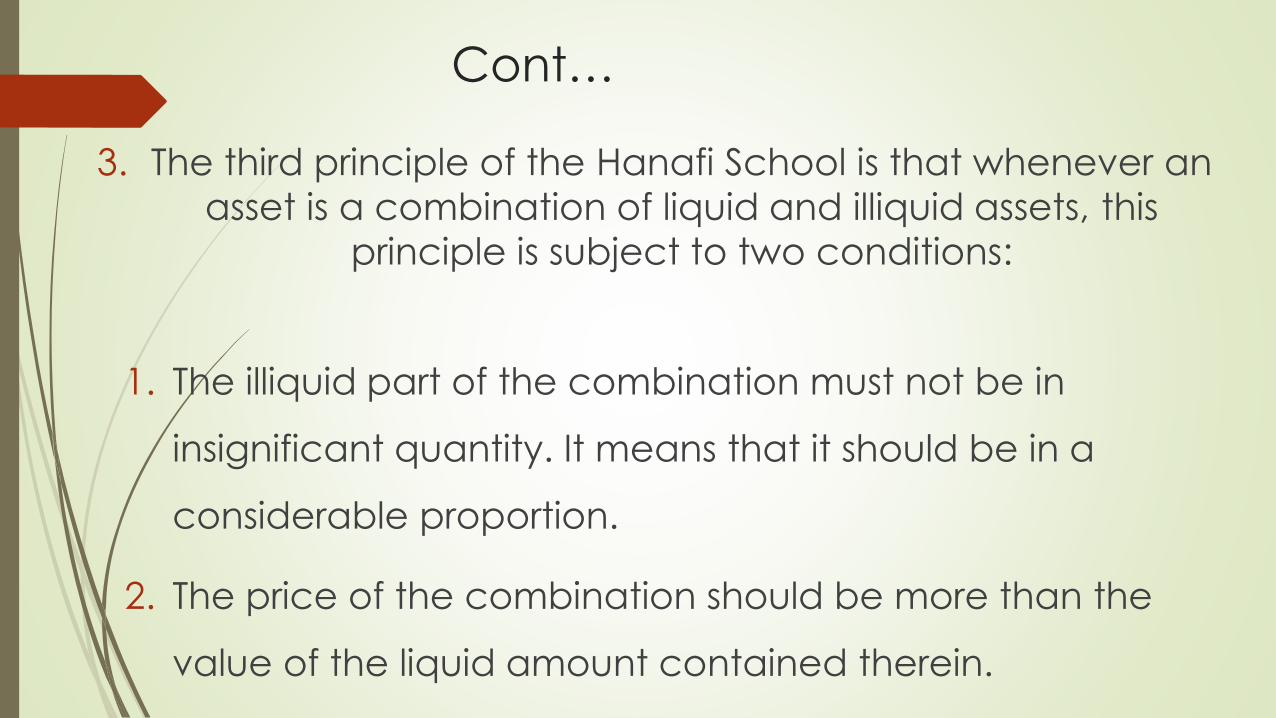

Cont…

3. The third principle of the Hanafi School is that whenever an

asset is a combination of liquid and illiquid assets, this

principle is subject to two conditions:

1. The illiquid part of the combination must not be in

insignificant quantity. It means that it should be in a

considerable proportion.

2. The price of the combination should be more than the

value of the liquid amount contained therein.

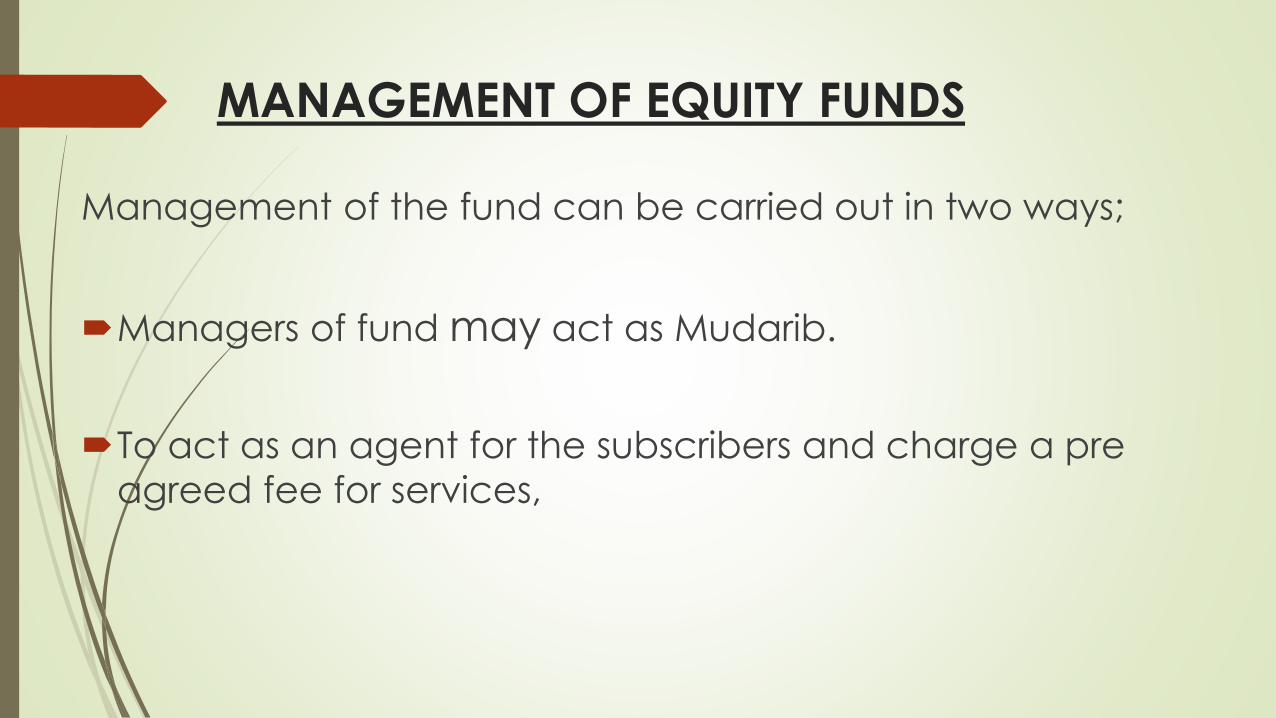

MANAGEMENT OF EQUITY FUNDS

Management of the fund can be carried out in two ways;

Managers of fund may act as Mudarib.

To act as an agent for the subscribers and charge a pre

agreed fee for services,

BAI'-AL-DAIN

Presented by :

MUHAMMAD AYUB

BAI'-AL-DAIN

Dain means "debt" and Bai' means sale. Bai'-al-dain,

therefore, it means the sale of debt

WHETHER OR NOT BAI'-AL-DAIN

IS ALLOWED IN SHARIAH

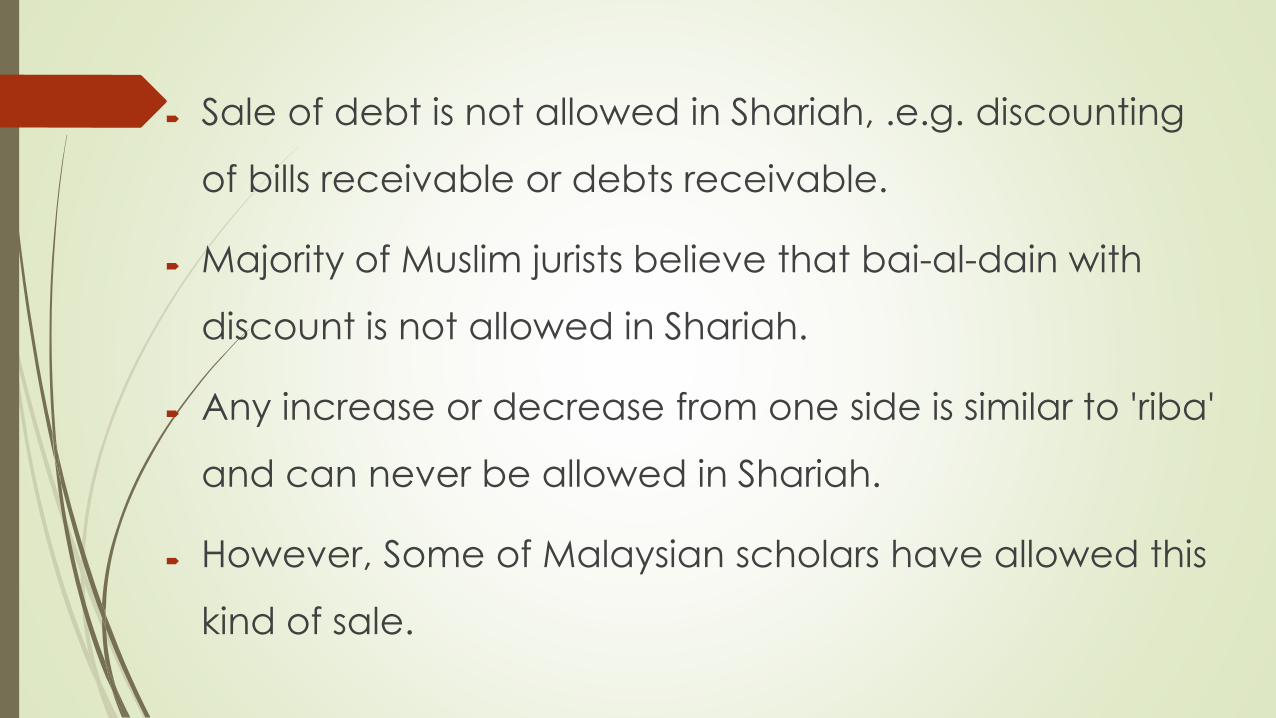

Sale of debt is not allowed in Shariah, .e.g. discounting

of bills receivable or debts receivable.

Majority of Muslim jurists believe that bai-al-dain with

discount is not allowed in Shariah.

Any increase or decrease from one side is similar to 'riba'

and can never be allowed in Shariah.

However, Some of Malaysian scholars have allowed this

kind of sale.

ACCORDING TO FIQH ACADEMY OF JEDDAH

AND MALAYSIA

The Islamic Fiqh Academy of Jeddah, which is the largest

representative body of the Shariah scholars and has the

representation of all the Muslim countries, including

Malaysia, has approved the prohibition of bai-al-dain

unanimously without a single dissent.

MIXED FUND

A fund where the subscription amount is invested in different

types of investments, like equities, leasing, commodities, etc.

Certificates of units of funds are tradable in the secondary market

only if the tangible assets are more than 51% while the liquidity

and debts are less than 50%.

Otherwise it will be a closed end fund.

WAQF

Presented by :

USMAN ALI

WAQF – INTRODUCTION

Waqf, in Arabic language, means hold, confinement or prohibition.

The word waqf is used in Islam in the meaning of holding certain property and preserving

it for the confined benefit of certain philanthropy and prohibiting any use or disposition of

it outside that specific objective.

In the history of Islam, the first religious waqf is the mosque of Quba’ in Madinah, a city 400

kilometer north of Makkah, which was built upon the arrival of the Prophet Muhammad in

622

DEFINITION OF WAQF

According to Waqf act 1954 sec 3(i):

“Waqf Means the permanent dedication by a person

professing islam of any movable and immovable

property for any purpose recognized by muslim law as

pious, religious or charitable.”

MANAGEMENT OF WAQF

The waqf manager is usually called “MUTAWALLI” and his\her

responsibility is to administer the waqf property to the best interest of

the beneficiaries.

The person who creates waqf is called Wqaif.

CONDITIONS OF WAQIF

Waqif may be male or female

Waqif must be sound mind.

Waqif must be the owner of the property.

Waqif must be the age of the maturity.

CONDITIONS OF MUTAWALLI

MUTAWALLI must be sound mind.

MUTAWALLI must be the age of the maturity.

MUTAWALLI must be a muslim

OWNERSHIP OF WAQF

From legal point of view, the ownership of waqf property lies outside the person who

created the waqf.

Some Muslim jurists argue that the right of ownership of waqf belongs to Allah.

Others believe that it belongs to the beneficiaries although their ownership is not complete

in the sense that they are not permitted to dispose of the property or use it in a way

different from what was decreed by the founder of waqf.

CHARACTERISTICS OF WAQF

perpetuity:

It means that once a property, often a real estate, is dedicated as waqf it remains waqf for ever.

Permanence of stipulations of waqf founder:

Since waqf is a voluntary act of benevolence, conditions specified by the founder must be fulfilled to

their letter as long as they do not contradict or violate any of the Shariah rulings.

LEGAL CONDITIONS OF WAQF

The property must be a real estate or a thing which has some meaning

of perpetuity.

The property should be given on a permanent basis. Some jurists approve

temporary waqf only in the case of family waqf.

The waqf founder should be legally fit and apt to take such an action,

The purpose of the waqf must, in the ultimate analysis be an act of

charity from both points of view of Sharicah and of the founder.

Finally, beneficiaries, person(s) or purpose(s), must be alive and

legitimate. Waqf on the dead is not permissible.

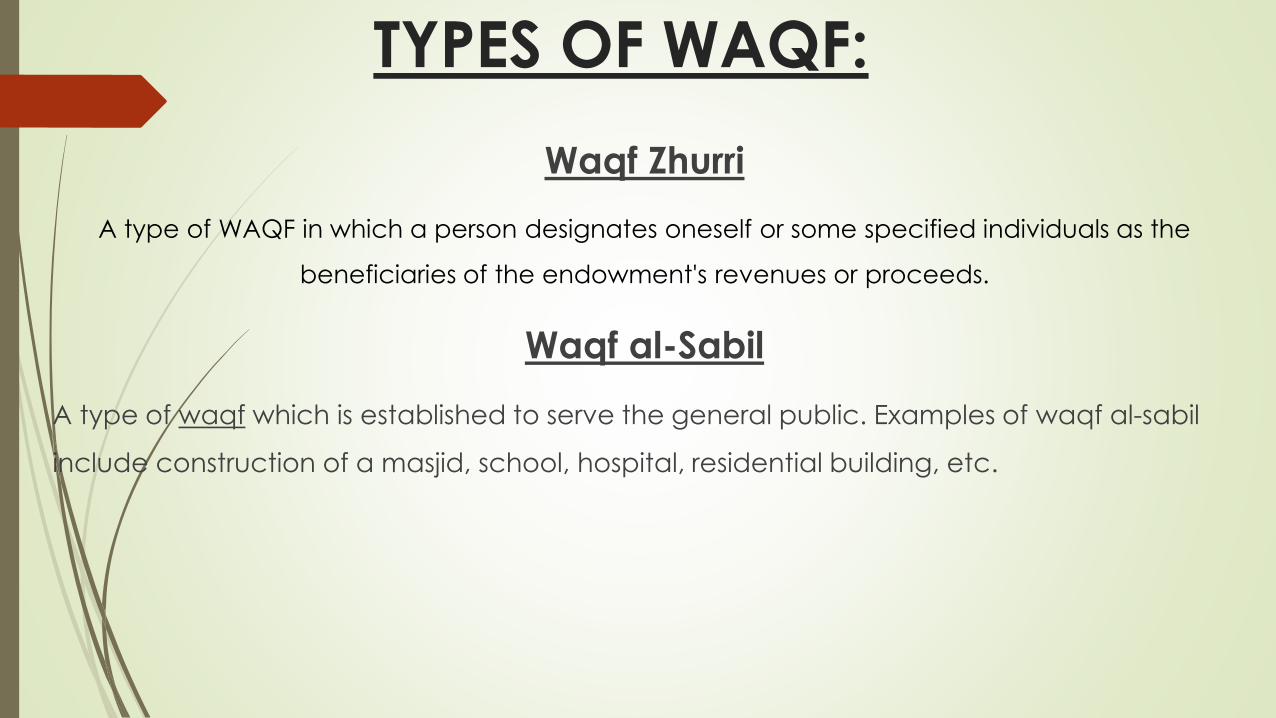

TYPES OF WAQF:

Waqf Zhurri

A type of WAQF in which a person designates oneself or some specified individuals as the

beneficiaries of the endowment's revenues or proceeds.

Waqf al-Sabil

A type of waqf which is established to serve the general public. Examples of waqf al-sabil

include construction of a masjid, school, hospital, residential building, etc.

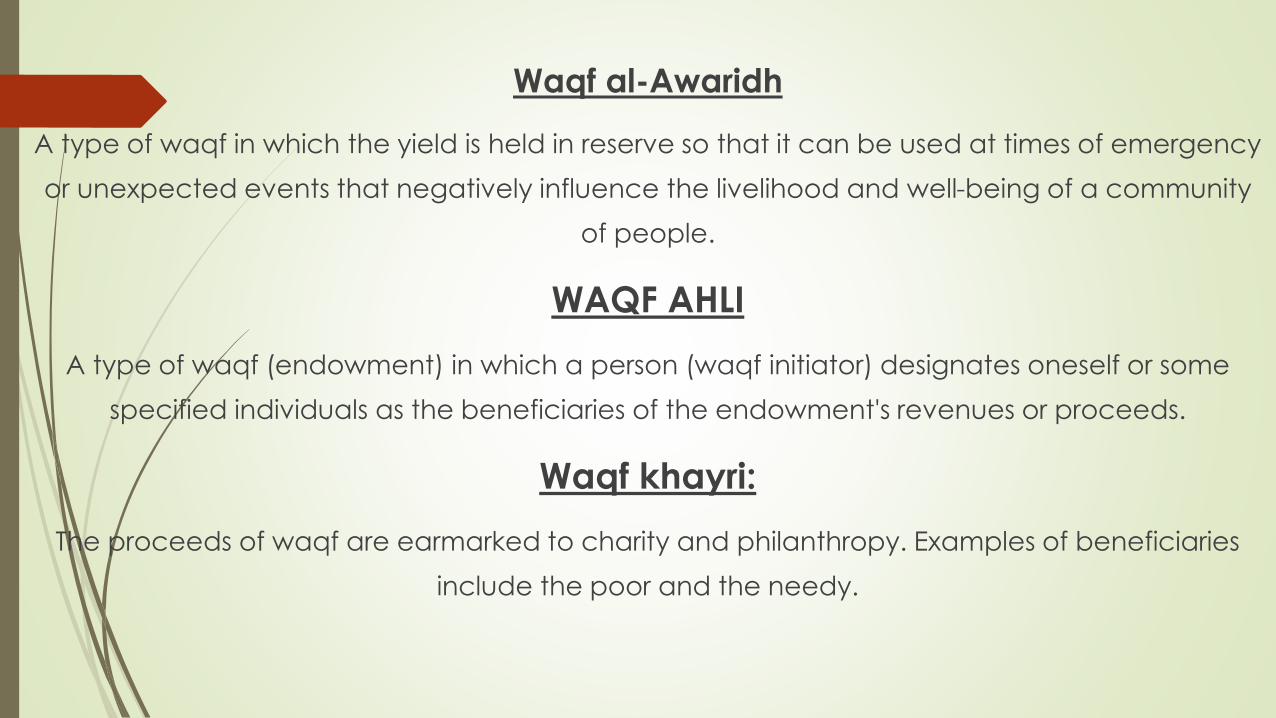

Waqf al-Awaridh

A type of waqf in which the yield is held in reserve so that it can be used at times of emergency

or unexpected events that negatively influence the livelihood and well-being of a community

of people.

WAQF AHLI

A type of waqf (endowment) in which a person (waqf initiator) designates oneself or some

specified individuals as the beneficiaries of the endowment's revenues or proceeds.

Waqf khayri:

The proceeds of waqf are earmarked to charity and philanthropy. Examples of beneficiaries

include the poor and the needy.

BAT-UL-MAL

Presented by :

UMER KHURSEED

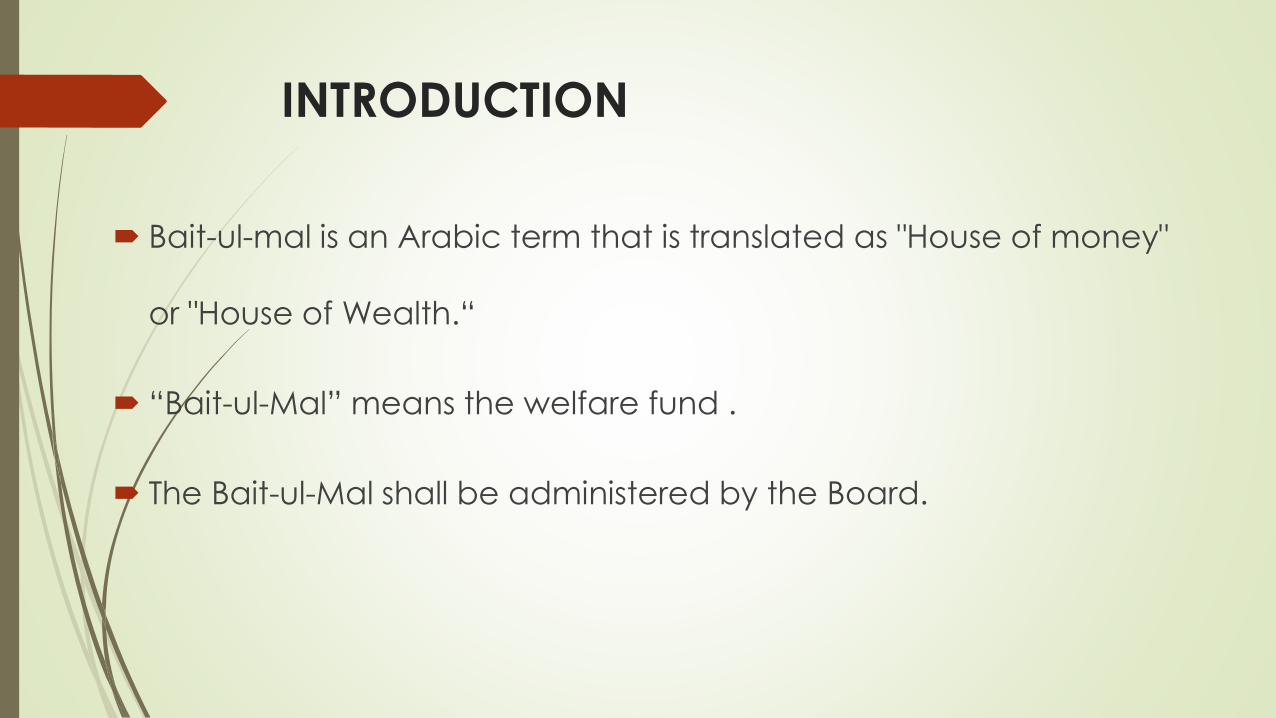

INTRODUCTION

Bait-ul-mal is an Arabic term that is translated as "House of money"

or "House of Wealth.“

“Bait-ul-Mal” means the welfare fund .

The Bait-ul-Mal shall be administered by the Board.

HISTORY OF BAIT UL MAAL

Bait ul maal was developed as a financial institution in the Islamic states, this financial

institution used to administer the taxes.

The bait ul maal was established in the era of the Islamic caliphate.

It was formed as the royal reserves for sultans and caliphs; another purpose of bait ul

maal was to manage personal finances and the expenditures of the government.

Moreover, the bait ul maal was used to manage the distributions of zakat for the

public works.

HISTORY OF BAIT UL MAAL

During the reign of Hazrat Muhammad (SAW) a permanent bait ul maal

was not established

During the caliphate of Hazrat Abu Bakr bait ul maal was also not kept as

there was no prominent need for the reserves to be kept

Hazrat Umar established a permanent bait ul maal after consulting with

his companions

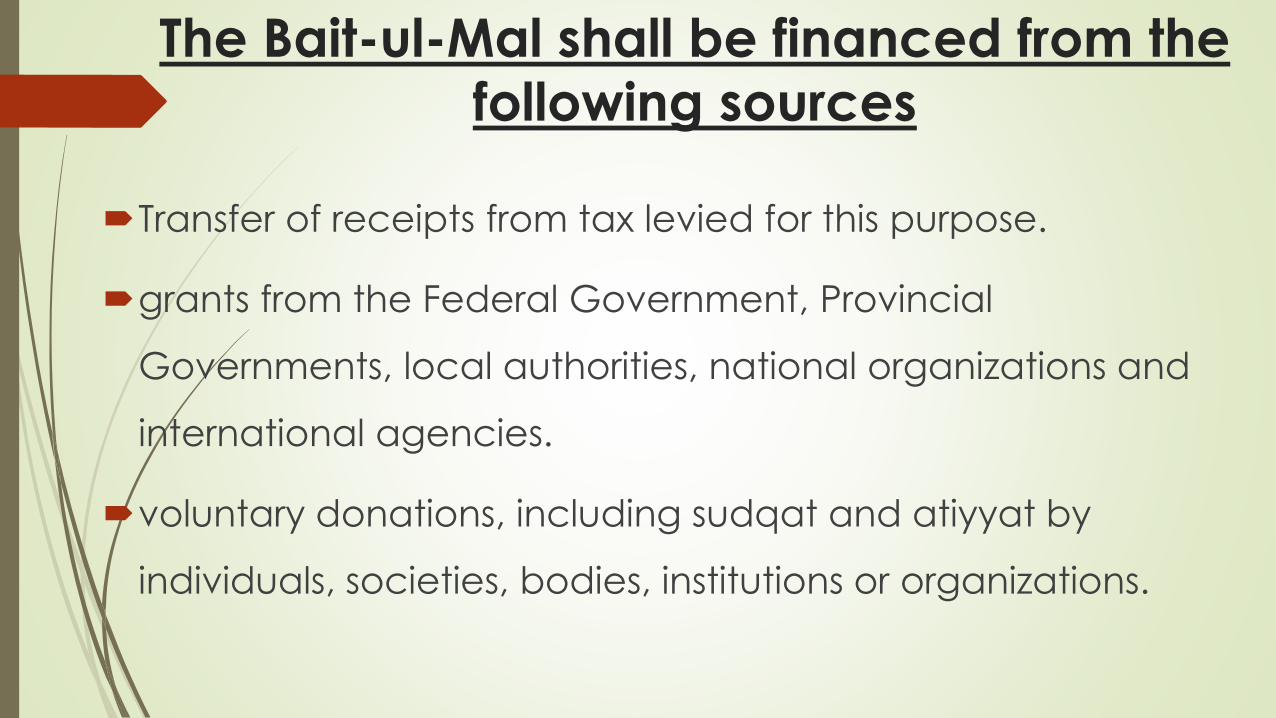

The Bait-ul-Mal shall be financed from the

following sources

Transfer of receipts from tax levied for this purpose.

grants from the Federal Government, Provincial

Governments, local authorities, national organizations and

international agencies.

voluntary donations, including sudqat and atiyyat by

individuals, societies, bodies, institutions or organizations.

The moneys in the Bait-ul-Mal shall be utilized

for the following purposes namely to provide financial assistance to destitute and needy widows, orphans,

invalid, infirm and other needy persons;

to provide residential accommodation and necessary facilities to the

persons specified.

to provide for free medical treatment for indigent sick persons and to set up

free hospitals, poor houses and rehabilitation centers and to give financial

aid to charitable institutions, including industrial homes and other

educational institutions established specially for poor and needy.

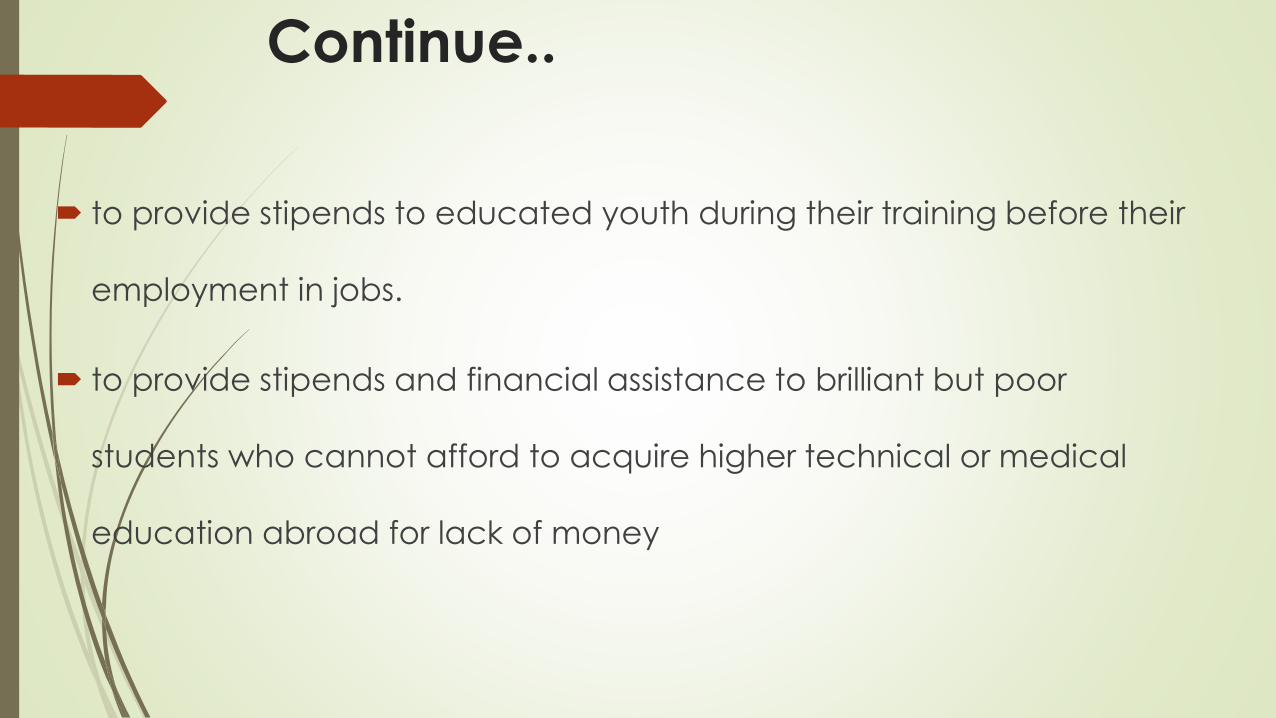

Continue..

to provide stipends to educated youth during their training before their

employment in jobs.

to provide stipends and financial assistance to brilliant but poor

students who cannot afford to acquire higher technical or medical

education abroad for lack of money

REALISTIC EVALUATION OF

ISLAMIC BANKING IN PAKISTAN

Presented by :

Saad Iftikhar wani

REALISTIC EVALUATION OF ISLAMIC BANKING IN PAKISTAN

Islamic banking has become today an undeniable reality.

The number of islamic banks and the financial institution is ever increasing in Pakistan.

New islamic banks with huge amount of capital are being established. Conventional banks

are opening Islamic windows or Islamic subsidiaries for the operation of islamaic banking.

It seems that the size of Islamic banking will be at least multiplied during the next decade

and the operation of islmic banks are expected to cover a large area of financial

transaction of Pakistan.

Cont……

Efforts to Islamize the economy of Pakistan started in the mid-60s. However a significant

attempt was made in the mid 80sto convert the banking system to an Islamic banking

system.

The Banking Companies Ordinance (BCO, 1962) was amended to accommodate non-

interest based transactions and the industry was given a specific timeline to convert to

the non-interest based system.

As at end of the year 2003 only one bank operated as a full-fledged Islamic bank

and three conventional banks were operating Islamic banking branches. Today there

are 6 full fledge licensed Islamic banks (IBs) and 12 conventional banks have licenses to

operate dedicated Islamic banking branches (IBBs).The total assets of the Islamic

banking industry are over PRs. 225 billion as of 30th June, 2008which accounts for a

market share of 4.5% of total banking industry assets.