islamic financial system: the malaysian experience · pdf fileislamic financial system: the...

TRANSCRIPT

ISLAMIC FINANCIAL SYSTEM: THE MALAYSIAN EXPERIENCE AND THE

WAY FORWARD

DR. MOHAMAD AKRAM LALDIN

Abstract

Islamic financial services are considered as one of the fast growing industry in Banking and

finance sector and has now gained wide acceptance as a form of financial intermediation. The

purpose of this paper is to elaborate the experience of Malaysia in developing the Islamic

Financial System by explaining the different developments that has taken place since its inception

in 1963 until now. The focus was on the different stages of the development in the Banking

System, Takaful (Islamic Insurance), Islamic capital market and Islamic Unit Trust in Malaysia.

Finally, the paper shares the ten key focal areas in the development of the 10 Year Master Plan

for Islamic Financial Services Industry laid down by the Central Bank Governor. The paper is

concluded by discussing the challenges ahead and the way forward in ensuring the excellence

future development of the industry. The methodology used in this paper is library research by

gathering the relevant information related to the subject from various sources particularly

presentations and conference papers and analyzing them accordingly. The paper found that

Malaysia has a very encouraging history of Islamic Banking and has big potential to succeed in

this area. However, there are some areas need to be improved as suggested in the paper. Finally,

this paper is important for those who would like to obtain an in depth exposure about the

development of Islamic Banking in Malaysia and to set up a benchmark with the development of

this industry in their respective country.

Key Words: Banking History, Islamic Banking, Malaysia, Pilgrimage fund, Islamic

Capital Market, Takaful, Master plan

Type of Paper: General review

Introduction

Islam is a comprehensive way of life, which strikes the balance between the spiritual and

the material need of human being. One of the important aspects in human life is the need

for a comprehensive system in order to govern their life and to ensure all the needs are

2

catered adequately including the material needs such as the financial management. This

aspect of life is closely related to the fast growing industry in the world nowadays, which

is the Islamic financial services industry.

Looking at the history of Islamic financial institutions, it started with a number of interest

free saving and loan societies which are reported to have been established in the Indian

subcontinent during 1940s. But efforts to arrange finance for business enterprises seem to

have started later. Among the pioneering experience in this sector is the establishment of

Pilgrimage Fund Board in Malaysia. Money being saved for meeting the cost of the

pilgrimage to Makkah is profitably invested by this organization, which is still in

operation at present. In the private corporate sector, the early efforts begins with the

establishment of the Dubai Islamic Bank in 1975 under a special law allowing it to

engage in business enterprise while accepting deposits into checking accounts. Ten years

later, twenty seven more similar banks were established in the Gulf countries, Egypt,

Sudan, etc. Around the same time, over 50 conventional banks, some of them located at

money centers like London were offering Islamic financial products. This was followed

by some of the major conventional banks establishing Islamic branches dealing

exclusively in Islamic products. Citi-Islamic in Bahrain and Grindlays in Karachi were

followed by the National Commercial Bank in Saudi Arabia establishing over 50 Islamic

branches by 1990s. By the year 2000, there were 200 Islamic financial institutions with

over US $8 billion in capital, over US $100 billion in deposits, managing assets worth

more than $160 billion. About 40% of these activities and concentrated are in the Persian

Gulf and the Middle East, another 40% in South and South-East Asia, the remaining

equally divided between Africa and Europe and the Americas. Two thirds of these

institutions are very small, with assets less than US $100.1 At present, more than two

hundred and fifty Islamic financial institutions are operating world-wide and Islamic

banking is estimated to be managing funds up to the value of US$ 400 billion. The annual

growth of Islamic financial institutions has been estimated 15% worldwide over the past

10 years and is expected to accelerate in the foreseeable future.2

Encouraged by the above tremendous developments, this paper aims at highlighting the

different development that has taken place in the Islamic financial services institutions in

3

Malaysia. In addition, the paper intends to highlight the ten key strategies adopted by the

Malaysian Government in devising the ten years master plan for Islamic Financial

services industry.

Indeed, the development of the Islamic financial system in Malaysia started with the

establishment of Pilgrimage Fund (Tabung Haji) in 1963 as the first Islamic savings

institution. After a few years of break, the first full-fledged Islamic bank was established

in 1983 with the name Bank Islam Malaysia (Islamic Bank of Malaysia). As for the non

banking financial service institution, it begins with the establishment of the first Takaful

or Islamic insurance company under the Takaful Act in 1984. These developments were

subsequently expanded with the introduction of Islamic windows by conventional

banking institutions which began in 1993 where Islamic products and services could be

offered by the conventional banking institutions. In the same year, Islamic money market

has developed and considered was seen and this segment is one of the fastest growing

segments in Islamic financial instrument. In order to internationalize the Islamic Banking

industry and making Malaysia as Islamic financial hub, the Malaysian government has

started opening it market to international players in this field. It started by allowing

international banks which operates Islamic product to open their branches in Malaysia.

At present there are three international players which are Al-Rajhi Banking and

Investment Corporation, Kuwait Finance House and RUSD Bank-led consortium which

includes Qatar Islamic Bank and Global Investment House. The most recent

development is the Islamic subsidiaries which saw the interest of some conventional

banks to operate full fledge Islamic bank. At present, there are three Banks which are

operating as subsidiaries.

In order for the Islamic financial sector to be competitive and to ensure the vision of

making Malaysia as global financial hub, it is important to have adequate advance

planning in this area. Therefore, during the Seminar on the Ten-Year Master Plan for the

Islamic financial services industry organized by the Islamic Development Bank (IDB)

and the Islamic Financial Services Board (IFSB), the Malaysian Government has initiated

the drafting of the ten years master plan for the Islamic financial services industry. Two

4

important areas of focus namely, building institutional capacity and the development

of the supporting financial infrastructure has been identified as the strategic element

in the development of a progressive Islamic financial services. Ten key areas of the above

strategies have been identified in order to be success in the focus areas mentioned above.

The ten areas and the way forward will be discussed at the end of this paper.

Early Development (The Establishment of Pilgrims Fund Cooperation)

The early effort in developing the Islamic financial sector services in Malaysia begins

with the birth of the Pilgrims Fund Corporation or better known as „Tabung Haji” which

was established in November 1962 and commenced operation on September 30, 1963. Its

existence was also strongly attributed to a working paper presented by the Royal

Professor Ungku Aziz titled, “Plan to Improve the Economy of Prospective Pilgrims” in

1959. The idea was mooted out of the necessity to develop a mechanism to encourage the

Muslims to save for their pilgrimage as the Malaysian Muslims in the past had resorted to

various traditional means of saving and keeping their money for the sacred journey.

There were also those who sold their livestock and other properties in order to earn

sufficient fund for their pilgrimage. Such practices caused negative financial and social

implications on them and their families during and after their pilgrimage. In addition, it is

also damaging the rural economic structure and threatening the national economic

growth. Apart from the above reason, there was also need for an institution which can

guarantee the savings of Muslims are free from elements of usury and its activities are

done according to Shariah requirement.

The objectives of the establishment of Tabung Haji under Act 8 of Pilgrimage

Management and Fund Board 1969 are:

To enable Muslims to save gradually to support their expenditure during

pilgrimage and for other beneficial purposes

To enable Muslims to have active and effective participations in investment

activities permissible in Islam through their savings and

5

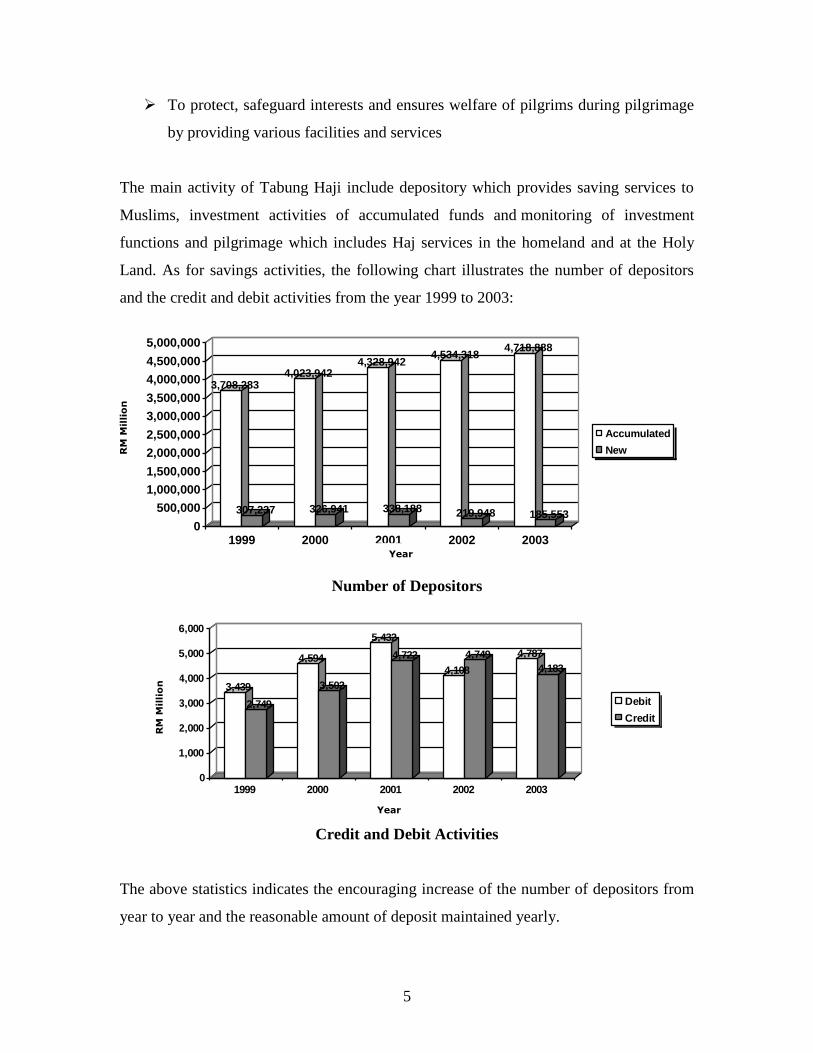

To protect, safeguard interests and ensures welfare of pilgrims during pilgrimage

by providing various facilities and services

The main activity of Tabung Haji include depository which provides saving services to

Muslims, investment activities of accumulated funds and monitoring of investment

functions and pilgrimage which includes Haj services in the homeland and at the Holy

Land. As for savings activities, the following chart illustrates the number of depositors

and the credit and debit activities from the year 1999 to 2003:

3,708,283

307,237

4,023,942

326,941

4,328,942

338,188

4,534,318

219,948

4,718,888

185,5530

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

1999 2000 2001 2002 2003

Accumulated

New

Number of Depositors

3,439

2,749

4,594

3,502

5,432

4,722

4,108

4,749 4,787

4,183

0

1,000

2,000

3,000

4,000

5,000

6,000

1999 2000 2001 2002 2003

Debit

Credit

Credit and Debit Activities

The above statistics indicates the encouraging increase of the number of depositors from

year to year and the reasonable amount of deposit maintained yearly.

RM

Mil

lio

n

Year

Year

RM

Mil

lio

n

6

With regard to the net asset value, net profit, bonuses and zakah paid, as of the end of

financial year 2003, the figures stands as follows:

Net asset value RM 11,635 million

Net profit RM 404 million

Bonus to the depositors RM 411 Million

Zakah RM 14.5 million.

The following charts illustrate the flow of the profit, asset value, bonus paid and zakah

paid from the year 1999 to 2003:3

459

338 336368

414

0

50

100

150

200

250

300

350

400

450

500

1999 2000 2001 2002 2003

Profit After Zakah

8,416

9,846

10,892 10,619

11,635

0

2,000

4,000

6,000

8,000

10,000

12,000

1999 2000 2001 2002 2003

Year

RM

Mil

lio

n

Year

RM

Mil

lio

n

7

Net Assets

543

455

322346

411

0

100

200

300

400

500

600

1999 2000 2001 2002 2003

1999 2000 2001 2002 2003

Bonus

Percentage

(%)

8.0 5.5 3.25 3.5 4.0

Bonuses for Depositors

19.320.2

13.515 14.5

0

5

10

15

20

25

1419 1420 1421 1422 1423

Zakah

In term of investment, one of the interesting aspects of Tabung Haji is that it has

diversified its investment activities in various Shariah compliance investment

instruments such as Bonds, Corporate Notes, Government Investment Certificates,

Mudharabah Bank Account and Bill of Acceptance. In addition, Tabung Haji's

investment in subsidiaries is part of its strategy to participate directly in potential and

viable sectors. Emphasis is given to the plantation, construction, real estate development,

and services sectors. The four subsidiaries fully owned by Tabung Haji are:

Year

RM

Mil

lio

n

Year Hijri

RM

Mil

lio

n

8

TH Plantations Sdn. Bhd. (plantation sector)

TH Technologies Sdn. Bhd. (construction sector)

TH Properties Sdn. Bhd. (real estate development sector)

TH Travel & Services Sdn. Bhd. (hajj, umrah, and tour services sector)

The investment and earnings of Tabung Haji is illustrated in the following chart:

INCOME RM

Million Percentage (%)

Profit from Shares Trading 131.32 18.94

Cash Investment and Mudharabah Profits 139.32 20.10

Shares Dividends 201.06 29.00

Rentals income 39.85 5.75

Subsidiaries Companies Profits 118.49 17.09

Profit from Asset Selling 38.57 5.56

Others 26.64 3.56

Total 639.25 100 %

INVESTMENT RM

Million Percentage (%)

Equity Investment 3,696.18 32.36

Public Listed Companies 877.73 7.68

Subsidiaries Companies 410.05 3.59

Financing of Subsidiaries Companies 1,284.96 11.25

Equity Investment 1,671.08 14.63

Mudharabah Investment 1,644.19 14.39

Investment in Immovable Assets 1,839.30 16.10

Total 11,423.49 100 %

Finally, Tabung Haji is considered as one of the popular investment institutions for

Malaysian Muslim as it offers very competitive bonus to the depositors. This very

foundation of the Islamic financial services in Malaysia indicates that this country has

9

taken a bold step in order to provide an Islamic alternative to the Muslims in order for

them to move forward towards building their future economics strength.

After the establishment of Tabung Haji, there has been a stagnant period for about twenty

years till the establishment of the first Islamic Bank in Malaysia. The second phase saw

the rapid development in Islamic Banking and Financial Services in Malaysia with the

establishment of several Islamic Banking and Financial Institutions.

Second Phase of Development

The encouraging success of Tabung Haji has prompted several organizations and

individuals interested in developing the Islamic Financial Services sector to put forward

suggestion to the Malaysian Government to establish a full fledge Islamic Bank. The

move begins with the recommendations from several conferences and meeting which has

prompted the government to establish a National Council which comprise of twenty

experts in the field in the year 1981 to study the idea of establishing Islamic financial

institution in Malaysia. The council submitted the following recommendation to the

Malaysian cabinet for their consideration:

To establish an Islamic financial institution based on the principles of Shariah.

The institution shall be registered as a limited company govern by the Malaysian

company act

Drafting of a special act which is called Islamic Banking Act that will govern the

activities of Islamic financial institution.

The Central Bank shall be the regulator that regulates the activities of the Islamic

financial institution based on the Islamic Banking Act.

The Islamic financial institution shall appoint Shariah Advisory Council which

will advice and ensure the activities carried out by the institution are in line with

Shariah requirements.4

10

Based on the above recommendation, the Malaysian Cabinet has endorsed the

establishment of the first Islamic Bank in Malaysia in the year 1983. The bank is named

as Bank Islam Malaysia Berhad (Islamic Bank of Malaysia) and is regulated by the

Islamic Banking Act 1983. One of the special features that distinct this bank with the

conventional banks is that it is registered under the Companies Act 1965 which regulates

the activities of the bank. This is mentioned in part VII section 55 of the Islamic Banking

Act 1983 which states:

“An Islamic bank which is incorporated under the Companies Act 1965 shall be subject

to the provisions of that Act as well as to the provisions of this Act, save that where there

is any conflict or inconsistency between the provisions of that Act and the provisions of

this Act the provisions of this Act shall prevail”.5

The advantages of incorporating Islamic bank under the Companies Act 1965 among

other allows the bank to carry out trading activities including owning of asset and

dispersing them. In addition, the act has made it mandatory for the bank to follow the

advice given by the Shariah Advisory Council in order to ensure that all its activities are

in line with Shariah requirement. This is stated in part II under section 13A (1) of the act

which reads:

“An Islamic bank may seek the advice of the Shariah Advisory Council on Shariah

matters relating to its banking business and the Islamic bank shall comply with the advice

of the Shariah Advisory Council”.6

The progress of Bank Islam Malaysia Berhad is very encouraging particularly after a

decade of operation and it was proved to be a viable banking institution with its activity

expanding rapidly throughout the country. The bank has expanded with a network of 80

branches and 1,200 employees and was listed on the Main Board of the Kuala Lumpur

Stock Exchange on 17 January 1992.

The above developments in Bank Islam Malaysia Berhad have prompted the Government

to look forward in expanding the Islamic Banking industry in the country. The authority

11

was aware of the fact that, in order for the Islamic Banking industry to be viable there are

four important elements that must be secured by the institutions namely:

large number of players;

a broad variety of instruments;

an Islamic money market and

a system that reflect the socio-economic values in Islam, and must be Islamic

in both substance and form.

Realizing the important of the above factor, the Malaysian Government has adopted a

step-by-step approach to achieve the above objective. The first step to spread the virtues

of Islamic banking was to disseminate Islamic banking on a nation-wide basis, with as

many players as possible and to be able to reach all Malaysians. After a careful

consideration of various factors, the Government decided to allow the existing banking

institutions to offer Islamic banking services using their existing infrastructure and

branches. The option was seen as the most effective and efficient mode of increasing the

number of institutions offering Islamic banking services at the lowest cost and within the

shortest time frame. Therefore, on 4 March 1993 the Central Bank introduced a scheme

known as "Skim Perbankan Tanpa Faedah" (Interest-free Banking Scheme) or SPTF in

short and was later known as Islamic windows in conventional banks.7 This arrangement

allows the conventional banks to offer Islamic product within their institutions. In order

to ensure the integrity of the banking operation, effective firewalls was implemented to

ensure complete segregation and no co-mingling between Islamic and conventional

portfolio. This was done by:

1. Establishment of Islamic Banking Division within the conventional

setup;

2. Allocation of capital for Islamic banking operations;

3. Segregation of Islamic funds from the conventional;

4. Separate clearing accounts;

5. Separate membership code to electronic transfer of funds and

securities system.

12

Apart from the operational excellence, the banks are required to appoint Shariah

consultants in order to advice and ensure their activities are in compliance with Shariah

requirements. Indeed, the implementation of such scheme has accelerated market

penetration nationwide and there was immediate increase in delivery channel with the

increase from three to fifty four participants in the span of six years. It is also cost

effective and contributes to the economies of scale and synergies in addition to

optimizing the existing banking infrastructure and resources. This Islamic banking

product can also compete effectively in a well entrenches financial system.8

The encouraging progress of Islamic financial institutions does not stop there, on 1

October 1999, a second full fledge Islamic bank, namely Bank Muamalat Malaysia

Berhad (BMMB) begins its operations. The establishment of BMMB was the effect of the

spin-off following the merger between Bank Bumiputra Malaysia Berhad (BBMB) and

Bank of Commerce (Malaysia) Berhad (BOCB). Under the merger arrangement, the

Islamic banking assets and liabilities of BBMB, BOCB and BBMB Kewangan Berhad

(BBMBK) were transferred to BBMB, while the conventional operations of BBMB,

BOCB and BBMBK were transferred to BOCB accordingly. In addition, BMMB was

given 40 branches of BBMB and BBMBK in various locations throughout Malaysia and

a staff workforce of 1,000, migrated from BBMB, BOCB and BBMBK.9

More recently, the industry has been strengthened. Conventional banking institutions that

have achieved a critical mass in their Islamic finance operations have the option to

transform their operations into a dedicated Islamic subsidiary. This means that, these

conventional banks operate a separate full fledge Islamic banks under the same banner. In

addition, the Government has also provided licenses for foreign Banks to operate full

fledge Islamic banks in Malaysia. Within this framework, Islamic finance in Malaysia has

proven to be resilient and able to function effectively and efficiently alongside the

conventional financial system. The ability of the Islamic banking institutions to arrange

and offer products with attractive and innovative features at competitive prices has

appealed to both Muslim and non-Muslim customers, reflecting the competitiveness of

Islamic finance as a form of financial intermediation.

13

Indeed, the numbers of Islamic financial institutions are increasing in Malaysia and the

current statistics lies as follows10

:

Full fledge Malaysian Islamic Banks:

1. Bank Islam Malaysia Berhad

2. Bank Muamalat Malaysia Berhad

Full fledged Foreign Islamic Banks:

1. Kuwait Finance House(Malaysia) Berhad

2. Al Rajhi Banking and Investment Corporation

3. Qatar Islamic Bank

Islamic Subsidiary:

1. Commerce TIJARI Bank Berhad

2. Hong Leong Islamic Bank Berhad

3. RHB Islamic Bank Berhad

Participating banks in the Islamic Banking Scheme (Islamic Windows)

Commercial Banks:

1. Affin Bank Berhad

2. Alliance Bank Berhad

3. AmBank (M) Berhad

4. Citibank Berhad

5. EON Bank Berhad

6. HSBC (Amanah) Bank (M) Berhad

7. Malayan Banking Berhad

8. OCBC Bank (Malaysia) Berhad

9. Public Bank Berhad

10. Southern Bank Berhad

14

11. Standard Chartered Bank Malaysia Berhad

Finance Companies:

1. Southern Finance Berhad

Merchant Banks:

1. Affin Merchant Bank Berhad

2. Alliance Merchant Bank Berhad

3. AmMerchant Bank Berhad

4. Commerce International Merchant Bankers Berhad

Discount Houses:

1. Abrar Discounts Berhad

2. Affin Discount Berhad

3. Amanah Short Deposits Berhad

4. CIMB Discount House Berhad

5. KAF Discounts Berhad

6. Malaysia Discount Berhad

7. Mayban Discount Berhad

As for the growth since 2000, the domestic Islamic banking industry has been growing at

an average of 18% per annum in terms of assets. The recorded growth since year 2000 till

present is illustrated in the following chart11

:

Year IB CB FC MB DH SPI Total

2000 14,008,934 20,058,475 7,149,872 1,507,952 4,288,350 33,004,649 47,013,583

2001 17,404,759 27,026,076 9,821,594 1,352,925 3,747,833 41,948,428 59,353,187

2002 20,159,627 29,109,751 12,622,883 1,429,589 4,748,576 47,910,799 68,070,426

2003 20,929,723 36,829,959 17,915,089 1,715,826 4,826,243 61,287,117 82,216,840

2004 24,857,416 53,912,593 7,819,857 2,552,364 5,843,826 70,128,640 94,986,056

Sep- 41,687,000 55,595,000 953,000 1,932,000 5,878,000 64,358,000 106,045,000

15

05

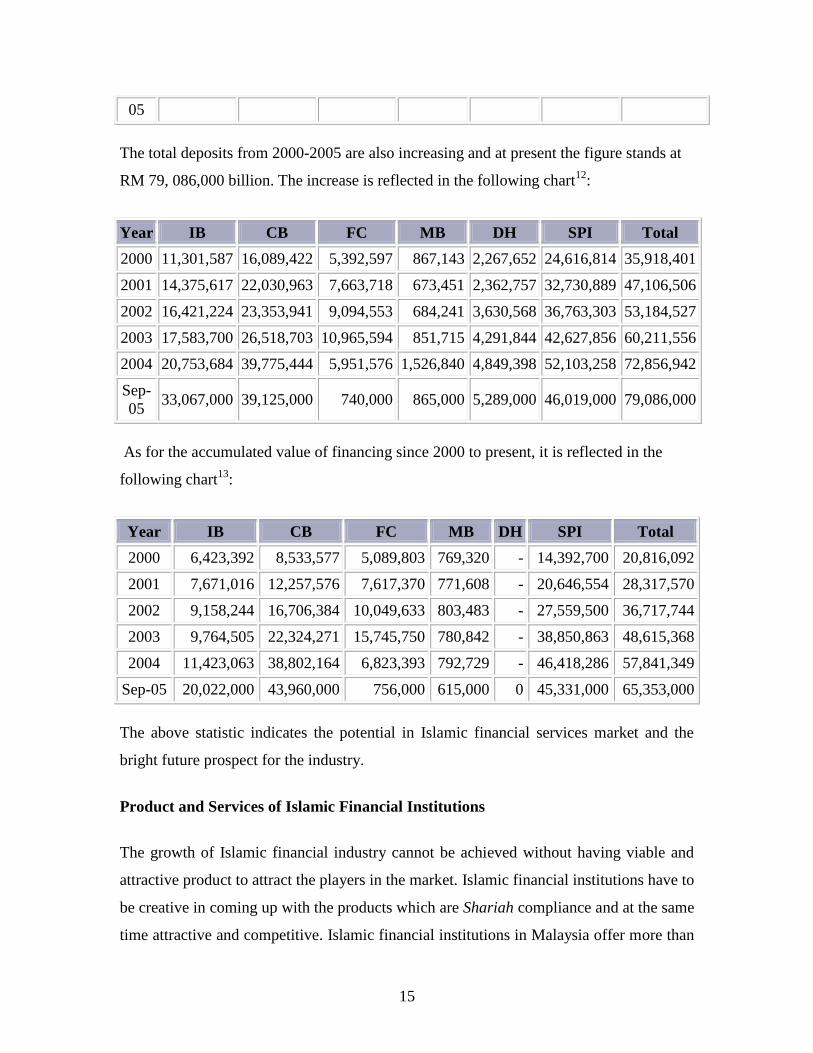

The total deposits from 2000-2005 are also increasing and at present the figure stands at

RM 79, 086,000 billion. The increase is reflected in the following chart12

:

Year IB CB FC MB DH SPI Total

2000 11,301,587 16,089,422 5,392,597 867,143 2,267,652 24,616,814 35,918,401

2001 14,375,617 22,030,963 7,663,718 673,451 2,362,757 32,730,889 47,106,506

2002 16,421,224 23,353,941 9,094,553 684,241 3,630,568 36,763,303 53,184,527

2003 17,583,700 26,518,703 10,965,594 851,715 4,291,844 42,627,856 60,211,556

2004 20,753,684 39,775,444 5,951,576 1,526,840 4,849,398 52,103,258 72,856,942

Sep-

05 33,067,000 39,125,000 740,000 865,000 5,289,000 46,019,000 79,086,000

As for the accumulated value of financing since 2000 to present, it is reflected in the

following chart13

:

Year IB CB FC MB DH SPI Total

2000 6,423,392 8,533,577 5,089,803 769,320 - 14,392,700 20,816,092

2001 7,671,016 12,257,576 7,617,370 771,608 - 20,646,554 28,317,570

2002 9,158,244 16,706,384 10,049,633 803,483 - 27,559,500 36,717,744

2003 9,764,505 22,324,271 15,745,750 780,842 - 38,850,863 48,615,368

2004 11,423,063 38,802,164 6,823,393 792,729 - 46,418,286 57,841,349

Sep-05 20,022,000 43,960,000 756,000 615,000 0 45,331,000 65,353,000

The above statistic indicates the potential in Islamic financial services market and the

bright future prospect for the industry.

Product and Services of Islamic Financial Institutions

The growth of Islamic financial industry cannot be achieved without having viable and

attractive product to attract the players in the market. Islamic financial institutions have to

be creative in coming up with the products which are Shariah compliance and at the same

time attractive and competitive. Islamic financial institutions in Malaysia offer more than

16

40 Islamic financial products and services that may be offered by the banks using various

Islamic concepts such as Mudharabah, Musyarakah, Murabahah, Bai’ Bithaman Ajil

(Bai’ Muajjal), Ijarah, Qardhul Hasan, Istisna’ and Ijarah Thumma Al-Bai’. Among the

product and the concepts used are as follows:

Deposit

Products / Services Applicable Concepts

Current account- i Wadiah Yad Dhamanah/Mudharabah

Savings account-i Wadiah Yad Dhamanah/Mudharabah

General investment account-i Mudharabah

Special investment account-i Mudharabah

Specific investment account-i Mudharabah

Financing

Products / Services Applicable Concepts

Benevolent loan-i Qard

Block discounting-i Bai' Dayn

Bridging finance-i Istisna'/Bai Bithaman Ajil

Bungalow lots financing-i Bai' Bithaman Ajil

Cash line facility-i Bai' Inah/Bai' Bithaman Ajil/Murabahah

Club membership financing-i Bai' Bithaman Ajil

Computer financing-i Bai' Bithaman Ajil

Contract financing-i Murabahah/Bai' Bithaman Ajil/Istisna

Education financing-i Murabahah /Bai' Bithaman Ajil /Bai' Inah

Equipment financing-i Bai' Bithaman Ajil

Factoring facility-i Bai' Dayn

Fixed asset financing-i Bai Bithaman Ajil

Floor stocking financing-i Murabahah/Bai' Bithaman Ajil

Hire purchase agency-i Wakalah

Hire purchase-i Ijarah Thumma Bai'

Home/house financing-i Bai' Bithaman Ajil/Istisna'/Variable Rate

Ijarah

Industrial hire purchase-i Ijarah Thumma Bai'

Land financing-i Bai' Bithaman Ajil

17

Leasing-i Ijarah

Pawn broking-i Rahnu (Qard and Wadiah Yad

Dhamanah)/Rahnu

Personal financing-i Bai' Bithaman Ajil/Murabahah/Bai' Inah

Plant & machinery financing-i Bai' Bithaman Ajil/Istisna'/Variable Rate

Ijarah

Project financing-i Bai' Bithaman Ajil/Istisna/Ijarah

Property financing-i Bai' Bithaman Ajil/Istisna'/Variable Rate

Ijarah

Revolving credit facility-i Bai Bithaman

Ajil/Murabahah/Hiwalah/Bai' Inah

Share financing-i Bai' Bithaman Ajil/Bai'Inah

Shop house financing-i Bai' Bithaman Ajil/Istisna'/Variable Rate

Ijarah

Sundry financing-i Bai' Bithaman Ajil

Syndicated financing-i Istisna'/Bithaman Ajil/Ijarah Thumma Bai'

Term financing-i Bai' Bithaman Ajil

Tour financing-i Bai' Bithaman Ajil

Umrah & visitation financing-i Bai' Bithaman Ajil

Working capital financing-i Murabahah/Bai' Bithaman Ajil

Treasury / Money Market Investment

Products / Services Applicable Concepts

Government investment issues-i Bai' al-Inah

Malaysian Islamic treasury bills Bai' al-Inah

Bank Negara negotiable notes-i Bai' al-Inah

Cagamas papers Bai Bithaman Ajil Mudaharabah

Commercial papers-i Murabahah

Negotiable debt certificate-i Bai' Bithaman Ajil

Negotiable instrument of deposit-i Mudaharabah

Sell and buy back agreements (Repo-i) Bai' al-Inah

Foreign exchange Ujr

Trade Financing

Products / Services Applicable Concepts

18

Accepted bills-i Murabahah/Bai' Dayn

Bank guarantee-i Kafalah

Export credit refinancing-i Murabahah/Bai' Dayn

Letter of credit-i Wakalah/Murabahah/Ijarah/Bai' Bithaman

Ajil

Shipping guarantee-i Kafalah

Trust receipt-i Wakalah/Murabahah

Card Services

Products / Services Applicable Concepts

Charge card-i Qard

Credit card-i Bai' Inah/Bai' Bithaman Ajil

Debit card-i Ujr

Banking Services

Products/Services Applicable Concepts

Stockbroking services Ujr

TT/funds transfer Ujr

Travellers' cheques Ujr

Cashiers' order Ujr

Demand draft Ujr

Standing instruction Ujr

ATM service Ujr

Telebanking Ujr

Developments of Islamic Capital Market (ICM)

The creation of Islamic money market and capital market is another landmark

development in the area of Islamic finance in Malaysia. A wide range of instruments has

been developed to facilitate the effective management of liquidity and funding by the

Islamic financial institutions. This has facilitated the smooth flow of funds in the Islamic

19

financial system. The development of the bond market in Malaysia is very encouraging in

which it now accounts for 81% of GDP, the Islamic private debt securities account for

about 44% of the total outstanding amount of private debt securities in the market, while

the monthly traded volume of the Islamic money market is now about RM30 to RM40

billion. The money market also effectively serves as a channel for the conduct of liquidity

operations by Bank Negara Malaysia as part of its monetary policy. The Government of

Malaysia has been very supportive in the development of ICM. In 2001, the Minister of

Finance launched the Capital Market Master plan and one of the six strategic initiatives in

the plan was to establish Malaysia as an international centre for Islamic capital market

activities.

The rapid development of Islamic Capital Market (ICM) started in 1990 when Shell

MDS Sdn Bhd issued the country's first Islamic bond. In 1994, Malaysia's first full-

fledged Islamic stock broking company, BIMB Securities Sdn, Bhd, was formed. With

the increasing prospects for Islamic securities, the Securities Commission of Malaysia

(SC) established the Islamic Capital Market Unit which comprises researchers trained in

both Fiqh Muamalat and capital market practices to undertake research on product

origination and Islamic capital market operations. This was followed by the formation of

the Securities Commission's (SC) Shariah Advisory Council (SAC) in 1996, comprising

Islamic scholars, academicians and Islamic finance experts, whose role was to advise the

SC on Shariah related matters for ICM activities. The SAC introduced the first Shariah

approved securities, which was listed on the Kuala Lumpur Stock Exchange (now known

as Bursa Malaysia) in June 1997.

The development of the ICM intensified when the Malaysia Securities Exchange Berhad

(now known as Bursa Malaysia Securities Berhad) launched the country's Islamic equity

index, the KLSE Shariah Index, in 1999. The index includes all Main Board shares

that are on the Shariah approved securities list. In addition, the Securities Commission

introduced an official list of Shariah-approved securities that are traded on Bursa

Malaysia. The criteria for Shariah-approved securities are based on the nature of the core

activities of a company. This list is updated twice a year, in April and October.

20

In the development of ICM in Malaysia, the regulators and authorities play an important

role as they exist to maintain the confidence of the public, particularly amongst Muslims,

on the halal status of the financial products in the marketplace, thus offering Muslim

investors peace of mind knowing that their investments are made according to Shariah

law.

Bursa Malaysia’s (Malaysia Bourse) Shariah Market

The Bursa Malaysia Shariah Market trades only Shariah approved stocks and as at 31

May 2005 there are 816 stocks which are Shariah compliant. These stocks represent the

components of Bursa Malaysia‟s Shariah Index, amounting to 82.5% of the total listed

companies or 64.0% of the market capitalization. These Shariah compliant stocks are

derived from all 3 sub-markets within Bursa, namely the Main Board, Second Board and

the MESDAQ market. In fact, 36% of all Shariah listed equity funds in the world are

listed in Bursa Malaysia and as at 31 December 2004 the total value of these funds stood

at US$1.8 billion compared to a total of US$5.0 billion worldwide.14

List of Major Sukuk

The encouraging development in the ICM has encouraged major market players to issue sukuk

(Islamic bonds) and some of the major sukuk issued since 1997 to 2005 are listed below:

1. In 1997, Khazanah Nasional Berhad launched the Khazanah Murabahah Bond,

which is a zero coupon bond based on murabahah and bay’ al-dayn concept.

2. In 2002, Kumpulan Guthrie Bhd issued a US$150 million sukuk ijarah: the first

global corporate Islamic bond issue ever recorded. The issue was listed on the

Labuan International Financial Exchange (LFX) and constituted the first tranche

of a US$395 million sukuk ijarah programme.

3. The Malaysian government launched a landmark sukuk ijarah bond issue

(Malaysian Global Sukuk) worth US$600 million, becoming the first country in

21

the world to issue a global sovereign Islamic bond in 2002

4. In 2004, Sarawak Corporate Sukuk Inc a special purpose vehicle established by the

Sarawak Economic Development Corporation (SEDC) launched a maiden five -

year US$350 million global sukuk ijarah.

5. International Finance Corporation (IFC), the private arm of the World Bank issued

RM500 million Islamic bonds, which was the first issuance of ringgit-

denominated Islamic bonds by a supranational body in 2004

6. In 2005, The World Bank issued RM760 million Islamic bonds that will mature

in 2010. This ringgit-denominated issue is the largest supranational deal in the

ringgit bond market.15

Legal Framework and Tax Incentives

The strengthening of the legal framework and tax incentive is also important in

developing a viable Islamic capital market. Realizing the important of this area, the

Malaysian government, in its Federal Budget 2003, allowed tax deduction for five

years on expenses incurred in the issuance of Islamic bonds, based on the Shariah

principles of ijarah mudharabah and musyarakah. More comprehensive tax treatment

for Islamic securities, similar to that for conventional securities, was announced in the

Federal Budget 2004 including the allowance of tax deduction for five years on

expenses incurred in the issuance of Islamic bonds based on the Shariah principle of

istisna'. Additional tax measures were announced in Budget 2005 to remove any tax or

duty on Islamic capital market products, provided that such products were approved by

the Shariah Advisory Committee of the Securities Commission. In order to strengthen

the regulatory framework, the SC released the Guidelines on the Offering of Islamic

Securities (IS Guidelines). The IS Guidelines introduced an "umbrella" framework for

Islamic securities, enabling and facilitating the development of a more innovative and

sophisticated Islamic capital market in Malaysia.

Islamic Unit Trust Funds

22

Another important area that was developed in this respect is the Islamic unit trust funds being an

integral part of the Islamic Capital Market (ICM). Islamic funds are funds managed in compliance

with Shariah principles; and invested only in Shariah approved financial assets such as Shariah

approved stocks (halal counters), Islamic bonds, Islamic deposits and money market instruments.

Islamic funds typically engage Shariah boards to advise and ensure that the investment operations

and portfolios are managed in accordance to Shariah principles. In Malaysia, the retention of

Shariah boards for Islamic funds is required by the law.

The emergence of Islamic funds in Malaysia has been a relatively recent development, in

comparison with the more established and broader conventional unit trust funds. Local Islamic

funds have only been in existence since the launch of the first Islamic equity fund namely, Arab-

Malaysian Tabung Ittikal managed by Arab-Malaysian Unit Trust Berhad in 1993. Since

then, however, the Islamic unit trust segment has grown tremendously. Such funds have become an

increasingly popular way for investors to participate in the ICM.

According to the Central Bank of Malaysia (Bank Negara Malaysia), the Islamic fund segment of

the unit trust industry has grown by leaps and bounds in recent years. This has been independently

verified by Lipper Asia Ltd which reported that in 2004, 14 new Islamic funds were launched,

representing 23% of the 61 new fund offerings, and were among the most successful products in

terms of unit subscriptions (take-up rate). The Net Asset Value (NAV) of Malaysian Islamic funds

also grew substantially in 2004, swelling by almost 40% to RM 6.0 billion, with a total of 59

Islamic unit trust schemes available on the market, comprising 15.8% of private unit trust funds.

According to data posted in Federation of Malaysian Unit Trust Managers website (www

fmutm.com.my), the total NAV of Islamic private sector funds has increased from RM 465.36

million in 1998 to RM 6,008.09 million in 2004.16

Development of Takaful (Islamic Insurance)

The growth in Islamic financial services in Malaysia is not limited to banking and finance

institution and money market. It has developed to include another important product that

23

is Islamic insurance or widely known as Takaful.The concept of Takaful (Islamic

insurance) was first introduced in Malaysia in 1985 when the first Takaful operator was

established to fulfil the need of the general public to be protected based on the Islamic

principles. The legal basis for the establishment of Takaful operators was the Takaful Act

which came into effect in 1984. Takaful in Malaysia follows the concept in Shariah

whereby a group of participants mutually agree among themselves to guarantee each

other against defined loss or damage that may inflict upon any of them by contributing as

tabarru’ or donation in the Takaful funds. Tabarru‟ is the agreement by a participant to

relinquish as donation, a certain proportion of the Takaful contribution that he agrees or

undertakes to pay, thus enabling him to fulfil his obligation of mutual help and joint

guarantee should any of his fellow participants suffer a defined loss. The concept of

tabarru‟ eliminates the element of uncertainty in the Takaful contract. The sharing of

profit or surplus that may emerge from the operations of Takaful is made only after the

obligation of assisting the fellow participants has been fulfilled. Thus, the operation of

Takaful may be envisaged as a profit sharing business venture between the Takaful

operator and the individual members of a group of participants.

Types of Business

The Takaful businesses carried out by the Malaysian Takaful operators are broadly

divided into family Takaful business (Islamic "life" insurance) and general Takaful

business (Islamic general insurance).

Family Takaful Business

In general, a family Takaful plan is a combination of long-term investment and mutual

financial assistance scheme. The objectives of this plan are: -

to save regularly over a fixed period of time;

to earn investment returns in accordance with Islamic principles; and

to obtain coverage in the event of death prior to maturity from a mutual aid

scheme.

24

Each contribution paid by the participant is divided and credited into two separate

accounts, namely the participants' special account (PSA) and the participants'

account (PA). A certain proportion of the contribution is credited into the PSA on the

basis of tabarru'. The amount depends on the age of the participant and the cover period.

The balance goes into the PA which is meant for savings and investments only.

Examples of covers available under family Takaful business are as follows: -

Individual family Takaful plans;

Takaful mortgage plans;

Takaful plans for education;

Group Takaful plans; and

Health/Medical Takaful.

General Takaful Business

The general Takaful scheme is purely for mutual financial help on a short-term basis,

usually 12 months to compensate its participants for any material loss, damage or

destruction that any of them might suffer arising from a misfortune that might inflict

upon his properties or belongings. The contribution that a participant pays into the

general Takaful fund is wholly on the basis of tabarru'. If at the end of the period of

Takaful, there is a net surplus in the general Takaful fund, the same shall be shared

between the participant and the operator in accordance with the principle of al-

Mudharabah, provided that the participant has not incurred any claim and/or not received

any benefits under the general Takaful certificate.

The various types of general Takaful scheme provided by the Takaful operators include: -

Fire Takaful Scheme;

Motor Takaful Scheme;

Accident/Miscellaneous Takaful Scheme;

Marine Takaful Scheme; and

Engineering Takaful Scheme.

25

Takaful Operators in Malaysia

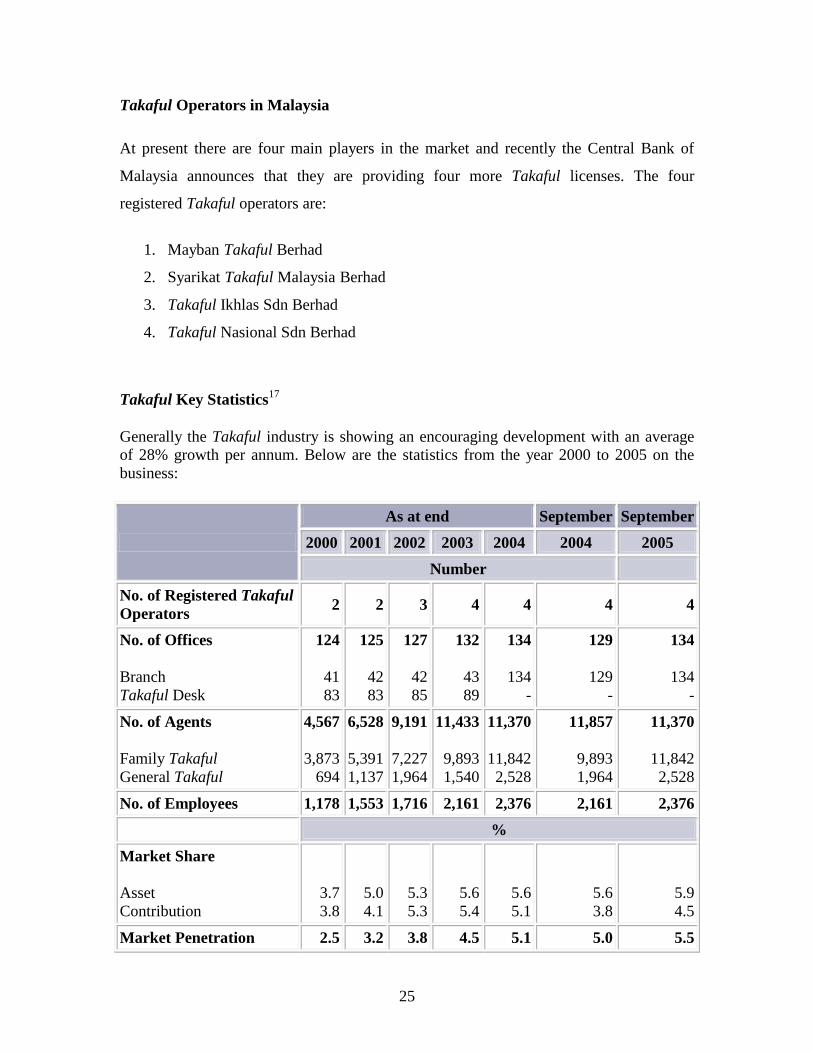

At present there are four main players in the market and recently the Central Bank of

Malaysia announces that they are providing four more Takaful licenses. The four

registered Takaful operators are:

1. Mayban Takaful Berhad

2. Syarikat Takaful Malaysia Berhad

3. Takaful Ikhlas Sdn Berhad

4. Takaful Nasional Sdn Berhad

Takaful Key Statistics17

Generally the Takaful industry is showing an encouraging development with an average

of 28% growth per annum. Below are the statistics from the year 2000 to 2005 on the

business:

As at end September September

2000 2001 2002 2003 2004 2004 2005

Number

No. of Registered Takaful

Operators 2 2 3 4 4 4 4

No. of Offices

Branch

Takaful Desk

124

41

83

125

42

83

127

42

85

132

43

89

134

134

-

129

129

-

134

134

-

No. of Agents

Family Takaful

General Takaful

4,567

3,873

694

6,528

5,391

1,137

9,191

7,227

1,964

11,433

9,893

1,540

11,370

11,842

2,528

11,857

9,893

1,964

11,370

11,842

2,528

No. of Employees 1,178 1,553 1,716 2,161 2,376 2,161 2,376

%

Market Share

Asset

Contribution

3.7

3.8

5.0

4.1

5.3

5.3

5.6

5.4

5.6

5.1

5.6

3.8

5.9

4.5

Market Penetration 2.5 3.2 3.8 4.5 5.1 5.0 5.5

26

Ten Years Master Plan for Financial Sector

The Government of Malaysia has announced its ten year master plan for financial sector

which comprises of three stages of plan. The objective of the first phase which extended

from 2001 to 2004 was to strengthen the operational and institutional infrastructure

whereas phase two which stretches from 2005 to 2007 will focus on stimulating

competition. The final stage that extends from 2008 to 2010 will mainly geared towards

progressive liberalization and effective infrastructure. As far as the Islamic financial

sector is concern, it is important to have a master plan for the reason mentioned by the

Governor of Malaysian Central Bank:

“Islamic finance is now taking on a new dimension to meet the changing requirements of

consumers and businesses; to participate in a more liberalized and globalize environment

and to become increasingly more internationally integrated. The financial system is also

operating in an era of change. Indeed, the national and international financial landscape is

being shaped by powerful forces of change, creating an environment of increased

uncertainty. However, with clarity of vision on the ultimate goals that the financial

system aims to achieve, we can, by our actions and initiatives taken today, help realize

our vision of the future”18

.

Thus, the master plan will help in providing a common vision, and template for countries

in developing the Islamic financial services industry. In addition, it will also serve as a

key reference document to guide countries in charting an orderly development of the

Islamic financial system. A master plan that has a meaningful role in a nation's future

economic and social development requires well-defined strategies that focus on two main

areas, building institutional capacity and the development of the supporting financial

infrastructure. There are ten key focal areas of the strategies that have been identified as

follows:

27

1. Identifying the nature of Islamic banking system that is appropriate for the

country - whether to ultimately adopt a dual banking system where Islamic banks

and conventional banks offering Islamic banking products operate in parallel with

the conventional banking system, or alternatively to adopt a single banking

system that fully accords the Shariah injunctions where all the banks are Islamic.

2. Ensuring that the Islamic banks are well-capitalized and resilient. For Islamic

banks that are already in existence, clear criteria need to be specified on the

minimum capital size that would enable them to be significant players in the

market, be able to gain from economies of scale, have a diversified earnings base

and stronger market presence. Such minimum size can either be achieved through

organic growth or merger with a partner bank which would bring about the

desired outcome in a shorter period of time. Incentives can be provided to induce

the banks to consolidate while guidelines on minimum capital size can be

imposed to ensure that the banks either merge or undergo a recapitalization

exercise. In the case of countries that are just embarking on the introduction of

Islamic banks, this could be achieved by the issue of new Islamic banking

licenses.

3. For countries that have a dual banking system, where conventional banks are

allowed to offer Islamic banking products, there must be adequate firewalls to

ensure absolute separation of banking operations to avoid co-mingling

between the Islamic and conventional funds. This is to ensure the integrity of

Islamic banking operations and the sanctity of Islamic funds. The firewalls would

need to include separate capital funds, cheque clearing systems, clearing accounts

with the Central Bank, settlement accounts and reporting systems.

4. Stakeholders of Islamic institutions playing their role effectively and

efficiently to generate improvements in the entity. This includes strong

leadership in the management team that has a firm commitment toward

performance and capacity enhancements. In addition, investments in the requisite

28

talent and skills are essential to spearhead the development of Islamic financial

products.

5. Ensuring adequate and comprehensive legal infrastructure. Enactment of an

Islamic banking law is an important part of this process. For conventional banks

offering Islamic banking products, amendments to the existing banking legislation

may be necessary to allow such banks to undertake trade-related activities and

other multi-faceted functions. The investment policy of the Government may need

to be reviewed to provide for the issue of Islamic investment instruments to

facilitate the liquidity operations of such banking institutions. In addition, a legal

fraternity that is competent in both Shariah and civil laws is very important

including the tax legislation that accord neutrality in treatment between Islamic

and conventional banking products.

6. Development of a comprehensive Shariah framework is a fundamental part of

the process. Each institution offering Islamic products will need to establish a

Shariah advisory committee to ensure that all Islamic transactions, products and

operations are Shariah-compliant. Shariah decisions need to be made transparent

to promote greater understanding and the acceptance of such decisions.

7. A robust and effective regulatory and supervisory framework particularly in

the areas such as capital adequacy and the liquidity framework taking into account

the unique risk characteristics of the Islamic banking models that accord the

Shariah requirements. In addition, sound corporate governance, transparency,

accountability, disclosure, market discipline, risk management and consumer

protection are common issues that need to be addressed.

8. Research and development to incorporate core Islamic values into banking

products and business models. Research and development and leveraging on the

advances in information and communication technology are critical in ensuring

performance and a more equitable distribution of profits and wealth among all

29

stakeholders. In addition, it can be utilized to enhance product development and

risk management.

9. Development of financial market infrastructure in order to ensure the

sustainability of Islamic banking. This can materialize through the introduction of

Islamic interbank and foreign exchange markets as it is essential for the efficient

functioning of the Islamic banking system. They facilitate the liquidity operations

of Islamic banks and promote financial stability. In addition, they serve as an

important transmission channel for the implementation of monetary policy as well

as the central bank's role as lender of last resort. In addition, the creation of a

well-developed Islamic capital market is essential as it provides the users of

capital with an alternative and cost-efficient source of longer-term financing, and

accords investors with a wider range of financial instruments to suit their different

risk profiles. Apart from the above, an efficient and robust payment system for

the clearing and settlement of payments shall be emphasis. Other financial

infrastructure that provides support to the development of the Islamic banking

sector includes the mortgage corporation to undertake the securitization of house

financing, a credit guarantee corporation to provide guarantee schemes to the

SME industry, and a rating agency to rate the Islamic financial instruments and a

deposit insurance scheme to provide the necessary safety net for depositors should

also be developed. In addition, the auditing, tax and legal firms must have the

right talents to provide their services to the Islamic financial institutions. These

ancillary institutions must have the ability to provide their services that are in

accordance with the Shariah principles.

10. Consumer education and awareness about Islamic banking is critical to its

success and future development. A consumer education program needs to be

developed to enhance public awareness of the features of Islamic banking

products and services.19

30

These are the key areas of challenges that need to be translated into action for the Islamic

Finance sector to grow. Apart from what has been outlined, specific countries might have

their own focal area in order to advance in this industry. The appropriate Islamic banking

system for a country would be largely based on the national agenda of the respective

countries, the objectives that the system hopes to achieve and the available resources.20

Key Challenges and Way Forward

A vibrant and excellence Islamic Financial industry is the dream of everyone who is

seriously involve in this industry. This can be achieve only if all those who participated in

the industry work collectively and seriously in order to ensure a success. There are key

challenges that need to be thought and in the humble opinion of the writer these areas can

be summarized as follows:

1. Ensuring greater Shariah compliant and convergence. This can be achieve

through dialogue and greater interaction between the Shariah scholars. It is also

important for the Shariah scholars to adapt specific standards in deciding upon

specific issues pertaining to the industry. It is suggested that a global Shariah

Advisory Council be established specifically to address issues related to Shariah

matters and this body shall be recognized by the Islamic financial institutions

globally. One of the important role of the body shall be finding the ways for a

greater convergence in Shariah views and opinion related to banking and finance.

The Malaysian Government has recently announced the allocation of RM200

million endowment fund to meet the financing requirements of the Shariah

Scholars' Dialogue research activities and the provision of scholarships. It is

hoped that this will contribute towards greater understanding in the process of

harmonizing the international implementation of Shariah in Islamic finance.

Apart from the dialogue, a comprehensive Shariah legal framework is also very

important taking into consideration the different requirements of each respective

country.

31

2. Ensuring compliance with internationally acceptable standards. In order for

the industry to be viable and valued it is important to ensure the industry comply

with internationally accepted standards. An important initiative in this area is the

establishment of the Islamic Financial Services Board (IFSB) in 2002. It was

established to promulgate the international regulatory and supervisory standards

for Islamic financial institutions worldwide aimed at achieving harmonization of

Islamic banking practices, fostering best practices and securing soundness and

stability in Islamic finance. In addition, the accounting and Auditing Organization

for Islamic Financial Institutions (AAOIFI) has introduced several Shariah and

accounting standard which can be adopted by Islamic Financial institutions.

3. Ensuring availability of human capital. It is also important to emphasis on

human talent management to create a sufficient pool of competent bankers and

Shariah experts essential to spearhead innovation in Islamic financial products

and services. To meet the increasing manpower requirements, institutions of

higher learning and the Islamic banking and finance institutes have to initiate new

programmes and trainings on Islamic finance.

4. Ensuring greater international cooperation and coordination. In order for the

industry to be competitive, it is important to focus on internationalizing the

industry. This can be achieve by collation, sharing, exchange and dissemination of

information between different institutions internationally. One of the pioneer

initiatives in this area was the setting up of the International Islamic Financial

Market or IIFM in 2002. The IIFM provides the environment to link all the

financial centers around the world that participate in Islamic finance, thereby

encouraging active participation by both Islamic and non-Islamic financial

institutions in the secondary market for Islamic financial instruments. As the

volume increases, it would strengthen the inter-linkages and integration amongst

the Islamic financial centers.

32

5. Introduction of universally acceptable products and services. This is the

challenge that has to be a taken by the bankers as well as the Shariah scholars to

provide universally acceptable products and services. This will assist in boosting

inter banking transactions and fostering greater cooperation between Islamic

financial institutions globally.

Finally, it has to be noted that the rapid progress of Islamic banking over the last two

decades would not have been possible without the pioneering efforts of the Islamic

financial institutions and all those who have put tremendous effort in building up a

successful and vibrant industry. Despite that, the opportunity and prospect for a greater

future success lies in the hand of all. Allah says in the Qur‟an: “…Verily! Allah will not

change the good condition of a people as long as they do not change their state of

goodness themselves…” (Al-Ra‟d: 11)

List of References:

1. Lecture by Dr. Mohammad Nejatullah Siddiqi, Recent History Of Islamic

Banking And Finance, (Anderson Graduate School of Management, University

of California, Los Angeles, 7 November 2001

2. Tabung Haji Annual Report 2003

3. Ismail, Abdul Halim. Bank Islam Malaysia Berhad: Structure and Functions

(Paper presented at the Seminar on Current Trends and Development of the

Banking Industry in Malaysia, 6-7 June 1983)

4. Islamic Banking Act 1983

5. Overview of Islamic Banking in Malaysia, Central Bank of Malaysia

6. Governor's Speech at the Seminar on 10-Year Master Plan for Islamic Financial

Services Industry: "Building a Progressive Islamic Banking Sector: Charting the

33

Way Forward". Governor Tan Sri Dato' Sri Dr. Zeti Akhtar Aziz , Putrajaya,

Malaysia, 22 June 2005.

7. Nik Roslin. Pasaran Modal Islam – Sektor Pemantap Industri Kewangan Islam,

Presentation at Muzakarah Pasaran Modal Islam, Kuala Lumpur, September 2005

8. The Islamic Bond Market in Malaysia published by Rating Agency Malaysia

Berhad (Brochure)

9. Development in the Malaysian Capital Market, Securities Commission Malaysia

(Brochure)

10. Development in the Malaysian Islamic Capital Market, Securities Commission

Malaysia (Brochure)

11. Breadth & Depth, Complementing the Islamic Capital Market by Federation of

Malaysian Unit Trust Managers (Brochure)

12. Developing the Islamic Capital Market – Malaysia‟s Experience and the Way

Forward by Nik Ramlah Mahmod at Shariah Scholars Dialogue, Kuala Lumpur,

June 2005

13. Mohd Razif Abd. Kadir, Islamic Financial System: Malaysia‟s Experience and the

Way Forward, presentation at Shariah Scholars Dialogue, Kuala Lumpur, June

2005

14. Islamic Banking Practice from the Practitioner‟s Perspective, Bank Islam

Malaysia Berhad, Kuala Lumpur, 1994

15. Takaful (Islamic Insurance) Concept & Operational System from the

Practitioner‟s Perspective, BIMB Institute of Research and Training Sdn. Bhd.

Kuala Lumpur, 1996

34

Endnotes:

1 Excerpt from the lecture by Dr. Mohammad Nejatullah Siddiqi, Recent History Of Islamic Banking And

Finance, (Anderson Graduate School of Management, University of California, Los Angeles, 7 November 2001) 2 Source obtained from the presentation in Kuala Lumpur Islamic Finance Forum 2005, Kuala Lumpur, December 2005. 3 Tabung Haji Annual Report 2003 obtained from: http://www.tabunghaji.gov.my/th/bi/bi-latarbelakang_th.asp?lthmenu=0 4 Ismail, Abdul Halim. Bank Islam Malaysia Berhad: Structure and Functions (Paper presented at the Seminar on Current Trends and Development of the Banking Industry in Malaysia, 6-7 June 1983)

35

5 Islamic Banking Act 1983 6 Islamic Banking Act 1983 7 Overview of Islamic Banking in Malaysia, Central Bank of Malaysia write-ups. 8 Mohd Razif Abdul Kadir. Presentation on Islamic Financial System: Malaysia’s Experience and the Way Forward during Shariah Scholar Dialogue, Kuala Lumpur, June 2005. 9 Overview of Islamic Banking in Malaysia, Central Bank of Malaysia write-ups. 10 As at October 2005 11 Source: Bank Negara Malaysia (Central Bank of Malaysia) 12 Source: Bank Negara Malaysia (Central Bank of Malaysia) 13 Source: Bank Negara Malaysia (Central Bank of Malaysia) 14 The Islamic Capital Market published by Bursa Malaysia 15 The Malaysia Islamic Capital Market issued by Securities Commission of Malaysia 16 ibid 17 Source: Bank Negara Malaysia (Central Bank of Malaysia) 18 Governor's Speech at the Seminar on 10-Year Master Plan for Islamic Financial Services Industry: "Building a Progressive Islamic Banking Sector: Charting the Way Forward". Governor Tan Sri Dato' Sri Dr. Zeti Akhtar Aziz , Putrajaya, Malaysia, 22 June 2005. 19 Excerpts from the Governor's Speech at the Seminar on 10-Year Master Plan for Islamic Financial Services Industry: "Building a Progressive Islamic Banking Sector: Charting the Way Forward". Governor Tan Sri Dato' Sri Dr. Zeti Akhtar Aziz , Putrajaya, Malaysia, 22 June 2005. 20 Ibid