islamic banker asia - shariah compliance and audit - february 2015

TRANSCRIPT

12

ISSUE

ISSUE

12

ISSUE

12

ISSUE

12

ISSUE13 2015 __ ISLAMIC BANKER __ 6564 __ ISLAMIC BANKER __ ISSUE12 2015

SHARI’A COMPLIANCE AND AUDIT

SHARI’A COMPLIANCE AND AUDIT – KEY TO SUCCESS IN ISLAMIC FINANCE INDUSTRYIn 2013 the Islamic financial services industry was reported to have reached beyond US$1.8 trillion, averaging a growth rate of 17.5% from 2009 to 2013 (GIFR, 2014). The industry continues to enjoy a period of strong growth, albeit seeing a degree of slowdown compared to previous years. Nonetheless, against this backdrop of growth, a number of key industry stakeholders (including senior Shari’a scholars) have highlighted their concerns regarding the overly engineered nature of contemporary structures, which seem to lose the industry’s essence that believe in equity-based form of investment. BY MUJTABA KHALID

Shari’a compliance of financial products is assessed and certified by Shari’a scholars either in their individual

capacities or more typically by the collective decision making of the Shari’a Supervisory Boards (SSB) within Islamic financial institutions (IFI). Undoubtedly, the demand placed on top tier scholars

is uniquely challenging as Islamic finance is a horizontal discipline spread across multiple asset classes, sectors and locations. Hence, the need to reinforce and enhance Shari’a governance frameworks to keep pace with the rapid growth of the industry is paramount in maintaining stakeholder confidence.

The fundamental requirement for any Islamic finance product is simply to comply with the Islamic law. Assurance and governance is by no means alien to Islamic practice. The principle itself is deeply rooted in the established concept of Islamic governance also known as the institution of hisbah (ombudsman/ market regulator). Historically, hisbah was initiated by Prophet Muhammad (pbuh) as an institution to govern and supervise commercial transactions in the market. The Prophet appointed a number of officers to supervise and monitor market operations and other trading activities.

This article will evaluate the steps that can be taken for effective Shari’a compliance and audit in the IFIs.

SHARI’A COMPLIANCEShari’a compliance for IFIs may be divided into three categories:

1. Acceptable LevelFailing to ensure compliance with the acceptable level will result in Haram (non-Shari’a complaint) status of the organisation or its activities.The following are elements of acceptable level of Shari’a compliance –l Not dealing with any business activity that is impermissible according

Shari’a Audit is one of the important pillars of upholding the integrity of Islamic financial institutions

ISSUE13 2015 __ ISLAMIC BANKER __ 6564 __ ISLAMIC BANKER __ ISSUE12 2015

THERE ARE RESERVATIONS BY SCHOLARS REGARDING THE STRUCTURING OF CERTAIN BANKING PRODUCTS AND CONTRACTS, SUCH AS – COMMODITY MURABAHAH, BAI’AL INAH, ISLAMIC CREDIT CARDS, WHICH LIE IN THE GREY AREA AND CANNOT BE DEEMED HARAM OUTRIGHT.

http

://up

load

.wik

imed

ia.o

rg/ h

ttp://

gard

adev

.bla

dede

v.co

.uk

to Islamic teachings e.g. alcoholic beverages, pork etc.l Not dealing in Riba (interest)l Not Involved in Gharar and Maisir (uncertainty and excessive risk taking)l Implementing Islamic laws of contract in normal course of business

Although Islamic banks remain Shari’a compliant if they meet the acceptable level of compliance, there are reservations by scholars regarding the structuring of certain banking products and contracts, such as – commodity Murabahah, Bai’Al Inah, Islamic credit cards, which lie in the grey area and cannot be deemed haram outright.

2. Satisfactory LevelThis level is a step further from just meeting the bare minimum level of Shari’a assurance.The following entail elements of a satisfactory level of Shari’a compliance –l No doubtful transactions, e.g. commodity Murabahah, Bai’Al Inahl Active Shari’a compliance mechanism – periodic Shari’a review, internal Shari’a audits on a regular basisl Full Shari’a compliance in agreements and processesl Comprehensive Shari’a training to the staff members – general Islamic banking trainings, specific product-wise trainings, continuous professional development programs, workshops and conferencesl Shari’a compliant marketing and strategy

3. Desirable LevelThis level of adherence means best practices that reflect the essence of Islamic teachings and values. This is, however a difficult and long run task.The desirable level of compliance means l Product innovation; copying and mimicking conventional products is

not a proper reflection of the Islamic financial system’l Real involvement in trade and business activities; symbolic and artificial involvement creates doubts among consumers

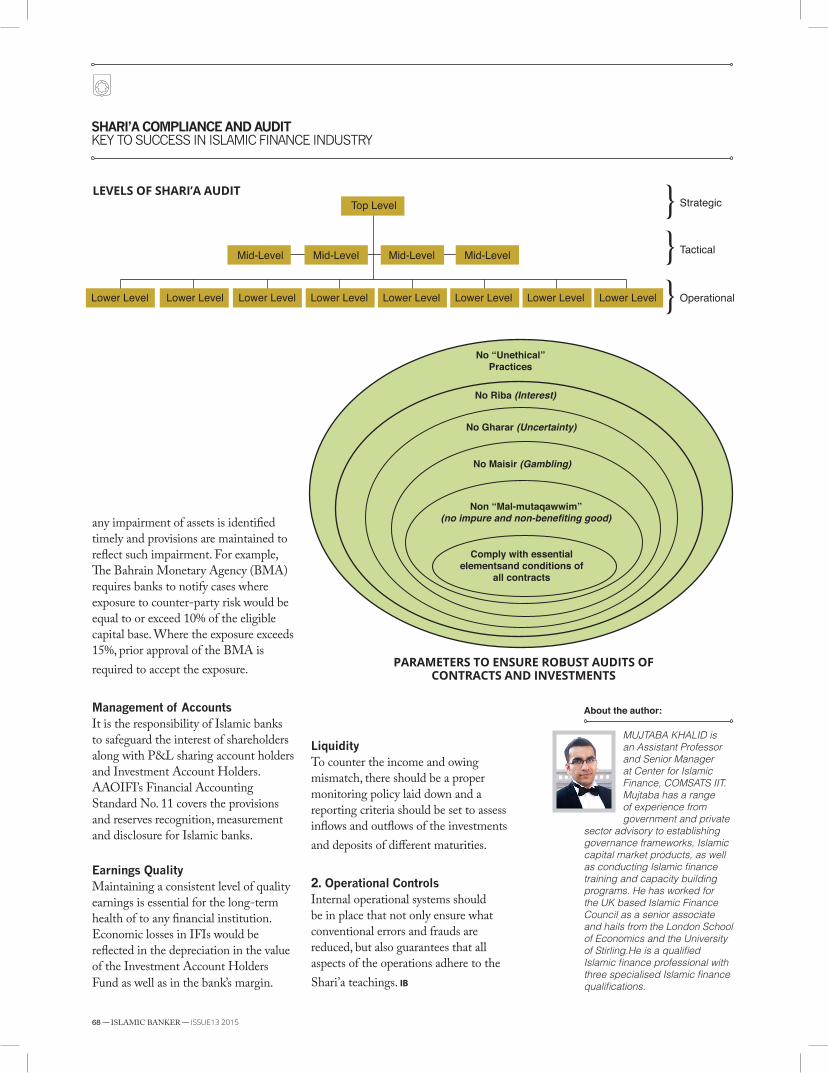

Strategic

Tactical

Operational

Shari’a audit and compliance – key to success for the Islamic finance industry

l Less role of Hiba (gift) and rebatesl Islamic values of equitable distribution of wealth in society

SHARI’A COMPLIANCE HIERARCHY

THREE LEVELS OF SHARI’A COMPLIANCE

n Top Level (Strategic)n Mid-Level (Tactical)n Lower Level (Operational)

Strategic – Top LevelThis is an important level from where Shari’a compliance is initiated.

12

ISSUE

ISSUE

12

ISSUE

12

ISSUE

12

66 __ ISLAMIC BANKER __ ISSUE13 2015 ISSUE13 2015 __ ISLAMIC BANKER __ 67

SHARI’A COMPLIANCE AND AUDITKEY TO SUCCESS IN ISLAMIC FINANCE INDUSTRY

This includes shareholders and top-management relationship.

Shareholders and top-management

relationship

l Cultural and behaviour issues of managementl Dealing with shareholders – dealing with minority shareholders and their rightsl Managing shareholder engagement inconjunction with other haram business for example, foreign banks with Islamic windows

Organisational

l Organisational culture – promotion of Islamic values throughout the businessl Relationship within management – HR policies and other relationshipsl Marketing Strategiesl Shari’a governance – system to improve and evolve Shari’a compliance and “quality”l Readiness for change

Tactical – Mid Level

l Organizational culture – promotion of Islamic values among subordinatesl Relationship within management – mid-level management and subordinatesl Marketing techniquesn Forcing sales team to meet targets in any form possible is not recommendedl Customer Relationshipn No cheating and lyingn No unattainable promisesl Creating awareness of rights and obligations – among both customers and subordinatesl Ethical/Islamic motivation of employees

Operational – Lower Level

l Awareness of ethical responsibilities – very important at this stagel Marketing and relationshipl Behaviourl Awareness of Islamic system; e.g.: bank sales team should have in-depth knowledge of the products they are sellingl Knowledge of the advantages and shortcomings of Islamic based e.g. bankingl Dealings with public – religious minded people, ethically motivated

Ensure underlying transaction, investment, activity complies with the teachings of Shariah -qualitative testing

Test the existence of the essential element for the contract

Examine salient conditions and clauses of the agreement - ensure compliance with regulations

IS ESSENTIAL FOR THE LONG-TERM HEALTH OF TO ANY FINANCIAL INSTITUTION. ECONOMIC LOSSES IN IFIS WOULD BE REFLECTED IN THE DEPRECIATION IN THE VALUE OF THE INVESTMENT ACCOUNT HOLDERS FUND AS WELL AS IN THE BANK’S MARGIN.

Operational level efficiency forms an important tangent for success for an IFI

66 __ ISLAMIC BANKER __ ISSUE13 2015 ISSUE13 2015 __ ISLAMIC BANKER __ 67

people. Non-believersl Respect of ethical values of Islam – e.g. Recommend specific dress code for women, prayer breaks etc.

INTERNAL SHARI’A AUDITSimilar to the conventional financial system, the Islamic financial system also requires internal operational controls to:

i) Ensure sound error free information is available to investors

ii) To protect the interests of the customers (depositors etc.)

iii) Ensuring the workings of the organization comply with Shari’a

Effective prudential supervision of Islamic financial institutes (IFIs) would require an internal controls system based on:

i) Standardised contracts

ii) Uniform and appropriate accounting system

iii) Frequent financial reporting

TYPES OF FRAMEWORKS AND

CONTROLS FOR IFIs

1. Regulatory ControlsThis is to ensure that the IFIs comply with the regulation put in place by the central bank for the operations of Shari’a compliant financial institutes. In jurisdictions where the central bank does not have any such laws, the IFIs shall follow a self-regulatory model making relevant information available to all stakeholders and related parties.

The regulations on assessing IFIs mainly base on the assessment of capital adequacy, asset quality, management of Investment Accounts, earning quality, profit and loss of Islamic banks and liquidity management:

Capital AdequacyIslamic banks, like conventional banks are required to maintain an adequate level of capital. The Basel Committee has set this level at 12% (Basel III is not applicable until 2019). AAOIFI has

approved and recommended a Statement on the Purpose and Calculation of the Capital Adequacy Ratio for Islamic banks. The statement focuses on two main issues:

(a) Funds of Investment Accounts of Islamic banks are not liabilities, but act as financing assets managed by the bank as Mudarib.

(b) Whereas legally the bank’s own capital is not exposed to the risk of the assets under management (except in cases of misconduct and negligence), banks are at times under pressure to absorb some of that risk in order to give competitive returns (displaced commercial risk). There is also the risk of misconduct or negligence and its implications for risk to the bank’s own capital (fiduciary risk)

Asset QualityLike conventional banks, Islamic banks are to maintain good quality assets. They are also expected to have policies and procedures in place to ensure that

Country’s regulatory controls must ensure IFIs comply with the parameters and regulations and also promote self-regulatory model to make information available to the stakeholders

http

://up

load

.wik

imed

ia.o

rg/ h

ttp://

ww

w.n

arci

ssis

ticab

use.

com

ISSUE13 2015 __ ISLAMIC BANKER __ 00

12

ISSUE

ISSUE

12

ISSUE

12

ISSUE

12

68 __ ISLAMIC BANKER __ ISSUE13 2015

SHARI’A COMPLIANCE AND AUDITKEY TO SUCCESS IN ISLAMIC FINANCE INDUSTRY

About the author:

MUJTABA KHALID is an Assistant Professor and Senior Manager at Center for Islamic Finance, COMSATS IIT. Mujtaba has a range of experience from government and private

sector advisory to establishing governance frameworks, Islamic capital market products, as well as conducting Islamic finance training and capacity building programs. He has worked for the UK based Islamic Finance Council as a senior associate and hails from the London School of Economics and the University of Stirling.He is a qualified Islamic finance professional with three specialised Islamic finance qualifications.

any impairment of assets is identified timely and provisions are maintained to reflect such impairment. For example, The Bahrain Monetary Agency (BMA) requires banks to notify cases where exposure to counter-party risk would be equal to or exceed 10% of the eligible capital base. Where the exposure exceeds 15%, prior approval of the BMA is required to accept the exposure.

Management of AccountsIt is the responsibility of Islamic banks to safeguard the interest of shareholders along with P&L sharing account holders and Investment Account Holders. AAOIFI’s Financial Accounting Standard No. 11 covers the provisions and reserves recognition, measurement and disclosure for Islamic banks.

Earnings QualityMaintaining a consistent level of quality earnings is essential for the long-term health of to any financial institution. Economic losses in IFIs would be reflected in the depreciation in the value of the Investment Account Holders Fund as well as in the bank’s margin.

No “Unethical”Practices

Comply with essential elementsand conditions of

all contracts

Non “Mal-mutaqawwim”(no impure and non-benefiting good)

No Gharar (Uncertainty)

No Maisir (Gambling)

No Riba (Interest)

PARAMETERS TO ENSURE ROBUST AUDITS OF CONTRACTS AND INVESTMENTS

Top Level Strategic

Tactical

Operational

Mid-Level Mid-Level Mid-Level Mid-Level

Lower Level Lower Level Lower Level Lower Level Lower Level Lower Level Lower Level Lower Level

}}}

LEVELS OF SHARI’A AUDIT

LiquidityTo counter the income and owing mismatch, there should be a proper monitoring policy laid down and a reporting criteria should be set to assess inflows and outflows of the investments and deposits of different maturities.

2. Operational ControlsInternal operational systems should be in place that not only ensure what conventional errors and frauds are reduced, but also guarantees that all aspects of the operations adhere to the Shari’a teachings. IB