irs rules & best practices for international & … · donor advised fund (daf) caf america...

TRANSCRIPT

IRS Rules & Best Practices for International & Enhanced Domestic Grant Making

Ted Hart, ACFRE CEO, CAF America

CAF America 2013

1. Expenditure Responsibility 2. Equivalency Determination 3. Enhanced Domestic Vetting (Due Diligence)

Three Protocols

CAF America 2013

• Pension Protection Act of 2006 for the first time defined donor

advised funds and placed new rules on their use.

• Owned by a sponsoring public charity

• Separately tracked funds identified by reference to one or more

specific donors

• Donors or their designees reasonably expect to have advisory

privileges

• Can make distributions to multiple grantees

Donor Advised Fund (DAF)

CAF America 2013

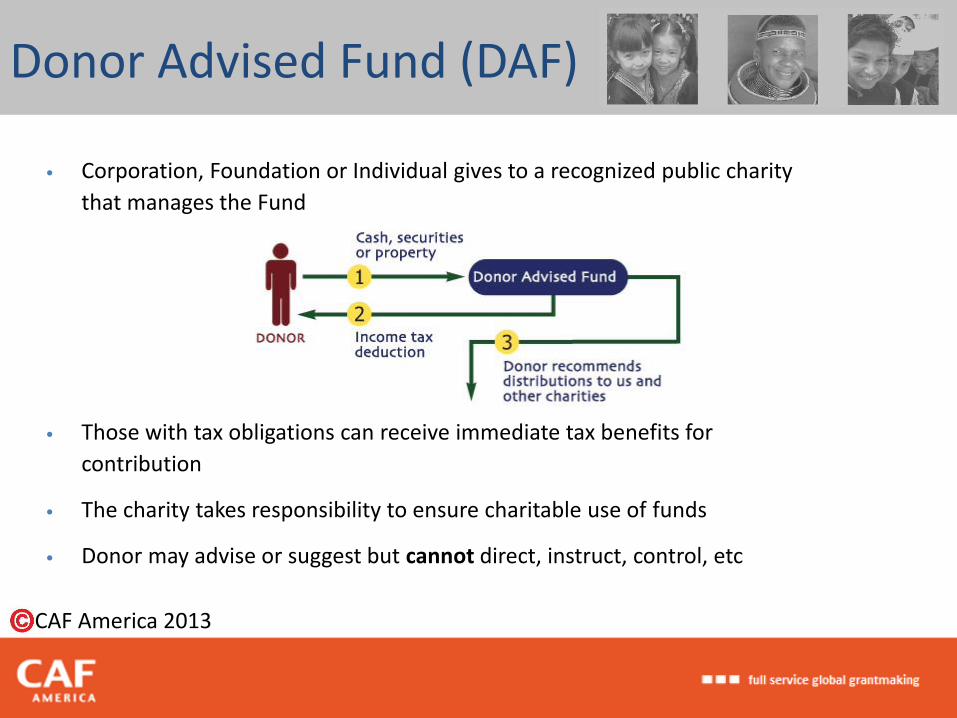

• Corporation, Foundation or Individual gives to a recognized public charity

that manages the Fund

• Those with tax obligations can receive immediate tax benefits for

contribution

• The charity takes responsibility to ensure charitable use of funds

• Donor may advise or suggest but cannot direct, instruct, control, etc

Donor Advised Fund (DAF)

CAF America 2013

• Donor can get a tax deduction now and give later

• Private foundations can make grants without

exercising normal oversight

• Sponsoring charity handles due diligence process

Benefits of a DAF

CAF America 2013

• Must exercise expenditure responsibility if grantee is

not a certain kind of public charity or private

operating foundation

• No distributions to individuals

• No distributions for non-charitable purposes

• 20% (of value of grant) tax on sponsoring

charity for violations

Restrictions on DAFs

CAF America 2013

• 25% tax on donor for any grant, loan, compensation

or similar payment to donor, advisor or related

parties (repayment required).

• 125% tax on other substantial return benefit

• Tickets, tuition credit, member dues, etc.

• Recognition for gift OK

• Round-tripping?

Restrictions Donor Benefit

CAF America 2013

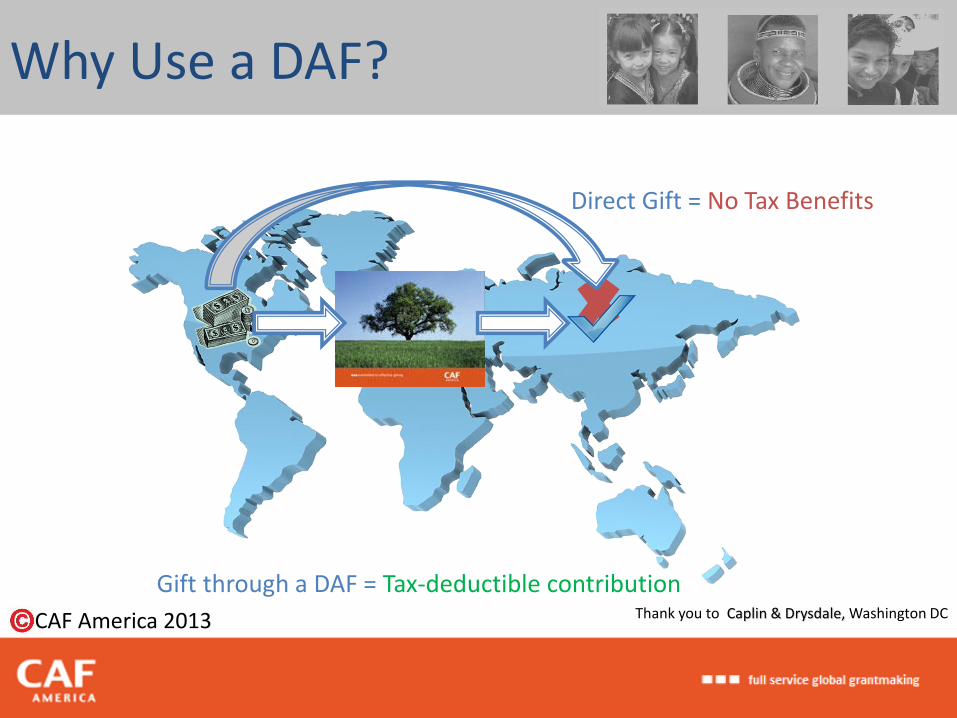

Direct Gift = No Tax Benefits

Gift through a DAF = Tax-deductible contribution

Why Use a DAF?

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

• No “earmarking/ pledging”: No agreement, oral or

otherwise, that funds must go to predetermined

recipient or to recipient of donor’s choice.

• Must clearly inform donor that donor advised fund

has ultimate discretion/control over funds – donor

does not!

• IRS looks to reality, not just form

• Do we inevitably follow donor’s advice? Do we

provide our own expertise?

• Are we serious about making sure grants further

our charitable purposes?

IRS Requirements

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

The Preapproved Grant Relationship model of fiscal sponsorship is widely misunderstood and easily abused as a “conduit” when the fiscal grant maker fails to exercise the requisite “discretion and control.” The key element to avoid in grant making relationships is the creation of a “pass-through” or “conduit” arrangement. The grant maker must exercise “variance power” or independent “discretion and control” over the grant funds for the relationship to pass IRS muster.

No Conduit

“discretion and

control”

CAF America 2013

• Relief of poverty, combating community deterioration

• Education, promotion of the arts

• Scientific research

• Combating prejudice, protecting human rights, helping

disadvantaged

• Protecting the environment

• Lessening burdens of government

• Promotion of health (e.g., hospitals)

• Religious purposes

Charitable Purposes

CAF America 2013

• No substantial private benefit or commercial purpose—benefit to

private parties must be incidental:

• Organization improving a public lake is charitable even if neighboring property owners are benefitted

• Community hospitals can be funded

• Private practices cannot

• Watch for close relationships with a related commercial entity

• Make sure benefits are designed to serve a charitable class

(not an individual or small group, not businesses)

• Watch for organizations acting like a for-profit business

Charitable Benefit

CAF America 2013

No candidate endorsements, contributions, in-kind

assistance

Ban any non-neutral expression of favoritism (e.g.,

voter guides, voter registration or mobilization,

etc.)

No highlighting candidate positions that

exclusively agree/disagree with organization

Do not support activities that provide candidates

unequal speaking opportunities

Do not fund activities that ask candidates to sign

onto the organization’s “pledge”

No Political Activity

CAF America 2013

You must not fund activities that “attempt to influence

legislation” at any level

But you can seek to influence rules and regulations

once laws are passed

Do not fund communications with legislators, staff, or

other officials, or encouraging the public to make such

communications, for the purpose of influencing

legislation

You can fund advocacy for broad causes and issues

Do not fund activities that directly advocate

for/against legislation

Lobbying vs. Advocacy

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

Pre-grant inquiry: “reasonable assurance” that

the expenditure is charitable

Grant agreement restricts use of funds to

specific charitable projects

Financial & narrative reports at least annually

& final cumulative report

Reporting to IRS: Coming soon?

20% tax on amount of the grant if you get it wrong

Expenditure Responsibility

IRS Requirements and Penalty

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

Certifies that selected organizations meet the highest standards of our proprietary due diligence

vetting process:

• Organization Identification and Contact

• Document Collection:

Grant Eligibility Application (GEA) Financials Governing Documents Board and Executive Staff rosters Proof of Charitable status Country-specific relevant documentation

• Ongoing weekly watch list scanning

Scan the nonprofit, key staff and board members against 450 + global databases.

• Three-tier CAFAmerica review

CAF America’s 100-step industry leading due diligence process is a combination of both Expenditure Responsibility and Equivalency Determination.

Beyond The Minimum

CAF America 2013

Complete enough to give a reasonable person assurance that the

grantee will use the grant for proper purposes

Identity and prior history and experience of grantee and its

managers.

Information about management and practices of grantee

Prior successful completion of grants normally enough

Rigor may depend on size of grant

Pre-Grant Inquiry

Requirements and Best Practices

CAF America 2013

Must include certain terms & be signed by an officer:

Specify use of funds, which must be charitable

Prohibit lobbying, political campaign intervention, non-charitable

activity

Prohibit grants that would violate IRS section 4945 rules on

individual travel/study/scholarship grants or ER requirements

Require funds to be tracked in a separate account

(does not require a separate bank account)

Require access to files on request and written reports

Grant Agreement

Requirements and Best Practices

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

Annual Narrative and Financial Reports

Reports collected at end of each accounting

period of the grantee

Final cumulative reports at the end of grant period

Must report on use of grant funds, progress toward goals, and

compliance with grant terms

IMPORTANT: you must not make additional grants when reports

are outstanding or if there are unresolved concerns raised over

use of funds or compliance;

IMPORTANT: you must make reasonable efforts to obtain reports

Reporting

Requirements and Best Practices

CAF America 2013

When a report indicates funds have been misspent:

Grant maker must try to get funds restored /

returned

Must withhold further grants until special

measures in place to avoid future misuses

Normally, IRS requires a summary report on each ER

grant indicating purpose of grant, name and address

of grantee, dates of reports received, amounts

expended by grantee (per report), and information

about any diversions / verification efforts.

This is not required yet on the Form 990, but IRS has

indicated informally that orgs should maintain this

information

Verification & Reporting

MISSPENT FUNDS

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

Still can’t be a conduit relationship in granting funds

Still need to make sure funds are used for charitable

purposes

Specific penalties for failure to get ER right don’t apply

No prohibition on grants to individuals, if such payments

and the charitable purpose served are documented

Donors can receive benefits in return for gift if the grant

maker properly indicates value of benefit received and

reduces charitable deduction receipt accordingly

Non-DAF Funded Grants

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

If grantee uses funds to purchase capital

equipment, arguably those funds are not spent

until end of useful life of that equipment—longer

period of ER reports required.

Normally, easiest to have grantee use our funds

for something else.

If recipient is a 501(c)(3) or equivalent, can stop

reports after 3 years.

[Equivalency Determination Rules Will Help Here]

Funding Capital Equipment

CAF America 2013

Private foundation ER rules require grantee to

agree not to make any grants that a grant maker

couldn’t make itself.

If grantee will re-grant to organizations, you

need to require the grantee to exercise

expenditure responsibility as grant maker

would.

It is less clear how re-grants to individuals

would work—conservative view is that

grantee’s individual grant procedures would

need to meet Private Foundation

requirements, including IRS preapproval.

Re-granting Rules

CAF America 2013

IRS tracks a long history of abuse.

“Donations” in lieu of tuition payments

Grants for junkets or no charitable activity at all

Do not grant directly from a DAF scholarship awards (or

any other awards) to individuals

Equivalency Determination grants to charities for

scholarships are OK, so long as grantee selects recipients

“completely independently”

No grantee rep or donor/advisor rep on selection

committee

No non-charitable constraints (e.g., requirement

that only corporate executive children need apply)

Scholarships

CAF America 2013

Focused on Grantee as a Whole

Grant maker must make reasonable judgment / good

faith determination that grantee meets U.S. standards

IRS Rev. Proc. 92-94 issued September 2012

http://www.irs.gov/pub/irs-tege/rp_1992-94.pdf

New Guidance: Qualified Tax Practioners can provide

opinions to third parties

Equivalency Determination

CAF America 2013

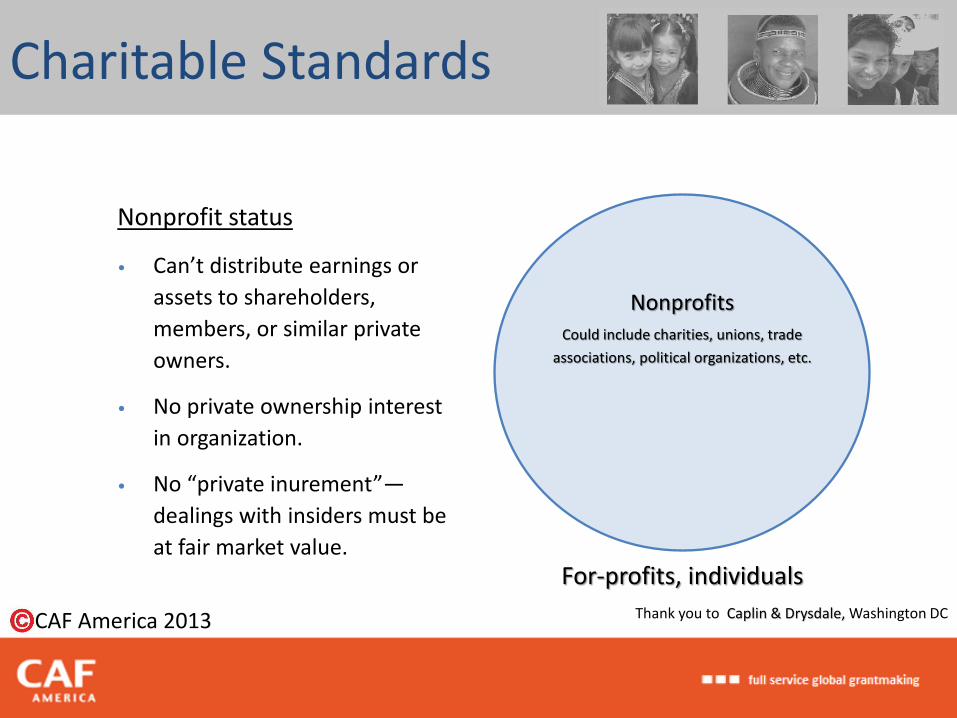

For-profits, individuals

Nonprofits Could include charities, unions, trade

associations, political organizations, etc.

Nonprofit status

• Can’t distribute earnings or

assets to shareholders,

members, or similar private

owners.

• No private ownership interest

in organization.

• No “private inurement”—

dealings with insiders must be

at fair market value.

Charitable Standards

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

For-profits, individuals

Nonprofits Charitable status

• Nonprofit

• Organized and operated

“exclusively” for charitable

purposes.

• Private benefit must be incidental

• No substantial lobbying

• No campaign intervention

• Permanently dedicated to

charitable purposes (dissolution

clause)

Charities

501(c)(3)

Charitable Standards

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

For-profits, individuals

Nonprofits

Charities

501(c)(3)

Private

Foundations

Public Charities

509(a)(1), (2),

(3)

Public Charities

• Churches, schools, hospitals

• Medical research organizations

• Orgs supported by gov’t, public, or other

publicly supported charities

• Orgs supported by combination of

donations & revenue from charitable

activity from public

• Supporting organizations

Private Foundations

• Supported by investments or a few

donors

• Operating or non-operating

Charitable Standards

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

For-profits, individuals

Nonprofits

Charities (501(c)(3))

Operating

Foundations

4942(j)(3)

Schools, hospitals,

churches, MROs

Publicly supported

(donations)

509(a)(2)

509(a)(3)

Non-Operating

Foundations

Public Charities

• Churches, schools, hospitals

• Medical research organizations

• Orgs supported by gov’t, public, or other

publicly supported charities

• Orgs supported by combination of

donations & revenue from charitable

activity from public

• Supporting organizations

Private Foundations

• Supported by investments or a few

donors

• Operating or non-operating

509(a)(1)

Charitable Standards

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

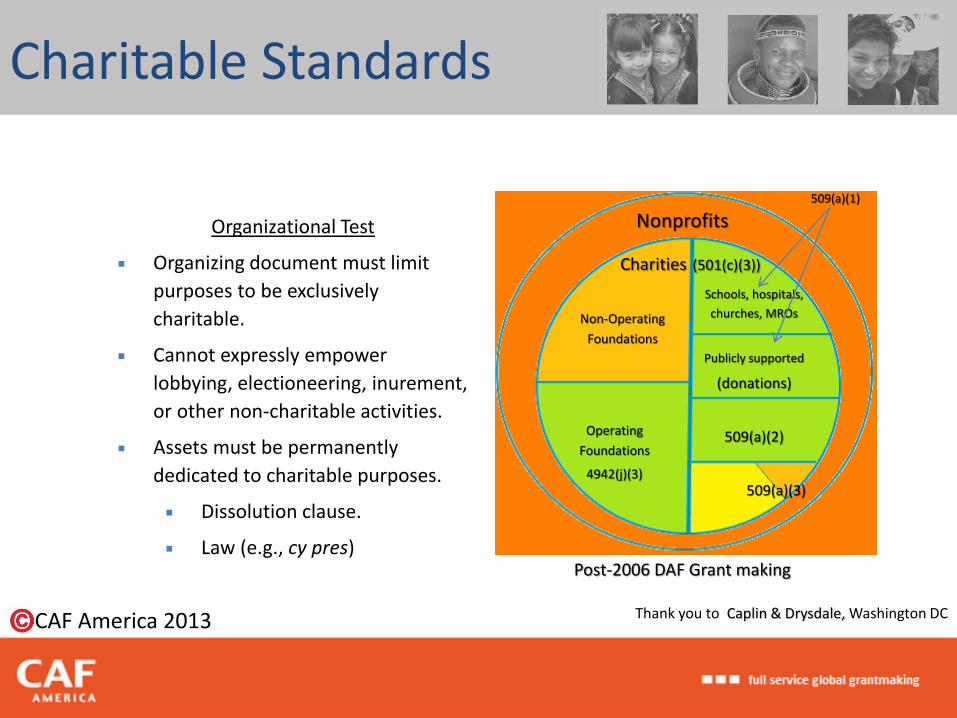

Organizational Test

Organizing document must limit

purposes to be exclusively

charitable.

Cannot expressly empower

lobbying, electioneering, inurement,

or other non-charitable activities.

Assets must be permanently

dedicated to charitable purposes.

Dissolution clause.

Law (e.g., cy pres) Post-2006 DAF Grant making

Nonprofits

Charities (501(c)(3))

Operating

Foundations

4942(j)(3)

Schools, hospitals,

churches, MROs

Publicly supported

(donations)

509(a)(2)

509(a)(3)

Non-Operating

Foundations

509(a)(1)

Charitable Standards

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

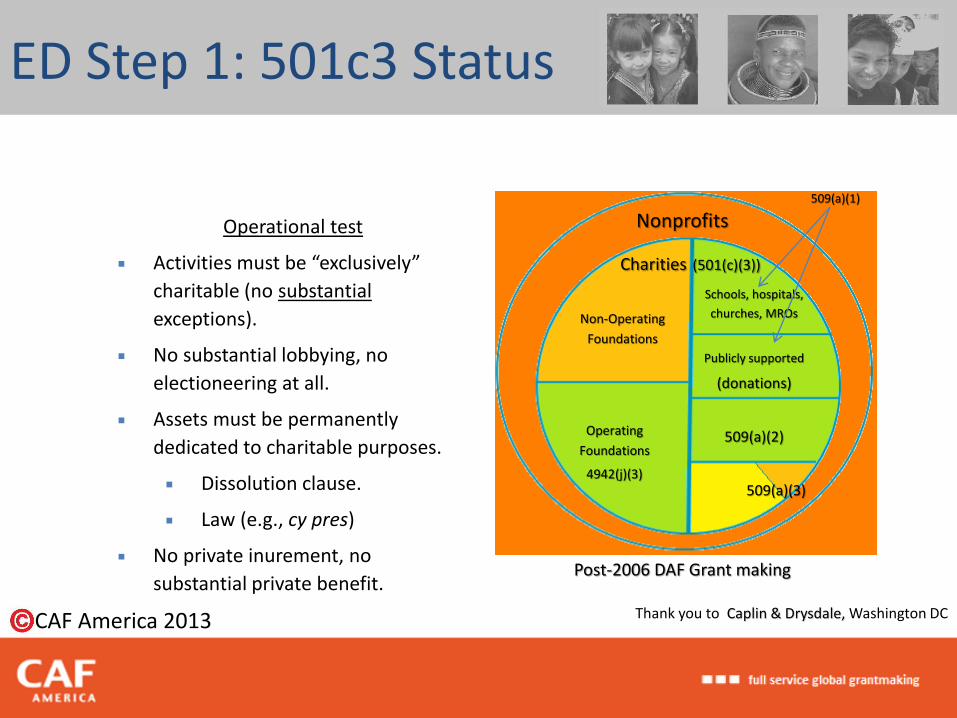

Operational test

Activities must be “exclusively”

charitable (no substantial

exceptions).

No substantial lobbying, no

electioneering at all.

Assets must be permanently

dedicated to charitable purposes.

Dissolution clause.

Law (e.g., cy pres)

No private inurement, no

substantial private benefit. Post-2006 DAF Grant making

Nonprofits

Charities (501(c)(3))

Operating

Foundations

4942(j)(3)

Schools, hospitals,

churches, MROs

Publicly supported

(donations)

509(a)(2)

509(a)(3)

Non-Operating

Foundations

509(a)(1)

ED Step 1: 501c3 Status

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

No Substantial Lobbying

Contacting government officials for

the purpose of influencing

legislation.

Urging the public to do so.

Advocating the adoption or

rejection of legislation.

Exceptions for discussions of broad

social issues, nonpartisan analysis &

research, technical advice, self-

defense.

5% rule of thumb. Post-2006 DAF Grant making

Nonprofits

Charities (501(c)(3))

Operating

Foundations

4942(j)(3)

Schools, hospitals,

churches, MROs

Publicly supported

(donations)

509(a)(2)

509(a)(3)

Non-Operating

Foundations

509(a)(1)

ED Step 1: 501c3 Status

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

No Electioneering

Candidate forums, voter

registration, voter education OK if

absolutely nonpartisan.

Can’t focus charitable activities on

one candidate or party.

Educating the public on candidates’

position on single issue on which

organization has a clear position is

not OK.

Even insubstantial electioneering is

forbidden. Post-2006 DAF Grant making

Nonprofits

Charities (501(c)(3))

Operating

Foundations

4942(j)(3)

Schools, hospitals,

churches, MROs

Publicly supported

(donations)

509(a)(2)

509(a)(3)

Non-Operating

Foundations

509(a)(1)

ED Step 1: 501c3 Status

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

“Per Se” Public Charities

Educational Institutions

Churches

Hospitals

“Honorary” public charities:

Government entities

Certain international

organizations

Post-2006 DAF Grant making

Nonprofits

Charities (501(c)(3))

Operating

Foundations

4942(j)(3)

Schools, hospitals,

churches, MROs

Publicly supported

(donations)

509(a)(2)

509(a)(3)

Non-Operating

Foundations

509(a)(1)

ED Step 2: Public Charity

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

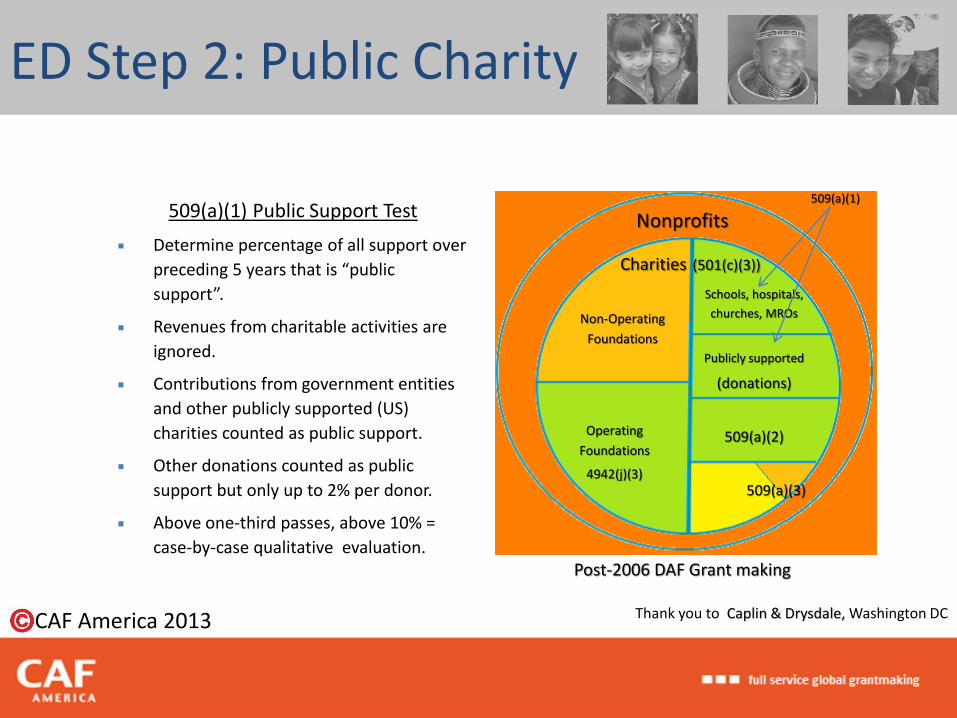

509(a)(1) Public Support Test

Determine percentage of all support over

preceding 5 years that is “public

support”.

Revenues from charitable activities are

ignored.

Contributions from government entities

and other publicly supported (US)

charities counted as public support.

Other donations counted as public

support but only up to 2% per donor.

Above one-third passes, above 10% =

case-by-case qualitative evaluation. Post-2006 DAF Grant making

Nonprofits

Charities (501(c)(3))

Operating

Foundations

4942(j)(3)

Schools, hospitals,

churches, MROs

Publicly supported

(donations)

509(a)(2)

509(a)(3)

Non-Operating

Foundations

509(a)(1)

ED Step 2: Public Charity

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

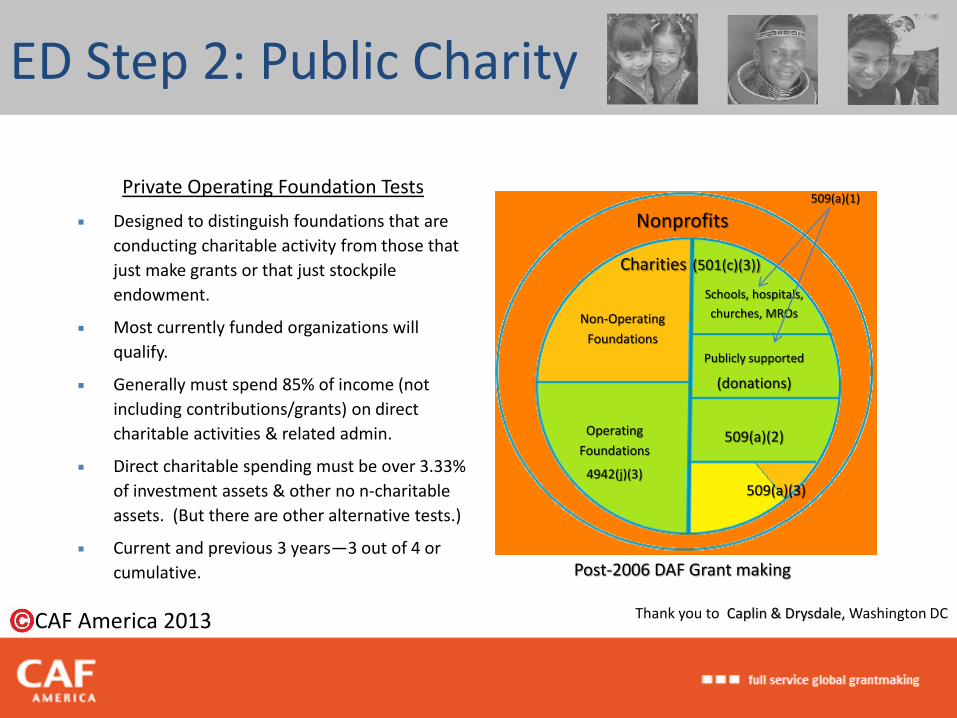

Private Operating Foundation Tests

Designed to distinguish foundations that are

conducting charitable activity from those that

just make grants or that just stockpile

endowment.

Most currently funded organizations will

qualify.

Generally must spend 85% of income (not

including contributions/grants) on direct

charitable activities & related admin.

Direct charitable spending must be over 3.33%

of investment assets & other no n-charitable

assets. (But there are other alternative tests.)

Current and previous 3 years—3 out of 4 or

cumulative. Post-2006 DAF Grant making

Nonprofits

Charities (501(c)(3))

Operating

Foundations

4942(j)(3)

Schools, hospitals,

churches, MROs

Publicly supported

(donations)

509(a)(2)

509(a)(3)

Non-Operating

Foundations

509(a)(1)

ED Step 2: Public Charity

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

Generally, foreign charity

classification is helpful but not a

guarantee.

BUT Canadian registered charities

are automatically classified as

501(c)(3).

Mexican Article 70-B organizations

(now renumbered to Article 97) are

automatically classified as 509(a)(1).

Post-2006 DAF Grant making

Nonprofits

Charities (501(c)(3))

Operating

Foundations

4942(j)(3)

Schools, hospitals,

churches, MROs

Publicly supported

(donations)

509(a)(2)

509(a)(3)

Non-Operating

Foundations

509(a)(1)

ED : Treaty Agreements

Thank you to Caplin & Drysdale, Washington DC

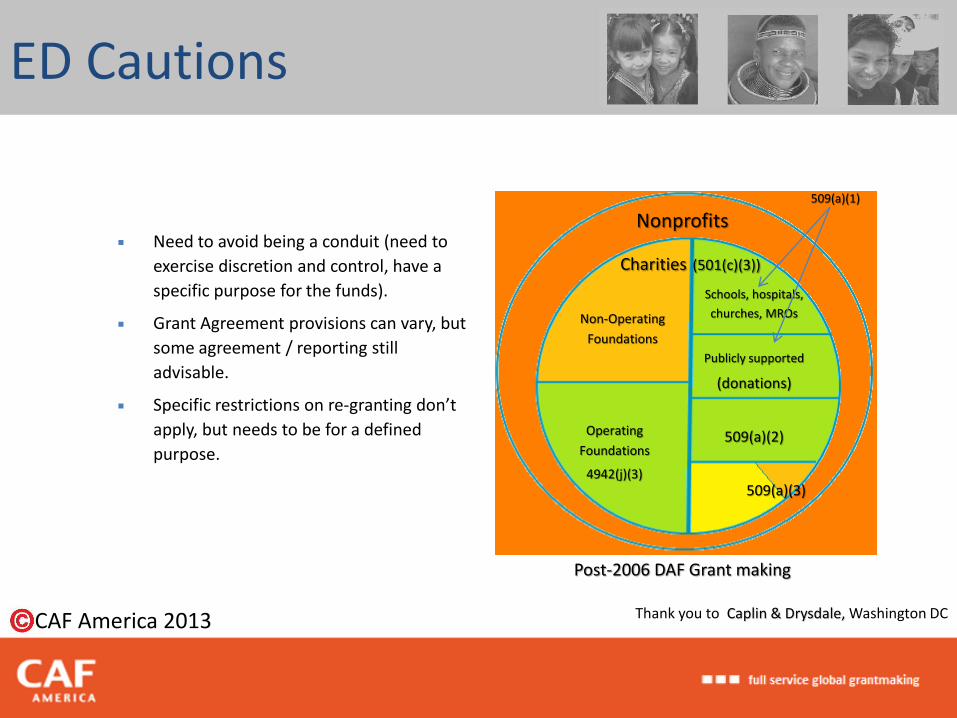

CAF America 2013

Need to avoid being a conduit (need to

exercise discretion and control, have a

specific purpose for the funds).

Grant Agreement provisions can vary, but

some agreement / reporting still

advisable.

Specific restrictions on re-granting don’t

apply, but needs to be for a defined

purpose.

Post-2006 DAF Grant making

Nonprofits

Charities (501(c)(3))

Operating

Foundations

4942(j)(3)

Schools, hospitals,

churches, MROs

Publicly supported

(donations)

509(a)(2)

509(a)(3)

Non-Operating

Foundations

509(a)(1)

ED Cautions

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

Expenditure Responsibility

• Focused on specific funds

• Pre-grant Inquiry

• Restrictive agreements

• Detailed reporting (to CAFA

and to IRS) until all spent.

• Awkward for capital

equipment, regranting

Equivalency

• Focused on the nature of the

grantee.

• Grantee must meet same legal

requirements as US public

charity/operating foundation.

• General support OK, less reporting

required.

• Depends on governing documents

& detailed formulas applied to

finances.

Post-2006 DAF Grant making

Nonprofits

Charities (501(c)(3))

Operating

Foundations

4942(j)(3)

Schools, hospitals,

churches, MROs

Publicly supported

(donations)

509(a)(2)

509(a)(3)

Non-Operating

Foundations

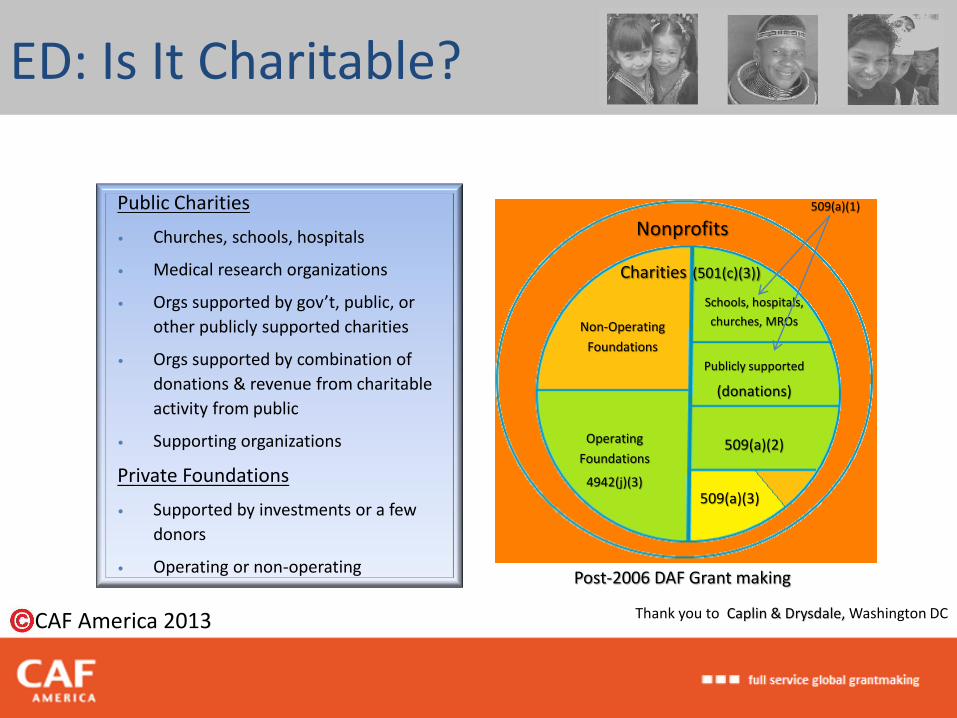

509(a)(1) Public Charities

• Churches, schools, hospitals

• Medical research organizations

• Orgs supported by gov’t, public, or

other publicly supported charities

• Orgs supported by combination of

donations & revenue from charitable

activity from public

• Supporting organizations

Private Foundations

• Supported by investments or a few

donors

• Operating or non-operating

ED: Is It Charitable?

Thank you to Caplin & Drysdale, Washington DC

CAF America 2013

A unique enhanced domestic nonprofit vetting process goes far beyond the standard practice of only verifying IRS charitable status for USA based Charities. We dig deep to ensure our donors are making safe and secure grants; providing confidence regarding governance structure and the application of funds through:

Online grant eligibility application

Ongoing weekly watch list scanning

Verification of current nonprofit business address and banking information.

Identification of nonprofits whose exemption status has been revoked due to IRS BMF exclusion, Pub 78 exclusion, OFAC inclusion and compliance with the Pension Protection Act.

These additional screenings provide peace of mind regarding the governance, leadership and administration of the organization.

Enhanced Domestic

CAF America 2013

Specially Designated Nations (SDN) List: Grant maker may not

engage in transactions with listed persons (or others it knows

to be terrorists or terrorism supporters).

www.treasury.gov/sdn

Voluntary guidelines. Treasury recommends routine

screening of grantees, their officers, directors, and key

employees, especially in high-risk areas.

Controversy over material support. Example of Palestine.

Sanctioned countries. Transactions in certain countries or

with their nationals are forbidden: Cuba, Iran, North Korea,

Sudan (with some exceptions). Other countries have more

limited restrictions.

Office of Foreign Assets Control (OFAC)

CAF America 2013

Foreign organizations owe 30% tax on U.S. source income.

Safe interpretation: Grant maker must withhold

30% of portion of grants to foreign organizations

spent on U.S. activities.

Exceptions. Grant maker can obtain

documentation making such withholding

unnecessary.

W-8BEN if a treaty applies

W-8EXP & opinion of counsel otherwise

Standard GEA prohibits these activities for simplicity.

1441 withholding of tax on nonresident aliens

1441 Withholding

CAF America 2013

CAFAmerica 1800 Diagonal Road, Suite 150

Alexandria, VA 22314

www.CAFAmerica.org

Ted Hart Chief Executive Officer T: +1 (703) 549-8931 F: +1 (703) 549-8934 [email protected]

Serving Corporations, Foundations, Families and Individuals

Thank you