ipo ready – game planning for a public offering

TRANSCRIPT

IPO Ready – Game Planning for a Public OfferingDecember 4,2014D&O Conference

2

© 2014 Protiviti Inc. An Equal Opportunity Employer.

Today’s Discussion

IPO Market Trends

CFO Perspective

IPO Readiness – What Should You Consider?

Call to Action

Legal Considerations

4

IPO MARKET TRENDS

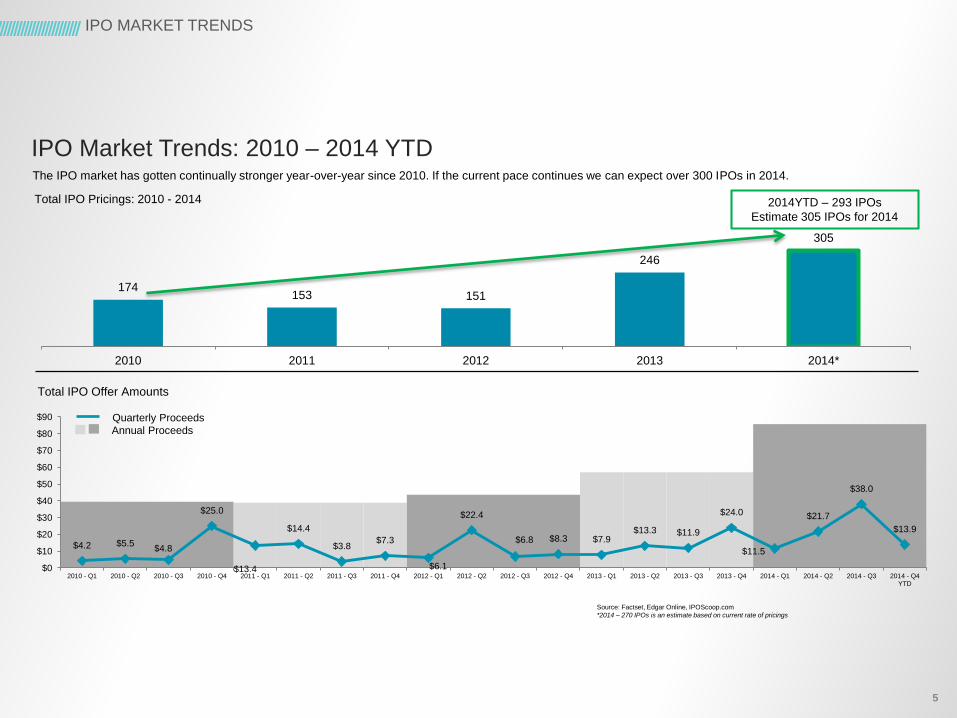

$4.2 $5.5$4.8

$25.0

$13.4

$14.4

$3.8$7.3

$6.1

$22.4

$6.8 $8.3 $7.9$13.3 $11.9

$24.0

$11.5

$21.7

$38.0

$13.9

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

2010 - Q1 2010 - Q2 2010 - Q3 2010 - Q4 2011 - Q1 2011 - Q2 2011 - Q3 2011 - Q4 2012 - Q1 2012 - Q2 2012 - Q3 2012 - Q4 2013 - Q1 2013 - Q2 2013 - Q3 2013 - Q4 2014 - Q1 2014 - Q2 2014 - Q3 2014 - Q4YTD

5

IPO MARKET TRENDS

174153 151

246

305

2010 2011 2012 2013 2014*

Total IPO Pricings: 2010 - 2014

Total IPO Offer Amounts

Source: Factset, Edgar Online, IPOScoop.com

*2014 – 270 IPOs is an estimate based on current rate of pricings

2014YTD – 293 IPOs

Estimate 305 IPOs for 2014

The IPO market has gotten continually stronger year-over-year since 2010. If the current pace continues we can expect over 300 IPOs in 2014.

Quarterly Proceeds

Annual Proceeds

IPO Market Trends: 2010 – 2014 YTD

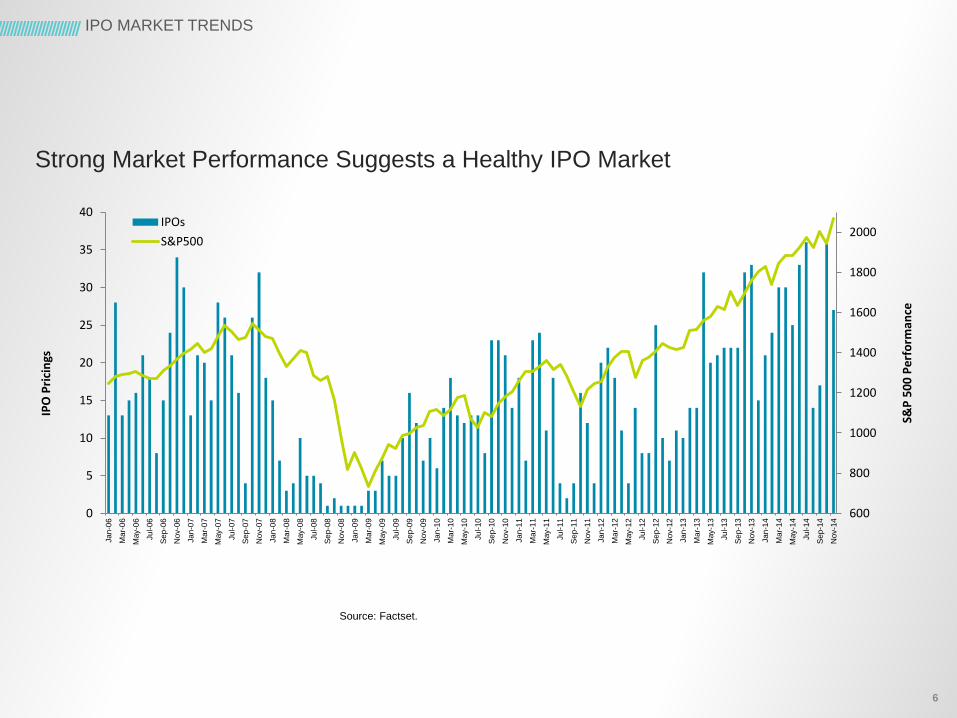

6

IPO MARKET TRENDS

Strong Market Performance Suggests a Healthy IPO Market

Source: Factset.

600

800

1000

1200

1400

1600

1800

2000

0

5

10

15

20

25

30

35

40

Ja

n-0

6

Mar-

06

May-0

6

Ju

l-06

Se

p-0

6

Nov-0

6

Ja

n-0

7

Mar-

07

May-0

7

Ju

l-07

Se

p-0

7

Nov-0

7

Ja

n-0

8

Mar-

08

May-0

8

Ju

l-08

Se

p-0

8

Nov-0

8

Ja

n-0

9

Mar-

09

May-0

9

Ju

l-09

Se

p-0

9

Nov-0

9

Ja

n-1

0

Mar-

10

May-1

0

Ju

l-10

Se

p-1

0

Nov-1

0

Ja

n-1

1

Mar-

11

May-1

1

Ju

l-11

Se

p-1

1

Nov-1

1

Ja

n-1

2

Mar-

12

May-1

2

Ju

l-12

Se

p-1

2

Nov-1

2

Ja

n-1

3

Mar-

13

May-1

3

Ju

l-13

Se

p-1

3

Nov-1

3

Ja

n-1

4

Mar-

14

May-1

4

Ju

l-14

Se

p-1

4

Nov-1

4

S&P

50

0 P

erf

orm

ance

IPO

Pri

cin

gs

IPOs

S&P500

7

IPO MARKET TRENDS

Market Volatility is at Levels Seen in 2006

Source: Factset.

0

10

20

30

40

50

60

70

80

0

5

10

15

20

25

30

35

40

Ja

n-0

6

Mar-

06

May-0

6

Ju

l-06

Se

p-0

6

Nov-0

6

Ja

n-0

7

Mar-

07

May-0

7

Ju

l-07

Se

p-0

7

Nov-0

7

Ja

n-0

8

Mar-

08

May-0

8

Ju

l-08

Se

p-0

8

Nov-0

8

Ja

n-0

9

Mar-

09

May-0

9

Ju

l-09

Se

p-0

9

Nov-0

9

Ja

n-1

0

Mar-

10

May-1

0

Ju

l-10

Se

p-1

0

Nov-1

0

Ja

n-1

1

Mar-

11

May-1

1

Ju

l-11

Se

p-1

1

Nov-1

1

Ja

n-1

2

Mar-

12

May-1

2

Ju

l-12

Se

p-1

2

Nov-1

2

Ja

n-1

3

Mar-

13

May-1

3

Ju

l-13

Se

p-1

3

Nov-1

3

Ja

n-1

4

Mar-

14

May-1

4

Ju

l-14

Se

p-1

4

Nov-1

4

VIX

Mar

ket

Vo

lati

lity

Ind

ex

IPO

Pri

cin

gs

IPOs

VIX

8

IPO MARKET TRENDS

IPO filing activity suggests a robust market

Source: Renaissance Capital.

314

256 263

300

104118

253 257

141

256

347

0

50

100

150

200

250

300

350

400

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Historical New IPO Filings

JOBS Act

Passed

9

IPO MARKET TRENDS

Source: Factset.

13%

2%

19%

16%

9%

4%6%

17%

11%

3%

22%

36%

-1%

4%

-1%

7%

Health Care Financials Info Tech Consumer Energy Industrials Materials Utilities

First Day Return

YTD Returns

2014 IPO Summary (Q1-Q4 YTD) – Positive Returns Across All Sectors

10

IPO MARKET TRENDS

Source: Factset.

20%

17%

18%

15%

20%

7%3%1%

2013 IPO Proceeds

Financials

Health Care

Info Tech

Consumer

Energy

Industrials

Materials

Telecom

23%

11%

38%

6%

16%

4% 2%

2014 YTD IPO Proceeds

2014 IPO Summary (Q1-Q4 YTD) – No Single Dominant Sector

11

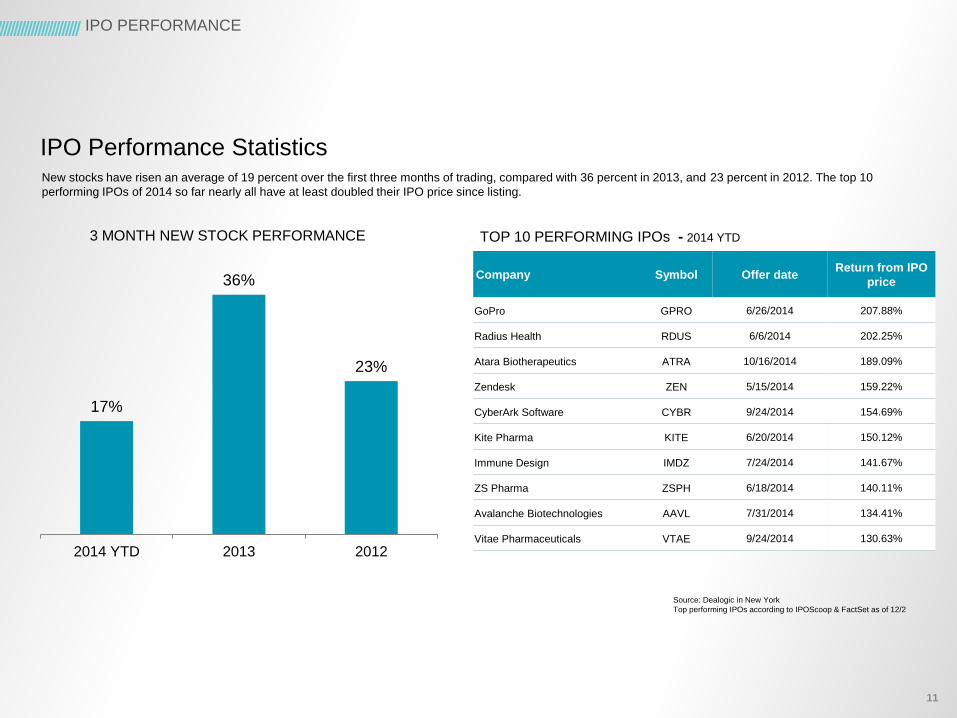

IPO PERFORMANCE

New stocks have risen an average of 19 percent over the first three months of trading, compared with 36 percent in 2013, and 23 percent in 2012. The top 10

performing IPOs of 2014 so far nearly all have at least doubled their IPO price since listing.

17%

36%

23%

2014 YTD 2013 2012

3 MONTH NEW STOCK PERFORMANCE

IPO Performance Statistics

Source: Dealogic in New York

Top performing IPOs according to IPOScoop & FactSet as of 12/2

Company Symbol Offer dateReturn from IPO

price

GoPro GPRO 6/26/2014 207.88%

Radius Health RDUS 6/6/2014 202.25%

Atara Biotherapeutics ATRA 10/16/2014 189.09%

Zendesk ZEN 5/15/2014 159.22%

CyberArk Software CYBR 9/24/2014 154.69%

Kite Pharma KITE 6/20/2014 150.12%

Immune Design IMDZ 7/24/2014 141.67%

ZS Pharma ZSPH 6/18/2014 140.11%

Avalanche Biotechnologies AAVL 7/31/2014 134.41%

Vitae Pharmaceuticals VTAE 9/24/2014 130.63%

TOP 10 PERFORMING IPOs - 2014 YTD

Our approach is our promise—

and your advantage.

• JOE BRANTUK• VICE PRESIDENT // NASDAQ

• +1 415 243 2378 // [email protected]

13

© 2014 Protiviti Inc. An Equal Opportunity Employer.

Legal Considerations

• In April 2012, the Jumpstart Our Business Startups (JOBS) Act became law

• JOBS Act changed the IPO playbook

• Created a new type of issuer – Emerging Growth Company (EGC)

• 85% of IPO issuers since April 2012 were identified as EGCs

• Purposes of JOBS Act

• Easier to go public

• Significant cost savings for IPO process

• On-ramp period provides newly public companies transitional relief from more costly requirements

Background

Testing the waters

Confidential SEC review

Scaled financial disclosure

Reduced executive compensation disclosure

Delayed internal controls audit

Extended phase-in for new GAAP

Primary EGC Accommodations

• Testing the Waters: EGCs can engage in oral or written communications with potential investors that are QIBs or IAIs

• Communications, including offers, permitted before or afterinitial filing of registration statement

• Be prepared to share any testing the waters materials with the SEC

• Confidential Submission: EGCs may submit confidential draft registration statements to SEC

• Does not require board signatures or auditor consent

• No filing fee paid until public filing

• Must publicly file initial submission plus all amendments at least 21 days before conducting traditional road show

EGC Accommodations

• Scaled Financial Disclosure: EGCs may go public

using two years, rather than three years, of audited

financial statements

• Approximately 65% of EGCs have taken advantage of this

accommodation

• Reduced executive compensation disclosure:

• Exempt from full-length CD&A disclosure

• Exempt from Dodd-Frank comp requirements

• Say-on-pay, say-on-frequency and say-on-golden-parachutes

• Pay-for-performance graph and CEO pay ratio disclosure

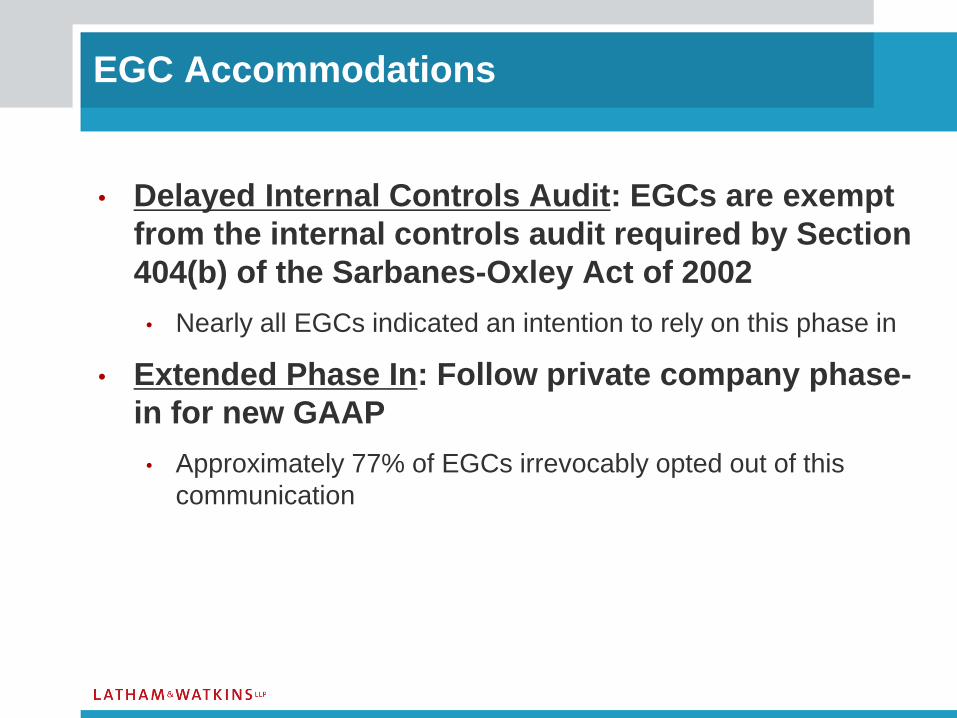

EGC Accommodations

• Delayed Internal Controls Audit: EGCs are exempt

from the internal controls audit required by Section

404(b) of the Sarbanes-Oxley Act of 2002

• Nearly all EGCs indicated an intention to rely on this phase in

• Extended Phase In: Follow private company phase-

in for new GAAP

• Approximately 77% of EGCs irrevocably opted out of this

communication

EGC Accommodations

19

© 2014 Protiviti Inc. An Equal Opportunity Employer.

CFO Perspective

Copyright © 2013 HealthEquity, Inc. All rights reserved. HealthEquity and the HealthEquity logo are registered trademarks and service marks of HealthEquity, Inc.

Confidential and proprietary. Reproduction without express written consent is prohibited.

Darcy Mott

HealthEquity, Inc.

EVP & CFO

HQY IPO Timeline

HQY initial public offering (IPO) timeline

IPO Preparation

11.01.12 – PwC appointed as the Company’s auditors.

01.22.14 – PwC IPO readiness study issued

01.30.14 – JP Morgan & Wells Fargo were selected as lead bankers for

the IPO; Willkie Farr Gallagher was appointed as the Company’s external

corporate counsel.

02.04.14 – Hired Westwicke as the Company’s investor relations (IR) firm.

02.14.14 – HQY’s IPO organizational meeting.

04.05.12 – The Jumpstart Our Business Startups Act or JOBS Act was

signed into law by President Obama.

HQY initial public offering (IPO) timeline

04.02.14 – Filed Form S-1 (confidential filing).

05.09.14 – Filed Form S-1 Amendment 1

(confidential filing).

06.06.14 – Analyst Day: JP Morgan, Wells

Fargo, Raymond James, Baird, SunTrust.

06.10.14 – Filed Form S-1 publicly with the SEC

which included the FY15 Q1 financials.

IPO Process

07.16.14 – The Board passed numerous

resolutions authorizing the Company to

proceed with the IPO.

07.17.14 – Filed S-1 Amendment 2 with

price range on cover ($10-$12/share);

print preliminary prospectus (Red

Herring).

07.18.14 – IPO launched (teach-ins &

roadshow).

Baltimore, New Jersey, New York, Boston,

New York, Chicago, San Francisco, Los

Angeles, Denver, Portland, Seattle.

07.30.14 – Concluded roadshow; pricing

$14/share; HQY effective with the SEC;

finalized share allocation; issued pricing

press release; Final preparations to

starting trading on 07.31.

07.31.14 – Issued 10.465M shares;

raising $132.4M net, including the over

allotment shares; Ringing the NASDAQ

opening bell celebration, Open trading at

$20/share.

08.01.14 – Filed the final prospectus with

the SEC.

HQY initial public offering (IPO) timeline

Post-IPO activities

09.12.14 – HQY files FY15 Q2, Form 10-Q with the SEC.

09.09.14 – HQY FY15 second quarter earnings release and call.

08.25.14 – HQY Post-IPO quiet period expires. Research analysts

Release first set of research reports on HQY.

09.04.14 – HQY conducted its first Board of Directors Meeting,

as a publicly traded company.

09.03.14 – HQY conducted its first Audit and Compensation Committee

Meetings of the Board of Directors, as a publicly traded company.

LET’S GO

PUBLIC!

maybe…

25

Which image comes to your mind

when you hear the word “IPO”?

Let’s Go Public!maybe…

29

Here are a few of my personal

favorites…

Let’s Go Public!maybe…

Table of Contents

Copyright © 2014 Vivint Solar All Rights Reserved

39

Cash

Liquidity – stockholders /

employees

Acquisition currency

Access to public markets for

future financings

Enhancement of company’s

stature

Perceived stability and

competitive position

Enhancement of market value

IPO 101 Is it really worth it?

Benefits:

Distraction

Restrictions on publicity and

other marketing activities

Compliance obligations – SEC

reporting, Reg. FD, Frank-

Dodd, SOX, NYSE/Nasdaq,

etc.

Reduced flexibility

Liability

Loss of control

Vulnerability to takeover

Burdens:

40

Running a public company is NOT for the faint of heart

Does your company have the “right stuff”?

Disciplined and experienced management team?

Strong internal financial and accounting team and internal controls?

Large TAM, sustainable growth rate and reasonable visibility as to future

financial results?

Sustainable and scalable business model and defensible competitive

position?

Is an IPO really the best route to achieving the company’s objectives?

Why do you want to go public?

Be thoughtful and deliberate

IPO 101 Are you Ready?

41

Running a public company is NOT for the faint of heart

Does your company meet the criteria of underwriters and the market?

Would your company’s offering benefit from the achievement of

additional milestones?

Can company management participate in the offering process without

jeopardizing the company’s business operations?

Is your company prepared to operate under strict publicity guidelines?

Is your company prepared to make the level of disclosure required in

connection with the IPO and on an on-going basis?

Is your company prepared to meet the ongoing obligations of being a

public company?

IPO 101 Are you Ready?

42

Running a public company is NOT for the faint of heart

Are your insiders willing to relinquish control and answer to the

company’s new public stockholders (and the shareholder advisory

groups – e.g., ISS and Glass Lewis)

Can your company meet stock exchange listing requirements?

Is an IPO really the best route to achieving the company’s objectives?

Is your company prepared to make the level of disclosure required in

connection with the IPO and on an on-going basis?

Is your company prepared to meet the ongoing obligations of being a

public company?

IPO 101 Are you Ready?

43

Build for success

Hire good, honest people who possess the right skillsets and have the right

experience – THIS IS CRITICAL, SO DON’T SETTLE!

The Chief Financial Officer and his accounting and finance team more

important than you might think

The Chief Legal Officer is more important than you might want to

acknowledge

Build a “real” board of directors and set expectations

Build a good relationship with experienced legal counsel and independent

auditors

Build a good relationship with investment banks and financial analysts

TripleLindy’s IPO Tips

44

Perform regular independent 409A valuations

Stock option exercise pricing is a hot button for the SEC (and the IRS)

Involve your auditors

Run your company like a public company for at least 2 quarters before

starting the IPO process

Ensure that your systems and controls are run through the simulator before

you head into deep space

Involve your auditors in a simulated quarter close

Simulate an earnings call and all of the prep work required

Perform annual audits of your financials

Have your auditors perform annual audits each year

As you near preparations for an IPO, prepare quarterly information

TripleLindy’s IPO Tips

45

In the year or two leading up to an IPO, devote appropriate time to

developing relationships with investment banks and their analysts

Attend and speak at conferences

Get to know the analysts who cover your space and let them get to know

you

Ensure that your records are “squeaky clean” and create a dynamic data

room that you keep up to date on a regular basis

Review your stock and stock option records

Review your employment documents and material contracts – with

suppliers, customers, partners

Build the best IPO team you possibly can

Remember – You will be judged by the company you keep

Legal counsel, independent auditors, underwriters, compensation

consultant, D&O insurance broker and carriers, investor relations, stock

exchange, transfer agent, financial printer, stock administrator

TripleLindy’s IPO Tips

46

© 2014 Protiviti Inc. An Equal Opportunity Employer.

IPO Readiness – What Should You Consider?

Call to Action - IPO Musts and Common Pitfalls

IPO Musts and Common Pitfalls

Musts

• Operate like a public company

• Develop solid infrastructure

• Assemble a superb team

• Establish excellent corporate governance

• Execute well planned positioning and communication strategy

• Develop a public company consciousness among employees

IPO Musts and Common Pitfalls

Common Pitfalls

• Under-estimating the effort required

• Failure to develop sound processes and infrastructure

- especially those around financial reporting

• Not having the right team assembled

• Not assessing IT infrastructure readiness

• Under-estimating the intrusiveness of being a public

company, including the time demands from the

investment community

This document contains material proprietary to Protiviti Inc. ("Protiviti"), a wholly-owned subsidiary of Robert Half International Inc. ("RHI"). RHI is a publicly- traded company.

51

© 2014 Protiviti Inc. An Equal Opportunity Employer.

Today’s Moderator: Steve Hobbs

Steve Hobbs is Protiviti's Managing

Director leading the Public Company

Transformation solution. He works

extensively with a number of pre-IPO

companies in the social media, technology,

and consumer products industries. He has

served over 100 public companies during

his 30 year career with support in IPO

preparation & execution, M&A

transactions, international expansion and

numerous operational issues. He has

served on the board of directors of three

companies, one as Chairman and two as

Audit Committee Chair.