investor teleconference presentation - avalonbay...

TRANSCRIPT

Fourth Quarter 2014 January 29, 2015

Investor Teleconference

Presentation

AVALON ALDERWOOD

Lynnwood, WA

EAVES CREEKSIDE

Mountain View, CA

AVA HIGH LINE

New York, NY

2

See Appendix for information about

Forward-Looking Statements and definitions

of non-GAAP financial measures and other terms.

INTRODUCTION

Participants:

Tim Naughton, Chairman & CEO

Kevin O’Shea, Chief Financial Officer

Matt Birenbaum, Chief Investment Officer

Sean Breslin, Chief Operating Officer

3

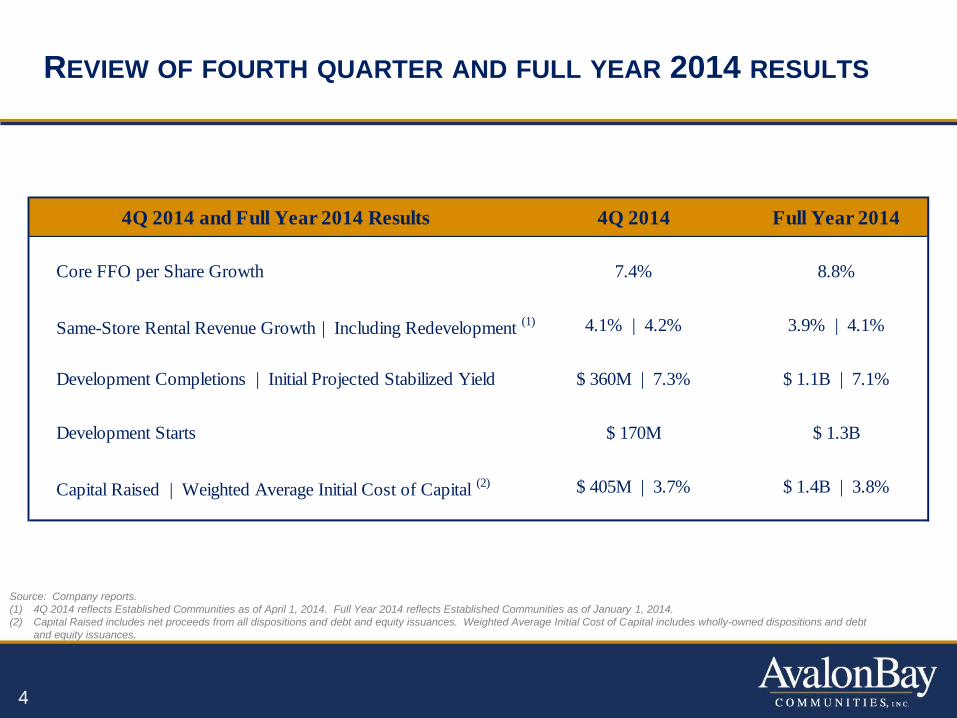

REVIEW OF FOURTH QUARTER AND FULL YEAR 2014 RESULTS

Source: Company reports.

(1) 4Q 2014 reflects Established Communities as of April 1, 2014. Full Year 2014 reflects Established Communities as of January 1, 2014.

(2) Capital Raised includes net proceeds from all dispositions and debt and equity issuances. Weighted Average Initial Cost of Capital includes wholly-owned dispositions and debt

and equity issuances.

4

4Q 2014 and Full Year 2014 Results 4Q 2014 Full Year 2014

Core FFO per Share Growth 7.4% 8.8%

Same-Store Rental Revenue Growth | Including Redevelopment

(1) 4.1% | 4.2% 3.9% | 4.1%

Development Completions | Initial Projected Stabilized Yield $ 360M | 7.3% $ 1.1B | 7.1%

Development Starts $ 170M $ 1.3B

Capital Raised | Weighted Average Initial Cost of Capital (2) $ 405M | 3.7% $ 1.4B | 3.8%

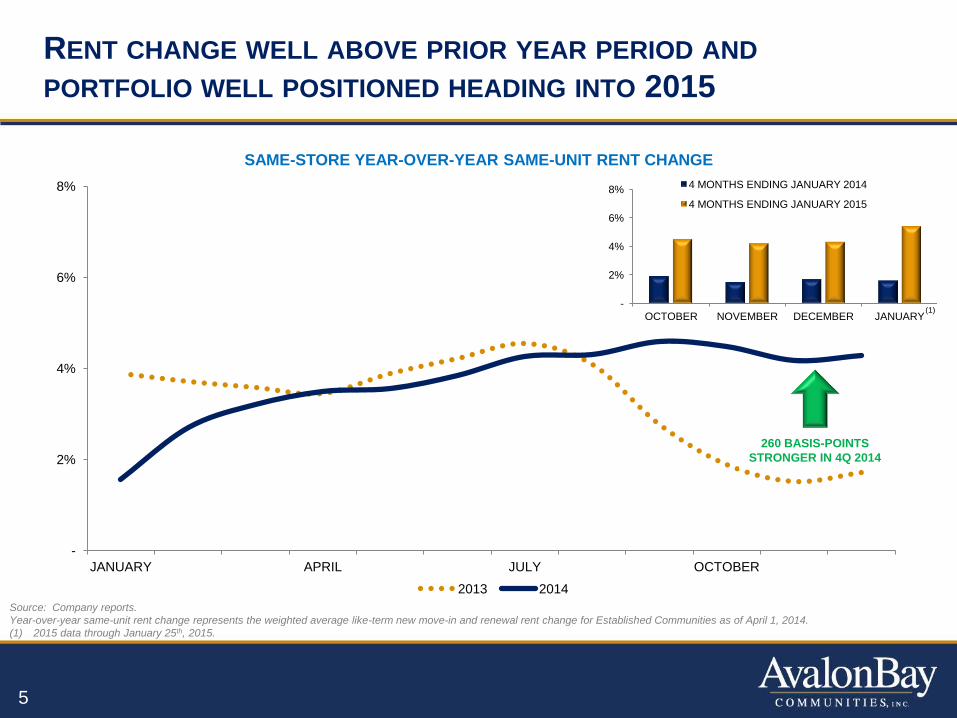

RENT CHANGE WELL ABOVE PRIOR YEAR PERIOD AND

PORTFOLIO WELL POSITIONED HEADING INTO 2015

Source: Company reports.

Year-over-year same-unit rent change represents the weighted average like-term new move-in and renewal rent change for Established Communities as of April 1, 2014.

(1) 2015 data through January 25th, 2015.

SAME-STORE YEAR-OVER-YEAR SAME-UNIT RENT CHANGE

-

2%

4%

6%

8%

JANUARY APRIL JULY OCTOBER

2013 2014

-

2%

4%

6%

8%

OCTOBER NOVEMBER DECEMBER JANUARY

4 MONTHS ENDING JANUARY 2014

4 MONTHS ENDING JANUARY 2015

(1)

260 BASIS-POINTS

STRONGER IN 4Q 2014

5

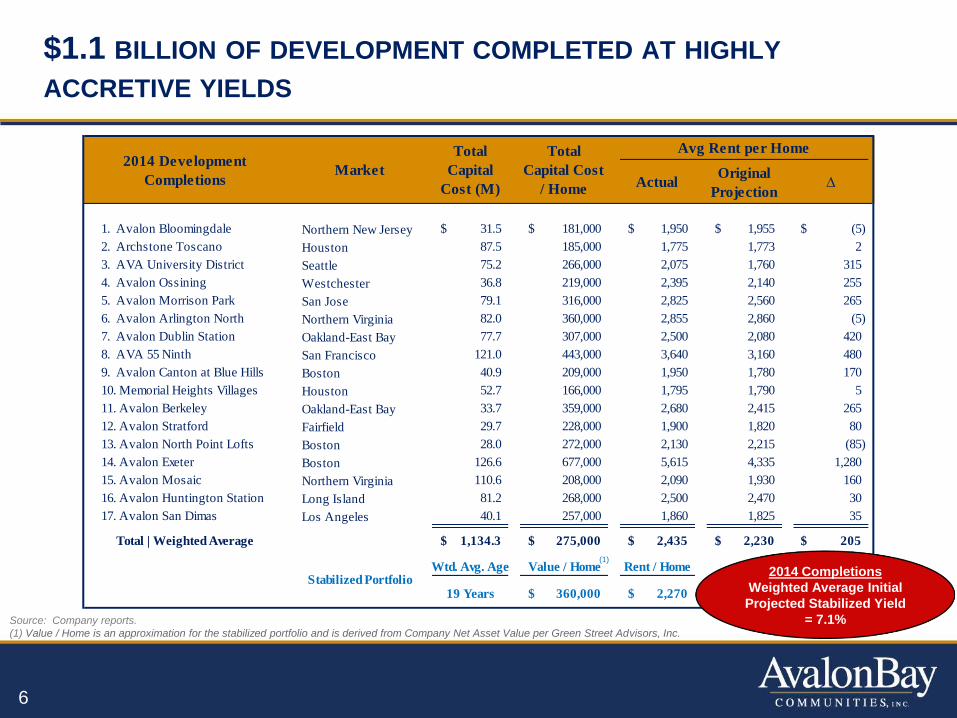

ActualOriginal

ProjectionD

1. Avalon Bloomingdale Northern New Jersey 31.5$ 181,000$ 1,950$ 1,955$ (5)$

2. Archstone Toscano Houston 87.5 185,000 1,775 1,773 2

3. AVA University District Seattle 75.2 266,000 2,075 1,760 315

4. Avalon Ossining Westchester 36.8 219,000 2,395 2,140 255

5. Avalon Morrison Park San Jose 79.1 316,000 2,825 2,560 265

6. Avalon Arlington North Northern Virginia 82.0 360,000 2,855 2,860 (5)

7. Avalon Dublin Station Oakland-East Bay 77.7 307,000 2,500 2,080 420

8. AVA 55 Ninth San Francisco 121.0 443,000 3,640 3,160 480

9. Avalon Canton at Blue Hills Boston 40.9 209,000 1,950 1,780 170

10. Memorial Heights Villages Houston 52.7 166,000 1,795 1,790 5

11. Avalon Berkeley Oakland-East Bay 33.7 359,000 2,680 2,415 265

12. Avalon Stratford Fairfield 29.7 228,000 1,900 1,820 80

13. Avalon North Point Lofts Boston 28.0 272,000 2,130 2,215 (85)

14. Avalon Exeter Boston 126.6 677,000 5,615 4,335 1,280

15. Avalon Mosaic Northern Virginia 110.6 208,000 2,090 1,930 160

16. Avalon Huntington Station Long Island 81.2 268,000 2,500 2,470 30

17. Avalon San Dimas Los Angeles 40.1 257,000 1,860 1,825 35

Total | Weighted Average 1,134.3$ 275,000$ 2,435$ 2,230$ 205$

Wtd. Avg. Age Value / Home Rent / Home

19 Years 360,000$ 2,270$ Stabilized Portfolio

2014 Development

Completions

Total

Capital

Cost (M)

Total

Capital Cost

/ Home

Market

Avg Rent per Home

$1.1 BILLION OF DEVELOPMENT COMPLETED AT HIGHLY

ACCRETIVE YIELDS

Source: Company reports.

(1) Value / Home is an approximation for the stabilized portfolio and is derived from Company Net Asset Value per Green Street Advisors, Inc.

(1)

6

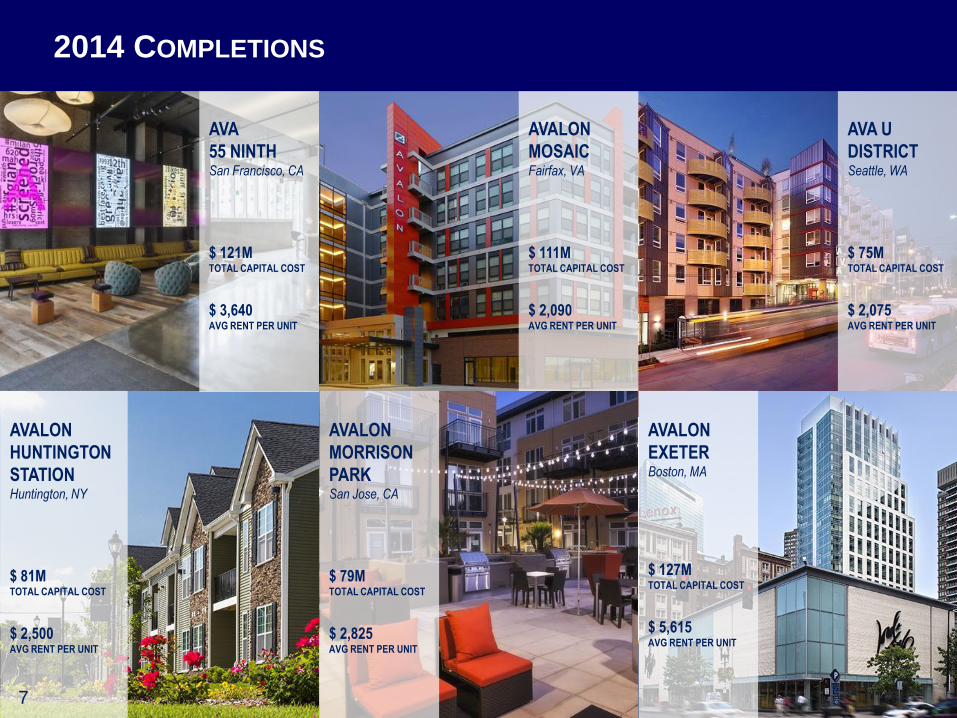

2014 Completions

Weighted Average Initial

Projected Stabilized Yield

= 7.1%

AVA U

DISTRICT Seattle, WA

$ 75M TOTAL CAPITAL COST

$ 2,075 AVG RENT PER UNIT

AVALON

MOSAIC Fairfax, VA

$ 111M TOTAL CAPITAL COST

$ 2,090 AVG RENT PER UNIT

AVA

55 NINTH San Francisco, CA

$ 121M TOTAL CAPITAL COST

$ 3,640 AVG RENT PER UNIT

AVALON

EXETER Boston, MA

$ 127M TOTAL CAPITAL COST

$ 5,615 AVG RENT PER UNIT

AVALON

MORRISON

PARK San Jose, CA

$ 79M TOTAL CAPITAL COST

$ 2,825 AVG RENT PER UNIT

AVALON

HUNTINGTON

STATION Huntington, NY

$ 81M TOTAL CAPITAL COST

$ 2,500 AVG RENT PER UNIT

2014 COMPLETIONS

7

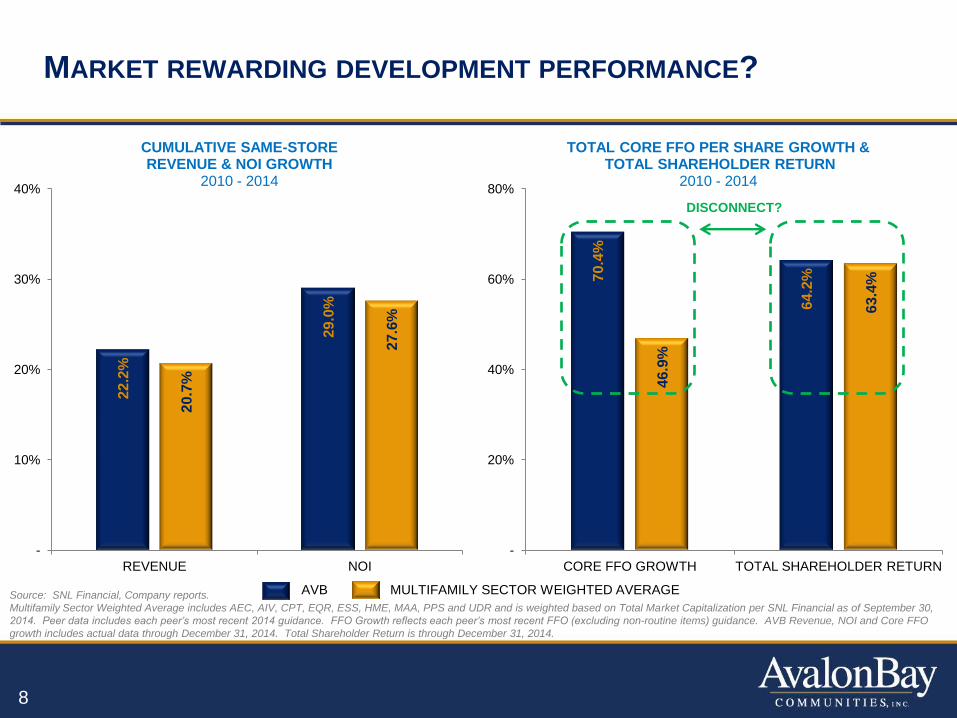

MARKET REWARDING DEVELOPMENT PERFORMANCE?

Source: SNL Financial, Company reports.

Multifamily Sector Weighted Average includes AEC, AIV, CPT, EQR, ESS, HME, MAA, PPS and UDR and is weighted based on Total Market Capitalization per SNL Financial as of September 30,

2014. Peer data includes each peer’s most recent 2014 guidance. FFO Growth reflects each peer’s most recent FFO (excluding non-routine items) guidance. AVB Revenue, NOI and Core FFO

growth includes actual data through December 31, 2014. Total Shareholder Return is through December 31, 2014.

22.2

%

29.0

%

20.7

%

27.6

%

-

10%

20%

30%

40%

REVENUE NOI

CUMULATIVE SAME-STORE REVENUE & NOI GROWTH

2010 - 2014

70.4

%

64.2

%

46.9

%

63.4

%

-

20%

40%

60%

80%

CORE FFO GROWTH TOTAL SHAREHOLDER RETURN

TOTAL CORE FFO PER SHARE GROWTH & TOTAL SHAREHOLDER RETURN

2010 - 2014

AVB MULTIFAMILY SECTOR WEIGHTED AVERAGE

8

DISCONNECT?

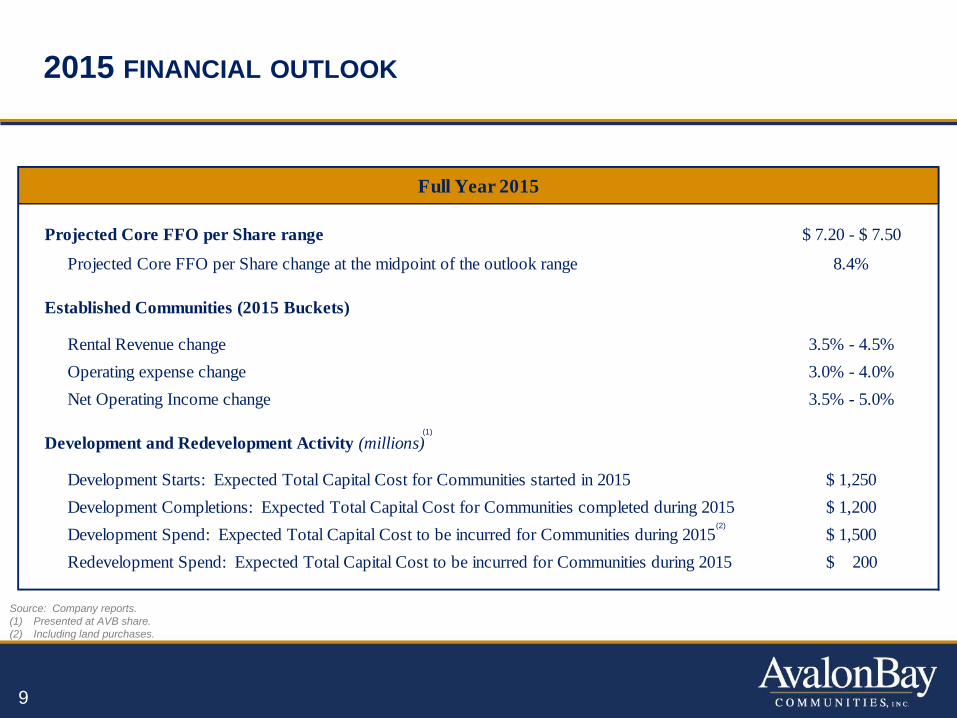

Full Year 2015

Projected Core FFO per Share range $ 7.20 - $ 7.50

Projected Core FFO per Share change at the midpoint of the outlook range 8.4%

Established Communities (2015 Buckets)

Rental Revenue change 3.5% - 4.5%

Operating expense change 3.0% - 4.0%

Net Operating Income change 3.5% - 5.0%

Development and Redevelopment Activity (millions)

Development Starts: Expected Total Capital Cost for Communities started in 2015 $ 1,250

Development Completions: Expected Total Capital Cost for Communities completed during 2015 $ 1,200

Development Spend: Expected Total Capital Cost to be incurred for Communities during 2015 $ 1,500

Redevelopment Spend: Expected Total Capital Cost to be incurred for Communities during 2015 $ 200

2015 FINANCIAL OUTLOOK

Source: Company reports.

(1) Presented at AVB share.

(2) Including land purchases.

9

(1)

(2)

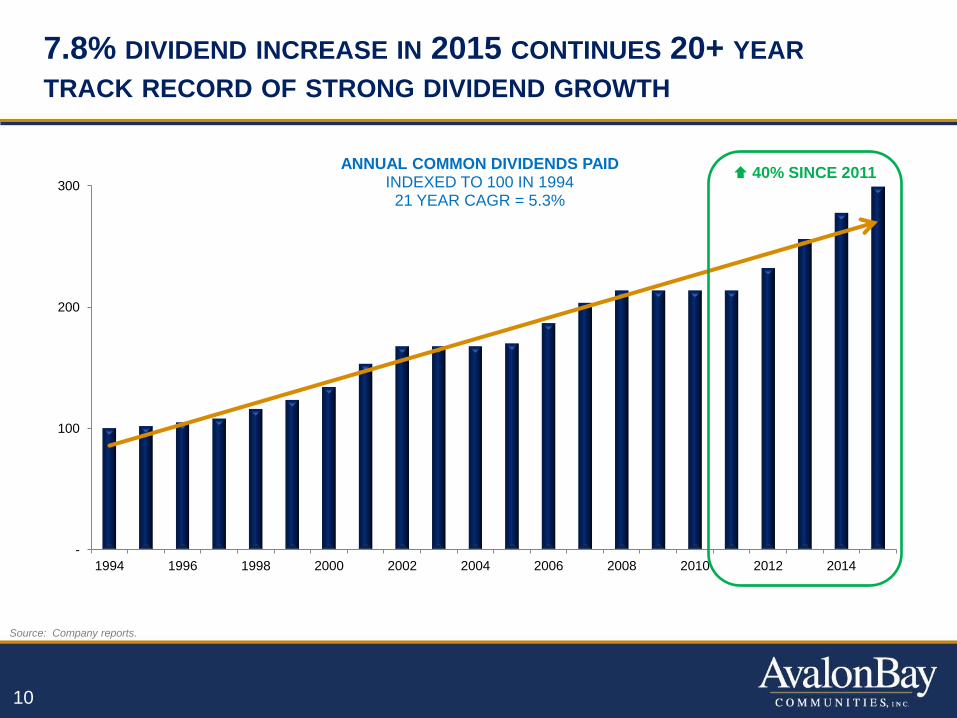

7.8% DIVIDEND INCREASE IN 2015 CONTINUES 20+ YEAR

TRACK RECORD OF STRONG DIVIDEND GROWTH

Source: Company reports.

-

100

200

300

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

ANNUAL COMMON DIVIDENDS PAID INDEXED TO 100 IN 1994

21 YEAR CAGR = 5.3%

40% SINCE 2011

10

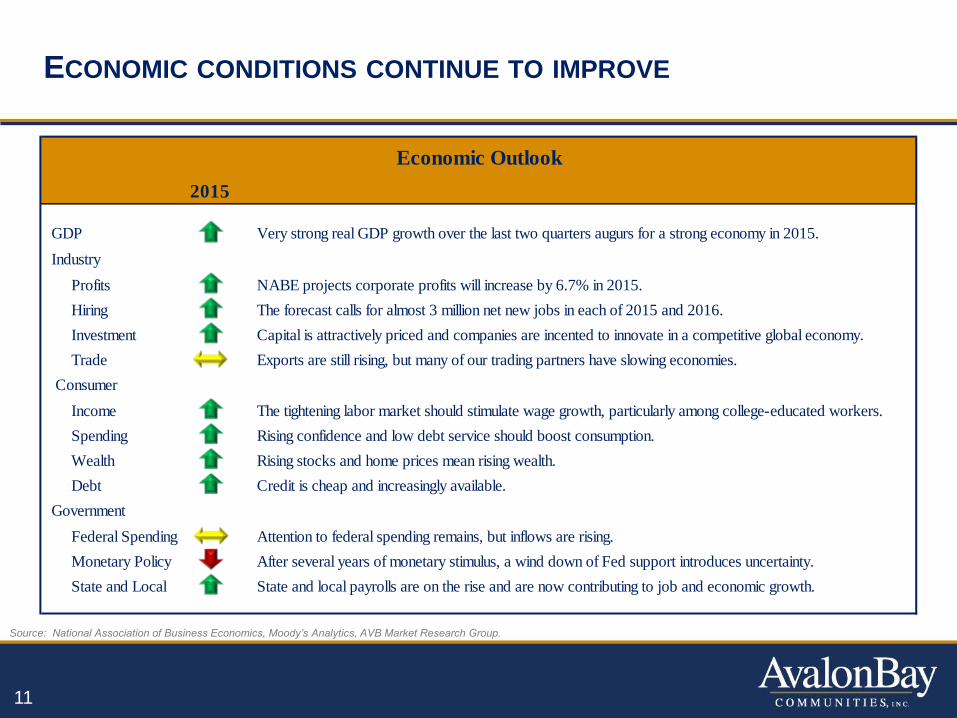

ECONOMIC CONDITIONS CONTINUE TO IMPROVE

11

Source: National Association of Business Economics, Moody’s Analytics, AVB Market Research Group.

Economic Outlook

2015

GDP Very strong real GDP growth over the last two quarters augurs for a strong economy in 2015.

Industry

Profits NABE projects corporate profits will increase by 6.7% in 2015.

Hiring The forecast calls for almost 3 million net new jobs in each of 2015 and 2016.

Investment Capital is attractively priced and companies are incented to innovate in a competitive global economy.

Trade Exports are still rising, but many of our trading partners have slowing economies.

Consumer

Income The tightening labor market should stimulate wage growth, particularly among college-educated workers.

Spending Rising confidence and low debt service should boost consumption.

Wealth Rising stocks and home prices mean rising wealth.

Debt Credit is cheap and increasingly available.

Government

Federal Spending Attention to federal spending remains, but inflows are rising.

Monetary Policy After several years of monetary stimulus, a wind down of Fed support introduces uncertainty.

State and Local State and local payrolls are on the rise and are now contributing to job and economic growth.

2.1

%

1.9

%

1.9

%

1.7

%

0.4

%

3.6

%

3.0

%

2.3

%

2.2

% 2.5

%

2.5

%

2.4

%

2.0

%

2.9

%

2.6

%

2.6

%

-

1%

2%

3%

4%

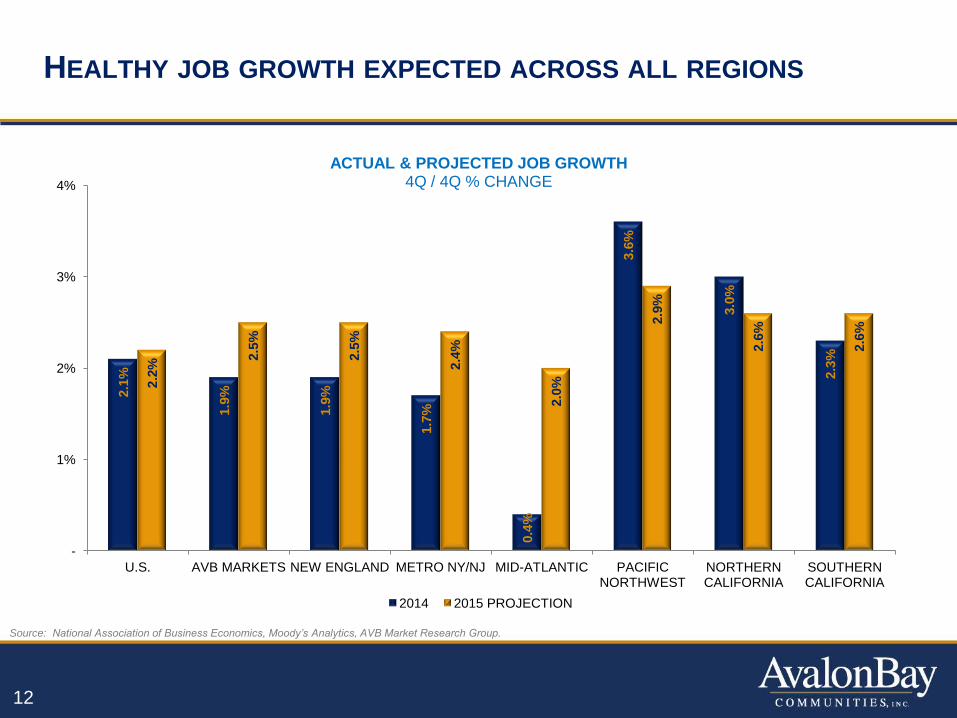

U.S. AVB MARKETS NEW ENGLAND METRO NY/NJ MID-ATLANTIC PACIFIC NORTHWEST

NORTHERN CALIFORNIA

SOUTHERN CALIFORNIA

ACTUAL & PROJECTED JOB GROWTH 4Q / 4Q % CHANGE

2014 2015 PROJECTION

HEALTHY JOB GROWTH EXPECTED ACROSS ALL REGIONS

12

Source: National Association of Business Economics, Moody’s Analytics, AVB Market Research Group.

4.2

%

4.8

%

4.9

%

4.8

%

3.9

%

7.0

%

5.1

%

4.8

%

6.0

% 6.7

%

6.7

%

6.6

%

6.4

% 7.2

%

6.9

%

6.9

%

-

2%

4%

6%

8%

10%

U.S. AVB MARKETS NEW ENGLAND METRO NY/NJ MID-ATLANTIC PACIFIC NORTHWEST

NORTHERN CALIFORNIA

SOUTHERN CALIFORNIA

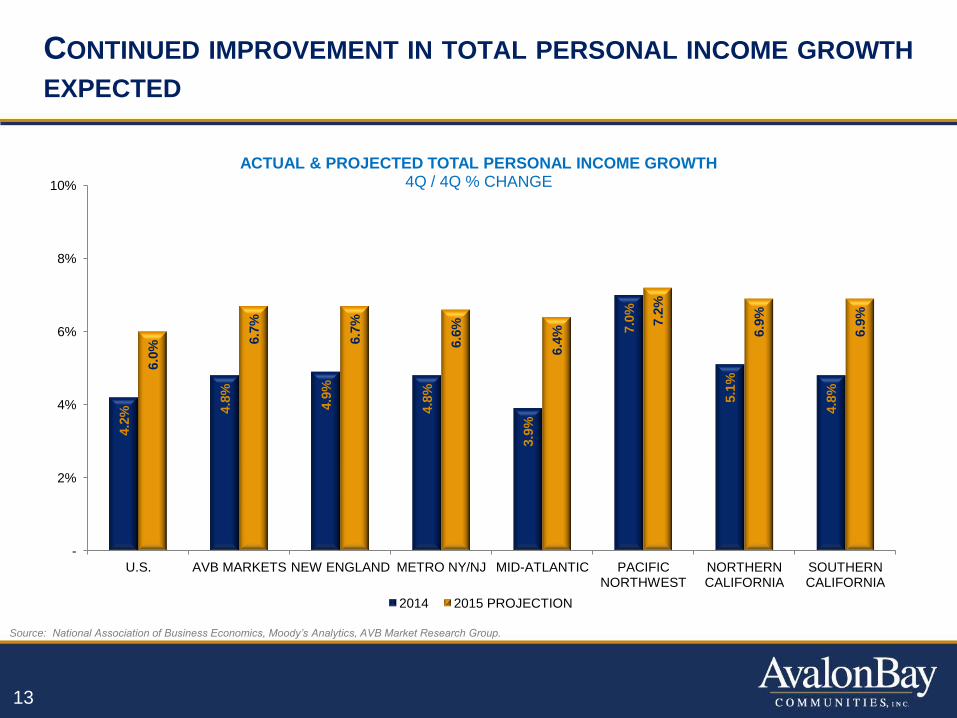

ACTUAL & PROJECTED TOTAL PERSONAL INCOME GROWTH 4Q / 4Q % CHANGE

2014 2015 PROJECTION

CONTINUED IMPROVEMENT IN TOTAL PERSONAL INCOME GROWTH

EXPECTED

13

Source: National Association of Business Economics, Moody’s Analytics, AVB Market Research Group.

1.8

%

2.1

%

1.5

%

3.4

%

3.6

%

1.4

%

0.8

%

2.4

%

2.7

%

2.0

%

4.1

%

4.1

%

2.7

%

1.3

%

1.9

%

2.2

%

1.9

%

2.9

%

3.2

%

1.4

%

1.1

%

-

2%

4%

6%

AVB MARKETS NEW ENGLAND METRO NY/NJ MID-ATLANTIC PACIFIC NORTHWEST

NORTHERN CALIFORNIA

SOUTHERN CALIFORNIA

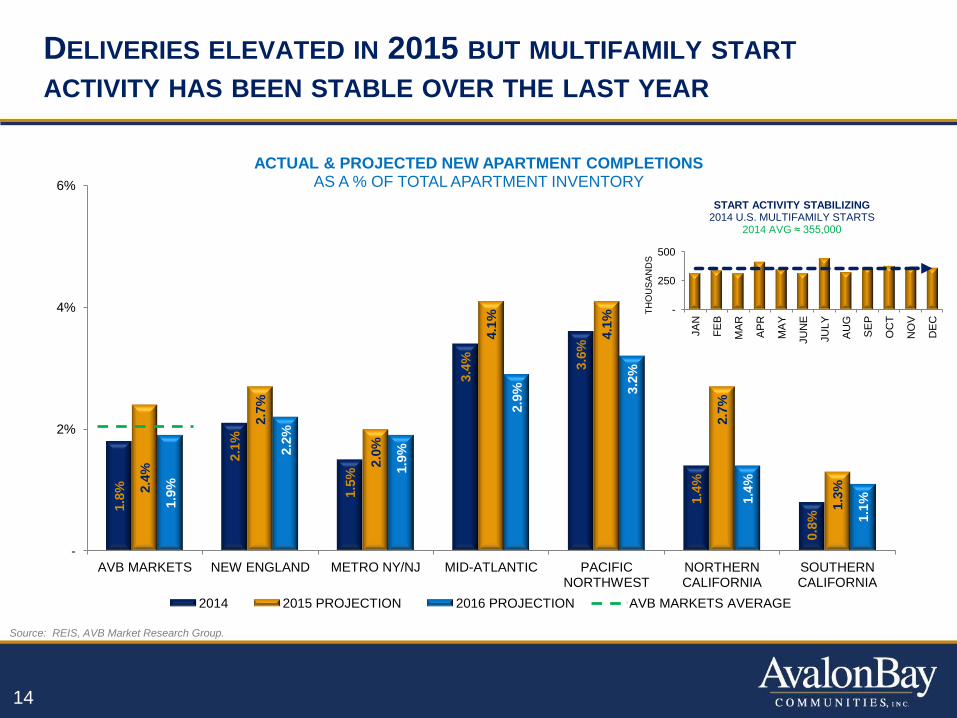

ACTUAL & PROJECTED NEW APARTMENT COMPLETIONS AS A % OF TOTAL APARTMENT INVENTORY

2014 2015 PROJECTION 2016 PROJECTION AVB MARKETS AVERAGE

DELIVERIES ELEVATED IN 2015 BUT MULTIFAMILY START

ACTIVITY HAS BEEN STABLE OVER THE LAST YEAR

14

Source: REIS, AVB Market Research Group.

-

250

500

JA

N

FE

B

MA

R

AP

R

MA

Y

JU

NE

JU

LY

AU

G

SE

P

OC

T

NO

V

DE

C T

HO

US

AN

DS

START ACTIVITY STABILIZING 2014 U.S. MULTIFAMILY STARTS

2014 AVG ≈ 355,000

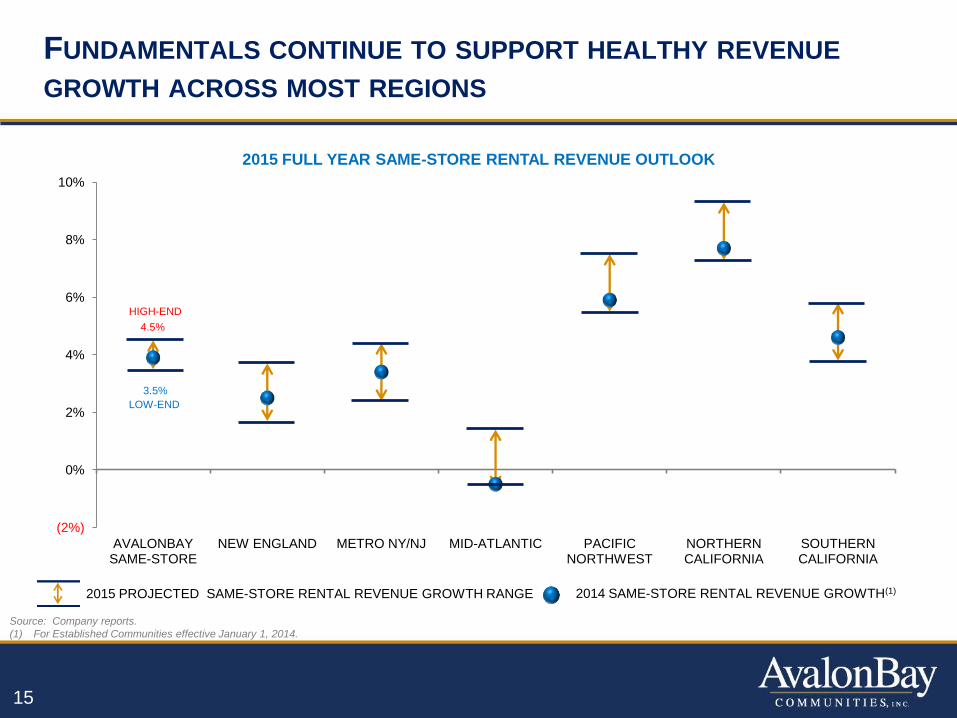

FUNDAMENTALS CONTINUE TO SUPPORT HEALTHY REVENUE

GROWTH ACROSS MOST REGIONS

15

Source: Company reports.

(1) For Established Communities effective January 1, 2014.

4.5%

3.5%

(2%)

0%

2%

4%

6%

8%

10%

AVALONBAY SAME-STORE

NEW ENGLAND METRO NY/NJ MID-ATLANTIC PACIFIC NORTHWEST

NORTHERN CALIFORNIA

SOUTHERN CALIFORNIA

2015 FULL YEAR SAME-STORE RENTAL REVENUE OUTLOOK

HIGH-END

LOW-END

2014 SAME-STORE RENTAL REVENUE GROWTH(1) 2015 PROJECTED SAME-STORE RENTAL REVENUE GROWTH RANGE

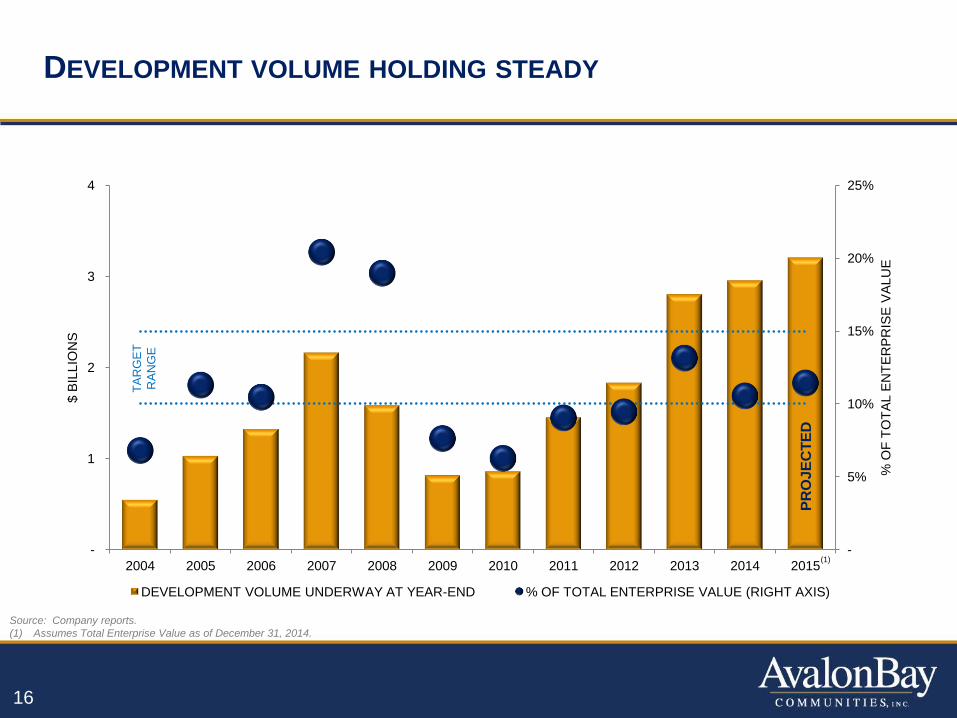

DEVELOPMENT VOLUME HOLDING STEADY

-

5%

10%

15%

20%

25%

-

1

2

3

4

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

% O

F T

OT

AL E

NT

ER

PR

ISE

VA

LU

E

$ B

ILLIO

NS

DEVELOPMENT VOLUME UNDERWAY AT YEAR-END % OF TOTAL ENTERPRISE VALUE (RIGHT AXIS)

PR

OJ

EC

TE

D

TA

RG

ET

RA

NG

E

Source: Company reports.

(1) Assumes Total Enterprise Value as of December 31, 2014.

16

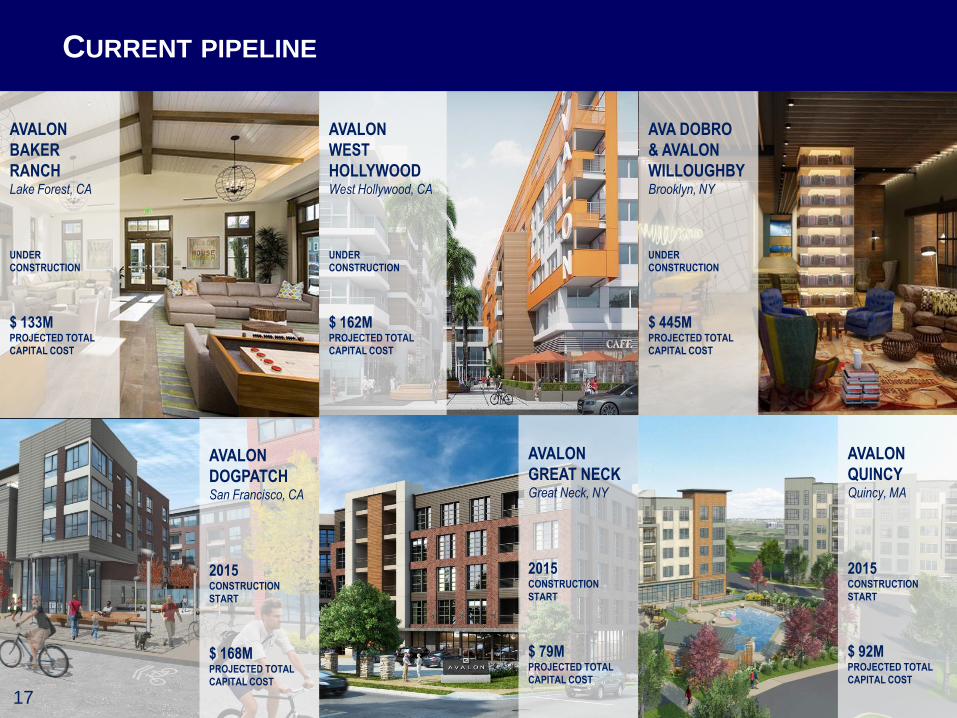

(1)

AVALON

BAKER

RANCH Lake Forest, CA

UNDER

CONSTRUCTION

$ 133M PROJECTED TOTAL

CAPITAL COST

AVA DOBRO

& AVALON

WILLOUGHBY Brooklyn, NY

UNDER

CONSTRUCTION

$ 445M PROJECTED TOTAL

CAPITAL COST

AVALON

WEST

HOLLYWOOD West Hollywood, CA

UNDER

CONSTRUCTION

$ 162M PROJECTED TOTAL

CAPITAL COST

AVALON

QUINCY Quincy, MA

2015 CONSTRUCTION

START

$ 92M PROJECTED TOTAL

CAPITAL COST

AVALON

DOGPATCH San Francisco, CA

2015 CONSTRUCTION

START

$ 168M PROJECTED TOTAL

CAPITAL COST

AVALON

GREAT NECK Great Neck, NY

2015 CONSTRUCTION

START

$ 79M PROJECTED TOTAL

CAPITAL COST

CURRENT PIPELINE

17

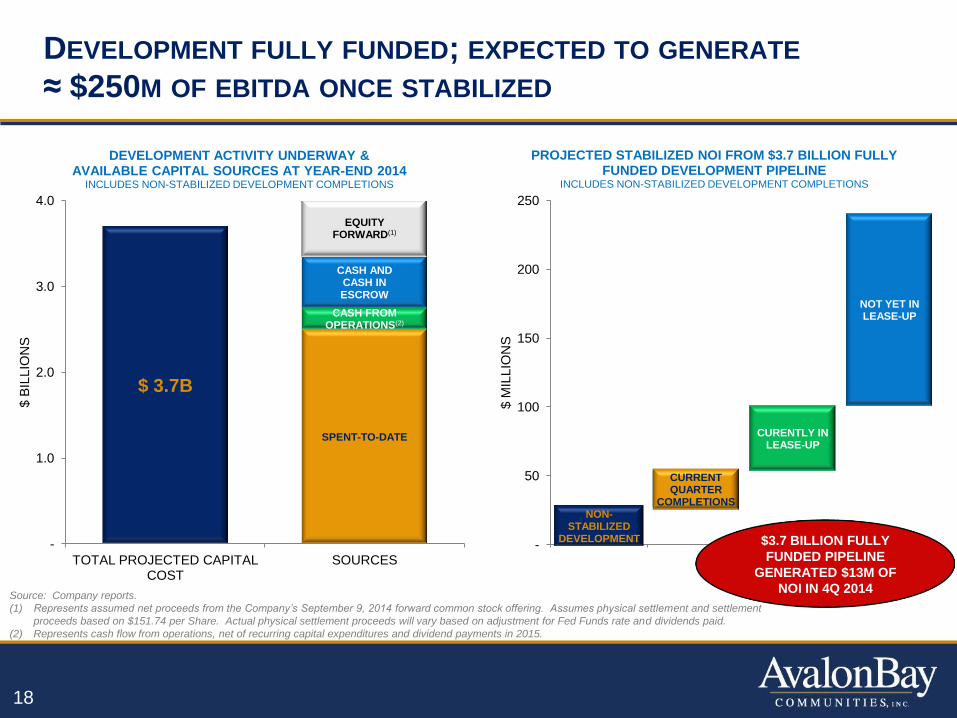

DEVELOPMENT FULLY FUNDED; EXPECTED TO GENERATE

≈ $250M OF EBITDA ONCE STABILIZED

$ 3.7B

SPENT-TO-DATE

CASH FROM OPERATIONS(2)

CASH AND CASH IN ESCROW

EQUITY FORWARD(1)

-

1.0

2.0

3.0

4.0

TOTAL PROJECTED CAPITAL COST

SOURCES

$ B

ILLIO

NS

DEVELOPMENT ACTIVITY UNDERWAY & AVAILABLE CAPITAL SOURCES AT YEAR-END 2014

INCLUDES NON-STABILIZED DEVELOPMENT COMPLETIONS

18

NON-STABILIZED

DEVELOPMENT

CURRENT QUARTER

COMPLETIONS

CURENTLY IN LEASE-UP

NOT YET IN LEASE-UP

-

50

100

150

200

250

$ M

ILLIO

NS

PROJECTED STABILIZED NOI FROM $3.7 BILLION FULLY FUNDED DEVELOPMENT PIPELINE

INCLUDES NON-STABILIZED DEVELOPMENT COMPLETIONS

Source: Company reports.

(1) Represents assumed net proceeds from the Company’s September 9, 2014 forward common stock offering. Assumes physical settlement and settlement

proceeds based on $151.74 per Share. Actual physical settlement proceeds will vary based on adjustment for Fed Funds rate and dividends paid.

(2) Represents cash flow from operations, net of recurring capital expenditures and dividend payments in 2015.

$3.7 BILLION FULLY

FUNDED PIPELINE

GENERATED $13M OF

NOI IN 4Q 2014

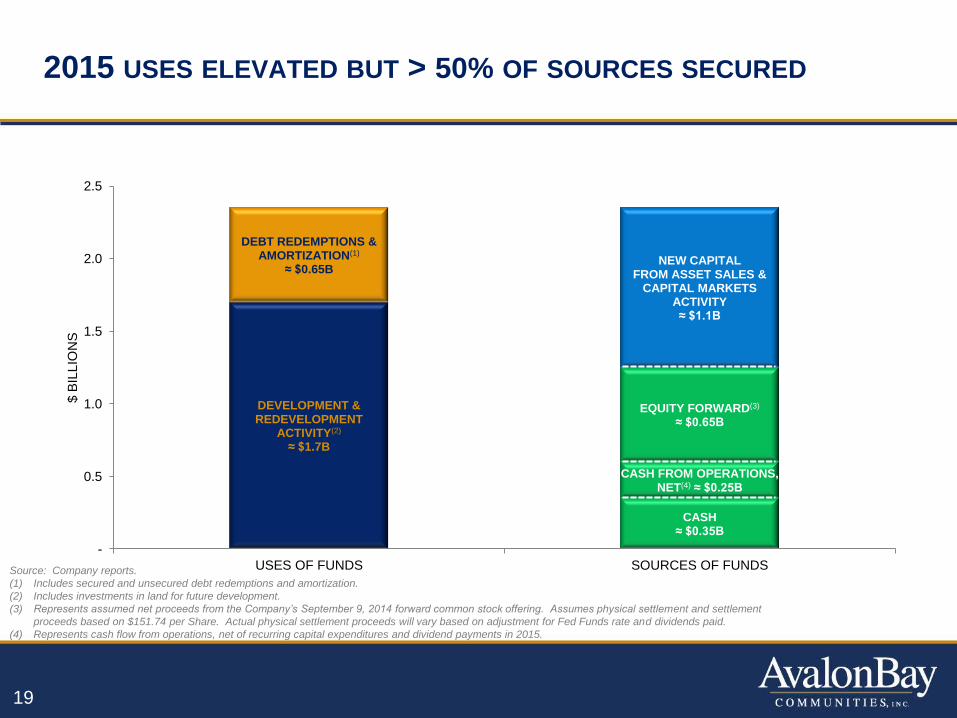

2015 USES ELEVATED BUT > 50% OF SOURCES SECURED

CASH ≈ $0.35B

CASH FROM OPERATIONS, NET(4) ≈ $0.25B

EQUITY FORWARD(3)

≈ $0.65B

NEW CAPITAL FROM ASSET SALES &

CAPITAL MARKETS ACTIVITY ≈ $1.1B

DEVELOPMENT & REDEVELOPMENT

ACTIVITY(2) ≈ $1.7B

DEBT REDEMPTIONS & AMORTIZATION(1)

≈ $0.65B

-

0.5

1.0

1.5

2.0

2.5

USES OF FUNDS SOURCES OF FUNDS

$ B

ILLIO

NS

Source: Company reports.

(1) Includes secured and unsecured debt redemptions and amortization.

(2) Includes investments in land for future development.

(3) Represents assumed net proceeds from the Company’s September 9, 2014 forward common stock offering. Assumes physical settlement and settlement

proceeds based on $151.74 per Share. Actual physical settlement proceeds will vary based on adjustment for Fed Funds rate and dividends paid.

(4) Represents cash flow from operations, net of recurring capital expenditures and dividend payments in 2015.

19

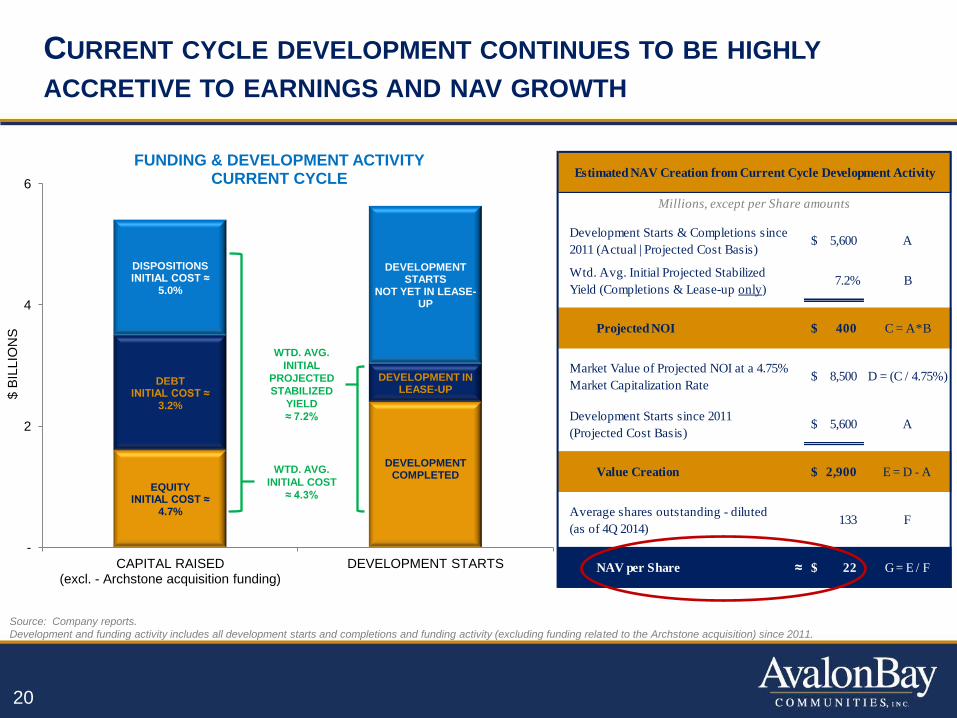

Estimated NAV Creation from Current Cycle Development Activity

Millions, except per Share amounts

Development Starts & Completions since

2011 (Actual | Projected Cost Basis)5,600$ A

Wtd. Avg. Initial Projected Stabilized

Yield (Completions & Lease-up only)7.2% B

Projected NOI 400$ C = A*B

Market Value of Projected NOI at a 4.75%

Market Capitalization Rate8,500$ D = (C / 4.75%)

Development Starts since 2011

(Projected Cost Basis)5,600$ A

Value Creation 2,900$ E = D - A

Average shares outstanding - diluted

(as of 4Q 2014)133 F

NAV per Share ≈ 22$ G = E / F

CURRENT CYCLE DEVELOPMENT CONTINUES TO BE HIGHLY

ACCRETIVE TO EARNINGS AND NAV GROWTH

EQUITY INITIAL COST ≈

4.7%

DEBT INITIAL COST ≈

3.2%

DISPOSITIONS INITIAL COST ≈

5.0%

DEVELOPMENT COMPLETED

DEVELOPMENT IN LEASE-UP

DEVELOPMENT STARTS

NOT YET IN LEASE-UP

-

2

4

6

CAPITAL RAISED (excl. - Archstone acquisition funding)

DEVELOPMENT STARTS

$ B

ILLIO

NS

FUNDING & DEVELOPMENT ACTIVITY CURRENT CYCLE

Source: Company reports.

Development and funding activity includes all development starts and completions and funding activity (excluding funding related to the Archstone acquisition) since 2011.

20

WTD. AVG.

INITIAL COST

≈ 4.3%

WTD. AVG.

INITIAL

PROJECTED

STABILIZED

YIELD

≈ 7.2%

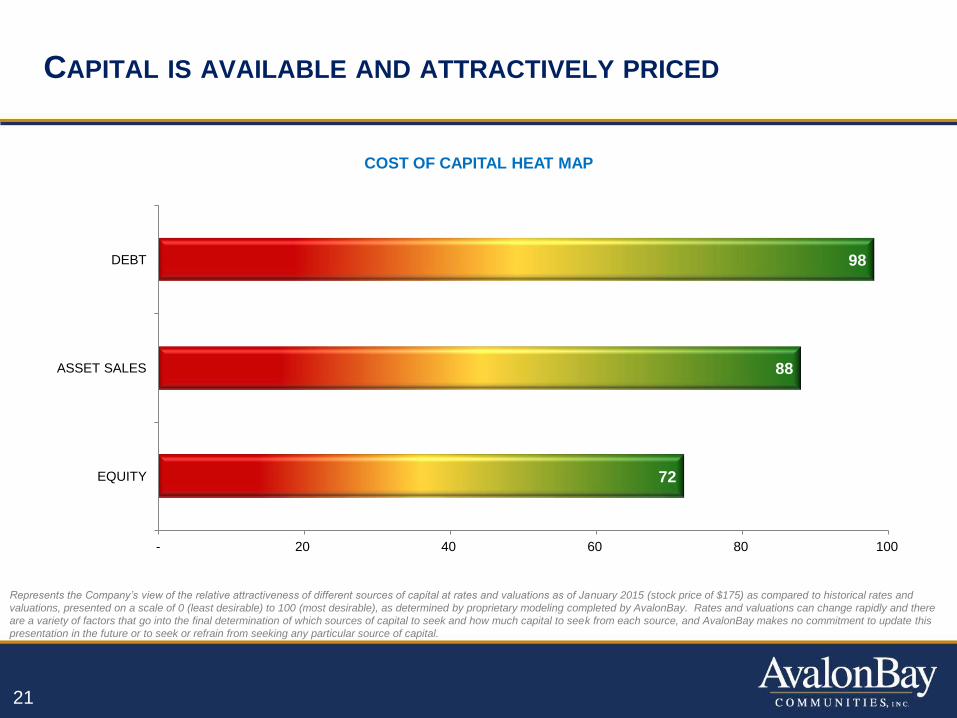

CAPITAL IS AVAILABLE AND ATTRACTIVELY PRICED

Represents the Company’s view of the relative attractiveness of different sources of capital at rates and valuations as of January 2015 (stock price of $175) as compared to historical rates and

valuations, presented on a scale of 0 (least desirable) to 100 (most desirable), as determined by proprietary modeling completed by AvalonBay. Rates and valuations can change rapidly and there

are a variety of factors that go into the final determination of which sources of capital to seek and how much capital to seek from each source, and AvalonBay makes no commitment to update this

presentation in the future or to seek or refrain from seeking any particular source of capital.

72

88

98

- 20 40 60 80 100

EQUITY

ASSET SALES

DEBT

COST OF CAPITAL HEAT MAP

21

22

FORWARD-LOOKING STATEMENTS

This presentation and the related Management Letter dated January 29, 2015 contain

forward-looking statements, which are indicated by the use of words such as “expects,”

“projects,” “forecast,” “outlook,” “estimate” and other words that do not relate to historical

matters. Actual results may differ materially. For information concerning risks and other

factors that could cause such differences, see “Forward Looking Statements” in AvalonBay’s

earnings release dated January 28, 2015. For definitions and additional information

concerning certain defined terms and non-GAAP financial information included in this

presentation, see Attachment 20 to the earnings release.

This presentation and the related Management Letter are provided in connection with

AvalonBay’s fourth quarter 2014 earnings conference call on January 29, 2015. This

presentation and the Management Letter are intended to accompany the earnings release,

and should be read in conjunction with the earnings release. AvalonBay does not intend to

update any of these documents, which speak only as of their respective dates.

The earnings release is available on AvalonBay’s website at www.avalonbay.com

23

ADDITIONAL DEFINITIONS & RECONCILIATIONS OF NON-GAAP

FINANCIAL MEASURES AND OTHER TERMS

Total Enterprise Value represents the aggregate of the market value of the

Company’s common stock, the market value of the Company’s operating partnership

units outstanding (based on the market value of the Company’s common stock) and

the outstanding principal balance of the Company’s debt. Total Enterprise Value is

subject to change depending on market prices, which may be volatile.

24