investor day 2016 presentation

TRANSCRIPT

The world's leading premium schools organization

Nord Anglia Education

1

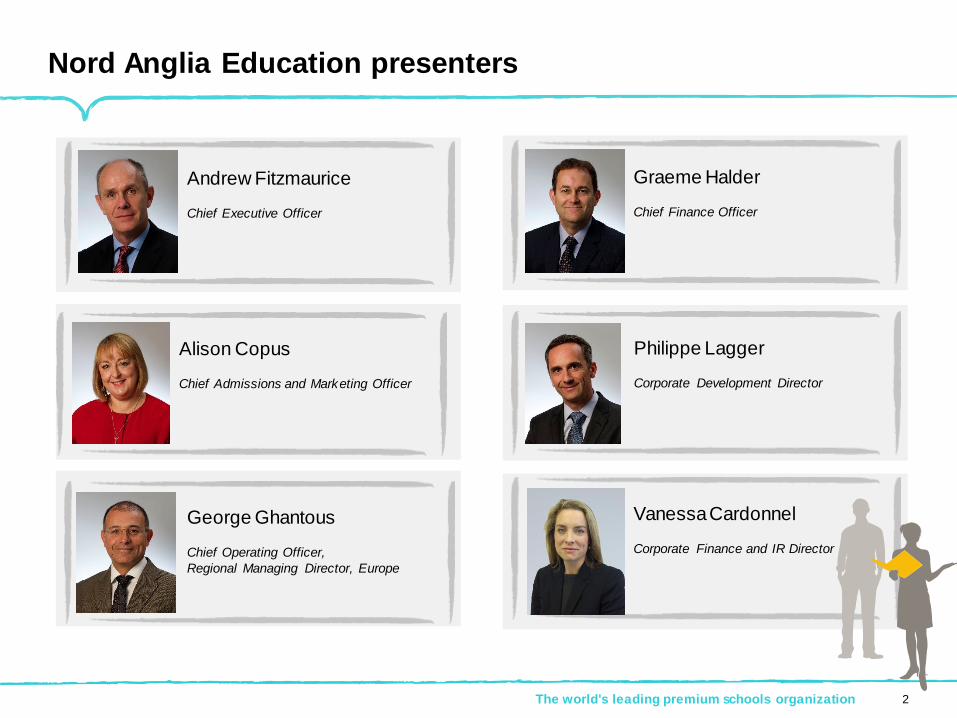

Nord Anglia Education presenters

Andrew Fitzmaurice

Chief Executive Officer

Graeme Halder

Chief Finance Officer

Philippe Lagger

Corporate Development Director

Alison Copus

Chief Admissions and Marketing Officer

George Ghantous

Chief Operating Officer,

Regional Managing Director, Europe

Vanessa Cardonnel

Corporate Finance and IR Director

The world's leading premium schools organization 2

The world's leading premium schools organization 3

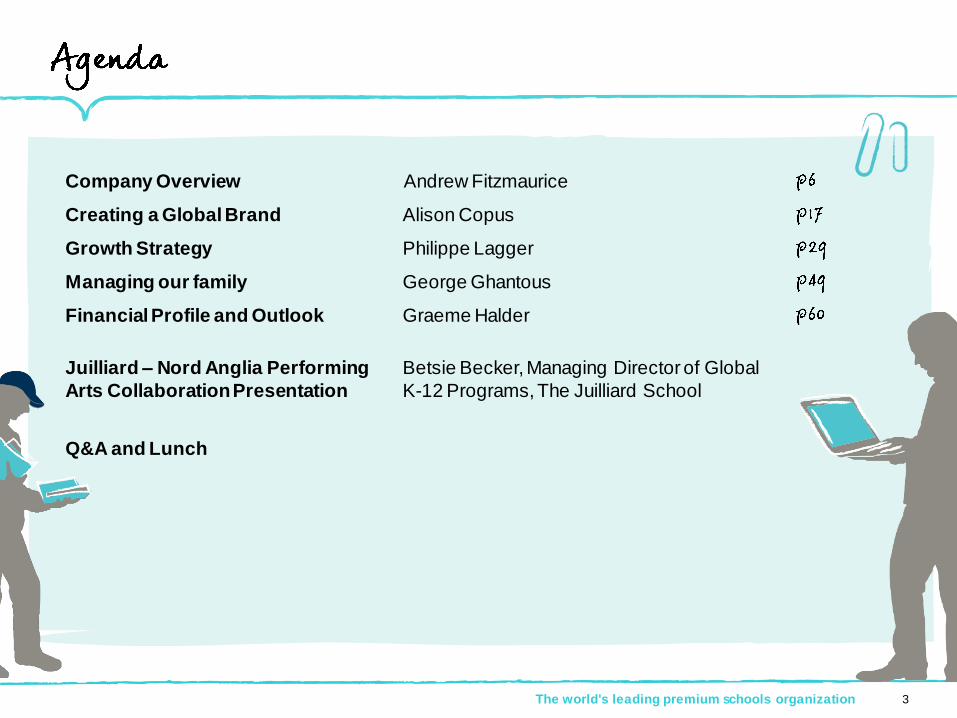

Company Overview Andrew Fitzmaurice

Creating a Global Brand Alison Copus

Growth Strategy Philippe Lagger

Managing our family George Ghantous

Financial Profile and Outlook Graeme Halder

Juilliard – Nord Anglia Performing

Arts Collaboration Presentation

Betsie Becker, Managing Director of Global

K-12 Programs, The Juilliard School

Q&A and Lunch

Neither Nord Anglia Education, Inc. (NYSE: NORD) nor any of its subsidiaries or affiliates

is making any representation or warranty, expressed or implied, as to the accuracy or

completeness of the attached materials.

Please note that the attached materials and our oral explanations of the attached materials

may constitute forward-looking statements within the meaning of applicable U.S. securities

laws and such forward-looking statements are made based on our current

expectations. Forward-looking statements relate to events involving certain risks and

uncertainties, and actual results may differ materially from the views expressed.

A number of potential risks and uncertainties are outlined in our public filings with the

Securities and Exchange Commission. Nord Anglia Education, Inc. does not undertake

any obligation to update any forward-looking statement, except as required under

applicable law. You are cautioned not to place undue reliance on any forward-looking

statements.

Disclaimer

The world's leading premium schools organization 4

5

Our brand

The world's leading premium schools organization

Company

6

Acknowledged

as the

ONE GOAL

schools

organization

The world's leading premium schools organization 7

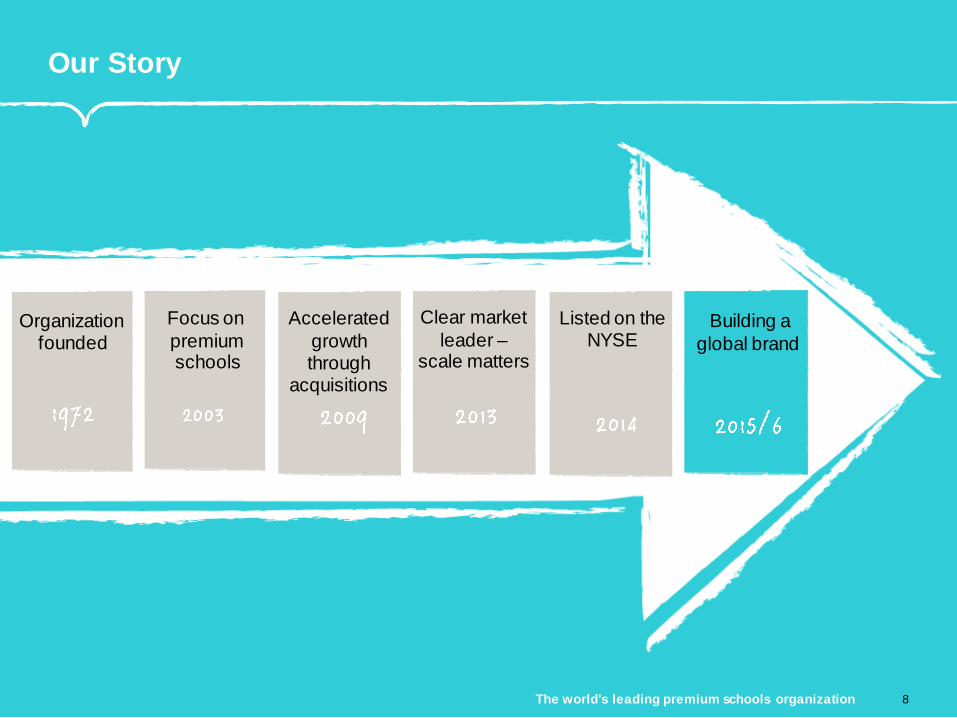

Our Story

Organization founded

Focus on

premium schools

Accelerated

growth through

acquisitions

Listed on the NYSE

Building a

global brand

Clear market

leader –scale matters

The world's leading premium schools organization 8

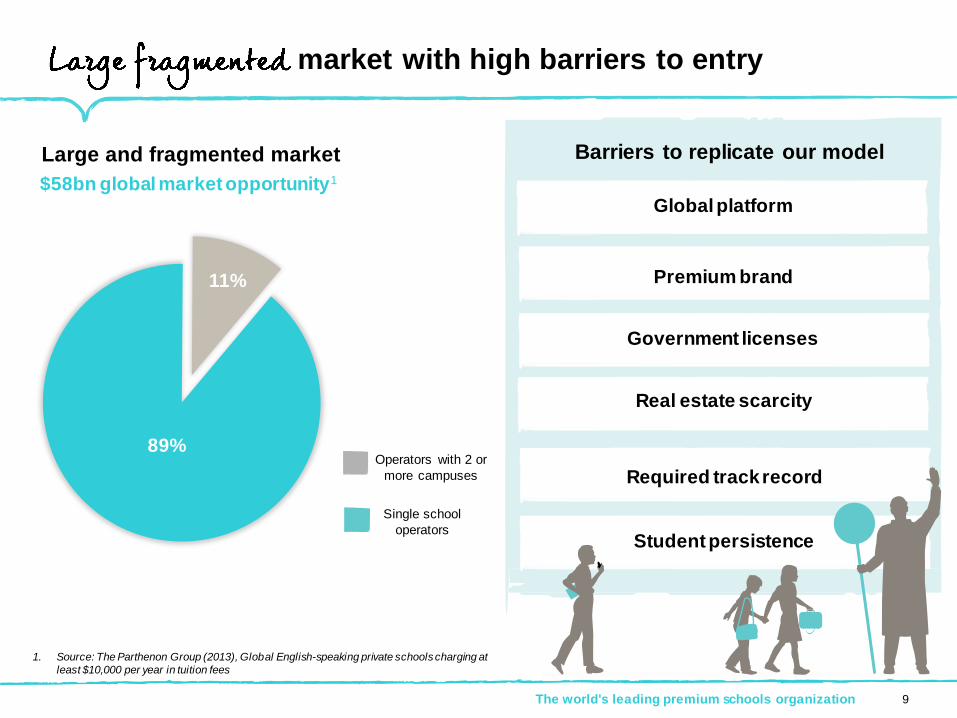

market with high barriers to entry

Large and fragmented market

Single school

operators

Operators with 2 or

more campuses

$58bn global market opportunity1

1. Source: The Parthenon Group (2013), Global English-speaking private schools charging at

least $10,000 per year in tuition fees

Global platform

Barriers to replicate our model

Premium brand

Real estate scarcity

Government licenses

Required track record

Student persistence

11%

89%

The world's leading premium schools organization 9

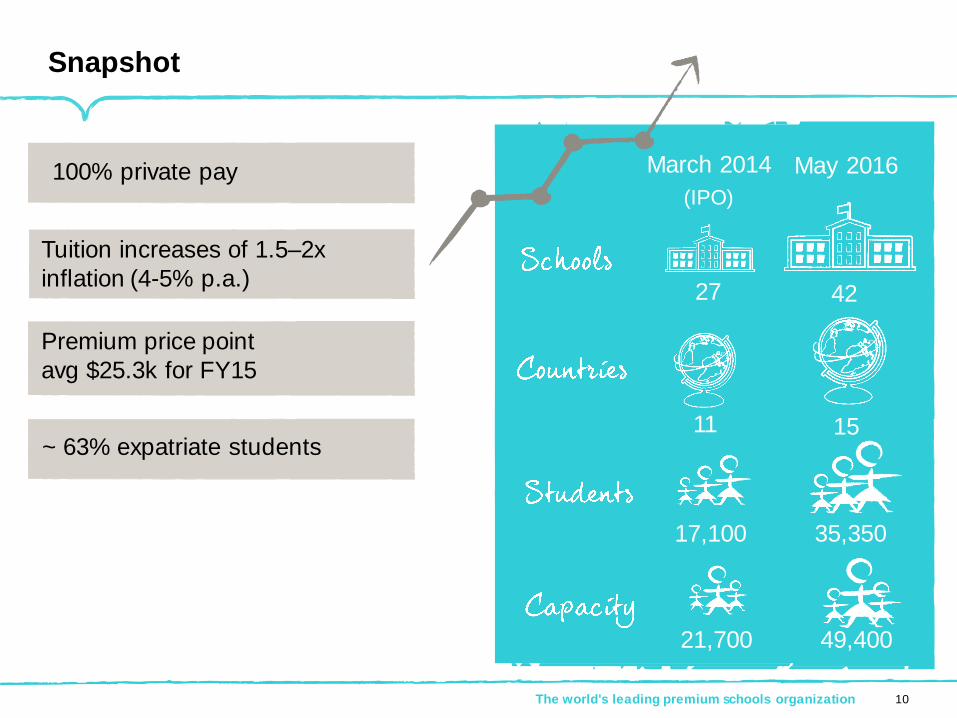

Snapshot

March 2014

(IPO)

11

May 2016

15

4227

17,100

21,700

35,350

49,400

The world's leading premium schools organization 10

100% private pay

Tuition increases of 1.5–2x

inflation (4-5% p.a.)

Premium price point

avg $25.3k for FY15

~ 63% expatriate students

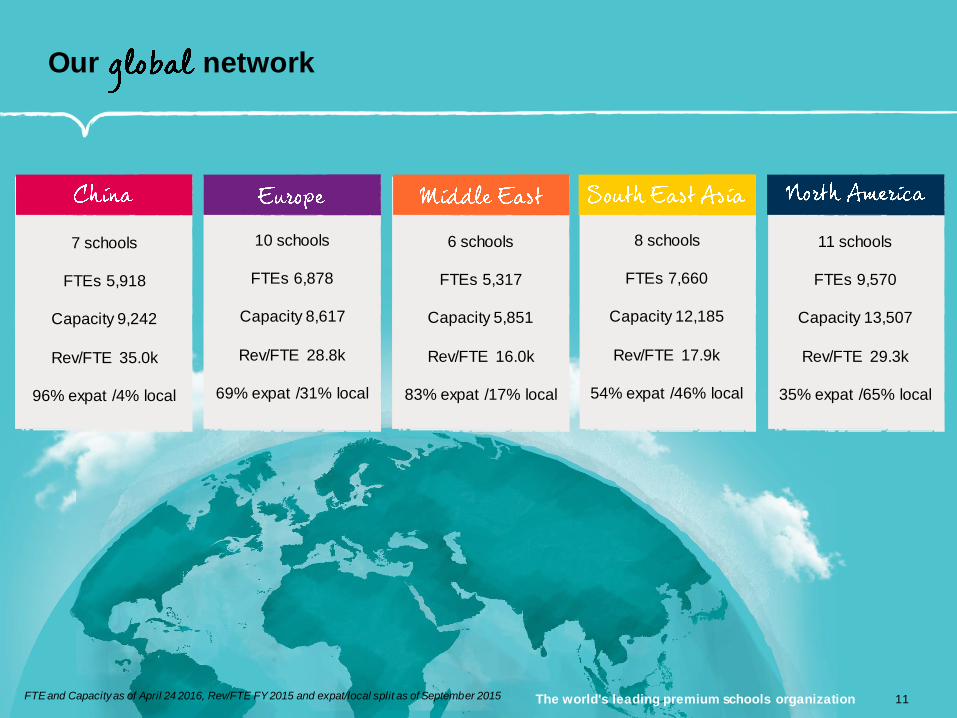

Our network

7 schools

FTEs 5,918

Capacity 9,242

Rev/FTE 35.0k

96% expat /4% local

10 schools

FTEs 6,878

Capacity 8,617

Rev/FTE 28.8k

69% expat /31% local

6 schools

FTEs 5,317

Capacity 5,851

Rev/FTE 16.0k

83% expat /17% local

8 schools

FTEs 7,660

Capacity 12,185

Rev/FTE 17.9k

54% expat /46% local

11 schools

FTEs 9,570

Capacity 13,507

Rev/FTE 29.3k

35% expat /65% local

FTE and Capacity as of April 24 2016, Rev/FTE FY 2015 and expat/local split as of September 2015 The world's leading premium schools organization 11

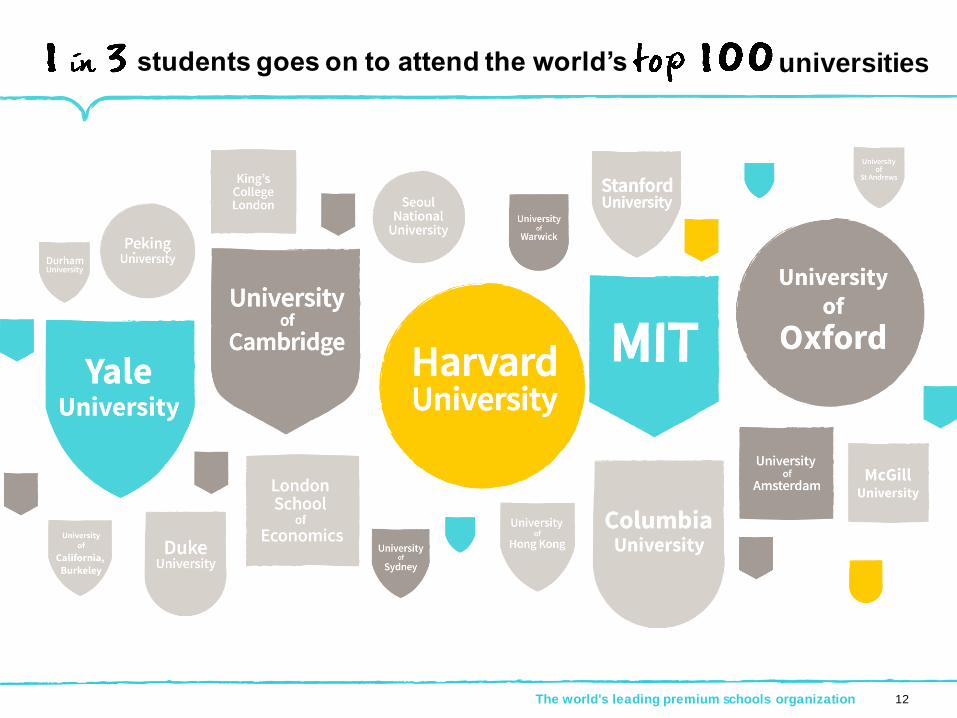

students goes on to attend the world’s universities

The world's leading premium schools organization 12

The world's leading premium schools organization 13

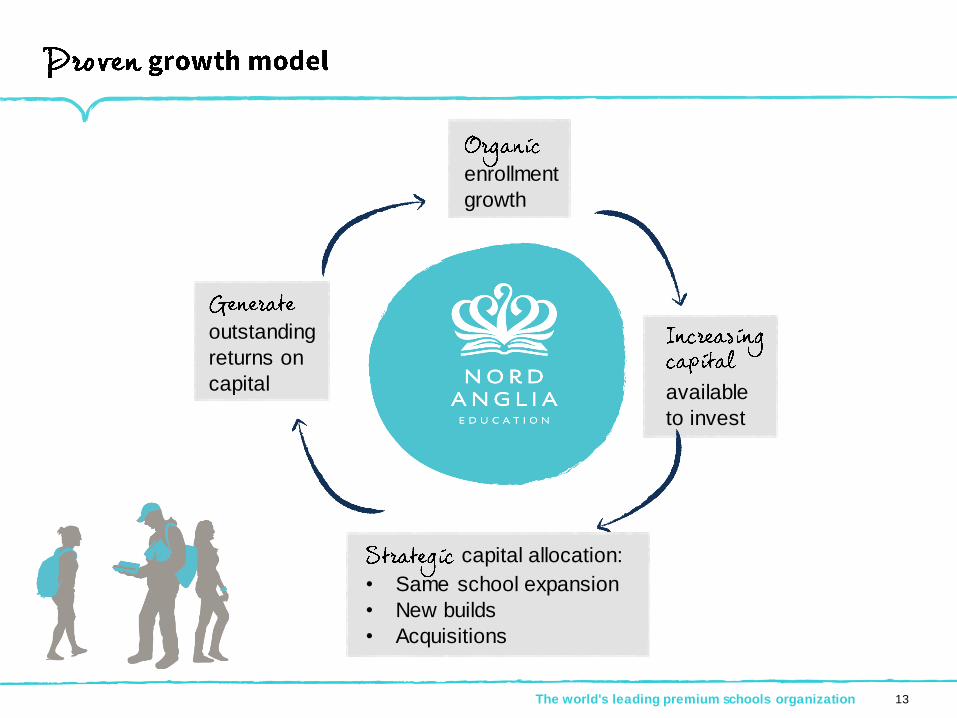

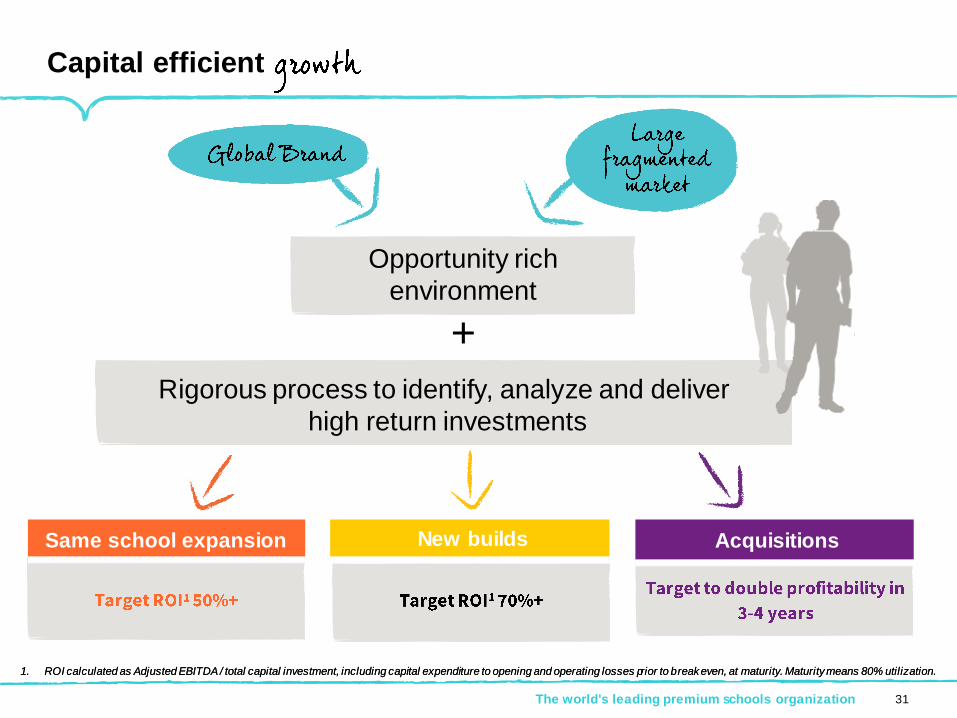

capital allocation:

• Same school expansion

• New builds

• Acquisitions

outstanding

returns on

capital available

to invest

enrollment

growth

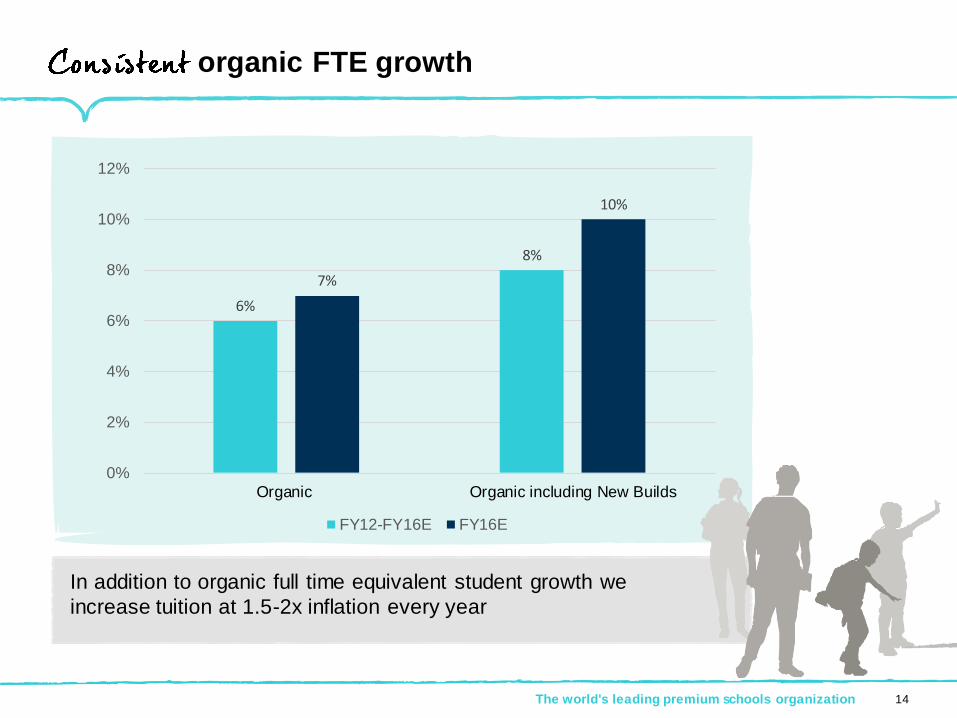

organic FTE growth

The world's leading premium schools organization 14

6%

8%

7%

10%

0%

2%

4%

6%

8%

10%

12%

Organic Organic including New Builds

FY12-FY16E FY16E

In addition to organic full time equivalent student growth we

increase tuition at 1.5-2x inflation every year

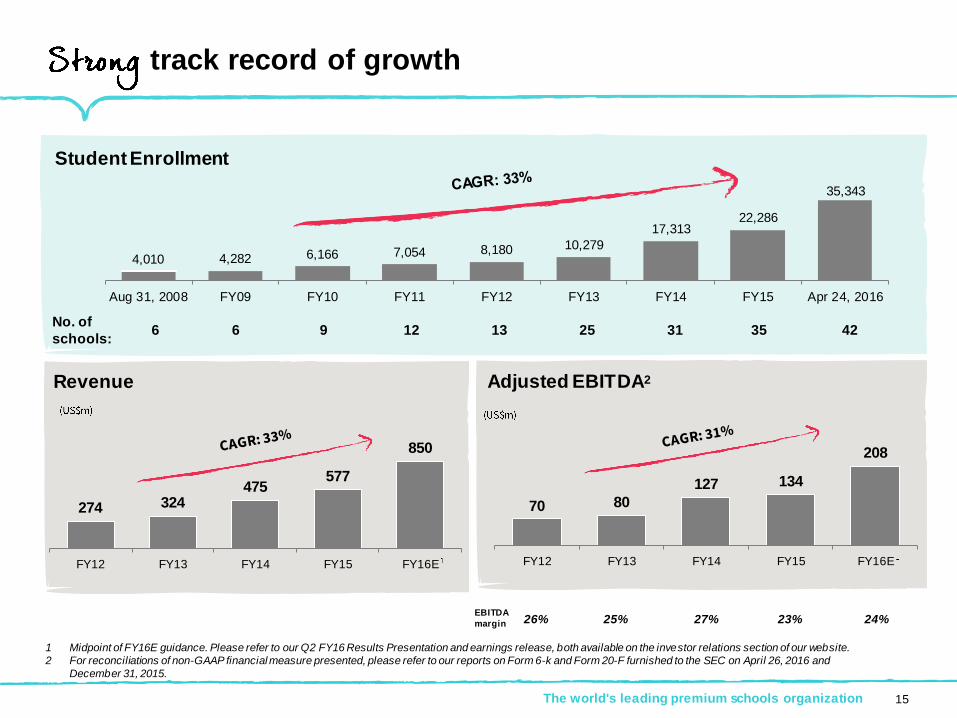

35,343

4,010 4,282 6,166 7,054 8,180 10,279

17,31322,286

Aug 31, 2008 FY09 FY10 FY11 FY12 FY13 FY14 FY15 Apr 24, 2016

No. of

schools:6 6 9 12 13 25 31 35 42

274 324 475

577

850

FY12 FY13 FY14 FY15 FY16E

70 80

127 134

208

FY12 FY13 FY14 FY15 FY16E

EBITDA

margin 26% 25% 27% 23% 24%

1 Midpoint of FY16E guidance. Please refer to our Q2 FY16 Results Presentation and earnings release, both available on the investor relations section of our website.

2 For reconciliations of non-GAAP financial measure presented, please refer to our reports on Form 6-k and Form 20-F furnished to the SEC on April 26, 2016 and

December 31, 2015.

Student Enrollment

track record of growth

Revenue Adjusted EBITDA2

The world's leading premium schools organization 15

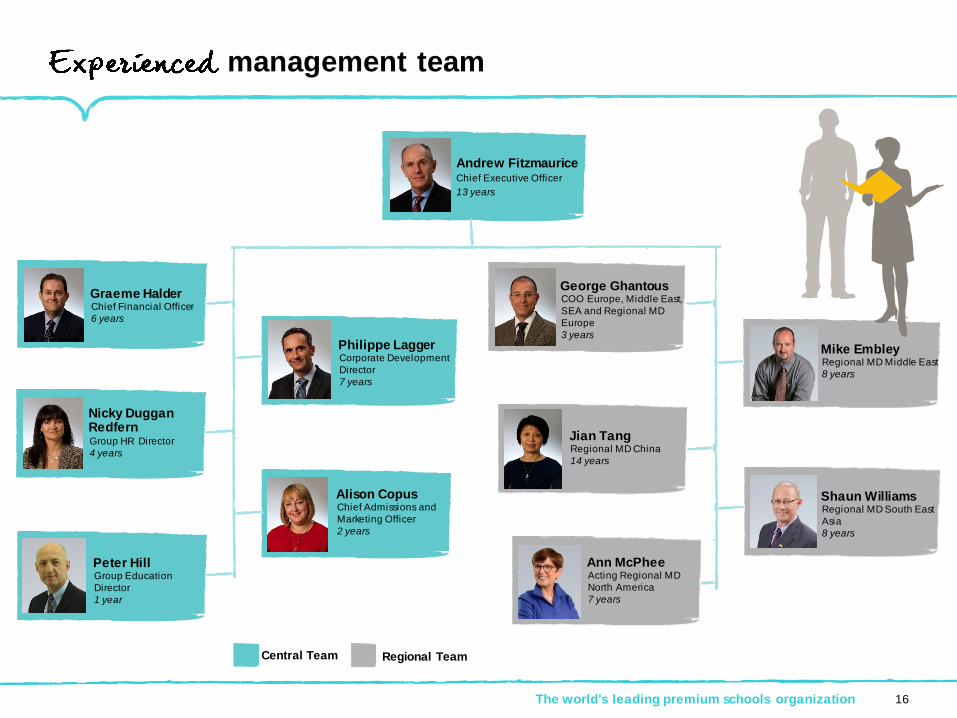

management team

Andrew FitzmauriceChief Executive Officer

13 years

Graeme HalderChief Financial Officer

6 years

Philippe LaggerCorporate Development

Director

7 years

Nicky Duggan RedfernGroup HR Director

4 years

Alison CopusChief Admissions and

Marketing Officer

2 years

George GhantousCOO Europe, Middle East,

SEA and Regional MD

Europe

3 years

Jian TangRegional MD China

14 years

Shaun WilliamsRegional MD South East

Asia

8 years

Mike EmbleyRegional MD Middle East

8 years

Ann McPheeActing Regional MD

North America

7 years

Central Team Regional Team

The world's leading premium schools organization 16

Peter HillGroup Education

Director

1 year

The world's leading premium schools organization

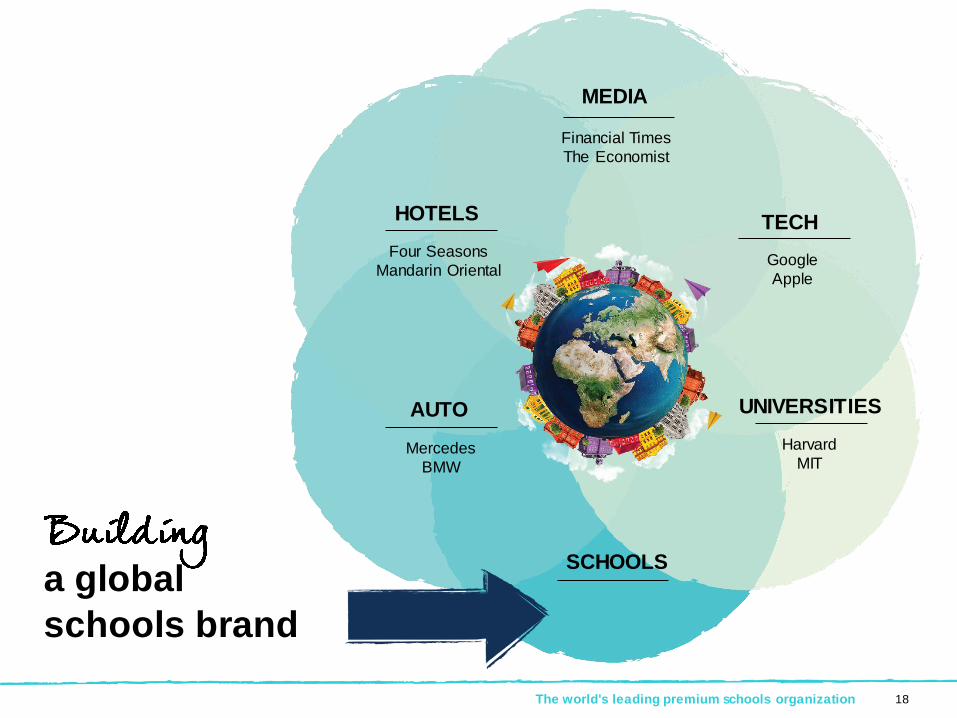

Building a

17

a global

schools brand

AUTO

HOTELS

MEDIA

TECH

UNIVERSITIES

SCHOOLS

Mercedes

BMW

Four Seasons

Mandarin Oriental

Financial Times

The Economist

Apple

Harvard

MIT

The world's leading premium schools organization 18

Leveraging our to set us apart

The world's leading premium schools organization 19

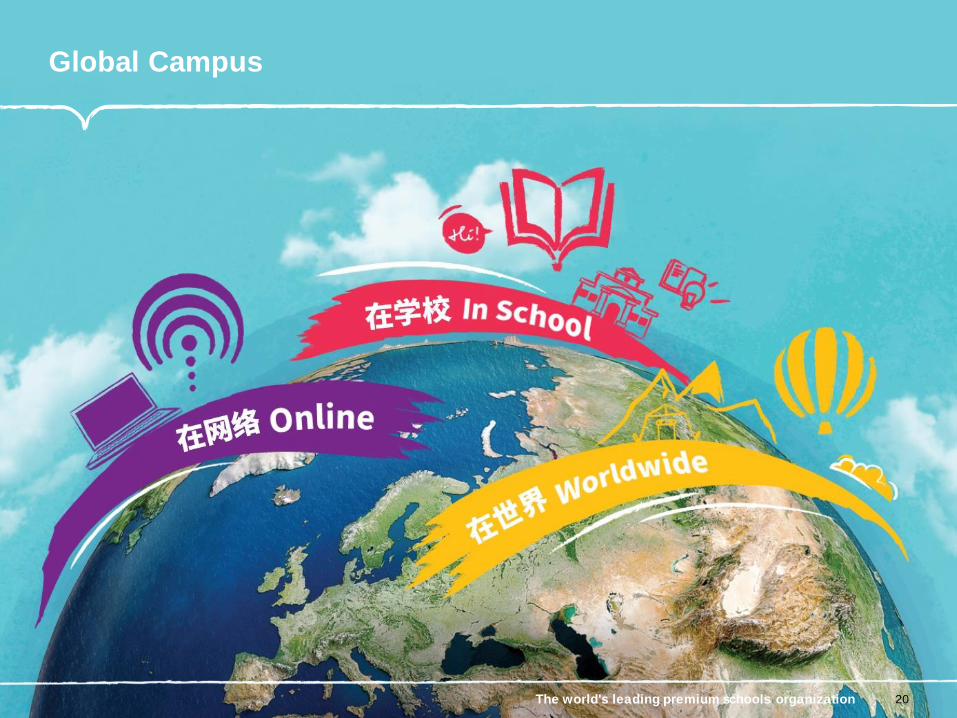

Students Faculty Schools

Global Campus

The world's leading premium schools organization 20

The world's leading premium schools organization

Global Campus: Unique global experiences

We believe learning should not be

confined to the classroom

Expedition Programs

Tanzania Les Martinets

Summer Programs Summer Performing Arts with

Juilliard Nord Anglia Summer Leadership

Academy at Balliol College, Oxford

Global Experiences

Cambridge Science Festival Global Orchestra Global Games

21

Citizenship expedition film -

22

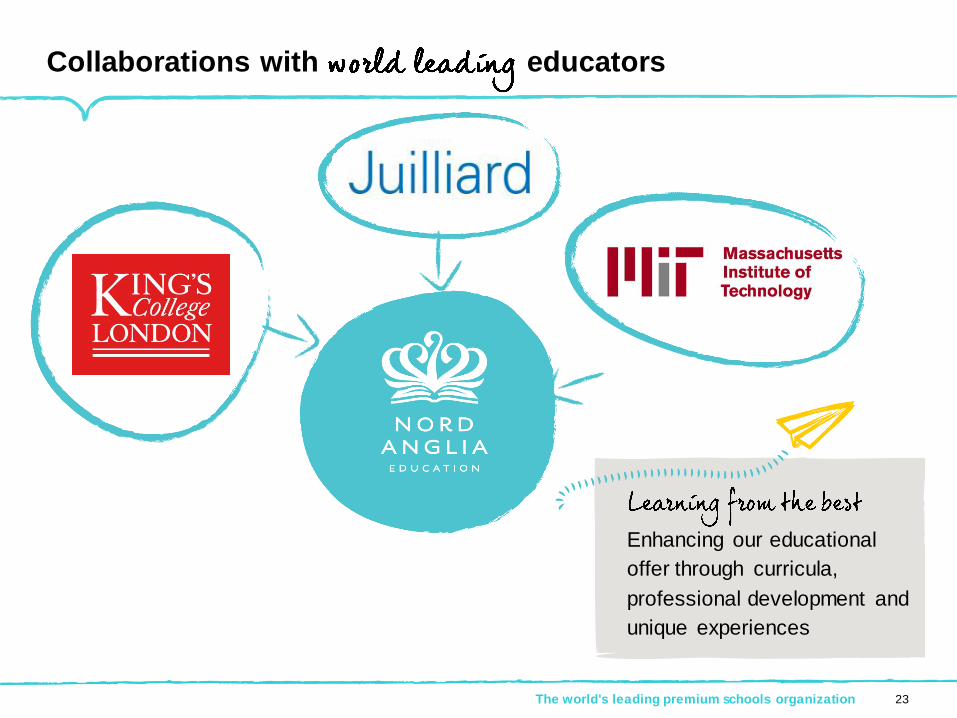

Collaborations with educators

The world's leading premium schools organization 23

Enhancing our educational

offer through curricula,

professional development and

unique experiences

24

Our collaboration film

25The world's leading premium schools organization

High quality teachers are the

most important factor when

choosing a school

, and highest quality faculty

The world's leading premium schools organization 26

Making our schools

FIRSTchoice for families

27

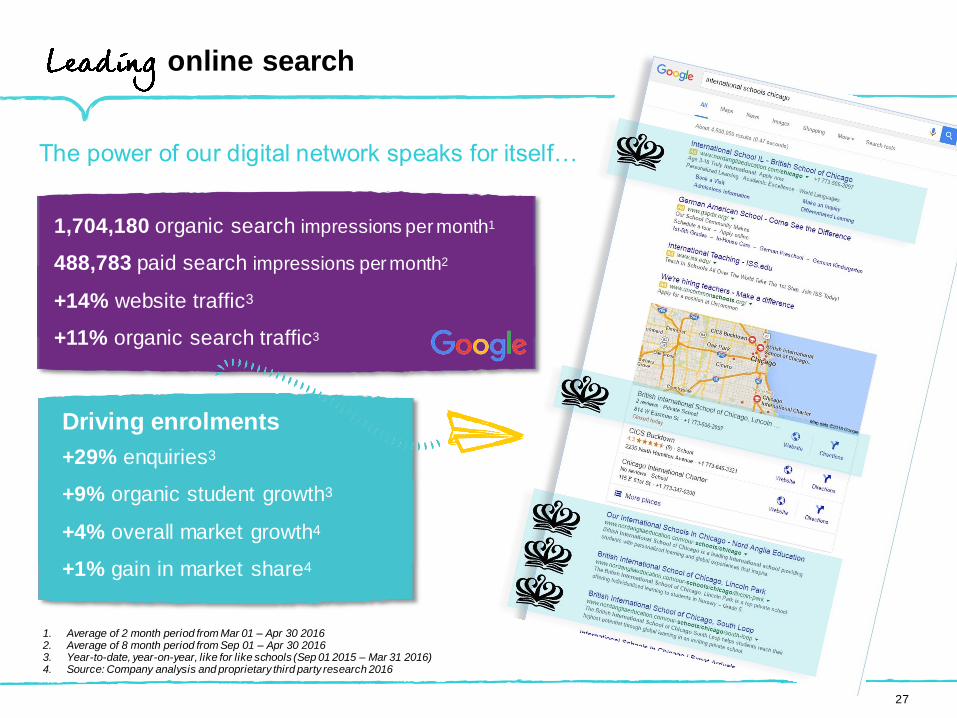

+29% enquiries3

+9% organic student growth3

+4% overall market growth4

+1% gain in market share4

online search

The power of our digital network speaks for itself…

1,704,180 organic search impressions per month1

488,783 paid search impressions per month2

+14% website traffic3

+11% organic search traffic3

1. Average of 2 month period from Mar 01 – Apr 30 20162. Average of 8 month period from Sep 01 – Apr 30 20163. Year-to-date, year-on-year, like for like schools (Sep 01 2015 – Mar 31 2016) 4. Source: Company analysis and proprietary third party research 2016

Driving enrolments

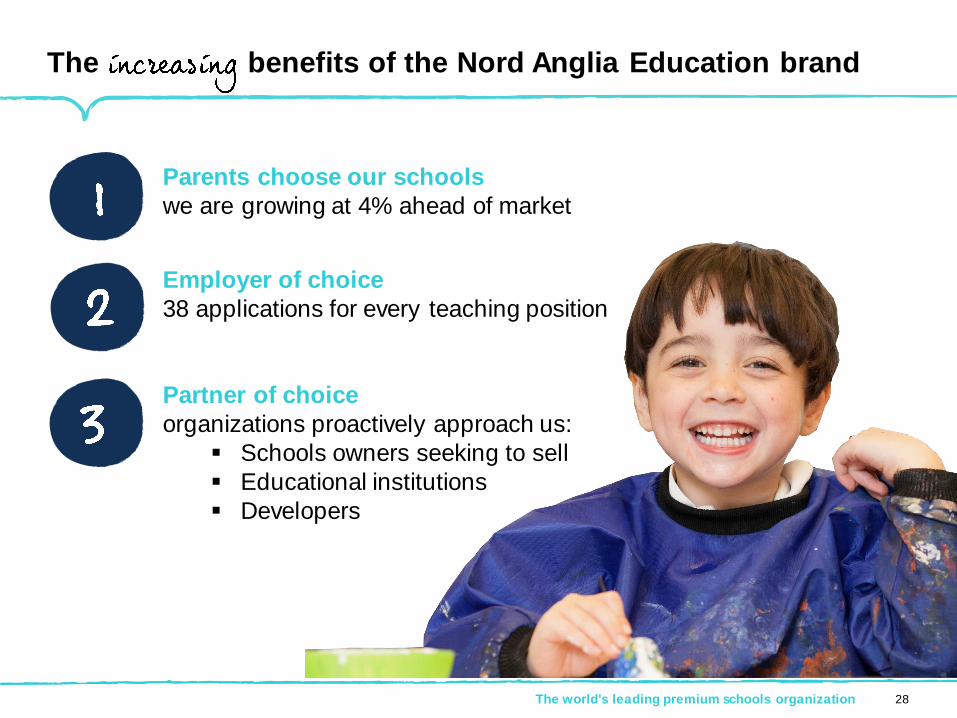

The benefits of the Nord Anglia Education brand

The world's leading premium schools organization 28

Parents choose our schools

we are growing at 4% ahead of market

Employer of choice

38 applications for every teaching position

Partner of choice

organizations proactively approach us:

Schools owners seeking to sell

Educational institutions

Developers

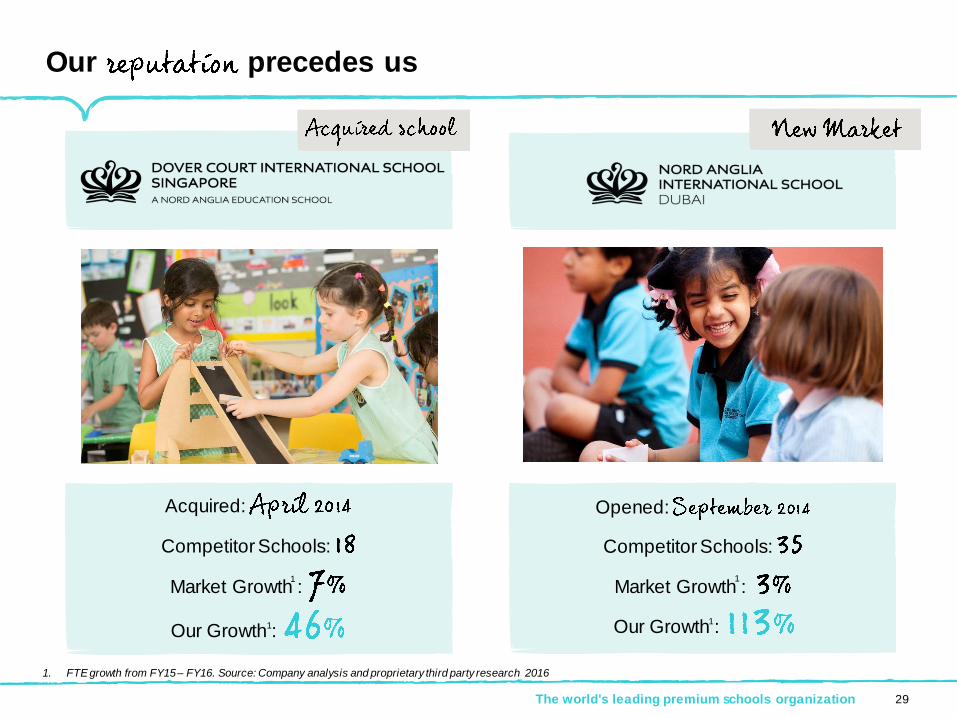

Our precedes us

29The world's leading premium schools organization

Competitor Schools:

Market Growth :

Our Growth :

Competitor Schools:

Market Growth :

Our Growth :

1. FTE growth from FY15 – FY16. Source: Company analysis and proprietary third party research 2016

1

1 1

1

Acquired: Opened:

The world's leading premium schools organization

Strategy30

Capital efficient

The world's leading premium schools organization 31

1. ROI calculated as Adjusted EBITDA / total capital investment, including capital expenditure to opening and operating losses prior to break even, at maturity. Maturity means 80% utilization.

Same school expansion New builds Acquisitions

1. ROI calculated as Adjusted EBITDA / total capital investment, including capital expenditure to opening and operating losses prior to break even, at maturity. Maturity means 80% utilization.

Opportunity rich

environment

+

Rigorous process to identify, analyze and deliver

high return investments

The world's leading premium schools organization 32

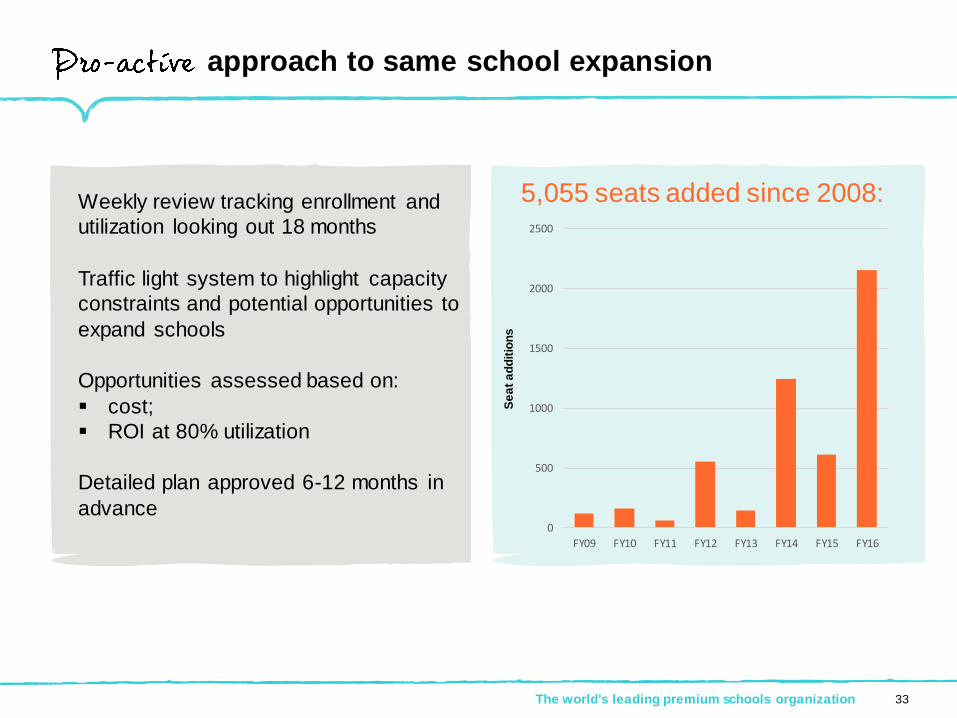

expansion

Building capacity onto existing schools

Improve facilities

Predictable enrollment and margin

improvement

Typically developer/landlord funded

Lowest risk

Target ROI 50%+

5,055 seats added since 2008

0

500

1000

1500

2000

2500

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

approach to same school expansion

The world's leading premium schools organization 33

Weekly review tracking enrollment and

utilization looking out 18 months

Traffic light system to highlight capacity

constraints and potential opportunities to

expand schools

Opportunities assessed based on:

cost;

ROI at 80% utilization

Detailed plan approved 6-12 months in

advanceS

ea

t a

dd

itio

ns

5,055 seats added since 2008:

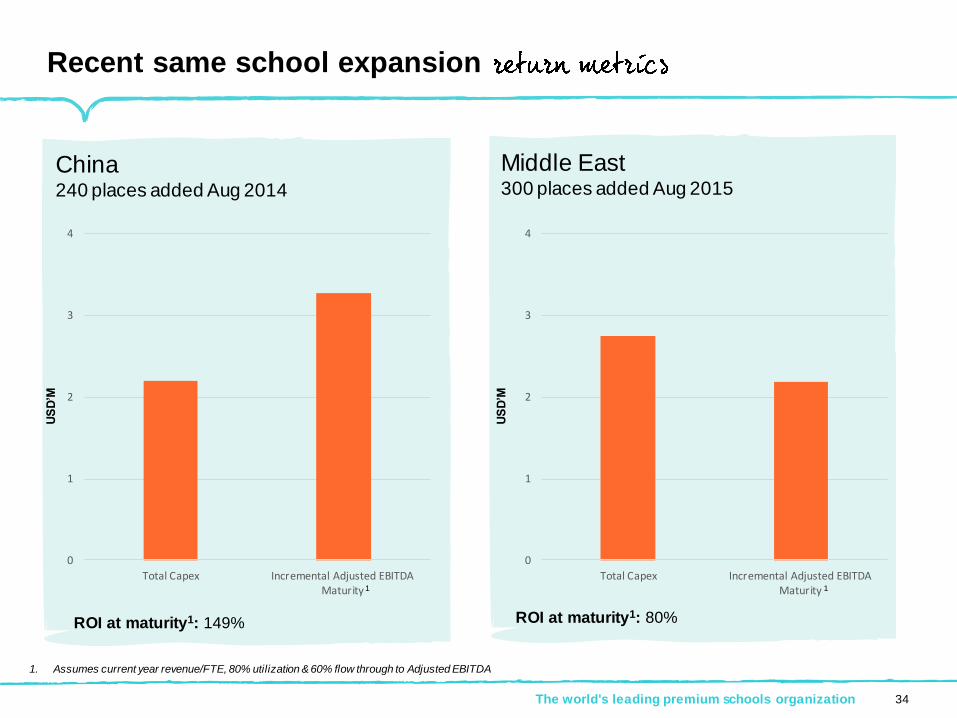

Recent same school expansion

China240 places added Aug 2014

US

D’M

Middle East 300 places added Aug 2015

ROI at maturity1: 80%ROI at maturity1: 149%

US

D’M

1. Assumes current year revenue/FTE, 80% utilization & 60% flow through to Adjusted EBITDA

The world's leading premium schools organization 34

1 1

0

1

2

3

4

Total Capex Incremental Adjusted EBITDAMaturity

0

1

2

3

4

Total Capex Incremental Adjusted EBITDAMaturity

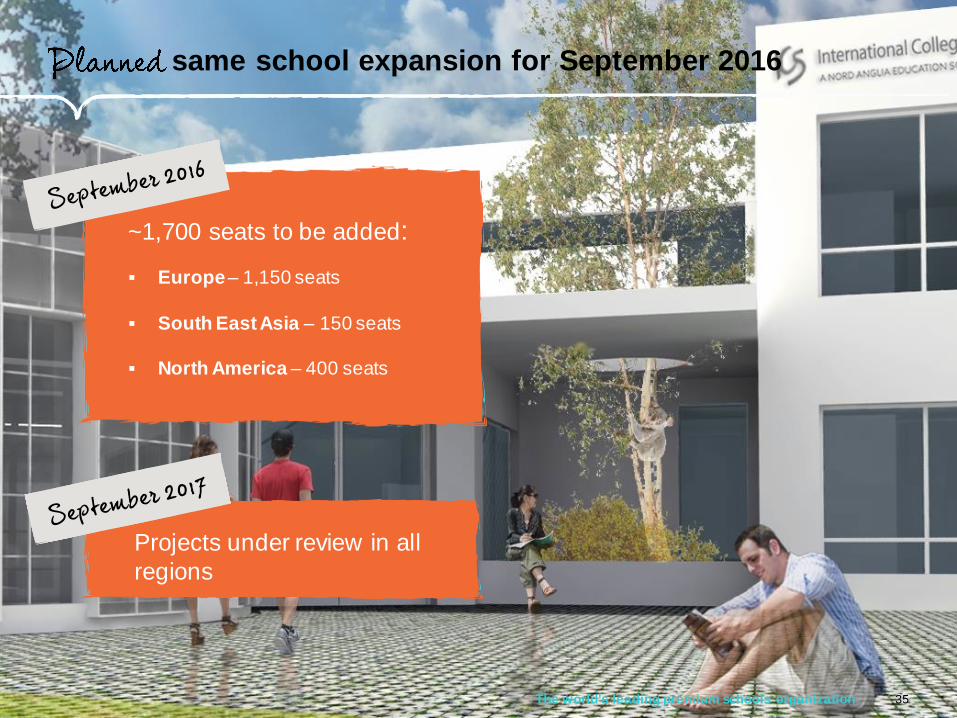

same school expansion for September 2016

The world's leading premium schools organization 35

~1,700 seats to be added:

Europe– 1,150 seats

South East Asia – 150 seats

North America – 400 seats

Projects under review in all

regions

Same school expansion film -

36

The world's leading premium schools organization

builds

37

Typically developer funded

Nord Anglia Education reputation for

quality

Adjacent property value enhanced

6 new schools opened since 2008:

Abu Dhabi, Beijing, Dubai, Aubonne, Hong Kong, Chicago

2 new schools opening Sept 2016:Shanghai, Houston

2 new schools opening Sept 2017:Abu Dhabi, Bangkok

Target ROI 70%+

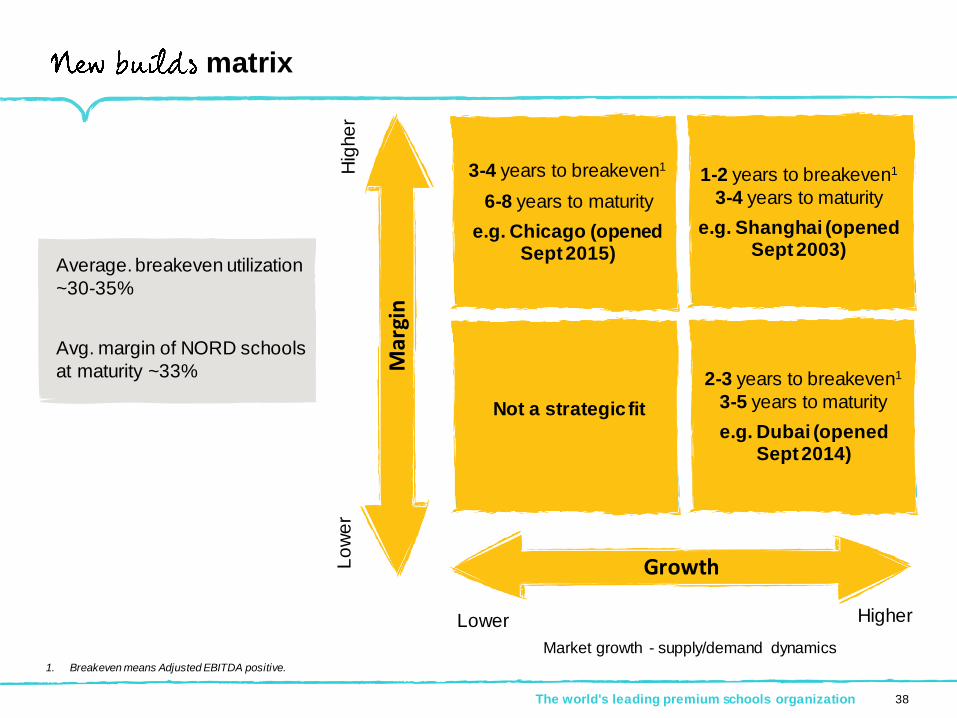

matrix

Lower Higher

Hig

he

rL

ow

er

Market growth - supply/demand dynamics1. Breakeven means Adjusted EBITDA positive.

The world's leading premium schools organization 38

3-4 years to breakeven1

6-8 years to maturity

e.g. Chicago (opened Sept 2015)

1-2 years to breakeven1

3-4 years to maturity

e.g. Shanghai (opened Sept 2003)

Not a strategic fit

2-3 years to breakeven1

3-5 years to maturity

e.g. Dubai (opened Sept 2014)

Growth

Margin

Average. breakeven utilization

~30-35%

Avg. margin of NORD schools

at maturity ~33%

Recent new build examples -

The world's leading premium schools organization

Nord Anglia International School Dubai

1

1,500 seat school opened in September 2014

Initial investment of ~$7.7m

Fast growth market with expected adjusted EBITDA margin around company average at maturity

Breakeven year 2/maturity year 3

ROI 55% at maturity

Ad

jus

ted

EB

ITD

A

US

D’M

Ave

rag

e F

TE

’s

39

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

0

200

400

600

800

1000

1200

1400

1600

Year 1 FY15 Year 2 FY16E Year 3 FY17F

Enrolment Adjusted EBITDA

Ave

rag

e F

TE

’sRecent new build examples –

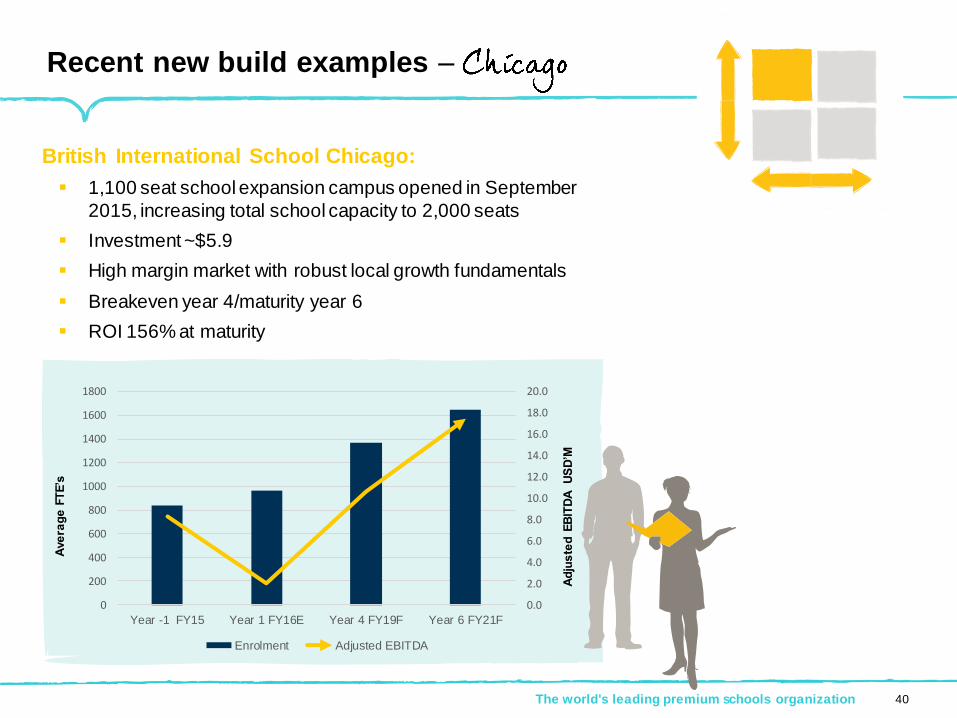

The world's leading premium schools organization

British International School Chicago:

1,100 seat school expansion campus opened in September

2015, increasing total school capacity to 2,000 seats

Investment ~$5.9

High margin market with robust local growth fundamentals

Breakeven year 4/maturity year 6

ROI 156% at maturity

40

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

0

200

400

600

800

1000

1200

1400

1600

1800

Year -1 FY15 Year 1 FY16E Year 4 FY19F Year 6 FY21F

Enrolment Adjusted EBITDA

Ad

jus

ted

EB

ITD

A

US

D’M

Ave

rag

e F

TE

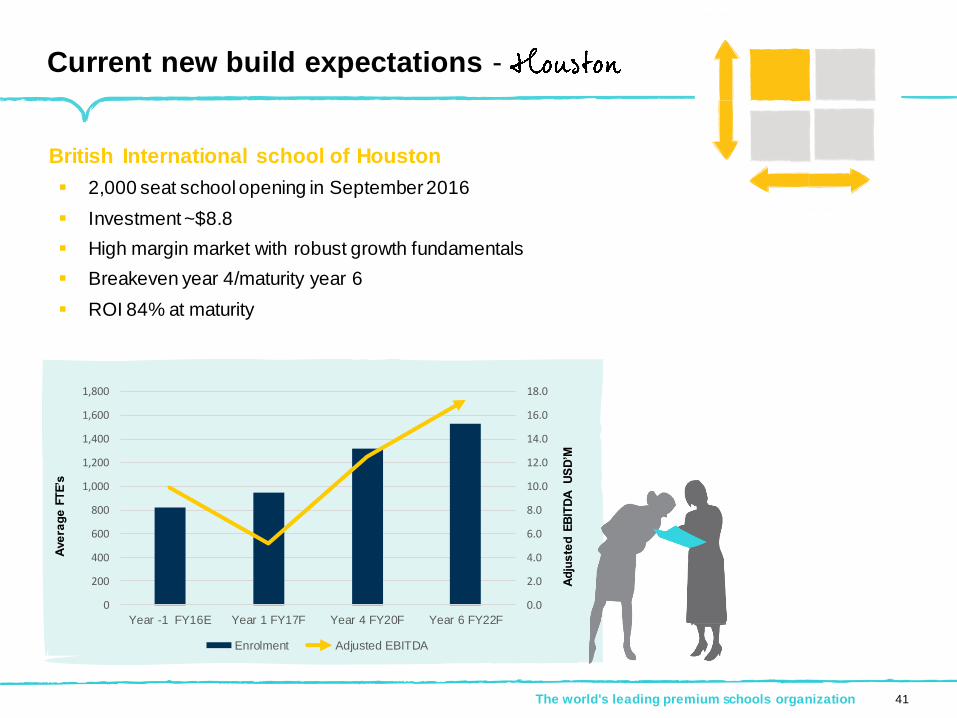

’sCurrent new build expectations -

The world's leading premium schools organization

British International school of Houston

2,000 seat school opening in September 2016

Investment ~$8.8

High margin market with robust growth fundamentals

Breakeven year 4/maturity year 6

ROI 84% at maturity

41

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Year -1 FY16E Year 1 FY17F Year 4 FY20F Year 6 FY22F

Enrolment Adjusted EBITDA

Ad

jus

ted

EB

ITD

A

US

D’M

Ave

rag

e F

TE

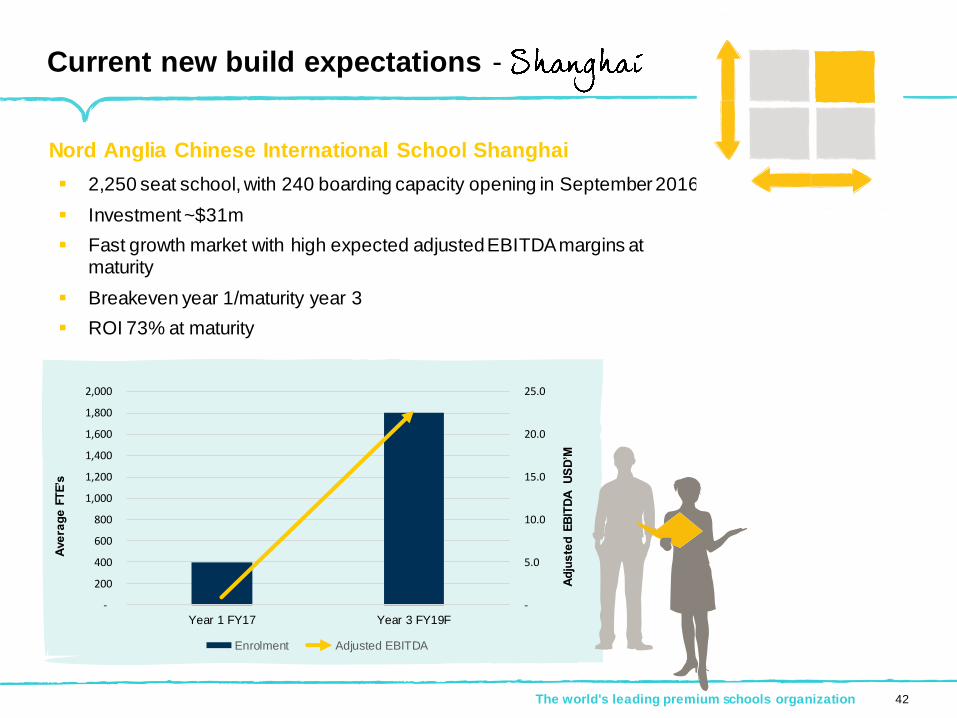

’sCurrent new build expectations -

The world's leading premium schools organization

Nord Anglia Chinese International School Shanghai

2,250 seat school, with 240 boarding capacity opening in September 2016

Investment ~$31m

Fast growth market with high expected adjusted EBITDA margins at maturity

Breakeven year 1/maturity year 3

ROI 73% at maturity

42

-

5.0

10.0

15.0

20.0

25.0

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Year 1 FY17 Year 3 FY19F

Enrolment Adjusted EBITDA

Ad

jus

ted

EB

ITD

A

US

D’M

New build film –

43

The world's leading premium schools organization

Combine with 47

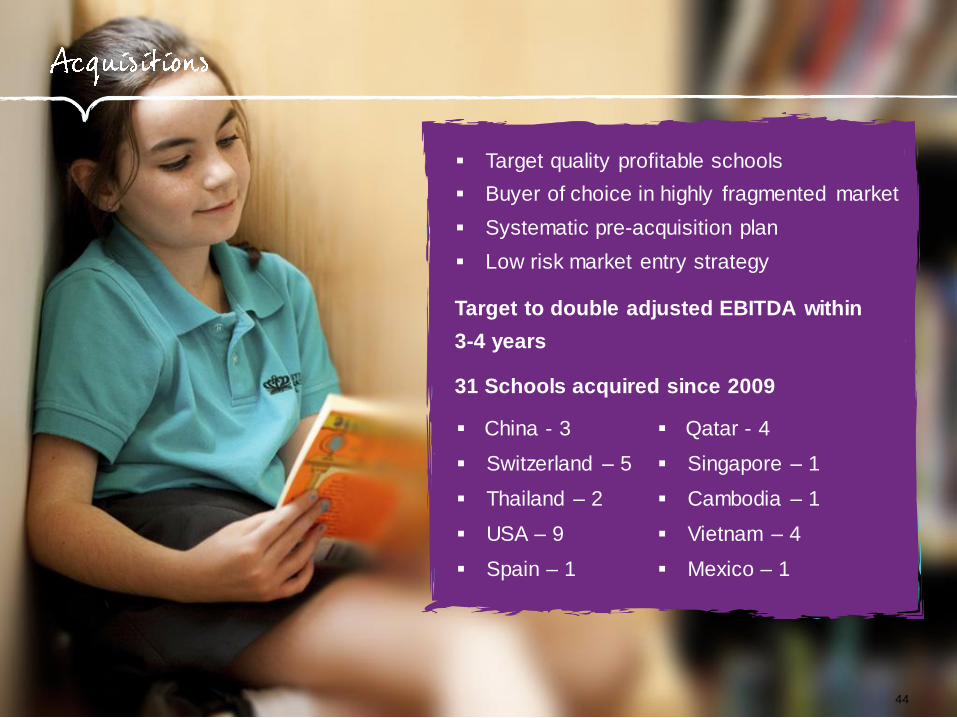

Target quality profitable schools

Buyer of choice in highly fragmented market

Systematic pre-acquisition plan

Low risk market entry strategy

Target to double adjusted EBITDA within

3-4 years

31 Schools acquired since 2009

China - 3 Qatar - 4

Switzerland – 5 Singapore – 1

Thailand – 2 Cambodia – 1

USA – 9 Vietnam – 4

Spain – 1 Mexico – 1

44

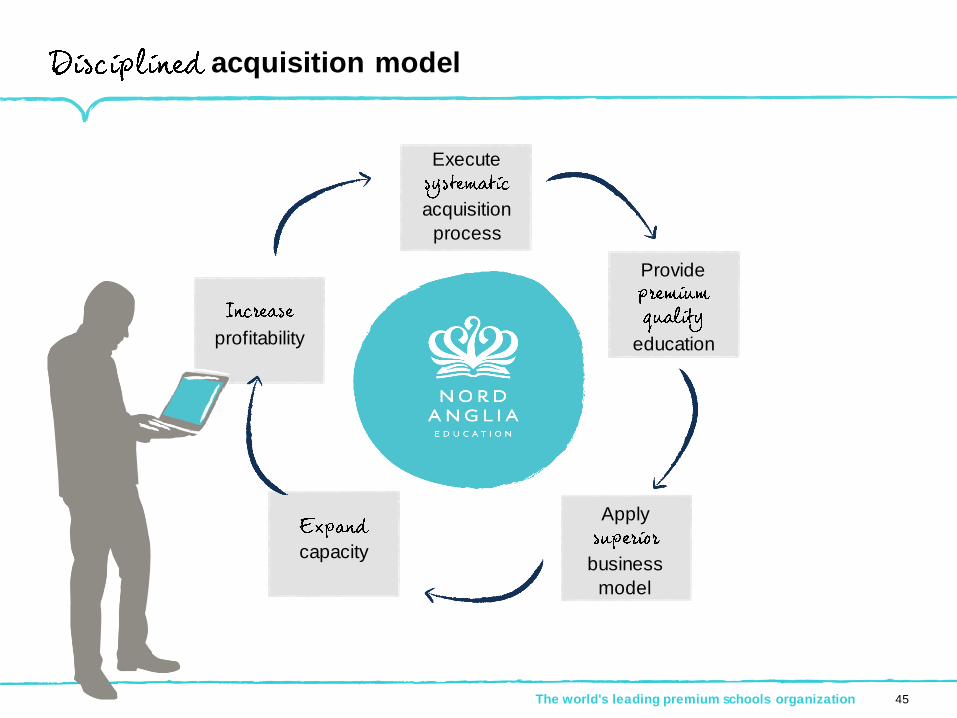

The world's leading premium schools organization 45

Execute

acquisition

process

Provide

education

Apply

business

model

capacity

profitability

acquisition model

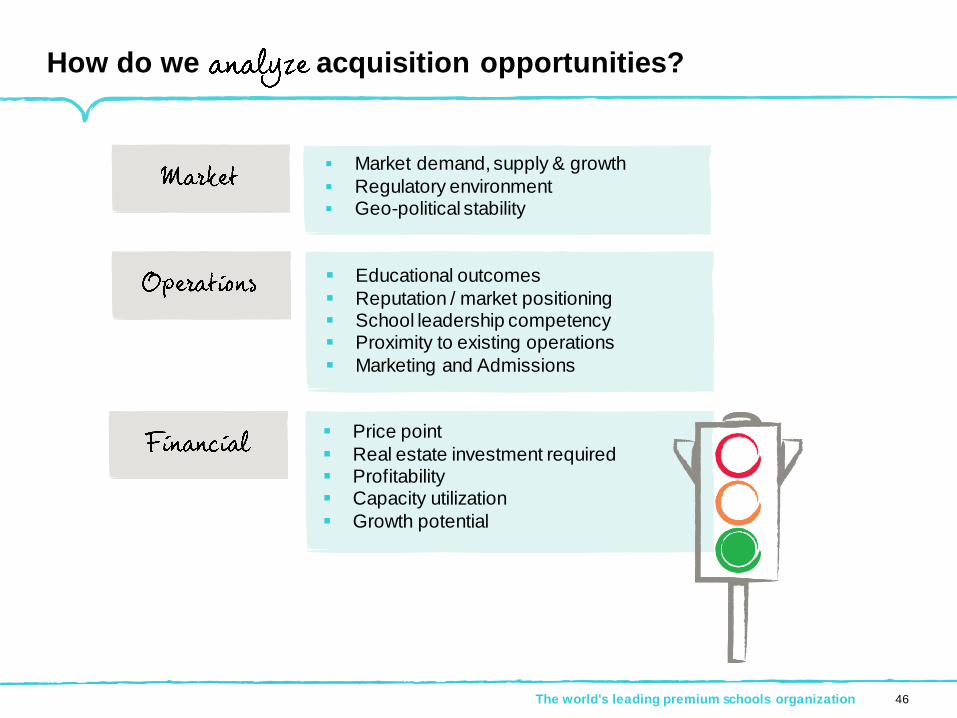

How do we acquisition opportunities?

The world's leading premium schools organization 46

Market demand, supply & growth

Regulatory environment Geo-political stability

Educational outcomes

Reputation / market positioning School leadership competency Proximity to existing operations

Marketing and Admissions

Price point

Real estate investment required Profitability Capacity utilization

Growth potential

The world's leading premium schools organization

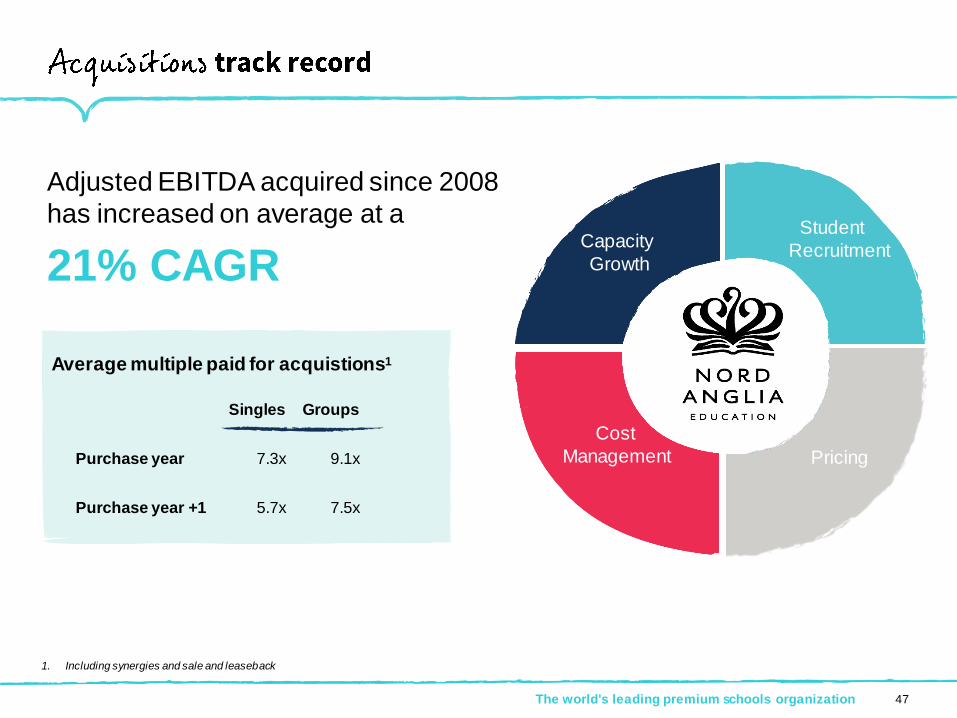

Adjusted EBITDA acquired since 2008

has increased on average at a

21% CAGR

Singles Groups

Purchase year 7.3x 9.1x

Purchase year +1 5.7x 7.5x

1. Including synergies and sale and leaseback

47

Average multiple paid for acquistions1

Capacity

Growth

Student

Recruitment

Pricing

Cost

Management

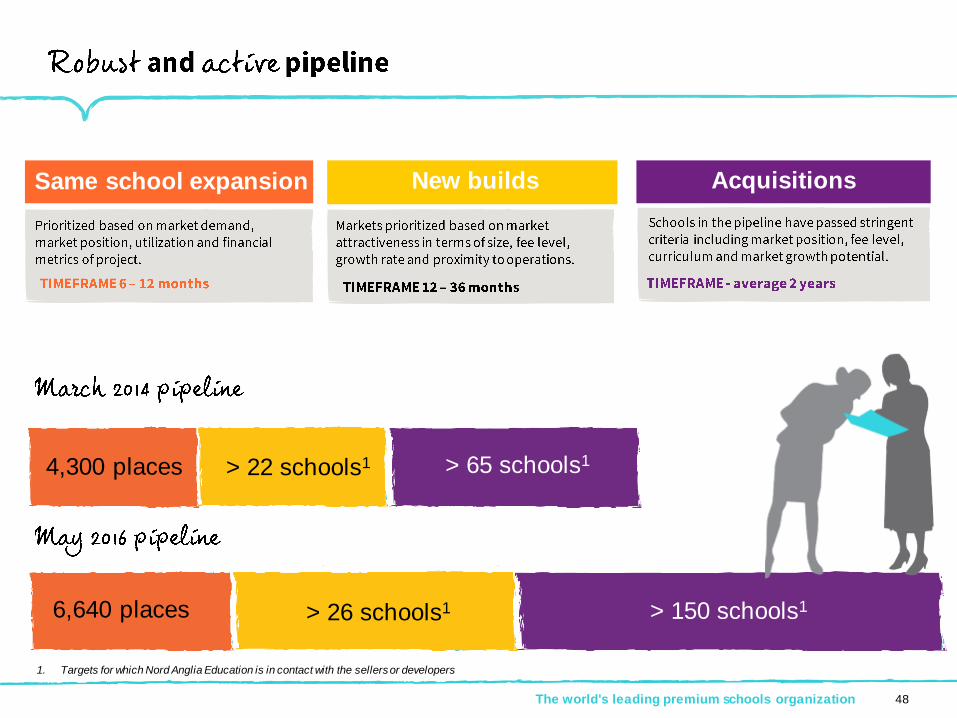

4,300 places > 22 schools1 > 65 schools1

6,640 places > 26 schools1 > 150 schools1

Same school expansion New builds Acquisitions

The world's leading premium schools organization 48

1. Targets for which Nord Anglia Education is in contact with the sellers or developers

Corporate Development team

Corporate Development Director

Origination

The world's leading premium schools organization 49

Acquisitions

Same school

expansions and

new builds

Integration

The world's leading premium schools organization

our family

50

The world's leading premium schools organization

school, regional

and central

51

The world's leading premium schools organization

China

Europe

Middle East

Southeast Asia

North America

RE

GIO

NS

ST

UD

EN

TS

& P

AR

EN

TS

Fin

ance

Ed

uca

tio

n

Ad

mis

sio

ns

& M

ark

eting

H.R

.

Co

rpo

rate

De

velo

pm

ent

CENTRAL

FUNCTIONAL TEAMS

SC

HO

OL

S

Strong

52

Regional management structure –

Balazs Szegedi

Regional Finance Director

Europe

Nadia Gardon

Regional HR DirectorEurope

Rob Breare

Regional Director of Marketing and

Admissions, Europe

Bartłomiej Cezak

Regional IT DirectorEurope

The world's leading premium schools organization 53

George GhantousRegional MD Europe

Philippe de Korodi

Principal, Collège Champittet

Tomas Schadler

Principal, Collège du Léman

Victoria Del Federio

Principal, Collège Beau Soleil

Wendy Ellis

Principal,La Côte International School

Aubonne

Jerry Singer

Principal, International College Spain

Matthew Farthing

Principal, The British International School

Bratislava

Dr. John Kennard

Principal, The British School Warsaw

Richard Dyer

Principal, The British International School

Budapest

Stephen Rogers

Principal, The English International School

Prague

approach to school management

Continuous improvement driven by

KPI’s measuring every aspect of our

schools’ performance on a weekly,

monthly and annual basis

The world's leading premium schools organization 54

Admissions

Health and

safety

Financials

HR

Academic

Performance

University

Destinations

Parent

voice

Effective process for acquisitions and new builds

55The world's leading premium schools organization

Pre-Acquisition

Regional & Corporate

Development teams

create tailored

integration plan in line

with acquisition plan

School

Acquired

Financial control

on closing

KPIs introduced

immediately

Ongoing

operations

Regional

implementation to

achieve plan

The world's leading premium schools organization

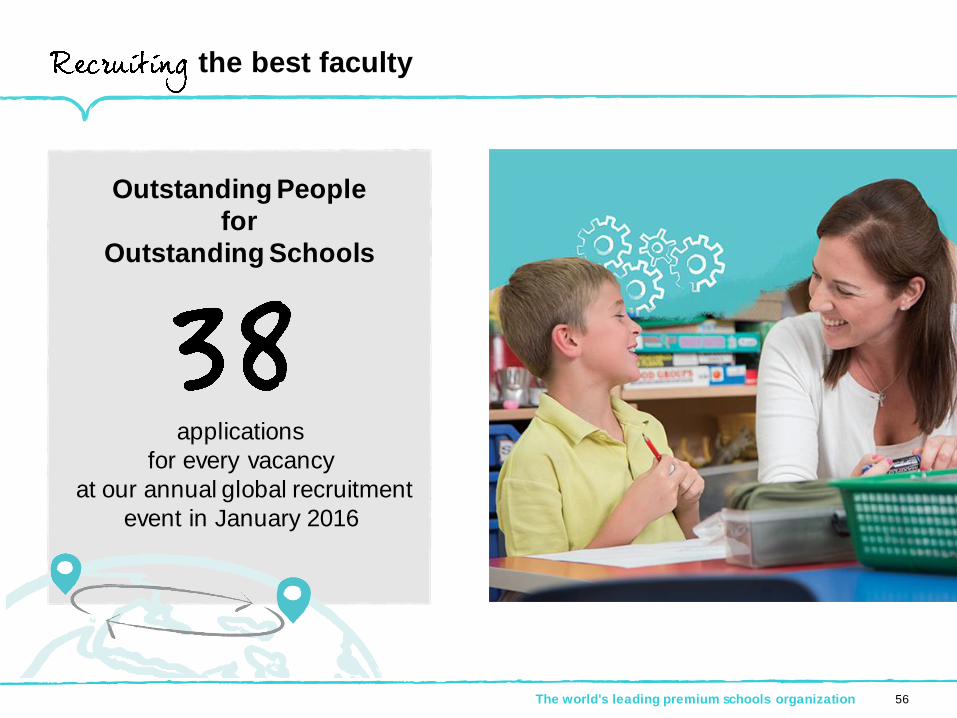

the best faculty

applications

for every vacancy

at our annual global recruitment

event in January 2016

Outstanding People

for

Outstanding Schools

56

through leading edge professional learning

The world's leading premium schools organization

Investment in professional

development to ensure the

highest quality faculty in every

school

57

leaders from within our organization

The world's leading premium schools organization 58

Talent Framework

Talent Review Boards

Promote from within

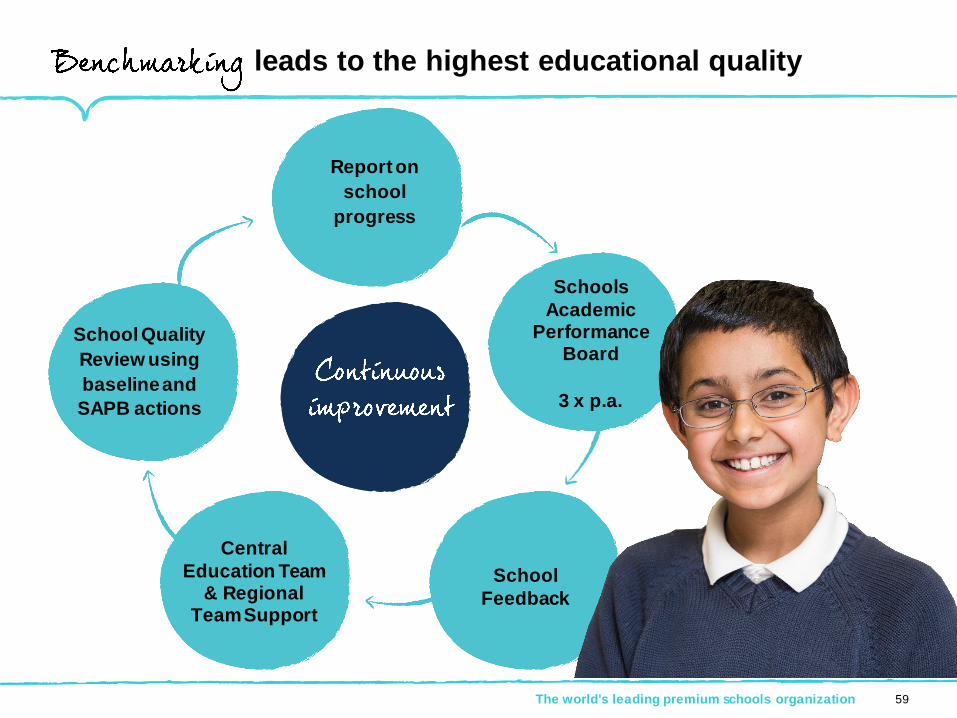

leads to the highest educational quality

The world's leading premium schools organization

Report on

school

progress

59

Schools

Academic Performance

Board

3 x p.a.

School

Feedback

Central

Education Team & Regional

Team Support

School Quality

Review using

baseline and

SAPB actions

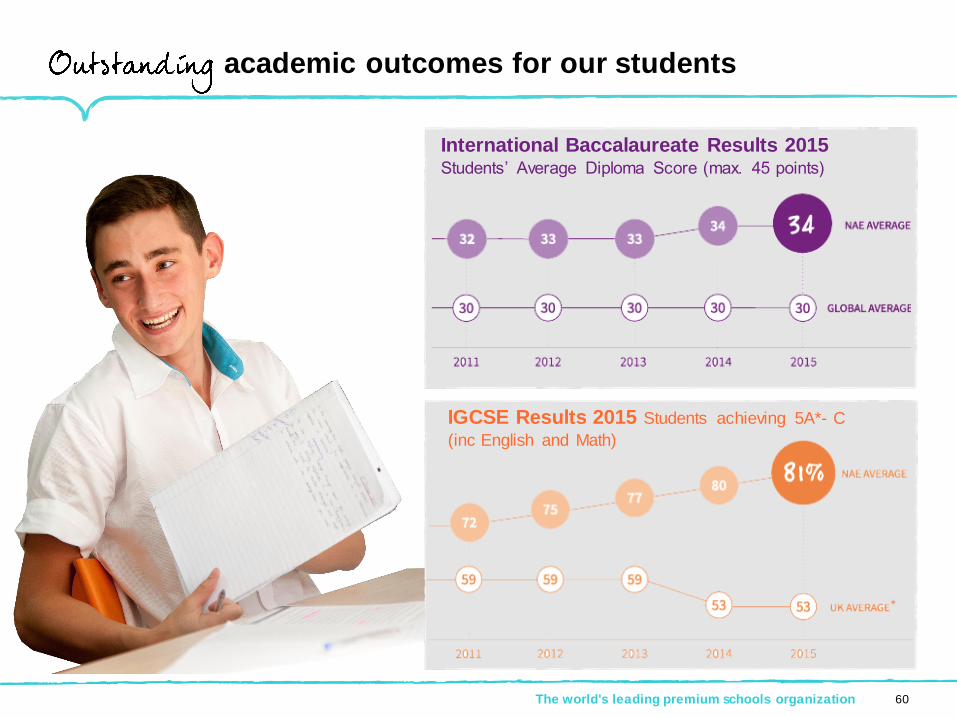

academic outcomes for our students

International Baccalaureate Results 2015Students’ Average Diploma Score (max. 45 points)

IGCSE Results 2015 Students achieving 5A*- C

(inc English and Math)

The world's leading premium schools organization 60

The world's leading premium schools organization

profile and targets61

The world's leading premium schools organization

financial profile

62

High growth

Strong visibility

High margins and operating leverage

Significant free cashflow

Outstanding returns on investment

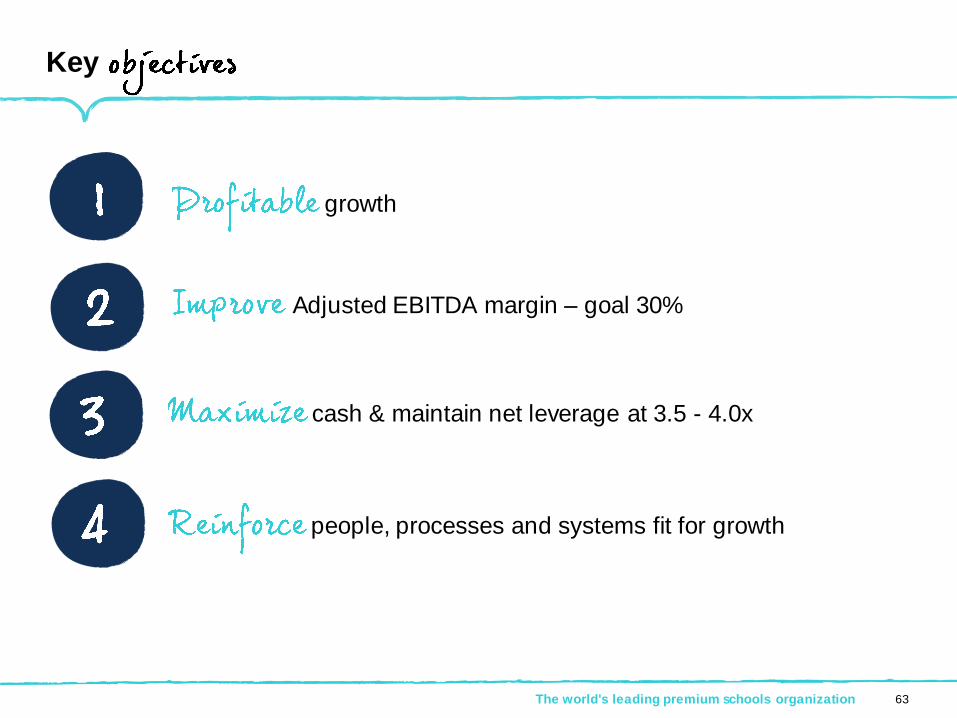

Key

63The world's leading premium schools organization

growth

cash & maintain net leverage at 3.5 - 4.0x

people, processes and systems fit for growth

Adjusted EBITDA margin – goal 30%

1. Midpoint of FY16E guidance

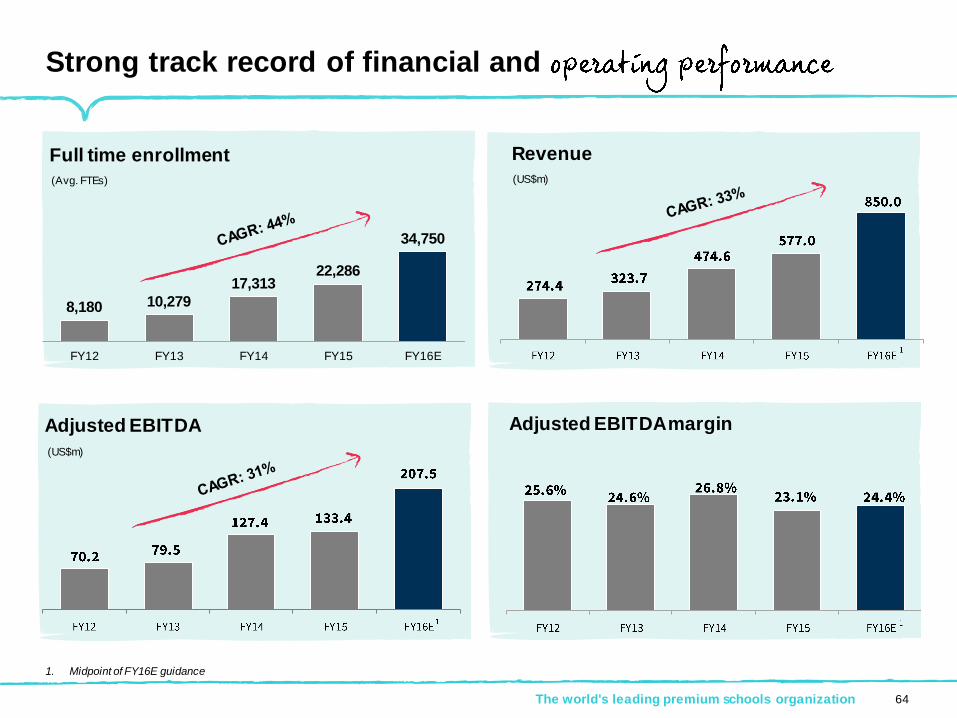

Strong track record of financial and

8,180 10,279

17,313 22,286

34,750

FY12 FY13 FY14 FY15 FY16E

Full time enrollment

(Avg. FTEs)

Revenue

(US$m)

Adjusted EBITDA

(US$m)

Adjusted EBITDA margin

The world's leading premium schools organization 64

The world's leading premium schools organization

Adjusted

EBITDA

margin

goal

65

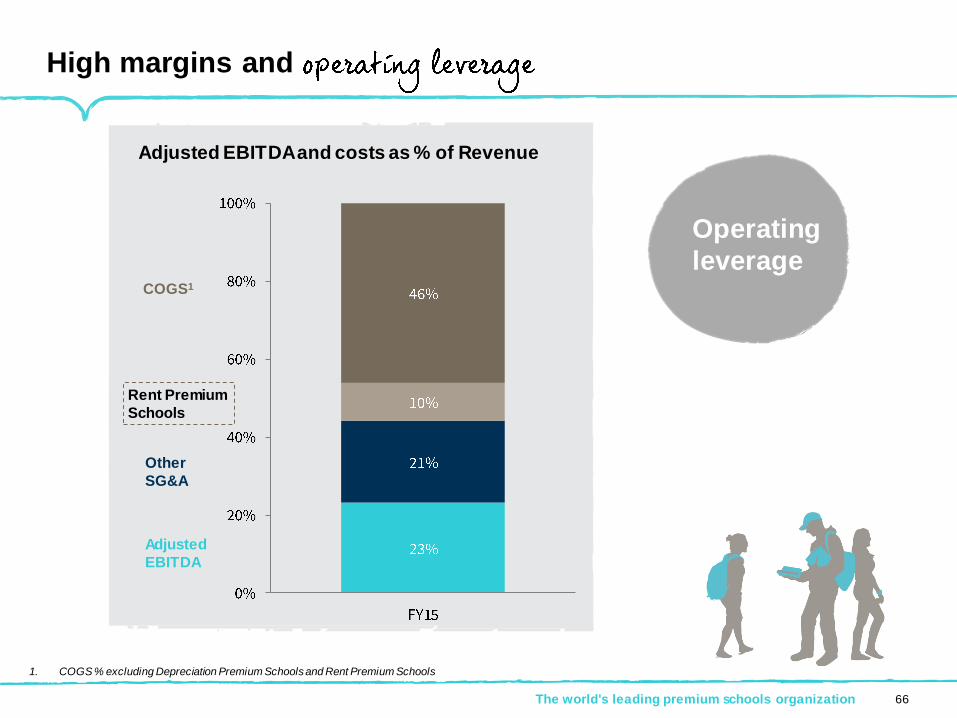

High margins and

Other

SG&A

COGS1

Adjusted

EBITDA

Rent Premium

Schools

1. COGS % excluding Depreciation Premium Schools and Rent Premium Schools

The world's leading premium schools organization 66

Adjusted EBITDA and costs as % of Revenue

Operating

leverage

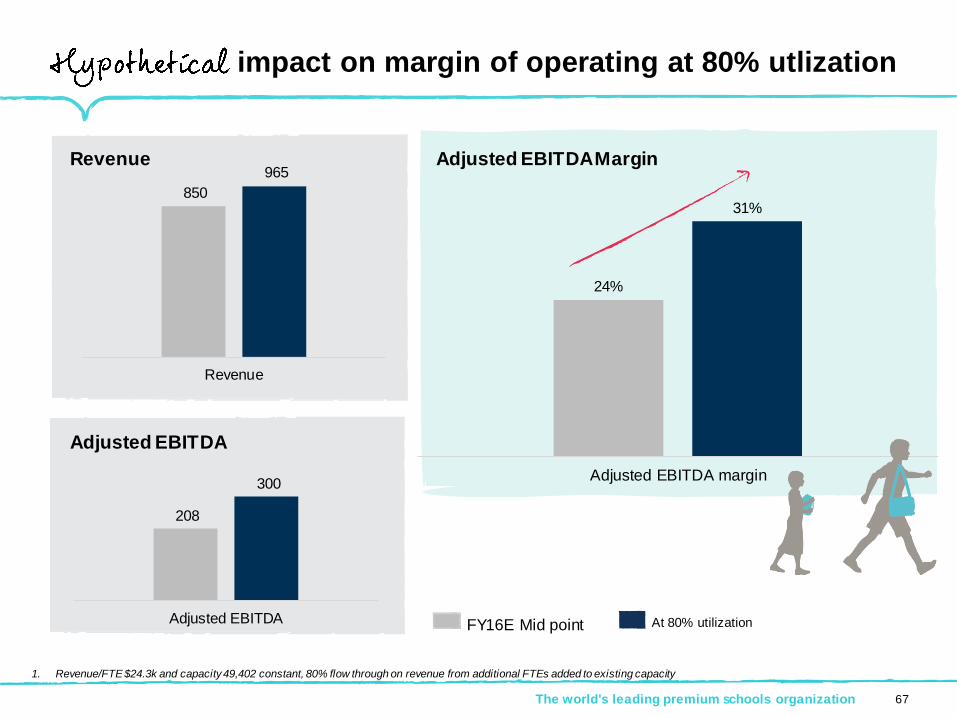

impact on margin of operating at 80% utlization

1. Revenue/FTE $24.3k and capacity 49,402 constant, 80% flow through on revenue from additional FTEs added to existing capacity

The world's leading premium schools organization 67

850

965

Revenue

208

300

Adjusted EBITDA

24%

31%

Adjusted EBITDA margin

Revenue

Adjusted EBITDA

Adjusted EBITDA Margin

FY16E Mid point At 80% utilization

The world's leading premium schools organization

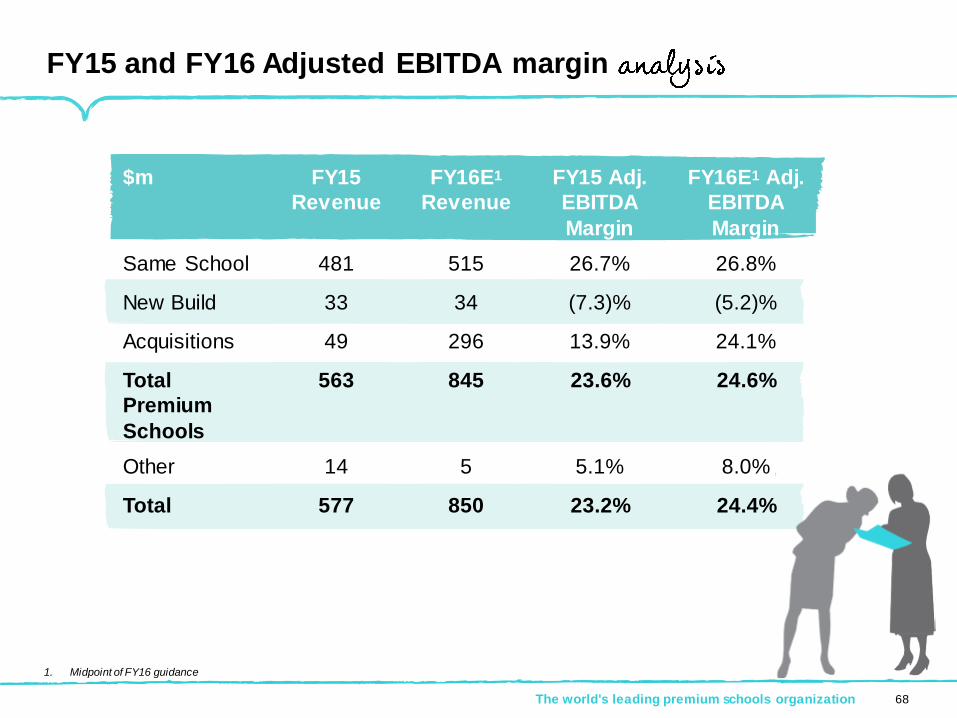

$m FY15

Revenue

FY16E1

Revenue

FY15 Adj.

EBITDA

Margin

FY16E1 Adj.

EBITDA

Margin

Same School 481 515 26.7% 26.8%

New Build 33 34 (7.3)% (5.2)%

Acquisitions 49 296 13.9% 24.1%

Total

Premium

Schools

563 845 23.6% 24.6%

Other 14 5 5.1% 8.0%

Total 577 850 23.2% 24.4%

FY15 and FY16 Adjusted EBITDA margin

68

1. Midpoint of FY16 guidance

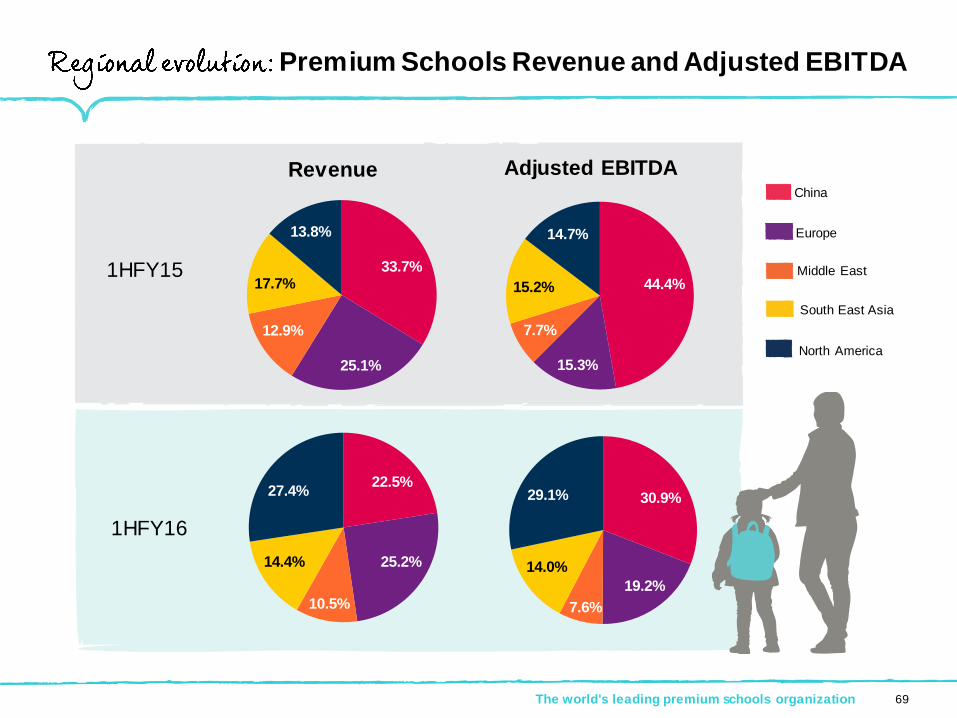

Premium Schools Revenue and Adjusted EBITDA

30.9%

19.2%

7.6%

14.0%

29.1%

Adjusted EBITDA

44.4%

15.3%

7.7%

15.2%

14.7%

China

Europe

Middle East

South East Asia

North America

1HFY16

The world's leading premium schools organization 69

Revenue

33.7%

25.1%

12.9%

17.7%

13.8%

22.5%

25.2%

10.5%

14.4%

27.4%

1HFY15

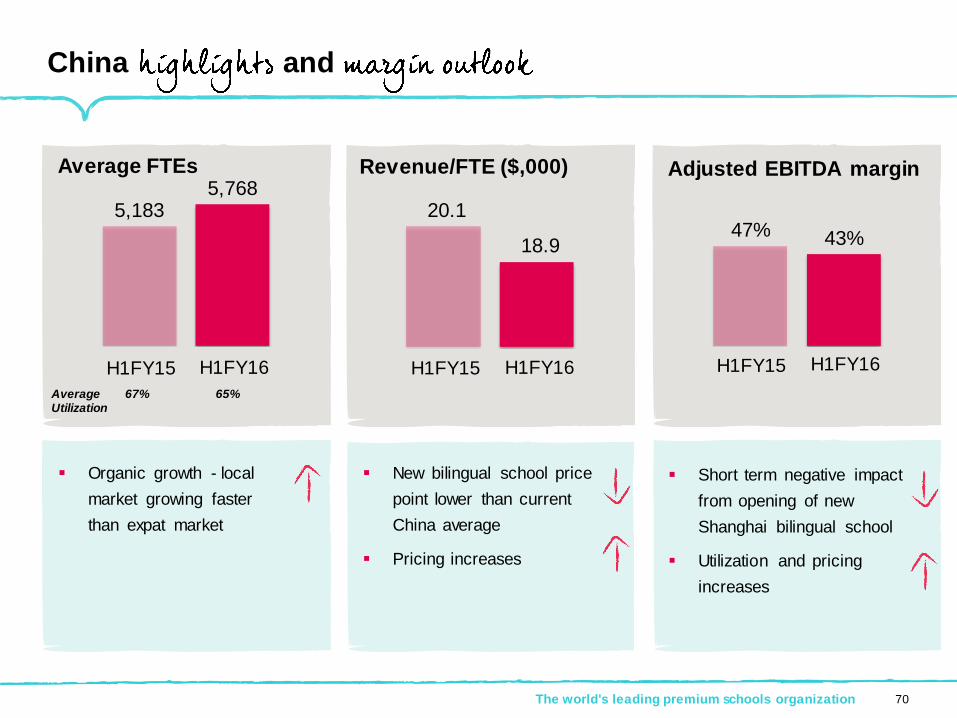

5,1835,768

20.1

18.9

China and

Organic growth - local

market growing faster

than expat market

H1FY15 H1FY16

The world's leading premium schools organization 70

47% 43%

H1FY15 H1FY16

Average 67% 65%Utilization

H1FY15 H1FY16

Revenue/FTE ($,000) Adjusted EBITDA margin Average FTEs

Short term negative impact

from opening of new

Shanghai bilingual school

Utilization and pricing

increases

New bilingual school price

point lower than current

China average

Pricing increases

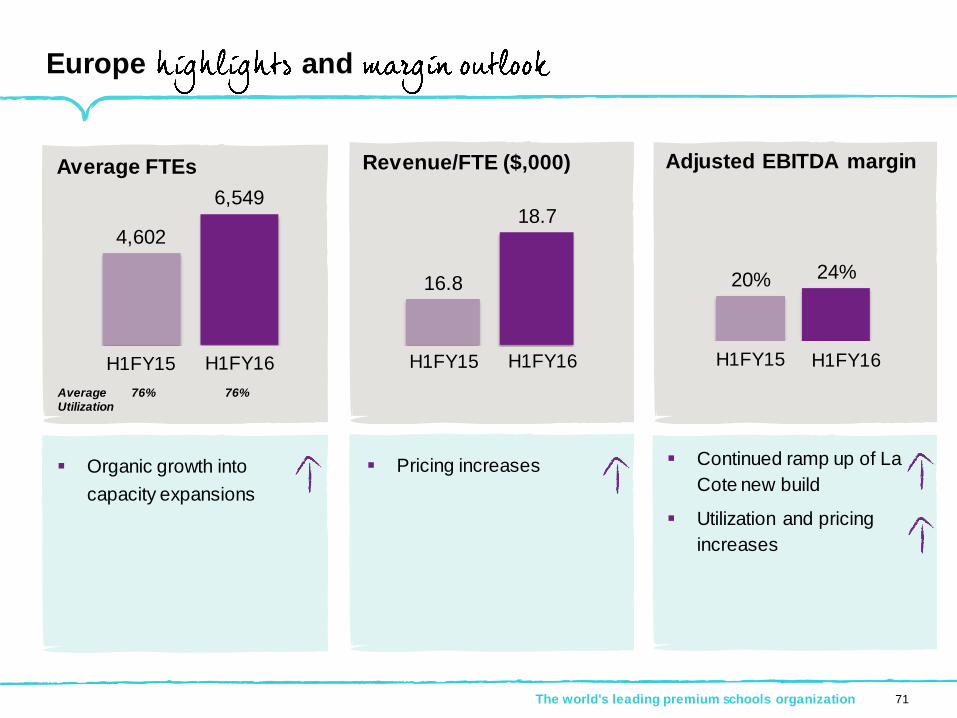

16.8

18.74,602

6,549

Europe and

The world's leading premium schools organization 71

H1FY15 H1FY16

20% 24%

H1FY15 H1FY16

Average 76% 76%Utilization

Revenue/FTE ($,000) Adjusted EBITDA margin Average FTEs

H1FY15 H1FY16

Continued ramp up of La

Cote new build

Utilization and pricing

increases

Pricing increases Organic growth into

capacity expansions

9.4

9.6

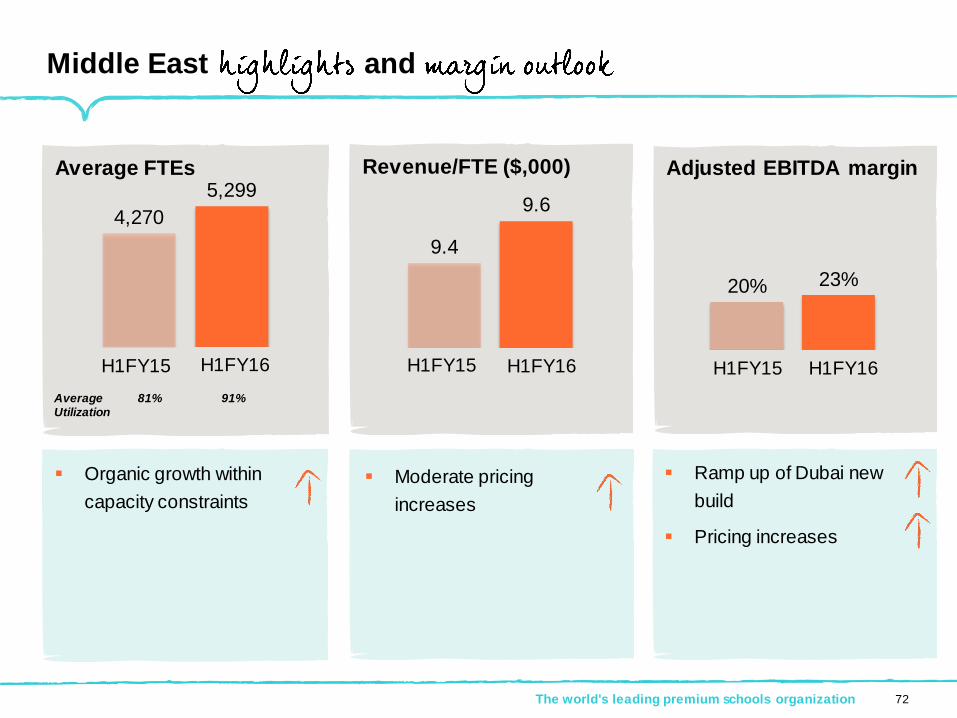

Middle East and

The world's leading premium schools organization 72

20% 23%

H1FY15 H1FY16

4,270

5,299

H1FY15 H1FY16

Average 81% 91%Utilization

Adjusted EBITDA margin Average FTEs Revenue/FTE ($,000)

Ramp up of Dubai new

build

Pricing increases

Moderate pricing

increases

Organic growth within

capacity constraints

H1FY15 H1FY16

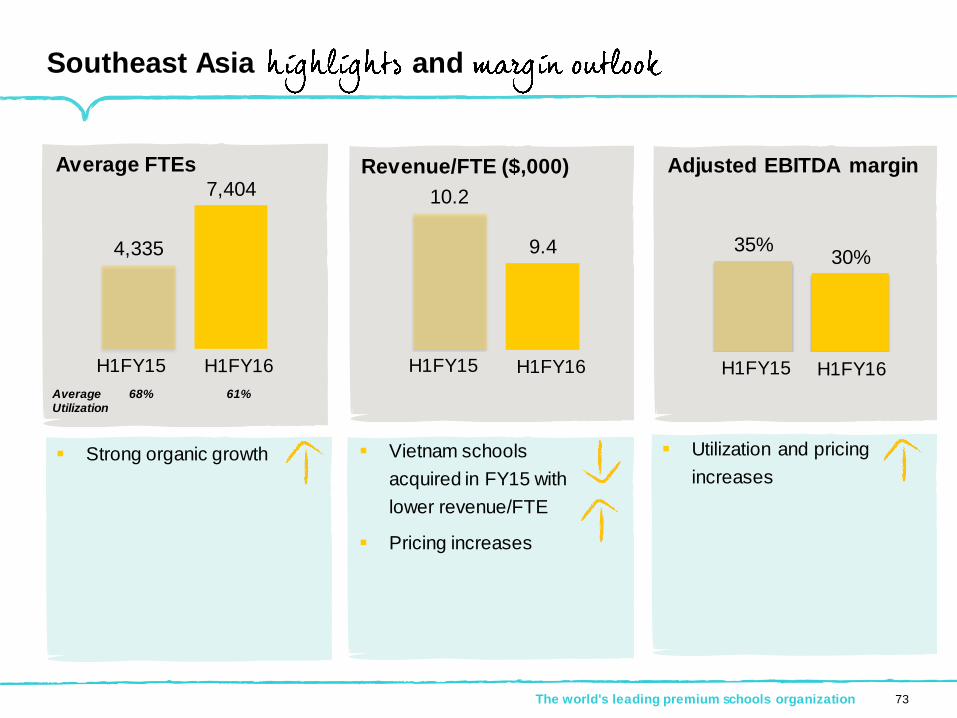

35%30%

Southeast Asia and

The world's leading premium schools organization 73

H1FY15 H1FY16

Average 68% 61%Utilization

4,335

7,404

H1FY15 H1FY16

Adjusted EBITDA margin Average FTEs Revenue/FTE ($,000)

10.2

9.4

H1FY15 H1FY16

Utilization and pricing

increases

Vietnam schools

acquired in FY15 with

lower revenue/FTE

Pricing increases

Strong organic growth

35% 32%

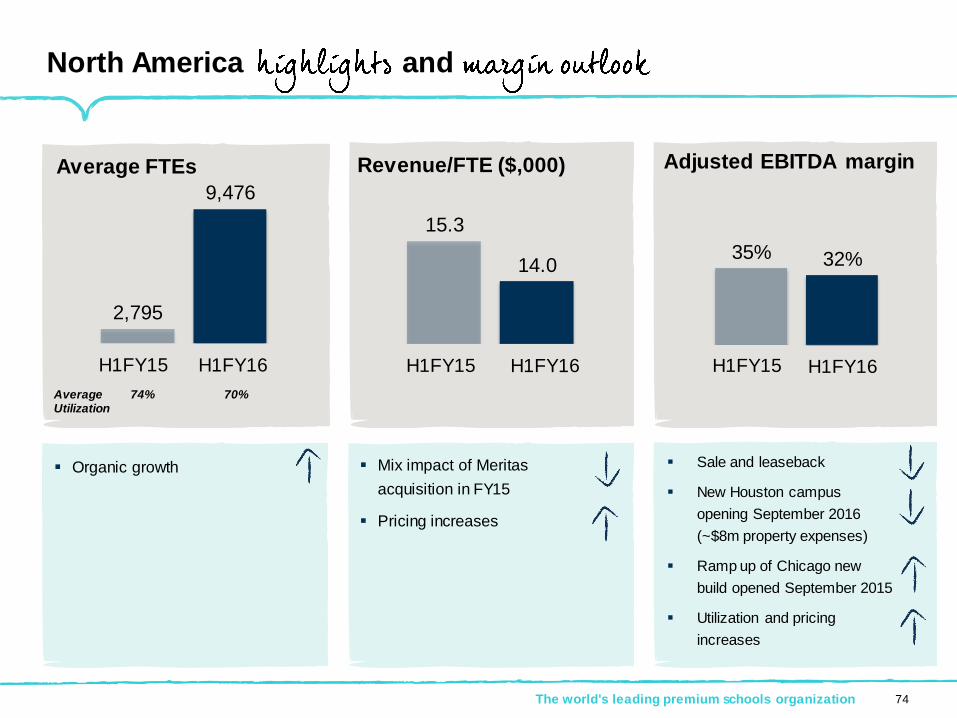

15.3

14.0

2,795

9,476

North America and

The world's leading premium schools organization 74

H1FY15 H1FY16H1FY15 H1FY16

Adjusted EBITDA margin Average FTEs Revenue/FTE ($,000)

H1FY15 H1FY16

Sale and leaseback

New Houston campus

opening September 2016

(~$8m property expenses)

Ramp up of Chicago new

build opened September 2015

Utilization and pricing

increases

Mix impact of Meritas

acquisition in FY15

Pricing increases

Organic growth

Average 74% 70%Utilization

The world's leading premium schools organization

Maximize

and maintain

75

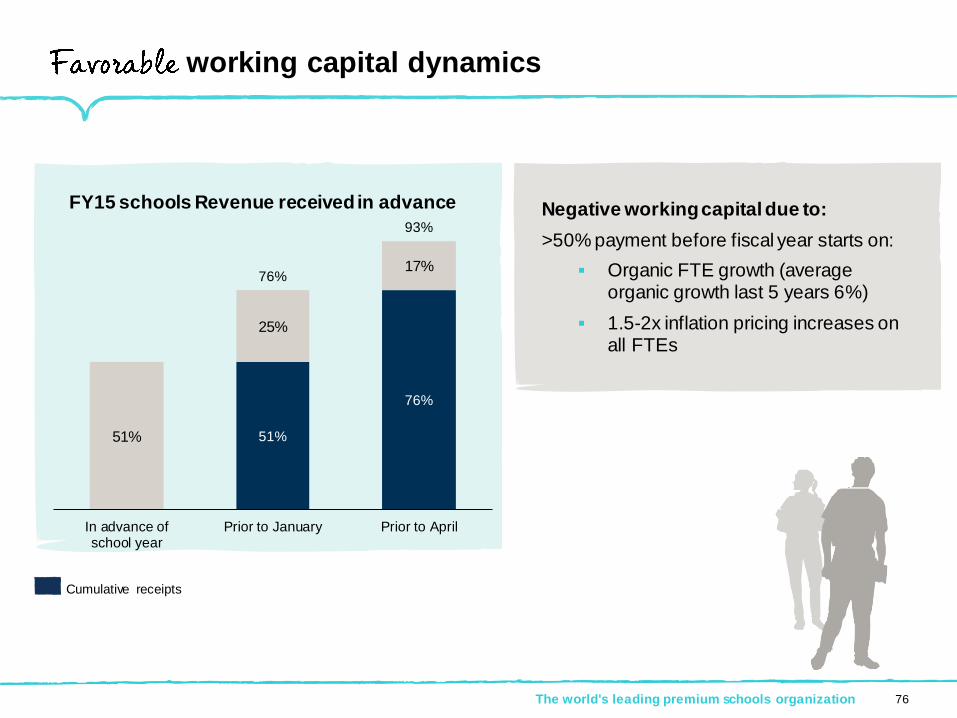

Negative working capital due to:

>50% payment before fiscal year starts on:

Organic FTE growth (average organic growth last 5 years 6%)

1.5-2x inflation pricing increases on all FTEs

The world's leading premium schools organization

working capital dynamics

51%

76%

51%

25%

17%76%

93%

In advance ofschool year

Prior to January Prior to April

76

FY15 schools Revenue received in advance

Cumulative receipts

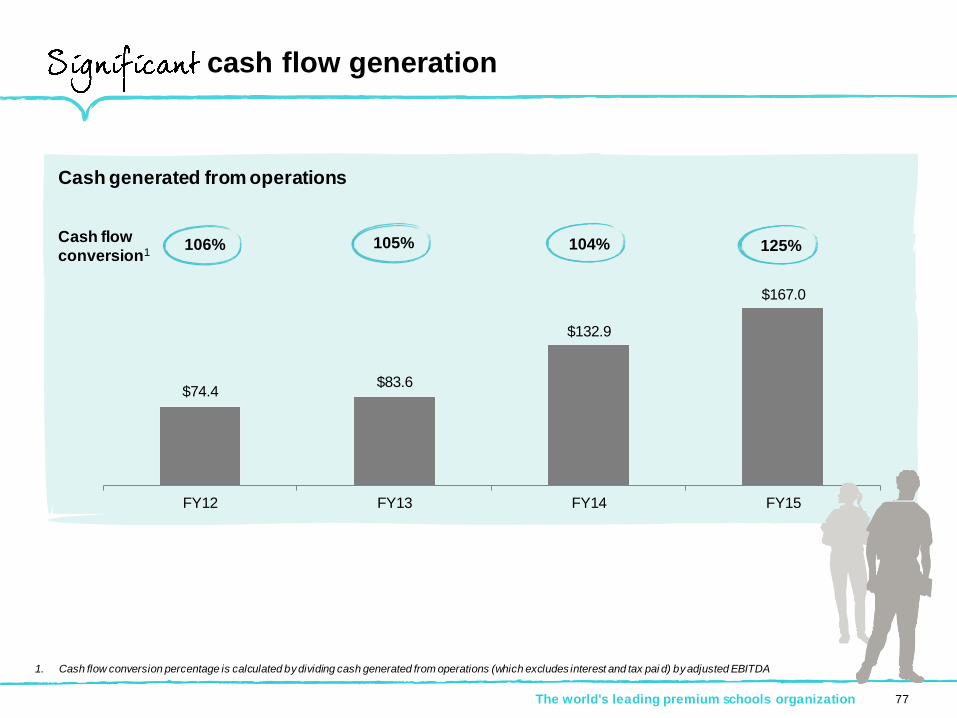

cash flow generation

$74.4$83.6

$132.9

$167.0

FY12 FY13 FY14 FY15

Cash flow

conversion1

1. Cash flow conversion percentage is calculated by dividing cash generated from operations (which excludes interest and tax pai d) by adjusted EBITDA

The world's leading premium schools organization 77

Cash generated from operations

106% 105% 104% 125%

Strong cash generation

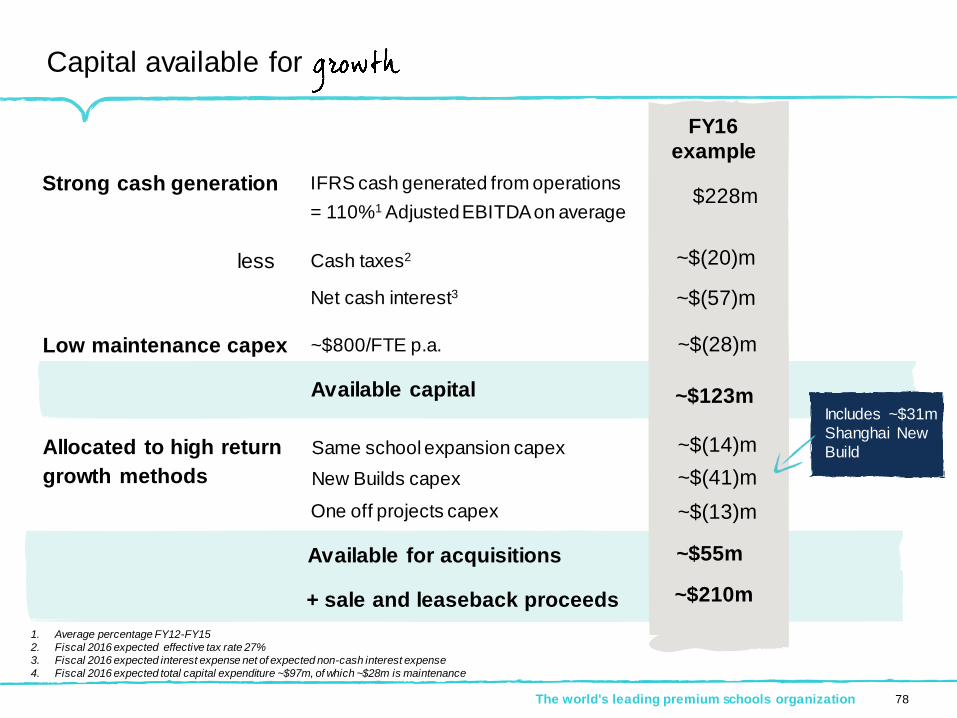

Capital available for

78The world's leading premium schools organization

IFRS cash generated from operations

= 110%1 Adjusted EBITDA on average

FY16

example

less Cash taxes2

Net cash interest3

Low maintenance capex ~$800/FTE p.a.

Available capital

Same school expansion capex

New Builds capex

One off projects capex

Allocated to high return

growth methods

~$(14)m

~$(41)m

~$(28)m

~$(57)m

~$(20)m

$228m

~$123m

~$(13)m

~$55m

1. Average percentage FY12-FY15

2. Fiscal 2016 expected effective tax rate 27%

3. Fiscal 2016 expected interest expense net of expected non-cash interest expense

4. Fiscal 2016 expected total capital expenditure ~$97m, of which ~$28m is maintenance

Includes ~$31m

Shanghai New

Build

Available for acquisitions

+ sale and leaseback proceeds ~$210m

79The world's leading premium schools organization

Net leverage target

2.9 x

4.7 x

3.8 x

FY14 FY15PF FY16E

38%

62%

Net Leverage profile Debt by currency1

USD

CHF, RMB

EUR

Debt capacity up to 4.0x provides additional available capital for growth

1. After giving effect to $120m USD CNH cross currency swap and $90m USD EUR cross currency swap entered into Q3 FY16.

The world's leading premium schools organization

Reinforcing

for

growth

80

Recruiting additional resources –

Finance, Internal Audit, Compliance,

Sarbanes-Oxley

Improved systems – accounting,

reporting, consolidation

Revised procedures – increased

quarterly auditor review

The world's leading premium schools organization 81

capital allocation targets

~5-10% of capacity 2 -3 per year

The world's leading premium schools organization 82

Remaining capital

50%+ ROI 70%+ ROI 21% CAGR

Favorable

demographics

83The world's leading premium schools organization

Constantly exceptional new opportunities

Unique

Opportunities

Strength of

Nord Anglia

Education

Brand

=+

The world's leading premium schools organization

Building a global brand that everyone

84

The world's leading premium schools organization 85