investing for your future chapter 11. lesson 11.1 investing fundamentals i.stages of investing...

TRANSCRIPT

Investing for Your Investing for Your FutureFutureChapter 11Chapter 11

Lesson 11.1 Investing Lesson 11.1 Investing FundamentalsFundamentals

I.I. Stages of Investing Stages of Investing

A.A. Stage 1. Put-and-Take Stage 1. Put-and-Take Account Account (Emergency Fund)(Emergency Fund)

1. When you first begin to 1. When you first begin to earn a earn a paycheckpaycheck

2. Recommend that you have 2. Recommend that you have three to six three to six months’ net pay months’ net pay set aside for this type set aside for this type of of fundfund

3. Main concern in saving 3. Main concern in saving these funds is these funds is safetysafety

B.B. Stage 2. Beginning Stage 2. Beginning InvestingInvesting

1.1. Investing—Investing—the use of savings to the use of savings to earn a earn a financial return, earn money financial return, earn money with moneywith money

2.2. Make permanent investments Make permanent investments in addition in addition to temporary emergency to temporary emergency fundsfunds

3.3. Initial investments should be Initial investments should be conservative and low riskconservative and low risk

4.4. Typically, workers in 20s and Typically, workers in 20s and 30s begin 30s begin investing when their investing when their budgets and budgets and spending are stable spending are stable and excess cash is and excess cash is increasingincreasing

Stage 3. Systematic Stage 3. Systematic InvestingInvesting

1.1. Systematic Systematic InvestingInvesting — — investing investing on a regular on a regular and and planned basisplanned basis

2.2. Goals are Goals are long-range, long-range, investing for a investing for a secure secure future, 30s future, 30s and 40sand 40s

Stage 4. Strategic Stage 4. Strategic Investing Investing

1. 1. Strategic investing—the Strategic investing—the careful careful management of management of investment alternatives investment alternatives to to maximize growth of your portfolio maximize growth of your portfolio

(collection of investments) (collection of investments) over the next over the next 5—10 years 5—10 years

2.2. Invest in different types of Invest in different types of securities to securities to try to maximize try to maximize your returnsyour returns

Stage 5. Speculative Stage 5. Speculative Investing Investing

1.1. Speculative Speculative investing—take investing—take greater risks; greater risks; can make or lose can make or lose a great deal of a great deal of moneymoney

2.2. Many investors Many investors never choose to never choose to speculatespeculate

II.II. Reasons for InvestingReasons for Investing

A.A. Investing Helps Beat InflationInvesting Helps Beat Inflation

1.1. InflationInflation—rise in the —rise in the general level general level of prices. of prices. Inflation reduces Inflation reduces purchasing power over timepurchasing power over time

2.2. Investors seek investments Investors seek investments for the for the long term that will long term that will grow faster than grow faster than the inflation the inflation raterate

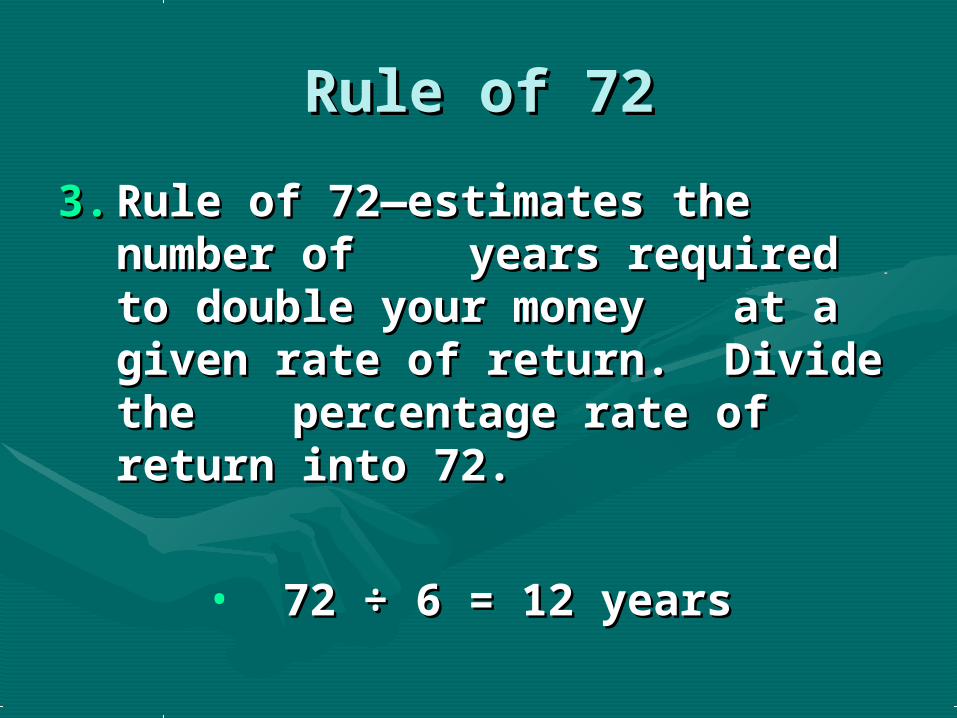

Rule of 72Rule of 72

3.3. Rule of 72—estimates the Rule of 72—estimates the number of number of years required years required to double your money to double your money at a at a given rate of return. Divide given rate of return. Divide the the percentage rate of percentage rate of return into 72.return into 72.

• 72 ÷ 6 = 12 years72 ÷ 6 = 12 years

Reasons for InvestingReasons for Investing

B.B. Investing Increases WealthInvesting Increases Wealth

1.1. Over the long run, Over the long run, investments earn investments earn higher profits higher profits than savings dothan savings do

2.2. When you invest in stocks When you invest in stocks and and bonds, bonds, you are helping you are helping businessesbusinesses

C.C. Investing is Fun and Investing is Fun and ChallengingChallenging

III.III. Risk and ReturnRisk and ReturnA.A. RiskRisk—the chance that an —the chance that an

investment’s investment’s value will value will decreasedecrease

1.1. Risk averse—afraid to make Risk averse—afraid to make risky risky investmentsinvestments

2.2. Risk-takers—can make or Risk-takers—can make or lose a lotlose a lot

B.B. Diversification—Diversification—minimizes riskminimizes risk

1.1. Spreads the risk Spreads the risk among many among many types of types of investmentsinvestments

2.2. Stocks, bonds, Stocks, bonds, real estatereal estate

3.3. Diversify types of Diversify types of stocksstocks

C.C. Types of RiskTypes of Risk

1.1. Interest-rate risk—during Interest-rate risk—during inflation, inflation, return on investment will return on investment will not keep pace not keep pace with inflation rate, with inflation rate, “locked in” at lower “locked in” at lower ratesrates

2.2. Political risk—government Political risk—government actions that actions that affect business affect business conditionsconditions

3.3. Market risk—caused by business Market risk—caused by business declines or interest rate declines or interest rate

fluctuationsfluctuations

Types of RiskTypes of Risk

4.4. Nonmarket risk—Nonmarket risk—risk unrelated to risk unrelated to market trends market trends (terrorism)(terrorism)

5.5. Company or Company or industry risk—industry risk—produced by events produced by events that affect only one that affect only one company or company or industryindustry

IV.IV.Investment StrategiesInvestment Strategies

A.A. Criteria for Choosing an Criteria for Choosing an InvestmentInvestment

1.1. Degree of safety (risk of Degree of safety (risk of loss)loss)

2.2. Degree of liquidity (ability Degree of liquidity (ability to get to get your money quickly)your money quickly)

3.3. Expected dividends or Expected dividends or interestinterest

Criteria for Choosing an Criteria for Choosing an InvestmentInvestment

4.4. Expected growth in value, Expected growth in value, preferably preferably exceeding inflation rateexceeding inflation rate

5.5. Reasonable purchase price and Reasonable purchase price and feesfees

6.6. Tax benefits (saving or Tax benefits (saving or postponing tax postponing tax liability)liability)

B.B. Wise Investment Wise Investment PracticesPractices

1.1. Define your financial goals—specific Define your financial goals—specific and measurable, set $ targetsand measurable, set $ targets

2.2. Go slowly—gather info and make a Go slowly—gather info and make a wise decision. If is sounds too good to be wise decision. If is sounds too good to be true, it probably is true, it probably is

3.3. Follow through—act on your Follow through—act on your important goals nowimportant goals now

4.4. Keep good records—personal net Keep good records—personal net worth statement, lists of insurance worth statement, lists of insurance policies and investments, account policies and investments, account balances, location of bank accounts, balances, location of bank accounts, contents and location of safe deposit box. contents and location of safe deposit box. Keep statements.Keep statements.

Wise Investment Wise Investment PracticesPractices

5.5. Seek good investment advice—Seek good investment advice—don’t be afraid to ask questions, don’t be afraid to ask questions, attend investment seminarattend investment seminar

6.6. Keep investment knowledge Keep investment knowledge current—it is your responsibility current—it is your responsibility to make final decisionsto make final decisions

7.7. Know your limits—understand Know your limits—understand your risk tolerance. The chance of your risk tolerance. The chance of making huge profits is not worth making huge profits is not worth being stressed out by the risk.being stressed out by the risk.

Lesson 11.2Lesson 11.2

•Exploring Exploring InvestmeInvestment nt OptionsOptions

I.I. Sources of Financial Sources of Financial InformationInformation

A.A. Newspapers—contain Newspapers—contain financial pagesfinancial pages

1.1. Wall Street JournalWall Street Journal—daily —daily with detailed with detailed coverage of coverage of business and financial worldbusiness and financial world

2.2. Barron’sBarron’s—weekly with charts —weekly with charts of trends, of trends, financial news, financial news, analysis of financial dataanalysis of financial data

Sources of Financial Sources of Financial Information Information

B.B. Investor Services and Investor Services and NewslettersNewsletters

1.1. Investor Services provide Investor Services provide extensive extensive financial data to financial data to clients clients

2.2. Moody’s Investors ServiceMoody’s Investors Service ((www.moodys.comwww.moodys.com))

3.3. Standard and Poor’s ReportsStandard and Poor’s Reports (www.standardandpoors.com)(www.standardandpoors.com)

Sources of Financial Sources of Financial Information Information

C.C. Financial MagazinesFinancial Magazines

1.1. Business Week Business Week

((www.businessweek.com)www.businessweek.com)

2.2. Forbes Forbes (www.forbes.com)(www.forbes.com)

3.3. Money (Money (www.money.cnn.comwww.money.cnn.com) ) Fortune (Fortune (www.fortune.comwww.fortune.com))

Sources of Financial Sources of Financial Information Information D.D. BrokersBrokers

1.1. Full-service brokers—provide Full-service brokers—provide clients with analysis and opinions clients with analysis and opinions based on their judgments and the based on their judgments and the opinions of experts at their company opinions of experts at their company (Merrill Lynch, Fidelity Investments, (Merrill Lynch, Fidelity Investments, American Express)American Express)2.2. Discount brokers—buy and sell Discount brokers—buy and sell securities for clients at a reduced securities for clients at a reduced commission; usually provides little commission; usually provides little or no investment advice. (Charles or no investment advice. (Charles Schwab, Ameritrade, E*Trade)Schwab, Ameritrade, E*Trade)3.3. Many banks, credit unions, S&Ls Many banks, credit unions, S&Ls have discount brokers availablehave discount brokers available4.4. With most brokerage accounts, With most brokerage accounts, you can manage your account online.you can manage your account online.

Sources of Financial Sources of Financial Information Information

E.E. Financial AdvisorsFinancial Advisors

1.1. Professional investment Professional investment planners (CFP—Certified planners (CFP—Certified Financial Planners). Trained Financial Planners). Trained to give investment advice to give investment advice based on your goals, age, based on your goals, age, lifestyle. lifestyle.

2.2. Usually receive a feeUsually receive a fee

Sources of Financial Sources of Financial Information Information

F.F. Annual ReportsAnnual Reports

1.1. Summary of a corporation’s Summary of a corporation’s financial results for the year financial results for the year

and and prospects for the futureprospects for the future

2.2. SEC requires all corporations to SEC requires all corporations to prepare prepare this report yearly and this report yearly and send it to send it to stockholders. Can also stockholders. Can also find annual find annual reports online (reports online (www.sec.govwww.sec.gov))

Sources of Financial Sources of Financial Information Information

G.G. Online Investor EducationOnline Investor Education

1.1. Teenvestor (Teenvestor (www.teenvestor.comwww.teenvestor.com))

2.2. The Motley Fool (The Motley Fool (www.fool.comwww.fool.com))

II.II. Investment OptionsInvestment OptionsA.A. Low Risk/Low Return Low Risk/Low Return

1.1. Corporate and Municipal BondsCorporate and Municipal Bondsa. Bonds are debt obligations a. Bonds are debt obligations

of corpor-of corpor- ations ations (corporate bonds) or state or local(corporate bonds) or state or local

governments (municipal bonds)governments (municipal bonds)b. Corporation pays you a fixed b. Corporation pays you a fixed

amount of amount of money (interest) at a money (interest) at a fixed interval, and fixed interval, and then pays then pays the principal at maturitythe principal at maturity

c. Interest on govt bonds is c. Interest on govt bonds is usually tax-freeusually tax-free

Low Risk/Low Return Low Risk/Low Return

2.2. U.S. Government Savings BondsU.S. Government Savings Bondsa. Lending money to the U.S. a. Lending money to the U.S.

governmentgovernmentb. Series EE bond is a discount bond, b. Series EE bond is a discount bond,

pay $25, pay $25, receive $50 at maturityreceive $50 at maturityc. Series HH bond, purchased in c. Series HH bond, purchased in

exchange of exchange of maturing EE bondsmaturing EE bondsd. Series I bond, sold at face value, d. Series I bond, sold at face value,

grow with grow with inflation based earningsinflation based earningse. Buy at bank, store in safe deposit e. Buy at bank, store in safe deposit

box. Safe box. Safe and liquid.and liquid.

Low Risk/Low Return Low Risk/Low Return

3. 3. Treasury SecuritiesTreasury Securities

a. U.S. Treasury bills (t-bills) a. U.S. Treasury bills (t-bills) available available $10,000 + $5000 $10,000 + $5000 increments. increments. Matures in one Matures in one year or less.year or less.

b. Treasury Notes—units of $1000 b. Treasury Notes—units of $1000 or or $5000, 2—10 years$5000, 2—10 years

c. Treasury bonds--$1000 units, c. Treasury bonds--$1000 units, 10—30 10—30 year maturityyear maturity

B.B. Medium Risk/Medium Medium Risk/Medium Return Return

1.1. Stocks—unit of ownership in a Stocks—unit of ownership in a corporation; stockholders corporation; stockholders earnings depend on the earnings depend on the company’s fortunescompany’s fortunes

2.2. Mutual Funds—shares in a large, Mutual Funds—shares in a large, professional managed group of professional managed group of investments. Pools the money of investments. Pools the money of many investors and buys a large many investors and buys a large selection of securities. Some selection of securities. Some have different objectives.have different objectives.

Medium Risk/Medium Medium Risk/Medium Return Return

3.3. Annuity—a contract sold Annuity—a contract sold by an insurance company that by an insurance company that provides the investor with a series provides the investor with a series of regular payments, usually after of regular payments, usually after retirement. Taxes are deferred retirement. Taxes are deferred until you receive payment of your until you receive payment of your annuity.annuity.

4.4. Real Estate—houses and Real Estate—houses and land. Protection against inflation. land. Protection against inflation. Own homeOwn home

C. C. High Risk/High High Risk/High ReturnReturn

1.1. Involves considerable uncertaintyInvolves considerable uncertainty

2.2. Futures—contracts to buy and Futures—contracts to buy and sell commodities or stocks for a sell commodities or stocks for a specified price on a specified date in specified price on a specified date in the future.the future.

3.3. Options—the right, but not the Options—the right, but not the obligation, to buy or sell a obligation, to buy or sell a commodity or stock for a specified commodity or stock for a specified price within a specified time period. price within a specified time period. Short-term investment devices used Short-term investment devices used by speculators to make a quick profit.by speculators to make a quick profit.

High Risk/High ReturnHigh Risk/High Return

4.4. Penny stocks—low-Penny stocks—low-priced stocks of small priced stocks of small companies that have no track companies that have no track record. Usually sells record. Usually sells <$1.00/share. <$1.00/share.

5.5. Collectibles—coins, Collectibles—coins, art, memorabilia, ceramics, art, memorabilia, ceramics, antiquesantiques