investigating the relationship between...

TRANSCRIPT

تحقیقات جدید در علوم انسانیفصلنامه

Human Sciences Research Journal

Vol 3 / No 12 / 2016 / P 23-37 39-97صص /5931 پاییز /دهمزادوشماره / سال سوم

Investigating the relationship between macroeconomic indicators

and indicator of Tehran Stock Exchange

Mehdi Parvaresh1, Mohsen Molaiesiroie

2, Vahab Ghasemi

3, Abdolreza

Mir4

1Department of Accounting, Roudan Branch, Islamic Azad University,

Roudan, Iran

Email:[email protected] 2MSc in Accounting and Auditor of Senior Hormozgan Audit Court,

Hormozgan, Iran

Email: [email protected] 3Auditor of Senior Hormozgan Audit Court, Hormozgan, Iran

Email:[email protected] 4Auditor of Senior Hormozgan Audit Court, Hormozgan, Iran

Email:[email protected] Abstract:

In studying the behavior of factors influencing market and therefore market

economy, the search for the variable or variables that could explain the relationship

between the financial sector of the economy and the real sector is very important.

Money and capital markets as pillars of the financial sector are responsible for

financing the real sector. Performance of the financial sector leads to the efficient

allocation of scarce resources to economic activities. Optimal allocation of

resources, in turn, leads to efficient savings and investment and thus economic

growth close to the potential of the economy. Financial sector of the economy of

each country is the supplier of financial resources and real economic activities

which are divided into two parts:

1. Money market mainly run by the banking system of a country the most

important function of which is providing short-term credits

ISSN (2476-7018) 5931، پاییز دوازدهم، شماره سال سوم، تحقیقات جدید در علوم انسانی/ 42

2. And capital markets the main function of which is long-term financing needed in

productive activities of production and services

Keywords: Behavior of factors influencing market, market economy, efficient

savings and investment, Money market

Introduction

In studying the behavior of factors influencing market and therefore market

economy, the search for the variable or variables that could explain the relationship

between the financial sector of the economy and the real sector is very important.

Money and capital markets as pillars of the financial sector are responsible for

financing the real sector.

Performance of the financial sector leads to the efficient allocation of scarce

resources to economic activities. Optimal allocation of resources, in turn, leads to

efficient savings and investment and thus economic growth close to the potential of

the economy. Economists such as Goldsmith (1969), Miknon (1973) and Shaw

(1973) believed that financial markets have a key role in the development and

economic growth.

Statement of the problem and the need for research

Generally, regarding economic policies, economists focus on issues such as full

employment, price stability (inflation), fair distribution of income, and steady

growth of the economy. Financial sector of the economy of each country is the

supplier of financial resources and real economic activities which are divided into

two parts:

1. Money market mainly run by the banking system of a country the most

important function of which is providing short-term credits

2. And capital markets the main function of which is long-term financing needed in

productive activities of production and services (Sahmiran. 1,2007)

Stock market works within a larger system called Iran's socio-economic system. it

is therefore severely affected by the environment. This influence is considerable

because the stock market in Iran is very young and is consequently affected by

environmental changes. Therefore, factors such as economic growth, exchange

rates, profit margins of other economic activities, foreign exchange earnings, the

degree of severity of liberalization and opening up and expanding the economy of

Iran, and increasing the liquidity are important environmental factors that affect the

stock market. The tax law can also be influential as a factor along with other

factors in the development of stock market (Moshrefi, 2,2005). Economic stability

is one of the most important factors affecting investment in each country. Among

the factors having effects on the capital markets in the world, as well as on the

amount of investment involved in these markets are macroeconomic variables that

affect the volatility of stock returns. During the economic boom with relatively

stable prices, manufacturing investment is in its normal process and investors

Investing the relationship between macroeconomic indicators ……. / 41

spend money to build factories, buy equipment, and increase inventory. As a result,

economic capacity goes up regularly, causing an increase in economic efficiency (

Tafazoli,1998, 564).

The effect of stock exchange on economic growth

According to classical economic theories, if efficient sectors of economy expand,

they will be able to absorb the additional production factors from inefficient parts.

Efficient and profitable companies and projects should be first identified. With an

efficient mechanism in the capital market this can be done easily. In an economy

whose capital markets function properly, on the one hand investment volume

increases and on the other hand the quality and security of investments go up.

In such a context, it is also possible to increase economic growth. Some economic

analysts believe that the stock market and the stock exchange in developing

countries do not have a positive effect on economic growth, but evidence and

recent studies have shown that the stock market can have a profound impact on

economic growth and development. By collecting liquidity, these markets can both

provide short-term capital for financing needy units and provide long-term capital

for profitable investments. In addition to stock market, banks are also major

sources of financing. In developing countries, due to lack of knowledge of

managers about efficient tools such as stock, the bulk of capital required is

provided through the banking system, as borrowing from the banking system has

severe inflation consequences (Mushrefi. 2005)

Index of Tehran Stock Exchange and its calculation method

As Tehran Stock resumed working in 1986, the need to calculate the price index

was put in the agenda of the Tehran Stock Exchange. The price index in the stock

market was called Tepix in 1986 and has been known internationally by this name,

ever after. Tepix is an abbreviation for TEHRAN PRICE INDEX.

Following this decision, the calculation of Tehran stock exchange index started in

1989 based on the average price of shares traded during the second half of 1986. In

the beginning of the year 1989, in the formula, the number of shares traded was

replaced by the number of shares issued by companies listed on the stock

exchange. The general formula prepared by the method of weighted average index

at Tehran Stock Exchange, as well as other exchanges in the world, is the formula

below(Davani ,: 2005,11): current value of stocks issued by listed companies/ the

base value of stocks shared by listed companies*100TEPIX

Generally, stock market index reflects the overall condition of the stock market. In

advanced economies, an increase in the index means the economy is booming it

and a decrease in it shows depression. To calculate the stock price index, the latest

information about the changes in stock prices and trading volumes is required.

The basis for calculating is base year, 1997. The index shows that the total market

value has multiplied compared to the base year. Price index at Tehran Stock

Exchange is calculated for three groups, namely:

ISSN (2476-7018) 5931، پاییز دوازدهم، شماره سال سوم، تحقیقات جدید در علوم انسانی/ 42

1. General Market Price Index: in its calculation, stock price of all companies

traded is taken into account.

2. Price index of the main hall: in calculating it, only stock price of traded

companies on the main board is taken into account.

3. Price index of secondary hall: in calculating it, only stock price of traded

companies on the secondary board is taken into account (ibid, p. 117). There is not

perfect correlation between rising equity prices and the general price index. Change

percentage of common stock is usually more than the percentage change in the

general level of price index. With inflation and rising interest rates, expected rate

of return goes up and consequently, common stock price decreases.

In assessing the environment, investor should consider several factors such

inflation, interest rate, risk of return, and business risk. Inflation, instability of

profits, and rising interest rates are factors considered undesirable and reduce the

stock price.

Research objectives

The main purpose of this research is to explain the relationship between

macroeconomic indicators and efficiency of Tehran Stock Exchange indicator

Research detailed objectives

- To explain the relationship between oil price yield and indicator of Tehran Stock

Exchange

- To explain the relationship between changes in GDP and returns of indicator of

Tehran Stock Exchange

- To explain the relationship between exchange rates yield and the yield of Tehran

Stock Exchange indicator

- To explain the relationship between inflation and the yield of Tehran Stock

Exchange indicator

Research Methodology

Research methodology is deductive – inductive. In terms of purpose, the present

study is applied and in terms of data collection, it is descriptive and correlational.

Realms of time and place of the research

Subject domain: To investigate the relationship between macroeconomic indicators

and indicators of Tehran Stock Exchange

Time domain: the time domain of the research is from 2009 to 2013 (a 5-year

period).

Place domain: it contains all companies listed on the Stock Exchange of Tehran.

Research Hypotheses

The main hypothesis: there is significant relationship between macroeconomic

indicators and return of Tehran Stock Exchange index

Investing the relationship between macroeconomic indicators ……. / 42

Secondary hypotheses

H1: There is a significant relationship between oil price and return of Tehran Stock

Exchange index.

H2: there is a significant relationship between changes in GDP and return of

Tehran Stock Exchange index.

H3: there is a significant relationship between the exchange rate yield and return of

Tehran Stock Exchange index

H 4: there is a significant relationship between inflation and return of Tehran Stock

Exchange index

Research variables and the method of measuring them

The relationship examined in this study is the following relationship:

Where,

In=inflation

OI= oil

GDP= gross domestic product

EX= exchange rate

Alpha and beta are the regression coefficients. Correlation coefficient is the best

criterion for diagnosis of relation between two or more variables and it is the

expression of strength or weakness. If the correlation is between two variables, it is

simple correlation and if it is between more than two variables, it is multivariable

correlation.

Kolmogorov-Smirnov test

Kolmogorov-Smirnov test is a simple non-parametric method to determine the

homogeneity of the experimental data with selected statistical distribution shown

2008, p. 310). Kolmogorov - Smirnov is a

correspondence of distribution test for quantity data. Using this test, it can be found

out whether sample data have a special theoretical distribution.

ed to compare four different distributions:

normal, Poisson, exponential, and uniform. The null distribution of this statistic is

calculated under the null hypothesis that the sample is drawn from the reference

distribution (in the one-sample case) or that the samples are drawn from the same

distribution (in the two-sample case). In each case, the distributions considered

under the null hypothesis are continuous distributions but are otherwise

n. If the test statistic is less than

the value in the table, the null hypothesis is confirmed. Otherwise, it is rejected.

The test statistic is obtained through the formula below:

oen FFMaximumD

ISSN (2476-7018) 5931، پاییز دوازدهم، شماره سال سوم، تحقیقات جدید در علوم انسانی/ 42

Correlation coefficient

In this study, regression and analysis of variance were used to test the hypotheses.

According to what was said earlier, the number of observations is more than 30 and

based on the central limit theorem data can be assumed normal. Therefore, t

distribution is used for testing the hypotheses and F is used for general

confirmation. Correlation coefficient is the best measure for the relationship

between two or more variables. If the correlation is between two variables, it is

simple correlation and if it is between more than two variables, it is multivariable

correlation. For calculating Pearson correlation coefficient, if the variables are

integers, the following formula is used:

R represents the linear relationship between x and y is, and its sign indicates the

direction of this relationship. The couple may be variables with strong relationship

without necessarily being linear. In this case, r is not an appropriate measure. In the

following, a table for linearity of the relationship between x and y is seen.

H0:β1=0 the existence of linear relationship

H1: β1=0 no linear relationship

The test of significance of coefficient correlation

The question that arises is that whether the correlation between the variables x and

y is significant or not? or whether the existence of a linear causal relationship can

be proven or the coefficient correlation has been obtained by chance and

correlation coefficient, shown as P, is equal to zero.

To test the correlation between two random variables x and y or to simply test

whether the correlation coefficient is zero or not, we need a proper statistic. This

statistic testing the correlation coefficient of zero with a distribution t and degrees

of freedom of n-2 is as follows:

With the following hypotheses:

If the statistic is in critical area, null hypothesis can-not be rejected and the

correlation coefficient obtained is not significant. If it is in critical area, H1 is

confirmed and the existence of a correlation is proven. Based on the results

obtained by SPSS software:

If p-value >0.05, the results are not significant.

If 0.01≤ p-value ≤0.05, the results are significant.

If 0.001≤ p-value ≤0.01, the results are highly significant.

If p-value ≤0.001, the results are highly significant.

Investing the relationship between macroeconomic indicators ……. / 43

Degree of freedom is obtained from n-2 formula, where n is the number of

observations.

Data analysis

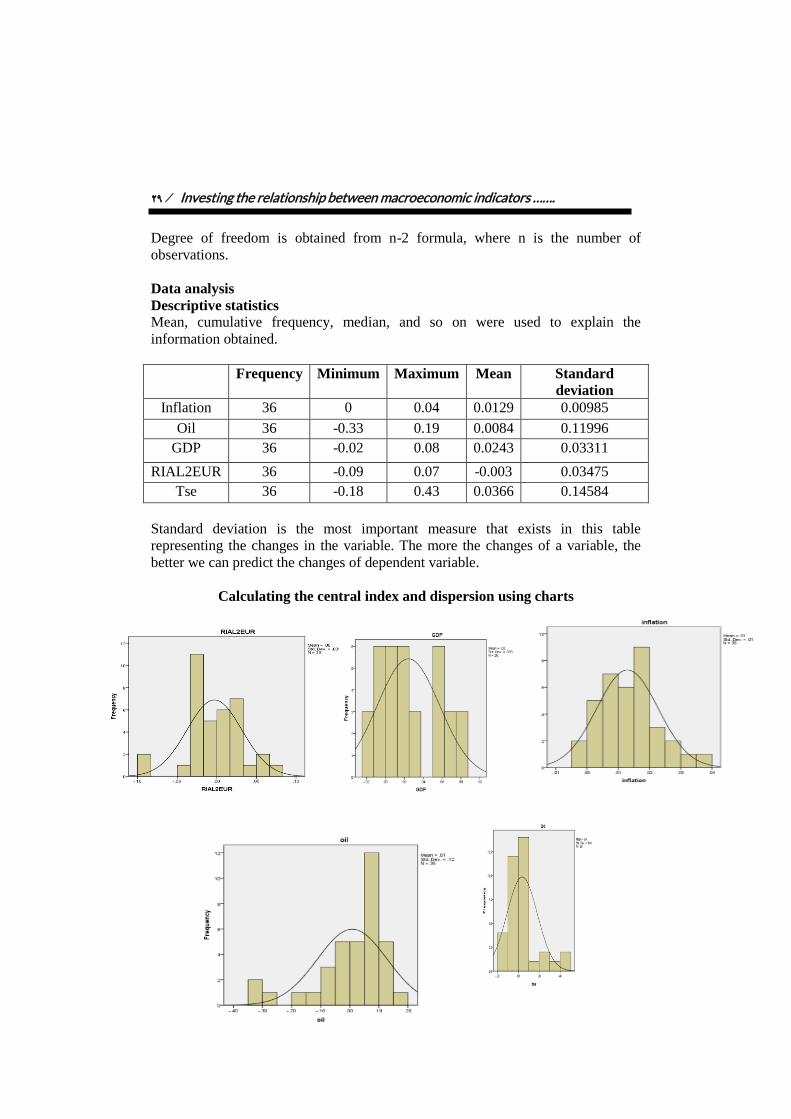

Descriptive statistics

Mean, cumulative frequency, median, and so on were used to explain the

information obtained.

Frequency Minimum Maximum Mean Standard

deviation

Inflation 36 0 0.04 0.0129 0.00985

Oil 36 -0.33 0.19 0.0084 0.11996

GDP 36 -0.02 0.08 0.0243 0.03311

RIAL2EUR 36 -0.09 0.07 -0.003 0.03475

Tse 36 -0.18 0.43 0.0366 0.14584

Standard deviation is the most important measure that exists in this table

representing the changes in the variable. The more the changes of a variable, the

better we can predict the changes of dependent variable.

Calculating the central index and dispersion using charts

ISSN (2476-7018) 5931، پاییز دوازدهم، شماره سال سوم، تحقیقات جدید در علوم انسانی/ 93

Regression defaults

The result is an output representing the number of data, the parameters in the

presence of distribution, and the absolute value of the maximum deviation,

maximum positive deviation, the largest negative deviation, value of Z, and the

value of sig.

As sig. is under 5%, H0 is rejected and normality is not confirmed. If it is over 55,

it is normal. The results of this table show all the variables are normal.

Table 1: Kolmogorov-Smirnov test

inflation Oil GDP RIAL2EUR Tse

Kolmogorov-

Smirnov Z

0.635 0.914 0.958 0.779 1.176

Asymp. Sig. (2-

tailed)

0.815 0.373 0.318 0.579 0.126

One of the assumptions considered in regression is the independence of errors (the

difference between actual and predicted values using a regression model) from

each other. If the assumption of the independence of errors is rejected and errors

are correlated with each other, regression can-not be used. To achieve this

important aim, Durbin-Watson test can be used.

Linearity is a situation in which an independent variable is a function of other

independent variables.

If linearity in a regression equation is high, it means there is a strong correlation

between the independent variables.

The less the tolerance (the closer it is to zero), the more problems there are for

using regression. The variance inflation factor acts reversely. The higher it is, the

higher the variance of regression coefficients and the less appropriate the

regression for predicting.

Table 3: collinearity test

Model

Collinearity Statistics

Tolerance VIF

2 (Constant)

Oil .906 1.103

inflation .818 1.223

Model Summaryc

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate Durbin-Watson

2 1.000b 1.000 1.000 .00320 2.296

Investing the relationship between macroeconomic indicators ……. / 95

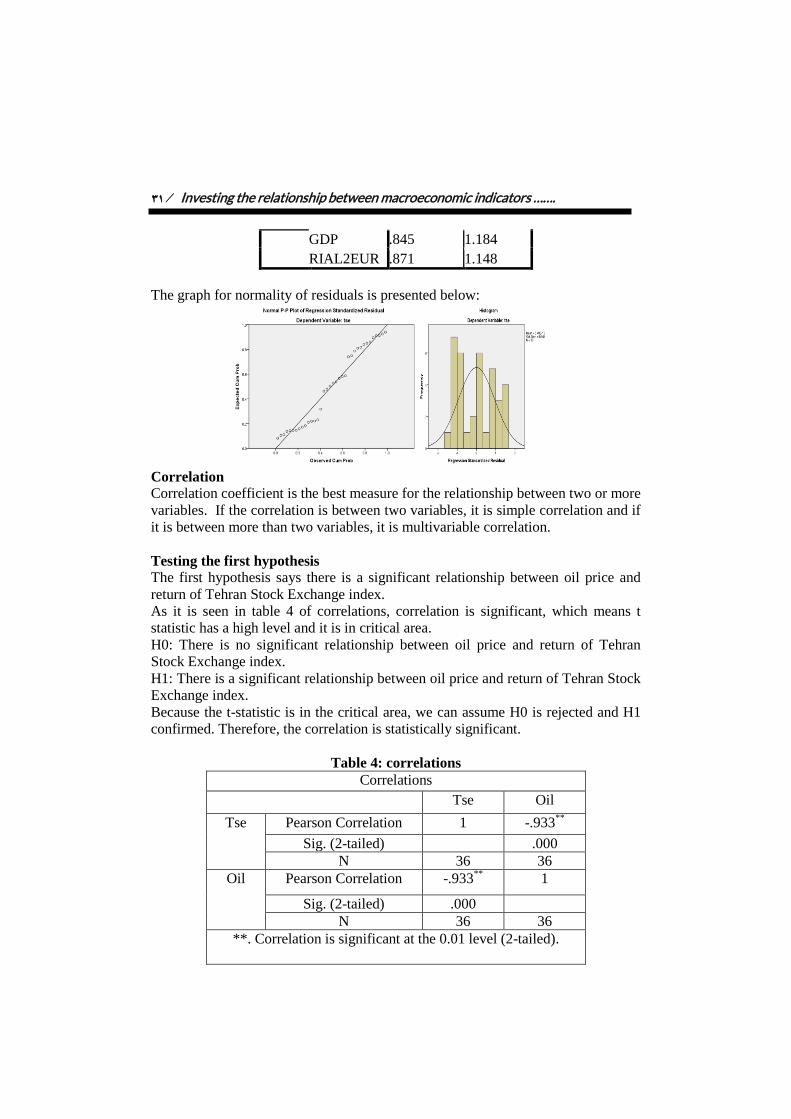

GDP .845 1.184

RIAL2EUR .871 1.148

The graph for normality of residuals is presented below:

Correlation

Correlation coefficient is the best measure for the relationship between two or more

variables. If the correlation is between two variables, it is simple correlation and if

it is between more than two variables, it is multivariable correlation.

Testing the first hypothesis

The first hypothesis says there is a significant relationship between oil price and

return of Tehran Stock Exchange index.

As it is seen in table 4 of correlations, correlation is significant, which means t

statistic has a high level and it is in critical area.

H0: There is no significant relationship between oil price and return of Tehran

Stock Exchange index.

H1: There is a significant relationship between oil price and return of Tehran Stock

Exchange index.

Because the t-statistic is in the critical area, we can assume H0 is rejected and H1

confirmed. Therefore, the correlation is statistically significant.

Table 4: correlations

Correlations

Tse Oil

Tse Pearson Correlation 1 -.933**

Sig. (2-tailed) .000

N 36 36

Oil Pearson Correlation -.933**

1

Sig. (2-tailed) .000

N 36 36

**. Correlation is significant at the 0.01 level (2-tailed).

ISSN (2476-7018) 5931، پاییز دوازدهم، شماره سال سوم، تحقیقات جدید در علوم انسانی/ 94

Testing the second hypothesis

The second hypothesis states there is a significant relationship between changes in

GDP and return of Tehran Stock Exchange index.

As it is seen in table 5 of correlations, correlation is not significant, which means t

statistic does not have a high level and it is not in critical area.

H0: there is no significant relationship between changes in GDP and return of

Tehran Stock Exchange index.

H1: there is a significant relationship between changes in GDP and return of

Tehran Stock Exchange index.

Because the t-statistic is not in the critical area, we can assume H0 is confirmed

and H1 is rejected. Therefore, the correlation is not statistically significant.

Table 5: correlations

Correlations

Tse GDP

Tse Pearson

Correlation

1 .318

Sig. (2-tailed) .059

N 36 36

GDP Pearson

Correlation

.318 1

Sig. (2-tailed) .059

N 36 36

Testing the third hypothesis

The third hypothesis states there is a significant relationship between the exchange

rate yield and return of Tehran Stock Exchange index.

As it is seen in table 6 of correlations, correlation is not significant, which means t

statistic does not have a high level and it is not in critical area.

H0: there is no significant relationship between the exchange rate yield and return

of Tehran Stock Exchange index

H1: there is a significant relationship between the exchange rate yield and return of

Tehran Stock Exchange index

Because the t-statistic is not in the critical area, we can assume H0 is confirmed

and H1 is rejected. Therefore, the correlation is not statistically significant.

Table 6: correlations

Correlations

tse RIAL2EUR

Tse

Pearson Correlation 1 .048

Sig. (2-tailed) .783

N 36 36

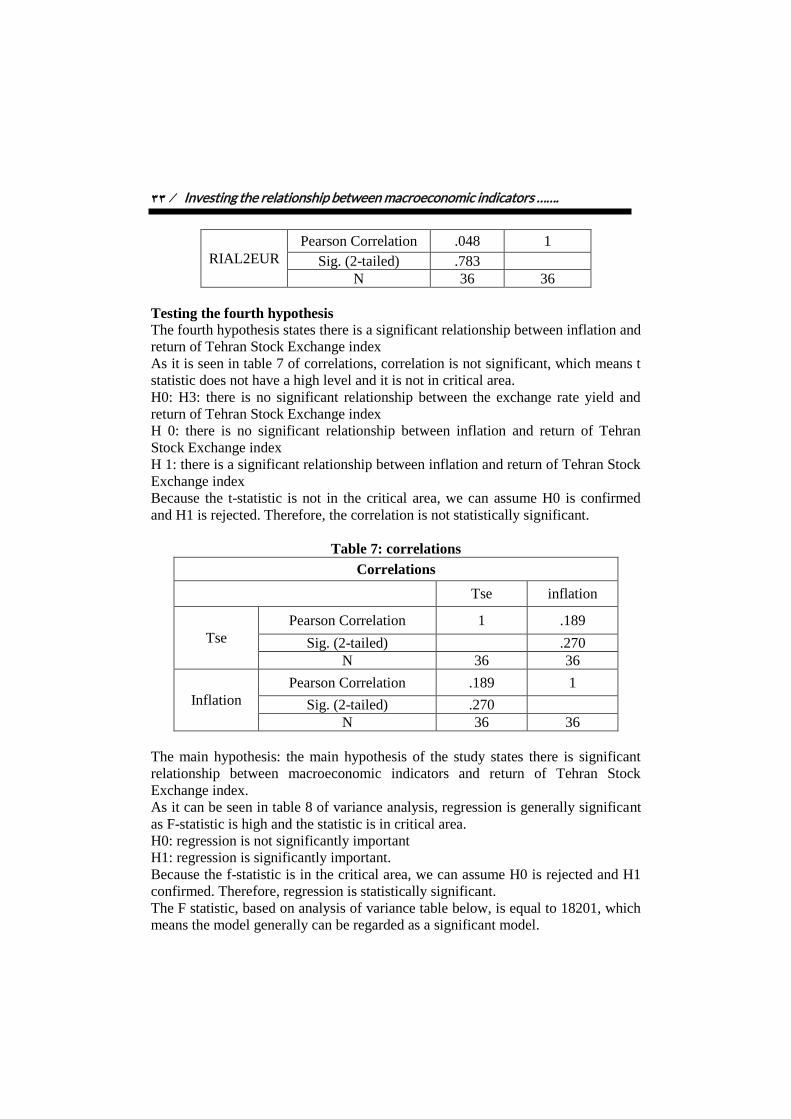

Investing the relationship between macroeconomic indicators ……. / 99

RIAL2EUR

Pearson Correlation .048 1

Sig. (2-tailed) .783

N 36 36

Testing the fourth hypothesis

The fourth hypothesis states there is a significant relationship between inflation and

return of Tehran Stock Exchange index

As it is seen in table 7 of correlations, correlation is not significant, which means t

statistic does not have a high level and it is not in critical area.

H0: H3: there is no significant relationship between the exchange rate yield and

return of Tehran Stock Exchange index

H 0: there is no significant relationship between inflation and return of Tehran

Stock Exchange index

H 1: there is a significant relationship between inflation and return of Tehran Stock

Exchange index

Because the t-statistic is not in the critical area, we can assume H0 is confirmed

and H1 is rejected. Therefore, the correlation is not statistically significant.

Table 7: correlations

Correlations

Tse inflation

Tse

Pearson Correlation 1 .189

Sig. (2-tailed) .270

N 36 36

Inflation

Pearson Correlation .189 1

Sig. (2-tailed) .270

N 36 36

The main hypothesis: the main hypothesis of the study states there is significant

relationship between macroeconomic indicators and return of Tehran Stock

Exchange index.

As it can be seen in table 8 of variance analysis, regression is generally significant

as F-statistic is high and the statistic is in critical area.

H0: regression is not significantly important

H1: regression is significantly important.

Because the f-statistic is in the critical area, we can assume H0 is rejected and H1

confirmed. Therefore, regression is statistically significant.

The F statistic, based on analysis of variance table below, is equal to 18201, which

means the model generally can be regarded as a significant model.

ISSN (2476-7018) 5931، پاییز دوازدهم، شماره سال سوم، تحقیقات جدید در علوم انسانی/ 92

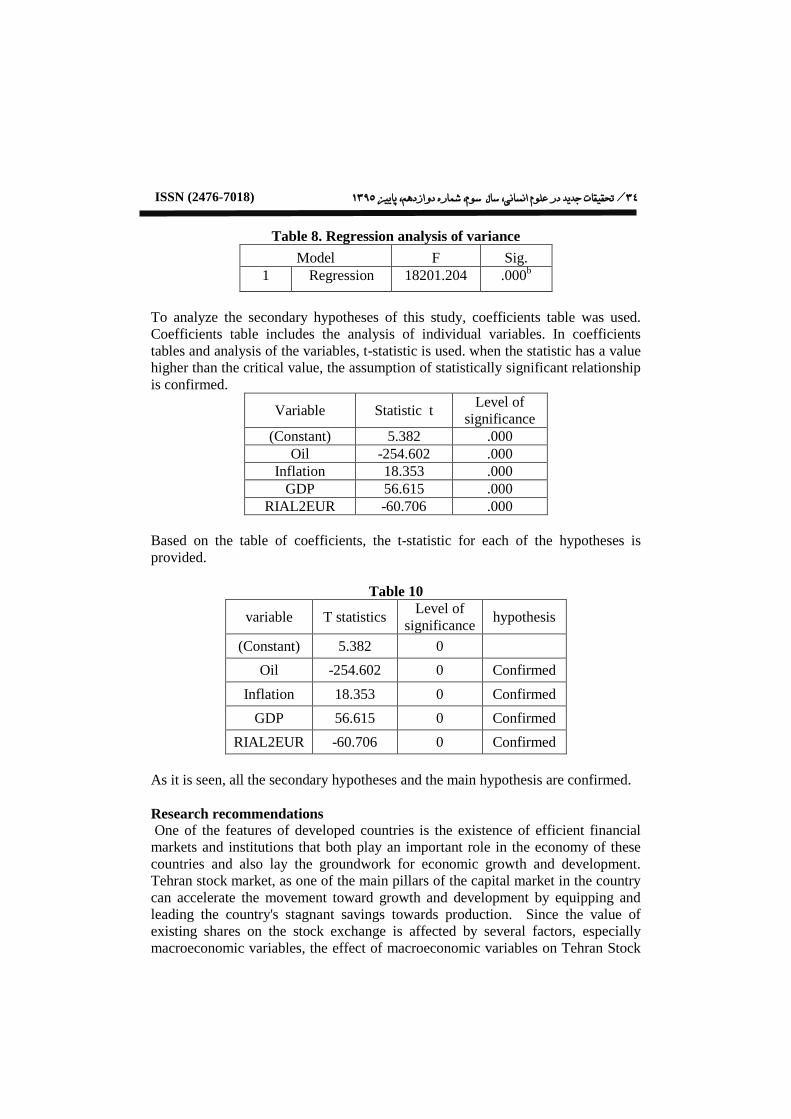

Table 8. Regression analysis of variance

Model F Sig.

1 Regression 18201.204 .000b

To analyze the secondary hypotheses of this study, coefficients table was used.

Coefficients table includes the analysis of individual variables. In coefficients

tables and analysis of the variables, t-statistic is used. when the statistic has a value

higher than the critical value, the assumption of statistically significant relationship

is confirmed.

Variable Statistic t Level of

significance

(Constant) 5.382 .000

Oil -254.602 .000

Inflation 18.353 .000

GDP 56.615 .000

RIAL2EUR -60.706 .000

Based on the table of coefficients, the t-statistic for each of the hypotheses is

provided.

Table 10

variable T statistics Level of

significance hypothesis

(Constant) 5.382 0

Oil -254.602 0 Confirmed

Inflation 18.353 0 Confirmed

GDP 56.615 0 Confirmed

RIAL2EUR -60.706 0 Confirmed

As it is seen, all the secondary hypotheses and the main hypothesis are confirmed.

Research recommendations

One of the features of developed countries is the existence of efficient financial

markets and institutions that both play an important role in the economy of these

countries and also lay the groundwork for economic growth and development.

Tehran stock market, as one of the main pillars of the capital market in the country

can accelerate the movement toward growth and development by equipping and

leading the country's stagnant savings towards production. Since the value of

existing shares on the stock exchange is affected by several factors, especially

macroeconomic variables, the effect of macroeconomic variables on Tehran Stock

Investing the relationship between macroeconomic indicators ……. / 91

Exchange Index has been examined in this work. The results generally show a

relationship between macroeconomic indicators and indicators of Tehran Stock

Exchange. Therefore, it can be concluded that the model is efficient. The model

can be found below, based on statistical analysis and its results:

References

1. Sakaran, Omaa, research methods in management, translation: Mohammad

Saeb and Mahmoud Shirazi, Tehran, Institute of Research Management

and Planning, Second Edition, 2002, p. 532.

2. Delavar, Ali, Research Methods in Psychology and Education (Science

Education), Tehran, PNU, 2003, p. 366

3. Taheri, A., Research Methodology and Bibliography (Administration),

Tehran, PNU, 1999, p. 164

4. Khaki Sadegh, Seyed Reza Seyed Nezhad Fahim, Mojtaba Maleki

Chubari. (1997) the role of operational items in the cash flow statement

explaining the stock returns of companies listed on the Stock Exchange;

Quarterly Survey of accounting and auditing.

5. Soofiani, Azam. (2005). Investigating the relationship between capital

structure and EVA. Alzahra University.

6. Adib Lida (2003) investigating long-term relationship between stock

prices, inflation, and economic growth by using the VAR and ECM

patterns. Master's thesis. University of Alzahra.

7. Shah Rezaei, Mahmoud. (2002) the effect of financial ratios adjusted for

the effects of inflation based on the decisions of users of financial

information. Master's thesis. University of Tehran.

8. Tabibi, M. (2001). Forecasting inflation in Iranian economy. Master's

thesis. Shahid Beheshti University.

9. Ghaffari, N. (2005). Effects of long-run equilibrium relationship between

exchange rate and inflation on the financial and industrial indices in

Tehran Stock Exchange. Master's thesis. Al-Zahra University.

10. Ghavami, Hadi. (2003) investigating the structural changes in employment,

unemployment, and inflation factors affecting it and its relationship with

Iran. PhD thesis. Tarbiat Modares University.

ISSN (2476-7018) 5931، پاییز دوازدهم، شماره سال سوم، تحقیقات جدید در علوم انسانی/ 92

11. Mufti, Shadi. (2003) investigating the effect of exchange rate and inflation

on the pattern of exports and imports over the period 1350-1378. Master's

thesis. Al-Zahra University.

12. Balduzzi, Pierluingi, Stock Return inflation and the proxy hypothesis: A

new look at the data. Economics letters No48 1995,P.47-53

13. Boudoukh,J.,Richardson,M,1993.Stock returns and inflation: a long

horizon perspective. American Economic Review 83, 1346-1355.

14. Choudhry, T2001. Inflation and rates of return on stocks: evidence from

high inflation countries. Journal of International Financial Markets,

Institution &Money 11, 75-96

15. Engsted, T., Tanggaard,C., 2002. The relation between asset returns and

inflation at 16-short and long horizons. Journal of International Financial

Markets, Institutions &Money 12, 101-118

16. Evgene . F. Fama. Stock Returns, Real Activity, inflation and Money.

American Economic Review, Sep 1981.PP. 545-564

17. Fama,E.F.,Schwert,G.W.,1977.Stock market returns and inflation .Journal

of Financial Economics5, 115-146

18. Groene wold, Rolke,G,and Thomas .Stock returns and inflation :a macro

analysis .Applied financial economics 1992,No 7 , P127-136

19. Gultekin, N. Bulent . Stock Market Returns and Inflation :Evidence from

other countries .Journal of finance , No 38 march 1983, P.49-65

20. Solnik, B.,Solnik, V.,19997.Amulti-contry test of the Fisher model for

stock returns.Journal of International Financial Markets, Institution &

Money 7, 289-30

21. N. Bulent Gultekin, “Stock Market Returns and Inflation Evidence From

Other Countries”, The Journal of Finance, March 1983.

22. Bruno Solnik, “The Relation between Stock Prices and Inflationary

Exceptions; The International Evidence”, The Journal of Finance, March

1983.

23. Lev, B. (1974).Financial Statement Analysis: A New Approach. First

Edition, New Jersy, Engelwood Cliffs: Prentic Hall.

24. Marshall, Alfred.(1890). Principles of Economics . New York: MacMillan

& Co. Vol. 1,p. 142

Investing the relationship between macroeconomic indicators ……. / 92

25. Morely, KE (1988). The new organizational wealth: managing and

measuring knowledge based assets. Berret Koehler, San Francisco.

26. Tully, Shawn.(1993). “The Real Key to Creating Wealth,” Fortune,

September 20.

27. Weygandt , Jerry J., Paul D. Kimmel and Donald E. Kieso Financial

Accounting (2009) .John Wiley and Sons Vernon Kam.(1990). Accounting

theory. Wiley

28. Yook C. Kenneth and George M. McCabe. (2001) , “An Examination of

MVA in the Cross-Section of Expected Stock Returns, Journal of Portfolio

Management.