international standard serial number (issn): 2319 …. rp13140018520014.pdfinternational journal of...

TRANSCRIPT

International Standard Serial Number (ISSN): 2319-8141 International Journal of Universal Pharmacy and Bio Sciences 2(5): September-October 2013

INTERNATIONAL JOURNAL OF UNIVERSAL

PHARMACY AND BIO SCIENCES IMPACT FACTOR 1.89***

ICV 2.40*** Pharmaceutical Sciences REVIEW ARTICLE……!!!

Received: 03-09-2013; Accepted: 06-09-2013

PHARMACEUTICAL DISTRIBUTION IN INDIA

P.Parveen*, P.Usha, V.Vasu naik, Rajesh Akki

Hindu college of Pharmacy.Amaravathi road Guntur-522002.

KEYWORDS:

Drug Price Control Order

(DPCO), Indian

Pharmaceutical Industry,

Compounded Annual

Growth Rate (CAGR).

For Correspondence:

P.Parveen*

Address:

Hindu college of

Pharmacy.Amaravathi

road Guntur-522002.

Email:

pothukantiparveen@gmai

l.com

ABSTRACT

It is often said that the pharma sector has no cyclical factor attached

to it. Irrespective of whether the economy is in a downturn or in an

upturn, the general belief is that demand for drugs is likely to grow

steadily over the long-term. The Indian pharmaceutical industry is

fragmented, but has grown rapidly due to friendly patent regime and

low cost manufacturing structure. Intense competition, high volumes

and low prices characterize the Indian domestic market. Exports have

been raising at around 30% Compounded Annual Growth Rate

(CAGR) over last few years. There is a shift in export profile towards

value added formulations from low value bulk drugs. The drug

pricing control order (DPCO) has been mile stone around the neck of

Indian industry as its severely restricted profitability and innovation.

My study focuses on the processes and outcomes of globally

distributed pharmaceutical companies. This article will present the

changing marketing strategies when a pharma company shifts from

Acute base to Chronic therapy base.

070 Full Text Available On www.ijupbs.com

International Standard Serial Number (ISSN): 2319-8141

INTRODUCTION:

INDIAN PHARMACEUTICAL MARKET

Pharmaceutical companies in India both Indian and foreign, manufacture bulk drugs in several

therapeutic categories and the industry has facilities to manufacture various types of dosage namely

capsule, tablets, injectables, orals, and liquids. Of the 400 bulk drugs in the Indian market, it is

estimated that 300 are domestically produced. Moreover, India is emerging as the most favoured

destinations for collaborative Research & Development bioinformatics, contract research and

manufacturing and clinical research as a result of growing compliance with internationally

harmonized standards such as Good Laboratory Practices (GLP), current Good

Manufacturing Practices (cGMP) and Good Clinical Practices (GCP).

Factors contributing to the growth of the Pharmaceutical Market:

India today has the distinction of producing high quality generic medicines that are sold around the

world. Further, India is poised to be one of the fastest growing pharmaceutical markets in the world.

The following factors have fuelled the growth for the drugs and pharmaceutical market:

The growing population of over a billion

A huge patient base

Increasing incomes

Improving healthcare infrastructure

An increase in lifestyle-related diseases such as diabetes, cardiovascular

diseases, and central nervous system

Penetration of health insurance

Adoption of patented products

Patent expiries and aging population in the US, Europe, and Japan.

The following challenges faced by the global pharmaceutical industry also open up a number of

opportunities for the Indian Pharmaceutical Industry:

higher healthcare costs

competition from generics

patent expiries of blockbuster drugs

drying R&D pipelines

increasing R&D costs.

This offers immense growth opportunity for the Indian Pharmaceutical Industry in the following

segments:

Bulk-drugs

Domestic formulations.

071 Full Text Available On www.ijupbs.com

International Standard Serial Number (ISSN): 2319-8141

Exports to non regulated markets

CRAMS

Exports of generics to regulated markets

NCE research for global pharmaceutical companies

Key Characteristics of the Indian Pharma Sector:

The Indian pharmaceutical market is marked by the following significant features:

Self-reliance displayed by the production of 70% of bulk drugs and almost the entire

requirement of formulations within the country;

Low cost of production;

Low R&D costs;

Innovative Scientific Manpower;

Excellent and world-class national laboratories specializing in process

development and development of cost effective technologies;

Increasing balance of trade in pharma sector;

An efficient and cost effective source for procuring generic drugs

especially the drugs going off patent in the next few years;

An excellent centre for clinical trials in view of the diversity in population

Laws and Regulations governing Indian Pharmaceuticals:

The Drugs and Cosmetics Act, 1940: This Act regulates the import, manufacture, distribution and

sale of drugs in India.

The Pharmacy Act, 1948: This legislation regulates the profession of Pharmacy in India. Under the

provisions of this act the Central Government constitutes a Central Pharmacy Council of India and

the State Governments constitute State Pharmacy Councils.

The Drugs Price Control Order (DPCO), 1995: This is an order issued by the Government of

India under the Essential Commodities Act, 1955 to regulate the ,prices of drugs. The Order

provides the list of price controlled drugs, procedures for fixation of prices of drugs, method of

implementation of prices fixed by Government and penalties for contravention of provisions among

other things.

For the purpose of implementing provisions of DPCO, powers of the Government have been vested

in the National Pharmaceutical Pricing Authority (NPPA).

Regulatory Bodies:

The Ministry of Health & Family Welfare (MoHFW) and the Ministry of Chemicals and Fertilisers

(MoC&F) of the Government of India play a major role in regulating the pharmaceutical sector in

the country.

072 Full Text Available On www.ijupbs.com

International Standard Serial Number (ISSN): 2319-8141

Drug Application Procedures:

Foreign pharmaceutical firms looking to export drugs to India must first obtain a license from the

Drugs Controller of India (DCI) which is granted upon assurance that the firm's manufacturer abroad

complies with Indian production and safety standards. Prior to the release of any drugs for import

into India, the importer must submit the following documents to the Central Drug Control

Organization:

documents of import (Bills of Entry),

protocols test and analysis,

a sample of the product(s) label, and

a drug sample

Companies looking to manufacture drugs locally must go through a "preparatory" or Pre-Licensing

Phase to show that their manufacturing facilities are up to standard. After being granted a license,

the manufacturer must also produce a test batch of drugs that is approved by the government for

safety. All companies must also follow specific labeling requirements. Pharmaceutical companies

must have their label and pack insert approved by

the DCI before the drug is marketed.

Pharmaceutical Registration:

To register a new drug in India, a New Drug Application must be submitted to the regulatory

authority Drugs Controller General of India, along with the documents such as details of the drug's

regulatory status in other countries; restrictions of use in approved countries; a free sale certificate

from the country of origin; results of clinical data based on approved protocol; published data of

confirmatory Phase III trials undertaken abroad; details of bio-availability and

dissolution studies; a sample of the marketing information, including draft labels and cartons and

inserts; a sample of the pure drug substance along with testing protocol for analysis at the Central

Drugs Laboratory (CDL) Generally, local Phase III clinical trials are required for the registration

and marketing approval of all new drugs in India. According to the industry, drug registration can

take 12-18 months, longer time if delays are encountered. Decisions on fast track approvals for

drugs are on the basis of demand for the drug and in public interest.

Pharmaceutical Clusters:

Andhra Pradesh, Gujarat, Maharashtra and Goa are the major pharmaceutical manufacturing clusters

in the country.

The bulk drug clusters are located primarily in the following regions:

Gujarat - Ahmedabad, Ankleshwar, Vapi, Vadodara

Maharashtra - Mumbai, Tarapur, Aurangabad, Pune.

073 Full Text Available On www.ijupbs.com

International Standard Serial Number (ISSN): 2319-8141

Andhra Pradesh - Hyderabad, Medak

Tamil Nadu – Chennai, Pondicherry

Karnataka - Mysore, Bangalore, Goa

Visakhapatnam (Vizag) in Andhra Pradesh is the upcoming bulk drug cluster that has generated

significant interest in the APIs players.

The captive R&D Units are located in the following regions:

National Capital Region

Ahmedabad

Mumbai

Aurangabad

Hyderabad

Bangalore

Chennai

Key Research Institutes:

Central Drug Research Institute (CDRI), Lucknow.

National Institute of Pharmaceutical Education & Research (NIPER), Mohali.

Indian Institute of Chemical Technology (IICT), Hyderabad.

Centre for Cell & Molecular Biology (CCMB), Hyderabad.

Indian Institute of Chemical Biology (IICB), Kolkata.

Indian Toxicology Research Institute (ITRI), Lucknow.

Institute of Genomic and Integrated Biology (IGIB), New Delhi.

Institute of Microbial Technology (IMTECH), Chandigarh

National Chemical Laboratory (NCL), Pune .

National Centre for Biological Sciences (NCBS), Bangalore.

Jawaharlal Nehru Centre for Advanced Scientific Research (JNCASR), Bangalore.

Centre for DNA Fingerprinting and Diagnostics (CDFD), Hyderabad

Indian Institute of Science (IISc), Bangalore.

National Institute of Immunology (NII), New Delhi.

The Indian pharmaceutical industry is continuing its high growth rate at 13% for the last six years.

From foreign control, to domestic grass-roots growth, the Indian pharmaceutical segment has

evolved over the last three decades.

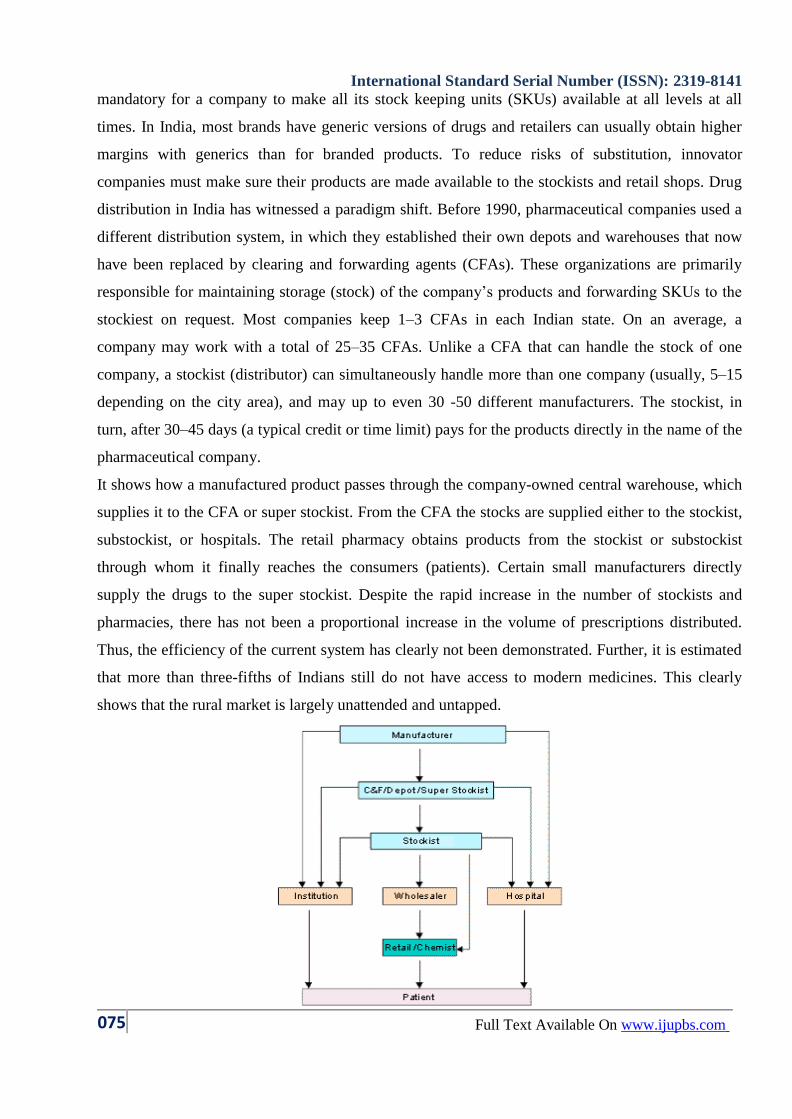

Indian distribution system: The Current State

India is a geographically diverse country with extreme climates that make distribution a critical

function. The long channel of distribution and high incidence of brand substitution makes it

074 Full Text Available On www.ijupbs.com

International Standard Serial Number (ISSN): 2319-8141

mandatory for a company to make all its stock keeping units (SKUs) available at all levels at all

times. In India, most brands have generic versions of drugs and retailers can usually obtain higher

margins with generics than for branded products. To reduce risks of substitution, innovator

companies must make sure their products are made available to the stockists and retail shops. Drug

distribution in India has witnessed a paradigm shift. Before 1990, pharmaceutical companies used a

different distribution system, in which they established their own depots and warehouses that now

have been replaced by clearing and forwarding agents (CFAs). These organizations are primarily

responsible for maintaining storage (stock) of the company‟s products and forwarding SKUs to the

stockiest on request. Most companies keep 1–3 CFAs in each Indian state. On an average, a

company may work with a total of 25–35 CFAs. Unlike a CFA that can handle the stock of one

company, a stockist (distributor) can simultaneously handle more than one company (usually, 5–15

depending on the city area), and may up to even 30 -50 different manufacturers. The stockist, in

turn, after 30–45 days (a typical credit or time limit) pays for the products directly in the name of the

pharmaceutical company.

It shows how a manufactured product passes through the company-owned central warehouse, which

supplies it to the CFA or super stockist. From the CFA the stocks are supplied either to the stockist,

substockist, or hospitals. The retail pharmacy obtains products from the stockist or substockist

through whom it finally reaches the consumers (patients). Certain small manufacturers directly

supply the drugs to the super stockist. Despite the rapid increase in the number of stockists and

pharmacies, there has not been a proportional increase in the volume of prescriptions distributed.

Thus, the efficiency of the current system has clearly not been demonstrated. Further, it is estimated

that more than three-fifths of Indians still do not have access to modern medicines. This clearly

shows that the rural market is largely unattended and untapped.

075 Full Text Available On www.ijupbs.com

International Standard Serial Number (ISSN): 2319-8141

DIAGNOSIS OF INDIAN PHARMA INDUSTRY

The SWOT analysis of the industry reveals the position of the Indian pharma industry in respect to

its internal and external environment.

Strengths

Indian with a population of over a billion is a largely untapped market. In fact the penetration of

modern medicine is less than 30% in India. To put things in perspective, per capital expenditure on

health care in India is US$ 93 while the same for countries like Brazil is US$ 453 and Malaysia

US$189. The growth of middle class in the country has resulted in fast changing lifestyles in urban

and to some extent rural centers. This opens a huge market for lifestyle drugs, which has a very low

contribution in the Indian markets. Indian manufacturers are one of the lowest cost producers of

drugs in the world. With a scalable labor force, Indian manufactures can produce drugs at 40% to

50% of the cost to the rest of the world. In some cases, this cost is as low as 90%. Indian

pharmaceutical industry posses excellent chemistry and process reengineering skills. This adds to

the competitive advantage of the Indian companies. The strength in chemistry skill help Indian

companies to develop processes, which are cost

effective.

Weakness

1. The Indian pharma companies are marred by the price regulation. Over a period of time, this

regulation has reduced the pricing ability of companies. The NPPA (National Pharma Pricing

Authority), which is the authority to decide the various pricing parameters, sets prices of different

drugs, which leads to lower profitability for the companies. The companies, which are lowest cost

producers, are at advantage while those who cannot produce have either to stop production or bear

losses.

2. Indian pharma sector has been marred by lack of product patent, which prevents global pharma

companies to introduce new drugs in the country and discourages innovation and drug discovery.

But this has provided an upper hand to the Indian pharma companies.

3. Indian pharma market is one of the least penetrated in the world. However, growth has been slow

to come by. As a result, Indian majors are relying on exports for growth. To put things in to

perspective, India accounts for almost 16% of the world population while the total size of industry is

just 1% of the global pharma industry.

4. Due to very low barriers to entry, Indian pharma industry is highly fragmented with about 300

large manufacturing units and about 18,000 small units spread across the country. This makes Indian

pharma market increasingly competitive.

076 Full Text Available On www.ijupbs.com

International Standard Serial Number (ISSN): 2319-8141

The industry witnesses price competition, which reduces the growth of the industry in value term.

To put things in perspective, the industry actually grew by 10.4% but due to price competition, the

growth in value terms was 8.2% (prices actually declined by 2.2%)

Opportunities

1. The migration into a product patent based regime is likely to transform industry fortunes in the

long term. The new patent product regime will bring with it new innovative drugs. This will increase

the profitability of MNC pharma companies and will force domestic pharma companies to focus

more on R&D. This migration could result in consolidation as well. Very small players may not be

able to cope up with the challenging environment and may succumb to giants.

2. Large number of drugs going off-patent in Europe and in the US offers a big opportunity for the

Indian companies to capture this market. Since generic drugs are commodities by nature, Indian

producers have the competitive advantage, as they are the lowest cost producers of drugs in the

world.

3. Opening up of health insurance sector and the expected growth in per capita income are key

growth drivers from a long-term perspective. This leads to the expansion of healthcare industry of

which pharma industry is an integral part.

4. Being the lowest cost producer combined with FDA approved plants, Indian companies can

become a global outsourcing hub for pharmaceutical products.

Threats

1. There are certain concerns over the patent regime regarding its current structure. It might be

possible that the new government may change certain provisions of the patent act formulated by the

preceding government.

2. Threats from other low cost countries like China and Israel exist. However, on the quality front,

India is better placed relative to China. So, differentiation in the contract manufacturing side may

wane.

3. The short-term threat for the pharma industry is the uncertainty regarding the implementation of

VAT. Though this is likely to have a negative impact in the short-term, the implications over the

long-term are positive for the industry.

CHALLENGES AHEAD

As pharmaceuticals require great handling care during storage and transportation, the demand for

temperature-controlled transport in particular will continue to grow substantially in the coming

years.While the growing demand for temperature- sensitive freight transport has spurred an

opportunity f or logistics providers, the market poses various challenges. The foremost is the dearth

of time-bound and temperature-sensitive services from the point of origin to the point of

077 Full Text Available On www.ijupbs.com

International Standard Serial Number (ISSN): 2319-8141

consumption. In addition, India's cold-chain market is still developing and is further marred with

low capacity utilization. Another bottleneck is created by the lack of modern transport infrastructure

and the delay in customs clearance in India. In order to compensate for these hurdles, logistics

service players in India will need to improve their performance in various areas by providing cost-

effective, customized packaging services and expertise in handling pharmaceutical cargo. In addition

to this the following are some important issues to be focused by the industry.

Research & Development

Currently, however, the industry's R&D pipeline is relatively sparse, with few potential blockbuster

products, that represent the industry's primary source of growth, in view. This has led to some

consolidation within the industry with many key industry players purchasing either existing product

lines or biotech firms with a few products in the later stages of development, rather than relying

exclusively on their own R&D operations. The mainstay of the pharmaceutical industry's long-term

competitiveness is its ability to pay for Research & Development. Pharma R&D is extremely costly

and has a high failure rate, even at the later testing stage. The time taken to develop a new drug

varies, but recent evidence suggests the average is around 12 years. It has also led to a process of

concentration of R&D in the US, the fastest-growing pharmaceutical market. However, the pharma

industry is faced with stakeholders such as pressure groups, NGOs and international organizations –

– notably the WHO –– that are demanding further evaluation of and philosophical debate on the

social and ethical implications of biotechnology in medicine. Their goal is to ensure a balance

between scientific progress and public accountability, respect and transparency in terms of the

potential future risks in research in this area.

The pharma industry also faces social and ethical questions in both clinical research and animal

testing. As research becomes driven by ever more costly technologies, stakeholders are asking

whether pharma companies and their external partners are ensuring the safety, rights, integrity,

confidentiality and well being of clinical trial subjects. Following successful clinical trials, the next

step concerns government scrutiny and regulatory requirements. In this area, first, the Food and

Drug Administration (FDA) must approve the new drugs.

Manufacturing

Pharma companies' manufacturing facilities are often in many locations around the world, including

many developing countries. Companies are, therefore, challenged to ensure consistently high quality

manufacturing standards on a global level. Pharma manufacturing quality is an important driver in

successful and timely product launches, the optimization of revenue streams, the enhancement of a

company's reputation, and ultimately the maximization of shareholder value. The Good

Manufacturing Practices Regulations (GMP), promulgated by the FDA, denotes good practices and

078 Full Text Available On www.ijupbs.com

International Standard Serial Number (ISSN): 2319-8141

addresses issues including record keeping, personnel qualifications, sanitation, cleanliness,

equipment verification process validation, and complaint handling. Pharma companies are widely

expected to address the corporate.

Sales and Marketing

Pharma Companies should focus their sales and marketing efforts towards different groups in order

to maximize the use of their products. Unlike many other goods, the end consumer of pharma

products––the patient––does not usually purchase or pay for the product directly. End payers tend to

be either public bodies or private organizations. Various groups influence which drugs are purchased

and prescribed. The influencers vary, depending on different countries' local regulatory and legal

environments.

Counterfeiting

Counterfeit drugs have been a serious issue in India. The Organisation of Pharmaceutical Producers

of India (OPPI) has spearheaded various initiatives to combat the problem. It has conducted several

seminars and worked closely with the Ministry of Health to develop policies for controlling the

production and sale of „spurious‟ drugs. It has also published a series of anti counterfeiting

guidelines for the industry as a whole.

Infrastructure

Insufficient energy infrastructure and inadequate transport infrastructure has historically posed

challenges for companies operating in India. The situation is definitely improving, as the

Government focuses attention on infrastructure needs. The Indian infrastructure sector continues to

be viewed as an investment opportunity, despite the global slowdown.

Tax Related Issues for Special Economic Zone (SEZ)

In an effort to attract companies to SEZs, some of these are located in modern industrial areas. The

Jawaharlal Nehru Pharma City, India‟s first and largest pharma industrial estate, includes a SEZ.

The facility is located near Visakhapatnam, in close proximity to many chemical manufacturing

hubs, and offers common infrastructure for resident pharma companies. There are three other

pharma SEZs located in Andhra Pradesh, and four in Maharashtra, as well as one on the outskirts of

Dehra Dun in Uttarakhand, so global pharma companies have a range of options. At this stage, it

may also be pertinent to note that the draft Direct Tax Code Bill published by the Government

presently does not provide for SEZ related incentive schemes. However, recent press releases

suggest that the Finance Minister has identified proposed incentive provisions as one of the areas for

detailed examination prior to finalization of the Direct Tax Code.

FUTURE VISION

Under its Vision 2020 initiative the Indian government aims to spend up to $20bn a year on research

079 Full Text Available On www.ijupbs.com

International Standard Serial Number (ISSN): 2319-8141

and development (R&D), in an effort to establish India as a global pharmaceutical hub. Various

R&D centers are also being set up in Chennai, Kolkata, and Mumbai. Initiatives such as these will

help the Indian healthcare market to become self-sufficient, ending its reliance on foreign imports.

The resultant growth in pharmaceutical exports is expected to strengthen the demand for logistics in

the country, creating an opportunity for logistics service providers. The market is expected to grow

to a value of $48m in 2014 from $33m in 2010, recording a CAGR of around 10% over 2010-14.

Pricing and margins

The prices and the margins of drugs for the wholesaler and retailers are largely decided by the

National Pharmaceutical Pricing Authority (NPPA), which varies depending on whether the active

constituent of the product is a scheduled drug or a nonscheduled drug. Scheduled drugs are price

controlled whereas nonscheduled drugs are not. The NPPA is an organization of the government of

India established to fix or revise prices of controlled bulk drugs and formulations. Companies must

keep drug prices affordable to the general public. To keep medicines within reach of the poor

population, the government has covered 76 scheduled drugs.

In addition to the above mentioned margins, wholesalers and retailers are also compensated with

additional trade offers. Hospitals and large institutions sometimes directly negotiate with the

manufacturing company and get the drugs in their pharmacy at lower costs. Stockists compete with

each other in a given city. Generally, hospitals order large quantities and can negotiate with

stockists, who provide payment terms, credit periods, and margins. Further, retailers and distributors

form associations locally and nationally, and manufacturing companies must comply with their

terms.

Increasing Competition Between Wholesalers and Retailers

Today, with so many mergers and acquisitions in the Indian pharmaceutical industry, the number of

stockists for each company has increased. Now two stockists of the same company may be

competing against each other. Retailers take advantage of this situation by prolonging the credit

period and asking for more discounts, which has an adverse effect on stockists, because they have to

comply with the retailers to sustain their business.

Six Trends in Pharmaceutical Distribution:

What To Expect Today

• Situation and trend analysis

• Influence of trends on distributors

• Where is your opportunity for more of the pie?

Situation and Trend Analysis

080 Full Text Available On www.ijupbs.com

International Standard Serial Number (ISSN): 2319-8141

Global Pharmaceutical Market Today

125 pharmaceutical drugs generate >$1B each per year and the top 100 have accumulated sales

of $285B, accounting for 35.3% of the total market.

The top 20 pharmaceutical products all generate sales in excess of $4B each and accounted for

14.6% of the total pharmaceutical market.

-The global pharmaceutical market is forecast to grow to $1.1T by 2014

Domestic Pharmaceutical Distribution Market

The Center for Healthcare Supply Chain Research reports:

· 5% growth in pharmaceutical sales revenues through primary distributors, who

handle 87% of the total $307B healthcare distribution market.

· Primary distributors account for 79%, while specialty distributors account for the

remaining 21% or $68B. Specialty distributors growing 7.5% versus 4% for primary.

· Primary Distributors deliver products to 200,000 providers daily; while Specialty

distributors deliver products to 40,000 individual ship-to points.

Generic drugs comprise 74% of prescriptions and $107B for 2010

Big Three (AmerisourceBergen, Cardinal, McKesson) compose $272B

Generics and Drug Proliferation

• 2/3 of all US patents, $142B in sales, will expire in next 4 years

Shift to lower-cost generics in major therapy areas such as cholesterol regulators,

antipsychotics and anti-ulcerants will reduce total drug spending by about $80 - $100B

worldwide through 2014.

Patent expirations in the U.S. peak this year and next when six of today‟s ten largest products

are expected to face generic competition.

• 150,000 preparations are now in use, 90% didn‟t exist 25 years ago, 75% didn‟t exist ten years ago

• New product types and incremental product launches will alter sales curve

Drug Shortages Increase

• 11-9-2011 Executive Order from President Obama instructed FDA to take steps to reduce drug

shortages.

Manufacturers required to alert of discontinuances sooner to help divert crises

FDA will let DoJ know if shortages could lead to stockpiling or price gouging

• According to Lori Clapper at Pharmaceuticalonline:

In past 5 years, disruptions in crucial medicines supply have nearly tripled, 200+ in 2011

Affected drugs include many critical to serious disease treatment.

081 Full Text Available On www.ijupbs.com

International Standard Serial Number (ISSN): 2319-8141

Use of injectable cancer treatments increased 20%, without related production growth.

It could be years before there will be a noticeable increase in production.

• IMS Institute for Healthcare Informatics

Drug shortage problem highly concentrated

Large number of suppliers but only 1-2 manufacturers

Total volume has increased but month-to-month variance is volatile

For 75 drugs, supply volume has decreased

Globalization

• 40 % of the drugs Americans take are manufactured outside our borders, and 80 % of the active

pharmaceutical ingredients comes from foreign sources.

• Executives report 70% have key suppliers in China and close to 60% in India.

• Axendia‟s research shows that 78% of industry executives expect global sourcing to increase and

76% anticipate their global manufacturing to grow.

Systems to meet compliance, reduce risk and counterfeits

Pedigree

Controlled Substance Ordering System

Arcos Reporting

DEA Licensing

National Drug Code (NDC) Tracking

Bar Coding

Electronic Product Code (EPC), RFID

Suspicious Order Monitoring

Electronic Data Interchange (EDI)

Increased front office complexity

Contract Administration

Rebates

Chargebacks

Medicare Average Sales Price

New modes of delivery and the subsequent reverse logistics

• Health reform shifts emphasis from product features to patient outcomes

• Greater use of electronic health records, e-prescribing, mobile health applications, and remote

monitoring are moving delivery beyond hospitals and physicians offices into homes, communities,

and direct to patients.

082 Full Text Available On www.ijupbs.com

International Standard Serial Number (ISSN): 2319-8141

• Returns management and corresponding credits

– Recalls

– Expiration handling

– Non-saleable

Trend affects on distributors

Generics & drug proliferation allow focus

1. Longer Tail in The Demand Curve

2. More SKU‟s Required to Stock

3. Higher Average Cost per SKU

4. Lower Velocity, or Turnover, of Average SKU

5. Margin Erosion – moving more products, for same or less money

6. Added cost, complexity of using third parties

7. Need for EDI or other previously unnecessary supply chain visibility and technology

infrastructure. All contribute to underperforming inventory and higher costs while your customer‟s

expectations remain the same or even increase

Globalization = visibility, virtualization, control, regulation

• Distributors must work with the expanded supplier network, master distributors, and virtual

inventory to ensure product arrives and meets quality expectation

• Regulators are raising the bar on supply chain safety, demanding sophisticated technology

solutions to track and trace products from raw materials to patient.

“The current pharmaceutical supply chain worked well when the blockbuster‟ paradigm prevailed,

but pharma‟s focus in a post-health reform world is shifting from products to patients, and their

supply chain processes need to adopt the speed and agility of other, more consumer oriented

industries such as consumer electronics and mass retailing. In a world where outcomes count for

everything, health organizations need to acquire a much deeper understanding of patients and their

healthcare needs. Information is the new currency, and the data behind the product may soon be as

valuable as the product itself.”

• Pharma IQ asked survey participants the 3 main solutions they are investing:

Tracking or supply chain visibility solution ranked first at 38.5%

Closely followed by data monitoring technology or software at 34.6%

Interestingly, both road and air temperature-controlled transport was identified by 30.8%

• Booz Allen found in The Role of Distributors study:

Distributors deliver $42B value to the pharmaceutical supply chain.

083 Full Text Available On www.ijupbs.com

International Standard Serial Number (ISSN): 2319-8141

Significant investments by distributors in data and technology systems help distributors

administer core services to lower business costs for manufacturers and providers alike

Efficiency improvements driven by investments in technology and business operations,

reduced distributors‟ “cost to serve” as a percentage of sales from 6.5% to 5.7%

Average operating margin has remained consistent over the past four years at 1.6%

Globalization has affected where and how you do business

• Consolidation

• Your customer and suppliers expectations are changing

• Efficiency of doing business online

• The drive to eliminate waste

• The challenge of self-service & on-demand

Opportunity for interaction has increased exponentially due to multi-channel, multi

generational approaches

70% of companies are not yet designing their websites for smart phones or tablets,

according to a report from Econsultancy and RedEye.

Babyboomers less likely to go online for directions or purchases while first place for

Millenials (GenY, the Net Generation).

• Everyone wants it all and they want it now

New modes of delivery, product types, and the subsequent reverse logistics allow distributors to

position themselves

• When it comes to positioning and messaging, the overwhelming majority of distributors in a recent

MDM survey have three things in common:

– About 90% believe they deliver more value than their competitors for a comparable price.

– 88% place a large emphasis in their messaging on a handful of features

• Product selection

• Availability

• Speed of delivery

• Pre/Post-sales support

• Professional sales representatives

– Nearly 70 percent of distributors use informal methods for positioning and messaging.

• If everybody is messaging on the same items, it means nobody is really differentiating.

How do you get more of the $307,000,000,000 pie?

Deliver value instead of positioning value

• Your customers choose the how and when to interact today, you can choose the content and quality

of the interaction.

084 Full Text Available On www.ijupbs.com

International Standard Serial Number (ISSN): 2319-8141

• Increased end-user or customer interactions is good

Generate revenue during every customer interaction

• Webstore

• Customer Service

• Consultation

• Bundling

• Purchase History

• Rebate Management

• Loyalty Program

• Value-Added Services

• Returns Management

• Inventory Visibility

Back office opportunities to increase profitability

• Get it right the first time

• Allow Self-Service

• Sell-up when appropriate

• Totally satisfy the customer

• Pay employees commissions for their efforts

• Automatic/recurring orders for incremental maintenance

• Communicate with suppliers and customers. EDI

• What is your buying network? Is it cost effective

• Is your customer status profitable for the supplier

• Visibility into virtual or expanded network inventory Profit KPI‟s

CONCLUSION

Manufacturers must ensure that their drug reaches customers with uncompromised quality. In India,

because manufacturers do not retain control over the multi layered distribution system, the cold-

chain management process continues to be difficult and expensive. However, manufacturers are

increasingly realizing the importance of an effective distribution system, all the way to the end-

customer. Coping with the challenges of streamlining the systems in India will ultimately benefit the

patient and the healthcare system.The Pharmaceutical industry is a knowledge driven industry and is

heavily dependant on research and development for new products and growth, However, basic

research is a time consuming and expensive process and is thus, dominated by large global

multinationals. Indian companies have recently entered the area and initial results have been

encouraging. In the global pharmaceutical market, western markets are the largest and fastest

growing due to introduction of newer molecules of higher prices.

085 Full Text Available On www.ijupbs.com

International Standard Serial Number (ISSN): 2319-8141

REFERENCES:

1. Eric Langer, Abhijeet Kelkar. (2008), Pharmaceutical Distribution in India. BioPharm

International, 2-5.

2. Carroll A. (2000), Ethical challenges for business in the new millennium: corporate social

responsibility and models of management morality. Business Ethics Quarterly, 10 (1), 33–

42.1.

3. BioPharm International, www.biopharminternational.com September 2008.

4. Price Waterhouse Coopers report on Global Pharma Looks To India-Prospects For Growth,

2012.

5. Agarwal, S., Desai, S., Holcomb, M. and Oberoi, A. (2001), „Unlocking the value of Big

Pharma‟,The McKinsey Quarterly, No. 2.pp. 65-73.

6. AstraZeneca (2001), „AstraZeneca Approach to E-Business‟, presentation to analysts, New

York.

7. Blumberg, D. and Perrone, F. (2001), How Much are Marketing and Sales Capabilities

ReallyWorth? A European Study on How the Capabilities Drive Performance, the European

Study.

8. Pharmaceutical Research and Manufacturers of America (PHARMA) (2001),

PharmaceuticalIndustry Profile 2001, Washington.

9. AZOULAY,Pierre (2001), working paper, Management Department, Columbia University.

10. Tufts Centre for the Study of Drug Development (2001), „Tufts Center for the Study of Drug

Development Pegs Cost of a New Prescription Medicine at $802 Million‟, Press Release,

30November.

11. ORG MARG Retail Audit, (2002). ORG MARG: New Delhi.

12. Venugopal, P.V., (1999), Industrial property and pharmaceutical industry: opportunities and

challenges for developing countries.

13. Smarta, Raja B. (1994). Strategic Pharmaceutical Marketing

086 Full Text Available On www.ijupbs.com